I’m shedding a different light on consumer debt.

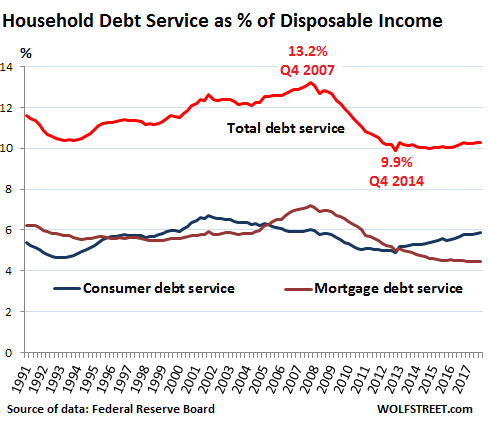

This type of chart is trotted out constantly these days to show that American households are in fabulous shape when it comes to their ability to service their blistering record debts. The red line in the chart shows household debt-service payments (combined monthly payments on mortgages, credit cards, auto loans, and student loans) as a percent of disposable (after-tax) income. Since 1980, the ratio has ranged from 9.9% to 13.2%. It hit that top in Q4 2007 just before it all came apart. Ten years later, it was at 10.3%. Hence the conclusion that households won’t have any trouble servicing their record debts. In a moment, we’ll get to the trap in this conclusion.

The chart above also shows separately the ratios of mortgage-debt-service to disposable-income (brown line) and of non-housing consumer-debt-service to disposable-income (blue line). Both combined make up the red line.

These debt-service ratios are a function mostly of three factors: The dollar amount of the debt; the interest rate on that debt; and the amount of disposable income. The logic is that rising disposable income supports rising indebtedness.

The large decline of the debt-service ratio from the peak of 13.2% in Q4 2007 to the all-time low in the data of 9.9% in Q4 2012 was caused by several factors:

- Consumers “deleveraged” mostly by shedding their debts via defaults and bankruptcies.

- Homeownership dropped to lows not seen since the 1960s. As households became renters, their mortgage debts were eliminated.

- Mortgage debt plunged by $1.2 trillion, or by 11.3%, from $10.6 trillion in 2007 to $9.4 trillion at the end of 2014. It has since risen to $10.1 trillion.

- Non-mortgage consumer debt dropped by $150 billion or 5% by late 2010, as student loans continued to surge while auto loans and credit card debt experienced sharper declines. It has since surged 47% past the prior peak.

- Interest rates also plunged. This allowed the remaining homeowners to refinance at a lower interest rate, and it allowed homebuyers to get lower-interest-rate mortgages. Interest rates on many consumer loans also dropped.

- Disposable income rose from $10.7 trillion at the end of 2007 to $14.6 trillion at the end of 2017 (not adjusted for inflation), largely due to an additional 9.2 million jobs and nominal wage gains.

It all looks good, in terms of the debt burden. And so the red line in the chart above is trotted out to show that the American consumer – this unified, amorphous, monolithic structure whose job it is to hold up the entire global economy – is strong and won’t buckle.

But there’s another way to look at this — and not as a monolithic structure. Many consumers are debt free and have lots of money and good jobs, and they check their 3 credit scores regularly. Other consumers have large amounts of debt, lousy jobs or no jobs, and are paying for groceries by charging them on their credit cards. Credit problems always involve the most vulnerable consumers. During the mortgage crisis, the delinquency rate peaked at 11.5% in 2010. It wasn’t the 60% of homeowners that had significantly payed down their mortgages or owed no money on their homes who triggered that event. It was the financial mayhem among the smaller portion of the most exposed and most vulnerable.

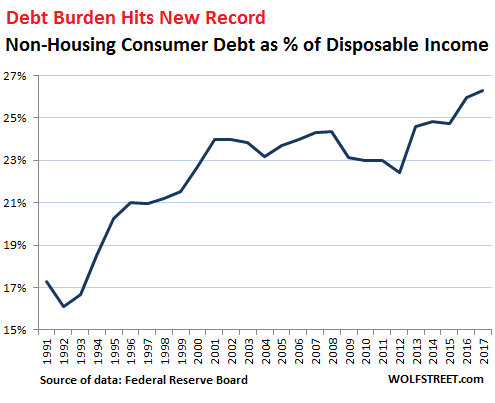

For a different view of the burden of debt, let’s look at non-housing consumer debt, because this is where the music is playing right now. To eliminate for a moment the impact of interest rates, let’s look at the amount of debt – not the monthly payments – as percent of disposable income.

And suddenly, the risks emerge a little more clearly. At year-end 2017, the ratio of non-housing debt – revolving credit such as credit card balances, plus auto loans and student loans – to disposable income reached a new record of 26.3%, up from 23% at the end of 2010, and up from 24% in 2007, the peak before it all came apart during the Great Recession:

So the ratio of non-housing consumer debt to disposable income – the burden these consumers carry on the backs in relationship to their incomes – is higher than ever, and only historically low interest rates have kept it manageable.

But interest rates are now rising, and many of these consumer debts have variable rates.

This explains a phenomenon that is already appearing: How this toxic mix – rising interest rates and record high consumer debt in relationship to disposable income – has now started to bite the most vulnerable consumers once again. And for them, debt service is getting very difficult.

In Q1, the delinquency rate on credit card debt at banks other than the largest 100 – so at the 4,788 smaller banks – spiked to 5.9%, higher than at the peak during the Financial Crisis, and the credit-card charge-off rate spiked to 8%. These smaller banks marketed to the most vulnerable consumers that had been rejected by the biggest banks. And now, once again, subprime is calling. Read… Credit Card Delinquencies Spike Past Financial-Crisis Peak at the 4,788 Smaller US Banks

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I have been wondering about these stats for some time? It is my opinion that ‘lumping in’ all groups and coming up with a lower debt number overall makes little sense. I just remember when I was starting out with a young family and spotty work during the ’81 Canadian recession. Our mortgage was affordable and we did not miss a payment, but…… it was freaking tight for us and we spent absolutely nothing on any discretionary purchases; no car loan, no meals out, etc. There were no credit cards in those days beyond gas cards, therefore we had no other debts. (Remember the good old days of balancing a cheque book and the walls of shame behind cash registers for those who used an nsf cheque?)

From the outside looking in (as we now have no debt), it appears that the same type of young consumer that we once were is in a much more precarious state than we ever were. It looks like people have more ‘stuff’ these days, but in actual fact they do not.

Plus, you have to live somewhere and if that requires a rent payment it is still implied debt. No cash = homelessness, or couch surfing. No cash means a food bank visit.

regards

Also you where amortizing through the high inflation, which is not separated out of the debt service costs.

An inflation rate of 8% and an interest rate of 10%, means 8% of yearly indirect amortization. Calculated as a cost but is in practice equal to an amortization of approx. 8%. Compare that to the same debt service level (as today) but at 2% inflation and 4% interest rate -> big difference… in the first case you get almost debt free within some years and in the other you need decades …

No, debt-service ratios eliminate the impact of inflation. That’s why they’re used.

How? Both data (income and debt) are subject to inflation over the same period, and the inflation cancels out. Mathematically, the inflation factor is both in the numerator (debt) and the denominator (income) and thus cancels out.

However, you’re correct about absolute debt numbers, which run into the problem of being distorted by inflation. So total consumer debt jumped 47% from the prior peak in 2007, which includes the impact of inflation (ca. 17% CPI).

Wolf,

What would be even MORE interesting is a chart showing the absolute consumer debt levels after adjusting for both CPI and the changes in interest rates (i.e. showing how much debt a particular interest rate payment could support actually over time). This could lead to a model to predict how badly asset values (those supported by debt that is…like mortgages or autos) might fall as interest rates normalize….which is the environment we are transitioning to (slowly in the U.S….but probably very rapidly in EMs and certain EU countries)

This is a difficult problems since the interest rate curve isn’t constant and shifts over time….while each individual debt itself is constantly moving along the maturity curve as well. You would probably need to make general statements about various time buckets…sacrificing precision that many look for. (i.e. look at consumer debt with maturities in 9-11 years vs. gov’t 10-year benchmark over time).

One other distortion: rent doesn’t show as a debt, even though it must be paid each month to keep a roof over one’s head. Swapping a home mortgage for a rented home only helps to the extent that the rent is lower than the mortgage (plus maintenance)

Wolf, I am feeling a bit stupid, but I do not see how debt service ratios (measured as interest payments / income) adjust for debt re-valuation in real terms and make a high inflation period comparable to a low inflation period. Assuming the nominal amount of debt stays the same during a high inflation period you will inflate away a large part of the real value of your debt in a few years. It is not a free lunch of course so you pay a higher interest rate (measured as debt service costs)… and hence you carry less debt due to higher “costs” but the large (inflation) part of the interest payments is indirect a re-paying of the debt measured n real terms.

The debt service ratio does not adjust for the loss of real value in the debt you carry over this period, or? … Or maybe we calculate debt service costs differently in Europe, but of what I can see on the Internet the methods look pretty much the same all over

I would like to see a graph that measures total household debt/ real interest paid. To me that would roughly do the trick. I would eat my hat if debt service ratio measured this way is as flat as your first graph :-)

where is inflation 8%

It’s like the old joke in which Bill Gates walks into a working-class bar, whereupon everyone in the bar instantly becomes a billionaire – on average.

“Plus, you have to live somewhere and if that requires a rent payment it is still implied debt.”

This is an excellent point that I have wondered about for years (I’m not an economist). To me, the debt isn’t implied it’s real. It’s a contractual financial obligation as is a mortgage. Is it calculated in somehow?

Rent is like utilities. It is payment for a service. Its not debt.

Great work Watson, you can see the forest for the trees! thanks!

great work Watson! You can see the forest for the trees!

Wut?

The chart indicates that debt load was 24% at the height of the craziness of pre-crash 2008, and is 26% now–an 8% increase, over 10 years (yawn)

Consumer debt increased by 47% in 10 years. What you mentioned is an increase in a ratio — that’s very different. The debt to disposable income ratio was 24% last time it blew up. Now the ratio is 26%.

Right. The bubble is about to pop – certainly with rising interest rates, rising fuel cost, rising inflation, rising “anything” except your income.

Yes, Wolf, but you see, it’s different now. That chipper young perma-bull “analyst” on CNBC said so, with great conviction. And the inestimable Janet Yellen assured us there would be no new financial crisis in our time. So rest assured, this debt thingy is nothing to worry about.

If there was a problem, our financial regulators, enforcers, and elected officials, ever vigilant to safeguard the public interest, would’ve stepped in with their usual alacrity. And the Fed’s models, which have unerringly predicted every financial crash to date, would’ve sounded the alarm by now.

Oh, wait….

True. But the last time it was highlyleveraged defaults in housing debt, and the homes could be taken back. This time it will be defaults on credit cards, autos and student loans-a less disruptive process, and the banks are supposedly smarter and better stress tested this time around. Supposedly you can’t default on a student loan, but many will, and the taxpayers will ultimately be on the hook for this. At least the auto lenders can track down their cars with GPS and retrieve some of their money. I feel for these folks at the bottom, but I doubt their defaults will bring down the entire economy, unlike 2009 where the tail was fat enough to wag the dog.

Subprime home loans were supposed to an only incidental part of the housing market but when they popped the whole market crashed along with everything that had been tied to the housing bubble. Supposedly, the world is now a tottering bubble everything all propped up on a huge pile of private debt. If credit dries up or becomes much more expensive then we will all look back and realize the cracks seen coming from the bottom were really cracks in the whole foundation.

Not sure if debt and leverage are the same thing. Doug Noland thinks the consumer is not over leveraged, and I would say because housing values have gone up, when housing drops it deleverages the consumer, and wages at the margin are improving. The stock market is also deleveraging consumers by putting a floor under the private investors nestegg. It may all be an illusion but it will take a deep bear market before mortgage companies start asking their clients to make up the difference. In stocks the top of the 2007 market is a watershed for a lot of investors before they deleverage.

I was walking around our neighborhood and it dawned on me how nearly all my neighbors have so much stuff in their garages (some have 3 car garages too) few can park even one car inside. Now I’ve got a two car garage but I can put both our cars inside and other than the mortgage we have no debt. I’ve wondered how much debt some of those households with garages full of stuff collecting dust have.

Of course my neighbors have much better garage sales than I……………..

Storage units are a booming business and they’re all over in my area.

You should feel smug and so do I for the same reason, although my house is paid off.

To add, one of my hobbies is finding Hawaiian shirts and sweaters from eBay, used but in excellent condition, for sometimes up to 90% off of what they cost new. It’s basically thrift store shopping but I look good and my shirts cost less than new paint rags from a big box store. I wear Tommy Bahama and Nat Nast for cents on the dollar and I look great.

I’m also a believer in used off lease laptops. Once you learn to read specs you can find 3rd, 4th, and 5th generation intel laptops for under $400, sometimes much much less. My home media center is being run on a HP 2170P laptop (i5 gen 3, 17 watt TDW, 180GB ssd, 8GB ram, gigabit network port) I bought on eBay for $150 early last year. Passmark score of about 3400. I added a wireless AC card for $30 and attached an old USB drive for media files. By next year, 6th gen intel processor based laptops will be in this price range. My other laptops are similarly equipped and priced.

Sorry to break it ya buddy, but no one looks good in a Hawaiian shirt, unless inebriated with a combination of juice and Rum.

Good advice on the laptops though. ;)

THAT’S HILARIOUS! i was so NOT gonna say anything because it’s the same guys thinking cargo shorts are stylin’ or how we women think house muumuus are flattering on ANYONE.

What’s your point?

You lost me at ‘looks good in a Hawaiian shirt.’ Not possible.

Jon,

That’s the point. I don’t care. I’m old and I look good. Plus, in my cargo shorts my only concern is I don’t wear my cammy cargo shorts with the flowered shirts. Must wear solid color cargo shorts that more or less color match with fronds or pineapples. I’m not a heathen .. no socks and sandals with my cargo shorts until I reach age 80 or more. The rum and fruit juice sounds perfectly natural and as American as Oreos or outdoor barbecues.

This dude has style!!

okay, CDR, you won me over because you proudly swagger and OWN it. i am now thoroughly convinced that you ARE sexy and mad STYLIN’ in your cargo shorts and crazy colorful hawaiian shirts! no sarc tag needed. i’m for hella REAL!

x

Compared to many other first world countries this article shows the US is an underachiever debt wise.

Canada is now at over 165% debt to disposable income, and the place is quite nice, the trains run on time and people and have health care.

https://www.thestar.com/business/2017/03/15/canadian-household-debt-hits-another-record-in-fourth-quarter.html

Canada is heading into a financial crisis. Australia is too. Everyone sees it coming. But it’s moving in slo-mo. So it’s easy to just avert your eyes for a while longer and ridicule those that warn about it.

The US is not. Been there, done that. But a portion of consumers in the US are buckling under their debts. This isn’t about big banks collapsing — they won’t — but about the most vulnerable consumers running into trouble.

And the UK.

April retail sales was the worst month in 22 years.

Home prices (nationally) are up 2.2% Y/Y, and down the last 4 months.

Also, luxury Manhattan Condos ($3 million and up) are priced all the way back to where they were in 2013.

Donald and Jared are beginning to look nervous. Kings of debt, don’t ya know.

What is it with the Anglosaxon world and consumer debt? I don’t have any numbers at hand to back me up, but here in Western Europe the debt dynamic seems to evolve differently: high to very high debt levels due to state expenditures (guaranteeing comfortable social protection but in many countries unsustainable nonetheless in the long run), yet on a personal level most people here think twice before they buy stuff they can hardly afford or commit to long term financial obligations. In my own environment people clearly do not buy more than they can digest financially.

“Anglosaxon world”

Its not the “Anglosaxon world”.

It’s the unsustainable American credit based consumerism world model.

That American Corporates have successfully exported to much of the English speaking world and beyond.

America exported it, as it is unsustainable, but only, when it finally stops growing.

Look at the deliberate declining life cycles of most mobile electronic devices.

china is still trying to move to a consumption and credit based economy. As are others.

The model works, Untill it falls over.

These days I make an effort to only consume food, and I prefer to catch/hunt or grow most of that.

Wolf – You are correct about Canada.

From the Office of the Superintendant of Financial Institutions.

Re:

Loans secured against residential real estate.

Outstanding balance $284.64 billion

That’s up $994 billion from the month before

A total increase of 7.73% from the same month last year

The loan growth rate now outpaces that of national home price growth.

How nice will Canada be after our debt crisis? That’s the key question. The US had its debt crisis in 2008. We skated on it. And then spent another ten years gorging on debt and real estate. There is a price to be paid for that, unless we Canadians have invented the free lunch.

Interesting factoid: Those countries that fared relatively well in 2008-09 (Canada, Australia, Netherlands, Switzerland, South Korea, Scandinavian countries) are the same ones now carrying the largest private sector debt levels. By far. What are their odds of skating on the next financial crisis?

Alistair and Out,

Stats again. Don’t you think the numbers cited are skewed by Vancouver and TO mortgage, LOC, reno financing, dining-out CC charges, etc?

I know of no one who carries much, if any, debt. Furthermore, would the rest of Canada realy care if TO and YVR ran into difficulties? I don’t think so. I think the national sentiment would be, ‘it’s about time.’ My Credit Union is in good shape so I could give a rats a.. about RBC, Commerce Bank, etc.

But I don’t know, that is why I am asking your opinion.

I’ll take stats over someone’s anecdotes…

Paulo, how can you look at a Canadian economy supported by just over 35 million people and say that 6.5 million people in the GTA and 2.3 million in the GVA don’t count because you are fine.

I live in Saskatchewan, I won’t collapse the economy with my 5 figures of debt. But I won’t look at the stats of nearly 1/3 of the population and say they don’t count.

So in a nut shell, Canada cares if they collapse in Toronto or Vancouver.

Paulo –

Numbers are what they are. Statistics from StatsCan stem from bona fide sources on the whole and are relied upon by nearly everyone.

You state, “I know of no one who carries much, if any, debt”.

All I can say is… WOW! You swim in rarefied air! May I suggest you get out into the general public more and mingle with the paroles.

You will be surprised what you find. When the majority of Canada’s citizens live within a short drive of the Can/USA border and reside in large urban centers, what happens there effects everyone else. Don’t fall into the trap of sticking your head in the sand. Someone may creep up behind you and kick you where it hurts! lol

“Consumer” …

I’m sorry to rant, Wolf, but I really hate how that word has supplanted what used to be referred to as a “Citizen” !

From a person with rights and responsibilities … to an inhuman cog, with nothing favored but a devouring intent ! This whole way of being as the modern Homo economicus needs to change, and fast, or we’ll go the way of the Neanderthals !

My apologies if this seems over the top … delete if you must !

Get over it, polecat, nobody remembers psychoanalyst Erich Fromm or his book “The Sane Society” anymore. Criticism of society is a thing of the past, unless there is no real intent to change it. Today, we are born for one reason only, and that is to consume.

How many people do you actually know who think change is necessary? There are supposedly over 7 billion people in this world and most have access to the internet. So how hard can it be to find enough others like you to create an anti-consumer society? After all, if you’re gonna rant, might as well take action and do something, right? Show us how it can be done better in an actual anti-consumer society.

Does such a thing exist? Has it ever been done before? Of course, not. We’ve all been sold.

It looks like your post isn’t getting deleted, so maybe you should retract what you said. A simple “just kidding” or “I’m okay with consumerism” would suffice.

“How many people do you actually know who think change is necessary? There are supposedly over 7 billion people in this world and most have access to the internet. So how hard can it be to find enough others like you to create an anti-consumer society? After all, if you’re gonna rant, might as well take action and do something, right? Show us how it can be done better in an actual anti-consumer society.”

To create an anti consumerism society you need an anti consumerism government.

This in itself is a problem as most existing states have debts and are locked into the ever expanding population consumerism model.

Never to mind the planet is going to bite the consumerism model quiet hard in the next 150 years.

By then central india will be a desert and much of coastal and lowland china and india today will be 50 + feet under water.

The chances of countries like india and china changing their ways are so minuscule, they are nonexistent.

So even a return to sustainable capitalism although possible in the next 150 years is strewn with huge obstacles. The EU is making a start with some laws regarding service and repairability of some items.

The crunch will come when they finally move on the Auto manufacturers, for using pricing of sealed electronic components (many of which have a cycle number, failure points in them, which the manufacturers claim is safety related) to make it uneconomic to repair older vehicles.

“we really need to discover another planet to live on, as we a swiftly destroying this one” Unknown Arms Dealer/Researcher.

“….Criticism of society is a thing of the past, unless there is no real intent to change it. Today, we are born for one reason only, and that is to consume….”

i type this with every ounce of HUMAN brotherhood and respect….but please do speak very much for YOURSELF, Future Historian.

(smile)

as i wrote to Alex… punk was only really three people. the rest were visitors and tourists… and as Vonnegut said and so it goes…

(and i remember Erich Fromme)

signed,

a sometimes impatient woman very much jumping on the fault lines of an injust/cruel society and SYSTEM, and will pass the skills of fighting this “ish” on…

I have some Neanderthal in me. They lived on :-]

More seriously, this society has monetized everything, even the people, who are now “consumers.”

Me too, 4%. That works out to it being mathematically possible for me to have a Neanderthal ancestor 5 generations back, but of course it doesn’t work like that.

Slave. Freeman. Noble/Priest.

The three main categories of civilized life.

‘Citizen’ and ‘Consumer’ are just used to make the slaves feel better about themselves: the former in Communism, the latter in Capitalism. :)

When writing about consumer debt, then referring to them as consumers only makes sense.

nah, i agree, polecat. thanks for saying that. i ALWAYS chafe when i see that anywhere because Wolf is right: “More seriously, this society has monetized everything, even the people, who are now ‘consumers.'”

To understand the economy, you have to understand the dynamics of debt. Mainstream economics relies on static equilibrium models and ignores banks, debt and money. The Australian economist Steve Keen has developed mathematical models of the economy that include these things that show that the total level of debt is not the only important factor, but also the dynamics of the rate of change of debt. That provides an explanation for why in the GFC of 2008-9 with a small amount of deleveraging, it almost seemed like the world was going to end. Steve Keen, Michael Hudson and Hyman Minsky are among the few contemporary economists worth reading. Mainstream neoliberal economics is better off ignored completely.

Anyway, when the tide goes out we will find out who was swimming nude. You are better off staying out of personal debt or paying it off regardless of your income or life circumstances.

There are many times debt has worked out very well for me. The most striking example is borrowing $1200 to buy a hoard of electronics surplus…. I got about $20k for it when I sold it, and a lot of that was at swap meet prices.

Since it was a face-to-face debt with nothing written, I considered it much, much more important to pay back than some thing a bank sends through the mail.

A great example of what credit can accomplish when utilized appropriately. Sounds like a great experience.

In contrast, I refinanced a mortgage a few years ago @3%/15 yr. ….it took over an hour just to sign the papers. One of the forms provided me with a toll free number to call to seek mortgage education and counseling. Just for kicks, I called …and called…and finally got through to someone who had no idea what I was calling about until I explained what the form said. Then it sounded like she was reading something idiotic from a script …thanks Chris Dodd and Barney Frank.

Add Dr Tim Morgan to that list: a very fine, Cambridge-trained mind with extensive experience in the City of London.

Well worth reading, IMHO.

Would be good to see how much impact student loan debt has on these stat’s.

“This explains a phenomenon that is already appearing: How this toxic mix – rising interest rates and record high consumer debt in relationship to disposable income – has now started to bite the most vulnerable consumers once again. And for them, debt service is getting very difficult.”

I distinctly remember writing to that effect the other day here and am happy to see it expressed with charts in an article.

This is a huge red flashing light for those who are willing to see it.

The same Socioeconomic group that triggered 08 are in trouble, AGAIN.

If you ignore this, you are a Fum Duck, that deserves everything bad that happens to you.

My crystal ball however, is not giving me a when, to go with this relevant information.

As a (very) wealthy person said after GFCI:

‘This shows what happens when you let poor people think they can own things!’

Quite right.

Poor people need better wages enabling them to actually buy goods and services, and regular work, not access to debt.

In other words, they need to stop being poor.

However, at this stage of our civilizational collapse, I doubt this can be done.

“Poor people need better wages enabling them to actually buy goods and services, and regular work, not access to debt.”

VERY true

“In other words, they need to stop being poor.”

should read

In other words, they need to stop being KEPT poor.

“However, at this stage of our civilizational collapse, I doubt this can be done.”

If you wish to arrest the collapse enabling the prro to improve their lot by other than handouts is one of the first things you do along with limiting population growth and replacing consumerism with sustainable capitalism.

However as you note the cronys in charge in both Beijing and Washington have no interest in doing that.

150 years from now thing are going to be very different. I also fear they will not be very nice at all.

It especially can’t be done when the wealth of the Overclass increasingly depends on extracting it from the poor and working class…

That is very true: the wealthy are in fact destroying the foundation of their own lives.

But as we collapse, increasingly those outside the magic circle of wealth and privilege will prey on one another.

As one can see when dealing with salespersons of all kinds. They will screw you because otherwise they themselves are on the street or living in a van.

It can only get nastier, dirtier and more hopeless going forward.

Just as in the last decades of every civilization.

As a local “bigwig” once remarked; “You make friends with the rich people, but you make your money on the poor people”. So, same as it ever was.

“In a market like today where rates are increasing and home prices are increasing fairly rapidly, using an ARM really extends purchasing power for particularly that first-time buyer,” Mike Fratantoni, chief economist at the Mortgage Bankers Association in Washington, told WTOP.

Were they saying that back in 2010-2012 at the housing bottom? (Rhetorical question)

It’s now time for the muppets to make good on the investors’ bets on housing. Rinse, repeat.

From Forbes (March 2018):

Joe Tyrrell, executive vice president of corporate strategy at Ellie Mae, said tight inventory has also been driving ARM demand upward for some time.

“We’ve seen a pretty slow, yet steady increase in ARMs since November of 2015, as there has been a lack of affordable housing inventory and a steady appreciation of home prices,” Tyrrell said.

ARM usage is likely to grow, too—especially with the Federal Reserve expected to raise rates two more times this year. According to Chris Lewis, manager of sales and operations at Angel Oak Home Loans, we can expect higher ARM usage for the foreseeable future—particularly from buyers with higher-priced home purchases.

I remember back in 2006, around 85% of all mortgages in San Diego county had become ARMs, because that was the only way most people could “afford” the rising prices of homes.

Not a bad a indicator of a topping in the market?

The use of averages for economic policy or insight is fraught with danger.

For example, if we raise the income of the top 4% of filers by 22% then we can zero the income of the bottom 54%, and *average* income will still go up. (Source: 2014 IRS income tax data.)

By the same arithmetical token, debt service as a % of disposable income could be quite low for richer households yet dangerously high for poorer households, without changing the average very much.

Nailed it.

RE is local. The ramifications of debt is also local. Stats are misleading and don’t always indicate the fundamental health of an economy or location.

Collapse, or the fundamentals leading into it, is often mentioned on this WS site by a few commentors. Assuming the slo-mo decline is currently unfolding, what location and situation would readers prefer to be in if it does play out as feared? That is what folks might think about and address, imho. :-) To me, stats play no part in my evaluation of events or our family situation. On one hand stats are used to wring hands and prod thought into how bad things are, and at the same time boosters look in their cupboard and say how wonderful the economy is unfolding. I am thinking of the Market boosters.

Wolf, thanks for taking the time and drilling down for us. I learn more every day reading your articles and reader comments. It provides direction and ideas to consider, even if only to confirm my biases. :-)

Students loans are the biggest scam ever in the US because it targets people too young and lacking experience to have any clue of what they are getting into.

“Students” are just the conduit used to feed easy money to the schools and associated businesses like textbooks, construction and Apple. And the government supports it! They are not your friend, average American citizen.

Well…follow the money trail all the way back to November 1999, when President Bill Clinton publicly declared “the Glass–Steagall law is no longer appropriate” and signed into law the Gramm–Leach–Bliley Act . Merry Christmas America, something that ensured balance was now ‘no longer appropriate’.

When the Gramm-Rudman-Hollings Act was destroyed, that was the beginning. When Glass–Steagall was destroyed, the doors to the future debt was opened as wide as the Pacific.

The day they made student debt exempt from bankruptcy, was the day the pigs came home to feast.

All the while everyone stood by knowing a match had been lit, and piled dry timber on the barn floor.

I’ve preached what you stated until I was/am hoarse…….But, who the HE$% really cares or listens? Their eyes glaze over. Maybe that’s best then they can’t see the tsunami coming!!

Most people don’t want to have to figure out what they can buy or not. They want it simple. Just a decent job, raise their kids decently, good schools, not much……but the financiers and the bought and paid for politicians want it all. I can hear the grinding wheels in the background sharpening the pitchforks. I’m ashamed at what our society is teaching our children who seek upper class education. May the souls of all the “I made a mistake handmaidens of capitalism” gag on their paper dollars!

This system of ours could not have gotten so rotten without the most deplorable propaganda system in history. People today who pay off their credit cards every 30 days are considered, “deadbeats”. I’m proud to be one.

Debt Free,

I grew up in the 50’s…To my then- young mind it appeared that the Government made decisions based on the common good, or at least the good of the country in general. Not so much today. Was I wrong in my youth, or am I just jaded and cynical in my old age?

The government was at least somewhat honest and accountable to the people, right up until November 22, 1963. There were still some shady elements of criminality in the government before then, no doubt. For example, Americans were overwhelmingly anti-war (isolationist) in the late 1930s having been badly burned in the unpopular involvement in WWI. FDR’s popularity was on the decline. When it appeared that the Republicans would select an isolationist candidate in 1940 who would likely win the general, pro-war Democrat Wendell Willkie appears, changes his party affiliation and wins the Republican nomination. There were now two pro-war candidates on the ballot. I recommend the book Desperate Deception by Thomas Mahl which details the deceptive tactics that the Roosevelt regime used to involve the U.S. in WWII despite the wishes of the people.

We can dispute the analysis of statistics and the way that they are assembled, but the trends shown in this article and past changes to our U.S. society that are visible to our own eyes are inescapable. Closing our eyes, nitpicking over numbers, and wishing them away will not accomplish anything.

However, debt-slavery is just one symptom of a chronic disease that affects our nation. I would call it wealth corruption: it is when the small percentage of the population that is wealthy take over our institutions, so they only serve their best interests and not the best interests of society. Our politicians then pass and our judges (who can practice corruption in the secrecy of courts in which no cameras or recordings are allowed, as in LA) then interpret laws in such a way as to benefit their wealthy sponsors.

That is how we get to the point where 11% of Americans now admit to owning 76% of all assets and goods in America. As an attorney that represented the wealthy for years, I can tell you, if they admit to 76%, given the asset hiding, creation of trusts, use of foreign shell corporations to hide asset ownership, etc., it is probably likely that 4% own 94% or more of the total assets and goods in the U.S. Tax fraud, accounting fraud, and asset hiding are endemic and now standard practice. Remember Enron? That is just one type of accounting/tax fraud.

There are many. The IRS has been deprived of funding, when it is clear that a small increase in funding would result in vastly greater tax revenues: from the wealthy tax cheaters.

I saw those kinds of things when I represented banks and insurance companies: documents are made to disappear from files by senior company executives or law firm partners; witnesses were encouraged with promotions or promised bonuses or by moving them to other locations so they cannot be located for subpoenas not to harm the institution with testimony; even judges that were not bribed tried to curry favor in the hope that by pleasing a large institution they would receive sponsorship to higher political office or their relatives received other benefits. I felt troubled at the time, because I realized that I was winning not on the merits or on legal grounds but due to such tactics by crooks and due to crooked judges’ biased interpretation of the law and facts of each case.

Corruption has been with us for hundreds of years. How have the rich corrupted our prior system in the last few decades to benefit themselves? For example, they have limited the benefits of the bankruptcy process to themselves. The Trump family can declare bankruptcy of their corporations and get rid of millions of dollars in debt.

However, you and me cannot discharge student debt anymore, even if we qualify for bankruptcy. Bankruptcy Chapter 7 is the section of laws that lets you discharge all of your debts in less than a year and keep certain exempt assets. Now, after “reforms” it is only available to the very poorest members of the population with the lowest income: those who have so few assets that they really do not need it and very rarely use it.

That was the goal: to eliminate bankruptcy benefits to all but the rich, by pretending to reform it. Who was enriched? The banks and credit card companies that were enraged at seeing the bankrupt walk away from their debts and build new lives, without paying them.

Bankrupcty Chapter 13 allows discharge but only with payments over years and with plans and expensive legal representation. Many, many people that desire bankruptcy cannot even afford to pay the initial legal fees and court fees for Chapter 13, so how can the bankrupt pay for years of legal help up front? Thus, it is out of the question for those who are bankrupt and do not have a wealthy uncle.

Chapter 13 has also been made as expensive and complicated as possible, with onerous requirements that payments be made for years, so many do not complete the process. Those and other forms are made overly complicated to ensure the need for expensive legal help. Thus, the wealthy have ensured that few of the peons (and by those I mean the poorer 75% of Americans) will be able to effectively use it.

Starting the process does not accomplish anything, if you do not get the ultimate bankruptcy discharge. That discharge is only available after a long, complex process and years of payments, which most do not complete.

Bankruptcy “reform” is just an example of one of the tactics of the wealthy. Putting justice outside of the reach of the poorest 75% of Americans. You will say that is not correct.

It is correct. How many of you can afford to pay $500 per hour for thousands of hours of expert attorneys plus tens of thousands of dollars in expert fees, tens of thousands of dollars in court reporter fees, and thousands of dollars in jury fees to take a case through trial, while missing work for weeks?

Few Americans can afford that. Even most attorneys now cannot afford to finance a case which they are not 100% certain of winning.

you’re right. when our publishing business went tits up, i couldn’t even AFFORD to file for bankruptcy. i LAUGHED when i read the processes available to me. i just gave up and cackled in the fetal position for a few years.

and losing everything i thought i was supposed to be or do as an “american” really upended my take on REALITY. nothing made sense once i stopped being so distracted and caring about even staying legit and alive.

i’ve heard it said and i’ve lived it: there’s nothing scarier than people with nothing left to lose… so all the sudden i got how OTHERS were feeling for a change.

Mike

Powerful commentary, thank you sir. And again, thank you Mr. Richter for providing this valuable venue.

An economic “boom” fueled by runaway, non-secured debt. What could possibly go wrong?

Depends who you are in the scenario. The poor find out what can go wrong, while the wealthy transfer more funds up the ladder which wouldn’t feel wrong at all. In the trickle down effect they really mean the wealthy are at the bottom, the little money left for the poor slowly trickles to the wealthy with every recession as the “haves” buy low and “have nots” sit on the sideline saving.

It always starts at the margins.

Be that individuals (this aricle) or countries (Argentina, Turkey).

Then it moves towards the centre, at different rates depending on the time in history and exact circumstance.

The final domino is the US Gov. How fast?

Out of interest how are car leases treated in this (as debt?). With the shift to more and more car leases, if not counted as debt, this might have an impact on the overall numbers.

I used total consumer debt, which includes auto loans and leases. So car leases are in these figures.

I would also add that some consumer debt falls under the business debt classification. I have had personnel at the bank where I have my business accounts suggest that I could use a business line of credit to re-finance an auto loan, so apparently this is a common practice for some business owners. The appeal (I am assuming) of doing this is to benefit both from lower interest rates and to have the principal and interest paid on a car loan exempt from FICA tax under a sub-S corporation.

Needless to say, I declined the offer.

I don’t know what the tax advantages are or may be for business owners to lease their car instead of buying, but I assume there are some if one’s business requires driving to meet clients/customers outside of where a person’s company is located.

Our tax codes are complex to say the least, and if a business owner has a financial advantage by leasing versus owning, then more power to them. Otherwise, it’s better to pay cash when buying a ride.

I do like the name you comment under Debt Free.

Wolf, yesterday it was all about how transportation was straining at the seams to deliver. I said…deliver what, arms? As I pointed out it sure is not goods to be bought, be it new or used. Certainly not when there are massive closing of stores all over the country, the web sites to sell new and used are dead for buyers, car lots are bumper to bumper, even pet shops closing ( like when has that happened before in such numbers).

On top of that, these web sellers including AMAZON are cutting off customers for returning items and/or filing complaints. Take that seriously and think about how and why they became so big to begin with. A nail in the coffin of web retailing? Web wars for consumers is nearing the end, just look at the discount offers which are off the charts.

Wolf, the headlines do not match up with observations. The truckers can not be enjoying a bumper year of deliveries when the dumpsters out back are empty. Again, unless they are delivering arms to the military. I will say I can understand if they are busy with good to repair houses from the hurricanes, but otherwise is just does not add up.

Everyday I feel like I am in a story living a life of imaginary numbers and fantasy. …… Until the bills arrive.

Curious.

This is the second time in two days I have read of web sellers like amazon cutting off consumers.

How extensive is this?

What is the spectrum of these cutoffs?

Is this how consumers are divided and conquered?

It is not just web sellers cutting back on returns, some brick & mortar retailers have systems that track the number of returns and disallow them them after a certain number. There are articles about it online.

You’re conflating the most vulnerable consumers that have a lot of debt (the subject of this article) with the majority of Americans who are doing anywhere from OK-ish to very well. And those doing OK-ish to very well are buying a lot of stuff.

Retail sales are up over 5% in Q1 compared to a year ago. Online sales are up over 16%! Trucking companies and railroads are hauling a record volume of merchandise, including industrial loads, as my transportation article the other day pointed out. The goods-based economy is doing well at the moment. But there are credit problems are appearing at the margin, which is what this article points out.

BTW, if you’re waiting for the “nail in the coffin of web retailing,” as you said, you will need infinite patience :-]

Debt slaves biggest expense is their rent.If too many of them

fall apart at once-that is the time it matters- many rental units

open up at vastly lower rents.As well the current strong economy

offers plenty of runway for gov’t to pitch in if need be.Not to

worried about it all right now.

10 years ago I had a good medical insurance plan. Go to the hospital I had a $200 copay. Didn’t matter what my bill was I only paid $200.

I’m on medicare now but the year prior to that that same employer plan had been Obamasized. I know had a $5000 deductible when I went into the hospital. Oh and premiums kept on rising both for me and my employer. In fact, my employer contribution exceeded my pension benefit.

This doesn’t show up as ‘consumer debt’ until it does but it hangs over most Americans as implied debt.

I never would have guessed that CC + auto + student loans is more than mortgage debt. Great article. I thought it was bad enough that we’ve got monopoly money propping up zombie companies. As if I needed another red pill!

ZeroBrain,

Based on your conclusion, I think you may have mis-read the first chart. In absolute dollars, mortgage debt = $10.1 trillion and non-housing consumer debt = $3.8 trillion.

The first chart shows the MONTHLY payment obligations (not total debt) as percent of disposable income. Monthly payments on mortgages benefit from very low mortgage rates. Non-housing consumer debt, particularly credit card debt has very high interest rates, and so the monthly obligations are higher.

Indeed I did. I am trying to make good on my handle.

The lowest wage earners are usually the most vulnerable. Nothing new here. The difference these days is that the ability for this group to borrow up to their eye balls has never been easier. They know that they’ll probably have to default. But they don’t care. I see it every day.

The transfer of wealth doesn’t apply to them as they’ve never had any wealth to transfer. The money they borrowed was created for thin air. The asset they “purchased” with money they could never earn, will be sold at a severe discount. The ones with residual value, anyway. It’s a cycle.

One question I have is the degree that cash-out refinancing is having on economic activity and inflation. Housing “inventory” might be low, but that wouldn’t hold back refis. Why borrow on a credit card at 16% when you can borrow at a lower rate on a refi? I have even heard of some lenders offering to roll student loan balances into a mortgage. This can’t end well.

Wolf, love your out-of-the-box analytical approach to sift the truth out of the “statistics” government provides us. Have you considered also trying to strip out the recent years trend of all increases in personal income going to the very top income brackets from your chart? Since any additional income accruing to even the top 10% is de facto disposable income the denominator used to plot your points would appear to be increasingly distorted the farther away we get from the Great Financial Crisis and QE.

I do something like this once a year, in September, when the data of the Census’ annual American Community Survey are released. This is a huge amount of data that comes in all kinds of layers that are suitable for this type of analysis.

Thanks for the info. I tried to do a quick google search for the data necessary to strip out the disposable income of the top 10% (or 5% or 1%) over the period of time covered in your chart and came up short.

I think the Affordable Health Care Act has done a lot to reduce consumer debt. Used to be you went to emergency you had to use your CC. Monthly premiums aren’t figured into debt calculations but CC debt for HC is. And student debt is personal CAPEX, an investment in the future. People use mortgages and auto loans who don’t need them, for the convenience. You can pay cash, but whats the advantage? Corporations represent a bigger problem buying your own shares is like somebody self publishing their own (embellished) autobiography and giving copies to all their friends. It Increases you self worth, marginally.

I’m not sure if the GFC was primarily triggered by high debt loads, or by financial instruments containing hidden tranches of junk debt misassigned a higher credit rating by rating agencies and held on the balance sheets of major banks. Their mark to market resulted in the capital of these institutions being impaired, a major counterparty failing and a massive contraction of credit.

The bottom line here was that all those bonuses and fees collected for packaging that junk was ultimately paid for by taxpayers and homeowners. I stand to be corrected on all the above but it was not a problem so much of high debt loads but a concentration of the most toxic elements of it in key institutions and a weak and compromised regulatory environment and perhaps to aggressive action by the Fed. The poor lending practices that were enabled for political reasons were just part of the picture. Hopefully the regulatory environment is a lot tighter across the board these days.

“Hopefully the regulatory environment is a lot tighter across the board these days.”

Oh, puh-leeze.

The US has been increasingly legalising bank fraud for years, and did so again big time just today. In due course they’ll be able to send most of the population into destitution and early graves, and you won’t be safe in Canada or Europe either.

What are you going to do about it? Vote? Sign a petition?

It’s a long-term goal, always has been. It’s what they do. Where do you suppose those record-breaking profits are coming from anyway? It’s not as if banksters actually produce anything themselves. Where do you suppose that $20,000,000,000,000.00 tacked on to the US national debt disappeared to?

Parasites uber alles, dude. Count on it.

You could take the position that the banks role in the GFC was primarily reactive rather than proactive. The liberalization of the lending rules and the expansion of sub prime credit was I believe a political initiative with the regulators essentially acquiescing to the process. House prices after all don’t go down. With this comforting assumption lending against future capital gains seemed less risky than it was.

The banks were left to be creative with a critical mass of mortgages that were going to be non performing. One can argue about the delinquency of the various parties involved in resolving this issue but the prime causal factors may not reside with the banks.

At least the whole mess was dealt with quickly rather than sweeping under the carpet as is the practice in other parts of the world.

“I’m not sure if the GFC was primarily triggered by high debt loads, or by financial instruments containing hidden tranches of junk debt misassigned a higher credit rating by rating agencies and held on the balance sheets of major banks. Their mark to market resulted in the capital of these institutions being impaired, a major counterparty failing and a massive contraction of credit.”

The Lehman implosion triggered an American correction event.

What turned it into the GFC. Was the revaluation of the fraudulent greek loans. Hiding under the MASSIVE rug in Athens. Which had not been declared, when greece fraudulently joined the Eur.

Just as wall street 1929 was a US correction event that was turned into a global depression by the collapse of Credit anstalt. In Austria.

In Both events, the US got the blame for Europe’s misdeeds, which turned the events global.

“Hopefully the regulatory environment is a lot tighter across the board these days.”

Dreams are free mate.

It would be very instructive to see this class of data disaggregated by income quintile (or similar).

The consumer debt/income ratio of the top 1,5 or 10% is often not relevant to the overall health of the economy.

If recession comes, it will be when the bottom 50% throw in the towel because they can’t make the payments anymore. The debt ratio to watch is that of the canaries in the coal mine…

So non housing consumer debt as percent of income went from just under 25% right before the last recession to just over 26% now… well, not good but also not the end of the world, either.

When it comes to credit expansion, governments and corporates is where it’s at. They’re the ones who’ve really levered up in the past couple decades. Consumers — not so much.