A vicious cycle, kicked off by cheap debt that’s suddenly not cheap, after 8 years of experimental monetary policies.

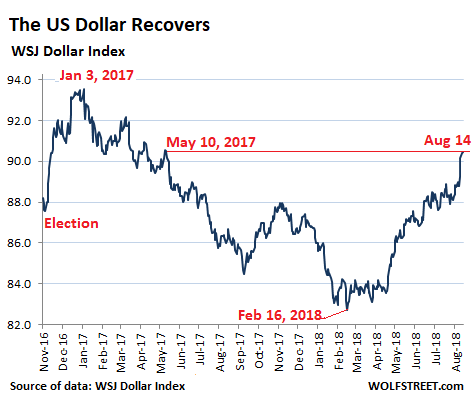

The dollar has risen nearly 2% since Thursday last week. Since April 17, when this move started, the dollar has surged over 8%, based on the WSJ Dollar Index, which tracks the dollar against the currencies of 16 key trading partners, including Mexico and China. From its low on February 16, the dollar has now risen 9.3% to the highest level since May 10, 2017:

The narrower Dollar Index (DXY), which tracks the dollar against six other currencies but not the Mexican peso and the renminbi, rose to 96.73, the highest since June 2017.

Not included in the two dollar indices are the Turkish lira and the Argentine peso, both of which have collapsed, with the lira down 43% and the peso down 33% against the dollar since April.

That recent surge in the dollar makes dollar-denominated debt across the emerging economies harder to service. After the collapse of the Turkish lira and the Argentine peso, this is particularly the case for dollar-debt and other foreign-currency debt in those countries.

Over $200 billion of USD-denominated bonds and loans, issued by emerging market governments and companies will come due during the remainder of 2018, according to the Wall Street Journal. About $500 billion will come due in 2019. They will need to be paid off or refinanced.

When financial conditions in the emerging markets get tight, some economies will find it difficult to pay off or refinance that debt because dollar investors are going to be leery and would want to be compensated for large risks – a consideration that was absent as little as a year ago, when Argentina was able to sell 100-year dollar-bonds. As far as these bondholders and creditors are concerned, it will take either an IMF-bailout to make them whole, or a default. Argentina has already made a deal with the IMF to bail out its bondholders.

Through 2025, emerging market governments and companies face $2.7 trillion in USD-denominated bonds and loans that will come due and have to be paid off or refinanced. This does not include euro and yen-denominated debt, of which these countries also have a pile.

For example, in April this year, the Mexican government was able to sell ¥135 billion ($1.26 billion) in “samurai bonds” with maturities of five, seven, 10 and 20 years, at what the Ministry of Finance termed “a historically low cost.”

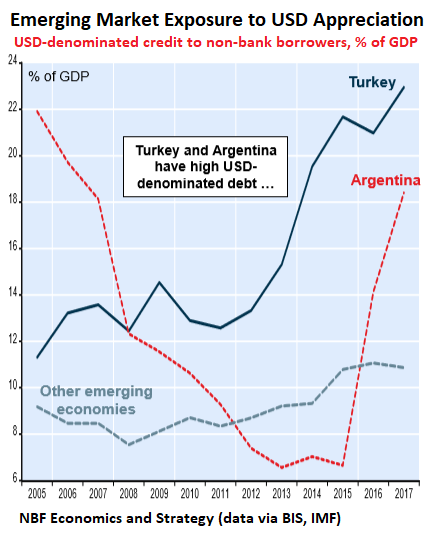

In terms of the USD-denominated debt as percent of GDP – not including other foreign currency debt – Turkey is on the forefront, followed by Argentina, according to a report by Krishen Rangasamy, Senior Economist at Economics and Strategy at NBF. These two countries have gotten hit not only by the USD-appreciation but more importantly by the separate collapse of their own currencies. Citing data by the Bank for International Settlements, he writes that in Turkey, USD-denominated debt by non-bank borrowers “hit a record $195 billion at the end of 2017, or a stunning 23% of GDP.”

Turkey also has a heavy load of euro-denominated debt, and its total foreign-currency debt now amounts to over 50% of GDP.

Total foreign-currency denominated debt also amounts to over 50% of GDP in Argentina, Hungary, Poland, and Chile, according to the Wall Street Journal, citing Deutsche Bank.

A country like Turkey can destroy its own currency and thus diminish the burden of its local-currency debt. But it cannot do this with foreign-currency debt. Instead the reverse is true: Foreign-currency debt becomes more burdensome. And this creates a vicious cycle; as this debt becomes more difficult to service, the default risk rises, and foreign currency investors are then even more inclined to stay away, leading to more capital outflows, and making it nearly impossible to refinance and service that debt – thus speeding up the trip to a default.

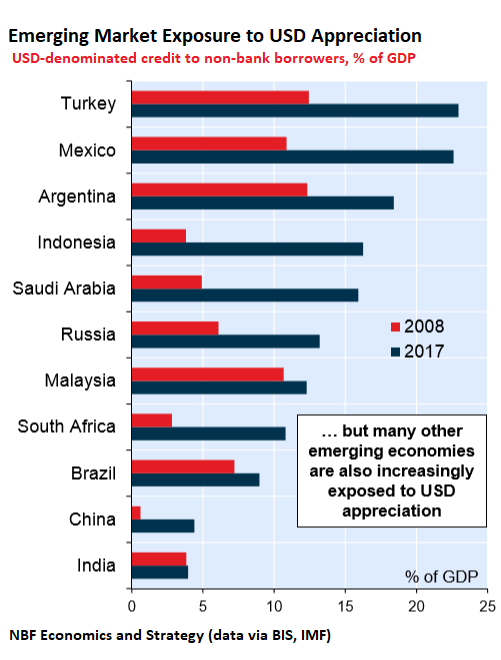

The chart below shows the increase in USD-denominated debt for the top emerging market economies from 2008 (red) to 2017 (blue) as a percent of GDP. Note how that USD-denominated debt has surged as a percent of GDP since 2008:

Mexico is right up there, and it’s vulnerable, but compared to Turkey and Argentina, it has better current-account balances and higher foreign exchange reserves. And Indonesia has seriously arrived on the risk scene over the past few years.

This period between 2008 and 2017, during which this surge in foreign-currency debt occurred in the emerging markets, happens to be the era of experimental monetary policies in the US, Europe, and Japan that entailed an enormous amount of money-printing to artificially repress interest rates – in other words, cheap debt. These experimental monetary policies had the express purpose of encouraging a debt-fueled binge of consumption and investment. That is now in the past, and what remains is the hangover – the debt that these countries cannot control or inflate away.

A Grand Collapse in Turkey; and to avoid the same fate, Argentina hikes its policy rate to 45%. Read… The Price of Cheap Dollar/Euro Debts: Local Currencies Come Unglued, Debt Crises Ensue

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So what happens if several or many of these nations organize and default on purpose to inflict damage on the U.S.? Many already have a motive to do so. And I am surprised Russia still has not completely de-dollarized. It knows the U.S. will only use any dependence of the USD to further attack it’s sovereignty. Russia has vast reserves – it should use them and get off the USD.

Erdogan repeated his call for Turks to sell dollars and buy lira to shore up the currency, while telling business owners not to stock up on dollars.

He can blame “foreign powers” all he wants but the crisis has been largely of Turkey’s own making. Erdogan has sacked, or imprisoned, thousands of civil servants in high places. He has replaced them with family, friends and an assortment of cronies. He’s financially illiterate (e.g. he thinks high interests produce inflation) and won’t listen to people who actually know the stuff. He thinks that loyalty to his persona is more important than integrity and competence. The Turkish central bank can’t do anything without Erdogan’s approval. Etc. etc.

Then he gets all worked up when lenders say that Turkey has become a banana republic and refuse to lend him money at the rates he wants.

Berat Albayrak, the finance minister and Erdogan’s son in law, said (quote from Reuters):

“From Monday morning onwards our institutions will take the necessary steps and will share the announcements with the market”

Translation to English: I don’t have the foggiest idea of what to do next but I’m sure my father-in-law knows what he’s doing.

In other words he has the mentality of your typical totalitarian dictator (which he’ll soon become).

All middle eastern leaders are tribal leaders. Taking care of the tribe is seen as their responsibility and is expected by the tribe.

And how would that be different from the US?

Petunia Turkey is certainly NOT the Middle East Please consult a MAP thanxx And the reference to tribalism definitely does not apply in Turkey

Frederick,

You should study the hereditary titles and honors in Turkey connected to ruling provinces. The title pasha and bey are still common for a reason.

Old Engineer,

The biggest difference is that in the ME the system is transparent. Here in the US it exists — the black caucus, jewish lobby, counsel on foreign affairs, — but is denied.

Seems to be working temporarily as the currency has rebounded over 10%, but I don’t think it’s going to hold loo term.

Dead cat bounce.

He’s financially illiterate and won’t listen to people who actually know the stuff. He thinks that loyalty to his persona is more important than integrity and competence.

Gee, that reminds me of some other head of government.

You will call it default. They will call it taking control of their economic futures. Who is on the right side of history?

It’s very hard for these economies to live without borrowed money. If they default, their ability to borrow ends. Then they have two options:

1. Live within their means (“austerity”);

2. Print the money to fill the holes and destroy their currency even faster.

Neither are very palatable options to them.

This is incorrect. “These economies” have been encouraged to borrow USD because USD interest rates have been made available to “these economies” by their own govt at much lower rates than their sovereign currencies, and access to USD has been encouraged when “these economies” could and should easily do the opposite.

What is “hard” is “austerity” which has destroyed economies in every single instance it has been applied including Obamanomics.

The antidote is for “these economies” is to make their currencies more attractive than the low interest rate USD and restrict access to USD.

When you can walk into a Russian bank and open a USD account at will – the nation that is massing armies at your borders as we speak – and the Russian Bank keeps it’s interest rates so high no sensible person would borrow rubbles when the Russian govt has made USD so much cheaper – clearly Russian has embraced neoliberalism to such an extreme degree that they are undermining their own national interests.

1. Live within their means (“austerity”) !!!

WR: are you familiar with the hazards of suggesting the A-word to the flock?

Don’t forget Robespierre :)

Austerity = Live below their means!!!

As a penance for their past excesses

Neither would work for the U.S. either. The difference is we’re borrowing in our own currency so we can get away with (for now) before it bites us in the ass.

We’re basically guaranteed to go for option 2 eventually. Cleanest dirty shirt theory sums it up and may be the case for quite awhile, but it’s headed there as U.S. debt to gdp levels keep rising and monetization is the most politically acceptable way to deal with debt, mostly because the public doesn’t understand inflation nearly as well as “the government won’t give me muh munny.”

“Live within their means” ? “Austerity” ?

I guess that includes selling off their PRIME public infrastructure and property at pennies on the dollar to Goldman Sachs, et al.

If I remember correctly, Lloyd Blankfein said that was part of “doing the Lord’s work”.

How soon we forget.

Look Goy….just put your head back down, and enjoy your stupor….I mean slumber.

Austerity = Live below their means!!!

As a penance for their past excesses

Doesn’t this open up the prospect for some “good Samaritan” country to come in and “help out?” Maybe there’s a country out there with huge wealth that the US has been gifting it over the decades which now has developed expansionist ambitions. That country might be quietly “lending” money to many regimes in its region in return for “favorable consideration” in the future. If Turkey is of strategic value (due US military bases there), I’m sure they might come knocking to help out. The days of large scale military actions are over. It is now all about economics and the waiting game: a strategy that this “other country” might be very very good at, while the West is obsessed with the idiotic quarterly reporting mindset.

Right on the mark! Russia already in talks with Turkey and nice way to lock up the Black Sea totally. I’m sure waiting in the wings is another rebuilding empire….

Mike We brought it on ourselves and everybody hates a bully

If Turkey wants to ally with another power they’d be better off with China. which is not as close as Russia but way closer than the US.

China has issues but Russia is arguably in worse shape than Turkey.

Back out oil and gas and there is not much to the Russian economy. Ever see anything made in Russia?

Maybe that’s one reason Trump gets along with Putin. No trade deficit!

China could give Turkey a loan (with strings, of course)

Good luck getting money out of Russia.

In the regions of Russia bordering China, virtually all consumer goods are Chinese. Economically, a swath of Russia is Chinese.

I sold my bitcoin and bought Turkish lira. Looks like all 3 of us are losers.

Defaults/restructuring seems inevitable. Or will there be some kind of can that will be kicked down the road? Perhaps the ECB can loan them €’s that can be exchanged for $’s?

The responsibility for this mess rests with Turkey’s central bank governor of the past, when the borrowing was taking place. If he is not in jail already, he should be. But then, where do central bankers go to jail for the crash they create.

Except that Erdogan was pushing hard for lower interest rates for years.

https://www.bloomberg.com/news/articles/2016-09-23/erdogan-to-turkey-s-central-bank-nice-rate-cut-do-more-please

Wait. Are you saying Erdogan is a secret admirer of ZIRP, and maybe even has a copy of Courage to Print on his presidential desk? /s

The Turkish central bank governor is not independent. He answers to the Turkish president. In today’s mashup, Erdogan tells him what to do regarding monetary policy. Then Erdogan tells his son-in-law (the newly appointed finance secretary) what to do regarding fiscal policy. What could go wrong?

Draghi is immune from prosecution as chief of ECB. Why did the Euro countries agree to it?

Because of trixy stuff like “The Energy Charter Treaty” being liberally used to sue everyone over the potential losses of imaginary profits?

And “sue” is maybe overcooking it, since these cases go to arbitration under ISDA-rules -> 3-lawyer secret kangaroo court’s.

https://corporateeurope.org/international-trade/2018/06/one-treaty-rule-them-all

One would be crazy to set interest rates and bank policies while being open to disputes by everyone on the wrong side of the bet.

Dammit! ISDS or investor-state dispute settlement. Too many things in me head.

Answer – Because all these countries have their leadership installed (sorry, elected) the same way we do here….the best that money can buy.

In the overall scheme of things, 500B US dollars is nothing. This is a non issue economically; simply gives the US more power to manipulate the rest of the world.

Now, socially, that is a totally different story. Makes the world hate us even more.

It’s not a “non-issue” for Turkey. Argentina defaulted on tens of billions of dollars, not on hundreds of billions.

But you’re correct in terms of the US: a default by Turkey is a non-issue, and the Fed knows this and will continue to raise rates no matter what happens in Turkey or Argentina.

therefore old Recep Tayyip is right, the US is against Turkey, if nothing else by being inattention. The Fed couldn’t care less what happens to Turkey, so if Turkey is squished on the way… too bad… so sad.

But fear not, China and Russia will come to the rescue. I’m sure of it. If nothing else, plenty of strategic options there in Turkey, what with it being the crossroad between Europe and Asia. Controlling Istanbul alone might well be worth it given the access to the Black sea and such.

This was inevitable and predicted. After all, interest rates couldn’t stay low forever.

Wolf…Are you suggesting that the FED can weather any storm? Can we trust that they are THAT smart?

I think I read the other day that interest on the debt right now is on course to be 40% of the yearly debt. You bet they will be lots of printing going on.

Don’t forget the contagion aspect of default. If banks or other financial organizations outside of the countries have significant risks in loans they could come under stress as well. And then you have those that have sold CDS on those banks or bonds, expanding out further. Sometimes it is not just the original amount as to how it has been amplified across the system.

Yep, the death of the Petro-Dollar, or whatever ominous-sounding catch phrase newsletter writers are paid to spew.

A couple things I wonder, how will this compare to the Tequila Crisis of 1994 both in terms of percentage of debt denominated in foreign currency and overall scale? And wasn’t the Tequila Crisis the precursor of the Asian Financial Crisis a few years later by driving more hot money there?

There are always financial crises somewhere. It’s only when there is a financial crisis in the huge US economy or in China that the entire world quakes. A financial crisis in Mexico just causes some ripples in the US.

perhaps you’ve read Doug Noland’s thoughts on the credit bubble collapse expanding from the periphery to the core. I would say under ideal economic conditions you are correct, and that under stress, trade wars and currency imbalances, that he is correct.

gee Em feeding from the dollar liquidity trough. Too bad the Yankee bucks weren’t spent stateside on plant , property and equipment . Heck i would even settle on some infrastructure.

Wolf,

“These experimental monetary policies had the express purpose of encouraging a debt-fueled binge of consumption and investment. That is now in the past,…”

I was hoping you would do a post on the non-accomodative monetary policy that you think has gripped the central bankers now

As you would have inferred from my comments I do not believe that the non-accomodative policies will remain so should the market crash (more than 20% would be my guess). The US market is presently ignoring all the risks (sanguine in the belief that the Fed will not let them down) and is also probably helped along by dollar inflows and the currency crises sprouting all over the place. How many countries need to get into trouble before we get a contagion? If the currency crisis hits more countries will IMF itself not be tested? After all, IMF does not have the printing press that the Fed has.

In short, if the crises creates a contagion (it well might if the currency involved is Euro) the Fed is going to be really tested. Then and only then we will know what the central bankers will do. Let us see how it plays out.

Withdrawal is always painful when the drug is withdrawn from the addict.

Financial crisis in Turkey, Argentina, Indonesia, Brazil…… if you don’t live there it is all small beer. Crisis in USA, EU or China and we all will be frightened. Question is are these events related to underlying issues which will blow us all up?

Yes, a rising dollar and a sinking yuan. When the yuan crashes, so will everything else.

Ambrose Evans Pritchard, amongst others, point out that EM economies now account for 50% of global GDP and even more of global ‘growth’. For them, as a group, to have to retrench and engage in ‘austerity’ is going to have a major impact on DM as no one else, save perhaps Germany, is in a position to ‘reflate’ their economy and even Germany is fiscally constrained by its own fiscal rules.

Ambrose Evans Pritchard is a perma-doom- monger. Developing economies are growing two to three times (or more) faster than developed economies. There will be bumps, but the growth will continue.

Such complex situation

There are just so many debts and outstanding obligations around the world, and everyone is trying to keep the wheel spinning so it doesn’t land on their square. So far the illusion is supported by just “hand quicker than the eye stuff”-numbers in stock win columns, derivatives, algorithms, fake pension reporting, etc….But now the strong arm tactics are taking over. If you don’t buy the narrative, back the meme or seek the global vision of endless prosperity for all, then out comes the hot poker. China, Iran and Turkey banning shorts, threatening speculators. It’s just a whiff of what’s to come…I see the world, not just fake, but Mad Max like-getting crazier and potentially brazier by the day-new zillions, new genders, billionaires wanting everything, drugs everywhere, Street people living by every garbage can in every neighbourhood… How is this going to end…I don’t know, but how does the song go, “when it all comes down, I hope it doesn’t land on you”

off topic warning:

However, it speaks to the themes of debt and housing price crisis so common to WS. Plus, those damn fungible currencies meddling in the sovereign wealth of other countries. :-) aka laundry.

New Zealand just outright banned the purchase of homes by most foreigners in the hopes of ensuring their own citizens can afford to buy homes going forward.

Maybe Turkey could do the same. (There, fixed the off topic problem :-)

http://www.cbc.ca/news/business/new-zealand-bans-foreigners-buying-homes-1.4785782

Paulo – “New Zealand just outright banned the purchase of homes by most foreigners in the hopes of ensuring their own citizens can afford to buy homes going forward.”

Should have been done years ago, before the damage was done, but there were too many elite (who manufactured and engineered it) cashing in on it.

Notice the timing – just at a time when China is stopping outflows of money from China, putting an end to foreign Chinese buying, all of a sudden our “benevolent” governments rush in to save the day!

Coincidence?

– I disagree with the notion that the US won’t be hurt at all.

– Investors were – in the last few years – trying to get a higher yield. And found that higher yield in e.g. Turkey, Argentina and Brazil. And that included investors from the US, although I haven’t figures on how much of that emerging market debt was bought by US investors.