Paying even more to get even less. Exactly what American consumers need the most in these trying times.

By Wolf Richter for WOLF STREET.

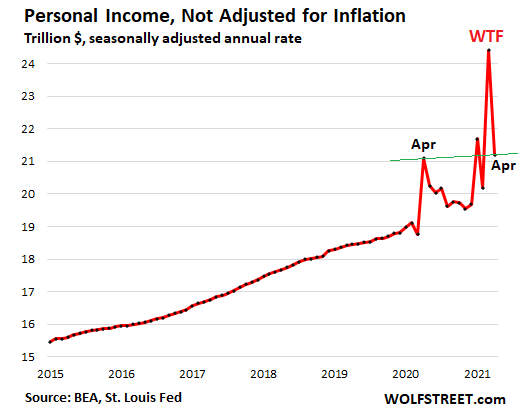

So we’ve got a little situation here. We’ve got a little bitty inflation uptick, I mean the worst inflation spike in three decades, and now total personal income from all sources, including from the now fading free-money-from-the-sky stimmies, rose 0.5% in April compared to April a year ago; but adjusted for inflation, “real personal income,” fell 3.0% year-over-year, according to the Bureau of Economic Analysis on Friday.

Month-over-month, and not adjusted for inflation, personal income from all sources plunged 13% in April from March to a seasonally adjusted annual rate of $21.2 trillion – after having spiked by 21% in March for a stimmie-powered historic WTF moment. Every one of the three waves of stimmies triggered a glorious overshoot. So going forward, most of those stimmies have been received and accounted for.

I indicated the 0.5% year-over-year increase in total personal income from all sources, not adjusted for inflation, with the upward-sloping green line. In a moment, we’ll get to what that green line looks like adjusted for inflation.

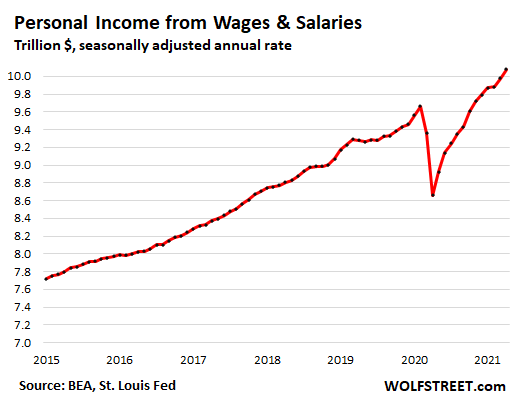

Personal income just from wages and salaries, not adjusted for inflation, rose 1.0% in April, from March, and will likely increase further in May, as more consumers re-enter the workforce and as employers raise wages in order to attract these people back into the workforce, in what is one of the weirdest labor markets ever, with record job openings, while 16 million people are still claiming state or federal unemployment compensation.

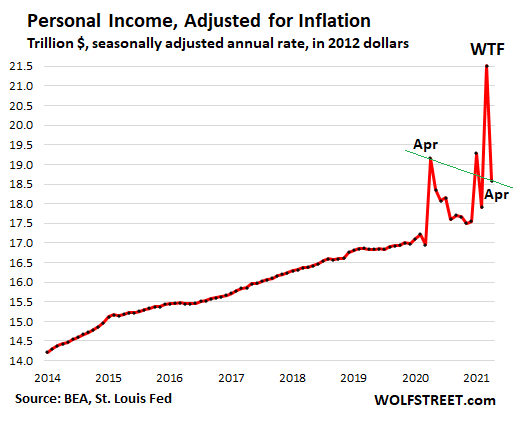

But then there’s inflation, and thereby the erosion of the purchasing power of “real” personal income. Total “real” personal income from all sources — adjusted for inflation and expressed in chained 2012 dollars – according to the Bureau of Economic Analysis, fell by 3.0% year-over-year – hence the downward-sloping green line:

Yup, inflation – the decline of the purchasing power of the dollar, and thereby the decline of the purchasing power of labor – is exactly what the American consumer needs the most in these trying times.

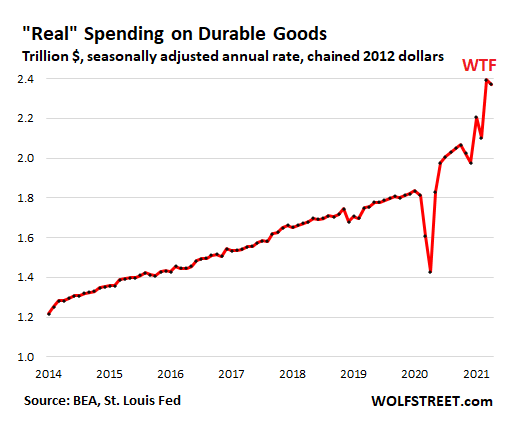

Nevertheless, American consumers gave their darndest to hold up the global economy. In March, consumer spending on durable and nondurable goods had performed a stimmie-driven WTF spike of historic proportions, triggering record trade deficits as many of these goods or their components and materials are imported. But spending on services was still lagging woefully behind.

In April, some consumers still got their stimmies and spent them, and other consumers were spending the stimmies that they’d gotten in March, and overall spending in April held up near the WTF level in March. But what we’re now seeing too is the impact of inflation.

March and April were the first two months back-to-back in three decades where large-scale inflation has cropped up in the data. So it’s time to see how that worked out.

“Real” spending on durable goods dropped by 0.9% in April from March. But not-adjusted for inflation, it rose 0.5%. This includes the mega price increases in used and new vehicles.

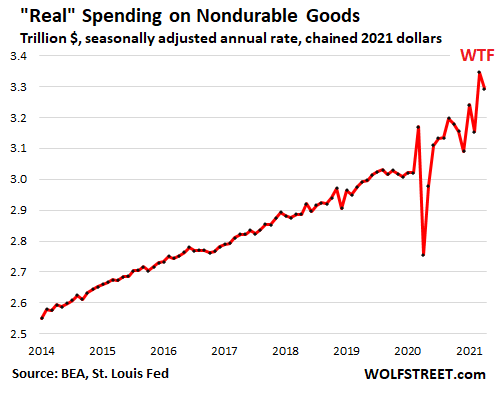

“Real” spending on nondurable goods dropped 1.6% in April from March. Not-adjusted for inflation, it dropped 1.3%.

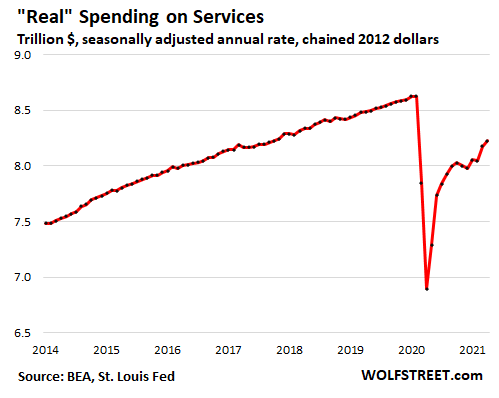

“Real” spending on services ticked up 0.6% in April from March. But not-adjusted for inflation, it rose 1.1%. While spending on goods has spiked to historic highs, spending on services – from airline tickets and hotel bookings to rent – has lagged behind. In April, real spending on services was about where it had been in late 2017.

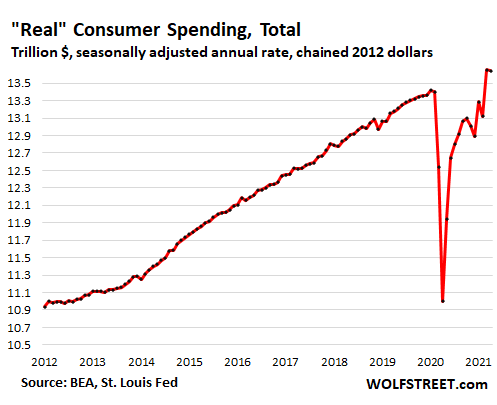

In total, “real” consumer spending on all goods and services fell 0.1%, but not-adjusted for inflation, it rose 0.5%. You get the drift. Consumers spent even more money to get even less for it:

Everyone now has their own laundry list of goods and services that have suddenly gotten a lot more expensive, or where the price stayed the same, but the goods have gotten smaller or the quality was lowered, or a combination. Astute consumers have been reporting this for months, but in March and April, it started to seriously show up in the data.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just a waiting game at this point. Lot of ink being spilled right now but the only thing to do is twiddle your thumbs and look shiftily around the room as the walls close in. If you’re already in the game and didn’t leverage yourself like everyone else with new toys or crapola stocks/buttcoins then you’ll weather the storm well. Meanwhile people who buried themselves in debt and crappy assets like overblown housing and a 9 year loan on a 70k dollar pickup truck only have runaway inflation to save them which will destroy them in the long term anyways or young people like me who would have been set up to be debt free aside from a mortgage seeing themselves and their pathetic salary and down payment dissolve as the days go by from “transitory” inflation that a bunch of crooks promise won’t hurt them.

Can only hope the whole thing goes up in smoke and the blue collar folks who are financially responsible can get back in at some point. It’s all wait and see. And I’m tired of waiting in a 1br apartment that costs me 1800 a month where I can’t sleep because of noisy families and their wild kids. If otr trucking wasn’t so unbelievably awful I’d go back to just living in a truck and working nearly everyday a year. But who wants to do that when all the money you saved from doing that before means diddly due to “temporary inflation.”

The saying goes we are all dead in the long run anyway and we are all condition to think very short term in this country. You drill the new normal narrative into the public even if they don’t like it, most will except it that’s just the way . Just suck it up and just shut up and take my money.

This is the new narrative.

“The faster than expected increase in some of those prices is actually a good sign in the sense that it’s a sign that the economy is recovering faster than a lot of people expected…”

— White House National Economic Council Deputy Director Bharat Ramamurti on May 28, 2021.

I just discussed that yesterday. Rising prices do not indicate a recovering, let alone a growing economy. Spending more for less is not growth, it’s shrinkage. Less is produced or delivered as a service at higher costs. Consumers get less for their currency. No matter how economists try to spin it, that’s no improvement in my book.

Those gov economist have all the same mindset. Lie ’till someone takes over. They know most people will not think for themselves anyway.

“Rising prices do not indicate a recovering, let alone a growing economy.”

Consider the source of the ridiculous claim:

“Bharat Ramamurti is an American attorney and political advisor who is serving as a member of the COVID-19 Congressional Oversight Commission, a congressional oversight body tasked with overseeing the Department of the Treasury’s and the Federal Reserve Board’s management of stimulus and loan programs mandated by the CARES Act. In 2020, he was chosen to serve as Deputy Director of the National Economic Council.”

The price increase is not because of increasing demand , it is because our supply chain is disfunctional, such as lumber supply, chip shortage problem,etc, these are showing that the prices economy has huge problem, Mr. Baharat is B.S.ing don’t listen to him no matter of he is Director of some organization

thank you I will

got 45 days to put out notice of 10% rent increase

don’t care if you’re retired and living on fake cpi fixed income

Enjoy your vacancy.

And I hope they trash your rental before they move out.

The people getting hurt by the inflation are the less wealthy, 95% of Americans, whose wages, savings, pension payments, social security payments, CDs, and other dollar-tied holdings are being drastically reduced by inflation. That inflation is being fostered by the creation of over $2 TRILLION since 2019 (PLUS $40 billion more a month for months in 2021 until today) by the “Fed” to gift to its banksters in exchange for their garbage, uncollectible, mortgage-backed-securities, which are probably suffering HUGE defaults.

In other words, a huge part of inflation for decades has been due to the current and prior TRILLION dollar bailouts for decades of free money given by their “Federal” Reserve to the banksters. Those are the true “dependents” on most government handouts: the corrupt ultra rich. See Simon Johnson’s “The Quiet Coup” in The Atlantic Magazine.

Also, do not count on all Americans being able to survive. Remember that almost half of Americans (before all of this orgy of money creation by the “Fed”) could not even afford an emergency $400 expense. They were living from day to day in 2919 and often, only by getting paycheck loans at ludicrously high interest rates (counting the huge service fees as a percentage of their tiny paychecks.) See “40% of Americans don’t have $400 in the bank for emergency expenses: Federal Reserve” in CNBC and ABC news.

That has only worsened due to the inflation. Loss of their jobs, even if they later got them back, also put millions in the hole, so they have even less net capital or have nothing but huge debts: due to the business closures, they now owe gigantic rent arrearages and mortgage arrearages.

More business closures are coming which will hurt most the majority of less wealthy Americans: increase their debts and decrease their income. Keep in mind that most of the younger generations are in that position. The opportunities for them dried up because of the banksters’ actions.

The cherry on top is that the costs of what they need, food, housing, education, and medical care are the ones mostly rising. The banksters really ripped off the younger generations, which harm will “trickle down” to those generations’ children, because younger generations will not have the funds to help their even younger children.

The only “trickle down” that actually exists in economics is the trickle down that we are seeing of misery and generations living in poverty with few opportunities. Schools that get government funding turn around and charge such high tuition costs that only the wealthiest (e.g., corrupt banksters) can afford to attend them now.

Others face getting so deeply into debt to get an education that they may never be able to pay down their student loans: I know various professionals who have been in such financial holes their whole lives. Financial parasites have done their best to use their “Federal” Reserve to suck the wealth out of all Americans for too long.

For a young person, you are wise.

So you touched on some points which reveal the real source of inflation.

You know, there is no reason to PRINT money if a certain .1% were not HOARDING money (Bezos, Gates, Buffet, Musk). If wealth were distributed more evenly there would never be inflation because we would not need stimulus, etc.

Only taxes that cure the hoarding of wealth will cure inflation.

but but but the hoarded money is being invested in companies, or buying bonds that were issued by companies to make investments… surely those companies are hiring workers which helps the common man.

Corporate America used the pandemic to automate more jobs. When a retailer installs four self service checkout machines, they need one cashier to oversee them, and that person works twice as hard as they used to.

Although capital expenditures appear to be rising, the negative current account for the US suggests these investments are being made in foreign goods and services.

I would think capex would rise as the dollar falls in value, so I’m not sure what to make of capex vs current account at this point.

see tradingeconomics.com for current-account data.

and fred.stlouisfed.org for capex data.

Those self service checkout machines were a little too convenient at my local Walmart and they removed them.

@Apple – I think it depends on the Wal Mart. At one store I was in recently (Fla.) they just finished roughly quadrupling the number of self service registers whereby now they have almost no regular registers left. The new self service registers they are using have been redesigned with more space to hold the scanned merchandise (and also more space to move about generally).

Ditto Palm Desert, CA, what was about 24 serviced check outs now down to 4. Must say the new layout is much faster with more room, portable scanner, ect., but as noted requires many less employees.

See this same application at HD, much better. Lowes staying with original system which is slow and tedious, falling behind.

Wonder in desert given level of educational achievement and various other factors whether WM, HD, LOW, others have a hard time filling these very low skilled jobs and that is part of the reason for the switch. My experience is those employees watching over the self check are way more capable when you need assistance with an item, bad or missing sku, etc.

It’s the game of Monopoly.. Collect all the pieces and raise the rents until all your opponents are wiped out.

In the real world version there are lots of bribes and pay offs and politicians and corruption but it is the same game you played as a kid.

Inflation is not caused by hoarding money, it is caused by buying on credit. Every time a person buys something using credit, the money to facilitate that transaction is created right when they swipe their card.

Taxes do not cure inflation, curtailing credit does. Had you been around during the 80’s you would know that…

^ This ^

Hoarding money is the opposite of inflation as that would imply low money velocity. Greatly expanding the money supply whether through credit or FED actions causes inflation.

Alot, probably most of current inflation though, is caused by shortages, monopolistic behavior, reckless investment, supply+demand, and price gouging; all of the stimulus money and easy credit is definitely apart of it as well. This all applies pre-pandemic as well.

You are way overthinking this. Inflation is simple, it is when the supply of money outpaces the supply of goods and service.

But what is causing the oversupply of money that is the question?

It is, and always has been credit. Credit creates money from thin air. In addition, it inflates the price of the credit purchased item by the amount of interest paid on that purchase..

For those of you who think the FED creates inflation by printing, then you must explain the mechanism by which that printed money gets into the economy. Until just this past year, helicopter money did not exist, and yet inflation did.

There is a direct correlation between inflation, and the use of credit. The only time when inflation outpaces credit expansion is when frontrunning begins as it did in the 1970’s and becomes a “built in” mechanism in itself due to price increases based on anticipation of inflation.

Good point, Song of the Dao.

The renowned economist, Dr. Michael Hudson defines this current issue in the US as “DEBT DEFLATION.”

Meaning, that wages have NOT increased in the last 40 years for average citizens. Millions of low wage earners were offered easy credit from banks/others to make up for the miserable wages.

So average citizens are experiencing a kind of “inflation” whereby those millions are heavily in debt, with stagnant waves.

Thank all those banks/others who make billions off of these debts.

No wonder the society is beginning to collapse.

In 20 years real personal median income is supposedly up 12%. Real GDP is supposedly up 50%, and real GDP per capita is 26%. Meanwhile if you look up the TCMDO on FRED for total securities, loans and liabilities, then inflation adjust that, it’s up 100%.

Regardless of what inflation numbers you use to adjust the numbers, the relative increases tell you a few things. Mainly that most economic gains are going to the top (or if you believe inflation is understated that they’re taking it away from us zero sum style). Also, the system is becoming ever more leveraged as debt never ceases to balloon upward faster than incomes. Debt is the reason the Fed can’t raise rates. Debt is part of the reason they are blowing money out trying to spur inflation.

Who wants to bet wages won’t rise fast enough to drive inflation faster than debt growth? Or do they think stagflation fixes overleveraged economies? Boy, if Powell came out and said that… Well if QE showed us something between 2009 and 2020, it’s that it made no apparent difference to the growth of total system leverage (remember this is how the money supply gets expanded, and you can look at total bank deposits to be reminded of this), so sooner or later we’ll still have to face a reckoning.

Don’t worry, be happy!! It will TRICKLE DOWN!!!

hahahahahahahahahaha!!!!! Wheeeeee!!!!

A nation of suckers going for a ride!!!! Wheeeee!!!!

I’m reading People magazine while I watch TMZ….

Amen. Taxation on the richest Americans is the only thing that can fix our country’s massive inequality and take back the trillions taken by the ultra rich. We must index taxation to a person’s total wealth, including hidden wealth, because it would not be fair if a person who earns $50 million a year and owns little else pays as much as a trillionaire who hides everything via foreign trusts and companies except for earnings of $40 million from one company.

Hike estate, gift, and generation-skipping taxes (which have frequently not even been enforced by the IRS) to the sky and fund the IRS adequately to collect the trillions in taxes in hidden, foreign trusts and companies that have never been paid. Watch “Britain’s Second Empire: The Spider’s Web” even though its estimation that only $55 trillion is being hidden is a gross under-estimation.

Note that I am not advocating anything other than fairness: that the trillionaires and billionaires finally be forced to pay their fair share of taxes, not continue to skate by avoiding taxes. Search Apple, tax avoidance, and $40 billion to understand a tiny portion of the problem.

New housing starts surged in March to the highest level since 2006. The Great Recession that followed the 2006 spike in new construction was triggered by housing speculation. In April the pace of new housing starts diminished compared to March due to shortages, except new multifamily apartment and condo starts increased. Zoning regulations limit the building of multifamily housing to certain areas.

My brother won with an all cash bid on a house that received multiple offers. He and his wife are not rushing to sell their other house as prices are in a strong uptrend.

Until they aren’t. Me – I’d take the money and run.

I talked to my brother yesterday. He put his house on the market a few days ago and accepted an offer above his real estate agent’s suggested price. They have a $60k deposit and scheduled closing date.

They will be forced to sell because the peoperty taxes rise next year by 20% at least.

Your brother must be rich.

Good comment T Guy. It seems to be a realistic assessment. As a 65 year old the only addition I would make is that what we see today will not always be this way. Things change. Can they get worse? You bet. The amount of debt being added to the daily narrative scares me, to be honest. I look at increasing debt (day in and day out) as an accelerant to collapse if this doesn’t change. However, in the past it seems the only belt tightening we see is at the bottom end for workers and everyday people. If ‘they’ pull out this solution I don’t think people will put up with it anymore. There’s already mass shootings every day or two. What the hell will happen if things really go sideways?

Thoma you are absolutely right. Who owns who is the root of all of IT. Who has any rights really complicates the big picture in the real world.

Ah yes, feminism. The cause of lead in the water, Jerome Powell’s RBF mugshot, stagnant wages, inflation and a housing bubble. Particularly it makes sense that women not having children would cause a housing bubble.

There is one solution to this problem, and it’s a very good one. Thomas Roberts should crawl back into the hole under his favorite rock and try to get over his divorce. Meanwhile the rest of us can have a serious discussion.

No need to worry, Thomas, I am IN CHARGE in my house. And after two divorces, I have this stuff down pat. /s

rhodium,

Housing bubbles are caused by many things such as government policies and over demand for certain areas. Over demand for certain areas can be itself caused by many things such as government policies.

Government policies over the last decades have been caused by one gender far more than the other. If certain policies get passed, other ones are allowed to slide by. One gender in effect, entirely controls the media and makes up majority of votes at all times. Certain movements have leaders who actively lie and lead many, if not most of their followers to ruin.

A certain women’s movement has greatly changed the basic ways society interacts and that changes everything else.

And rhodium, it’s very brave to insullt someone anonymously online. Shows your strong intelligent character. FYI, I’m not divorced.

Sorry I have to ask, although I kind of don’t want to. Can you be more specific about what this “women’s movement” you are describing is?

Feminiism.

It sounds ridiculous at first, I know, that it’s at the root of most western problems; but once you really hear everything about it, how it operates, and it’s effects. You will actually have a clear understanding of why America and other western countries are doing things the way they are. Once, you fully consider it’s effects and you combine that with the Financial/economic/political side of things, everything going on in America today, will make complete sense.

There is limitless evidence backing this up. For a start, you can find online the social media influencers that most young girls, including kids listen to and hear what they have to say about how young girls should live their lives. The majority of all girls in their teens and 20s are listening to these “influencers” on a regular basis.

All the ills of the world are caused be feminism???!!!!

What about the class system, neoliberalism, organised religion, greed, etc.

Imo most of the ills are caused by industrialization.

Trucker

If its got teats, tracks, or tires, it’s going to cost you.

Learn basic carpentry, house wiring, plumbing, how to run a small excavator. Build your own home. Level, square and a the rule of 3/4/5.

There is no greater tax-free investment than sweat equity and you need a place to live anyway.

K

“Learn basic carpentry, house wiring, plumbing, how to run a small excavator. Build your own home. Level, square and a the rule of 3/4/5.”

Any thoughts on the best places to learn these skills most efficiently (books, youtube, community college? Where do you go to get excavator practice? What certifications are available?)

Cas:

Re: excavator or grading learning curve:

1. Get a piece of land and a grading project. Pond, driveway, leveling a pad for a greenhouse, equipment shed.

2. Do an have-now and to-be grading plan. How much dirt do you need to move from place A to place B (“cuts and fills”). If you can’t eye-ball it, buy yourself a cheap laser-level and a tall measuring stick to calc how much dirt you have to move

3. Rent a track-loader, or if the project is small, a skid loader on tracks. Get the damage waiver. Get the delivery-truck driver to give you a 10 minute tutorial. That’s all I ever got.

4. Pick the place to start pushing dirt. Start at high elevations, and move the dirt to the lowers. Start somewhere where there’s nothing you can damage, and you can’t tip the machine over

5. Spend about a half day getting good at setting the blade depth low enough to move dirt, and high enough not to stall

6. Spend another half day un-doing the first day’s screw-ups

7. At mid-point day 2, if you have any hand-eye coordination at all, you’re productive

8. After 1-7, you’ve got enough skill and confidence to be productive.

A decent machine costs somewhere between $4-500 a day, plus $200 or so round-trip transport. Fuel is < $50 day.

For plumbing and wiring, there's plenty books and YT vids. It's not hard.

Wiring. Start at your house's entry point of power wiring. Pop the cover on your load center (breaker box) (after turn off main breaker, of course) and take the time to understand what each and every wire does. Everything in there is there for a reason, and it's the single point where all the parts tie together.

Then (while power's off) open up a switch box (unscrew the cover and look inside) and a plug box. Look at the colors of the wires, where they're connected on the switch/plug, and make the mental connection to what you saw in the main breaker box. What does black, red, white, green wire do? Once you've got that conceptually, you're most of the way there. The rest is "what device do I need to get X job done". Bring a project plan (wire a new light circuit and outlet for the dark corner of my basement) to your local elec supply house, and ask them to give ya what ya need. It's what they're paid to do.

Plumbing is two main things: supply of water, and drain of waste-water.

ID the main supply-side components – pipe, elbow, T, valve, check-valve, etc. – and learn how to join them. Soldering. It's cake after the first 2 screw-ups. Home depot / Lowes/ Menards plumbing aisle is your one-stop learn-shop.

Drains: make sure the drains slope down so gravity works (exhausts waste water to lowest point of exit @ your house), and learn about PVC. Go to home depot, look at their PVC plumbing aisle (valves, elbows, Ts, pipe, pipe-cement/glue) and bring a project diagram with you. Ask the salesperson to "I wanna put a new sink in my basement, and connect it to the existing drain system. What do I need, and how does it all fit together?".

HD "helps doers do more", or so they say. Put 'em to the test.

Reading is OK, but doing a test project with low-cost-of-failure is the way to get there fast.

Problem with a lot of trades is the boom and bust cycle of construction I’ve know framers who are sending their kids to yuppie private schools and living in mansions for a few years and are building fences and dog houses for 10 dollars an hour to scrape by. Right now in northern Idaho motor grader operators are clearing 30+ dollars an hour but for how long? I’ve seen people offering me jobs on indeed to run heavy equipment around SLC for 45 dollars an hour at times. But I doubt it will last. Some trades are a lot more stable than others. I always had a job machining or welding. Same with trucking. Heavy equipment, grading, logging, and construction not so much. Bid falls through, contractor runs out of money, whatever it was always something. When the getting’s good, boy is it good for a roughneck with no degree. When it slows, it is alcoholism, divorce and hoping from one rental to the next. Not so much my personal experience just what I’ve seen to boys around me. It’s the same old cycle too, right now a lot of guys back home are living high on the hog with new diesel “work” pickups without a scratch on them pulling boats or RVs and taking up 4 parking spots at the bars on the weekend. Saw it as a burgeoning teenager after 2009 when it all withered away.

You’re selling yourself short though in my opinion. This whole new paradigm of transitory this and no collapse that and permanent fed fixers… Eh, I don’t buy it. Everyone says it’s different this time but nobody says why it’s different other than we don’t have a subprime loan crisis and lending standards are “better” and this is just some global pandemic induced issues that will clear once we have herd immunity. The economy looked like it was on crackling ice before covid happened and I remember sitting in a bank with the teller saying I should close out money market savings accounts and open one of their weird trading deals that she couldn’t explain and I was expecting a crash in 2019. She was right up to and including now but I’m skeptical. Trump fueled the economy because he had nothing else to run on but for chants and the Facebooking numb-butt crowd. Biden doesn’t want to be Trump’s bag holder and the fed have painted themselves into a corner. We’ve cut taxes on the rich, passed some of it onto the middle class and gave the money printers a shot of nitrous and rained free money into the hands of the American people to the point of labor shortages. And somehow we can all sit around calmly knowing that nothing bad is going to come from any of this?

I’ll take my union job with amazing benefits that can’t hire anyone because we pay a couple bucks less an hour and set myself up for the long run rather than chase the last extra penny in wages working for slave drivers that will cut me loose the second things turn down. People are so short sighted. I’m betting on a crash and one of larger proportions than 08. Might be wrong, but if I am, I won’t lose as much as most other working class. And if it gets so bad that joe-blow can’t afford ramen while I eat walmart tv dinners, the ensuing riots in the streets will be far more important anyways.

The nature of capitalism is boom and bust cycles. I don’t think we’ve fundamentally changed much of anything in a handful of months time and a worldwide flu that we already have a vaccine for. I don’t see a new normal firsthand and I don’t see an explanation for a new normal and I also don’t see anyone even defining what this new normal is other than a couple of foolish ideas like no more recessions and we can just all work from home in a cabin in the woods using Tesla brand satellites and Tesla brand solar panels. You can’t bullshit and bullshitter.

You rent one and use it. It is a lost skill called self taught….

Certifications are worthless except in advertising…

I built two, still living with wife in the last one, finished in 1987.

Worked out great for me. Yes, a big project.

As far as books: the best one I found: Modern Carpentry. Very straightforward. Very basic. Very clear. Tells how to do everything in great detail, starting from foundation up. My edition was 30 years ago. Hope it’s still as good as it was then.

DO NOT use any book that claims their method is the latest thing, better than anybody else has ever managed to figure out except by the author who brags that their unique genius has greatly exceeded those dumb folks that have been building them for fifty years. I saw too many of these books.

Things are done the way they are usually done for a reason.

C10, and Tom,

Wonderful synopsis/summary for those starting out… I just hope you will extend your obviously extensive knowledge into the web as much as you can stand to do.

Taught Construction Technology classes at two side by each High Schools in CA many years ago, where I learned that ”most” of the drop outs were mostly bored,,, and got them to learn arithmetic and so forth with real live examples, and damn sure got them to understand they were NOT going to support a family with $10/hour wages,,, etc., etc.

NOW a days, with the advent of UT videos, mostly ”right on”,,, I can and do hope most folks will figure out how to build their own house,,, as I have done several times with great benefit!

Last time I was looking, admittedly a while ago,,, there was tons and tons of cheap land almost everywhere in USA other than the coastal areas.

Good Luck and may the Great Spirits Bless all the ”young uns” going forward. ( Including the young ”boomers.” )

Contractors, electricians, plumbers all need help. Go to any site. If they’re framing. Start with that. Drywall? Watch them. Carry mud for them. Electrician. Drill holes for new construction to run wire. They’ll teach you. Roofing. They’ll hire you on spot. Exactly how I learned. Did flat work and concrete too. Then start building. Eventually got my contractors license. I’m out of the building game now. But what I learned? Priceless. Electrical? I’ve got friends in all the trades. Can’t figure it out? I take a picture of my problem and they tell me what to do. Best thing I ever did. Roofing was by far the most profitable for me. And the hardest. Good luck.

You mention OTR trucking, implying you’re not tied to a specific location. So why would you pay $1800 for a 1 bedroom apartment with noisy neighbors when you can relocate to some place where rents are a third of that?

I’m a local route driver in the northwest US. Used to live in a “low cost of living” area. The issue is areas like that are limited in well educated and advanced jobs. Blue collar stuff in those areas is a tight market because the labor is everywhere. Good old boys can be quite skilled with their hands and tools despite a lack of formal education. I’m no different I was poor and worked a lot of odd jobs from heavy equipment, welding, car repair, framing, etc to make some kind of money. But it’s simple supply and demand. Everyone around you can do all this stuff so labor market is inevitably tight. Wages are surpressed and a lot of those blue collar jobs are under the table for mom n pop type outfits. I’ve worked 80 hours a week Monday through Monday for 10 dollars an hour flat rate that I have to pay self employment taxes on with no way to write anything off. After 2 hours of commuting to the job site both ways I’d sleep maybe 4-5 hours and barely have time to eat. Lots of boys on those job sites were smoking meth to keep that kind of pace. It’s a rough life to lead. It’s not really a life either, you end up existing just to work like a slave. And will only have maybe 500 bucks at the end of the week to show for it; wells that just sucks. Otr trucking is the same, 90-95% turn over rates and only marginally more pay then that.

So I moved to an area where skilled trades has a tighter labor market and suddenly I’m in a union job with amazing benefits, a pension if you can believe that, and more pay than I could have ever had before. The only issue with the whole ordeal is housing. Or even land for that matter as I could build something myself if necessary. The area I’m in has seen real estate jump 4-5 times since the bottom in 2013-2015. At least for the bottom end of the spectrum. Supposedly the multimillion dollar mcmansions aren’t inflated as badly go figure.

“The only issue with the whole ordeal is housing. ”

This is a very common dynamic…the best jobs being overly concentrated in a handful of mega metros with very overpriced residential real estate and punitive tax regimes.

As Wolf as pointed out, the Covid diaspora away from such places should help to lower housing costs (even, in the long term, in the destination metros since they have much better land availability).

This is why monthly rent surveys from Zumper, ApartmentList, etc are so valuable…they give a real time picture of where your money/labor can go furthest.

The “Covid diaspora” is over, and prices just kept going up in the cities that everyone was supposedly leaving.

“prices just kept going up in the cities that everyone was supposedly leaving.”

Factually inaccurate, per the surveys mentioned…just take a look.

In the last month or two, there may have been some leveling off or slight bounce up, but yr over yr most of the highest cost mega metros have seen marked declines (altho they started at such insane nosebleed levels, such mega metros are *still* the most expensive…but just by $500 per month vs. Prior $1500).

For me, the bigger issue is the 10%+ rent hikes in some dispersed destination metros…but hopefully those places’ lack of land constraints will lead to new building, lowering rents again over time.

Hey trucker guy- you’ve got your eyes open. You are surviving. And, you are doing it right on! Try to relocate with your union to another area where you have a chance to buy some property, but keep remembering that long term horizon is what counts to survive. I was able to do it twice, with bonuses.

I have been an astute observer of market and I can tell you buying because of FOMO is never good

It pays to have patience but not everyone has in them to be patient.

I also see long term deflationary trend

I don’t know if last 20year FED experiment shows deflation is impossible, what else can show you. 50T or 100T debt?

If you think 20yrs indicates a historical perspective, you need to study history…

“I also see long term deflationary trend”

in housing maybe..

but a halt to inflation, or a retracement of inflation, is not Deflation.

Who has ever seen deflation other than Big Foot?

The scare era of deflation….2009 to 2020…..CPI went from 214 to 254 …about 17% …wow, that was close.

You state the facts, unfortunately this is how the game is being played. The game is rigged. Your choice is to soldier on and hope you get lucky (ala the next GME, BTC…) or quit the game.

The Fed can print money but they can’t print wealth so those who do productive work must support those who are given conjured money for doing nothing.

The working class are left with the monumental task of supporting an ever growing army of government bureaucrats, an underclass who can’t or won’t work and the growing investor class who charge you $1800/month for your crappy apartment.

As more people become disillusioned and drop out of the productive work force the ones who are left to soldier on carry a larger burden and their voice is silenced at the voting booth as politician bribe a growing class of do-nothings with free money.

I’m a US citizen but I’m not a resident so I can’t vote and at this point I don’t care because opposing a tidal wave of free loaders is like bailing the ocean with a thimble.

Poor you having to suffer in a one bedroom apartment that costs $1800 a month (which is cheap and below market in the NYC area)… Its only recently that a 3000 sq ft house for a couple with no kids is the new normal in a 90 / 6 town (90% + white, six figure average income).

BTW, you forgot monthly auto insurance for that ‘$70K pickup truck with the 9 year loan’

Prices for EVERYTHING now are crazy but people ARE paying them. remember it is due to EASY CREDIT and millenials who are just a cookie cutter of one another

Nice to criticize millennials who are in a terrible situation due to the generations before them being greedy.

“Its only recently that a 3000 sq ft house for a couple with no kids is the new normal in a 90 / 6 town (90% + white, six figure average income).”

That’s exactly us. Except we have a (single) kid and the house is more than 3000 sq ft. I wouldn’t trade my white, high income neighborhood for any of those high crime cities

One possibility is that due to excessive debt and record asset prices we have a quick market clearing event later this year. Complacency is everywhere and asset prices are priced as if future is going to be trouble free.

If that happens it’s going to require courage to buy when the ship looks like it’s is sinking. Try to have a plan for what you want to buy and how much you should pay. Recessions can be a great time to buy nearly anything as there will be people that have to sell even at a loss.

Everything is getting more expensive, if and only if buyer strike is a thing then maybe the playing field could be even out a little bit but nope we just kick everything into the next high gear and let FOMO go into overdrive..

No wonder the people making these ridiculous monetary policy get away with everything..general public seems to get punch in the face everyday and our response is may I please have another please?

“… the people making these ridiculous monetary policy get away with everything…”

Indeed. The Fed and Powell wanted this to happen…INFLATION.

This was premeditated and intentional. And this is arranged theft, from one group to another. When central planners “decide”, they always intentionally assist one group and harm another.

The Fed is instructed, mandated to “stable prices”. Yet, when the Fed Chairman stands before a group of “journalists” and promotes an inflation rate, any inflation rate, there is no “Hey, aren’t you supposed to promote STABLE prices?”

Why isnt Jerome Powell indicted for the many breaches of his fiduciary responsibilities at the Fed?

Have Fed Funds ever been 4% below inflation?

Has the Fed ever purchased 30yr mortgages below inflation?

Markets are locked up (housing, construction) and we have supply chain shortages…..and we have a fake interest rate environment that has a lot to do with all of it.

Has a Fed ever partnered with a non pubic entity (Blackrock)?

Has a Fed ever dealt in non federally backed securities?

The Fed takes it’s instructions from the ultra wealthy.

You? You are the guarantor and the victim. That’s U.S. law.

My point is that there was an agreement as to what the Fed would do…and COULD do…

and both have been violated..

The Fed and the powers behind the Fed know that there is ..

no one watching

no one accountable

and that Congress, for the time being, is enjoying ever free dollar the Fed creates

Government will look out for its needs first, especially when times get tough. It’s our job to look out for our needs first starting with our own family. That by nature is in conflict with government policy.

If government becomes totally oppressive then black markets thrive. Its not really natural for government to be involved with every transaction between human beings.

because are PAYING those prices mostly for things that are unnecessary… Ex. going out for dinner 5 nights a week, buying a $45,000 SUV on a $50,000 a year salary, buying a new Iphone every year which costs $1399 + tax

I might be wrong, but is this not the main route we deliberately chose? Biden’s plan does not contain any measures to reduce debt, on the contrary, it will increase deficit and spending to unsustainable levels. This is only possible if the purchasing power of the dollar declines sharply thus the GDP grows faster than the government accumulates new debt.

So most likely this is not an error or an anomaly, but the new normal for at least a decade.

Was there a choice?

Was there a viable media approved candidate or party who was going to put us on a sustainable fiscal path?

Did Trump reduce deficits? Deficits were over a trillion prior to Covid!

Both parties are culpable. The media is culpable. The people are culpable. It’s an unstoppable rolling dumpster fire of doom. I’m glad I got out.

Our government has been working contrary to the interests of the United States as a whole, for several decades. You cannot decimate the jobs base by offshoring , and increase the labor force by importing millions of illegals and not expect it to have ramification across the board. Our corporate laws encourage and reward offshoring when they should be doing the opposite.

Lowering the interest rates and inflating asset values are a ponzie scheme to distract the attention of the masses until it is too late.

This massive debt that the government is running up must be serviced, and that will mean drastically higher taxes in the future.

The ever growing immigration will continue to displace Citizens at the lower end of the income scale increasing homelessness, crime, and the need to spend billions more supporting them.

Everything that is being done will have increasingly negative ramifications in the future and yet no one is calling the government and the lying media on the lies and deceit. Like they say, you get the government you deserve.

When you have a populace largely consisting of dumbed-down, high-fructose-laden mouthbreathers swallowing narratives hook, line and sinker, this is what you get.

What is this “mouthbreather” thing? I get it’s an insult, but I have no idea what it’s based on. Is it just your invention or did you pick it up from somewhere?

Inquiring minds want to know. I’m sure I’m not the only one.

When you are governed by tweets you get a nation of twits.

Reduce debt? Where were you when President Cheney and Baby Bush the Lesser started TWO WARS and cut taxes for the wealthy?

That was 2 decades ago and the bills will be coming for decades yet.

Reduce debt? Didn’t you just watch Covid Don (“It’s a hoax.”) give away TRILLIONS to the corporations (who were already making record profits) an and the 1%?

Reduce debt? What world are you living in? The corporations, the wealthy and the Military Industrial Complex will decide what happens.

Too bad nobody listened to President Eisenhower’s last televised speech.

I am still saving every single dollar I can and will continue to for the rest of my working days. The only discretionary purchases I make are 2 or 3 meals at my favorite deli per month, which is $60 total. I am saving 90% of my net income. Meanwhile, I watch mouthbreathers loading up on debt and talking about how msrp on a new truck is a “good deal.” I will be way ahead of these dillweeds in the long run.

Best are the ones who indulge in $7 half-caff/half-decafe soy lattes all day long while whinging how capitalism has failed them.

There is nothing more stupid than spending money on things you can make at home yourself. People spend 30. a class to sit on a spin bike for one hour. Then they go buy their lattes. I hear them complain they don’t have enough money. I don’t get it

Whereas if they saved that money every day, in a mere 39 years they would have $100,000, which will be the approximate amount required for the deposit on an apartment at that time. God bless our economic system! Muh freedom!

Maybe or maybe not.

Debt junkies never come out on top.

– “I am saving 90% of my net income.”

A truly impressive feat.

Might come naturally for all adepts of the “Know thyself” (c) Socrates.

That leaves a question of the savings management. But if you are not obsessed by money, let the inflation take it by an act of charity.

Are you familiar with Keynes’ Paradox of Thrift?

Speaking of Keynes…

even Keynes said that at some point stimulus must be restrained or even halted. I guess the Fed folk never read that chapter….and I guess MMT doesnt discuss that.

Keynes may be the most misunderstood, misquoted guy in history. (not yrs btw)

The Left tends to think his ideas amount to MMT and approves, the Right thinks the same and disapproves.

Keynes believed in balanced budgets, but balanced over the economic cycle, not year end. The government would spend during recessions, using the SURPLUS accumulated in the boom time.

Then politicians got hold of the idea. Keeping a surplus? Why not spend it?

Although overspending is usually associated with the Left, the US era of ‘deficits and debt don’t matter’ began with Reagan, who doubled the US debt accumulated over 200 years in 4 years, from one trillion to two trillion. But now this at least is bipartisan.

If everybody becomes thrifty, it affects the economy negatively, almost canceling the value of savings. However, this will never happen. Most people will always be foolish with their money. An individual who is prudent will reap the rewards of his actions. Keynes’ Paradox Of Thrift is a Straw Man.

Has it occurred to you that people might curtail spending because they have to?

Max’d out their credit cards, lost their job, upside-down on a mortgage they can’t afford?

Check out what I posted here about income, savings, and investment. Read it and weep.

The opposite end of that paradox is that when everyone lives beyond their income on credit, eventually they become insolvent and the economy crashes in catastrophe.

You cannot become wealthy spending your money faster than you make it….

Keynes Paradox of Thrift was a macro economic piece. It did not care about the individual armed with savings of sound money to protect from old age, hunger or an infirmity. Keynes perch was from the Fiat Central Bankers field of view which hates thrift and sound money. The whole point of a fiat system is to expose the peasants work product to an arbitrary system of fiat and fleecing. Engin-ear is worried about his future not yours or mine if we choose to embrace fiat consumption. Engin-ear has it right.

If we have deflation he’s right. If the inflationistas are right he’ll get hammered.

What else can you do, DC? I’m retired and still save money. What, are we supposed to just spend everything we make all the time and live like we are old time sailors on shore leave with pockets full of prize money?

You will be ahead in the long run. Just smell a few roses along the way. :-)

Concur. And savings can save your bacon when the unexpected hits. And you don’t know it’s coming because, dah, it’s ‘unexpected.’

But the trick is, how to save ‘money’ that won’t get eaten-up by inflation.

Isn’t saving money in a way that doesn’t get destroyed by inflation pretty straightforward? Put it in things that benefit from inflation. Also, if you have the means to store things, buy as far out as you are comfortable with. I like Darn Tough brand wool socks. $20 a pair. I know they’re going to get more expensive, so why not buy buy enough to last me several years?

Well the elastic in a sock is typically latex. That degrades over the years…

Easy. Diversify among non-correlated assets. Unfortunately the Fed has kind of messed this up by not allowing true discovery of the cost of money.

Divide your assets into cash, gold, stocks, bonds, real estate, etc. No matter what happens something will save your ass.

This will definitely cut your performance compared to any given metric. My strategy has underperformed the S&P 500 by 50% in recent years but at 68 and retired Rule #1 is Don’t Lose Money.

In this century stocks have been cut off at the knees twice and long term S&P 500 returns have not been impressive. I don’t regret my strategy at all.

We are all old time sailors on shore leave.

I wish but shore leave was a hell of a lot more fun than this!

The sailors that have the best time on shore leave are those that spend the voyage fleecing their comrades with cards and dice. This methodology is now used by government banks on land.

Yellin’ said quite a while ago, when she was head of the Fed – LOAD UP ON ASSETS! Sadly, the homeless did not comply.

The age old strategy may be the best you can do – diversify. RE, stocks, bonds, and yes, cash.

Yes, that is right, Yellin is looking out after your interests…. just keep believing that….

@Crush the Peasants

Just diversify won’t save any one, if there are no uncorrelated assets in the current ‘everything’ bubble mkts.

Uncorrelated predominantly with re S&P 500. That means even having some bearish positions, even though there is a cost for that. If one wants ‘downside’ protection, one has to give up ‘upside’ potential!

NOW that upside potential carries more risk than rewards. Flashing reds has become permanent staring at you. Btw, no one rings a bell, when the bear mkt starts,

(Been in the mkt since ’82)

anyone who can save is already ahead ,,,,,

Everyone can.. most choose not to.

“just smell a few roses along the way” You stole that line from the great Ben Hogan. Ben stayed ahead with the money and minded his own business well right until the end.

Over time, the debt will be paid for the price of a marble. Credit card companies will give easy credit to the indebted more than financially responsible. I wonder if the whole humanity in the hunter-gatherer period survived as free loaders from the mother nature without giving anything back. The polar opposite argument of the frugality is also a valid one. Money is a man-made concept. May be the top-brass in the feds see something good that we cannot see. Just enjoy the decline. It might be good idea to violate the rules and be sorry later.

worst case scenario: we go back to hunter gatherer world. and those people were in touch with nature. not so terrible, as you say. can the world support 7 billion hunter/gatherers?

Obviously we cant. Now, the population is reducing in the west compared to baby boomers. So are marriages and child birth in developed nations. Soon, the population will drop even in countries like India or China. The hunter-gatherer example is to say, in future, we may not need a huge forest to sustain the human race. US alone can produce surplus basic food. There will not be a lot of people to feed.

Living below your means and saving is a good thing.

Hopefully you are not putting the savings into cash at 0.001% – especially with inflation at least at 4%.

What do you suggest putting the savings in?

Others on this site have recommended I Bonds, and/ or paying down debt.

Precious metals are good. When inflation comes back with a vengeance, the price bump will cancel the loss of buying power. It’s a kind of insurance, not a stock or investment. Other than that, you can’t do much about inflation except to reduce expenses and increase savings.

i just cannot imagine why saving in gold is not the main choice. it totally dumbfounds me. i too save a tremendous amount of my income and have no real debt. the last few years i have bought tools, materials and equipment cos they are still cheap. but as for pure savings? to just sit there? that’s what gold is for. you hate the fed but you stack their notes? wassup with that?

and there’s another comment somewhere on this page about the rich hoarding all the money, which really brings us to the main conflict; that saving in money creates all kinds of social tension. saving in gold doesn’t have that problem.

anyways it just absolutely amazes me, watching this in real time, reading comments on blogs about inflation and wealth preservation and gold not being the number one strategy.

the shortages and price rises will come in waves and then all at once. for young people with no real wealth to preserve, my advice is skills. get some. if you want to stay busy just open a handy man service in any large city. your phone will never stop ringing and you will learn a ton about building and repair as well as money and people and law and language and yourself and work….and more.

Gold is one leg of the diversification table. Do you know what happens to a table with one leg?

I own gold and it is physical in one form or another. But I also hold cash, stocks, bonds (however repellent they seem right now), and real estate. Bonds have been problematic for me.

For instance, back in 2009 my daughter was dating a guy who worked for a hedge fund. I mentioned that I wouldn’t be surprised to see the long bond hit 1%. He didn’t say anything but I could hear his eyeballs rolling in his head. I was slightly off, but the 30 year did dip below 2% and the 10 year has not broken 2% for a long time.

I kept buying the 10 year until it fell below 2%. Who’d have thunk it would work out? I feel like I should dump my bonds but a little voice keeps whispering in my ear “You never know”. One day I’m gonna shoot that little bastard.

The time to buy bonds is when the yield is high, like 18% in the early Eighties. After the peak, you get back above market dividends for the term of the bond. Buying bonds at or near the bottom is asking for it.

@M. Gorback

Bonds offer buffer (in a portfolio) in case of flash crash or slow downturn. Once the GDP growth goes below 2% probably in after 4th qtr of 2022, bonds may be sought after. If nervous, reduce the % to your sleepong point.

Why not try etf – TDTF (FlexShares iBoxx 5-Year Target Duration TIPS Index Fund) or MORT (VanEck Vectors Mortgage REIT Income ETF) I nibble them slowly and add when they dip and try to park some of my cash holdings.Check them out at yahoo.finance.

If you live in the USA you have to buy stuff with dollars so at least your short term savings must be in dollars.

Gold even though it stays the same has a standard annual deviation of around 13% so it is best thought of as a long term savings vehicle.

Even though it’s a little hokey I like to use standard deviation an estimate for the time horizon for an asset so for gold it’s 13 year minimum and for sp500 17 year minimum.

Is that $60 a MONTH at that deli or $60 a week.. Where in Manhattan is this place??

$60 per month, $20 per lunch.

“I am saving 90% of my net income.” DC, PLEASE!….explain that trick, along with this “mouthbreathers” insult and source/basis.

Thanks, although I seriously doubt delivering verbal clarity is one of your abilities…..delivering insults and bitching/blaming seems to be about it.

Not that I care much if you don’t respond, and likely won’t.

“Paying even more to get even less.”

a.k.a. “Build Back Better”?

There are two kinds of people in America: those who survived the Carter administration in the 1970’s economy, and those who think the glamour of Studio 54 was the defining facet of the decade.

Average GDP growth per year under the Carter administration was 3.25%, compare to a more recent admiration such as Trump where average annual growth was 1.03%. All numbers in constant dollars.

3.25% growth, with 17% inflation is not a situation you ever want to be in, believe me…

You are not understanding constant dollars.

Long term growth rate for USA keeps getting lower since world war 2. The bigger government gets the lower growth will get because by nature government is focused on politics and not efficiency.

The concept of growth rate is pretty simple. The increase in the number of people working plus the average increase in productivity. Covid took a whack out of number of people working.

You are talking nonsense. I lived through it,

There was a lot more oil around when Carter was president.

What! The US is more oil independent now by a long shot than it was in the 70’s, apparently you never heard of the oil embargo that resulted in skyrocketing gas prices and major shortages and rationing…

I was partying heavily during the Seventies, and did not even realize that the economy was fuxored. As Flip Wilson said “What you see is what you get”.

The thing is is that no criminality of top import EVER gets their peepee whacked!

So go ahead. Compare and contrast the Carter economy to the economy of today, or the past 10 years. Tell us which was better for people willing to work.

Carter allowed badly needed austerity to take root and he put Paul Volcker in charge at the Fed to finally snuff out inflation.

Reagan showed up and fired Volcker, put Greenspan in charge and began the government policy of “deficits don’t matter”.

Carter saved the country from an inflationary death spiral brought on by LBJ/Nixon/Ford. The price for saving the economy is being dragged through the mud. For those with integrity that is a price worth paying.

Wrong, wrong, wrong. That is some real revisionist history you got going there pal.

Carter appointed Volcker but then handcuffed him. Volcker tried to impose his interest rate hikes in early 1980 but Carter made him back down. Volcker started them back up again in November 1980… just three weeks after the election was over. Reagan (who had a degree in Economics let’s not forget) let Volcker impose the medicine and we got the Recession of 1981-1982 as a result… and FORTY YEARS of no real inflation to speak of… until now perhaps.

Carter did NOTHING to save us from the inflationary spiral. Or nothing EFFECTIVE at least. All four years of his one term, inflation was 6.5% or higher… and it was higher each and every year of that term… ending at 13.55% in 1980.

And far from “firing” Volcker, Reagan reappointed him in 1983. I think that Volcker felt pushed out at the end because he didn’t get reappointed to a THIRD term as Fed Chairman… but it certainly wasn’t because Greenspan was a loose money advocate as he prove in 1991 to George H. W. Bush’s detriment.

Nor did Reagan begin a policy of “deficits don’t matter.” He had a war to win… and wars cost money. No one criticizes FDR for deficit spending to stop right-wing totalitarianism… but there are those who are appalled that Reagan did the same to stop leftist totalitarianism. They tell us more about themselves than they do either FDR or Ronald Reagan.

SpencerG said: “and FORTY YEARS of no real inflation to speak of… until now perhaps.”

———————————————-

Money expansion (inflation 1) and rising prices (inflation2) has been continuous over the past 40 years.

The recession of 81-82 was only about 9 months long, followed by the Eighties. Life was good then.

It’s mind-boggling to me that people will defend Reagan still. Propaganda is a hell of a drug. If there is a god, Reagan is burning in hell as we speak

cb…

There is always supposed to be SOME inflation. but in the eight years prior to Reagan’s election it exceeded 6% seven different years (and reached 5.74% in the other year)… and got as high as 13.55% in 1980. In the 40 years after the Volcker medicine was applied, it NEVER exceeded 6%. In fact it only exceeded 5% one time (in 1990 which prompted Greenspan to jack up interest rates and brought on the 1991 recession). It only exceeded FOUR percent in 1984, 1988, 1989, and 1991.

Even with those small outliers, the inflation rate since the end of the 81-82 recession has averaged only 2.76%.

Spencer G

Right you are … thanks.

SpencerG said: “There is always supposed to be SOME inflation.”

———————————-

FED and Bankster/Wall Street propaganda.

@ historicus –

Reagan: Many love him, but part of his legacy

1, deficit spender

2. amnesty granter

Greenspan: Gag. Need I say anything?

Inflation: Have you not noticed?

phoenix…

“Defend” Reagan? I am happy to praise Reagan to the moon and stars. He was quite simply the best President of my lifetime… and his understudy (the first George Bush) wasn’t half bad himself.

The Baby Boomer presidents who have followed have been pale imitators to the throne. I am always laughing at how they bounce taxes between a range of 35% and 39.6% and act like they have accomplished something. Ronald Reagan is like, “Hold my beer.” When he took office:

-The top tax rate was 70%…he got it down to 50% and then 28%.

-There were SEVENTEEN tax brackets… if you or your family got even the slightest pay raise it got taxed at a higher level. Reagan got it down to TWO brackets… but it is now back up to seven.

-And because of inflation you were definitely going to get taxed more… the income tax brackets were not indexed for inflation!!! Reagan fixed that and there is no politician alive proposing to undo that reform.

In addition to all of that, he defeated the Soviet Union with nary a shot being fired, rebuilt America’s military, restored America’s standing with other nations, extended the Social Security Trust Fund by 40 years, negotiated a tax reform that cleaned up the tax code, defeated inflation (or let Volcker do it), and put the American economy on an entrepreneurial high tech glidepath that it remains on to this day.

Not for nothing did Barack Obama call Reagan’s presidency a “transformational” one. Combined with George H.W. Bush those twelve years created the very world that we live in today. The Baby Boomer presidents have tinkered around on the edges… but by and large they haven’t been able to undermine it… despite some concerted efforts they have EACH made.

Liberals love to revise history to the way it never was….

Spencer-

“…those 12 years created the very world we live in today.”

Same one we are all here bitching about?..

..or am I just being “revisionist”, Jdog?

Everything is built on the past, but not just 12 years. If you believe that, you not dealing in reality. Every time there is an election there is the opportunity to change the past. The fact is the Congress has far more to do with the condition of the country than any President, but then you need to understand civics to realize that..

“Everything is built on the past”

What keen insights you have!

I’m out of my mental league, I defer to your wisdom and complete understanding of “civics”….I must have been asleep in grade school.

I don’t see any inflation here in central Ohio. I think it’s because inflation hasn’t started talking about talking about coming to flyover country. and no, that last sentence wasn’t a typo.

Much of the “growth” of the past years is actually inflation. Think about it: real GDP growth is calculated by taking nominal growth and correct that for inflation. If inflation is consistently under-reported, that means that real growth is also consistently lower than reported.

How real is GDP if roughly one third of it is government spending…? and spending newly created money from deficit spending?

Printing new money, then spending it is a barometer of the health of the economy? Or is it an indication of a “life support” system allowed by the Federal Reserve’s machinations?

Right, exactly. I’m so tired of hearing about the economic “recovery” or how the economy is “booming.” Of course you can get “booming” numbers if you borrow and print money and then hand it out.

But the consequences don’t come until later.

Things are booming here in Swampland. The county dropped Covid restrictions and everyone is out there spending money like drunkin sailors. Traffic jams are back. My Irish pub was playing hard classic rock live music and the place was packed wall to wall. It was hard to find someone to serve you a beer. You can;t even get a tee time on the golf course.

You doomsayers are off the mark. Its Weimer time a la 1924! Get with the program! Screw the future. There ain’t any. Enjoy the present!

Swamp Creature,

Fed’s have emergency force Fed a lot of cash into society. Once stimulus is over we have to go back to a debt ridden economy with poor demographics.

We have a nominal 4% economy addicted to stimulus. Assets can’t keep growing at double digit rates. The bad debts are going to have to be written off and assets adjust to reality.

Right! The only two sustainable sources of growth are population growth and productivity growth. And of these two, population growth doesn’t benefit the individual so it is really only about productivity growth per capita.

Productivity growth can come from innovation (working smarter, using machines, using slave labour, etc) or from working longer.

That’s it!

@ YuShan –

Productivity growth often doesn’t help the individual either, more and more so these days. It all depends on the distribution of that productivity growth and that benefit often disproportionately goes to the asset owning class.

We have a concentrated wealth and power problem, consciously nurtured by the FED, allowed by owned lobbyists and politicians. The result being a debt slave society over-lorded by a rentier class. Interspersed we have groups that are making it, which keeps the system glued together.

Working people don’t generally get the benefits of productivity.

That’s the problem we’re not solving, YuShan.

Takes a lot of skill and effort to capture the benefits of your productivity, and most of us (currently) don’t have what it takes to do so.

Therefore we must accept what the people who actually do know how to capture the benefits of productivity are willing to offer us “laborers”.

If you think productivity growth benefits workers in any way you need to study the increases in profits vs the increases in pay. There is a divergence big enough to drive a fleet of tankers through….

Make your eyes bleed:

“APRIL 2021

The U.S. productivity slowdown: an economy-wide and industry-level analysis

Labor productivity—defined as output per labor hour—has grown at a below-average rate since 2005, representing a dramatic reversal of the above-average growth of the late 1990s and early 2000s. The productivity slowdown during these years has left many economic observers wondering why this situation has occurred and what factors may have contributed. To clarify potential sources of the productivity slowdown, this article presents an analysis of labor productivity and its component series—multifactor productivity, contribution of capital intensity, and contribution of labor composition—at both the economy-wide and industry levels, complemented with a survey of the contemporary productivity literature.”

bls DOT gov/opub/mlr/2021/article/the-us-productivity-slowdown-the-economy-wide-and-industry-level-analysis.htm

@cb, @Tom Pfotzer, @Jdog

Definitely agree! I was just pointing out which factors grow GDP in a durable way. But GDP is just what it is by it’s definition and it is not a good measure of how well the general population is doing economically and socially. (You may have noticed that I mentioned using slave labour as a way to increase productivity)

Productivity growth per capita in the strict sense does not reveal any increase in wealth per capita. Productivity per capita is quite limited by physicality issues of the individual. What is most revealing about the “distribution” and “redistribution” issues that are revealed in that decrease in productivity is found in investigating the sales of supposedly family-owned businesses in the US, and in land transaction sales. As more and more business are NOT owned, and more and more land is NOT owned by citizens, productivity per capita will continue to decrease. Redistribution of any wealth extracted by any opportunities to extract real wealth from US commerce activities is going increasingly out-of-the-US, and primarily to a few Multi-National entities.

“The U.S. productivity slowdown: an economy-wide and industry-level analysis”

This is a perfect example of cherry picking data. In the 90’s and early 2000’s computers were just coming online and were increasing the productivity of the workplace by bounds. An office employee with a computer and a few programs could replace 3 or 4 workers from previous times. Of course that unusually high level of productivity gains could not be sustained, but if you look at say a 100yr time period, productivity is near an all time high. The problem is all the profit from those productivity gains have gone to the top 1% while the rest saw a decline in wealth.

Productivity growth requires more available energy. We’ve maxed out the oil so we are fcked.

Fake it till you make it. Works for business I think the government is giving a full 110% effort.

There are a lot of programs out there where extra money is being hosed to the people. PAU, Stimulus, QE, suppressed interest rates…

This is an experiment that will be studied for 100 years

@ historicus –

the more I read you, the smarter you get ……..

you and the missed commenter, Unamused,,,,,,, bastions of common sense …………. and solid knowledge to back it

Because government spending is 1 of the 4 addends used to compute GDP?

The whole thing is a zombie.

Only this is not a movie.

@ historicus –

the more I read you, the smarter you get ……..

you and the missed commenter, Unamused,,,,,,, bastions of common sense …………. and solid knowledge to back it

Yep, Yushan, it’s smoke and mirrors. The debt increasing at a high exponential rate is just a necessary measure in order to sustain the illusion of achievement and prosperity, even as we drop off from the artificial and unsustainable boost of the past couple of centuries.

And still most like to sit around and blame their own favourite local political targets for the growing instability, inequality and insecurity in their particular locality. But the rising tide of discontent is not just some local or national concern, but rather a broader global trend that transcends political regimes ruling some given place.

If we were smart we’d be looking for more fundamental causes for the issues we face. Changing policies within the existing framework of thought and trying to paper over symptoms we observe will get us nothing but even more pain eventually.

I would claim that we have a problem with our expectations as to what the future can and should bring us, and we have a problem with our marriage to an idea of what we call ‘economic growth’ as being necessarily a positive outcome…

These graphs look like the perfect boom-bust cycle setup to me. If the high prices stick, I see stagflation ahead because people are simply getting squeezed. If as a result companies go bankrupt, then we could get a debt deflation spiral.

In the past decade, we have seen massive asset inflation combined with relatively low CPI inflation (per official calculation). But the opposite is also possible: massive asset DEflation while CPI inflation is high. Perhaps that will be the next stage. Central banks will be powerless to stop that.

Quite right. And, it is a whole loat easier to squeeze the life out of one little bug at a time, than a whole lot of bugs all at once. The mess is a lot easier to hide, and clean-up too. Strategy counts, especially with an invisible hand, and a fly-swatter. You gotta watch where you hit, when, and what. Who designs the fly-swatter, cleans up the bug, and how long the fly-swatters holdup in real time counts. Cheap ones, and poorly designed ones don’t last long.

It is good to know some hard facts about inflation like the national average.

Its main quality is availability (yet some would criticize the design).

My understanding is that there are not many insights to be inferred from it. It is just an invitation to look closely to discover what is happening.

It is primarily an accounting KPI, certainly correlated with uncertainty and peaceful wealth transfer+destruction. Peaceful means in comparison with alternative methods.

So it is a game changer.

Now the game could be changed peacefully or violently. The failure to predict the food riots is bad. The ability to provide the cash lifelines with credits or stimmies is good.

We could also choose to follow the variation of GDP per capita to judge the prosperity creation over time, but we don’t do it.

We could also follow the variation – and the number & % – of people under poverty line, but we don’t do it.

Instead of GDP per capita, I think median real wage would be a much better indicator because wealth is so concentrated.

That helps to establish a correlation, especially to PPP, and changes in real poverty indexes of specific nation. Presently the correlation is based on the USD as a relative reference point. The PPP from the OECD conversion rate website also helps. There is little easy access to the correlation points that really report the real opportunity to any wealth in any nation. Productivity, and wages alone do not reveal true long-term wealth, of the mundane examples of wealth that are commonly used. The real essential wealth items water, air, and land that can support life, and not only man’s life.

Even if inflation isn’t transient, it’s time central banks stop funding government spending to address asset price inflation. It’s exacerbating wealth inequality and creating a huge divide between asset owners and people who live from pay cheque to pay cheque.

Inflation is theft of previous labors (savings) and current wages.

It has been promoted by the Federal Reserve and the policies they implement.

Thus, it can only be described as a prearranged theft.

What I see on both the personal income and total spending graphs are some aberrant swings with a return to the pre-pandemic trend line. Actually income returned to the trendline in late 2020 and then went haywire, probably due to stimulus checks.l

Just put a ruler along the steady pre-pandemic segment and look at where both income and total spending are now. It’s pretty close to a straight extrapolation. Give it another month or three and see if the shakeups induced by relaxation of covid restrictions normalize. Powell just might turn out to be right.

What would throw sand in the gears of this hypothesis is if they keep handing out free money. Then those charts will continue to gyrate.

I’d like to see the income and total spending on the same graph. It looks to me as though the long-term income trend line has a steeper slope than total spending.

My pets and farm animals are looking for hand-outs and treats, they live for them, people aren’t supposed to do that, we’re supposed to commit to something and try to be productive. I was a teacher, a grueling demanding and sometimes demeaning job but I tried to find ways to help kids learn to read and write. Now teaching is beneath the dignity of most college grads. Instead, we get “stimmies”. Bah, humbug!

“Instead, we get “stimmies”” ….

I think Larry Fink et al would agree with you on that ‘$core’.

“Give it another month or three and see if the shakeups induced by relaxation of covid restrictions normalize” [normalization of the trends relating income to total spending].

If those trends do revert to “normal” that might not be a particularly good thing. Because along with those normal income/spending trends, total revolving consumer debt was on a long-term increase. So the previous normal relationship between income and spending was not adequate to stop the overall death march toward the debt crisis cliff.

I didn’t say that persistence of the trend was good or bad, just that Powell might be right that this is a temporary shakeup.

I think my posts have been quite clear that we’re in a horrible long term trend no matter what has transpired in the past few months, and that debt is the main obstacle to economic recovery.