Even the Fed is getting antsy about this raging mania house-price inflation. Housing Bubble 1 is starting to look cute in comparison.

By Wolf Richter for WOLF STREET.

House prices spiked 19.7% from a year ago, the biggest year-over-year increase in the data going back to 1987, according to the National Case-Shiller Home Price Index today. But the national index of this raging mania doesn’t do justice to individual metropolitan areas, where price spikes reached up to 32%.

The Fed is getting seriously antsy about this massive house price inflation, on top to the regular consumer price inflation that has hit 30-year highs. Just today, the president of the Federal Reserve Bank of St. Louis, James Bullard, who’d been fretting months ago about the “threatening housing bubble,” came out with a proposal to reduce the assets on the Fed’s balance sheet right after the taper is completed by mid-2022, which would purposefully allow long-term interest rates, including mortgage rates, to rise significantly.

“Everything can occur much faster than it could have in the previous recovery,” he said.

Markets have started to anticipate the end of QE. Long-term interest rates have started to rise. The 10-year Treasury yield is currently at 1.55%, the highest since mid-June. The average 30-year fixed mortgage rate today was 3.16%.

The mind-boggling price spikes in the charts below for individual metropolitan areas are based on the “July” Case-Shiller Index. The July data are a three-month moving average of closed sales that were entered into public records in April, May, and June. That’s the time frame we’re looking at here.

House price inflation. The Case-Shiller Index uses the “sales pairs method,” comparing the sales price of a house to the price of the same house when it sold previously, and includes adjustments for home improvements. By tracking the amount required to buy the same house over time, it is a measure of house price inflation.

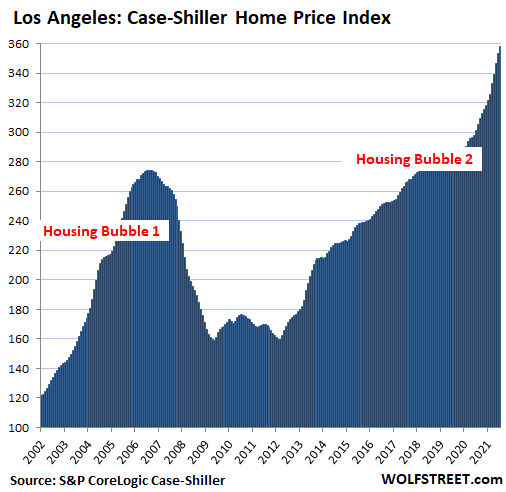

Los Angeles metro: Prices of single-family houses rose 1.4% in July from June and spiked by 19.1% year-over-year.

All Case-Shiller Indices were set at 100 for January 2000. The index value for Los Angeles of 359 means that house prices have soared by 259% since January 2000, despite the Housing Bust in between. The Consumer Price Index (CPI) has risen by 62% over the same period.

This puts Los Angeles on the dubious pedestal of being the most splendid housing bubble on this list. All charts below are on the same scale as Los Angeles to show the relative heat of house price inflation in each market since 2000.

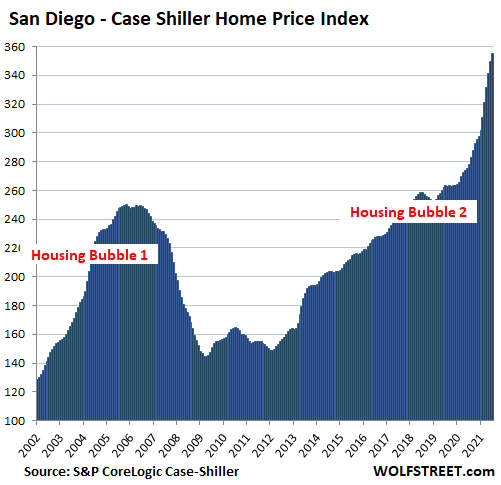

San Diego metro: House prices rose 1.6% for the month and by 27.8% year-over-year. Since 2000, prices have exploded by 255%:

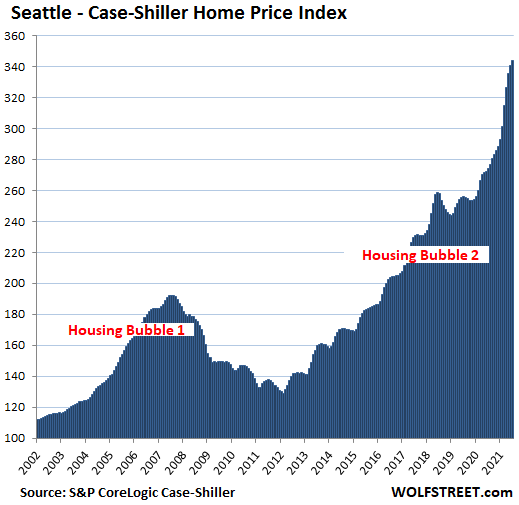

Seattle metro: House prices rose by 0.9% for the month and by 25.5% year-over-year. Since January 2000, house prices have soared 244%:

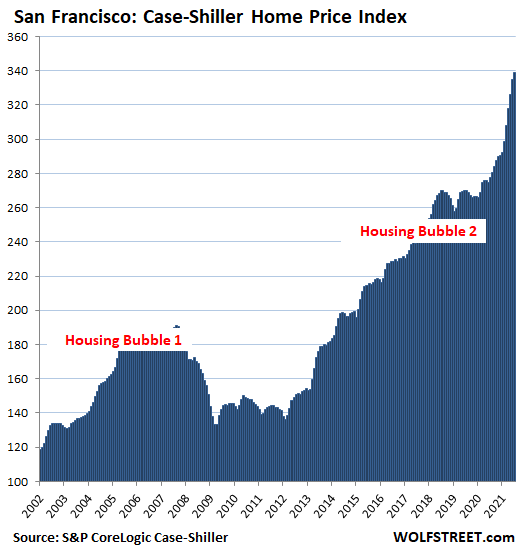

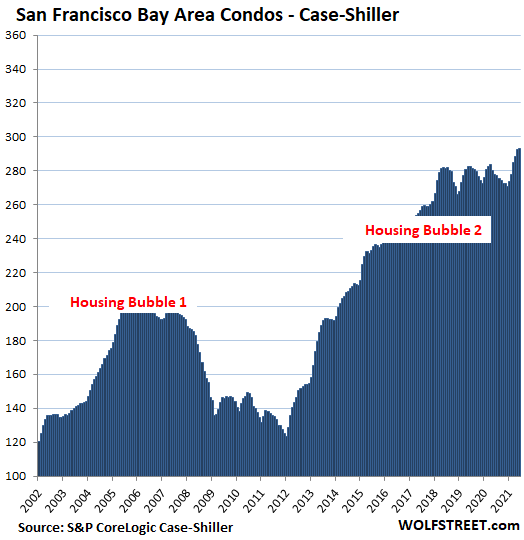

The San Francisco Index covers the five counties of San Francisco, San Mateo, Alameda, Contra Costa, and Marin. The peculiar thing here is that while prices of single-family houses have been spiking, condo prices have gone nowhere in years.

The Case-Shiller Index for houses rose 1.2% for the month and 22.0% year-over-year. Since 2000, prices soared by 239%.

Condo prices have been wobbling along the flat-line since early 2018. For the month, condos rose 0.3% and were up 5.4% from the beaten down levels last year:

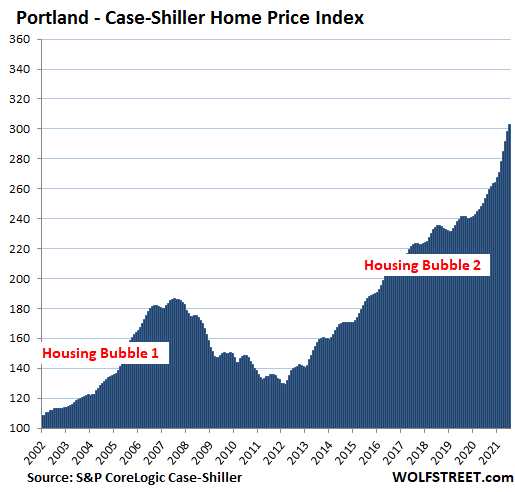

Portland metro: House prices jumped 1.5% for the month and 19.5% year-over-year, and are up 203% since 2000:

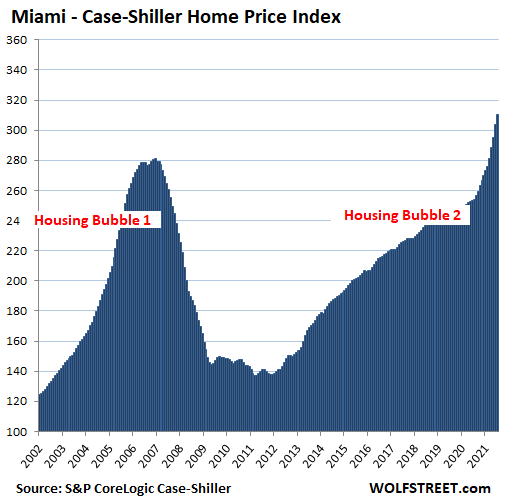

Miami metro: +2.2% for the month, +22.2% year-over-year. Prices are up 210% since 2000:

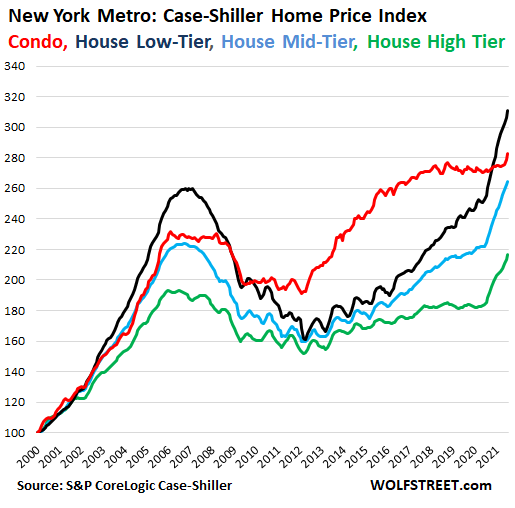

The New York metro covers New York City plus counties in the states of New York, New Jersey, and Connecticut, ranging from some of the most expensive real estate in the US to less expensive areas:

- Low-tier house prices have spiked the most, up 1.6% for the month and 21.8% year-over-year (black line).

- Condo prices have been about flat since February 2018, with an uptick over the past few months. +1.8% for the month, +3.8% year-over-year (red line).

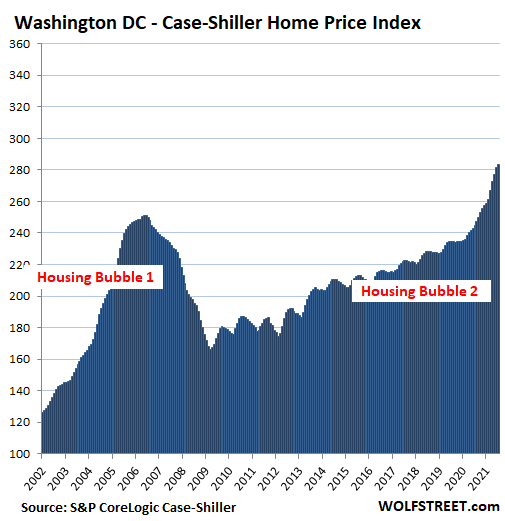

Washington D.C. metro: +0.8% for the month, +15.8% year-over-year:

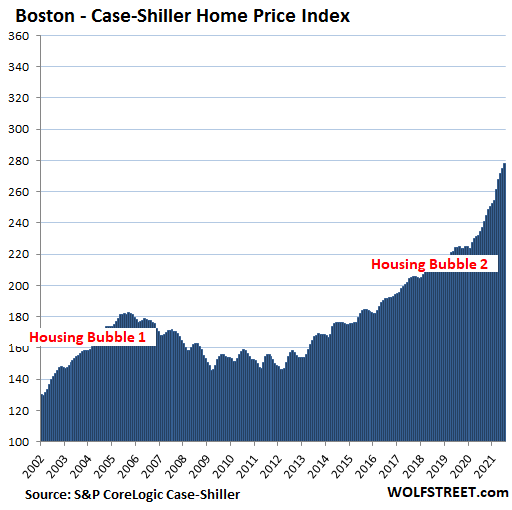

Boston metro: +1.1% for the month, +18.7% year-over-year:

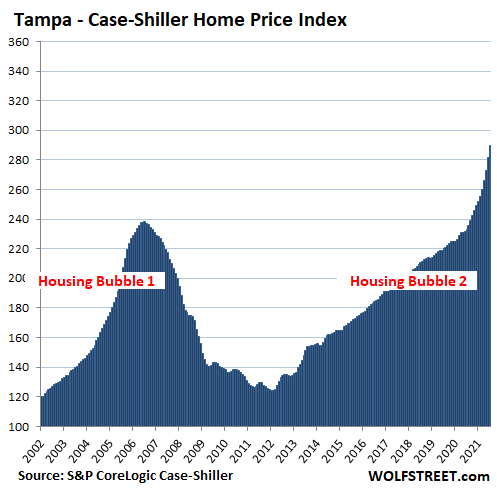

Tampa metro: +2.9% for the month, +24.4% year-over-year:

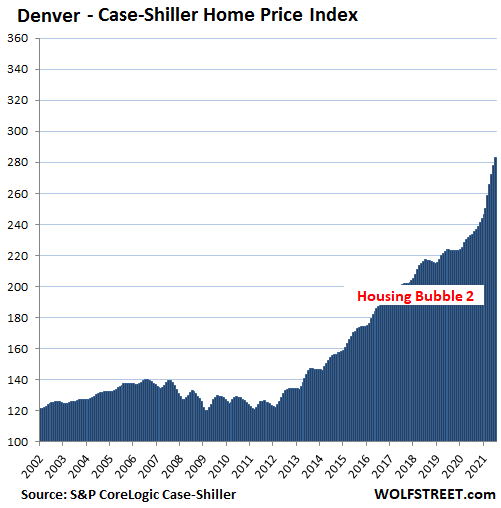

Denver metro: +1.8% for the month, +21.3% year-over-year:

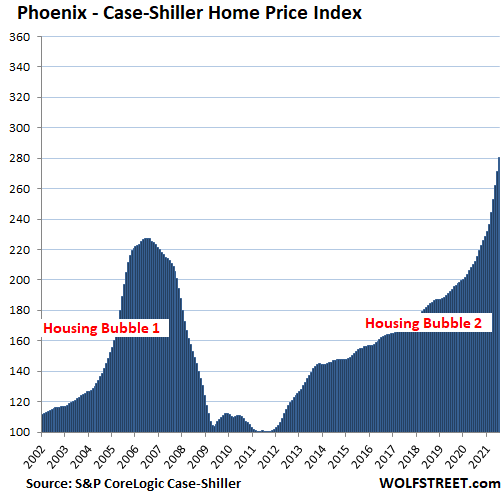

Phoenix metro, holy cow: +3.3% for the month, +32.4% year-over-year. The reddest-hottest annual house price inflation among the most splendid housing bubbles here:

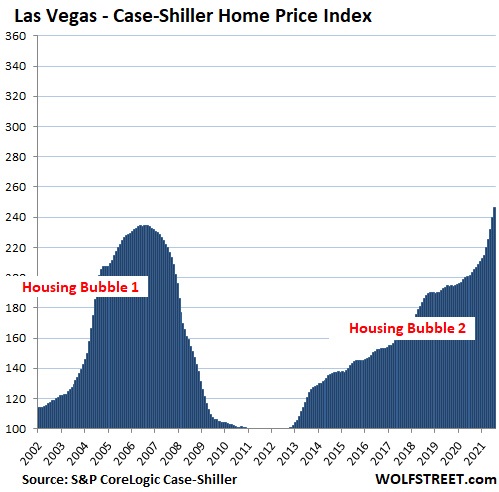

Las Vegas metro: +2.8% for the month, +15.8% year-over-year:

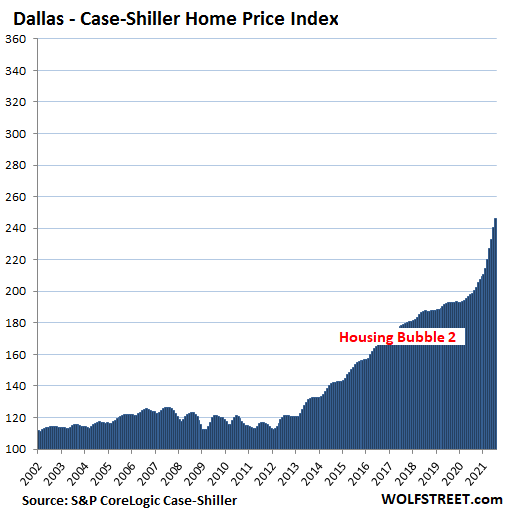

Dallas metro: +2.4% for the month, +23.7% year-over-year. The index is up 146% since 2000.

The remaining cities in the 20-City Case-Shiller Index have experiences less-hot house price inflation since 2000 and thereby don’t yet qualify for this list of the most splendid housing bubbles.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Federal Reserve Board is suppressing market forces and assuming responsibility for the economy. If stocks and RE prices crash, and I lose my job, is the Federal Reserve Board going to fund my bank account, educate my kids, and pay my rent? If not, they should let me make my own economic decisions in a free and open market.

They Federal Reserve Board has no business tinkering and experimenting with things that can backfire on the population.

why not?

if the federal government can experiment on the massive scale that they do with UBL program under the guise of pandemic stimulus, why can’t the Fed have a party too?

I mean… fair is fair right?

The interesting thing is what the initiation of the crash will be this time. I would imagine what will happen over the next few months is that people will be rushing like made to lock in loans

Hi. I really hope it all crashes hard. Too much inequity. For us working people, we cant afford a house let alone the rent costs! Paying 40% of income for rent only is criminal. It must end.

Q. for MCH.

What is UBL and what is it supposed to do?

Universal basic income. You get some free money for being alive. Not enough to get rich, enough to get by.

Just look up Andrew Yang and UBL and you get the idea.

I actually think a big part of this whole thing could be a result of people seeking out SFHs with yards for the social distancing opportunities they afford- this could also be part of why demand for Condos/apartments has fallen

Bobber you lost the thread with “If not, they should let me…”

Once you mentally give “them” any power over “you”, you’ve lost.

Just go ahead and make your own decisions, and vote out anyone who tries to tell you otherwise. Vote at the polls. Vote with your wallet. Vote with your feet.

Find out who funds the weasels trying to control you, and boycott all of them. You don’t have to be perfect, just do the best you can, and get your friends to join you. Even a 10% drop in their revenue will kill them financially.

And every time they try to tell you what to do? Just laugh at them.

Politicians cannot survive the scornful laughter of a public who no longer believes in their leadership.

Great words of wisdom!

“Politicians cannot survive the scornful laughter of a public who no longer believes in their leadership.”

This comment should win the thread.

A close runner-up from ‘Jon W’:

“The best way to beat them is just don’t have an income in the first place. Move somewhere cheap and do something else for work. The big city career thing is a rentier trap. Winning is committing to a giant mortgage for life. Losing is paying massive rent for life. Either way they’ve got you. If enough of us refuse to play the whole thing falls apart, and this is starting to happen but it will take time.”

Sometimes the only winning move is not to take part.

@GC

OMG The light from the neurons firing is blinding!

I’m very worried about the future but at least we can all feel very lucky to have a President Biden at the helm to steer us through troubling waters! He’s been through these situations before and I trust him. If Trump were in office then we would be in trouble!

I don’t respect the Federal Reserve power in any way, because they have abused it.

I was merely exposing the half-brained logic of the Fed’s interventions. Even a two year-old knows what happened to Winnie the Pooh. He stuck his nose in the cookie jar, and couldn’t get it out. Anybody notice Powell has the same problem on his hands?

WS,

Politicians believe they can survive anything as long as they give away enough money. Or promise to.

Just look at the latest equalizers from the jackasses, subsidized 20 year mortgage for first time home buyers within limits. Program is called LIFT.

I am waiting for these guys to come up with a program acronymed SHIT or F***.

As Safe Harbor mentioned above, those private corporations printing currencies and buying real estate like no tomorrow. That is the reason of house price rising as well as all other prices because of value of 💲 Decreasing. That’s not a bubble that’s end of the system. Also they don’t care about struggle population will have to endure due to hyper inflation since they are part of population reduction program.

Nah, you are screwed.

Capitalism is for the trickled down upon.

Repeat after me, socialism for the rich, capitalism for the poor.

This is not a housing bubble. It’s a dollar crash. Track RE against M1 and you’ll see no bubble.

It is a housing bubble, made possible by credit inflation which includes M1.

Anything close to “normal” interest rates will freeze the housing market. It’s only through the loosest aggregate credit conditions and credit standards that housing remains “affordable”.

That advertisement for Classic Metal Roofing Systems is looking more and more accurate by the housing bubble articles. The whole dang thing is ready to go to flames here.

Depends. do you work for Goldman Sachs?

Ahh but in case you missed it, its working out great for a couple of Fed bank presidents who have been insider trading in REIT’s. Its a rigged game. I imagine this has been going on for a long time its just that these are the first 2 Fed bank presidents to get caught. Must be nice to make the decisions that control the money and make bank on it. Its a big club that you and i aint in. Its the same big club they keep beating us over our heads with each and every day. Nothing suprises me any more. It’s a country led by crooks. I believe it’s all planned the FED aint worried about how high housing prices get. If anybody thinks they give a crap about the little guy they should go see a shrink.

Yes it is rigged.

Should have bought two…

Can it really be a true bubble this time? While I agree that it’s gotten completely out of control, I see multiple factors that make me concerned that this will be a persistent inflation of price.

To start with, we don’t seem to have the risky mortgages that we had in ‘08. Secondly, this time around, supply has dropped dramatically behind demand. Thirdly, the effects of Covid have resulted in supply and labor shortages and raw material price spikes, further delaying the period in which new housing construction could bounce back, not to mention persistent zoning problems preventing affordable housing from being built.

I’m just a damn millennial trying to be a first time homebuyer feeling crushed under the weight of it all and the goalposts always rocket forward just as they start to get within grasp. I was thinking about waiting out what appeared to be a “bubble” but now I’m thinking that there may only be a “correction”, and failing to move now will result in higher interest rates with little chance of a truly massive house price drop. I’m naturally cautious about FOMO fallacies, but the factors just don’t seem to be there to truly bring housing back into a more affordable area. I feel as though the only true way would be for a massive amount of the population to literally die or stop looking for housing. Someone tell me if I’m overlooking something.

Well mortgage apps are on a steep decline so that’s good news for us.

Same boat though, 90% increase in pay YoY and what would’ve been a comfortable easy purchase in a house I’d be happy with 18months ago is now out of reach. What was $300k is now $400k.

Feels incredibly unfair.

I went back to school, spent more money on education, have a great side gig, sold my used car for a profit(thanks to Wolfs reporting)bought a truck cash. Still isn’t enough. I guess I’ll stop eating? Not really sure where else I can make cuts tbh.

Cem,

The cuts you need to make are in your own expectations…

There are actually plenty of opportunities all over the place, perhaps not in the wheelhouse of what you think you deserve…

This blog is full of wise folks who think outside the box…

Relax, settle back, and soak up the words of wisdom and think rationally and logically…

Determine what you really want and wait for it to come to you…

Sometimes, my friend, the best thing to do… is nothing…

You’ll be fine…

You could not have put it better! Instead, we have panicky FOMO going on in society and markets. As JFK said when urged to run for President, “No, things are not bad enough yet.” But they will be. Free money for borrowers will not go on forever.

Good advice COWG. Here in the Bay Area prices jumps are crazy and at eventually will be unrealistic. So I keep paying my rent which fortunately hasn’t changed and wait. Meanwhile, I enjoy my job which pays me, my friends who don’t charge me, the air I breathe for free, the hills I walk where nature freely abounds, then take my Chevy Volt to the nearby McLaren and ask them if they can tune up my care, just to get a whiff of their free sniffiness.

The free stuff in life is best, ESPECIALLY when it’s funny!

Amen.

Cem, please don’t join the FOMO crowd, you will regret it. I’m early 40s and completely know where you are coming from. This time actually IS different, but not in the way you think.

We aren’t going to have a correction, and we aren’t going to have a bubble pop. Instead we are going to have a depression level turn that will crush those who have leveraged themselves. It’s not going to be 2020, 2008 or 2000. It’s 1929.

I know, it’s very hard to believe that right now where we have prices going wild, stock market going wild, and things seeming to be getting “better.” But that’s the story of how these turns happen.

You will need to hang on for a few more years. We are not there yet. SPX needs to get to about 6000 and the madness needs to get to a true fever pitch. That’s when it will begin to fall apart.

Just don’t get in over your head, make sure whatever choices you make will allow you to weather a major economic downturn and crisis.

Nothing a war can’t sort out.

Anyone making claims on what WILL happen is to be considered with a very small grain of salt.

Fact is, nobody knows nothing. And furthermore, they ain’t going to.

A depression is but one possible scenario.

Longer term, noticeably declining living standards for most Americans is about as certain an economic outcome as there is.

Without a middle class, we will turn into another Russia-like society.

Replying to Augustus Frost:

At least in my hood/san Diego, the living standards have been going down quite a lot for middle class for last decade or so.

You have single family homes with 3 bedrooms where 3 families are living. I am sure one family can easily living in the living room as well.

I don’t think any crash coming as people are expecting here

Since you know exactly what the future holds, please share some more of what your Magik 8-ball told you.

Or is simply: The Future is Unknown

Augustus Frost has it right. No one knows exactly what will happen, but declining standard of living for middle class is a lock.

Are you a first time home buyer?

If so, vote Jackass, and they will help you with the LIFT bill, but remember you must vote Jackass, not Dumbo. Then you too can afford your first home

If first time buyers are priced out,eventually the sellers will have to lower their prices. The market can’t move or turn over without starter homes selling.

More homes were bought last year by 2nd home buyers than 1st home buyers ( I saw that somewhere, may have been on this blog).

… It means more people are falling into renting.

The price level is set at the margins when supply is low – the few buyers with the most money determine the price, not the highest number of buyers with average money. This is the kind of market we are in, at least in Silicon Valley, where the supply is ~1 home for sale to 5-10,000 people (per my crude calculations).

I have seen that kind of market in a country with income level 1/10th of the US, where supply is low and only the top 5% of the population can afford to buy.

The result of this is a massive restructuring of society towards renting, and as a result, massive impoverishment for 90% of the population.

I think this is the direction America is going, and I have seen it happen in Eastern Europe in the 1990ies.

It’s scary as f**k. But Eastern Europeans like me emigrated, while Americans, where would we go?

Or sell to Zillow, second home buyers/foreigners/speculators who will be post it in AirBnB…

It’s the outside money that messes everything up. The wages of the locals don’t seem to matter anymore.

I think that’s the biggest factor. Cash purchases seem to be driving it. Soon corporations will own all the places to live, all the vehicles to drive, and rent them to the rest of us for as much as they can get as we slide into corporate feudalism (breathes into a paper bag). I have no idea whether that would be a sustainable shift to a new normal or just bubble fodder.

What I do hear from the development side is that land prices are high, many of the buyers are foreign and seem like finance people instead of development people (they think development potential is much more predictable than it is). Due diligence periods are down to 48 hours. So that part looks bubbly, anyway.

We have been in an asset price inflationary period for a long time. Remember if you aren’t paying cash for a home it’s a leveraged investment that can wipe your down payment out. Fed went all-in in 2009. If they don’t soft land the bubble then the government or the Fed may not be in a position to save everyone this time.

Put down as little as possible, buy at the peak and live there for 5+ years without paying any mortgage while the bank hides it from the market? Just like what happened last time?

Rising mortgage rates will correct the high prices. 4.5% or so will be a problem for many. Fed kept rates via manipulation too low for too long like the did before last housing crisis.

Wake me when the Mortgage rates go over 10% and you can actually make some money by saving it.

We have two generations that have never saved a dime, nor have they learned how to. It’s going to be very hard for them.

As usual, their intent will be to pass the cost onto someone else. After all, apparently Americans have a guaranteed birthright to minimal living standards at someone else’s expense.

😂 amen. Hopefully that’s not a lifetime

Fellow millennial here. Unfortunately, there are no good options. Just realise that the govt/retirees/rich want the bulk of your income for the rest of your career. This is what all the big brains on Wall Street are trying to figure out every day, while you’re toiling away.

The best way to beat them is just don’t have an income in the first place. Move somewhere cheap and do something else for work. The big city career thing is a rentier trap. Winning is committing to a giant mortgage for life. Losing is paying massive rent for life. Either way they’ve got you. If enough of us refuse to play the whole thing falls apart, and this is starting to happen but it will take time.

Once you realise your dream is but an illusion it’s much easier to give it up. Sadly our generation will have to fight hard to bring things back to fair, but other generations have had to sacrifice far more, and unfortunately life just isn’t fair, and uuu can’t choose when you are born.

So many willing to play along. Many who must not be looking at retirement unless retirement means selling the home they’ve spent all their money on for their entire life.

I refuse to go in debt like that. I’ve got a life to live.

Cheers to you!

In order to live without income you have to live in a fertile farmland so you can grow your own food and feed your own animals. But constructing houses at farmlands prohibited by governments under disguise of protecting farmlands. Moreover rivers and water canals have been sold by governments to private corporations so finding fresh water to live will be problem.

You seem to be better informed than most on this forum. Whatever you do just realize that either way there is alway a risk but it never pays to bet against the US. Those hoping for a crash are assuming that the Fed would allow it when in fact the Fed would much rather have inflation than a contraction.

Uhh, uncontrolled inflation IS a crash.

“Someone tell me if I’m overlooking something.”

There are other ways to obtain a place to live besides 30 year mortgages or renting for life. In Olden Days people would start with land. From that point there are many options, such as a used trailer house (good ones are hard to find), or build a small house then add on later.

If a person has to depend on $100 an hour tradespeople for all the labor they are not going to get very far. Better to buy a few tools and learn to use them. Yes one’s results may only be adequate and less than what an “expert” can do (when they are motivated to do quality work) but at some point good enough is good enough.

My point is that there are other ways to do things besides narrow options presented by people who want to make us all life-long debt slaves.

I totally agree with your comment and have said the same for years.

One problem is permits and approvals + fees which can be an expensive process. (As an aside, I live in a non building permit rural location.) Another problem is the quality of work that do-it-yourselfers often finish up with it. I’ve been a carpenter for over 40 years and pretty much immediately spot deficiencies and it can be pretty bad. One neighbour down the road from me had taken the title of the ‘worst construction I have ever seen’. Several years ago someone actually bought the place and then spent at least a hundred thousand dollars just bringing it up to snuff and making it safe. The electrical work was dangerous, the structure was crooked and out of square and sometimes ceiling/floor joists were unsupported. The septic was condemned.

But I really agree with your comment and have one suggestion to add for DIY home builders. Take lots of pictures at all stages that prove you built to code or better. It will be good to have for insurance or a future sale. The fit and finish might be lacking, but that is always an easy cosmetic fix for another time.

Or you can hire a GC to sign off on it

“permits and approvals + fees which can be an expensive process”

This is one of the biggest rackets of the lot!

Vested interests lobby Governments to impose ‘over the top’ requirements which are so expensive they exclude incomers who could easily compete against them on price.

An early instance of this use of ‘safety’ as a means to lobby against competition, was James Watt who lobbied against, and bankrupted, Richard Trevithick, who’s high pressure steam engine went on to drive the industrial revolution. Watt who made an atmospheric pressure engine argued that high pressure was dangerous and could kill people. That was true, but engineers went on to make 250psi steam engines normal and taken for granted all over the world. Watt set back progress for years but he’s a hero.

The same techniques are extensively used today particularly by EU bureaucrats in relation to all sorts of things eg. atomic energy, etc, etc.

Trailer Trash – I looked carefully at this option about 10 years ago, back when I was in my 20s and land was more affordable. As an engineer with no college debt I was better placed than most to make it work, but I couldn’t.

1) I was working 50 hours a week and so was my wife to have “good careers”. So were kept busy.

2) you need a significantly higher down payment before a bank will consider lending to you to build a house (vs. buying a home)

3) when you’re in your 20s making a meager salary and paying rent, it takes a very long time to save that big down payment.

4) by the time you get the means together to do all of this, it’s time to have kids. Now you and your wife are still working 100 hours a week, trying to raise kids, paying your rent and paying a very hefty childcare bill every month. Now you don’t have the time or the money to build your own place.

The solution to all of this is family. If you happen to have a retired Dad or father in-law, with a few bucks they could lend you to help with the down payment and some carpentry skills to help you build your place (because they are retired and have some time), then you can make it work. I know people who have done this. I didn’t have any family to help me.

The compromise for me was to buy a fixer upper. I am still stuck in that limbo of not enough time to finish the house myself and not enough money to hire trades to do it. It’s not a nice limbo to be in and it’s easy to wind up there.

The solution is family to many of life’s challenges, but very few Americans born into this country (excluding relatively recent immigrants) are willing to make any personal sacrifice or inconvenience. Always ready to volunteer someone else to make the sacrifice, especially progressives who love big government programs.

You act like getting someone else to sacrifice on your behalf is some progressive flaw instead of something more universal. How many conservatives do you know that wouldn’t mind using military action for a whole host of global issues… so long as it isn’t anyone in their family volunteering for that military service?

Let’s bypass partisan politics and examine something more fundamental: why is self-sacrifice for others considered a *heroic* quality in most morality tales? Who is assigning the heroic quality, and why?

Context matters.

You are so right on. My first home was $35,000 with a 1st and 2nd mortgage in 1975. Paid off the 2nd and sold the house for $65,000 after 5 years. Moved to another state; bought 5 acres and built a home myself with the proceeds. Never mortgaged it except for $10,000 against the 5 acres. Split off 4.5 acres and sold it. Employment was difficult but we simply cut spending. Even with 3 kids, we got ahead since we had a place to live with no mortgage. Sold that home and moved again and repeated. Lived in that home 10 years and repeated. No mortgages ever. Sold that home and moved. 70 years old then and bought a home, free and clear. Still free and clear with new $375,000 home. All because of no mortgage.

People say they can’t build a home. Well, get a job framing and knowledge comes real fast. That’s how I learned. Then I specked about 5 homes and made a living on all of them. It can be done.

In order to live without income you have to live in a fertile farmland so you can grow your own food and feed your own animals. But constructing houses at farmlands prohibited by governments under disguise of protecting farmlands. Moreover rivers and water canals have been sold by governments to private corporations so finding fresh water to live will be the problem.

On the other hand people who came to cities were the inheriters of buildings remained from old world order. They didn’t spend money to construct just cleaned mud around. While other people were free to build a home anywhere they wish. Many living town constructed that way. But unfortunately todays world all people are slave to private banks and central banks.

No risky mortgages? Hahahaha, the government (FHA) is insuring 3% down-payment mortgages to buyers with subprime credit scores, no problem.

But it’s not the banks that carry the risks, it’s the taxpayers. So the banks aren’t going to blow up this time because they have shuffled most of the mortgage risks off to the GSEs.

What about the risk to investors who hold the MBS? What are the implications of that?

You mean the FED, who’s buying all of them? Pffffft…..

If the government insures the mortgages, there are nearly no risks to these “agency” MBS. That’s why they trade similarly to Treasuries.

Taxpayer takes the risks.

@W

Awe sh**. They’re never doing Northern Rock again are they?

No, they’ve cut out the private bankruptcy this time and gone straight for the bail out. I get it.

Loss or not, that is accounting and bookkeeping.

The central bank can issue money as they will if there is will to do it. They can even issue the money straight away without any counterpart. Ok, they may have to change their accounting rules, but if there is the will that is possible.

Issue money, buy bad debt, write off bad debt and depending on the accounting total amount of money could be more, less or the same.

Fiat money in bank accounts have no serial numbers, no identity and are not related to anything physical. There are records and bookkeeping rules, but rules can be changed and records modified as long as it is done by the rules.

This is hilarious. AirBNB encouraging people to buy properties with Motley Fool’s ‘Millionacres’ thinking short term rentals will pay off the mortgage. Otherwise seemingly normal intelligent humans holding onto their empty second and third homes to continue to capture the price appreciation. I have seen this movie before. It was in 2007 when I was the only human I knew piling up cash when everyone else at the party was buying as many properties as they could leveraged up to their eyeballs. In early 2009 I was also alone scooping up lots with houses for less than the impact fees.

I can smell the crash coming.

That’s residential real estate. What’s your take on commercial real estate holdings by the banks?

It’s ok Wolf, you have been through this before with Bear, ML, AIG, etc. just bend over and take it like every other tax payer will, it won’t hurt, we promise, you won’t even notice anything is wrong.

Exactly Wolf. It’s a disgrace and we reward this type of behavior. It needs to stop. Risky mortgages are everywhere right now.

By 2013, they were down to 3% on conventional loans. I bought a house with one.

An excellent point. I guess I just sort of edited it out in my mind because it was the fed backing it and will do everything it can to manipulate itself out of a crash for the wealthy at the expense of taxpayers.

I was really just referring to the NINJA loans of yesteryear, and thinking the forces don’t seem right for the same style of correction.

This is, however, an area where you have greater experience than I about analyzing the implications of such things. I do think my generation is completely fucked at the end of the day and that our retirement plan should just be heroin. Which is what they want. Work for us then die immediately.

I don’t believe it is a bubble at all because of the reasons mentioned. Housing has been “discovered” by the financial class and there is money to be made in it. There will be corrections but prices in the future will not be less than they are now they will be more.

Show me any area where prices are less in the last five, ten, twenty years, excluding major cities with blighted conditions, disasters etc.

Everyone is chasing yields and housing shows a great potential for yield, more so than any other financial vehicle. It is a hard asset that has a very real and steady return and will continue to do so in the foreseeable future.

The best hope is a correction in the market that allows the prepared to act. Interest rates will go up at some point, confidence will waver at some point and then the chance will appear.

It’s an everything bubble. Yes, everyone is chasing yield but those that are levered up will soon find out that you can’t buy your groceries and pay your bills with falling house and stock prices. Cash is trash right now but just wait a little longer.

Finally someone who gets it. I’m nervous that the OP is going to read doom posts from people like “Here it Comes” who go “I’ve been around and have seen it, a depression is coming”, with very little to no theory or evidence to support the claim. There are so many reasons why the entire economy is worlds different than 1929.

OP should buy when they’re ready and can comfortably afford a place with savings.

The only reason you wrote this is because you do not grasp what causes an asset mania and it’s termination. It isn’t driven by “fundamental” events but collective psychology.

The economic and social conditions which market participants call the “fundamentals” aren’t even close to actually being favorable. It only appears to be due to manic crowd psychology (including central bankers and government officials who implement these idiotic policies) which makes people collectively optimistic enough to inflate the asset mania to such ridiculous heights and live beyond their collective means for so long, as in decades.

The actual “fundamentals” are mediocre to terrible, depending which aspect you have in mind and where. When collective psychology reverses, whenever that is and regardless of the supposed reason, the actual state of American society will be revealed, like those who are actually swimming naked but no one knows it until the tide goes out.

Do a simple google search on the 18 year real estate cycle. To give this realization the validity it deserves a paper was published from Harvard. This is a credit bubble. And once credit dries up the illusion bursts.

You’re probably thinking the Fed will keep the money flowing forever but then you’re looking at hyperinflation

It’s okay, I was initially holding out because I believed it was a true “capitalist” market bubble, where too much leverage and risk will correct sharply. But I thought about it more and think that it is as wolf pointed out, the loans and the market may be garbage in reality, but it is backed by the fed this time, who refuse to let the wealthy lose. They will just force taxpayers to bear the burden. I have plenty of savings and can buy comfortably (a condo, can’t reach for a house). I just think that the market isn’t set for an asset price correction and is set for rates to rise. But I’m always open to competing viewpoints.

In the long run, I think the future for my gen and younger is fucked because of the long term federal policies for this sort of thing socializing the loss and privatizing the profit. And if anyone thinks the human race will pull its collective shit together and fix the climate, I think they’re naive. This is why I’m a high functioning borderline alcoholic LOL

Didn’t Soros warn Blackrock not to go into China, and didn’t Blackrock do it anyway? It’s another thing altogether to have the house you are living in “margin called”. P43 called it the “home ownership society”, a New Deal without the government, how did that work out? In the 30s the family farm disappeared and now ask yourself what is the state of American agriculture? Don’t expect any better outcome when the national housing industry is financialized.

@DP

“Everyone is chasing yields and housing shows a great potential for yield, more so than any other financial vehicle.”

That’s because interest rates have been artificially supressed by the Fed using QE for 12yrs. If QE stops the scramble for yields stops which would take us into a whole new (or old) World.

Just sayin’

Agreed, that is in part the reason, but a reason nevertheless. Investors follow gain no matter where it might lie. And now it lies in housing and will for some time I believe. The reasons don’t matter, only the opportunity that presents itself to those that are prepared to see it and take advantage of it.

Things change all the time and housing at some point might not be a vehicle for investment (more rent control, taxes, fees and fines etc.) replaced by some other asset class that pays out more. But for now housing is what everyone wants and those with the money to attain it will, while those that don’t will feel that the system is against them.

And those without, feeling that the system is against them, will either resort to drastic political steps (like nationalizing housing) or setting corporate owned houses on fire.

You can only extract so much wealth and leave the common people as chattel slaves before they revolt.

You said it correct. Everyone is chasing yields. 10 years ago most alternative investments, currently, weren’t around or being hyped. Now everyone knows of all the alternatives. And that’s what the market manipulators wanted—-the masses participating in investments they don’t understand.

LOL. Real and steady return until people can no longer pay the rents. Oh also, don’t forget that in a community of all renters, those renters will have no issue voting into office local politicians who will raise property taxes, as it won’t affect them anyway! You’ll say that the landlords will just raise the rents. But rents are determined not by what the landlord “needs” to make a good return, but by what the renting population can afford to pay.

Not to mention that there are major costs and aggravation to being a landlord that I suspect many of these “investors” haven’t internalized.

The housing market is creating a gigantic island top. Look at the lumber market as an example. Interest rates will reset higher creating a greater income gap to affordable price gap. A gap which is already historically high. Reversion to the mean is inevitable. When jobs are lost,and owners that purchased a home in the last 18 months are forced to sell, the market will start to correct. Additionally, the number of house not being occupied on a continuous basis is astounding. Supply wouldn’t be so perilous if non-occupied homes were taxed appropriately. The left leaning Dems will eventually pass legislation to mitigate corporate owned housing.

Just want to comment that “reversion to the mean” doesn’t work the same way in the post-2008 “QE forever” world as it did before 2008. And it didn’t work the same from 1971-2008 as it did under the pre-1971 gold standard either.

The dollar isn’t a fixed unit of measure. Don’t look for reversion to mean in things measured in dollars. (Rising interest rates don’t always imply lower prices, when the supply of dollars is soaring. Look at the 1970s for many examples.)

The more fundamental units are energy and hours of labor, and nowadays neither of those is entirely stable either.

If anyone knows a better way to measure relative-values to look for situations prone to reversion-to-mean, I would love to hear it!

Does Wolf have a comment on this insight?

Supply has been constrainted by COVID and by the belief that prices will be higher in the future, so why sell now? Give it another year.

Interest rates will spike much higher, which will drive down demand. We just need to see a plunge in the stock prices and the housing prices will follow.

The current bubble is completely driven by low interest rates, but inflation will force higher rates, even if it means lower economic activity.

Higher inflation expectations have driven housing prices higher, but persistent inflation will mean higher interest rates, which will ultimately lead to much lower home prices.

Both bonds and homes will see falling prices in the coming years.

Rental applications reason for leaving current home are dang near 50% “owner is selling”….

About 25% are snake oil salesman excuses.

And about 25% legit reasons..

Gotta believe the market is gonna flood..

1. Folks are cashing out at the peak

2. Moratorium is over.

It’s really hard to say. Anyone can speak endlessly about all of the negative these days from ballooning home / rent prices, national debt, “transitory” inflation, etc. Yet on the other side is the acute housing shortage that’s only going to get worse. Without getting political, where are these millions of illegal immigrants that Biden is welcoming going to live? That’s an honest to goodness, a-political question. Well, for the most part, they’re not going to be living in tents.

But, just because there’s not the poor lending standards from 15 years ago doesn’t mean they aren’t an accumulation of other factors that aren’t equally as bad or worse. When you have the amount of debt here in the US, China (commerical) and other parts of the world, this has to be of grave concern and can’t be looked past. The social unrest is something to seriously consider as is the geopolitical situation with Israel vs Iran’s nuclear standoff or the China vs Taiwan risk.

For those of us who were really paying attention back in 2006, we all said the same thing from 2006 – Sept 2008: How much longer can this craziness last? Well, I would say we’ve reached the point of 2006. As such, we’re probably 2 years out from a fairly major event rearing its ugly head. Between now and then, the housing market will slowly pull back about 5%, certainly not enough to convince you to jump in.

Today, it’s not lax lending standards. It’s hedge funds paying 2 times asking price for turning whole subdivisions into rentals. It’s all these crazy stats that Wolf throws at us.

Good luck with making your decision.

in 2006 you saw the mortgage companies starting to file bankruptcy. Business was starting to dry up. it was the canary in the Coal min. Housing companies started struggling soon after as there were no mortgages for their spec homes. Then the investment bankers.

I have not yet seen the canary. I thought perhaps the end of forebearance but that event looks to be a meh.

You said it right. Hedge funds drive the pricing by taking most of the supply.

Last housing crash, Congress, the fed and its member banks stepped in and funded the sale of large batches of foreclosed homes to the big PE funds.. Keeping the prices from falling as much as they should..

I imagine they will do the same again..

So don’t get your hopes up for cheap houses and decent interest rates.

The game is rigged.

While RE rises and falls in value, I, too, wonder if an overall increase is permanent. Like the permanent high prices in California, the factors you mention point to permanently higher valuations. I’d also like to know if this thinking is missing something. Thanks for posting.

Everyone is saying we don’t have the risky mortgages we did. Is that actually true? Or is that what TikTok is saying and then everyone should flood in to buy at “Incredibly low interest rates!!!!”.

You are in a situation right now where:

– People haven’t paid rent (it’s not coming due)

– People have deferred payment on mortgages (that’s coming due now, or are being refinanced to the back end of existing mortgages)

– People haven’t had to pay student loans (coming due in January @ 2x)

– People have received massive stimulus and PPP loans

– People have been YOLOing the stock market/nfts/GME/AMC/crypto

– People have great credit because they don’t owe anything, for the moment

– People are buying houses far above ask value (not considering the tax appraisal coming from that)

– People are not working

– People are leveraging existing, already inflated, assets to buy second homes

– People are pulling equity out of their homes at over inflated prices to do renovations

– People are still getting Variable Rate Mortgages saying “I’ll refinance when interest starts going up” but by then will be too late

I mean the list goes on and on here. You’ve essentially got the Fed backed into a corner with two options: A. Let inflation occur, devalue the dollar to allow the crazy economy we have now (Will never happen because they don’t want to lose credibility globally)

Or B: Raise interest rates, and as things start to crumble when everything comes due and people get foreclosed on, they will have to go higher and higher because they own the MBS’s, not the hedge funds, this time.

If the long cycle of ever increasing debt and lower inflation goes into reverse (or debt increasing faster than spending), the reverse will be ever decreasing debt and increasing inflation(or debt reducing slower than spending). So a steady management of this process could be an equally long cycle of rising interest rates. And now is the cusp. Housing could then be in for a multi-decade decline (yes possible look at Japan).

Japan has had a declining population and has historically had housing built with a finite (~30 year) lifespan. Very different than the US.

There are mobile homes for sale in Florida built 1958-1963, lasted 60 years, in solid condition, listed for under $100k, 2000 – 4000 sq ft lots. Factory built homes are usually cheaper than site built homes.

Japan has been printing money since the early 1990’s. And the USA has followed suit.

Collapse is coming, it’s inevitable.

Nah, the chart is so vertical it begins turning to the left.

I’m ok with this

Housing is still RELATIVELY cheap here in Texas. But with all the Californians buying everything here that looks like a habitable house for cash and way above “asking price”, this may change.

After leaving California in 1992 for Texas, I knew we couldn’t afford to move back. Now California is coming here instead.

In the past, high property taxes have acted as a drag on house prices in Texas. Some how that has become disconnected.

Speculators don’t care about property taxes, only end users do. This is a speculators’ market.

Back in the Eighties, when I was a flipper, we ignored property taxes. We cut expenses by not paying them. It takes years for the city to foreclose because of back taxes. When the deal is done, the taxes are paid with the profits.

Roddy, the issue with that is that if a larger and larger percentage of houses are corporate/investor owned, the towns and cities aren’t going to let the process drag on for years. They’re going to need the money then.

If that is true, then speculators are the first to cut and run when prices start to decline.

There is very little supply now, but just wait for what happens in 2022.

If house price inflation continues to outpace CPI and income growth then Texas will become a high tax state due to its property taxes.

Assuming 2% property tax rate in TX, 0.5% in CO and 1% in MA.

Income tax is 0% in TX, 4.5% in CO and 5% in MA.

If house prices are 2 times incomes, Texas taxes are 4% of incomes compared to 5.5% in CO and 7% in MA so TX is low tax.

If house prices are 5 times incomes, TX taxes are 10% of incomes same as Taxachusetts compared to just 7% in CO.

Re: After leaving California in 1992 for Texas, I knew we couldn’t afford to

move back.

Have you thought about the consequences of that statement? First, I think you’re right. California is in the same boat as other populous, liberal states. They are in their own little world. That world is at odds with less populous, conservative states. Hence we have the blue/red state divide. These large blue states have been living high off the hog for decades. But it was a false wealth funded with borrowed money and promises. They seem to be at a stage where there is no more money available to borrow nor are their promises working. The only thing left to try is to have the red states bail them out. No wonder tempers are flaring.

Blue states pay more in federal taxes than they receive back in federal benefits. The opposite is true for red states, they are the takers. 70% of economic production in the US comes from Blue states. If red states seceded tomorrow, they’d be even worse off, despite already being significantly behind in education, infrastructure, business and healthcare.

This is getting tiresome. States don’t pay anything, and they receive very little (as states). People do. And it’s well established that redistribution goes from red voters to blue voters.

Not to mention that each $1 of “production” is not made equal. You might think that if Instagram produces $10 billion in profits, it’s equal to 1,000 farms making $10 million each. But the farms don’t need Instagram. Instagram needs food, energy, and water.

How dare you interject facts and logic into this ridiculous blather.

@RightNYer

You are just wrong. Blue state voters in aggregate, pay in more in federal taxes than they receive back in benefits. Red state voters in aggregate pay less in taxes than they receive in federal benefits.

You can say the opposite all you want and call it “well established”, but data and numerous studies say you are wrong. I can provide links if Wolf allows. Blue states run the country’s modern economic engine. Other than farms, red states are supported by blue states from a federal funds level.

@RightNYer: From AP in late 2017:

“Connecticut residents paid an average of $15,643 per person in federal taxes in 2015, according to a report by the Rockefeller Institute of Government. Massachusetts paid $13,582 per person, New Jersey paid $13,137 and New York paid $12,820.

California residents paid an average of $10,510.

At the other end, Mississippi residents paid an average of $5,740 per person, while West Virginia paid $6,349, Kentucky paid $6,626 and South Carolina paid $6,665.

Mississippi received $2.13 for every tax dollar the state sent to Washington in 2015, according to the Rockefeller study. West Virginia received $2.07, Kentucky got $1.90 and South Carolina got $1.71.

Meanwhile, New Jersey received 74 cents in federal spending for tax every dollar the state sent to Washington. New York received 81 cents, Connecticut received 82 cents and Massachusetts received 83 cents.

California fared a bit better than other blue states. It received 96 cents for every dollar the state sent to Washington.

On average, states received $1.14 in federal spending for every tax dollar they sent to Washington. That’s why the federal government has a budget deficit.”

Maybe you can make an argument that some cities within blue states don’t pay what they take in, but they’re more than supported by their suburbs.

As a blue-state worker, voter and tax-payer, I’m more than happy to help other countrymen and women in need, even if they’re in a different state and vote differently than me. Many are stuck in this situation because of poor primary education and a cycle of poverty brought on by states that aren’t willing to fund education. A simple look at economic mobility ratings by state will show red states are consistently and significantly worse for economic mobility, which correlates nearly perfectly with education rankings and academic achievement. Like it or not, the modern workforce in today’s economy requires education.

Blue states have their own share of problems, but this isn’t one of them.

sc7

This is true in a static sense. CA and the urban northeast we’re “red” politically when they achieved economic supremacy 50 years ago, and the south was poor and “blue”. CA elected R governors as recently as the 90s, and the state legislature in the 90s was evenly divided. Point being that things aren’t static, it takes decades for states to see the fruit their economic policies in either direction.

It’s very clear that the economic trends are toward low tax, low regulation states, most of which are red (WA excepted as a blue state with no income tax). FL and TN and TX and the relatively low tax inland western states are on the rise and population and income statistics show this. The urban northeast and CA have enormous built-in economic advantages with high quality universities and deep water seaports, they should be the wealthiest places in the country.

Happy1,

“CA elected R governors as recently as the 90s”

Minor correction: Last Republican governor was Schwarzenegger, Nov 2003 – Jan 2011

It’s true that the inflation is unevenly distributed, and this creates geographic wealth-inequality issues.

Those living in less-inflated states have less to fear from deflation, and lose out (in a relative way) when inflation raises the paper-wealth of others even further.

As I have noted above, red states are dependent on blue states for revenue that drives federal benefits. So, if blue states suffer from deflation, red states will suffer as a byproduct.

sc7

You presume that red states would continue the social programs that account for this money transfer. If the red states were a separate country you can be assured they would not.

Blue state finances, by and large, are also far worse off than the red states, with the exception of KY for red, and MN for blue. The structural budget deficits in IL, NY, and the urban northeast are well documented. CA is always one major stock market decline from fiscal catastrophe. There is a reason people are moving away aside from cost of living and economic opportunity, there are some people and especially businesses who make long-term decisions about their domicile based on these reasons.

Most Red states, as you say, can’t feed themselves without the big blue states funding. So I doubt if Mississippi, Louisiana, Oklahoma, Arkansas, Alabama etc contribute a quarter of what California does to the feds coffers, combined.

Yep. Better start buying in the Midwest now. In 20 years after a big rise the price of housing will mean the Texans will start moving to the cheaper Midwest. :)

And still, the Fed buys $40 billion in mortgage backed securities a month.

All during the most WTF out the wazoo housing bubble 2.0.

“The Fed is getting seriously antsy about this massive house price inflation, on top to the regular consumer price inflation that has hit 30-year highs.”

That the FED can continue to juice housing at the same time they pretent to worry about house inflation, yet never get asked about it in MSM is had to handle.

Yes. I don’t think they actually care about the inflation they’ve caused. They only care that the effects were so great that it is impossible not to connect the dots and blame them for what has happened.

They actually LOVE the inflation. They’ve been gunning for it for years. Now it’s here and they’re probably gleefully diddling themselves in private. Look how wealthy these guys have become. They are evil robber barons.

That’s EXACTLY right in my opinion and I’ve said it from the start … they want the inflation, they just don’t want to look like they were asking for it. That’s the only reason they keep jawboning about “maybe we’ll raise rates when the economy improves” … nonsense! For 10 years they have been saying everything is great but they still have to keep up emergency measures while the markets tripled!

They will just do this for a little while and either the market falls just from the talk or they have to raise once or twice and the market falls….then they will come in with QE again and it will have to be bigger than ever before.

The frustrating thing is watching the gold and silver prices react to the news as if this is the start of some rate hike cycle that will raise rates to “normal” like 5% or something and as if more QE isn’t coming. Higher rates should mean higher gold because the ensuing crash in stocks guarantees even bigger QE.

Yes. They purposely under measure inflation using fake hedonics and ignoring the fact that human beings need to eat and drive and heat their homes. They are aiming to prop up assets owned by the ultra wealthy and to decrease the true cost of government borrowing for their political overseers.

Assume these prices hold. Rich get richer, and homelessness explodes as more and more middle class sink into the why work 50 hours per week just to be short on rent and pay extraordinary healthcare costs.

The cost of housing is already driving thousands to tents.

Expect local policies that attempt to increase supply of more “affordable housing”. Problem there is that all you get, without more distortion of market forces and all the things that come with that, is more supply at current prices. So then begin the various subsidies to builders and buyers (paid for by the rest) paired with a nice dose of confiscatory policies. You know, in the name of equality and fairness, which only became necessary because of the excesses of the Fed and .gov’s actions in the first place.

They are trying to goose housing through NATIONAL policies. Have you seen what’s in the $3.5T proposal? It’s repeating all the mistakes of the last 30 years, which is to provide housing and rent subsidies, which soon lead to even higher housing prices, requiring even more stimulus, etc…. They mean well, but my advice is to not follow the recommendations of well-meaning folks who lack critical thinking skills and can’t fight their way out of a paper bag.

Why don’t they force the Fed to stop repressing the interest rate, so people can save their money, earn an unobstructed return, and buy a reasonably-priced home when the time is right for them?

my taxes paid are high and I watch that money being hand out through subsidies and grants… affordable housing for those who choose to not work, and unaffordable housing for those who do. I’d be better off sucking the govt teets

From memory I believe you were looking to save and put down a down payment. It truly is a thing to watch this beast take off. Almost like the school bus that is down the street with tail lights blazing. Your only hope is that you have a parent home that can take you (i.e lend you $250k) to get to school

We were saving. Now we have a child in long term mental care and our savings is dwindling. $1100 per month just for healthcare premiums, and they don’t cover a lot of the mental care. Savings are sliding. Rents are higher. Why even try.

Yes it is.

Here in SoCal, they are building millions of apartment units. If you look at recent pictures of Lake Mead, Lake Powell and Oroville Dam, you can see a water and power crisis coming soon. Now that Newscum is past the recall election, expect a series of serious water and power restrictions. As if new construction doesn’t require more water and power. Build, Build, Build! What happens to the value of your house if the yard is dead and your power and water bills are higher than your house payment?

“Oroville Dam”

It was only four years ago that plentiful rain nearly caused the main and emergency spillways to fail. Chicken Little keeps telling us the sky is falling, but somehow it never lands.

I do agree that some central planning is required to keep from exceeding available water and energy resources. The question is, who is going to do it: public agencies that answer to the public (assuming that is possible) or private bankers that answer to billionaire parasites.

Well if there is a housing shortage how can you be against building of apartments? Whether you or anyone else likes to live in an apartment it is a more energy, water and other resource efficient housing stock than single family developments. Water in the state is a problem but urban areas use a very small fraction of water in the state, and restrictions on use have more to do with water rights laws in the West than any particular politician’s position. If you want to look at low value use of water, perhaps cast your eyes upon forage crop usage in the Imperial Valley.

Power is a separate interesting question, and would love to see a more up to date post by Wolf on power generation in the state. It’s been a while since we’ve seen one from him.

Yep. Water is a big problem for us in the west. And getting worse.

You don’t have a chart big enough for Austin, TX.

Same chart everywhere, every hot bs corporatized and anesthetized blue haired city. Same chart.

It is a chart of a couple of waves. What do waves do?

They come crashing down.

I know a secret. If I was incontrol of the levers at the fed I could erase all the money creation with mouth malarkey in an instant, profit on puts, and retire.

It’s realy not more complicated than that. Don’t study finance, kids. Study crime.

The Case-Shiller Index includes only one metro in Texas: Dallas. It doesn’t even include Houston. Something to do with the rules governing public records of property transactions in Texas. They found a way around the rules in Dallas, but not in the the other metros.

The Case-Shiller uses public records for its source of data.

FOMC’s job is to control RUN AWAY INFLATION, of which any high school graduate or an average house wife can tell you that house prices have gone through the stratosphere, FOMC did NOT do it’s job. Therefore FOMC is a CORRUPT institution led by a servant POWELL to it’s masters,,, the elites pumped up their investments and come up with BS excuses why they are NOT controlling or doing their jobs, at least they should give back their paychecks for they did NOT do their jobs and the poor and middle class have suffered financially hearing from different people about they’re being evicted due to rents have skyrocketed and these are the ones with jobs! These stories are in the news or online and in every neighborhood. These charts ARE A GIVEN AND NOT SURPRISINGLY AT ALL.IF ANY, It’s a CONFIRMATION that FOMC is CORRUPT!!

Inflation didn’t rear its head until this year. And it’s a component of printing too much money. Which they restarted last year.

Unlike many states, Texas does not require disclosure of actual sale prices. This is why someone can buy a $10 million house, get an appraisal notice for $5 million, then protest that appraisal and have its value cut to $3 million for property tax purposes.

Appraised values are often fairly close to actual value in middle class subdivisions where there are plenty of comparative sales, but it’s one giant scam at the very high end (like so many other things in our society today).

I’m not sure how Case-Shiller got around this in Dallas, to get the data they need for their index.

In Dallas, they worked a deal with the local Realtors board to get the price data for each home. But that was a lot of hassles, so they decided not to do that in Houston. This was decades ago.

There is an interview out there with one of the architects of the Case-Shiller index, in which he explained why Houston isn’t in the index. I forgot the details, but you can google it. It’s an interesting read.

Austin is on it’s own planet at this point. I invest in land across multiple states, and have some land in Austin, and the land value has increased 4-fold in the last 10 years, versus 6-8% per year average in other states and areas.

And Austin housing has increased about 3-fold in the last 10 years, with a 2-fold increase in the last 3 years alone. Now this of course depends on location, location, location…and a close second is school ranking as the schools in the area are some of the top rated in America (largely due to the wealth and intellect moving to the area daily and thus raising the ratings).

My land company does not buy in the Austin area at this point, as I can not compete with the wealth that is moving there from India, Asia, Russia, etc…plus a lot of foreigners are grouping together and buying anything they can get their hands on, and just renting out the houses and holding on to the land for future development decades from now. Austin is truly a global city, sort of a mini-Epcot if you ever visit…and as such, a lot of the new citizens happen to have been extremely wealthy individuals and families from other parts of the world. If you look at ethnic percentages, no ethnic group holds a majority, which is a very rare thing for a metro with around 2 million people…

Texans are always crowing about their state is a conservative stronghold. They ignore a few things. The big cities are all run by liberals. In Texas schools, white kids are now a minority. In a few brief years, the black and Mexican children will be 18 and voting. They will replace every elected official from governer and senator down to dogcatcher with politicians representing their interests.

Which means Texas will be turned into a new California. Sounds great!

That was the point of mass immigration all along. To secure permanent Democratic Party power.

RNY, I mentioned that above….Texas is becoming the new Cali.

It’s a slow process, but it is headed that way. Sooner or later, Texas will have a state income tax along with city income taxes like in Los Angeles. Then the incoming California folks will feel like they are at home here.

You are making a big presumption that people vote the way they do because of the color of their skin. This is already being proven incorrect in TX with an increasing percentage of latinx voting R in the last cycle.

It’s been said before that houses aren’t worth more, it’s that the dollar is worth less. And if the money supply increased by 27% in one year, is it a big surprise that housing is up 20%? It’s not enough to taper, the Fed has to start pulling this $8 trillion out of the economy before things really go to hell.

This was supposed to be under my name RightNYer. I hit enter too soon.

When everything is in a bubble, it’s simply because the currency is worth less. But the excess trillions can never be drained, or it will cause GDP shrinkage. The current inflation is forever. New inflation is debatable. Most likely all governments will use inflation to soft default on debts and deflate asset bubbles. Expect ‘lost’ decades ahead.

The Fed should have stopped buying MBS over 12 months ago, too.

The fact that we are just now discussing tapering is completely ridiculous.

Today’s Fed officials make Arthur Burns look like a hero.

Such dereliction of duty from our elite is an economic crime.

We will suffer the consequences for years to come.

Those charts look more akin to hyperinflation.

Yet Powell keeps buying $40billion a month in MBS, why?

Why? Good question. It’s not as if housing prices will completely tank on the news or the eventual slowly rising rates. A modest drop seems reasonable from that, same as what we’ll get when they’ve finished tapering purchases anyway.

What’s been baffling me is how prices have spiked so much. Rates have been zero for awhile. Income hasn’t risen that much. So it’s not like the combo of lower rates and slightly higher income has suddenly made buyers able to pay so much more. The rise must be coming from the *willingness* and the ability to pay more. Funny, because going into c-19, I thought most housing markets were already maxed out, that buyers had already hit their maximum willingness and ability to pay, that there really wasn’t any slack. At least in California. Wrong, I guess.

investors and games are afoot, my friends grandma passed 2 months ago, had 60’s fixer upper in Lakewood. Ca. they went to price it on Zillow tool and Zillow offered them 956K, 1% fees, 16L in work as part of sale, netted a huge sum…on sale today at 819,000…..I have other friends same thing…

Break away gains like this always find their way back….I expect it sooner than later, the fed trading the market is all the reason they need to take it down, 2 fed folks gone. more stuff coming out, debt limit….juicy

goodbye mr spalding

It worries me either way, whether it’s willingness or ability to pay.

If it’s only willingness, a whole lot of people are going to find themselves house poor and it will be a drag on the economy overall as they struggle to make the payments by cutting spending elsewhere, or they walk away altogether at some point.

If it’s ability…how? Was it stimulus money that made all the difference? What happens when they stops as it must? If wages are indeed rising, then it might make all these house prices more affordable, BUT that means inflation has just run really really hot and prices might stay that elevated. That’s not a pleasant direction either.

I’ve been seeing a top in the housing and stock markets for 3-4 years and have been wrong so far. Are we there yet?

I don’t think it is willingness or ability to pay. The Fed has put a gun to peoples’ heads. If you don’t want to lose 4% to inflation every year by “investing” in fixed income instruments, housing and stocks are the only thing you can buy. However, when prices are this high, evading the bullet is like trying to do one of those quick roll-around moves out of a Jason Bourne movie. It works well in the movies.

Interest rates have been low for a long time, but recent inflation talk now has people really scared about financial survival. People without housing are left out on a limb. If they don’t buy now, they feel they’ll lose the opportunity forever.

What was an economy is now a gambling hall, courtesy of Federal Reserve policy.

J-Pow is a lawyer who has a B.S. in politics…and thus we get behavior and actions that mimics a lawyer who is an expert in politics.

Kind of like hiring the mall cop to perform heart surgery…sure they can “do the job”, but you might not like the results…

Well isn’t a PhD in economics really mathematics and politics now about how to influence people’s behavior.

How much more is there to a market economy than supply and demand and price discovery and sound money?

He’s buying MBS to support the prices, otherwise housing would be tanking due to higher interest rates. He’s supporting the mortgage industry, and the reits, primarily. The higher stock prices are probably a secondary effect of the higher profits in housing and the corresponding wealth effect.

Q: When the government owns MBSs do they increase in value as the underlying home prices get medieval on ..?

So if the government bought $40B in MBSs a year ago would they still be valued at $40B or do they also get to increase in value with the market?

Sorry for the silly question on such a serious site.

Assuming they can successfully force a price rise in their portfolio of homes then yes, the mbs value would improve all else being equal. But, they aren’t equal because they also raise comparable rates over time which eats into that gain.

It is really just compelling investors to get out of bonds and driving their money anywhere else … and eventually everywhere as asset inflation. Anyone seeing that yet?? :)

No. An mbs is a collection of sliced and diced mortgages. No mortgage that I’m aware of has any claim to the future price appreciation of the collateral if payments are made on time.

MBS acts like most bonds except the pay down on the bond is faster. As the bond pays down, assuming the same interest rate, the bonds are worth less. This is true of a regular bond that has been paying out a coupon for a time.

What really affects the prices is a change in interest rates. If the market rate goes up or down, the price will move in an inverse fashion. MBS may react more violently depending on how it was sliced up. Every pool is different too. Which is why even most professionals don’t know what they are worth until the look at the pool and price each slice.

It’s been said before that houses aren’t worth more, it’s that the dollar is worth less. And if the money supply increased by 27% in one year, is it a big surprise that housing is up 20%? It’s not enough to taper, the Fed has to start pulling this $8 trillion out of the economy before things really go to hell.

Wolf, can you please delete the mistaken post up above? Thanks.

Good point and right on.

I had the same thought when watching baseball tonight and they were talking about a players recent contract on the Yankees for 90 million over 6 years. I think he was hitting .227.

Whatever. There are just so many things that make a mockery of normal lives and aspirations. No, it is not unreasonable for a young person to desire a house/home and expect to be able to buy one with normal employment.

I think when we look back in history this period will come to be known as the Last Housing Bubble. That is because the economic devastation to the entire RE, home building,mortgage, landlording business , when this one pops will be so great there will be no fuel left for another one ever. By the time those involved pick themselves up out of the ditch, bury the casualties and move on there won’t be enough energy, resources or economic credit left for another one.

Seems like we are at peak stock and housing and junk bond market. Everything will be different as the pendulum swings the other way. Fed has rewarded risk taking for a long time and has people over their skis.

In a way the government is running mmt by overspending and then trying to control inflation by new taxes. Problem is politically it’s easy to get the votes on spending, but not many want to tax their donors so the inflation tax it is.

Paulo,

“Normal employment” was shipped overseas or automated…

Then those displaced were sold on the college scam and were told they were smarter than they really were…

Then they found new and exciting lives in the service industries …

Lot of truth to that statement for sure.

Well, let’s just work harder at buying North American and support our friends and neighbours. I don’t know what else we can do in the short term?

Paulo,

How do we “buy American”, though? Do I buy a Chevy made outside the US, which benefits a US corporation and its wealthy shareholders? Or, do I buy a Toyota built in a US plant, which gives jobs to middle-class workers, but benefits a Japanese company?

Milwaukee Tool is owned by Hong-Kong based TTI, yet they have expanded manufacturing in the US in recent years. Stanley Black & Decker owned DeWalt has been moving more and more production offshore, yet some people buy DeWalt just because it is supposedly American.

I have gone the Toyota & Milwaukee route on both of these decisions. Primarily driven by quality, though I wonder if that is a byproduct of the US-based manufacturing and quality control.

It is a tricky decision to make that unfortunately requires research on every purchase, which most won’t do.

@COWG

You’re as cynical as I am, which is difficult, but your humour far exceeds mine!

LoL again.

Spot on. Twenty something family friend with college degree is a waitress and so is her 30 year old husband who also has a degree.

Inflation is what they want!

People are fighting for pay increases! They get something and then is all taken away by this conspiracy (Artificial inflation)

Promoted inflation is nothing more than promoted THEFT….one group benefits, one is harmed.

When free unfettered markets are allowed to operate, imbalances will be balanced.

Yet, when central bankers, ie the Fed, has their FOOT on the scale of interest rates, an intentional decision to aid one group at the expense of another is DECIDED by powerful unelected people. How is this fair or right?

So, who benefits from the Fed policies regarding fake low rates (5% below inflation) and who directs the Fed to buy $40 Billion a month in MBSs….essentially lending created money to a real estate market 3% below inflation?

Who manages J Powell’s personal money?

Who is partnered up with the Fed?

Who developed an “emergency” bailout plan for Fed chairman Powell in March 2019 as financial markets appeared on the brink of another meltdown. As “thank you,” Jerome Powell named who to a no-bid role to manage all of the Fed’s corporate bond purchase programs, including bonds where whom itself invests?

Who ran the program and got $75 billion of the $454 billion in taxpayers’ money to eat the losses on its corporate bond purchases, which will include its own ETFs, which the Fed is allowing it to buy…?

Who has a massive investment in residential real estate?

Powell continued to have the same entity manage an estimated $25 million of Powell’s private investments. Records show that in this time Powell held direct phone calls with the CEO of this entity. According to financial disclosure, this firm managed to double the value of Powell’s investments from the year before!

That’s who benefits from an inverted world where water runs uphill, lender is slave to borrower, and Congress spends future generations into oblivion.

“ People are fighting for pay increases”

Um, no, they are not…

Pay increases are usually the result of increases in responsibility…

What you see today is a social reaction meme of $15 an hour…

Who decided that number? Why can’t it be $13 or $18?

What you see today is the result of gov giveaways that haven’t yet run their course and these people feel empowered while flush with cash…

The jobs they don’t want today will look pretty damn good in a little while…

It should have been expected that after the housing bubble crash there would be some type of normal bounce. But what is different is Wall Street has been given cheap money and are part of the reason why houses are going up so fast. Then again, all people have been given an opportunity to get cheap money. Of course, there are other reasons too….Millennials coming to age, pandemic, etc.

But one buyer, who has lots of money, and was not a participant in HB1 is now in this market and they want to win and will be TBTF as normal. From an article. I own a couple rentals free and clear. I have been solicited by calls, text, email, and post cards. I would say over 50 different companies / individual have offered to buy my rentals this year. I get at least 2 text, 2 calls, and 2 post cards a week.

From a recent news article. I guess the good news from this article is if we start to have a housing crash…..there will be plenty of buyers on Wall Street. They love to get assets at pennies on the dollar.

———————————————–