But still up 4.9% from a year ago – outside of the prior quarter, the hottest year-over-year growth in 20 years.

By Wolf Richter for WOLF STREET.

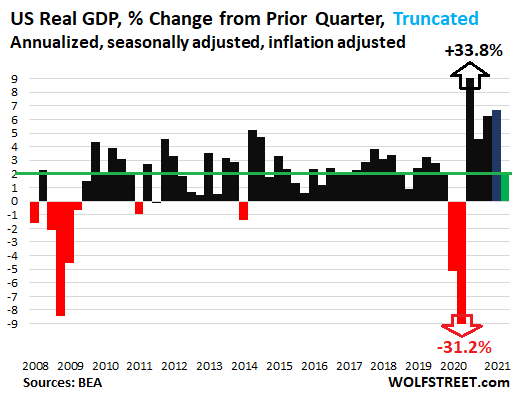

The US economy, as measured by GDP, adjusted for inflation, grew by an annualized rate of 2.0% in Q3 from Q2. This is far below the pandemic growth rates of the past four quarters. But hey, those were special. In the decade from 2010 through 2019, annual GDP growth averaged 2.3% and never reached 3% in any single year. So 2.0% is in that normal range for the US economy.

But Q3 wasn’t normal. It was marred by rampant inflation, labor shortages, and supply chain chaos that led to a continued drop in inventories (a negative for GDP) and caused manufacturers, industrial companies, and retailers – particularly in the huge auto industry – to run out of product for consumers to buy. And it was further marred by a huge record massive blistering trade deficit, which is a negative for GDP.

To show the detail of that 2.0% annualized GDP growth in the chart below, I have truncated the two historic outliers, the 31.2% plunge in Q2 2020 and the 33.8% spike in Q3 2020:

Compared to Q3 2020, GDP still soared by 4.9% from Q3 a year ago – outside of Q2, the highest year-over-year growth rate since Q2 2000.

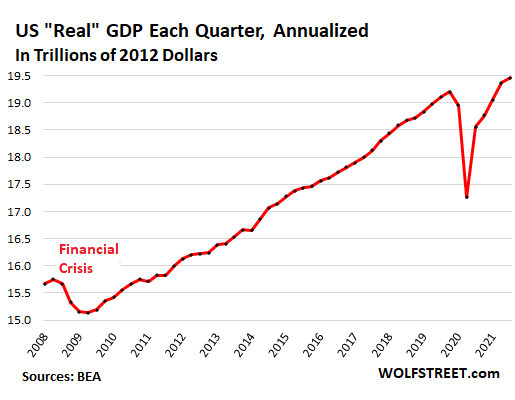

Real GDP, expressed in “chained 2012 dollars,” in Q3 rose to a new record of a “seasonally adjusted annual rate” of $19.5 trillion:

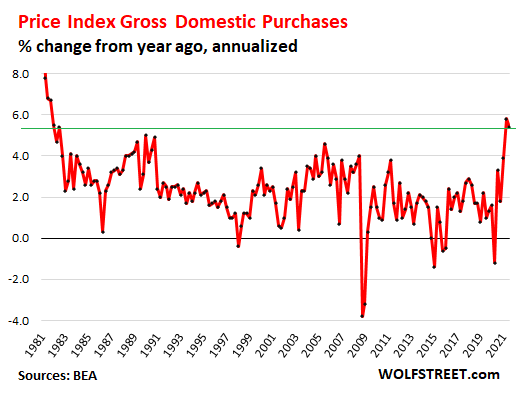

Inflation ate everyone’s lunch: The BEA’s PCE price index, which relates to consumer spending, increased by an annualized rate of 5.3% in Q3, down from an annualized rate of 6.5% in Q2, which had been the highest since 1982.

The broad Price Index for Gross Domestic Purchases, the BEA’s inflation measure that roughly parallels its inflation adjustments to GDP, rose by an annualized rate of 5.4% in Q3, down from an increase of 5.8% in the prior quarter. Both were the highest since 1982.

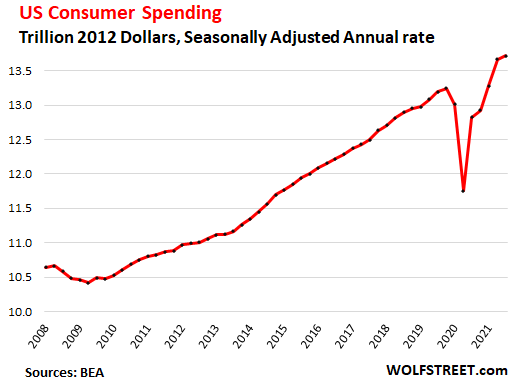

Consumer spending – after the stimulus-powered gigantic gains in Q1 and Q2 – edged up by only 0.4% in Q3 from Q2, which amounts to an annualized growth rate of 1.6%, to an annual rate of $13.72 trillion in chained 2012 dollars, a new record.

Consumers had trouble outspending the rampant price increases. And with some products, such as new vehicles, they had trouble finding something to buy, as inventories had been depleted. Inventories at auto dealers collapsed, and new vehicle sales plunged.

Consumer spending accounted for 70.5% of total GDP, the second time ever that it was above 70%, Q2 having been the first time. This shows to what extent stimulus has powered consumer spending.

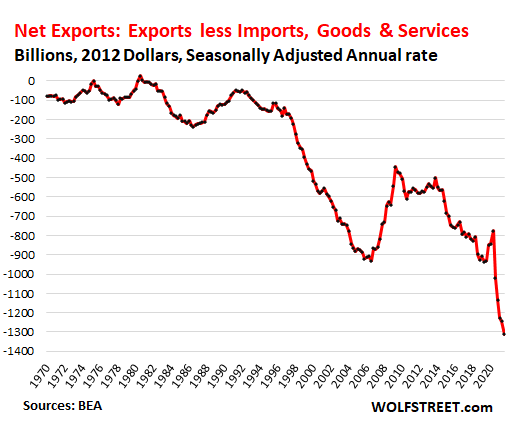

The Trade Deficit in goods and services, oh my, fueled by imports, which are fueled by consumer spending on imported goods, sharply worsened to a new worst. Exports add to GDP, imports lower GDP. The balance (exports minus imports), or “net exports,” worsened by $67 billion, or by 5.4%, to a record worst of -$1.31 trillion annual rate (in 2012 dollars). This 50-year chart is an indictment of globalization over the past three decades by Corporate America:

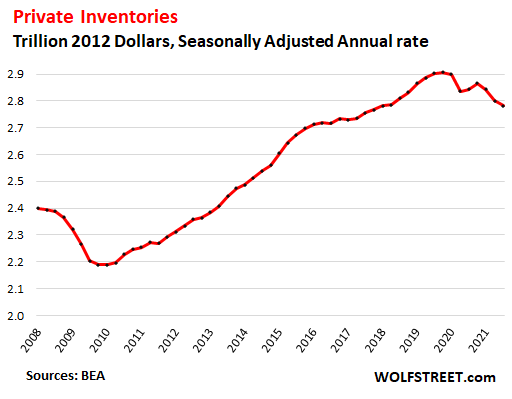

Gross private domestic investment rose by 2.8%, after two quarters of declines, to a seasonally adjusted annual rate of $3.6 trillion. This category includes the major sub-categories “change in private inventories” and “fixed private investment.”

Inventories continued to drop amid widespread shortages of materials, components, and finished products across the economy, but most catastrophically in the auto industry, which has been waylaid by the semiconductor shortages, and inventories of new vehicles at auto dealers have collapsed. Auto dealer inventories normally account for over one-third of total retailer inventories, and they move the needle, but many other retailers too where in short supply.

A drop in private inventories lowers GDP. An increase adds to GDP. Private inventories dropped by $78 billion annualized, or by 2.8%, in Q3 from Q2, to $2.78 trillion, a level first seen in Q1 2018:

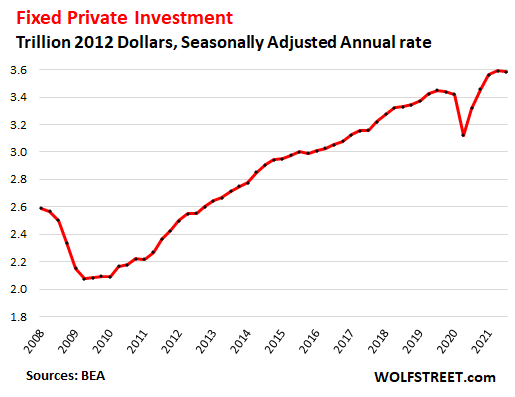

Fixed private investment – includes investment in residential structures, nonresidential structures and equipment, and intellectual property – ticked down a smidgen to an annual rate of $3.59 trillion:

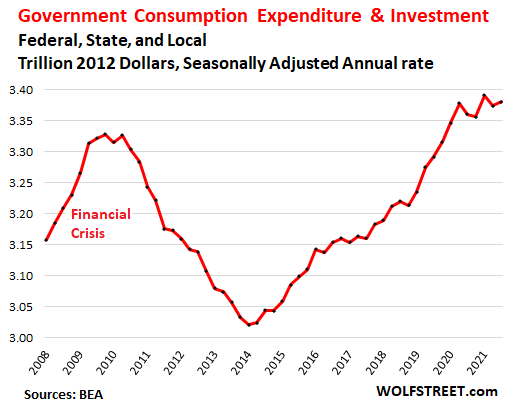

Government consumption and investment ticked up, after the drop in Q2, to an annual rate of $3.38 trillion. Despite the ups and downs, it has remained roughly in the same range since in Q1 2020.

Note: This does not include transfer payments to consumers and companies, such as stimulus payments, unemployment payments, Social Security payments, and it does not include government salaries, and other direct payments to consumers. Those payments enter GDP when consumers spend this money as part of consumer spending. And funds that businesses received enter GDP when businesses spend or invest the money.

Government consumption and investment includes only what governments at all levels spend on goods and services, such as fuel, supplies, furniture, office rents, consulting services, cloud contracts, software, IT services, etc., and investments, such as in equipment and infrastructure.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

sooo….good?

I think it goes something like this. Real GDP 2% plus inflation of 6% = 8% Nominal. Subtract out government deficit spending of 15% GDP and it’s a negative what ever you want to call it. The affects are Tesla $1070 per share. Grandma’s interest payment on $50,000 = $250.

Exactly. All growth was the result of the change in the deficit between FY19 (still inflated but from the pre-COVID “normal” economy) and FY21.

More fake prosperity from ultimately unsustainable debt.

Ditto…

Bit Coin will save as all. Create a few trillions of Bit Coins,

Dog Coins, S… Coins and other…..add this from thin air created value to GDP, and you do not have to pay an interest as on treasuries, and after all another 100 billions of coins and we can buy the whole world

gotta screw retiree’s == yessir

Supplies are getting shorter than I thought. I received a notification today that an electric utility doesn’t have transformers or know when they will get more to be able to finish construction on a new residential subdivision. Can’t build a house without electricity.

Well, you can build it without power from an electric utility.

You just can’t sell it or move into it without power from an electric utility.

Maybe make it an “off grid” community?

Problems is is that as the initial cap investment thermodymamically amortizes down the proverbial road .. all the stuff you bought – panels, contervters, BATTERIES,hardware etc. .. wear out to eventual non-functionality. What then?? .. Assuming as I do, that we’re, collectively – as a ‘late modern’ civilization .. are headed down Resourse’s diminishing slus shoot, the things You .. I .. and Everyone else, takes what we’ve All become accustomed to – clean water .. well, somewhat, basic sanitation, ejuice at the flick of one’s finger, juice for the Ride .. uhh, what did I forget .. Oh, FOOD! .. affordable-like – for granted STOPS! .. what then, when the so called ‘fr e e’ market’s vending machine no longer puts out …? I think people have no idea just how low we modern hominids might go.

“Got Burros??”

How are you going to electrify economy without utility electrical equipment? Takes a lot of special equipment to get from where we are to new grid.

With new tech coming from advancements in physics and the engineering following, the existing ”grid” and all such infrastructure is already anachronistic and clearly very brittle and not defendable without huge additional expense.

In a few decades, the world will be back to the local production and distribution of electricity similar to how it was up to at least the middle of the 1950s, but different from then in that the majority of production will be from non fuel sources because of the development of long term massive battery storage currently happening.

”Youngsters,” ( boomers and younger, ) will benefit by investing in companies currently working in this direction, as well as ”refitting” buildings to be able to deal with various DC voltages.

1927, southwestern Pa. my grandparents and their 5 children moved into their new 1200 sqft house. No electricity or running water. They survived and prospered. Five more children were born there and all of the children became middle class or upper middle class and the grandchildren too.

My God how the world has changed.

GDP has been negative for years. It is masked by phony inflation numbers. The homeless will continue to increase as the middle class is decimated. Inflation is a regressive tax. This is why more social nets will be required.

..and for bonus points, much of what counts as GDP is a very long way from stuff which is actually productive.

Yes, like last I read, about 70% of the world’s lawyers.

an underestimate by 29.9999999999% ;)

(I knew 2 good ones, but they’ve both retired).

A house of cards economy (from debt and an asset bubble) is supposed to indefinitely sustain noticeable increased social spending to hold up or increase living the populations’ standards?

A lot of financialization is included in GDP. Stock jockies and “financial advisors” take cash from workers and put it into stocks and funds. They keep a slice of it. This goes toward GDP, as if it were a factory making a valuable piece of machinery. There are more funds than stocks to invest in and more commisioned sales agents than cockroaches. A lot of money is moved from one pocket to another pocket without contributing anything real to the nation. There are commissions and fees chopped off the money every step of the way. A GDP calculated without these money changers in the temple would be smaller every year.

How are the figures for some of these broad categories ACCURATELY known? I think this is another case of a level of certainty that isn’t justified. Comparisons between years IF always using the same methodology to measure the components of the GDP would be the only useful figure.

C = consumption

I = investment

G = government spending

X = exports

M = imports

GDP = C + I + G + X – M

As an example of how things can go wrong, it always makes me chuckle when I see people who act as authorities comparing government CPI figures over the years and then claiming things aren’t as bad now as they have been in the past when, in fact, the methods for calculating the CPI have changed over time. They’d need to make their own calculations using the same method over the period they’re analyzing, but that’s difficult.

Economics, the “dismal science.” Actually, it doesn’t even fit the definition of a “science.”

including government spending in gdp is the biggest scam, as it means that government can create whatever gdp numbers it wants by stimulus spending. i laugh whenever i hear people talk about how it was a great accomplishment that gdp was so high in q1 and q2.

Folks,

The sugar-high stimulus spending is over and I expect Q4 to be zero. Inflation will be HOT as all supplies from China will be stuck in the near-permanent bottlenecks of a J-I-T supply system and people will be able to start charging anything. Labor shortages will be the least of our worries.

Food supplies are the real danger.

A couple plants that make fertilizer just declared force majeure because their inputs are too expensive to run the production facilities. Spring plantings could really be hampered but that is the inflationary crisis soon to come.

One of my tennis doubles partners is a top-level supply chain exec here in the Pacific NW for chemicals. He told me one of his big-time buyers said that if he could get him a shipment of one his industrial chemicals coming out of the Louisiana Delta, (which is still recovering from Ida) he could name ANY price.

Jack Dorsey is right. When the panic in the food sector really sets in, we will have hyper-inflation.

That Twitter twit, Dorsey, is right! We will have hyper inflation. GDP will grow every year from here on out! I have brought America back from the ashes to prosperity!!!! Buy now or be priced out forever!!!! BBBBRRRRRRRRR!!!!!

Read up again on French revolutionary money printing. Ended in currency going to zero in about 7 years and central banker getting executed. It all started out with good intentions and an economic boom.

I don’t know how to read. BBBBBRRRRRRRR!!!!!!

gotta love the french and their guillotines

Hyper-inflation will be very brief, as the vast majority will be unable to pay. The big crash will follow within a few months.

It kinda reminds of the book “900 Days: The Siege of Leningrad.”

Weeks into Operation Barbarossa, there were still restuarants and cafes open, enjoying the beautiful weather, in the city. Then, everything shut down and the entire city went into hoarding mode as the reality of what was coming finally hit.

2banana,

Love big historical analogies in world shaking events.

One of the biggest problems facing this supply chain crisis is the over-reliance on these HUGE ships that carry north of 5000 containers, built by Cosco / Maersk to save a few bux. In the same breathe, they act as de facto storage facilites, warehouses on the sea, beyond the rules and regs of us landlubbers. ( if you think there are any rules/gov out there on the high seas….)

So many problems with these GIGANTIC ships – they can’t fit through the canals, Panama or Suez… Most American ports cannot handle them. Our ports are one of last places still unionized. Since we dont use trains in a JIT supply chain, our trucking sector is too puny and dated to handle these loads. Clearing a load from just ONE of those boats can take up to a week.

And we got 70+ now waiting offshore.

Now with the stack of many of these boats off the California coast, they could be sitting out there for years (maybe if we get some more dockhands down there….) ignores that we don’t have the infrastructure to deal with just some of these bottlenecks.

Stop blaming workers in a country where it is a dictatorship of the bankers and their corporate henchmen. who wants to work for these jerks.

Blame the putting all of our eggs in ONE big ship’s basket. Empires have fallen from this thinking.

My favorite hi-story tale of this thinking is also one of the best maritime museums in the world. The Vasa was commissioned by the Swedish King when they were at the height of their powers in the 1620’s. They went to a Dutch boat builder who warned them that he thought the ship was TOO high for its length.

The Swedes built it anyways, with almost a fourth of their treasury sunk into the project. It rolled over in the first breeze and sank on its maiden voyage, taking with it, the Swedish Empire.

Amazon is unloading 53′ containers, off the ships they rented with cranes, at the Port of Houston. These ships unload anywhere, right onto loaders. Amazon will be stocked for Xmas.

I think 53 containers won’t even fill up one warehouse, based on square footage. Peter Thiel and Elon Must could barely fit their toys in there.

Bob,

It’s not 53 separate containers. It’s 53 foot containers, a whole ship full.

They are gigantic for a reason. Doubling the ship length quadruples the cargo capacity.

The 53′ containers are trailers for trucks. It’s the longest trailer you can haul down the road without special permits. They are dropped onto the truck and they head to the store. A lot of them are shipped by train to the rest of the country. Walmart loads a lot of their trucks in Asia, while most American retailers have to empty the container and resort it before sending to the store.

I have a lot of friends in the shipping industry and it is just crazy sometimes. Three years ago they were sending relatively new ships to the breakers because they were “too small.” Now if you own one of those “small” ships you can name your price because they can go into the smaller ports instead of waiting in line at Long Beach.

2Banana:

One of the great books written about WW2……..I’ve read re-read. “900 Days”.

“panic in the food sector”

And I wonder how the largest private farmland owner will stoke that panic to get richer (Bill Gates)

Godwin’s Law v1: As an online discussion grows longer (regardless of topic or scope), the probability of a comparison involving Nazis or Adolf Hitler approaches 1

Godwin’s Law v2: As an online discussion grows longer (regardless of topic or scope), the probability of a comparison involving Bill Gates or George Soros approaches 1

Did work for a client who owns a propane business.

He has zero confidence they will be able to meet normal

winter demands. And price………..

I’m sure its a win for lower carbon emissions.

“panic in the food sector”

There will be plenty of potatoes in the Northeast. My neighbors are reporting bumper crops of hay and potatoes. Potato houses are so full that growers are using aircraft hangars, according to the grapevine.

My dairy-farming friend cut nearly two years worth of feed this past summer. My next-door neighbor is steady building his sheep herd, soon to be 1000 ewes. That’s a lot of lamb for his Boston market.

The media keeps insisting that the sky is falling, but actual observations of the world around us suggest otherwise.

Potato crops are indeed mega this year. One of the problems with overflow storage is that it doesn’t have the correct ventilation and insulation. Anything stored in a hanger will be rotten after the first couple of days hard frost – about a month at best at this time of year. It’s fine if they can rapidly process and distribute the excess, however our potato plants have big Help Wanted signs up for every job category (never seen before), as do all the trucking companies.

Then you have a huge tonnage of rotten potatoes to shift.

My wife bought dehydrated potatoes last shopping trip. We have enough freeze dried spud boxes to handle another Houston freeze out this winter (I also have stockpiled firewood). But she forgot that I am on a low carb diet. Looks like she will have to eat the spuds while I feast on steamed brussel spouts and broccoli. Our dog will get the leftovers.

Being very old, retired and on a fixed income presents its challenges. This year will be one of “low spending” like Petunia is practicing.

So on the one hand, we’ve got Jackwad Duncey calling for hyperinflation, and on the other hand Weimar Boy Powell printing $120 BILLION per month, telling us inflation is transitory, with that trollfaced Treasury Secretary assuring us as well.

Otherwise known in some circles as the Hobbit of Hyperinflation :)

Sure was a hell of price to pay for “two weeks to break to curve.”

Governments everywhere are full of incompetants. Their politics dwarfs into insignificance compared to their ability to make any crisis worse, and at an exponential rate. They’ve surrounded themselves with spineless technocrats who will find a way to justify what crazy idiocy they come up with, and a media who will accept their every press release.

You are led by idiots, become independent.

Need a third party. These clowns have taken us from the greatest creditor nation in the world, to the greatest debtor nation. Only took 60 years!

Welcome to week 90 of “2 weeks to flatten the curve.”

Wow, wa’ happened to our exports?

We need to force China to take our recyclables again, fill those empty TEU’s!

Recyclables are super low value exports and don’t move the dollar-needle.

Who cares about the money element, turn those compacting machines back on and fill those empty cargo containers, make it look as if we’re doing business, like back in the day a few years ago!

My guess is that REAL GDP is negative in the same pattern as REAL interest rates are negative.

And, if depreciation and government “overhead” are deducted, the numbers are grim.

The protected political/bureaucratic class is clueless.

Cheers,

b

Brewski,

I agree. The numbers have been fake for so long, faking numbers is now a science.

The political/ bureacratic is paid not to know anything. Just keep your job and your mouth shut.

Agree with you guys, but have you ever tried to explain this POV to people who accept the doctored info? They look at you like you’re talking about Roswell. I simply ask them, if everything is so rosy then why are people taking on 7 year auto loans, 30 year mortgages, or where did all the homeless come from?

Many folks under 40 with decent 5 year degrees are on the treadmill, stuck, and lucky if they own (payments) on a house or condo. That is not what I call prosperity by any stretch.

I agree also, just look at the infrastructure in most of America. It tells a story.

Because politicians and their cronies are essentially just looting the treasury at this point – the last act of a failed nation.

By living beyond it’s collective means for decades through borrowing, the country is effectively eating its seed corn.

It’s taken a 5X increase in the national debt since 2000 and a 9X fold increase in the Fed’s balance sheet since 2007 to (supposedly) increase “real” median incomes by 6% (total. not annually) since 1999. Median net worth has (supposedly) increased 10% since 1998.

The country and most of the populace are actually broke, which will become obvious once the asset mania finally collapses, whenever it happens. There is a day of reckoning in store for American living standards and nothing can stop it.

Yes, I know there has been increasingly unequal income and wealth distribution. Unfortunately for the populists, more equal sharing of predominantly fake wealth won’t work more than temporarily either.

It’s still a mirage, no matter how it’s divided.

High, but still understated inflation. And inflation subtracts from nominal GDP growth to arrive at real GDP growth. In other words: if inflation is a lie, then real GDP growth is also a lie.

Fifty years ago, you could raise a family on one income. Yes, a TV was relatively more expensive and so was air travel. But the basics that you really need like food, shelter and healthcare could be provided for.

Try to raise a family on one income today! So, where is this phenomenal “growth” of the past 50 years? We really need new definitions.

That “Trade Deficit in goods and services” gets offset by investment flows from foreigners buying bonds, stocks and real estate. (in other words: the bubbles).

Just imagine what happens when these bubbles burst…

WOLF is up 33% today. No, unfortunately I don’t own any shares.

Just for fun, look at their 30-year chart!

This ‘flation is getting very ‘staggy.

We are right back on the trend before the C19 hit. Down and faster. After Trillions of sugar water all got we got is inflation and more off-shoring and more non-productive consumption. Congress had better start printing another dose of sugar 3 times the size. The Fed is becoming a political liability for Congress. The Military needs trillions to counter hyper-sonic weapons of which you will be hearing hair on fire MSM/security complex jabber jaws start telling you that we have no defense and are doomed. Rocket Boy will have them also. This will start as soon as the dust settles one way or another on the 1.75T spending thingy that is rattling around Congress. We got a lot to be thankful for and the holidays need to reflect that. To hell with blind consumption.

Wouldn’t rampant house price increases add to the GDP? They may be discounted in inflation calculation fudge, but should still show up in GDP, shouldn’t it?

Only for new construction.

“This 50-year chart is an indictment of globalization over the past three decades by Corporate America.”

We owe the next generation of Americans an apology…

NOT “we.” I had nothing to do with it, been railing against it for years. Most people had nothing to do with, many railed against it. There is only a relatively small number of people that did this – politicians and corporate decision makers. And they got immensely rich off it. Nothing to do with generational — plenty of millennials in power that are also driving this forward.

They destroyed the future of the children, and they’re still doing it. Not to mention the fact that, as a Gen Xer, I never got to enjoy the benefits my parents had.

Ditto Wolf.

Mr. Richter

Could you double check the inventory number.

My eyesight for these GDP tables is not great but I read that the 3Q 2021 real private inventories increased +90.8 billion from 2Q 2021, which is a +2.07% annual growth rate.

If this is correct, that would mean private inventory growth accounted for slightly more than 100% of the 3Q real GDP’s +2.0% annual growth rate.

And that would mean Real Final Sales were negative, which seems like bad news to me.

Perhaps we are talking about different aspects of inventories?

Richard Greene,

OK, I see where you’re looking at. Your figure is the difference between two changes.

Go to page 9, line 40:

Change in inventories was a decline of $77.7 billion (5th column from the right). So inventories fell to a multi-year low as I pointed out.

But the decline was smaller than the decline in Q2 of $168.5 billion. You can see in the chart as well that the decline was smaller by comparing the lengths the last two segments.

The difference between the decline in Q2 and the decline in Q3 was a $90.8 billion.

This means that inventories declined further, to a multi-year low, but at a slower rate than in Q2.

In terms of what contributed what to QoQ GDP growth, it’s conceptually a little strange. For example, household consumption of services contributed 3.7% to the 2.0% GDP growth. But services account for about 70% of GDP. That page measures the change of a change. IMHO, this whole page of what contributed to GDP growth is somewhat silly when taken by line-item.

Thanks for the details

I’ve followed Real Final Sales for decades rather than Rea GDP including volatile inventories.

I know the advance Real GDP estimate can easily change by one percentage point after a year of revisions.

But 99% of my attention is on leading indicators, not GDP for the prior quarter.

For one example:

There has been a large decline of U of M consumer sentiment since Spring 2021 — a decline of that amount is typical in the year before a recession begins:

https://tradingeconomics.com/united-states/consumer-confidence

And then there is the “Biden Factor”:

— No matter what the numbers are today, Biden will figure out how to make them worse !

“You cannot taper a ponzi scheme”

I really like the quote, just heard it for the first time. We’re about to find out if it can be done! I think we should start a betting pool on whether the Fed completes the taper to 0 asset purchases, my next stop is predictit.org.

What if low interest rates are the PROBLEM and not the SOLUTION?

What if it is discovered that low rates initially are stimulating, but protracted, they breed bad things in the economy and market.

What if the Federal Reserve is supposed to do certain things, and is then hijacked and directed to ignore those directives and mandates…and there is no one to stop them?

Ahhh, regarding:

What if it is discovered that low rates initially are stimulating, but protracted, they breed bad things in the economy and market.

We all believe you here on WS because that is why we are here. Great comment. Unfortunately, if it crashed tomorrow the Powers would simply say, “We didn’t see that one coming, or no one could foresee”…..

Then the news cycle would focus on a few nearsighted stories.

I’ve been buying more tools and fixing my shop this past month. At least it feels like positive action in these crazy times.

Wolf, do you agree that the next decade of SP500 average annualized returns will be below the historical average? I suspect 2-6% per year through 2030.

Since you didn’t get an answer:

When stock valuations are very high, which they certainly are today, stocks returns over the next ten to twelve years tend to be very low.

The correlation of the Price to Sales Ratio and the stock returns in the next 10 to 12 years is very high. The P/S Ratio is currently at record highs.

https://www.multpl.com/s-p-500-price-to-sales

GDP, has still not been hit by the inevitable high end job losses that are coming.

The economy has fundamentally changed and there are many high end jobs that are going to vanish.

It was amazing how quickly things turned during the Dotcom meltdown. Everything changed within literally a few months. There are literally generations that have no idea their employment and financial futures are in jeopardy. Unemployment is never enough and it does not last.

U.S. trade balance, or net exports of goods and services, has been negative for 41 years. It started on the scary death spiral downward in the 1990s. For me, thinking about it became sort of like thinking about death – try to keep it mostly out of consciousness so one can function without anxiety.

Why is consumer spending on foreign goods and services considered a “domestic product”? How much of the Consumer Spending (70.5% of total GDP) is on foreign goods and services?

For me concept of GDP has always been nebulous. How is it actually used, and by what institutions?

“Why is consumer spending on foreign goods and services considered a “domestic product”?”

The costs of those products that were imported are subtracted from GDP; exports are added.

I’ve been following Wolf now for a few months and love the depth and perspective. Based on what I’ve read here I’ve taken some actions I believe to be, and hope will turn out to have been the right path.

On a positive note:

Expecting hyperinflation and shortages my wife and I pulled the trigger on building a house this spring- thinking if we waited a year we’d probably have to pay a lot more. We’ve run into a variety of logistical issues with ICF Forms, re-rod, and rising prices on everything.

Now we’re down to just plain unavailability. I’ve given up on ordering a 16×8 garage door or any windows until perhaps the dead of winter when perhaps nobody is ordering windows here in the Midwest. But on the garage door; I found a local craftsman who will build a wooden garage door for me- and these can be really beautiful. At current prices for the garbage coming from Asia stuck on ships I’m actually glad to pay a little more, and glad the money stays here in the local economy.

I wonder- at what point would enough product substitutions like my garage door start to make a difference. These things are happening – who’s counting? Wolf wrote about business formation a while back- hopefully those numbers keep climbing. All we here is mostly bad news from the media. Why is whatever cheap plastic junk on those ships so important? There is a lot of fear propaganda everywhere.

The velocity of money no longer measures the number of times that the average unit of currency is used to purchase goods and services within a given time period.

The velocity of money has likely remained relatively steady but that is not how it is reported.

The massive wealth transfer to a few billionaires has rendered the measurement useless.

Money that makes it into the real economy, likely goes through a similar purchasing cycle as seen in the past. The way that the velocity of money indicator is currently measured, simply reflects that billionaire acquired money is dead money.

It’s worse than that. The real growth rate is overstated, because the inflation adjustment is understated.

Didn’t I just read Wolf’s article on how rent increases are going to push up CPI next year? This 2% number may just be a single point on a downward slope.

I am hoping that things do not continue on this path. As noted by others, this is going to produce hardship on people who had nothing to do with creating the monster. But that is always the way. Sometimes, some of the people who are responsible get caught up in the turmoil. Often times they are not. think: Hindenburgh disaster, the Johnstown Flood, Collapse of Levis during Katrina, forest fires in California, Colorado, etc. Nature is brutal enough without our less-than-useless political hacks making decisions that cause more harm than good. Add to those, bureaucratic institutions like the FED, and we have a real mess to deal with.

The question we need answered is: Can we recover from this state or are we entering a total collapse of civilization?

I know that sounds pretty grim.

What is happening now to pull our economy out of a nose dive? Does anyone believe that this proposed tax on “billionaires” unrealized capital gains will somehow help? Many of the Congress Critters may be stupid (albeit greedy), but their staffers are not. Are they looking at what happens next? I have no love for billionaires, in general. Are we so naive

a population that we think billionaires have a vault full of gold like the dragons in movies? If we are going to collect a trillion dollars in taxes via that method, where does the actual money come from? Can you imagine dumping a trillion dollars worth of stock for sale in early April to pay taxes? What happens to stock values? This isn’t simply a shifting from one asset to another. This is totally extracting that kind of money from the market. Or perhaps, this isn’t a serious proposal at all – merely a distraction from the presentation of election fraud and chants of “Lt’e Go Bandon.” We still need some serious thinking on how to recover our economy.

Boy… that inflation chart. Damn! You gotta go back to Volcker doing his thing to see inflation this high.

i’ll try to clarify how inventories impacted the 3rd quarter by quoting my own paragraph on them (not yet published, so you’re getting an exclusive…)

a smaller shrinkage of private inventories in the 3rd quarter increased gross investment and hence GDP, as real private inventories fell by an inflation adjusted $77.7 billion in the quarter, down from the $168.5 billion of inflation adjusted inventory shrinkage reported for the second quarter, and as a result the $90.9 billion relative increase in real inventory growth added 2.07 percentage points to the 3rd quarter’s growth rate, after an inflation adjusted $80.2 billion decrease in real inventory growth in the 2nd quarter had subtracted 1.26 percentage points from that quarter’s GDP growth rate…however, a smaller shrinkage in inventories indicates that relatively more of the goods produced during the quarter were left sitting in a warehouse or on a shelf, so their quarter over quarter increase by $90.8 billion meant that real final sales of GDP were relatively smaller by that much, and hence real final sales of GDP shrunk at a 0.1% rate in the 2nd quarter, after real final sales had increased at a 9.1% rate in the 2nd quarter, when the larger decrease in inventories meant that real final sales of GDP were that much higher…

“a result the $90.9 billion relative increase in real inventory growth added 2.07 percentage points to the 3rd quarter’s growth rate,”

The phrasing is wrong. I have seen this everywhere. In Q3, inventories fell at a slower rate than they fell in Q2 and therefore SUBTRACTED LESS from GDP in Q3 and than they’d subtracted in Q2.

This wasn’t quarter-to-quarter growth of any kind. It was a decline that subtracted less than the decline in the prior quarter. That smaller subtraction reduced the overall subtractions from GDP growth by 2.07 percentage points. It didn’t “add” to growth. It “subtracted” less from growth.

here’s the full release & tables from this report, Wolf:

https://www.bea.gov/sites/default/files/2021-10/gdp3q21_adv.pdf

see line 40 in Table 2 for the +2.07 percentage point addition to GDP from 3rd quarter inventories

see line 40 in Table 3 for the actual changes in 2012 $ used to arrive at that…the last column has the +$90.8 billion change in real inventories from the preceding period, ie the difference between the 2nd Quarters -$168.5 Billion and the 3rd Quarter’s -$77.7 Billion..

i know it doesn’t seem logical, but it’s that +$90.8 billion that’s added to GDP..

I know this table inside out. Read what I said again. What the BLS said is expressed wrongly because the BLS text and table are boilerplate that is not designed for this inventory situation — the boilerplate is designed to express flow of money (GDP), not changes in level of stock (inventories). This is the only place were “level of stock” enters GDP, which is otherwise a measure of “flow.”

And the media keep repeating that boilerplate, and you keep repeating it, though it’s wrongly expressed and is misleading. So read again what I said:

“It was a decline that subtracted less than the decline in the prior quarter. That smaller subtraction reduced the overall subtractions from GDP growth by 2.07 percentage points. It didn’t “add” to growth. It “subtracted” less from growth.”

I don’t do boilerplate. I cut through boilerplate. That’s why people come to my site. And I provided a chart so you can see what’s happening once you get away from boilerplate.

it occurred to me that we were talking about two different metrics, Wolf, and that i was probably misrepresenting what i am obviously referring to…so i went back and read what you wrote (in the original post) and i agree with it…you’re talking about GDP in dollars, such as would add up to something near $23.2 billion as of Q3…i’ve been talking about the percentage change from quarter to quarter, and often just referring to it as GDP (incorrectly)….obviously, a lower value for Q3 inventories results in a lower value for Q3 GDP….but when that lower Q3 value is less than Q2 inventories subtracted from GDP in that quarter, it results in a relative positive change in the change of Q3 GDP…

so yes, my initial wording is incorrect in that i should be referring to “the change of” in each case, ie “the change in gross investment” and so on…i’ll try to come up with a better way to express what i’m referring to with the next release…

all that notwithstanding, the drop in inventories in the wake of the pandemic sets us up for some pretty large boosts to GDP when it unwinds..

the following are the changes to private inventories (in inflation adjusted 2012 dollars) for the prior quarters of this year, all at annual rates, from the pdf i cited above: 1st Quarter: -$88.3 Billion; 2nd Quarter: -$168.5 Billion; 3rd Quarter: -$77.7 Billion

those are historically large decreases, as your graph above shows…

so i believe that inventories will eventually be rebuilt from the current levels…to illustrate what that would mean to the future change in GDP, if half of the inventory drop over the first three quarters of this year should be restored in the 4th quarter, real inventories would grow by $167 billion…that would mean a $244.7 billion relative increase would be applied to the change in private inventories in 4th quarter GDP (ie, the change from -$77.7 billion to + $167 billion) …that alone would boost the change in 4th quarter GDP by ~5.5%, even before one adds in any other GDP components…

“all that notwithstanding, the drop in inventories in the wake of the pandemic sets us up for some pretty large boosts to GDP when it unwinds.”

Yes, and it will be spectacular. When production and transportation catches up, or demand slows down, there will be a magnificent boost in inventories. Auto dealers are so low and automakers so backlogged that this increase in inventories will go on for a long time.