What we’re looking at: Raging House-Price Inflation.

By Wolf Richter for WOLF STREET.

House prices soared by 14.6% from a year ago, according to the National Case-Shiller Home Price Index, the biggest increase in the data going back to 1987. But it pales compared to the raging mania that has taken hold of individual metros.

Today’s release, called “April,” is based on a three-month average of sales recorded in public records in February, March, and April, of deals made a month or two earlier. So that’s the time frame. The metros here – the most splendid housing bubbles – are in order of the biggest house price increases since the year 2000:

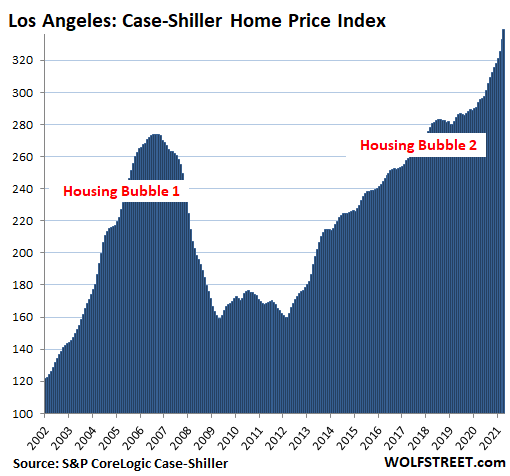

Los Angeles metro:

Prices of single-family houses in the Los Angeles metro jumped by 1.8% in April from March and by 14.7% year-over-year. All Case-Shiller Indices were set at 100 for January 2000. The index value for Los Angeles of 339 indicates that house prices soared by 239% since January 2000, despite the collapse during the Housing Bust, which makes Los Angeles the most splendid housing bubble on this list.

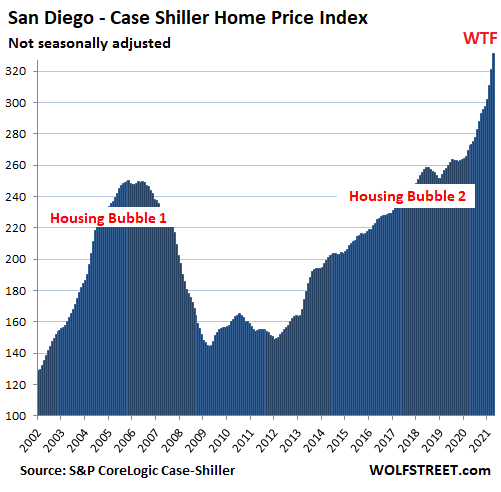

San Diego metro:

House prices jumped by 3.2% in April from March, after having jumped by 3.4% in March from February, and are up 21.6% year-over-year, the second-hottest annual house price increase behind Phoenix. Prices have soared 231% since 2000:

What is this? Raging “House-Price Inflation.”

The Case-Shiller Index, by using the “sales pairs method,” compares the price of a house that sold in the current month to its price when it sold previously. Home improvements are taken into account. The index tracks the amount of dollars it takes to buy the same house over time. This makes the index a measure of house price inflation as it shows the extent to which the purchasing power of the dollar has dropped with regards to the same house.

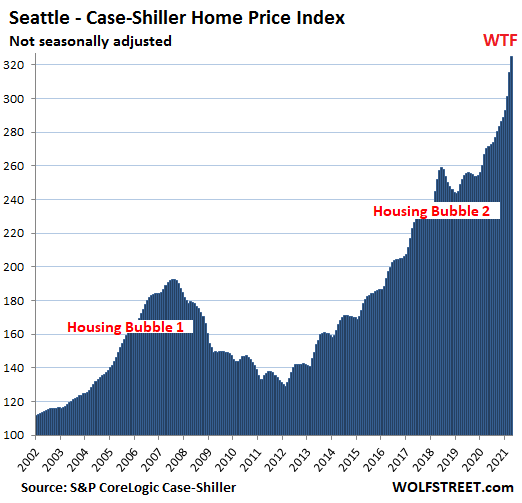

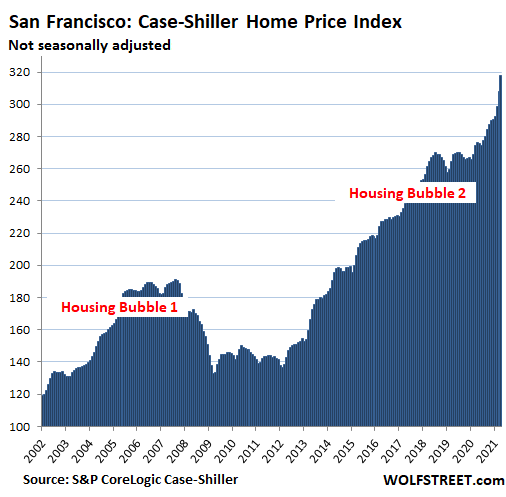

The charts below are on the same scale as Los Angeles and San Diego to show the relative magnitude of house price inflation between the individual markets since 2000.

Seattle.

House prices in the Seattle metro jumped by 3.1% in April, after having spiked by 4.7% in March, for a classic WTF moment. Year-over-year, the index is up 20.2%, the third-hottest annual house price inflation on this list, after Phoenix and San Diego. Since 2000, house prices have skyrocketed 225%.

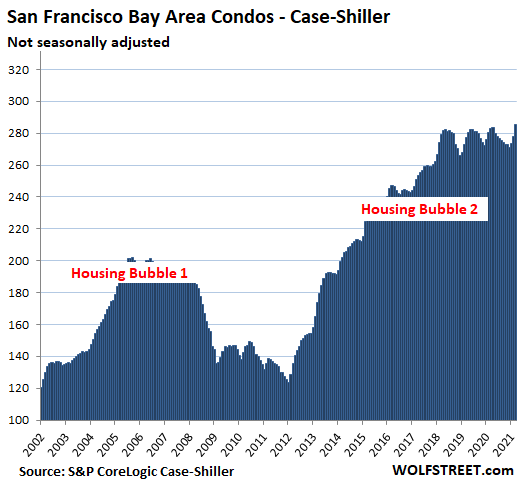

San Francisco Bay Area Houses and Condos:

The Case-Shiller Index for “San Francisco” – it covers the five counties of San Francisco, San Mateo, Alameda, Contra Costa, and Marin – spiked by 3.1% in April after having spiked by 3.3% in March, and is up 15.1% year-over-year. House prices have skyrocketed 218% since 2000.

But condo prices in the San Francisco Bay Area have been roughly flat since April 2018:

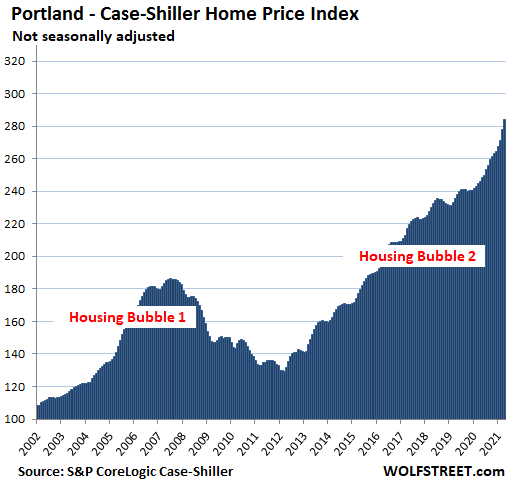

Portland metro:

House prices jumped 2.1% in April and by 15.4% year-over-year. Since 2000, they’re up 184%:

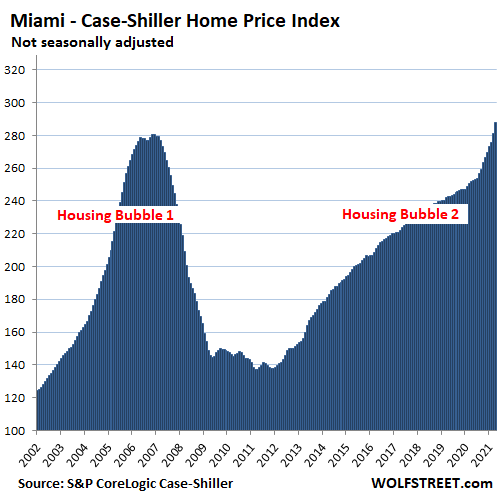

Miami metro:

House prices jumped 2.4% in April and 14.2% year-over-year. Up 187% since 2000, they have now surpassed the insane peak of Housing Bubble 1:

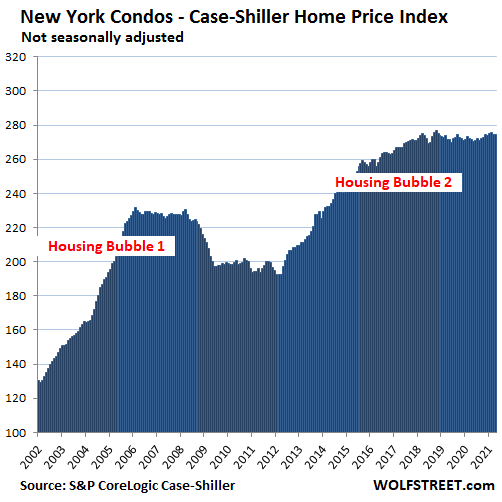

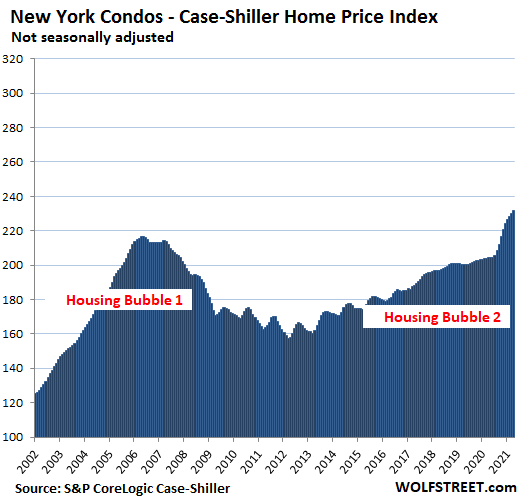

New York City metro: Condos and Houses:

For the Case-Shiller Index, the New York City metro includes New York City proper plus numerous counties in the states of New York, New Jersey, and Connecticut. This is a vast housing market that includes some of the most expensive submarkets in the US.

Condo prices for New York – condos are heavily concentrated in New York City, particularly Manhattan – declined 0.1% in April and have roughly been at the same level since February 2018, with the high in October 2018. Since 2000, and despite the last three years of flat-lining, prices have soared 174%:

House prices in the New York metro rose 0.8% in April from March and are up 13.5% year-over-year. It took the index 15 years to surpass the peak of Housing Bubble 1:

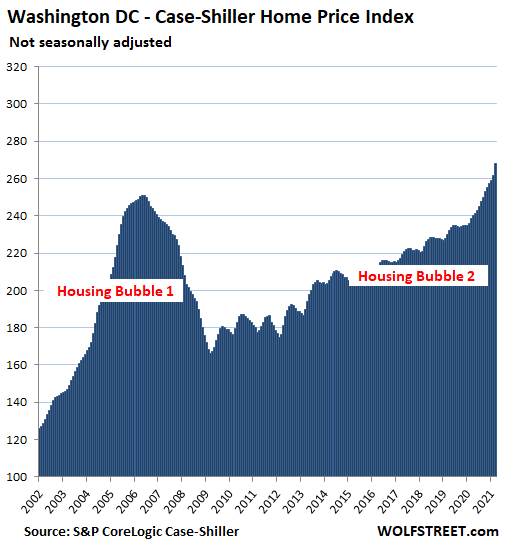

Washington D.C. metro:

House prices rose 2.3% for the month and are up 13.6% year-over-year:

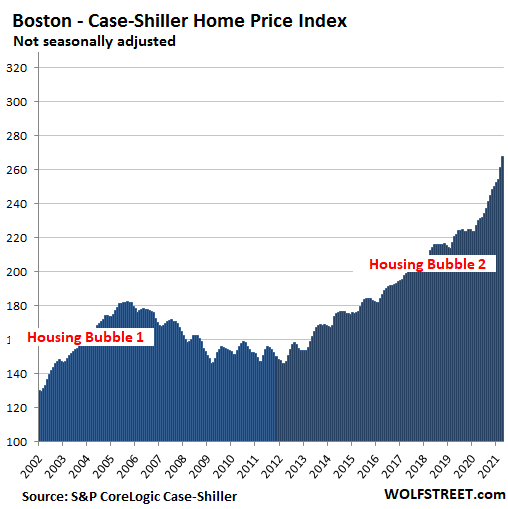

Boston:

The Case-Shiller Index for the Boston metro jumped 2.5% for the month and 16.2% year-over-year.

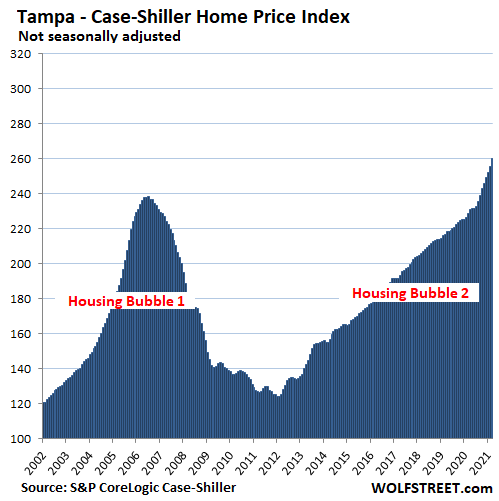

Tampa metro:

House prices jumped 2.3% in April and 15.4% year-over-year:

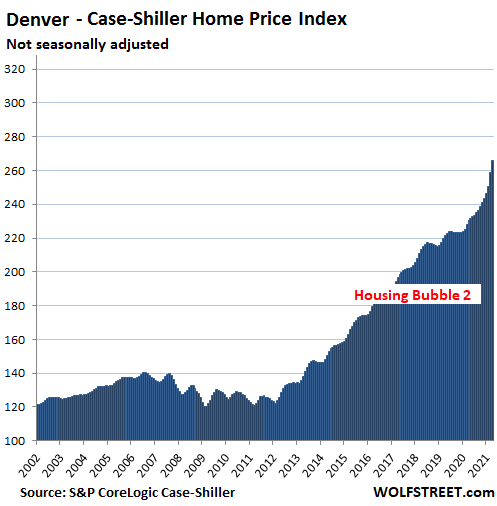

Denver metro:

House prices jumped 2.7% for the month and are up 15.4% year-over-year:

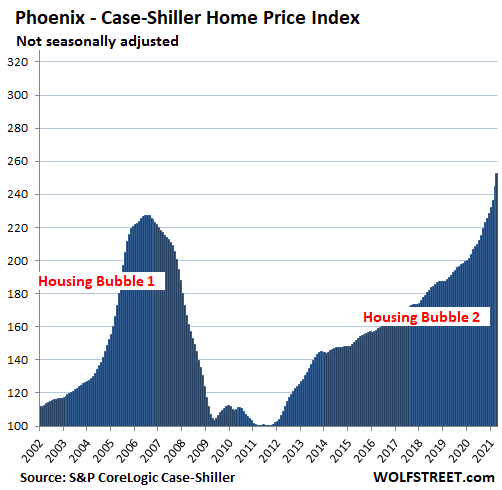

Phoenix:

The Case -Shiller index for the Phoenix metro spiked 3.3% in April, after having spiked 3.4% in March, and is up 22.3% year-over-year, the biggest year-over-year increase in Phoenix since the peak months of the insane bubble days in 2005, and the hottest annual house price inflation among the Most Splendid Housing Bubbles here:

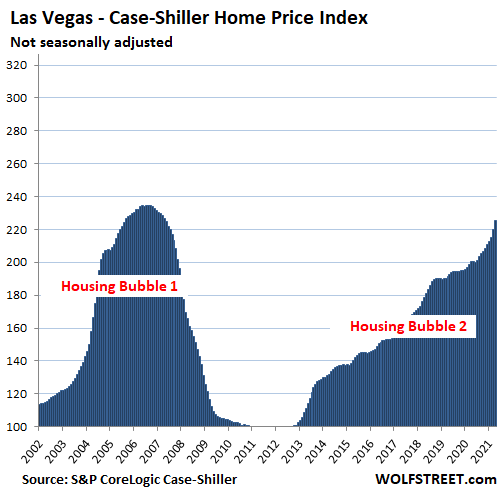

Las Vegas metro:

House prices jumped 2.5% in April and 12.5% year-over-year:

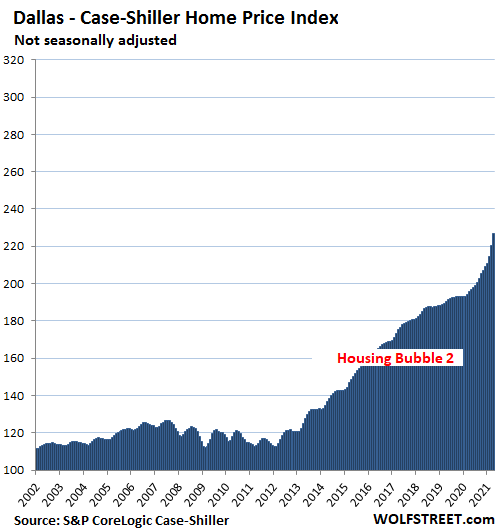

Dallas metro:

House prices spiked 2.9% in April and 15.9% year-over-year. The index is up 126% since 2000. In the other cities in the 20-city Case-Shiller Index, the two-decade house price inflation amount to less than 120%, the cut-off mark for this list. By comparison, the Consumer Price Index, one-third of which is composed of understated housing components, rose by 59% over the same period):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Whelp. Guess I’ll die.

The holiest home town , Los Angeles, is No. 1,

Shall I die too??

Well, funerals are way cheaper than a mortgage.

Joking aside, I hope this is the end of the price peak, I am getting married and really need to afford a shelter for me and my life partner.

Inflation and not bubble! Wolf you need to get a grasp on what an increase in $$$ does to hard assets. If and when $$$ is drained from the system then a so called bubble will deflate. Only $$$ printing in america’s future until the bubble bursts! But that is years away!

Wolf, buddy, this is the same headline u’all ran when prices were 60-70% lower!

Indeed a manipulated inflation !!! where no one can afford to buy a crap shack , with this next to nothing pay rate and high unemployment numbers. Go ahead and buy more properties , someone has to hold the bag when bubble pops.

There’s some difference between “bubble” and “inflation”.

If only credit is expanding, then it’s a bubble; the bubble pops when the credit expansion stalls. Dot-Com ’99; Housing ’06; GFC ’08. Credit is definitely expanding now…

But if incomes are also expanding, making bubble prices “affordable” (eventually), then it’s inflation.

I think the jury’s still out on the income expansion.

Wisdom Seeker … It’s inflation the whole way through. Inflation doesn’t affect all prices the same amount at the same time. Asset prices are the canary in the coal mine. Wages lag … unlike real time markets, they are negotiated much less frequently, and since consumer prices embed a large wage component, they lag too.

Inflation is not recognized as such when it’s mostly asset prices, because asset price inflation is fun … at least for the owners of assets … and TPTB prefer to put off recognizing inflation as long as possible.

If all these houses become ‘worth’ half as much, and all the stocks the same, then isn’t that “money being drained from the system”?

Just look at the charts.

They go up, then pop, up, then pop. It’s human nature.

Anyone who thinks otherwise or that this time is different has to assume humans have changed.

“I think the jury’s still out on the income expansion.”

No, it isn’t:

https://www.oftwominds.com/photos2021/inequality-income2-21.jpg

Can’t we have both inflation and a bubble? It doesn’t have to be just one or the other.

There are still cheap houses in rural areas. May require a big commute though. The key is to fix the inside up like a palace and keep the outside like a poor man’s house. I actually like renting though. Most of our utilities are paid with the rent and rent hasn’t risen since 2017. We save more renting than we did owning. Seemed like we were always spending money on some improvement. Little expenses add up!

One downside to renting I hadn’t considered: in California, at least, your landlord can kick you out with 60 days’ notice if s/he wants to put the property up for sale. This just happened to us; I got a 60-day notice on May 26, we were planning on moving into my mother’s house after a remodel later this year, but now we have to move out, remodel Mom’s house, and move in just 60 days (looks like we’re in for an extended motel stay). To add insult to injury, I’d already paid rent through September. The rental market is tight in this CV town; a neighbor’s landlord told me he put his property on Craigslist, and got over 40 inquiries the first couple days; he said some were offering $200-300 more than he was asking. If we didn’t have an (accelerated) Plan B we could have ended up on the streets.

Cali Bob- ahhh, I had not considered that. That is a great point. I’m so sorry that happened to you, but it sounds like you have a great Plan B…even if it means living with a few renovations at the same time.

There are still reasonably priced homes in many of the slightly better than average Texas suburbs, too. The problem seems to me to me mostly in HCOL area and the formerly LCOL areas that people from HCOL areas have been fleeing to (the Boises and Renos). Some areas were so cheap that even after nearly doubling, they’re still in accordance with median household incomes.

“…a neighbor’s landlord told me he put his property on Craigslist, and got over 40 inquiries the first couple days; he said some were offering $200-300 more than he was asking.”

Sounds like the car salesman who called me the other day. He told me he had 3 for me to look at, but to hurry up or they’d be gone. I asked him why he was calling me if he didn’t need to sell a car.

Depth Charge,

In terms of car sales, your salesman is likely paid a commission or bonus for the vehicles he sells. So if the other salespeople sell the three cars that are available, he won’t get paid. So HE wants to sell you a car so that HE can get paid. And if you don’t hurry up and buy from him, then another salesperson will get paid for that sale. I think that’s the logic here. For commissioned salespeople, it’s a dog-eat-dog world.

Hah, I inquired about a car and the sales dude wanted above MSRP. “It’s the hottest car on the market today.” My wife called a salesperson at their sister dealership and had a a much more reasonable salesperson drive the car over to his dealership so we could buy it at the price we wanted. Dog eat dog – no kidding!

Funny also how when you walk in, they say, “Wait here while I go check if it hasn’t been sold already.” And when they invite you out to take a look at it some back office guy will come out and act like a customer, saying “I just wanted to see this. Think of getting one myself!”

Not sure why anybody would ever want to get into being a car salesperson. Disgusting tactics.

re: “… Sounds like the car salesman who called me the other day.”

Except, unlike the car salesman, this guy had no incentive to shill to me (this was just a friendly conversation, and he already had a new tenant). It’s widely known the rental market is very tight in any remotely desirable area in California. I’ll be watching to see if this results in one of the construction ‘booms’–and subsequent oversupply–I’ve witnessed several times.

One other thing: According to his RE agent, my landlord is selling all or most of the 20+ houses he owns to finance a couple of apartment complexes along the ‘580 Corridor’ in Manteca and Lathrop (essentially bedroom communities for the SFBA). Multi-family dwellings may be the future for CA; however, Mountain House–one of the ‘ground zeroes’ for the ’08 boom-and-bust—appears to be experiencing massive SFH development again. History rhymes.

In my rural area, the place is poor so the county residents defunded law enforcement 20 years ago.. Now we have so much illegal activity going on that people are seriously worried about their safety.

There are no free lunches.. Where homes are cheap, there is a reason.

I am a little surprised by Phoenix and Las Vegas… as in other places in the desert SW as there is a serious problem with water. People are acting like it doesn’t exist or it doesn’t matter but when the reservoirs and the Colorado River dry up, their property will be worthless..

Janna- Bob,

Ahhhh, the humanity, the terrible suffering…..are donations helping any?

Good luck, Mill, I mean that… Be patient. Time will be on your side.

What’s a life partner ?

Once LOL

Modern lingo for spouse, I think. I prefer Soul Mate myself.

Turtle,

Yes , soulmate is much better word:)

Water…as long as you exist, 70% of “you” is partnered with it…..and it’s a VERY promiscuous relationship.

Why don’t you look for a home in a more affordable country? Does the US really provide a standard of living that justifies such an enormous price of admission? I don’t understand why anyone would consider paying over $1,000,000 for a shack in Seattle even though it has become such an awful city to live in.

I got the hell out of the US and I’m glad I did. I can’t understand why the US has not experienced a mass outflow migration. What a horror story. I’m never going back, not ever for a visit (that being said I still love US entertainment, movies and streaming).

Where do you find a more affordable country? In my experience, everything tends to cost more in foreign countries when you compare similar quality. I suppose life could be cheaper if you can blend into the favelas in Brazil, settle down in a Nipa hut in the Philippine countryside, or rent a tiny, dilapidated apartment in a third-tier city somewhere in Eastern Europe. But it’s not clear to me that you’d be getting any more bang for your buck.

Fruits and vegetables tend to taste better and are much cheaper in other countries, but if you can’t afford those, you can always get food stamps or unemployment bonuses here to pay for them. Unless you happen to be fluent in the local language, you’re always at a disadvantage living in a foreign country.

If I ever start requiring regular medical care, I’m probably moving out of the US because from what I can tell there does not seem to be any upper limit to medical bills. Almost everything else seems less expensive to me here.

Russia was the hot topic yesterday. Leading the world in responsible fiscal policy, I think it was. And very safe from invasion. They got the nukes, you see.

Turtle, you forgot to mention that no other country really wants to invade and eventually own Russia. There are better targets.

There are still plenty of nice neighborhoods in many suburbs of the US. I am fortunate enough to live in one.

I live in rural America, it’s paradise, went kayaking down the river today,beautiful river and afterwards went to s local eatery that was incredibly busy. All the local eateries are busy and reasonable. We have s small farm, grow s lot of our good, bees, chickens. I wouldn’t trade my place for anywhere in the world, but that’s me.. yesterday we went fishing.

@MyLadyHumps

Good question and I think we are seeing a lot more outflow migration from the US, at least in my experience contracting overseas. I’m based all over but mainly in central or eastern-side Europe, Southern Cone (Uruguay, Chile, Argentina, south Brazil) and occasionally in SE Asia. There was a time back in the 90s when I was the only American in whatever town I got sent to (engineering), now all these places are teeming with American expats, plus plenty of Australians, Canadians, New Zealanders and Brits. I don’t always get a chance to ask them why they emigrated from the USA, but based on the source countries and the fact they all have this corrupt monetary policy and housing bubbles (just like with our Federal Reserve), I suspect that insane US house prices ARE a big factor in the expatriation of the non-Americans too.

Many of the expat Americans I’ve talked to have indicated that the US housing bubble was a factor, since it’s not just in big cities anymore but spreading out into US suburbs, rural towns and once second tier cities, and at any rate the jobs and incomes usually aren’t sufficient even in the few (shrinking) islands where US home prices are still a bit saner. Even though Europe has had the reputation for expensive housing, that’s simply not true anymore, a myth 2 decades out of date. Especially with the recent housing bubbles in North America, Australia and NZ, I’ve been finding homes esp. in central and eastern Europe to be much, much cheaper, even some of the sub-Paris level cities in France, Germany or the Nordics now have much more affordable housing. And these aren’t backwaters either, they’re full of good jobs and services, even more so now with WFH.

A lot of expats mention it’s much easier to raise kids outside North America but I suspect, again, a lot of this is due to more affordable housing (and childcare). As I understand, the US governmental agencies only partially keep tabs on the number of expats since they’ve drunk the “US immigrant nation” Kool Aid so long they’re only now starting to realize millions of Americans are emigrating too. In fact when you think about it, selling your overpriced, asset-inflated US home and moving overseas is about the only true way to take advantage of the housing bubble. Your house isn’t exactly a liquid asset, and for US homeowners now, the only “gain” from the housing bubble is higher property taxes and maintenance costs. And if you try to move elsewhere in the USA, whatever proceeds you make selling your home will just get eaten up by higher costs wherever you’re buying. Whereas moving overseas can actually net you real gains. Besides the US expat families where I work, I imagine huge numbers of retirees are selling up and moving to Latin America for the same reason.

Brilliant! Imho the best way to compensate for the artificially inflated housing costs is by saying “no, thanks” to spending on healthcare in the US. If you are super healthy and you have a very healthy family history, that’s a great way to compensate.

Healthcare spending in the US has a horrible ROI anyway.

I have to agree with you. For the second time in my life I am considering leaving the US. First time was during Carter administration. Where did you move to and what is it like to live there?

Most of the people are wearing colored glasses in general.

People who have vested interest in home prices going up ( realtors, landlords ) have justifications that prices would either not go down or remain stable.

Other people think a crash is coming or deflation.

What about me: I have no idea although I do agree prices are damn high.

Exactly. Ain’t no crystal balls. Not even the Wolfster, with all that fine data running through his magnificent brain, can predict what will happen or when. All we can know for sure is what we see right now and boy is it wacky.

We do know history has a tendency to repeat itself and what we see now is reminiscent of the 2006 crash. Housing and other prices cannot simply keep rising at these insane levels.

If I had to place a bet, my bet would be on a significant drop in the housing market within the next give years. But I said that five years ago too. We’ll see.

It’s hilarious that my $200-something house is “making” $10K per month lately. Definitely not sustainable.

You can’t die until you first shuffle all whats left of you to the “Health Care” industry.

Every year, I get an information booklet from my health care provider. According to the booklet, my maximum out of pocket liability this year is under $5,000 for covered procedures. I can live with that without worrying myself to death over medical bills.

Nah. I have the opposite view, the best way to adjust for housing cost inflation in the US is to avoid spending on healthcare. It’s the key to leanFIRE as well.

(Nods in agreement with an economically induced tick from Reno). No way this will end well based on how inhumane the situation is for the majority of the population who isn’t into property gambling tomorrow’s stability for gains today.

Well in Auckland New Zealand house prices have gone up 800% or so since 1990. A house that was $120,000 is now $1,000,000. In a good area expect to pay $3,000,000 to $5,000,000 for nice but not top properties.

And, many parts of the country are up 30% in the last year.

Lots of stuff going exponential.

Rents are following but nobody seems to notice that there is very little rentals available and everything is priced 20% than January.

At least we know who to blame for rent increases : greedy landlords

Try the government , for grossly intervening (subsidizing) in the housing markets.

Try both

Landlords will charge what the market will bear and why not? Who expects them to be saintly? This is entirely the government’s doing.

At some point the landlords will have to charge more than tenants can pay.

Here in Austin our property taxes are going up exponentially. As a landlord I am not passing on all the higher costs we are experiencing because we have long term and older residents. So don’t paint us all as greedy. I’m 75 and worked my ass off to get where I am today. I drive a Kia, don’t own a yacht and don’t eat out very often. I want to have a sign that says…Stop the Steal of our property through taxes…it’s confiscation in Texas. 3% Taxes based on increasing value…let me tell you it is a huge burden on unrealized gains.

And no income tax. Try NJ. Same property taxes plus high income taxes.

We are in The Woodlands, TX and housing prices are still sane. Nobody seems to be fighting over home here yet.

Our property tax is about 2.1% but will probably go up once the fools that run the township incorporate the place.

Incorrect. TX housing prices are insane. The first cause of insane housing prices is the federal govts unconstitutional monstrosity of the Federal Reserve and it’s interference into millions of areas of life that are not interstate commerce. For example the Fedgov purchases almost every mortgage issued in the USA – local mortgages are not interstate commerce this is unconstitutional. Also instead of using the interstate commerce clause to protect us from monopolies, the Fedgov rigs up abominable huge interstate banking and investor oligopolies and monopolies to buy the houses and drive up prices.

Also, TX houses are extremely low quality overall and the foundations are garbage. TX houses should be very cheap or free to anyone willing to pay the taxes and maintenance. The annual homeowners insurance premiums are double or triple what I paid in other states when I was a homeowner due to constant damage from weather and also the poor quality. Mold is a huge problem for TX homeowners. Plumbing maintenance is a huge problem for TX homeowners – bring a jackhammer into your master bathroom to fix the plumbing- really! Slab leaks are a major problem for TX homeowners. Nowhere else have I lived do I hear many homeowners complaining about random bills for $5,000 to $20,000 for foundation repair and maintenance.

For all of the above reasons, and also due to the general housing bubble, I am one of the four Americas on a housing strike. I currently rent and have an exit plan to move elsewhere and rent where property taxes and rents are much cheaper- very soon. And later, after a few more years, will gladly move into a camper. I do not need any stuff or a house to be happy. I will be the homeless multimillionaire enjoying every minute of my life. I feel sorry for so many of my friends burdened with their huge mortgages & property maintenance bills, and making life decisions based on where they think they can buy their next house.

And the only thing I can think of to restore constitutional order is that I only vote for candidates who will do so. Not Republican or Democrat.

You can’t spell Texas without taxes.

Property taxes in Texas are among the highest in the US (and the world)

Don’t kid yourself, if your taxes are equal to a rent payment you own nothing.

Well, they gotta make up for the lack of a state income tax some way.

Florida too has relatively high property taxes, at least partially for the same reason

I’m pretty sure on a rate basis, NJ has the highest property taxes in the U.S.

Anthony, don’t let the local governments get away with that nonsense by adopting their language. The idea that taxes should be based on a percentage of value plays into their hands.

As an example, say a $500,000 house in Houston would cost $3,500,000 in Palo Alto. It does not (or should not) cost 7 times as much to provide schools, sanitation, police, fire, sewer, etc. to the house in Palo Alto. So don’t let them get away with the argument that an increase in values means that taxes should necessarily be higher.

I hope your leaders hear you. Up north of Dallas values in Collin County where some many CA headquarters like to move (if not Austin) pretty much went exponential and as a result property tax rates actually went down (did that ever happen before?), but the leadership there is very conservative.

Godspeed. Oh, and enjoy your Kia. The new ones are better than Cadillacs these days, if you ask me. Love mine.

At least in CA, I am protected from ever increasing property taxes on my rentals by Prop 13, a godsend to landlords and homeowners. However, here in WA, property is assessed every year and the increase has been near exponential. I have fought the assessor 3 times and prevailed twice, reducing my property taxes by a significant amount. Find a seasoned Realtor to run comps for your properties, study the average increase in sold properties and make your case. These appraisers sit on their asses at a computer, know nothing about your house and raise taxes as if their salary and raises depend on it (and it does). I encourage EVERYONE to appeal their property tax bill as a form of protest and a way to reduce your taxes. If everyone appealed, these leeches would have no time to reassess our properties year after year. They will never have enough of our money, make them work for it.

Good on you. Eventually, when you die you’ll be a peace with yourself. Seriously. Nice to see someone who is happy with what they have and concerned about their community. That is real class. I think I’ve had 3 landlords like you. One of which I had coffee with almost every Saturday morning. Good man. He had enough and was happy. Was very good to his family too. Before he sold he contracted with the city for repairs which put us under rent control.

3% is outrageous. In California the taxes are usually lower but with inflation and greed the investors buying up housing are increasing the rents beyond what people can pay. Or just leaving the houses empty to sit and rot. As soon as stimulus peters out we will have another boom in homelessness. And squatting. Not good for anyone’s quality of living.

Rents in NYC are lower 15% since march 2020.

Yeah, I’m never having kids at this rate. Early 30’s, highly educated, work in tech and I can barely afford the real estate in my area. Not sure how anyone in my age group does it. Massive amounts of debt I suppose. Stick a fork in us. This country is done

Phoenix,

Give the charts another look. What happened last time?

Market declined in 2008 due to poor underwriting and loan frauds. Underwriting standards have since become extremely strict and there are multiple checks these days. Banks are in an excellent shape with very low loan losses. In 2008, anybody with a pulse could get a loan and that is not happening now or in near future.

Sure, it’s not exactly the same as the ’08 bubble, but the bubble is real. And worse. And there are like ten of them.

American International Group Inc., better known as AIG sold CDO credit default swaps, so many in fact, that they could never hope to cover.

I wonder what AIG is up to today?

The losses have been nationalized. Next time it will be the US and minions in bankruptcy.

LOL. What do banks have to do with anything? Banks don’t hold much residential mortgages on their own books. Nearly all of it gets sold to the GSEs (and thus, the Fed) or to investors via securitization vehicles.

Underwriting might be slightly better than before, but the mortgages are all based on an LTV created by a bubble. When the bubble pops, the mortgages are underwater. Then, even people who can afford to pay stop paying.

To deny the parallels to the past is to bury one’s head in the sand.

Underwriting standards are not strict, except compared to recent history. A 3% down payment is not “strict”, regardless of someone’s credit score and other underwriting criteria.. It’s viewed as “low risk” due the government taking over most of the mortgage market through the GSE’s and other moral hazard (most it also government created).

Those underwriting standards weren’t an issue until home prices started to fall. Nothing is an issue when home prices rise by the double digits because you can always sell the home and pay off the mortgage. Problem solved. It’s when home prices decline and you cannot sell the home and pay off the mortgage that issues arise.

Joe, we’ve simply moved from “anyone with a pulse can get a loan” to “anyone with a pulse and a steady paycheck can get a loan for 5-6x their gross income.”

What happens to these people during the next recession when jobs are cut? Ignoring the service industry workers who lost their jobs in 2020, at least in my area of Boston they ain’t the ones buying houses. These people are leveraged up to the gills on housing and car debt, and many are barely skating by on making their debt payments. Emergency fund, what is that LOL. Wait until when white collar folks start losing their jobs, we’ll see how “high quality” today’s borrowers are after a couple months.

I understand Fannnie Mae is buying most of the mortgages from the originators. I see their stock is selling for a little over $1/share below the low during the 2008 Global financial crisis. They are insolvent. Went by their building in the Swamp and it looks like it is being demolished. A real s%ithole. No one even goes to work there anymore. All the workers all WFH.

Its nice to know that all these trillions of MBSs are in solid hands. No wonder the Fed is buying them.

People sometimes over extend themselves with mortgages. They don’t always consider the increase in taxes and insurance plus the maintenance. Also, no one can see the future so what are the chances that your income will pay your mortgage 10 years from now? When you combine these factors with over inflated purchase prices, you can very easily run into a problem if prices decrease and you must sell.

SwampC,

Fannie & Freddie are in conservatorship and will continue to be administered by the FHFA as per the Supreme Court last week. The shareholders sued to get past dividends that were seized by the US Treasury during the GFC to this day. The entities are merely a ward of the treasury at this point and their should have no value in the market imho.

The state of the building is an odd observation but perhaps some of the Jan 6th crew got poor google directions.

My understanding is that to promote fairness the Biden administration is in the process of loosening underwriting standards because so many people cannot qualify currently.

I’ve been told the best remedy for high prices are high prices. Stability is sustainable, rising prices without corresponding rising incomes gets to a point where the existing high prices can no longer be maintained/serviced.. Then the entire pyramidal structure comes tumbling down.. History shows this ALWAYS happens.. So all of you who are in denial will pay the price and learn a valuable lesson. Manias and Bubbles are not sustainable. No way! No How!

A recession will usher in another apocalypse, no income, little or no equity and Armageddon ensues.

Oh but remember Wolf, this time is different right? The fundamental is strong and there’s no subprime, interest rates is low, I can go on and on and on…

and in this new normal, pigs do fly 360..

Unless this time is different we are in for a good bubble pop. Hundred year trend is stocks return about 6% over inflation and housing 1% above inflation.

Look at a stock chart or a housing chart. Fed has blown the grandaddy of financial asset bubbles.

Thanks for giving me hope lol. And of course, my situation could be much worse.

Looking like it’s time to change my screen name ;-)

Nothing melts up forever. And the backside of the melt is always one hot skid down into the fondue pot. When this is all over, and the experts are picking through the remains, they’ll find something or someone else to blame it on than 2008, but it the end result of this insanity will be the same.

Amen. Last time my house “earned” more than I did, was within a few months of the bubble peak (in late 2005 in my area).

BTW, the Case-Shiller numbers are laggy. Zillow and local comps say my house is “up” 30% year over year.

That’s insane and unsustainable … unless Congress and the Fed keep printing out more money to give to their cronies via nice-sounding “stimulus” bills, which get spent into the hands of the crony-corporate titans who then buy “investment properties” to rent to the rest of us…

Ok but when? Is it in the next six months or three years from now. That makes a big difference.

Supply vs demand. When? When supply hits the market.

In my area…..not even close to “normal” inventory.

If its like flyover country…good luck.

Out here wealth is built by owning assets.

Large number of buyers & $$$ sitting on the sidelines

waiting to buy “deals” & turn rentals.

Well, last time it took four or five years to play out before hitting bottom. In Japan, it took over 30 years to play out before hitting bottom. Spikes cannot and do not go on forever, that’s all we know.

@Wolf,

What is the situation with the Japanese economy? isn’t it more or less still just going along?

Yes, seems like it. The Olympics are big mess. Vaccination rates are minuscule. People are getting infected. But trains are crowded. Everyone is wearing masks, and that helps keep infections from blowing up.

Hahahaha, and the Bank of Japan has been tapering its asset purchases down down to very little. That hasn’t been getting a lot of attention on this site. So maybe I should unleash an article about it.

My guess is when the Stimmy runs out..

Then there will be lots of inventory building up and buyers will have run out of fuel.

The infrastructure bill will take at least a year to put any money into the system, that is after and if it is passed… So don’t count on it to keep adding stimulus.

Good charts. In several charts we saw a complete price reversal in prices during HB1.

HB1 was created by a lot of sub prime borrowers. This time most everyone buying a home can afford the payments because of low interest rates. What would the chart look like if interest rates never dropped below HB1 5%ish range. HB2 probably would not be as high as it is?

I guess what I am saying are those graphs probably should be normalized versus interest rates to get a better understanding of trough to peak?

It was nasty in Phoenix and Las Vegas last time. Worse I think than in California itself.

I imagine something similar will happen and also in places like Boise and Reno too. People are starting to make these increases all about inflation but forget that housing prices were far above the mean trend line before the money printing machine geared up. Housing actually showed signs of stalling before COVID provided the Miraculous Boost.

@Phoenix Nobody knows what will happen but it seems to me reality always kicks in and that up is not always the way housing goes, especially in HCOL areas and places like the desert cities just outside of California that get pumped up by the exiles.

But who knows. Nobody does. There’s always Texas. ;)

Turtle, housing values will be in a world of hurt in places the Phoenix valley if “heat domes” like the one currently scorching the Pacific Northwest become a much more frequent occurrence. It won’t take much temp increase to make Phoenix a lot less desirable place to live than it ostensibly is today. I’ve lived here since 2007, and know what 120+ deg temps feel like. Not good on any sustained basis…regardless of AC. Just another unknown to throw in the mix.

Yet Fed buys 40 billion dollars worth of MBS. Why? What are they trying to do?

It’s hot but nothing nothing lasts forever

Those charts are not a crystal ball. Its not the same scenario this time. Last time they were selling houses for zero down to people who didnt have the income revenue to pay for them. This time its the criminal counterfeiting agency known as the Fed causing it. The working stiff is not buying houses, its the well to do income earners and investment corporations buying them up. There are now plenty of backdrops(BlackRock and other investment firms) in place to keep prices from fallling. Prices are rising because the purchasing power of the monopoly money is being strippped away. Its not just housing going up its everything because fiat currency is going back to its true value of zero. Definition of a dollar is 1 ounce of silver not a digit in a computer or monopoly money. 50 years of cutting all ties to the gold standard is August 15th. Prices will not go down on anything. All fiat eventually goes back to its true value of zero. And its way overdue. The Fed is destroying fiat on purpose. Currency reset coming. Fedcoin coming soon. The country is now just a criminal organization run by the uber wealthy and controlled by bought and payed for puppet politicians.

I’m sorry but Federal Reserve Members should be sent to prison for their large part in this Economic and Social calamity

Completely reckless …

You’re not alone. I’m 41, bought my first house in 2005. Was backwards til 2015, paid $400 at closing to get out. I’ve been waiting for prices to drop since 2015. Lmfao, stick a fork in all of us.

It goes to show that nobody knows what will happen. It cannot be timed and region matters too. I bought in 2007 in TX and was never underwater because the drop was only about 12% and by now the value has gone 2X purchase price.

I too was expecting a drop in SoCal probably starting five years ago and it never happened. Then, this. I never imagined the pandemic would trigger inflation and a massive increase in home values on top of near-record highs. My plan to move back to my CA is on hold or possibly off the table indefinitely.

It really is best not to try and time housing but to buy when totally comfortable and only if you love the home and are absolutely sure to stay for a very long time (10 or 15 years, at least). That’s a hard thing for most people to do today in many places. All the best to you.

Thanks COVID and Jerome, you scallywags.

Someone knows, who benefitted from the last crash? The Feinstein’s, Pelosi’s, et. al., are master manipulators and when the time is right, will orchestrate yet another massive transfer of wealth. Our economy is controlled by these people (aka, ba$tard$), not the other way around, it’s all by design. Did you see any of them go broke, or did they all become wealthier?

Hey, that’s about the same age when I bought my first home! (1973) A Ford bread van. Lived in it for 4 years and then sold it for $300 more when I moved in with a girl. Of course I took Janna’s advice and turned the inside into a palace, and left the outside looking sorta dumpy. Which allowed me to often park on the street (I moved around maybe 10-15 times), paid around $20/mo to whoever was the main man of the shared rental house, (plus a couple of married or shacked couples), and even at work for a while, till I discovered calling in sick was problematic, and usually got to run a power cord and use the shower and toilet sometimes, but sparingly. The rest of the time I used the ones at work. #1 was easy, my little sink with water pump fixture and 5 gal tank drained into the street or lawn.

You can get pretty clean with a wet towel, too. Still do. But I wasted all the saved money on skydiving, as I didn’t know anything about investing. But I did know the value of altitude very well.

Time is on your side. Live beneath your means and save, save, save. When the reversion to the mean arrives (it always does), buy a home cash or with a large down payment.

I agree with your advice. But just know that as a saver, the Fed has you in their sights. (Cash) savers are Public Enemy #1 to the Fed. They seem to equate savers with deflation, and deflation with failure.

Savers are terrorists in their eyes.

My savings are losing value too fast.

Already feel like I need a new job with a huge pay bump to keep up with the inflation (housing costs.)

…and groceries.

How about you move to a LCOL area of the US? Why do you ‘have’ to live where you live?

As someone in a similar position, my work won’t allow it.

Sucks that I doubled my income in the last year too.

If I had done it 24mo. Earlier I’d be in a very nice house now..

That is called the Golden Chain. An employee stays at a job that he really doesn’t like because he makes good money. He puts all his other life choices on hold because of that. Take a sheet of paper. Write down all the reasons to remain at the job in one column, and all the reasons to leave in the other column. Pin it up on a wall where you see it many times a day. There is more to life than a paycheck.

Most LCOL areas are LCOL for a reason….boring to be frank.

But even if I wanted to my wife and love our jobs.

They are low cost because rich f’ers haven’t showed up yet with truckloads of cash to drive real estate prices to the moon.

Rich f’ers have recently discovered my corner of the world and are driving prices way beyond what any of our young people here will ever be able to afford. The net result is even faster out-migration of people who know how to grow food, cut wood, and fix stuff.

The new residents will be in for a rude awakening when they find there is no one left who can fix their plumbing, maintain cars, or even clean their toilets.

Dear Leaders don’t care about rural areas, but they might change their tune when they find out that food and toilet paper don’t grow themselves. Might be a bit late by then.

“They are low cost because rich f’ers haven’t showed up yet with truckloads of cash to drive real estate prices to the moon. ”

That makes the poor people rich, because their assets are worth a ton now.

My friend bought a crappy house he ended up hating in Atlanta, just sold it. $140K in the pocket for 2-3 years of owning a house. Beats my rate of savings. *shrug*

@Ethan in NoVA

That sounds nice but I wonder if your friend really came out ahead as much as those numbers indicate. He probably had wicked awful high property taxes as his home appreciated plus increased repair, maintenance and insurance costs, not to mention closing costs. And now on top of that, he has to find a home somewhere else that’s going to be sold at a crazy inflated home price. This is what I’ve been hearing from talking to homeowners throughout the United States, Canada and Australia, even the ones with huge appreciations in home price value are unhappy. On paper they might have done well, but in reality there were lots of extra costs going with that appreciation, and since they’re now looking for a new home themselves, they’re at best breaking even financially even with having sold their homes at an (apparent) profit.

Go have kids, Phoenix. You will find they will be your greatest asset and motivator… as well as your greatest joy. If we waited for the perfect economy to have kids, this would be a lonely planet.

Well, at some point, it all looked massive. Perspective, in the valley, mid 2000s, houses were at $800K level, if you’re earning lets say $80 to $90K annually, and may be had 20% down, $160K, facing a 5% plus interest rate. It seems pretty insurmountable at that time too.

I guess the difference now is that both the pay and the house cost had doubled or tripled. Now, you have to figure out what’s reasonable. If it’s not a SFH, may be you’re stuck in a condo or a TH for a while, and have to work you way in.

It sucks, but it sucked back then too. Now though, everyone clearly recognize that there will be a time when the party is over. Mid 2000s, most people didn’t see that coming.

It’s funny when somebody in their early 30’s declared the “country is done”. You’ve been an adult for a decade and half and you think you know what the future holds? I doubt it.

Like Wolf said…look at the charts. You can see what happens next.

Nothing is “done”. The opportunities are coming for the patient people.

And if you don’t have kids, who cares? Try this experiment, ask about 100 people why they had children. You’ll get 2 good answers if you’re lucky and 98 answers that will make you think “Nobody seems have a good answer to this question.”

Most people get married and have kids because they were programmed by society (or their families, churches, etc.) to do so. Ask them “Why” and most are stumped. They don’t know why they did it…..

I think you need to step in the man’s shoes to understand his views.

Early 30s means that he was in early 20s to teens when the recession happened, and that can be very formative when you’re young.

I have no idea how old you are, but think about it, for the people who grew up in the 80s to 90s, the world transitioned from dangerous to getting better. That was the general feeling. The 70s were harder, but people saw things improving toward the second half of it.

Now, people like Phoenix look at the time frames in which they are growing up, and one can say without any argument that things are getting worse. So, the “country is done” comment is understandable.

Thanks to the media with its steady cadence of bad news, this is now a racist country with a bunch of ignorant people who will get you sick because they won’t follow the rules and is on the way to the bottom since China is eating our lunch with the help of our corporation.

That’s the general narrative today, and the news has been getting steadily worse since Bush Jr, how would you expect people to react when they see their futures being a dark hellscape (according to the media), and getting a steady diet of this over the last twenty years.

That said, the message you have is still very reasonable, there are opportunities coming. Potentially very big ones. The only uncertainty is timing.

Take a look at this post by Phoenix to see what the FED and politicians are doing to the young. It’s CRIMINAL. And these guys just won’t stop. They are hell-bent on destroying everything in the name of GREED.

Phoenix kids really don’t care where you live or what you live in or if their school is fancy or not or what you drive or how big their allowance is or how often they go on vacation. Education has now been liberated you can get a great education for your kids online cheap if your local school is bad. Kids just want attention from their parents that is all they really need. I am raising lots of kids without owning a house it’s great fun. I used to own a house it was a major downer done with that. My kids also told me they like me better now without being a homeowner.

@Phoenix

Totally hear you, and I agree that the insane US housing prices and housing bubble are probably one of the top factors in the downward-spiraling US birth rate and “baby bust” the American media is trembling about. As I wrote above, I’ve been meeting more and more American expats who’ve been moving elsewhere in the world, and the single most common reason I hear for the move is that it’s much easier to start and raise a family overseas. A lot of that is probably more affordable housing and saner home prices. Even most of Europe now has much more affordable housing than the US, with good enough jobs (and WFH) for American expats who go there.

What’s the current draw to Portland and Seattle, considering all the lawlessness going on?

The weather.

100+ degrees there lately and you say the weather?!

What else is there to say at this point?

Watch less TV and get out more?

But “out” is scary! The TV man say so!

My town kind of is scary. At about 200k residents, we already have 39 murders this year. That number is probably higher, but our PD tends to classify some as death investigations, at least initially.

In our town, suicides are kept quiet and never make the town rag. A local sheriff I am good friends with tells me it’s more common than you think.

During the early 1990’s the crime rate here in the DC Swamp was so high that the public officials went to great lengths to keep their numbers down. There were over 400 murders per year in a small geographic area. One of their tricks was to dump the dead bodies just over the border of DC into the adjacent counties in Maryland, Montgomery and PG counties so they didn’t count in the homicide totals. It worked. The mayor at the time, Mayor Berry, a coccane addict bragged about how he lowered the crime rate in DC and he got re-elected by a landslide.

What lawlessness?

I’m with Joe. I have friends in the NW. They aren’t complaining of lawlessness. They’re complaining about the heat. Gotta realize that the news can sometimes overplay situations to scare people, not to mention sway their views.

For instance, I survived the 1994 Northridge Earthquake while living in the Valley. Tons of damage, yes, but consider that of the millions who lived there at the time, just 52 people died in the quake. Not to minimize their losses in any way, but your odds of perishing in the event were low.

I have family in Bellevue, and they do say crime is a problem in Seattle. They avoid it. Also told me that Bellevue is positioning itself as the anti-Seattle, pro business and law and order.

@Keith, Not surprising. I would pretty much expect that of Bellevue. And Mercer Island, as well.

Andy-i heartily concur-whatever the leaning of a journalistic outlet, “…if it bleeds, it leads…” has always overwhelmingly been its prime directive (apologies, Wolf, as your stellar reporting illustrates the path to a slow death from a thousand cuts while most seem to only process a couple of big ones before rejecting a truly-objective ‘rest of the world’ analysis as too much to deal with…).

may we all find a better day.

Emergency dept physicians are noticing the uptick in violence…stab wounds, gunshot injuries, etc…

Yeah, we should have listened to us hippies and then Carter’s final plea to dispense with the mindless growth and consumerism.

But then how is anyone gonna get richer or have better “lifestyles” and all that important stuff?

Seattle is awesome. You’re surrounded by 3 national parks, with views of the sea and snow-capped mountains pretty much everywhere in the city. It’s the fastest growing major city in the US in 2020. I’m not surprised at all Seattle home prices are rocketing and will likely continue for another decade.

Naysayers are largely people who have never been here or think the ultimate in quality of life is living in an OSB 4000 sqft tract housing on top of each other in the middle of flat nowhere with the nearest store being a Subway and Wendy’s.

Its not the sea, its Puget Sound.. Okay, okay some people call it the Salish Sea, but you did not say that.

Puget Sound is part of the Salish Sea, ergo it is a sea. It has tides, smells like ocean and is super deep.

I lived there for for 5 months and it was the worst 5 months of my life. I had an apartment on Capitol Hill. Nice view of the Space Needle. Part of the problem was the place was in a depression when I was there. Boeing had just laid off nearly their entire workforce. The other problem was the Univ of Washington where I was in graduate school. They were such snobs and looked down on the military Vets. I got out of there as soon as I could and came here to the Swamp where I’ve been ever since.

Seattle is okay in the summer. Not so much in the winter when the rain feels endless and nothing ever dries out. I lived there for five years. Driving home to L.A. when an older relative needed help was a shock. Sunshine instead of gloom. After all that time, I’d forgotten.

There is no lawlessness except in the boardrooms of major corporations and banks and govt offices in NY, LA, DC and all the state capitals.

People keep asking buffoonish questions like “Why would anybody want to live in San Fran, Chicago, Portland, Seattle or ___________?”

The answer is obvious…because they are great and wonderful cities for a wide variety of reasons. If you’ve ever visited any of these places, you’d never ask such an inane question.

I guess it’s the Fox “News” effect where people think what those multi-millionaire professional liar “regular guys” Trust-Fund Tucker and $40M/year Sean tell their mindless hoard has an actual basis in reality.

Try seeing some of this great country (and the world) and thinking for yourself. Or, continue to humiliate yourself on the internet.

You should take an elevator from the platform level to the street level at BART stations in SF, without mask.

If you survive the urine smell, come back and make another FoxNews comment.

I used to go to SF at least twice a month ( two hours round trip by BART ) for the thirty-plus years to do shopping, eating etc. Until that elevator ride two and a half years ago.

Up until a few years pre-pandemic, I used to go to SF several weekends per year and regularly took BART to and from SFO, to attend the SFB. Early one Sunday am, a group of guys on the platform were intimidating riders, no police in sight. That was my last trip to SF.

(oh, and the street we parked our rental car on to go to the WMOH had gotten really dicey).

Pure, 100% real estate speculation. Nothing more.

Every major city has protests, and every major city has dangerous neighborhoods, drug addicts and a homeless population. The right wing news media would have you believe that Portland is in flames and people are fleeing which is nonsense. It’s just more divisive bullshit brought to you by people who profit from divisive bullshit. If they had a different target audience they would be doing daily stories about violence in Dallas and Miami.

Nobody is trying to burn down federal courthouses in Dallas or Miami.

Portland is a very big small city. Yes there are some issues with protests and crime but there are hundreds of neighborhoods with lots of small businesses, coffee shops, small ethnic restaurants and unique businesses. It is a city where the Corporatization of America has been held back. Lots of parks, lots to do, lots of quiet neighborhoods. People in Portland love the outdoors, Seattle too. The Pacific NW is their back yard and play ground. As a city, Portland is a pretty nice place. I have spent quite a bit of time there as my daughter and her husband and our two grand kids live there. So many plants of all kinds. Walking down almost any residential street in the older parts of the city is like walking thru an Arboretum.

I agree economicminor. Those 20 and 30 somethings are moving west. For economic opportunity and the great outdoors. My oldest and her childhood best friends all moved to Denver after the Great Recession. Her trainer is from HS. My niece and her husband moved out there from TN. Her best friend followed changed careers learned to code and followed her now fiancé to Portland. My youngest moved to Seattle last October. Lost her job in the travel industry but with the extra Covid Cash and some help from us took a job in aerospace. Yes it is very expensive but the great outdoors is free after an initial investment. One of her HS best friends after finishing his residency has taken a fellowship in Seattle and starts in a few weeks.,My very best friends in South Florida all have children in Denver. We are thinking that maybe we need to get a shared condo because the grandkids are coming. This educated generation is all inclusive and are taking their talents and money west after living a lifetime in the south. They will demand and address climate change. Generation Y and Z are now more than 50% of the population. It may take a few elections but they will bury the old white men in the Republican Party.,

Microsoft and larger ethnic Chinese communities. Which spurs big money speculation.

I am pretty sure this will end in tears.

Agreed. Everything reverts to the mean, even government driven unstable markets like housing. We are currently in a government subsidized parabolic home price blow-off top. It will end. Key is not to be a bag holder when it does.

Miami real estate is castles made on sand.

Yeah, the condo shakeout (and I use that term respectfully) has just started.

I was reading a news report that a condo owner of the recently collapsed building had just signed up for a monthly repair assessment a day or two before….of $583/monthly!!! On top of strata fees (what we call them here). Plus, a mortgage payment, etc.

I also saw an inspection report on a similar building that was also 40 years old. The spalling was so bad in structural members the concrete crumbled away from the rebar. The rebar, itself, was rusting away to shards. It looked like frayed cable.

Surely this will make people reconsider buying a high rise property going forward.

To think people used to worry about nails and screws popping out of drywall, or cheap carpet.

The fees for maintenance and the assessments don’t include the insurance, which depending on value, could be another $10K-$20K a year. And the hassle of obtaining insurance in Florida in the first place. Insurance companies there are always bailing out after every major disaster.

There’s no way Miami can be affordable for the average person after this disaster. I think people will be walking away or mailing in the keys.

Wait until the next hurricane hits. My wife was there during Andrew years ago (we were not married then) and won’t even consider going near the place if we were to leave Texas.

“Insurance companies there are always bailing out after every major disaster.”

I have a correction:

Insurance companies don’t bail after the disaster. The bail in the middle of the disaster. They call wind damage flood damage so that it is not covered. Read the fine print. They don’t want to pay jack. They are mostly corrupt criminal enterprises, glorified protection rackets.

Agree with SC here. Insurance companies are not in business to pay claims. They are in business to collect premiums and make profits.

Since I believe you used to live there is there an area of Florida the you consider still livable and desirable.?

RH,

If I had a lot of money I would own a place in Palm Beach or Jupiter. But generally, after living there for many years, I would only vacation there regularly in season. As you age the hassle of dealing with hurricanes every year is tiring and if you don’t have a lot of money, too expensive.

I don’t hate it by any means, for me in my situation, it’s just not worth it.

After hurricane Andrew hit South Fla in 1992, homeowners had their insurance cancelled and had to go to shiester ins companies that charged more than their mortgage payments. I found this out while I was down there on business one year after the hurricane. All the high rise condo buildings in Miami on the water are going to have the same thing happen to them. The owners will be unable to insure these units, unable to sell these units, and be unable to live in them. I see a lot of them going into foreclosure, and the buildings being demolished. The owners will be s$it out of luck.

Ins companies have turned into private equity funds. The insurance is a just a front operation to draw lemmings into their investment portfolio orbit. I’ve filed about 8 claims in my lifetime with my insurance company. They’ve made a killing on me. They’ve managed to screw up every claim I processed and they are one of the better ins companies. Now they won’t even do any work. They want you to do all the work with their mobiles apps and other bull s$it.

Florida upgraded the building code after Hurricane Andrew. South Florida is subtropical. They grow mangos, avocados and bananas. Coastal flood zone home mortgages require flood insurance. The Federal Flood Insurance Program is running a massive deficit. When they raised flood insurance prices, special interest groups lobbied to lower them again. Huge deficit.

Swamp-reminds me of a wise elder who told me in the ’60’s that most insurance companies can never resist gambling/playing the lottery, BADLY, in the stock market as they felt their losses could always be weaseled out of, if not legally and/or by rate increases…

may we all find a better day.

Salt in air from ocean corrodes everything

Nope. Roman concrete likes salt water a lot, it makes it stronger and more durable. The best part is that the Romans knew this at the time.

https://www.nature.com/articles/nature.2017.22231

Paulo, the repair bill for the one that collapsed was estimated at $12-15MM and I believe it was debated and disputed for the last 2-3 years.

I also saw some pics of disintegrating concrete and rebar. Under the pool. Scary what chlorinated water does to concrete and rebar within – thanks to the waterproofing which seems to have failed on the entire building.

I also saw a pic of a disintegrating column – spalled concrete, black, disintegrating, exposed rebar. There was a car next to it, so the column was in the basement.

Maybe that was the trigger? A car slamming into a most heavily loaded column which has lost 1/2 of its strength. 2am. What as way to finish off a night on the piss.

Nice scenario. The revelers in that car were likely too drunk to have known a thing…..or ever be blamed.

Falls into the sea, eventually…

LL

True

The ground under these high rise condo buildings is dropping 2 millimeters every year. When this fact becomes common knowledge it will be game over. Look for the government to blame this all on climate change.

Most of the ”waterfront” condo’s these days are built upon some sort of deep foundation, either pilings ”driven to refusal” with a certain weight of hammer, or drilled piers that are filled with concrete and rebar, both of which bear on solid rock, sometimes down as much as 80-100 feet.

Last new condo estimated, ( 2017 ) the concrete structure from top of pilings to roof was $30MM,,, and the pilings were likely another $5MM, but done under another contract.

The older buildings in FL, of which we estimated structural repairs to many, were not made nearly as well as the new ones, and the entire world of coatings and caulkings has advanced tremendously the last 20-30 years.

Most of these old buildings ”should” be torn down and replaced, and they will be eventually, sooner in the case of those that have not or do not get soon the kind of expensive repairs and structural rehabilitation that the one that fell required and did not get in a timely manner.

Anecdotally: At one of the condos we repaired, the original selling price in the 80s had been about $65K per unit, and the cost of the rehab in the oughts was about $300K. Lot of dismay, but the option was tear it down and start over for about $600K at that time.

This already happened. The Energy Sec blamed it all on Climate change and global warming.

Actually, I took a look at the report about the 2mm subsidence. Tragically, the 2mm is only in one tiny spot on the eastern side of that barrier island. The rest of the eastern edge where all the condos are located is still solid bedrock. Want to guess where that one tine spot was located?

Not to diminish the crap condo building standards that defined Florida in the 80s, as well as the wrecked condition of other highrises on that stretch—AND the condo association that stalled, rolled the dice and lost—but it looks like Champlain South had a little help from Mother Nature.

Well yeah…that’s because a big part of it does have to do with climate change or related issues. Most of the world understands this other than the 30% of the U.S. that only listens to Fox entertainment and denies reality…you know, facts n stuff.

Love that one LongtimeListener..but Paulo isn’t listening to Hendrix. We are probably a little out of place on this website. But I do like and learn what is what from people out there who are doing unique work nobody else is doing..hence Wolf Richter.

Castles made of sand tend to do that.

The price of a home has been rising faster than wages. This evidence supports the theory of a housing bubble.

May privately owned housing starts increased nearly 50% compared to the year before (Census/HUD report).

Wages don’t tell the whole story. Housing has been turned into a speculative asset class where a voracious army of investors are bidding up prices in a frenetic attempt to get out of cash that is being relentlessly pummeled by ultra-low interest rates.

Maybe when the assets begin to lose value there will be a rush of homes hitting the market

They need to get some of this investment speculation out of the market so that regular first-time homebuyers can compete.

Best bubble ever! We did it

The amount of wealth created in this recession was phenomenal!

This is such a fraud economy right now.

Used auto sales are booming because people stopped using public transportation and needed a car. But as people start to venture back into public spaces and public transport, this will quickly end. With many out of work and without stimulus, the market for autos is about six months from plummeting to new lows.

Of course home prices shot up. The combination of stimulus and record low mortgage rates and forcing people to stay home so they couldnt go out and spend their money created massive upward pressure on home prices. But will it last? Wait for more inventory to build, wait for higher interest rates and for investors to become net sellers of properties. Wait for the foreclosure moratoriums to end and forebearance to end. It all hits in the coming six months and the housing market goes back down rapidly. And those people that bought? Upside down on their mortgage with no equity and falling prices means many will just foreclose. Adding more pressure.

So the Fed in all its stupidity has blown a massive bubble to what end? The downside of bubbles are always more damaging to the economy than the upside was beneficial. There is far too much malinvestment on the upside, so that money just gets wasted and doesnt find its way into solid future investments.

When does the downside hit? Real simple. Once the Fed runs through the money in the Treasury and is forced to sell Treasuries at a pace of $250 billion per month above what is happening now. Instead of selling zero Treasuries and buying another $150 billion, the equation flips to a net of $100 billion needed from the markets. That might hold up for a month, as supply catches up to demand, and then overwhelms the demand and interest rates pressure starts unfolding. Look at what happened in late 2018 as the Fed tried to reduce the balance sheet. The stock market will also respond to this drain, since money is fungible and with higher interest rates taking risk in stocks will become less attractive.

And with inflation running hot, the Fed simply cant just turn on more monetary support. They will be backed into a corner. The Fed in all their brilliance created the perfect trap for themselves. So both stocks and bonds fall simultaneously, the same as what happened in the first COVID market collapse. But this time there is no way the Fed can continue this monetary whack-a-mole. The hot inflation prevents massive action. Or the Fed tries to do it, and the market views it as massive risk and simply sells until the Fed relents. At some point, the Fed needs to learn its lesson – stop distorting markets for short term gain.

Just stop digging us further into this hole!

“Wait for more inventory to build, wait for higher interest rates and for investors to become net sellers of properties.”

That may take a long, long time. RE investors are pulling far higher yields renting out property than they’re going to earn from any fixed income sources (including junk bonds, even leveraged junk bond funds like some closed-end funds). And that’s before the very favorable tax treatment from depreciation, etc. It would take a pretty hard shake-up to dislodge that money — something like a big fall in rents, higher financing costs (assuming many are floating rate), etc.

Agreed on all else. Fed, stop screwing with markets and trying to “fix” everything by kicking cans!

Boston Fed President Eric Rosengren said we can’t afford another cycle of boom and bust in the housing market. It’s too bad that he didn’t offer this warning before the housing boom started again. Though the Fed isn’t totally to blame for the latest bubble, those geniuses clearly deserve a lot of it.

The Fed is totally to blame for the latest housing bubble. Complete culpability – 100%.

With prices at nose bleed levels and continuing to soar out of control the Fed is:

1) Continuing to create $40,000,000,000/month and dumping it into the housing market.

2) Continuing to hold interest rates for the investor class at artificially low rates to allow them to speculate with no skin in the game.

3) Continue to debase the currency and make people desperate to own any hard asset at any price.

Unbelievably reckless and arrogant.

Exactly. The FED has the pedal to the metal and won’t stop. They’re like an angry drunk.

It’s going to crash “eventually” but agree with the above post that all parts of government will fight it. This bubble is worse than the first one, look at the charts of the cities that did not participate in the first one, like Dallas and Denver.

This moratorium will end, but I won’t be surprised if another one is arbitrarily implemented just because of the business cycle.

If enough mortgages refinance to near 3%, I can also see the government deciding to finance the carrying costs when the housing market or economy start tanking. $1T mortgages @3% is only $2.5B per month and less if means tested. It can be added to loan and re-amortized, just as I have heard for this moratorium.

Any interference is possible, until the credit markets revolt or the USD starts crashing versus FX.

Technically this housing bubble is not worse than HB1, as DTIs were much higher then?

The truth will not be known until bubble pops. I am sure there will be a few surprises.

Completely untrue. DTI is worse, and house prices to incomes are worse. I posted a link from years ago highlighting how subprime loans were back, just like last time. This thing was way out of line 3 years ago. In fact, in 2014, the housing market started buckling, but Barry and his boy Mel Watt announced their intentions to blow another bubble.

I think this too, but at same time the government will come up with some new program to prolong the pain. People getting kicked out of their houses is not a good look when you’re running for election.

What election? We just had one.

The Fed is still squinting hard straining to find a housing bubble… but it will find them in the worst way.

Their frothy delicious bubble will be followed by severe heartburn and gas pains across the country.

I was in the housing market here in my dumpy, second-tier New England city. From February to May, it was insane — oh, the dumps I saw go for $20,000 – $50,000 over asking. (My neighbor bought two years ago for $300,000 and just sold for $525,000.) I decided to rent another year.

But I’m still watching the MLS listings, and these past two weeks I’ve seen the first price drops. I had come to think those were a thing of the past, that the madness wouldn’t end. But they are coming more frequently now. And my landlord decided to get in on the action. Put his dumpy rental up for sale last week. It’s in one of the hottest neighborhoods, but it’s a dump, and you can tell that from the photos. Still, he thought he could get top dollar, as others had just a couple months ago for their dumps. Lo and behold, not one person came to the showing. Now he’s panicking, and is praying to the RE gods he can still sell at top dollar. I’m not sure if he can or cannot, but something in the market seems to be changing…

Yep the libertarian survivalist shacks here in rural north Idaho are sitting on the market for more than 45 minutes. They were selling like hotcakes and still sort of are but I’ve seen a couple of them have to lower their insane asking price and a few have been on the market a couple weeks.

Here’s hoping we’re hearing the final clicks of the roller coaster topping out before it plummets back to earth. Those who kept a calm hand will be paid back in full.

Or maybe “It’s different this time!” After all the MSM runs dopey articles titled, “Are we headed for another housing bubble?” 20 times a day.

Are you not willing to buy in Central Spokane area? Houses can be had for 300s. Not nice neighborhoods but still.

Spokane used to be littered with $85,000 houses.

If the area is known as a neighborhood I don’t want to be anywhere near it. I’d rather not live in Washington anyways and be forced to live under state wide gun control because Seattle said so. I’m not republican or worse yet, libertarian, but I’m not on board with Seattle’s politics and their omnipotent control of Washington state. /Political rant

I’d much rather be up in the woods than a subdivision. I only drive into work once a week so I can get pretty far out. There is cheaper stuff farther out but these are properties that were sitting on the market for 6-12 months 6 years ago for 50-120k. No way in hell will I ever be willing to toss out 350-500k for these hovels. Most of them don’t even have power or a hope to get it in 10 years.

There’s meat to LA, Seattle, Phoenix, Austin, Boston etc. Those markets are able to bear the weight of insane housing costs. These rural dumps with nothing to offer except a pat on the back from neighbors for taking your tractor and grading the roads because the county can’t buy a motorgrader won’t be able to bear these insane price increases. People are just panicking now. The type of home I’m buying will see a price bust, there’s no way it can’t. These hot new up and coming cities are going to get hit pretty hard I think. But boy howdy, if you spent 500k for 5 acres of land in boundary county with a trailer without power or water? Yeesh. Call me heartless but I’m willing to say you get what you deserve for making major financial decisions out of emotions.

“ Those who kept a calm hand will be paid back in full.”

I really really hope so.

Same here in San Diego. I’m starting to see price drops and numerous properties coming back in the market. I think we are topping. The next round of data will show this I’m guessing.

Geoff,

If this turns out to be the case, it won’t show up in the Case-Shiller data for another four months, at least. That’s how far CS is behind. I think the CS data is the most reliable RE data there is, but it’s just so far behind.

Stats are always backward looking (I’m not telling you this, I’m agreeing with you). My boots on the ground observation says that the frenzy in new and used car and truck sales is over with. In a few months time, I believe the data will support this.

Those 320 index numbers indicate that CA home prices have increased 3.2 times since 2000.

Can anybody name a single positive real world economic metric that has increased 3.2 times in the last 20 yrs? That might support/justify this absurd home price inflation?

This is almost entirely about Fed-destroyed interest rates, creating fictional “affordability” that will evaporate the second the Fed is forced to stop money printing/interest rate destruction.

I was going to answer “Federal Reserve Egos”, but then when I tried to divide infinity/infinity I got “NaN” instead of 3.2…

Honestly though, Congress is equally to blame, since they are legally in charge of the Fed.

In the end, though, it’s all of us. We got the government we deserved, for voting in all the scumbags and/or for tolerating election systems vulnerable to fraud. Shame on everyone for thinking high house prices are good when they aren’t!

No one is “in charge” of the Fed…legally or otherwise.

I believe you are wrong. The Federal Reserve exists solely because of an Act of Congress, and Congress has routine, legally mandated annual hearings to implement its oversight responsibility. This is no different than for any other part of the government which exists because of legislative choices.