Spooked by inflation not being temporary.

By Wolf Richter for WOLF STREET.

Following its policy meeting today, the Bank of Canada announced that it would end QE outright beginning November 1. And – unexpected by economists – it moved rate hikes closer, with April 2022 now showing up as the expected date of a liftoff, up from the second half in 2022, with four rate hikes expected next year.

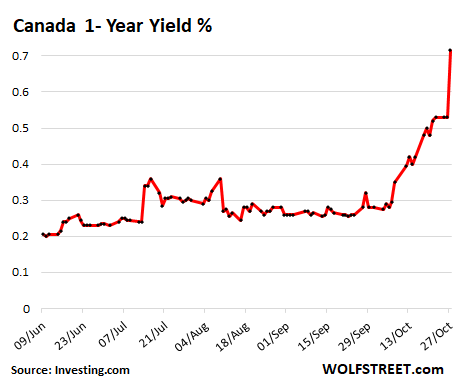

In response, the Canada 2-year yield spiked by 21 basis points, to 1.08%, having more than doubled over the past four weeks. The 1-year yield spiked by 19 basis points today to 0.72%, having nearly tripled over the past five weeks:

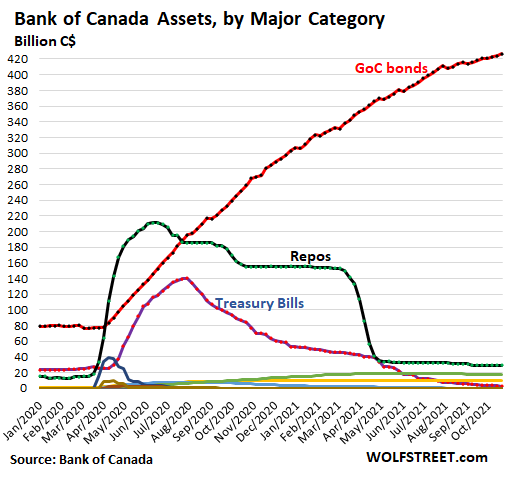

The BoC started tapering its purchases of securities a year ago by ending its MBS purchases outright and tapering its GoC bond purchases multiple times. In the spring, it began to reduce its holdings of short-term Canada Treasury bills and repos. And it ended other smaller programs.

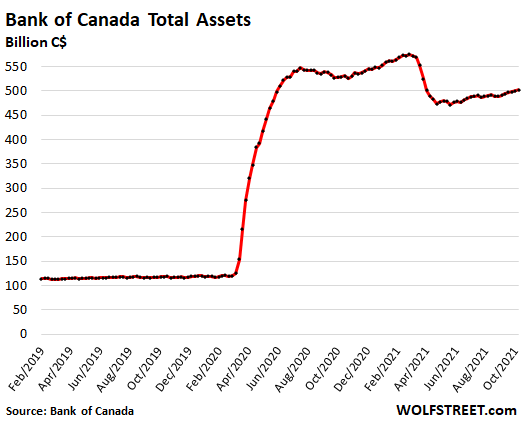

Its total assets, at C$502 billion, are down by 13% from the peak in March:

The BoC holds C$426 billion in GoC bonds. Its announcement today said that it would roughly maintain this level for the time being.

Repos, the biggest asset category on its balance sheet during the 2020 bailout spree, are down to just C$30 billion. Government of Canada short-term Treasury bills, formerly the third biggest asset category, are nearly gone.

It still holds C$17 billion of Provincial bonds, C$5 billion of Government of Canada Real Return bonds (what we’d call TIPS in the US), C$10 billion in derivatives, and C$5 billion of MBS. Other asset categories have already been whittled down to nothing, including corporate bonds, Commercial Paper, and Provincial Money Market securities.

As per today’s announcement, the top red line, GoC bonds, is going to flatten going forward:

So this is the end of QE in Canada. The BoC said it would shift to the “reinvestment phase,” where it no longer adds to its holdings of government securities, but only replaces maturing government securities with new GoC bonds.

These replacement purchases will not match “one-for-one” the securities that are maturing and rolling off the balance sheet “because the maturities are large and unevenly spaced,” it said in the separate Market Notice. Instead, the BoC will space the replacement purchases out over time.

It will buy only GoC bonds. The maturing Real Return bonds will be replaced with GoC bonds. It will buy roughly one third of the replacement GoC bonds in the primary market and two thirds in the secondary market.

The BoC didn’t specify when it would start letting the GoC bonds roll off the balance sheet without replacement to reduce its holdings, which would allow long-term yields to drift higher. The beginning of this roll-off period may be timed to occur around the first rate hike. Allowing long-term yields to drift higher while raising short-term rates would keep the yield steeper. The roll-off also would reverse some of the prior QE. In the chart above, this would show up with the top red line bending downward, as other securities categories have already done.

This is all about inflation not being temporary.

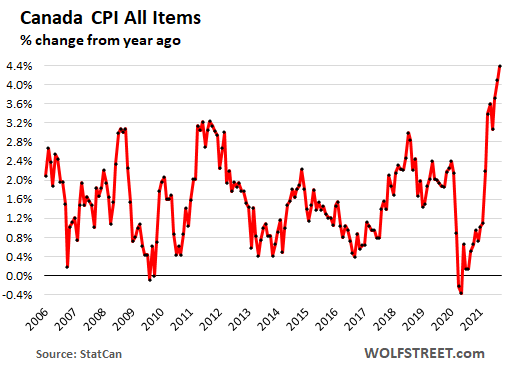

The Canadian Consumer Price Index in September spiked 4.4%, the fastest increase since 1992, and it’s not exactly making a lot of effort at being “temporary,” and this rattled some nerves:

“The main forces pushing up prices – higher energy prices and pandemic-related supply bottlenecks – now appear to be stronger and more persistent than expected,” the BoC said in the statement today.

“The Bank now expects CPI inflation to be elevated into next year, and ease back to around the 2 percent target by late 2022,” it said.

Clearly, the BoC has moved away from the Fed-sponsored theme that this surge in inflation is nothing to worry about because it’s temporary and will go away on its own, despite the massive ongoing monetary stimulus. It seems, only the Fed is still clinging to this hope of “temporary,” though even there, doubts have emerged.

Today’s inflation worries in the BoC’s statement are a hawkish deviation from BoC Governor Tiff Macklem’s observations earlier in October that largely dismissed the inflation spike. So the BoC is now turning to efforts to crack down on inflation by at least removing the monetary stimulus.

This, despite reduced growth, as housing activity is expected to decline faster.

This hawkish tone comes despite the BoC’s dialing back of growth expectations. In its Monetary Policy Report, also released today, the BoC downgraded GDP growth in Canada to 5.1% for 2021, which is still huge, but down from its 6.0% projection in July. Among the factors leading to the lower but still red-hot growth expectation for 2021 were lower exports, softer business investment due to the supply chain chaos, and notably, a sharper decline in housing activity.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I can’t find any U.S. law that says using the dollar is mandatory.

Why is Wolf and his readers crying foul on the Fed and inflation running hot? Maybe demand your services to be paid in gold/silver? Food for thought.

“Maybe demand your services to be paid in gold/silver?”

Sheesh. Buying gold and silver to keep around is one thing. Using it to make or receive online payments in the modern world is quite another. This is the nuttiest idea I’ve heard in a long time. Thank god I don’t live in the middle ages.

Or in Utah (the Utah Legal Tender Act of 2011)… But I would love to receive my invoices via mounted messenger. Must be a sight to see.

good idea wolf – got plenty worthless cash

Or thank God you don’t live in Venezuala :)

Gold and silver were used for thousands of years, in a global economy for “online” payments, except those were trusted gold dealers notes.

Paper dollars were used as an exact exchange for gold and silver, for convenience, up to the 1960s.

There was just a recent article of Venezuela is now a gold and silver economy using “gold flakes” which really was just a link in a gold chain broken off.

There are cryptocurrencies backed by gold and silver.

Fiats are nothing new throughout history and always end the same.

We all play the game we are forced to play but the new monetary world we are in is extremely fragile and has yet to play out.

The problem was, as economies and trade got larger, was that pirates invented ways to “tap in” to all the payment pipelines of gold and silver.

Then someone came up with the bright idea of keeping it all in one place and just moving it from room to room, forcing the pirates to change their life style and move to these places, in order to continue using their “tapping in” skills. I.e., the City of London, etc, etc, etc.

Pirates are highly adaptable and creative fellows, with, of course, no scruples or empathy whatsoever….and they are still at it, in many forms.

The form of government means absolutely nothing to a good pirate, although some may specialize due to place of birth or, later on, choice.

The skills lie in how to access ANY current “value pipeline” for tapping purposes……and nothing more.

And of course keeping your loot safe.

What is even nuttier, Wolf, is accepting Bitcoin in payment for something as expensive as an automobile! Bitcoin is more volatile than either gold or silver. Maybe we have reverted back to the Stone Age with crypto-currencies!

That’s why the vendors accepting Bitcoin are immediately converting their Bitcoin as if you were paying in a foreign currency.

It allows companies like PayPal to ride the crypto wave without exposing themselves to the risk in holding Bitcoins.

Gold and silver are like any currency. You’ll lose 3-4% when you convert it from your home currency, and then lose another 3-4 % when you convert it back to your home currency.

Gold and silver are about as volatile as the worse 3rd world currency too.

Maybe have a little since it’s pretty, but it’s worse than crypto when it comes to transactions IMO.

Coming back to the BOC, I’ll be surprised if they have the guts to do more than two .25 rate hikes before they lose their resolve.

I personally think the cost of living is greatly over stated. If it was really bad, restaurants here in Vancouver wouldn’t be packed all the time with people dishing out the cost of 4x meals in groceries for a single meal at the restaurant.

To be fair, we lose 5-10% from inflation after 1-2 years, which is on par with gold conversion costs. And if anyone dares to create a gold-backed currency, then forex costs would be de minimis as you wouldn’t be handling the precious yourself. I doubt it’ll happen though as the last guy to try got a bayonet shoved up his ass (Gaddafi). Governments will kill to maintain their stranglehold on counterfeiting. As for the volatility, yes it’s volatile, but long term it goes only one direction versus fiat.

gonna say I guess the 5-10% I lost when I paid $330 for oz gold

oh, 5 banger so far

I buy to diversify not to USE(though I have paid for different higher priced items in past with it)

that is before my boating accident

If you lose 3% – 4% on a gold transaction you are probably in a hurry. If you are dealing in 1 oz coins it’s going to have a premium over spot for the utility cost of minting it into coin.

Selling it for the same markup or higher is up to you. If you are patient you can find someone you trust who wants gold or silver especially in a hot market and wants to do a private transaction.

The spreads for buy/sell are pretty terrible. It’s probably worse at the grifter coin shops too.

I have a few hundred ounces of silver and a few ounces of gold and can’t be bothered to go down and sell them. (kinda like my huge jars of 2-3k in change I’m too lazy to bring to the bank)

Maybe if silver ever manages to get into the $40s or gold back above 2k then it’s worth my time to wait in line.

Until then, the equities and cryptos is where I put my spare cash for returns.

I used to be very bullish pms, but if anyone ever asks me, I tell them it’s a guaranteed way to lose money.

Precious metals have their place as insurance free from counter party risk, privacy from big brother and store of value When I was 8 you could trade four quarters for a paper dollar, going to take about $20 for those four mostly silver 1964 quarters now. You could have done worse.

Digital currency, with the stroke of a keypad it is vanished without a trace in thin air. As for easy Money, well credit is coming out of everybody’s pocket. How to pay it back let the Gouvernment do something about it.

“inflation has to have distributional propagation – the wage-price spiral – for it to become sustained rather than just reflect ephemeral supply constraints.”–economist Bill Mitchell

You can only pay taxes in USD.

That’s how the government induces demand for their currency.

Otherwise, we’d all be using scrip.

The problem with exchanging metal objects is that they must be assayed each transaction…forgery is too easy.

“forgery is too easy” hahahaha

Tell that to Greenspan, Bernanke, Yellen and Powell ……

the masters of counterfeiting …… the best buddies of the rich .

that too

Forgery is easy if you are buying off eBay and have no clue on what you are doing.

Standard coins are pretty easy verify. Size, weight, look and a ping test would take about 10 seconds and detect 99.9% of the fakes.

And, for an “average” transaction, no one is going to counterfeit those small value coins.

For a large transaction, let’s say buying a house, yeah take a few minutes to verify or have an expert do it. Heck, you are paying a realtor 6% of the transaction to open the front door and explain how many bedrooms you got…

The more widely traded gold coinage can be verified with the Fisch Instrument It verifies the weight and width. They also have a sound tester now.

The federal reserve act is the law and it is written on every single dollar note they issue, “all debts public and private” is the phrase that does it.

When you accept a service or product for purchase, you have incurred a debt. When you eat a meal at a restaurant before you pay, you have incurred a debt. When you take an item off a shelf and are willing to pay the price of the item, you have made yourself a customer and have incurred a debt, and the merchant must accept your dollars.

I have tried to get a haircut at a few salons that told me I must have a credit card to use their services. I think I could sue all of them for not accepting dollars for their services. One day soon I may do just that, I offered them dollars and they refused to accept them. Technically this is a federal offense.

I believe you are right. legal tender law.

A few businesses are accepting payment in gold and silver already (notably in the precious metal space itself), but soon it will be completely transparent with cards being able to handle it.

Kinesis money has this week added their 13th vaulting partner to their worldwide network (that holds the monetary base), this time in Panama. This will mainly serve users in Latin America, which is great, because these countries often have unstable money and unstable governments and now they also have access to sound money based on precious metals safely stored offshore, which previously was only available to the rich.

This month, the first utility-based yield was paid out (which in itself is a revolutionary change from debt-based yield). I received 6.7% yield on gold that I’m holding since March (paid out in gold of course, because that is the new money). I expect this yield to be much lower going forward (yield was so high due to very high monetary velocity on a small monetary base), but even if it drops to 1% or so, it will still be much better than what bonds or bank accounts are offering on decaying fiat money.

Thinking about the future: we know the dollar and euro are doomed. Some people think Bitcoin is the future (I certainly don’t) but China and some others have just banned that… So how do they want to get paid in the future if the current “reserve” currencies are not viable anymore? I think precious metals will be the obvious choice once again. I’m not all-in, because the future always turns out different than you think, but it would be prudent to hold some precious metals now.

You are lending your gold out?

No way! Never!

Russia, China and Turkey central banks were stacking gold instead of Bitcoin and treasuries. Bitcoin might be the go to when countri s begin falling apart, but right now it’s gold and dollars.

Russia, and especially Turkey, are too poor to have much gold although Russia loves to talk theirs up to help shore up the ruble. The German public, private citizens, owns more gold than the Russian CB.

If you really step out and look at history the big con is to get you to trade your hard earned savings for some scam of an investment. In old days where you got paid in hard currency, a nearly bankrupt government would try to get you to turn in your hard money for a paper promise to pay you interest. Even made it a capital crime if you were caught transacting in gold in some cases.

The universal law is if people have a choice when government issues debased money, the real money gets stored away at home.

Central banks have the advantage today that they can easily debase your hard earned money with keystrokes. As government gets closer to insolvency, they will try more schemes to separate you from your savings. Going to take wisdom to keep what you earned in life.

Where is the master QE genius Bernanke hiding these days? We have not seen him for months…he knows what is coming for his grand, reckless global and hubristic economic experiment with people’s livelihoods and lives.

I remember when Bernanke first appeared on the scene. All I could think was how screwed we were.

He is on the pay back tour….speaking fees for speeches delivered to groups of people sent by their bosses to fill chairs…

just like Yellen, and probably just like Powell.

I am kinda disappointed at the chart labeling.

The Canadian 1 year chart looks like either a:

1. Out the wazoo

2. WTF

Ha!

Yes, terrible lapse on my part :-]

So what does this say about us? Yellen says inflation to go until the end of 2022 (which really means a lot longer), CPI is grossly understated, anyone paying attention knows we’re getting hosed on prices, but there’s no talk of pulling the reins in on this. Other countries are figuring it out. I think we’re doing this, in part, to screw our creditors.

Biden wants Powell to make the call to raise rates because politically it’s suicide. Then he can fire him for causing a downturn. Powell’s no fool, he knows he just needs to keep the balls in the air until February when his term is renewed.

Whoever raises rates will destroy the fragile economy after the stock market self destructs from all the deleveraging. Layoffs multiply and all those firms that doubled and tripled their regular orders all of sudden cancel them again thereby inducing more layoffs.

Too much inflation sucks but the guaranteed mauling that would happen with a rate hike is not something Biden or Powell want to take on.

Better for Biden or Powell to let some other shock kill the stock market than to intentionally shoot it down with a rate hike. Then they can have cover for raising rates.

Raising interest rates might be political suicide for Joe Biden, but consider a bit of history. Years of stagflation put Ronald Reagan in the White House. In 1981, Chairman Volcker raised interest rates to about 20 percent to end the persistent inflation, which induced a bad recession. The economy recovered, and in 1984, Reagan won his re-election bid handily.

If Biden waits until 2023 to get inflation under control, he will likely be governing with a Republican-controlled Congress after the midterm elections and will have an uphill battle for re-election in 2024. Put differently, the voters will pummel Biden if he puts his political self interest ahead of the country’s interest. On the other hand, they will likely forgive Biden for the pain if he ends inflation before it gets totally out of control.

Confused,

The environment is totally different from 1981. I don’t think society as a whole is feeling the inflationary pinch as much as we did in ’81. As much as this inflation sucks, a lot of voters are enjoying the home price and equity market appreciation (even if they don’t understand inflation’s additional hidden tax penalty and the double-edge sword of property gains).

And it’s highly unlikely voters would forgive him for the pain of ending inflation. Hell, the GOP is already blaming him for it, and they’ll definitely propagandize any effort to quash it. Any efforts will have to be tactical, like with the supply chain stuff, and not involving sacrifice from the pocketbooks.

Way too much doom and gloom.

A 1/4 rate hike would do none of that – and also wouldn’t fix anything.

But all involved could say “Look, we did something!!!!”

no, it would need to be around 2% to fix anything.

1/4 will do nothing. We need positive real rates to root out inflation. Normally you would be looking at 6%-ish.

However, from 3% onward we should see deleveraging happening on a big scale, which would be (very) deflationary at least in asset prices.

The question is if deflating asset prices will also deflate CPI. It may not! Remember that we had a decade of high asset inflation but moderate CPI inflation. So I guess the opposite can also happen: asset price deflation, while CPI inflation remains stubbornly high.

The inevitable collapse of asset prices will also take capacity offline (through bankruptcies), and while overall demand would fall, capacity would also fall. So CPI may still be high.

And with central banks sitting on their hands for way too long, they will discover again what it means when inflation becomes ingrained in people’s mindsets. It is not easy to reverse that once it takes hold. And inflation is the talk of the day now, so they are already too late! A few 1/4 hikes won’t cut it….

Brainard will be made chief.

The dominoes are already lining up. The reconciliation is crumbling and Biden is a “unifier”. What better way to unify than to stick a climate doomsday cultist in as the head of the fed?

We haven’t even seen the tiniest speck of what’s to come. They will justify negative rates somehow. It’s inevitable. Powell is bad but it can get much much worse.

Roger Pedactor,

“They will justify negative rates somehow. It’s inevitable.”

The Fed will not do “negative rates” because they’re bad for the BANKS. Look at a long-term chart of European and Japanese bank stocks. But the 12 regional Federal Reserve Banks are owned by the banks in their districts. So the Fed will never do anything that’s bad for the banks. The Bank of Japan and the ECB are NOT owned by the banks.

The Fed is using $1.4 Trillion in reverse repos and other measures to keep short-term rates from dipping into the negative.

No need to do negative rates as long as they can do QE and there are things to buy.

As Gunlach says he will take the over on the Fed’s time line on inflation.

Slow play….

Those who promote inflation will not be quick to extinguish inflation…

just a wild guess.

GoC bonds seem to be heading off the chart. Might be WTF terriroty in 12 short months. This being based on current trajectory plus the statement about replace the other assets as they mature with GoC bonds. 1/2 Trillion C$ and rising

Way to go little brother Canada

Nathan Dumbrowski,

Misunderstanding? Read it again. The BoC announced today that it will stop adding to the GoC bonds, as I said in the first paragraph. So they wont go off the chart. The line will become flat starting Nov 1.

For example: When C$1 billion GoC bonds mature, they’re paid off by the government, and the BoC gets its C$1 billion in cash back. It will buy C$1 billion in new GoC bonds to replace the maturing bonds. And the total balance will remain flat.

And when the roll-off period begins, the line will begin to dip, as I said.

What it happening right here :-]

Read it again. It looks like from the read through…It will buy only GoC bonds. The maturing Real Return bonds will be replaced with GoC bonds. It will buy roughly one third of the replacement GoC bonds in the primary market and two thirds in the secondary market

It looks like they have plans to shift all future purchases towards GoC bonds

In the chart and in the data, the Real Return bonds are included in the GoC bonds, lust like the Fed’s TIPS are included in its Treasury holdings. They’re not separated. They’re all government bonds.

In case you’re confused, the maturing GoC bonds will be replaced by GoC bonds.

That line of government bonds will become flat.

Also note this line right under the chart:

“The BoC holds C$426 billion in GoC bonds. Its announcement today said that it would roughly maintain this level for the time being.”

And this line:

“As per today’s announcement, the top red line, GoC bonds, is going to flatten going forward:”

This — “It will buy only GoC bonds. The maturing Real Return bonds will be replaced with GoC bonds. It will buy roughly one third of the replacement GoC bonds in the primary market and two thirds in the secondary market.” — means exactly what it says, namely that it will not buy bonds other than GoC bonds to make those replacements.

My takeaway on this is no more MBBs or corporates. Fed has a way to go.

BOC has 500 billion in assets, mostly govt bonds.

US economy is 10 times larger.

Correcting for size: BOC equivalent is 5 trillion.

US Fed assets are over eight trillion.

Conclusion: US Fed has purchased assets at over 1.5 times BOC rate.

BOC no longer buying mortgage backed bonds: Fed is still a major player.

The whole currency of debt has fuelled far too much wanton consumption. I’m glad to hear credit costs will rise.

Slow news day? talking about Northern Exposure (Canada). What smokescreen will they run with to avoid talking about rising rates? Thank god for a climate summit hey Trudeau.

?? It’s on the CBC news, and the announcement was pretty clear compared to Fed Greenspanish: first rate hike early 22, no more buying MB bonds or corporate bonds.

This is an example of the use of the “tools” the Fed says it has available to tame inflation should it become desirable to do so, which in Canada the BOC has decided it is. Of course with all central bank actions it is the signalling of it in advance that is hoped to cause the desired effect, which may make the actual doing of it unnecessary. The message is, if this keeps up here is what we are going to do, but of course if it gets worse they may do more, and if it gets better they may do less. The real question is are the labor shortages and supply chain blockages causing the spike in prices a long or short term problem. If they resolve and costs return to pre pandemic levels action like the BOC is taking should help push prices back and quell inflation, on the other hand if these are long term problems the BOC action may just add to the cooling of demand. Depending on action other countries take the BOC action could effect the value of the Cdn$, which will also be a factor in their decision making.

I think Wolf’s point is that Canada thinks it’s time to act, time to pull out the tools and show a willingness to use them to counter the possibility this is not temporary.

Australian central bank announced not buying their 2yrs today.

Coordinated effort?

So what will Powell’s handlers tell him to do?

Stick to the script, inflation is always 2%-tops.

Biden’s point of view is that putting people to work modernizing infrastructure plus spending money on so-called ‘soft’ infrastructures is probably the way to go. Stability of employment and income stabilizes a lot of prices. Re-regulating the financial markets is required also. It’s applied economics, not financial speculation and private debt increases, that will benefit commerce.

I always read several Canadian news feeds every day and this has been signaled for some time. In fact, I have been sending my son periodic little hints and tidbits in the occasional email just doing the Dad thing about debt, etc. He is 37, and of a generation that really knows no other situation than deficit financing. The election is over, CERB has been mostly taken away (our Covid relief package) 90% is at 1st dose/83% fully vaccinated, the economy is rebounding, and inflation cannot be denied. There was really no other option than to make this all official.

It is going to take awhile, but we should start seeing a decline in RE prices in many locations as interest rates rise accordingly. Where I live we have a lot of cash buyers of new homes as retirees relocate, but hopefully that will decline as well.

My opinion, so take it for what is worth, is that the final push was forecast energy prices. This forecast is for increasingly higher prices of both NG and petroleum, and there is an economic surge underway because of it. (We produce 2X+ of domestic needs). With higher energy costs being the driver of everything, including shortages pushing from behind, the prospects of doing nothing wouldn’t fly much longer. Everyone talks about higher prices here.

It will be interesting looking at this in both near and long term. Will the Cdn dollar spike on this news? If so import costs will drop easing inflation worries. Will there be overt manipulation of news and reaction by other countries to leverage advantages? Our exports of steel aluminum and lumber will increase in price if our dollar climbs, so will tariffs come off in the US? Interesting times.

I’m a saver, so it would be nice to earn some interest income one day instead of getting the short end. :-)

And:

A couple of direct quotes from Global News this morning, it is in CBC as well: (This drumbeat is also on TV news broadcasts, etc)

Those revised forecasts have implications for current and prospective borrowers, including homebuyers and current mortgage holders.

“Barring another economic calamity, rates are going up. And they’re going up before the end of spring, possibly sooner,” says mortgage strategist Robert McLister.

Amid soaring inflation, the central bank hinted that the first interest rate hike could take place as soon as the April-to-June quarter of 2022. Analysts had previously expected rates to begin rising from record lows in the second half of 2022.

and:

The sooner-than-expected rate increases analysts now expect sometime around the middle of next year would influence the cost of loans and credit with variable interest rates, such as variable-rate mortgages and most lines of credit.

“Barring another economic calamity, rates are going up. And they’re going up before the end of spring, possibly sooner,” says mortgage strategist Robert McLister.

Ah, there’s the rub. Won’t it be rising rates that bring about said economic calamity? All the large CB’s may start hiking rates, but who will actually complete the task?

Good comment P,,, very to the point, and somewhat ”non personal” to boot…

Thanks again for your boots on the dirt reports from BC…

(Just giving some positive ”feedback” to a reliable source,,,, Wolf already knows how much I ”appreciate” his wonder full work with my $$,,,

Which I really hope all of the readers on here copy what I DO with support for the Wolf!!

Mainly/somewhat because of ancestors saying, ”do what I say, NOT what I do.”

looks like lagarde is as much of a deranged lunatic as powell.

“as much of a” should read “even more of a”

it’s like picking between hitler and stalin.

You got that right. S C A R Y . I have a hard time understanding how society has allowed these absolutely evil people and their diabolical schemes to hijack their lives.

If there were futures contracts for nutjobs – we’d be in money. They’d never go down :)

When our neighbors to the North start teaching us Yanks how to attempt to stop a runaway Monetary Train, we look pretty foolish with a central bank that is way too politicized. When they preach (US. Fedheads) to us sheeple about Climate Change out of one side of their self-interested mouths while creating huge Wealth Divergences out of the other side via policies, it shows that this organ of the State either needs replacement or outright closure. The Canadian central bank is going to make the Canadian Dollar a better performing fiat currency than the Almighty Dollar, at least in the near-term.

However, all fiat paper currencies are in trouble with evaporating Purchasing Powers in a world set ablaze with raging inflation.

Good article on Bbc web site that carbon footprint of the Uber rich is about 100 times that of average person. Remrmber that when Bloomberg tells you you are evil for wanting to ride in a V8 pickup

A very good example of what you have observed is Al Gore flying his private jet to Climate Change speaking engagements at whopping fees to preach to the unwashed masses.

A view from the Great White North.

Lots of job vacancies appearing which never appeared pre-Covid, with wages offered jumping 10-15% from 6 months ago. Vaccine mandate firings will be biting over the next 8 weeks, as will the ending of furlough payments. There could be big changes by Christmas. Medical and other service provision is dropping rapidly, e.g. the video referral program instituted because people couldn’t get a family doctor has itself just been suspended due to lack of staff. My garbage pickup didn’t turn up this week, no explanation offered (that’s never happened before).

Goods price inflation is happening in many ways that the government doesn’t measure. Flyers are 4 pages not the pre-Covid 16 pages. Discounts are smaller. Prices are bumped massively now pre-sale so the following sale percentage looks bigger. Package sizes are changed (sometimes upwards now also) to hide the price per oz/unit change. Interestingly, some items are now being discounted but NOT being advertised in flyers – no idea what’s going on there but it’s widespread. The internal materials and construction (I take things apart – I’m an engineer) are poorer/cheaper, but the item has the same stock number. Sometime whole functions are missing from what is described on the packaging. My local big box store has rearranged its help desk to accomodate a second cart for rejects/returns, which I think says a lot.

So, the GoC official data is way off measuring how bad things really are, and I am pretty sure the BoC knows it.

If the labor situation does deteriorate rapidly by Christmas, especially in crucial areas like medical and transportation, stand by for more announcements.

Tiff Macklem ticked off a bunch of Torontonians and Ontarians who witnessed a home go from C$350,000 to C$1.3M over a course of a year money printer go brrrr

“The BoC said it would shift to the “reinvestment phase,” where it no longer adds to its holdings of government securities, but only replaces maturing government securities with new GoC bonds.”

What would you call that? Stealth QE? Quantitative Maintaining? Interesting to note that the magnitude of our housing bubble here in Canada is significantly worse than the US, with average prices being about double(ish), and with fewer mortgage-related tax advantages than Americans. All by way of saying that I think these little moves are way, waaaaay too late, but I sure am curious what happens to real estate over the next couple of years.

It’s called “maintenance,” like a boozehound alcoholic who needs to drink half a 5th of vodka just to keep the shakes at bay.

Only question for DC is, ”where do you get that ”half” stuff?>???

child of two parents formerly known as ”heavy drinkers” who would put at least a quart of booze

down their throats before noon every day,,,

and then go to work and to the bar after work and consume another quart or so,,, EVERY day +…

Both died younger than me, by decades now,,, because they did their best, with total hypocrisy IMO to make us kids learn how NOT to ”drink.”

Decades later, all my sibs still alive, mostly not drinking much, if at all…

Yet Weimar Boy Powell has still got the pedal to the metal, with over a hundred billion in QE per month, juicing the largest asset price bubble in the history of mankind. I said it a year ago, that these clowns should end QE immediately, not taper. This is a grotesque distortion of the economy by an irredeemably reckless cabal of financial terrorists. Put ’em in jail!

120 billion …

I like to call it

120,000 MILLION a month…….

has a better ring to the magnitude.

.12T USD

$364.19 stolen from every man, woman and child in America.

the qe should have ended in the summer of 2020, when it was clear that it was not needed. keeping it going for an additional 18 months is a disgrace.

And that’s the tell right there. These guys are not doing this out of necessity, it’s to line their own pockets. The “programs” have absolutely NOTHING to do with fundamentals.

The end of QE will hammer bonds in Canada across the board, I expect.

For those of us in Canada who like to “keep our powder dry” instead of buying “stuff”, it is nice to see a first step in moving back to sanity. Getting out of the gate ahead of the US is a smart move on many levels. Other countries seem to feel the same way. The last time this scenario played out in the early 80’s, I had a young family, and was not in a position financially to capitalize on it. I did observe more elderly family members patiently wait to lock in higher rates for longer terms on their safer investments such as Canada Savings Bonds. They did very well in the years that followed, and had a more comfortable retirement. They knew that all thing would pass, including high inflation and high rates. Good things come to those that wait.

Google total central bank assets and you can see the big picture since it’s a global world. Last time I looked it was about $31 trillion dollars that would peak toward the end of this year. We will see if they can ever reduce it without crashing things.

The Canadian central bank’s invitation to Davos has be withdrawn

People can barely afford to live today, but what about next year when prices will be 10% higher for rents, housing, and food?

Meanwhile, central banks fiddle around adjusting dots on dot plots, which purport to represent future interest rate hikes that will never happen on their watch.

It’s time to allow asset prices to drop so that the working man gets a well-earned break!!! Keep your measly stimulus checks and low-paying service jobs, which only perpetuate poverty. Raise interest rates, so the free market can create jobs and flourish!!!!

Why are central banks attacking people who don’t own substantial amounts of stock, bonds, and expensive housing?

you can always trim expenses and save…

no.

wait.

if you save, you lose 5%…..right now…

You must go buy what the string pullers already own…..stocks and real estate.

Its kinda like a cattle drive run by central bankers for the benefit of a small %…and you know what happens at the end of a cattle drive? The cowboys get drunk, and the cattle gets slaughtered.

Learn to live with less, because that’s what they’re doing to you – destroying your standard of living. In the end you’ll be lucky to have a tent and a full belly.

I have been watching Joe Robinet and Matt Posa camping to brush up ony camping and bushcraft skills. Just in case.

You do not have to live with less. You can in fact live with more if you do it yourself.

Grow food, do your own repairs, learn more skills.

Homegrown food has more nutrients, tastes better (so you eat less), and stores much better. Don’t grow potatoes if you are surrounded by them, grow things that are relatively expensive in the shops but easy to grow (like salad greens and bell peppers).

When you repair your own stuff you know how good the repair is, and can check for future problems whilst you have the thingie in bits.

Good skills makes you more independent, and helps you both recognize and appreciate tradesmen with real talent.

The likely reason is the Chinese pushing home prices into the stratosphere and now immigrants can’t afford to come to Canada because of the cost of living. The government tells the people total lies about why home prices are so high except the real reason right here:

https://vancouversun.com/opinion/columnists/douglas-todd-why-has-ottawa-downplayed-china-shock-on-housing

There are a lot of variable loans in Canada (e.g. variable mortgages, HELOCs, reverse mortgages, secured and unsecured lines of credit, shadow bank loans).

If the Bank of Canada raised rates on these people, the next monthly payment would have the increased interest payment amounts. I am not convinced the Bank of Canada has the guts to raise rates on these people within the next 12 months, given the fact they don’t know how big this iceberg is and they don’t know how fragile the financial situation of the borrowers are.

if it all crashes to hell, a barrel woodstove and a hundred pounds of whole wheat flour should get you through the winter. I’m experimenting with this right now here in the yukon. surround the stove with walls of big round bales or even cordwood chinked with moss or snow.

that and snowshoes, a .22 to supplement thr diet and if you make it through the minus 50 snaps, berry season cometh and you should be golden.

societal shifts are on the way and things will lively never be the same.