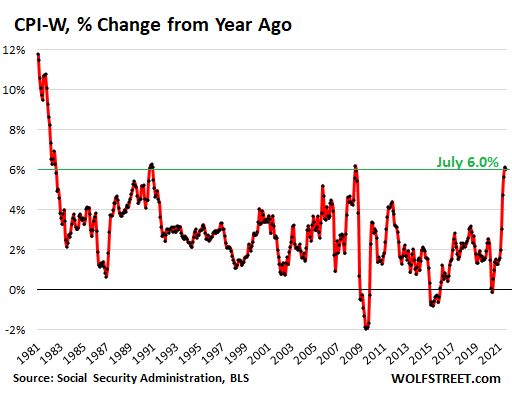

It’s based on CPI-W for the third quarter. July came in at 6.0%.

By Wolf Richter for WOLF STREET.

One of the inflation measures released today, in addition to the regular Consumer Price Index data, was the CPI-W which is used to figure the Cost of Living Adjustment (COLA) for Social Security benefits.

The COLA is based on the average percentage increase of CPI-W in the third quarter compared to the same period in the prior year. So today’s report for July, figured by the Bureau of Labor Statistics and released by the Social Security Administration, covers the first month of the three months that will determine the Social Security COLA applied to benefits paid in the year starting in January 2022.

The CPI-W for July jumped by 6.0% year-over-year, following the June increase of 6.1%. Both were the biggest since July 2008 (6.2%). All three of them were the biggest since November 1990 (6.3%).

In contrast to the increase in the CPI-W of 6.0% for July and 6.1% for June, the regular CPI (the CPI-U), rose 5.4% for both months.

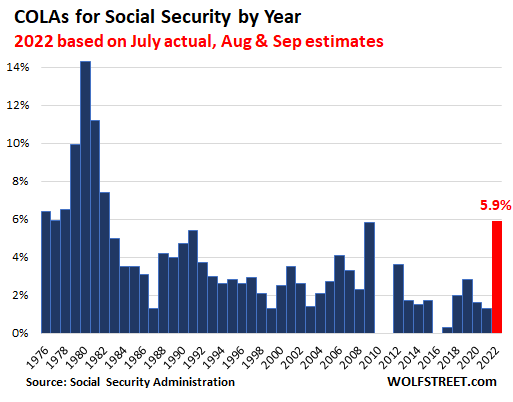

The average year-over-year increase of July, August, and September will determine the COLA applied to Social Security benefits paid in 2022.

For example, if the CPI-W for August rises 5.9% and for September 5.8%, the average year-over-year increase in Q3 would be 5.9%, and the COLA for 2022 would also be 5.9%.

Using these estimates for August and September, it would produce the highest Social Security COLA since 1982 (7.4%). In recent memory, the highest COLA was 5.8% in 2009. The September value of CPI-W, to be released in about two months, will allow us to predict with some accuracy the COLA for 2022.

A COLA of around 6% might sound exciting, but given the extent to which prices are rising, 6% might not even get close to making up for actual cost increases, depending on the personal situation of the beneficiary.

If you get hit with a 10% rent increase, and the price of gasoline jumps another 30%, and the stuff you buy at the supermarket is up 8%, then the COLA won’t be nearly enough. In other situations, you might fare better.

But given how suppressed housing costs and new and used vehicle costs and other costs are in the regular CPI (which I discuss here), these COLAs over time will not compensate for the actual increases in the costs of maintaining the current standard of living. This is why it’s super important to have a nest egg with at least some assets to supplement Social Security.

And having a fun and exciting gig for as long as possible that generates income is a huge benefit – for all kinds of reasons, not just money, or maybe least of all money. I mean, look at all the old politicians: They’re having a total blast. They get to be on TV, give speeches, and play beach volleyball with trillions of dollars, and get paid to do it. Way to go!

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My mom is on social security and a few other incomes, but if she were on just social security she’d be screwed and would be living in an extra room at our place. Inflation numbers fact and fiction (stuff the govt publishes) are way higher than any COLA number. Anyone taking a stroll through a supermarket is deciding beef, pork, chicken, or cat food. You’re gonna start seeing tons of old people fill the carts with dog and cat food again just like back in the late 70’s and early 80’s.

Actually, you’re going to see a lot of older people moving in with their kids, or even grandkids. It’s going to create a huge Sandwich Generation where three generations are living in the same household. Other countries have a lot more experience with this than we do in the U.S. It’s going to be interesting…

Ground report from San Diego. Most of the Single Family homes in San Diego are multi generational. A 2 car garage home would have 5 or 6 cars.

I saw $1,000,000 new construction in Bonita. The homepage had minority stock photography of three generations front and center. And it was actually in Spring Valley.

Whatever it takes, I guess. I’m never going back to San Diego except to visit. It’s just no way to live any more, unless you’re an attorney or surgeon married to another attorney or surgeon.

If you have someone to move in with. Some of us don’t.

And unfortunately, those are the people that are going to be hit the hardest by this inflation spiral that the Fed was so eager to create. But make no mistake…the generation(s) that are in the middle of that “sandwich” are going to feel the pressure of inflation from both ends. Some people can be cavalier about inflation all they want…but it is NOT a good thing.

It is a very unkind band-aid. They’re literally throwing the bottom 50% under the bus. Those folks won’t realize it until the free money stops, but it will. And I hope they learn to bite the hand that “fed” them.

Get a roommate

Or move to Detroit. A lot of the homes are still cheaper than a used Hyundai.

Not a lot of great choices these days.

“If you have someone to move in with. Some of us don’t.”

The “A woman needs a man like a fish needs a bicycle” crowd, with no mate, no children and probably alienated extended family is in for a difficult old age.

“Sensitive artistic woman, seeking emergency shelter, free spirit, seeks inexpensive rental in exchange for dog walking, errands, life coaching, massage or other things. Have a cat named______.”

Meanwhile the extended families living together will save on everything with one rent, or one property tax bill, one utility bill, large inexpensive meal preparation and built in security and babysitters.

do what ron said. get a roommate or two.

We are all in for the distraction of us all . This is going to be bad on us. Help us god.

I saw this back in FL during the GFC. The last place we lived, almost the entire block was multi-generational, minus 2 houses out of about 20. We had our millennial with us and still do, most families had married children and grand kids living with them too.

It would be interesting to see a comparison of satellite photos showing an increase in cars parked on the street over the last and next couple of years, especially in HCOL areas with low disposable household incomes like most of SoCal.

Like those fantastic charts showing COVID Delta transmissibility over the last several weeks. Or a better comparison may be night time satellite photos of North Korea and South Korea.

Test: If somebody says “You commie”, does the comment hit moderation?

Of course, as you saw :-]

FYI grandparents and young children are a great combination, IMHO. The grandkids keep their elders young, and the elders keep the grandkids out of trouble. Wisdom and creativity can flow in both directions.

Wolf, I can see you have all bases covered. :)

Why is this weird to merikants?

It should be normal for generations of a family to live together.

multi-generational is a good step, but what we will really need is multi-clan multi-generational. How many multi-generational clans can you fit in a single family home?

Open floor plan will be a liability. Rooms will be cut out with plywood, cardboard, curtains whatever. Non-permitted kitchens and bathrooms added all over. And an engine crane in every driveway.

Sound absurd? I’ve already seen it in the USA in many single family home neighborhoods in San Bernardino County in the 1990’s.

Coming soon to your Single family home neighborhood.

At least lumbar prices have plummeted, so they can afford to build on that extension.

My back never went up in price………….

Good time to get real friendly with a local contractor who specializes in mother-in-law suite additions.

Every house that I’ve built for myself has had a guest house, carriage house, or accessory dwelling. My current house has a 750 sq.ft. apartment upstairs with a water view. I’m renting the apartment to a semi retired film critic this winter while we’re in Mexico. I’m only charging $1500/month but I’m getting a free house sitter.

When my mother was alive & on a pension ..

The Aged Pension would increase by a few signal digit dollars

& so would every item at the supermarket.

The $2.75 bought you very little ?? + ??

Catfood Grandmas are a thing of the past. Snap!

Homeless Grandmas in a tent with a can opener is 2021!

Has anyone actually priced pet food, lately? (Good-quality dry cat food qualifies as emergency disaster rations, though…).

may we all find a better day.

my dry catfood? $85 for 17lbs. but i have a special cat that needs his special food. the stuff i feed the strays is more like $15 for 30lbs.

but you’re right, quality food for cats & dogs ain’t cheap.

> You’re gonna start seeing tons of old people fill the carts with dog and cat food again just like back in the late 70’s and early 80’s.

Longevity in the US was between 70 and 73 back then, instead of the current 78.

It doesn’t seem as much, but a nest egg able to finance just from 65 to 70 or 73… is a lot smaller than the necessary nest egg to finance from 65 to 78. It needs to be double as big in real terms and it will be exposed to much more risk.

Americans keep on glorifying longevity, all it will do is force more people into poverty into their later years and Alzheimer’s/dementia. Going for quality instead of quantity is the way forward imho.

Back in 1982, I went to a company offsite meeting held at a hotel in Reno. I was amazed to see so many seniors gambling their Social Security money away at the slot machines.

It’s still a ongoing event with seniors. Some casinos even have penny slots.

Cigarette smoking, oxygen tank strapped on old man in wheelchair with little American flag worshipping at a slot machine in Vegas. That’s a horror show.

Just got back from Costco. New York Sirloin was a shocking $15.99 a pound. Last winter it was $8.99. Didn’t buy.. instead substituted pork lion $2.49/pound. They had beef tenderloin at $32.99. Have never seen prices like this I will miss a nice steak on the grill. Somehow I am not buying Powell statements on transitory inflation.

Last year the pork loin was $1.49 on sale.

Apparently Bob has not strolled down the cat food aisle lately. That stuff is not cheap. Not only are prices going up, but packages are getting smaller (notice how cereal boxes are harder to stand up-the boxes keep getting narrower-before long they may start using envelopes). I also noticed another inflation trick. Red leaf lettuce is no longer sold by the pound. Instead of $1.69 per lb it is now $1.69 per head, which is only about 12 ounces for a big head.

So according to this article, the COLA for SS is based on a annualized from a three month period and not 12 months? I understand it would be a 3 month period x 4, but boy, if they could shave a 0.1% off of that three month period, think how much money they could move from SS payments to their favorite pork barrel projects.

“So according to this article, the COLA for SS is based on a annualized from a three month period and not 12 months?”

No. It’s based on the 3-month Q3 2021 average compared to the 3-month Q3 2020 average. So this year-over-year inflation, not annualized, but using three-month averages at both ends.

Might that explain the smash down of commodities in the futures markets?

As mentioned in the header of Wolf’s article, it’s based on the CPI-W for the 3rd Qtr of each year. July is in the books at 6.0%. Wait for August and September’s numbers, sum the three values, divide by three and you’ll have a fairly close approximation if the 2022 SSA benefits increase.

Typically, our benevolent government gives the COLA to SS recipients with one hand, then raises Medicare premiums to gobble back a portion of this. Meanwhile, those walking across the southern border are being well taken care of for free, compliments of those of us who work to support ourselves and all the foreign and domestic leeches.

I guarantee you don’t know any illegals. They do every job that worthless US citizens refuse to do. The entire economy would grind to a halt without them. They pay taxes and get nothing in return.

Those coming across the border will be doing the jobs young americans refuse to do,because most of them are just the loosers.

“young americans refuse to do,because most of them are just the loosers.”

Isn’t that said by the oldsters about every new generation?

“Those coming across the border will be doing the jobs young americans refuse to do…”

What is the pay of those jobs compared to living expenses?

People who crap on millennials always forget the economic conditions they have been “gifted” with.

Foreign and domestic leeches ? They are hard working people and deserve our respect. The only leeches I know about are the giant multi national corporations and ruling class criminals who are tax evaders. Spare me the “ but it’s legal “ BS. The real problem begins and ends with their corporate lobbyists masquerading as representatives in Washington DC and every state capitol.

Son owns concrete business Hispanics work hard 25$ a hour buying houses some save to go back home our high tech economy created this government needs to get out of the way

You can qualify for Medicaid and get free care as well if your income is low enough.

“They are hard working people and deserve our respect. ”

Yes, they are hard working people, but no they don’t deserve any respect.

They are breaking the law by entering the USA illegally. They are working illegally and more than likely have fake and illegal documentation as well.

Illegal immigration results in an increased supply of labor to the market.

The illegal immigrants labor provided to the market is targeted at the lowest paid type of work. Those people coming across the border in that manner aren’t lawyers and programmers.

Why do you think that after years and years of illegal immigration being stopped during the Trump administration that wages for low income workers in the USA finally started to increase?

ninja_warrior,

Require that ALL employers, including households, to use E-Verify on everyone they pay, and impose a $1,000 fine per day per worker for violations. And then go enforce it as a revenue source to help lower the deficit. That will solve part of the problem.

Wolf-spot-on, but many protesting here will continue to be shocked, shocked to find gambling in the casino (applies to the illegal drug trade, as well) hall of broken mirrors…

may we all find a better day.

Plus an additional increase in Medicare supplemental plans. Even a 6% increase gets gobbled up quickly. There is never a chance of breaking even with a failing US dollar.

Red Leaf Lettuce .. sprinkle just a few seeds in a Styrofoam box with a bit of soil & water .. pick the outer leave .. it will grow faster that you can eat it.

Should people without much money to spend go with a vegan diet or mostly vegan diet? As I recall much more energy goes into producing meat as compared to grains.

Some Americans are very fit and in excellent health. But an increasing number are in poor health and a record number are obese.

Many do not exercise and many eat a diet that is high in saturated fat, sugars, simple carbohydrates and saturated fats.

Cutting back on junk food, bread , sweets and red meat and increasing vegetables will not only save money , but will save money

“Cutting back on junk food, bread , sweets and red meat and increasing vegetables will not only save money , but will save money”

you might accidentally get a wee bit more healthy in the bargain. while saving money!

Reverse mortgage time, will delay price discovery a bit longer.

Yeah. That reverse mortgage commercial with Selleck is getting more airtime, and is sickeningly long. Almost as sickening as he is and always was. Must be designed for widows with home equity.

There is still money yet to be extracted by the corps, and they WILL extract it, it’s what they were designed for.

Just wait till they get obesity defined as a “disease” so Medicare, Medicaid will have to pay for it. The ACA (and other things) pretty much proved to me, at least, the Dems are in bed with the Medical Industrial Insurance Complex, (we could have had single payer triage like Canada), and the GOP with fossil fuel. I’d love to see a good full breakdown of just who owns who. I met or knew most of whom my lobbyist uncle owned for his corp.

“Elected” Office isn’t quite just up for bid/sale to corps like in the City of London, but with Citizens United, dark money, PACS, etc, they might as well be.

The long and winding road (to being a surf).

serf not surf

Turns out Rand Paul did not secretly invest in the company (Gilead Sciences) that makes remdesivir back in February 2020 after the Congressional briefings on Covid.

His wife did.

oh, that makes it ok then. Thanks for clearing it up Harold

Harrold, (btw, nice subtle and incisive commenting style)

I watched ALL of that ALL GOP dog and pony show, you are sorta referring to. One of the four guys “testifying” was company CEO of one of the 4 or so Covid therapeutics they (and the good doctor Paul) were pushing. I looked it up and it’s a damn worm pill….maybe more were. Guess all these “miracle magic bullets” can somehow be “aimed” at a lot of different diseases?

They also had all kinds of “proof” charts, from the EXACT same “proof” outfit, and it wasn’t the government. Think it was one small drug company’s research, but I forgot. (Been a while since I took notes and researched it all).

Kinda blows my Dem/MIIC notion…oh well. But just like all too many of the rest of us, increasing wealth IS the National Sport….but no limits, no boundaries, and few rules/refs, though…makes for a pretty shitty game, I think. I guess a good “Entrepreneur” can easily become an all-star, though.

If you are retired and short of money, and if you have a decent property in a blue chip city, the reverse mortgage may be the way to go.

In the long term, blue chip property values should keep rising, and the lending limit for federally backed reverse mortgages should keep rising, leaving the retiree with a cash fountain. Recently, the limit was raised to 822K, which is more than a 50K jump in one year.

All that’s required is for boomers to look their grandchildren in the eye as they reach for the free money, and keep voting for a system that will destroy their kid’s kids.

Just like the last 20 years.

> We had no choice

You sure didn’t fight it

Either that or sell it to a contractor who can make 2 or more apartments in the house, and rent from the new landlord for at most .5 of the mortgage you were paying for a set period of years, like till you die. The new experienced contractor/ landlord would have to dump some money back in for all the renovations, permits and possible septic improvements. The house would need to be well constructed to begin with.

A Reverse mort. without the middlemen. Most of the time the mortgage will pay for itself with the size of the house directly proportional to the number of apts..

georgist:

spot on. but in the grandparent’s defense- they might just need the cash to afford the hot $-mas presents for the grandkids what with the shortages expected and supply lines getting fubared.

you always have to think of the children…

Cash Fountain! Har-Har!!! Says the modern alchemist.

Implicit’s notion sounds good, actually surprised it hasn’t started. They did it a lot around here during WW2, and still are with older Mansions.

NIMBY, I guess.

Instead of “Senator from Kentucky” the titles should read “Senator for the Healthcare Industry” etc…

He doesn’t really care WHERE he makes money, just like his old man, who was selling “inside financial tips” for years….maybe he died doing it, don’t really know, don’t really care. Total scumbags…doctors?…..my ass.

WS – I really like that – truth in voting! The Senators from Defense Manufacturing, the Senators from the Major Banks, the Senators from the National Media, &c, &c.

Obesity is already a disease. You get SSI if you have arthritis in the knee and obesity. Obesity and mental problems. Obesity and high blood pressure gets you SSI and Medicare. Get a lawyer and apply. If they turn you down reapply and then reapply again. On the third go around everyone gets it. The lawyer is free he just gets the SS payments that were due so if your case lasts three years he gets the money.

Yeah. Metabolic Syndrome, aka, diabetes 2, and other stuff you mentioned.

I guess maybe the only diff would be selling weight loss drugs, programs, in home exercise machines, whatever. But they ARE working on getting it defined as a disease, so there is still more extraction of $$$s for some corp or PE outfit there.

But I hope you aren’t implying people trash their bodies just to earn a living…what horrible life situation would make someone do that?……you do know what a “food desert” is, right?

The other “no hope at all” action taken would be just shooting drugs…..and maybe get a quick painless death.

Somebody told me the best way to become a millionaire is to buy real estate in California. My thought is that that’s also a good way to end up with social security alone in retirement. I just can’t imagine most $80K households with $4,000 house payments saving much for the future. Enter the reverse mortgage to suck away their “millionaire” status in the Golden Years.

It’s worked for a lot of people. You make the mortgage payment and the equity is half your retirement plan, so you don’t need to save as much elsewhere.

However, future returns in real estate may be much lower since interest rates can no longer go down significantly… But if inflation stays high and rates are held artificially low then housing will do okay, and once you lock in the fixed-rate mortgage you also lock out all the inflation risk from renting.

We have all been trained by 40 years of falling interest rates. What comes next might not look like the past. In fact, when making money takes no brains or effort you know it’s about over.

@OS – touché

Actually the best way to become a Millionaire is to start 40 years ago to live beneath your means and put the difference into an IRA investment in a highly diversified and extremely low expense mutual fund. And continue to keep investing for those 40 years.

When stock prices plummet – and they will – stay invested and keep adding to your portfolio.

When stock prices wildly zoom up – and they will – stay invested and keep adding to your portfolio.

Even on a max 5 figure annual income after 40 years – especially the LAST 40 years ( where the S&P’s CAGR has been over 11% ) – you will have accumulated over $1,000,000.

That’s exactly what I told them! They said all that Boglehead stuff makes them uncomfortable and that tech stocks, crypto and SoCal real estate are their ticket to riches. Don’t fight the fed and all that. We’re both millennials (me one of the “old” ones).

See you at the finish line, anon. :)

People will be eating cat food. Hedonic equivalent of salmon.

Putter…

that is how the PCE index works, the metric that the Fed uses to measure inflation.

Substitute out the things that rise “too much” in price…and replace with a similar but cheaper item (cat food).

hisroricus, never mentioned (yet) by our *leadership* is the fact that a very high percentage of the U.S. population are obese.

Downsizing food packaging, substituting small portion cat and dog food for fatty steaks, and not having extra money to buy fattening foods like cake or ice cream will be a PLUS, and will be advertised as a way to get us citizens and voters back to good health by trimming the waistline.

I suspect the Gov is working on those TV commercials as we speak!

> Substitute out the things that rise “too much” in price…and replace with a similar but cheaper item (cat food).

Indeed, the cost of living in a van is soon going to replace housing.

leanFIRE_Queen,

The price of used vans is up 26% year-over-year:-]

My friend who is an artist and a little bit of an hippie, bought an old Chevy 1 ton van camper with the sleep over the cab. She got it untitled for $2,000. Jumped through all the hoops getting title and tags, new tires, full service done on it and with about $5,000 in it she got her a decent camper. She will eventually flip and make a little money on it. She flips a camper or rv every couple years for a little adventure and pocket money.

Good grief, why are people buying AMC stock when they could be investing in used vans?

I can remember the time when salmon was considered cat food, not human food. It was about the same time people in my neck of the woods didn’t know what pasta was let alone eat it.

Times sure have changes.

Was that like 1880?

Canned salmon has been around since then.

Where is your neck of the woods, anyway?

^^^ Question for RedRaider.

Grits is pasta, Red…..just from a different grain.

Quick – someone explain to me the difference between the “veggie burgers” being pushed and nice vegetarian pet food.

Last time we had inflation like this was 2008. People couldn’t afford the inflation then and I bet the same people and businesses can’t afford it now. Maybe this time is different.

It must’ve lasted 5 minutes because I don’t remember.

This is great news IMO. Our government will be paying out a noticeable increase SS recipients. Better than most annual raises can expect. That the government didn’t yank the chain and show (cook the books) a reduction in payments shocked me.

Nathan, the official numbers are not out yet. It’s possible they will figure a way to short change the SS recipients. Give them time…..

Also realize, a ~5% increase in SS money is still a small number for most recipients since the SS benefit is pretty low in the vast majority of people collecting. And that 5% also has to cover any increase in Medicare premium paid by the SS recipients.

I too think they will find a way to make sure the SS increase is close to zero.

Does anybody remember our current leader’s promises about SS during the campaign. He wanted to boost the lowest SS payments to 125% of the poverty level, about $1070. The idea seems to have fallen off a cliff along with a bunch of other things.

Fed printed money so government can hand out money to nearly everyone. Billionaires got the most through asset inflation. We just keep moving closer to real economy collapsing and plugging the hole with printed money, til the jig is up.

Maybe our *leader* forgot about that promise? Is that possible?

anthony a:

not a chance. the man has kept a job in dc for ~50years. he has to have mind like a steel trap to have held onto that privilege for so long. right?

I wonder what rates are being used for the latest calculation of the solvency for the fund.

Isn’t it suposed to be solvent only until 2033 or so?

Maybe a big increase for Grandma may not be so good after all for you…..

benefit amount and the paycheck ‘contribution’ can, and are, adjustable. SS is a great plan, until the politicians get their grubby greedy hands in to it, and provide for what it isn’t.

Taxman100,

I’ll do my annual update on the fund in early October (after end of fiscal year). The low interest rates are not helpful for sure; they dramatically cut the interest income of the fund.

Also “insolvent” — whenever that would happen — means that the fund’s balance has been used up and that the revenues to the fund are slightly lower than the outlays. the difference is not huge, so it wouldn’t require a big fix.

Here is the SS fund balance through the last fiscal year. At the end of the last fiscal year, the balance was $2.8 trillion, essentially unchanged for four years, so it’s not going “insolvent” anytime soon:

How does that chart compare to the chart of how many times I’ve stuck my foot in my mouth and gotten moderated? I think I’ve leveled off a bit as well.

I was thinking that maybe once a year one of your posts could be about conspiracy theories and you can let us all loose to get it out of our system. I have a bad feeling my chart would end up looking like a global warming hockey stick, though.

Regardless, thank you for running this site. Your knowledge of things and quick access to valid stats is great.

AGREE B,,, but Wolf absolutely MUST insist that all of OUR conspiracy type posts MUST include all the back up data.

That way, WE the Peons can not only get off our ya ya’s,,, but might just have some impact on the clearly similar rediculousnessessess that continue to impeded us on our way to financial independence and all our other wishes,,, as in:

”If wishes were horses, every beggar would ride.”

( One of my mom’s fave replies to us kids begging for stuff back in the 40s and early 50s… )

Many sages have indicated clearly that there is no end to desires,,, as soon as one is satisfied another dozen spring up… and, as such, best idea is to cultivate ”non attachment” and the giving up of any and all ”desires.”

I enjoy a number of commenters input/insight which helps me select which ones to read during lively convo’s. Your prior comments get me to read what you take time to write.

Keep up the good work

it looks like it may have reached a new “permanently high plateau.” but what do i know?

If the SS tax base keeps expanding and the payout in real dollar terms keeps dropping the program can in theory stay solvent for a long time.

With interest rates so low, with payroll numbers being lower, COLA increase of 6%, the tip-off point (outlays > inlays) might get closer this year.

Today, Aug 11,2021, the grocery store tab was $180. Six months ago it was $110-115. By Xmas 2021 I expect the same grocery tab for same items will be over $300…… and these will be the good old days…..

Really makes you start to look at what you are buying. Perhaps the increase will prompt you to look at want vs. need. For sure this environment has adjusted my spending and consumerism contribution to frivolous spending.

Listed my motorcycle as I would like to extract maximum value in this current market as well as cut out the expense. Do not need it at this time

And then they tax your SS money and spent on new guns and planes

Yes, back in the 80’s when SS was ‘fixed’, everyone agreed that rich people making more than $25k/yr should pay taxes.

I live simply and steadily, so food and utilities are predictable.

Real inflation in these basic expenses has been about 8% annually for the last decade. SS has been going up about 2%.

I’m not seeing an unusual jump in this year’s expenses.

A larger SS increase will be nice, but it still won’t make up for the last decade.

Since 2000, Social Security benefits have lost roughly 30% of their purchasing power due to inadequate adjustments that underestimate inflation and rising health care costs, according to the Senior Citizens League.

Currently, Social Security Cost-of-Living (COLA) adjustments are based on the CPI-W index, calculated by the Bureau of Labor Statistics (BLS). This index is based on the expenses of wage-earners, most of whom are young or middle aged. But the expenses of senior citizens are very different from those of wage-earners. Consequently, the COLA adjustments are ridiculously low. Any senior citizen can testify that these increases do not even come close to matching the real increases in the cost of living for seniors.

However, the Bureau of Labor Statistics calculates another Consumer Price Index, the CPI-E. That index specifically tracks the spending of households with people aged 62 and older. But this index is considered “experimental.”

There is a movement in Congress to require that Social Security cost-of-living adjustments be based on the CPI-E instead of the CPI-W. Implementing this change would significantly increase the incomes of seniors to more closely match the real increases in our expenses.

I am a senior living in Florida. On July 21, I wrote my two senators and my representative urging them to support this move. As of August 11, 2021, not one of them had bothered to reply to me.

Ronald W. Kenyon,

Don’t get too excited about basing COLAs on CPI-E. Look at the numbers instead. Here is why, for July year-over-year:

CPI-E: +4.7%

CPI-U (regular CPI): +5.4%

CPI-W (used for COLA): +6.0%.

Great, then base SS COLAs on the highest of the bs inflation measures, plus a certain % to compensate for the fact even the highest one is understated by fudge factors like hedonics. It’s like the ’70s FRAM oil filter commercials….”You can pay me now, or pay me later.”

Doesn’t this still outpace wage growth?

Thank you, Wolf. I am learning. That said, it still seems illogical that the CPI-E would be less than the CPI-U or the CPI-W. But I’m not an economist.

Conclusion: we seniors should shut up and be grateful that we might receive a pitiful COLA of +6% for 2022. Wow!

Still, having served as a congressional aide a couple of decades ago, I find it incomprehensible that neither senator nor my representative in the House has condescended to respond to a letter from a constituent about an important matter. Back in my days on the Hill, I can assure you, we answered every letter from a constituent. If I were younger, I would run against these people who disdain and ignore the patriotic American citizens who put them in office.

Ronald W. Kenyon,

In terms of politicians not responding to you, don’t feel too bad. I wrote to the Trump White House about trade, trying to be helpful because Trump needed help on this topic, and got a form letter back. I live in Pelosi’s district, and she doesn’t even campaign here anymore.

In terms of CPI: Each of these indices has a different basket. I’m guessing (because I don’t have time to look it up) that the weighing of new and used vehicles in CPI-E is lower than in CPI-U and in CPI-W, and healthcare is higher. But this time, it was vehicle prices that jumped, so they pushed up CPI-U and CPI-W more than CPI-E. These things can have a big impact.

The assumption is that a 75-year old is going to spend less money on cars and more money on healthcare.

I compared the 10-year change, and the difference between them was smaller because some of this balances out over time.

I just pointed that out because the process of “inflation adjustment” is based on wild assumptions, and it’s important to understand those assumptions.

I’m very leery of politicians and bureaucrats wanting to change the SS COLA. It usually means that they want to reduce the COLAs. For years, they have been talking about switching to a chain-type index, which are the worst (like PCE). It will ruin retirees. If a switch to a chain-type index moves to the foreground, I’m going to make a mini-ruckus about it here :-]

RWK/Wolf-not to run offtrack, (here i go, anyway), but we have been dealing with a Congressional representation problem baked in by Congress themselves in the interests of ‘efficiency’, i believe, in 1929.

The Constitution specifies a LOWER limit for House District populations of 30,000, but NO upper limit (like many, many planetary realities that have changed since the 1790’s, could the founders have imagined such population growth and attendant mass communications/media reach going forward?). After the House fixed its current numbers (435-6 reps post-Alaska/Hawaii statehood, 1930 Census pop. prox. 123 million) in ’29, the nation’s population has continued to grow to almost triple what it was back then. The effect has been to reduce the power of your vote for House Rep. (your actual link to DC, unless one has adopted the ‘President as elected king’ way of thinking seemingly in vogue with many) mightily (current U.S. pop. prox. 331 million) . Ballooning district populations have made it much easier for a Rep.-no matter their party-to knuckle under to their party’s, and more important, large political donors, agenda and ignore more and more LOCAL issues and concerns (i share your outrage RWK, but not your incomprehension-thank you for even stepping into the box in those years). As the House sets the budget, inhabitants of low-population states have lost more and more say over the Federal purse (one can see the current conundrum of the states that have two senators, but only one Congressperson. Those states brought the issue to the Supreme Court a few years ago, but the Court refused to consider it, kicking it back to Congress…).

Given the current, and not altogether undeserved, low public opinion of Congress (elections ARE term limits, people,) and associated low bars of Congressional financial oversight, my preferred, and admittedly unlikely, way of trying to improve things would be to limit District upper populations to about 50,000 (some now are well in excess of 100,000)-a small enough number that a rep would have to pay very close attention to their district’s population’s specific needs and opinions, plus make political campaigning much more expensive for out-of-district money inputs, and, hopefully, allow reps. to spend more time on district business than they do now fundraising/national media shilling, over the brief two years of their term…

Though begging much more discussion (i’ve taken too much of everyone’s time, here) but i respectfully ask you to think about this as a citizen who sees their ELECTED public servant as that, rather than as a public master. (Moderation, as always, understood, Wolf).

may we all find a better day.

Ronald W. Kenyon

Your letter found its way into the shredder before it was even read.

He’s got crappy senators. I wrote both of our senators here in AZ about how inflationary student loan forgiveness would be and received surprisingly comprehensive replies from both of them…especially Kyrsten Sinema.

I am a proud American citizen and a resident of Florida.

In the 2018 election, Rick Scott (R) [check out HIS background bio!] defeated incumbent Bill Nelson (D) by about 0.2 percentage points.

In the 2016 election, Marco Rubio (R) [check out HIS background bio!] won the election by only 52% of the popular vote.

My representative, Lois Frankel (D), appears to believe that she holds her office by “the divine right of kings,” which exempts her from responding to the people who voted for her. I repeat: If I were younger, I would run against these people who disdain and ignore the patriotic American citizens who put them in office.

I held out applying for Social Security until age 70, so am getting about 10% or so more. It could end up a bad decision, because I could suddenly croak and not have got much out of it (unless my wife green cards and lives in U.S. for six months before I die). Otherwise, I’ll just be a dot added to the actuarial table .

I’ve have had to pay Medicare premiums for 5 years out of pocket – and no coverage here in Thailand. I’m healthy and glad to avoid the medical system. But hey, that’s insurance, it helps someone else.

Lot’s of medical services here in Thailand are cheaper than even an insured person in the United States. My sister took a medical holiday here – the reduced cost of her husband’s hip replacement, compared to the U.S., paid for a nice holiday.

Dental here is also BIG savings if you don’t have dental insurance in the U.S. (for example, implants). Of course there’s hype involved, and they buyer has to beware. Unfortunately coronavirus has pretty much halted to profits of the big medical tourism system here.

Most men delay SS to age 70 to protect their spouse with an increased benefit. Personally, I don’t think it’s a good idea. Assuming your reduced benefit at age 62 was only $1000. You could have banked the money for 8 years and at 70 would have an estate of up to $96K to leave to your wife. That’s a decent amount of money in Thailand.

I read if female was lower wage earner she should take at 62 and husband wait til 70 if he can. That way if he croaks before her she is well protected with a higher check.

If you live your “expected” (actuarial) life span, it makes no difference if you start at 62 or at 70. The amount of money you will receive in total is the same.

I elected to start at 62 :)

That said, if you live longer than “expected” it would be better to start late, and if you lived shorter than “expected” it would be better to start early.

Isn’t the average expected life age used by actuaries to figure the point where it is equal amounts of money for starting at 62.5 or waiting till 70 (i.e if you die at 77-78)?

I know I seem to repeat what you wrote but if the amounts are figured with the same formula for everyone-men and women, you would think the average between 77m an d 81w (just looked it up) would be 79 for everyone in the US. If you live longer than that it would be better to have started at 70. Women should start later not men if that is the case.

Ridiculous! Very FEW men file at such a late age. I do agree with your age 62 assessment.

Retiring at 62, a $1000 benefit would be reduced to about $720 or so (depending on when you were born).

Waiting until 70, a $1000 benefit would be increased to about $1,320.

So the person would get about $600 (60%) more per month than I would be getting he or she I retired at 62.

drift,

I specifically said if the reduced benefit was $1000. I was not referring to the full retirement benefit at full retirement age or increased benefit at 70.

I was also referring to your situation with a wife that was not eligible for the spousal benefit because of age or residency.

Since you were already forgoing the SS benefit, I assumed you had other income and didn’t need it for the 8 years between 62 and 70.

Had you taken your benefit at 62, assuming it was ~1K, or any other amount. You would have been able to bank it for 8 years and created an estate for your younger or ineligible wife. That money would be in the bank or invested and available to her from your age of 62 until your death and thereafter, regardless of her eligibility for SS.

Now you have a bigger payout, but if she is ineligible to receive the spousal benefit or the widows benefit, for whatever reason, and you die sooner than you expect. You are screwed and so is she.

Re: protect their spouse with an increased benefit.

More accurately, it protects the wife from the husband’s early death. Since men die younger than women every married couple needs to consider this carefully. My older brother’s case illustrates this.

My brother started taking SS when he turned 62. He signed up for survivors benefits. He died when he was 63. So they paid the penalty of reduced benefit for 1 year. Now his wife is collecting a increased benefit for as long as she lives.

I guess if you’re in excellent health when you turn 62 you can afford to assume some risk. In my brother’s case he was in good health but he was overweight. Or is that a contradiction in terms?

My wife has a pension of about $700 a month, as well as some modest insurance polices. So it kind of equals out, with me living rent free on her nice property, and not having to drive or purchase my own car. She can play the long game too. No need for a sugar daddy.

We are the same age, so my monthly Social Security payment being about 75% more than if I started at 62 will most likely help out in the long game. My increased monthly payment starts turning a profit (compared to starting at 62) around age 79. Maybe we can get some robot care-takers and autonomous driving cars by then. Although it’s not expensive to have human services do that here.

Petunia – you wrote:

“I was also referring to your situation with a wife that was not eligible for the spousal benefit because of age or residency…Had you taken your benefit at 62, assuming it was ~1K, or any other amount. You would have been able to bank it for 8 years and created an estate for your younger or ineligible wife.”

My wife already has her own estate. I helped her with paying off the last part of the loan she took out to build her (very nice) house. I get the benefit of living in a peaceful area on a property which she has made into a tropical flower and fruit tree garden.

She’ll actually do better if I croak. My legal will designates her sole heir of my assets. My sister is executor, so it would be risky for her to off me :-) No way would I leave an opening for my lazy narcissist brother to do any of his lying hustling to grab any of my money.

Since my wife and I are the same age, if we get into our 80s together my delayed start of social security will have turned profitable. Life is sweet with a compatible partner.

Yes it is, best of luck.

You say you have inflation .. ??

We in Australia do not have inflation .. according to our PM & the price of everything is in a constant state of evolving in a up ward direction

I worry how the big money splurge on everything covid will translate in the not to distant future .. where did this money come from anyway & how will Australia ever repay it (??)

I listened to Parliament on TV today as they talked of millions & in which directions they flew.

A generation that was taught thrift a virtue….and savings a good thing.

Now, the Fed intentionally punishes savers at a 5% per year clip.

Somehow, that seems unAmerican. Work, earn, save, invest…..those were the ways. The Fed would FIGHT inflation if it occurred.

Now, what’s the formula? And who changed the game and by what powers and edict?

The Fed is nothing but an unelected group of Monetary Dictators…short circuiting the most basic fundamental of free markets, Supply/Demand price discovery…specifically regarding government debt.

I think it was Larry Lindsey that said people are getting what they voted for the last few elections, dealing with our financial problem with inflation. Eventually inflation will get hot enough people will vote for relief and then we are going to get the the big inflation busting recession.

When you are broke it’s one or the other.

the weird thing is virtually no politician alive has any kind of fiscally conservative/balanced budget campaign theme. you would imagine by now at least some small fraction of the electorate would wise up and want someone more fiscally responsible??

Are the boomers really “thrifty”?

Defined benefit pensions

Huge asset appreciation

Decaying infra

Surely the USA has gone financially backwards massively during their tenure?

It’s been a period of extraction, the first generation to hand worse living standards to the next. I’d say it was a period of total recklessness.

I always get a chuckle out of George Carlin’s bit on this.

Paraphrasing…

Boomers are generation of people who live by one simple philosophy: “Gimme that! It’s mine!”

Of course there are exceptions, but it wouldn’t be funny without a shred of truth to it.

I am a young boomer. I handed both my children college degrees with no debt. Plus some nice cash gifts along the way. I am probably going to leave them a nice inheritance when I croak. Worked hard 50 -60 hour work week. Started at 15 1/2 years old. Paid a lot of taxes during my time. Don’t believe I took more than I gave.

I believe you are a boomer as when faced with data they invariably produce an anecdote!

Anecdotes don’t refute systemic points.

All your comments display a great disdain and hate for boomers. Be careful. Such hate is not good for you or society.

Not all boomers stole your livelihood, and left you with nothing or worse. How about you getting up and working your ass off for 50-60 hours a week to provide for a family? My education wasn’t paid for, and I don’t see a need to pay for yours! You are not entitled, and nor are the boomers, except when we talk of S.S. we have PAID for this payout. Yes, there are problems with the system,

Are you telling me you are a more enlightened young aged group of people? That you won’t mess things up for your kids? Not with your truculent attitude. You need to do some critical thinking and soul searching.

historicus-i see it more as ‘thrift’-touting as an effort to keep the population’s wool growing while the truly financially-‘clever’ periodically sheared the sheep. Problem now is twofold: One-the number of ‘clever’ has multiplied. Two-not only have the number of shearers grown, they’ve lost the calendar that showed the necessary time for the wool to regrow…

(i’m sure Pet could comment on the decline in general fabric quality over the last 30 years…).

may we all find a better day.

In the PBS documentary “The Power of the Federal Reserve”

found on their web site…..

worth the watch

Gov Fisher at the 8:20 mark…..we FORCED the investor to take more risk by dropping the yields all the way out the curve.

We knew the markets would react this way.

“Forcing “…. where can we find that word in the Federal Reserve Act?

and what of the 3rd mandate of the Fed…”promote MODERATE long term interest rates..” (moderate = not extreme, 4000 yr lows are “extremely low” wouldnt you say?)

Terrible situation. The only addition I have is that ‘cutting back’ means more pasta and rice dishes….even spuds at the store are quite expensive. Pet food and dollar store tuna is one of those memes trotted out. The cat food is for the cat, like my tenant illustrates whose two cats are his family.

I sometimes irritate my wife. I’ll cook a great meal and say, “This cost us only $1.75 per serving. Can you imagine? At a restaurant it would be $30 per and not 1/2 as good”. Can’t help it, it’s like beating the man and arises out of raising kids during the late ’70s inflation and losing my job in ’81. The other thing I say, “If times get tough, at least we can live on potatoes and home made bread for a few months”. We never do, but we could if we had to (goes the tune).

The pie started shrinking for regular ‘folks’ when Gobalisation began. They told us it would be addition and multiplication, but it was subtraction and division. Sharing means…….

I think the trend is pretty clear what is going on. Prep accordingly as complaints will fall on deaf ears. And vote like a mad man. :-) Maybe key some Audis for a pick-me-up.

I mentally track all meal costs like you. Some benefited from globalization. Many US citizens especially in towns that had manufacturing became third world places as factories left or imported cheap labor across the southern border.

I gave up on restaurants when the quality of food went down. I swear peoples taste buds in the US went down as fast as their IQs.

Earing street food was good in many countries, but mostly illegal in the US. Can’t go anywhere now, so I’ve lost track.

Careful with the street cameras.

I agree, salt seems to have replaced taste at most restaurants and few seem to have noticed.

Add high prices and servers who don’t have a clue how to service a table but still expect a 20%+ tip and I find I have little interest in eating out anymore.

Thankfully I know how to cook well and can and pour a good drink :)

Even better, key some Audi’s in government employee parking lots. Start with the special parking at Reagan National Airport.

The restaurants are all FULL with “wait times” around here (North side of Houston, TX) – Seven_Days_A-Week. I really wonder how many households actually know how to cook these days?

I suspect when times get tough, these same people will just order all their meals delivered.

Add some beans, lentils and peas for cheap protein.

Paulo,

Another great post. My meals cost less than tax and tip for lower quality meal in a restaurant, a LOT less.

And to the other poster. Ignore the generational haters. I have the same mantra: work hard, work for yourself, live well below you means, save the surplus and invest. Wash, rinse, repeat. I told my children who both have masters plus daughter graduated with honors from a top world law skool, “DO NOT UPSCALE YOUR LIFE.” They have no student loan debt, and their schooling was not cheap, neither lived at home and all the advance degrees are abroad. Its always easier to blame someone else instead of sucking it up and producing. There are no guarantees of success and getting up unemployed (self-employed) until you sell someone your services keeps one grounded.

Wolf, I want to propose the creation of the CPI-Wolf that takes private sector price indices’ year-over-year changes, forget baseline effects, and adds to the component percentage changes stated by Uncle Sam via the BS CPI. So for used/new vehicle price increases, we add the real world private sector number less 10% to 15% to allow for Hedonic Magic. We are adding the difference between the BS number and adjusted Real World, no compound math required.

Since we are staying away from High Math here, same with Homeowners’ Equivalent Rent, we are taking the difference between say Case-Shiller index increase and BS percentage change and adding to the weighted component in question. We would do this for Existing and New Home price increases times their respective weightings in the BS CPI index. We will keep it simple. Do not know the innards of the chicken, CPI calculation details, but we will address the 3 to 4 biggest distorters of the true rate of inflation via the CPI report. As far as the Substitution Effect from Uncle Sam, we will let that travesty slide. Steak does not taste like chicken, although snake does.

I would guess that the recent print, year-over-year, would be closer to 12% to 13% with the CPI-Wolf adjustments (vs. July’s 8.6% yoy print), and I can finally buy that 60-foot yacht with my 12% Third Quarter Average CPI-Wolf COLA bonanza!

Not trying to give you anymore things to do, Wolf, but when we American Peons eventually have had enough and march on Washington, we do want to have a realistic inflation number on our Protesting Signs as we are caught on camera and the NSA drones that are filming us.

Thanks for real numbers. I like the fact they leave out food, rent, fuel. I live very close to the ground and I didn’t have the greatest landlords I couldn’t live near Tracy, Calif.

Thanks Wolf

Inflation, when it gets big enough, turns into a political bitch. It’s hard to persuade regular people that being able to buy less and less with their labor is somehow good for them :-]

LOL and yes they keep voting against their own interest;-)

Wolf, you assume people will understand the concept of shrinkflation, and other tricky means of increasing prices while the sticker price look the same.

Oh sure, some will catch on, but most will see the allure of UBI, and other giveaways that the government comes up with and go, see, they are watching out for us.

As I said many times, this is what you get with the dumbing down of Americans via ever accelerating decline of the education system. See OR for latest example, reading comprehension and math not important for getting through high school for the next five years. And they did this via stealth signing… the supporters say because education has to be flexible…. and you guessed it, equitable graduation standards.

Yeah sure. Thank you “no child left behind,” now all of you can be stupid…. you’ve been given permission by our government. This way employers will have even less notion of what they’re hiring. See, they have a HS diploma… and they get 1+1=4

So, Wolf, I agree with you up to a point, if regular people notices, it becomes a political bitch. But that’s why the people must be dumbed down, so that they don’t notice.

Wolf, I too would love to see a CPI-Wolf tracked!

You can even recycle keyword for those posts: #WTF_Charts

Hmmmm.

I am spending the next 2 years retooling and reconfiguring my business so that I can operate it myself as long in to my “retirement “years as possible. I can see the handwriting on the wall for the fate of people my age ( tail end boomers) who try and retire on SS, plus an ordinary amount of savings. I think it will be worse than just cat food folks.

I was thinking of starting a company giving “Plan for Retirement” tours to Venezuela. So people could pick up some tips. Want to sign up?

Or Zimbabwe

Or maybe a video of Jay Powell in your bank account taking 5% and then walking it across the street to Wall Street.

This past week, I saw a video of Ken Langone of HomeDepot, on the tv talking about means testing SS. He wants people who have other income and retirement savings to lose their SS benefits. He himself receives $3K a month, and his wife another $1K, and he thinks he is too rich to receive the benefit.

What Langone didn’t explain was that SS is not automatically sent to anyone. He receives the retirement benefit because he applied for it and so did his wife. If he didn’t need the money, he could have simply not applied for the benefit. Or, I know this is extreme, he could give the $4K a month to one of his underpaid employees.

There is obviously a campaign to get folks ready to means test SS or simply tax it away with the rest of people’s retirement savings. They are also trying to create a committee to improve SS benefits. I can guarantee you the “committee” is a cover to take away benefits without one party or politician having to take the blame.

Hey Ken Langone, I have a better idea. Let’s just take back the huge tax breaks we gave you and Home Depot back in late 2017. It’ll make the Social Security payments you and your wife receive look like lunch money.

And by the way, it’s amazing how those tax breaks that keep on giving through at least 2027 made Home Depot so much more “globally competitive” such that you didn’t need to screw your customers with price increases in the last several months. Then again, I’m sure you had to spend a lot more on extra-wide price labels in order to fit all those digits.

I love it when billionaires want to save our country by taking money away from senior citizens.

Additionally, Lagone can take his ( and wife’s ) Social Security payments and donate those proceeds to the Treasury to reduce the national debt.

Problem solved !

But that aporoach isn’t in keeping with his agenda.

Welcome to the policies of the Democrat Party and RINOs. It took Reagan and outsider Jimmy Carter ( through Paul Volker) to tame inflation the last time. Of course everyone working for the government gets pay raises and pension increases.

We liked it so much we asked for more :

1) One Thousand thank u check to teachers.

2) Six hundreds check for residents of Ca.

3) Fourth stimulus check of $2,000/m for adults and $1,000/m for

children for the remainder of the pandemic, so we can keep our heads

above water.

1) There are 2.8 millions signatures calling for new stimulus checks of $2K/m for adult and $1K/m for a child. It’s a large cluster. It attract more signatures. It might reach a critical point and metastasize.

2) The stimmie checks positive feedback loop increase the output

exponentially.

3) The cause is covid. The effects are the gov stimulus checks.

4) The price is driven by the progressive screamers and the organizers above.

5) The louder they scream, the more signatures they get.

6) The “mob” imitate themselves, herd together and ask for more.

7) More is great, more in higher amplitude. More is the new cause, covid became is the reason.

8) The stimmie is not proportional to the covid. This collective behavior is reaching a critical point.

9) The stimmie will dominate the market square and cancel the rest.

The cause was the U.S. government giving money to lazy bums who don’t deserve one red cent and who should have prepared for their own future but didn’t and never will. Up in Canada only the people who lost their job got money unlike in America. This is the main reason inflation is a lot lower in Canada. No one got free money who didn’t need it.

Prices of major appliances, including refrigerators, rose 12.3% in July compared to the year before, the Labor Department reported Wednesday (11 Aug 2021).

Meanwhile, Craigslist and the hideous NextDoor Nosey is full of free working refrigerators, sofas, couches, TVs futons, beds and furniture. In addition people are trying to wring a few bucks out of things that cost thousands new. Thrift stores are overflowing with good clothing, tools, kitchen items etc.

Shop for used first and preserve your capital.

Wolf – I see where the PPI come in at 7.8% for July. What is the typical lag time for inflation in PPI to show up in the CPI? Will it show up in Q3 or Q4?

Social Security began in the 1930s coming from the horror witnessed seeing countless old people starving to death and/or freezing to death during the Depression. This may be forgotten now but hopefully, we won’t be refreshed on how bad times can get. We don’t realize how low the standard of living was less than a hundred years ago, and is still for most people in the world.

Thank you for reminding us and I do pray we don’t end up in that place again. I do not want to know what it was like.

All I know is that my grandparents always had way too much food in their pantry and garage.

Back in 2018, the US population made up only 4% of the world’s population and yet we consumed 17% of the world’s total energy output. Our standard of living still has a very long way to fall.

> Back in 2018, the US population made up only 4% of the world’s population and yet we consumed 17% of the world’s total energy output. Our standard of living still has a very long way to fall.

Indeed. The entire planet is paying the consequences of consumption addiction.

I see that kind of comment frequently put up by people with no other background or references.

In and of itself it is a ridiculous comment.

In 2018 how much of that energy was used to produce products for export that were consumed by other countries?

For example, agriculture products and petroleum products come to mind.

That amount of energy was not “consumed” just by Americans.

With inflation running so high, why would anyone buy the 10 year @1.36%

The 10 year Treasury market is bigger and probably smarter than stock market. Ignore what it says at your own risk.

Just like Turkish 10 year Treasury is 17.8%. There is a reason for the yield.

Hoping to sell to someone else at 1.0% yield and making a bundle doing so? There are also many forced buyers that have to hold a certain portion of their assets in these types of securities, and there are lots of foreign buyers whose 10-year yields are even worse and negative… plus the Fed… millions of bad reasons.

Venezuela 10-year is at 10.4% while inflation (official, low-ball figure) is 2,450%.

The lesson there is that fake, worthless “money” cannot and does not earn interest.

Soon to be learned by the people of the USA.

Thread derivative

Airbnb reports after hours today.

Their ABITDA will show a profit guaranteed. What’s ABITDA? Airhead-adjusted BITDA.

Anyone watch Cramer’s rant on CNBC about “the benefit of the doubt” for JPOW yesterday? He called all you “inflationists” dead wrong for decades and are too cheap to raise wages. Somehow inflation is good for the poor and middle class.

Any opinions? Refutes?

Wolf,

I read in Wall Street Journal today, Medicare will be able to negotiate drug prices according to the President. Medicare would provide eye care, dental and hearing aids. Sounds good until they would like to lower Medicare age. Seems like Medicare wins and social security recipients would end up paying more no matter what the cola increase.

I think Medicare negotiating with hospitals and doctors means they force hospitals and doctors to shift cost to private payers.

As you know, Medicare is not free for people who are on it. Only Part A is free. But then there are all kinds of things you pay for. But it’s a lot cheaper than regular insurance. So if there is a Medicare “buy-in” for younger people, they would pay for the insurance buy-in and they would still contribute to the system via their payroll taxes. I’m not sure that would be a huge problem for anyone but the insurance industry and the healthcare industry, which are vigorously lobbying against it.

Not sure if they’re now talking about a buy-in, as they did a while back, or just lowering the qualifying age.

They want to lower the age to qualify to 60, probably because so many older workers are losing their jobs and getting stuck paying cobra.

Wolf, I pay some $150 for Part B every month that is auto deducted from my Social Security check and then another $200 plus for USAA Medicare Supplemental insurance, Plan F, which pretty much covers everything. Then you will possibly have a Part D, Medicare Prescription Drug Plan, mine thru Humana, which is kind of a joke sometimes without anyone laughing when they see the covered amount and final tab. I is the co-pays for certain drugs that can eat your lunch. Drug Plan about $17 per month premium, but that is just an opening salvo. So about $370 per month in premiums before out-of-pocket drug costs. Try out-of-country pharmacies cause Congress don’t pay a penny for their own drugs.

On another topic above, I can hear the roar from the WS crowd rising: CPI-Wolf, CPI-Wolf, CPI-Wolf to a deafening roar!!!!

There are buyers, who need to hold government paper , but they are NOT forced to hold 10 year paper instead of short term paper.

Real 10 year yields in most countries , although negative in many instances , are not as negative as in the US. Plus any foreign buyer of US paper is taking on dollar risk. Unless you are a believer in the transitory inflation BS, higher inflation in the US vs other countries will cause the dollar to decline .

Please name the many others

Rcohn,

If you’re foreign buyer (say, with euros), you don’t care about inflation in the US. You care about the exchange rate (which you can hedge) and the yield in USD. So whatever the “real” yield is in the US is irrelevant to you.

Why would you buy bills with 0% yield and roll them over all the time if you can get 1.36% on a 10-year? You’d buy bills only as cash replacement. Anything else goes into longer-term maturities where you get some yield. You have to remember: the alternative = 0%. And in some countries below 0%.

Good luck living with the kids. When they lose their homes acquired during the bubble, they’ll be lucky to be able to afford to rent a one bedroom apt from a hedge fund.

You forgot the retirees’ annuities payments will earn just about zilch in interest while inflation is ten percent. Up in Canada they’re increasing old age security ten percent next year due to zero interest rates on annuity money and skyrocketing rents due to the Chinese driving home prices to the moon. Bandaid solutions don’t work and have never worked. The only solution is the root causes.