Credit card balances up 3.0% from March 2019, but CPI inflation up 13%, LOL. Auto sales plunged, but auto loans jumped. You guessed it, ridiculous price increases.

By Wolf Richter for WOLF STREET.

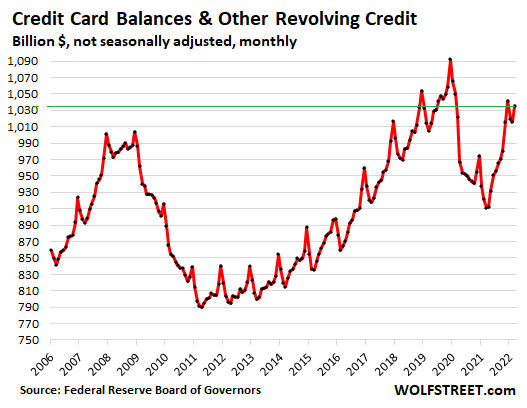

Credit card balances ticked up 1.9% in March from February, not seasonally adjusted, to $1.036 billion, according to the Federal Reserve today. Compared to three years ago, March 2019, the last March before the pandemic, this was up by only 3.0%.

In other words, credit card balances are now just 3% higher than there were three years ago, after three years of inflation, including raging inflation for the past 12 months that increased the prices of nearly everything that consumers buy with their credit cards.

Over the three years, during which credit card balances rose a total of 3%, CPI inflation jumped by 13%. In other words, even credit card borrowing cannot keep up with this raging inflation, LOL, and that their credit card debts, the most onerously expensive debt, is growing more slowly than inflation over the longer term is for once a good thing for the American debt slaves:

Note in the chart above how consumers paid down their credit cards and other revolving credit during the first 12 months of the pandemic, and then they started charging again, gradually getting back to where they’d been on a nominal basis, but never catching up with inflation and a “real” basis.

Seasonal adjustments galore.

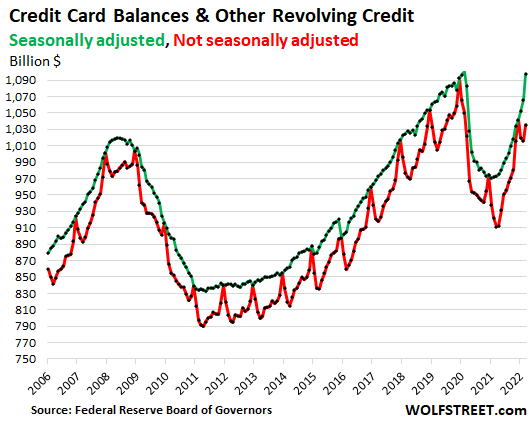

Consumer spending is very seasonal, and so is the usage of credit cards. Balances peak in December every year, and fall off in January and February. Massive seasonal adjustments are used to smooth this out. In March, these seasonal adjustments added $62 billion to the revolving credit balance and pushed the figure up to $1.097 trillion, seasonally adjusted, up by 2.9% from February.

This chart shows the actual revolving credit balances (red line) and the seasonally adjusted revolving credit balances (green line):

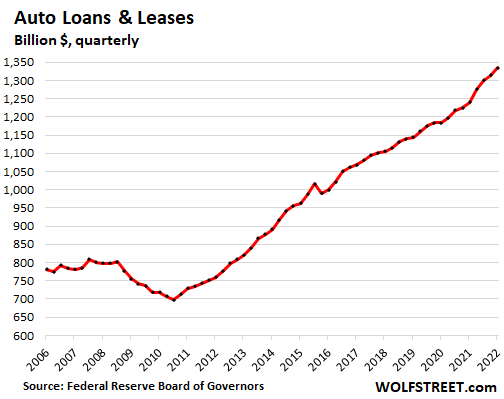

Auto loans and leases in the first quarter – this is quarterly data, not monthly – jumped by 1.6% from Q4 and by 7.6% year-over-year, to a record 1.34 trillion, according to the Federal Reserve today.

This increase in auto loans and leases came amid a plunge in purchases of new vehicles and a drop in purchases of used vehicles, accompanied by holy-moly price increases.

- The CPI for use vehicles in Q1 spiked by 35% year-over-year.

- The CPI for new vehicles jumped by 12.5%.

These ridiculous price increases had the bizarre effect that consumers cut way back on their purchases of vehicles but borrowed a lot more to finance them:

The majority of auto loan balances outstanding derive from the purchase of new vehicles, rather than used vehicles, due to their much higher prices – the average transaction price of new vehicles in Q1 was around $47,000.

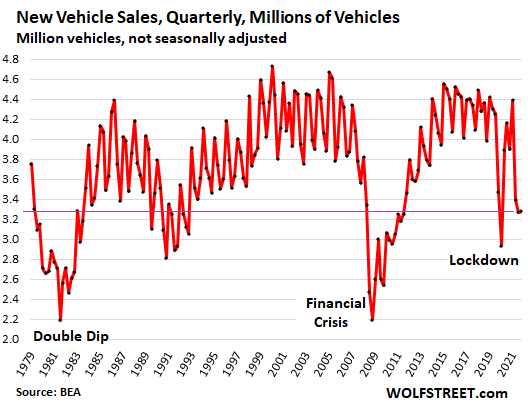

But new vehicle sales in Q1 plunged by 15.8% year-over-year and by 17.7% from Q1 2019, to 3.28 million vehicles, the worst Q1 since 2011, and right back where they’d been in 1979. This was due to semiconductor shortages, supply-chain chaos, production delays, inventory shortages, and nearly empty dealer lots.

The number of used vehicles sold retail by dealers in Q1 fell, including by 15% year-over-year in March.

So what you’re seeing reflected in the increase of the auto loan balances are two big factors, going in the opposite direction, with the ridiculous price increases winning the game:

- A plunge in the number of vehicles sold

- A ridiculous spike in vehicle prices.

So this is the status of the American debt slaves: They’re having to borrow a lot more to fund the purchases of a lot less because everything has gotten so much more expensive, thanks to this raging inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

That’s money is long gone. As Wolf pointed out, it was used to pay down debt.

Apple is funny – you bet money is long GONE to 1%

called TRICKLE UP THEORY

and $33,000,000,000 is GOING DIRECTLY INTO mic EXECUTIVES BONUSES

so sorry we only paid you $100,000,000 a year

would more STOCK OPTIONS be good????

“status of the American debt slaves: They’re having to borrow a lot more to fund the purchases of a lot less”

Such is the case for everything.

The real question I have is, should the fed keep on their track and not fold to using their tools to stop a plunge, what happens when consumers get turned upside down on all of the assets they own?

I guess the fed realizes that destroying the world reserve currency was a bad idea so the lower and middle class eat it now? Not that they don’t necessarily deserve it if you ask me. I’ve been uncomfortable watching the show for a few years now. Reminds me of when I was a youngin and everyone had a realtor wife, pontoon boat, Hummer, and jetski.

Maybe I should get studied up on being a repo man. Or perhaps a foreclosure specialist if such a thing exists.

Autos, toys, beanie babies, who cares. I don’t suspect the stock market will be saved either as the real money will cash out before they really go insolvent. The main thing is housing though. With the run up we’ve seen recently, I’m wondering if we are heading towards the realm of Canada, western Europe, or Australia. Save for Japan, seems like the highly developed western world all tracks towards an apartment renter society where housing is only achieved through inheritance or by dint of extreme wealth.

I wonder if the real estate market isn’t bailed out or propped up. Didn’t happen last time, likely won’t this time. Again, I’d really like to stop living as a room renter from a stranger in an HOA dictated suburb so there is emotional investment weighing my skepticism.

I really hope all of it crashes. I’d like a reasonably affordable vehicle that isn’t 40 years old and requires the ethanol to be cleaned from the carb every 4 months and a modest 2br house in the woods that isn’t a million dollars. Even still, being on the outside, I’d say I’m better off than 90% of the current lot of low to middle class Americans.

This is a very good point. I recently learned about a condominium building, which association decided to sell to an investment firm of some sort. Apparently, if 70% of all condo owners decide to sell, the remaining 30% have no choice, but to sell also. Long story short, this investment firm will now convert those condos into rental units. I don’t know why, but it seems like your rent prediction is on track and there is a bigger plan in works behind the scenes.

@Nissanfan: Good point. That deconversion process is active in nearby Chicago, and throughout the US. Like the Surfside condo collapse showed, deferred maintenance is a massive deal, and it’s hard to get a quorum of HOA members to agree to actually pay for big ticket repairs. In a deconversion, PE has carte blanche to make the needed repairs/updates, passed along in the form of (higher) rent to new/existing tenants. On one hand, the market clearly has solutions to intractable problems like this. On the other hand, it is taking owners, who cannot agree to spend in their own best interests, and making them renters. This issue deserves much more attention, as the unintended consequences are intricate and far-reaching.

https://www.ksnlaw.com/blog/reasons-condo-associations-deconversion/

Don’t most HOAs have a committee which can make decisions about the upkeep without the votes of individual owners? So you vote for your committee member and that is your vote. Like an indirect democracy. And those members must make reasonable efforts to upkeep or they are legally culpable for neglect.

I knew somebody who owned a condo and decided they wanted to sell. Right before they were ready to put it on the market the association hit everybody with a “special assessment” of $35,000 for building repairs. Let’s just say that this destroyed her financial situation to put it mildly, because she didn’t have the money for that nor was she able to sell. I wouldn’t even want a condo for free.

That was a very poorly managed association. We have a big surplus so we can handle anything that happens without having to bankrupt the owners. In fact my HOA fees have remained the same for the last six years.

All of the responsibilities of homeownership without any of the benefits. The worst of both worlds.

I don’t think US residential real estate will come to resemble those countries nationally. To my knowledge, what most people believe of those countries doesn’t reflect reality. It’s mostly *better areas in) the larger cities and locations with desirable amenities. like beach property.

The end of the bond market mania means the end of cheap corporate financing and the loosest credit standards in history. So, I expect it also means the end of mass corporate buying of residential housing, not immediately but not that far in the future either. Years from now, I expect it to turn into selling.

I also expect a government moratorium when the economy tanks if housing market gets anywhere near as bad as GFC. Most homeowners have presumably refinanced to rates between 3% and 4% by now. At 3%, a moratorium costs $2.5B per month for every $1T in mortage debt. That’s a lot cheaper than massive foreclosures and the additional economic contagion, temporarily anyway.

Question is how long the bond market will accommodate it. At some point, the USG is going to have to choose what it’s going to subsidize because the days of subsidizing everything simultaneously at essentially no visible cost are going to end.

I don’t believe housing is anywhere near the top of the list. It’s not last either but there are many other things ahead of it, starting with the Empire. It’s always first.

Housing is so linked to inflation down the road, I believe. My folks bit off a big chunk of mortgage in 1970 with the expectation that inflation would make it much more affordable in a few years. Then, for my family, it worked out.

So, let’s say you buy a house for $400k today; at a mortgage closing in on 6%. Project to the future horizon with a couple probable scenarios.

1) Inflation stays at 10% for the next decade. And interest rates rise only partway to that level.

2) Inflation levels off at 5%, but interest rates climb to 8% & mortgage rates are at 9%.

In case #1, the cost to get a mortgage stays within reach, and the house appreciates and the cost to pay for it goes down. Buy now = winning.

In case #2, the cost to get a mortgage reduces potential buyers; the house does not really appreciate to keep pace since were are in a bubble at this time & demand will go down. And the mortgage payments will not be made much easier by inflation. Buy now = losing.

These are fairly possible scenarios. What’s behind the curtain? Door #1, Door #2, or some other door?

Life ain’t easy, is it?

2) is my fear. That we become conditioned to think 5% inflation is “leveled off”. I’m also fearing that this is the new norm. Yes, we will get a correction but the old days will never return.

Al Loco,

Great point!

“Inflation drops down, to half of 10%, but is still 5%, thereby relentlessly robbing people of their wealth and purchasing power.” would have been a better choice of words.

Thank you.

Later at some point yes, but not at current prices. It’s already absurdly expensive.

The only reason for both large corporate buying and any remaining “affordability” is cheap credit and loose credit standards.

If the bond bull market from 1981 is over, cheap credit ends with it. The government may subsidize limited favored political constituencies but it’s not going to offer substantially below market financing to every new buyer, not with $2T+ annual deficits as far the eye can see.

Loose credit standards? It will last longer but won’t last indefinitely either for the same reason. End of the bond bull market also means the USG isn’t going to be able to subsidize everyone on the government balance sheet without trade-offs.

Practically everyone has gotten used to the USG being able to subsidize practically everything simultaneously because the 5X increase in the national debt since 2000 has appeared to be virtually cost free.

They also subscribe to the economic idiocy that if the government guarantees some random economic activity, risk has been eliminated. The end of the bond mania means those days are over. It’s not happening tomorrow but it’s coming.

Lastly, both your scenarios seem to assume a mostly robust job market. The end of cheap credit and stricter lending standards also equal a lot less fake “growth”.

With less or no fake “growth”, the current artificial labor shortage (no, it isn’t self-sustaining or remotely natural) goes with it and so does the financial capacity to afford anything close to current prices.

Unemployment and labor participation has been low most or all of the 21st century because of fake prosperity, not because of demographics or some other supposed reason. People only stop working economics permitting. Otherwise, they starve.

If inflation gets too high, cities will start to burn. What you are not factoring in is that energy will become more and more limited in the future, reducing the value of certain types of homes. If there’s nothing to heat your home with, then those homes will have to come down in value no?

This is not the 1970s. Yes there was the OPEC oil embargo then, but energy was still plentiful back then. And no, renewables etc will not save the US or any other country. Russia with its plentiful supply of energy AND food is best placed to weather the storm until another source of credible energy can be found.

What about 3) inflation rages the next year and a half, starts to decline and then five years down the road we are back at ZIRP because the impacts of Covid are all in the rear view mirror and we are back to trying to support a house of cards with zero rates like most developed nations were doing pre Covid?

Actually for AF:

One of YOUR BEST, far damn shore AF!!!

Thank you.

would really like to be able to say that WE have been saying the same thing for decades, but NOT…

really only been saying, ”Clean HOUSE,,, SENATE TOO” because a real estate professional lady explained SO much to me in early 1980s, including what now appears to have been SO prescient.

Between 1980 and 1990, 30 yr fixed mortgage rates were 10% or more. The median price of a home more than doubled. Too many buyers, not enough carpenters.

I bought a new car in January. Its value may be rising faster than the value of the stock market.

The amount of grain available for shipping might drop 3-4% this year due to the invasion of Ukraine. Are there widespread shortages of everything?

“My folks bit off a big chunk of mortgage in 1970 with the expectation that inflation would make it much more affordable in a few years. Then, for my family, it worked out.”

This is like comparing apples and shoes. There is not even a remote similarity between what’s going on right now and 1970.

Just sold my 1977 home on Vancouver Island. Blue collar pulp mill town. 4 beds 2 baths $780k. A week later the market turned here and sales are waay down.

houses in at least Spain and Italy going for basically nothing, as long as you can put up the cash to fix them, most need around $20K from what I read recently

some have old and older groves and land, some are in cities and small towns with little or no land

suspect this will happen here too ONCE AGAIN,,, just as it did in the last crash when a really handy friend was working for a guy buying houses for single digit thousands

friend told me guy was spending couple or so thousands to make needed repairs, maybe a thousand or so more to ”gussy up” a bit, then selling for good money or renting ditto and refinancing

middle flyover of course,,,

but know of houses that were $800K+ in 2006 that went for low $200Ks in 2009

”keep your powder dry”

Exactly, with remote work, the Mediterranean offers sky high quality of life compared to the US. The old will not benefit, too late for them, but the young are already doing it.

RemoteWorks,

To update your knowledge:

1. “The old will not benefit, too late for them”. Well, “the old” love retiring to the Mediterranean, and those with enough money do it in droves. There are whole towns that cater to retirees (and vacationers) from other countries.

2. The European side of the Mediterranean is fairly expensive. If you want cheap, you need to go to the African side, though some places are getting expensive too, or maybe Lebanon and Syria, which you should be able to get some deals currently. Israel is expensive. Turkey is affordable though, and with all the inflation they have there (70%), it’s a good deal if you earn dollars.

Screw Europe (figuratively speaking). Too many unity-oriented and leverage-based problems.

Simply own paid off So. Cal. beach-front property; clearly the way to go. Avoid profligate expenditures and watch the logarithmic wealth growth.

I’m a used truck dealer and sales are at severe recession numbers. I barely survived 2008-2012 before the fed made boom kicked in. Looking at the math I’d say we’re facing 5 to 10 times worse consequences of all the new debt facing possible default by all kinds of parties including the Government. And that’s not taking into account Wars, Supply shortages from lockdowns and water shortage in CA. My economics study says the only solution to survive is a deep depression. To get inflation truly down for good hard assets will need to be repriced at fractions of their current value to begin a new low-cost basis. Then for example new Property Owners can rent their places for much less than today. The current system of debt expansion and derivatives by central banks has come to its conclusion in my opinion. It remains to be seen if they will allow the depression but I rather think the central banks will lead countries to World War when currencies fail(inflation) as history has always shown. And they will bring in their new system of control and monetary oppression and we’ll be happy because it (greed) was never their fault and they told us we must be happy.

Governments cannot prevent declining living standards because these entities produce no actual wealth. This belief is a complete myth.

Look at US “real” household median income and net worth reported by FRED. Since 1998/1999, both have essentially flatlined. This is an entire generation (over 20 years) and probably the worst performance in US history over a comparable timeframe.

This mediocre performance also occurred during the biggest asset, credit and debt mania in the history of human civilization. Most inflated asset markets ever for 20+ years, lowest interest rates in history since about 2008, ridiculously lax credit standards the entire time, fake “growth” since 2008 almost entirely from above trend USG deficits, and FRB QE “printing”. Many of the same attributes in other major economies.

In other words, it took the most distorted artificial economy and financial system in history to produce these pathetic results.

So, the question then becomes, what’s the economic and financial environment going to look like with any return remotely resembling “normalcy”?

It’s a rhetorical question.

Governments can protect living standards by avoiding budget deficits and enforcing balanced trade. If they did those two basic things the country would not be in a pickle.

The filthy wealthiest people are damn good at promoting American cultural wars and gridlock that prevents almost all pragmatic compromises which would achieve those goals.

Not from current conditions.

An unprecedented economic depression is required to get to the starting point implied in your post first, at minimum.

I consistently read (everywhere, not from you) what solution is available to this mess.

By “solution”, the implicit unstated premise is without the majority of the population suffering the consequences of current and past excesses which are the worst in history, hands down.

Anyone can envision as many “doors” as they like but it leads to the same outcome. There are no “pragmatic compromises” that can escape noticeably declining living standards for the country because it’s not just a result of a lack money, but extensive economic and social decay. There is no putting lipstick on that pig to pretend it never happened.

The majority of Americans are destined to become poorer or a lot poorer over the indefinite future.

The USA has a wide range of governmental hierarchies. But at the core, Uncle Sam has three, and only three jobs.

1) Protect the sovereignty of the of our land; land which geographically defines the borders of this nation.

2) Protect the sovereignty and rights, as enumerated in the Bill of Rights and the Constitution, of individuals and corporations within the borders of this nation.

3) Facilitate commerce within the borders of this nation.

That is how “Government can protect living standards” in my philosophy and set of values. Many citizens in the USA would disagree, and certainly, that is not how the federal government is operating.

The banking arm of the “Congressionally Delegated” Federal Reserve has been very successful in a well planned and deliberate orchestration of actions in order to shift the wealth to a smaller percentage, and to make the dollar worth less by inflating the money supply.

Is the end game to make the dollar not only worth less, but worthless?

Cue the Nick Lowe song again ….

“And so it goes and so it goes

And so it goes and so it goes

But where it’s going no one knows”

“Governments can protect living standards by avoiding budget deficits and enforcing balanced trade.”

But they do neither, at least in the US, because their incentives are diametrically opposed to both.

Garbage economic theory tells them deficits don’t matter which is what they want to hear and lobbyists from multinational corporations who fund their campaigns export manufacturing and massive trade deficits result.

Finally, the “financialization” of everything allows the general public to also go into debt to buy anything, not just major purchases like cars and homes. As a result, a percentage of their income goes just to service their debt while too many live outside their means, just like “their” government.

Dan, you said:

“Is the end game to make the dollar not only worth less, but worthless?”

That end game would not work for the ultra rich who run the show here.

“Governments cannot prevent declining living standards because these entities produce no actual wealth.”

Nah! The government can just print more money! I’ll bet if that was offered in a survey as an answer to rising prices a disturbingly large number of our idiocracy by design population would agree with it.

That’s the answer in my state which was once red, but turned blue by blue staters moving here after fouling their previous nest. Last I heard, I’ll be getting $400 just prior to the midterms. Apparently, they think I bother to vote and can therefore buy me with my own money.

People in forums like this often don’t realize how clueless most people are about these things. There should be a MANDATORY course in high school called something like “How not to get scr*wed financially” which, since it involves money, would probably be extremely popular and definitely beneficial to students.

No we are completely screwed. The cr@pforbrains previous generation is now teaching. Here in Arizona, we went to check a middle prep school, and the principal who was a black guy from CA, was proudly showing us gender neutral bathrooms. That was the first thing he showed us as he walked us through the premises.

These guys are bringing their hyper progressive politics and misplaced priorities to schools; which should be a place of learning only.

Let’s get ther war with Russia going, people have gotten too comfortable and fat on account of zero accountability.

Why do red state residents blame blue state newcomers for changes? Does not seem logical or evidence based.

“Look at US “real” household median income and net worth reported by FRED.”

Net worth is not a good measure of prosperity because it assumes everyone is trying to build wealth. Also, household income is flawed because it’s gross income, before taxes. What matters it discretionary income.

“In other words, it took the most distorted artificial economy and financial system in history to produce these pathetic results.”

And lot’s of willing participants (US citizens, aka, consumers) that went along with it.

“So, the question then becomes, what’s the economic and financial environment going to look like with any return remotely resembling “normalcy”?”

More and more subsidies. The people will demand it.

If Weimar Boy Powell and his ilk end up destroying the currency and it fails, I hope they are hunted down and dealt with.

” I hope they are hunted down and dealt with.”

For sure. Any of us “little people” would go to jail for decades for counterfeiting. Not the Fed.

Reckless driving is a felony for any of us “little people”.

Not for the Fed.

I dont see how its possible for the Central Banks to now save the economy from a severe recession/ depression. 30 years of unrelenting interest rate decreases and printing money have finally let out the inflation genie. Changing demographics, massive loads of debt everywhere, super asset bubbles in just about asset class, totally out of proportion housing and rent prices relative to income, hollowed out middle class etc., All of this portends total economic disaster. Meanwhile the rich get richer and maybe we are in the era of peak billionaires at some 1800 globally and probably 2 million millionaires. I know we create new ones nearly every week just with the lotterys.

Watch Uncle WArrens interview = he let it slip 1 world currency

And there’s more…

Flat and declining housing prices means no more sweet equity to borrow against to pay down those cards.

It would be interesting to know how many people did borrow against home equity to pay down credit cards.

Seems like a good idea on the face of it, if you’re the type that would run up a large credit card balance (which I would NEVER do unless under some kind of duress). One would save roughly 15% in interest charges by switching from about 20% credit card interest charges to about 5% home loan interest charges. And if you were confident about your income not lagging too much behind inflation, you also win by paying back money that has lesser value.

But adding balance to a home loan would give me a very uneasy feeling of sands shifting beneath my feet.

Unfortunately, consumer debt and credit card debt are perennials that tend to sprout again, for most families.

Success at dealing with his consumer debt reinforces the debtor’s belief that the credit tool is a harmless and controllable solution to the economic problem: unlimited wants and needs, but limited resources.

Ignorance, trickery and societal pressures play their part, but debt slavery is a choice (and a harmful and addictive one, at that).

You’re describing a form of “can kicking”, at the household level.

It’s living beyond someone’s means by those who won’t reduce their consumption and living standards.

The credit markets will eventually do it for them because the end of the bond mania means the loose credit terms that enable (mostly) institutions to provide the funding for serial loan defaults and bankruptcy are coming to an end.

John H

‘Unfortunately, consumer debt and credit card debt are perennials that tend to sprout again, for most families’

I agree.

Since late 80s, most of the americans below 60% , started using the CC to maintain ‘middle class’ life style. the wage growth is/was stagnant. Then came the home as new ATM machine! Those bought (with leverage) about 2 yrs ago, will be under water, if the rates going up. There are always exceptions depending upon the location and the demand.

The recession is already baked in. Soft landing is a delusion of the hopium crowd, along with Mr. Powell. Debts of all kind are in record territory!

Rising inflation may slowly turn into dis-inflation and the demand destruction picks up (time frame?) back to deflation!?

we are in uncharted waters!

AF, those that manage to kick can down the road beyond their expire date have actually won the game.😉

It’s sad that so much of the consumer attitude toward debt seems to have been hatched from above. With congressional spending in perma-deficit, (enabled thus far by the monetary authority) it’s no wonder consumers feel they have a green light to charge up a storm.

“There is a natural tendency in men to follow the example of the Government under which they live.” – Walter Bagehot, Lombard Street

If you search for stats of overall death rates in America, it’s barely a statistical blip.

About a 1% increase, smaller than increases in the years 2014-2018.

So, if you are relying on that to free up cash and assets for folks to spend, it’s a nope.

Well, you didn’t detect the sarcasm of my post which was a reaction to the word “scamdemic,” not a serious assertion about excess liquidity in the economy. Should I assume you are one of those who thinks the pandemic has been a hoax?

Citing death rates is a tricky statistic, being dependent on gross population, composition of the population, and general health of the population over time, as well as other factors.

Excess mortality is a better measure: Percent excess deaths over time can be estimated by this formula:

(Reported Deaths – Projected Deaths) divided by Projected Deaths

For reference, check out ourworldindata website which has interactive graphs that show excessive deaths spiking as high as 35 to 40 percent above expected during the pandemic.

Tnere was and is a pandemic. Do us a favor and die for your beliefs. RIP

For all those calling for demand destruction, an excess of goods could result in a severe recession.

RobertM700

Once the supply chain squeeze unwinds, that’s what exactly will happen.

Recovery will be a long dream! Piper is here to collect!

Recession started last November,pay attention

“Okay Lou, I get your point. Wait a minute, I just lost it.” The mix has shifted from goods to services…fine. But if the card balances have fallen behind the price inflation, might this not suggest general souring of demand for all things not needed? My impression is that real shortages have been in things that are needed or closely wanted. That leaves about 90% of store shelves (and maybe warehouses) full of crap that ain’t gonna go anywhere fast. Howard the Duck may live in a world he did not create, but in a normal situation would this not be a sign of serious potential retrenchment on the horizon? “C’mon Lou. Let us keep fight club here in the basement and we won’t bother you anymore big fella.” [Insert scene of Wolf delivering yet another punch.]

People have a huge amount of money, from all kinds of sources. Overall spending is huge. They just don’t rely on credit cards as much. And consumers are outspending inflation.

This is consumer spending adjusted for inflation:

Yes, I get it’s gone up, but it doesn’t explain what they’re really doing. Perhaps a rush for product and price while still possible to get it…..Then the sobering withdrawl? I see lots of nutz flying in and out of driveways but those shelves aren’t going bare except in select spots which looks like panic buying. Of course, meanwhile back at the ranch, the delivery guys are dumping boxes as though cardboard were going out of style. (I’ll try not to get blood on your shirt Lou.) 🤕

At the end of the day it is all driven by expansion of total credit (public + private), so no surprises here.

But it won’t last much longer. If you look at the GFC in 2008-2009, this was just a minor slowdown in the debt expansion trajectory.

I’m expecting this to end in an (asset)deflationary bust. There is trillions of mispriced assets that will have to be repriced / defaulted on.

At the same time, CPI inflation could still remain elevated (because defaults and supply chain disruption, war and sanctions will take production offline and input costs remain high).

In the past decade we had the opposite situation with massive asset inflation while CPI inflation was relatively low, so asset inflation and CPI inflation do not necessarily move together (everybody seems to assume that!)

Central banks are still almost all in (years behind the curve!), which will limit their ability to counter it.

Interesting times…

I expect the same as you, just worse.

Yushan

‘There is trillions of mispriced assets that will have to be repriced / defaulted on.

exactly!

This includes NOT just equity mkts but also housing, which may a bit longer than sliding of stock mkts. The main reasons are record levels of DEBT of all or any kind, throught the World, unlike any time in human history.

Mr. Powell cannot save assets and at the same time contain inflation! He is trapped (beside being clueless) although there is continuous denial!

And that’s what printing/ digitizing $40T (Inflation) over the past dozen years created via massive bubbles in equity markets/RE/Art/Collectibles etc….

This is a global contagion, worldwide bonds are very nervous. Bond market will create ,GreatReset

New home prices have exceeded CPI inflation much of the time.

Real auto prices have exceeded CPI inflation from time to time. Some used adjusted new auto prices to hide inflation.

Wages are growing, jobs are available. They have money to spend, bidding for goods and services. A rich man can get what he wants in the market place; shortages or not.

At this point it’s clear that Powell or Biden are simply stooges doing what they are scripted to do and take a fall for the system if need be.

How many of us really believe that Powell or Biden come in the office believing that they need to be careful because “God help me if I make a bad decision!”

No. They are just the frontmen that sign off on everything that’s thrown on their desk.

Like that scene in Goodfellas where the mob (who was really in control) are about to burn down the restaurant for insurance fraud and the mob is having the “owner” sign off on the documents.

There are three or more ways to free the debt slaves.

As in the US civil war, a party like the Republicans can go against the slave owning Democrats, fight, and “free” them or

some new owner can “buy” them and set them “free” or,

as in England in 1774, a court case, found slavery to be rather disgusting and passed a precedent which freed all slaves (via parliament) in the British Empire by 1806.

So which way will debt slaves be freed….

Civil war(riots) or

A new “generous” owner who took on their debt (as with stimmies) or

Such general disgust at the thought of debt and the banning of credit cards for running up debt…(like many of the comment section)

My guess is civil war……sorry…..

It’s ridiculous to create analogies comparing historical human slavery (a person being property and completely at the mercy of another person) with current “debt slaves” (people who made choices, and can declare bankruptcy or just leave some kind of jingle mail and walk away).

The type of irresponsible people who get themselves into a debt-slave type crisis will likely get themselves into another debt crisis eventually. Especially if they are rescued from the previous one with no skin in the game.

Making the greedy lenders pay would be a better solution. Civil war almost certainly would make things worse for the majority of responsible people.

Making the greedy lenders pay would be a better solution.

Sorry, I don’t live in a fairytale world….

Slavery is slavery, just as it is to be an economic slave making sneekers for Western feet or to be one of the 10,000 thirteen year old sex slaves brought into the USA every year for $25 a pop….(I like the USA because you do not hide your stats, ten out of ten for that)

You can also become a slave through crazed and immoral education/political policies (especially California, which is a zowie ha ha) One of the latest ones, in the USA, is that certain racial groups can become rich by getting involved in the “legal” cannabis trade…how dumb is that….

You can become a debt slave by allowing doctors to make huge profits by dishing out Morphine tablets for a sore arm…..or your child being very ill and having medical bills…

The list goes on……

I’m lucky and blessed not to have debt…….

Sure you do live in a fairytale world to compare Americans irresponsibly running up credit card bills with historical slavery such as pre-civil war African Americans.

Nice try shifting to describe foreign wage earner “debt slaves” etc. who are completely different from what you had asserted about Americans with high credit card balances (which is what the article described).

You know it’s ridiculous to compare “debt slavery” of people in the United States to historical slavery where one person could own another and do anything they wanted to them like a piece of property.

Whining about people’s various weaknesses causing them to have dependences, and random incoherent flaming about California etc., is not a logical basis for predicting a civil war.

d.- I’m not going to defend his position for him, but if someone had been watching the Rock Island Bridge case in the 1850’s they might have said it was “not a logical basis for predicting a civil war”. In fact, it was a pre-cursor to the very question of a nation splitting apart under the leadership of two warring economic factions with opposed views of where to take the country. The pot was simmering and no one saw it better than that hired lawyer Mr. Lincoln. At the same time, most people thought John Brown was just a raving, ranting looney tune and they did not give a rat’s ass about people who obviously were to be blamed for their condition because they had chosen to be born in the wrong suit and were not willing to fight back. Point is…you never can tell what will set off catastrophic cascading of events, but it usually doesn’t come down to just one thing. A lot of seemingly unrelated conditions just happen to line up such that clipping that iceberg starts the chain.

Poor old drifterprof,

I guess the months of riots, two years ago in over 60 American cities, was just a myth.

Yes, many people do stupid things and get into debt for crazy reasons but you can’t use the word debt slavery without calling it slavery…it’s the same thing, as you will find out later in the summer when the riots break out…

Read your history books….debt and inflation always causes hunger, wars and riots and death….always…even in the USA….

Regarding slavery, there has not been one nation or peoples in the world that at one time or another have not been slaves(or slave owners) and slavery has always been based on power, finance, profit and debt…and in the past, sadly, many people became slaves because they were first in debt and had to be sold into slavery to pay off their debt….

Crazy inflation and debt is a slippy slope, especially for the 40% of US workers(40 million workers?? I don’t know the number) who live paycheck to paycheck……..and will by August or so, be feeling angry they can’t feed their children…

Shit, I had riots in my neighborhood two years ago. Sat on my front porch throughout a few nights, guns at my side, to watch over my ‘hood & my next door neighbor’s home . He is a City Council member.

My Post Office, 55406, still has not been rebuilt. East Lake Liquors had neighbors and customers guard the business by staking out the roof with rifles and shotguns at the ready.

Three weeks ago, the FBI put out notice that City Council members’ home may be targeted with pipe bombs and or long range gunfire.

“All things considered, life is good in Minneapolis.” -DanBob

You are right someone did force the poor guy to buy the 5 series beemer… and get $20 avocado toast for breakfast and lattes all day long, it’s not his mistake. And if he jacked off at school that was the school’s fault as well. It’s never the fault of the person that took on the debt, always someone else… those mean banks forcing people to buy cr@p at gunpoint… sheesh

really for driftr:

ancestor was on ”THE Mayflower” and parents said to get the scholarship,,, child tried and found ancestor was a SLAVE…

can say and rationalize all one wants, but fact is that many folks then, and now were slaves by their choice,,, including

many many from places other than northern areas who CHOSE to be ”slaves”

until WE the PEONs come to grip with this concept and proceed to fair resolution, USA will continue to be ”less than blessed”

and anyone considering otherwise really and truly MUST deal with USA genocide(s) for early peoples, THE greatest shame for the Ice People here now.

All the debt slaves are sitting at Starbucks buying $10 fraps posting selfies on IG to show off the lifestyle their liberal arts degree bought them. They are so oppressed.

And I’m related to them. I keep a low profile because I know when their debt runs out, which is taking way longer then I thought it would thanks to stimmies, they’ll come knocking at my door.

Good points Anthony and that’s my take on this. In the US at least not all debts are equal in showing profligacy or moral failings. Sure, the fool who runs up 5 credit cards buying up yachts and leasing a Mercedes, or going on drunken benders to impress friends and gamble away in Vegas? Yeah, they’re poster boys and girls for “poor decisions” and clearly got themselves in debt. (And even they can clear it in bankruptcy.) But Americans running up credit cards because they’re being crushed by medical debt? They have a sick kid and their health insurance “drops” them through some convenient backdoor clause? They lose their job and can’t afford their already overpriced diabetes meds? A surgeon saving thousands of lives a year gets wiped out in divorce (hey, divorce courts are big money for lawyers) and then the alimony and child support rackets force him or her into non-dischargeable debt (a judge can impute ridiculous demands based on an unsustainable earning year)? Or even just credit card debt for essentials like rent and food, as Wolf is showing with incomes way behind inflation? Yeah, that kind of debt is totally immoral, not the fault of the debtor and fully the fault of a corrupt, unethical system. And needs to be brought down. We can’t just conflate all kinds of debt, and it’s an indictment esp of the United States that we’re the only modern developed country forcing people deep into debt for medical bills, or where divorce is a profit opportunity in the family courts. That’s debt slavery.

I’d also add student loans is somewhere in middle on debt as moral failings scale. Yeah, there are cases of dumb naive American 20-somethings who major in a non-employable field and run up tuition debt of $200,000, clear case of bad decisions. But from when I was doing student advising, a lot of other US undergrads in debt do major in legit fields that should have jobs at the end of it, try to do community colleges and public universities. But they still get forced into debt because universities in the USA have become so corrupt with their tuition increases to pay for shiny new stadiums and admin buildings, rent is going way up (housing bubble) and they have to go to school half-time because a relative is sick and they have to work (but of course jobs don’t pay enough). These kids are financially responsible but they didn’t pick rich parents, they’d like to minimize debt but lazy HR depts at many companies won’t hire without a bachelor’s (even for trade school)–so what are they supposed to do? This Calvinist finger waving at the individual in such cases for “moral failings” is dumb and wrong–the culprit isn’t the kids, it’s the corrupt profiteering by the power elite and academia (fed by US student loan policy), and kids have little alternative or they’re unhirable. In most of Europe and Asia you have to test go to university, but you graduate without debt, it’s only the US and a few other places that use debt-financing. Again, debt slavery here.

good start driftr,,,

how some ever and IMHO, the VAST and continuing ”issue” FKA “problem” is that in the USA, ( and one can suppose many other places are similar)

Most folks are completely brainwashed by any ”classical” metric.

Not sure if this is Still True today, but damn sure it WAS true for far, far too long that USA was still allowing the brainwashing techniques perfected by some really ugly folks trying to take over the world back in the 1930s and early 1940s.

These included MOST of the techniques used today by the so called advertising industry who know exactly what they are doing based on tons and tons of feedback, etc., etc.

Please do NOT take my word for this,,, LOOK it up on our, WE the PEONs our, now much much more available information sources thanks to SO many wonderful folks contributing…

1) The Republican invaded the south to extract commodities for

New England infant industries, that compete with old England. The south enriched their Scottish Tobacco Kings bros. Cotton for the industrial revolution in England that produced sheets and pillow cases. London bankers ruled the world from India, China and Alabama.

2) Who need black slaves if u have steam engines.

3) The British navy had the right to search ship for slaves.

4) The sugar island slaves kept 750,000 English slaves on the nulls and in the coal mines in Manchester and Birmingham on sugar high. Life expectancy was 40Y.

I was very young then, but I remember that trial. Press coverage was swift and harsh and after hearing the respondent’s case in chief, the justice was noticed to be quite bored and hear to have exclaimed ” I feel as though I’ve been savaged by a dead sheep.”

Wolf, What is a plunge for you? A Drop in 10%, or 20%, or 30%? Trying to get a handle on what is significant here

The Q1 “plunge” in new vehicle sales took sales back to the level of sales 50 years ago (1970s, Nixon, et al). Is that plunged big enough?

The automakers seem tickled pink with their prices yet they are losing billions. What kind of illicit substances are they using? They are headed toward a business model where they produce one car a year for Jeff Bezos, and that’s their entire profit.

When you raise prices to levels only the rich can afford, you are missing the mark. Henry Ford understood this. Unfortunately, we seem to be going backwards in a hurry. I happen to think this country is finished.

Amen. Relief of a sort is coming. Nothing like quasi-slave labor in companies that do not have to worry about releasing toxic waste, are CCP-government-subsidized, get CCP-government-subsidized loans, etc., to make cars cheaply.

Reportedly, CCP-connected manufacturers/others are trying to import cars made in China into the USA. They are “environmentally” clean, so long as you ignore bloodshed involved in producing them: the horrific oppression of Chinese workers, lack of any environmental protection laws to prevent discharge of toxic wastes or anti-pollution laws in China, prevention of unions to protect workers in China, lack of any labor rights, murder and organ harvesting from any persons who oppose these CCP policies, etc.

I am waiting for hydrogen stations to be created throughout California, at least, or for a truly desirable battery that can be charged in 20 minutes to be created to buy my next car. Lots of people are now holding on to their ICE cars for a longer time. Sadly, I suspect that my next car will be from a Japanese brand. RIP, US auto-makers; you could never have competed against the power, technological theft, and entire finances of the CCP but Americans were too stupid to realize that.

Bought a 1970 Dodge Challenger from a local dealer and financed through a local bank. Per the usual the dealership folded, the engine stuck a valve, I shamed another dealer into repairing it, and traded the car for a 1963 Ford. The used car dealer allowed me to pay off the loan while he sat in the parking lot. I was happy to see it go bye bye. The used ford was a great car as it was mine.

“There are two ways to conquer and enslave a nation. One is by the sword. The other is by debt.”

– John Adams

“The way to crush the bourgeoisie is to grind them between the millstones of taxation and inflation.”

– Lenin?

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered.”

– Jefferson

These three quotes summarize State of the Union, and where we are headed as inflation spreads like California wild fires.

My mortgage was sure helpful to me. My credit card makes life a lot easier. It is not merely a plague, if used responsibly. Nobody forced me to over-leverage. And I’m not rich, but I am quite disciplined. If not used responsibly, well, there are available spaces under the overpass.

I teach at a school where college is affordable.

I don’t see widely available credit as a conspiracy. It is like anything else: it can be used foolishly and to excess.

“I don’t see widely available credit as a conspiracy. It is like anything else: it can be used foolishly and to excess.”

Read and understand what John Adams said. Your government is foolishly borrowing on your behalf, and several generations down the road that you have not even seen yet. The Fed was responsible for making that credit available so we could live beyond our means and spend unproductively.

You had better look again if you think there is space under the overpass. That prime real estate was taken years ago, especially on the west coast. Maybe you can get a spot in Alaska if you want west.

A cardboard box on the lower coasts is the next best option. But hurry.

I spent a good bit of time in Trinidad working in the 1990’s. Lovely place if you are fortunate to be staying at the Hilton in Port of Spain (biggest city) like I was.

My time there was to research a suitable location to build a large anhydrous ammonia plant for a foreign owner (U.S. based), so I got to see the country side….

The thing that impressed me the most was that to be considered “middle class” in Trinidad meant that your shack had tin sides instead of cardboard. But all children went to school wearing proper uniforms.

Wait, you mean free speech on Twitter won’t save all of us? I continue to be amazed at how our founding fathers’ statements are so relevant yet ignored today. We are now behind the UK on the Economic Freedom Index. Rolling in their graves is a massive understatement.

Paid off my mortgage at age 38, never borrowed another penny for anything and never looked back. I still see revolving debt as revolting debt.

Are you still driving that old, but probably paid off, P-1800 Volvo?

Definitely.

Great car!

Ditto here except age 37. Best feeling in the world when the debt monster leaves.

Good for you!

Here (San Diego) there is lots of very visible (mid-rise and high-rise) housing being built and opened. It seems a mixed bag, not the worst possible scenario. Lots of nice cars are visible. People aren’t driving old wrecks like they used to be. But I can’t see their balance sheets. Plenty of homeless are here: it seems a tiered society.

My folks and I both got houses here at pretty good times. Nice to be on that track. But it always meant making sound decisions to keep it and build equity. For me that meant going without, at some stretches.

Normalcy Bias is one of the greatest narcotics of all time. I remember the same stories about San Diego in 2008.

A favorite joke about the present raging inflation.

A customer purchases a couple of bags of groceries at the local supermarket. When time comes to pay, the customer pulls out a bill from his pocket.

“Can you break a hundred dollar bill?” the customer.

“Yes I can,” replies the checker, who takes the $100 bill out the customer’s hand. “You owe me five dollars more.”

1) Personal Saving Rate are down from 34% in Apr 2020 to 6% in

March 2022.

2) Our standard of living was higher in the 60’s and the early 70’s

than ever before.

3) The saving rates were rising for decades until 1975.

4) If u connect the dots between the highs they aim at Apr 2020 peak.

5) The lowest saving rate on record was 2% in July 2005.

6) Between 1975 and 2005, for 30 years, saving rates were falling, along

with interest rates.

7) If u connect the highs of the descending saving rates they aim at

negative rates.

8) Negative saving rates during inflation…what does it mean.

Michael, that means that the Debt Slaves are borrowing their butts off like Wolfburger said!! And buying less per Dollar due to inflation and getting less satisfaction a la the Rolling Stones. Ah, Einstein’s definition of insanity is well at work with the American Consumer: spend all you got and then pile up the debt to spend what you ain’t got. Good analysis above, Michael. Understandable and very fitting to the times we are in.

All of these spending trends, however, are about to hit a brick wall when adjusted for Fed Fed Inflation. Fourth Quarter, 2021 was all about the hoarding of materials and finished goods at the reseller/producer level in order to try to beat the supply chain constipation and to avoid some of the inevitable price hikes in the supply python. Imports went nuts while the stronger Dollar helped to put a kibosh on our struggling exports, so negative GDP may print again in the Second Quarter, stay tuned, Sports fans.

For the current quarter, a country (USA) that freezes another country’s foreign exchange reserves does not enamor itself to overseas markets that would have to buy Dollars (way up in relative value!) to do so. The Dollar rocket should run out of fuel any trading day now. Down on Powell Pablum Day!!!

David Young, Q1 2022 was not negative . The economy is slowing. It might accelerate, slow down again, pickup speed…until the crazy stock market goes vertically up, when everybody move in.

Good catch, Michael Engel. Rate of change is what recessions are about, and I misspoke when I did not use the term, “GDP Growth”, which was a negative 1.4% in First Qtr., 2022, at least on this print from the Numbers Smiths in Washington, from 4th Quarter’s abnormally high quarter-to-quarter growth due to hoarding of inventory and ballooning Net Imports. A receding in these quarter-to-quarter stats is what I meant for readers/investors to look out for, negative GDP Growth from First Quarter, 2022 to Second Quarter, 2022 and beyond. Growth is equivalent to rate of change, and deceleration is usually observed on a quarter to quarter basis for GDP.

The probability of recession blooming as we converse is quite high in a debt saturated economy and financial system and Central Bank and Government when internal and external shocks occur to affect the spending habits and capabilities of consumers. The Fed has not only pulled away the punch bowl, it intends, at face value, to put it empty up in the attic.

I was in finance/financial analysis for almost 50 years, I should have been more precise and accurate. But still, batten down the hatches.

Online definition of Recession: “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters”.

The dollar rocket is headed MUCH higher. The DXY is just south of 104 on its way to 120. This will absolutely destroy American exporters at the same time it bankrupts foreign holders of USD denominated debt. We are headed for an epic economic catastrophe!

Prices up 13%, wages up 3%.

Where does the difference go?

Water and money seek their own level.

Water flows downhill.

Money flows uphill.

“Whoever controls the volume of money in our country is absolute master of all industry and commerce … and when you realize that the entire system is very easily controlled, one way or another by a few powerful men at the top, you will not have to be told how periods of inflation and depression originate.”

– James A. Garfield

“We disapprove of slavery and the cost of the maintenance and upkeep of slaves. We prefer our English model in which we control the issuance of currency, and control of money, it allows us to control labor without the cost of maintaining it.”

– Anthony de Rothschild

“Advocates of capitalism are very apt to appeal to the sacred principles of liberty, which are embodied in one maxim: The fortunate must not be restrained in the exercise of tyranny over the unfortunate.”

– Bertrand Russell

“The issue which has swept down the centuries and which will have to be fought sooner or later is the people versus the banks.”

– John Emerich Edward Dalberg-Acton, 1st Baron Acton

Thank you unamused.

To add to the quote by Garfield, it was made in 1881, two weeks before he was assassinated. He was in office 200 days.

On 21 April 1933, FDR wrote to Colonel House, “The real truth of the matter is, as you and I know, that a financial element in the larger centers has owned the Government ever since the days of Andrew Jackson.”

The Federal Reserve System controls the economic blood flow, and thereby life of the USA. Plain and simple. That’s just how it will be until I no longer process oxygen. C’est la vie.

I can only wish you would have included the dates of ALL of your very very relevant quotes una…

Thank you for continuing to help folks like me to continue to increase our understanding of the economy and our ”possibilites” for safe and secure ”investment” for our children and especially grandchildren and spouses…

LOVE the results of the work of THE Wolfster!!!!!!!!!!!

AND will report I ”CONTRIBUTE” twice every year when clear about “”OUR”” savings for my spouse,,,

Sure, it’s not that much, but, IMO, if everyone on here did what WE do, Wolf would be at least able to continue…

Thanks again W.

As BEN said neither a borrower or a lender be ,has worked well for me .Grandma said never buy anything you can’t pay for = wisdom

good one Flea,,, and will only add something my similar GM said, and I passed on:

”Don’t agree to ”regular payments” unless you have ”regular income.”

Having been there and done that otherwise,,,

I can really and truly encourage ALL to pay attention to that basic concept…

Agree with this wisdom, but sometimes the corrupt rent seekers in the US system force massive debt on you anyway, even the thrifty. Medical debt is the worst, my cousin is a hard worker and saver, never got in debt, but had a daughter premature stuck in a NICU for a few weeks and somehow the hospital and insurer colluded to to say his expenses were “outside the network”. Boom, medical bills of over $250K–bankruptcy. Same thing with an old friend, military, 2 tours of duty to fight for America, never in debt, one credit card minimal expenses. Wife back home? Sleeps around, divorces him and HE becomes liable to pay for alimony and the kid she has with another guy she won’t identify. Divorce court makes him pay both alimony and child support for the other guy’s kid. Instant poverty and debt. So good advice, but there’s so much corruption in United States that the rentier groups can force debt on you anyway. If you want to really be thrifty and avoid debt, best thing may be to become an expat out of the USA somewhere else where they don’t dump debt on you. Almost all other developed countries in Europe and Asia (even less developed in S. America) don’t force you in debt for a medical bill or divorce, you can actually save money for the frugal.

You’d think the hospital would have told your buddy he was out of the network BEFORE the expenses were incurred. That’s the problem with medical care today. No transparency. No courtesy or forethought.

“That’s the problem with medical care today. No transparency. No courtesy or forethought.”

Yep, so true, couldn’t of said it better. It’s organized fraud and robbery esp of middle-class Americans who have the savings for them to steal. (Or even the upper-class with enough money to seize but not enough to buy a member of Congress with lobbying bribes.)

But yet all they’ve wanted to do the past two years is save you…… from yourself….. right!

1) Small central banks adopted the Yuan to their currencies basket, besides dollars and the Euros..

2) The polarized elite might punish Tesla for promoting promoting

free speech.

3) We are out of the stupid, unprofitable European market. Four doors sedan are too small for me. I am married Chevy and Cadillac Lyriq ev.

4) Ford is fully committed to pickup trucks, ev and self driving cars.

5) Most consumers are still infatuated with inexpensive stuff from China and cars that move from point A to B.

6) Toyota have options for small cars, suv, pickup trucks, Ice, hybrid,

ev from Lexus to Corolla and Camry.

7) A global recession might punish Ford and GM for their untested malnvestment.

They learnt nothing from the Great Recession.

It is about the distance between the image of a lifestyle people are anchored to (feel entitled to), and the economic realities. That is a long term thing. It is not 1967, or 2007. Realizing that is the path toward a meaningful and stable life. But one must back up and plan on a pretty long time horizon, to set the levels of debt to achieve sustainable value.

My caffeine jolts in this hurricane of supposed inflation cost me 2 cents per dose, not $4.

1) SPX daily : a small, hesitating doji.

2) SPX daily, Heineken Ashi : buying tails. // SPX weekly, candle : a large selling tail (or buying at the bottom, a stopping action). Much larger candle on the same volume. Something is wrong. // SPX weekly, Heineken : buying tails.

3) NDX daily : a small doji. Heineken : buying tails. Larger bar on smaller

volume : something is wrong. // NDX weekly : a large selling tail at the bottom, much larger candle, same volume. Heineken weekly: buying tails.

4) IWM daily : a tiny bar, half the size, on higher volume. What’s going on.

IWM Heineken : buying tails. // Weekly : large selling tail at the bottom, larger candle on the same volume. // Weekly Heineken : three buying tails.

5) SPX monthly, log : take a line from Apr 2010 to Feb 2011 to Jan 2022 highs.

Take a parallel line from July 2010 to May 2022 low.

6) We don’t know what will happen next, but on Fri close SPX is > support.

May 2022 low is a spring under Feb 2022 low.

7) For entertainment only….

8) What concern do u have when all women and children have been

evacuated from the steel plant.

Every market cycle has stagflation at the top. Seems like customers borrow more to buy less is what happens right as a recession hits.

I don’t even remotely see a recession yet. I had to run some errands today. The traffic was as bad as ever, and there were cars spilling out onto the street from all the Starbucks and coffee house drive-thrus with a lot of single occupant cars happily idling along, burning $5.60 per gallon gasoline like it’s free.

As Wolf says, “this is the most grotesquely overstimulated economy in history, due to the most reckless FED in history.” How these disgusting, immoral, fraudulent creeps can even look in the mirror let alone show their faces in public is beyond me. But I never understood psychopaths.

Debt, people want to get out of the house, to get something “good”,

to be serves. The longer the line, the longer they delay driving back to the house.

Every single move the FED and .gov make benefits the wealthy, yet they’re sold as benefiting those who they hurt the most. The inflation these monsters have created is now eating the poor and middle class like never before seen. It would be bad enough when house prices, rents, autos etc. were based upon wages, but this insidious inflation took off well after the bubbles in these assets had peaked. This is the most toxic brew ever created in the history of the US. These are the worst, most corrupt politicians the country has ever seen, by far.

What if people are out of the workforce because they are surplus to the economy as it is arranged? And that the debt they take on to sustain as consumers only mask that even more people are surplus by keeping them busy for a little longer?

Less production follow less consum and then there is even less need for workers.

What you missed in the article is that there is huge DEMAND for workers. But lots of people don’t want to work, for whatever reason.

At the time beeing with easy credit. Without easy and ever expanding credit? Credit expansion have pulled forvard demand and consumption, but aftewards?

There may also be a mismatch between what is in demand and what is available of workers.

One more thing. Thanks for a great site and great work!

I do greatly apreciate the information and insight you provide!

But Wolf, if you believe economists, (which I admit I don’t always) DEMAND always equals SUPPLY.

So we COULD say: Lots of employers, for whatever reason, don’t want to pay for what workers, for whatever reason, want to get paid.

Nonsense. All of it. First read about supply and demand and the point when they’re in “equilibrium,” and then read about what it takes to get to this equilibrium (and that whole theory has been discredited by how the real world operates). Then look at the rest of your comment.

Another great article with lots of good comments. Thank you WolfR.🦊🦊

Wolf, I’m trying to follow your inflation logic. I’m having a problem.

You would have CONVINCED me if you had said: The SAME number of cars of about the same quality, sold over a past year was just like it has been the year before, but WOW auto loan balances jumped up by 13%–which is the inflation figure you seem to favor. I would have said “WOW, that is good evidence to show that the dollar seemed to take a dive of 13% over a year if the SAME number of vehicles, of SAME quality now ccost 13% more.

But that’s NOT your claim. You say sales volume went DOWN BY 16%/year over a period where loan balances went up 7.6%. But 16% lower supply does strongly suggest possibility for a Economics 101 reason that lowered supply goes with higher prices.

Of course that does not PROVE that all was caused by 16% lower supply. Could be a combination with some inflation. In addition, the cars that were sold at higher prices were likely to be the higher quality ones, because that’s where they probably put whatever chips they did have in inventory to get the maximum total sales revenue.

Given your evidence, what makes you so sure it’s ALL caused by inflation? I only claim to know that there are two likely factors–inflation and supply. When we get back to full supply we will know how much of each.

Ralph Hiesey,

For a whole year in your comments, you have denied and downplayed and brushed off the causes of this inflation that I have piled up here. And so here we are now at 8.5% CPI-U and 9.4% CPI-W. You can believe whatever you want. If that works for you, great. I will make no effort to change your beliefs. That’s up to you.

“A plunge in the number of vehicles sold.

A ridiculous spike in vehicle prices.”

But the $0.50 microprocessor ‘shortage’ is what brought the billion dollar industry to it’s knees (as Ford’s stock doubles)

Bruce,

“(as Ford’s stock doubles)”

Correction: Ford’s share price halved, not doubled, since January 2022, now at $13.50

Thanks, Wolf.

I hadn’t checked the recent decline, but was going off of the 2020 lockdown retraction to $5, then ballooning to $20 as headlines screamed ‘chip shortage’ and ‘auto layoffs’.

The chip shortage is still a huge problem, not just for automakers.