Russia, Japan, and the Fed dumped, China hung in there…. But who bought?

“Official” foreign investors – this would be central banks, governments, etc. – and private-sector foreign investors held $6.21 trillion of US Treasury Securities at the end of June, up by $61 billion from a year earlier, according to the Treasury Department’s TIC data released Wednesday afternoon.

But over the same period, the US gross national debt, fired up by a stupendous spending binge, soared by a breath-taking $1.36 trillion. So who bought this $1.36 trillion in new debt?

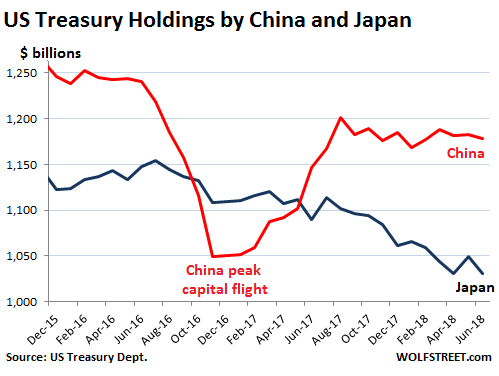

The largest holder of marketable Treasury securities remains China, whose holdings in June fell by $4.4 billion from May to $1.18 trillion, within the same range since August 2017, despite escalating threats and counter-threats over trade.

But Japan has been systematically reducing its Treasury holdings. They’d peaked at the end of 2014 at $1.24 trillion. In June, its holdings dropped by $18.4 billion from May, to $1.03 trillion, the lowest since October 2011:

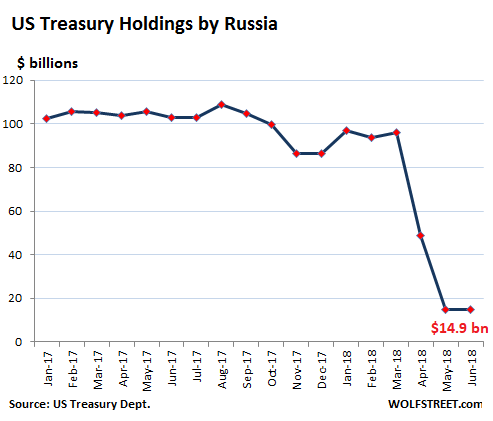

Russia never held as many Treasury securities as China and Japan. But it stands out because it has liquidated 90% of its holdings since May 2013. At the time, it held $153 billion in Treasuries. Then it started shedding them. By March, it was down to $96.1 billion. In April, it dumped $47.4 billion. In May, it liquidated another $33.8 billion of its holdings and disappeared from the TIC’s list of the 33 largest foreign holders of Treasuries. That was a milestone. In June, it just hung on to what it had and ended the month unchanged at $14.9 billion:

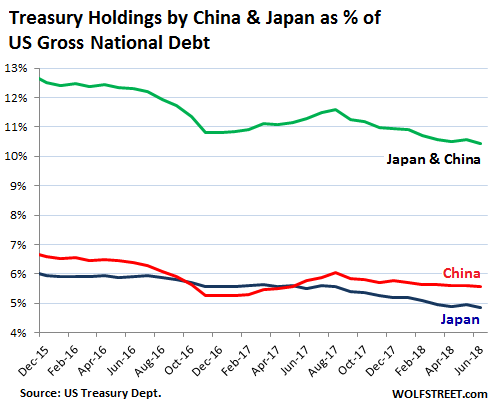

China’s and Japan’s outsized role as creditor to the US government has been diminishing in proportion to the US gross national debt for two reasons: The total pile of debt has soared; and the holdings of China and Japan have edged down. At the end of 2015, their combined holdings amounted to nearly 13% of the total US debt. By the end of June, this was down to 10.4% (green line), with Japan’s holdings (blue line) now down to 4.9% of total US government debt, and China’s stash (red line) down to 5.6%:

The Runners-up

Perhaps not so ironically: Of the 12 largest holders of US Treasuries, after China and Japan, seven are tax havens for foreign corporate and/or individual entities (bold):

- Brazil: $300 billion

- Ireland: $300 billion

- UK (“City of London”): $274 billion

- Switzerland: $236 billion

- Luxembourg: $220 billion

- Cayman Islands: $197 billion… down from $250 billion in April 2017!

- Hong Kong: $192 billion

- Saudi Arabia: $165 billion

- Taiwan: $163 billion

- Belgium: $155 billion

- India: $147 billion

- Singapore: $122 billion

Germany runs the third largest trade surplus with the US, behind China, Mexico, and Japan (2017), and it’s the fourth largest economy in the world, but it held only $71 billion in Treasuries in June. This disproves the common assertion that a country with a large trade imbalance with the US has to get stuck with its debt.

The Americans did it.

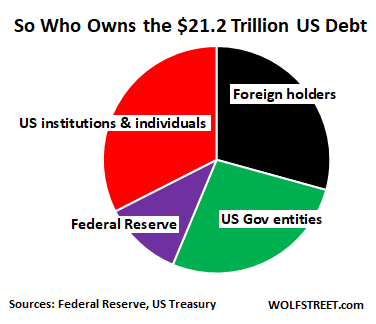

By the end of June, the US gross national debt had reached $21.21 trillion, up $1.36 trillion from June last year. Here’s who bought all this paper over those 12 months:

- Foreign official and private-sector holders bought $61 billion, raising their stake to $6.21 trillion, or 29.3% of the total US national debt (see above).

- The US government (pension funds, Social Security, etc.) raised its stake by $263 billion, bringing “debt held internally” to $5.73 trillion, or 27.0% of the total.

- The Federal Reserve shed $85 billion as part of its QE Unwind, bringing its stash down to $2.38 trillion by the end of June, or 11.2% of total US national debt.

- American institutional and individual investors, directly and indirectly, through bond funds, corporate or state pension funds, and other ways, owned $6.89 trillion, or 32.5% of the total US debt at the end of June, having added $1.13 trillion to their stash over those 12 months!

And here’s the proud ownership of the elephantine US debt:

The Fed, Japan, Russia, and whoever might be selling. But Americans are buying avidly – now that yields have come up substantially, with the one-month yield at nearly 2%, the one-year yield at 2.45%, and the two-year yield at 2.61%. There is even huge demand for long-term maturities, as evidenced by the 10-year yield, which is only 2.86%. If there were less demand, the yield would have to rise to lure new investors out of the woodwork.

Core CPI jumps the most since 2008. Read… Rate Hike Ammo, Even Without Food & Energy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If Americans institutions and individuals bought $1.13T in treasuries, where did that money come from? Lower consumption, sale of equities? My guess is it’s a combination of both. In any case, it’s not good for the stock market.

Tax reform. Savings were recycled into sit-on-ass guaranteed government interest payment vehicles by corporations, banks, and wealthy people out of a lack of any better idea about what to do with the money.

Foreign holders that had been trying to keep their currencies low against the dollar to grab an outsize slice of their unearned share of the U.S. domestic market, making them buyers, saw the writing on the wall on trade and started giving up on these purchases, as they knew their currencies would just start falling anyway. In Japan it’s been because debt there can’t yield anything and oh in the U.S. it will now. In China this has been because their propeller-cap kickstart funding is about to pull a vanishing act. DJT is taking their allowance away.

The Fed just “prints” money. The US has no need of investors when the Fed can invoke such super powers anytime. My left hand can feed my right hand anytime. What did you say? “Arms length transaction?” Did you see my statement about my left and my right?

For those of you who don’t get how it works:

U.S. Government (treasury department) issues $1.13T in bonds, receiving $1.13T in bank credit from the Primary Dealers.

U.S. Government spends the bank credit. Now the government contractors and employees have that money. They spend that money and now it’s all over the world.

Then that money comes back to the banks as the public buys the bonds. The banks pocket some interest as well as the bid-ask spread on the bonds.

They don’t call it “fiscal stimulus” for no reason.

My understanding is the treasury just prints and spends the money first, with it all ending up in the banks. Then the treasury issues the bonds. And because the money is sitting in the banks, the banks have it available to purchase the bonds.

Bob Prechter calls monetization a check kiting scheme, Greenspan once said he didn’t understand it himself. Obama said we have to raise the debt ceiling “its money we already spent.” The Fed can also raise the reserve requirement which makes the sale of the bonds a little easier. Treasury sets the rate at auction according to their perception of what the market will accept, if they are wrong they make up the difference.

Just gives you that fuzzy warm feeling all over to know that pension funds hold such a massive amount of unpayable debt issued by an insolvent vendor!.

Those receiving the bigger crumbs must be parking them in treasuries. Mine went to a new computer.

I transferred from my savings account into treasury. I did NoT have to do that when rate is zero. Now Injave to do it because rate is 2. I did NOT need to sell anything else.

Could the 1.1 trillion confirm the rumors that Uncle Sam is the new tax haven?

I have a bit of money saved that I don’t want to throw in the market at this time. I don’t want to lock up low yields for years, so I don’t want long bonds. I have too much precious metals allocation already and whatever pittance the banks offer for savings accounts could easily be dwarfed by hidden fees.

My conclusion – look for an ETF or money market fund focusing completely on US Treasury notes and/or short term us bonds. Decent interest, highly liquid to use when market opportunities arise, and backed by the Fed.

When junk rated bonds yield 5%, a 2% risk-free rate thats highly liquid sounds very attractive.

If you just want to hold a 1-year to maturity, it’s a reasonable deal. The rate is about the same as a 1-year CD, and the income is exempt from state and local income tax.

US commercial banks still have close to $2T of excess reserve parked at the Fed. They can easily absorb a large amount of Treasuries as the Fed winds down its balance sheet. For the banks they are simply swapping IOER paying excess reserve for interest paying Treasuries on the asset side the balance sheet.

The Fed pays the banks 1.95% on excess reserves. That’s likely go to 2.20% at the next rate hike. That’s a good deal, with no work at all. That’s perhaps why banks haven’t massively jumped into Treasuries.

2.2% sure beats the risk and all the work involved finding debt slaves.

It is also why QE didn’t do much for the economy, as the money never entered the economy.

It has simply sat at the Fed as excess reserves.

Personally, I don’t see much demand for the kind of money that actually stimulates the economy.

I guess that is why the fractional banking system multiplier is near 1 now?

If you look at QE as a Bank Bailout, it makes more sense. It was always about recapitalizing the banks while increasing asset prices which lowered LTVs on outstanding loans. Any economic stimulus was knock-on.

QE did enter the economy! It went to investors to buy assets with, all of which grew tremendously in value – stocks, bonds, real estate, etc. The Been Bernanke claimed that this “Wealth Effect” would trickle down to the people. It has in the form of construction jobs coming back to a degree, but costs of living skyrocketed at the same time.

This hasn’t led to any meaningful wage inflation, which correlates much better with the CPI than the actual cost of living for median income Americans.

Given that you can find CDs in the 2.5 to 3.0 apt range why would you not just use those? Granted these do have penalties of you pull out early but they can be as little as 2 quarters of interest….

Maybe taxes?

View IOER on ER as sorta like getting a wage for just sitting around and being available. It may be appealing at first, but will prove to be self-defeating for all parties in the longer run if it continues. So, why hasn’t IOER been pulled back?

I see banks buying Treasuries differently. Sorta like being hungry on the road. Only thing available is fast food, but you have to eat something so it’s okay occasionally. But why would I buy shares in a bank that buys too many treasuries? I would simply find a better bank stock or buy Treasuries direct.

When I watch the US debt clock, ticking today at $21.348 trillion, I freak out. But then I remember that one has to think about debt in relation to productivity. When one looks at both sides of the balance sheet, the US’s public debt load is manageable relative to the country’s annual GDP and government revenues. In 2016, the US debt was $19.8 trillion debt. It doesn’t look too bad next to the $18.62 trillion GDP (2016 figures).

Here’s a practical example. In 2012, Mark Zuckerberg was able to refinance a six-million-dollar mortgage at 1% because the lender knew that Zuckerberg wouldn’t have any trouble paying the mortgage. If his house appreciates in sync with a 2%-4% inflation, he will have lived in his six-million-dollar house in Palo Alto for free, assuming normal maintenance & insurance costs.

It’s all relative.

Oops, pressed the “Post Comment” button too soon.

The 10-year T-note is trading today at 2.8% when it should be more than 5%, considering current levels of inflation. If the “American institutional and individual investors” who bought $1.13T of treasuries bought the long-term type (7, 10, 30 years) around 2.5%-3.5%, me thinks they are getting a raw deal!

Agreed on the raw deal comment, but where is one to take refuge?

And what would GDP have been without the corresponding increase in the debt? Seems that Productivity net of increased debt has really sucked until recently and maybe even that recent tick up to 4.1% is not good enough unless it stays 4-5% for a while.

Maybe I am missing something

Definitely agree that the ten year should be 5%+….but, that would tranquilize the struggling proles for further slavery…………Just my two cents but the whole “recovery” program has been a crush for the ordinary individual…….Hail Caesar!!

“The 10-year T-note is trading today at 2.8% when it should be more than 5%, considering current levels of inflation.”

Unless you think future growth and inflation will both be lower– and they will be. We’ll see a deflationary crisis before we see an inflationary crisis.

Man, I wish I can remain wistful and innocent like you. I have one word for you: Pension. Unfunded liabilities in the US is THROUGH the roof.

The unfunded liabilities problem would be catastrophic if they were due next year. They are not.

Furthermore, Congress will renege on the promises made to retirees. As time goes by and interest payments start crowding out discretionary expenses, Congress will cut down on benefits and replace the measures by which liabilities are calculated.

Last time I checked, no Congress has ever been executed for reneging on promises. We’re talking about politicians here.

If you want to worry about something, you should worry about loss of productivity as the population ages.

Yes, they will trim the benefits. IMO, it would be far better they do that (or raise taxes, ha) sooner than later.

The problem with your reasoning is that you know it will be due quick enough. Also cutting benefits? We’ll see, you talk about politicians and you win seats by cutting pensions? Not sure what kind of country you live in? Now I am not saying that benefits will not eventually be cut, but that will happen as the last option after tons of money printing, after tax raises, after all sorts of shenanigans.

Also, we haven’t spoken about the coming recession. The nation’s debt has exploded in this great recovery. I am just afraid about the what it will look like when the recession arrives. That national debt to GDP number will get ugly in a hurry. AND if we add in corporate debt + household debt right now, we are looking at 200% plus total debt to GDP ratio. Not sure how anyone can be comfortable with that.

Being a retired member of a large retail union I follow the annual reports of our own pension funds (we really have very modest pensions in this sector) and have seen the fund in a large “red zone” back after the GFC and have seen that red zone slowly decreasing and more on the plus side. That was accomplished by ongoing contract changes that cut into future hire’s pensions, medical co-payments, more “tiers” for entry level participants…etc, etc.

Of course the pre GFC idiots (remember Orange County?) that managed so many pension investments funds during the glory days based their future earnings calculations on around a consistent 7% returns. We all know how that turned out.

But changes have been and are being made and it’s on the backs of the proles. And, well that it should be so that they will understand the penalties for no oversight of their money handlers.

What seems to be missing in this scenario is that cutting promised benefits has the negative effect upon spending. Once cuts start, the consumer spending will go down as will the GDP. Once these start downward, there won’t be enough income to corporations and they will cut spending and jobs.. Less taxes collected means bigger deficits and more cuts… It is a negative spiral that has no good outcome.

When no one is paying attention, the kid runs his finger through the icing on the cake. Then smooths it back over as best as possible. That method proves irresistable but it will ultimately be exposed. But wait, the kid then blames the dog. And if he can find a crony/witness, he might just create enough confusion to perpetuate his folly.

There is still a problem – he knows the truth. And it will ultimately rob him of any happiness the icing provided. That is a hard lesson to learn and many don’t.

Re: “will ultimately rob him of any happiness…” that’s only true if he’s not psychopathically greedy. Unfortunately, too many of the corporate crooks will never become unhappy about robbing others. Instead they choose the Bastiat Escape: “When plunder becomes a way of life for a group of men in a society, over the course of time they create for themselves a legal system that authorizes it and a moral code that glorifies it.”

@Wisdom Seeker, thanks for the follow up. Certainly agree in most respects, though I would make a key distinction between individuals and groups. As a group, most people will do and participate in (or simply go along) with things they would rarely do as an individual. Corporations being treated as individuals is a big mistake. Yes, there are some psychopaths.

When I was young, my mother did a fair amount of baking. One day she baked an angel food cake and covered it with a nice thick butter cream frosting. After frosting it, she put it on top of the refrigerator to cool.

While the frosted cake was cooling, she made a big mistake and went next door to the neighbors.

My younger brother, sisters, and I kept checking out the cake on top of the refrigerator. The frosting was so thick that we thought we could scrape a little off and our mother would never notice.

We pulled up a chair and took turns scraping off some frosting with a table knife. We were careful to keep turning the cake and smoothing the frosting so it would look even and unmolested.

There was only one problem with this plan – we didn’t know when to stop. When my mother came home, the frosting on the cake was so thin it was almost transparent.

She was NOT amused.

The unfunded liability problem is being solved by fake inflation number. Did you believe inflation was too low with housing prices through the roof?

It’s all relative, especially when all the stats re: GDP, employment, inflation, etc are all suspect.

This article and comments re: internal debt holders reminds me of Tesla employees buying shares in Tesla. It’s about the same level of insolvency, irrationality, in-fighting, hype, and craziness. I forgot ‘Great Leadership’, and trust in institutions. sarc/

Where’s Slim Pickens when you need a mascot to ride this sucker all the way down?

Citi’s Jamie Dimon is saying the 10 could hit 5%

That would puncture a lot of bubbles

Jamie is of the Morgans.

I think we’re at an important short-term junction for the 10.

It’s traded between 2.80 and 3.00 for the majority of the year. It looks to me like it has been in a topping out process the whole year.

It’s quickly approaching a trendline connecting 1.3% (June 2016), 2.0% (Sep 2017), and ~2.8% (~Sep 2018).

If you believe that we just frontloaded a bunch of growth in Q1 and Q2 with tax cuts and the dramatic rush to beat tariffs in Q2 (which may have added as much as 1-1.5% to Q2 GDP), the 10-year is likely going lower. I think that is what fixed income markets are signaling, and I think breaking that trendline may be the trigger that sends the 10-year lower.

Jamie Dimon is JPM, but while we’re mentioning his forecasts, let’s not forget that he called 4% this year in April, and reiterated that call again in May… and has been dead wrong. The 10-year is lower today than it was in May.

Also I don’t think you can find many credible fixed income traders (key word: trader, not analyst, not CIO, not CEO) who expects the 10 year to go significantly higher than it is today. I think the consensus analyst prediction was about 3.1%, and they (the analysts) have been consistently wrong on the high side almost every single year for the last decade.

I keep it in my 401K for safe keeping.

Can’t help but wonder if import taxes (i.e. tariffs) are allowing US Gov to run up deficits w/o having to issue so much UST paper. 10%, 25% & 50% import taxes sure look like a nice cash cow worth milking, to pay Uncle Scam’s bills..at American consumers’ expense of course.

This is why I wonder if there will be no trade deal to remove tariffs, even if China or other countries are amicable. If it’s really about covering expanding US Gov debt, the import taxes will remain in place until something breaks. And if I’m correct, when they go away, UST yields will spike until the Fed (buyer of first resort) steps back in.

While we wait for 2018 tariff revenues, we have the 2017 data.

The Treasury levied $36 billion in tariffs, which may sound like a lot but is actually just 1% of Federal revenues.

Intriguingly enough tariffs have long been a very small part of the Federal revenues: since Richard Nixon was sworn in they never accounted for more than 1.8%, and that happened in 1988, under Ronald Reagan’s watch.

Tariff revenues fell sharply under Bush I and Clinton, bottoming at 0.9% in 1999. Under Bush II and Obama they picked up somehow but more due to the increased volume of imports, not higher tariffs.

So no chance of increased tariffs going towards a balanced budget, sorry. Even if revenues increased tenfold, tariffs would amount to just 10% of 2017 revenues.

It’s interesting to note that some of the heaviest tariffs are levied on items so-called First World economies have long stopped manufacturing, or manufacture in minuscule quantities, mostly for the luxury market: sweaters and women’s dresses are slapped with a 16.1% tariff, albeit those originating from Mexico get reduced rates through NAFTA.

Tariffs are schizophrenic and have long been in need of some harmonization: for example shoes (without leather) are hit with a 15.6% tariffs while shoes (with leather) get away with an 8.6% tariff. Shoes (with plastic) contribute to the general confusion as they have their own 9.8% tariff.

I’d like to add to the tax haven list Belgium: it’s no coincidence JP Morgan chose it as Euroclear’s base of operations.

Under Belgian law, custody accounts are anonymous if they meet certain conditions, such as where the account owner is fiscally domiciliated, what’s owner’s legal status (individual, government-owned-enterprise, corporation etc), what’s in the custody account, what it’s used for etc.

While Belgium jumped to the forefront back in 2014, when US Treasuries held in custody accounts were worth over US $300 billion, it has long been used by extra-EU corporations, chiefly from East Asia, to stash part of their offshore profits in US Treasuries held in anonymous custody accounts.

However a number of governments have been suspected of using anonymous custody accounts domicialiated in Belgium, especially when large scale movements register on the charts: buying and selling US Treasuries through Belgium is seen as more discrete than doing so directly and usually by the time temperamental financial markets notice the transactions are long completed.

Informative article, thank you.

“The US government (pension funds, Social Security, etc.) raised its stake by $263 billion, bringing “debt held internally” to $5.73 trillion, or 27.0% of the total.”

However, isn’t the SS trust fund shrinking now?

Their roll-offs must be in excess of any new purchases.

I’m still not sure what the advantage is to foreign countries of holding Treasuries. The plan seems to be: use various methods (currency manipulation and protectionism) to build up a large trade surplus. Use that surplus to buy treasuries. Then, when your currency starts to weaken, frantically sell off those reserves to defendant the currency. Americans are constantly lectured to by economists about the advantages of free trade, but they never seem to mention the pointlessness of it all.

->Who Bought the $1.36 Trillion of New US National Debt over the Past 12 Months?

Oh gee, the world’s biggest debt peon doesn’t really care who enslaves it so long as they kick back some campaign contributions. Even the biggest scams have overhead costs, ya know. Loyalty oaths and NDAs not required.

Federal debt is issued in 30yr maturities. According to the yield curve banks who want to borrow at the short end and lend at the long end will soon be underwater on rates. We are clearly at the end of times, and if you choose to believe that widows and orphans are paying for the new massive spending without revenue, you could also believe without straining your credibility at all, that those bonds are off balance sheet.

Isn’t “everything” “….off balance sheet”? Nowadays????? LOL!!

No real “Mark to Market” rules anymore since April ’09???? Wwwhhheeeeeeeee!!

But banks don’t lend for 30 years at the 30-year Treasury yield. Many credit card rates are in the double digits and plenty go beyond 30%. 30-year fixed-rate mortgages start at around 4.6% and go up from there. The best 5-year Auto loans are at about 3.5% and up.

Banks’ average cost of funding is still below 1% as many deposits still carry near-zero interest rates.

Banks’ net interest rate margins bottomed out in Q1 2015 at 2.95% and have since risen to 3.23% (Q1 2018).

So the reality for the banks in this interest rate environment still looks pretty good, whether or not the yield curve flattens or even inverts a little.

Two problems with the banks, one is they are lending to the USG, and that spending is historically past its limits. The Fed is paying them to borrow at higher rates. Its great to have a higher marginal rate if there’s anyone on the other end. Banks were refusing high value depositors (Chase) now they’re refusing cash (BoA), and some places are banning Visa. Turkey to Paribas to The Bank of the West.

Wolf, I have a bit of a different take on this…I won’t rewrite a recent article here but I believe the picture is a bit different than you paint. Welcome to read.

Regards

https://econimica.blogspot.com/2018/08/economic-fear-mongeringchina-to-disrupt.html

You didn’t even read my article, it seems, from what you said. You just used this opportunity to promote your own blog post :-]

Wolf, I read this one and quite a few others you’ve written recently on the Fed’s balance sheet. I was trying to politely disagree with your conclusions…but nevermind.

You STILL didn’t read the article, apparently. This article isn’t about any of the things you mention in your own article. I simply reported who exactly bought the $1.3 trillion in new Treasuries over the past 12 months (this is historic data).

The article just reported the numbers — not my own opinion, theory, or forecast, and there was nothing in this article that would lend itself to “disagree” with me, or offer a “different take on.”

If my numbers were wrong, you can point that out, but you did not.

In your own post, you discuss a whole slew of other things and projections far into the future and demographics and what not that have zero to do with the historic data I reported.

If you “disagree” with me, you need to point out why and how, and not use this phrase to promote your own unrelated stuff.

So, who says “Buy Made in the USA” is dead?

That right right, we sure know how to very efficiently mass-produce large amounts of debt :-]

“reverse factoring” ?????

When I was involved in factoring it was effectively financing outstanding invoices to a loan shark.

so “reverse” suggests financing product not yet produced or invoiced in the hope it one day will be???

The answer to your title question Wolf is “suckers.”

I’m not so sure. Short-term Treasuries are starting to look pretty good at those yields. A few more rate hikes later, they’ll look even better :-]

Good point, though I wonder if Fed subsidized rate hikes are sustainable, but what if real market rates are higher? LIBOR has pulled back a few bps, which might cast some light on the Feds position on future rate hikes.

Wealthy Americans that don’t pay a lot of taxes bought that debt

All parts of that pie are cronies except the individuals. I would like to see a slice of just individuals. Its probably a house of cards.