Home prices fell in Vancouver, Ottawa, and Montreal; were flat in Toronto, other cities for the first time since 2019.

By Wolf Richter for WOLF STREET.

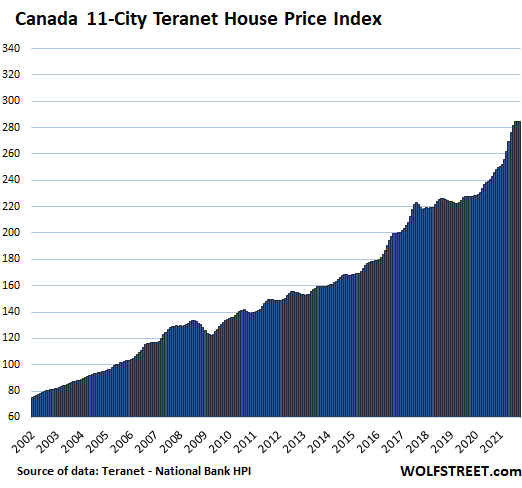

So this is something that hasn’t happened in the Canadian housing market since 2019: The Teranet-National Bank House Price Index for October, released today, failed to rise from the prior month.

The index for Vancouver, a red-hot housing market, fell for the second month in a row, something the market hasn’t seen since September 2019. The indices for Ottawa and Montreal also fell. The index for Toronto was flat for the month, as were the indices for some of the other cities.

What has changed that caused this “pause,” as it is now being called, in one of the biggest housing bubbles in the world?

The Bank of Canada got hawkish.

For a year now, the BoC has repeatedly cited the craziness in the Canadian housing market – a historic spike in home prices – the result of the BoC’s crazy asset purchases and interest rate repression.

The BoC started tapering its purchases of securities a year ago by ending its MBS purchases and tapering its purchases of Government of Canada bonds. It then shed nearly all its repos and short-term Canada Treasury bills, ended other smaller programs, and tapered its GoC bond purchases multiple times. Then in October, a suddenly hawkish Bank of Canada ended QE entirely and surprised markets by moving the next rate hikes forward. Meanwhile, inflation in Canada hit an 18-year high.

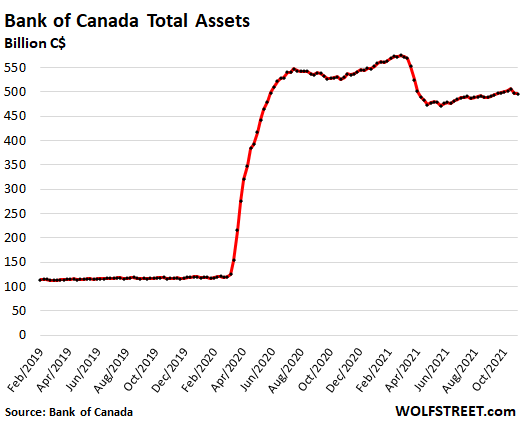

Total assets on the BoC’s balance sheet, as of last week, fell to C$496 billion, down 14% from the peak in March.

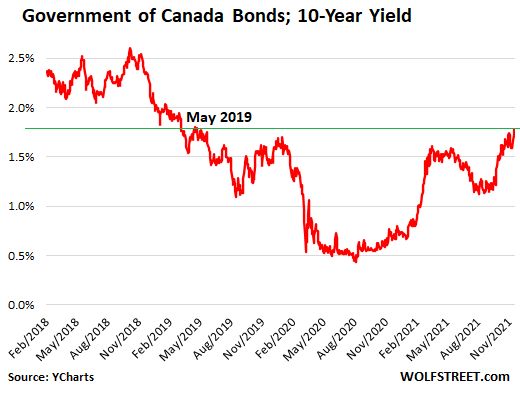

Yields of Government of Canada (GoC) bonds have risen. And banks have raised their mortgage rates in parallel. The 10-year yield of GoC bonds has tripled in the span of 12 months and hit 1.78% at the close on Monday, the highest since May 2019:

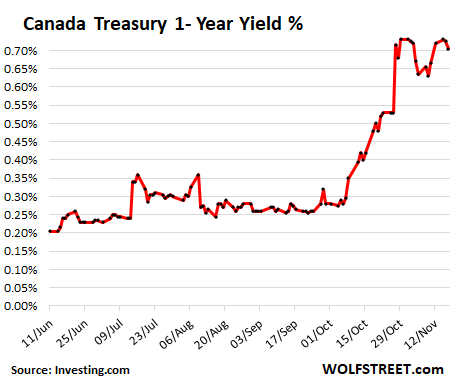

The one-year yield nearly tripled within two months, jumping from 0.26% in late September to 0.71% now:

There is a substantial lag between changes in monetary policies and changes in the housing market. But now the changes in the housing market are starting to show up.

One of the world’s biggest housing bubble starts to, well, “pause.”

In October, the overall Teranet-National Bank House Price Index, covering the 11 largest metros, edged down a tad, the first decline since October 2019, after having edged up by nearly nothing in September. The year-over-year increase got whittled down from a record 18.4% two months ago, to 15.7% in October. You can see the first flat-spot on top since 2019:

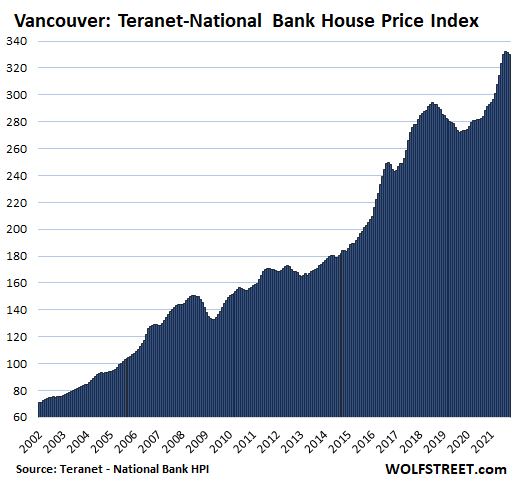

In Greater Vancouver, house prices fell by 0.4% in October from September, after having falling by 0.3% in the prior month. The BoC’s radical monetary policies starting in March 2020 turned Vancouver’s budding housing downturn that had started in August 2018 into another spike. But now the top of the spike is getting rounded off:

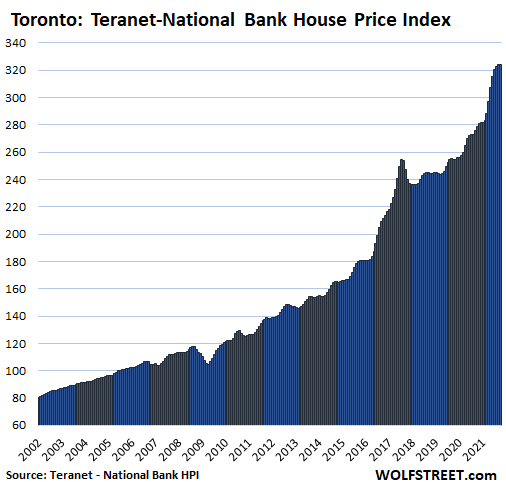

In the Greater Toronto Area, home prices were essentially flat in October compared to September, after four months in a row of ever smaller month-to-month increases. The year-over-year increase was whittled down from 18% in August to 16.3%:

The Teranet-National Bank House Price Index, by using the “sales pairs” method similar to the Case-Shiller Home Price Index in the US, compares the price of a house that sold in the current month to the price of the same house when it sold previously, tracking how many more Canadian dollars it takes to buy the same house over time, and is thereby a measure of house price inflation, which is precisely what the BoC’s radical policies have fueled. But now the BoC has made a U-Turn.

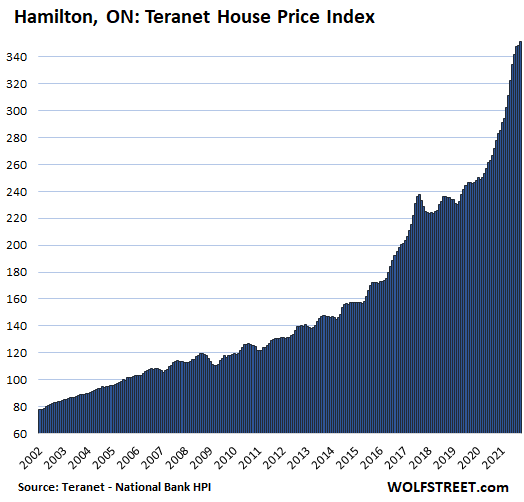

In Hamilton, Ontario, house prices rose 0.9% for the month, after having eked out a 0.3% gain in September, after the majestic spikes from February through July, topping out with a 3.8% gain in June, from May. The year-over-year gain was whittled down from over 30% in July and August to a still nutty 26% in October.

The charts here are on the same scale as Hamilton. As we go down the list, the remaining markets have smaller two-decade house price increases, resulting in larger white spaces above the curve.

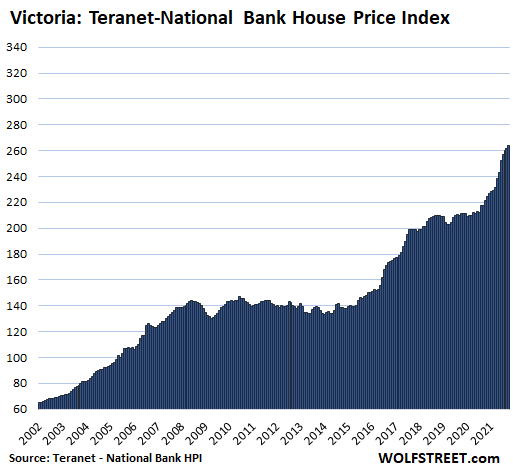

In Victoria, house prices rose 0.7% for the month, down from a 3.6% increase in June. The year-over-year increase was whittled down to a still mind-boggling 18.9%. Note how the housing market had flattened from 2018 through June 2020, when the effects of the BoC’s money-printing took effect.

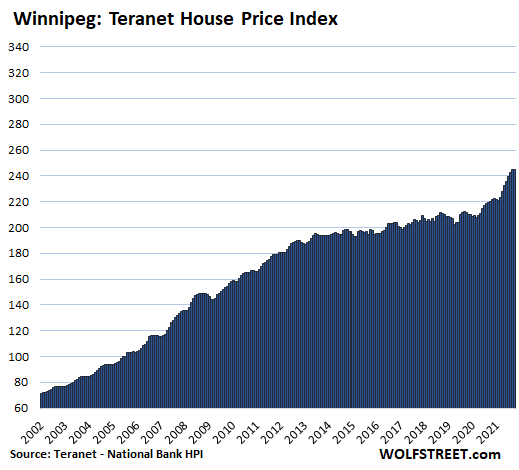

In Winnipeg, house prices remained flat in October, and were up 10.8% year-over-year, after having gone essentially nowhere following the housing boom through 2013:

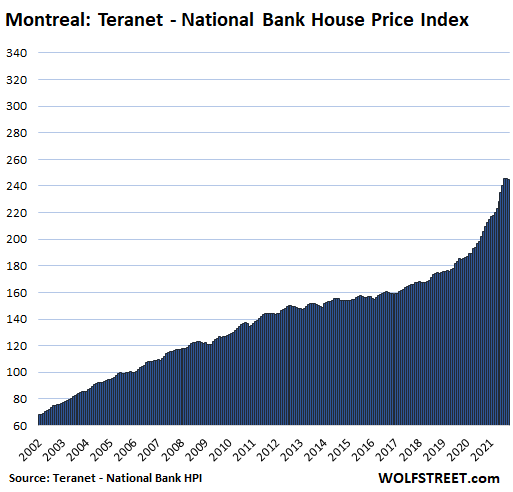

In Montreal, house prices fell by 0.2% for the month after having been flat in September. This whittled down the year-over-year gain from 21.6% in August to 17.1% in October:

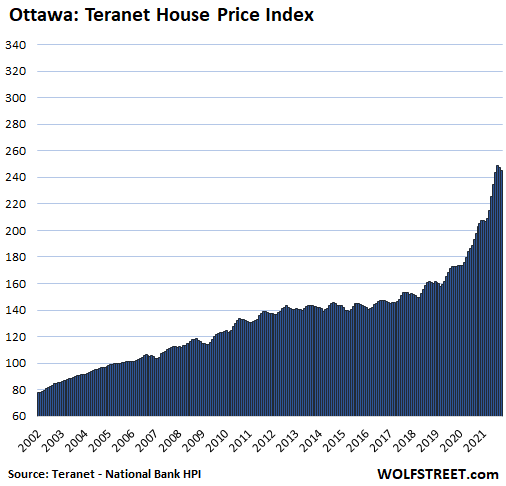

In Ottawa, house prices fell by 1.0%, the second month in a row of declines. This whittled down the year-over-year gain from 28.9% in July to a still mind-boggling 20.9% in October:

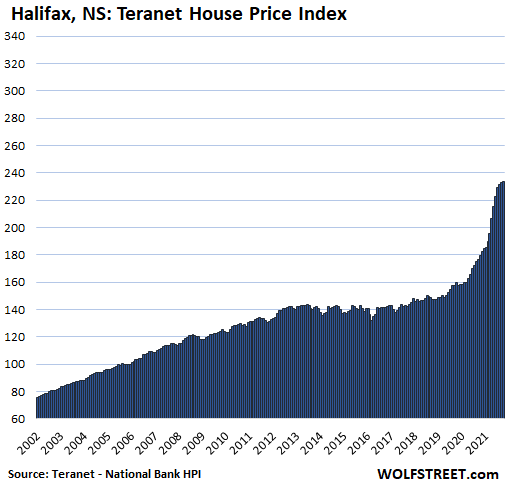

In Halifax, house prices rose 0.5% for the month, down from the crazy gain of 5.4% in April. The month-over-month gains have now declined six months in a row. This whittled down the mind-boggling 33.4% in July to a still mind-boggling 30.3% in October:

In Quebec City, house prices inched up 0.2% for the month, and were up 8.4% year-over-year.

In the oil-bust towns Calgary and Edmonton, the last two cities in the Teranet index, house prices had their bubbles during Canada’s oil boom. But since 2007, not much has happened until the BoC started its money-printing mania in March 2020, and some of it ended up in those cities.

In Calgary, house prices inched up 0.2% in October and were up 8.5% year-over-year. In Edmonton, prices inched up 0.3% for the month and were up 5.5% year-over-year. But with house prices barely above the oil-bubble peak in 2007 in Calgary and below it in Edmonton, the cities don’t qualify for inclusion in this crazy list of the most splendid housing bubbles in Canada.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Noooooooooooooooo!!!!!!!!

Been reading about price reduction in Vance for last 10 years.

Didn’t happen.

I don’t think we need to get too excited with this small dip and it does not really signify anything.

Lets revisit this after 6 months.

these increments…may signify a change of direction, but they are so small …tiny …itty bitty rate changes

We havent seen anything yet. The bond market in the US will be where the blood letting will first occur, and it will be geometric .

Exactly and it will be a rude awakening based on the tough time the US is having in bond auctions.

Anything but up at this stage becomes a problem quickly. MSM is mentioning inflation now. People have reason to believe rates will rise. Now rates are rising.

I see a nice inverse head and shoulders on that 2 year bond chart. Tells me rates are about to spike.

I can not see how rates don’t rise from here. The last US CPI print had a big impact on sentiment. And now Europe is joining the party. All eyes are now on inflation, if it doesn’t retreat soon there will be a stampede to sell.

Also, looks like a seasonal dip, here’s Toronto:

https://www.zolo.ca/toronto-real-estate/trends

To find for some different Canadian cities just replace the city name in the URL.

Hahahaha, there was NO seasonal dip last year — on the contrary. So if it’s in fact a seasonal dip this year, it means that the exponential Covid spike is over, and whatever comes now, with higher interest rates and sky-high prices and all sorts of affordability issues is different than the situation over the past 20 months. That much we know already.

I refer to the Toronto chart.

Last year averages went from 1MM October ’20 to 850K Jan ’21.

In the last month, averages are down about 6%, and barring catastrophe/black swan we should be heading for ‘normal’ lows in January.

Definitely I agree that the market is overvalued, possibly as much as 100%, and that should interest rates sharply rise, a lot of buyers in recent years are going to get a real shock. Most of them probably don’t even remember when 6% was normal.

They also wouldn’t remember when condos and exurbia prices dropped by up to 50%, and sat for months or even years without a serious bid.

Hmmm… it is curious to me that the Bank of Canada is letting its Assets rise over the past six months. Assets may be down 14% since March… but when the BoC first started tapering they dropped them by almost 19%. They took their foot off the brake sometime this summer it seems.

SpencerG,

The BoC shed nearly all its categories of assets other than Government of Canada bonds. It now stopped adding to the GoC bonds, after shedding all its other stuff. This created the funny-looking overall shape that you found so objectionable. Here is the detail by category of asset:

Wolf,

Thank you for the explanation… and chart!

Wolfe, I read somewhere the Canadian central bank bought gold recently. Do you know if this is true?

Sorry, I gave you an e in wolf

No it’s not true. Marin Katusa was flat wrong.

Jacob Hunt,

Doesn’t look like it from its holdings listed on the balance sheet. And it doesn’t have any reason to buy gold.

The only Canada government buys of gold would be the Mint for producing and selling retail coins.

In the handful of high end east and west coast zip codes I am involved in, the market is still very hot with inventory continuing to hit new lows. The spring should see another leg up on the east and west coast.

However, in high end metro Detroit zip codes, I am seeing a very substantial slowdown. In that area homes that would have been snapped up in hours are now sitting with no bids. This is a problem that could spread.

So, the picture is now mixed. Perhaps Canada looks like the Detroit story?

Windsor, ON maybe. Vancouver, BC like Bloomfield Hills? Probs not.

The picture on Vancouver Island is exemplified by my city of Nanaimo. The ‘benchmark’ (median) price for a single-family home is Ca$757,300, up 29% over October 2020. Sales have declined by 23% because of the dearth of available properties (46% fewer listings than a year ago).

Condo inventory is 63% down over October 2020 and townhouses 39% fewer.

Other cities on the Island show similar trends.

The buying won’t stop until the rate hikes actually show up. Halifax is the alarm bell to watch. That spike over the last year is most likely fueled by people leaving the insane Ontario market since they can move data jobs to a cheaper market with what I found out from how easy it is to work remote in todays world. Halifax itself couldn’t fuel that bubble, it has to be money moving out of other cities that are unaffordable.

In the rural Maritimes, every property is still being sold within 3 weeks, going for asking or above. The only limit is that contractors are maxed out at the current new building/reno rate due to lack of labour and lack of materials. The buyers appear to be largely from urban Ontario and BC, either retirees or with at least one partner able to work remotely.

SocalJim,

Just curious, how high do the RE assets you hold have to go for you to sell, 2X, 5X, 10X, ….

He might not want to sell at all if he rents them out. I once asked him if he believed the appreciation would continue indefinitely. Don’t recall the exact answer, but the idea was that at least as long as inflation continues, yes.

Uncontrolled inflation leads to collapse. And we are definitely in a form of collapse, which leads to political outcomes. So if you are in it, what do you do, and at what point.

Price doesn’t factor into when the Chinese buys or sells although they buy in a frenzy when prices skyrocket. They all buy at the same time and all sell at the same time. The Chinese are the only buyers of new homes in southern Ontario. Presently the Chinese are all still buyers.

Canada has second biggest housing bubble, per link.

https://wolfstreet.com/2021/06/24/central-banks-did-it-wont-admit-it-top-oecd-housing-bubbles-are-1-new-zealand-2-canada-7-usa/

Number one is New Zealand. Large interest rate rises are coming here in the next few months, to stem high inflation. Could be messy.

It won’t be as messy as Australia, whose politicians steadfastly continue to promise low interest rates forever.

They were saying that here in NZ too…interest rate rises years away…but inflation crashed the party and the punchbowl has to be withdrawn very quickly.

I suspect Australia’s central bank could be forced into a similar position, bringing forward interest rate rises, which will likely prick the property bubble…watch inflation.

I saw Lowe recently write that luckily this inflation storm will miss us…. lucky.

Canada and New Zealand seem to be starting to realise rates might have to rise. Australian political system is lockstep with the US. Head in the sand

Come on now, get with the MMT craze – now that electronic money has been invented, you don’t need a wheelbarrow to buy that coffee at Timmy’s.

Adam Vaughan will find a way to help the foreign investors maintain their property values.

Adam said on live TVO that he will not let Canadian prices go down, and that Canadian real estate is good for foreign [money launderers], but bad for [hardworking and honest living] Canadians.

That sounds about right ……

GZ

I agree; I too feel badly for the “hardworking and honest living” real Canadians. Very discouraging when pillagers from outside your country or state (in this case, province) come in and shoot housing prices to the moon.

Those charts are quite impressive. Not much of a pause…but I hope it’s a turning point towards something that matches middle-class incomes.

That raises the issue, who do rate hikes hurt, (Canadians) while foreign buyers come with cash..

The ones competing with the Chinese for homes and lying about their income.

Recently bought and sold in the Ottawa market. Demand is still strong but seems well down from the mania back in the winter/spring. Comparables look slightly up from what I bought, but within the margin of error. Was offered 1.15% variable/2.4% fixed for a 5-year term. It will take 8 rate hikes in consecutive quarters to end up worse with the variable. A majority of Canadians are now taking variable and playing a game of chicken with the BoC by calling out their jawboning.

It is kind of pathetic that a central bank that has a mandate to guard the alue of the currency encourages home prices to go up 3X or 4X in 20 years.

It’s a long term problem. My parents built a small brick home just before I was born for $8800 in 1954. To build it now would be about 20X that. It’s all a big lie.

The Fed is in constant violation of 2, if not 3, of its “mandates”.

Read today’s WSJ “How the Fed Rigs the Bond Market”

This era will go down as the most irresponsible one of our financial lives, IMO.

But the problem is, how do you sell house price corrections to those who have little else than the equity in their homes.

How do you get re-elected if anyone who bought a house within the past, I dunno, 5-10 years, might be phk’d if variable rates went to 5% and fixed to7.5%?

Problem of overvaluation has to correct, but only when a clear alternative bogeyman can be found… ( Thank You China!)

In clarification, I mean China’s real estate debacle.

Who cares how to sell it. I’ve chose not to participate knowing I’d be supporting these criminals by participating. It isn’t easy and sometimes I feel foolish, but I sleep well and still have all my hair. We need adults that say no and do what is right.

Wage inflation material inflation fuel increases really not a lie all leads to higher taxes that’s what this is all about

– Inflation is still lower in Canada vs. USA,

– we just had a federal election, Liberals have a strong minority; provincial elections in Ontario in 2022 could see return of Liberals there, Alberta could see an early election given very poor approval ratings of Conservative provincial government (and see the re-election of the lefty-NDP in oil country).

– Big natural disaster in BC will see huge investments in infrastructure.

– big push for more immigration, possibly 500k, given the Covid backlog.

– lots of talk of housing prices, but also look at rental prices, rising everywhere.

– in other words, it’s in no ones interests for housing prices to fall.

Never is, until everyone has too much to lose from the the alternatives.

Then the puritans arrive.

The disaster in BC is big enough to take down the reds in Victoria and Ottawa. The earliest that things could revert to near normal is next summer at the earliest and that is only if everything goes right. The big unknown is the underlying ground under miles of submerged highways. 3 million in Vancouver are going to see the results of being led by socialists with shelves already bare and the worse is yet to come.

Because rent isn’t included in the inflation rate like in America.

Rent accounts for about one-third of CPI via two rent measures, “owner’s equivalent of rent” and “rent.”

1) TSX, up from Mar 2020 low @11,173 to Nov 2021 high @21,796. TSX bubble might cont if WTI will rise to 100-120.

2) A reaction of 38% will send TSX to Feb 2020 high.

3) A reaction of 62% will send TSX to 15,300.

4) In 2014, when WTI and WCS plunged TSX was badly stung.

5) The low was in Jan 2016 @11,531, slightly above Mar 2020 low,

6) TSX downhill roller coaster slide might start in 2022.

7) Toronto RE & WCS will turn down, too.

8) USDCAD will rise, breaching the daily cloud.

Notes:

“WTI” is West Texas Intermediate (petroleum)

“WCS” is Western Canadian Select (petroleum)

The futility of pumping up asset prices only to watch them collapse again.

It seems futile to me, global policymakers seem to like it.

Real estate – the wealth is there and then it’s gone.

1990s – UK, US (S&L), Canada (Toronto), Scandinavia, Japan, Philippines, Thailand

2000s – Iceland, Dubai, US (2008), Vietnam

2010s – Ireland, Spain, Greece, India

Get ready to put Australia, Canada, Norway, Sweden and Hong Kong on the list.

It wasn’t real wealth, just a ponzi scheme of inflated asset prices.

They don’t just like it, they love it.

The neoliberals were always going to be in trouble with neoclassical economics.

They don’t know what real wealth creation is, and associate it with things like making money, rising asset prices and trade.

That explains it.

“The futility of pumping up asset prices only to watch them collapse again.

It seems futile to me, global policymakers seem to like it.”

Hardly a collapse as of yet.

But I think we agree, that Central Bankers, bolstered by beliefs in their own brilliance, enter into markets with a fist full of theories…..but never seem to have the exit plan. And once they attempt, what they caused becomes undone.

Central Bankers seem to believe in MAGIC, rather than

“For every action, there is an equal and opposite reaction.”

The cards have been dealt by the Fed.

Now we have to play the game. History points to hyperinflation.

B

Bruski,

The Fed sits on $8.5 trillion in bonds that it can sell. It can sell them whenever it wants to. It can announce that it will sell them, without even selling them. Any suggestion that the Fed will actually sell its bonds will cause long-term yields to spike, and any follow-through on sales will cause long-term yields to spike further, and the bond sales would remove liquidity, and bring down the money supply and bank reserves, and asset prices would crash, and this would very quickly remove the fuel for inflation.

There is no question that the Fed CAN stop inflation if it wants to because it now has that huge pile of assets it can sell.

The only question is at what point it WANTS to stop inflation.

And the Fed, representing the banks and the wealthy, does not want hyperinflation. No one wants hyperinflation outside of real tried-and-true gold bugs. And so we’re not going to get hyperinflation. We’re going to get as much inflation as the Fed allows.

It seems Dec 2018 and Mar 2020 showed they are unwilling to let asset prices crash. Asset prices have become a matter of national security so there is no political desire to threaten that even if that means letting inflation run hot.

What if no one wants to buy Fed’s bonds?

Who is going to buy 8.5 trillions of bonds anyway?

Rational theories abound and lots of them make sense but how would they work in practice?

I think this QE thing will go down in history like Havenstein’s belief in Weimar Germany that the inflation was caused by the fall in the external value of the mark against foreign currencies and that the role of the Reichsbank was to print sufficient money to sustain the higher price levels.

Looks ludicrous in hindsight but at that time was a theory that made sense, a little like QE today.

Money and economics looks like rational constructs because they involve a lot of numbers and math but in reality is all about human psychology and trust, it can turn and vanish quickly and suddenly.

Eastern Bunny,

The Fed won’t sell $8.5 trillion in one day. But if push comes to shove, it might sell $300 billion a month, every month, for a year, and long-term yields will spike, and the 10-year Treasury yield might go to 6% or 7% or 8% and the 30-year yield might go to 10%. This will be a bond massacre (bond prices plunge as yields spike).

And guess what? At that kind of juicy yield, the entire world, including me, will be jostling for position to buy these bonds.

Yield fixes a lot of things if it’s allowed to rise (meaning if bond prices are allowed to drop).

And we will buy those 10-year and 20-year maturities because we know if the Fed is selling its bonds, it’s going to knock inflation down eventually, and then when inflation goes back down a year or two after the bond massacre, those long-term bonds that we bought with a yield of 8% will pay us 8% every year for 10 years or 20 years, until they mature.

The 30-year long bonds that people bought at the peak of inflation in 1980, with a yield of 15%, when inflation was 15% and surging, were a courageous bet at the time but turned into one of the best bond deals ever: they paid 15% every year for 30 years. A $1,000 bond paid $4,500 in interest over its life of 30 years, and at maturity, you got the $1,000 back. And there’s zero credit risk because US cannot go bankrupt because it controls its own currency. The only risk was inflation (and even higher interest rates).

At what point in the selling would the unsold portion of the balance sheet become impaired, and is the Fed holding onto a liability?

This assumes the quality of the bonds the Fed holds – mostly impaired mortgage backed securities – are saleable. Suspect the Fed has been buying the worst securities, many of which would only sell at a steep discount if marked to market.

RP,

The Fed holds Treasury Securities = $5.6 trillion and “agency MBS” = $2.6 trillion. These MBS are “agency MBS” which means they’re guaranteed by the government/taxpayer, and the Fed is taking no credit risk; the government/taxpayer is taking that risk via Fannie Mae, Freddie Mac, and Ginnie Mae, which issued those MBS and guaranteed them.

https://wolfstreet.com/2021/10/28/feds-assets-from-crisis-to-crisis-to-raging-inflation-balance-sheet-update/

and…

The Fed can sell it’s debt paper. So long as there is a solvent, liquid, cash buyer.

It is a dangerous game, trying to create “wealth” by printing money.

So much misallocation into fake value by chasing the trend with algos and FOMO.

If the wobbling top falls over, the only buyer of Fed paper will be the Fed, eating it’s own tail.

Just read money supply in USA still growing at 12.8% (about 2X what it should be) plus money velocity is picking up. Fed did too much. Government gets a free lunch borrowing at -6% for a while until people catch on adjust behavior.

I’m not sure…

If a lot of people default on their mortgages and the banks have to eat the loss, couldn’t you call it some kind of “reverse money printing”? That money is gone with the wind.

“That money is gone with the wind.”

It can from the wind, and it will go with the wind.

The US is nowhere near hyperinflation, unless by “hyperinflation” you are referring to something like 10% annually.

A massive collapse of the global asset bubble is a lot more likely. No one can stop that when psychology turns, as that’s what is holding it up.

Seems helpful to watch Canada forerun the tapering, interest hiking and real estate bubbling. They are trying to rip off the bandaid first. US is determined to be last.

Real estate moves slowly, but I still don’t see a crash recipe in Canada or the US. Leveling yes, and maybe small corrections in less desirable zips.

I don’t know. I have seen some incredible two and three year flips and people pocket $300K – $500K on what was $400K properties three years ago. Usually making that kind of money for breathing is a sign of a bubble top.

I do understand when Fed is debasing currency you could make the argument that you should borrow and buy real estate, but you still have to carry it and that could be $2000 per month if you pay close to a million for a property.

I dunno wolf. As I understand, Canada is in a unique position with foreign money (china) buying up real estate. I don’t see a big correction there. Here in the US might be a different story. Canada has been on a tear for a long time. The US has had their real estate market fall apart several times in recent history and seems much more prone to market panic.

I’ve seen small dips like this in the local market a couple months ago only to go off on a rising streak immediately after. My county has hit 46 or 48% yoy increases. Even the absolute turds that have sat on the market all summer have closed or are pending. We’re talking about houses with busted out windows, no access to power, sometimes no roof etc.

Trucker guy,

I can beat your “absolute turds”! I know of a couple (from the Seattle area) who panic bought an undeveloped 5-acre plot. No power, no nothing…not even access! There’s no road to it and the new owners have to negotiate with surrounding land owners for access and build a road at their own cost. Maybe a heliport might be better.

Other than 2008, when has the US housing market “fallen apart”? A correction in the late 1980s and slump in the 90s is the only other close example in recent history, but a long cry from “fell apart”.

Look at the Vancouver chart. There was already a housing downturn brewing in 2018/2019 that then made a U-Turn following the March 2020 money-printing spree.

Google “Man making $40k/year bought $32m in Vancouver real estate via CCP-linked offshore accounts”

“Conservative estimates from a report Combatting Money Laundering in BC Real Estate, indicate there was $5.3 billion laundered into B.C. real estate in 2018 alone, thus leading to an increase in real estate prices.”

Driving around the lower mainland/Vancouver the other day and saw 8-10 30+ story high-rises’ finished and ready for people to move in. There must be another 20-30 that have various states of construction, then there are the 100’s low rises that are being built everywhere. I’ve lived here my entire life and never seen this kind of building going on..not even close!!!

A bond bear market will kill the Canadian housing market just like it will in the US. There is no need for a “trigger event” to make it happen.

In the US, it’s still an open question whether March, 2020 marked the top since 1981. I’d say “yes” but have been wrong before.

Consumer confidence is collapsing. CB’s will be “Hoist with their own petards”.

If something isn’t done quickly, the bubble will run out of steam IMHO. Direct stimulus checks, supercharged UE benefits, and PPP-type free money are needed to keep it going.

The recent 1.2T infrastructure bill and the 1.75T reconciliation bill are spread out over 10 (duration?) years so that’s only about 300B per year. Meanwhile every month the Fed is reducing the rate of asset purchases by 180B annualized (15B per month). So two months of tapering is enough to negate the fiscal stimulus of the recent and upcoming legislation and the massive free-money-handout programs are mostly ended.

Ivanislav:

Good “food for thought”!

Listening to most major media promoting the infrastructure bill hardly mention that the spending is over a ten year period. Which makes the annual spending less than half of our MIC budget.

Not negative against the principle of the bill itself, to attempt to “rebuild our infrastructure”. It is just a drop in the bucket as far as I’m concerned.

Spending it over ten years sounds like a good thing. We don’t need another year of sugar highs and grand one-offs. Spend consistently over the next decade and keep the improvements coming. Besides, as we keep reading there aren’t enough workers to accomplish it all quickly.

All the extend-and-pretend with low interest rates and inflating asset prices must reach an inflection point sometime. The fragility is piling up until an ever-smaller stumble or “pause” might induce sharp panic falls in valuations. How can interest rates not go up (hence markets dive, including realty)? Only by strong inflation. It’s Scylla and Charybidis. I think they are arriving.

Valuations feel like January 2000 or summer 2007 to me: pricing in ridiculous future success. (Not that this Canada data is a strong argument for that, for the moment.) Things, as then, can go south fast. My balance sheet is poised to weather 50 percent drops in everything, which would bring them close to historic valuations. (My house can stand a 95 percent drop before going underwater.) Not that I would be shouting whoopee. This is a product of long term effort, when things were outwardly “good.” Having a home very close to medical resources (and with year-long energy costs) is nice, especially if the government subsidies for aging care falter, in the deluge of all these other assets revaluing. For that, being physically active and healthy is a hedge.

When the tide shifts, so many will be seen swimming naked. Lots of corporate names will do the Enron walk of shame. So counter-party risk is here too. A lot of personal-psychological baselines I think will get a sharp jolt. I want to be ahead of that, inoculate myself with bits of it, as here.

These incremental changes are miniscule.

For those who remember the 70s and early 80s, the prime rate (remember that?) was jumping around 1/2% at a crack, sometimes on a weekly basis.

I shake my head at the hand wringing over 1/4pt raises, maybe sometime maybe over the horizon, maybe….

The Fed needs to re read their mandates….

the 2nd AND 3rd especially……and maybe Sherrod Brown, head of the Senate Finance committee might ask “what the eff is going on?”

Betting no.

Interest rates in Canada still remain very low. What has slowed down price increases has probably been the decline in annual immigration. The recent peak took place in the the fiscal year ended June 30, 2016. https://www.statista.com/statistics/443063/number-of-immigrants-in-canada/

In the fiscal year 2020-21, immigration was down by about 100,000 from 2015-16, most likely due to covid-19. The all time high in immigrants was actually reached in 1913, when over 400,000 immigrants arrived. Two of the immigrants were related to me. In 1913, Canada’s total population was under 8 million and was about 1/5 of its current population.

The only thing I see that can be effective in real “tightening” will not be the result of Central Banks doing it. It will be inflation . Devastating inflation is the only thing that will finally focus their dim vision and cause Congress to turn on The Fed. The Congress is no where close to doing that. Every Q&A session with Powell and Congress is a French kiss love fest with Congress espousing their admiration and gratitude that the Fed has made them wealthy. The Electorate thinks this is a good thing because they are told it’s a good thing. After a Fed love fest Congress gets busy trotting out new scary things it needs to protect the Electorate from. The Fed and inflation ain’t on that list. Ain’t no cure for stupid but pain will change behavior.

What is amazing is that so many people that know money and economics predicted 6 months ago Fed policy was going to cause very high inflation. Some even nailed it to the current rate, so problem must be so big Fed lied about the transitory all along.

My guess is they saw a shot to get real negative rates higher than the roughly 1.5% prior to covid to the current -6%. If you are a debtor -6% solves your debt problem pretty quick.

The explanation for transitory was that inflation will get so high in the coming months that next year’s inflation rate cannot not possibly go any higher. The Fed was not incorrect with that logic.

Multiple governors reframed inflation as not a problem, attempting to jawbone their way into the American psyche to the benefit of their wealthy bankster masters and asset holders across the globe. The Governors were wrong to think they have any influence at all over the regular American’s psyche and inflation is proving to immediately be completely unpalatable. The coming elections will be Americans voting with their wallets and not their hearts for the first time in a long time.

The Economist at the Fed (Powell is a lawyer) cannot recognize Milton Friedman and the Exchange Equation which Milton summed up in a nice little ditty.” Inflation is everywhere and always a monetary phenomenon”. To recognize The Exchange Equation would undermine their Keynesian Religeon which they define as spending and printing does not matter. They they claim that supply chain inflation is a special class of inflation. Bullshit. Their is no supply chain inputs into the Exchange Equation. As the very practical professor of economics Dr Hanke at Johns Hopkins likes to say when discussing inflation ” it’s the money supply stupid”.

So help me understand this Doctor. In the 70s there was no printing press or internet. So was the full cause of inflation the oil embargo? What else caused a once in a generation event if not the full press of Trillions being helicoptered to the people?

They aren’t making any more Medicine Hat or Okotoks!

As the Victoria chart indicates, prices have yet to begin actually falling on Vancouver Island despite interest rate changes. Although it seems the turds, (good one who coined that word), remain unclaimed and empty, especially the one down the street from me. :-)

I do want to add a wrinkle, though. We just had a pretty major flooding event in the lower SW part of BC. In fact, Vancouver is now cut off from the rest of the Country. Victoria is out of gas….my relatives cannot get to work and their companies are shut down until they can fuel up the work trucks. It might be a week or so yet before that is rectified. Idiots are buying up food and toilet paper….again. There is plenty of supply but not if everyone sets up their own warehouse at home. So why does just 8″ of rain last weekend make such an impact? The mountains, of course. All habitation is in the valleys. All farmland is on the valley floors. All transportation routes follow the valley corridors. And the rain falls on 100X the area, on the mountain sides, also melting the snow, and rushes for the coast one way or another. Our major freeway connecting to Canada will not be repaired for 6 months, anyway. The gas pipeline is down for now, as is the oil pipeline….until a proper engineering survey is completed. This means fuel will now run by tanker truck on alternate routes. Rail lines are closed down both ways for a while yet.

I have lived on Vancouver Island for most of my 66 years. Over that time the development here has been unrelenting. Once idyllic little logging and fishing towns are now butt ugly tourist attractions and full of condos. This recent weather event and terrible flooding may make people considering a move here for retirement take a big pause and delay. That is what we are hoping for, just a pause and more deliberate and thought out development going forward.

Oh, and even though I live on a river, in fact I am looking at it while I type this, we have normal flows. We had very little rain while the modified Mediterranean geography just 100 miles away got hammered. My home town has big time flood damage. Bizarro world, and where is Kramer and Jerry, anyway?

O/T, but I’d like to extend best wishes to citizens of our PNW and the Canadian ‘Southwest.’ I’ve traveled extensively in BC and some of Alberta–the Royal Tyrrell Museum of Palaeontology in Drumheller is a must see–and Canucks are some of the friendliest and most gracious people you will ever meet (a tire shop in Alberta stopped their other jobs to help us get our old British sports car back on the road). Hope our Canadian commenters and families are doing OK; this too shall pass.