Emerging Markets turmoil: The price of cheap debt & misallocation of capital.

“Excess liquidity usually leads to the misallocation of capital, masking any balance sheet constrains. As this tide of excess liquidity recedes, it reveals the misallocation of capital and the mispricing of risk,” Nedbank CIB strategists Neels Heyneke and Mehul Daya write in a note. And this is particularly the case for excess dollar-liquidity in the Emerging Markets (EMs).

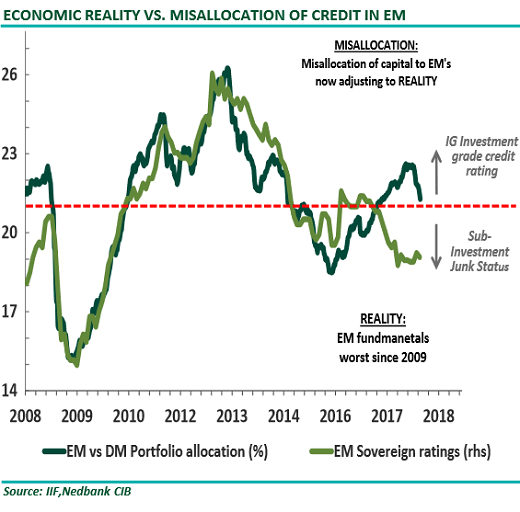

Sovereign credit ratings – such as those issued by Moody’s, Standard & Poor’s, and Fitch – of the emerging market countries have dropped sharply since late 2016. In Aggregate, they’re now solidly into “junk” (below investment grade) and have reached the lowest range since the Financial Crisis. Yet, despite the rising risks, “investors have allocated large amounts of their portfolio allocations to EMs relative to Developed Markets (DMs).”

These investors were induced to do so by:

- Scanty returns in Developed Markets

- Excess central bank liquidity

- The perception that a number of Emerging Markets have made the necessary structural changes to their economies.

“EMs, in particular financial markets, have benefited from this misallocation of credit,” the strategists write. “As the tide of excess liquidity recedes, EMs like South Africa will begin to pay the heavy price of this misallocation of credit.”

In the chart below, the dark green line shows the percentage of portfolio balances allocated to Emerging Markets (dark green) versus Developed Markets. Note how this percentage has surged starting in early 2016 and how it recently has begun to recede – the outflow of the hot money.

The strategists write:

One way to monitor the ebb and flow of excess liquidity is by analyzing the changes in the value of the USD. As long as the dollar remains the reserve currency and most of the foreign owned debt is denominated in US dollars, for example in the carry trade, the dollar will remain king.

A weaker dollar and a supply of low-cost dollar-debt is associated with a stable global environment. And a stronger dollar, they note, “is usually associated with volatility and a risk-off phase as liquidity contracts.”

Since the beginning of 2018, borrowed dollars have gotten more expensive in the EMs – and hence “scarce” – as investors that were chasing yield in the EMs are suddenly having second thoughts about the risks associated with these adventures.

In addition, trade tensions between the US and the EMs have added to those risks for EM investors. Credit growth in China has slowed. And some commodity prices, which are crucial to some EMs, have declined.

In addition, the Fed is accelerating its QE Unwind, which has the effect that the market now has to absorb the Treasury securities that the Treasury Department is issuing, and the Treasury Department is issuing ever larger piles of them. With US yields being higher – and more attractive – they’re drawing liquidity from riskier EMs.

In addition, other central banks are backpedaling on QE. The ECB, which already tapered its QE program to €30 billion a month, will taper it to zero by the end of the year. And the Bank of Japan has changed its approach as well.

“Except for an expected short-term reprieve, we expect these tighter USD conditions to remain in place for the rest of the year,” the strategists write. “That is unless policy makers react soon to stimulate financial markets with liquidity.”

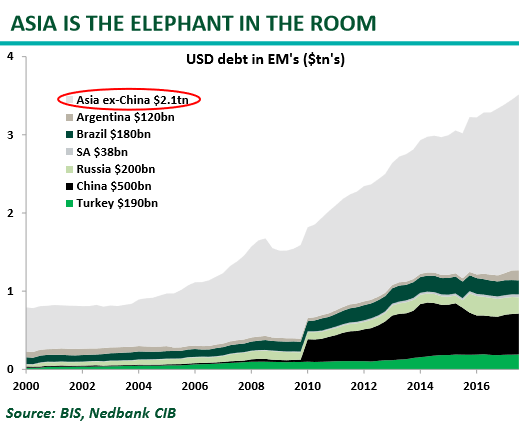

“Asia is the elephant in the room.”

“Southeast Asia stands out again as in 1997/8, with a large amount of USD denominated debt outstanding,” the write. “The only difference is then Asia had fixed exchange rates and now they are floating! We believe Asia will be the next source of downside systemic risk for financial markets.”

The chart below shows dollar-denominated debt in the EMs, in trillion dollars. This does not include euro-denominated debt which plays a large role in Turkey. The fat gray area represents Asia without China:

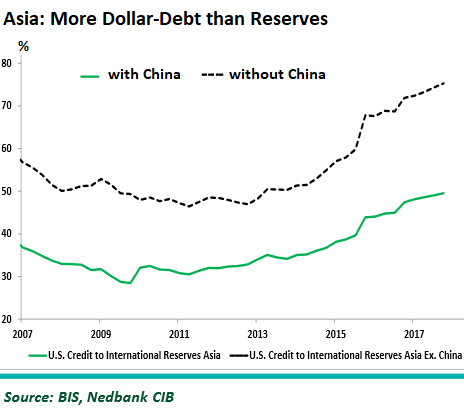

Asia’s dollar-denominated debt, relative to its foreign exchange reserves and exports, has risen significantly since 2009, they note. The chart below shows the ratio between dollar-denominated debt and foreign exchange reserves in Asia, with China (green line) and without China (black dotted line). Values over 50% mean that there is more dollar-debt than foreign exchange reserves:

“This leaves these nations susceptible to a shortage in USDs,” they write:

Notably, the Asian nations that have amassed record amounts of USD debt are also home to the largest technology companies i.e. Tencent (China), Alibaba (China), TSNC (Taiwan), Samsung (South Korea). The tech sector is now 28% of the MSCI EM index.

The rally in the US Dollar, dented global growth prospects, credit growth in China slowing down and escalating political tensions from the US leaves these nations very exposed to a shortage in USDs.

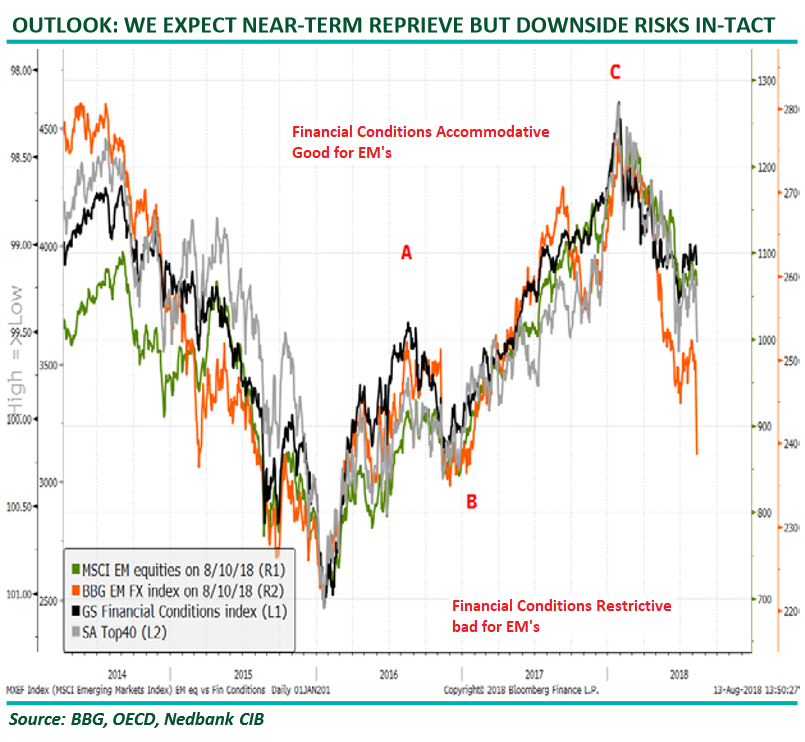

It is very evident on this chart (below) that the changing financial conditions have been the major driver of EM and SA asset prices over the last several years. The risk-on phase ended in January and all EM assets sold-off. EM-FX are however now taking the lead and the next few days will indicate whether this will spill over into the other asset classes.

The chart below depicts four EM asset classes through 8/10/18.

- Green line, MSCI EM equities (1st right axis);

- Orange line, BBG EM Forex index (2nd right axis);

- Black line, GS Financial Conditions Index (1st left axis);

- Gray line, SA Top40 (2nd left axis).

Note the orange line, representing Forex moves:

The strategists conclude: “A number of studies have emerged pointing out that the role of global factors has increased relative to country/corporate specific factors. This indicates that investors need to place more emphasis on the role of global liquidity (changing pool money and credit).”

A vicious cycle, kicked off by cheap debt that’s suddenly not cheap, after 8 years of experimental monetary policies. Read... Rise of US Dollar Haunts Emerging Market Debt

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Let’s be fair. The Fed too is guilty. It’s one thing to say: “we don’t care what happens outside of America.” if that’s actually true, but the blowback from Asia will reach these shores as well.

The Fed is not guilty, they have an explicit legal mandate to manage US rates for the US economy, and all the EM borrowers know it, or ought to anyway, because the cycle has repeated many times. If anyone is guilty it would be Congress for not fixing the system the Fed is part of.

However, even when the US cares what happens outside of the US, because of the blowback that you mention, the US has very little power to legally regulate borrowers in other nations.

Personally I fear the Fed has taken the punch bowl away far too late, with too much malinvestment baked into the cake. The EMs are the signal that tightening is having an impact… but the ECB hasn’t even gotten its hands back on the punch bowl, so they may have the worst time of it! Italy and Spain appear to be the flash points for the next European debt crisis.

They are guilty. They are only not guilty if the US is not a reserve currency and is not required to conduct international transaction for example if we use gold.

What the Fed is doing is similar to what the banks etc were doing during the mortgage crisis i.e. giving out money to unworthy borrowers. I realize that the Fed does not really “lend” out money except perhaps through swaps when there’s a distress, but they should be able to stipulate that borrowing be limited. After all they control FedWire as well and should be able to block huge dollar transfers.

If I recall, after WWII and agreements on making US dollar reserve currency, former Secretary of Treasury stated: “It’s our dollar but it’s your problem!”.

All this to say that FED runs it’s policy according to it’s mandate and the law. Right. But they should also act with other central banks as their decisions ripple on a global basis…

Sooner or later, as a boomerang, it will get back on the US as it did in 1997 (?) with the Asian financial crisis: IMF & World Bank had to step in so local “contagion” (Philippines, Singapore, Japan,…) wouldn’t extend on a global basis.

Which raises the following question: should US dollar remain as reserve currency – subject to the US administration and FED’s decisions – or switch to a “neutral currency” (i.e. SDR) or a basket of currencies?

Exactly this! Only in these globalized days, your problem is our problem is your problem. Go SDR basket of currencies for reserve currency!

And central bwankers; keeping interest rates a bit higher in coming decades might just help stability out too. Then the rich can just park their moneys in the bank / pension fund and not drive the price of stocks and houses out of the reach of swathes of the population.

“All this to say that FED runs it’s policy according to it’s mandate and the law. Right. But they should also act with other central banks as their decisions ripple on a global basis…”

Did those central banks cooperate with the FED in 2008 when against its own wishes the FED did what had to be done to aver something that would have made 1929 seem like childs play.

Nobody cooperates with the FED but the FED must cooperate with everybody.

TBH, it seems like the fed has managed to put the US in a pretty strong position economically right now. Money is still flowing into treasuries from overseas and it’s really reducing the impact of the QE unwind. When the next global recession does hit, it’s more of a question of what position the country is in to weather the storm. Looking at it right now, Asia is going to bear the brunt of it.

Please take a lot at the US debt and deficit numbers. Being reserve currency gets you only so far you know. Even American chickens will come home to roost.

The Fed finally tightening may be helping, but tax changes and deficit spending are AFAIK a large part of the high headline GDP number, see https://wolfstreet.com/2018/07/22/economy-to-pop-4-5-percent-q2-atlanta-fed-gdpnow-v-new-york-fed-nowcast/

Good.

I am increasing my allocation to emerging markets.

ishares Emerging Market ETF (EEM)

P/E: 12.5

P/B: 1.6

The S&P 500 has a P/E of close to 25, P/B of 3.35.

From personal experience, emerging markets have a growing middle class with an improving standard of living. The reverse seems to be true in the Developed world.

The share of emerging markets in global economic output has been steadily growing, that of the G-7 has been declining.

http://blogs.worldbank.org/developmenttalk/growing-economic-clout-biggest-emerging-markets-five-charts

Exactly, buy when there’s blood in the streets.

There is hardly blood on the EM street.

By historical standards, not even close.

Second this, you people are jumping in too early. It’s exactly why you see dead cat bounces in large crashes. These things play out over months not just days or a couple weeks and contagion along with fear will drive the bottom lower before this is all said and done barring some extreme political maneuvers.

We are not there yet, not even close.

Very true These facts are one reason that I moved to Turkey the other being personal

How are you daring with the Lira in Turkey. I visited Marmaris years back& it is truly beautiful

Sounds defensible.

I’d wait for the right time to buy….

This is a misdirect from the problems in Turkey, last night the MSM tried to build case for their financial problems being a personal feud with Erdogan. While Turkey is smaller it leverages itself in multiple ways. Argentina is next, having printed shaky bonds denominated in USD. How much debt is China issuing in dollars? Someone said there is blood in the streets? That’s the best laugh I have had in a while.

Blood in the streets? There is not even urine in the streets. Hell there is not even saliva in the streets.

There’s Chipolte…at 84:1

Maybe he meant short-sellers’ blood? ;-)

It seems the last crisis has become such a distant memory that people forget what “blood in the streets” really means. Right now, there’s only some excess kool-aid on the streets.

The old Asian Tigers have been up to a slew of their old tricks in recent years: Indonesia and Malaysia in particular seem to be headed for a 1997-redux.

The local godfathers and their political masters, some of which are exactly the same actors behind the 1997 Crisis (see Eka Tjipta Widjaja of Asian Pulp & Paper fame), have been busy overleveraging their companies, issuing a lot of debt denominated in currencies they cannot control and generally riding high both the commodity boom driven by China and the ready availability of mountains of cheap credit funneled into the region by the way of Singapore and Hong Kong.

If you want to see exactly how much has changed since the days of the Asian Tigers, the Malaysian government is again pushing hard the “Vision 2020” fantasy Mahathir Mohamad concocted back in 1995. The new capital of Putrajaya needs to be seen to be believed and I suspect the only high tech business going on in Cyberjaya is the aggressive online sales pitch on how this “Multimedia Super Corridor” will challenge Dubai as a financial center and Silicon Valley as a high tech powerhouse.

I honestly don’t think we’ll see another catastrophic regionwide collapse as we did in 1997 and 1998 because China still needs the commodities and we still need every scrap of yield we can find, but excesses will need to be corrected, from the excessive enthusiasm in issuing dollar-denominated bonds to the use of State-owned commodity companies such as Petronas and Pertamina to finance complete fantasies and white elephant projects.

Do some of those Godfathers come from Macau? I don’t remember where that one came from, but it was in one of these posts from Wolf Street within the last week.

Yes, we Chinese… no strike that, we Asians are everywhere. Our hands are into everything. If the rest of Asia ex China causes a meltdown… oh well, that’s nothing, wait until China’s debt blows up. It’ll make the last Asian financial crisis look like a picnic on the Sands.

Many godfathers and their families have deep ties with Macau: Stanley Ho the so-called Godfather of Gambling is the most celebrated, despite the fact he was actually born in Hong Kong.

He had been conscripted by British military authorities in WWII but when Japanese troops overran the Hong Kong defenses he threw away his uniform and, in the general chaos, took a boat to Macau.

His uncle, Sir Robert Ho Tung, had already been in Macau for months, allegedly tipped of the invasion by the Japanese consul in Hong Kong whom he had previously generously bribed to get some lucrative contracts.

Ho worked briefly for his uncle before finding a better job at the Macau Co-Operative Company, a commercial/manufacturing operation set up by Macau legendary godfather Pedro Lobo, which was effectively a legalized smuggling network on steroids: during WWII technically neutral Macau traded with everybody regardless of flag and alliance.

The octuagenarian Stanley Ho still relishes in regaling listeners with stories of hair-raising trips through the Pearl River Delta and having to deal with anybody from ruthless Guangzhou Triads to the fearsome and even more ruthless kempeitai (Imperial Japanese Army police) and trading in anything from bags of rice to whole oil refineries.

Macau’s fortune in the post WWII period is chiefly tied to two things: gambling and the gold trade.

A little known fact is that, either through chance or design, Macau was not included in the Bretton Woods agreement, putting it in an enviable legal position as a worldwide gold trading hub. Despite international protests the Estado Novo refused to address the situation until the US unilaterally withdrew from the Bretton Woods agreement, effectively declaring it empty and void.

Just like Hong Kong, Macau maintained very strong trading relationships, legal or otherwise, with Communist China. In spite of the rhethorics, the construction boom needed building materials and cheap labor and Beijing needed spare parts and machinery the Soviets couldn’t (or wouldn’t) provide.

The local godfathers made a killing from trade with China, something their colonial masters may have not been comfortable with, but which they had to concede.

->I honestly don’t think we’ll see another catastrophic regionwide collapse as we did in 1997 and 1998 because China still needs the commodities and we still need every scrap of yield we can find

China needed the commodities and you still needed every scrap of yield back in 1997-1998, and Asia still had a catastrophic regionwide collapse.

And yet, as it stands, and as pronounced as they are, the distortions aren’t big enough to initiate a crisis. Unless the distortions are actually larger than they appear to be there will be no crisis in the near term, East or West. But for reasons which should be obvious institutions are highly motivated to hide the distortions they create, so those distortions are virtually certain to be greater than they appear and will continue to increase until a tipping point and/or triggering event starts the cascade. That is inevitable, but concealment makes any accurate timing impossible to predict.

That said, in the long term the whole house of cards is unsustainable, terminally so, and eventually the state of your portfolio will be the least of your worries. All in good time.

China was nowhere as big an economy in 1997 as it is now. The impact of any slowdown there will be massive.

I don’t think I’ve made myself clear.

My point is, as SE Asia is structured today, the chances of a big regional catastrophe are very small indeed.

But I fully expect a long spell of “easy to ignore if you are far away” events, such as selective defaults, the usual stock market shenanigans and a long string of bailouts.

Indonesian private companies have been issuing a lot of foreign currency-denominated debt: latest data put it a 17% of the 2017 GDP. The rupiah has lost a lot of value against the euro and the US dollar over the past couple of years, but those losses pale against the yen, which appreciated 9.5% against the rupiah over the past six months. Plenty of yen-denominated bonds issued in Indonesia, hence that is not good, not good at all.

That’s a big problem, especially considering there are legal precedents in the Indonesian legal system which could encourage local companies to default on US dollar- (or yen-)denominated bonds with no ill consequences.

Yields have been ticking upward over the past months, but still do not reflect the risks: too many investors starved for yield, especially in Japan.

Morale: just because the Dow Jones hits all time high after all time high or idiot traders fall for Erdogan’s rather pathetic Qatari bluff it doesn’t mean there aren’t a whole lot of people eating a whole lot of losses.

I was wondering what set off Thursday’s huge Dow rally.

Answer: a Chinese delegation is coming to discuss trade.

And it’s not even a high level one!

The trade deficit with China just hit a record and it’s not going away. To make a dent in its two largest categories of imports to the US: consumer electronics (27%) and apparel (19%) Americans would have to work in sweat shops sewing or soldering. No more likely than picking lettuce.

Of course by hitting China with tariffs on this stuff and not its REAL competitors: India, Sri Lanka. Pakistan etc. you could transfer some of the deficit to them.

If that’s all it takes to juice the markets….

This is one to sell on the rumor, because another Trump tantrum is only a tweet away.

Whoever came up with the Orwellian term “emerging markets”? They seem to have been emerging over and over again for the last 40 years, only soon to be submerged again.

Emerging markets

rising liquid dollar tides

soon submerged again

-a petrodollar reserve currency liquidity haiku

V2:

emerging markets

rising liquid dollar tides

submerging markets again

-a petrodollar reserve currency liquidity haiku

Carp, the last “again” should not be there. Blog autocorrect gods?

Without export figures and GDP numbers these debt numbers can be very misleading imho. If a country is getting paid in USD it should be able to service its USD based debt.

Who in Asia are we talking about? I presume some countries are more over-extended than others? Saying “Asia” to me is like saying “Europe” or the “Americas”, or raises more questions than it answers. I think a breakdown of the Asian debt, with the most vulnerable countries identified would be useful.

Got Gold