Now it’s new vehicles, restaurants, energy. Game of Whac-A-Mole as some price spikes slow while others begin. But it’s a lot worse than it seems.

By Wolf Richter for WOLF STREET.

The Consumer Price Index (CPI) jumped 0.5% in July from June, after having jumped 0.9% in June, 0.6% in May, for a three-month annualized rate – the three-month momentum – of 8.1%. Year-over-year, CPI jumped 5.4%, same pace as in June, and the fastest since June 2008 (5.6%), all of which had been the fastest since January 1991, according to data released by the Bureau of Labor Statistics today.

The CPI without the volatile food and energy components (“core CPI”) rose by 0.3% for the month and by 4.3% year-over-year.

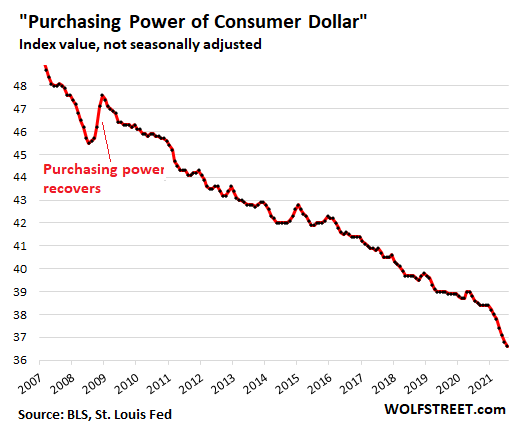

The CPI measures the loss of the purchasing power – well, part of the loss of the purchasing power, as we’ll see in a moment – of the consumer dollar and thereby the purchasing power of labor. In July, this purchasing power dropped another 0.5% for the month, and for the past three months annualized, it dropped by 8.6% – “Honey, where did my big raise go?”

CPI vastly understates one-third of its components: housing cost.

Homeownership costs and rents account for 31% of CPI. These are the largest categories, the most important categories, but they hardly budged despite exploding housing costs and thereby suppressed the CPI.

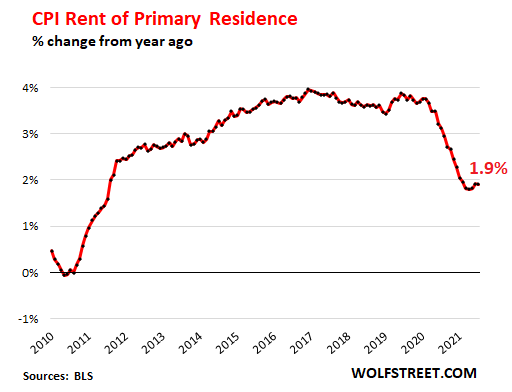

“Rent of primary residence,” which weighs 7.6% in the overall CPI, ticked up just 1.9% year-over-year despite the chaos going on in the rental market, as many cities experienced double-digit rent increases, while others experienced declines. Every month this year, it nudged up 0.2% from the prior month as if nothing had happened. This is the CPI for rent, which has dropped from the 4% range in 2019 to 1.9%:

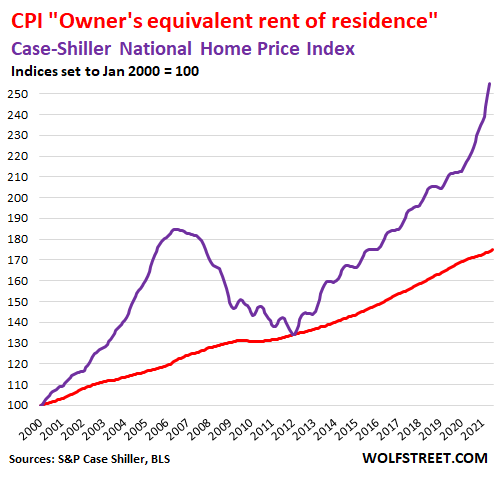

“Owners’ equivalent rent of residences” – the component that tracks the costs of homeownership and weighs 23.6% in the overall CPI – rose just 2.4% year-over-year despite the historic price explosion in the housing market.

The CPI’s homeownership component doesn’t track actual home-price inflation, but it is based on surveys that ask what homeowners think their home might rent for and is therefore a measure of rent as seen by the homeowner.

Meanwhile, back at the ranch, the national median price of existing homes spiked by 23.4% year-over-year, according to the National Association of Realtors.

The Case-Shiller Home Price Index, which tracks the price changes of the same house and is therefore a measure of house price inflation, spiked by 16.6% year-over year, the most in the data going back to 1987 (purple line). And yet, the measure for the costs of homeownership by the BLS barely budged (red line):

Energy costs spiked 23.8% year-over-year.

Energy accounts for 7.2% of the overall CPI. The spike was driven by gasoline, a surprise to no one who has filled up a tank of gas recently, which jumped 41.8% year-over-year. Natural gas jumped 19% year-over-year. The CPI for electricity service to the home rose 4.0% year-over-year.

Durable Goods inflation spiked 14.3% year-over-year, along with June the biggest since at least 1957.

The crazy new and used vehicle prices drove, so to speak, the spike in the CPI for durable goods. Other items in this category are appliances, consumer electronics, furniture, tools, bicycles, sports equipment, etc. The CPI for durable goods spiked by 14.3% year-over-year, after having spiked by 14.6% in June, both of which were the biggest jumps in the data going back to 1957.

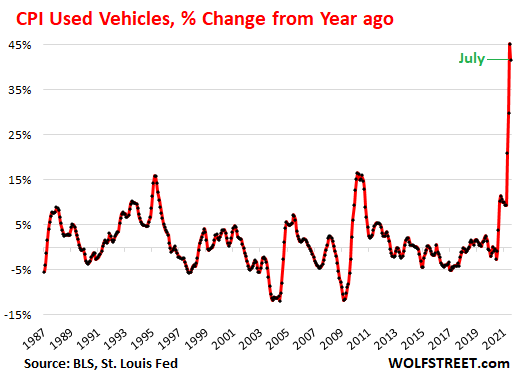

The CPI for used vehicles jumped by 0.8% in July, but given the crazy spike that began last summer, July’s jump was a lot smaller than the jump in July last year. And on a year-over-year basis – due to this base effect – it spiked a tad less than in June, but by a still mind-bending 41.7%. Not much comfort yet for used vehicle shoppers, but price resistance has finally started to crop up and a portion of this crazy price spike is going to unwind:

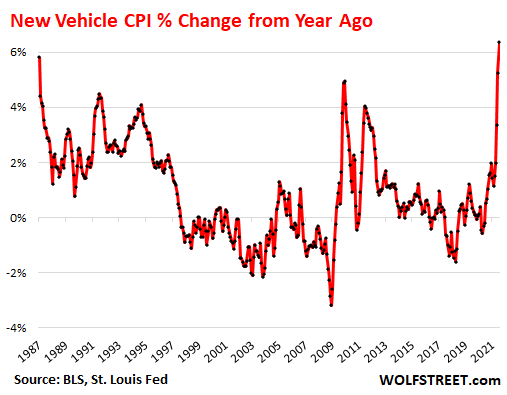

New Vehicle CPI spikes the most since 1982, even as the used vehicle CPI’s spike is slowing. This is the game of inflation Whac-A-Mole, where one price spike here is replaced by another price spike there.

The CPI for new cars and trucks jumped by 1.5% in July, the third month in a row of these types of price spikes, the biggest since the cash-for-clunkers program during the Great Recession. This brought the year-over-year spike to 6.4%, the fastest since January 1982. But as we’ll see in a moment that price spike is understated by “hedonic quality adjustments.”

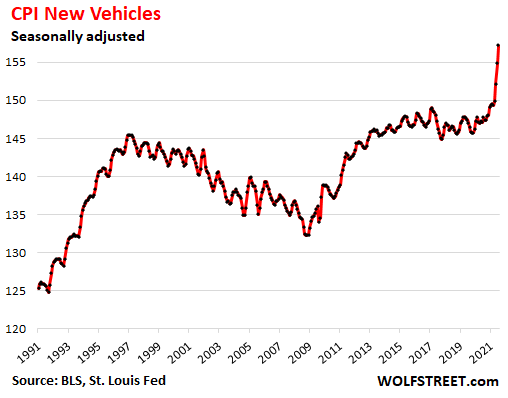

“Hedonic quality adjustments” suppress the CPIs for new & used vehicles. The BLS uses “hedonic quality adjustments” to account for improvements in vehicles over the years. For example, the estimated added costs of the decades-long transition from a four-speed automatic transmission to a 10-speed electronically controlled transmission are removed from the CPI at every step along the way. For an illustration what that means, here is my real-world F-150 and Camry price index compared to this CPI for new vehicles going back to 1989.

In theory, CPI measures price changes of the same item over time; and any improvements change the item, which then boils down to a price increase based on an improvement rather than just the loss of the purchasing power of the dollar. In theory, this makes sense.

In practice, these hedonic quality adjustments have been aggressively applied to push down the CPI, and thereby suppress the appearance of inflation. Under-reporting the loss of the purchasing power of the dollar is a convenient political thing, an effort to keep workers in the dark about the purchasing power of their labor.

The effect can be seen in the new vehicle CPI as an index, which shows that new vehicle prices fell in the years after hedonic quality adjustments took effect, and that in 2019, you could have bought a Camry or an F-150 for the same price as in 2000, which is of course a total farce. It’s only the recent spike that outran the hedonic quality adjustments, but it too will eventually be reeled in by them.

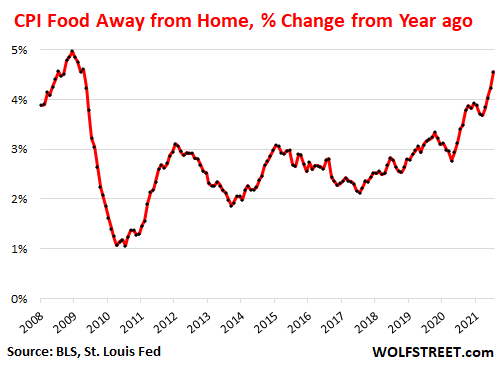

Restaurant prices are next in the inflation Whac-a-Mole.

Everyone who has been eating out or has followed the announcements by the fast-food chains knows that this has been happening, and it is now working itself ever so gradually into the CPI for “Food away from home,” which jumped by 0.8% in July from June, after having jumped 0.7% in June and 0.6% in May. Year-over-year, the index is up 4.6%, the most since 2009. But this is just the beginning.

Restaurants, struggling to hire workers, have increased their wages, and they also face increases in the costs of commodities, ingredients, and services they use, and they face higher operating costs due to the pandemic, and they’ve begun to pass those costs on to consumers:

This loss of purchasing power is “permanent.”

Only a period of deflation – with prices across the board actually dropping – would recuperate the purchasing power of the dollar. But that won’t be allowed. In my lifetime, there were only a few quarters of deflation. The rest of the time, it was either inflation or rampant inflation. And now, after a period of inflation, we’ve got rampant inflation. As the first chart above shows, the loss of purchasing power isn’t “transitory” or “temporary” but rock-solid permanent. What is transitory is the pace of the future losses of purchasing power.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just witnessed the Fed’s purchasing in real time on 8-11-21 11:30AM-12:00 noon CST at my desk.

https://www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation/treasury-securities/treasury-securities-operational-details#current-schedule

Long duration yield just dropped like a hammer. Noticed the corresponding drop on the TBT. I suspect they had to buy to cover the $1 trillion in reverse repos that hit the wire @12:15PM.

Fascinating seeing this happen in real time.

Nah. The Fed does this EVERY DAY as part of QE, as you can tell from the announcement that you linked so helpfully, which shows the purchases of the past 30 days. Have a look at it. It’s the most routine thing there is. This is QE and it’s on automatic pilot

What caused the long-rates to dip by a tiny bit (the 10-year dipped just 3 basis points to 1.33%) was the CPI announcement.

How can you so confidently say that it was due to CPI? I mean, at some level isn’t the bond market just as speculative as the stock market? Then isn’t some level of day to day volatility just expected/”normal”?

OK, maybe not CPI, maybe something else. Maybe someone held his tongue wrong. 3-4 basis points is nothing. Half of those already came back by now.

And it wasn’t the Fed’s buying because those every-day transactions took place several hours before that drop (between 10 am and 10:30 am. EST, and that drop occurred at around 1:30 pm EST

Well, then $2.025 billion in purchases must not move the needle very much at all (to overtly suppress bond yields). You can see a slight dip in yield through that purchasing time period, but nothing to write home about.

I would have expected more of an impact. They must still have plenty of bonds on hand to loan out through the reverse repo system, even at $1 trillion.

The Fed buys $80 billion in Treasuries a month to add to its pile of QE, not including the replacements for the Treasuries that mature. During the 20 or so trading days in a month, it would have to buy $4 billion every day to get to $80 billion a month.

The thing is, this is all scheduled and planned. That’s why it doesn’t have a minute to minute impact. Everyone knows it’s coming. But it has a long-term impact because it removes those bonds from circulation and throws cash into the market.

OK, so the daily amounts the Fed is dealing with don’t really affect the amounts traded daily, only in aggregate. This kind of dashes the whole overt manipulation scenario I’ve been reading about elsewhere, unless there is more being purchased than is being reported. By your best guesstimate, at what point in $ amounts would this be looking like it’s getting away from the Fed? Thanx ahead Wolf.

Hahahahahahaha!!!!! Wouldn’t anyone like to buy a car or house in this great economy I have created???? How about a bridge????? Hahahahahahahahahaha!!!!!!

About the only thing that outpaces inflation is stocks and housing. Wonder why?

For some reason, the “market” collectively thinks stocks are a good inflation hedge. Why, I don’t know, but they do.

Stocks are easy for the elite and politicians to put their funds into. And for the political class, trading on insider information is not illegal.

Didn’t Pelosi say the Fed has put a floor under equities? That makes it all the safer for those with “good” information.

Probably by examining the entrails of sacrificial animals. What else could be as reliable as that in a dysfunctional economy?

I suggest you read Barton Biggs 2008 book called “Wealth War & Wisdom” and learn how various countries in Europe performed financially in the first half of the 20th century. There is nothing like major conflicts to destroy wealth. My guess is that real estate in the Old South did not do well for decades after the Civil War.

During the hyperinflation of the 1922/1923 Weimer Republic stocks were one of the few hedges against inflation. They didn’t quite keep up but they did better than everything else. Read ” When Money Dies” for all the details.

Right, but that assumes that hyperinflation won’t hit public companies’ earnings.

Wait. I thought only public companies can sell stocks?

So if stocks did well during Germany’s hyperinflation, that must mean that public companies’ earnings weren’t hit.

Monkey, I don’t follow.

Total Real Return on German equities from 1900-1949: -60%

Total Real Return on German bonds from 1900-1949: -98%

From “Wealth War and Wisdom” page 314

Anon, what was Gold during that time?

In the US, the price of gold was fixed at $20.67 until 1933 and then at $35 through 1949. It could not have differed elsewhere more than minimally due to Bretton Woods.

Yes, hidden gold at least kept German savings from losing value. Which is where all this is heading at the current time. Cash, stocks, bonds, all depending on banks and other people will crash. Real estate and property? In the southern U.S. during the Great Depression, land was selling for as low as fifty cents per acre.

Probably soon, we’ll all just be looking for a way to hold on to what we have.

“About the only thing that outpaces inflation is stocks and housing. Wonder why?” — Old School

Lumber. The cost of lumber went up double-digit percentages and stayed there. It doesn’t help that there always seems to be a dispute between the American and Canadian government on softwood lumber, with the Americans accusing Canada of subsidizing its production of the wood.

Lumber futures were around 491 today which is way below the 2017 peak around 850.

That was in 2020. I got my dates wrong. there was a big run up in 2017 that culminated at 615 in 2018. My company was buying a lot of lumber in 2017 from my partner’s wife’s lumber yard. Truck loads offloaded with cranes.

In 2017 the price charts looked vertical. It would have cost double to build the same facility starting in 2021.

actually pre-covid lumber was under 500

of course in May 2021 it hit exponential peak(were all contractors basically shut down)

of 1700

now at 500 again – only $4.95 for 2×4 at homeless depot

big corps sopping up all stimi $$ as fast as they can and giving it to ultra .1%

Lumber, plywood and OSB prices, all have collapsed. Lumber off 75% from the peak.

The carnage has yet to be revealed.

Is the growth in stocks outpacing the growth of the Fed balance sheet since QE started in 2008?

It’s interesting that stocks are hanging in there with inflation at 6%. That’s out of the sweet spot of high valuations bell curve of 1% – 3% inflation. Might just take time for profit margins to get impacted.

How about space *under* the bridge? Prime space, getting a bit crowded under there.

Buying a bridge to nowhere.

Wouldn’t it but funny if this was really Jerome Powell?

Buy now… linear extrapolation of the last year in Wolf’s graph shows the dollar losing all purchasing power in 15-20 years!

Many people would easily mistake you for the real Jerome.

J-Pow!!!, I certainly see a lot of inflation in your posts. Each one takes more exclamation points, question marks, and repetitions of the word “ha” than the ones before.

We are definitely going down for a while. Most Americans will be poorer for some years to come. However, I do find hope in that I believe US politicians are finally seeing the economic juggernaut that has crushed our manufacturers for what it is.

The infrastructure bill that is passing to repair our dilapidated infrastructure is also going to put real pressure on our tires to get this economy moving. If the US manufacturers were to me out from the CCP now, before the CCP can confiscate their assets as will happen later if they remain, then the US can rebuild supply chains in any number of countries and bring the high value manufacturing to automated factories in nearby Mexico or some, lower income states in the US.

No question; the US is currently in dire straights. However, Mr. Peter Zeihan has correctly pointed to its remarkable advantages and blessings from geography. I will add another one: there is a gigantic amount of capital of trillionaires which has not been taxed for decades. We can search for and tax the US trillionaires’ concealed wealth and with it, readily pay all our bills.

For the next ten to twenty years, if the US does not forget what happened in the prior decades, the US may thus advance and avoid the fate of countries like Japan. After that, it depends on whether certain trends that will become increasingly obvious as time progresses continue. If we allow them to continue, truly “apres moi, le deluge.”

K

I’ve been saying here for ages that Mr T banned Huawei because they were about to beat Apple in phone sales.

His plan worked against Huawei who got hammered, and licked their wounds by developing their own OS. However, today Xiaomi announced that they were now ahead of Apple and second only to Samsung, who they confidently expected to overtake within three years.

W mentioned Wack-a-Mole, seems like that might be needed for Chinese companies going forward.

I’ve had a Xiaomi Mi Max 3 for about three years. Bought on Ebay, shipped from Chiner. Best phone I ever had, not counting the google on it.

Netflix and Hulu disabled their apps on my Xiaomi after I used them previously on the same phone. So, I cancelled them. Their garbage programming is all woke nonsense anyway.

Said something to me that these apps hate my phone for where it was born. Kinda like phone racism.

It really does not make sense for a large cell phone company to make their own OS.

Why anyone outside of China would buy a Chinese Cell phone with a Chinese OS would beyond my comprehension.

cheap….yes.

full of spyware….yes

I don’t trust Google / Android anymore.

Apple may be the only company that is making some type of attempt at protecting your data.

r

I guess it allows them to compete with the App Store as well as with the actual phone itself. For customers, a choice of 3 can only be better than a choice of 2 surely.

Re spying Edward Snowden??

Well not anymore. Apple now wants to get all your pictures. I am done with them.

Also for a company that supposedly cares about privacy, they didn’t have a problem making Google their primary search engine for 8 billion dollars a year.

@ru82

Dont trust most big tech. Don’t kid yourself, your choice to use their products are intended to benefit them, not you. Its messed up and wrong on so many levels.

If interest rates normalize there will not be much billionaires wealth to confiscate. It’s value without Fed Zirp policy is on about 25% of current market price and that’s not enough to pay off government obligations.

How do you propose to tax what is actually mostly fake wealth from a bubble and use this fake wealth to pay for anything in the real economy at the scale you are implying?

It’s another progressive fantasy dream and it’s never going to happen, even if politics permits it.

Right, as I’ve said here many times, that’s the problem with marginal valuation. The fact that you can get someone to pay $1,000 for one share of Company X doesn’t mean you can sell all billion shares for $1 trillion total.

Bubble “wealth” can evaporate very quickly.

That’s why certain billionaires are currently buying up farmland, timberland, mineral rights, etc. They know what’s coming and are positioning themselves for it.

When the big crash comes, guess who will still be in control no matter what stocks do?

Brutal repression will continue until morale improves

It’s nothing personal.

Market must like the inflation data today, another 200pts up, record after record…this good time ain’t gonna stop anytime soon apparently…insanity anyway you slice and dice it.

Speaking of used cars, the Porsche dealership west of Minneapolis now has a very nice selection of “previously owned” 911s, and that’s a noticeable change in the last few weeks.

The 911s will probably do fine. But this raises are larger point: dealers are buying vehicles at immensely inflated wholesale prices.

If retail prices begin to sag as price as resistance is setting in, the longer dealers hold on to their overpriced vehicles, hoping to find a buyer that will get them out at a better price, the more money they’ll lose on them. Most dealers know that, and they will try to shed those overpriced units ASAP at a loss if they have to, because that will be a lot cheaper than waiting.

Looks like the Jimmy Carter inflation days are on track to be supplanted by Joe Biden et al…..With my Democrat father convinced the party of Roosevelt “watches out for the little guy.”

JJohn-seem to remember Gerry Ford rolling out the ‘WIN’ buttons…in a period of STAGflation…

may we all find a better day.

Met a guy today at a body shop. He sells used cars. He was having a couple of tiny blemishes fixed on a beautiful black 2016 Mercedes S class. He said he had a buyer for the car before he purchased it. He gave $82,000. I don’t know what he was flipping it for. He said new ones list for $120,000. Unbelievable.

Okay Jerome, that’s enough.

No! The QE will continue until morale improves!

RE has definitely gone up 23% or thereabouts in my neck of the woods. Lumber hasn’t gone done much yet.

8 ft 2×4 $9.92

8 ft 2×6 $14.80

3/8ths ply $55.95

3/4 ply $94.95

And yes, this is from the least expensive lumber yard in my area. They are also requiring expensive PITA mounded septic systems with annual inspections in a lot of places to replace any failing septics already there. I wonder how long they will last..

Prices are stores are sticky.

Usually they don’t drop prices…they just leave the price the same and say it is on sale. ;)

The price of raw coffee dropped YOY from $3 to $1 from 2011 to about 2018. 60% drop but Starbucks never dropped their price of a cup of coffee during these 7 years?

2x4x8’s peaked over $10 near me. Now back below $4. Give it time.

The lumber futures chart is astounding on a monthly bar chart.

Home Depot in my area has 2×4 for about 5.5. But they are as twisty as a pile of snakes. The 3/4 sanded ply I bought had dropped from aprox 90 a sheet to 60. But it was about 25 percent lighter and not near as nice as the sheet I bought a few months ago

The Media assures you the emperor is not losing clothing any faster than they ever have! In fact! you will see that by next year the emperor will lose less clothing next year then they lost this year!

Which is all true… since the emperor has been clothing themselves with QE to artificially keep bond prices, Gold & Silver from exposing the true level of inflation since at least 2008.

However, this ruse has been going on for much longer… Since the Fed can replace items in their ‘basket of goods’ with a *like* item, the Fed has been able to continue the illusion that US inflation has historically been half that of the rest of the world… According to them.

While Wolf and others can show the US most certainly has not and will not be immune to the consequences of borrowing your way out of a crisis… and then cutting taxes on your top tax base contributors… Rather than making them pay for the bailouts that lined their pockets the most.

.

Inflation numbers are only half the story.

How much has GDP — economic activity — increased?

For example, ten percent inflation sounds bad.

But what if it is accompanied by ten percent inflation adjusted GDP growth?

Then it would be brilliant!

I think the goal here is to get the economy pumping, so expected inflation is only part of the story.

.

Doesn’t government spending add to GDP? They can make GDP rise rapidly by just spending more and more borrowed and printed money. Let’s hope that is real economic growth.

See bridge to nowhere.

That goosed GDP too…but was a waste of resources.

GDP measures *activity*…even if is stupid, wasteful, counterproductive activity.

See most wars, many/most gvt programs, etc.

Compare the government deficit since 2008 to prior years. Now look at GDP “growth”. You’ll quickly see that almost all or even more of supposed “growth” is predominantly increased government deficits.

Exactly. It only makes sense to count government spending toward GDP if you assume that such spending doesn’t crowd out private investment. Obviously, it does.

Yes, but the added debt and interest cost on the debt are not subtracted from GDP. Agreed interest cost are very low currently and inflation slowly washes away debt. That said the whole concept of GDP is bogus, we live in a limited world and GDP does not factor in a whole host of negative factors that are also real costs.

As an example take all the forest fires. Fire fighting wages, purchases of equipment, food, supplies for fire fighters adds to GDP. Loss of valuable forest, lumber, wildlife, erosion of soil, damage to watershed, loss of town’s burned down, air quality issues, loss of income and tax receipts from timber and lost towns, cost of people displaced in money and humanity.

GDP is an artificial construct to convince a populous who has almost no understanding of real economics that the country is moving forward and everything is improving as long as GDP is positive, irregardless of reality. Who does the calculation and publication of GDP really benefit?

10% inflation brings 10% nominal GDP growth to zero growth :-]

.

Ahem ….

I said “inflation adjusted GDP growth”.

If we get ten percent real inflation adjusted growth with ten percent inflation that is a truly wonderful thing.

.

Yeah, But when it takes 5 dollars of government deficit to get 1 dollar in economic growth.

Unicorns and rainbows are wonderful things too .l

Truly wonderful but truly very unlikely.

Avraam Jack Dectis,

Yes, you sure did, apologies, got caught speed-reading again :-]

.

Thanks Wolf, I hope my reply did not sound mean.

As above, there is skepticism that government policies can produce healthy growth.

If you look at the historical figures, especially in world war 2 and the sixties, we had incredible growth.

Incredible economic growth makes the country stronger and raising almost all living standards.

We should be informed by history.

.

Wolfe I like your podcast

I wish you would do more episodes

But more importantly they pumped at least 6 trillion into the economic system.

It doesn’t seem that the average American is benefiting at all from this exorbitant amount of money.

I may be naive but where the hell is all this money going?

And I don’t mean just this large dump but previous dumps from 2008 on never seems to reach the hands of what could actually make in an economy operate with any semblance of sanity.

I’ve tried to answer this question countless the times with a lot of research and still don’t come up with anything that makes sense to me.

I admire you a great deal and you are definitely one of the people I spend my time and energy listening to or shall I say reading articles you create

Your time is greatly appreciated thank you

Costs big money to go to Mars haha

Listened to Stockman again. He said real damage to economy was less than a trillion. Obvious it was a crisis government could take advantage of and pump 6X government influence into the economy. They are trying to FDR the US and change it forever.

And may I also add that I know it’s far more than 6 trillion.

But this is the figure that is bantied about is being the actual expenditure

How about that volatility in the longer term maturity UST bonds at the 10 year and 30 year??

I came across an almighty buck which had tried to hang itself, but having fallen so far as of late was unable to complete the task. I called the suicide prevention hotline, and they’d already been inundated with calls of a like nature, said they’d send out a Fed shrink.

We had to call the VA to try to get help collecting a bill from a deadbeat lender who was over 60 days behind making payment to us. We got routed to the suicide hot line.

“I called suicide prevention, and they put me on hold”

— Rodney “I don’t get no respect” Dangerfield

I miss Rodney.

There is an easy fix for high restaurant prices. Cook at home.

If you have to eat away from home, pack a brown bag lunch.

Masked Ghost,

You’re missing the point of eating out: Go to a good restaurant in a big competitive restaurant market, such as San Francisco or New York or Austin or anywhere, and ENJOY! You’re paying for pleasure and experience, not nutrients.

Maybe restaurant prices should, and need to be higher and stay that way. Dining out needs to be toned down, “paying for pleasure and experience, not nutrients” should occur once a week, not 3-4 times a week. People never went out to restaurants even close to this much back in pre-1990. Less, more expensive restaurants is an answer to having better paid employees. And that consists of many chains going away.

Jonzo-from the number of ads i see touting mail-order meals, reckon widespread loss of prep-cooking-cleanup skills associated with the advent of the microwave oven (among many, many other factors) could be at work here. Ease still triumphs over basic home economy at this point, it seems.

may we all find a better day.

To the above post, it doesn’t take rocket science skills to prepare home food, and this is form someone who isn’t very good at it.

It’s a personal choice.

Augustus (hey, another ‘Augie’-my middle moniker). Sorry i hit a nerve, thought we were talking reasonable cost of eating and i’m seeing a lot of expensive marketing pushing expensive ease…

may we all find a better day.

I unplugged the stove in my apt years ago. Never used at all. Civilized man cannot live without a microwave….and they are under $100.

And what’s a dishwasher for, anyway? All my “eating tools” will fit in one small box.

Still nicer to eat at my home…in all ways. Tonight bruschetta with a glass of wine. Tomatoes from the garden. Last night we had a curry.

I don’t like to eat out either. If I can’t cook for some strange reason I will pick up something to go and eat at home.

Took a cooking class at a junior college years ago when me and ex split up. Best thing I ever did! Eat healthy and save mucho money.

I have a difficult time eating out. Anything under 20 bucks is either burger, Mexican or Asian. Once in a rare while. Pack my own work lunches. Coffee outside? Rarely. Geez, can you put any more sugar in a mocha?

Best thing, I wash my hands when I meal prep. Teacher was a big advocate of food hygiene. I always laugh when I see that episode of Jerry Seinfeld “Poppy is a little sloppy!”

Agree totally Wolf and J:

We go out less often than many folks I guess, but when we do, we look for the very best dining option experience we can find.

With excellent food and, ahem, beverages, we expected to pay between $150 to $200 for the two of us, including generous cash tip ”pre covid.”

Have not been out lately due to being in the highest risk category and usually taking at least a couple of hours in the restaurant, including the beverage before and the espresso and best cognac after the food.

We are definitely planning to go asap the current surge passes, as we miss it a ton.

Generally, we do not patronize cheap or ”fast” food places, as we have extensive experience working in restaurants in past lives, including from ”pearl diving” and up to line chef, and know full well how it goes in such places…

As to cooking at home, it turns out to be a serious threat — to one’s waistline at least — to live with a retired chef who still loves to cook, and keeps the fridge full of deliciousities!!!

VintageVNvet,

In your bailiwick, do you have nice restaurants with outside seating? They’re all over San Francisco now. I think if you sit out in the breeze six feet away from the next group of people, you’re in a relatively low risk situation (of course, nothing is zero risk).

Don’t I wish we were in SF these days Wolf!!!

Around here, it’s 90 degrees by 1100,,, and at least 95 in the shade by the time we are ready to eat a meal,,

Remember the days of driving to work at 0600 and seeing the temp on the bank at 85 degrees already!!!

The federal government has a vested interest in camouflaging the true rate of inflation in order to minimize the cost-of-living adjustments on government programs. For example, the Treasury currently pays out $1 trillion in Social Security benefits annually. Every 100 basis point increase in the annual inflation rate (based on YoY average Q3 CPI-W) means an extra $10 billion in Social Security COLA payments. Screwing savers with negative real interest rates and suppressed SS COLAs based on “hedonically quality adjusted” inflation stats are not beyond these people.

“The CPI’s homeownership component doesn’t track actual home-price inflation, but it is based on surveys that ask what homeowners think their home might rent for and is therefore a measure of rent as seen by the homeowner.”

What a dumb way to measure home price inflation. First, rents are lagging home price appreciation by as much as 50%.

Second, as I posted before, any Realtor with a user-id and password and pays for the MLS service, can find out what actual rents are and not rely on what homeowners think.

Maybe they should use survey prices based on a ‘bidding war’ result. It would be more realistic in the current home valuation!

Or just use the final sale price, instead of all of this horseshit smoke and mirrors.

?

The main reason it’s dumb isn’t even that. It’s dumb because very few people ever rent single family houses, either as a landlord or a tenant. So if you asked someone how much their 4 bedroom single family home would rent for, they’d have no idea. Most people would literally be pulling the number from where the sun don’t shine.

Think of it this way. If you ask people how much a gallon of water costs at the supermarket, they’d probably have a pretty good idea. If you asked those same people how much it would cost to fill an empty gallon jug with water from their kitchen faucet, they wouldn’t have a clue.

Because people just pay their water bills at the end of the month. They don’t think of it in terms of gallons, just like people don’t think of their house in terms of “rent.”

Indeed I already told the children that Santa will be bringing far less this year due to inflation. They can write their elected official if they don’t like it.

Replacing science with surveys was a genius move by someone.

If there was an actual fire in the theater would you really want it announced over a loud speaker?

Better to pass the word slowly so your “friends” dont get smashed by the Proles.

Rents are set by wages.

Land prices are set by available credit.

Thus rents increase far, far less than prices.

Cutting rates multiplies available credit by cutting the cost of carry.

In a better time, prices, at least for rental properties, were set by the rental income you could expect to get from them, just like stock prices were set by earnings.

Now, as you point out, both are set by the availability of credit.

Garn with it!

Not in the saintly part of the TPA bay area…

Rents have tripled or more around here the last 3 or 4 years, and I can guarantee you wages have not gone up anywhere near that for anyone except maybe those on commission selling real estate.

Generally speaking, rents have gone up as much as the ”market” will bear everywhere I have rented in the last 50 years or so.

Consider alone the $50 a month one could rent a decent apt or ”flat” for in SF bay area 50 years ago compared to today’s at least $2500 a month : try getting wages anywhere near the rise to current rents versus the $5 per hour I was getting doing odd jobs and working for contractors then.

$50/$5 == 10 hours work per month,,, today, ???

Americans today are experiencing what most Southern Europeans have been going through since the GFC.

If you’ve got yours, cheers. If not, apologies.

Southern Europeans have been going financial issues since WWI. In 1913, 4 Italian Lira was the equivalent of $1 US. By about 1957, the exchange rate had gone to 600 Lira to the $US. 600 Lira was the price of an air mail stamp to send a letter to North America. In 1990, the exchange rate was about 1100 Lira to the dollar. At the time of the adoption of the Euro, the exchange rate was 1639 Lira to the US dollar. In 1913, a birthday gift of 100 Lira would have been considered very generous ($25US). In 2002, it was worth less than 1 American dime.

That may be part of the story A, but there is another side:

A ”clothes horse” older cousin loved Italian clothes and bought the best suit he could find in Rome in 1950 for about $50. Same, best suit in Rome in 2005 was $8,000.

Hats were similar price deltas according to him.

All way out of my price range, that’s far shore!

If the world decides it wants out of the dollar, what are they going to buy with it? One of the obvious and easy things is US stocks. For that reason, it seems to me that the market could continue to boom even (especially?) under a poor economic scenario that involves continued devaluation and increasing poverty. Stocks of US-listed global companies would do particularly well, like what we’re already seeing. Maybe the stock market should be expected to stay high even apart from Fed machinations. Thoughts?

But again, U.S. stocks are supported by the credit bubble. Unless the government continues to hand out money for consumers to spend at the public companies, their earnings will tank. At that point, the only way stocks say where they are is further multiple expansion. It’s already at 45. Will it go to 100? 200?

U;S; stocks are supported buy the FED and elected officials who can make stock trades using insider information without legal problems. I mean it’s right in our face….you can’t miss it.

They’re not REALLY supported by the Fed. People just think the Fed has their back, and it becomes a self fulfilling prophecy.

Most of what the Fed can do is jawboning. It works very well. Until it doesn’t.

Or they could go for raw materials and precious metals. China may do that and ship it back to China. That would inflate the price of raw materials for everyone and USA manufacturers would be no better off in the competition.

Exporting inflation to the USA, puting pressure on the trade deficit.

So where does this put me

My raise was quite significant this year.

But as in previous years there’s something that always eats it up like tinder to the flame.

Healthcare costs as is in insurance takes large chunk out of my paycheck

I’m very healthy with modest use

Yet I pay $292 a month towards the single policy.

And believe me my employer pays the Lion’s share.

I think out of all the years that I’ve watched my paycheck and what it can buy this year in 2021 inflation has been the most exorbitant.

I get bitter because my career stipulates that I am and have been an essential worker.

I make too much to qualify for any help.

And yet I’m living hand to mouth .

I’m not a spendthrift I’m very careful on where my money goes.

I guess the one benefit I have is I bought a house back in 2001 and the neighborhood is still very charming and eclectic..

But if you ask me everything is so fraudulent when it comes to monetary system

The haves and have not seems to increase exponentially every year

The question is, what more would you be looking to do if you made more money? Would you make a career change? Visit beautiful spots in nature? Read? You told us you have good health, a raise, an essential job, and you own your home in a nice and eclectic area. Sounds pretty good! I say count them blessings and don’t forget to have fun and take care of your family and friends whenever you can.

I stumbled across Marc J Koeler a tax attorney and CPA who does U tube videos once a week. If you are a wage earner he says have a side gig and then you can start writing off stuff. He has some incredible ideas. He runs a business out of his Health Savings Account. He shows how to get up to $64K into a Roth in one year.

If you are a wage earner only, you are too easy for government to fleece.

If you look at changes in median income and changes in the cost of living, after increased taxes on any income increase, the actual change for the majority is near zero or even negative.

Example: So you got a 6% increase and inflation is (supposedly) 5.5%? Well, my marginal tax rate is 37.5% (federal, state and FICA) which means my pay increase is actually less than 4%.

This is a simplification since many reduce the immediate tax hit with some increase in 401k contributions.

More than 75 years after the end of WWII, German taxpayers are still paying for the mistakes of the Third Reich. But almost all of the survivors of the slave labor camps have died and those still around, with few exceptions, would be in their 90’s. Then there were the older (over 50?) workers of the former East Germany who were simply pensioned off at taxpayers’ expense at the time of reunification.

American taxpayers will be paying for the mistakes of the Bush 43 administration for decades to come via assorted disability benefits paid to wounded veterans of the Middle East wars or survivor benefits paid to their spouses and young children. I think it was irresponsible for Congress not to repeal the 2001 tax cuts once the country went to war and even more irresponsible of them to approve a second round of tax cuts in 2003. So what were the voters thinking in 2004 when they re-elected Bush 43 with an even larger percentage of the votes than he received in 2000?

Anon-“…wartime tax cut…” the best example of the empire’s cognate dissonating, even better than “…guns and butter…”. (TANSTAAFL, in war, especially).

may we all find a better day.

“In my lifetime, there were only a few quarters of deflation.”

This comment sticks with me. Being a prophet of doom is a lonely job with scant compensation. Deflation is rare and brief, but violent. I have seen it twice.

I sense that deflation is just what the short order cooks, aka economics “doctors” working at the fed ordered. And it’s coming right up.

Quick and easy way to remove money (“money” = credit) from the system is for imaginary wealth based on financing to vanish.

And if it happens, catch it while you can.

Let me just comment on your headline.

Obviously the Fed and the government isn’t doing enough to decrease the value of the dollar, after all of this effort and all we have is a constant speed in terms of plunging purchasing power of the dollar.

Screw that noise, what needs to happen in order to accelerate the decline of dollar purchasing power? Obviously the J team is not doing its job right.

More stimulus, more QE, more eviction moratorium, more more more….

?

What is amazing is the way these US sector characteristics and movements and behaviours are being, more or less, mirrored in UK and EU (therefor all the European countries), so far as I can see from here without W’s charts.

Co-incidences are rare in statistics. This has got to raise a suspicion that there is a common tune for all the players in the orchestra, and there must be a maestro conductor. Is it the Fed, or the US Govt or the IMF or the G8 or Davros? . It seems no country can vote it’s way out of the mantras of QE and suppressed interest rates and massive deficit spending.

How can individual sovereignty be maintained in an Orwellian World where savings are at the mercy of rapacious rulers? We’re all in it together on a road to Global serfdom.

Yes who is the master of ceremonies. Somebody ha to be feed the game plan to the biggest players

Breton Woods morphed into fiat only in early 70’s. Since then all central banks must respond to whatever the Fed does. If the Fed devalues, they must eventually follow. It’s been 50 years and looks like it could have 10 years left but you never know for sure. Ten year is still positive, so a little life left in the old hag.

The fed continues to purchase MBS (mortgage backed securities) for Freddie Mac and Fannie Mae. I think the delinquency rate is near 2% for the previous month. I got to thinking and “they are buying MBS”.

Not mortgages – mortgage backed securities.

Was not the entire GFC caused by MBS. What is in these MBS? Was the pessimists query back then. Who rates these things? Those who rated them failed and are still rating them. Like a blind home plate umpire.

Is the fed buying CDO’s as a hedge to these MBS’s? Or is that another “tool” they can use later?

This whole economy is like being a passenger in a sports car your friend stole – it is scary and hilarious – I hope we don’t get caught.

I missed most of the continuing crazy ride and got out a few miles back.

Musical chairs, etc. Our dollars are being abused!

Great reporting as alway Wolf!

I think we’re gonna need a bigger boat

I remember thinking after the Great Recession that, going forward, central bankers would pay more attention to asset price inflation, particularly house price inflation. I couldn’t have been more wrong. Central bankers used to focus on asset prices – most people are aware of the “taking away the punch bowl” speech from the 1950s and even Greenspan referred to “irrational exuberance” during the tech boom. The most recent cycle of QE and interest rate cuts started with Draghi at the ECB and, presumably because other central bankers craved the media adulation he enjoyed, others have followed suit. Asset prices have surged.

Wolf’s observation that “the Case-Shiller Home Price Index, which tracks the price changes of the same house and is therefore a measure of house price inflation, spiked by 16.6% year-over year, the most in the data going back to 1987” is really interesting – and frightening. Asset price bubbles have a habit of bursting and the consequences are severe.

Even if this wasn’t an issue, housing affordability should be acknowledged as a huge social issue. Powell brushes it off as a supply problem, arguing that the supply of housing will increase and prices will normalise. He doesn’t seem to realise that the supply of land where most people want to live is fixed.

I worry about the social problems caused by asset price inflation. It’s widening wealth inequality. Young people and older people who haven’t built a decent asset base are the big losers. The problem is many of these people don’t realise that central bankers are the problem. If they did, there would be more pressure on central banks to act. I really hope this changes.

If young people knew their future wealth was being pulled foreward to fluff the present

Massive debt upon them

And the Fed punishes savers, now at a 5% clip

Punishing savers is unamerican

Yep. The big losers are young people, retirees and people saving for their retirement who are hurt by ultra-low interest rates, and people who live pay cheque to pay cheque. In other words, the big losers are the people who deserve the most support. People who have lots of assets, particularly if they’ve borrowed money to fund the purchases, are enormous beneficiaries. The rich get richer.

I’m telling everyone I know who is my age what’s going on. Hopefully, there’ll be enough political will to cut off the Boomers’ social security when the time comes.

I find it astounding…

that people dont know or care that their current earnings or any earnings in the past they may have saved is being depreciated on purpose by those who exist for the reason of promoting “stable prices”….the Fed.

NEVER have short rates been this far beneath the inflation rate.

People who own real estate and have enough invested in stocks dont seem to care….

and those who do not are left with no hope…..buy record high stock prices with what is left over after expenses?

Borrow big and buy a house that is 25% more than it was 2 years ago?

You can’t save…you go backwards…. WHAT DO YOU DO?

This is all an arrangement, contrary to the history of this nation, conducted by the Fed, an unelected body who answers to no one.

You’re preaching to the choir at this point. If Powell, Brainard and the other sociopaths were to get inoperable tumors, I would have a beer in jubilation.

historicus is right

I just heard that there was a 75 year period staring just after 1900 that stock market didn’t beat inflation. The catch is you got paid nice dividends for 75 years. Today the dividend yield is just above 1% so people are betting it all on cap gains.

There are lots of companies that pay dividends well above 1% of their recent value. See if your brokerage firm offers a data base showing higher yielding stocks. Mine does. After the US stock market crashed in 1929, it took the Dow Jones 25 years to recover to its old high. In that period of time there was the Great Depression and WWII. In early 1942, there was no assurance that the US would even win the war.

The only time dividend yields have been lower on US stocks was at the 2000 peak. But back then, at least other asset classes were a lot more reasonably priced. Additionally, corporate balance sheets have never been weaker in “good times”. Share buy backs since the GFC have gutted corporate balance sheets.

When this bubble finally bursts and it will, stock prices will crash, earnings will follow, and then dividends will be cut massively but even more than 2008. Despite the absurdly low div yields, many payout ratios aren’t that low or even if so, won’t be low once earnings (and cash flow) take a huge hit.

To my knowledge, there might be one US company (J&J) with a AAA rated balance sheet, and that’s under the very liberal standards of the rating agencies.

Any supposed strength in corporate balance sheets is due to artificially low interest rates and the fake economy.

Faced with asset deflation in March 2020, the Fed devalued the dollar. This has been a great deal for asset holders — SPX is up 100% since March 2020, while real inflation is up 10%.

America’s oligarchy has its act together.

While the Fed definitely started the process, the fact is, it’s more about people’s CONFIDENCE in the Fed than the printing itself. Asset prices are up like $40 trillion I read (in the U.S.), while the Fed only printed $4 trillion.

Yep. First page in my finance book. For every real asset there is a corresponding financial asset. My book is old enough not to contemplate that there would be a world that financial assets are 6 times larger than the real assets.

We sure have plenty of inflation. I guess the only options are to buy housing and stocks to hedge against inflation and then sit back and enjoy your wealth creation.

If your a gambler….do cryptos. ;)

What else can one do?

In my opinion the time to buy stocks and housing was 2009 and 2010. In my opinion the thing to do now is to try to keep the wealth that you have.

Short term treasuries, cash and gold are good places to put new money in my opinion. If you bought stocks or a house in 2009 or shortly after you don’t have to do anything. You locked in a good investment and don’t have to sell anything.

Always enjoy reading your articles.

I’ve see you mention the Case Shiller index as proof that actual inflation is a lot higher in view that CPI uses what homeowners think their house would rent for. I think that’s true and I agree completely.

But, in past years, the CPI has been calculated the same way (i.e. not using the Case Shiller Index). So, from a historical context, when comparing today with the past, we’re looking at apples and apples, are we not? Or Am I missing something?

Thanks.

Housing costs in CPI were calculated differently, but that was a long time ago, well before the year 2000. My chart of the CPI v. Case-Shiller starts in 2000.

In terms of the changes in how the CPI was calculated overall, there were millions of those changes over the decades, including the hedonic quality adjustments which were introduced in the 1990s.

CPI — and any inflation measure — has always been a political tool, as each generation of politicians comes up with new and more innovative ways to suppress the CPI and understate actual inflation.

“Right now, our experts believe that – the major independent forecasters agree as well – that these bottlenecks and price spikes will reduce as our economy continues to heal,” Mr Biden said. “While today’s consumer price report points in that direction, we will keep a careful eye on inflation each month, and trust the Fed to take appropriate action if and when it’s needed.”

Is this a veiled warning “Stop printing, or else” or is it a “I trust the Fed to claim they care about inflation, nudge nudge?”

I wonder who the experts are…

I love it when our “leaders” bandy about those words. Our experts, professionals in this field, leading people, and so on. It’s like I could come here and say: “experts have decided that everyone here shall donate half of their life savings to MCH so that the world will be a happier place.” Or “experts all agree that every poster here sending MCH a single bitcoin would help to improve income equality.”

EXPERTS, and if you dare question who the EXPERTS are or their credentials, you shall be branded as a spreader of misinformation and lies and be promptly deplatformed, demonetized and otherwise socially ostracized.

So everyone commenting here, please pay up, I’ll add the link to my public wallet below. Cause the EXPERTS said so.

:P

The dollar Purchasing Power Yes exactly Good post

Seems like the Fed wants and created the Inflation and I see them doing nothing to stop it. The Masses of the Population now Have the current cost’s associated . Are you ready for $5 / $6 / $7 / $8 Gas

costs if your not with a EV . Across the board Costs are rising sort of Humm you just pay more because the dollar is worth less . An adjustment ? come on its Inflation plane and simple

So ? what’s it going to take to get Interest rate’s the back on track like to 5% as clearly the Inflation Plan is not working , How are retired people going to pay their Tax’s in spite of planning for it years ago now derailed with the current Inflation

Old people who thought they were being prudent by keeping their savings in CDs will have to liquidate their savings over time to pay their property taxes. If their income is from Social Security and from CDs paying almost no interest, they won’t have to worry about paying income taxes or Medicare premium surcharges. They may even have to take in tenants to help with their expenses or move into smaller accommodations.

There are good reasons not to include house prices in the CPI methodology. However, this does not preclude central bankers from looking at this data. Their refusal to do so – or at least reference this data – is baffling. It’s almost like they only have the intellectual capacity to look at one set of numbers.

Central bankers myopic focus on CPI data will go down as the biggest ever failure in the history of central banking. History will not rate Draghi, Powell et al favourably.

If you get a chance catch some of Larry Lindsey’s videos where talks about the Fed. He worked at the Fed for about 5 years in a high up position. He says gold is too rigid for optimum economic performance, but the Fed is too undisciplined and so they have gotten us in a mess.

He also says Fed hates gold because it’s a competitor to fiat money, but they tolerate it since Gerald Ford made it legal to own. I have fond memories of Ford vetoing everything Congress passed and telling NYC to fix their own mess.

Ford was not a bad President looking back. His famous quote:

“NYC drop dead”

The government has a vested interest in understating the inflation rates. While paying lip service to fighting inflation the Feds secretly hope for higher inflation. This is the only politically acceptable way to cope with all the new debt.

At this point it seems only an extraordinarily over priced, over valued stock market is the only hedge. Precious metals haven’t moved or gone down the last year.