Mopping up liquidity.

The Fed’s QE Unwind – “balance sheet normalization,” as it calls this – is accelerating toward cruising speed. The first 12 months of the QE unwind, which started in October 2017, are the ramp-up period – just like there was the “Taper” during the final 12 months of QE. The plan calls for shedding up to $420 billion in securities in 2018 and up to $600 billion a year in each of the following years until the balance sheet is sufficiently “normalized” – or until something big breaks.

Treasuries

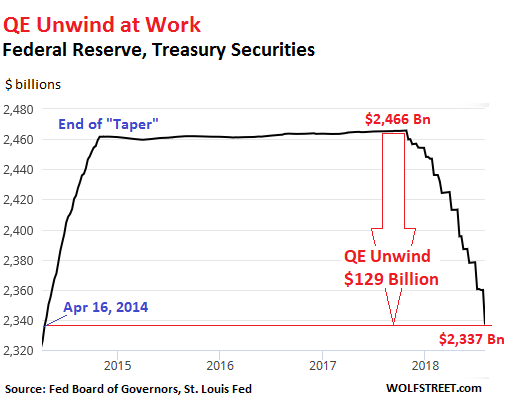

In July, the QE Unwind accelerated sharply. According to the plan, the Fed was supposed to shed up to $24 billion in Treasury Securities in July, up from $18 billion a month in the prior three months. And? The Fed released its weekly balance sheet Thursday afternoon. Over the four weeks ending August 1, the balance of Treasury securities fell by $23.5 billion to $2,337 billion, the lowest since April 16, 2014. Since the beginning of the QE-Unwind, the Fed has shed $129 billion in Treasuries.

The step-pattern in the chart above is a result of how the Fed sheds Treasury securities. It doesn’t sell them outright but allows them to “roll off” when they mature. Treasuries only mature mid-month or at the end of the month. Hence the stair-steps.

In mid-July, no Treasuries matured. But on July 31, $28.4 billion matured. The Fed replaced about $4 billion of them with new Treasury securities directly via its arrangement with the Treasury Department that cuts out Walls Street (its “primary dealers”) with which the Fed normally does business. Those $4 billion in securities, to use the jargon, were “rolled over.” But it did not replace about $24 billion of maturing Treasuries. They “rolled off.”

Mortgage-Backed Securities

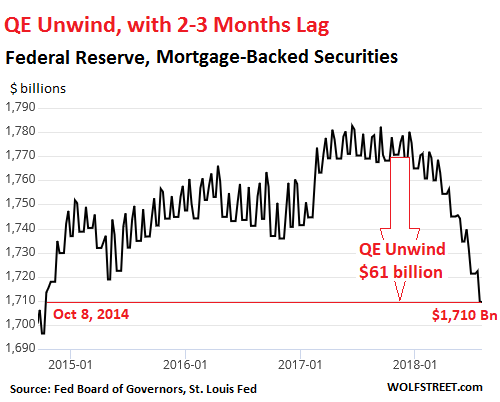

Under QE, the Fed also bought mortgage-backed securities, which were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Holders of residential MBS receive principal payments as the underlying mortgages are paid down or are paid off. At maturity, the remaining principal is paid off. So, to keep the MBS balance from declining on the Fed’s balance sheet after QE ended, the New York Fed’s Open Market Operations (OMO) kept buying MBS.

Settlement of those trades occurs two to three months later. Since the Fed books the trades at settlement, there’s a lag of two to three months between the date of the trade and when the trade appears on the Fed’s balance sheet [here’s my detailed explanation]. This is why it took a few months before the QE unwind in MBS showed up distinctively on the balance sheet.

The current changes of MBS on the balance sheet reflect trades from about two months ago. At the time, the cap for shedding MBS was $12 billion a month. And? Over the past four weeks, the balance of MBS fell by $11.8 billion, to $1,710 billion as of August 1, the lowest since October 8, 2014. In total, $61 billion in MBS have been shed since the beginning of the QE unwind:

Total Assets on the Balance Sheet

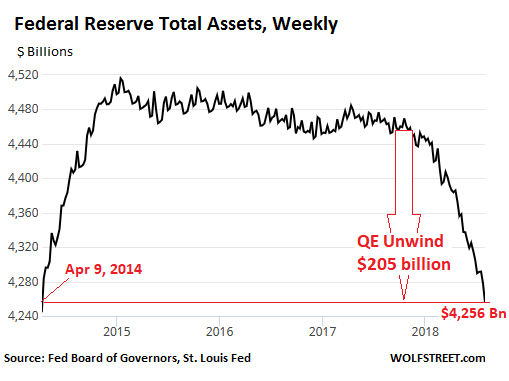

QE only involved Treasuries and MBS. And so the QE unwind only involves Treasuries and MBS. Since the beginning of the QE Unwind, Treasuries dropped by $129 billion and MBS by $61 billion, for a combined decline of $190 billion.

But the balance sheet of the Fed also reflects the Fed’s other functions and activities. And the decline in the overall balance sheet is not going to reflect exactly the amounts shed in Treasuries and MBS.

Total assets on the Fed’s balance sheet for the four weeks ending August 1 dropped by $34.1 billion. This brought the drop since October, when the QE unwind began, to $205 billion. At $4,256 billion, total assets are now at the lowest level since April 9, 2014, during the middle of the “taper.” It took the Fed about six years to pile on these securities, and now it’s going to take years to shed them:

So the pace of the QE Unwind has accelerated in July, as planned. The Fed has not blinked during the sell-offs in the market, and it’s not going to. It is targeting “elevated” asset prices and financial conditions. Asset prices remain elevated and financial conditions remain ultra-loose. Markets have essentially brushed off the Fed so far. And that only acts as an encouragement for the Fed to proceed.

The FOMC, in its August 1 statement, mentioned “strong” five times in describing various aspects of the economy and the labor market – the most hawkish statement in a long time. Rate hikes will continue, and the pace might pick up. And the QE unwind will accelerate to final cruising speed and proceed as planned. The Fed stopped flip-flopping in the fall of 2016 and hasn’t looked back since.

When the economy eventually slows down enough to where the Fed feels like it needs to act, it will cut rates, but it will let the QE unwind proceed on automatic pilot toward “normalization,” whatever that will mean. That’s the stated plan. And the Fed will stick to it – unless something big breaks, such as credit freezing up again in the credit-dependent US economy, at which point all bets are off.

Use of a financial instrument called “reverse factoring” has ballooned. No one knows to what extent because there’s no disclosure. But it was a “key contributor” to the sudden collapse of outsourcing giant Carillion. Read… “Hidden Debt Loophole Could be Widespread”: Fitch

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Fed increased it’s balance sheet 400% from 2008 to 2018. It has since dropped it by a miniscule 5%. “Normalization” will never happen.

Do you think the Fed should dump in one month the $3.4 trillion in assets it bought over a period of 6 years of QE? This would be totally nuts!

It took the Fed six years coming, it’s going take it years going. So be patient, it’s happening. The other thing you can do is fight the Fed. Good luck with that.

BTW, if you look at the historic data of the Fed’s balance sheet, you will see that over the five years from Jan 2003 to July 2008 (before QE), total assets rose from $720 billion to $920 billion: $200 billion in five years. Or about $40 billion a year.

Now extrapolate to see where the Fed would have been without QE in 2022. That would be 14 years since the onset of QE in late 2008. So 14 years x $40 billion a year in additional assets on its balance sheet = $560 billion. Plus $920 billion where it was in mid-2008 = $1.5 trillion.

So, using the historical trends before QE, the balance sheet assets would be at $1.5 trillion in 2022. Some of the Fed heads have suggested that a reasonable level might be just above $2 trillion by the end of the QE unwind when “normalization” has been achieved. This wouldn’t be much above the historical pre-QE trend.

How has this changed? Compare this to Bernanke (and Wall Street) who said not too long ago that the Fed would NEVER shed any of these assets. So stay tuned.

Wolf, this has been going on for almost a year – they should have mopped up much more liquidity by now.

Assets are dangerously inflated. The S&P yields a miniscule 1.6% (well below the rate of inflation) and house price inflation has put home ownership out of reach of all but the very wealthiest first time buyers. The Fed created a mess, have done almost nothing to unwind it and are already starting to suggest they may have gone far enough (saying monetary conditions are reaching a neutral level).

The stock market doesn’t seem to indicate monetary conditions are tight – quite the opposite.

The Fed removed 200 billion in a few months, Facebook removed 100 billion in a few hours.

There is a chorus coming from the financial advisers, pundits etc. that this is time to be cautious. Maybe it’s time to rotate out the FAANGS.

Into what? Coffee or burger chains? Yoga bras?

Even World War Two began with 8 months of almost no engagement between the majors. There is usually a calm before the storm.

This market can go sideways for a few months but at some point it’s going to occur that 250 times earnings is too much to pay for a warehouse and delivery outfit, no matter how big it is.

The only reason to buy the stock is the belief it will go up.

Absent that belief, which can evaporate in one day, it’s worth whatever profit it earns: so to be generous, the PE would be more like 25.

On my theory of an impending 1929 type implosion, even I was taken aback by WR’s call for the SEC to investigate Tesla.

Van, well said, especially the part about home ownership. I’ve said it before, I have 180k cash and make 72k a year. I live in San Diego. I have a credit score of 820 with no debt. I can’t afford a house here and I’ve seen my cash lose value. I don’t just put the blame on the government, I also blame greedy Americans and greedy American corporations. Don’t tell me to move, I love SD (born and raised here) and my family is here including Mom and dad and my 5 grandkids. I keep plugging though, I have a great job and wonderful life. I just really want my own home. Thx for listening.

Another good update Wolf.

What is a normal fed balance sheet? Normalization is like pornography: we’ll know it when we see it.

That is to say, the balance sheet will be said to have been normalized when the Fed decides to stop normalizing.

Unless it pauses.

The linear and paltry gradual methodology of the normalization has always been designed to sustain asset inflation.

If they had any goal of financial stability; they would have been shedding MBS at much greater amounts 3 years ago.

That course would have created stability and mitigated bubble dynamics. Obviously, this course runs averse to the ongoing detrimental financialization of the economy.

They will never materially reduce the BS before the next crisis causes further MBS purchases. I just hope the Fed doesn’t start accepting securitized auto loan for treasuries.

Thx Wolf

I wonder if “reverse factoring” will join the lexicon of, credit default swaps, credit default obligations, sublime, and derivatives?

Reverse factoring, another debt , so zombie companies can limb along a bit longer.

Step right up, one born every minute and two to took to take your money. The circus continues,for the show must go on.

Despite the QE unwind, money supply measures like M2 and MZM have still been increasing since Oct, 2017. So commercial bank credit creation, and/or something else, is more than offsetting the Fed’s draining operations.

Bank lending always increases in an expanding credit-based economy unless there is a recession. If bank lending contracts, it’s a sign that a recession is already in progress — and a contraction in bank lending can cause a recession (via a credit crunch).

“And the Fed will stick to it – unless something big breaks, such as credit freezing up again in the credit-dependent US economy, at which point all bets are off.”

Aren’t the chances of something big breaking quite high, especially with a trade war ending the flow of dollars worldwide? There are so many potential crisis points it’s hard to keep track of all of them, and all it takes is one to start a worldwide panic. There’s no such thing as a local financial crisis anymore.

->There are so many potential crisis points it’s hard to keep track of all of them, and all it takes is one to start a worldwide panic.

The disease theory of global finance. Haven’t lost the patient yet, but it’s not through a lack of trying.

The system doesn’t work for most people, but it does hold up despite all the distortions and corruption, more or less. That’s a clear sign that it’s still overregulated, and hence the need for more deregulation.

->There’s no such thing as a local financial crisis anymore.

That’s not exactly true. All my financial crises are local. They never start out that way, though. If I could just figure out how to keep the national and global crises from spilling over into my local economy, I’d be all set. I’ll let you know the next time it happens, assuming any of us are still here.

Here’s Bernanke arguing against QE unwind as recently as 2016.

https://www.brookings.edu/blog/ben-bernanke/2016/09/02/should-the-fed-keep-its-balance-sheet-large/

We should all be thankful he is no longer running the Fed.

->We should all be thankful he is no longer running the Fed.

Bernanke doesn’t suffer from financial crises. Maybe he’s smarter than we think.

Bernanke is a corrupt scoundrel working at a high frequency trading firm. My opinion of high frequency trading is it exists solely to manipulate market prices to steal money from investors. Even if my assessment is not exactly correct I don’t think anyone would deny that high frequency trading relies on skimming money from investors to make profits.

So here we have the Ex Fed Head profiting from unethical, corrupt behavior (only legal because the system is corrupt) and no part of the finance system says “no, you can’t do that”. Anything goes, nothing is beyond the pale, we have problems we are not confronting. This stuff needs to be illegal and lawbreakers need to be prosecuted – enough already!

Stay out of their sandbox. Buy gold coins.

Rich bankers don’t suffer from financial crisis. Thus, you’ve only proven that the head of the Fed was a rich banker.

That’s the whole problem right there, isn’t it? Rich bankers should suffer first and most, since they’re the cause. Instead they’re rewarded, which can only mean that the incentives are completely backwards.

Who could have known that fixing the global financial system could be so simple? It’s implementing the repair that eludes us.

I hate to say this, but I’ve seen no evidence that Bernanke has the horsepower to understand the consequences of his proposals. There seems to be a lack of common sense there, which he mistakenly calls “courage”.

The basic failure, of course, is failure to recognize asset bubbles, wealth inequality, and related financial instability.

He owns this next recession. Hopefully it won’t be a 20 year depression.

In his paper linked above, Bernanke proposes a permanently large Fed balance sheet. He fails to address key issues associated with that. For example, it would result in moral hazard, financialization, low productivity, permanently high asset prices, no upward mobility, continued wealth inequality, and permanent bondage for the bulk of society. No mention of any of that in his article. I call that academic tunnel vision.

two thumbs up to you sir!

Theft is courageous. That, I’ll give him.

Remember that the Fed is private and owned by for-profit banks, so don’t go confusing their motives. I believe that the Fed is at no risk of suffering losses in regards to its assets no matter which way things go. Talk about “TBTF”. Maybe they have decided that they own enough, that systemic failure is inevitable at this point, and that a smaller asset book would be more manageable as far as bail-ins and the like go.

Perhaps Powell has more virtuous motives than did Bernanke, but I don’t think that anything Bernanke did was accidental. He wanted the Fed to be at the center of everything, with total dictatorial powers. Having said that…..don’t trust Powell or believe that he is doing things for the reasons he says.

So the Fed has unwound 5% in roughly 1 year. 19 more years!!!!

BS. Why don’t you read the article and do some basic math (addition) before you post such mind-boggling obliterating nonsense on this site.

The Fed will shed close to $400 billion this year and up to $600 billion a year, starting in 2019. By 2022, it will have shed between $2 trillion and $2.5 trillion (there are some technical reasons why the roll-off will slow down as assets are drawn down), and the balance sheet will be down to around $2 trillion.

As I mentioned above, if the Fed had never done QE, the growth of the balance sheet, at the pre-QE rate of $40 billion a year, would have taken the balance sheet to $1.5 trillion by 2022. In other words, by 2022 or 2023, the balance sheet will be close to normalize, and the QE unwind ends.

Doing rough estimates in my head, those numbers say that the 6 years of QE Windup need about 6 years of QE Unwind to reverse the rubber band.

“By 2022, it will have shed between $2 trillion and $2.5 trillion”

You seem to be counting, as certain, something that would appear to have only a remote chance of occurring.

We are all entitled to our opinions (and lest you accuse me of BS, or not reading the excellent and interesting article, I provide this is only my perspective) and the reality I have experienced, over the last 10 years, leads me to the opinion that the balance sheet could easily be pushing 10 trillion by your date and will never have reached anything close to 2 trillion.

The is a very good chance that by 2022 trillion will not have the significance it has today. If the Fed loses control, and ignites a currency crisis, a trillion could conceivably be minimum wages for a year – no one has a crystal ball so I wouldn’t count Fed chickens that are still only egg yokes.

Wolf please calm yourself. The economy is so distorted i don’t know where to begin except to say the Fed is clueless.

Whoo!! Seldom does the Wolf howl at a provocateur. LIKE!

Commercial banks still have about $2T of excess reserve parked at the Fed. As the Fed sells down its Treasury holdings at this leisurely pace, wouldn’t those be mostly gobbled up by the commercial banks? For them it would be a simple matter of swapping Fed funds with Treasuries on the asset side of the balance sheet. After all, Basel 3 says that the banks won’t need to add equity capital for holding Treasuries. They also don’t have mark Treasuries holdings to the market.

QT could have a less effect than many predicted, at least until excess reserve is sufficiently drained.

I read recently an article that described how banks buy U.S treasuries. It appears that banks, since the crisis, can buy treasuries with NO reserve ratios, and NO mark to market? So, they can buy trillions of securities without putting up a penny of their own money and they get to cut the coupon. IF the price drops, so what? Basically, “they” are todays quantitative easers.

If this is truly the case, then maybe the Japanese model is where we need to be – cut out the middle man – simply allow banks to print money to buy treasuries at near zero. Why should taxpayer pay 3%? The larger the federal deficit, the greater the inflation.

It’s a new twist and I am trying to understand the ramifications.

(if I could buy $1T treasuries w/o having reserves, w/o mark to market, I would buy regardless of yield. Cut the coupon and enjoy free money)

If the price of a Treasury drops, you just hang on to it till maturity, collect the coupon as you go and then when it matures, you get face value.

The closer the maturity date gets, the closer to face value the security trades at. So a 10-year Treasury with one year left before it matures trades like a 1-year Treasury, and its market price is going to be close to face value.

So if a bank bought at face value, it’ll get all its money back at maturity. That’s in addition to the interest. Currently the 2-year yield is about 2.65%. Not too shabby. There is near-zero credit risk on Treasuries.

The Fed allows the banks to hold treasuries AT zero risk with zero reserves. This is pure counterfeiting. The larger the U.S deficit, the more QE we get – from the banks this time.

https://www.bis.org/publ/qtrpdf/r_qt1312v.htm

When a treasury rolls off the Feds balance sheet by maturing, the Treasury must redeem it for face value and interest. To obtain the money to redeem the note, the Treasury must have to issue new bonds in the continuing Ponzi scheme that goes on in the US. That likely helps to explain the explosion in new issues by the Treasury as they scramble to cover their expenditures for QT as well as Trumps record spending.

Near zero credit risk? I hope your right.

Yes, but it doesn’t mean that they won’t deflate the debt to smithereens via inflation :-]

After the crisis John Stewart referred to this as banks buying dollars at a cost of only 97 cents and having an endless supply of 97 cent pieces.

What he said rings true on an individual basis, but it’s actually idiotic. Any bank CEO I hire who is content buying dollars for 97 cents when they can be had for less will be shot on the spot.

Steve, Why would you, as a shareholder, own a bank that is content to only buy Treasuries when the bank exists to create a return on investment that is better than treasuries?

I wouldn’t.

The only limit a bank typically has on money creation is reserve requirements. Since 2008, US treasuries have (BIS) 0% chance of default and therefore no reserves required. WTF? THEN they take away “mark to market”? So, this creates a system whereby the bank then has the ability to print as much money as they want AS LONG AS it goes to buy UST.

The dumb part is this: IF the banks are going to print the money to buy UST, why pay 3%, get rid of the facade and go the Japanese route, take out the middle man and pay near 0%. With total debt servicing costs approaching a trillion dollars in the next few years, it only makes sense. Issue the debt, buy at 0% and save the taxpayer a trillion or so.

As part of the trade war, Trump should offer to buy ALL U.S paper owned by China – why give them $100B “free money” every year.

The whole fiat world is ridiculous.

I love it when money dies.

Money never dies. It moves to Switzerland and retires.

Then gets transferred to a trust fund for the next generation to hold onto it, you know. For safe-keeping.

Something I’m really interested in: how do you think QE unwind + rate hike is going to affect corporate debt market?

As far as I understand, lots of debt will mature on the next one to three years, meaning debtors will probably have to refinance. At which point the conditions for lending will worsen. Tightening credit rates + tightening economic conditions = perfect storm? Did anybody do at least ballpark estimate for this kind of stuff?

Wolf,

You should write an article on how the Treasury Dept. structures its debt auctions. This topic doesn’t receive enough attention in the media. The government has funding needs, but how is the decision reached to borrow at the various short and long maturities? Treasury interest rates set a “risk free” rate floor for the rest of the banking system. Politics probably plays a role; if they borrow a lot more at the long end will this force up interest rates for mortgages and crash the housing bubble?

Interesting (hehe) topic. For example, why are the short-term debt auctions early in the week (Tuesday) and then the longer term ones later?

I’ll keep it in mind.

The thing with Treasuries is that this is the most liquid bond market in the world. What happens at the auctions can be off a little from the market, but not a lot. From my perspective, it’s the market that drives what happens at the auctions in terms of yields, and not the other way around.

But you’re correct about the choice of Treasuries to be sold. For example, there are all kinds of reasons, including cash management reasons, to sell short-term bills. I get that. But right now, with 10-year and 30-year yields so low, why doesn’t the Treasury Department load the market up with long maturities? That would be great for the taxpayer, who ends up having to pay the interest.

In their announcements, you always get the standard fare, but it really doesn’t explain sufficiently why they’re choosing specific maturities.

What a strange concept….. the notion that the US government would do something that is good for the taxpayer.

From the perspective of a taxpayer, it would be great to lock in low rates on debt for 10 or more years. But what would be the political consequences if Treasury sold a bunch of long dated debt, and then the institutions who hold it are left with bonds whose principal gets cratered by a further rise in rates and/or inflation? With both possibilities of inflation and a rise in rates, maybe the market for long dated debt is more sensitive to a minor jump in auction size by Treasury? An economy that lives and dies on debt and interest rates is a complicated system to say the least.

I see the incidence of the word “Liquidity” was used only once in the heading of the first para. That’s okay, the term “mopping up liquidity” goes back to Greenspan, and I suppose even he knew it wasn’t a relevant term. It’s like mopping up “electricity”, a non sequitur. It does bring us back to the issue, are the effects of QE asymmetrical? (do they believe that?) If QE is asymmetrical why not make it a matter of policy? The answer to that might be yes and yes, if you consider that the US is the only central bank normalizing rates and so far corporate high yield is doing just fine. It goes to the core of what is capital formation, who does that, and what happens when bureaucrats take over? It may be that QE is not asymmetrical and we just don’t know it yet?

Similar in many ways to mopping up vomit but in the absence of karma cleanser (what goes around comes around).

The global financial and political, fundamental sovereign interactions are at the present time, negative and quickly weakening.

As usual the Fed begins to tighten into economic weakness, causing increasing stress in the markets. Don’t look beyond the mid-terms this Fall for the financial system to escape unscathed.

When 5% of investors own 80% of equities, any downturn will greatly effect the beltway elites. This group of permanently entrenched bureaucrats (which comprise the deep state), depend on the status quo continuing for their survival and will go to any length to defend it.

I’m generally a bull about the economy.I recently took a different route home through a poorer part of my city.There seems to be way more for rent signs .Granted they were small storefronts who

may be on the front lines of the online assault on physical locations .

But then again it may be a lack of access to credit for those willing to take risk that may be the cause of these vacancies. High rates and low liquidity always mess us up.

Rates are too low as it is. Risk is still totally mispriced to the low side. Easy credit and low borrowing rates are the poison that made a mess of things starting in the early 2000s, and possibly much earlier. They are poisoning us still.

Rates are low for the 1%.

Rates are too high for others.

“until something big breaks.”

Last time they accomplished this, many people lost a good percentage of their life savings. Also known as the largest transfer of wealth in human history.

Between the smoke from the Sierra fires and this article you have given me a huge headache!!

(Love your articles!)

Wolf, excellent article.

For those of you who would like to see the longer-term picture of the Fed’s balance sheet, to get a sense of what used to be normal, you can make your own graph here (for 2003-present):

https://fred.stlouisfed.org/series/WALCL

A longer term perspective, normalized to nominal GDP, is here:

https://www.stlouisfed.org/~/media/Publications/Regional-Economist/Image-Issues/January-2014/fig2_balancesheet.jpg?la=en

The latter graph suggests a “non-crisis normal” level is around 7% of nominal GDP. 2016 US GDP was about $18,600,000,000,000 (18.7 trillion dollars), and 7% of that would have been 1.3 trillion dollars. Assuming 15-20% overall growth in nominal GDP from 2016-2022, the “7% of GDP” measure is very consistent with Wolf’s estimate of 1.5 trillion dollars in 2022.

Bunch of Thieves!

Unfortunately the Fed has to fight fiscal policy, since 2011 we have had fiscal austerity, now late cycle we have fiscal expansion. That means the Fed will have to fight inflation on two fronts, and when the cycle ends there will be no money left for fiscal expansion when we need it. Idiots.

Austerity? In an environment of higher taxes, the US still piled on trillions in debt during this period. The post-crash “stimulus” was wasted on political pay-offs.

Tax receipts requires tax “payers” and there were fewer of them until recently.

Fiscal policy has been out of control for years regardless of the balance of power and for a very simple reason. The Founders tried to buttress the system against the lesser/lower aspects of human nature. We have become the kid in the candy store who can buy on credit. Meanwhile dad is broke and trying to make a living off of nothing but his family’s name.

Yes, it would be ‘nice’ if governments were responsible enough to build up some reserves when the economy is growing (i.e. at least pay down some of their debt) for the inevitable rainy recession days.

But hasn’t the US been in fiscal expansion mode since 2001? See https://en.wikipedia.org/wiki/National_debt_of_the_United_States#/media/File:US_Federal_Debt_as_Percent_of_GDP_by_President_(1940_to_2015).png

As in Britain fiscal ‘austerity’ was more jaw-boning spin than bottom line substance.

You can easily see the deficit was cut hugely reaching a third of the size of the financial crisis https://fred.stlouisfed.org/series/FYFSD

This is our big debt problem in a nutshell. We’ve started calling a reduction in the extra amounts we borrow each year (fiscal) austerity.

Call me old-fashioned, but to me austerity is when you actually reduce your outstanding debt, which you can easily see on your graph hasn’t happened since 2001.

////

I find it hard to believe that the unwind will be able to keep pace for long. With the debt ballooning, how much US treasuries can the market absorb?

////

This also makes the USA very voulnerable to foreign influence…think of it, China, Russia, Japan, EU, they only need to stop buying treasuries, they don’t even need to dump anything.

//// (Disclaimer: conspiracy theory in next line)

If my model is correct the next big financial crysis will be wallstreet triggered just after the next presidential election. The government is weakest during the transition period…2020, here we come.

////

Concerning line 1 and 2: Rising yields make US Treasuries more and more attractive to new buyers (though folks who bought a while back aren’t so happy). Right now there is so much demand for the longer maturities that the 10-year yield can’t get above 3%. Much of this is domestic buying.

The market will always “absorb” all Treasuries. It’s just a question at what yield. If the yield is high enough, Americans (individuals and institutions) will gobble them up. No foreigners needed.

The real question is: at what 10-year yield is the economy going to get hit because credit gets too expensive? So there is a fine line between having attractively priced bonds and a credit crunch where lending dries up.

Please correct me if I’m wrong. Wasn’t QE (kind of by definition) about the Fed purchasing treasuries? Meaning the market wasn’t able to absorb what was offered so the Fed had to step in?

Yes, I will correct you :-]

The market was able to absorb the Treasuries just fine. QE was about the “wealth effect” — driving up asset prices across the board (housing, stocks, commercial real estate, bonds, classic cars, art…) to make asset holders wealthier so that they might spend a little more and boost the economy. Bernanke himself explained this in an editorial to all Americans in 2010:

http://www.washingtonpost.com/wp-dyn/content/article/2010/11/03/AR2010110307372.html

Wolf, I beg to differ on one part of that.

I wouldn’t say Bernanke explained his intent to inflate asset prices to “all Americans” by putting a piece in the Washington post. I don’t remember seeing that. I doubt Average Joe saw that. When you want something to be heard, you don’t write a single piece in the Washington Post, which is a paper 99% of Americans don’t read. I don’t remember the message being disseminated throughout the country. Obviously, if everyone knew the Fed was going to pump asset prices until bubbles appeared, everyone would have bought stocks or RE. Everyone did not. I submit the message was mainly received by sophisticated firms and their wealthy clients.

This is the problem with the Fed. They transmit their actions through Wall Street. Average Joe only figures it out when he can’t buy a home because prices have risen too high. There’s a reason fire alarms are loud. Bernanke used a dog whistle that only his Wall Street friends would hear. That may have been inadvertent, but it highlights the fact that the Fed isn’t geared to conduct monetary experiments They make cryptic communications, pick winners and losers, and they mess things up in grand fashion.

If the goal was to create more purchasing power, the proper way was to hand out tax rebates. At least Average Joe gets a piece of that. This ensures important policies that impact the wealth of populations are conducted by legislators, not unelected officials.

Bobber,

You’re correct about “all Americans.” What I meant to say is that this wealth transfer to asset holders was the stated and explicit purpose of QE (rather than any perceived need to prop up the Treasury market, which is what the question had been that I responded to).

Also, as you can tell, I won’t let Bernanke’s editorial die. In case the WaPo pulls it and it disappears from the Internet, I have a copy of it on my computer and in my off-site backup so that this ignominious statement of intent by Bernanke to make asset holders richer at the expense of everyone and everything else can live for as long as I get to live.

Long live Wolf!!!!

I have been the biggest critic of the Fed since Tim Geithner was the NY fed governor. But I have to give them credit. They’re staying the course and finally doing the right thing. They’ve even adapted to the stupid things happening on the fiscal side (cutting taxes and increasing deficits when the economy is at full speed) by accelerating interest rate hikes.

I’m just curious how large parts of the market think this is still the old Greenspan or Bernanke Fed that would jump anytime the market complained. They should be bracing for the coming shock.

I do think part of the reason we’re not seeing much effects yet is because of banks’ excess reserves. However, as liquidity continues to be drained and credit requirements for a growing economy increase, this excess will soon be gone.that’s when I expect more rapid corrections in the market.

Yes, but it doesn’t mean that they won’t deflate the debt to smithereens via inflation :-]

“QE was about the “wealth effect” — driving up asset prices across the board (housing, stocks, commercial real estate, bonds, classic cars, art…) to make asset holders wealthier so that they might spend a little more and boost the economy.”

It sounds so simple but it’s still central planning. Winners and losers are picked and free-market forces cease to operate. Proceed at your peril. We’re not in Kansas anymore.

So, when are we going to see inflation at 10% + per annum, that is genuine?

Rate hikes, QE unwind, student and auto loan defaults rising. All point to deflation, inpsite of official figures claiming there’s inflation of 2.7%?

you know the reason they don’t sell more 10 and 30 year bonds is they believe once their tighting breaks something they’ll then go to negative interest rates. If Martin Armstrong is right their gonna be in for a rude awakening !

And meanwhile, as the ECB, BOJ and FED close the spigot of free cash, the Chinese open the fire-hose.

https://www.zerohedge.com/news/2018-07-18/china-launches-quasi-qe-support-banks-and-sliding-bond-market

Brace yourself for another tsunami of cash flooding the California coast.

And yet, the Fed is still WAY behind the curve. Dimon says we should be at 4% on the 10 year treasury, and no one should be surprised when it hits 5%. We haven’t had “normal” monetary times for over 18 years now, and so we’ve now become accustomed to the expectation of easy money. Its now a ‘horror’ to think of rates at 5%. This stock market is merely reflecting the trillions printed up out of thin air. There is no level of fear whatsover, despite Buffet’s favorite warning indicator where stocks are at 140% of GDP, virtually the same as in the year 2000. Honestly, that indicator is warped due to QE. Putting this in perspective, the inflation adjusted high in todays dollars for gold in 1980 is $16,500. This is not the highly manipulated CPI based adjustor. Look at the price of cars. A used piece of crap with 100000 miles on it, goes for between $8000 and $40000 depending on model. New car prices are obscene. Spamazon’s PE ratio of 144 is a joke. Its more like over 1000. Its all heavily manipulated, and that is the scary part of all of this. We are being told all is ok, despite high P/E ratios that are a result of fantasmic manipulations. (meaning reality is that they are actually much much higher, when you take out all the ‘one time’ events etc.) Why do people keep their money in this gambling pool ? because interest rates and easy money policy have so distorted everything that now nobody really knows what ‘normal’ should be.

Powell, keep raising them interest rates,higher , faster and unwind the balance sheet faster. It will be beautiful . The high priest at the Federal Reserve’s Eccles temple should not be meddling in the free market. Get rid of these socialist, Keynesian fools.