Bottom falls out at lower end. Fed-enriched high-end buyers doing fine.

By Wolf Richter for WOLF STREET.

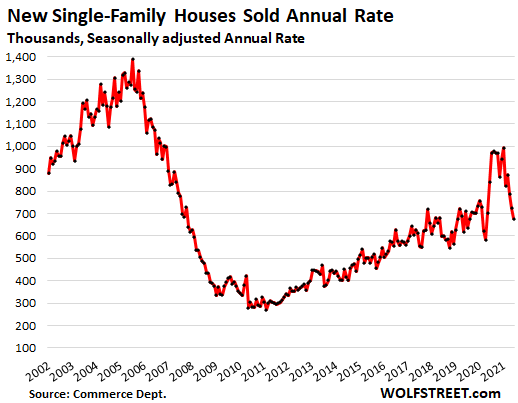

The concept of selling overpriced new houses to everyone is running into trouble. Sales of new single-family houses in June plunged by 6.6% from May, and by 32% from the peak in January, to a seasonally adjusted annual rate of 676,000 houses, the lowest June since 2018, according to the Census Bureau this morning. This multi-month plunge brought house sales back to pre-pandemic levels. And given the construction boom in apartments and condos in urban centers over the past decade, single-family house sales remain a fraction of the boom in 2002 through 2007:

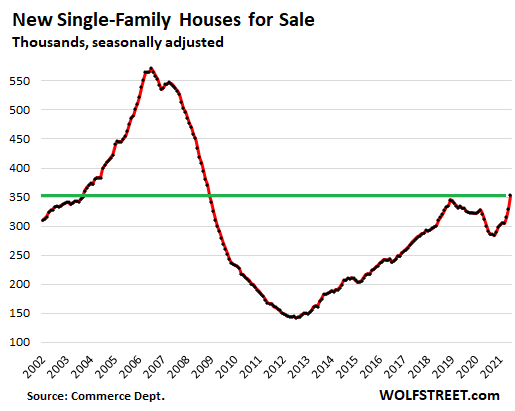

Soaring inventories of unsold new houses. Homebuilders are building, that’s for sure, even if more homes are now sitting on the market. Supply jumped to 6.3 months at the current rate of sales, as unsold speculative inventory for sale jumped to 353,000 houses (seasonally adjusted), the most since December 2008:

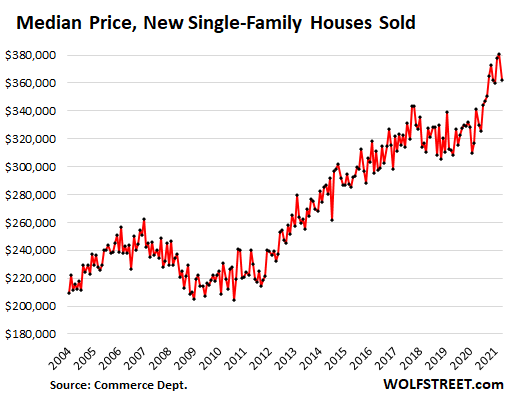

Prices dropped and unwound the spike of the past few months. The median price of new single-family houses sold fell by 5.0% in June from May, to $361,000, the lowest since March, having thus unwound part of the majestic spike that occurred starting in the summer last year. In April, the median price was up 22% year-over-year; in May it was still up 20%; in June, it was up 6.1% year-over-year:

What’s going on? Practically nothing was sold in the under $200,000 price category. The under $300,000 price category accounted for only 28% of total new house sales, down from 39% in June last year. That’s where the volume used to be, but people willing and able to buy a new house under $300,000 are out of luck – prices have moved away from them. And facing those higher house prices, and already struggling with soaring prices in the goods and services they need on a daily basis, they went on buyers’ strike.

But sales are booming at the high end, in the category of people that have the full and undivided love and support of the Fed through its dogma of the Wealth Effect. Houses with a price of over $500,000 accounted for 28% of total sales in June, up from a share of 23% in May, 15% in June 2020, and 14% in June 2019. At the high end, there was no buyers’ strike in June.

At the high end, this is where the money is. And the people that can only afford a house up to $300,000 can just go to heck. This is what this new Fed-directed money-printing economy has turned into.

But the other side of the coin is that demand falls off because there aren’t that many potential buyers in the high-end categories.

In addition, there is the whole issue of the shift to working from home that caused many people to go buy a house in a different location, a larger house to accommodate one or two home offices, and that trend may have run out of steam by now.

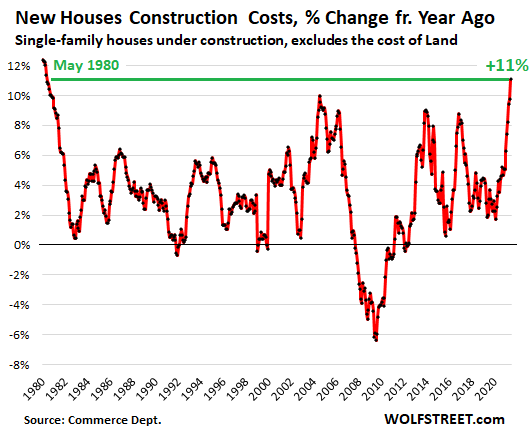

And of course, construction costs spike the most since 1980. OK, you knew this was coming. Lumber costs spiked to ridiculous highs by early May, then plunged but only part of the way, and recently have risen again. Chicago lumber futures are currently at $641 per thousand board feet, still up 60% year-over-year and 72% from July 2019. Steel futures have surged; for example, rebar futures are up 73% year-over-year. The prices of all kinds of other construction materials have surged. And labor costs have risen.

The Construction Cost Index by the Commerce Department, also released today, tracks construction-related costs of single-family houses under construction, but excludes the cost of land and other non-construction costs. In June the index rose by 0.7% from May. Over the past six months annualized, the index spiked by 13.8%. Year-over-year, the index spiked by 11.1%, the biggest year-over-year jump since May 1980:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

More MBS QE dialed up by the FED – LETS GOOOOO

Long-Term effects of QE over time on US Median House Prices:

1971: $ 25,200 (50 years ago.)

1981: $ 68,900 (40 years ago.) 2.7x increase from 1971.

1991: $120,000 (30 years ago.) 1.7x increase from 1981.

2001: $175,200 (20 years ago.) 1.5x increase from 1991.

2011: $227,200 (10 years ago.) 1.3x increase from 2001.

2021: $360,000 (today) 1.6x increase from 2011.

Overall: Dollar has lost 92% of its purchasing power vs. Median House. (Size and quality of house may not be the same but still a useful comparison.)

Yet another data point for the “Slow-Motion Hyperinflation” (perpetual devaluation) caused by the Fed translating “stable prices” into “steady inflation”.

Data from Census.gov New Residential Sales report.

WS,

Thanks for doing the work.

Unless people see these sort of stats, they don’t understand just how systematically they are getting ripped off.

Amazing how just a handful of government subsidized industries display ruthless, relentless inflation…while the march of technology makes everything else *cheaper*

And regarding ripped off:

the big kicker is the fact that that the tax code is not adjusted at the same speed/ amount as the inflation.

I recall in 2010 the “super-high-earners” making more than $250k that needed to chip in a bit more for the new healthcare program. That 250k is not that extreme anymore.

And regarding houses: the first $250k or $500k is exempt from capital gains. More and more are now way above that amount when they sell their home.

So I do have to give it to them.

Smart move to devaluate the currency, have everything become x-time more expensive and then sit back and see the capital gains tax confiscate more and more of everyone’s property.

With that in mind, don’t worry about the 28T$ government debt. It will be inflated away and paid for by taxation.

Good work wisdon seeker, good sorted out info.

The median house built today isn’t the median house built back in 1971. Its quality is not the same, the common sense in its floor plan totally gone.

Size-wise homes now reflect what’s happened to American waists in the exact same time period: undesirable bloating.

well, you can also buy a tiny home for $30-$60k.

It is a bit like boxes cornflakes at Costco. shrinkflation. Same price but way smaller.

Prices are also up due to all additional mandatory BS like solar panels and whatever building codes. That is all great but the bottom line is you need to live somewhere and for housing, it is just way more expensive.

There is a lot of wasted space in more modern floorplans, especially mater bathrooms.

What meaningless statistics. It’s worthless without adding the salary increase line to the chart.

Getting a bit nervous about your house purchase, huh?

LOL, why would I? My home value just jumped another 7% for the past month haha. No “Buyer Strike”, only people who didn’t have enough cash to get in.

Here in NYC one can work for just 30 minutes and buy a whole roasted Chicken at Costco for $6.00 that feed an entire family. And that is at the minimum wage $15. Go tell that to the world.

So a 1.5X increase takes us to $540,000 in 2031?

This comparison is not fair. You need to adjust that by wage growth even though it’s pretty clear that it would still result in a loss of purchasing power. Not 92% though

Federal minimum wage:

1971: $1.60/hour

2021: $7.25/hour

Full-time hours per year: 2,000

Annual compensation at federal minimum wage:

1971: $3,200

2021: $14,500

Valuation: Median house price to annual salary (at fed. Min. wage):

1971: $25,200 / $3,200 = 7.88x

2021: $360,000 / $14,500 = 24.83x

If purchasing power remained steady, 2021 median home price would be $114,260 (that’s 7.88x multiplied by $14,500).

So, the loss of purchasing power relative to fed. Min. wage of 1971 is 68.26% [ ($114,260 / $360,000) – 1.0 ]

As such, you’re right, @DJ.

However, if one uses the price of gold as the relative purchasing power benchmark, then the federal reserve note has lost 97.95% of its purchasing power relative to gold since 1971: the per ounce value of gold has increased from ~$37 in 1971 to about $1,800 in July 2021.

In the latter case (which is more accurate), the OP is correct (at least 92% is closer to the actual loss of purchasing power of nearly 98%).

Either way, the People of the Republic are being fleeced by its own elected representatives in Congress (since 1913) and federal government, which mandate and sponsor a privately-owned, for-profit, partly foreign-controlled “central bank” and fiat currency (not gold backed) – and, of course, continual forced taxpayer bailouts of financial institutions (banks, insurance companies, big hedge funds, etc.).

Wolf:

Thanks for the good, hard work.

FYI, Canfor shut down all their mills in BC under the guise of wild fires (no fires near Canfor mills).

And they have plenty of customers with $100,000 losses (per 120,000 board foot rail cars) rolling to destinations where bankruptcy looms.

Without reduction in supply from mills like Canfor prices would be down another $100-200/Mbf.

As to to inflation. Higher home prices, set at the margin, means higher property taxes for everyone.

And higher incomes means higher tax brackets for all income tax categories. Government and the Fed have a plan, and it is not good for you.

Well, there is always something with lumber :-]

Great points. I’ve too been wondering how excited the politicians and bureaucrats are about being able to continue to collect more tax dollars and grow government spending.

So does this mean I can go back home soon?

we first need to burn it down/s

I love the headlines, but not seeing any of this in my market. Just paid 45% more for a house than I would have a year ago in a bidding war. Still way light on inventory, it is improving, but nothing of what the headlines say here.

Which market?

Springfield Missouri & Metro 350,000 population. I’m hearing the same thing from my peers in various markets in the midwest.

I’m in SoCal and we put an offer on a home where the asking price was already high above the rest of the comps in the area that have sold in the past 3-6 months. We offered at asking and supposedly were neck-and-neck with another bidder. We submitted best and final $15k over asking w/ a $5k escalation clause. The sellers sat on it because apparently someone whispered something real nice in their ears… lo and behold, another bidder supposedly has come in hot on the scene with $100k over asking. I guess it’s “bye Felicia” to us…

This sounds suspiciously like something a used house salesman would say, as most people would rather keep their mistakes, like say knowingly overpaying by half for a house during the largest housing bubble ever, to themselves.

we put our $$ away for 2 years

if things change great

lucky for us we bought our home in 2003

and going no where

besides 3,000 SF is just about right now that kiddies have left

I can’t believe the fools who are playing into the lying REALTWHORES hands like this. You are bidding against yourselves. Wake up.

Just drop out of the market for God’s sake! A blind bidding war is tantamount to a confidence trick. Report that RE company to the authorities for scamming.

Latest headlines: “Real Estate commissions near 100 billion amid sales boom”

What’s the likelihood the whole INDUSTRY is rigged to reward the makers of the game??? Poor & working class never had a chance once Financialized housing took place & investors searching for profits get to play in the game.

Buyers of that home I talked about where we submitted $15k over asking ended up offering $150k over asking. No way this house is going to appraise for even close to what they offered, which is I’m 110% sure why they did not remove the appraisal contingency. They’re going to play some hardball negotiations with the sellers. This will be interesting to watch… lol

I saw the same thing in a Tacoma suburb. I looked at a house that sold for $1.2M last June. The same house just listed for $1.7M last week. That’s a 42% gain in one year, assuming it sells.

Crazy times brought on by a crazy Federal Reserve that loves funny money.

When I lived there for 5 months in the early 70s you couldn’t give your house away.

Since the 70’s they closed down the Lead Smelter in Tacoma. They smelted lead there for 100 years. The houses are not really worth 1.7 Million but after sniffing lead for a few decades anything makes sense.

When I lived in Seattle in the 80s I occasionally have to drive down to Tacoma. Every time I did, my windshield wipers started disintegrating and smeared black all over the windshield.

Tacoma is an ARMPIT.

My thoughts exactly. I’m trying to figure out what house in Tacoma is worth 1.7? Lol

Why did you pay 45% more in a bidding war? Do you really think prices will still move higher?

Despite Wolf’s figures, there are many markets where the supply is still so very tight that prices have not backed off at all. But that doesnt mean these inflated prices will hold

Higher interest rates are coming, just a few more months.

In a bidding war, the ultimate buyer is the loser. And the seller is the winner. You want to be a seller now, not a buyer.

As I have always said at the end of bidding wars… “congrats, you were willing to pay more for that house than anyone else in the universe. Enjoy.”

You might be correct, but in reality it all depends on what the Fed does. Did you ever think mortgage rates would get to 2.75%. I have already heard someone predicting we will live to see 1% mortgage rates. Makes payment pretty low.

“Makes payment pretty low.”

You can always refinance the rate, you can never re-negotiate the principle. In a high rate environment you can make huge principle payments and pay the loan off early, saving a boatload of interest. In a low rate environment, you’re stuck paying that same bloated principle. The people buying now are the ultimate SUCKERS.

Depth Charge,

I think you are right. You just can’t know for sure. Given a few decades the Fed has proven it can add a zero to stocks and house prices and cars.

DC is correct. Better to buy when interest rates are high and the principal lower. You can always refinance when rates drop. Locking in an exorbitant principal is not a good idea.

I know what you’re saying but it’s really dependent on the motivations of the buyer. Buyer often only concerned about mortgage payment and ability to lock in sub 3% rate 30-year fixed rate. Possibly a rate picture never to be seen again in our lifetime. Plenty of belief out there that home values won’t fall but most likely moderate in appreciation due to short supply and pent-up demand. Even if they do fall and it’s their ‘forever home’?

Just last night, I was talking to the recent owner of a home in my area. He beat out multiple offers 5 months ago. He is in his mid 50s and he just can believe how much his home appreciated since he moved in.

He said he almost made a huge mistake …. he nearly backed out after the appraisal came in low.

Cinderella was having a good time at 11:55 too. Got to watch the clock carefully or you will party one dance too many.

And then you woke up.

Socaljim is a rampant bubblemonger

I know people don’t like realtors and s

So SocalJim specifically but so far he has been proven absolutely right

My own realtor told me that she won’t buy a home at these crazy times.!!

“My own realtor told me that she won’t buy a home at these crazy times.!!”

Of course she won’t, because she can’t afford it. They’re are starving. Only a handful are making money. They need transactions – churn. That’s not happening.

It is an awesome time to make a good deal but only for the seller.

Bad deals are made during the best of the time for the buyers of anything.

I am definitely seeing softening in SoCal where I live in San Diego.. Still crazy but still.

Wolf, very very sorry to point out a mistake in your thinking:

when you sell your house, you still need to live somewhere.

So most sellers are also buyers (before or after).

And for those selling and then just renting , what are they going to do with the money from the sale (after subtracting the capital gains tax , city tax whatever tax , real-estate guy cut, bringing-up-to-code-when-you-sell-cost)?

Invest in the stockmarket bubble? put it in high yield savings account with that super generous /sarc 0.1% interest?

Or just wait until the bubble pops? And when it pops, when do you know it is down enough to buy something?

That is just as well speculation and picking the right moment is just sheer luck.

Is the winner not the person who stays on the side lines?

Who keeps his house forever and does not sell or buy?

My dad held the mortgages for several properties he owned. He had very good payers. For my dad, it was a good way to gain some interest and receive steady monthly income during retirement. It caused less headaches than rental properties. Of course now, mortgage interest rates are so low. There are still many people who will avoid using banks though.

Exactly. I’ve asked this same question on this board a few times and no one has an answer. One guy said buy Gold, but that has been flat, too.

If you sell now and wait two years, inflation will have eaten 10% of your money + the lost rent + RE transaction costs + no tax write off. So even if you sell now, RE drops 20% in two years and then you buy back, you’re really not being all that clever. And even if RE just stays flat from here you lose.

A friend of mine in France just bought an apartment for a 1.1% interest rate. Rates can go negative and I wouldn’t put it past the Fed.

Just addressing ”when to know the bubble popping” Mse,,

Been at least somewhat involved in the RE mkt in FL since the late 1940s, and similarly somewhat in CA and OR in years, too many years, since buying and selling in all those mkts, with some ”very nicely” rehabbed.

When the folks in the 7-11,,, FKA ”shoe shine folks”, start talking about their profits from ”daily” buys and sells, that is a very clear, if maybe a bit late, to know that the top is at least very near, if not already with the majority of transactions.

Been hearing this on here since 2017… Prices are how much higher, now?

I’ve been hearing that same in 2003 and 2004 and 2005.

“Supply of unsold homes on the market rose to 2.6 months, the fifth month in a row of increases, and the highest supply since last September (data via YCharts):”

This is a key metric to follow and a good predictor. In 2005/2006 this exploded over a 6 month period and marked the end of the RE boom, and the beginning of the GFC. It was also evident on the ground where houses started to sit for a while and “FOR SALE” signs were switched to “FOR RENT” signs, and then taken off the market completely. I saw it with my own eyes even in my own neighborhood.

Exactly…where are these new homes? In the middle of a corn field 50 miles from the grocery store?

Prices still stupidly high, but flattening some, on existing homes in my area

I wonder if some of the US contractors that occasionally provide good commentary here, have any recent experiences to share, about labour availability and/or pricing.

Apart from cost of materials, contract prices here in U.K. are also ballooning because of shortage of labour. A Polish contractor buddy of mine, just told me he can’t get anyone to work as a great deal of his guys went away to have time off in Poland while their U.K. accounts are being kept in black by our furlough scheme. Same thing being reported by English and Lithuanian contacts.

Thank you, corona?

I have a friend that does gutters for a living. He can’t get any color aluminum other than black and white. No commitment date for other colors. He is busy anyway.

My friend’s son can do it all and is doing a major add on to his personal home. He has had to pay up for materials, but generally available. All new high end appliances, some are in stock and some are being quoted out two months.

My friend has an older oven that is not the current standard and she is being told that it has unknown delivery date because of all production capacity going toward making standard product.

If the government subsidizes home ownership for decades through reduced interest rates, tax deductions, etc., at some point the government has priced out future generations. We reached that point a couple years ago.

Time to gradually raise interest rates to mitigate generational theft.

The United States is mostly empty.

Plenty of room to build houses.

Very true. I see no scarcity of land ( may be artificially restricted tho )and I am hopeful modern technologies would bring in more cost savings in due time.

Or send people who aren’t here legally back to where they came from so that they can get in line like they should and others do.

This would resolve the aggregate housing shortage substantially. The rest can be solved by terminating insane monetary policy.

Amen to that

What you think doesn’t really matter. Those that donate to politicians want more young cheap labor in the country and of course new arrivals vote for one party at 2:1 ratio.

I didn’t borrow another penny after I turned 45 and that’s not going to keep the debt based system afloat.

Long time since Long Island was empty.

Harold must not be that old. When I was born there were fewer than 200M people in the US. It’s now around 330M. To me it is insanely crowded. Vast areas that were open farmlands and fields are now chock full of houses and strip malls as far as the eye can see. Traffic is insane eveywhere, teacher-student ratios are a fraction of what they used to be. No matter where you go, even off the beaten path, is just swarming with people.

The quality of life used to be better when there were fewer of us more spaced out. Never mind power and water shortages since the people on both sides of the aisle who pushed for mass immigration didn’t plan for the required infrastructure.

For most Americans each immigrant coming in lowers the quality of life just a little bit, a hidden tax of more crowding, less nature, less teacher attention, a little less power and water to go around. All so lettuce could be ten cents cheaper and someone else can mow the lawn.

Well said.

Good thing we sent that dumb Statue of Liberty back to France. Keeping it here would be kinda hypocritical. We definitely wouldn’t want to be hypocritical.

what/trailer-the conundrum is that it’s a conundrum, and both of your points are valid.

One of our truly great national visions (not that cheap immigrant labor wasn’t demanded/derided then, either) proclaimed on Lady Liberty, placed at a time when opportunity and land (with no acknowledgement of the freed slave and defeated/corralled indigenous populations, ironically) appeared endless in the face of a national population of well under 150,000,000. The sciences that examined and realized the effects of human natural resource consumption were in a relatively unnoticed infancy (very slight nod to T. Roosevelt in terms of governance), and in any case, the biblical order to ‘multiply and subdue the earth’ was THE accepted article of faith…

The world population has expanded massively since then, relying on the products of the Industrial Revolution to fuel and maintain that expansion. Every individual now consumes more of everything, even those living at what we consider poverty levels. When i was very young, my elders, some who had been in immediate post-WWII China, would make a point of saying: “…there are so many people there that they don’t value human life!…”. Offensive and wrong, obviously (casually dehumanizing the ‘other’ is always an excuse to look away), but if looked at in terms of how we as a species value ANYTHING we perceive to be in surplus (ie: don’t value), there lies a very small nugget of applicable truth to we, as the human population, appear to an ‘economy’.

Given history, we appear to be fast approaching, if not already at, our greatest challenges to the age-old dream of a decent global existence at the current level of population. Will our innate powers of intelligent cooperation and ‘humanity’ be enough to offset and ameliorate the effects of our also innate and many extreme self-interests?

may we all find a better day.

Harrold-just don’t expect much potable water or a genuine, living-wage job/public infrastucture to be near one of those neighborhoods.

(…or, apres-vous, m’sieur…).

may we all find a better day.

Decades at least:

p. 15:

“Traditionally, commercial bank charters required a specific amount of paid-in capital from their shareholders in order to begin operations, and would only provide short-term loans –even for mortgages. In contrast, the charters of plantation banks required no paid-in capital to begin operations; the reserves of the bank were based entirely on borrowed money. Investors mortgaged a portion of their land and slaves in return for bank shares. For example, in 1836 [Bernard] Marigny and his wife Anne Mathilde Morales mortgaged their sugar plantation in Plaquemines Parish – including the house, sugar mill, hospital, kitchens, slave cabins, a warehouse, barn, stable, carts, plowing equipment, animals, and 70 slaves – in return for 490 shares of stock in the bank. The entirety of the bank’s capital stock was based on these mortgages of plantations and slaves. But this still left the bank with no specie reserves for the issuance of bank notes or loans.

Initially, plantation banks tried to sell bonds to raise the requisite specie, but investors were wary of investing in mortgaged-backed bonds without any further security. The state governments instead stepped in to enable the bank to raise specie. By an act passed in 1836, the state of Louisiana agreed to issue bonds, giving the bonds to the bank in exchange for collateral – the long-term mortgages on those plantations and slaves. The bank would then sell these state bonds to investors in the Northeast or overseas, who paid the bank in gold and silver. This specie would enable the bank to begin issuing bank notes and extending loans on a fractional reserve basis.”

-Banking on Slavery in the Antebellum South, Sharon Ann Murphy, economics.yale DOT edu /sites/default/files/banks_and_slavery_yale.pdf

The biggest conflict between bankers in the Northeast and those in the South was slavery. Most of the Northern banks relied heavily on London for gold and trade, and London banks would not accept slaves as collateral because they had outlawed slavery. The lack of good collateral in the South, because of slavery and govt land sales, created a permanent rife in banking between Southern states and the Northern bankers.

The primary form of specie in the South were bills of exchange issued by the London mill agents against the cotton crops. These bills of exchange became the primary form of paper money.

Thank you Petunia; I learned something new from your comment!

As I commented recently, in the Twin Cities as of the end of June:

The median price of the 6,738 pending sales for June was $350k.

This is a decline of 2.5% from June of last year for sales numbers, but an increase of 15% for median price.

To me as an outside observer, homes are selling quickly in my 55406 zip code.

An excellent argument in favor of reparations for the descendants of slaves.

How is that an argument for reparations?

Bobber…

The purposely IGNORED third mandate…..

The “dual mandate” game is an intentional DODGE of what could be the most critical, and the most abused mandate…

“promote moderate long term interest rates.”

Now why would the authors of the Federal Reserve Act put that in the mission statement, and for what purpose? Well, moderate means “not extreme”. Too high, and the effects are immediately manifest. But too low, EXTREMELY too low, record lows….allows the irresponsible generation of debt by the current generation and the burdening of future generations. Immoderately low long rates allow the pulling forward of wealth from the future to “fluff” the present. And this has been done in spades by this Fed.

The younger folk in this country should be outraged. The debt will be theirs to deal with, and add in they will have the ability to SAVE taken away. Inflation with zero interest rates punishes saving, once considered a virtue in the United States. Both condition intentionally implemented by this Fed. Which brings us to the second mandate, “Stable Prices” which is abused and ignored as well.

Who pushed for these low interest rates to begin with and why? What was the turning point?

We’re already outraged. That makes us bad machines. We are not welcome in polite company. We make our friends and family uncomfortable. Then they resort to calling us whiners. But thanks for the advice anyway.

Months ago, I read that there was/is a proposal for a $15,000 first time buyers credit. I don’t recall where I read it but it’s the kind of stupid policy government will implement to make housing even less affordable and turn even more people into debt serfs.

If it happens, then even more people who have no business buying or qualifying for a loan will inflate prices even more for everyone lese.

Yep. I read that as well. Think some congressional group proposed it, but it’s not passed yet.

BLND probably marked the top of the RE market.

Labor…

I heard some elected person on the radio wanting MORE imported farm workers and YEAR-ROUND not just seasonal (i.e. dairy workers, maybe meat-packers?).

SAY GOOD-BYE TO THE NOTION OF INCREASED WAGES, FOLKS. THIS IS WHAT THEY DO, EVERY TIME.

I know of farms with the *ENTIRETY* of their work-forces being non-Americans.

Someone else should research what’s all in this new proposal…

I once did some research on the effects of slavery in the Roman Empire. Lower wages for Roman citizens was the ultimate outcome. Those same citizens were farmer/soldiers during the Republic. Farmers most of the time and soldiers during war. They were self reliant and productive. They were bought out by large slaveholders who created latifunda, the Roman equivalent of plantations. The former soldier/farmers turned into insulae trash. The very same soldiers who fought to conquer the land that was bought out from underneath them. I couldn’t help but see the parallels with our own times.

Is money getting tight? The selloff in Bitcoin is over? Maybe a result of Feds latest hint at QT. Fiat dollars are scarce, home buyers pullback, prices rise, better have digital

I watch prices at Holden Beach, NC. After GFC a lot properties couldn’t find a buyer. Saw a nice home that the owner had to drop to $320,000 to sell about seven years ago. Asking about $720,000 now. About $450/ sq ft. Used to be pretty rare to see a million dollar property listing. Now not that unusual to see $1.7 million.

My friend’s place off the island hasn’t sold yet at $195,000. She had a couple offers at around $175,000. Her all in cost after improvements is about $130,000. Bought in May last year. She has been working remotely there and trying to hawk it all summer. An insane number of people looking, but she is trying to extract maximum price.

My friend just called me. Got three offers $185,000. Best and final tomorrow.

Funny how if you listen to majority of MSM, this is so counter to their narratives. All I hear is, housing just taking a pause, everything still red hot, individually selected cases of people still overbidding to create the optics of everyone is still doing this…

Doesn’t help that last month sales data ticked up and it’s business bad to usual again for the housing bull.

The lack of actual information on MSM about the housing market is startling.

The younger generation….under 30….

have had the ability to save taken away, as saving is now intentionally punished by the Fed….they bring you inflation and zero rates.

they also are having the dream of home ownership stolen from them…as the Fed continues to pour gas on the real estate market with their buying of MBSs 2% below inflation…remarkable and has never happened before. Why is the Fed doing this? Shameful, IMO.

Cant save, cant afford a house….two of great things that once was America.

Not just under 30. Most of my peers under 40 are in the same boat.

historicus

Goldman Sachs stock is up 47% YTD. What are you complaining about??

> The younger generation….under 30…. have had the ability to save taken away, as saving is now intentionally punished by the Fed….they bring you inflation and zero rates.

The old crowd benefited by the Fed will have to work their ass off to feed and put a roof over the under 30. The young will play video games meanwhile.

College education is a good example of what easy money does. A lot of the borrowing was foolishly spent because it was OPM. I know. I had a student. Trip to Europe. Many Apple products and plenty of restaurant meals. PhD degree.

It’s easy to do because that is the college culture.

The people I know buying housing right now are 30+, have had some kind of insurance payout or inheritance, and work in tech. That is the cross section of “young people” who are buying or looking to buy. People who got a financial break and didn’t screw it up.

Dude, I’m 40 and my down payment savings just got obliterated. It’s like we were standing still. My wife and I are still very much haves, but the divide in this country does not bode well for the future…

The MSM isn’t there to inform you, just to entertain you in ways that help enrich their sponsors.

Whoops, meant to answer down thread.

The MSM is the globalists propaganda arm. Of course they’re not going to highlight the repercussions of their graft rackets.

Sorry, but here in Boston, it never took a pause. Next to no inventory. Just saw a 1960-built split close this week. Listed for $600k, sold for $780k. Anything that is not a dump still gets multiple over-ask offers with waived contingencies.

Lower new home selling prices is a bad sign for the economy. I know Wolfe does not agree with me on this, but I have found that lower new home prices is a reliable leading indicator of recession. It is time to slowly start selling some big winners and slowly shifting more defensive. We’ve got about a year until the economy falls apart, maybe 18 months. The US is being terribly mis-managed right now and we are all going to pay a heavy price for it.

New homes selling lower canabalizes the prices of used homes. This happened in Florida in the 1980’s.

Last summer – first of seven homes to be built across the street from us sold for $260,000. As the lots were developed prices rose. Abode #5 sold into the $300,000 range. #6 going for 360,000. #7 timeline completion appears somewhat er, ‘stretched’. Then there’s the entire block behind us .. to be built out – by the same developing concern. Wondering how vacant that vacant block will stay, considering the uncertainties going forward ..

Wolf – You gave us the figures for the New Construction homes, but not existing homes. Inventories on existing homes are still very low. Prices are still considerably above the pre-pandemic levels. This is the first article where I feel you are reaching with your narrative and not really supporting it with data.

I went back and re-read the article and realized that you are only talking about the new construction market, not existing home sales, so I was just applying your analysis to the whole market incorrectly. Sorry for the diss, Wolf.

I gave you existing homes on July 22 when the data came out:

https://wolfstreet.com/2021/07/22/home-sellers-emerge-from-the-woodwork-new-listings-unsold-inventories-supply-rise/

It will be interesting to see what happens when the folks who have been living rent free without being kicked out finally hit the streets. I’m thinking all those empty houses and second homes are going to be targets for squatters.

I see a lot of media saying it’s higher unemployment benefits that are keeping folks from working, but nobody seems to add in the effect of not having to pay rent at the same time as they’re collecting those funds. That’s a lot of “free” pocket money for most folks in that boat.

People would have to be fools to go back to a “gig job” before collecting all the UI available. They can go back to their previous gig anytime they choose.

So do protracted periods of unemployment on a resume not matter anymore to prospective employers? What will they say when a hiring manager, even for a gig job, asks “So why were you unemployed for so long?” “Oh, it was just more fun to sit on my a$$ and collect the freebies from Uncle Sam.”

There are no hiring managers any more. Just an app now.

Worse yet Harrold…the app simply filters out resumes with protracted unemployment gaps. The candidate doesn’t even get an opportunity to explain that getting paid to sit on your butt was irresistible.

They were “consulting”.

There. Fixed.

@ 3D Modeler: that is not true and could easily qualify as discrimination. People can be unemployed for many reasons, including taking 6 months off to care for a dying parent in another state, heal from a serious injury or illness, travel while they can, etc.

Any reputable company knows these things and will not reject applicants just for having a “gap” in which they apparently were not slaves to a corporation for a little while.

You’re absolutely right Pat…there can be a myriad of valid reasons for the gaps. But saying “Any reputable company knows these things and will not reject applicants just for having a “gap”… ” is not unlike saying “Any reputable company knows that discriminating based on age is illegal.”

Yes. So my point is that any company worth working for will not discriminate because there is a gap (or any other reason, such as age). A good company will ask about a gap, but will not automatically reject applications for it. Any company who does that will exploit their workers in many other ways too.

Look for a job today – it is all hiring apps and HR. Those are easy enough to defeat by knowing how to word your application to get by them. Also, never list your gender, ethnicity, age, etc. as it is only used to screen you out.

The bigger problem is getting the approval of upper management for your hire. Even if the hiring manager and potential coworkers like you after interviewing, and want to make an offer, it is not over.

The more senior management has to sign off and is 100% woke as they do not have to live with the consequences of not hiring based upon merit. They only want cheap combined with the ability to virtue-signal to their peers at cocktail parties.

No wonder so many are going John Galt, especially those 50 and older.

In other works suck the system dry until there is nothing left to suck. Sounds like good moral values and a plan for success in life. As I posted previously, If I ever received a resume from one of these people without explanation it would find its way to the shredder so fast your head would spin. Same if it were an online application.

Ah, Swamp-but the human desire to emulate the ‘successful’ has never changed, it’s that the example of what grants ‘success’ has…

may we all find a better day.

I’m waiting to see if there is at least a little foreclosure spike in August despite the upcoming new CFPB rules. Many completed foreclosures still skew to low down payment buyers who were always comparatively bigger risks. Right now the foreclosures are cleared out due to the extended lack of filings. I don’t think that rising equity did much for people like this since it benefits them in the short term to stay rent-free rather than sell the house.

I’m not seeing the new builds sitting buyerless in the desirable states where I look, and there is nothing under $250K for new builds. Builders have been raising prices on new developments (townhomes), but I don’t know if it’s the market, construction costs, or both. I see people putting lots they’ve been hanging on to for years up for sale, but that’s usual. The working service sector two-income households are bidding $350K on places that were $100K cheaper 18 months ago. I don’t see that lasting, and the older houses (50+ years old) are sitting. Things are not going under contract nearly as fast as they were in May this year. These are the commuter communities for ski towns. You will pay less for a mortgage than for rent in these places.

I used to wait until fall and winter to see better deals, but seasonality is out the window with virtual tours and the pandemic.

I still say people have been suckered in to thinking economy is better than it is. Last I heard real economy, meaning hours worked is down 5% from Pandemic times. A lot printed money and Zirp has got people spending. Everyone I know spending is making good money, but are carrying high debt loads. No way are most prepared for a real recession.

Oops down from pre pandemic.

Still 6 or 7 million fewer employed compared to Feb 2020 (when about 151 million were employed).

MountainTime,

“I’m waiting to see if there is at least a little foreclosure spike in…”

You will not see many foreclosures if the home price is much higher than it was in prior years because the struggling homeowner can just sell the home, pay off the mortgage, and walk away with cash.

You only see foreclosures when home values dropped a lot below mortgage payoff amounts.

Chicken and egg. If high prices are due to low supply, and a bunch of struggling homeowners put their houses on the market at the same time, the supply will now not be as low, which will cause prices to drop. That’s not to say that it’ll get so bad that it’ll cause them to go underwater (which is where foreclosures would start), but my larger point is that we don’t know what the market would look like in the absence of these government interventions.

This last week I starting see price reductions on Zillow for the first time in a couple of years. The production builders are still raising prices on planned homes due to costs. But I see that trying to raises prices on homes to make up for rising costs will soon run in to the brick wall of declining prices ( and ability to pay). Around Here ( suburbs of PDX) builders are locked in to what they are building a year or more out, so I expect it will soon be type for belt tightening in the home builder business.

No one cares about builders costs. In fact, no one cares if builders go bankrupt. I sure don’t.

Starting to sound like sense getting into the market, hopefully deflate and not pop. But so many instances of the same thing. No idea where the ultimate break point will be in the “everything” bubble. But the clear fraud going on in the cryto space could end up being the trigger.

I think what is morphing in the minds of the Potential Home Buyer: A.) I am really stretching the household budget to afford this overpriced, so-so built, house. AND B.) I don’t want my neighbors laughing at me for the next 7 years for buying at the VERY TOP OF THE CRAZY 20-21 HOUSING MARKET.

Probably, more A than B, but the lack of supply and the Covid-driven location craze had more to do with Americans pushing the BUY button than any newfound acceptance of higher prices are okay as long as the Fed and Uncle Sam are subsidizing my existence. When two houses on my side of the court sell for almost $100k more than a similar house across the street from me a matter of weeks apart, even a drunken sailor would think that something is not quite Kosher. Price spikes are never good times to put your hard earned money down on anything, including stocks and bonds AND REAL ESTATE.

The Buyer’s Strike will come to the new and used vehicle markets by Fall, because the FREEBIES FROM HEAVEN are starting to trickle out, and the economy is not looking all that chipper, especially with all the new talk of encore Regional Lock-downs and Covid, Act II via DELTA Force hiding in the bushes. Throw in Mortgage and Rent Forbearance programs mainly going the way of the Doo-Doo Bird due to the untried legal cases getting prepped for the court circuits; a major State Supreme Court is destined to step in on the side of Lenders and Landlords any week now as Breach of Contract precedents in American law go back hundreds of years now.

And as was mentioned yesterday on these erudite pages, the Confidence Lever of the American Public is starting to wane. You must be really confidence in your continued good luck at putting manna on the table in the years ahead, otherwise you will not spring for that new adobe that just went up 22% in the last 12 months.

So home inflation may fit the Fed’s definition of TRANSITORY for the next 90 minutes, but rest assured that prices will stay over 2019 levels for many quarters into the future as more Americans choose to Shelter In Place in a sliding home marketplace and a SLIDING U.S. ECONOMY. The demand side is about to reassert itself in a big way.

I bought a condo in 2007 near the peak. Sold it for a loss in 2012. Bought a house in Florida in 2012. Sold it for a gain in 2016 and moved to a gated 55+ community the same year. Have been here five years. I have palm trees in my yard. My monthly expenses are cheaper than rent. Unsold housing inventory is slim.

Bought a $16k quarter acre lot in the spring. I have a contract to purchase a lot in a nicer community closing Friday. I figure long term holding two lots is insurance against hyperinflation.

Some algorithms show it is cheaper to rent than to buy. I bought land to diversify my portfolio as some suggested the stock market is a bubble too. Some think the bond market is a bubble. If I hold cash in an inflationary environment, time will erode its value.

I like your thought process. We had decent luck with farmland. It more than doubled in value in less than 20 years and brings in modest rent. The problem is buying more. It is very tough to find especially in the same area. It is also very expensive and, trying to save for a large down payment in this environment is a losing battle.

Bide your time, Janna. Prices are quasi-ridiculous right now in real estate and the adjustment process has just begun. Good things come to those who wait.

Why would there ever be a recession again. At the slightest downturn in the economy, the Fed will ramp up money printing to prevent it.

Wolf says it all of the time, “whenever Wall Street cries, The Fed steps up to satiate

them”.

There is no more “Creative Destruction”.

The Fed can’t do real stimulus on its own. QE does nothing. QE plus deficit spending does a whole lot, but that requires acts of Congress.

To combat a recession, Congress will have to continue deficit spending. Over the next year, we have a political environment to support that. Democrats can spend $2T to $3T by ramming it through reconciliation.

But if Democrats lose the House or Senate in Fall of 2022 (which is likely), it’s an entirely different story. Republicans will not agree to spending increases, and Democrats will not agree to tax cuts. Nothing will happen, and areal recession will begin. If stimulus comes at all, it will occur only after a stock market crash.

The year 2022 is shaping up to be a bad one. You have tapering on the schedule, plus election issues. That said, we’ll be lucky to get through 2021 without a crash.

Been watching Steve Van Metre. He shows chart showing how restrained consumer loan growth is. I think bank loans are 91% of money creation. He predicts Fed is going to keep trying to press rates lower til they get bank lending higher. Big banks don’t want to lend to the people that want to borrow and many credit worthy people still remember GFC.

Because “printing” money and government deficit spending can’t keep living standards from declining forever?

Ah!, but for the FED, tis ALL about the process of Destructive Creation .. where the lowlyMokestanis’ dwindling assets are blown away like a bad fart in a foul bankster wind .. only to be reconstituted into oodles of free 1’$ & 0’$ of the reserveRealm, to be spent acquiring megaYatchs, Art, PMs, bugout real-estate, hot babies, ROCKETS, or whatever .. by their fellow psychoavaricious chums!

New houses sold “woke & stopped” after reaching 1998 high.

Houses are the most expensive item anyone will buy in their lifetime. But they are overpriced for a reason: they are hand-built piece by piece. Pre-fabricated homes make much more sense. The only quibbling point is the aesthetics of it. You don’t want neighborhoods of tin cans that look like all the other tin cans out there.

Most of the neighborhood homes are cookie cutter homes anyway

Florida is the most architecturally boring place in the world.

In higher end SoCal beach cities, about 1 year ago, you could get a decent older 3BD home on a quiet street for just under 2M. Now, you are looking at high 2Ms, and another strong buying wave seems to have started several weeks ago. Inventory, which was slowly rising 1 month ago, has just tumbled to the lowest I have ever seen. No buyers strike here.

I have friends in metro Detroit, in metro Chicago and in the Ft Latuderdale area. They all report red hot markets.

Boston is smoking hot.

I am shocked at the strength given the massive runup in prices, but it sure looks like there is more room to the upside.

Friends of mine who rent are asking me what to do … I tell them if they buy, only buy a quality location. Eventually, this will come to an end, but prices might move much higher before it ends, or they might not.

Agreed on Boston being smoking hot. The slowdown has not hit the suburbs *at all*. 1960s/70s split levels in working class suburbs that were $430k three years ago are now going for over $600k. From what people I know in the market are telling me, they can’t win anything without going at least $50k over and waiving all contingencies. Now, even offers with rent-backs are becoming the norm.

I will make a bold prediction here:

Home prices will be much higher next year, mortgages much lower.

Look at Europe where you can get a mortgage for under 1%. We are heading that way.

That which we do not wish, we cannot perceive.

I can sense that most commenters here aren’t homeowners and wish to become one but don’t want to pay the price. It’s the wrong mindset.

Best time to buy real estate is yesterday.

Fed owns the housing market through their MBS purchases.

If the market were to crush, Fed will buy more , ban foreclosures and keep homeowners in their homes by renegotiating their mortgages.

This sucker can’t allowed to go down we are far passed the point of no return.

It could play out that way. Most of the time asset bubbles reset to a lower price. We are in a new spot as this time Fed is on the lower bound and it might take $10 trillion QE to try to stop asset deflation. Will people accept homes costing 10 times income? That’s usually about the upper limit, but time will tell

Your bold predictions assume that the younger generations will continue getting smashed so that the boomers and wealthy can keep their assets.

Those are assumptions I wouldn’t count on.

Younger generation don’t vote.

They will be screwed over and over.

Look what happened with the virus, We shut their schools to protect some old 80 years old farts then we sprayed trillions around , the young got nothing but the future bill, and now we are having them take an experimental vaccine for a virus that affects them least.

“Younger generation don’t vote. They will be screwed over and over.”

But they grow older, just like everybody, and they will eventually vote against all of this graft. Don’t count on this situation continuing on for long. It can’t and won’t.

Depth, they won’t necessarily vote against graft, but they’ll expect the graft to benefit themselves, this time. And it’s clear that printing money to inflate the value of assets doesn’t benefit the younger generations without assets.

So you are lamenting the fact that the younger generation won’t be voting in sufficient numbers to protect their interests. That includes sending their children to school regardless if the results are to kill off a percentage of their elder family members, elder friends or acquaintances or any other “old farts” that they encounter. The experimental vaccine was actually first taken by volunteers in clinical trials. Once approved, it was distributed first to the medical community and some essential workers. Then the vaccine was primarily (USA) only available to the “old farts”, who voluntarily took it. The rate of hospitalizations and deaths plummeted. Among the unvaccinated, which is now a younger cohort, there are increasing hospitalizations, health complications and increasing deaths. So now that we have evidence of a vaccine that can protect younger people also, it is a bad thing that they have that choice?

What exactly are they going to do? Put off having families and raising kids (once they can afford to squeeze in at nosebleed prices) for an indefinite amount of time to wait for “the crash”? Or, will they pay boomer and genX landlords ever escalating rents with no return and stability?

Homeownership can be a trap especially in this crazy environment. And, if you need a 30 yr mortgage, that’s even worse. Personally, we like the freedom that renting offers. Maybe if you are retired or planning to work the same job for 30+ years, that’s different.

I always say to purchase or rent is really complex calculation especially with Fed monkeying around so much with asset values. If you are good at real estate and want to stay put for a decade then buying at the right time is the way to go. If you like liquidity and flexibility and are good with stocks you probably will be better off renting.

Being “good with stocks” means very little today in the distorted market we have.

The stock market is distorted, that’s why we invest long-term. Once we get closer to retirement, we will change strategy, but for now we *believe* we have time to ride out the highs and even very lows. You really just have to diversify whatever it is that you have. From my experience, it seems that the best returns are the ones that always take the longest. That’s why I don’t like homes because we have never been in a state longer than 10 years. If you have time to babysit them, they can be a good investment as long as the neighborhood doesn’t go downhill.

The freedom to see your rent kicked up at any time? The freedom to have your landlord sell the place out from under you? The freedom to have entry level appliances? The freedom to not be able to paint your walls? The freedom to wait for cheap repairs to issues in the place? The freedom to owe rent when you hit 65 instead of owning your dwelling?

If you buy in the right area, you don’t have to stay in the same job to make a house work.

We have had great luck renting in 4 states. The key is that you must pay on time every time and you must take care of your rental. We have very few restrictions as long as we get approval first. Renting is about trust. I’ve had more restrictions with an HOA than where we rent now. We rent a 4bd house, have a garden, have painted, and screened in our porch.

Staying flexible has allowed us to invest in our careers which has brought a much better return than owning a home.

Right now there are several dynamics at work. The Pandemic forced a lot of people out of the city into the suburbs and in the WFH mode. Now, with the massive crime wave hitting the cities there is no reason to move back in there. A lot of them are stuck with second rental properties in the city which they kept and which they can now rent for zero or negative cash flow as rents are lagging way behind the market values of the properties. They are starting to unload these properties in droves. The properties that they want to unload have gone up so much that they are now un affordable. So there is going to be a gigantic reset. This could happen pretty quickly. It is not going to be pretty.

I’ve been wondering about the impact these inflated home prices in San Diego will have on the rental market since many of the homebuyers this year are investors. Based on the prices the homes are selling for, they would need to increase the rent at least 40% just to cover the new mortgage payment (from what rental rates were with previous owner), and that’s not including taxes, maintenance costs, insurance, etc. That’s assuming they have a mortgage and didn’t pay all cash, but I digress.

San Diego locals cannot afford to have their rent doubled, considering a huge portion of the population works in tourism, hospitality, military, etc.

So what are the investors going to do when they cannot rent out these homes at those inflated rates to compensate for the inflated prices they paid? I’ve already seen homes in undesirable neighborhoods (North Park) being listed for 50% above the market rate for renting. Those homes are just sitting there empty for weeks.. waiting for renters who cannot pay that much.

Four or five guest workers per house does the trick. Every Chinese landlord has this one figured out.

Rumors from my wall street buddies is retail is seeing money being pulled from their 401K so they can get into a home. This is a new significant trend.

They 401K owners are willing to pay the early withdrawl penality just to get into a home.

I think that is true. Plus there are more people doing self directed IRA’s and borrowing from 401K’s I believe. It kind of make sense if you believe the pundants saying you need to own something real.

Anybody that rode the stock market out since 2009 plus dropped in $10 – 15K in every year must be pretty confident.

A bad sign to me is someone buying a house and letting it sit. It’s negative carry and it’s a sign of too much speculation.

Exactly.

I know some people who were at peak earning in 2009 and their 401k is up so much they bought vacation homes. Prices could drop 30% on these vacation homes an it still will not hurt them financially. Even if they had to sell.

There aren’t many 401k plans permitting in-service withdrawals, except for hardship. I have never heard of a down payment qualifying as a “hardship”.

You must be referring to IRA or self directed plans, not a 401K.

That is not true. You are allowed to do a hardship withdrawl for a downpayment on a principal residence. You can even do a hardship withdrawl for necessary repairs on a principal residence.

Not many plans allow for that. You’re just desperate to create demand narratives.

I believe the Cares Act temporarily changed how funds from 401ks could be accessed.

Also…gov TSP plans allow workers to borrow against their plans. That rate is currently 1.5%. If they fail to pay it back, they then pay taxes and penalties. I would imagine that is like IRAs where you only borrow principle. There are many well paid gov workers and those plans are often additional retirement savings. This option existed pre-covid though, but borrow rates weren’t ever this low.

Each 401K is different. A friend had one that you could borrow 50% for any reason. She didn’t even have to pay it back on leaving the company. Just keep making the payment until it was paid off.

The unpaid loan balance would be treated as an early withdrawal and subject to the 10% penalty, as well as being treated as income.

None of the plans I was party to would permit the loan to exist beyond termination of employment. But I suppose that is possible. Otherwise, you’re on the hook for the early penalty and an income tax hit.

Many employer plans have loan provisions, which are not hardship withdrawals and usually must be repaid within 5 years.

There’s also something odd going on with people who collected unemployment for over a year and didn’t pay rent. I read an article the other day about a couple in the Bay area who both collected unemployment, didn’t pay rent, and had saved $80k for a downpayment on a house…. While not having jobs..

Now, I would hope people like that do not actually succeed in getting a mortgage, but it worries me that longterm unemployed people were able to save that much. It makes it seem like my $80k is worth next to nothing now.

I’ve had multiple people suggest that I borrow from my 401K in order to buy a home outside of Seattle. Of course, I didn’t do it because I think that is insane and another indicator that this is a bubble.

I know there is not an equivalent, but isn’t it odd that buyers on the one hand are ignoring increases in car prices and buying sight unseen, but on the other hand have become more cautious with housing. Ok, I know that’s not exactly what this report says, and it is talking about new construction more than anything else.

But still, I seem to recall from Wolf’s comments previously, house buying has tapered off in terms of both new and existing houses sold. This makes me wonder about the type of people that are paying for cars and houses. I know they are substantially different categories in terms of dollar amounts, but both are still major purchases.

Would perhaps economic status of the buyers explain the difference?

If there’s any truth to the notion that a lot of big city dwellers who owned no vehicles suddenly needed one or more vehicles when they moved to the suburbs (pandemic, WFH) is true, that may explain some of it. But I’ve seen no concrete numbers that would help explain how much of a factor that has been to the vehicle buying behavior of the past several months.

It’s people who are bad with money. People who got flush with government money and splurged on new (or used) cars, no matter the price. And maybe even a house if they could convince the bank to lend to them.

But yeah, people who are good with money do not pay those inflated prices. They wait for prices to drop instead.

People who are not accustomed to having money will be the quickest to spend all of it. They don’t realize how fast it will disappear

Looks like Facebook will be entering the Real Estate market soon. The proposed Willow Village is a pretty smart move in my opinion. It’s one way of turning existing office real estate slowly into a mixed residential/commercial use. Facebook might be borrowing a couple pages from Japanese companies here i.e. they might soon be providing housing for their employees.

I can’t abide having Mark Zuckerberg as my landlord though.

My grandparents and parents lived in Company houses in Pennsylvania when they were working in the coal mines between 1910 and approximately 1950. I’m sure there are other instances of this type of arrangement here in the U.S. over its history.

Pullman was the first who built a company town with cheap housing,libraries,hospitals,bowling alleys etc… around 1850’s.US Steel,Bethlehem Steel,Jones & Laughlin,Ford,GM,Eastman Kodak followed suit later on.It was called “paternalistic capitalism”.

Also you may google:

“The steel workers : the Pittsburgh survey findings in six volumes

by Fitch, John A. (John Andrews), 1881-1959”

High-res 600dpi scan of this book is in public domain.My grand-grand-parents look at me from b&w photos.I am afraid to even guess what they are thinking about me and the Big Picture in general ☺

My home town had one of those housing arrangements. Houses were located on Cotton Mill Hill.

If I am not mistaken the town of Concord, NC was owned by Concord Mills up til about 1980.

Milton Hershey did this. Not all went well.

Zucktown…. Haha, the autocorrect kept wanting to put in Sucktown.

Whatever float Zuck’s boat I guess. Seriously though, if Zuck wants to help alleviate the housing problem near Menlo Park, more power to him.

1) The charts speak for themselves : prices & sales are down.

2) WFH : game over. Back to the office before back to school.

3) Covid is here to stay.

4) The infrastructure bill is not for bridges, but for the chronic

covid disease.

5) The gov declared total victory will not admit defeat.

6) The other side might constrict money for the sick economy.

7) A semi comatose economy is bad for RE.

8) Add Didi and Xi re-edu : muzzle up America, or a pincer attack.

Michael, I just understood everything you wrote. A fine day, indeed!!

Micheal Engel

We’ve compressed 30 years of economic deformation into one and 1/2 years. Nothing makes sense anymore. David Stockman needs to update his book “The Great Deformation” and add a new chapter.

In the Golden horseshoe around Ontario, Canada the average 30×100 foot lot sells for more than $361,000. Just the 30×100 foot lot itself.

The Olympic Vile : gold medals and Olympic gold digging. Disability income for life, because she was sexually abused by an Olympic doctor.

Are you meant to say, every Olympic participant is promised a bright future of medals, pension and permanent job offer which is not given. So they took advantage of the system to file grievances?

Do you even know what is the current disability income for a thirty year old?

Simone Biles US Olympic superstar, adored by the media, in her interview, she was focused on a list of grievances, since she became a victim… preparing a deep pocket lawsuit.

When American athletes are sent to the Games partially funded by American taxpayers AND THEY KNEEL DURING THE NATIONAL ANTHEM, I then turn the channel and no longer watch these ingratiates. Good luck getting corporate sponsorships and advertising contracts!

Thought about making an offer on a house today. Was best by noon. They had SEVEN other offers. I wasn’t willing to bid over. The seller’s realtor refused to disclose any other bids if mine won with an escalation clause. These people are crooks!

M

The whole RE industry is infested with crooks and lowlifes. We have to deal with them every day. Its getting old. About 15% are honest and competent. Usually they are in the lower income and poorer neighborhoods.

Perhaps the curve is Set Now on hold waiting for a Heavy Hitter. Some Central Bank’s raising rates Perhaps > Another Huge attempt from the Fed to buy off an unavoidable avalanche. Could be the Race is setting up and the end is the means . Time to pick sides now / soon and place your bets before the “odds change” and nothing becomes worth betting on . Perhaps the Politicians ( Quite aren’t they ) will gauge and guess what side to take. A country run on a Gut feeling ?. Looks like Inflation is a hard to kill Virus of its own. Raise then Lower Home prices, interest rates.

Seems simple to guess what might happen from what’s been going on , more or less of the same or not what else is their ?

I am beginning to understand the illogical dreams of just flying away to space and beyond , making a spinning wheel to throw darts at . RIP.

Home building/buying/refinancing is the US Economy.

That is what the Fed does when they lower interest rates, nothing more.

The service economy follows the housing market and is not self sufficient nor can it drive the economy out of a recession/depression.

At $29 trillion, there is no turning back.

The Fed. Must figure out how to drive mortgage rates ever lower, anything else will lead to a quick catastrophe.

Article mentions 500K as the cut-off for “high end” I live in metro ATL which is hardly a high priced market though housing is no longer cheap. I don’t consider this price point “high end” in the areas where people prefer to live. It’s doable in nice neighborhoods which aren’t very convenient commutes but otherwise, only in locations that I would rate average to mediocre where I’d never pay this type of price.

Hmmm… So the housing run up might be transitory after all. Yet it’s all different this time around of course.(can we trademark this phrase?) Statistics and probability point to an “unprecedented” run up always faltering with prices plummeting to “unprecedented” lows which are actually just still marginally higher than the previous crash back to Earth the previous time.

Maybe things will be different but history implies it won’t be and the preliminary evidence and stats are showing us history might rhyme once more.

I’m still being patient but I might buy the right property over value because the interest rates are so low. An FHA or USDA loan on a turd with a miniscule down payment might pay off in the long run. I’m not going to get into a bidding war on some crap shack 2 hours from work but if I saw it sitting for months with a desperate seller I might play the role of patsy on a listing labeled (needs a lil tlc.)

I just saw such a thing in my local market. A crap shack 1 hour from town that was listed and didn’t sell for 6 months in 2019 for 175000 get listed in may for 325000. The listing was pulled after a month and I thought it was gone and sold. Came up again last week for 275000. I’d bite on it at 220000. 10 acres with a run down but liveable log cabin ain’t too shabby these days for a handyman like myself not trying to impress my neighbors.

Who knows. Gonna keep being patient but looking like I might go and hunt down some pre quals from a loan officer this fall or winter. Here’s hoping. Renting in town in an apartment when you’re a hermit that likes to tinker is a miserable life to lead. I don’t know how city folk do it. Sit around and watch TV or play video games I guess. City life is beyond awful for a misanthrope.

Of course the current runup is transitory. It will correct. And then it will continue on again. Does anyone here really believe that home prices will be less than they are now five years from now?

If you buy now and stay you won’t care if you value drops for a while. If you sell soon you lose. but if you can afford the home and stay for longer term you will win.

Biggest housing crash in history was when? Oh right, a short 12 years ago? And were are we now?

Trucker guy, I know you are in Spokane. We sold in Seattle and bought in Spokane.

If you can find anything that tickles your fancy for less than 300K then don’t quibble over a few thousand. Just get it and deal with PMI for a little while.

Spokane has cooled off a little, but I heard overall prices went up 34 percent. A major crash in values seems unlikely at this point and at some point you need to do what makes you happy and have a place to call home

Of course you will be reasonable and not overpay (too much). You will overpay a little. But in the big scheme of things sub 300 in Spokane is still Cheap!

Hate to break it to you, but Spokane gets annihilated in a real estate crash. To say it ain’t pretty is an understatement. There’s a reason you could buy a $50,000 house as recently as 2012.

300k in Spokane is cheap sure but in places like Bonners ferry or priest river it isn’t exactly a deal. Especially if it isn’t carrying much land. I don’t want to be anywhere near Spokane for a home. Or wa state for that matter. Even CDA and the valley down there is way way too crowded for my tastes.

In normal times the ultra secluded dumps are unmovable at low prices. Hence why I’m still waiting. I think the way overpriced rural dumps will collapse the hardest. Most people commute daily and wfh doesn’t work where mere electricity is scant.

When this all crashes, you’ll be able to buy 10 acres for a song in those areas.

Yep, most of these properties I see appraised for 30-70k 5 years ago. Most people don’t want to live in sasquatch land and have to plow snow for an hour before they can get to work with a 2 hour drive one way. Yet lots are trying to push off these (lovely mountain view off the grid private paradises with just some tlc needed.) For several hundred thousands.

Right there with you Trkr,, except for the last word…

SO challenged in a small city, trying to help take care of 90+ year old MIL,,,

In spite of the wonderful neighbors on almost all sides who either work hard now, or did enough to be OK now,, very mixed in all ways ”hood”,,, mostly worker bees, old and younger…

Good luck with the 10 acres plus situation,,, though it’s very clear from Wolf’s reporting that now is NOT the time to buy,,, just get ready to buy,,, eh?

Similar with vehicles,,, probably similar in all mkts.

Home building, Mic and Fast Food…

The common denominator is there is no import/export competition for these industries.

Money flows to where it is treated best.

The MIC, has no competition, it can’t be imported and there is always a willing buyer( US Taxpayer ).

Home building, nope this can’t really be imported either, why build anything else.

Fast food, why risk money on export commodities where there is competition.

Worker shortage? There are now 50 fast food restaurants per neighborhood where there used to be 2.

This is nothing, try 800k for a townhouse or 3bdr apartment, 1.3 Milion for a starter home.

While federal government talking about tackling inequality.

1.3M CAD for a starter home is only a little over 1M in USD. In LA, 1M single family will get you a in an area that is scary.

And, 800K CAD for a townhouse is a little more than 600K in USD. In LA, SF, NY, Boston, and Seattle, that is considered small money.

At what point does the Fed finally lift their foot from the QE/MBS/ZIRP gas pedal?

International investors bailed out of the Turkish stock market over less than what currently happening here, yet the madness continues because apparently there is no other way out.

When all these asset bubbles eventually blow up, what’s the fed going to do then?

promote gold back assets…..it will a complete circle…..

anyone thinking this will go on forever is pretty much clueless…I laugh at my estimated price…..

pink ponies and such are cool but this whole blow up of prices is all about the taxes coming….high taxes will lock in as your property goes down…..count on it

Anyone have thoughts or considerations on cashing out on the west coast and buying a home cash in the Midwest? Central Illinois has affordable real estate but somewhat high property taxes. If you own the home outright, then basically is your “rent” just the property taxes?

Anyone thinking about doing something similar, would love to hear your thoughts.

could be a dust bowl migration to great lakes…..

the west without a significant rain event over next 2 years will struggle to get water to people….who wants a home where there is no water?

there is a sliver of hope with el nino just beginning, surfers know weather better than any so called weather person……this drought will bring the west to its knees

Not really. I prefer to stay put and buy for 30 cents on the dollar where I actually want to live.

Get OUT of any state that does not have some sort of cap on raise of property taxes IMO…

Otherwise PG, you don’t have a chance to be safe long term when you pension or SS does not rise enough per year or per decade to get close to the rise of the taxes,

Makes one wonder in this crazy economy if houses prices will ever drop to normal levels if they increase interest rates? If supply will bring down the cost of a new build due to logistic issues solved? Or will the house price stabilize at these numbers even if inventory grows? What are your thoughts?

Probably a bit of everything. I do think the opportunity for disruptive innovation is happening with housing. Once they get 3D printing done right, it may be very game changing.

3D printed houses that are desirable and livable are multiple decades away. They also don’t solve the lack of land in desirable areas with good schools and medical care problem.

Rent where I live is near 3 grand for an outdated 3 bedroom crappy shack in the worst part of town. 4 grand for an okay house.

22% down on a 900,000 home – monthly is 4 grand at 3.1%…

72 grand guaranteed lost to renting after 2 years. Or 75 grand spent on principal after 5 years.

I’m paying 3,200 dollars to have some trees chopped in a couple of weeks. They are my trees, and I will get a couple of cords of wood out of it. Or I could have that go towards rent if I was still renting.

Owning is expensive, but cheaper than renting. Life is short, how long to wait? Make the best deal you can when you can and move on. Don’t look back.

Sounds like you grossly overpaid for a house. Condolences.

If the cost to own is only 33% more (in terms of payment), it seems like a good deal to me, especially when considering future rent increases. Where I live, cost to own is twice the rental price, so renting is a better deal. You really have to compare the cost of owning v. renting. Also, some people like the stability of owning a home and don’t care about missing other more lucrative wealth-building opportunities that may arise.

Sounds like you are a bitter renter. Condolences.

“22% down on a 900,000 home – monthly is 4 grand at 3.1%…

72 grand guaranteed lost to renting after 2 years. Or 75 grand spent on principal after 5 years.”

Hernando you forgot to factor in how much your $198,000 downpayment will grow to in those 5 years if you keep it in the market instead of putting it into the property. Average market returns would result in it growing to about $300K.

Student loans due, UI benefits ending, Moratoriums ending… September will be interesting

All Real Estate is local. But some areas seem to be trend setters. SF is one of them. What happens there seems to happen here in the Swamp a few months down the road. Flyover country is even farther behind, and always lags the trends on the coasts. What I hear on this post bears no resemblance to what is happening here in this urban area. DC RE has leveled off. Sales are down and there are no bidding wars in the city. Investors and homeowners with second homes are happy to unload their properties and get the hell out of dodge. The two factors are affordability and crime. I don’t see this changing in the near term.

True that first sentence SC: