Consumers and companies keep plugging, the world has not come to an end.

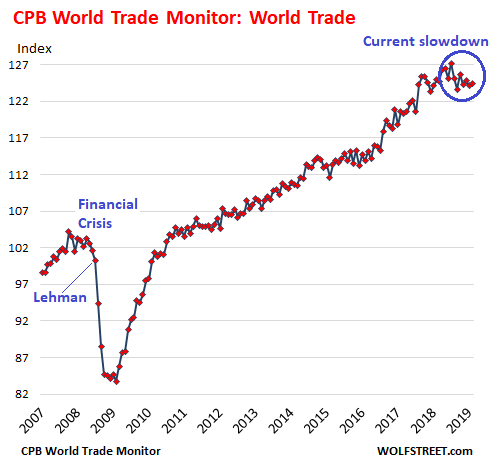

World trade volume – imports and exports of merchandise across the globe – increased 0.3% in May from April, after falling 0.6% in the prior month, according to the Merchandise World Trade Monitor, released today by CPB Netherlands Bureau for Economic Policy Analysis. On a year-over-year basis, the index fell 0.4%. And it is down 2.1% from the peak in October 2018. This isn’t exactly stellar, compared to 2017 and 2018, when the world trade index increased between 2% and 6% year-over-year.

But it isn’t a “collapse” either. A collapse of world trade occurred during the Global Financial Crisis when companies shut down their ordering process – not knowing if the banking system would still be there the next morning – and when consumers closed their wallets, particularly American consumers who provide much of the oomph behind world trade, given their penchant for imports, but they were losing their jobs by the millions. From September 2008 through the trough in May 2009, the World Trade Monitor plunged 17.5%:

The manufacturing slowdown has been going on for months in the US, the EU, China, Japan, South Korea, and other countries. This is a slowdown, meaning anything from slower growth to actual declines. Manufacturing is still growing in some countries, but more slowly, and is declining in other countries.

The slowdown in auto sales in the largest markets in the world has been one of the drivers, so to speak, in the manufacturing slowdown. New vehicle sales have been falling sharply in China for nearly a year, and they are plunging in India. Auto sales are also declining in the US, but at a much milder pace. And they’re declining in the EU and Japan. The auto market is mature in developed economies and is becoming more mature in China. So, flat or lower demand – as vehicles last longer and people drive less – is going to be the norm going forward. This has hit manufacturing.

Another factor in the manufacturing slowdown was the effort in 2017 and 2018 to front-run the tariff threats bandied about at the time. This caused a surge in orders of manufactured goods, which caused a surge in inventories, which are now dragging down orders as companies are trying to whittle them down by ordering less. This is particularly the case in the US where the inventory pileup is enormous.

Manufacturing is only a small part of the US economy, which is dominated by services, such as finance, healthcare, information services (such as telecoms), professional services (such as computer programming, lawyering, and engineering), and housing. And services are growing at a good clip.

In South Korea, China, Japan, and Germany, manufacturing plays a larger part in the economy, and these countries are more dependent on the manufacturing sector for economic growth. Germany faces a slowdown exacerbated by its focus on the auto industry – automakers, component makers, robotics makers that make and install the industrial robots for auto plants, and producers of specialty materials such as adhesives.

But even in these countries, services play the dominant role, and services are growing. Consumers in Germany are doing their job, consuming.

World trade of merchandise, given this slowdown in manufacturing, has taken a hit, but not the massive hit you’d expect after all the vibrant and daily rhetoric of trade war and tariffs. Turns out, companies are still doing what they need to do, and consumers are still consuming.

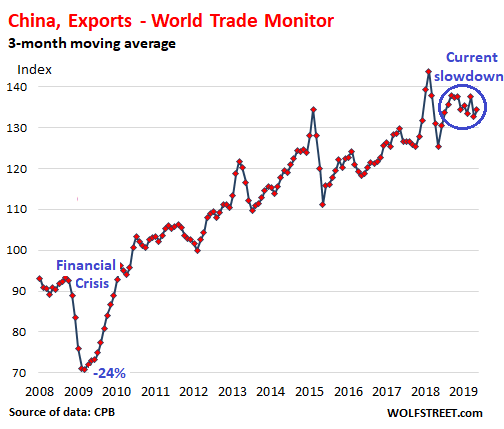

Of the largest trade partners of the US, China got walloped the hardest, as you’d expect, but compared to the drubbing China’s trade with the rest of the world took during the Financial Crisis, the current decline is relatively modest, and appears to have bottomed out already.

This chart shows exports from China to the rest of the world, according to data from the World Trade Monitor converted to a three-month moving average. Note the 24% plunge during the Financial Crisis:

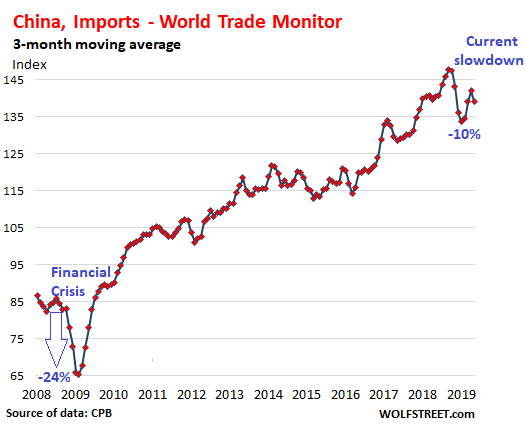

And this chart shows imports into China:

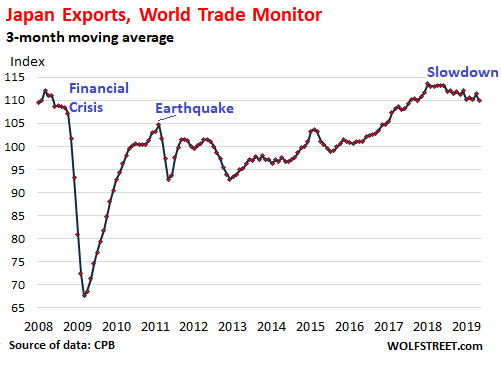

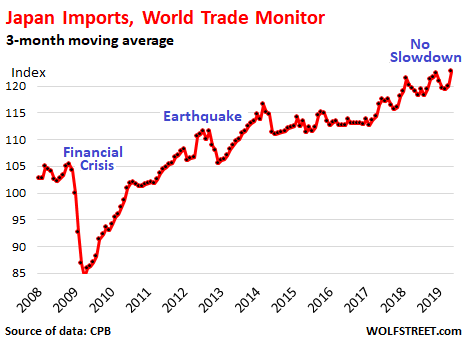

Japan’s exports have been showing declines for the past year, but those declines pale compared to the collapse of Japan’s exports during the Financial Crisis and the sharp falloff following the March 2011 earthquake and tsunami, when Japan’s infrastructure was severely damaged:

However, Japan’s imports are not showing any decline, with the index reaching a new high in May:

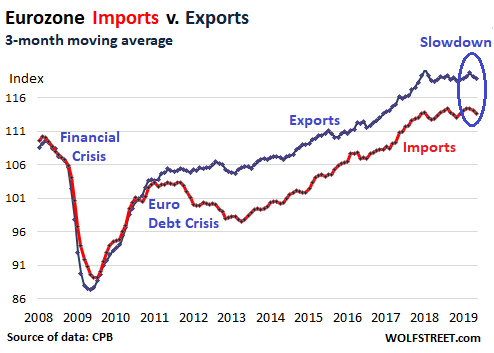

In the Eurozone, there has been some decline in both imports and exports in recent months. While Germany is heavily exposed to the automotive sector and is getting hit harder, other countries such as Greece, Italy, Portugal, and France, are not. Especially in Southern Europe, food exports – such as olive oil, wine, salami, cheese, and other specialty foods – play a larger role among their exports, and there is no slowdown in food products. Also note the impact of the euro debt crisis on imports (red line):

It boils down to this: the trade war and tarriffmageddon have an impact, but companies are still doing what they always do, except they’re shifting their supply chains around, such as from China to Vietnam. Consumers have largely brushed off the rhetoric so far. And services are still strong around the globe.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

Thanks once again.

Trade may have grown but perhaps this is due to a couple of factors related to the trade war.

Could it be that China is shipping goods through new channels to intermediate destinations before they finally get routed to the U.S. in an effort to circumvent tariffs? So the products perhaps go through two or more countries in the shipping process. Might result in product being counted more than once.

Secondly, for some products from China that are unable to be shipped to the U.S. due to tariffs, they still have to be sold somewhere. Read recently that China has been dumping textiles in Indonesia and this is harming the Indonesian textile manufacturers. So trade goes on, perhaps just with different partners.

As an aside, if China is dumping its stuff on its neighbors then perhaps we might read of an intra-Asia trade war somewhere down the road.

I can give one example. I’m in Egypt, countries like Turkey, china, and India are busy building factories here (many textile, also automotive ect…). The finished goods are exported duty free to the US, thanks to the long standing US/Egypt/Israel peacetreaty. Of course, Africa just ratified a new free trade zone this year after lengthly negotiations, so trade is also booming on the continent between partners, China is getting in on that action as well. The US is losing out.

I’ve read that 40% of EM debt is held by China. This level is even higher in Africa, making African economies very motivated to trade with China.

For several years now, Chinese companies have been using labor in Vietnam, Cambodia, and Bangladesh. They have corporations in those countries which export the products to America with a large Country Of Origin label that does not read “China”. Of course, all the profits flow back to a bank in China eventually. Tariffs are so easy to circumvent.

China is consistent in its policies. They view a global slowdown as an opportunity to gain export market share, while other industrial nations pull back. inventory is not a problem. Anecdotally one writer thinks China may be trying to corner the Silver market. This again is what they do, they seek to control the market in any commodity in order to drive down prices and put offshore suppliers (miners) out of business. When you want something with silver in it, you have to go to them.

March was a record expansion of credit in China, and what you are seeing on Wall St is bleed through. Unless tariff revenues can change the Federal deficit they will prove worthless. From my vantage the Chinese are winning and it’s not hard to see why.

As Dr. Krugman says my spending is your income and your spending is my income. the manufacturing sector consumes services. the services do not consume themselves. fewer factory goods will mean fewer goods to transport that is why the transport industries are contracting. the world will go into a recession.

ooe,

There was no recession the last time this happened (2015/16). And in the US, that slowdown in manufacturing and in the broader industrial production was far bigger than today’s. And there was a spike in commercial bankruptcies, which I covered. It also caused a “transportation recession,” which I covered. But no recession. And now the consumer is in better shape than in 2015. Consumer spending is 70% of GDP!

Didn’t because of more stimulus.

Rates are negative or at record lows.

Markets are not responding to lower rates

Interest rates set a kind of baseline for the return on all assets. As they fall, bond values rise and stocks often do, too. But once rates have settled at or near rock bottom, there’s less room for that kind of price appreciation.

https://www.bnnbloomberg.ca/businessweek/a-decade-of-low-interest-rates-is-changing-everything-1.1290927

What do you think about the fact that consumer spending is on the backdrop of increasing credit card balances? I saw that balances have spiked in the last two months.

There was no “spike” in credit card balances. They ticked up to $1.028 trillion, not seasonally adjusted. This is just 2% above where they had been in 2007, but now these balances are spread over 13 million more working people, and consumer price inflation is 22% since 2007. So accounting for the growth of the working population and for inflation, “real” credit-card balances per consumer are relatively low.

Q2 Personal Consumption: 2.85%, up from 0.62% in Q1

Q2 Fixed Investment: -0.14%, down from 0.53%

Q2 Change in Private Inventories: -0.86%, down from 0.55%

Q2 Net Exports -0.64%, down from 0.90%

Q2 Government consumption: 0.85%, up from 0.48%

More debt fueled gov spending too. The party is raging for now.

You mean former Enron adviser Dr. Krugman who predicted a recession in 2002, 2003, 2004, 2005, 2006 and 2007? That Dr. Krugman?

It’s a day that ends in “y” during a period of time that a Republican is in the White House. Therefore Krugman says the economy is about to go into recession.

‘Just Some Random Guy’

I’d say you have a pretty good handle on this idiot. :)

All these celebrities get way too much credit for knowing everything. Even within economics, the Nobel winners basically know their narrow field. If they start pontificating about world macroeconomics and that’s not their field, best to ignore them; like ignoring movie star statements about such things.

I think Krugman predicted the stock market would immediately tank and a big recession would happen right after Trump’s inauguration. ‘Nuff said.

WR already challenged ooe post. Why beat dead horse or Krugman?

Also, there is NO, NADA, ZILCH, etc, etc, ETC, Nobel prize for Economics, it is simply NOT a science as Nobels defined one. At least PLEASE look it up in Wikipedia, and get clear on the ongoing and original debate over that, and why. Hey, I’ll even give you guys something else about Krugman for your bad-mouthing fun, if you promise to do it. Saw Chris Hedges (another breed of cat) tear him a whole new one on Democracy Now. Krugman was sputtering for words, and really looked ridiculously stupid! You’ll love it! Was 2-3 yrs ago.

Echo Delta, would also like to add reductio ad absurdum as being common to these folks “debating” style; i.e.”credit for knowing everything”. From a chart of what has already happened, they decide to extrapolate their own predictions…..as obviously they all have far more educated opinions than Krugman ever could.

It’s fine as long as you’re ad homming with no citations and simply joining the anti-Goldstein chant with the kids down at the Junior Anti-Sex League.

World trade: steady straight increases, year after year, since 2009.

Looks like a top in 2017 and roll over.

Time will tell.

Aw Shucks–they didn’t repeal the business cycle after all.

My dad did his best to help the economy last year. Spent over $1M in health services. Didn’t really change his outcome.

Wow this scares me. My brother in law is a doctor. He always advices no heroic orders. My mother passed away the other year after a period of cancer. Even if death is certain, it’s hard to deal with.

“Spent over $1M in health services. Didn’t really change his outcome.”

Hence, the criminal racketeering of the US health system ….. pay 5 times

as much as the rest of the world, for the same results and services.

The definition of “criminal racketeering”. Congress is in on it.

Fear not, Son-san will save the day. His second Vision fund will help to unleash the next phase of the internet and add unfathomable value to the world, and disrupt countless stodgy old ways of doing things. After all, everybody from Apple, to Microsoft, to Foxconn, but not the Saudis are investing in it.

As the pundits were busy saying a couple of years ago, who needs low wage, low value manufacturing, we can all be value added in the service sector.

Wait, what was that… “oh, ok, three latte with extra foam, a grande chai tea, and a Venti extra scalding hot coffee… yes sir, coming right up, sir.” see extra value add, much more rewarding than some manufacturing jobs.

Really, Wolf? “This unified, amorphous, monolithic structure whose job it is to hold up the entire global economy – is strong and won’t buckle”?

Somewhere said “Debt Slaves Are the Most Vulnerable”

https://wolfstreet.com/2018/05/22/where-the-debt-slaves-are-the-most-vulnerable/

buda atum,

No, you misrepresented the title of the article you linked. The title starts out with “WHERE” … meaning that the article points to a layer of consumers that are vulnerable. Please actually READ the article before trying to use it to make a fake point. Or at least read the whole title. This is what the article says:

“Many consumers are debt free and have lots of money and good jobs, and they check their 3 credit scores regularly. Other consumers have large amounts of debt, lousy jobs or no jobs, and are paying for groceries by charging them on their credit cards. Credit problems always involve the most vulnerable consumers.”

“Many consumers are debt free and have lots of money and good jobs, and they check their 3 credit scores regularly”

Count me among these.

However, in the eyes of the MSM and many posters here, I don’t exist. That’s because in the eyes of the MSM and many posters here, everyone in America is broke and has 7 credit cards with $50K balances at 27% along with $200K of student debt, all while making $11/hr. It’s a narrative pushed to elect people like Bernie. And it is working, unfortunately.

So just watch Hannity then, and “let not your heart be troubled”. He’s worth $100M, debt free, and likely never checks his credit score.

You also mentioned that non-mortgage debt holders are riskier than the years leading up to the last buckle event.

“At year-end 2017, the ratio of non-housing debt – revolving credit such as credit card balances, plus auto loans and student loans – to disposable income reached a new record of 26.3%”

With so many people forced to rent they have less asset leverage to pay back these debts in the future when hardship comes. The asset holders are doing fine, but today’s asset holders are quite greedy. They refuse to accept asset devaluation for the sake of protecting the currency value. It seems minor but in Canada we can’t even afford to produce pennies, the prices of goods are so inflated people didn’t even flinch.

Isn’t true that it takes $3.02 of DEBT to produce 1$ of GDP? I guess all that debt has to from Govt compared to consumers? Or Am I wrong?

Exports from India dropped 9% in June.

The UK reported recent annual export growth.

A world record heat wave in France is supposed to cause a drop in wine exports due to lack of moisture.

New high for global negative yield debt at $13.7 trillion dollars.

The Swiss yield curve is negative out to 50 years!

Consumer is in better shape? Highly doubtful.

Credit card debt is whats filling the gap.

What gap you ask? Disposable income.

Consumer loans, credit cards, other revolving debt, close to $1 trillion.

58% have less than $1,000 in savings.

27% cannot afford an unexpected $400 expense.

78% of US workers live paycheck to paycheck.

Sub-prime mortgages to borrowers with little or no credit score.

New home sales down and revised lower.

Manufacturing PMI now at a 10 year low.

Global stocks slump as German manufacturing craters.

Mario Draghi recommends the ECB begin more stimulus.

As the Fed is about to lower rates by 25 basis points.

Wolf, I consider this article to be below your usual standard. In my humble opinion, it is much too wishy washy. The US may be at this time, the cleanest dirty shirt in the laundry, but the global economic headwinds are approaching at hurricane force. Little time left.

“Permanently high plateau” for all

great comment

Grim reading this

Every immigrant is a credit and consumer expansion engine with the US taxpayer funding the basics.

Look at today’s GDP report, consumer spending is hot! I’ll write about it. Just look at the numbers. People want the US economy to collapse, and they’re disappointed that it doesn’t. So you will be disappointed again.

The consumer was on fire in the 2nd quarter after a weak 4th quarter of 2018 and 1st quarter. Did you note that the 3% 4q-4q for 2018 was revised to 2.5%?

What economy? Call me old fashioned but if a product isn’t really needed, or a service required, or either category really really sought after, then why does it exist?

Regarding: “Manufacturing is only a small part of the US economy, which is dominated by services, such as finance, healthcare, information services (such as telecoms), professional services (such as computer programming, lawyering, and engineering), and housing. And services are growing at a good clip.”

Finance: a skim on handling debt. Healthcare: Rowen gave a good example of a poor situation, along with $100 aspirins and 1,000 mattresses for an overnight stay (and people don’t have doctors?). Info Services: Gotta have that $1,000 phone to play angry birds and text the bros. Lawyering: The service poor people always wonder about and the rest are afraid to do without. Engineering: Well, manufacturing is in decline and there are no replacement bridges being built, so…..hmmm must be about avoiding lawyers…Boeing Max? Housing: day workers for framing crews and the inevitable bling fest of unaffordable happiness (note to house buyer: see the lawyer after the lender to sue the builder and maybe the engineer for the leaky foundation growing the mold that made me go to the doctor and I had that damn $1,000 co-pay to cough up. Well, I could just put it on Visa).

I apologize for my flippancy, but the point I am trying to make is that, imho, we are in a World of Hurt as regards to the economy. I was brought up with the idea of ‘build the better mousetrap’ (whatever). But a mental wander through ‘the above list’ reinforces for me that most of the ‘Economy’ isn’t really needed. But, we need affordable housing, affordable health care (in some countries), and some new bridges. etc etc. Seems to me the Economy would work much better if that pesky income distribution problem was addressed first. Then, there might even be some necessary manufacturing going on, even if it is just pre-fab housing and affordable transportation.

There is a two-tier economy …

either you have a solid career-track job or you’re in the newfangled gig economy, and either you benefit from high asset prices or you’re hurt by them.

Politics are reflecting this struggle throughout the world. There will be plenty of change this next decade as increasing numbers of people don’t see the system working for them.

As for economic numbers, everyone’s after different things. You can find data to back up any view you’d like, as conflicting signals are common when you have massive central bank intervention. They are what they are, and it’s anyone’s guess when the next political cycle or stock market correction will hit.

So if we hand more of our wealth to those who don’t build bridges, play pesky birds, allocate an a large portion of their income to alcohol, drugs, cigarettes, gambling, fast food, etc. then we are going to force the economy into a better place where it focuses on things that matter to you? Stick with your hammer.

Isn’t that Consumer spending dominantly DEBT based?

I’ll give your question a shot.

Consumers spent about $15 trillion over the past year. Total consumer credit (credit cards, auto loans, student loans) increased by $200 billion over the same period. That is 1.3% of $15 trillion. So 1.3% of total consumer spending during those 12 months was funded by new debt. The rest was funded by income.

And consumers managed to save about 6% of their disposable income.

But there is a divergence.

There are a lot of consumers in the US that have no debt. About 1/3 of homeowners own their homes free and clear. A large portion of consumers carry zero credit card debt, have no auto loans, and no student loans.

And there is another portion of consumers that are drowning in debt.

“Just look at todays GDP report”.

It has been conclusively shown that the GDP numbers are massaged, birth/death modeled, revised, adjusted, right out of reality.

“So you will be disappointed again”.

Could not have said it better Wolf!

“Surely when looking at such grotesque data manipulation, China can only stand in silent awe and watch as the US shows the world how data fudging is truly done”,

http://www.zerohedge.com/news/2019-07-26/what-americans-spent-most-money-second-quarter

The bare numbers in the ZH article are correct, but just about everything else in the article is BS, including this line above the chart, “Here is the breakdown of all the categories that constituted Personal Consumption in the second quarter:” This is just plain wrong and clueless. Here is why:

Personal Consumption in the quarter was $14.5 trillion annual rate, Trillion with a T. The numbers cited in the ZH article refer to contributions to consumption growth, meaning contributions to the increase from prior quarter, not total consumer spending.

For example, the biggest fattest item on that list was RV sales, $22 billion annual rate. That was the biggest item, out of $14.5 trillion in total consumer spending, trillion with a T. Where is healthcare? Rents? Cars, food…. that consumers spend trillion on every quarter?

This article totally misrepresented the numbers in the GDP report. Whoever wrote this was clueless – and also had an agenda.

The article is actually so stupid and obviously wrong that I suspect that you didn’t read it attentively, because if you had read it attentively, you would have seen how wrong it is.

ZH publishes a lot of excellent pieces, articles that you cannot get anywhere else. But these articles get clicked on the least. ZH publishes everything, from the best to the worst. Unfortunately, it’s the worst that often gets the most clicks and that gets shared the most, including by dumping the links into the comments on other websites.

Saying that some of your readers “want to the US economy to collapse, and they’re disappointed that it doesn’t” might be a little strident Wolf. After all we all live in, and thus depend on, our local economy. Everyone of us wants it to be as strong and healthy as possibly. So I think you’re unfairly misrepresenting angry people who think their leadership is deliberately trying to deceive them with blatant lies that they can see are false each and every day from their own experiences. Never forget that this is a long standing oligarchy which has actually struck down a long standing US law that forbade propagandizing its own American citizenry.

P.S. Before you write that piece you might want to read today’s Zero Hedge’s article titled “This is What Americans Spent the Most Money On In the Second Quarter”. A good example of why we shouldn’t take government statistics at face value.

Scott Busfield,

My response to that ZH article you cite is in my reply to OutLookingIn above.

I wonder about the details here, and the background. As you’ll no doubt point out (haven’t read your article yet) this red hot consumer spending is likely built on the back of debt slaves who will at some point uniformly declare bankruptcy and crush our system.

But having said that, I am also curious about the details behind the optimism. Can’t wait to read this particular article and have a good chuckle.

No rate cut coming. Only wall street has predicted a cut, they are overly biased since they rely on negative rates to keep the scam alive. When the Fed says I will believe it, but it has to come from the horse’s mouth before I take it serious.

But the Fed has openly admitted that a healthy market is one of its highest priorities (a market crash would almost certainly undercut the incredibly unstable mountain of debt our economies are built upon and bring about a deflationary collapse). Consequently expect a cut of 25 basis points next week rather than the hoped for 50.

I think what you are seeing is the cost of us getting here. Even in very poor countries, despite all the problems, life goes on. Ask anyone (civilians) who’s been through WW2.

LIFE goes on!

true.

But what kind of standard of living one is having, now compared to before and how many people aspire for better life but cannot get it!

Minimalists will complains the least!

“the cleanest dirty shirt in the laundry” Yep same as:

The best horse in the glue factory

The leper with the most fingers

The least ugly girl at closing time

Interesting blurb from the Markit US flash PMI, being from Markit take it for what it is worth.

“Business expectations for the next 12 months dropped sharply across the service sector in July. Moreover, the latest reading was the lowest since this index began in October 2009.”

When any economy slows (as is currently the case around the world and for various and sundry reasons), more money is “pumped” into the economies (again, in various amounts and locations). This leads back to more economy (building things no one needs) and of course inflated asset prices. Eventually it leads to inflated general prices.

This is the new “growth” normal. It’s all a mirage of inflation that is masked to look like “growth”. Productivity increases are largely dead taken as a total across all industries, services, etc. Sure there are pockets of productivity increases, but by and large the world’s great productivity gains are over with. Other than productivity gains, only population increases can drive true economic growth. That isn’t happening either.

Q2 GDP number came in at 2.1%. Wasn’t everyone here predicting low 1s or even sub 1? Looks like the death of the booming economy has been greatly exaggerated…….again.

The GDP was 2018 has been revised down to 2.5% not the 3% claimed, before!

Just wait for the revision down the road!

And the PCE deflator came in at 2.3%. Mission accomplished Fed?

ZH

Not wanting to entirely rain on America’s parade, after a stronger than expected set of data on growth this morning, President Trump’s much-heralded 3.0% GDP growth in 2018 – “greatest economy ever” – has been slashed by annual revisions

As Bloomberg reports, updated government figures show that gross domestic product expanded 2.5% on a fourth-quarter-over-fourth-quarter basis last year.

Finally, WSJ notes that the 2.3% average annual economic growth of the current decade-long expansion compares with 2.9% during the previous expansion from late 2001 to 2007, and 3.6% in the 10-year expansion that ended in early 2001.

Rv sales?

– I had a dream : the DOW will land on the moon, anytime soon, on a weekly log chart, because the moon isn’t too far.

– SPX, daily, line chart, indicate a bearish divergence.

– AMZN on LPSY.

– Starbucks on strong coffee, this morning, went vertical. If today close slightly lower, SBUX might signal a bearish divergence.

– In 1929 strong momentum carried the leaders of the pack higher,

up in the air, while the rest lost ground, until the winners fell from the cliff and crashed.

– Shanghai stock market in a bear market, since Oct last year,

when SSEC breached 2016(L). 2019(H) is a rally in a bear market.

– The DOW of the 1980’s & 90’s was tilting up, aiming higher at 2008/09 lows, giving the DOW support. Since 1995 the DOW went vertical.

– The 2000 to 2007 highs and 2002(L) in between was a trading

range tilting up. It became a booster, giving the DOW an enormous propulsion for a liftoff.

– The 2014/16 period are backup, waiting for the NASDAQ

to pump muscles, in order to breach NASDAQ 2000 peak..

– From 2016(L) the DOW went vertical.

– But Congress will salivate if the DOW will correct. Despite good

economical news, a 38% to 62% normal correction, will give them a chance.

– The little people will pay the price..

Iamafan,

For doctors u are an app. The need u in repetitions.

Buildup your defense system, because u are the only one

who can help yourself.

The x2 books I mentioned yesterday contradict each other.

Both autodidact. Alfred Noble blew himself up.

Filter them out, avoid their extremes, move in one step at a time.

Look for the cause, not the symptoms.

In the aggregate are consumers TBTF? You wonder how much of consumer confidence is politically inspired? Americans love the guy in the executive office but they really look forward to the guys and gals in charge (Democrats). The GOP might counter with direct rebates, once the economy slows, it is the silly season, and consumers are also voters.

Consumer confidence is very bifurcated. Some consumers just have a lot of spending power combined with the cash. Others spend because they have no hope of doing any better by waiting or saving, they know they are never catching up.

“Shop till you drop” has different meanings for different people

When people talk about trade, they usually assume B2B, but shopping has now become international as well. Americans are shopping via the internet in Asia and Europe regularly. All the well known brands, regardless of country of origin, are available for sale on the internet.

I live in flyover country and can get a package from Europe faster than from California.

Excellent work Wolf:

Thanks.

K.

p.s. I had to jump to my handy Merriam-Webster, and yes, there it was, “oomph”.

A plethora of oomph.

Glad I didn’t have to dust off my Oxford.

There are too many economic blogs out there today peddling doom. I understand there is a vibrant market for it, but nonetheless, I do not see the appeal. There seems to be an entire cottage industry of gloomy blogs catering the over 60 white guy.

Google is up today. Great stock great Company. Starbucks continues firing on all cylinders year in year out. Twitter is on a tear as well.

I just wish we had a market sell off so i could add to my positions in these names.. But this market is even a bit too giddy for me lately.

On a different note. Fred Hickey deleted the bejesus out of my posts about 5 years ago because i called BS on his approach of going long second tier gold miners and shorting tech names like Salesforce.com.

Likewise, Mish sent me packing a a long time ago (around 2013) because i was questioning him on why Bill McBride was giving the thumbs up to the incoming housing reports while Mish was more or less saying that the reports stink.

All in all, other things being equal, i would rather be in the company of wrong eternal optimists than wrong eternal pessimists.

I’m going to start a new trend by pointing out that for a sustainable economy, there’s no such thing as “production” or “consumption”. There are only transformations and uses. The “produce and consume” vocabulary needs to be replaced with a “use and recycle” vocabulary.

The business and Econ vocabulary derives from an outdated single-use, source-to-sink mindset. In that mindset, iron is mined, made into steel, “consumed”, and then dumped in a landfill. Food is grown, harvested, “consumed” and then mostly goes down a sewer. And so on. Wastes are thereby forgotten, as though Earth were infinite and could absorb anything. We now know that’s not true.

So that old mindset doesn’t work, especially for non-sustainable resources. Iron and other mined materials need to be recycled, not consumed and dumped. And the flow-through mindset only kinda works for food, which is sustainably grown – since sunshine and rain are renewable, just take good care of the land. But even in agriculture there are many byproducts, and the process of dealing with them (even if it’s simply composting) should be accounted for in the vocabulary.

So instead of “producers” and “consumers”, “products” and “wastes”, we need to start talking, and thinking, in terms of “processors”, “resources”, “inputs” and “outputs”.

Processors transform input resources into output resources, generally rapidly: sunshine, water, land, fertilizer, energy and seeds are transformed into crops. Crops are harvested using fuel and machinery into food and compost materials. Food is then delivered to packagers using fuel and vehicles. The packagers use as inputs cardboard, glue and ink (for instance) as well as food, and deliver retail packages. The retail process doesn’t change the packages but it has land and energy inputs. The food is then sold to individuals, stored, eventually eaten and then processed into compostable wastes which can be processed into more fertilizer. But there is no “final step”, the material which was eaten goes back to the land and helps to grow more food, so the cycle renews.

Looked at this way, there are very few actual “producers” or “consumers”. The physical laws of conservation of mass and energy preclude the actual production or destruction of anything, they only allow processing and transformations. One has to think ecologically, in terms of systems and resource flow cycles. Like the water cycle or the carbon cycle. The Earth is not a source-to-sink world.

For instance, in the natural food cycle, photosynthesis, metabolism and respiration ideally result in a zero net balance: sunshine, CO2 and H2O produce sugar in plants. Plants are eaten (or decompose) releasing the same CO2 and H2O. Even the sunshine is re-radiated into space as infrared (heat) radiation.

So instead of “producers”, then, one might think in terms of “mass-processors”. And “consumers” would perhaps become “individual processors” – and this might include small businesses too.

This is only a small beginning. Large swathes of economics will need to be rethought if we are to live in a sustainable world.

the reason wolf street is so popular is because Wolf tells it as it is and has no agenda other than the truth! Very much appreciated. The fed will cut 1/4 and then try and walk it back. Will be interesting to see if “patient” increases in the minutes. The fed has become the worlds central bank and Europe is slowing.

the service economy will bring the mfg economy to its knees in this trade war by way of the latter being crushed under the shear weight of having to bus their own tables, thus restoring truth, justice and the ..

lies, all lies.

Unfortunately, the consumers in America will face credit limits soon due to their enormous debts and limited incomes. As an attorney that formerly handled bankruptcy cases, i am amazed that much of the bottom 50% of the American population does not declare bankruptcy ASAP and get rid of their debts.

Huge parts can never repay their debts. Rational evaluation of their prospects should make them go into bankruptcy. Irrationality prevails so far.