With a sense of urgency. No more dilly-dallying around.

The Fed’s balance sheet for the week ending January 31, released this afternoon, completes the fourth month of QE-unwind. And it’s starting to be a doozie.

This “balance sheet normalization” impacts two types of assets: Treasury securities and mortgage backed securities (MBS) that the Fed acquired during the years of QE and maintained afterwards.

The Fed’s plan, as announced in September, is to shrink the balances of Treasuries and MBS by up to $10 billion per month in October, November, and December 2017, then to accelerate the pace every three months. In January, February, and March 2018, the unwind would be capped at $20 billion a month; in Q2, at $30 billion a month; in Q3, at $40 billion a month; and starting in Q4, at $50 billion a month.

According to this plan, balances of Treasuries and MBS will shrink by up to $420 billion in 2018, by up to $600 billion in 2019, and by up to $600 billion every year going forward until the Fed deems the level of its holdings “normal.” Whatever this level may turn out to be, it will be much higher than the level suggested by the growth trajectory before the Financial Crisis.

For January, the plan called for shedding up to $20 billion: $12 billion in Treasuries and $8 billion in MBS.

So how did it go?

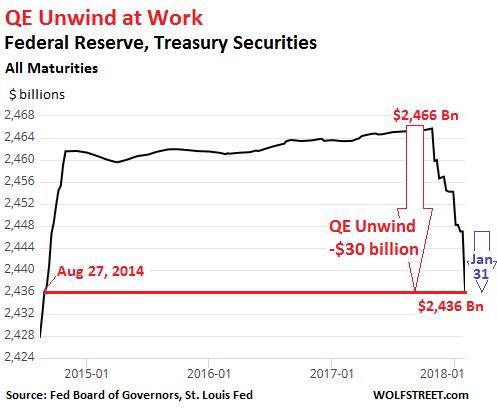

On its December 27 balance sheet, the Fed had $2,454 billion of Treasuries. By January 31, it had $2,436 billion: a drop of $18 billion in one month!

This exceeds the planned drop of $12 billion for January. But hey, over the holidays, most folks at the New York Fed, which does the balance sheet operations, were probably off and not much happened. And so this may have been a catch-up action, with a sense of urgency.

In total, since the beginning of the QE Unwind, the balance of Treasuries has plunged by $30 billion, to hit the lowest since August 27, 2014. This part of the QE Unwind is happening:

The jagged down movement in the chart is a result of the way the Fed unwinds its QE. It does not sell the securities. It allows them to “roll off” its balance sheet. It works this way:

Treasuries mature in mid-month and at the end of the month. For example, on January 31, about $27 billion of the Fed’s Treasuries matured. The Treasury Department redeemed those securities (normal bondholders would be paid face value). But the Fed has a special arrangement with the Treasury Department that cuts out the middlemen.

To maintain the level of Treasuries, the Fed would “roll over” these securities directly with the Treasury Department – replacing maturing securities with new securities.

But under the QE unwind, the Fed allows part of those securities to “roll off” rather than allowing them to “roll over.” In other words, the Fed does not replace some of the maturing securities and instead gets paid for them.

Of the $27 billion in Treasuries that matured yesterday, the Fed “rolled over” $16 billion (replaced them) and allowed $11 billion to “roll off” (got paid for them). The blue arrow in the chart above shows this big one-day move.

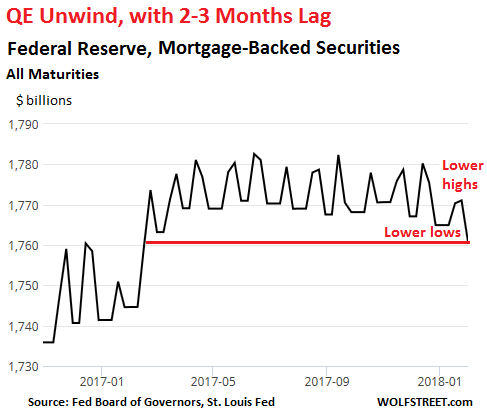

MBS: a jagged line and a lag of two to three months.

The Fed acquired residential MBS guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae as part of QE. Now, it’s supposed to shed them at a pace of $4 billion a month in Q4 last year and $8 billion a month in Q1 this year. So how did it go?

Residential MBS differ from regular bonds. The issuer (Fannie Mae et al.) passes through principal payments to MBS holders as underlying mortgages get paid down or get paid off. Thus, the principal shrinks in uneven increments until the remainder is redeemed at maturity.

To keep the MBS balance steady, the New York Fed’s Open Market Operations (OMO) buys MBS in the “to-be-announced market” (TBA market). The actual MBS is not designated at the time of the trade but will be announced 48 hours before the established settlement date, which can be two to three months later.

The Fed accounts for its MBS on a settlement-date basis. So there is a mismatch between the date the Fed receives principal payments and the date reinvestment trades settle. Hence the jagged line in the chart below.

Since MBS take two to three months to settle, the first declines weren’t expected to show up on the Fed’s balance sheet until sometime December. But since MBS balances have large weekly variations due to the timing issues, those early declines were hard to see.

This is why we look for “lower highs” and “lower lows” with a lag of two to three months, which is what we see in January, a reflection of trades that took place around November:

At the end of October, before the MBS Unwind became visible, the Fed held $1,770.2 billion in MBS, at the low point of the period. On today’s balance sheet, also the low point in the chart, the Fed shows $1,760.7 billion. From low to low, the balance dropped $9.5 billion. This reflects trades from two to three months ago. So even the MBS Unwind is now clearly visible.

In early December, I published my article with the above explanations about why we hadn’t yet seen the MBS Unwind. About a month later, the NY Fed published its own article, confirming my explanations, including the reasons behind the jagged line and that MBS take two to three months to settle.

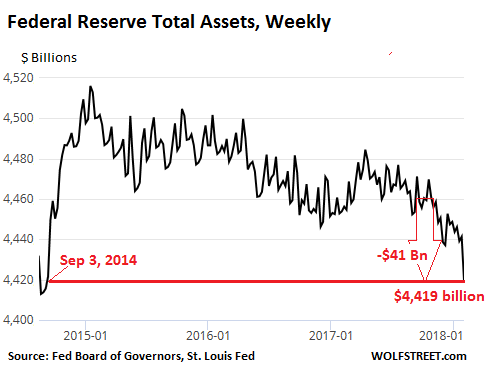

So why all this noise in the overall balance sheet?

Total assets have dropped by $41 billion since the QE Unwind began, the lowest since September 3, 2014:

But why all this noise in the chart? The Fed has other roles that cause assets and liabilities to fluctuate. Among them: it is the official banker of the US government. The US Treasury keeps its cash balances on deposit at the Fed (rather than JP Morgan). When the balance fluctuates, is causes the Fed’s assets and liabilities to fluctuate, as they would with any bank.

Similarly, the Fed holds “Foreign Official Deposits” by other central banks and governments. And the Fed has other functions that impact the overall balance sheet (explained here). But movements caused by these functions have nothing to do with QE or with the QE Unwind.

For the QE Unwind, only Treasuries and MBS matter. And the Fed is shedding them — after everyone had said for years that it could never shed them. The Treasury market may be finally paying attention: The 10-year yield closed today at 2.78%, the highest since April 2014.

Just as the Fed accelerates its QE Unwind, and as Treasuries react, the government is planning to sell a massive pile of new debt. Read… US National Debt Will Jump by $617 Billion in 5 Months

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Can’t come at a worse time. It appears as if the muppets have started to stop buying iPhones and clicking those ads. Although it appears they are stepping up their purchases on Amazon.

After reading this article it seems unwinding is more complex than buying. Buying is usually easier then selling. Try buying a new boat and then selling it a year later. Better yet, see how easy it is getting married and then what it takes to get divorced a year or more later. It’s called unwinding the marriage. And of course, everyone should know that mother’s day comes 9 month after father’s day.

Spilling $4 Trillion into a market is easy….disguised by flowery theory charts and curves…it was nothing more than a money dump.

“According to this plan, balances of Treasuries and MBS will shrink by $420 billion in 2018, by an additional $600 billion in 2019, and by an additional $600 billion every year going forward until the Fed deems the level of its holdings “normal.””

So in 3 years they will trim the balance sheet by $1.6 Trillion……

betting no…..betting they will find out that when they take the “patient” off the “machine”, the patient will die.

They’re buying fewer iPhones but they’re paying a heck of a lot more for each of them, and Apple’s revenues (in dollars) rose though unit sales declined. All of corporate America loves inflation.

its best to also show the 0 to x chart, otherwise, you lose perspective of how insignificant these accelerations are in the larger scheme of things. They are important in a directional sense, and a rate of change sense, but this isnt even the start of the beginning. (and look at the mess all this long rate related stuff is causing, despite having hardly begun in any kind of earnest.) Translation. This will end badly. WASS. (Keep yer power dry.

Yeah, the y-axis only goes from 4.4T to 4.5T. Honestly, it’s impossible to tell from these charts alone if this is anything more than noise.

Uncle Bob,

$420 billion a year is just noise? $600 billion a year just noise? Look at the steepness of the curve on the way and on the way down. It tells you the story.

When the Fed is paid for Treasuries (i.e. they don’t roll them over) – do they refund the proceeds back to Washington? (as they do with interest). Just wondering.

“When the Fed is paid for Treasuries (i.e. they don’t roll them over) – do they refund the proceeds back to Washington? (as they do with interest).”

As far as I can tell, no. Interest paid on reserve balances is a different kind of thing.

When Treasury sells a bond to the Fed, the Fed credits Treasury’s reserve account and keeps the bond. (The bond represents the right to collect money from Treasury.)

When the bond matures, the Fed debits Treasury’s reserve account, and Treasury nullifies the bond.

Even if somebody else bought the bond and sold it to the Fed, the Fed still holds the right to collect, nothing really has changed.

The Fed doesn’t keep the money it receives from a maturing bond. It “destroys” that money – just like it “created” that money during QE to buy the bond. The process of QE now reverses.

Wolf is right that the steepness of the selloff is highly suspect in that the story being told is one of a Federal Reserve dumping MBS as fast as they can possibly dump it without causing undo notice from the mainstream press. In actuality, the rate they are dumping at is indicative of panic on the part of the Federal Reserve, and it also indicates that they want that Fannie May toxic waste off their balance sheets pronto.

Market participants know it is merely old toxic waste from the 08 crash that the Federal Reserve had to take on when they took over control of the imploding Fannie Mae corporate balance sheets, and warehoused all that unproductive debt that emanated out of Countrywide Financial, Bear Stearns, & Lehman Bros.

Turns out Alan Greenspan’s 100 year storm analogy is inaccurate in light of the toxic waste MBS that the Federal Reserve now wants to dump from their balance sheets faster than your heads can spin.

Why would they be so reckless to dump at such a rate?

Will the toxic waste MBS being dumped by the Fed get bought up at the rate they are dumping it?

Who in their right mind will buy the toxic MBS being sold?

The rate of MBS dumping is wholly indicative of panicked selling.

MOU

Gee,

It took them seven YEARS to buy those assets. They’re not going to sell them in three months. They will unload $420 billion this year and $600 billion next year, etc. This is a pace that is somewhat slower than the pace with which they loaded up on them. Insignificant? Just watch the 10-year yield.

The ten year went parabolic last night

And even more after that “hot” payrolls report this morning. It’s going to be an “interesting” year.

“The ten year went parabolic last night”

That had nothing to do with the portfolio unwind and EVERYTHING to do with the change in management at the Federal Reserve in Feb.

The old guard with the radical central planning ideas to live off printed money, asset bubbles, and interest rate management are gone. Out the door. Never to return. Their ideas went bust. They’re on the run in the US. Hiding. History will call them failures and morons. The ‘financial markets’ are running for cover.

These sellers today are the ones who made it to the door and booked real gains.

The rest will follow soon and the real ginormous decline is coming because no ‘financial market’ money will return until the ‘financial markets’ perceive a bottom, or a quick buck if a few suckers tiptoe in.

US rate normalization will be one motivator. Since the big idea going bust now depended on all central banks doing the same thing at the same time, the weakest will fall next. Will it be the ECB or the BOJ or the Swiss? Regardless, they will all fall like dominoes in the coming months. It will be the biggest bust ever. By far.

I’m really looking forward to surfing that wave. I don’t think the US economy will be hurt. The massive money printers will flinch a lot. As long as the Fed provides liquidity and forces lending down the throats of the real financial market and bans interest on excess reserves, aka paying banks to not lend, the US will sail through it nicely.

Wolf,

I’m not actually disagreeing with you. I think putting it in perspective would make your case even stronger. This hasnt even started, and look at the effect! Of course, it’s not just the QE unwind affecting the 10 year, but I watch that every day and think about the various factors, as the 10 year now is critical to the housing market. We arent even back to the taper tantrum rates, when housing sale fell about 12%, before, of course, rates were rolled back.

I tend to be one with Edward Harrison on this. Short term up for the 10 year, but ultimately, when we realize the economy cant handle higher rates, back down, and during the next recession, down to 0% or negative for the 10 year. This is just the melt up recovery before the long awaited double dip. We think we are in the clear, but hardly. The financial crisis will be playing out for many years. This is the illusion part, where bullish types pretend we are past it.

To quote Gary Gordon (who often quotes Wolf):

“In the 2000 quagmire, we watched the overnight lending rate stateside go from 6.25% down to 1%. In the 2008 financial crisis, the Fed Funds rate went from 5.25% to 0%, yet that was not even enough. We also required approximately $3.75 trillion in QE stimulus.

It follows that the Fed’s normalization plans to make it to 2.75% in this tightening cycle still leaves the institution without adequate ammunition. Almost assuredly, upon hitting the zero bound on the way back down, they will be forced to employ some combination of negative interest rates and additional QE policies. The biggest winners? Those with the cash and the borrowing wherewithal to profit from a 2% 30-year fixed rate mortgage.

Remember, the 1980s served up a 10% 30-year fixed rate mortgage. We experienced the 8% 30-year in the 1990s, the 6% mortgage in the 2000s, and the 4% 30-year fixed rate mortgage here in the 2010s. Plan now to profit from the 2% 30-year fixed rate mortgage of the 2020s with a stash of 1.5-2% yielding cash equivalents.”

https://seekingalpha.com/article/4141892-state-stock-market-sotsm

The new debt goes in part to.pay the new tax cut.

I’m afraid this all is “much ado about nothing”.

Window dressing. The Fed will never significantly reduce these levels. The economy can’t handle it.

Any prediction as to what you think will be the final (“equilibrium”) balance sheet level? (Or equivalently, what will be the “Equilibrium” Fed Funds Rate/10 year bond rate?) We are probably not far from it now i bet.

As it happens, the vast majority of the Fed’s MBS holdings are of long duration and relatively recent vintage. It may be a challenge for them to reduce those holdings on the schedule they have proposed. They are apparently counting on prepayments.

ALL MBS are of “long duration.” Not replacing the principal reductions that occur with MBS is a big part of the QE unwind. It’s planned that way.

When I woke up from my ‘nap’ ten years ago I saw someone slicing and dicing MBS data. Trying to pull estimates out of my dodgy brain. Only a tiny fraction of mortgages are held for the full term. Most are paid off by refinancing or when the house is sold within ten years, maybe sooner if rates drop.

I assume if the fed just holds MBS the value falls off as the principal get repaid. If the Fed doesn’t use the repayments to buy more MBS’s then the value of their holdings declines automagically. So they can reduce their holding without having to sell anything.

I wonder whether the downpayment of principal is enough to achieve the goal in QE unwind. Isn’t there also the component of early repayments (aka refinancing) on the side of the home owners? If so, does the Fed in some way make assumptions about these refinancings in order to determine how much of the incoming proceeds from MBS should be reinvested and how much rolled off? I think refinancing activity should come down big time if rates continue to rise. So it must be extremely difficult to figure out, how much money will come back. Maybe the Fed will fall behind its schedule once refinancings fall off the charts.

Home sales (mortgage payoffs) and mortgage refinancings are included as part of the principal repayments. And you’re correct, there are lot of them. This is roughly reflected in the size of the weekly zig-zags (chart above). The down-moves are caused by repayments of principal. The up-moves occur when the Fed replaces them by buying new MBS. The magnitude of the zig-zags is a rough reflection of the magnitude of the principal repayments. If the NY Fed never replaced them, the QE Unwind of MBS would be very rapid.

Typical “duration” of 30-yr mortgage is 8 years or so.

Yield curve could explode higher and as long as the 2/10_spread is stable and stocks continue to catch a bid from fresh paper coming out of bonds ? Any hint of real infrastructure spending and basics catch a bid also? Cheap dollars create their own velocity? Professional and government funds could use an other year to blister the bears? Hogs get slaughtered/ never buy from a out of breath seller? There are 27 doors on to the exchange and one exit door!

Stocks might not catch a bid as bonds fall. Demand for LT bonds could decrease while demand for ST bonds increases. Remember, LT bond holders are looking for something safe. Stocks are nothing close to safe, even the blue chip.

The Fed had ten plus years to peddle the MBS into a negative rate environment while booking massive gains from QE? The fact that this balance sheet item is treated with neglect should be investigated! A lack of a custody chain speaks volumes about how this crap became the publics liability? Its worst than Greece and Cyprus! Ten years of booking profits from interest on excess reserves and the banks still whistle past the graveyard?

If they pull $420 billion out of the base money supply in 2018, even more will out of M2 as a result of the money multiplier operating in reverse. Could get interesting.

We saw some secondary effects today. Several stocks reported what usually would be considered positive earnings, and their stock prices dropped. Equity investors are starting to get a little nervous about valuations in a rising rate environment. I suppose the Fed would be happy to see stocks drop a good 10-20% to take the froth out.

The money supply will not be reduced because new issuance of Treasuries to pay government budgetary debt obligations exceeds the Fed unwind rate.

The QE unwind doesn’t happen in a vacuum. The US government is still spending money and the net of money not covered by tax receipts is paid for with new US debt issuance. Sadly, the national debt and money supply are expanding further, which means inflation.

Yes continuation of monetary inflation but with the consumers so overly indebted how much blood can they squeeze out of a turnip?

At some point the reality will set in. Monetary inflation with low interest rates means loss of principal unless the price continues to grow. Yet in a world where 70% of the economy is consumers buying IF much of this monetary inflation shows up in a further rising of prices of goods and services? Rather than stocks, yachts, high end real estate and art.

When is enough enough? I guess we’ll find out.

I agree. The Fed would like a gentle 10-20% decline. That is why I expect the market to react by buying every dip and getting burned for the first time in years. Incidentally, this may not be the last of the highs for this cycle IMO. Years of learned behavior to unwind. Things get interesting once traders realize the Fed doe not have their back to the same degree. Do they panic? If they do, does that panic the Fed? Also, the other CBs (cough, Japan, cough) do not appear as anxious to see increasing yields.

This is the sound of the butterfly flapping it’s wings.

Wolf,

I’m not sure if I missed this but what about all the “Offshore” money parked in US Treasuries that supposedly $2Trillion of US Corporate assets? That wants to unwind now that the Trumpy Tax bill has gone through? You know the money that Apple had and came in at $300 billion that they wanted to share with their share holders (yet) with lower rates of taxation?

Did you mention that on another blog because those guys want to pay out (just like Tim Cook does too). That surely must be putting pressure on market pricing?

This “offshore” money is unrelated to the QE unwind the Fed and has no impact on it.

The thing is, this corporate money is not “offshore” to begin with – it’s registered in a an offshore account but is invested in US assets, such as US Treasuries or US corporate bonds, or bonds of other nations too. For example, Apple manages all these investments from the US. The only thing that is offshore is the mailbox entity in which these assets are registered for accounting and tax purposes.

However, there are certain things companies cannot use this “offshore” money for without triggering tax consequences, among them: dividend payments and share buybacks. The new tax law will cut the tax consequences for this.

Cramer calls Apples 350B investment in America a “Marshall Plan”.

Wolf

Agreed, on all points. Yet when Tim Cook ( and all the rest of his ilk) wants his dividends paid out they have sell their position in the treasury market. That has to put added pressure on the bond market that is already sagging under its own weight?

Is that not the case here or is there something I’m missing?

Yes it will add pressure, but it will also relieve pressure on the other side.

Because here’s the other end of this deal: under the old tax law, Apple issued huge amounts of bonds to raise the cash needed to pay for dividends and share buybacks without having to use its “overseas” cash.

Under the new tax situation, it won’t have to issue bonds. It can just use the cash.

So in the end, if I’m looking at both sides of the ledger correctly, it will sell some investments (Treasuries and corporate bonds) BUT it will not issue new bonds for the same amount. So it looks like a wash in terms of the bond market.

I wonder if the 10 year will be at 3% by the time they pass the debt ceiling and go on a bond buying spree. They moved it up from April to March to cover the less revenue they are getting from corporate and pass-through. The payroll tables should be ready by mid-Feb. I wonder what assumptions the CBO used on additional debt service when they came up with the 1.4 trillion I don’t see them in the report https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/53415-hr1conferenceagreement.pdf

At the rate it’s accelerating we may surpass 3 % by mid February

I expect it to back off pretty soon — on the principle that nothing goes to heck in a straight line.

It’s at 2.83% now. It has been a huge move from 2.3% in Dec. At some point, the dip buyers are going to come in. That point may come any time. But I think at 3% at the latest, it will unleash a lot of buying.

Giddy over the fact there are finally some banks paying 1.5%. Transferred just a bit of my money over and it posted 1/31 so just for one day I made a bit over $3, which is far more than I’ve made per month for since the early 2010s.

Just to see that $3 change in a 5 figure account is great. Bring on the rate hikes!!!

Do you feel like you might be building your neighbor a new bathroom or soon we can throw green beer in the Chicago river and call it TEA? Has any of your neighbors stopped paying their mortgage(s) or perfectly sound businesses issued new equity? Where is Hank Paulson and his magic blackmail number? How many Jamie dimon clones exist? BTFD (the Fed can’t catch its tail alone) give them what they want a CHEAP DOLLAR and a fresh RX!

At the moment the USD is pressured by fixed income liquidation and repatriation of capital back to Europe, but I think soon as the QE unwind bites it has to rally.

https://strategicmacro.blogspot.co.uk/2018/01/us-bear-flattening-and-euro.html

Wolf –

Your site is a daily stop for me. Has been for a few years now (since the first time I visited). Articles like this are why – a great deal of information I did not know. It is bookmarked for review.

Thanks (once again), Prof Wolf!

Thanks for lucid explanation.

It’s probably too late. A systemic crisis will happen long before there is any significant wind down. When China is forced to start liquidating treasuries again as “capital outflows” pick up, the bond market will be in chaos. Forget the Asian Flu, the Asian Plague will soon be upon us.

So a lot of money is going missing at UST? I mean those bonds represent collateral received, even if it was an accounting gimmick. They will have to either float more bonds of a longer duration probably, or raise revenue somehow, after giving away a portion of their tax receipts, or cut spending. Running a deficit is easy on paper, how do you manage when the paper solutions are this difficult?

Suspicious timing as economic data is surprising many. Note that the Fed BOUGHT $4 billion in TIPS and Floating Rate Notes. Inflation fears anyone>

Sure, the largest employer in the country is an importer and they’re beginning to jettison their workforce in favor of automated hubs and online commerce.

I made a post about the recent TIP auction, which got dumped, see their website for the numbers or go here.

https://tipswatch.com/upcoming-tips-auctions/

The FLRN is also useful, and the STPZ for short term inflation trends.

It got “bumped” because it said: “The recent ten year auction they only sold about 1/3 of the amount tendered at yield a bit over 1/2%.” Which is total BS. Both 10-year Treasury note auctions over the past few weeks were oversubscribed and their yields were in line with market yields at the time (not “a bit over 1/2%” but more somewhere near 2.5% and 2.7% … I don’t remember the exact percentage.

Now, from your current comment, I can imagine that you were talking about a 10-year TIPS auction, not a regular 10-year Treasury auction. But that’s not what your comment said. There was no mention of TIPS in your comment.

It was RE: MS I realize what it looks like out of context. That yield (the TIP) was highest in a long while and the PMs got very little of it. I wouldn’t put a lot of stock in the regular Treasury auction, or the yield for that matter. The massive market for regular Treasury paper tends to create its own (wishful) destiny, and attract financial repression. (The Fed can put about just about any yield and the bond vigilantes will not slap them down, neither will the buyers (captive market) boycott much. The Fed is going to create a synthetic version of $LIBOR?? LIBOR is certainly no worse than the committee of eggheads. Or the Taylor rules, rates could certainly do as well set in turnkey fashion.

The QE unwind will drive 10yr treasury yields up, driving mortgage rates up, cooling the housing market. Home prices are at bubble levels too, so it sounds like this spring would be a good time to sell.

People should sell at a discount off the highs to close the quick sale, otherwise they’ll be chasing the market down for years. The prices drop silently before the news picks it up months later.

I agree , will be selling my home/flip in the spring . will pocket nice tax free gain after 3 years of residency .

You gonna pay inflated rent prices or buy another house at inflated prices?

Lessons from Wallstreet, they taught me well

What goes up hard and fast , comes down harder and faster

the markets lead the economy by 6 to 9 months

Bulls make money, bears make money ,pigs get slaughtered

Wallstreet loves to rip the faces off the retail muppets…quote from the

squid

bonds can break the financials

Stock market steadily drifting down …..

Will the Fed stick to its guns? Or chicken out and stop the QE unwind again, even with rising inflation?

It’s not even been 10% yet. The Fed will see 10 to 20% as “healthy”. Heck 30% down for the year would be good as long as the economy is steady.

I wonder how/if the change in leadership at the FED will affect their response time?

Sure seems to me that there is enough in place to trigger a sever sell off of both bonds and stocks. Lots of margin and lots of new borrowing on the horizon. Rising interest rates will affect the consumer much faster than commercial or government… The consumer drives the economy and when they pull back the gig is over.

We’ll just have to wait and see how this plays.

I agree, this could go much lower as stocks trade like a broken elevator mauling any new comers and causing margin calls.

What the FED has done (once again) is criminal.

It’s no fun for the likes of Warren Buffet if it goes just up. They need to buy stocks at penny on the dollar so that later they can sell the same for stock at 10 times the price they purchased it. Muppets are pigs to slaughter; they are not worthy of attention. So, they are gonna sacrifice them like sacrificial lambs ??; muppets are stupid and the stupid deserve to be sacrificed.

No, muppets don’t deserve to be sacrificed, that’s totally wrong despite it may sound politically correct to say that is an example of the many ways responsibility for injustices is deflected..

So if you’re asleep in your bed at night, I’m welcome to raid your home as long as you don’t wake up? Gimme your address.

mean chicken: If someone goes and buys Tesla stocks when at valuation that puts Tesla at a higher market cap than GM that is at least 1000 times larger than Tesla, if someone goes and buys Bitcoin for $20000 while they know anyone can make crypt-currency now, if they go and buy the likes of Netflix and Uber which are losing money hand over fist, then they are stupid; and as I said the stupid deserves to be sacrificed by the likes of warren Buffets. I didn’t say it is moral; I just said they deserve their fates.

Here is the deal! The Donald knew all about this years ago and plans to borrow from D.B. against his own account using the Federal Reserve to implement a plan announced by the National Enquire? BTPhD while its still attainable/ not sarc.

Dow plunges 666 points…could it be….Satan???

-665.75

= 666 rounded up. One cannot make this stuff up. If memory serves me right, didn’t the S & P bottom out at 666 in March of 2009. Incredible coincidence or hidden omen? Again, if memory serves me right, I believe 666 (from the book of Revelations) was used to refer to Roman Emperor Nero as the Antichrist. But still, what strange coincidences.

Looks a lot like Kushner to me Ahh Just “pull it “

Sometimes this is the most valuable site on the web.

– Was the FED appalled when they noticed that the Trump tax plans would increase the budget deficits by some $ 100 (????) billion each year ?

The less destructive way to resolve the CPI problem that is building is to reverse the wealth effect. To sustain the wealth buildup generated by the super easing cycle following the GFC and at the same time impare consumers, highly leveraged corporations and the Federal Govt by higher interest rates would be a less optimal solution to the building inflation pressures. There is not much leverage in the stock market and hence a limited impact on the capital of the banking sector should a severe negative adjustment occur. As the valuations are generally recognized as stretched a corrective cycle would not be unexpected.

The benefits of swapping high priced equity for debit through share buybacks might be subject to review as well. After all even those completely hypnotized by the next quarters earnings and share price may consider that increased leverage for the sole purpose of goosing these numbers may have negative long term consequences.

The timid rate of QT shows how fragile and illiquid the gargantuan debt market is. What about those foreign CBs? What about all this talk about de-dollarization and new Yuan based trading? Seems like a media blackout since the Jan 18 launch date. Seems like a media blackout about the Chinese gold exchanges.

I think that concerted unloading of US debt by CBs wearied of watching USD fall and interest rates rise is driving the yield spike more than is being acknowledged. Maybe more than FED QT.

– Nomi Prins wrote a very critical article. In the article one Jerome Powell (the current FED chairman) also surfaces. When I combine the info in this article with the info in this thread then I fear that there’s a deliberate plan (conspiracy ???) to force the hand of the Trump administration in one or the other way. But in what way ?? To force more (unpopular ??) budget cutbacks ?

https://www.thenation.com/article/here-comes-the-next-financial-crisis/

– Do combine that with this article:

https://wolfstreet.com/2018/01/30/us-national-debt-will-jump-by-617-billion-in-5-months/

This is a bit too much coicidential for me.

JM Keynes,

I’ve been writing about the ballooning US gross national debt since I fist started blogging back in 2011. The first six years or so was under the watch of Obama, and now it’s under the watch of Trump. There is no coincidence. The ballooning US debt in its various aspects is a classic feature of this site — and will continue to be no matter who is in the White House.

No wonder equity investors are panicking…