Subprime is calling.

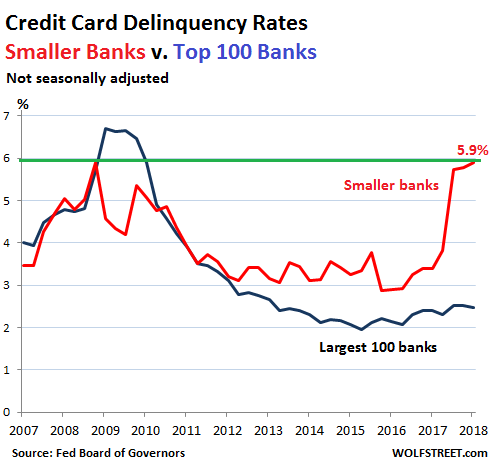

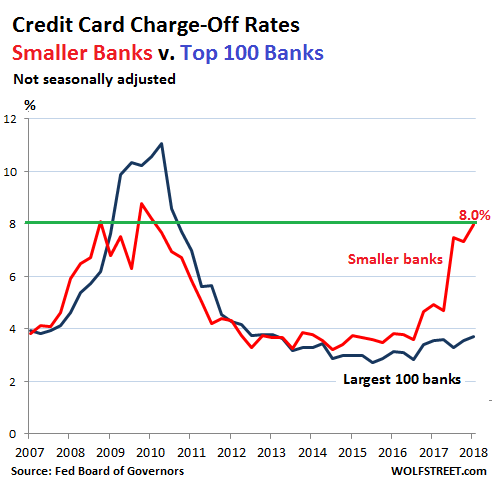

In the first quarter, the delinquency rate on credit-card loan balances at commercial banks other than the largest 100 – so at the 4,788 smaller banks in the US – spiked in to 5.9%. This exceeds the peak during the Financial Crisis. The credit-card charge-off rate at these banks spiked to 8%. This is approaching the peak during the Financial Crisis.

A sobering set of numbers the Federal Reserve Board of Governors released this afternoon.

But overall, across all commercial banks, including the largest banks with the largest credit-card loan balances outstanding, the delinquency rate was 2.54% (not seasonally adjusted). This overall rate was pushed down by the largest 100 banks, whose combined delinquency rate in Q1 was 2.48%.

These large banks have been offering appealing incentives to consumers for years, and they’ve been going after consumers with the higher credit ratings, and they’ve been following good underwriting practices – having not yet forgotten the lesson from the last debacle – and this conservative approach is now helping to keep losses down.

But the thousands of smaller banks couldn’t compete with those offers, and so they got deeply into subprime cloaked in sloppy underwriting. This way, they were able to reel in new credit-card customers that the big banks didn’t want, and those customers needed the money and charged up their new cards in no time, and the interest rates of 25% or 30% looked good on the banks’ income statement and helped maximize executive bonuses, yes even at smaller banks.

But turns out, those banks had reeled in the most fragile customers and had eagerly doused them in irresponsible levels of debt at usurious interest rates – and now what? These customers won’t ever be able to pay off the balances or even pay the interest. For many of them, there’s only one way out. This caused the delinquency rate to spike from 3.81% to 5.90% in just three quarters.

This chart shows delinquency rates for the largest 100 banks (blue line) and for the remaining 4,788 banks (red line):

Credit card balances are deemed “delinquent” when they’re 30 days or more past due. The rate is figured as a percent of total credit card balances. In other words, among the smaller banks, nearly 6% of the outstanding credit card balances are now delinquent.

The bank tries to collect these delinquent loans, and some customers are able to catch up. Others are not. After recovering what it could, the bank moves the remaining delinquent balance out of the delinquency basket and into the charge-off basket. This is when the loan is “charged off” against loan loss reserves.

These charge-offs among the largest 100 banks rose to 3.73% in Q1 (not seasonally adjusted), the highest since the first quarter 2013.

But among the remaining 4,788 banks, the charge-off rate spiked to 7.99%, the highest since Q2 2010. The rate among smaller banks had peaked during the Financial Crisis in Q4 2009 at 8.78%:

Both charts show that the largest 100 banks had suffered massive losses during the Financial Crisis as their credit card loans blew up, and as consumers, many of whom had lost their jobs, could no longer keep up with their credit card debts.

The smaller banks had been more conservative leading up to the Financial Crisis, and their delinquency and charge-off rates had been somewhat less catastrophic.

The difference between then and now is that back then, unemployment was heading toward 10% and millions of people had lost their jobs; now the unemployment rate is near historic lows and the economy is humming. Yet already the smaller banks are booking these losses on their credit card portfolios. What will they do when the economy ever slows down?

That was a rhetorical question.

In the overall scheme of things, these 4,788 smaller banks hold only a small portion of all banking assets, including credit card balances. Of the $1 trillion in credit debt outstanding, these small banks hold only a fraction. So they won’t jeopardize the US financial system. And that’s why the Fed, as banking regulator, is relatively sanguine about these dizzying charge-off rates at the smaller banks.

But the surge in charge-offs at these banks points at something fundamental: Credit problems at the margin. The consumer spending binge in recent years has been funded not by surging incomes at the lower 60% of the wage scale, where real wage stagnation has reigned, but by borrowing – particularly via credit cards and auto loans. Both of them have turned sour at the margins. And these are still the best of times.

Only about half of retail is under attack from e-commerce, but that half is getting crushed. Read… Brick & Mortar Meltdown Pummels These Stores the Most

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Making delinquencies great again!!!

Perhaps not being able to refinance your home without raising the mortgage rate

has slowed HELOC’s which in turn has hurt credit card repayment.

Sounds reasonable.

Could also be the repeal of the Healthcare Act

Which is less of a hassle, getting harassed for student loan delinquency or credit card debts ? I’m thinking letting the credit cards slide is better than letting student loans and/or car loans slide. I guess those will come next.

You can’t charge off student loan debt. You can charge off credit card debt. Some people have figured that out and used it to their advantage….

I get it. Wonder how many folks are using CC’s to get out from student loan debt ? If you’ve got nothing, you’ve got nothing to lose ?

If my friends were eliminating their student debt with CC’s then I may jump on that bus too………………..

I received a solicitation today and just put in the shred stack. One thing I have noticed in many of the articles regarding these different subprime loan products is the observation that they are too small to derail the greater economy. (Sorry for the long sentence) But what if they start a domino effect, or reveals that some other parts of the economy aren’t as strong as we have been given to believe?

The US financial system has been if not exactly strenghtened at least compartimentalized over the past decade to make sure when subprime does what it periodically does damages are limited to “specialized lenders” such as those small banks specializing in all sorts of risky loans.

In short the big US banks have little to fear.

Europe is another matter completely, but that’s another story for another day.

Except for the fact that the big banks are investors in the new finance companies that have big exposure to risk.

√

The top 100 US banks have from limited to very limited exposure to subprime credit, either directly or indirectly, they have reduced it steadily from 2011 onward.

As said, they have learned their lessons, unlike their European counterparts.

Of course this doesn’t mean they don’t face other big problems: Wells-Fargo’s continuing cavalier attitude towards their customers is going to lead to some huge lawsuit down the road, a lawsuit Wells-Fargo will either lose or be forced to settle out of court to the tune of billions of US dollars. And perhaps criminal charges will be pressed, who knows.

There’s a lot of wishful thinking around about a “meltdown” of the US financial system and make no mistake about it: over the next few years a lot of these small lenders are going to discover not merely that risk still exists but that they have priced it completely wrong. But right now there’s no Lehman on the horizon.

Personally I remain convinced if you want a big financial crisis (for either profit or schadenfreude) Europe is the place you should keep an eye on. The Austrian and Italian banking systems in particular are more broken than they were a decade ago and are primed for another and bigger meltdown.

It reminds me of what Greenspan used to say about the US financial system cca. 2005 or was it 1999? And I believed he knew what he was talking about, then.

If there is any lesson from 2009, prime quickly becomes sub-prime.

I wish you were right, but that doesn’t let me sleep better, at least until we test a recession without reverting to massive printing.

I agree that Europe is behind the curve.

There are so many little factors like this that keep me believing that the real economy hasn’t been growing as much as they say it has. For people in the bottom half of the payscale it’s a death by a thousand cuts economy. After graduating college and working my way up I had to live with my parents for awhile as I couldn’t afford rent and to pay my student loans and other bills. I was making money on the low side but had a lot of upward potential and kept thinking once I made this much or that much I could make it on my own but once getting there found that it didn’t buy me as much as I thought it would. I kept getting raises and I’ve gotten to the point now where I’m making a good sized premium over median wages and yet my pay does not afford me a lifestyle anywhere close to what I thought it would 5 years ago. I look around me and I’m just saddened by how I know so many of them are living on the edge. Whenever the economy rolls over, and I’m confident it will due to all the bad investments that seem literally everywhere these days, it just seems like the American way of life will be shattered in so many ways. Biggest prediction for the next decade between struggling indebted millennials and disappearing retirement funds for the boomers is the large scale return of multigenerational housing. It’s already happening but it’ll be way more prevalent. Dysfunctional families should be wary of homelessness.

I’m thinking the same thing, explain the unemployment rate though?

How does the employment rate metric account for people who have stopped looking for jobs, working part-time, perhaps multiple part-time jobs, jobs without benefits, or jobs paying so little the worker qualifies for food stamps and other categories besides what most of us think of as gainful employment? Some of that is considered under-employment, but my point is that a low unemployment rate may be far from describing many workers’ and would-be workers’ experiences.

I’m with you mean chicken and rhodium, i think that’s why uber grew so big, few promising jobs =gig economy ,and people cant afford cars theyl equest uber, interest levels stayed low at historic levels something does not jibe

Rhodium – I feel like I dodged a bullet. Yes, I was stupid and went to college, that’s money I never earned back and time I lost permanently, and had $10k in student debt, but in the mid-80s there were still such thing as electronics technician jobs. I started at $9.50 an hour and in a few years was making $11.50 an hour. That’s equivalent to something like $27 an hour now.

I had no idea what was coming. I had my own cute little apartment not too far from the beach in Costa Mesa, had motorcycles, ate lots of restaurant food, and in general goofed off and has as good a time as is possible when you’re working lots of overtime.

I also made my loan payments right on time. One time, I moved and got no student loan bills for a few months. They finally found me and called me at work, and I owed about $900 to get caught up, and I told the lady on the phone, “OK I’ll write you a check” and I think I heard her fall off her chair on the other end. She was certainly surprised.

I mean, it was great. You could be working class and live on what you made. I thought I was poor, and had no idea how bad things would get. If I knew what was coming, I’d have saved, saved, saved. Looked at buying any kind of house I could possibly buy, etc.

The reason I feel like I dodged a bullet is, I’d paid down half of that $10k when the economy turned sour, but the last of the electronics technician jobs were going “poof!” and I was out of work. But an inheritance came through that enabled me to write a check for the balance so I didn’t end up with student loans haunting me and growing exponentially.

You’re not alone in feeling that you are threading water, and feeling helpless about the future – if that is any consolation.

“the unemployment rate is near historic lows” : I’m quite interested in the definition of “employed.” Does this include people in the “gig economy” or those who have a “job” or “contract” but are effectively underemployed. Those with precarious employment situations are on the knife edge of suddenly being unable to pay off their credit card debts. They probably use their credit cards to even out the lumpiness of their income stream and thus have no buffer at all. 30 days seems real short under those conditions, even for the larger players if some “gig economy” hiccup happens. A percentage breakdown of the different classes of “employed” would be most interesting but probably quite hard to get.

If you sold something on Amazon or eBay last month, and you made $1.20 profit, then you are employed.

No!

There are 6 unemployment and underemployment indicators that the BLS publishes, U-1 through U-6. U-6 is the broadest and deems part-time workers who want to be full-time workers as “underemployed.”

There are well-defined definitions for each unemployment indicator. A friend of mine, a retired Doc, is riding his bicycle across America right now. He has no intention of ever working again. He is NOT “unemployed” — because he is not looking for a job and doesn’t want to have a job.

Many baby boomers are now retired and don’t ever want to work again. They don’t count as unemployed. College students who don’t want to work don’t count either. Homemakers, male and female, who don’t want to work don’t count. There are many people who don’t work because they don’t want to work, and thus they’re not “unemployed” and they’re not in the work force either.

And when a retired person sells one thing on Amazon that doesn’t make that person unemployed or employed. That person is still not in the workforce unless he want to have a job.

Wolf,

Does any of those U1-6 calculate just the amount of people of working age that have no job and are not in school.

Say ages 18-65?

Ignoring the interest in the quest for work.

Just plain number of people simply out.

It goes like this (simplified):

Working age population = anyone over 16 until they die.

Laborforce = anyone in the working age population with a job or wanting to have a job (this EXCLCUDES retirees, homemakers who don’t want a job, students who don’t want a job, etc. These folks are not in the laborforce)

Unemployed or underemployed (U-6) = anyone in the laborforce who is looking for a job (this is specifically defined) and doesn’t have a job, or who is part-time employed but wants to be full-time employed.

This measure is survey based. It’s what household are telling the BLS on the survey.

“This measure is survey based. It’s what household are telling the BLS on the survey.”

This is where America goes wrong, or perhaps deliberately manipulates the #.

Ours go off tax payments, If you are not paying, fortnightly, monthly, or bimonthly, income tax on earnings, listed as a non tax paying spouse, or receiving an unemployment, retirement, or invalids benefit benefit. WHY (instant IRD/IRS TARGET).

Which makes it very easy to track unemployment, and under employment, as part time work has a different earner tax code and rate, to full time work. Part time workers go in the under employed box as many of them also draw a partial unemployment or other assistance benefit.

This gives much more accurate and almost daily comparable employment data. It makes it much harder for the fattening girls assistants to hide the truth, as that data, is publicly available information.

I’m curious whether anyone on this site ever participated in a BLS employment survey? If not, I wonder if the survey is valid. I’ve never known anyone involved in such survey.

I have. I have been subject to several types of these government surveys.

When you get notification in the mail that you’ve been selected, they also tell you that you MUST complete the survey. This is NOT voluntary. Which makes the sample more valid because it removes some of the selection bias.

Then you go to the website they provide and you insert the code they gave you in the mail and you answer lots of questions. The questions are pretty good.

Just now, I got one for my little company (Wolf Street Corp) from the Commerce Dept’s “Economics and Statistics Administration.” It says as always in all-caps: “YOUR RESPONSE IS REQUIRED BY LAW.” And my responses will be kept “strictly CONFIDENTIAL.” This one is for the 5-year census.

It also says: “We estimate that the survey will take on average between 42 minutes and 5 hours and 36 minutes to complete depending on your principal industry classification and business activity.”

My deadline is June 12. I haven’t done it yet, but I know from other surveys, they’re fairly impressive in terms of the questions, and the online format is easy to navigate, but it’s still not how I would like spend a Sunday afternoon :-]

The household survey (employment) wasn’t that complicated but I don’t remember the details.

Bobber,

Yes, I just completed a survey and mailed it yesterday. Businesses are randomly selected by the state Department of Labor to collect statistics on their employees. When you run a business you will periodically be contacted by various agencies of the state and federal governments for data collection. I guess in theory you could fudge the numbers on the survey, but overall I would say the stats they collect are accurate.

I would want to have a job if the pay was right, but I was downsized into retirement.

Ambrose Bierce,

So this is something to think about when/if you get the household survey that creates the data for the unemployment rates. It will be up to you to answer this correctly so that the national averages reflect it :-]

Wolf, what’s your take on John William’s Shadow Stats? Is his assessment of true unemployment fair, do you think. I have used his work in my book, so maybe I am incorrect.

I like your clear and concise explanation above and it got me thinking – Opps!

Austrian Peter,

William’s stuff is based on current data from the government, but his formulas make this current data look a lot worse. That’s all he does. He doesn’t have his own data. It’s a pure joke. And he is having fun doing it! So that’s great. But take it seriously at your own risk.

I do think that you have be careful with employment data and similar data: you have to understand the definitions to understand what the cited results mean. Unfortunately, this isn’t done in the media. So we read 3.9% unemployment and take it as an absolute value of how many people don’t have a job in the US. This is very misleading. The data is good, but you have to know what it means.

Wolf,

You are correct. Many people in the ALT media think that the people who are “Not in the Labor Force” category are unemployed workers and that they should be included in the unemployment rate when the fact is most are retirees, high school and college school students, stay-at-home moms and disabled persons. Sure, there are a few million that are considered “long-term discouraged workers” that should be included in the government’s unemployment rate but are not. So the unemployment rate is probably somewhere around 10 percent, not 22 percent like ShadowStats says or 42 percent as David Stockman says. I am glad to see you know the truth which is not really hard for anyone to see.

Thanks JM, I am getting a clearer idea of how the stats are presented thanks to Wolf and other contributors. I am grateful for your patience – learning takes alittle time and some humilty too.

It would be useful to compare what “unemployed” means in the industrialized world to have a better idea. I am not talking about the prison population in which the US is a per capita leader, nor the armed forces, another unemployment obfuscator.

The only useful definition of “employed” is if the income from the job can support 2 adults and 2-3 children, with enough remaining to save 10-15% after expenses.

That would make for an official unemployment rate of over 50%!

Yes, I am sure it would be an embarrassing number for the government to publish. Obviously the figures would vary depending on the cost of living in each metro area, but the prevalence of dual income households is a symptom of a larger problem in the economy.

Debt Free,

Well if that was the case then my father was unemployed for 20 years since he had to support 2 adults and three children and was unable to save 10-15% after expenses. It was not until his children grew up that my father could save any money. I am glad we do not measure unemployment your way.

My comment is a criticism of our policy makers that do not seem to care that the economic system generates loads of low value-added service jobs but few high value-added capital and consumable goods producing jobs. The relatively few high paying jobs out there seem to be weighted heavily towards the rent-seeking sectors, FIRE and healthcare predominantly.

I think that Debtfree was inferring that employment (wages) in our day (1950-60s) allowed one breadwinner to provide adequately for a family of a wife plus 2 children and still be able to save 10-15% after all living costs. This condition for the majority may be defined as ‘adequately employed’.

We now find ourselves in an employment situation in which, with two people working, often with more than one job, hardly produces enough income to meet expenses without resorting to supplementing shortfalls with credit cards et al let alone save any money at all.

The conclusion must be that for the majority of working age people today income has gradually deteriorated over 60 years and our standard of living is inferior to that of former generations. And there is no sign of improvement.

I am of the ‘blessed’ Boomer generation; the only one in history that earned more than our parents and now have an income generally higher than that of our children. Thus indicating that something seems to be wrong with the economy as 60% of the working population are going backwards.

Borrowing at 1%-2% from the FED or %0.1 from savers, and lending at 25% or 30%; you got to love banksters; absolutely no shame.

The overall average APR is closer to 16% + interchange fees + other fees – funding cost – credit losses – operations – marketing – fraud losses = X% . X is generally 2%-3% and lower depending on where we are within the credit cycle.

Here’s a big embedded cost … some cardholders with higher IQs spend high amounts, say $50K/yr and pay the balance in full each month. So they get a continuous interest free loan, plus “rewards”, often 1-1.5% of spend ($500-$750/yr). My Amex card actually pays a 6% rebate on grocery.

So there is no reason not to actually make money using your credit card, plus enjoy other benefits such as chargeback rights, insurance, etc. It all comes down to people having the initiative and motivation to make good choices. Yea, I know that statement will drive some crazy.

Oh FFS. If You would read your own writing you would understand that it also comes down to having $5000 a month cash that you can use to pay off that credit card debt every month. The benefits you mention are available in significant amount only to those who are already wealthy. As is so very awesome of the case. This has never stopped anyone yet from from congratulating themselves on their virtue and genius.

Hey before the crash even I had $5000 a month cash.

This is what I do. I’ve never paid a dollar in interest or fees to the credit card companies, and I’ve collected thousands of dollars of free airline travel over the years. Just charge everything you can and pay the balance off in full each month.

The fees to merchants from everyone using credit cards over cash probably drives up overall purchase prices 2-3%, of course, you get that money back in the form of rewards if you know how to play the game.

Excellent advice – I hope my children and grandchildren take notice!

But what am I supposed to post on Instaface if I can’t charge up my cards and party in Cabo?

Deadbeat Nation, courtesy of the moral hazard created by the Fed and the culture of fiscal and lifestyle irresponsibility promoted by the Wall Street-owned Republicrat duopoly.

There are record levels of debt in all categories. This is what happens when the productive part of the economy dwindles to a hollow shell while the rent-seeking part grows like a cancer, fighting over the remaining scraps of true wealth while creating nothing. In such a situation it is not surprising that wealth flows to the top. The top 10-20% of the wealth spectrum is where the rent-seekers live in modern America. This is not too hard to figure out. All joking aside, many in the lower classes try to emulate the lifestyle of the top 10% rent-seekers by buying on credit. And the topic of the article is the result, in its early stages, likely to spread to auto loans next.

GFC II may very well spiral up from the bottom.

It may, in fact, be very close indeed now, so prepare.

Those at the top, and most financial commentators, are reading carelessly from the wrong instruments, with false assumptions, and do not realise how precarious the situation really is.

This indicates, that the inflation that does not exist combined, with the wage deflation and underemployment, that also does not exist.

IS biting those, who can afford it least, at the margins, NOW.

So.

Unless there are real wage increases, and real employment increase, REAL problems are not far away in America.

Okay so according to your numbers they’re still coming out ahead. Delinquency of 8%, but interest of ~20% (“25% or 30%” according to the article) on the remainder is still net positive. Are they losing money or not? And if not – well then party on!

EDIT: meant charge-off, not delinquency

It dosent take long for those growing charge-offs, to eat that usury based, profit margin.

ZeroBrain,

Because the risks are high on subprime-rated borrowers, banks charge a lot of interest, with the idea that overall, they’ll come out ahead. They might, and they might not. But the timing is different.

Banks accrue the theoretical interest income every month, even if the customer makes only minimum payments, which may not cover all of the accrued interest. At some point after the customer defaults, but not immediately, the banks stop accruing interest income on that loan. And eventually the bank writes off the unpaid balance. This charge-off amount includes the interest income that the bank already accrued but has not been paid and that is embedded in the loan balance (minimum payments may not cover it all).

The bank writes off in one day part of the income booked over the prior months or years on this card, plus the principal of the loan. Whether or not the bank lost money on this credit card over the card’s life depends on how much in interest the customer actually paid with the monthly payment, in relationship to the total loan balance that was then written off.

Overall, it’s tough for the bank to lose money in this environment because it also makes money from other sources – mortgage loans, auto loans, business loans, etc. And its cost of money is still very low. So banks are very profitable right now. That’s one of the reasons the Fed keeps an eye on it but is not reacting to it. It’s going to let this play out because it won’t dent the big banks and will unlikely take down the smaller banks (though some could lose money because of this).

The Fed is more worried about commercial real estate loans which are concentrated at regional banks (below $50 billion in assets). And these are big loans; and if one of them goes bad, it’s a hit; but when 10 of them go bad, they might take down the bank.

I think the point is not that payments that the delinquent previously made at that high interest rate will cover the cost of his default, more that the payments made by those who have not defaulted will make up for those that do (and then some). Obviously you know this — I just don’t understand the significance of the bank taking a loss on any given borrower when the aggregate is what is important to its bottom line. Of course, the bank has to hope that its interest rates are set high enough — and that enough borrowers don’t default — to keep that bottom line in the black.

This divergence is unusual and it is surprising that the small banks would have lax underwriting. Delinquencies overall for the entire $1T in card balances are rising, but up from very low levels, i.e. nobody is overly concerned.

If the small bank average APR is indeed 25%+, then they maybe getting adverse selection. Large card issuer APRs are much lower.

Yes, that “adverse selection” is part of the problem. They can’t compete with the offers the big banks are making. The big banks then sort through the applicants and take only those they want and that fit their underwriting requirements. Smaller banks, which cannot offer the rich benefits big banks are offering, then appeal to borrowers that were rejected by the big banks.

What if you bought bitcoin with your credit card and defaulted, can the banks get your bitcoin?

Credit cards are unsecured personal loans. So no, the banks don’t automatically get the purchased item after you default.

But they can sue you for the deficiency. And after they obtain a judgment, they get whatever assets they can extract from you. This may include wage garnishments and anything you have in any bank accounts or crypto wallets.

Gold? I can buy gold with a CC

My local Canadian coin shop told me that I cannot pay for gold bullion coins with a credit card.

(seems obvious to me why that wouldn’t be allowed)

Gary – can’t one take a cash advance on a credit card? The end result would be the same.

yes, very easy to do it, ebay, gold dealers.

If they sue and you have no job,no assets in the USA then they have nothing to extract from you? Can they go after your house and car for example?

This depends on the state. That’s as far as I’ll go. For the rest, you need to ask a bankruptcy lawyer :-]

Are banks able to secure judgement against your house and car? If you have no job, no financial assets within the USA but do own assets in another country then there is not much they can do. It happened to a friend of mine, no USA assets but owned property in Australia and had some investments and bank accounts there, the credit card banks could not collect a thing from him. I think they cant go after your house and car , am I correct? Thank you

“I pay my Visa with my Mastercard”

(bumper sticker)

You can’t discharge student loans in bankruptcy.

Makes sence to repay student loans with Visa & Mastercard then roll over and die (financially).

All I know is my wife and I received no less than five promotional mailings from banks yesterday, all of them offering a credit card, loan, or some other financial product.

I think the banks are back in business, and they aren’t too discriminating about where they get it, just like last time.

If a disaster hits I assume they are counting on more TARP, which would enable them to maintain executive bonuses, just like last time around.

OT: Hey Wolf, your site needs a favicon. I suggest:

https://www.gettyimages.com/detail/photo/wolf-baring-teeth-close-up-high-res-stock-photography/200515507-001

That wolf and our Wolf are 2 different things; our Wolf has sharp financial and accounting teeth :-).

Beware the new outlaw motorcycle gang in town: Hell’s Accountants. They ride around looking for hapless victims to gang-audit.

“Hells Accountants. They ride around looking for hapless victims to gang-audit.”

I understand they are the downtown street level affiliates of the uptown IRS.

Hi Wolf, is there really 4,788 smaller banks in the US? Sounds far too many.

There are 4,888 commercial banks in the US. Minus the 100 largest = 4,788

This is down from 14,000+ banks in 1986 and down from 7,200 just before the Financial Crisis.

https://fred.stlouisfed.org/series/USNUM

And as they kill off the smaller banks, there will be less and less competition for the big banks.

It’s silly (and in the case of Wells Fargo, possibly dangerous) for people to do their personal/private banking at one of the mega banks when there are a many good credit unions around.

and so the smaller banks which are left assume the greater share of subprime CC users, from a Wall St business perspective, you park your bad debt and your lowest decile of borrowers into one off balance sheet entity. Small banks

Oh goody, the 100 biggest banks will absorb the smaller banks that fail and then the “too big to fail” banks will become even bigger “too big to bail” banks………

A couple a years ago was on trip to the US and met up with a group of people. Every single one mid 20s had multiple credit cards completely maxed out. It was sad to see, just about afford the minimum monthly payment.

How pathetic is that? And theses are the people who should be saving every cent to buy a house after the big reset Or multiple houses if they are really smart

“buy a house after the big reset Or multiple houses if they are really smart”

This is the attitude that is behind the big problem.

America has turned a basic necessity into a profit center.

And it has exported that model to the rest of the planet.

Now there are housing bubbles everywhere and large % of the population in those bubble citys, living on the streets.

Thank you America for taking a basic human wright and necessity away from the rest of us who can now never afford to rent let alone own a house. At the same time forbidding us to live on state or municipal land. Thank you for turning the rest of us into tax and interest slaves for life, just so you can live in luxury.

Also thank you America for permeating the attitude that land and housing speculation is and acceptable, and respectable practice.

Rent seeking and gathering is not Capitalism. It is however today the greatest earner in America.

If therE is to be any justice in the next big reset, housing speculators, and housing renters will cease to exist. As will taxes, on owner occupied land.

I think medical debt is unsecured and fully dischargable – I think they can go after up to 25% of your home equity. I’ve had providers offer big (45%) discounts on my out-of-pocket balances. Just book your gold buys as “kidney infection” or even better “total hip replacement.”