There is already a sudden and historic housing glut in San Francisco.

By Wolf Richter for WOLF STREET.

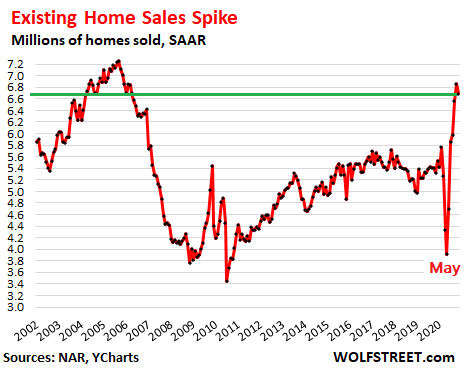

That the housing market has gone crazy in many parts of the country – a phenomenon of the Pandemic stimulus extend-and-pretend forbearance free-money foreclosure-ban economy while households reported a loss of 9.0 million jobs in November, from February – and that this crazy housing market couldn’t last has become apparent to everyone months ago. In October, Redfin CEO Glenn Kelman said just that. It wasn’t “sustainable,” and “there’s no way it can last forever,” he said. So today we got another dose of crazy housing numbers, with the first dip since all this started in the spring.

The National Association of Realtors reported today that sales of existing homes – single-family houses, condos, and co-ops – dipped 2.5% in November from October to a seasonally adjusted annual rate (SAAR) of sales of 6.69 million. But given the explosion of sales in the prior months, sales were still up 25.8% from November last year (data via YCharts):

In terms of monthly sales, not seasonally adjusted and not annualized, 442,000 homes were sold in November, up 21.4% from November last year.

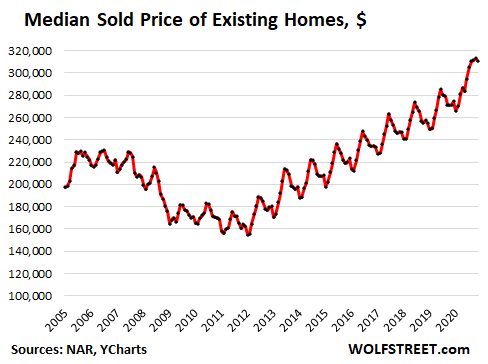

The median price of existing homes in November jumped 14.6% year-over-year to $310,800, with house prices up 15.1% and condo prices up 9.5%.

Over the past five years, the median home price has risen 42%, outrunning by a huge margin the wage gains of just about any category of wages, from the top 5% on down.

Since the median price is skewed by a shift in the mix, and with red-hot demand for higher-priced homes in this special economy of ours, the price increase could be partially a result of a larger portion of higher-priced homes in the sales mix.

And the seasonality of the median price has been upended. The median price normally peaks in June (the high points in the chart below), but not this year. In 2020, it peaked in October, with November being the first dip (data via YCharts):

“Given the COVID-19 pandemic, it’s amazing that the housing sector is outperforming expectations,” while “job recoveries have stalled in the past few months, and fast-rising coronavirus cases along with stricter lockdowns have weakened consumer confidence,” said the NAR report.

“Amazing” is the word. Echoing Redfin’s Kelman words that it “can’t last forever,” the NAR report said it will carry “well into the new year.” So five months? And then what? Those are rhetorical questions.

At the same time, many homeowners are struggling with their mortgages: 2.7 million mortgages are currently in forbearance, according to the Mortgage Bankers Association, and the delinquency rates of FHA-insured mortgages, which support the lower end of the market spiked to a record of over 17%, including mortgages that were delinquent before they entered into forbearance.

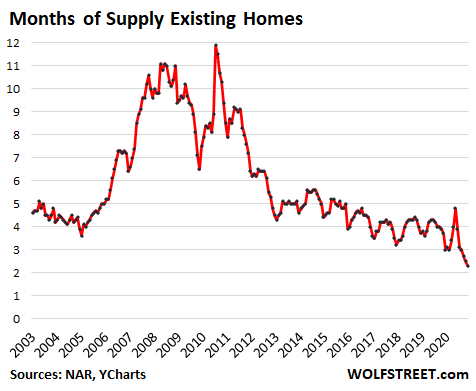

A lot of unsold inventory always gets pulled off the market before the holidays, to be put back on the market in the spring, which makes the “days on the market” look a lot better. Sharp seasonal declines in inventory are the rule this time of the year, but this November was nevertheless special.

Total inventory for sale at the end of November declined to 1.28 million homes, down 22% from November last year, for a supply at the current rate of sales of 2.3 months, an all-time low (data via YCharts):

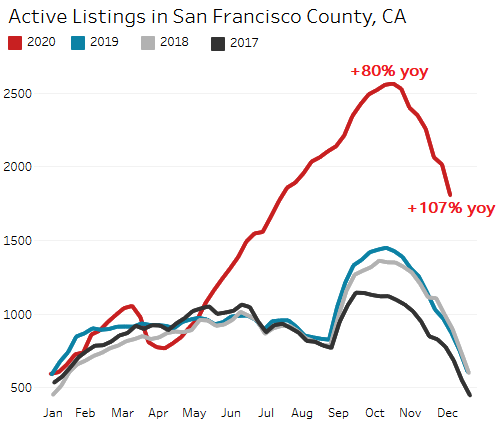

But real estate is local, and inventory isn’t down everywhere. In some cities, inventory of unsold homes has surged. This includes San Francisco, where there used to be a housing shortage until there suddenly was a historic housing glut.

In San Francisco, inventory of homes for sale has exploded to a record over the summer, peaking seasonally at over 2,500 homes in early fall, the highest ever, and up 80% from a year ago, according to weekly data from Redfin.

As the seasonal decline in inventory kicked in over the past two months, the glut, when compared to the prior year, increased further. In the week through December 13, inventory at 1,805 homes for sale, was more than double the inventory during the same period last year:

Some of these people who put their homes on the market recently had bought a home elsewhere earlier, in outlying areas or in other states, along with the national buying panic. And they now own both homes.

Condos, which are often used as investment properties, are particularly in a glut in San Francisco. There is talk that many condos that were used for rentals or vacation rentals have hit the market, as both of those segments have taken a huge beating, amid surging vacancy rates in apartment towers and amid rents that have plunged by over 25% since June last year. And with the high carrying costs of condos, the condo math collapses under these conditions.

And we coined “Management by Zooming Around.” Which is what Oracle’s Larry Ellison is doing. Read… California “Techsodus”: Tech Companies, Billionaires, Millionaires, Tech Employees Flee San Francisco & Silicon Valley

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interesting that it looks like many who fled to the countyside thought they would be able to sell their “Frisco” home easily. Could many of them, who now feel safer in their new homes, now have two mortgages and be facing doom if they can’t unload……we will see…..

They should transfer their Prop 13 property tax exemption/reduction/previous decades acknowledgment of taxes paid/gratitude to the country house, pull a second mortgage on the San Francisco house and use the money to pay off and improve the country house. Let the bank have the S.F. house. Do it now before values plunge!

re: “They should transfer their Prop 13 property tax”

I think Prop 19 has effectively eliminated this dodge (for second/vacation homes), but I’m not sure (even though I attended a 3-hr webcast on the subject from my estate lawyer).

BTW, guess who ‘championed’ Prop 19? If you guessed realtors, you win the prize.

You attended a 3 hour webcast and your still not sure about the subject? Sounds like you wasted 3 hours.

Glad to hear you understand all the ramifications of every complex subject instantly (I’m sure you’d make a great brain surgeon after a 3-hour webcast). A lot of us have to work at it for a while.

I understood the ‘subject’ well, but even in 3 hours they didn’t cover my specific case, since it was geared entirely to dwellings (first/second/vacation homes). I have a significant piece of property–a small ranch, with what will eventually be my home–and also a rental property. The lawyers didn’t touch that specific case. And, like every ‘proposition’–there’s a couple of meanings here–that was essentially written by a lobbyist group there will be hidden gotchas.

Realtors pushed this bill because they know it will trigger a lot of sales when heirs realize property taxes on Mom & Dad’s little vacation cabin will go asymptotic.

Before they may have had just 1 home with an underwater mortgage… now they’ll have two… lmfao

sarcasm?

typo, now fixed

Be positive Wolf. YES WE CAN.

Yes we can:

– inflate the asset bubble

– inflate the housing bubble

– inflate the debt bubble

– inflate corporate profits

Why, because of the dollar hegemony… and if you don’t like it, let me introduce you to a few of my friends, Nimitz, Eisenhower, Vision, Lincoln, Roosevelt, Washington… just to name a few. They’ll remind you why you should love the dollar.

If you can predict the future why you ain’t billionaire????

To me, the current froth reminds of me the last froth 12 yrs ago and I expect another crash…err, I mean, adjustment.

Just curious, are people really getting mortgages off of “apps”?!?! I see those rocketmortgage commercials and I think “No…., it can’t be.”

I’d suggest when making the biggest most important purchase of your life, you not do it at the height of a bubble or with an “app”!

I like to think you’re right…in this kind of insane environment, hard to make sense of it all. Group think is a dangerous thing and this market surely are creating a perfect perception that it can last forever, either that or I am suffering the worse case of cognitive dissonance ever when it comes to house prices or stock market (At least I am not alone judging from the readers on this site :P ) Everyone around me is buying..co-worker buying a house in OC, cousin in law bought a vacation home in Tahoe, I wonder if these people ever think about the economic disconnect out there and how much confident they have in their precise little white collar job.

Wake me up when this twilight zone episode is ever over..

re: ‘Just curious, are people really getting mortgages off of “apps”?!?! I see those rocketmortgage commercials and I think “No…., it can’t be.”’

I’m not much bothered by the idea of getting a mortgage on an app (there will be plenty of ‘paperwork’ later). What bothers me is the implication that buying a house is as simple and inconsequential a transaction as ordering pizza.

My friend worked on a project with one of the big banks to streamline the mortgage process to a fast paperless transaction working with Fannie Mae I believe. She said it was technically possible to do the whole transaction in two days.

Went with my friend to a used car purchase and it was all done on i-pad.

It’s a little like using credit card at first it doesn’t seem real and you can electronically sign a lot of important documents real fast.

Yeah, quite an improvement. But then, few ever actually read those documents. They just sign them because they “trust” the seller.

I didn’t make my point clear (my bad):

There are endeavors that, unintentionally or otherwise, have various roadblocks–aka ‘friction’–to achieving a goal; e.g. airline pilot. Before you become a left-seater in a Boeing or Airbus at an airline, you will have to endure decades of expensive–and sometimes arduous–training, low-paying regional jobs, a series of furloughs, etc. Rightly or wrongly, this regimen requires intense dedication and a will to succeed (though it doesn’t necessarily mean all will have ‘The Right Stuff’). Same can be said for buying a home; it’s not like buying something on Amazon, with a ‘no-hassle return policy’ (unless you count ‘jingle mail’). In the early 2000s, a proliferation of ‘NINJA Loans’ and a house-buying spree led to the GFC.

I’m not saying buying a house shouldn’t be friction-less, I just think it should be more considered than buying toilet paper (though online car-buying seems to be doing OK). The TV commercials showing a couple deciding instantly that they need a bigger house because the kids are getting rambunctious are particularly irritating to me. I hope it all works out.

I have never seen this much housing strength in a Christmas week. If anything decent appears, the buyers are all over it. There is a chance we are entering a higher inflation cycle than we have seen in decades. I put those odds at 1 out 3. Furthermore, I have never seen homes north of 4M have so many bids. The spring should be very strong. Three factors are driving this … easy money policies, outsourcing friction, and massive regulation reductions by the current administration.

Housing regulation adjustments? Like what?

Executive branch regulation reductions which caused US business to outperform expectations. If the regulations were not reduced, we would have seen a much weaker economy and house prices would have been trading off.

Which regulations were deregulated at the federal level that specifically impacted housing?? Or are you just speaking broadly that a deregulated economy will boost housing sales? Cuz i think those are different things & room for debate on Free Market effects on housing.

You don’t have to be Adam Smith or John Maynard Keynes to understand that allowing unregulated/unfettered and rampant corruption, destruction of our environment and ‘anything goes’ capitalism is a great stimulus (the drug cartels figured this out long ago). At least in the short term.

Sorry Jim that doesn’t cut it. Just cite one specific regulation reduction.

Agree, those three things are all bullet points in rebuff of higher prices, which will never materialize. The Fed will keep mortgage rates low, Trump throws a joke tariff on Vietnam on his way out, and the dreaded regulation onslaught that always comes with a Democrat in the WH, won’t happen until housing bubble III has popped. Corporate tax clawbacks are years down the road, now that RE is a hedge fund industry. This is a depression we are in, but like always it’s not a depression for everybody.

Did you run those odds by the Vegas bookies? Or you just making this stuff up?

PS: I knew you just couldn’t stay away from an article like this……

Is the skyrocketing stock market a factor? Many tech stocks have tripled or more this year.

Was thinking that too. Could be the ‘wealth effect’ that paper gains in the stock market have, leading to people feeling they have more cushion so spend more.

The sad history is that easy monetary policy causes gets us into boom and bust cycles that do more harm than good. We have added a lot of hot air to asset prices and not much real economic improvement . I read somewhere that since the last bust, retail sales are up 40% and stock market up 400%. That’s a one time paper gain.

“The sad history is that easy monetary policy causes gets us into boom and bust cycles that do more harm than good.”

More harm than good for the average person. Two steps forward, one step back for the wealthy. Look at the relative wealth plot to see that. There are great real asset bargains for them during the bust phase. And this also allows pols to promise and spend far more than tax revenues allow. SO, anyone in a position to reform things simply doesn’t want to and the general population is ignorant on most any topic, especially this one.

Good news for landlords. All of us poor saps who thought we were getting close to actually owning a home are now like “I can’t afford one now” and the economics of renting are looking better and better.

Bad news for landlords. You’re going to get screwed.

I wanted a home so badly when I was just married and living in an apartment. Now I am at the other end of life I realize it’s usually not that cut and dried. In fact, it’s probably not possible to make a good financial decision about it without having a long term plan for your life and using a computer program with ten or more variables. Most of the time if you are a couple there is a lot of emotion and excitement involved and the decision is not a rational one.

Depends SO much on individual circumstances/preferences OS,

Inlaws bought a house (for $10K) when he came back from Korea and they were married; she still lives there at age 90, with prop taxes limited to 3% per year rise, and is doing well living only on SS income and a paltry bit more from CDs.

(He died at 93.5 January, leaving their kids owning their own homes, all with good enough incomes, etc., etc.)

OTOH, some folks I know have bought and sold many homes in that period of time, mostly making good profits, after always fixing/improving the house/property.

Different strokes for different folks,,, and you pays your money and takes your chances to grab the brass (now gold I suppose) ring.

It doesn’t surprise me at all. Everybody’s discount rate (interest rate) is at an all time low. Of course asset prices have surged.

That’s a part of the disconnect between wage growth and house prices. But even considering this it doesn’t bring the 2 close together. I guess the monthly nut looks like a bargain.

Your Median Sold Price of Existing Homes graph reminds me of Robert Beckman’s 1980’s book; The Downwave . . . which postulated that house prices will follow Catastrophe Theory . . . a long period of growth, a setback, then additional growth, (as illustrated in the graph) ; before the entire system collapses back to 1939 price levels, which levels will need to be revised relative to the ~35 years since his work was published. Food for thought?

I can’t wait to see the look on the face of the house flippers , bankers and RE agents when house prices go back to 1939 levels.

You are right you can’t wait for that… because it is an event that will never occur.

Everything is confusing to me!! I think it’s best to not do anything right now Something is coming!!

Cmoore

Unpucker & take a deep breath.

News from the outside world: SOMETHING IS ALWAYS COMING.

Take it to the bank.

Yeah, as in a dark and stormy WINTER! Better watch out too, Kiddies .. THAT ain’t no candycane O’l Krampus be swingin!

Oh I want to believe this and large part of me still think this is the reality…however the other part of me is saying, market can stay irrational longer than you can stay solvent. With eggs on my face for pretty much a decade being the only one among most of my friends that held out on buying into this crazy market. The rational side of me sure do starting to feel like those Q’Anon believers. I guess if the market does pop but it won’t happen in my lifetime then it’s all relative since I won’t live long enough to see reality sets in anyway…

“and that this crazy housing market couldn’t last has become apparent to everyone months ago. In October, Redfin CEO Glenn Kelman said just that. It wasn’t “sustainable,” and “there’s no way it can last forever,”

I’ve resigned to never owning a home. I’ll just rent until my kids get to college and then I’m dropping out. I’ll live in a van, who cares.

p.s. I did own a home once, in New Zealand, so I’ve had the experience. Housing prices are crazy there now too.

Fellow priced-out renter w/young kids here too.

I haven’t given up yet. I’m so obsessed with housing affordability that it’s what brought me to Wolf & I even want to switch careers to work with homelessness &/or urban planning. It’s such a frustrating topic, especially when you watch your city & neighbors vote down new housing developments (for whatever NIMBY reason they come up with) knowing that they are directly contributing to unaffordability. So many homeowners climbed that latter & then pull it right back up after them.

NIMBYism is strong in this country, that and individual Murica freedom. Look at how wonderful our CV19 numbers are, a perfect illustration of how both are at running rampant in this society.

I am with you on that, sadly housing even though it’s a necessity is just another chip in this crazy casino, I can’t wait until water and air becomes commoditize just like housing. How much do you want to pay for the air you breadth? Better get in the market now, buy low and sell high…

Nimbism-

Our street is in a mini housing construction boom, with what was formerly a 2 block 2-growth forested land trust that was sold a couple yes ago, now being filled in with SFHs.

I’ve raised a few chickens (laying hens, no cocks), and kept bees for the most of the time we’ve been here since having bought (and paid off the mortgage) our humble abode. No lawn, mostly edible space (think Russian kitchen garden (raised beds front and backyards + berries and fruit trees .. with some ornamental areas spotted here there. The house is nothing special. I live for the personal outdoor surrounds, with provide a bit of sustenance for me, mine, and whomever I feel giving to, including the wildlife, mostly neodinosaurs and beneficial insect lifeforms – anything really, except those hooved rats .. othewise colloquially known as ‘deer’.

Soooo … with all the, uh .. impending ‘neighbors’ residing close by ….. will they be all good with it … or will the hot, fetid breath of NIMBY come calling, under the guise of municipal code enforcement via ‘citizen’ complaints .. and ‘Property VALUES at ALL COSTS !!!’, killing what little I have that makes life on my little spect of Gaia tolerable???

I hope not to fine out.

Around the world there is a long tradition of owner-built housing. Developers and contractors have worked overtime to impose regulations making this difficult in the US, in most places, but not all.

I predict owner-built housing will return. Unfortunately most of them will probably be tar paper shacks built out of desperation.

I realized the other day that I am just too rational to be a profitable investor. I am in that same boat. Sucks to be me.

Here is the thing, if you are trying to time housing market, good luck. It just never happens. The decision needs to be based around your current circumstances. When we bought in 2007, we had no idea the market was going to come apart in 2008, and not recover until 2011. But like many people we stuck through with it.

In the end, Wolf said it best, don’t think of a house you like a stock where you look at price every few minutes. You live in it, and that’s what it’s there for.

There is also economic reality, nothing wrong with renting if you’re in a favorable market like CA these days. Seriously, you can negotiate, and better yet, the government is backstopping people with eviction moratoriums. (I personally think that’s wrong, but my opinions doesn’t factor into it, it’s just reality). If you feel secure enough, buy and stop worrying about the drop. Heck, imagine if you lived in SF, one of the reason never to buy is you don’t know when the next earthquake will hit or how severe it’ll be. If you worry about everything, you’ll never get anything done.

When I took it on the chin during the last housing collapse in 2008, I googled “Florida housing crash” and was surprised to see it had happened several times before. It’s just cycles.

I learned my lesson and I pay closer attention now. We’re back to 2008 levels and beyond. It looks, sounds and acts just like 2008, with a few other factors at work of course, but I expect another loud pop. And then the bubble will begin again. Cycles…

PS: San Fran blows Phoenix out of the water of course…for all the obvious reasons.

Called my bank yesterday while on a long drive, just for fun. They said they have halted all conventional loans and are only doing VA loans at this current time.

Not sure about normal mortgage brokers, is lending tightening?

Considering that banks are on the hook for 80% to 95% of new home loan exposure…the fact they are closing the lending window should tell everybody something. (Although conforming loan risk gets sold on to Lady Bountiful/Fannie Mae)

Wolf, I wonder if there is some sort of decent numerical home mtg availability metric out there…if nothing else, quarterly aggregate FDIC bank reports probably have highly segmented data (by loan type, bank size, bank location, etc.)

I’d say look at Fannie rqmts, but they are in perpetual Jubilee mode so my guess is that Fannie enters its third decade of being looser than a $2 hooker.

There are no $2 hookers in this business due to inflation (Gov CPI notwithstanding_. Perhaps my great-grandfather once saw a $2 hooker, but I’m not sure.

More…”something is coming!”

Agreed, but what & WHEN?

James: “something is coming … but what and when?”

A long time ago, Ludwig Mises answered “the what” part of you question.

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

He left “the when” part for us to figure out.

Same thing is going on in Texas….and we are all “open”.

The kind of Californians who would move to Arizona are very welcome to do so. Good riddance. Let’s thin this crowd out.

Elon Musk would be these Californians poster boy for crying about moving to Texas or other states…won’t miss you anytime soon

Amen Javert Chip.

Zantetsu: Javert Chip makes a great point, only the truth and unfortunately, you simply can’t take it and resort to a somewhat childish – I would say – reply. Please try and make an coherent argument so we all may learn your point of view.

Furthermore, I don’t think Javert Chip has any evidence whatsoever about who exactly is moving out, aside from the obvious fact that people with more money and more mobile jobs will have an easier time moving out, and therefore logically would move out in greater numbers than those who are more constrained by economics.

Finally, people who care more about what CA has to offer than the McMansions they can more easily afford in the Phoenix area are the kind of people I want to be surrounded by which is why I say I am not sorry to see the others go, if in fact they are going.

I don’t see Wolf leaving for Phoenix, which kind of makes my point.

That would mostly be working class and middle class people priced out of buying a home. If you think that’s good news for CA, you are gravely mistaken.

I live in the SF Bay area and am still waiting for price decline to follow supply glut. Hasn’t happened yet:

John Mazotta,

I love the quote from the article you linked (I removed the link per commenting guideline #2):

“San Francisco County home values have gone up 0.9% over the past year and Zillow predicts they will rise 5.9% in the next twelve months.” This borders on hilarious.

Zillow is a ridiculously stupid company. The number of ways they could EASILY improve their metrics is countless. I myself have written to them and suggested some things, which they of course ignored. Their website is terrible to navigate. I never, ever believe anything I read on Zillow with regards to estimated price or expected price changes. Nor should you or anyone else.

Agreed. The only thing it’s good for is its aggregating of public data, including sale prices. I ignore it’s “Zestimates.”

I drove up the “Z estimate” on a property I owned.

It’s not hard to do! Please, do not believe a word of zillow or that of a realtor. My friend was taking advice from a realtor. I asked for his name and looked up his license. He had been licensed 6t months!

I also found his website where he said he “tried RE” since photography and cooking wasn’t working out!!!!! :)

@nodecentrepublicansleft,

how did you drive up the “Zestimate” on a property you owned?

Irving Fisher would be proud.

Housing busts seem to always start in SF & NY and work their way out (and they are where the run ups begin). And I don’t see how 110-120 degree temps are “good weather”. I guess it’s sunny there but so is the Sahara.

MarkinSF

For those who don’t get out much:

o Unlike the Sahara, Arizona has both water & air conditioning

o Unlike CA, Arizona has reliable, dependable electric power (a lot of it from renewable)

o CA retail electric rates are 50% higher than AZ (18.3 vs 12.1 cents/kWh)

Wild-ass guess: It’s not legal for humans to poop on the street/sidewalk in any AZ city

Javert Chip,

“CA retail electric rates are 50% higher than AZ (18.3 vs 12.1 cents/kWh)”

Yes, that could be the case on average (everything is different locally). But in coastal California, where the majority of people live, it doesn’t matter that much because there is little or no need for AC. Like most people in San Francisco, we don’t even have AC. In other places near the coast, people have AC but use it a lot less than they would in Phoenix. There is a difference in costs between cooling a home when it’s 85 degrees outside or 114 degrees. Our electricity bill is small, compared to what I paid in Oklahoma over 20 years ago in my condo between May and October.

Yes, cost of living is high in coastal California, but electricity is not the cause.

Couple of points.

– Water is going to be interesting to watch. You might have enough now, but the fighting over the Colorado River is just beginning. Who knows what the future will bring water wise. Not something I want to worry about. Put another couple of million people into AZ and let’s talk about water then.

– Reliable power. My brother is a practicing PE (EE) in WA state, having spent the last 35 years doing “power” stuff for various commercial/industrial customers. From him and others knowledgable about the power grid in America, I don’t know if I would qualify our infrastructure as necessarily something I would count on long term. Sure it’s working now, but what happens with another couple of decades of minimal to no investment? Just look at the trouble with PGE in CA. They haven’t been the only ones cutting corners.

We were discussing what would happen in AZ if something in the grid were to cause a two week power outage in the middle of summer. It didn’t sound like a fun time.

Phoenix (aka “the Valley”) sits on an aquifer estimated to hold about 400 years of water reserves at present consumption levels. About 70% of water used here is for agriculture. All it takes to more than double those water reserves is to stop growing corn, cotton and such. BTW, the water came there during the end of the last Ice Age, when melting glaciers (with the most southern edge somewhere around Flagstaff) filled it up. I don’t think Arizona will go dry any time soon.

As for electricity and what would happen with prolonged stoppage during summertime, I don’t really know. I know that the power grid, right now, is super reliable.

However, people lived here for hundreds of years before A/C. As a personal account, maybe 5 years ago, we had an outage for about 5 days. We just opened all doors and just laid down. After about 3 hours of profuse sweating, our bodies adapted and we felt okay for the rest of the time.

Personally, I would rather be caught in Arizona if the power goes out than in Boston or New York, and freeze to death.

But that’s just me. I can’t really say what the masses would do.

Yep Wolf… it would be our State government that’s the proximate cause of a good portion of this high cost of living.

Mr Chip

I know Arizona very well. Love the desert & the mountains there. Southern Utah is even more beautiful and awesome. I have lived in San Francisco going on 40 years and not once have I seen poop on the street (well maybe but I always assumed it was from a dog). All I said was Arizona is very very hot.

Whether you like it not San Francisco is a world class city with amazing landscapes as well as Cityscape. The neighborhood architecture is unparalleled (at least in the US). The mystique is indescribable and the walkability score is at least a 100.

If you love suburban sprawl and corporate chain restaurants then Phoenix might be a good place for you.

I’ll pay the extra utility rates because here you NEVER need air conditioning. And there’s never a deep freeze (I can’t remember the last time it dropped below 40. Also don’t know if I’ve ever had an electric bill higher than $100 a month.

My 12/17 PGE statement shows tier2 electric cost of $0.30743/kWh, excluding surcharges and user tax. So far, I have had to run my gasoline-powered generator twice this year. BTW, the people I know who are selling in my neighborhood are mostly relocating to AZ (sample size ~10). Oregon had been a popular relocation destination until everyone realized it’s government is more insane than CA’s. As to Wolf’s comment, it’s obvious he should take a BART ride out to Concord some summer day and see if AC is needed. I am going to guess more people live in the Dublin-Concord Area than in San Francisco.

R Bacon,

I lived for decades in Texas and Oklahoma, and I know what a HOT summer is. Arizona is even hotter. Yeah, and we hike on Mount Diablo right by Concord and Walnut Creek, and I have friends who live in Concord, and we visit them periodically. And it’s not HOT.

And yes, you use AC in those areas, exactly as I said, but not like you do in Arizona, as I said.

Phoenix: During hot season from May 28 to September 19: average daily high temperature above 98°F. The hottest day of the year is July 4, with an average high of 107°F and low of 84°F.

Concord: During hot season from June 6 to October 4: average daily high temperature above 81°F. The hottest day of the year is July 27, with an average high of 88°F and low of 58°F.

You see, the average high on the hottest day of the year in Concord is close to the average LOW on the hottest day in Phoenix ?

If you want HOT in California, go to the Central Valley, the Mojave Desert, and the like. We have plenty of HOT places in California, but Concord isn’t it.

Wolf,

Hot needs a redefinition in Phoenix, been there in June/July, where I literally dreaded walking from the parking lot to one of the campus buildings where I was seeing my customers.

And heaven help you if you can’t find parking under the shade. By contrast, bay area has very few hot days. Right now, it’s butt freezing cold… although this is nothing compared to some places up north like around the great lakes nowadays.

A common misconception. Yes, at times it’s 110F in the summer in Arizona. But have you ever experienced 3% humidity? It makes a *huge* difference. People wouldn’t be living here if it was so bad. And outside of the summer, Arizona has the best weather, better even than California.

Btw, I lived in SF for years. I do love the weather there. Basically 65F year long. Nice, good for you.

But the way California failed as a state, I wouldn’t go back there even with the nice weather.

Its basically in the 50s all year long. In fact the average temperature for every month of the year is somewhere in the 50s. Look it up.

And Arizona is very hot even without the humidity. Asphalt was melting last year.

As an Australian, I can assure you that you are overblowing California being a failed state. All the economic issues you cite are common in big cities full of working class people.

I tried to tell you guys some time ago that the real reason these issues exist is because our manufacturing industries have been hollowed out after decades of offshoring.

Real wages haven’t grown since the 90s because our dear leaders are desperately trying to compete with 3rd world and developing world nations where wages are low. I could cite many other issues such as these.

How do you afford an increasingly expensive property with such conditions? Yeah! Credit.

This is called secular stagnation. It’s going to get you whether you think you are safe or not. It will destroy your standard of living now, so your children’s wages will be comparable to China.

In Australia, we have a certain mining magnate called Gina Rinehart who has called for $2 per hour wages for working Australians. (Yep, she said the quiet part loud. Very loud.) She is a major donor to our Billionaires Club Party. She is getting her wish.

I think it is fair to say that AZ has great weather from November 1 to April 1, that’s why people live there, no one on earth lives there because they like the summer. So why pretend that summer there is anything but awful?

Coastal CA is beautiful and has the best weather in the world. But the state government is a one party nightmare built on confiscating your wealth and allowing homeless encampments to destroy the quality of urban life. People make trades no matter where they live.

Oh Roger. Us Californians love riots and despair. Especially despair. And $5 avocados & expensive real estate.

Looks like Arizona is going to be the new CA! Fingers crossed for mass migration of millions of people & jobs to your state like the one CA has had for decades. ? good luck w/affordability then!

AZ has hundreds and hundreds of miles of empty desert land in every direction, not a 20 mile by 400 mile coastal strip bisected by multiple mtn ranges (perfect weather tho)…it also only has 8 million people in that empty expanse, compared to CA’s 40 crowded millions.

And no water…

Are there jobs in those vast miles of deserts? Because growth happens where the jobs are….CA also has miles and miles of vast open space– in Central CA. Pretty sure it’s known as the “armpit of CA”.

The water gets routed to where the population is…just like in CA (it’s Chinatown, Jake).

But the broader point is valid.

That’s what most of Texas and all of Florida is for.

(And GA, MO, etc.).

From Cadillac Desert, a book by Mark Reisner:

“Water flows uphill to money”

If there isn’t any water to begin with, it gets a little harder.

The Colorado is over subscribed now, and the fighting over the allocations hasn’t really begin in earnest. Give it another decade and things might get interesting. :)

Lived in SoCal for 18 years and AZ for 18 years (and visited No Cal frequently). All of the comments here are valid on behalf of both states. CA is indeed a natural wonderland.

PHX Valley is a fantastic place but exit the Valley about 2 hours and you have CA weather and gorgeous landscapes at less than 1/2 the CA pricetag.

As for power and water, AZ has unlimited solar capacity and though it is a long ways off, rainwater harvesting can provide ample water for SFH owners.

I live in a 100% OTG home in the heart of Prescott AZ and it’s liberating and beautiful, but not for everyone.

Yes, that’s true. Arizona is now (jokingly, but maybe not) called “California East”. Arizona is turning blue.

Prices are rising to the point where it’s getting tough.

I remember in the early 2000s when prices in SoCal just jumped up and never came down. I fear the same for Arizona now.

Plus,

“Arizona is turning blue.”

So is every other state enjoying this influx of modern-thinking virtue-signaling social-justice warriors.

I dont know to say if you think I care about the income levels of my neighbors ?♀️

Well, only because I’d rather not live next to selfish d-bags that only care about money & land/ asset prices. I’m #TeamPoor&WorkingClassAmericans all the way.

Javert Chip,

What these numbers show is only DOMESTIC migration, between CA and other states. What numbers likes these always miss is the in-migration from other parts of the world. California, like other coast states, is a gateway. People come in from other countries (Asia a lot), and people come in from other states, and people who are already here leave to go to other states or to other countries.

The net effect is that over the period you reference, from 2017 to 2019, the population of California has grown by 154,000 people to a new record — there has been no population decline in the past 100 years in California.

But it’s true, that increase in population is way down from prior periods.

And there is a good chance that in 2020, the population has actually dropped for the first time in 100 years. But we’ll have to be patient to get that number.

Wolf

The IRS “migration” data I referenced (link below), includes 100% of Federal Individual Taxable Income, reported as 3 mutually exclusive classes, for each state:

a) “non-migration” – Taxable Individual Income remaining in-state from year to year

b) “foreign migration” – Taxable Individual Income moving in/out of USA

c) “inter-state migration” – Taxable Individual Income moving between US states

This IRS format accounted for both foreign (ie: Gateway) & domestic migration. Note: “Individual tax returns” includes some partnerships and LLCs.

My point was not that total CA population is declining, but that outbound migration of taxable income and people exceeds inbound migration. Additionally, those moving out appear to have higher incomes than those moving in.

Depending upon the long-term trends (which appears to be favoring outbound migration) , change for a given year may appear small, but change accumulated over a 10-year period could be material.

LINK: https://www.irs.gov/statistics/soi-tax-stats-migration-data

Javert Chip,

“those moving out appear to have higher incomes than those moving in.”

Yes, that’s almost always the case in gateway cities with international in-migration. These are people from poorer countries (India, etc.) that are trying to make it, and they’re working for less, at least initially.

Well, not so sure all those well heeled latte-loving refugees arriving from the Left Coast are a blessing to native Arizona residents.

There goes the neighborhood …

Conservatives like fancy coffee too!

One more thing, since I’m nearby.

Interest rates!!

I think rates will stay super low all of next year and beyond, so that sustained trend adds fuel to the buying fire. Like a broken record, I always turn to the current 2-yr Treasury yield ( 0.13%) which apparently is a proxy for where the 10-yr yield will be a year from now (based on Treasury futures). Thus, a year from now, mortgage rates will theoretically be lower. 30 yr rates are typically about 1.75% higher than a 10 year yield.

With that in mind, a recession is most likely in the cards, but with super low rates, there’s a huge amount of demand for homeownership — but I don’t see housing taking a big hit as a GDP downturn takes place.

The biggest threat is mass layoffs and bankruptcy and those are dynamics that everyone has been seeing every day for the last 10 months — and that would not cause a shock — if anything count on certain cities, even regions experiencing hardship, while others prosper (that’s not uncommon).

Nonetheless, low interest rates will support and sustain demand for housing. The other magic bullet will be (well-positioned) Baby Boomers that pay cash to live anywhere they can find a nice house. Between people with lots of cash and easy mortgage rates, housing will continue in an upward track …

The Fed cant keep rates down with what is going on…

Inflation is ripe….

Point: The new bailout gives money to the post office. Why?

How many catalogs come in the mail at what charge? The post office is broke and should raise their fees and stamps. Why not?

Because….Stamps are a big CPI input.

Inflation will grind down and punish the people of this nation…and for what purpose? To fuel the stock market in which about 90% have no investment, to deliver an inflation to the working families. This will not wash.

I can tell from your posting-name (which I like), that you wish to be as accurate as possible.

The following link demonstrates that over 50% of US families (not just 10%) have some investment in the stockmarket (either direct, or with a pension plan or 401-k).

LINK: https://www.pewresearch.org/fact-tank/2020/03/25/more-than-half-of-u-s-households-have-some-investment-in-the-stock-market/

“The Fed cant keep rates down with what is going on…”

The Fed will do anything (legal and illegal) to keep short term Treasury rates near zero.

Once the Fed debt is at 100% of GDP, each 1% rise in interest rates eats 1% of GDP…GDP rarely getting beyond 2-3% growth in recent decades.

So a 3% Treasury rate with 2% GDP growth rate means the ntl debt automatically rises by 1% (without *any* additional DC spending…and that never happens).

That is the debt death spiral fiscal conservatives have warned about for decades.

So the Fed will print whatever amount of money necessary to keep short term T rates at essentially zero.

Thus the DC satanic black magic of converting their debts into our inflation.

Which they will blame on invented fictional villains squeezed out by the MSM state sphincters (Real estate speculators! Russians!! Racists!! Readers of History!! Real asset holders!!)

First of all, stop issuing debt that does not fund Congressional spending. Problem solved. Private debt is a different critter. That’s where the debt deflation will land. Deflation. Not inflation. Private debts are supposed to be honored. But when incomes do not come anywhere near growing as fast as compound interest, debt will not be paid. Stuff will not be sold. Prices will drop. Unemployment will rise. And the government, if it has any brain cells left, will pass a national job guarantee program. This is the correct ‘buffer’ to have, not unemployment checks.

CH – the Government also could pass a national war guarantee program. It helped with the last depression. Buying bonds was patriotic.

All works until US$ hits the fan. Happened in late 70’s. US tourists around the world were asked to pay in local currency, including lira!

The US had to issue bonds denominated in Swiss francs ( Carter bonds) because no one wanted to get paid back in dollars that were losing 10% annually. You would get paid in US$ but the Swiss was used to determine how many)

One thing that has saved the US$ so far is the ‘cleanest dirty shirt’ theory. In the 78 era the D- Mark was still around, a shirt that was actually clean. If the euro could dump Italy, Spain and Greece to name 3, and contract to the Frugal Five, plus Deutschland Inc. (France has to be included for political reasons) the US$ would be a much dirtier shirt.

Fortunately for the US$, although a return to

the lira, drachma, etc. is popular with the US MMT crowd ( you can’t go bankrupt in your own currency, etc.) none of the European ‘patients’ like that medicine, especially their bloated, overpaid, inefficient public sectors.

With the populists in Italy threatening to print (counterfeit) their own euros, the solvent members might leave and create a new currency. All kinds of things seem unlikely until they happen.

The can and they will. This goes until it breaks. There’s no way to stop now. Even a slight increase in interest rates would send everything crashing.

The Fed’s last stand. Strongest country in the world but can’t withstand a quarter point jump in rates. That’s how strong it is.

Well, yes, they CAN raise rates. And it would be GOOD for the country because it deflate all that unproductive phony wealth.

That would punish foolishness and reward those who actually work.

And it would be good – GOOD – for the economy.

That, my friend, is called Economics. Or what’s left of it.

55% of Americans are invested in the stock market. It has been as high as 67% in 2002.

Yeah, but in what amount? Having $50k in a 401k doesn’t do you much good in that the harm from inflation and other negative effects will cancel out whatever gain you get.

Stock ownership was pretty high in 1928-29 too!

Very few people have an amount of stock of any significance. The median value of an American 401K is $22,000.

When the autopsy for the US economy is written, it will be shown to have asphyxiated during an auto-erotic attempt to make valuations pop with debt rather than growth.

Yeah, but at what cost was that $6,800 “gain?”

How much has the dollar been devalued? How much of the future earnings have been pulled forward?

FHA is certainly playing a key role in feeding this housing frenzy with their insanely risky loan practices (to support their mission statement “another American dream comes true”).

As Wolf says, they have huge numbers of delinquent loans resulting from easy money to dodgy borrowers, low, low down payments, and even generous down payment assistance as a cherry on top.

It does not take a rocket surgeon to see FHA is going to need a bailout from Uncle Sam before long.

Freddy Sachs and Fannie Stanley will own all the mortgages in the end!!!

The American Dream is finally coming true!!!

The short term interest rate is whatever the Fed decides it is. It should probably just set it at that 2% number. If that slows down credit, fine and dandy. That will at least bring some ‘price’ into price discovery. We have a debt laden, moribund economy. Post Office is understaffed and hiring is difficult. Why? To me, that’s an interesting question. Wal Mart is paying $16-$20 per hour. The reason we are sending money out to stimulate the economy is because wages are not high enough. Capitalism is not working all that well right now. Why? You cannot blame the government. It has been cutting taxes by the billions and eliminating pesky regulations almost as fast. It isn’t working. Why?

Chris, capitalism appears to be working quite well, however it’s not producing an outcome that makes everyone happy. Wages are at a level that a sufficient number of workers will accept. If they withheld their labor wages would go up. The problem is how to get from here to there. Currently you can’t go from here to there. Debt is in the way. You can’t withhold your labor when your are over your head in debt. We could establish minimum wages, but that will result in higher minimum prices, which will need higher minimum wages, which will result in higher minimum prices, &c, &c. It’s borrowing from the future that isn’t working out so well.

I have a wheelbarrow heaped full of money.

They have already stolen the value of the money.

Now, I am worried they will steal my wheelbarrow.

The ‘value’ of the money comes from the availability of resources. We don’t do ‘resource’ stuff anymore. We need to encourage work that actually makes something. And we need to pay, at minimum, a socially acceptable wage with benefits. Putting people on the permanent income skids is a lousy policy.

We do make “stuff.” We make Facebook and Twitter, &c. It’s quite apparent these are valued very highly. We’re focused on the wrong “resources.”

‘We’ .. Or “They”, actually .. make stuff up! … to our collective denoument.

In high priced markets like the swamp (DC) where a lot of houses routinely sell for over 1 million there are other factors influencing home prices and availability. That is, some of the tax advantages (under the new 2017 tax laws) of these big mortgages can be lost if one moves. So a lot of people are staying in there homes to retain their full mortgage interest deductibility which is grandfathered in, and not trading up or down, even if the house they are living in does not meet their current housing needs. And those who have paid off their mortgage and own their homes free and clear can easily rent them out and make a good income and then go live where ever they want. Both of these factors are limiting availability of homes on the market. The laws of supply and demand are causing the prices to keep going up in spite of an economy that is in a full fledged depression here and getting worse every day. This will not end well.

And there are Seniors with property assessment freezes which somewhat limit property taxes. If you move you start all over again.

Wolf…

Its called “legging a spread”…you buy first what you think is going up, then later hope to sell the other “leg” on an uptick.

People are legging their exits from Blue States.

I think this is a real danger to those with a leg up. But the leg they are waiting to sell is likely in a lousy market, ie NY CT IL, and that sale and that supply will be a trick.

Additionally, with VRBO and air BNB….investors looking for any kind of yield are buying homes to rent. Yield chasing, desperation investing, courtesy of Fed who knows better than the free market.

If rates ever tick up, this will change.

These markets are running too wild, too fast. When Greenspan was Fed Chair, I recall learning in the spring of one year…FL real estate had risen 20% so far that year. The over stimulation is a terrible situation, and I think we are there.

The most frightening part of owning RE is property taxes. They give away homes in Detroit and no one wants them. This is part of the exodus, but if you have lived in the same house in CA for a while, prop 13 is keeping your tax obligation in check. Emigrants from the cities may decide that taxes are higher in those places relative to value, as Buffett said when he was Arnold’s economic advisor for about a week.

Indeed. You are a target for taxation when you own property.

States like IL, you are gouged 3% per annum on your house in some areas…some less, some more.

Theft. To fund the overpromised public union pensions.

Now the counter stroke will be an exit tax. Freedom? Voting with your feet? The ‘rulers’ won’t allow it. Terrible situation to be trapped in a high tax situation, watch real estate rally in the places you wished to live someday, all because of ruinous politicians, who will live likely in those desirous locations someday, with their public union retired folk.

“You are a target for taxation when you own property.”

Exactly.

Any immobile asset is a hostage to the political integrity of “your” government (heh).

As much as when Saddam pawed that poor child hostage in Gulf War 1.

*And*…think about how “unique” property taxes are…based on *unrealized* valuation set by *government* with no netting out of huge mtg *debt* component.

For over 100 yrs, local G’s have been applying “wealth” taxes on *borrowed* money…and 95% of taxpayers in harness think that is normal.

“You are a target for taxation when you own property.”

I’m seeing mobile home sales are surging. Maybe mobile homes are one way to avoid ever rising local real estate taxes, fees, etc.?

Wrong villain Historicus. Ask yourself who is running the government? It ain’t ‘the people.’ It’s the capitalists. The unfettered capitalists who don’t pay taxes but hoover up every nickel in productivity gains. They are reality. And reality doesn’t give a hinds end about you. Blaming government is precisely what the real rulers want you to do.

Did the capitalists build unsustainable pension obligations in IL? Last I checked that was Madigan et al and the corrupt government.

What I find interesting is all the public employee pensioners all move to low-tax states when the retire.

That is the affordability issue, taxes in other states are higher relative to value but if you are trading down to half the cost of your CA home who cares? Should the national RE market get a dose of inflation there will be buyers remorse. None of these mark down markets have caps on property tax. You could end up paying CA level taxes with none of the benefits.

As a public pensioner, I think you are making too much of a blanket assessment (word ‘all’ is a deviously dangerous word to use, as is ‘never’, and ‘forever’).

My experience is that retired public pensioners will sometimes move out-of-state/out of town, but for different reasons.

Lower overall cost of living is often a compelling reason to move for many retirees that receive only modest pension benefits (that by the way, is the majority of them as a group– the myth that all public pension retirees are raking in fabulous retirement benefits is just that– a myth).

Some, by the way, are moving overseas, to lower cost third world countries (e.g. Latin America) in order to make it on a modest fixed income.

@heinz,

Public pensioners don’t all have it like those in CA, NY, and IL. There are many states that have much more prudent pension arrangements.

Contacted my real estate agent today to begin the sale of my SoCal rental condo. With some luck and quick action I will be “cash flush” and renting from the East coast. Waiting and watching for a deal.

This is one of the best websites around to get the pulse on a hodgepodge of finance topics. “owooooo”

re: exit tax

The following is from memory, so hopefully somebody who knows what they’re talking about can verify:

Tens of years ago, some states (I believe CA was one…) thought it would be a good idea to tax distribution of 401-k assets acquired in CA EVEN IF THE TAXPAYER HAD MOVED TO ANOTHER STATE.

The US Supreme Court ruled this was unconstitutional.

Unclear how this applies to “exit taxes” for citizens moving between states.

When CA gets desperate enough (soon) they will be lojacking residents exiting the state and hiring tax bounty hunters to hound out of state tax refugees.

CALPERS will launch a glossy, high profile mag listing nothing but CALPERS defined tax outlaws hiding out in neighboring states.

Re-entry to CA result in seizure of your auto (and wallet) for Sacramento defined arrearages.

CA/NY/NJ/IL will sign reciprocal tax seizure and extradition treaties.

“CA/NY/NJ/IL will sign reciprocal tax seizure and extradition treaties.”

Cas127 you’re just giving the enemy ideas!

Lol

“giving them ideas”

The taxing authorities in “progressive” states require no assistance…they are are like the demon ghost girl in “The Ring” who crawled out of the TV set…”she never sleeps”

Is there a possibility of another SPV (Special Purpose Vehicle) in Chairmen Powell’s future? One to buy distressed real estate in wealthy areas. Could it become part of the tools in his tool box?

I had a 14 year old car that I hoped the Fed’s SPV COPP (Car Owner Protection Program) would buy at face value, but it never did ?

Probably worth starting to look closely at how Weimar managed to finally wriggle free.

(I mean besides the hyper inflation, Nazis, and World War too…).

My vague recollection is that the Weimar G rebacked debts/destroyed currency with some phoney baloney Gvt “land backed” bonds (who was going to foreclose short of marching into Alsace?…ahem).

The key part was that the war creditor nations finally looked the other way, “thought of England”, and took the phoney baloney German “ntl mtgs”.

Everyone can learn much, much more at their friendly local Federal Reserve bank…

Gold standard was in effect. France and the good ol’ US had all the Gold. Germany had nothing. Britain was not in much better shape either. Read ‘The Lords of Finance.’

An even closer historical parallel to today might be 18th century France’s economic/social upheaval in reign of Louis XVI.

Excessive government spending and national bankruptcy, income inequality, high taxes (on peasants, mostly), and highly inflated food prices. Sound familiar?

In the end there was a revolt and heads were a’ rolling.

I too am hopeful as I have several old bicycles.

How about the new 2021 SPV ‘Iron Maiden’ .. on an SUV chassis – supplied with very bad shocks – as standard equipment? Works great over rocky rutted roads! .. as long as one is Not the ‘passenger’.

I wonder when the public is going to wake up to the fact that these huge home price increases also are generating huge tax revenues for the States? The house may go down in value but the taxes rarely do.

“generating huge tax revenues for the States”

On *unrealized* gains…across *every* home in locale…without netting out very large *debt* component of home “value”.

That’s rather more than an annual wealth tax.

The G has been running the gerbil wheels for a *very* long time…and they ain’t going to start concerning themselves with the gerbils *now*…at the end of all things.

Ah … you are right over the target about the great scam of real estate property taxes.

You will never own real estate outright– you essentially lease it from your guv overlords and pay tribute in form of property taxes and miscellaneous fees.

The trade off is that you supposedly get services in return– police, fire, roads, etc.

But in fact (except in best run jurisdictions) you do not get fair value for your taxes. Cities and counties in general are bureaucracies intent on doing what they do best– grow bigger and ever more expensive to maintain (pensions, developer subsidies, questionable civic projects, etc).

What puts this latest housing price bubble on center stage is that bubblelicious property tax increases at current rate (or even scaled back) will make housing ever more unaffordable, and it will lead inevitably to a landslide of more renters and homelessness.

It is worth repeating today the amazingly prescient quote of Thomas Jefferson:

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around [the banks] will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered.”

Gold, silver, bitcoin, land…….or a savings account & bonds??

My business went through & came out the other side of the housing collapse. This does not feel similar to 08-09 at all.

From April until now….nothing but a flight to freedom…..period.

Channeling my “inner SoCalJimbo”….buy now or forever be shut out !!! Real estate only goes up, besides I’m in it for the long term !!! We are on a perpetually high plateau as everything is great !!! (but gotta give these evil clowns credit for keeping the scam going this long…imagine things like Airbnb and Door Dash selling for a comibined 150billion – last I checked, could be higher now with a combined 6billion in gross sales….and, net income, what’s that ???? You don’t need no stinkin net income !!!!). Also, the Mercedes is paid for and it’s only a cold sore !!!

With that said, I wish all the Wolf Street community a wonderful holiday – sincerely!!!

I miss Socals RE wisdom, like a dog misses a tick

Amen to that Young Buck.

You forgot, illegal immigrants get $1800 in catchup payments. So adjust your math.

I wonder if those millions for Myanmar, Venezuela, Pakistan, et al are actually for Soros NGOs?

Thank you MCH for your pearls of wisdom. Of course the politicians, the lobbyists, the banks, the Fed, all part of the same scamming complex. I certainly don’t partake in this insanity and have kept all my risks calculated and protect myself by having no debts, owning real assets and living under the radar screen. As I’ve said before, what is coming will make the 1930’s look like a day in the park. Most folks are indeed their own worst enemies by never learning the lessons of history. I think it was Julius Caesar who said that people are going to believe what they want to believe. I love the simple live. All the best to you.

They could get all the money back by taxing the mega-corps and the top .01%.

I think one of the biggest fraud and scam is perpetuated by our elected officials and their lobbyist overlords. The eye opening part about this is how selective people are about what they hear and what they push.

Trump said: $2K to people, and remove the pork.

Pelosi’s response: yes, $2K to people, let’s do it now.

Did you notice what was missing? Yep, she figures what the heck, just put in the $2K for the suckers, as KGB from Rounders would say: “It is your money, anyways, I am paying you with your money. See”

What was left unsaid was: “let’s not remove any of the pork, or our favorite project, those bozos (and I mean both Democrats and Republicans) are thinking about how much more pork we can stuff in this sucker of a bill… let’s make it $2T or $3T.” And all the pundits and suckers on TV will hail it as a great bipartisan achievement, while we the people gets robbed blind.

Tidbits from the 1920’s Florida Land Boom.

In 1922 the Miami Newspaper became the heaviest in the world, with little besides real estate ads. Prices had quadrupled in one year.

It took little to get in. A deposit called a ‘binder’ would hold the lot ( there was almost never a structure) which could then be flipped for a new, bigger deposit and so on.

One man started with 1700 and was worth 300, 000 by 1925.

In expectation of the construction boom to follow, huge quantities of building material were shipped by rail, only to be stranded as no one was building. Although some ‘subdivisions’ could be drained, much was too low and is mosquito infested swamp today.

The exceptions were largely ocean front assisted by a brisk industry of beach creation with dredged sand.

The collapse began when a few flippers decided they’d rather have the money. It preceded the 1929 Crash, is considered a prelude to it, and was near total. Once the impossibility of flipping disappeared, the RE reverted to its inherent value, which in many cases was less than zero, because although unusable, it was taxed.

A newspaper offered a free lot with a subscription, only to be asked if one could subscribe and not take the lot.

Typo: ‘impossibility’ of flipping should be ‘possibility’

Where is Paul Volcker now that we need him. 18% mortgage rates, 21% prime rate. Savers got a decent return, and the dollar was a dollar. Houses were priced at reasonable levels. Those were the good old days.

I expect that the only ‘savers’ that got a decent return were those that already owned their home. Everyone else was no better off as the interest rate paid on their mortgage well eclipsed any of those great savings rates.

By the way my mom bought the house I lived in as a child in 1980 after divorcing my step-dad and she told me that her rates were high like that. And yet, as a single mother making very little money, somehow she could afford a home. It is true that it required sacrificing almost every other luxury that a person could experience, and we lived pretty meagerly for many years, but at least she could afford it. With prices as they are now, even with low rates, she never would have been able to afford that house.

How much did she pay for health care? If I wasn’t taxed ten percent of my salary every year for a family health insurance plan, I would be able to afford a much bigger home.

People always scream about taxes, but that health insurance that never stops increasing is larger than my Federal income tax.

Yes, health insurance, home prices, and cost of college inflation have devastated the middle class. Thanks Fed.

Property taxes for fixed income elderly are also a big deal though.

“and the dollar was a dollar.”

Now the dollar is the steamer trunk dwelling Gimp from Pulp Fiction.

ZIRP is Zed, baby.

“Contrast that to Arizona. Much cheaper real estate, nice new neighborhoods, safe, good weather. ”

You forgot to mention no water. With global warming I wouldn’t make a long term investment in Arizona based on the drought issues.

Not that California doesn’t have a potential water problem. But they do have the Pacific and desalination is a real option.

Desalination is only a real option if we perfect nuclear fusion, and thus have unlimited electricity.

The Poseidon deslination plant in Carlsbad is online and provides 7% of San Diego’s water. Other plants being built, restarted or proposed.

As I imagine more people will be leaving California in the future, desalination will not need to compensate for population growth.

. No fusion reactors needed (although that would sure help).

Southern California has the same water problem as AZ. Both states would have plenty of water if not for agriculture. The water problems in both states aren’t a likely reason for anyone living in the next hundred years to deter living in either place.

Deceased people cannot vote in this country.

Obviously you have never lived in Chicago or even Cook County.

We need to change the laws so dead people can only vote for other dead people.

Problem solved.

Move yo fly over country shovel snow rake leaves affordable good people quit crying pull your pants up be American our grandparents are rolling over in graves to see what we have become u all have created this mess by living above your means don’t cry when I buy it for 10 cents on the dollar

14% increase in median home price?

Case Shiller Index gives only round 6.5% YTD, on 10 and 20 cities composite.

Drunk Gambler,

I like the methodology of the Case-Shiller (sales pairs) a lot more than median price. But the CS lags 4-5 months behind by the time it is released, which is a huge problem when things move fast.

The last release on November 24 was for “September,” but the CS is a rolling three-month average of closings that were entered into public records in July, August, and September. So that’s the timeframe of the closings we’re looking at. Those deals – the moment of the meeting of the minds – were maybe a month on average before then. It will be next spring before we’ll see November fully reflected in the CS. That lag is its major disadvantage.

The effect is that the current median price and the most recent Case-Shiller Index are not comparable.

re: “I just saw Oakland Raiders sticker on the SUV in front of me.”

There goes your neighborhood.

LOL

When credit dries up it won’t matter how many people want to buy a house. That will define the crash. As it has for the last 200 years.

MarkinSF,

Yes, the matter of reserves will become an issue, so looking at that now ..

From Fed about Dec 11, 2020

“Total reservable liabilities of all depository institutions increased by 31.0 percent, from $8,321 billion to $10,902 billion, between June 30, 2019, and June 30, 2020. Accordingly, the Board is amending Regulation D (12 CFR part 204) to set the reserve requirement exemption amount for 2021 at $21.1 million, an increase of $4.2 million from its level in 2020.[1]”

Martha – back in April 2020 the Fed eliminated reserve requirement for a number of account types. Check the latest H.6.

Lisa H

Revisions to the H.6 Statistical Release

Release Date: December 17, 2020

The Board will combine H.6 statistical release items “Savings deposits” and “Other checkable deposits” and report the resulting sum as “Other liquid deposits.” Like other transaction accounts, other liquid deposits will be included in the M1 monetary aggregate. This action will increase the M1 monetary aggregate significantly while leaving the M2 monetary aggregate unchanged.

• “Decreasing the ratios leaves depositories initially with excess reserves, which can induce an expansion of bank credit and deposit levels and a decline in interest rates.

•

• Reserve Requirement Changes Affect the Money Stock

•

• Purpose and Functions (1994) describes how a change in the reserve requirement ratio affects bank credit and the money stock.4 Reserve requirements are the percentage of deposits that depository institutions must hold in reserve and not lend out. For example, with a 10 percent reserve requirement on net transaction accounts, a bank that experiences a net increase of $200 million in these deposits would be required to increase its required reserves by $20 million. The bank would be able to lend the remaining $180 million of deposits, resulting in an increase in bank credit. As those funds are lent, they create additional deposits in the banking system. The increase in deposits affects the money stock, because it is measured in several ways that primarily include various categories of deposits and currency in the hands of the public.5

==> In seems that the FED is obviously trying to goose the market and support growth. The money multiplier has increased lately, thus they hope that stimulus dollars, will add to growth — that’s my simple take.

Also see: ” researchers kept an eye on bank accounts into which CARES payouts were direct deposited and found that those whose accounts had balances of $3000 or more prior to the stimulus deposit saved 100% of their deposit, while those with less than $500 prior to the stimulus spent almost half of their CARES deposit within 10 days of receiving it.”

==> Some dude on 2nd-derivate effects:

“As government spending grows sequentially larger, each additional round of spending will have less and less impact on the total. Going back to 2016, not including the CARES Act, the government increased spending by roughly $50 billion each quarter on average. If we run a hypothetical model of government expenditures at $50 billion per quarter, you can see the issue of the “second derivative.”

I think this all adds up to the Fed doing whatever it takes to find ways to keep people feeling like there’s light at the end of the tunnel. In terms of a housing bubble, that bubble may be one of the primary legs of economic expansion, so, rates will stay low, homes will be ok, for the most part. I agree that location matters more than ever before, and the pandemic will expose the weakest areas next year, while rewarding areas where demand is exploding.

Markin, the Lenders to this grand fraud are going to have so many bodies floating to the surface in the Surging Sea of Compromised Borrowers, that these money peddlers will have to pull in their horns. I think rates will go up in 2021 regardless of what the Out of Control Fed does, the loss of faith in the ability of the U.S. to service its debts is just around the corner. Money is heading back home overseas, stay tuned.

So lending standards are going to go back to a semi-prudent level, 20% down will probably rule the day even for uber-nuts Federally insured programs (which will be coughing up giant hairballs by Fall), and this tightening of credit, on the ground, not at the Fed, is going to cause home prices to slump by the end of 2021. Good grief, we have a U.S. and global economy on life support, depending on Government Stimulus Money and ZIRP interest rates.

But please let my pet Groundhog get a mortgage for a modest place in the Hamptons. He has as much sense about him as many current two-legged buyers do today. He’s cute, but smelly!

I like this: ” Out of Control Fed”……or OOCF!

LOL at watching what the fed did this past year and still thinking credit is going to freeze up. Keep on waiting…

Right, the Fed’s actions unfroze the credit markets for good borrowers. But mediocre borrowers are still having a hard time getting credit. That’s true for businesses and individuals.

What happens when most of the people who are trying to borrow are bad risks?

Has everybody from Frisco moved to Bozeman? YOY median house price up 46%…

Housing is way up here, but not by anywhere near this much IMO.

It is astonishing isn’t it.

BTW How is my home town doing these days?

I do still love that city but most of it was hard core ghetto when I lived there in the 60s very early 70s.

I mean Georgetown was always pricy (not back in the 30s) but the rest of it?

Yes, and people can murder and rape too. But the way you talk about the deceased voting is as if it’s accepted. It’s not, any more than murder and rape, which happen also despite being illegal.

Heh I like it… dead people voting aren’t acceptable.

Yet, oddly enough, we accept our leaders “legitimately elected” who are utterly f**king incompetent with such startling regularity, and take the media’s point of view on what is “baseless” and what is “fact” with such gusto that we accept idiotic Covid relief bill like it’s mana from heaven. When in fact, it’s nothing more than another scam.

All the praises heaped upon these people because they got off their asses and handed their buddies a bunch of money. Consider, in terms of direct relief to Americans… how much of that $900B actually goes there?

– Hint, there are about 331M Americans.

– Stimulus check of $600 per person. (assuming if everyone gets one… which they won’t)

So, where is the rest of the money going to exactly?

Well, I suppose at least horse racing fans can all relax because there will be no more cheating since Congress is passing along some money to ensure proper steroid testing for horses in the Covid-19 relief bill. (yes, I know exactly who I’m picking on with that one)

P.S. my emotional support spitting cobra objects to the fact that you might want to take vote away from her…. (I know you said no such thing)

She feelsssssss she is so under represented and oppresssssssed, that each of her vote should count 10x.

Zantetsu you just don’t understand the Democratic Party in Cook County and Chicago. Accepted? It’s a tradition.

Lisa_Hooker, without some proof, your statement is not believable. I just did a google search and surveyed the results. What I saw is what I expected: it happens occasionally, sometimes due to error, sometimes due to actual cheating, but the rate is so low as to not be significant.

Pretty much like every other crime, it’s going to happen, but talking about it like it’s accepted and common is pure hyperbole.

Z,

Long time SS analyst said yesterday that there are approx 6MM SS recipients age 112 years or more..

Most references for folks that age are approx 40 actual living human beings..

and please understand that I am not arguing here that ”persons”,,, especially ”corporate persons” or whatever

WE the PEEDons are supposed to bow down and refer to them as these days, do not exist…

far be it for me to argue with the so called ”supreme” court,,, etc., at infinitum

This is a couple days late ZT, but they are being satirical. So yes, it is hyperbole. But half serious.

They believe dead people vote, which is NOT acceptable to them personally, but are satirically suggesting it must be acceptable to the government (and by extension- everyone else) because the problem isn’t dealt with or taken seriously.

“Dead people voting” is also a phrase which can connotate any voting corruption in some instances. Sometimes by even further extension it vaguely connotates political corruption in general.

Not meaning to be captain obvious here, but you did wonder if it was nonsensical hyperbole.

Wolf – For real estate we look at median price and then caveat with volume, and it’s complicated. For Amazon we look at GMV, and it’s simpler. Why don’t we use something like GMV for real estate? E.g. sum of dollar value of all homes purchased? Thanks

Tomaso,

That would be essentially the “average” price = total $ divided by total # of sales. That’s even worse than median price (half of the homes sell for more, half sell for less).

Average price is heavily skewed by a few outliers… that $50 million home that sold.

Median price is skewed by a change in mix, such as more high-end homes in the mix, or more low-end homes (this is what happened during the housing bust).

Sales pairs method, which tracks the price of the same home over time (Case-Shiller) is best but has a huge lag, which makes it irrelevant for seeing current developments.

Got it!

1) The Fed wants CPI > 2%, gov debt scorched the earth.

5) No peace, no work. That’s how small businesses get hurt.

6) Small businesses have to do a lot of work to find some work.

7) Executives WFH job can be done from the desert.

8) That’s why SF fell.

9) Cyber attacks and blackouts will chew up executives jobs.

10) When executive jobs dry out in the desert they will start small