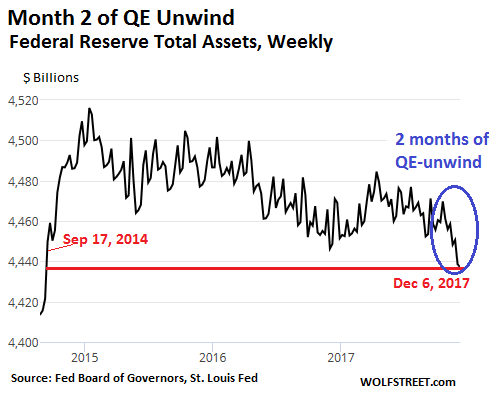

Fed’s assets drop to lowest level in over three years.

The Fed’s balance sheet for the week ending December 6, released today, completes the second month of the QE-unwind. Total assets initially zigzagged within a tight range to end October where it started, at $4,456 billion. But in November, holdings drifted lower, and by December 6 were at $4,437 billion, the lowest since September 17, 2014:

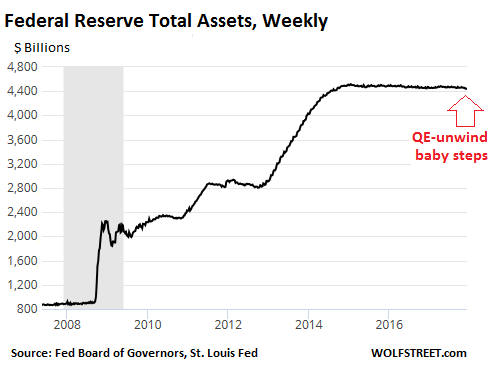

“Balance sheet normalization?” Well, in baby steps. But the devil is in the details.

The Fed’s announced plan is to shrink the balance sheet by $10 billion a month in October, November, and December, then accelerate the pace every three months. By October 2018, the Fed would reduce its holdings by up to $50 billion a month (= $600 billion a year) and continue at that rate until it deems the level of its holdings “normal” – the new normal, whatever that may turn out to be.

Still, the decline so far, given the gargantuan size of the balance sheet, barely shows up:

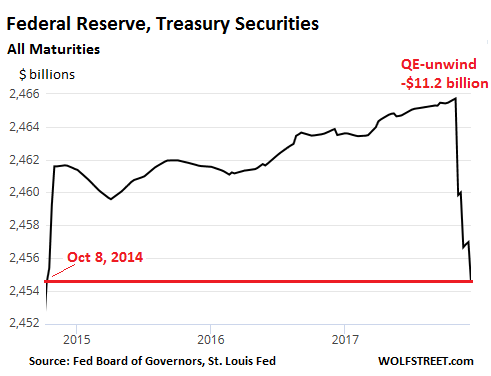

The Fed is unloading its Treasuries alright.

As part of the $10-billion-a-month unwind from October through December, the Fed is supposed to unload $6 billion in Treasury securities a month plus $4 billion in mortgage-backed securities (MBS) a month.

The Fed doesn’t actually sell Treasury securities outright. Instead, it allows some of them, when they mature, to “roll off” the balance sheet without replacement. When the securities mature, the Treasury Department pays the holder the face value. But the Fed, instead of reinvesting the money in new Treasuries, destroys the money – the opposite process of QE, when the Fed created the money to buy securities.

This happens only on dates when Treasuries that the Fed holds mature, usually once or twice a month.

In October, the big day was October 31, when $8.5 billion of Treasuries on the Fed’s books matured. The Fed reinvested $2.5 billion and let $6 billion “roll off.” Hence, the amount of Treasuries fell by about $6 billion from an all-time record $2,465.7 billion on October 25 to $2,459.8 billion on November 1.

In November, there were two big maturity dates:

- November 15, about $11 billion in Treasuries matured. The Fed allowed $3.4 billion to “roll off” without replacement.

- November 30, about $7.9 billion matured. The Fed allowed $2.5 billion to roll off without replacement.

For all of November, the balance of Treasuries fell by $5.3 billion to $2,454.5 billion, in line with the plan, and the lowest level since October 8, 2014:

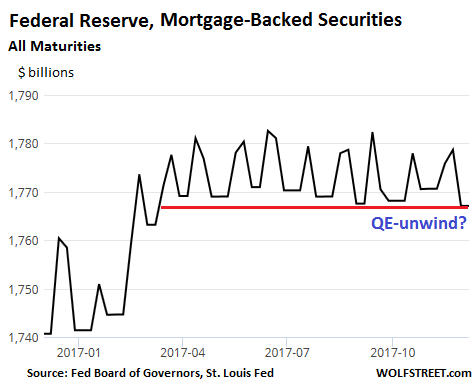

Mortgage-backed securities are a different animal.

As part of QE, the Fed acquired residential MBS guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Now, as part of its $10-billion-a-month QE-unwind, the Fed is supposed to shed up to $4 billion a month in these MBS. And?

At the beginning of October, the Fed held $1,768.2 billion in MBS. The balances then jumped up and down on a weekly basis and ended October at $1,770.6 billion, or $2.4 billion higher than at the beginning of the QE-unwind.

Same scenario in November, though they have started to edge down overall just a tiny bit to $1,767 billion, the lowest by a smidgen since March 8, 2017:

Residential MBS differ from bonds. Fannie Mae et al. regularly pass through principal payments to MBS holders as underlying mortgages get paid down or get paid off. Thus, the principal shrinks until the remainder is redeemed at maturity.

To keep the MBS balance steady, the Fed, via the New York Fed’s Open Market Operations (OMO), buys MBS in the “to-be-announced market,” or “TBA market.” This is a trade where the actual MBS is not designated at the time of the trade but will be announced 48 hours before the established settlement date, which can be two to three months later.

But the Fed books its MBS holdings on a settlement-date basis. So there is a mismatch between the date the Fed receives principal payments and the date reinvestment trades settle. Hence the jagged line in the chart above.

So when will the $4-billion-a-month in MBS reductions show up on the Fed’s balance sheet?

The first MBS reinvestment trades under the QE-unwind plan were conducted in October. Given the lag to settlement date of two to three months, the first visible impact on the balance sheet would start no earlier than December. This is where we are now, on the verge of seeing it.

The line in the MBS chart will always bounce up and down due to the mismatch between the date the Fed receives principal payments and the date reinvestment trades settle. But the line should start trending down, with noticeably lower lows and lower highs.

For the first three months, the QE unwind only removes about $10 billion a month, a negligible amount, given the vast markets and excess liquidity. But it picks up steam every three months. By October 2018, if the plan is still on, the QE unwind will remove $50 billion a month from the markets. This process will do the opposite of what QE had done: it will gradually destroy some of the $3.6 trillion that the Fed had created during QE. And by that time the broader effects of QE – asset price inflation – should also start to reverse.

There were no flashy announcements, to avoid alarming the markets. Read… Bank of Japan Tapers (Quietly), QE Party Over

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– Has Jennifer Lawrence already visited “Gershon’s” house ?

-Did perhaps the FED already write off those mortgages that became worthless as a result of the wildfires in California ?

#1: I don’t know.

#2: The Fed only holds mortgage-backed securities, not outright mortgages. The MBS it holds are guaranteed by the US government via Fannie Mae, et al. So the Fed is not going to take any losses, though Fannie Mae et al. might.

– “Gershon” wrote here on this blog that the chance of Jennifer Lawrence visiting his/her house was larger than that the FED would start unwinding QE.

Hahaha, I forgot.

The US Govt doesn’t guarantee FNMA loans, only Freddie Mac. FNMA has an implied “everything will be okay” associated with them, but there is no explicit guarantee, like there is with the lower yielding Freddie Macs.

Yes, JM Keynes, Jennifer Lawrence did indeed show up at my house, only to launch into a jealous rage when Emma Stone answered the door in a bathrobe instead of me, who was sleeping off my recent exertions. Happily, I was able to persuade responding local police to keep the incident out of the tabloid headlines. I do value my privacy, you know.

It looks like most of the decline in the balance sheet is due to a belated recognition of losses on mortgage-related assets. It’s in the prior week’s H4.1 release.

https://www.federalreserve.gov/releases/h41/20171130/

Define what you mean by losses.

In the event that there are defaults in any MBS the LOSS is absorbed by the issuer of the M BS Freddie and Fanny, not the FED.

The value of the MBS should shrink over time as there are principle and interest payments made. Any residual value (default’s) is remitted to the FED when the security matures.

Les, the second half of the article will tell you what’s going on with MBS on the Fed’s balance sheet, and it’s NOT because of “losses on mortgage related assets.” These MBS are guaranteed by the GSEs. The Fed won’t have any losses on them.

And the toxic assets it took on during the Financial Crisis have been sold or written off years ago. That stuff is gone.

√

This is probably one of the most important topics with relationship to the American economy.

And really not talked about ANYONE. Except here.

Thank you.

It’s not talked about because it’s the end. The Fed would have to buy quadrillions in the event of a meltdown, and that would be seen for what it is: a coup.

Remember that the Fed was asked to bail out the market in1929. It said, No can do. Its refusal is what caused the crash. It is sending that same message now.

Get out. And hope you have enough cash to see through another horrific depression–the worst EVER.

“Get out. And hope you have enough cash to see through another horrific depression…”

Yes, and also make sure you don’t loose your ‘cash’ to: being hypothesized (or rehypothesized) and your deposit claims being subordinate to counterparties in the collateral chain a la corzine. Agreed to Bail-in provisions and/or FDIC failure a la Cyprus. FDIC failure due to derivatives being FDIC covered a la ‘citigroup ammendment’. Subordinate bank deposit claims to bank bond holders (I forget the case name for that bank in Michigan) in a failed bank.

Oh, and not to mention the hard-on’s the powers that be have over negative deposit rates, cash depreciation against deposits, or banning cash alright (and then having it stolen in a bank account)..

Personally, I’m not sure why it’s such a big deal to destroy cash, since most people have no cash and only have debt, maybe there is no plan and it’s just fed jawboning.. But it seems clear to me that they don’t want any of the little people to have any cash when it matters..

Will,

Derivatives are not FDIC covered. Only deposit accounts up to $250,000 are covered by FDIC insurance. The “citi amendment” did not do anything to change that. Also insured depositors do not become subordinate to any counterparty if a bank fails. Insured depositors get paid first. Also no depositor in Cyprus lost money that was within the 100,000 euro insured amount as you imply.

How times have changed. Now the Fed’s main concern is propping up the market at all costs, with some token consideration given to the plebs who work for a living. The Feds decision to cave in to the Wall Street whiners during the last “taper tantrum” will be remembered as one of the most gutless decisions in financial history. No matter what the Fed does now, it’s probably already too late.

The degree of corruption and incompetence driving central bank policy is stunning. All of their efforts seem to focus on bailing out and continuing to enrich the investor class at the expense of people working to earn money. The willingness to put the currencies at risk to grow and preserve the wealth of the investor class is shocking.

The economy depends on confidence in the currencies – without it the economy will shut down. I design machinery for a living, I can’t barter food and shelter in exchange for machine designs. Peoples jobs are specialized and the world is too complex for barter. I need currency to maintain some value in order to exchange my services for the things I need, yet central banks are perfectly willing to destroy confidence in the currencies workers rely on.

Why won’t they stop? They are killing us. My life is more austere now than when I was a student working part time at a low skill job. Why are they hell bent on destroying our lives? Why aren’t people getting angry? What will it take to overthrow these tyrants?

Van down by river

The fed is a pernicious disease.

But yelling at disease and get angry about it will NOT help your health. If you destroy it, it may take down your organs and you get sicker. We are all infected and it encourages decay in moral standards and people’s behavior. My suggestion is to surrender and join the disease. Borrow money, buy assets and keep cranking it until the reset happens. By doing this, you either enjoyed the cranking part or you make it collapse sooner by your contribution. You have to be ready to die with it though. The corruption has reached a state beyond going back.

Just to be clear, I am being sarcastic and I am NOT following my own suggestions. I work, I save, i do not participate in assets that is so far away from fundamental value. Let the inflation bleed slowly, as long as it does not kill me, Inwillnsave to fight another day.

This situation can be blamed on the super computers:If it wasn’t for these their wouldn’t be enough accountants to cypher that many 1’s and 0’s by hand.

Now all the Fed has to do is allow independent audits, if only to placate the nay-sayers. After all, they have nothing to hide, now do they?

That said, I should probably stay sober when I post comments so I don’t end up saying something stupid.

Giving up drinking in these interesting times could be a mistake.

It’s never stupid to swim upstream. It just takes a lot of effort and you often have nothing to show for it except for the fact you didn’t go over the waterfall.

I’d like to see audits, too. The new guy proposed for the Fed board, Marvin Goodfriend, doesn’t seem to mind the idea. He’s sort of a mini Taylor. He also said legislative oversight is not necessarily a bad idea if not excessive. But, he claims to openly think about negative rates and cash confiscation. After me getting over the shock, I discovered he also seems to dislike QE balance sheet operations. Without them, negative rates are mostly theory and could never be a long term proposition. Heavy balance sheet operations like in the Eurozone and Japan are needed to make them work. Cash confiscation in the US is a fairy dream without some heavy handed govt involvement.

The Fed’s role in financing various government agencies is well known, when the Bush people airlifted palletloads of cash to Baghdad they were loaded up in Mariner Eccles. Ron Paul wants to audit in order to go back all the way to Nixon. You can’t run covert ops, like funding ISIS fighters if you don’t have a personal banker, or run a war off-balance sheet. Off-balance sheet is probably where the next bailout crisis will take us, and when they make an announcement that most of the budget is going off what will people say? Nothing probably, we are already numb.

” Off-balance sheet is probably where the next bailout crisis will take us”

Interesting concept when applied to the Fed. What does the law say about it occurring now or about it having ever occurred? The Fed is said to obey the law. However, anything not against the law is legal and permissible.

Bob Prechter lists many of the authorities in the Fed Charter in his book, but in reality Congress has placed limits on what the Fed can buy (bonds) and Janet made a statement she wanted “to be able to buy a broader range of assets”. The Fed is not truly a central bank, and the Fed is not independent. 43 brought Bernanke into the cabinet, while 44 left the Fed out. There is probably a quid pro quo with the SNB, to buy NYSE stocks, not sure how it works, and 45 has no clue at all. So far the Deep State has been very good to Donald Trump, as it was to Lucky Dutch Reagan, and his Fe chief, Greenspan. So much has happened since the forming of the Presidents Working Group on the Financial Markets,

If Bitcoin continues to rise, this will put more pressure on markets. To buy bitcoin, you have to sell other assets.

Bitcoin has a current market cap of over $250B. I think that means $250B came out of stock and RE flows.

This is a sign many people think there are not good opportunities elsewhere because asset prices are currently too high.

I bought my first bitcoin today (for fun). Could lose it all.

It would appear money is flowing out of gold to buy bitcoin – one worthless collectable for another. They will both fall out of fashion. Beanie Babies are the only truly safe investment these days – I have five storage lockers full of beanie babies so my future is secure.

Nonsense 5000 years of history tells me you have NO clue

I’ve never understood why gold sales people take cash in exchange for the gold they say is the only true money.

Or, why would they give cash to people who bring in gold?

Either way, very narrow buy sell / spread.

Depending on size of transaction they’ll buy it back for not much more than 1% of what they just sold it for.

Lots of currencies have bigger buy / sell spread. I’ve seen Brazilian one at a 20 % spread.

As I commented elsewhere, in 79- 82 the US$ was very unpopular. Of course I can’t pretend to know what the spread was (just not good) but I know what it would be with gold- about the same as now.

And true, you can’t spend it (or a US T-bill) at McDonalds. You have to go to the gold buyer who unless you are in the boonies, won’t be far away.

What is “true money”? Whatever it is with which you can pay your sovereign taxes. You cannot pay taxes with gold or silver, because they aren’t “real money”. During the California gold rush, miners paid for drinks and food with a “pinch” of gold dust, but the Callifornia government never took payment in gold.

Germany late 1945, a carton of cigarettes was the medium of exchange, and US servicemen were loaded with the “bit coins” of the day (as described to me by a scientist with personal onsite observations. But no sovereign government paid salaries in cigarettes, or gold, or Reichsmarks (the previous currency). True money, is the currency with which the government pays its bills, including salaries.

Note that the Zimbabwe Dollar, with tremendous inflation, was still “official” until the government declared it was ended. Was it “true money” up until the end? Yes. But US Dollars were physically more convenient, and were used everywhere they could be used.

When anyone writes “loose” for “lose” (“loose” rhymes with “juice”, “lose” rhymes with “views”) their credibility vanishes in my world. Same with “it’s”, which is a contraction of “it is”, not a possessive form. Where do people get these forms of misused spelling? And, why do they keep on doing it?

Watch out, the comment-section typo-police is coming….

Nick Kelley – Back when I used to hang around survivalist nutbags, I got into the gold and silver game, silver mostly.

I was buying rolls of Mercury dimes, and I discovered that when I bought, it was a bit over spot price because of reasons.

When I sold, it was a fair amount below spot again because of reasons.

I finally concluded that gold and silver only worked for me when I bought it at garage sales, for far, far below spot, because that “Italian Silver” necklace had been bought in the 1980s by that horrible boyfriend and who cares about that thing? At one garage sale, I looked and looked at a gold chain, not sure what the number on it meant, and the lady told me to just take it for free. It turned out to be gold.

One SN (survivalist nutbag) played the game far bigger than I did, though. He put something like $400,000 into silver at $40/oz. and silver promptly went down to less than $20/oz. Then he had to sell his silver because money reasons.

You can’t pay your taxes DIRECTLY with euros , pounds sterling or yen, which are all cash. Not can you pay them with a T-bill, a demand on the US Treasury. You have to go through a short procedure to do it with all four.

The thing about the bitcoin frenzy- it disqualifies it as medium of exchange. Say a guy has a car for sale for whatever BC spot is, 14K.

The guy with the BC is a believer, that’s why he has it, and will probably want more than spot. But the guy with the car will have to be a believer too to pay X more than spot.

If the guy with the car will take 14K US $, he doesn’t have to be a dollar bull. Like the vast majority of the population, he’s never INVESTED in US$. Sure it may fluctuate up or down a fraction of a percent overnite, but not enough to expose either party to risk.

Unless you are a professional trader trying to shave a fraction of a percent on a hundred million US$ against the yen or something the US$ is very boring as an investment.

That’s why it’s suitable medium of exchange.

This was exactly the way gold was back in the day. Basically useless as a medium of exchange.

And it becomes more worthless, if there is a widespread breakdown of authority. That’s why I do not understand people who stash gold “in case there is a total loss of civilian authority”. How would they be able to use it? If you had a Kruggerand and tried to use it to buy food, what would the guy selling you five loaves of bread, give you for “change”?? He’d tell someone you had “gold”, and soon you’d probably be using all those guns 24 hours a day, keeping thieves at bay!

Oh bullshit, people, there’s nothing wrong with Bitcoin magic money.

https://www.wired.com/story/bitcoin-mining-guzzles-energyand-its-carbon-footprint-just-keeps-growing/

To me gold’s most valuable property is “store of value”. Arguing about medium of exchange or what .gov uses for paying bills misses what is important. If one does NOT save, anything convenient can be used as medium of exchange. but in terms of saving instrument, can anybody reminds me what beats gold for 5000years of human history?

“but in terms of saving instrument, can anybody reminds me what beats gold for 5000years of human history?”

Exactly.

This current issue is, that the buying price, is $ US 1000.00 + above what it should be.

So now, is not the time, to buy, physical gold.

Hey d, if you are happy to sell gold at or below 500$, i borrow(short) US $ to get all of your gold if you have any or if anybody has any at price at or below 500$. And i will store them, they will NOT decay, 30 years later, they will still be the same as now, and 1OZ coin will still by me a nice suit as they did 500 years ago or 30 years from now on, regardless what US$ price of the suit is assuming US$ still exist.

If it’s so useless why are China and the Russians not only hoarding it, but manipulating the price lower only to purchase more?

I just wrote a letter to both my congressman and two senators, imploring them not to use a single dime of tax payer money to bail out and/or investigate Bitcoin and it’s investors once it collaspes and goes under 200 bucks.

If there is a total breakdown in authority, why would you accept a piece of paper, a check, drawn on an entity that no longer exists, the Fed?

Back in the days before humans discovered electricity, the use of gold was ornamental, but a greenback doesn’t even have that use if the government doesn’t exist.

If you really want to play this survivor/ prepper game, the choice is not between gold and paper money, it’s between 22 caliber ammo (optimist) or larger caliber (pessimist)

It’s only a matter of time that everyone’s bit wallets and passcodes get hacked. The fun has just started.

http://www.telegraph.co.uk/news/2017/12/03/bitcoin-crackdown-amid-fears-money-laundering-tax-dodging/

Tax avoidance, laundering drug money, I am shocked to learn gambling is going on here. Here are your winnings sir.

Correction: most people bought Bitcoin at lower price levels, so $250B wouldn’t have been taken from other asset flows. It would have been something smaller, but could be something a lot bigger in the future if the rally continues.

Well, at $50 billion per month it will take 20 years to reduce the balance by $1 trillion.

Charts on the growth in consumer credit (excluding mortgages) I saw today indicate that over the same time period the Fed balance grew by about $3.6 trillion, consumer borrowing increased by roughly $1.4 trillion. I guess that a lot of the rest went into mortgages. But what I wonder is how much they have to reduce the balance sheet before it has a measurable effect on the economy.

$50 billion per month would take 1 year and 8 months to reduce the balance by $1 trillion.

Don’t worry about it – aint gonna happen in any case. The first sniff of a bad treasury auction or mortgage rates approaching 5% and the Fed will come to the rescue with QE4. Money printing is permanent and structural to assume otherwise would be to assume people could or would pay back the debts they owe (if debts were paid what would we use for money? bitcoin? too funny!)

At 50 billion per month it will take 20 months to equal a trillion.

Whoops. That sounds better. Maybe there is hope. Thanks for the correction.

Yes and by then the Nasdaq will be hovering at somewhere around a million. Good observation above.

The observation may be good, but the math is wrong. At $50 billion a month, it only takes 20 months to get to $1 trillion.

20 months not 20 years. Carry the units when operating the slide rule O.E.

Especially when the tax cut deficit impact is considered……

Since Sept 2015 the 3M is rising.

So do other short duration rates.

When % rates are rising, notes value decline.

Will they sell assets and take a loss.

They don’t have to. If they wait until maturity there will be no loss.

The Fed can prove that they are serious about reducing assets, just by sitting on existing assets.

If they don’t replace some mature notes, the reduction accelerate.

Any balance sheet “normalization” would only reverse 1/3 of the QE gusher added to the balance sheet ($1.2 trillion of the $3.6 trillion added). Powell casually slipped this money printing announcement into his confirmation testimony and it passed by without notice or comment.

The financial press dismisses the consequences of the money printing by stating the excess liquidity has flooded into assets and harmlessly enriched those who were already rich and thus did not contribute to consumer inflation. The fact that tuition, housing and healthcare cost are rocketing higher is the fault of consumers not the Fed – the Fed will not take the blame for consumers who can’t control their spending after all. The Fed made gushers of money available to spend but will not be blamed after people accepted the money and spent it – they see it as a moral failing not a policy failing. Bernanke had the (self proclaimed) courage to act if only consumers were worthy of his courage.

“The fact that tuition, housing and healthcare cost are rocketing higher is the fault of consumers not the Fed – the Fed will not take the blame…” The “blame” for such debilitatingly high levels of inflation in three of the most crucial spending categories falls SQUARELY on the Fed. Inflation is not showing up (yet) in manufactured goods because of automation and (cheaper) foreign sourcing. But these 3 (highly REGULATED, btw) categories (housing, medical, education) create huge amounts of pain for consumers. QE was NOT a painless exercise. It made the collapse after the mortgage debacle less severe, but in the long run it stunted overall growth in the system because it made real risk taking unnecessary.

These numbers belong in an astronomy not an economic discussion.

Wolf, any chance you still have the data in a spreadsheet so you can calculate the percent change from prior month, possibly adjusting for CPI-U inflation, and graph the results, perhaps including a 3mo moving average and 1st degree LSBF trend lines for the various “zones?”

Worried about your stocks?

I’m 79 and retired with 60% in cash [insured savings accounts] across several banks and credit unions. 40% in TIPS [Treasury inflation Protected Securities].

Like watching a train wreck — you want to look away buy can’t…

I smell fear….

I smell fear of missing out.

The asset bubbles will not pop – the currencies will pop instead.

OK, sorry. Please delete; that is trillions

The unwinding seems necessary but also a negative on the economy by reducing the money supply. People can create there own financial instruments by selling covered calls.

So everything that doesn’t create huge bubbles is now considered BAD for the economy Do you see the insanity in that thinking because I sure do

Excellent article, Wolf. Most of your readers are having trouble understanding why even a small reduction in QE will lead to a correction in the stock market.

The market depends on a continuous “flow” of funds into the market to sustain and propel asset prices higher. Think about this. The central banks of the world created money out of thin air to buy bonds and that increase in liquidity found its way into the market and led to higher stock prices. As prices of stocks went up, it took an even greater flow of funds to buy those inflated assets and hence QE flows expanded. Without the continued expansion, stock prices would fall. So the Fed withdrawing even a small amount of money from the system reduces the liquidity in the market and creates volatility. That is what you have seen the last two weeks in the market, increased volatility.

You may ask why didn’t we see volatility when the Fed stopped QE. A couple of reasons. China increased its QE, investors increased margin to an all time high and retail returned to the market in droves.

Now the Fed is destroying money, the ECB and the PBOC have scaled back their QE and markets world wide are becoming more volatile. Follow the flow of money and you can figure out what is going to happen next.

David where have you followed the money to? I like your train of thought…

The money has gone into bitcoin. Stay away.

Could you elaborate a bit on why to stay away from Bitcoin, your personal perspective? There will be a correction, perhaps a long downturn. But there are many reasons to just ride it out and keep in the market.

I’m asking here, not saying, but if the TBTF banks and Goldman are buying, can’t they then turn around and use those assets as fodder for the fractional reserve machine to churn out credit to the usual rich suspects so that they can continue to buy stocks and bonds? This may be just a far-fetched scenario, but we’ve seen just such “creative” financial activity over the past two decades.

Jim

Good thought. People are margined to the hilt so Goldman & Morgan created a new loan vehicle that allows you to use your stocks to buy things other than stock.

Here is where your theory breaks down. Now that the public is buying this market with both hands, the wealthy, connected clients and the banks are selling. Dumb money in, smart money out.

The distribution process usually takes four or five months so look for the correction/crash to begin in earnest in late April or so.

I have been surprised at how low the VIX has been when I have thought events were most dire.

Will a ‘great unwind’ still need a stampeding event, (in your opinion David), or will a slow and steady decline of QE be enough?

I envision an oh oh moment, much like a cartoon snowball gathering speed, when all of a suden investors decide to just take some safety home.

What I wonder is just who is still buying these days? Someone is. Speaking for my wife and I, although we are probably of more modest means than many on this site, life looks okay at 62 with a house paid for and cash in the bank. I can’t talk about my investments with anyone, but hey…..Its nice to limit worries these days without self-inflicting your chance to survive going forward.

Sometimes, being a spectator is just fine. Examples: Skydiving, ski jumping, knife tossing tricks, stock picking…..

regards

Paulo

You are correct, there will be an event so that something other than QE is blamed. You have to remember that QE will be trotted out in the next crisis so it can’t be blamed.

The crisis will unfold in the following way. First, there will be a triggering event. The event is likely to emanate from China. There will be a slow down in the economy or a problem with real estate developers that infect the banks. This will cause a sell off in our market and the VIX to spike.

One of the Street’s favorite plays has been to naked short the VIX. When you short the VIX it is like selling out of the money calls that expire worthless. You keep all the money you got from the put that did not get exercised. People have been doing this for years and getting wealth. It is another Street favored trade and the common investor has picked up on it. The problem is that people have margined this position and a sudden spike fro 9 to 17 or 18 would wipe them out.

So you get the sudden spike to 18 and the margin clerks are on the phone, but the guy has no money to cover the position so the brokerage house covers it BECAUSE THE BROKERAGE HOUSE IS LIABLE FOR THE LOSS. The short covering drives the VIX higher and more margin call go out and the selling in the market feeds on itself.

Think I am making this up? All the brokerage houses us a 50% margin. Interactive Brokers just raised it margin requirement to 400% effective 1/1/18. All of the players will leave IB and go elsewhere, which is just fine with IB.

It would seem to me that at its current rate of growth, the US debt will be easily paid off with a few bitcoins in a couple of weeks.

All this debt stuff is just mumbo jumbo. It’s not real- create a virtual currency then pay off your debts with one coin. There are absolutely no consequences to simply printing money to pay off all this ‘virtual debt’. Use virtual money to pay off virtual debt and you will see no one will care.

The US is the reserve currency for the world – it can do anything it wants and the market MUST take it! The new generation of traders and economists know that there are no limits to growth, hence there are no limits to the amount of money you can print.

No currency is a reserve currency forever. The dollar’s share of reserve currencies is now about 63% or so. The euro is second largest reserve currency. There are a number of others. When folks across the globe lose confidence in a fiat currency, it’s over. So the central bank has to make sure that confidence in that currency remains high.

Meanwhile, de-dollarization is spreading. The Fed’s debasement of the currency and monetary malpractice can only hasten the process.

http://www.zerohedge.com/news/2017-12-05/de-dollarization-continues-china-iran-eliminate-greenback-bilateral-trade

Eliminating the dollar as a trading-currency between two countries, such as China and Iran, or China and Russia, is a good thing overall for trade and has no impact on the dollar.

Countries just have to have fairly stable currencies that are convertible, and they need to get the mechanics down. Once that’s done, it’s the way to go.

“Eliminating the dollar as a trading-currency between two countries, such as China and Iran, or China and Russia, is a good thing overall for trade and has no impact on the dollar.”

But a very negative effect, on the Economy, that is forced to take the printed on used toilet paper, RBL, CNY.

That can basically only be spent, in the countries that issued it.

After I have sold my GOOD QUALITY Organic produce. I want a Good German tractor and a German chainsaw.

Not some chinese or russian junk that will only last 5 minuites.

Which the QE Reduction does, more than anything else. Currently.

A lot of peopel want to see all those MBS OFF the FED’S balance sheet.

OT

I smell Fudge in Brussels. BIG Fudge.

“Nothing is agreed, until everything, is agreed.”

I don’t think the central banks care about confidence in the currency anymore. They seem to care a bit about the rate of loss of confidence but overall they seem hell bent on destroying their own currencies – no doubt confident people will accept their new and improved currencies after the collapse, after all what choice will people have?

Every action taken by central banks over the last decade seem to indicate a strong desire to devalue the currencies. We have all experienced a sharp drop in purchasing power during this decade, yet Yellen says the dollar must be devalued at a more rapid pace.

Savers in the 1920’s and 1930’s had their savings confiscated, via inflation, during the 40’s, 50’s and 60’s to pay for wars. The government compensated these lost savings by introducing social security, a new, unearned welfare entitlement, so the savers would not starve in the streets. How will the current generation of ripped off savers be compensated? I think the bankers will accept their starvation as a viable solution this go around.

yes, i think that’s the gist of it. they want to monetize the debt to keep the ponzi scheme afloat. they believe that if they can coordinate between the major banks and do the debasement gradually, they might last until the inevitable reset. the governments will use a carrot and stick approach to maintain social order. the carrot being SNAP, basic income, etc. the stick being the militarized police state. the other part of this is to get us all to go along. that’s why they are desperate to control the media narrative. is this evil? i don’t know. what other options are there?

– This the usual Modern Monetary Theory claptrap.

– Nope. We (the US) CAN NOT do whatever we want. If the US consumers reduces spending then tax revenues go down and the budget deficits grow and the Current Account will shrink. This combination is VERY toxic for EVERY economy.

Pete That’s just the kind of arrogance that gets you in trouble Wolfs right It won’t last forever

Let’s say you printed the money and paid off the debt. What would the holders of that money do with it? Buy up your economy, because the debt is now greater than the GDP. All you would be doing is transferring every asset that is not nailed down into the hands of the nations and institutions that hold the debt. This does not strike me as a happy scenario.

The US dollar almost collapsed in 1978- 81. That’s why the Fed had to push its rate to 18% just like Russia had to do recently when the ruble dropped 50%.

US tourists in Europe were asked to pay in the local currency.

A lot of people, some on this site. think the euro collapse would be a good thing and everyone could go back to their own currencies.

One thing for sure, if Germany goes back to D-Mark the US$ instantly has a tough competitor.

Along with anything but US$ (gold, art, old bicycles), the Swiss franc and the D-Mark were the currencies of choice in 79-81. Exporting manufacturers in both countries cried the blues ( the Swiss with their franc still do) but the German central bank ( independent by constitution not just tradition) pretty much ignored them.

All numbers in this article are in billions to make it easier with the smaller numbers (the monthly changes). So $4,456 billion in the article = ca. $4.5 trillion. By keeping it in billions, I can say “$4,456 billion” and “$10 billion,” rather than “$4.456 trillion” and “$10 billion.”

Meanwhile, the oligarchy’s media border collies are trying to lure the last of the retail-investor marks into Wall Street’s rigged casino where they can be fleeced at will by Da Boyz.

https://www.marketwatch.com/story/were-still-only-in-the-early-stages-of-stock-market-euphoria-2017-12-07

Based on the stick saves that have been going on in the bond market lately, every time it sells off, it looks like the Fed’s selling but some other entity is buying for the express purpose of propping it up. My guess is it’s another CB, the Fed, or PPT covertly. i.e. Sell with one hand:Buy with the other. That way they get to put a floor under the dollar but keep printing to prop up

The obvious question.

Who is buying what the Fed is said to be selling?

For the Fed to reduce it’s balance sheet, it has to sell what it holds. So who is buying the stuff which the Fed is selling?

When no one else was buying, the Fed and all the other central banks, became the only buyers.

For the Fed to reduce it’s balance sheet, someone else has to be buying.

Who would that be? And why?

My understanding of the article is that the Fed is not actually selling anything, but only buying new treasuries at a slower rate than that existing treasuries it possesses mature and are cashed in by the treasury department, thereby rendering them non-existent.

My question is what will happen when the treasury needs to sell more debt than the Fed is willing to buy, assuming that as usual there are no other buyers? Wouldn’t that end this balance-shrinking scheme pronto?

6-9 months? Wolf?

rx

Rex,

Your point #1 is correct.

To your #2: There will always be demand for US Treasuries, but perhaps not at this low yield.

When demand at the current yield disappears, motivated sellers will lower the price (yield goes up) until they find buyers. So the Treasury will be able to sell the bonds it needs to sell, but it may have to offer a higher yield in order to find buyers. This is what the rate hikes and the QE unwind are all about.

This is already happening on the short end. In 2015, the government was able to sell 2-year Treasuries at a near-zero yield. Now it has to pay about a 1.8% yield. This may move to 2.5% or even 2.8% a year from now. In other words, the government can still borrow, but it will be more expensive.

But this hasn’t happened on the longer-dated end — where it really matters. The 10-year yield is still below 2.4%. So once this is moving up, it will be a game changer for other asset classes, including housing (mortgage rates move largely in parallel with the 10-year yield).

Thanks for the explanation.

I take the point that there will always be some residual demand for American Treasuries.

The real difficulty here for all of the central banks is that volume of bonds held by them is vast. If bonds start to be disposed of at a greater greater than bonds being bought, bond values will fall and when bond values fall, yield (interest) starts to increase.

Given the size of the volume of bond market, a drop in the demand for bonds could prove fatal.

And if central banks cease to be buyers, what other entity is going to step in to the breach instead?

Financier Michael Pento is excellent when it comes to analysis of the bond market and the predicament therein

We had this discussion on another thread, bond sellers have more options than you suppose. They can fix the yield and allow the market to price the bond, thus rebating the buyer up front. Assuming the currency is weakening the seller has the advantage (much like buying a high yield sovereign and hoping the currency doesn’t collapse -LTCM?) Then after fixing yield they mandate all sales at par, they move the goal post. It’s their “How do you like me now” moment.

Your explanation implies the Fed would be willing to allow the free market to determine interest rates – I don’t see that happening.

The miniscule and trivial rate hikes and balance sheet reductions are about trying to control currency confidence and nothing else. If there was any meaningful increase in the cost of borrowing for the government or home buyers the Fed would come running to the rescue once again.

Do you really believe 30 year fixed rate mortgages will ever approach 5% again? Reality simply does not allow for that possibility. There is no tightening and there never will be, it’s all jaw boning and nonsense. 10 billion a month for a couple months at most – lets not start to lose our grip on reality here.

i think for the foreseeable future treasuries will have no trouble finding a market. we are a long way from no bid. there is a lot of international money that is desperate to get out of their local banking systems. the worse it gets out there, the better it is for the fed here. it’s the same thing that’s feeding all the asset bubbles.

Rex,

The Fed and other central banks control the general level of interest rates by performing massive balance sheet operation, called QE. Japan and the Eurozone won’t stop just because the Fed is winding down. Japan will do who knows what then do something else afterward for reasons nobody understands. The Eurozone needs QE to exist … it’s a kick the can device to support their socialist utopia.

Assuming the Fed cleans house well, the net effect will be rate normalization in the US. Markets will set rates here, not central bank central planning like today.

The US will issue debt until it can’t. Then someone will declare a crisis and the problem will be solved until goes off the rails again. Maybe we’ll kick the can like the ECB and Eurozone. Maybe not.

“Japan will do who knows what then do something else afterward for reasons nobody understands.”

Japan Kept a Massively Bankrupt administration alive and Stable, for over 250 years. It was still happily doing so, when Americans invaded it, Causing Massive Problems.

Simply as the Japanese refused to trade with America.

Pre the American civil war.

You dont understand them, that’s your problem.

Rex,

Google the “Primary Dealer System”. You’ll find how the system really works.

Correct me if I am wrong but I believe that this statement “But the Fed, instead of reinvesting the money in new Treasuries, destroys the money”, would mean no one is buying anything because the Fed isn’t selling anymore printed money. They are reducing the value of the market, not selling anything.

But I could be wrong.

The “value” of the market and everything in it remains exactly the same- only the number of dollars required to purchase a piece of the market- any market, from stocks to produce, can change. I.E. if it requires more dollars than last year to purchase a widget, that’s called inflation. The opposite is known as deflation.

The Fed never sells printed money, or even prints it. It only lends artificial funds to various banks which it conjures up out of thin air.

That said, contrary to “no one is buying anything” anyone is welcome to purchase as much treasury debt as they please- from the treasury.

rx

“For the Fed to reduce it’s balance sheet, it has to sell what it holds. So who is buying the stuff which the Fed is selling?”

?????????????????????????????

When the Bonds Mature, they are simply redeemed.

Your Question should be.

Who is buying the New bonds, the Debtor issues, to get the money, to PAY THE FED.

IIUC the “great unwind” is more accounting “slight of hand.”

The FRB doesn’t actually sell any of the bonds it holds, it simply allows them to mature, and returns that principal (re)payment to where the QE money came from in the first place. Note that nothing is in fact “paid off” as the U. S. Treasury borrows the money required for repayment by issuing new bonds.

What if the Fed is making all these numbers up?

I believe alot of the financial machinations in the past decade were conducted under the guise of national security. In that case, people involved would receive security clearances and have to remain silent about what is going on.

It’s not as if people are using suitcases of cash anymore. Basically key strokes on a computer.

good news Wolf; and finally!!! as the fed takes, Congress now gives —balancing the sheer volume of money supply tumbling out of helicopters to a fiscal policy that incentivizes some, hopefully a lot of, capital investment. best…PJS

I guarantee that LONG before they completely unwind there will be another crisis which will “require” their can kicking actions to a level which will unwind their unwind and far beyond.

That would be shocking! Hysterics like that would be unnatural to high level government officials. Why would someone in government manufacture a crisis for the purpose of greed and control over others? That makes no sense.

This bitcoin thing going on got me thinking about an old magazine cover by the economist

https://media.licdn.com/mpr/mpr/AAIA_wDGAAAAAQAAAAAAAA0tAAAAJGM3YmRjYmY0LTA5MWItNDJkOS04YjYyLTI1ZGJmNjg0OWU2YQ.jpg

if you look at that front cover closely replace it with a bitcoin and something interesting emerges .maybe bitcoin is the IMFS SDR currency in disguise it will be the new world reserve currency then gold and silver will back the SDR ,all countries can peg to the SDR of course the countries with more pms will fare better .a nyways just my 2 cents i told my financial advisor about that cover he laughed at me and btw check out the date on that magazine

“The Sun Also SETS”

I’ve said time and time again that Janet’s computer (money machine) has a magic zero key which she holds down for longer and longer periods of time in order to, when eventually necessary, “buy up” literally everything on the planet, as well as, most importantly, pay for the military-security-industrial complex that is the enforcement mechanism of the drone-standard fiat-USD. (You don’t want to accept fiat USD as payment-in-full for your REAL products, resources, etc.? Whether you ask for it or not, “democracy” is going to be delivered ASAP to your country via very-expedited air service.)

Back on track. Janet also has on her keyboard that similarly-magical little “delete” key. Never underestimate the power of smoke, mirrors and Fed-controlled zero and delete keys.

In short, never underestimate the power of the human imagination (INFALLIBLE greed).

The question is, what breed is the NEXT rabbit to be dragged by the ears out of the Fed’s (BoJ, BoE, BoC, etc.) top hat? Only the Group of 30 knows for sure, along with the “systemically important” VIPs they “leak” to. (Don’t you wish you were one of the “leakees”? Then we, too, could enjoy the “shower”. Now, THAT would be a “trickle down” economic system that I could live with!)

Depending on one’s particular definition of “collapse”, one could easily argue (and win) that the “traditional” US economy ALREADY collapsed with the bailout of TBTF banks, TARP, Dodd-Frank, NIRP, etc.

Of course all of that very unwise rescue stuff was necessitated by the previous repeal of all of the very-wise post-1929-depression legislation and the very predictable return by the TBTF banks to doing what caused The Great Depression 1.0.

At the very least, one would have to say that what the Elite’s governments and central-bank slaves have be doing since “the Financial Crisis” a few short years ago is “flying by the seat of their pants”. Or, as one Lord Rothschild recently said ….

http://sputniknews.com/politics/20160819/1044443930/rothschild-gold-dollar.html

“The six months under review have seen central bankers continuing what is surely the greatest experiment in monetary policy in the history of the world”.

Of course the irony is that if large investors were to start selling stocks, bonds, etc. and started buying PHYSICAL gold and silver (or homes in Toronto, London, Vancouver, etc.) in large quantities, this would not only cause the price of physical gold and silver to skyrocket, but might very well force the Fed, etc. to prevent the DJIA — the too-big-to-drop (TBTD) ulitimate symbol of “capitalism” — from crashing by becoming the share-buyer of last resort.

That is, if the Fed, etc. take their “whatever it takes” experiment to the extreme in order to prevent a stock market crash, the private Fed, etc. might end up “owning” or effectively controlling some or all of the corporations that are listed on the stock markets. (And what could possibly go wrong with that?!)

So lots and lots of astronomically-priced gold (or Bitcoin) would be owned by all of the stock/bond-sellers, and the central banks would effectively own or control lots and lots of shares of corporations. Now, THAT would be what I would call experimental, because if you think corporations are buying back their own shares to the extreme now, can you imagine how high Janet’s computer’s number-pad could boost the prices of ITS VERY OWN corporations’ shares “on the stock market”? To infinity and beyond!!

Dear Janet (etc.), what you’ve been doing so far has worked great, so you just keep spouting gibberish and using those zero and delete keys wisely and we’ll all enjoy another great sunset this evening.

(Now, how’s THAT for squeezing another shot out of a 1913 Fed musket that was “out of dry powder”, Mr. Stockman?)

The Fed is a sidebar to the second wave of populist anger. Point one, “You gave my tax cut to the wealthy?”, Point two, “You took away what HC options I had, and replaced it with what?”, Point three, “You raised interest rates to give rich depositors more money, while the real economy is slowing and I have no job, or I have a job that does not pay a living wage, and after buying a reliable car, paying day care, and payroll taxes withheld I am worse off?” The future is not bright.

“The future is not bright.”

Not so bright for many. Radiantly amazing for others. We’re not in this together anymore.

As long as the sheeple keep voting for the Republicrat duopoly and the crony capitalist status quo, they have no right to complain about how the financial elites and their political prostitutes are shafting them.

So the FED is destroying their imaginary money, but will it be enough? It seems unavoidable some bubbles will burst.

Let me just comment here that ANYTHING that will cause the crash of the US stock market will be fixed quickly by the US Fed.

Why?

Because

1) All of the US pension investments are heavily invested in the market. a crash and default in pensions would result on a march on Washington with pitchforks.

2) All of the 401K’s and IRA’s of the poor unfortunate majority without pensions are invested in the stock markets. More pitchforks.

With all of these pitchforks, most of them are bound to impale Trump and most of Congress if a crash should happen. Poiiticians are sly survivors. they will avoid deadly pitchforks.

Jim Kunstler has an interesting spin on the whole tax cut thingy and its relationship to the “QE unwind” Wolf is documenting.

“The hidden agenda in the so-called tax reform bill is to act as stop-gap quantitative easing to plug the “liquidity” hole that is opening up as the Federal Reserve (America’s central bank) makes a few gestures to winding down its balance sheet and “normalizing” interest rates.”

Interesting stuff, although Jim might be too bearish for even this site.

http://kunstler.com/clusterfuck-nation/stranger-things/

Wolf, you commented that this QE reduction was minuscule compared to the overall mountain of debt held by the Fed, and didn’t do the next obvious bit of math – at $10 billion a month, and over $4,400 billion in QE to unwind, this will take 35.67 years to unwind all of that debt. So, in other words, no, the Fed is NOT serious about unwinding the QE debt, not now or anytime soon, and will undoubtedly never unwind it.

No, that’s not how it works. It’s $10 billion a month for the first three months (Oct, Nov, Dec). Then it rises every three month. By Oct 2018, it’s $50 billion a month = $600 billion a year. At that pace, it will take only 20 months to unwind $1 trillion.

The plan is to start this slowly so markets can get used to it and then pick up the pace.

More math: suppose the Fed was to unwind the QE over TEN years instead, not a terribly short period either. That means it has to unload $440 billion a year, which is almost as much as the average annual budgeted Federal budget deficit per year. No way it can do that without seriously affecting the Treasury auctions.

Unwind over five years? $880 billion a year.

And with the looming Republican tax cuts, we are looking at even higher Federal budget deficits.

It pays to know what you are talking about.

The program incrementally increases over time (Obviously barring a black swan) just as QE Incrementally decreased overtime and taught the FED something, after the “Taper Tantrum”.

Will there be QE in the Future?

Probably. To some extent it is a useful tool. QE 1 Should have been the end.

Will it be the same as last time ( not in Conjunction with other Administration policies designed to aid the Economy, at the Bottom, where it is needed) Probably not.

As the lack of Administration policy’s and Actions, designed to Strongly target and aid the bottom of the Economy, is was turned QE into an asset bubble blower.

As the QE money had no way to get to the Bottom, then cycle up again, as “Profit”, as there was no work for it.

So it went into paper assets, which made the numbers look good, but did not aid the People on the Street.

It’s actually much faster. Starting in Oct 2018, the planned pace is $50 billion a month = $600 billion a year (see my comment above).

This was announced in September. Markets are not paying attention, or they’re not believing it.

typo: that’s 36.67 years to unwind QE at $10billion/month.

But you get the idea. This QE is a monster that simply cannot be unwound, except perhaps by hyperinflation. Modern industrialized nations are ALL experimenting right now with the untested concept of creating money out of thin air with their central banks …. and thinking that nothing bad will ever come out of it because

1) Everybody is doing it

2) it’s kept the economy and stock markets up up up …. so far

3) unending debt has no consequences

If the Fed actually starts unwinding $600 billion a year, and just make it disappear, what the heck? Isn’t that really borrowed money that the Federal government spent already? Doesn’t that mean the US government just decided to borrow this money and then never pay it back by destroying this debt? What’s that going to do to the value and reliability of US Treasuries?