After the party, the hangover.

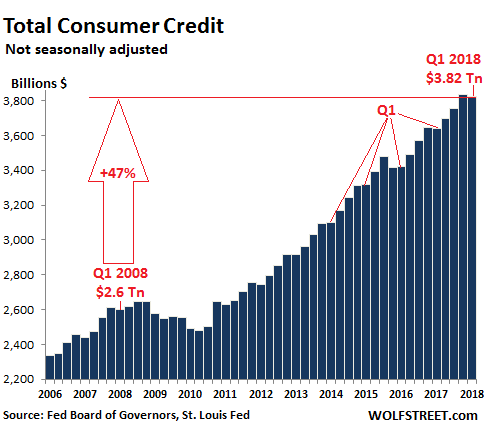

Total consumer credit rose 5.1% in the first quarter, compared to a year earlier, or by $184 billion, to $3.824 trillion (not seasonally adjusted), according to the Federal Reserve. This includes credit-card debt, auto loans, and student loans, but not mortgage-related debt. That 5.1% year-over-year increase isn’t setting any records – in 2011, year-over-year increases ran over 11%. But it does show that Americans are dealing with the economy and their joys and woes the American way: by piling on debt faster than the overall economy is growing.

The chart below shows the progression of consumer debt since 2006. In line with seasonal patterns for first quarters, consumer credit (not seasonally adjusted) edged down from Q4, as the spending binge of the holiday shopping season turned into hangover, an annual American ritual:

Note how the dip after the Financial Crisis – when consumers deleveraged mostly by defaulting on those debts – didn’t last long. Over the 10 years since Q1 2008, consumer debt has now surged 47%. Over the same period, the consumer price index has increased 16.9%:

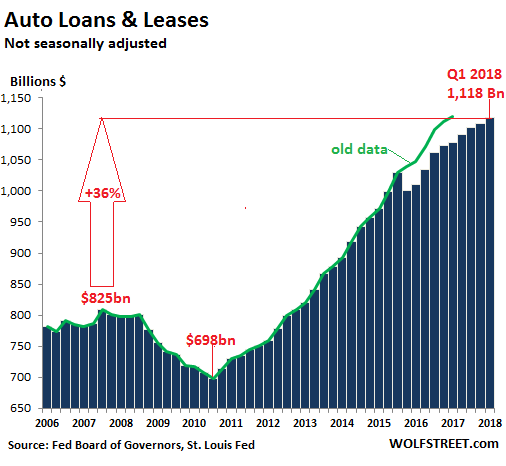

Auto loans and leases for new and used vehicles rose by 3.8% from a year ago, or by $41 billion, to $1.118 trillion.

It was one of the smaller increases since the Great Recession: The peak year-over-year jumps occurred at the peak of the new vehicle sales boom in the US in Q3 2015 ($87 billion or 9%). However, the still standing records were set in Q1 and Q2 2001 near the end of the recession, with each quarter adding around $93 billion, or 16%, year-over-year.

Loan balances are impacted by prices of vehicles, number of vehicles financed, the average loan-to-value ratio, duration of prior loans (when they’re paid off), and other factors. So this chart is not necessarily a reflection of how many new and used vehicles were sold.

The green line in the chart indicates the old data. In September 2017, the Federal Reserve implemented a big adjustment of consumer credit data going back through Q4 2015. This adjustment was based on survey data collected every five years. So routine. The adjustments hit auto-loan balances disproportionately, knocking them down by $38 billion retroactively for Q4 2015. To show the distortive effect of the adjustment – and to show that it wasn’t the collapse of the car business – I added the old data in green.

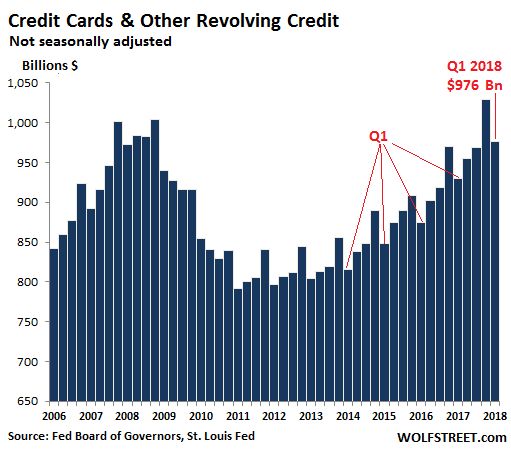

Credit card debt and other revolving credit in Q1 rose 5% year-over-year (not seasonally adjusted) to $977 billion. This growth rate was down from the 5.6%-6.8% Trump-bump increases that started in Q4 2016 and ran through Q4 2017. So it was somewhat of a disappointment for those wanting to see consumers drown in high-cost (or high-profit) debt.

On a quarterly basis, and in line with seasonal patterns, revolving credit card balances fell by $52 billion from the shopping season debt-pile up in Q4, as the annual hangover began. In dollar terms it was the steepest Q4-Q1 plunge since Q1 2010. In percentage terms (-5.1%), it was the steeped since Q1 2012.

But wait… Q4 credit card balances of $1.03 trillion had been an all-time record, finally beating the record of Q4 2008. And Q1 2018, at $977 billion, set a record for any first quarter, beating Q1 2008 by a smidgen ($973 billion). So Americans did their job piling on high-profit debt.

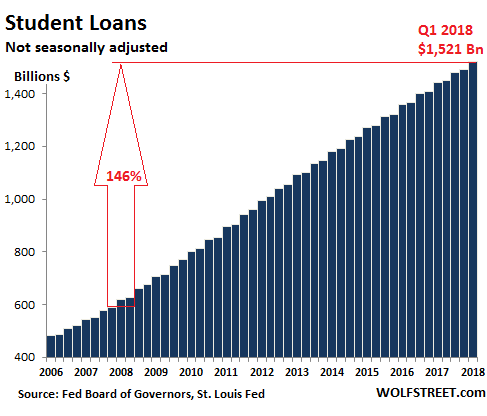

Student loans in Q1 jumped by 5.4% ($77.8 billion) year-over-year to $1.51 trillion. While a shocking increase, it was the slowest year-over-year percent increase going back to 2007, the beginning of the data series: In fact, between 2007 and Q3 2012, these year-over-year increases ranged from 11% to 15%!

But it’s not like more people are going to college. Higher-education enrollment had peaked in 2010 and declined at least through 2015, according to the last data available from the National Center for Education Statistics. And yet, over the 10 years from Q1 2008 to Q1 2018, student loan balances soared by 146%, from $619 billion to $1.521 trillion. Over the same period, the consumer price index rose 16.9%.

Students added $902 billion to their debts over the past 10 years — a debt that will dog them for decades to come. And for most of this debt, taxpayers are on the hook. But who obtained the money?

A whole economy has sprung up around this bonanza, with entire industries getting fat: Investors in private colleges; the student housing industry, which has become an asset class within commercial real estate; companies like Apple that supply students with whatever it takes; the textbook industry; overpaid top administrators; construction companies and affiliated industries building university-owned projects, from mega-stadiums to glitzy administrative buildings; Wall Street by making it all possible; and many more. But hey, that’s how you get GDP and corporate profits to grow. It’s a dirty job, but some’s got to do it.

This is the brick & mortar part of e-commerce. Read… As Malls Melt Down, Industrial Properties Heat Up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looks like the Z generation will be screwed up by debt even worse than Millennials if this trend continues.

Student debt is a structural problem with no easy or equitable solution that I can fathom. With jobs that provide a 1970s-style middle class income shrinking as a percentage of all employment, and most of those jobs that do pay such wages tied to at least a 4 year degree, anyone who can afford to is bidding up the price of those assets (degrees) because upper middle class families in particular will pay anything to get Biff and Muffy into “a good school.” Universities therefore charge whatever the market will bare, and drive up prices ad infinitum. The only way the middling sorts and the working poor can pay is to pile up the loans. Problem is, a combination of sloth, snobbery, and covering of HR departmental behinds makes only top “brand” degrees really worth much. But what are the rest of the population to do?

It will all end badly.

…And I feel like I snatched my head out of the guillotine just in time, too.

https://www.cnbc.com/amp/2018/05/05/for-some-student-loan-debt-is-doubling-tripling-and-even-quadrupling.html

Yea, college as a necessity for a prosperous life is a popular meme these days. With federal guarantees on loans and the impossbility of discharging student debt in bankruptcy, there is absolutely no discipline on Institutes of Higher Borrowing and banks that fund the loans. They are creating a class of indentured servants that is prone to erupt in violent revolution at some point. Well, maybe they would if their testosterone was a little higher.

The easy way to quell any revolution is to turn those Generations into mindless zombies, obsessively scrolling through their phone feeds, too busy to pay attention to what’s happening around them.

The Fluoride in the water plugs the thyroid reducing mitochondrial energy then the RoundUp (Glyphosate) binds minerals that eventually result in lower T in makes. Glyphosate also attacks the Appendix where we now know the body stores good bacteria to reseed the colon after pathogen attack.

So, so glad I left the “prepper” or “survivalist” place. I was required to practically bathe in glyphosate, doing weed control.

Here’s a hot tip for getting rid of weeds that grow in cracks in cement, between decorative rocks, etc. – just pour boiling water on ’em.

Most of the current college population should never have gone there. They have been brainwashed. Guys with IQ less then 110 should go into trades or try to start their own business or go to community college or teach themselves programming if they have aptitude for that. Most of the current college population is just taking a very expensive drinking, sex , drugs and cultural marxism indoctrination vacation.

I know two ‘college’ professors. One ‘male’ and one ‘female’, if it is still OK to say such, you know “gender specific”. Both make very good salaries. She can’t spell and is an ‘English” professor, he can’t put together a comprehensive sentence, and he teaches ‘communication’. Both get red eyed, loud and animated over the least thing that questions ‘social warrior’ behavior, or university “Safe Places”. Both are/were committed to Bernie Sanders, MOVEON, BLM, and the rest of these well oiled organizations, most founded in ” cultural Marxism”. BOTH judge their students on ‘attitude’ and make no bones about the line in the sand that is a A or B grade, or C grade if their personal opinions can be applied. If you are a student of theirs, you had best understand that. The end of “1984” you either agree that 2 plus 2 is five, or you are out.

These two examples are not unique for ‘college educators ‘, keep that in mind when to talk to your child about so called ‘higher education’. Programmed education is more like it, free and open thought be damned

Sounds like these two straw figures were invented to prove a political point. Arguing your own positions effectively works much better than trashing an imaginary opponent.

@Mary

Somehow whenever anything remotely political comes up, someone always has the perfect boogeyman to epitomize the enemy, which more often than not in these discussions is something more akin to a caricature of an ultra-left wing person (who is then used to represent liberals as a whole) rather than a person who actually exists.

Unfortunately in the era of fake news, and with critical thought diminishing more and more, it’s easier to create and denigrate imaginary foes, to tilt at windmills, than it is to engage in value-added discussion.

I’m just surprised that the non-existent female professor blindfaith knows didn’t teach gender studies in his fake example– that seems to be the default, usually.

Fortunately these made up anecdotes are easy to spot from a mile away.

Should have seen my Art Professor – he told me he was giving me a C because I was an engineer.

As a military historian with a strong liberal arts undergraduate education and a Ph.D., I have no idea what “cultural marxism” is. I studied Marx, and I had some postmodernist and critical theory professors, but as far as I know “cultural marxism” is just a right-wing buzz-term for “stuff I don’t like.” Like the way dopey people who happen to be Leftists throw around the word “fascist”. It’s just sloppy.

Guaranteed gov’t college loans are what drives up costs.

Somebody is eventually going to eat the costs of all this unserviceable debt, then it happens,*queue outage*… Why doesn’t somebody do something about it? Oh okay let’s put interest rates back down to zero, maybe negative, and we’ll do QE bigger and better, run larger deficits. K. Fixed it.

A central tenet of American Capitalism is not having to be accountable for your actions or your financial decisions. The 2008 crisis and our $22 Trillion debt are clear examples of that. We have sent a clear message to future generations that there is always a bailout. And spending beyond your means is completely acceptable; without any possibility of paying your debts back. They all expect a College Loan bailout will happen as well. And it will. It’s the American way.

Rick:

Right on! I grew up during the Great Depression and observing the amount of debts the “common people” have/are accumulating is the creation of a not too distant horror story. We don’t practice “capitalism”. We practice a political/social criminal conspiracy system. I hope it continues form the sake of my children/grandchildren who are no longer mostly into “defined pension plans” and are fully invested in 401k’s etc…….

Most of them live in the “kernel of imagination” Silicon Valley, have decent paying jobs and have hardly any idea of so much of the rest of the nation that has become “flyover country” for the major pols. I’m reminded of the scene in the late ’80’s Wall Street when one of the players acting the part of a stock brokerage scene (with those appropriate hundreds of cold callers under his supervision) where one of his underlings makes a stock sale loss says, “Well, somebody is gonna pay and it ain’t gonna be me!”

Then comes the big bailout.

A central tenet of CRONY capitalism.

This may come across as naive, but Why?

I understand that some people have strong current needs that make bad decisions an acceptable alternative. But, otherwise, why do people borrow so much? If these numbers balance out to incomes that support them, then OK. Otherwise, why would people indenture themselves for no good reason?

For over 40 years, I never, except once or twice out of necessity, charged more than I could pay off in a month. My 4 years of school loans were the horrific amount of $2500 in the1970s, and $500 was used on ‘unapproved’ things .. nobody claim that’s equal to $25,000 today unless you want total disrespect in a reply. Today, thanks to a little self discipline, I have savings that will aid me well in my retirement.

Seriously, if people want to encumber their future for the perfect cell phone today, why should I care? A little research can lower lots of expenses. I really don’t get it. Extreme Debt and the resulting consequences looks like a willing and happy choice for many.

Somebody, correct me on this.

To add on, a local community college charges maybe $100, more or less, per semester hour. They use the same text books as schools that charge several times that amount, basically all other schools. Going to a major school just because it’s a major school and paying through the nose for it looks really dumb to me. To me, these people look like debt sheep. Why should I care about their bad choices?

BTW, my CPA was based on studies later in life. I tool a lot of refresher courses, all online from community colleges. My CPA review came mostly from Amazon. I passed all 4 exams the first time. Very cheap.

Again, lots of debt appears, to me, to be a choice.

Good comments CDR. Thanks for sharing….and i agree!!! I also don’t get it either.

I’ve always wondered if we’re teaching our upcoming collegians to be wise consumers in getting their education. I got my degree later in life by going at night to community colleges and inexpensive state schools, and even one or two old fashioned pre-internet correspondence courses. I love that Payne Weber ad where daddy and his smiling daughter are roaming around this beautiful old style tree-lined campus (I want to go there!) and he’s on the phone to his broker hinting how expensive it’s going to be for him. Must be nice.

I think it was a case in North Carolina where IQ tests were banned as an employer screening tool and the college degree substituted as a proxy for certain jobs.

While knowledge of chemistry might be a necessary precondition to work at Dupont reading Chaucer or knowing what the Kellogg-Briand pact was probably isn’t worth the thousands of dollars it costs to verify you once did so to say nothing of the time lost in acquiring the academic credential.

Assuming one is intelligent and otherwise qualified to perform the job a cheaper workaround for the academic credential might be to claim attendance at a defunct private college. Not your fault that your transcripts are not available because the school went bankrupt and closed. One would merely have to look up and memorize the names of the various buildings and the names of a few former instructors for you to speak as fondly of the old alma mater as any graduate of any other private college. Might even be a lucrative opportunity in printing facsimile degrees from defunct colleges for those unwilling to spend $100,000 plus for a credential from a current but little known school.

Well done and totally agree. However, there are generally well worn paths for people to follow and most follow them without questioning. The lack of questioning is indeed a choice.

Well, I would say that there is something at play in attending the more “prominent, influential” institutions of learning such as Penn State, Harvard, Yale, Stanford, etc, etc…..when graduated one of the essential parts of that sheepskin is the “Rolodex” of names you have accumulated during your stay. You can’t deny that those kinds of contacts at those kinds of institutions can’t help you in your life career along the way. Many doors are opened by those names. Their alumni groups represent a very powerful force helping you along in the future.

Take the case of my sister-in-law. She has a deep, fundamental need to be respected by those around her. And she can’t do it by most normal processes (job, charities, community standing), so she does it by the stuff she has.

So she has a 3200 sq ft house, immaculately up to date kitchen and bathrooms, big pool, outdoor kitchen, brand new Honda Odyssey and she replaces the furniture in the house every 2 years. My dear brother, who is nearing retirement, maintains strictly separate bank accounts and credit cards.

She pays for all of this with minimum monthly payments with her salary as a billing clerk at the local hospital. She also drinks lots of wine out of boxes. My brother told her she has to divorce him before she declares bankruptcy.

You remind me of the old saying that the fastest way to become poor is to try to make other people think that you are rich.

Those debts belong to your brother at the divorce. Probably the house too. Your brother is not nearing retirement. He is nearing homelessness.

Need more often than not has little if anything to do with the current debt crisis . Its foundations are deeply embedded in ‘ want ‘ , desire , keeping up with the Jones’s and the ideology of he who dies with the most ( and the biggest ) toys wins constantly being reinforced by the marketing mavens across all sectors .. and now this present administration as well .

Have any doubts ? Just take a look in the majority of garages across the land full to the brim with unused and more often forgotten junk to the point where 50% of two car garages can only accommodate one vehicle .. with another 30% able to accommodate none leaving a mere 20% of two car garages able to contain two cars ( PEW research ) And thats not counting basements .

Even higher ed has succumbed as everyone is desperate to get into the expensive upper tier colleges and universities rather than get more often than not an equal if not better education more than able to fulfill their career goals etc

And then there’s the vacation / resort trap with far too many people overspending for a week or two of perceived luxury and pleasure

Not to mention the current addiction / fad for new overly expensive and unnecessary gas guzzling full size pickups and SUVs ( that’ll work out real well what with rising gas prices ) rather than a sensible car or van .

Then tack on the few additional that fall into debt due to unforeseen circumstances and / or emergencies and you’ll begin to see the picture on the ground more clearly .e.g;

Todays debt nine times out of ten is volitional .. not circumstantial

So sorry cdr .. but you’re spot on the money with no correction what so ever needed .

Speaking of vacation/resort ‘options’ … mine is my yard ! I can grab a glass of homemade beer or mead, maybe a sandwich .. head for the loungechair, and watch the local birds and honeybees (mine), and whatever other creatures that find their way to this oasis flitting to and fro, drinking from the fountain not 4 feet from where I sit ! Cost to do so .. ZERO ! When I want to partake in an exotic meal, I cook it ! If I die with the most berries, cherries, and honey on Jone’s Street, rather than toiling over a useless lawn (manicured, or otherwise), or drive a beatup used pickup (rather than a new vanity truck straight off the lot), does that make me a loser ?? .. hell no !

We have NO debt whatsoever .. and I hope to die that way, while wandering the staycation. ‘:]

TJ, you make it sound like those who consume do NOT have any emotion control. But there is a darker side to this. It is competition. If all the other guys have bigger houses, toys and vacation all the time and you don’t? You don’t get laid. If all the other ladies have all the gears and you don’t? You don’t get the guy with most toys and vacations. The power of “social” recognition and evolutionary competition FORCED one to consume. It is NOT like he/she so much desire or WANT TO consume IS THE ONLY driver of these behaviors.

In front the choice of “stuff” and social recognition, “freedom” does NOT matter. Therefore, let’s be slaves to debt.

A mature and wise person would say who cares. This is not the high school life where if you are not cooool, you don’t have any friends; this is real life.

And even in high school, kids who are born in a successful family , learn that result of being cooool in high school is working in a fast food restaurant when you get older.

“If all the other guys have bigger houses, toys and vacation all the time and you don’t? You don’t get laid.”

You might like to visit a few PUA sites, try their advice, and find out what *really* gets a man laid. Toys are not high on the list. Sucking up to women is on the bottom of the list.

First on the list is to make yourself the center of your world. Women are herd creatures, and they are looking for a man who will lead them. That is just how they are.

First on the list is to be dominant in your personality, independent in your thinking, and socially competent – for example, you need a sense of humor.

If you can’t manage to put yourself first, if you are a stale and correct nu-man type, if you go along with current anti-man propaganda, hoping to curry favor, women will despise your weakness, find you unexciting, unpromising and un-intriguing, and you will find that the current sexual market place is a horror show, no matter how many toys you are polishing in the driveway.

Two “firsts” on my list. We’ll call it a draw.

These PUA stuff contains lots of “fake it until you make it” stuff, such as “behaving dominantly, confidence, humor “, those “looks and traits” of the “winners”. This is EXACTLY the evolutionary competition driver of debt fueled consumption, which is to make you “look good/winning/rich” until you “be good/winning/rich”. The PUA stuff takes effort and time, but take on debt is EASY!

I mean even Elizabeth Holmes has to fake blood test to “look like” Steve Jobs, that’s what you need to survive silicon valley. Is she immature? I myself think it dumb to take on debt and consume houses/cars/degrees/shoes. But I understand the human nature behind this. This is neither naive or immature. This is same as drug taking or competitive evolution game.

That’s why you should get in the gym and lift, bro. I’m talking legit lifts like squat, bench, deadlift. Get your deadlift up to 500 lb and then we can talk if you still need to compensate with consumer spending.

@Kim

“You might like to visit a few PUA sites, try their advice, and find out what *really* gets a man laid. Toys are not high on the list. Sucking up to women is on the bottom of the list.

First on the list is to make yourself the center of your world. Women are herd creatures, and they are looking for a man who will lead them. That is just how they are.

First on the list is to be dominant in your personality, independent in your thinking, and socially competent – for example, you need a sense of humor.”

Had to LOL at this. Very off topic but I had to respond.

The dynamics of relationships are infinitely complex, and simplifying women down “Women are herd creatures, and they are looking for a man who will lead them” is incredibly dumb, full stop. I assume you’re a woman, but I almost have a hard time believing it based on that statement. It’s just enormously stupid. You’ll find that most of these dudes who try PUA tactics end up single, because they’re lame to begin with, and you can’t fake it in the long run. Most women will see right through their bull. Does it work for picking up the random drunk chick in the bar occasionally? Sure. So don’t a million other ‘tactics’ that don’t involve acting like a supreme douchebag.

PUA tactics rely on the shotgun approach. For every woman who you can trick into thinking you are a sly, confident man, dozens more will see you for the manipulative dweeb you are and shut you down. The ironic thing is, drop the manipulation and use the same shotgun approach, and you will get laid just as often, if not more, without the need to lie about who you are. If you’re enormously socially awkward, they might help you learn the basics of how to start conversations and act more like a normal human being, but that’s about it.

Professional “pick up artists” report success rates of between 1-5%. They’re talking to literally hundreds of women, and sleeping with a handful. I would even argue that’s potentially worse than the average guy would do just being himself and talking to the same women.

PUA success lies in just getting guys out there talking to women, not in the underlying tactics. So I guess in that regard it works.

Smingles, I know toys are NOT on the list for PUA practices. But majority of people THINK toys or other labels of status is. You can easily catch women being insecure without make up and gucci bags and man being insecure if he drives Honda among others who drives BMW. Would the toys get you laid? Maybe NOT, and you can run science and statistics on it. BUT most people THINK it could, at least remove insecurities and get SOME attention or even just avoid being ignored.

I am NOT suggesting what people THINK works in reality. The PUA stuff may work better but it takes patience, hard work and self cultivating. Debt buying toys are much easier and straight forward although it may NOT work as well.

Too many families (and, of course individuals) have not learned the difference between “life-styles” and “quality of life” to their detriment. And, in America the heavily indebted are usually sticking to the former and have no clue as to the latter.

Who in the right mind would take eccastasy, inject some heroines, get some cokes? Credit for consumption issuer is the drug dealer. Human nature will take it.

If you are the sober one, you don’t even get recognized, you don’t get a date, because you are boring, everybody wants to be cool and have fun, you will be left out.

Be the debt slaves, you are “IN”, you are cool. Or be the drug dealers, you are having fun and making lots of money as well. Just do NOT be the sober one.

Naive would be too kind.

You’re really showing your age if you have to ask “Why?”.

If I called you a stereotypical Boomer, would you be offended?

Yes, 2500 of those old-time dollars do indeed work out to around $25k today.

I have a receipt for a sports car from “back in your day” and it cost around $3300 – today a similar sports car costs around…$25-30k. And I know all things are not identical in the economy, but I had to prove the error of your way.

If a free market, I would agree with you,…who cares. But due to the bail out mentality in Govt, YOU will end up paying. Higher taxes on savings ( interest rates below inflation )

It looks to me as though by far the biggest chunk of the increase in debt is due to student loans.

Am I reading the graphs wrong?

If so, it looks like more people are getting degrees. I’ve heard more employers are demanding bachelor’s degrees for many jobs that didn’t require them 20 or more years ago (when most of us were in school or considering school).

Your question is apt. To add just a little bit of a additional perspective — this is not sudden. There has been a generational shift in attitudes that took about three generations to mature.

The greatest generation gave their children a good life — not using credit much, those G.G. folks. A mortgage mostly, maybe a car.

The baby boom (me) had that good life, very good, thank you very much. I got my first C.C. right after college. I bought a hundred year old house, and used equity-line credit, properly, for (i) new windows (ii) new furnace and water heater and (iii) blown in fiberglass insulation. I did it because it had payback, but I also used credit extensively as the years passed.

And I am not sure what generation we are in now — millennial ? Not sure. And I do not know how they really use credit except for this student loan boondoggle. I fell sad for them and also for their (non)future.

(I forgot to mention that my immigrant g’parents, immigrants born in 1900, used credit PRECISELY ONCE, the family home mortgage.)

One generation rich, three generations poor . . . I first encountered this as Chinese Wisdom passed down :

http://www.famcap.com/articles/2015/11/18/the-three-generations-phenomenon-is-it-really-true

I agree with this — I think two big things have changed. One, families in general are less stable, and have less ability to amass resources and pass them down to their kids. A lot of trends have joined together to cause this: rates of pay increase over time, loss of factory jobs, loss of unionization, even an increase in divorce rates (it’s good for individuals, but man can it destroy resources).

Two, people spend their money on enjoying themselves. My grandparents were reasonably well off — they never went abroad. A family trip back to see relatives half the country away happened every 6-8 years or so. They had less stuff, and did fewer things.

I was born in 1971 — my parents paid for my entire education, so I hit the work force with no debt. It was a huge boon, but it was also easier back then. Skyrocketing tuition and wage stagnation make it tough. An economy where everyone starts out $30,000 in debt is a very different economy.

Community college is a good option for starting, if you’re not sure what you want to study, or if you want to get an ‘applied’ degree (by which I mean a BA/BS that you then use to get into the work force). There’s nothing worse than going deep into debt to dork around for a few years trying to figure out what interests you, and in the process probably dragging down your GPA.

However, if you do know what you want to study, or if you’re academically ambitious and are planning on getting a master’s or a PhD, then community college is not a great choice — quite frankly, the education you’ll get there is not as good as at a university, and you’ll be handicapping yourself. This might not be as true today as it was a generation ago, given that many universities now rely on the same adjunct pool as community colleges; but there is still a world of difference between a decent university and a decent community college.

The real bargain of higher education is the flagship state schools. If you want to balance cost and education, search these out. Even the mid-range ones, like the University of Kansas, University of Vermont, etc., will give you the CHANCE to get a great education; you just have to pay attention to what you do, and grab your opportunities. The best ones, like the University of Michigan, California, North Carolina, etc., are for my money as good as a good private school. What they lose in exclusiveness they make up for in size and breadth. Just don’t go out of state unless you have a trust fund.

I used to think that way. Later, I realized all schools use the same books and teachers come in ranges from horrible to excellent, with most about average. Later I learned first hand all schools circle the wagons around any criticism of horrible teachers – it takes real communication skills and experienced persistence to even get them to look into a problem teacher. And horrible ones I had to deal with all had tenure.

I won most but it took masterful effort to make it happen .. The ones I had problems with were either lazy to the point of obvious incompetence or just plain nuts and it affected my class efforts. One I just dropped because I didn’t need those particular hours, that one was a retired hubris filled man who was off way point on the described scope of the course, but scoredto the level of inconsequential minutia.

College is overrated by a lot. Education is a necessity. Don’t conflate one necessarily with the other.

BTW, CPA review is where you really learn accounting. College testing is just over the most recent chapters. Each of the 4 CPA exams requires you to recall virtually all details from the relevant coursework on demand with questions that you can’t outguess. If you studied it, or should have studied it, it may be on the exam. This is why fail rates are high on the CPA exam. Virtually nobody no matter what school they went to, anywhere, will pass the CPA exam without CPA review. My CPA review came mostly from Amazon books with minor parts from eBay and the internet. I passed all 4 the first try. Many others get their CPA review the same way – no colleges involved.

When it comes to consumer goods and taking on debt, my guess is it’s primarily a result of ‘keeping up with the Jones.’ As relative inequality continues to increase, I expect the trend to worsen. More and more people will be left out of the middle to upper middle class, but will still be trying to live that lifestyle, e.g. the expensive phone, the nice car, the big house. The only way to do that is debt. My theory is that if you were to go back in time, relative inequality was much less, the gap between the lower and upper middle class was smaller, so it didn’t take as much to ‘keep up with the Jones.’ Just one of many factors, but I suspect it’s a large one.

As for school, I would say it’s difficult to compare the 70s to today. In the 70s, for starters, you could skip out on ANY sort of post-high school education, whether it was the trades, a 2 year associate degree, 4 year bachelors, etc. and still get a decent paying job that could even be turned into a full career. That’s just not true today.

As for community colleges, unfortunately most don’t offer four year degrees. I just looked at two local community colleges, neither offer any classes that you would expect to take in your third or fourth year of college in accounting, finance, econ, etc. If you’re talking just the entry level classes, you’re correct, they’re using the same books, etc.

The thing is, ANYONE can go to a four-year school for cheap. There are TONS of smaller public schools that are super cheap. They may not have the big name, you won’t get a top-tier job in your industry out of college, but they’re legitimate four-year degrees.

You can pay $50,000+ to go to USC (Southern Cal), or you can pay $11,000 to go to UCLA (if you could get in). The truth is the range of costs is enormous, and kids don’t want to ‘settle’, they want to go to their dream school (even if it’s just because it’s pretty and has a good party scene) and their parents are willing to co-sign their enormous $200,000+ loans.

My advice would be to go to a community college for two years in a state where credit transfers are mandatory, get good grades, and then transfer to your four year school of choice for the last two years. At that point, you can often qualify for merit scholarships, and if not, you’re only paying two years of tuition (and you’re hopefully not going to a school that costs $50k a year). Or go to a cheap 4 year school for 1-2 years, get good grades, and try to transfer to the school you really want to go to. A friend went to UMass for a year before transferring to Harvard (he didn’t get in to Harvard from high school). It was much easier than either of us expected.

You nailed it. The only addition I would consider regards a nephew of mine. He’s going to be an electrician and decided to go to school for it about 100 miles away from his home just to get a perspective about being away from home. He will be employed forever and live a nice life. Lots of people could do the same for little money.

Economics, today, makes a 4 year college, or even a 2 year general ed community college a total waste of money unless it’s for the purpose of training for a specific purpose. Most people at this time are debt sheep and will ignore that concept and go to school because of the lemming call. The entire concept of higher education needs a work-over, but I’ll be long gone before it happens. They’re too entrenched as-is.

I can’t feel sorry for debt sheep. Not even a little.

It’s all good. Everybody says the economy is booming. And it does seems like its on its tracks…I don’t know under the hood though.

But It’s depressing to see everything so expensive, from a burger to a movie, from a car to a house…

What do you mean expensive? According to the government statistics, there has been little to none inflation in the last 10 years, and everything is rosey. I think someone has forgotten to drink his kool-aid. See, the rest of us drink from that kool-aid and never ask questions like that.

All debts will be forgiven courtesy of unrelenting inflation fed to us by our government, reserve bank and the banking system. Grab as much cheap cash as you can and don’t worry because debts are repaid in nominal value not real value. You have been given every incentive to dip into the honey pot and party like it’s 1999 pooh-bear so remember we are all forgiven (to quote the who).

That only worked back in the ’60’s and ’70’s when workers had annual COLAs. Your income inflated faster than your debt payments.

Those days are gone. Today, inflation just eats away at your income but your debt is always there, staring you in the face.

Simply another fine example of privatized profits and socialized losses with artificially low interest rates causing asset inflation.

Would you lend $1 trillion to college students at 7%? Of course not, as defaults and inflation would ruin you.

But what if you had access to money for 1.75% and the government (taxpayer) would take all non-performing loans off your hands? Then sure, why not?!!

The government already owns and enables virtually the entire student debt market.

The debt slaves are still optimistic though. https://www.marketwatch.com/story/americans-havent-been-this-optimistic-about-buying-property-since-just-before-the-housing-crash-2018-05-07

Muppets. Can someone do God’s work and send these guys to the cleaners already?

Which ‘optimistic americans’ are those ?? .. the credentialed 20% on up ? Hedgefunders .. Wallstreet ?? .. the Goldensacmen ?? , Congress and their sycophants ?? .. who ? .. not anyone I know.

Meanwhile, ‘Muricans are “plagued by financial anxiety” but still can’t resist piling on more debt.

https://www.marketwatch.com/story/americans-have-more-anxiety-about-paying-their-bills-than-they-did-a-year-ago-2018-05-08

Let’s go to Steve Keen, one of the (very) few economists that’s worth a damn:

https://www.youtube.com/watch?v=DyrDbmuhfH4

And margin debt, corporate debt, government debt, municipal debt, underfunded pensions, etc., etc., etc.

Like a pile of tinder waiting for a match.

Is there such a thing as credit exhaustion? Can’t that be calculated? Why can’t the borrowing limits of the consumers be known?

If you extrapolate these trend lines, both salaries and spending, far enough into the future at some point won’t it become obvious the debt expansion would have to have ended?

one would think so. however, here we are. personally, i”m surprised each and every day that it somehow manages to go on.

May 2 – Bloomberg (Shannon D. Harrington and Erik Schatzker): “Greg Lippmann, who helped design the trade against subprime mortgages that became known as the Big Short, says the next financial tremors will come from corporate debt. The former Deutsche Bank AG trader who now oversees about $3 billion at his LibreMax Capital LLC said… that corporate debt and equities will face the biggest pain when the next downturn comes. Investments linked to consumer debt, unlike the last crisis, will be relatively safe because companies have been the ones gorging the most on the ultra cheap interest rates during the past decade. ‘If the first quarter’s volatility is a harbinger of something bigger, I think that you’re going to see a lot more trouble in the corporate market and the equity market than the structured products market,’ Lippmann said on the sidelines of the Milken Institute Global Conference… ‘The consumer is in much better shape than corporates. Consumers are less levered than they were pre-crisis. Corporates are more levered than they were pre-crisis, and I think structured products are not going to be the epicenter.'”

I also doubt that structured products will be at the epicenter of the next crisis. Subprime, mortgage Credit, and Wall Street Alchemy were the nexus for Financial Arbitrage Capitalism period excess. Government Finance Quasi Capitalism fundamentally altered the prevailing Financial Structure financing what is now one of the U.S. history’s longest expansions. [Doug Noland]

http://creditbubblebulletin.blogspot.com/2018/05/weekly-commentary-old-roach-motel.html

Circumstances seem to shaping up as a redux of the 70s, where stagflation became a wedge between corporate and consumers common interest. We learned to shop for generic products in warehouse stores. So if corporations do have pricing power to what end will it be if consumers are tapped out?

The story with corporate debt is very simple – thanks to central banks the past decade has been a gargantuan debt-for-equity swap exercise carried out by corporations.

Works great as long as the economy is trending up and interest rates are low. Once either of those start turning though it’s game over since it’s okay for equity to fall but debts never go away except in bankruptcy. This will probably be “the story” of the next recession, like real estate was the story of the previous way.

As for consumers, they are not quite in as bad of a shape. Remember that the figures in the article above are in nominal, not constant/real dollars. If you adjust for inflation, with the possible exception of student loans, the situation is really not that dire.

Indeed. I agree that student loans really, really stand out.

I suppose the student loan data seems like it might be another sign the job market is tougher for some folks than the headline number suggests. Why so many people racking up student loan debt? I really don’t think it’s solely tuition inflation because that’s been nuts for years and years. The student loan debt explosion seems more recent.

It’s a pointless arms race. Person A gets a job in a a position that does not require a degree over person B who doesn’t have a degree. Well, now person B feel they should get a degree… then person C, then D, etc…

In the meantime a lot of kids end up wasting a lot of time and money on useless degrees and the taxpayer is on the hook for many these loans, either through some kind of forgiveness program or an effective default.

Thanks, Ambrose. And thanks to James Levy. Excellent comments, imho. Actually, all of the comments have been pretty sober.

P.S. I have a copy of “The Devil’s Dictionary”, Mr. Bierce. Painfully good reading.

My pension fund is offering a buy in program, and what it says to me is, I can invest money I have languishing at still historically low rates, in order to preserve my current benefits. On the face of it that seems like a dilemma, but I used the same logic to buy a solar system ten years ago, which returns about 5% a year on the investment. Call it inverse leverage if you like. Consumers have choices, and in the 70s there were a lot of good investments, though very few of them were stocks. College students become teachers to pay off their loans. The national walkout is raising pay, pretty soon you will need a Masters degree to teach preschool. Inflation in higher education will migrate down the ladder, and while teachers make more, they pay more into their pension funds.

Yup, I thought the same thing about the walk out, it is effectively those who have it earlier closing the doors on those who come in later. It is a very good tactic of pulling up the ladders after you have used it.

Years ago when I was at university in the 70’s textbooks were expensive and the practice was to sell them after the end of the course. (Do people still do that?

(So maybe they still have the expensive textbook scam? That assumes students can actually read!!)

When the kid was going to university here in Oz the situation in regards to textbooks was the same. Really expensive and usually ended up costing me a huge bundle every semester.

It’s worse than it used to be. The publishers update the books regularly so often you CANNOT sell them back. :\

(because you need the right problem sets, which are only in the latest edition)

Not only that, they make a slightly different version for each large college so you cannot buy a used one on ebay or amazon.

Oh, you mean like mattresses?

Now the textbooks contain on online component that requires a log-in code; buy your textbook used, you don’t have that, and you’re frozen out of a portion of a class. I teach an online course with this problem; students don’t have money to purchase the new book, the publisher refuses to make the code available to them.

As an older millennial who mostly snuck through a 4 year college before prices kept rocketing up, the cost of college will keep rising unchecked simply because the loans are available for vast amounts of money.

And the previous generation, our parents, raised us in an environment that basically said the measure of your success is how good a college you get into. With zero concern for how much they cost, because you can always get scholarships and loans. In the end it will be worth it they say…….

For the majority of us, only once we are out do we realize this is mostly bullshit. You can get higher education within your means in many cases. And status can but not always gives way to talent and hard work.

Many parents will now bitch that, kids are so expensive to raise, with the cost of college and all…. Then they look at you baffled when you say you might not kill yourself to pay for a full 4 year private education. How can you say no to your child dreams?

“How can you say no to your childs dreams?”

I seem to recall George Carlin mentioning something about ‘dreams’ .. of the American kind ..

Show THAT skit to the kiddies, and I’d betcha they’d get it in a heartbeat !

George Carlin cracked the code and spoke truth to power. “It’s a big club and you ain’t in it.”

https://www.youtube.com/watch?v=acLW1vFO-2Q

IMO too many people are going to universities and getting degrees that are worthless.

Worthless in the knowledge that they supposedly learn, worthless because to be perfectly frank, many people are really too dumb and should never go, and worthless because there will never be a positive payback of all the costs involved.

And what is even worse is that many of those getting basic degrees go on to get higher degrees and end up teaching and should never, ever have been given a position where they can influence young people.

Too many PhD’s in ridiculous subjects and qualification inflation.

in twenty years, an entreprenerial type that knows how to successfully operate a screwdriver may be able to live like a 1950’s era union plumber at the rate things are going.

My neighbor just had a plumber come and change his bathroom faucet.

$125.00 per hour folks. The AC guy is 145.00 per hour. That is what a good lawyer got not even ten years ago.

The Blind leading the Blind.

I went to parents day at my daughter’s HS. Her HS is rated well nationally. I would cringe when her teachers would make mistakes in grammar.

This stuff just gets passed along.

The tuition per semester when I paid for my MBA was something like US$2000 a semester.

Last time I checked the cost to complete the degree – just for tuition and fees had increased to something around US$75,000. Add in all the other costs such as books, food, housing, and everything else along with the foregone income during that period of time and you are probably looking well past a quarter of a million dollars now………………….

Oh, can I get a refund at current prices?

I looked at getting a PhD about 15 years ago and then sat down and did an analysis of my age, benefit, payback, cost and effort. Decided it wasn’t worth it. It was an easy decision at the time. It’s a good exercise to do for any major decision.

Stop learning? Not likely,….just finished obtaining my amatuer radio license and now belong to our local Regional District emergency prep team. Lifelong learning for its own sake is free:-)

As a good friend once said, “When a person finally leaves work behind, it is just like pulling your hand out of a bucket of water. It’s as if you were never there”.

The kid has one year left on her PhD and is doing quite well with writing her dissertation.

She’ll be debt free from any school loans (thanks to daddy!) too.

In her field the only way to get a better position was to get a PhD and hopefully she’ll be able to get a decent job once finished. Demand is high and salaries are good too………….

Congratulations, Paulo!

I also have an Amateur radio license and have formerly volunteered with ARES. I also spent a couple of hundred dollars to obtain an EMT certification. Not much money in volunteering but it is my goal to return after I retire.

I will continue lifelong learning long after I retire.

Good to see someone write about the circular nature of tuition price increases and the availability of student loans. Many schools owe their existence to the easy money.

In the first graph, net of student loans, my take-away is that the consumer has been reasonably cautious. Student lending accounts for a very large portion of the overall increase in consumer debt.

It is already a drag on other parts of the economy, but will prove very useful in buying future votes. Ironically, the “educated” will jump at the chance to vote for those promising relief and will not connect their suffering to its root causes.

Wolf, I really appreciate your charts but I do wish that you would also include inflation-adjusted figures in most of your graphs that represent dollars (perhaps using a line indicating constant dollars set against the bars you use now for nominal dollars).

Unfortunately, thanks to our loosy-goosy central banks one trillion of 2007 is not the same as one trillion of 2018.

That’s why I indicate CPI changes along with the charts to give you a feel. You can then ballpark the math.

Ideally, these types of debt charts should be indexed to wage inflation of those people who have this debt. For example, credit card debt. High-income wealthy people might not have a lot of credit card debt since they’re likely to pay off their balances every month. But some people in the lower 60% of the income spectrum have a lot of credit card debt, and their incomes are precisely the incomes that have not seen much if any wage inflation. And it’s wage inflation that matters to debt service, not CPI.

Holy Moley ! Tripled in 12 years !!! (2006 – 2018 $500B to $1.5 T)

We can only hope they don’t realize the toilet paper their College Degrees are written on is worth only that much in the real world of business as college these days doesn’t teach subjects of much worth anymore. BA’s and MA’s working at McDonalds, Borders, and Starbucks, while they wait for their resumes to be answered. Maybe if the preponderance of ‘students’ didn’t have ‘paper writing’ services write most of their class papers for them, they might have a shred of credibility with employers who know what is really going on in colleges today.

Living in a State University Town, I have seen the student housing boom and the rise in administrators’ pay and the increase in number of administrators. Schools now have a V.P. of everything.

The housing demand is driven by students demanding luxury living while in school. Here comes the “in my day” part. In my day you lived in a concrete block apartment complex that looked like everyone else’s apartment. You swam and sunned in the apartment pool, if you had one, or the school’s pool. Your complex didn’t have a full on spa.

Another point regarding student loans, a fair amount of that loan money finds it’s way into swanky spring break trips and other entertainment venues. So, before we start forgiving student loan debts, figure out a way to parse out what actually was spent on education costs. I don’t feel obligated to send other people’s kids on spring break cruises to Cancun.

I agree with others that think a for lot of people college is a waste. $100k in debt and graduating with a liberal arts degree that gives you no real skills. I felt I wasted a ton of time in college on stuff I never used. I hated most of it, and did it just because I knew I need that piece of paper. Honestly I’ve never used more the I learned in high school (ability to write, basic math, ability to read critically). And I worked in the corporate world and had a small business.

I think for specialized careers like doctors, lawyers, some types of engineers college is still needed. But not as much for everyone else. I think we should transform our community colleges and align them closely with the private sector. So kids can come directly out of high school and get the EXACT skills they need to get tech jobs and skilled jobs. The latest and greatest. Even software engineer jobs Instead of wasting 4 years on stuff they will never use.

I also think more practical skills should be emphasized in high school in college. I have gotten SO MUCH more out of skills I taught myself like investing, personal finance, starting a business, health eating skills…NONE of this is taught in schools! Yet is so much more important to your life! Instead I learned a ton of worthless stuff I never, ever used once and never remembered once the class was over.

But there is a lot of people that get rich off the status quo, and academic institutions will lobby and smear attempts to change this outdated education system we have. So they can keep stuffing their pockets.

“Lenin is said to have declared that the best way to destroy the Capitalistic System was to debauch the currency… Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million can diagnose.”

— JM Keynes, ideological godfather to the Keynesian currency debauchers at the Federal Reserve

It’s a dirty job, but some’s got to do it.

It would be interesting to see what these graphs will look like with mortgage debt added in. I can imagine it will look even uglier than it is now especially the so much FOMO sentiment in the market, low to no interest downpayment back on again. People are once again feeling comfortable buying houses they simply cannot afford unless it’s loaded with debt.

The converse to this is if you major in a STEM field from a decent school and have a decent head on your shoulders, you’ve got the world by the balls.

Employers all over the country will compete to hire you straight from college at $100k+. Or you could continue on in school and further specialize, and command even more money on graduation. Play your cards right, when you’re in your early 30s like me, you will have no debt and a very comfortable life. It’s not all bad, provided you understand the game.

Also, for god’s same, knock your gen ed courses out at a community college the first two years at 1/3 the price of real college. After graduation, no one will ever ask or care where you took anthropology 101 or intro to film 104…

Mark,

If you are brilliant, you may have a chance. Otherwise, STEM is being destroyed by H1B. If you get into the field as a new or recent grad, your chances of a lifelong career are slim unless you are brilliant, or maintain the political connections to get into management and stay there.

The 40+ year old IT worker is a target now. if you are a 50+ IT worker, your chances of a new job are very slim. Pro Publica recently had an article on the subject as practiced by IBM, and this practice is widespread.

I’ve been in IT for 30+ years and the only reason I’ve survived this long is I’m very good at what I do.

In all financial transactions, there is a debtor and there is a creditor.

When a debt is not repaid, the failure to repay gets imposed on the creditor.

People who think that unrepaid carries no cost are either stupid or willfully ignorant.

Every debt costs. Whether or not it gets repaid or is unrepaid.