And the utter craziness has begun to “decelerate” in some markets.

By Wolf Richter for WOLF STREET.

At least the Bank of Canada is officially acknowledging the craziness of the Canadian housing market, which has been deemed to be the second biggest housing bubble in the world, behind New Zealand, whose central bank also officially acknowledged its housing bubble, and stopped QE cold turkey, unlike the Fed, which has refused to officially acknowledge anything.

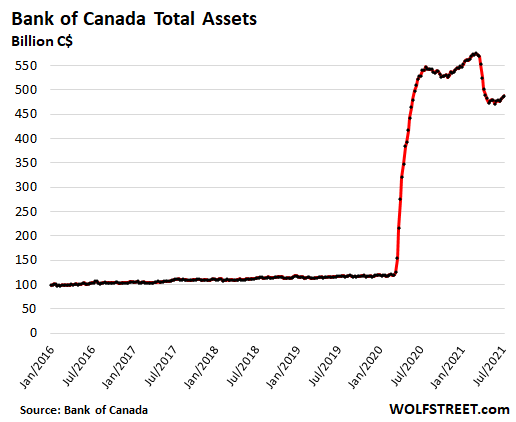

Starting last October, the Bank of Canada began the process of ending its asset purchases. Since then, it stopped buying mortgage-backed securities, unwound its holdings of repos and Treasury bills, and cut the amount of its weekly purchases of Government of Canada bonds for the third time, from C$5 billion per week last year to C$2 billion per week now. The assets on its balance sheet dropped from C$575 billion in March to C$487 billion as of last week. And in its pronouncements, the housing bubble looms large.

Housing markets react slowly, spread over years, and Canada’s housing market has started to react just a teeny-weeny bit. Home sales in June dropped by 8.4% from May, the third month in a row of declines, and inventory increased to 2.3 months’ supply, up from 2.1 months. And in a few markets, such as Greater Toronto, the historic price spikes have started to “decelerate,” as it’s now called, on a month-to-month basis, but they’re still crazy.

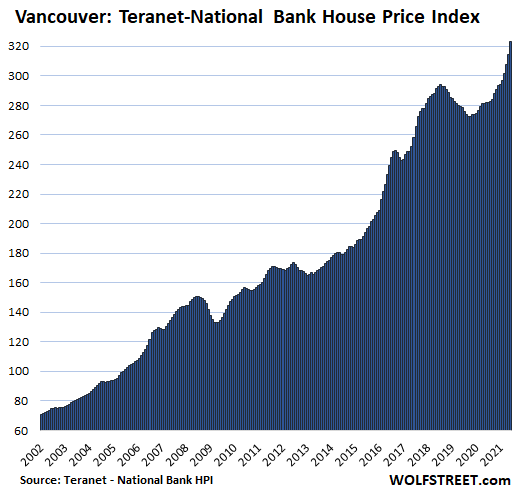

In Greater Vancouver, house prices jumped by 2.7% in June from May and are up 14.7% year-over-year, according to the Teranet-National Bank House Price Index today. Note how the Bank of Canada’s radical monetary policies starting in March 2020 turned around Vancouver’s housing bust that had already been under way for a couple of years:

The Teranet-National Bank House Price Index tracks prices of single-family houses through “sales pairs,” similar to the Case-Shiller Home Price Index in the US, comparing the price of a house that sold in the current month to the price of the same house when it sold previously. Since it tracks how many more Canadian dollars it takes to buy the same house over time, it is a measure of house price inflation.

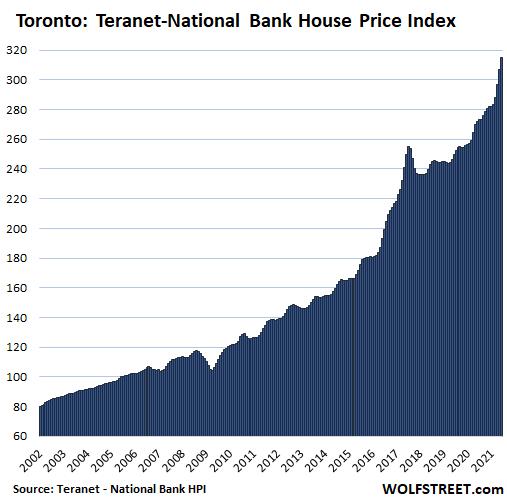

In the Greater Toronto Area, the house price spike “decelerated”: In June, the index jumped by 2.7% from May, but that crazy increase (annualized 32%!) was the slowest increase since March. Year-over-year, the index jumped by 15.9%. Note the decline in house prices in 2017, and the wavering that followed, until the BoC opened its vault:

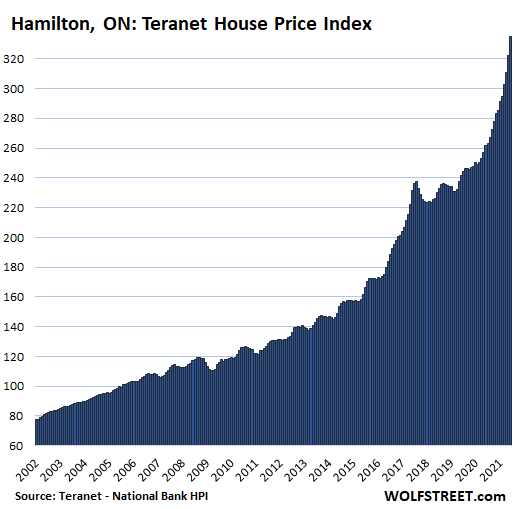

All charts here are on the same scale as the chart for Vancouver, with more white space appearing at the top as we go down the list, indicating the slower price increases over the past 20 years, compared to Vancouver.

In Hamilton, Ontario, house prices spiked by 3.8% in June from May, and by a mind-boggling 28.0% year-over-year, thank you Bank of Canada hallelujah. But now the BoC, with an eye on this exponential increase in house price inflation, is pulling back its radical monetary policies. Here too, the housing market had started to decline and waver in 2017, and it was the BoC’s pandemic policies that triggered this spike:

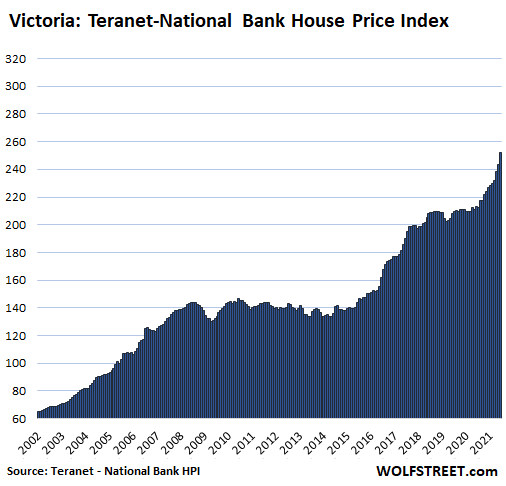

In Victoria, house prices spiked 2.7% in June and 18.5% year-over-year. The housing market had flattened in 2018 and stayed that way until the BoC opened its vault in March 2020:

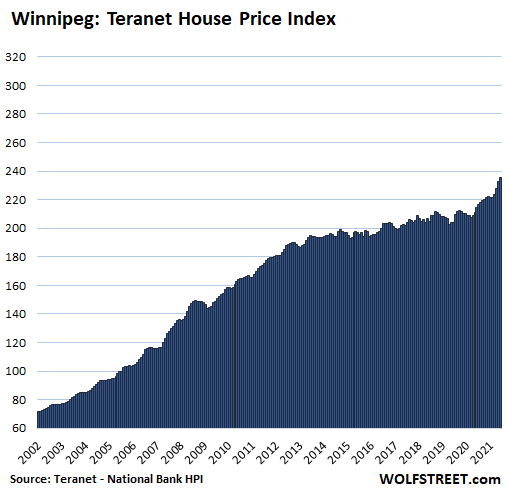

In Winnipeg, house prices jumped 1.3% for the month, the slowest increase since March, a sign of this “deceleration,” and are up 9.9% year-over-year. There too, house prices had flattened in 2013, but the BoC’s policies knocked them loose:

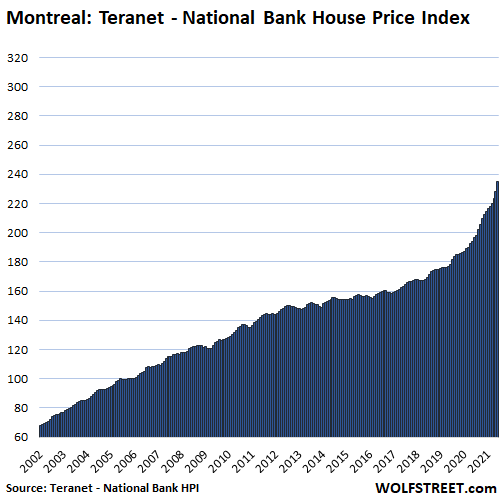

In Montreal, house prices jumped 2.8% for the month and 19.4% year-over-year:

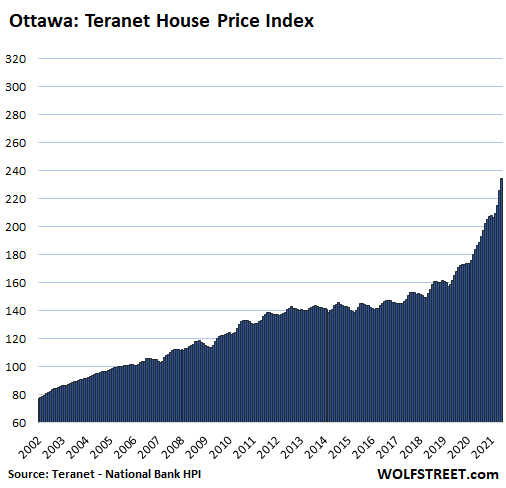

In Ottawa, house prices spiked by a whopping 4.0% for the month (48% annualized!) and by 25.8% year-over-year. But wait, that crazy 4.0% increase in June was down from the scary-crazy increase of 4.9% (59% annualized) in May:

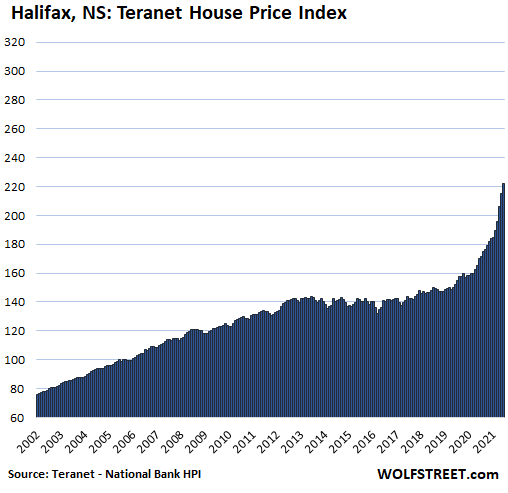

In Halifax, house prices spiked 3.5% in June, and as much of a whopper as that was, it was a deceleration from the 4.3% spike in May and the 5.4% spike in April. Year-over-year, prices have shot up by 30.8%:

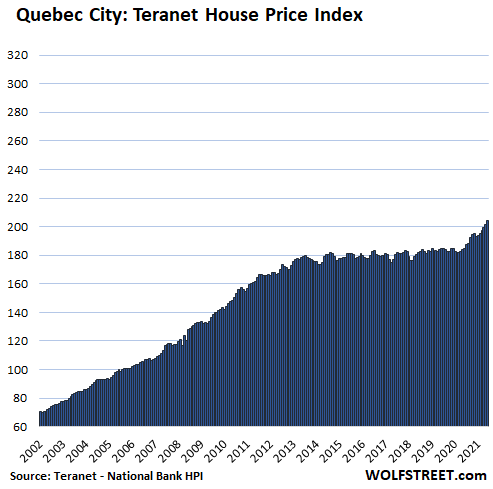

In Quebec City, house prices rose 1.3% for the month and by 10.8% year-over-year:

Calgary and Edmonton, the last two cities in the Teranet-National Bank House Price Index, are Canada’s oil-bust cities. In Calgary, house prices were still below where they’d been in 2014, and just above where they’d been in 2007; and the index for Edmonton remains substantially below the oil-boom peak of 2007. In recent years, some form of reasonability has moved in. And so neither one of the cities qualifies for this list of the most splendid housing bubbles in Canada.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think that qualifies as a smidgen.

“Housing markets react slowly, spread over years, and Canada’s housing market has started to react just a teeny-weeny bit. Home sales in June dropped by 8.4% from May…”

From BNNBloomberg;

Canadian home prices increased in June to mark the largest 12-month gain on record as prices climbed in all 11 markets, says the Teranet National Bank composite price index.

The index was up 16 per cent from June 2020, beating the 14.2 per cent rise of June 2017 that preceded the introduction of macroprudential measures designed to restrain home prices.

Prices were up 10 per cent or more in an unprecedented 90 per cent of 32 urban markets and up 30 per cent or more in 42 per cent of these markets.

People here will just keep trying to wish the housing crash into existence. The fundamentals have simply changed. Housing will never be as affordable as it was in the 1970s, at least not in desirable, supply-constrained areas.

As population increases, SFH will become a luxury.

I heard this same nonsense before the last crash – “new paradigms,” etc.

The main component of the price is land.

Has Canada run out?

You can’t even begin to explain the housing bubble with the Canadian pop increase, which with a birth rate at about 1.3 per thousand is below replacement. And puleese don’t cite immigration, it is nowhere near enough to explain it.

It’s very simple. When the cost of a mortgage at 2.5 % is below the rate of inflation at 3+ (this was before it hit 5+) even if housing appreciation was a mere 3 % per annum, it is riskless to buy RE. So everyone who can buy does buy, making RE scarcer, and a self-perpetuating cycle begins.

These things always end, and because this one has been the most violent, its end will be also.

If you weren’t there in 1982, this will be your first rodeo.

“It is different this time”

Sound Familiar?

“As population increases, SFH will become a luxury”

Are we living in a small country where there is no land? Marked is being controlled and manipulated and for sure there will be a crash..

Rule of 72 which is (actually just under 70) shows that top three charts have housing going up 7% plus for 20 years. That will be a problem when interest rates go the other way.

And yet the BOC still didnt just flat out stop the money printing. These bankers are just idiots.

Pull the support and let markets correct properly.

Canada

The Home you live in:

All Real Estate Gains on your sole Residence are TAX FREE..

Think about it…

It is the ONLY major loophole that the average middle class Canadian has.

It is a very big factor..

Which the Canadian Feds are looking to close by slapping capitol gains tax on sales of primary properties.

What fraction of Canadian citizens own and live in their homes, and has this proportion changed over the years?

Wondering how much of the price spike is due to capital flight from other countries, or other “investment” spending driving up prices for everyone though the owner doesn’t actually make year-round use of the house.

Wisdom,

Canadian home ownership is very very complicated with several factors that pushes the urge to buy instead of rent. The fear of missing out, tax incentives to buy as opposed to rent like being able to borrow from your RRSP (retirement plan) to repay later, and other incentives for first time buyers. Plus, the RE industry constantly hypes home ownership.

There has been a slight slight decline over the past few years in ownership, but the lack of affordable rentals still keeps home ownership more attractive than renting for a long term plan. Plus, our CPP is not as generous as US SS. So, outright ownership is important for retirement. A mitigating factor is our medical system as opposed to private health care and Medicare requiring supplementals.

I have read several studies about this topic and always conclude the most confusing factor is the decline of the dollars purchasing power relative to other markets besides RE. “It’s the number of zeros”….placeholders (not buyers :-)….that raises alarm with people, but is it really concerning? I don’t think it is. It is always relative.

The absolute numbers of homeowners by percentage has remained fairly stable for decades in Canada. But the purchase price numbers makes everything look scary scary scary. It always comes back did you buy in a rising market, just before a decline, and/or what will the interest rates do? Just like everywhere and always.

So, how does one compare the past with now, especially when market forces changes so much? Take Vancouver Island, specifically the Cowichan Valley which was my childhood home and a highly sought after place to buy, especially today. It has a modified Mediterranean climate with vinyards, farming, lots of recreation, and is just 30-40 miles from Victoria. In 1973, I remember my dad buying a starter home (shack) for a rental investment. It was an older bungalow, and needed work. He paid around 24K for it. That same year I bought my first truck, brand new for around $3500. So in that simple comparison, the starter home was about 7X what my truck cost. The same truck today would be of better quality, but something of similar size would start at $55,000 cdn. If you could find a similar quality bungalow of that tired rental, which would be still be considered a shack needing work by most readers on WS, the cost would be very very similar at 7-8X the price of the small truck used in the example.

What hasn’t kept up is wages. Then, I was working as a carpenter apprentice making between $6-7 dollars per hour. I guarantee you that an apprentice does not make $40-$50 dollars today, not even close. With Globalisation there has been a downward pressure on manufacturing wages, which has filtered throughout the economy and negatively affected all wage earners. In the past we had booming highly paid forestry jobs. Today? Gone for the most part just like the US Rust Belt jobs. This has forced a tremendous number of people into tech and commerce careers, namely in Toronto, Vancouver, Victoria…etc etc. Thus, their housing costs have skyrocketed.

I have a friend with 6 kids. 3 are now RE agents, one is a carpenter, and another is in the RCMP. The last works in business. The dad and grandparents were in forestry. My fisherman buddy has a son who is a computer scientist type in Toronto. Another logger buddy has a son in London in commerce. etc. England, not London Ontario.

Price spikes spread everywhere:

People younger and younger these days sell out of the city and move to places like where I now live, driving up our prices as well. Add to that fibre optic connectivity, WFH due to Covid, low interest rates, etc, prices are climbing everywhere, not as much as in the major centres, but still under pressure. Everywhere.

I have been raised to believe, and (like all indoctrinated people :-) continue to believe, that the path to security lies in home ownership. Also, that the path to wealth lies in property (land) ownership. It was true in 1973, and is still true today. It is also true that if you are not born wealthy, you cannot have it all when you wish. You have to let go of some things to buy that first house. Pay the mortgage but eat at home. Pay the mortgage but do a staycation. Pay the mortgage, but drive a clunker. etc etc. If you do that, housing is still affordable for almost anyone. Maybe not in Vancouver or Toronto unless you earn big money, but certainly in many many fine places to live. My son is 37 and owns two homes, (with mortgages), but rents pay for everything but $1000 per month. This includes taxes and insurance. For the $1000 he gets to stay in his basement suite which suits him just fine. My daughter is just renovating her home. She is 41. The cost of the reno is less than the RE fees if they were to move to a bigger place to match the family. The house was built 70 years ago and is on its third update. They will soon have it paid for and will be retiring by age 55. They managed to buy the place by sacrifice, fixing up a tired townhouse, and using that profit as a down payment on the house…..15 years ago.

3 of your friends 6 kids are real estate agents and you don’t think there’s a bubble in Canada Paulo? Let’s think here.

Point taken. Home ownership can lead to financial stability if a home is kept over a long period of time, but I wouldn’t say it’s for everyone.

At this time, I don’t think home ownership makes sense for people who want to build maximum wealth. Housing appreciation in the future will be limited given the drastic price run we’ve seen, and the stock market is likely to crash sometime in the next few years, if not weeks. This everything bubble looks like a once-in-a-lifetime scenario, and there may be a HUGE opportunity cost to locking up your money (and your future money, assuming a mortgage is taken out) in a low-appreciation asset for decades.

Liquid money invested at opportune times can grow 10x in a short period.

Buying a home with a big mortgage is akin to putting all your eggs in one basket. It may be a reasonable stable basket, but it’s no high flyer.

Then you’ll remember in the mid-late ‘90’s the CMHC held 25% of the available real estate listings on Vancouver Island and property values declined 25% on average, and more when other factors were considered.

Values did not begin recovery until ~2001.

The future of owning a home is very different from the past.

Over the past 40 years, there were two megatrends. One was the increase in 2 income families. That trend has either ended or even reversed a little. As women entered the working world, there were two incomes to support higher home prices. That really drove home prices in the late 1900’s.

The second great trend was the decrease in interest rates. That is the really big trend that allowed home prices to keep moving higher.

It is very possible that interest rates reverse themselves and head much higher at some point in the future. It is very hard to see mortgage rates headed much lower. When that happens, the real estate markets will begin a long downward trend. And home ownership will turn out to the foundation for foreclosure and wiping out equity, not long term prosperity.

The big problem for every borrower, whether it be home owners or governments, is that they have become accustomed to these very low interest rates and the low payments that are a result. This is pure insanity.

The world markets are all interlinked and if the BOJ stops buying assets in Japan, it stops crowding out investors in that market and will after a period of time impact every other market. If Europe and Japan and China all start to raise rates and pull back the support at the same time, then that alone will tighten the US markets.

Everything is a big charade now. The endless stimulus money is crazy and it is still working its way through our system. But the ability to keep this money flowing is very precarious. The whole thing is built on quicksand.

Its about 70 percent but all the generations after generation X got shut completely out of the hosing market and none of them can even afford rent so the 70 figure should drop unless everyone sells to the Chinese and the Chinese take all of Canada.

I wonder how much of this manic increase in prices is generated by wealthy immigrants, esp. B.C.

The last 18 months? None. Guess why (for 10 pts). Hint, the border reopens on Sept 7th to intl travelers. :-)

Plus, current BC Govt has stopped casino money laundering which had been endemic until 2 years ago.

The biggest problem is the low interest rates and need to export to US market. If US rates are low, ours has to be as low or lower. Otherwise, our dollar rises and exports drop. We are an export commodity economy with some tech added on.

I figured that they could buy remotely.

Absolutely! Using wire transfers, online showing, hiring inspection service, “docusign” for contracts. That’s what we did when we bought our current home 5 years ago. No need to be there in person.

That’s also the way I sold my home in California years ago as I was living in Texas at the time.

You definitely can buy virtually, however, the last year has proven that the stats are telling the truth. The purported rises due to immigration (once you get rid of the money laundering a couple of years ago) is too small of a % to blow the bubble. This is definitely us doing it to ourselves and regardless of the stagflation that has been occurring for decades. Paulo is hitting the nail on the head about price increases but wages not following suit. To give you an idea of how bad it is. I considered picking up an equivalent job to one that I held around 20 years ago. I couldn’t justify it given that the wage has only gone up by $4 per hour during 2 decades! Twenty years ago a decent starter home was around $250,000. That same starter home today is worth well over $1,000,000! Pretty sure none of us has to do the math to know exactly how insane that is or the problematic fruit it’s bearing.

Outside Toronto my folks bought a place 40 years ago. Houses now all in the $2 million plus range. Every one of their adjacent neighbours is now Chinese. Often houses bought for Mom to stay in Canada, kids to go to school and dad stays in China.

Newest is house now renting for $9000/mth for 3 kids and a guardian to go to school (private at $20,000 a year+ each). Chinese of course.

This DOES push prices up!

I can tell you with 100 percent certainty its the local Chinese who drive the home prices skyward. The Canadian government never addresses this issue. Also in some cases a local Chinese will buy for a foreign Chinese but its the Chinese locals who drive home prices. What Americans can’t grasp is the fact that price doesn’t matter to a Chinese so the concept of something being overpriced doesn’t factor into things up in Canada.

Does price matter to Local Italians, Tony?

Last I saw, the Los Angeles metro Case Shiller index was north of 338 … higher than any of the Canadian metros.

Canada has nothing on Los Angeles.

Yes, LA so far is still the top. Hamilton is at 335. LA is at 339 most recent CS. But Hamilton is rising faster than LA and at the current pace will likely surpass LA in a few months :-]

At current rate it will surpass all real estate in the world in a few years.

To the moon!

I don’t think that’s right.

The Case-Shiller indexes are baselined at 100 in 2000 whereas this Canadian index seems to be baselined at 100 in 2006.

So Vancouver and Toronto at least seem to have seen much bigger gains over the last 2 decades than any US cities (LA, San Diego, Seattle etc.).

So according to the official website of Teranet-National bank house price index:

the index is actually baselined at June 2005 = 100

but the overall point of Vancouver, Toronto etc. having bigger bubbles than anywhere in US is still valid.

You’re right! Thanks for looking it up.

Oh … Canadian markets have a different index with a different algorithm. So, they are not comparable. I would guess the Canadian methodology more aggressively states appreciation. I am making this assumption since I know someone who owns a home in Toronto, and it is only up 4x since they bought it 30 years ago …

Of course, you have to adjust for currency … CAD appreciation is worth less than USD appreciation … that takes a chunk away.

So who would actually want to move to Hamilton? I have always wondered why anyone would live in Hamilton if they did not have to? It’s a dying steel town. The winters suck and summer is worse. Snow, mud, humidity, and crime.

Paulo,

Look, I live in San Francisco, and love it, and there are commenters here who swear up and down that they would never even visit that hell hole, ever. So you know, it just kind of depends…

Hamilton hasn’t been much of a steel town for a long time. The area covered by the index actually is pretty suburban and has been growing economically in lock-step with the Toronto suburbs in general. Your list of alleged ills boils down to preferring Vancouver Island to southern Ontario and that is definitely not for everyone. I could list quite a few negative stereotypes about just about anywhere, and if that was all that mattered, no one would live anywhere.

It’s called city mouse, country mouse. Unlike Pauio, I’m kind of stuck between the two. I live in Nanaimo on central Van Isle which gives about as close to a blend as you can find. There is pretty serious wilderness a ten- minute drive and then a 20 minute walk from a shopping center. Love it. But Nanaimo is not REALLY a city. The hundred thou pop are along a 14 mile long, one mile string of unconnected ‘towns’. ‘Downtown’ is a block long about a third vacant. Residents brag about never going there.

So for the city ‘fix’ it’s off to Victoria, which has a big vibrant downtown, little shops, a Chinatown, old buildings, etc. But after about two days there I start thinking how nice it would be to go for a walk not in a park with all kinds of joggers, benches, SIGNS, etc. etc.

The places the locals flock to for an outdoors ex are kind of pathetic. My bro who lives in Vic has about had it. Thinking of moving to Nam. But if he does where will I get my city fix?

LOL. Yey Hamilton is now a suburb of TO and effectively has been for a few years. If you don’t watch closely you will miss the sign saying your now in Hamilton. For over 10 years, a lot of folks chose Hamilton due to the RE prices being significantly lower and commuted often 1 to 2 hours each way. Compare that to Nick’s times of any more than a 10-15 minute drive and it’s too far and a 1.5 hr trip down to Victoria is considered an overnighter (and, LOL, he isn’t even dealing with the ferries!). You’re perception of commuting and what you consider a good place to live is very community dependent.

I haven’t been tracking Hamilton’s RE but I have been on Van Isle and the gap in cost between Victoria and Nam has been significantly closing, if not gone. Based on the news, it sounds like that may have occurred in Hamilton as well. Without truly ending up in the boonies, changing RE location is doing very little.

According to the latest numbers from realtor boards, the LA Metro is appreciating about 4% more than Hamilton … YoY. We will see if Case Shiller agrees.

Canadians at best may get a 2 percent wage increase but most get no wage increase. There’s no jobs except areas where no one can afford the residential rents so basically there’s no jobs at all.

Even before this last years 30-40% run up, Vancouver was having difficulty obtaining and retaining teachers, PO’s, paramedics, firefighters, etc. because the cost of living vs wage is so out of wack. Housing is one of the worst culperts in this and it is causing real problems. JT’s latest affordable housing optic isn’t going to put a dent in that problem. Only a serious correction to crash will.

Meanwhile, in podunk unincorporated North Carolina, this doublewide, on a $65,000 lot, came on the market at 7 X assessed value. This is beyond inflation. It’s more like Monopoly money:

And this “bargain” just hit the market in West LA.

This is insanity.

Can you check the Baja housing market. Recent changes to the laws make US ownership more reliable. I browsed the internet for properties. Quite a bit of land, for (developments). Baja is a popular destination for Mexican nationals. Lots of beach front property. See what the cross border inflation is compared to Canada. I would move to Canada but the weathers too hot :)

MaxOviedoFLA

Spent some time in LA over the last few years. Spent some time in Vancouver about 18 months ago. Many reasons why Vancouver would win my vote for places to live vs. LA. However, I will likely just stay in Florida.

Since the drop in interest rates anyone buying a house with a mortgage, even though the price is 20% more, will pay the same or less each month. Cash buyers, however, got inflation squeezed! Unless liar loans become norm as they did in the runup to the 2008 housing collapse, affordability will dictate pricing! Hey, if interest rates go negative house price will jump another 10 to 20% higher.

Wolf, the house prices spiked many months after BoC stopped buying MBS, after cutting qe from 5billion a month to 3billion. The drop to 2 billion/mo printing of fake fiat isn’t the reason the market has topped, it’s affordability due to top being reached at the interest rate drop in 2020!

One thing about houses and housing markets everywhere, forever: nobody’s ever been able to afford one, even when they were 10,000 bucks.

Nobody has ever been able to afford rent, either.

Reading old newspapers can be enlightening, and make you realize nothing really changes.

Utterly, totally wrong.

Income to house price ratios in the 1970s were 2 or less to 1, vs. the 6 to 10 (or more) today.

I’m fairly certain relative tax burdens were lower as well. Food costs were probably relatively higher.

Exactly. Historically, in my area, houses were 2x yearly household income. Then they spiked to 10 with the FED’s low rate and QE infinity nonsense.

And sales have been booming for years, the point of this article.

Are you sure. I’m buying a very nice house tomorrow for 125,000euros. My salary was 68,000e 2019 and 63,000e 2020. Bike path directly to work, 30m from the lake, no house’s between the house and lake, 200m to 2 grocery stores. Ski trail 30m away, hockey rink 100m away. I wasn’t going to buy but my landlord wants to sell the rental I’m in. Fixed 10year at .72 percent. It just depends on how the government views housing, if they really want to have people live a normal life then they allow zoning and development to reflect the needs of the area. Interest rates don’t affect housing when the government views housing as a basic necessity rather than an investment.

And where would this be? Southern Europe, Portugal, Greece?

Sounds like the Nordics, most likely sweden or western part of Finland judging on the nickname ’gris’ which means pig in Swedish :)

Greg,

Canada doesn’t have a widely used, standard 30-year-fixed rate mortgage like the US has. Mortgages are either variable rate and adjust at certain intervals, such as annually; or they’re “fixed rate” for five years and then need to be refinanced at the new rate in effect at the time. There is considerable interest-rate risk for Canadian borrowers.

Is it correct that the US is fairly unique in its fixed rate mortgage product?

I am curious on how the bank sustains this churn through lower rates, granted it’s unique.

MCH

how the bank sustains this churn through lower rates?

It doesn’t. Banks have to either lever higher and take more risk, take in more reserves, or cut costs.

Sell a 30-year bond to cover a 30-year mortgage with a spread of 1%?

I don’t think that the 30-year fixed rate mortgage would exist as primary mortgage without government support.

Do you think the idea is to get the churn going with variations in the rates? I mean if you look at an amortization schedule, the interest part of the payment is in front, the principle is toward the end of the schedule. So, if you refi at a lower rate, it’s actually not to bad for the bank who now gets another bite of more interest up front.

Although that game has its limits given where we are today with mortgage rates.

Europe does long term fixed rate.

Many of the mortgages in Canada and the commonwealth are interest only mortgages. Prices were rising so fast for the last 5-10 years borrowers didn’t have a need to pay down principal to gain equity. Another feature of those markets.

Not really true at all. There is one company that now offers one, but they were phased out in 2010 after what happened in the GFC. They are very seldom used and occupies a niche market for those with sporadic incomes. It operates like a HELOC and allows certain buyers to get in to the housing market, and pay down other higher interest rate debts or make other investments. They can only go to 65% of the amount required.

I know lots of home buyers and know many in RE and have never heard of anyone getting this type of mortgage. It would be like number last to never on options.

There are virtually no interest-only mortgages up here. As in none. There are interest-only HEKOCs however. And plenty of them.

And the economy destructive 2008 rate rise, occupy wallstreet and the brutal housing collapse has been understood by BoC and Fed reserve! Rate hikes laeading to a housing price collapse and followed by a heavy recession will not be fomented by central banks interest rate hikes. Printing press going Brrrrrh to inflate assets while many in society will be thrown under the inflationary bus–but not home owners!

Why is it a risk? Only if idiots like greenspan are in control!

Wolf’s point has huge implications and impacts for the Canadian market. Additionally, all mortgages are recourse which creates additional risk and blow back. It makes our bubble even more ludicrous.

Just to clarify:

In the US, there are only 12 states were mortgages are non-recourse (including California). In the remaining 38 states (including Florida and Texas) and DC, mortgages are full-recourse.

In Canada, mortgages are full-recourse except in two provinces that have non-recourse mortgages but with big limitations: Alberta and Saskatchewan.

https://wolfstreet.com/2018/06/20/us-style-housing-bust-mortgage-crisis-in-canada-australia-recourse-non-recourse/

Thanks Wolf. I knew that recourse vs non recourse mortgages are state dependent but wasn’t sure how what the balance was or whom. Given that some of the recourse states had some of the most significant run ups, particularly with lots of immigration from non recourse states, any thoughts on what the implications maybe?

As for Alberta, huh! Okay, did not know that but suspect that there is more to the story. During the bust in the ’80’s a lot of folks tried to not walk way. Their lifestyle was decimated if they could manage the 18-19% interest rates and a lot of people got hit with it due to our 1-5 year renewals. If you couldn’t manage and if your mortgage was @ value or underwater with an 18-19% interest rate attached, a lot of people sold the property for $1. In fact, they were know as dollar sales. These folks basically lost everything and it severly impacted their quality of life on a go forward basis. The only ones that I remember walking away were those that had nothing left to loose. After all, you can’t get blood/money from a stone. The vast majority I knew, it would have been easier to mail the keys back but they didn’t which makes me think that either they were too ethical or that there were consequences of some type even if they couldn’t be on the hook for the difference on the mortgage.

I will talk to some of the insolvency boys to see if they have any thoughts or insight.

The problem in Canada is housing never tanked in 2008 like the USA. For most, housing has being a steady growth area above bond rate for 20+ years. I hear frequently the adage “house prices never go down” from real estate agents and investors. Its ingrained now, that you leverage to the max to buy anything you can. At nearly 10% of GDP it is also “too big to fail”

Foreign buyers will come to their rescue!!!

MB

Heard somewhere recently (Keiser??) Chinese citizens have ‘savings’ of $57 Trn. They’re great savers with memory of poverty. Their Govt apparently restricts overseas investment to $50k per head, but an increase to $150k is on the cards. We could all end up renting from a Chinese landlord.

I’m trying to flog them the Forth Bridge but they’re far too smart to buy that.

You’ve got highly skilled tech workers to Vancouver/Toronto, thousands of Hongkongers fleeing China democracy crackdown, top immigrant group are actually Indians (and then Chinese of course), and the official government target of 400K immigrants per year – which on a proportional basis is nearly 3.5x more than the US – the immigration rate should probably be even higher.

There is a reason why Canada was ranked best country in the world this year.

I don’t see a housing crash ever happening (a correction? sure).

I can see a future where California and Western Canada become a part of the Greater Bay Area (China, Taiwan, Hong Kong, Japan and South Korea).

Make no mistake about it the Chinese will take all of America and all of Canada. Its just a matter of time if no safeguards are put into place. Canada has none and never addresses the root cause of the housing fiasco which is the Chinese.

With what army?

Why don’t Canadian cities just introduce a punitive confiscatory property tax on non-resident homeowners e.g. 5-10% per year of current property valuation?

This seems to be a big new source of revenue with no downside since the taxpayers don’t get to vote in local elections since they are not residents.

Am I missing something?

A none residence tax was introduced in BC a couple of years ago. It didn’t do too much since it’s not actually the source of the problem.

There is an empty home tax in British Columbia and Ontario just brought in a 1 percent empty home tax in this years budget. Of course it doesn’t do anything as the Chinese just keep on buying up everything. The fallacy is everyone blames the foreign Chinese but its actually the local Chinese that drive prices skyward. What happens here is one local will buy up all the new townhouses developments or new apartment complexes. Remember many of the local Chinese have a net worth well over a billion Canadian dollars but a lot of their money is spread around the world so they don’t show up as Canadian billionaires.

The historically low interest rates courtesy of our elected officals and the completely irrational behaviour by Canadians has a lot to do with this.

In California, I have heard that for years and particularly now due to the pandemic, there has still been a huge inventory of homes which the banks are not foreclosing upon which means that the housing recovery is a mirage. When the banks eventually start mass foreclosures, the housing prices will tank when the foreclosure sales result in thousands of homes being sold then at a reduced price or thereafter, (at least in California, after the banks have made a credit bid way above the true, FMV, to avoid booking a huge loss for a while, because they cannot get a deficiency judgment against residential buyers) to a later purchaser for a pittance.

They might want to make deals with financial players that can purchase real estate for fake, inflated values in exchange for lower interest rates loans or other perks. For example, apparently, certain major financial players have decided to acquire huge masses of real estate and become landlords. Those players would only buy such distressed real estate at a discount below FMV but might work with banks to disguise the low prices of such purchases.

I am not sure as to Canada. However, an article in ZeroHedge, “”Stunning Divergence”: Latest Bank Data Reveals Something Is Terminally Broken In The Financial System,” claims that the banks will be “forced” to suddenly lend out the sums that they are holding. I doubt that. The reverse repos are probably occurring because the banks do NOT want to risk more real estate loans in an inflated market.

The banks already are being bailed out by their privately owned, “Federal” Reserve of mortgage backed securities (“MBS”) to the tune of $2.3 trillion with $40 billion in MBS being bought by it each month, so they may not have an appetite to dive back into the inflated real estate market with their OWN money, particularly if they have an inventory of real estate loans that they cannot foreclose upon. Remember, the plan in 2008 was not for them to bear any losses on their real estate gambling: it was the ordinary investors, a.k.a., the dumb money or the suckers, who were supposed to lose everything.

The banksters were essentially bottling garbage, subprime loans (as accurately depicted in The Big Short, to sell to the dumb money (pensions and other gullible persons) for juicy fees and gambling on it with synthetic CDOs (now essentially Bespoke Tranch Opportunities) but they got caught still holding lots of that garbage when the market went south. They also gambled foolishly on those CDOs in the erroneous expectation that their “Fed” could prevent the RE collapsed.

Now, they are supposed to be forced to lend huge sums and bear those risks while being bailed out of prior stupid gambles? Fat chance.

I think that the reverse repos indicate that the banks may be expecting a stock market, real estate market, and bond market collapse, so they do not want to touch those areas. See “Jamie Dimon says JPMorgan is hoarding cash because ‘very good chance’ inflation is here to stay” in cnbc. It is true that bonds will decrease in price as interest rates rise due to inflation.

However, because of the federal interest payments, which will increase dramatically if treasuries have to be doubled at higher interest rates, the banksters “Fed” cannot allow interest rates to normalize. Thus, the bonds cannot decline in value a lot.

I think that it is more likely that a stock and real estate market crash would provide great opportunities to buy assets for a song, since the market for some assets often goes lower than its long term valuation (over corrects), so for a while, some assets can be bought for a song which will soon go up in value. That would also explain Wells Fargo’s recent closing of credit lines and willingness to offend so many of its customers by doing so. Hoarded cash will enable such purchases.

“In California, I have heard that for years and particularly now due to the pandemic, there has still been a huge inventory of homes which the banks are not foreclosing…”

Fake news. However, there are some mortgages in forbearance, but not as many as there are in the rest of the US.

“The banks already are being bailed out by…”

More fake news. Banks are swimming in profits and don’t need to be bailed out. The Fed created this environment for the banks to profit from, starting in 2009, and banks have been profiting from it.

And more fake news about MBS. The only MBS that the Fed buys are those that are guaranteed by the taxpayer. The Fed takes zero risk on those. If something goes wrong, the taxpayer is on the hook.

“I think that the reverse repos indicate that the banks may be expecting a stock market, real estate market, and bond market collapse,…”

More fake news. It’s money market funds with too much cash that are the primary user of the RRP. Fidelity on top.

Typo: Thus, by purchasing Fannie Mae and Freddie Mac (in unspecified amounts versus Ginnie Mae’s MBS from what I have seen on the Fed’s websites)

Correction: Thus, by purchasing Fannie Mae and Freddie Mac (agency) MBS (in unspecified amounts versus Ginnie Mae’s MBS from what I have seen on the Fed’s websites)

Clarification: Fannie Mae and Freddie Mac would only be in trouble if their guarantees of MBS resulted in their incurring liabilities of billions or trillions when and if that MBS went bad. Regardless whatever, other profits the banks are making, if you hold non-agency MBS, so you bear the entire loss from any depreciation of such MBS and the guarantors of your agency MBS (meaning Fannie Mae and Freddie Mac since Ginnie Mae IS federally guaranteed) may also become legally insolvent (absent yet another, federal government enacted bailout), will the losses from your MBS investments and gambling in BTOs (formerly called CDOs crush your profits dead?

I was always told how US banks operate using a thin shell of capital, like the shell covering an egg, which any significant decreases in the value of their investments (now BTO gambles also), could crush like any egg shell. Is that no longer the case? How?

Like fiction? Read balance sheets.

To the best of my knowledge only Cali has Prop 13

Back in the 70’s people got tired of that never-ending RE skyrocketing BS,which always led to increased property taxes and cancerous growth of government agencies.

Solution for non-Cali residents:

Everybody simultaneously sells his house to his neighbor across the street for $1

But it must be kept secret,carefully planned and precisely executed,like Landing in Normandy 6/6/44 or Dallas 11/22/63

Florida has a portable real estate tax rate. The rate of increase is limited and owners can also transfer equity/homestead to keep old rates, but I don’t remember exactly how it works.

I often visit South Side Chicago.Not because I am some kind of daredevil Erroll Flynn but because everybody else is even less “In like Flynn !!!” than I am ☺

Recently I bought a local newspaper and read how one woman’s property taxes skyrocketed from $2K to $20K in the past 20 years.Which is 90% of her pension from US Steel-she worked there 40 years as an accountant.

Property taxes are one of the two big differences between the US and the UK.(not sure about Canada.) In the US you can get 30 year mortgages (we can’t) but you also have massive property taxes. The biggest property tax anywhere in the UK is around £4000 and that would be for the most expensive of houses.( in the millions of ££££) I pay £1000 a year but I only have a small house worth about £200,000 or so.

Anthony,

Property taxes vary greatly between states and metro regions. One can’t lump them together.

I pay ~$2500 a year on a $450k home w/10 acres.

@Anthony

I heard that HM Liz the Deuce is exempt from property and all other taxes.

That’s something we all simple cotters must look up to and try to emulate.

Other Privileges of Nobility are even more important:

-carry arms

-wage private wars

-be judged only by the Court of One’s Peers…

Local governments in Canada love the constantly rising housing prices because the tax assessment keeps going up evey year bringing in more property taxes without having to raise property tax rates. This helps hide much of their fiscal mismanagement.

In Ontario, property assessments are nicely done by a so called independent provincial crown corporation, so people get mad at a faceless entity, instead of local majors. All by design!

That is so not true, Wes. Local Govt set the tax rates well before the new financial year, and list the percentage increase based on last years amount.

For example, this year our regional district raised taxes by 1.4% compared to last year. If the value of my house increased, the mil rate drops as the budget is determined by what the Govt needs to supply publicly announced services, and not what they rake in on a rising market.

Tax Rates (where I live)

By May 15 of each year, Council approves the annual tax rates bylaw on which property taxes are based. The rates are expressed as an amount per thousand dollars of assessed property value. For example, if the rate is 7.5000, property taxes would be $7.50 for each $1,000 of assessed value, and a home valued at $100,000 would pay $750 in property taxes for that year.

Annual Tax Notice

Tax notices are usually mailed out the third week of May each year, shortly after Council approves the tax rates bylaw. The tax notice shows the amount of property taxes due, and may include parcel taxes and user fees applicable to your property. The City also serves as the collector for other taxing bodies, such as

Provincial School Taxes

Strathcona Regional District

Comox-Strathcona Regional Hospital District

BC Assessment

Municipal Finance Authority

Paulo:

You live in BC!

I live in Ontario! I can only dream of property tax increases of 1.4%!

So do the companies who do reverse mortgages. The average Torontonian can’t afford their annual property tax so many of the older ones take out reverse mortgages because they’re too senile to sell and move to a place that costs less.

@The Real Tony,

My Ontario real-estate lawyer talk her elderly clients out of getting a reverse mortgage all the time, for 2 reasons:

• the interest rate is usually much higher than other secured-lending products, and

• after asking what they want the money for, she usually finds out that it’s to finance a temporary problem, but it’s a permanent solution.

If they still need some money, she recommends a line of credit, where the senior only pays interest on what they actually use, or to get a lower interest rate, a line of credit secured on the home (home-equity line of credit or “HELOC”).

I saw some article on CNN about how this recession was the shortest on record. Now that governments have seen that they can borrow money and hand it out to artificially increase GDP, maybe it’s time to remove government spending from GDP?

These clowns are addicted to money printing. The next hint of a downturn and they’re going to send out even more. Whodathunk Maxine Waters and Co. would ever be in control of a country’s currency? This lady couldn’t even count change from a $20 bill. We’re doomed.

Honestly, even if the money was borrowed, instead of printed from nothing, it would still be bad. Counting government spending into GDP is like embezzling from your company and counting that as income.

Waters is an example of what you get when you have universal franchise.

The Fed’s new mandate is a page out of Weimer Germany. Havenstein the country’s mad central banker who was quoted as saying the reason he was printing all the money was to maintain law and order. He said that if they stopped printing the country would descend into chaos. I think J Powel might be thinking the same thing.

Weimar Germany had 3% of global gold reserves in 1920 which declined to 1.3% by 1923 at the end of their inflationary spiral. The US has 60%+ of global reserves and its allies have another 35%. As long as the US and Central Banks of Allies print in tandem there is no possibility of a Weimar collapse.

To stimulate home ownership, they reduce the mortgage, which increases housing prices within a few months, which makes it harder for anybody in the future to buy a home.

It’s rewarding one generation of home buyers to the detriment of another generation.

Any government that condones this type of generational theft is beholden to special interests and does not legitimately serve its population.

I’ve long argued that current policies are to benefit the asset owning portion of the Boomers at the expense of everyone else.

Just wait until they’re no longer in charge.

Tons of baby boomers passing homes to children no house issues

From Mrs Swamp Creature

Anyone buying a home now at these inflated prices will lose money over the next few years unless we go into hyperinflation which is unlikely. Housing affordability has now reached a peak and the only direction from here on is south. When interest rates normalize the house payments will go up for the same price home which will result in a decline in the market/selling price of most homes. This happened in 1981 and 1982 in Capital Hill a very desirable area in the Swamp and will happen again nationwide. A lot of homeowners will be underwater just like they were during the GFC but for a different reason. Banks are not doing what they did in 2005/2006/2007. They would rather not make these loans. There is no pressure on appraisers to hit values and make deals. Those who think this is like 2005/2006/2007 are way off. The lemmings are heading for slaughter but they need to look in the mirror before shifting the blame to someone else.

This time is different

The prices have reached permanent high plateau

Worst case is stagflation

Up in Canada its a little different. Price doesn’t factor into anything as the Chinese will buy up all the homes no matter what the price is and the Pakistani’s and Punjabs always copy what the Chinese do. If it doesn’t work out for the Paki’s and the Punjabs they just leave Canada and go back home after losing their homes. This is what happened last time in the 1987 to 1990 timeframe.

From Mrs Swamp

One thing I’ve noticed lately is a lot of RE deals are starting to kick out. This is the only similarity to 2005/2006/2007. Buyers are getting cold feet. They hear the headlines in the media about “Delta Variants” and potential lockdowns and are starting to run for the exits. They fear they may not even have a job to pay the mortgage. Lenders like Wells Fargo are cutting out personal credit lines and raising down payment requirements. Wells Fargo could care less if they even make another mortgage loan in this environment. Afforability is the elephant in the room. Prices have gotten above the amount that people can afford or are willing to pay. The only direction now for RE is no appreciation or south.

1) Canada GDP = $512.4B. Canada M2 = $1,537B/1.275 = $1.2T.

2) Canada M2 velocity ; 512.4/1,205 = 0.43.

3) China GDP = $14.7T. China M2 =$193.55T/6.49 = $29.827T.

4) China M2 velocity = 14.7/8.57 = 0.49

5) US Real GDP = $19.086T. US Real M2 (!) = $7.585T.

6) US real M2 Velocity =19.086/7.585 = 2.5.

7) US GDP = $22.06$. US M2 = $20.37T.

8) US M2 velocity = 22.06/20.37 = 1.08.

9) Canada money stock is twice as much as US, relative to it’s GDP,

thanks to the foreign RE boom and higher WTI.

10) Canada deflated currency peaked in Mar 2020 at USD/CAD =1.5. Currently @1.275.

11) If SPX tank, USD/CAD might breached the previous high.

12) But after US shale deflate, Canada WCS will fly.

Canada’s GDP last year was about 1.6 Trillion US, so your numbers don’t fly. In fact, using the rest of your calculation, Canada’s per capita money stock is less than the US.

Wolf…

Pardon me if this has been discussed…

did you see the PBS special on “The Power of the Federal Reserve”?

Fisher, former Fed Gov said a remarkable thing…

“When you drive interest rates down all the way out IT FORCES INVESTORS into taking bigger steps on the risk spectrum.” Fisher

8:40 mark

FRONTLINE | The Power of the Fed | Season 2021 | Episode 14 | PBS

So the Fed deliberately conducted a “cattle drive”. I wonder who got the word first. They focused on the market, not the economy. Central planning and insider gamesmanship go hand in hand.

And I guess this is the Fed’s fourth mandate which is a direct negation of the third mandate “promote moderate long term interest rates”…(not extreme)

I guess the Fed somehow acquired the power to rewrite the Federal Reserve Act and their mandates.

The FED works for the wealthy. Period. All we can do is accept that and try to navigate through life accordingly. I am cutting spending TO THE BONE, and saving everything I earn. I am betting that the FED can’t continue to do what they’re doing forever, and that there’s going to be an asset price crash.

When the Federal Reserve Act was being debated in Congress, Elihu Root said ‘if you pass this legislation you will have created an engine of inflation’. Since then it’s been boom and bust, with the first cycle 1918-1921, the next about 1924-1930 with land/property speculation etc, and the 2021 dollar worth 2 cents compared to 1913.

And the latest mandate of the Fed includes something about social equity.

Can’t speak as to the housing market for the snow Mexicans but locally I’m seeing the market start to slow somewhat here in fervent North Idaho. The crap shacks are actually taking price cuts and sitting, the days on market have jumped substantially and goofy little metrics like the buyer/seller ratio on realtor.com have swing to 100% buyer in most counties now.

I was looking at the area my parents live in and the unbelievable run up in housing is just as aggressive there as most other places. I’m talking 2-3x price increase in a matter of 5 years.

Here’s hoping to interest rate hikes at some point soon. I don’t think they’d have to raise them much at this point to take the wind out of the sails. 30/yr mortgages going to 5-6% would probably devastate the market for the financially unfit but for savers who use money responsibly, well they’d have a windfall if they were in the market for homes.

Will be interesting where the market would be when the FED and mortgage companies increase the rates. Mortgages @ 6% would result in a reduction in value and price. Wouldn’t that equally upset homeowners who are no longer valued at $MM? These are so strange times. Nutty as an acorn tree. Wait and see is about all we can do as there is no way to fight the system

I expect to see people get rather upset when their $900k home is only valued at $690k. The FED will have to pay for that in the comments

There is no housing bubble unless it burst or crashes.

Housing bubble exists only in the hindsight

I don’t think FEd would ever raise rates.

Before raising rates they need to taper down the bond purchase

The housing “unwind” will be slow and may only be a plateau which flattens for awhile, regardless of when tapering of MBS occurs. Crash unlikely.

LOL yeah okay. This time is different.

It’s amazing the home price increases have been allowed to go this far without a serious revolt. Instead of anger, the response has been FOMO.

Central banks have abused their discretion and their mandates. The job of a central bank is to provide liquidity in times of crisis, not function as an unelected treasury administration with power to tax via inflation, thereby re-allocating wealth from savers to spenders, renters to home owners, prudent to speculators, and from young to old.

‘Starting last October, the Bank of Canada began the process of ending its asset purchases’

This has more to do with the fact that the Finance Ministry and the BOC colluded to ignore the statutes in the Bank of Canada Act (Section 18, sub section J) that gives a hard cap on debt monetization at 33% of current fiscal year revenue. Currently for fiscal year 2020 the BOC monetized 300% of that cap. There is some wiggle room, as in estimated revenue and short term purchases that are sold back to private investors. This is actually why the BOC has ‘scaled back’, they are still in violation but are hoping no one noticed. Too bad, one of the only sane members of Parliament Pierre Poilievre, has called a point of privilege and is now demanding a full independent audit and report to Parliament to expose that unlawful collusion.

The BOC couldn’t give a frig about ‘housing bubbles’ or double digit consumer inflation, they are all fascists controlled by a fascist/communist regime operating under the great reset order issued by their masters at the WEF.

The Bank of Canada does care because if the price of homes goes too high Trudeau’s immigration plan is shot. Virtually none of the immigrants can afford the residential rents and the rents are about double what minimum wage pays in a year. So the Bank of Canada will be forced to do everything to bring down the price of homes so rents fall.

Tony, sorry…but your comment makes no sense!

On another note, Winky’s point is that the government (in collusion with the Bank of Canada) has nonchalantly broken the law by taking on ~3x more debt than legally able…thereby creating a serious “taxation without representation” issue.

Also, just want to throw this into the mix: the government of Canada has no gold reserves…zero.

Additionally, the Bank of Canada has the power (and arguably, the obligation) to print debt-free currency.

And lastly, private property isn’t even a real thing in Canada…legally. Nowhere are private property rights for individuals even hinted at or mentioned in its highest law–the Canadian Constitution

…incidentally, the Constitution re-written and enacted by Trudeau the 1st.

In Edmonton, Alberta Canada resale townhouses and resale apartments are selling at half the price of what they sold for way back in the summer of 2007 15 years ago. These are the identical townhouses and apartments that sold in 2007. Still a lot of foreclosures, unlike Americans Canadians never migrated out of the province of Ontario to Alberta like the Americans did from California to Texas. Canadians tend to be behind the 8 ball when it comes to rational thinking.

Its about 70 percent but all the generations after generation X got shut completely out of the hosing market and none of them can even afford rent so the 70 figure should drop unless everyone sells to the Chinese and the Chinese take all of Canada.

Western nations were happier when houses were homes to raise families in, rather than investments. Society has degenerated.

What is happening in Canada is a huge experiment.

The main cost of housing is land as most is location based, that is to say buying the same area of land in the middle of Toronto is far, far more than in the middle of a field in the middle of nowhere.

Canada has very low population density. They are essentially looking to farm their population by insisting that we can’t build, even if we can see land as far as the horizon, in every direction. Just because it doesn’t have “planning permission”.

Living here now is basically a huge pain. You either own a house already, or you do not. If you do not, you can’t work your way out. Why? High taxes. If you earn 200k you see nearly half go in tax. So how can you purchase a 1mm CAD home? Yet on a street of homes valued at $1mm if you knocked on every door for 1,000 homes, you will find most residents never came close to 200k household income in their lives.

Here is a graph of several G7 since 2000:

https://i.imgur.com/N0ebZIG.png

Canada has moved from a place where working hard saw your life improve to near-feudal.

I came here for a better life for my kids, but now they are going to be in a nightmare.

It’s a whole new paradigm in the last year or so. The objective of the federal government (as with most such governments in the Western world right now) is to turn Canada into 1980s East Germany without the fun. We’re about halfway there, and people keep voting for it, so I suppose that’s what they want.

People on our street recently bought a house in Nova Scotia. A lot of big city people are doing that – cashing out and buying cheap (80% cheaper) down East. After buying it they had to apply for permission to move there: interprovincial borders closed, with checkpoints. Their application was refused and they were told to reapply later. They moved into temporary rental accommodation here, but we haven’t heard from them for a while, so I hope they got permission to move.

Something about a virus that you have a 99.93% chance of Not dying from in Canada. Nova Scotia: 99.99% chance of Not dying. Average age of death: 78. 93 deaths in a year and a half in a population of under a million.

…

About ‘on a street of homes’, the common reaction for the long term residents is that they couldn’t afford to buy there. Strangely, that was a similar response when we bought 35 years ago, with 11% interest. Also strangely, the prices have increased (5x) in direct inverse proportion to the rate of interest (1/5).

In the really old days, people used to get a down payment together, fib about source of funds if they got help or borrowed for the down payment, fib about income, get the house, and rent rooms and share The Bathroom (yes, one) until it costs were either manageable or the house paid off and they could enjoy the whole house for themselves.

The cycle is now repeating, the main difference being that there’s more than one bathroom.

And finally, some good news: Toronto prices down 0.8% for the last year, down 4.2% for the month, and down 4.1% for the last quarter. Summer doldrums? The usual pattern is for prices to drop up to 20% by the end of the year. Timing does matter, and don’t try to buy when everyone else is.