Consumers cut back on applying for credit cards, and the Fed is not amused.

By Wolf Richter for WOLF STREET.

Consumers in aggregate backpedaled massively on credit card applications since the Pandemic; and they also backpedaled on asking for a higher credit limit on credit cards they already had. And a larger percentage of those that did apply for a credit card or for a higher credit limit were rejected. These are some of the findings of the New York Fed’s Survey of Consumer Expectations “Credit Access Survey,” released today. The Credit Access Survey is undertaken three times a year (also in February and June).

The notion that consumers are cutting back on credit-card borrowing frazzles the Fed; the sky-high interest rates, in many cases over 20%, in a near-zero interest rate environment, is where banks make extraordinary profits. And consumers, those who can least afford it, are paying out of their nose for these bank profits.

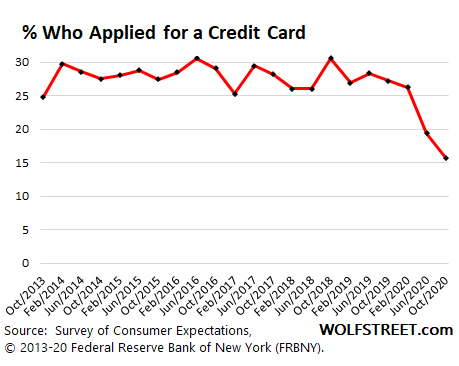

Only 15.7% of consumers said they applied for a credit card over the past 12 months, down from the 25% to 31% range before the Pandemic, and down from 26.3% in February, and by far the lowest in the survey data going back to 2013:

The New York Fed, which, like all 12 Federal Reserve Banks, is owned by the largest financial institutions in its district, laments: “The latest Credit Access Survey reveals the stark imprint of the pandemic on consumer credit markets.”

Consumers also cut back on applying for auto loans, but only a tad compared to the steep cuts in credit card applications, the survey found.

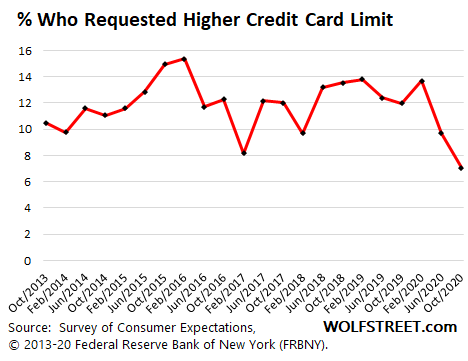

And only 7.1% of consumers requested a higher credit limit on the credit cards they already had, the lowest in the survey data, and down from the 8% to 15% range in prior years.

So there is clearly an issue with consumers not falling in line with the Fed. One reason might be that credit card interest remains usuriously high even as the Fed has engaged in historic interest rate repression that is cleaning out savers and Treasury security holders who earn minuscule to no interest on their funds.

To borrow at 10%, 20%, 25% or god forbid 30% – credit card issuers have no compunction about going there – in this low-interest environment, folks would have to be ultra-desperate consumers or, well, just good consumers in the eye of the Fed, surrendering their hard-earned dollars to the banks in form of usurious interest.

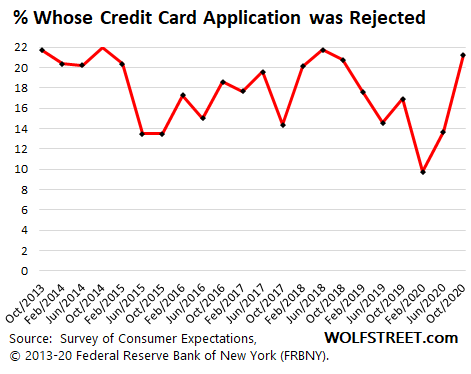

But of those people who did apply for a credit card, perhaps to make the Fed happy, 21.3% were rejected, the third-highest rejection rate in the data series:

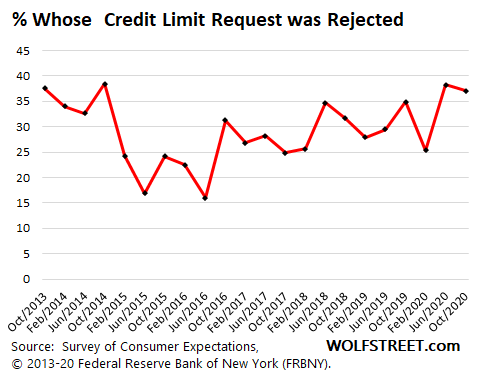

And 37.1% of those that had requested a higher credit limit were rejected:

These higher rejection rates might indicate a combination of two things: One, a shift in the mix of applications to consumers with bigger debt burdens and iffier credit histories, while other consumers are not applying, thereby raising the overall rejection rates; and tighter underwriting from banks.

These findings of consumers backpedaling on credit cards add another piece to the puzzle of why credit card balances overall have plunged in a historic and for the Fed in a nerve-wracking manner.

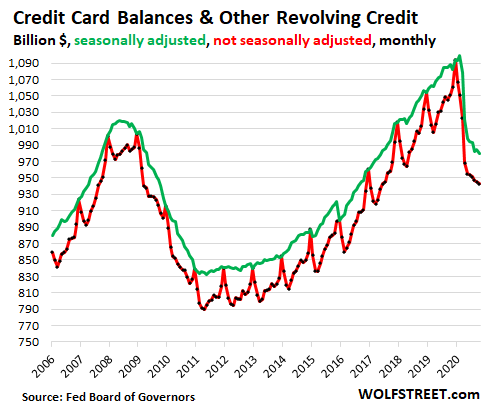

Credit card balances and other revolving credit balances in October plunged by 10.3% from a year earlier, the largest year-over-year decline in the data going back to the early days of credit cards, to $943 billion (not seasonally adjusted, red line), a balance first seen in August 2007, despite 13 years of inflation and population growth:

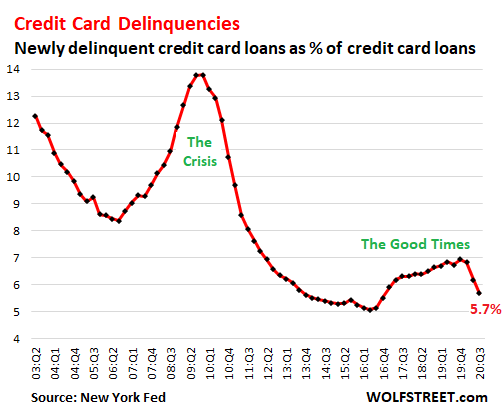

During the Financial Crisis, when credit card balances declined from June 2008 through May 2011 on a seasonally adjusted basis (green line above), there was another huge factor playing a role: Delinquencies and subsequent write-offs by lenders. Consumers massively defaulted on their credit cards – in 2009, nearly 14% of all credit card balances were delinquent – and many deleveraged by walking away from their debts and dealt with the consequences.

But this is not happening now. Newly delinquent credit card balances have dropped in the second and third quarter, powered by the mix of extend-and-pretend deferral programs and stimulus money:

What we’re witnessing are the bizarre effects of the Pandemic stimulus extend-and-pretend economy. And there just may be a flickering in consumers’ minds – I doubt it though – that borrowing at 10% or 20% in a near-zero interest rate environment is good only for bank stockholders, and is otherwise a stupid deal, and that it’s time to starve the banks of that big-fat source of revenue by paying off that high-interest debt.

Stimulus Fatigue sets in. Second month of declining retail sales in a row. But online sales eked out a new record, if barely. Read... Where Americans Splurged & Where They Cut Back in 13 Whiplash-Charts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maybe the people see the writing on the wall and figure their meager income prospects during the second half of the Covid economy and the scary one to follow are so bad they better stay clear of credit they won’t be able to pay off.

I stay away from credit, but they keep sending me offers like $250 cashback for $1000 spent in the first 90 days. Got similar offers from most major banks in the last two years.

That’s like 100% API 3-months CD. Too good to pass up.

That’s what I do also. Recently opened chase CC for personal and business. They gave me $1300 for spending $8,000. Which i spend anyway. So its not a problem. Free money.

Agree. The downturn is so obviously underway only a Robinhood trader could miss it.

It’s a symptom of this era that the emergency injection of borrowed money to make up for lost production and therefore wages is called ‘stimulus’.

In the some uses of the word, ‘stimulus’ results in higher performance: e.g. a supercharger supplies more oxygen (via air) to an engine and it is stimulated to higher power.

But when a doctor supplies oxygen to a hospital patient, it is not to increase his performance, it’s to keep him alive. If the Covid-19 stimulus is a net bonus for the economy, then the vaccine is a negative.

The Fed’s ‘stimulus’ is a desperate attempt to keep the economy alive.

Any really old person, or one with an incurable terminal disease, who has done proper estate planning, already distributed and handed off physical wealth etc, should help the stimulus along by charging as much as his or her cards will allow, for the benefit of their favored younger relatives. :-)

Love,Love,Love That idea!!Also could buy silentauction privey stuff to donate to animal welfare charities to fundraise with!!! :-)

Seneca’s cliff,

That would be ideal, but, more realistically, i would say the average person/family has alot less places to spend money. No reason to get credit if you aren’t going to or cannot spend it. Especially, if they choose not to leave house.

Consumers could be getting more cautious.. and more frightened.. I see a lot of people in all walks of life.. becoming very nervous and many are just talking a good game.. while preparing for tough times..

Game Face!!

Brace for Impact..

Is that an Iceberg????

I believe that much of the debt reduction in the cc balances of consumers is coming from the eviction moratorium. Redirecting rent money to pay down interest accruing debt. Will be interesting to see if anyone will pay their back-rent when the moratorium ends. Maybe we learned well from leaders of Western Society over the past decades… deficits don’t matter, we were never going to pay it back anyway!

Maybe FinTech players on aggregate are making an impact? Affirm, for example offers lower rates when you buy things in installment. And it’s not just Affirm, many other FinTech players are offering the same thing. You can also go to LendingClub, etc to pay off your balance at lower rates.

Note, I am NOT advertising here, but I don’t think FinTech players are not required to report their lending activity to the Fed. If they are, then I am mistaken.

I haven’t read the article yet but I wanted to make a quick comment because I started following WolfStreet a couple years ago when I got interested in the Fed’s Balance Sheet Reduction. Wolf explained both what was happening and what was likely to happen next better than anyone else.

To put it simply… this is one of the best websites on the Internet. Both because of the quality of the articles that Wolf and his fellow writers post as well as the quality of the discussions.

Thank you ALL for keeping the standards high here. may you have a Merry Christmas and a Happy New Year!

Agree, very much.

Re: ‘..Fed’s Balance Sheet Reduction.’

Totally new concept. Thanks for sharing. :-)

Hardee Har Har!

Amen to that!!

Merry Christmas and Happy New year to all

Bob

Amen,and a witness to starving the credit cards of usery level interest.

These banks are like leeches; imagine the poor people who are trapped in the clutches of these banks, and the likes of Jamie Demon (Yeah, I know the spelling).

It’s ok. Banks have just been authorized to go another round of share buy-back. And to think we were feeling sorry for these guy’s credit card lost revenue.

Dan

Yea! How dare banks give credit cards to people with poor credit scores, especially those who have no concept of personal responsibility.

Everybody knows banks (and the likes of Jamie Dimon) FORCE people to buy “stuff” on credit.

“Yea! How dare banks give credit cards to people with poor credit scores, especially those who have no concept of personal responsibility.”

Then come hat in hand to the FED and demand a bailout when their reckless gambling results in economy derailing losses!

I am a travel hacker. I don’t sign up for a credit card offer nowadays without at least a $1k return for jumping through their hoops. Their hoops are designed to trap me in high interest debt… 29.6% is legal usury.

When the profit engine for a multi-trillion dollar enterprise is usury… I’d argue the problem is with the institution… Not the consumer desperate enough to borrow at those rates.

WyleeEconomist

I’d STRONGLY support a policy that any bank needing taxpayer funds first gets a clean sweep of the institution’s senior management (for your local bank, that’s probably about 10 people; for a top-100 bank, that’s a few hundred people).

In fact, this is exactly what happens when a smaller bank is “resolved” (banks can’t go bankrupt – it’s not their money). Regulators come in on a Friday, take over the failed bank, fire all management except some accountants, and execute a pre-arranged sale to another bank (note: most lower-level staff retain their jobs).

“Too big to fail banks” are never “resolved”, they are recapitalized with taxpayer money, legacy management team mostly stays in place, and lower level staff is severely reduced to cut expense. Rinse & repeat.

All my proposal does is recognize that “Too Big To Fail” banks would, indeed, fail without taxpayer money, so, the 1st order of business is to throw out the bums.

Knowing as a certainty that that screwing up the bank will cost you your job, income & corner office has an amazing power to focus executive minds on continued employment. Is this unfair to some of the managers involved – yea, but if the bank actually failed, they’d all be out of jobs.

all the same, they are a bunch of low-life larcenous bastards.

I have a family member who is trapped this way. He just stopped making payments. Guess what? Nothing bad happened.

There’s no debtor’s prison, so there isn’t anything they can do. If you don’t mind having a bad credit score for a while, there is no trap.

It’s those 100% defaults that keep the average card interest rate high, not the FFR. If it were profitable some bank would undercut with lower rates and grab market share. Generally speaking it’s good to stay profitable. I’ve been waiting for the above bank for years and I’m not holding my breath.

Go to Capital One for a credit card. Take a bankruptcy, wait a month, apply for a card from CapOne, get $10,000 in credit. No problem.

29%+ interest rate but, hey, you got credit!

Sierra Steve

Kind of depends on your ethics, self respect and the circumstances of your bankruptcy. A commenter on this site (Petunia) frequently writes poignantly about little pieces of the emotional & financial price she is/has paid.

I find some of that difficult to read because, even though I don’t know her, she comes across as a reasonably accomplished woman.

Not everybody is like Petunia, but I’d bet she doesn’t recommend the serial bankruptcy life style to anyone. It’s no fun growing old with a cow-pie for a credit record.

Not quite! Bad credit history=less and less-paying jobs.It means,for years,higher interestrates on car/homeloans-If you can get them!Wolf’s data showed a good # of consimers Declined by banks!If you are one of millions of people worldwide who have little cashflow,bad credit,no usable creditcards or helpful friends/relatives,the next step is the nonbank lenders who trap people with even more Criminally cruel rates of +%100!Besides all this Fun,your car insurance rates will be higher.If you can get another creditcard after a couple of years,the line of credit will be lower and the interest and fees higher!Should I mention the eventual billcollecting harassers,the courtcase suing you and court fees or maybe taxrefund/wage garnishment??!

How dare these peons not keep spending; who do they think they are. we need debt slaves, not responsible people. What’s next? You peons won’t speculate your $600 stimulus check on Tesla or bitcoin?

Seems like these FED freaks are in trouble; today’s market was just unreal. DXY went up by 0.9 and then ended up negative; such a huge swing in one day. I think only plunge protection team came to the rescue and saved the day.

I feel that something big is brewing underneath this so call super-v recovery, and is about to explode. But that’s just what I feel; I don’t have any numbers to back it up.

crap my cc last month was over $5k

being dead beat – I paid it ALL as usual

Interest paid since 1995 = $000,000.00

It is time to make cc transactions flat fee instead of COMMISSION BASED %

based on my purchases last month banksters ‘STOLE’ $150 from companies

…”based on my purchases last month banksters ‘STOLE’ $150 from companies”

It’s time to make the “swipe-fees” explicit by having a “cash price” and a “card price”. It feels like there is a “soft ban” on cash, much to the benefit of banking criminal syndicate and the tax collectors. This will not end well…

Credit card companies often make merchants sign contracts prohibiting cash discounts. For same reason, gas stations give cash discounts and limit some CCs acceptance.

How to approach a merchant an get a cash discount: Split whatever fee they pay to CC company. Assume 2-6% withheld by CC for money charged on card; You should ask for 2% discount, thus both come out 2% ahead, plus merchant has immediate use of money instead of the and pay late; ~6 week delay in payment, and can simplify various paperwork.

Tradesmen and merchants save the ~29% they would pay to CC company to buy needed supplies and thus should at least split that with even a larger discount to you.

My understanding is Federal law (Dodd-Frank; see link below) explicitly allows merchants to give discount for use of cash. On substantial transactions, generally all you have to do is ask the merchant for the cash discount. WalMart clerks can’t approve this discount, but the owner/manager of a high-end clothing store probably can…and will.

Merchants accepting cards usually receive cash in their account within 24-48 hours (merchants pay card & bank fees to the merchant’s bank at the end of the month).

Merchant credit card fees are a deliberately murky topic, but I’d guess 95% of merchants negotiate an “interchange fee” in the range of 2-4% of the card transaction amount (AMEX slightly higher). This “interchange fee” pays for a variety of things:

1) IT transaction processing fee: This is an approximately flat fee (probably averaging $0.15 or less) paid to the card organization (Visa, MasterCard, Discover), not the bank who issues your card.

2) The remainder essentially goes to the bank issuing the card used for the transaction:

a) If this is a “premium card” (eg: Visa Signature), most of it goes to fund cardholder rewards (eg: airline & hotel miles, X% cash back, et al)

b) The less premium the card, the more the merchant fee goes to fund card operations, including credit loss reserves.

LINK: https://www.paymentsjournal.com/surcharge-vs-cash-discount-program-whats-difference/

HOW DARE YOU!!!!

HOW IS OUR GODD***ED SOCIETY SUPPOSED TO FUNCTION WITH RESPONSIBLE PEOPLE LIKE YOU!!!

WE NEED SLAVES!!!!

Heh, actually, screw the banks, if they want to charge me fees, I better be getting commensurate perks with it. Otherwise… well, last time I checked, Costco still accepted cash.

MCH

I’m curious: in your opinion, which do you think is the better “commensurate perk”:

a) Airline (or hotel) miles @ 1 mile per dollar charged

b) 2% cash back on all transactions

Opened the free cash gate to save the day only to have this Credit card after effect stab itself on the foot… who would have thought? Well the big financial institutions have made their more than fair share from the growing balance sheet, so still a huge win for them, right? LOL

This seems pretty obvious, i.e., people with low wages and increased debt required several credit cards to pretend to be solvent, up until now — then along came pandemic, and stimulus — thus, people paid down balances and didn’t want extra credit cards … maybe.

Now what, will those people suddenly want extra cards and increased debt, as unemployment rises?

I did notice the limits on future Fed lending facilities had an exemption for both credit cards and student loans, so it seems both parties are planning on allowing the Fed to print money for both student loans and credit cards, as why allow the exemption as it was a very specific exemption to future Fed fund facilities. So perhaps people should be recklessly running up their CCs just like is occurring with student loans (as most understand that will be “vanquished” at some point). Sure it may be irresponsible in a pure capitalism system, it is “just good business” with our current money printing regime, right? I mean when you see via the new stimulus bill that companies can both write off the free PPP money, and ALSO double dip a second time by writing off expenses from spending that tax free PPP grant/loan…yet those who get unemployment have to pay taxes on that “income”…seems like Corporates 2, Peasants 0. So I ask… is it irresponsible for the peasants to drive up loans that the Fed may forgive soon enough? The rules are changing fast…and the rules apply differently for people versus corporations, and it seems like the corporations are winning…

On a side note, U.S. Bank bought out my CC bank recently, and sent me a letter to tell me about “the exciting news” that they are dumping the 1.5% cash back bonus once you hit 100,000 reward points. I was glad they dumped the bonus, as I found a 2% cash back at another major bank with no annual fee, and there is a 2.5% cash back with $99 fee at a smaller bank. So right now, my best possible “safe CD investment” opportunity is 2-2.5% cash back via CC rewards. How crazy that debt is now a “High Yield Asset”? I look forward to owning a million dollar mortgage that pays me $25,000 per year…fingers crossed (sarcasm)…

I love it!

My PenFed Visa pays me 2% cash back on purchases and I pay it off in full each month out of a Premium Savings account that pays 0.5%.

Almost as good as a 2.5% CD, although with the CD I have to pay income tax on the yield.

Sooner or later, these banks are going to kill the cash back on the CC’s.

Banks won’t have to kill cash back when they raise the percentage they charge their captive customers – the vendors. It’s all on-line credit cards now my friend.

Yup. Credit cards are the ultimate man in the middle scam. I used to run a company that sold a bit direct to the public. After the first year the credit card company called us and said our fee was going up by 1.5%. I asked why and they said most of our customers were platinum card holders so they had to recover the cost of the freebies.

If I tried to get the customers to pay with debit or added a credit card fee they would get angry because they wanted their ‘free’ stuff. Ultimately they were all paying for their free stuff in higher prices but that was far to abstract a concept for most of them.

Brilliant business model really.

Actually, it is you and all the other consumers who really pay the 2%.

Merchants get charged these “perks” by the credit card companies and so adjust their prices accordingly.

My auto and lawn mower mechanics both give cash discounts.

Yort,

Clarification on PPP. It is not “tax-free”. It is taxed as revenue, offset by the expenses covered. The expenses covered are no longer deductible as a business expense. For some, the increased revenue from PPP will create a tax bill they can’t pay, think struggling restaurants as an example.

I agree with your assessment of the cash-back schemes. If you want profit, usurious rates will cover the cash-back.

Holiday Greetings to all. May 2021 bring better times …

Well except for the Churches… That get to rob the congregation again… This time from government till instead of collection plate…

The wall between church and state is the one we need to fortify.

Root Farmer,

There is change underway: According to my superficial understanding of superficial reporting, in the new stimulus bill, there seems to be a provision that would allow companies to deduct the expenses paid for with the forgiven PPP loan money, therefore making the PPP loan forgiveness completely tax free. This would apply to the first & second PPP generation. Regulations will have to be written to clarify this. So check with a tax expert before you do your taxes.

Wolf,

Thanks for the tip. My info is stale as I haven’t talked to my accountant in 2 months. I rarely file without an extension so waiting for final rules shouldn’t be a problem.

These are strange times indeed.

Fed allows banks to resume share buybacks,

3 days ago.

Fed eliminates required reserves for many types of accounts in April 2020. Fed aggregates savings, checking and money market accounts in H.6 in September 2020. H.3 going away. More creative Fed accounting to come in 2021. This indicates something significant. I don’t know what. Yet.

Spur of the moment spending (lattes, lunches, grooming treatment) arent high on the spending list.

My Millennial kid (tech) is spending her $$ on 2 kittens — toys, jungle gyms. I kept my mouth shut but drew the line at a kitten baby stroller.

Save your money, kid.

The baby stroller was sarcasm right?

Had two cards for years, never paid a dime in fees or interest……and never will.

Same here Andy.

Business travel charges of $100K per year and paid balance off every month. The banks hate guys like us.

Seems like they love folks who spend a lot, they’re getting their profit via the merchant fees…

When I traveled on business for 30+ years, it was hard to use cash. They got the transaction fees from my spending, but no carrying interest.

Merchant fee’s and revenue to refinance bad debt with better terms.

I am one of the so called credit card abusers, but the system does not work without people like us. They need to continually recycle bad debt with our revenue. You can’t have a debt business with only bad borrowers.

Actually, you DID pay both.

CC deduct commissions of somewhere between 2%-6% and pay late; ~6 weeks.

Wherever you purchase by cc, these 2 factors are factored in, of course.

Same here. Never ran a balance since 2004.

About 2 months ago I called up my credit card company and had them reduce my credit limit from $5,000 to $1,000. I only use it for online purchases anyway, so I decided to limit my risk. I also have a credit freeze in place with all three credit rating agencies.

Interestingly enough it caused my credit score to drop from 810 to 780. I’m really heartbroken!

Dave — The reason is a cut in available credit is not a good thing… Example you have 10K outstanding overall and available credit of 30K —Great 30% utilization. Have them cut the available and closing an empty card now puts your 10K outstanding at 70% of the total available. The credit bureau reads that as maxed out and a higher balance as a percentage of total available credit. Your score will drop

My definition of freedom is one should not get punished for not doing anything wrong. But in your case, it appears you have been punished …. for not doing anything wrong.

Such are the facts of life in the USSA.

What makes you say he’s been punished? He decided he doesn’t want to spend more or take on more debt. The credit agencies help him out by reducing his credit rating, thus making it difficult to acquire more debt … which he didn’t want anyway. Where’s the punishment?

LOL. If that’s the case why not reduce his rating to 700? 600? or 500?

Definition of credit rating: “A credit rating is an evaluation of the credit risk of a prospective debtor, predicting their ability to pay back the debt, and an implicit forecast of the likelihood of the debtor defaulting.”

It doesn’t say there that credit rating is a measure of a person’s willingness to take debt. But hei it’s obvious you eat propaganda for breakfast, lunch and dinner.

Exactly. When he asked for a lower limit, he explicitly told them that he doesn’t want to handle a higher debt level. They don’t care why he did it. They just agreed with his own assessment and lowered his credit score.

If you tell the bartender to cut you off, don’t complain when he refuses to serve you a drink.

Don’t be a d*** MonkeyBusiness. Your statement was questionable and I questioned it. It gets hard to sort the complaining and whining on these forums from actual reasonable thesis, sorry if my trying to sort it out offended you.

Zantetsu,

I agree with your point. CC companies do not change your credit rating, your credit experience does. Your credit score comes from the credit bureaus who use data from banks to assess “credit-slavishness”. As pointed out above, if your credit limit is lowered, so is your credit score. Blaming the bank for this makes no sense. The have committed enough real crimes that whining over what they are not responsible for is … tedious.

Insurance companies use credit scores in underwriting, ultimately how much premium they will charge.

Best government money can buy.

Dave Kunkel

I’m not a credit score guru, but I do know credit utilization (% of credit limit used) is a big factor in credit scores. So the same amount of credit card spending with a lower credit limit will result in a higher credit utilization.

Having said all that, a 40 point drop sounds stiff.

I really don’t care what my credit score is. In 40 years I’ve never had an outstanding balance on a credit card. I paid off the mortgage on our first house in 10 years. I paid off the mortgage on our second house in 5 years. I’m not much of a credit risk.

I just find the whole thing rather amusing.

Dave Kunkel

I’m an 8-year retired CFO, but I was recently surprised to discover credit scores are used for a variety of things other than providing credit; I’m sure the following is a very incomplete list:

a) Credit (you knew this and don’t use or care about it)

b) Pricing your car insurance (you may not have known this)

c) Employment decisions

d) god knows what else

I think your risk with credit cards in the US is limited to $50 in case of fraud (unauthorized charge). Check the documentation.

But debit cards may not have that limit as there is no such requirement and banks may all do it their own way. Debit cards are linked to your bank account. I don’t ever buy anything online with a debit card.

I don’t use a debit card,,, PERIOD…

It is a pipeline straight into your bank account.

And you are correct… the biggest hit you can take is 50 bucks on a CC. And even that never happens. And yes my CC has been compromised several times over the years, but who cares, it’s cost me nothing…

And yes,,, you want a high limit so you can keep your utilization below 30%… Heck all this stuff is free,, especially if you pay the balance off every month… Merry Christmas ALL…

If I’m not mistaken this is the perfect application in which to use PayPal.

Never ever use a debit card online ??

I keep all my real money in a brokerage account and move it to a bank account when I need it. The transfers take two days to clear and the account emails and texts me whenever a transfer is initiated. So if something did go wrong it can be easily stopped.

You are correct. And corporate or business credit cards have different rules from personal cards. Be careful.

Banks will lie to your face to get you to sign up, and then act amazed when they later point out the fine print the told you you did not need to read.

As soon as your bill comes in the mail, pay it asap. That’s one of the best ways to keep a FICO higher — the FICO folks don’t like to see last minute payments. In addition, a higher credit limit is better, but always pay early — it’s a good habit to get into!

MC

I doubt “last minute payments” have any direct impact on credit scores…with one minor exception:

Credit card issuers generally spread “payment due dates” throughout the 1st 27 business days of the month (plus “last day of month”); however, banks usually report all their account balances to credit unions on a single given day of the month.

If, by pure chance, your early payment was processed by the bank BEFORE the credit union reporting date, your balance would be lower by the early payment amount, lowering your credit utilization, and perhaps, somewhat increasing your credit score.

for 35+ years, all 3 of my bankcard accounts are paid off with auto-pay from my checking account, so each is always paid to $0 balance on its exact date-due (never early). This “last minute payment” has never had any impact on my >800 credit score.

The hiccup I sometimes have is paying for a couple international trips in a single month. Even though this is always paid to $0 at the end of the payment period (usually 30 days after the billing date), for a brief period, this causes my credit utilization rate to skyrocket, and, for about a month, my credit score gets dinged as much as 20 points.

It’s not last minute. All that matters is your balance on the last day of the month, and late payments.

If you zero out on the last day of the month you are golden.

Your debt holders report every month as of the last day of the month.

But I agree the credit reporting system is a joke.

I abuse every loop hole I can find, I never pay interest (other than mortgage). I manufacture spend and churn high value credit cards and my score is constantly flirting with 850.

I really hope they never institute the rumored system where I would be a ‘B’ class borrower and people who pay interest and late fees… but do not ever default are ‘A’s’

Plus, Martha, you are earning ZERO on your bank balances, so might as well pay ASAP before a meteorite hits the earth or Uncle Same does an Idle Cash Seizure. The Fed has eliminated the age-old practice of lagging payables and leading receipts. Leads and Lags. Maybe leading receipts is still a smart thing to do, but good luck on that one in a cash-poor business environment.

What is this “mail” thing you speak of?

The perfect storm is brewing for the U.S. banking system. Not only will these bloodsuckers have less revenue from usurious credit spreads on credit cards, but the Loan Default Tsunami is rising to a peak. Commercial real estate loans, apartment loans, auto loans, home mortgages, and signature loans are about to start stinking up the Einstein Insane Banks’ Balance Sheets in about 11 days.

Now the Fed has been subsidizing the banking industry since the year 2000 in one fashion or the other, their favorite vehicle being interest rate margin subsidies with below inflation interest rates manipulated by the Fed. But despite the Trillions of savers and taxpayers dollars that the Banker’s Bank has thrown at the morons, the Banks are once again sitting of the Precipice. Or, they have already teetered over the edge as

bank-failure-wary consumers move funds from Time Deposits (M2) to Demand Deposits (M1) with one foot out the door to buy THINGS with rotting Dollars before Consumer Inflation erodes them further.

Another BANK BAILOUT in this country will cause rioting in the streets. So many Americans are suffering financially and emotionally right now, that the mere thought of this group of Connected Insider Elites receiving additional Taxpayer Liabilities known as Bail-Outs is enough to boil one’s blood, figuratively. If one looks at the Financial Sector ETF, XLF, as with the majority of financial stock ETF’s in 2020, it is down YTD 2020. XLF is down 5.6% in a runaway stock market. Hum. COULD THE WRITING BE ON THE WALL, and Broad.

Of course, today’s Stimulus Bill includes $12 Billion for the bankrupt airline industry, so madness still reins in Washington.

David

Moving money from M2 to M1 might not help if the FED pulls a new tool from it’s bag, Bail-Ins. The first trial run occurred in Cyprus circa 2013, originally all accounts would be dinged. After months of wrangling in their Parliament accounts under 100,000 Euros were exempted.

I read the Canada discussed adding language for Bail-IN inclusion but I’m not sure if it was adopted.

The BIS wrote a white paper in 2010 which examined the use of Bail-Ins and I’m sure it’s been discussed within maybe closed doors at the FED. If it ever happens in the USA it will come out of the blue, done deal from our friendly all powerful FED.

I remember language of bailins being in the Dodd Frank bill. If I remember correctly it allows for bailins of saving accounts but not checking accounts. I don’t know if that has since been modified.

Remember chatter of bailins just in the last year.Cyprus/Greece,anyone?Made sure to keep the minimum and $1 only in my savings.Heard of the FED simply putting regular banks down like a malformed,useless animal.Observe:FED direct accounts were introduced a few months ago.Also note the increasing closure of bank branches as well as reduced hours.This very topic was the subject of lengthy and heated U.K. Blog months ago.Problems accessing$$,long waits,being hungup on/no help,fewer closeby banks,etc!!

The Fed has subsidized the creation of debt..

and when you subsidize something, you get more of it.

Rates are artificially too low and have been so for 12 years.

(excepting 2018)

Free markets work when allowed to, but central bankers think they know better, interfere, and create eventual havoc. Here it comes.

‘Another BANK BAILOUT in this country will cause rioting in the streets.’

I doubt that. Helping rich folks get richer has been going on for good while now in congress. With only tepid response from ‘the people’.

I don’t see that changing.

Doug, just wait until the wait times in food bank lines becomes 12 hours plus and the homeless hordes are roaming the streets near you and me. People ignore the news until they become the news. You keep poking the caged beast in the nose and he eventually comes after you. This developing Depression will exceed the pain and suffering of the 1929 Collapse, stay tuned. I hope not, but the odds now are against a mild recession going forward and any quick resolution of the impending Debt Collapse.

This has been a recession for years,it is just that certain parties lie,massage the numbers,hide the numbers,distract us with Shiny things.Many other insightful people agree that a Depression is fomenting.Data backs this up.Lines at many foodbanks Are quite long.Just read about a s. Side Chicago foodbank newly opened this year where there were lines going back blocks and wait times were two hours.Antihunger charities here and in Getmany as well as the U.K. Are talking about twentyfive-200% increase in demand.Just saw video about French foodbanks last night.It said they also have Huge increases in people seeking food,especially students as they are not eligible for covd relief and its Very difficult to find decent work,especially for foreign students.Donate to foodbanks/petpantries!!

So wait, China can’t get the stuff here fast enough, (by container) and we are all paying cash?? People in the midwest can’t sell product??? Lame Duck Pres wants to throw down a few more tariffs as he leaves. Is it 1932 yet?

It speaks volumes that we’re at a place now where encouraging consumers to use credit cards with rates that are blatantly usurious is a good thing.

Let me off at the next stop.

In the last financial crisis Macys closed my account because my credit score dropped due to foreclosure. I’ve been in a Macys maybe twice in the last 10 years because they closed my account when I didn’t owe them any money.

This time around Saks closed my account because I hadn’t used it in a year. They didn’t get any of my Xmas money this year and I don’t expect to be spending much there in the future.

People have had enough and it’s showing up in these numbers. I think many are utilizing products in the shadow banking arena which the fed is not even tracking.

BTW, at the beginning of the pandemic, I heard some guys bragging about how they were using all their deferral money and zero interest credit card deals to buy gold and silver. If they really did it, they are sitting on some nice profits. Same as anybody who used this strategy to speculate in the equity markets.

I have since heard credit card companies have banned their use to buy PMs. Could be something to the boast.

Petunia, as a former Precious Metals broker, it makes no sense to allow purchases to be made with credit cards. My average gross margin was 1.4%, so the cost of processing a credit card payment would pretty much kill my gross profit line. It was always by bank wire with a minimum $10,000 purchase. Had a great business with clients buying in size as early as 1998 at $280 per oz. Gold. My clients have done very well almost without exception.

They are still taking CCs they charge more, and with premiums to spot already wide it either does or does not make sense to use credit. If you want to leverage up, go all in, then by all means. Carrying a balance for a few months is probably no more onerous than paying option premium.

Petunia, Capital One cut my lightly used card limit in half. Now I buy only one $5 hamburger every month, and they buy a paper statement, an envelope and a stamp every month. They get paid on the due date every month.

Half in jest: It’s the travel slowdown. People get credit cards to rack up airline and hotel points. With discretionary travel and tourism down, who needs travel points.

Wolf-i don’t know how you keep up with the sheer bulk of mopery, dopery and general bizarrity, but i DO know i’m glad you do.

Your final paragraph is a gem-reminds me of discussing credit with the younger folks in the moto shop back in the day, and watching the range of understanding (from thunderbolt impact to total incomprehension) on a face when i said: “…well, what you’re REALLY doing is buying MONEY on time, NOT the (fill in the blank)-are those dollars at that rate a good value versus what you can really afford?…”.

Again, thanks for all you present here, and to all who read and to those who go on to comment.

may we all find a better day and holiday season.

1) Credit cards balances peaked in Jan 2009, at peak crisis.

2) Credit cards delinquencies peaked in Q3 & Q4 2009, in Dec 2009, a full year later.

3) Q3 2020 c/c delinquencies ‘wonderful life” low is a test of 2016(L) previous bottom.

4) The banks dressed their balance sheet for the Fed stress test.

5) Credit cards balances : in the last x6 months all the dots are glued together, shortening their thrust, hardly moving lower.

6) The banks swept existing delinquencies under the rug, constrict available lending, rejected new applications, in order to get a passing grades for buyback, at (perhaps) beyond peak markets, when it’s too late, so it’s a fake…

I started using a $500 gift cards instead of credit cards for on-line purchases. Much safer. My AAA BOA Visa was hacked at least 3 times last year alone. They even upped my limit from $1,000 to $5,000 by using public domain info to raise the limit w/o my authorization and then spent the entire 5k. Must have been an inside job or an incompetent employee who allowed this to happen. Still have the credit card. Use for gas and car expenses only.

Look into a credit freeze, that will stop that BS.

I was exposed in the Equifax breech, but the Freeze has kept me safe.

Hey I was just thinking — if our government is gonna act like Argentina, does that mean we can be good at soccer now? Can’t we at least buy Messi with some of that money?

Argentina is better than we are at Rugby Union and I’d much rather we be better than them at that. Wouldn’t even cost that much.

Another factor that may contributing to the falling credit card balances is the fact that cities like DC and Baltimore are nearly completely shut down, and there is virtually nowhere to go an nothing to do. There is nowhere to go and spend the money. If you have all the “stuff” you need and spent most of your money on services and entertainment, these latter two things are in short supply right now. My big entertainment is going into my backyard and feeding birds and squirrels. That doesn’t run up too much credit card debt.

True, on the hit to things like travel and dining expenses.

I do notice a lot of people spending on hobbies like there is no tomorrow. I’ve probably spent close to $2000 at Sweetwater.com on music stuff, and maybe another $1000 on amateur radio in the last year. If you are going to be inside might as well pick your instrument back up. :)

Watch out for that HF bug, it’s addictive.

VE7 PSW

The birds and squirrels,say ThankYou! I,too feed the animals.Simple pleasures! :-)

Greedy banks with sky high credit card rates.

Those with bleeding nose woke up and saw the writings on the wall that greedy banks would not or refuse to lower the credit card rates in good faith.

Not!

I’m paying down my balance as quickly as I can and assume most common folks are hellbent to free themselves from usury institutions that the Pope wants to banish into eternity!

For years I kept 100K at Citi so I could enjoy all the freebies that entailed, plus they paid me 6% interest on it. Towards the end of the game in 2008, a bank officer yelled at me in the lobby: WE’RE LOSING MONEY ON YOU!!!! I knew it and so did they. I paid off my VISA card completely every 30 days, it drove em nuts. Plus I refused to refinance my paid-off mortgage.

The bank officer drove a new Benz, btw. So did they all. They lived like royalty off the backs of working stiffs who could barely make ends meet.

I’ve got a decent amount of cash in my credit union and the more it accumulates the more polite they are. Of course credit unions exist to support working people as the first ones were basically financial collectives run by the members for the members. Anyone can run to be a director.

I bailed from banks in my twenties when they wanted to charge me to renew my mortgage, something they made money on. Screw ’em.

Great comment down below about saving harder. Words to live by for sure. Remember the old adage of, “Pay yourself first”, which of course meant take the first 5-10-whatever percentage of your pay cheque and throw it in savings and pretend it didn’t exist. It works.

I got rid of check book a few years ago and this year my only credit card. It’s all Vanguard, a credit union and a debit card now.

Paying yourself first is all fine and dandy, if there’s anything left after paying for life’s increasingly inflated basics …

Sure it works, until it don’t!

Banks used to say that 80% of the customers provided 120% of the profits. That bottom 20% of customers were unprofitable so they devised ways to drive them out.

Wolf, I noticed something curious about the Credit Card Balances seasonally / not seasonally adjusted chart above. Why does the seasonally adjusted line not sit half way between the peaks and troughs of the not adjusted line, instead of at the peaks? I thought that seasonal adjustments should average to zero. More jiggery-pokery?

Yea, assuming the peaks are the 4-5 wk Thanksgiving/Christmas retail season, the other 11 months of the “seasonally adjusted” graph always seem to approximate the next year’s peak.

BoyfromTottenham,

Yes, excellent observation. I’ve been wondering about this ever since I started comparing them like this. It’s clearly not an “average.” Seasonal adjustments are purposeful and decided by the people that design the aglo. That’s the only explanation I have — that the seasonally adjusted number, which is the ONLY number cited in the media, only reflects the peaks :-]

Which is why I increasingly put both into one chart so people can see this on their own.

I think the fed is using all the top line numbers because they want to be able to accommodate peak credit demand periods during the year. Their job is to have credit available to fund the economy at peak demand, low credit demand periods are another issue and not as important.

Their thought may be as follows:

If they focus on capacity then the run rates can take care of themselves.

Love my Costco CC and my Alaska Airlines.

Buy everything on them. I get more bennies than my savings account that used to be 2.5% and now is something like .65%

Ugh, I wish I knew what cash was worth.

Also, I wonder wat the current state of subscription services like carwashes. It seems like there are a lot more dirty cars driving insanely these days.

Zero interest doesn’t work, because people in my circle don’t spend or “invest”. They *save harder*. Hard times are a comin’ and if people have the ability they are hunkering down.

> Zero interest doesn’t work, because people in my circle don’t spend or “invest”. They *save harder*.

BOJ hasn’t learned this yet either… they’re on QE 23… lol

Interest rates are really the “grease” of the economy.

Interest rates create and income to the saver that turns into consumption.

Zero interest rates remove that economic engine.

For every action…there is an equal and opposite reaction.

The Fed doesnt seem to notice..

they are busy with rate cuts, printing, and pushing on a string with a bull dozier …

Put interest rates where they should be, equal to real inflation, and normalcy will return. The fluffed markets may not like it….

Historicus, I have seen estimates of $16 to $18 Trillion having been robbed from American Savers since the Great Fed Rate Suppression Campaign began in earnest since 2008. NOT SMALL POTATOES.

The Great Unwashed will stamped into risky, dubious “investments” to compensate for interest rates not even paying for inflation. Some will make more money, most won’t, and some will lose a lot. The smart people “save harder”, like you save. It is the only prudent thing to do.

Most people have tons of things they buy every month that can be cut out of the budget.

Curious if a drop in cc payments has anything to do with people refinancing their homes and paying off higher interest debt. I’ve heard this is a pretty widely used strategy from someone who went from the hospitality industry to mortgage refinancing.

Yep, we’re doing a lot of cash out refinancing appraisals here while everything is shut down. What the heck are these people going to do with the cash out money but pay down debt. Ain’t nothin open.

SC, I was thinking of doing a cash out refi to pay down my mortgage. But then I realized that was the kind of thinking the Fed is doing so I dropped the idea.

With the new tax laws capping the size of the mortgage that you can deduct and hence the amount of interest you can deduct and the limit on State & local income taxes that can be written off, its no longer a slam dunk to take out a big mortgage and leverage your home even at these low rates. Run the numbers and you may be surprised. Of course everyone’s situation in unique. Mortgage bankers, loan officers, Realtors, and most accountants are the last persons to listen to for advice on this matter.

At least in part, credit card applications are probably down because tourism is down and other perks associated with opening new credit cards is also down across the board.

Americans have become rather savvy when it comes to opening new cards to get free travel points. Less free travel opportunities is probably associated with less great sign up bonuses and less credit card activity.

That’s my hunch.

How are these numbers affected by consumers who purchase on credit, but pay off the balance by the payment due date before interest is charged?

Here in the UK we get treated nightly to adverts from some loan company iffering quick loans. At the bottom of the screen it clearly states 99.9% APR. You think to yourself, how in any decent society can that pass by the regulators? Clearly this is set just below some allowable threshold, so someone has authorised that up to 100% is allowable. As pointed out here this is while they depress central bank rates and destroy savers.

Restaurants, airlines, hotels and sports/cultural events are restricted or discouraged. Every time you leave the house there’s tense reminders everywhere that the world is in distress. It doesn’t encourage freewheeling credit card spending.

1) The Fed put a puzzling muzzle on bank’s cash advance.

2) As early as next week, a couple with two dependents can get : $600 x 4 = $2,400 from the gov.

3) For them, 2020 total is : $3,600 + $2,400 = $7,000 in less than a year, tax free !!

4) US treasury compete directly with bank’s cash advance, especially with a new round of ppp loans. We are going to hate and miss that good ole billionaire gov.

5) The banks offer a teaser rates for nine to fourteen months,

thereafter raise rates to c/c market rates. That’s how poor people are trapped.

6) The gov disrupted this process twice this year.

7) But the Q3 2020 stress test is over (the test wasn’t done in Q1 2021). Dressing bank’s balance sheet isn’t necessary anymore until the one. The wild risk on behavior phase is next.

8) Use the unused vacations days fast, thanksgiving, Xmas spending

and traveling, the last gasp of small businesses c/c usage, along with ppp loans, to survive.

9) Credit cards balances will rise in Q 42020. Credit card delinquencies will shorten their thrust and turn backup in 2021.

10) The Covid cause is on, but the pain is treated by another dose of

cash treatment.

2020 total for :

1) a single man : $1,800.

2) a single woman with x4 kids : 1,200 + 4 x 600 + 5 x 600 = $6,600.

Micheal Micheal Micheal, you must have figured it out by now, that only irresponsibility is rewarded in America today.

Divorce happens to the best of us.

Who says they were ever married?

Who says they weren’t??? Get it?

In any financial planning software, you can input monthly savings, interest rate, how many years, etc. I have never seen one that accounts for divorce, which happens to 60% of married people.

Cue the Eddie Murphy routine on YouTube about “HALF!”.

Roddy6667, “community property” does not mean the split in a divorce will be 50/50. Ask me know I know!

Oh yeah, I get it. It doesn’t matter one way or the other.

Met a single mom with six kids who admitted to four different dads. She said no sign of those four horsemen around the corral.

Micheal Engel,

Two things:

1. The fist stimulus was $500 per child, not $600. So…

A single woman with x4 kids: 1,200 + 4 x 500 + 5 x 600 = $6,200.

2. The stimulus for the kids doesn’t go to mom automatically, but to the person who claims the kids as dependents on their tax return, which could be mom or dad or grandparents.

A single man with 4 kids: 1,200 + 4 x 500 + 5 x 600 = $6,200. Ironically, same as single woman with 4 kids.

Fathers are granted custody only 18.3% of the time

88% of the time, willingly.

In 2009 I know of many people who walked away from their excessive new homes and mortgages and in 2 years they were accessing loans at very competitive rates…not high credit risk rates. The electronic revolution has cut into banks fees dramatically…when was the last time anyone bought checks? I have my brokerage account connected to my checking account so when my Direct Deposit check comes in I immediately transfer a portion to Brokerage account…Bans now charge $3.00 “transfer fee”…just like they charge you fees for using ATM’s…the banks earnings on fees have not really diminished in the past 12 years as they always “find a way” to fee you…which leaves many searching for ways to cut fees and/or find another way…the banks have always been the true “robber barons” of our times…and now Jerome allowing for stock repurchases is just getting paid for all of his work in creating the wealth division started by Bernanke…

1) Xmas 2020 cash envelops is a growing trend.

2) Every Fri afternoon, small business bookkeepers, or owners, are driving to the bank takeout window, waiting in lines for the vacuum shoot, to collect their envelop with thousands of dollars in cash.

3) NYC + SF executives with > $104,000 salary will not get their $600 gov stimulus.

4) Small businesses pay employees smaller salaries, off the books cash and Xmas bonuses.

5) Xmas party 2020 is on thx to the gov ppp loans.

Maybe the big picture is the Siamese twin the Fed govt and the Fed has finally gotten to what they believe is nirvana where they are the only game in town about keeping the economy alive. Where the US government gets paid (in real terms 1.2%) to borrow money and hand it out as if the government is Santa Claus. Where billionaires preach green energy after early stake holding this sector while jetting and boating between mansions.

There is another factor not mentioned in the article. Credit Card companies and banks cancelling cards when those cards aren’t used enough. Here’s my example.

I hadn’t used one of my cards in 2020. I got an email saying my card had been cancelled due to non-use. No letter in advance. Just an email telling me it was cancelled.

I have tried 6 times to get the card re-opened. I’ve memorized the questions they ask. I need to re-apply to have my account re-opened. With the hard hit on the credit report. Each time it fails; and for a different reason. My credit reports are locked (thanks Equifax hack). We can’t use the one-time code Experian provides, our systems can’t use it, you need to unlock the credit report for everyone. We messed up and thought this was a credit limit increase request (on a closed account). We messed up and didn’t try to access your credit report, oops. We messed up again but don’t know what that was. Etc. It’s almost like they don’t want my business.

BTW, my credit score is >800.

I have a CC I haven’t used in 6+ years and they haven’t cancelled it.

On a trip for the holiday I decided to call my bank or whatever they are and ask about home loans. They told me at this point they are not doing any conventional loans, only VA.

A good strategy to use with credit cards is to assume they will be hacked and divide your expenditures into tranches that will limit the damage if any one of them goes down. Did this after 3 hacks this year and 2 last year. The hacks occurred without warning and devastated my financial accounting and budgeting becausue everything was mixed together on the card that got hacked.

So I went to the system below which has worked great

1. On-line purchases – $500 gift debit card from Giant Food

2. Periodic monthly billing – i.e. Internet, insurance on appliances, home maint ctr, ans service, periodic medical exp

3. car expenses – gas, oil chg etc, AAA, parking

4. business expenses – cap expenditures, software licenses, educational , travel.

5. Home impr – Home Depot credit card

The 5 cards are paid off in full every month. Everything else that doesn’t fall into the above categories are paid with personal check or cash.

The holder is not liable if their credit card is stolen, so why would I care about the bank’s money? If they paid me then yeah I could add some extra security. Otherwise it’ll go towards their losses which the customers and shareholders already paying for.

Swamp Creature

Proposed new strategy for you to consider:

ENVIRONMENT:

I only have 3 credit cards (one is Amazon store card) and 1 debit card. All credit is paid to $0 each month.

STRATEGY:

All my bankcards offer comprehensive text alerts for various events; I’ve set mine to text me for any withdrawal or charge exceeding $1 (the allowed minimum).

I get texts on my iPhone within 15-30 seconds of the card swipe (I also get them for vendor auto-pay, like the water bill).

I recently became aware of a new internet scam (unauthorized Zelle person to person electronic DDA cash transfers), so I’ve added a daily report showing opening DDA balance, the day’s DDA activity, closing DDA balance.

COLLATERAL BENEFIT:

I’m retired and, pre-Covid, traveled 2-3 months/year throughout the world. These alerts keep coming as long as my phone connects to the web (I always travel with the international plan, which just keeps getting cheaper). The intensity of the effort to steal from you electronically in some parts of the world is just plain spooky (Europe is especially bad).

General comment on digital payment systems in America:

If you think cash will disappear anytime soon, fear not, we are so behind in the digital integration of payment systems it is an embarrassment. Every time I hear AI is being used to advance payment systems, I think it must be a top secret project, because I haven’t seen it yet.

There are too many examples to illustrate my point, but here is a common one. Debit Xmas cards cannot be used as partial payment online at most/any retailers. You cannot use the gift card issued by a credit card company to make a partial payment, then pay the balance with another payment method, even if the other payment method is the retailer credit card. I have overcome this on occasion by using the gift card at the physical store and paying the balance in cash. Online, the same retailer would lose the sale, because they are that far behind in their ability to take digital payments.

This is not a trivial issue because many people now get income on different debit cards, and can be closed out of a transaction because their money is on separate cards. They must then cash out of one card, if they can, and add the money(less fees) to another card.

Nothing about this looks like an advanced payment system. They are all payment silos with cash bridging the gap.

Funny thing is, the financial system used to be the lubricant of markets and the economy, the pride of US capitalism. It has now become a parasitic rent extraction mechanism, as the country is slowly working its way towards Neo Feudalism.

Record-breaking low mortgage interest rates are now well below the real rate of inflation (ignore for a moment the fake headline CPI). This is one of the primary reasons residential housing is in another huge bubble in terms of inflated market values.

So people are back once again to using their house asset as an ATM machine (cash out refis, HELOCs). They never learn the lessons of past.

Who needs credit card or other types of consumer loans when you have access to extra funds by siphoning off your newly-minted home equity riches (on paper, that is)?

Only in a clown car degenerate financial system can mortgage debtors be given the gift of a leg up savers via Fed’s financial repression regime by using ultra cheap easy money courtesy of clueless but greedy lenders.

You’re witnessing Greenspan 3.0. It will not end well.

1) The stimulus is working wonders, because it’s all about love. Love from our gov :

2) After two negative quarters, US GDP is up $1.650T from $19,520T,

or up 8.5%, in the third quarter.

3) Next quarter, Q4 2020, is very likely positive.

4) By Jan 2021 we are out of recession. The Nasdaq will keep flying to another all time high.

5) My x2 dogs (fake) depend on me…

6) They smelled some storm clouds gathering for 2021.

7) QQQ daily PnF : x3 reversal, 2pt/box, can easily send QQQ lower to Sept TR.

8) Add a min of x2 columns on the right, to those on the left, until Sept 2 high, for a total of : 23 columns x 3 reversal x 2 pt = (-)138 pt. // min target : 310 – 138 = 172.

9) A conservative count only to Nov 9 high : 9 columns x3 reversal x 2pt = 54 pt, to dma200. A bounce from dma200 can send QQQ higher, or add a count to Sept 2 high, for a further down draft.

10) Our weathermen promise that the Nasdaq Rolling Hills on shift higher for two more years.

Micheal:

In the second round of congressional pork giving, each race horses got more money than each American did!

It’s all taxpayer money funding these boondoggles in the Covid-19 stimulus bill. All has to be paid back eventually through inflation, tax increases, or higher borrowing costs. Nothing in there for struggling restaurants that are forced to close. Should be vetoed and sent back to the drawing board.

Thanks for smacking those banking bas&*^%$ in the face. I wish all media outlets would be as frank and honest as you!!

Thanks, Randy

Well I don’t know about anybody else but ive been getting slammed with pre approved credit card offers with 0 percent introductory rates from 12 to 18 months long. So I don’t believe crap the Fed has to say. I trust the Fed like I trust a rattlesnake. Do you think it could be that all entertainment has been put to a standstill? No cruises, airline travel, nights out at restaurants, bars, etc. People can only spend so much money being locked up in there house. And credit card interest rates have always been high. Do you think banks are gonna lower them just because the Fed lowers there interest rates? This is now the land of the mask wearing crazies living in the Lunatic Asylum. There scared of there own shadow so there not about to venture out for a night on the town even in the states that aren’t under lockdown. Much less take a vacation. There’s more to it than statistics the Fed pushes out. Do you also believe in there inflation data too? ?