The liquidity drain of Quantitative Tightening has come entirely from ON RRPs. Reserves have lots of liquidity left to drain.

By Wolf Richter for WOLF STREET.

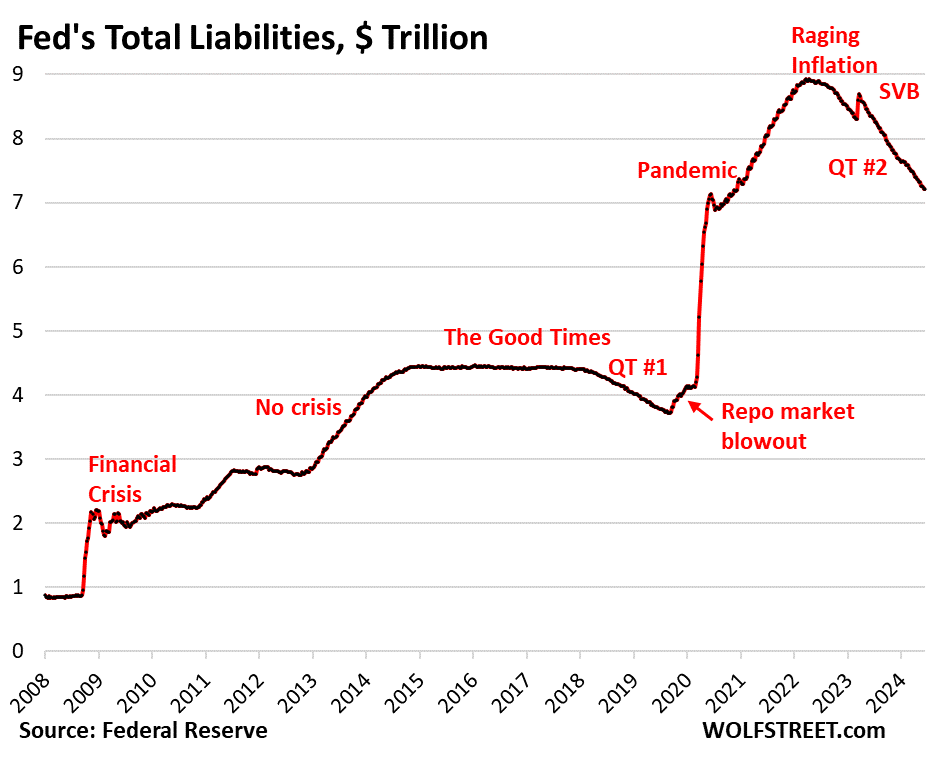

Total liabilities on the Fed’s balance sheet have dropped by $1.71 trillion since the end of QE in April 2022, to $7.22 trillion, the lowest since December 2020, according to the Fed’s weekly balance sheet today. The liabilities have dropped as a result of QT, in lockstep with the Fed’s assets, which have also dropped by $1.71 trillion over the same period.

There are five big liabilities. Two of them – “reserves” and “ON RRPs” – are hotly discussed by Powell and Fed governors, and by everyone on Wall Street, because they represent liquidity in the financial system that is now getting drained by QT:

- Reserves: cash that banks deposit at the Fed

- Overnight reverse repurchase agreements (ON RRPs): cash from domestic counterparties, mostly approved money market funds

- Currency in circulation: paper dollars in pockets and under mattresses globally

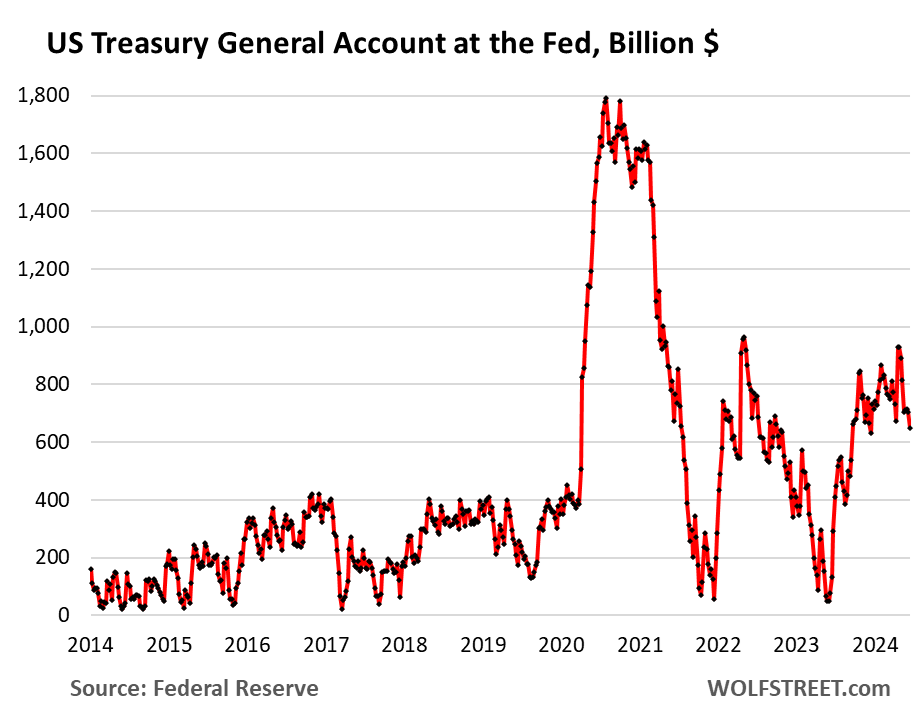

- Treasury General Account (TGA), cash the government puts into its checking account

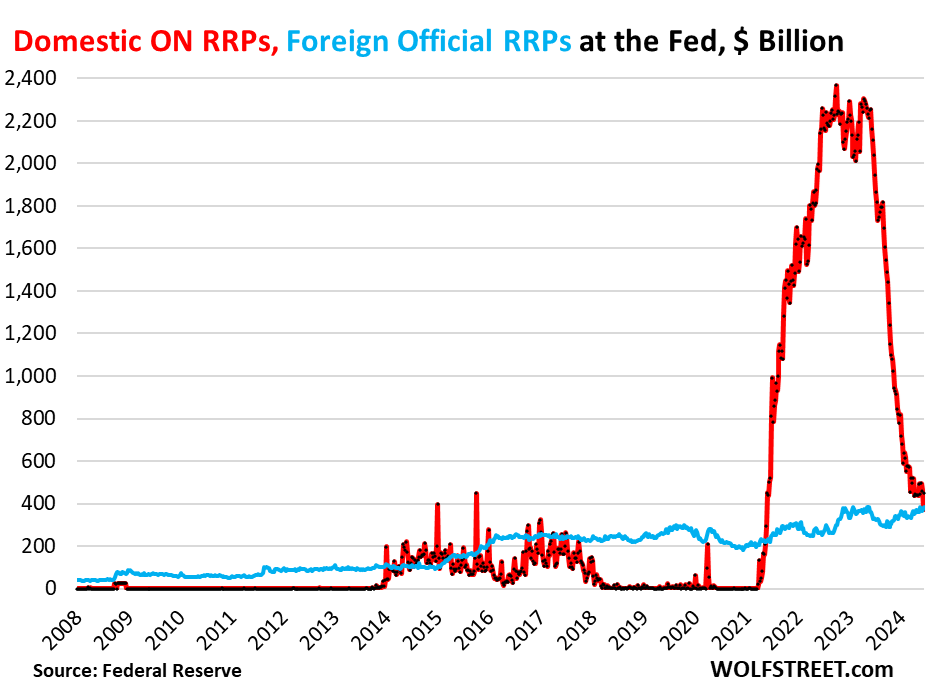

- Reverse repurchase agreements with foreign official counterparties.

The Fed’s assets are mostly securities and loans. The Fed’s liabilities are forms of liquidity – cash that the Fed owes other entities.

During QE, the Fed’s purchases of securities pumped up its assets to nearly $9 trillion, and its liabilities followed in lockstep because a balance sheet must balance. On any balance sheet: assets = liabilities + capital. The Fed’s capital is fixed by Congress, so what moves in lockstep are its assets and liabilities.

The two liabilities that move with QE/QT.

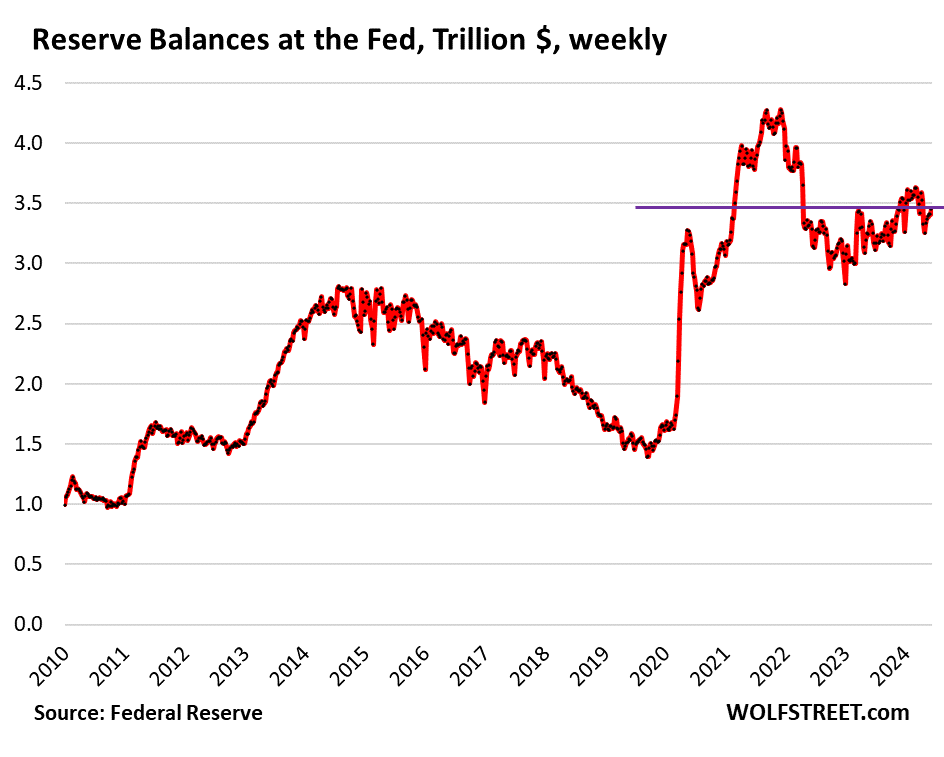

Reserves: -$265 billion since the beginning of QT in July 2022, to $3.46 trillion.

Reserves are liquidity in the banking system. Banks pay each other out of their reserve accounts at the Fed once a day. They’re the center of the US payments system for banks. The Fed has been paying banks 5.4% in interest on their reserve balances since the last rate hike in July 2023.

QT is draining liquidity from the financial system, and reserves are one place where this liquidity drains out of. But it’s not the only place – the Fed’s ON RRPs are mostly where the QT liquidity drain has taken place so far.

Cash also shifted between reserves and ON RRPs. Reserves peaked just before the Fed began tapering QT in late 2021, then fell sharply as the funds shifted to ON RRPs via the money markets. Since that December 2021 peak, reserves have dropped by $821 billion.

The level of reserves is what the Fed looks at to determine how far it can take QT. Toward the end of QT-1, reserve balances dropped so low (below $1.4 trillion) that banks stopped lending to the repo market, even as repo rates began to rise sharply and it would have been profitable for banks to lend to the repo market. And so the $5-trillion repo market blew out, and the Fed ended up stepping in to calm the panic, thereby undoing a big part of QT-1.

As a result of this repo market blowout in 2019, the Fed, in July 2021, revived its Standing Repo Facility that it had killed in 2009 during QE, and that it then didn’t have in September 2019 when it needed it. The SRF is designed to supply cash to approved banks via repos, the way it had done it before 2009. Banks can then use this cash to lend to the repo market at higher rates and make money on the spread.

Powell and other Fed governors have said that no one knows how low reserves can drop without causing issues in the banking system – they’re shooting for “ample” reserves, down from the currently “abundant” reserves. And they will keep their eyes out for signs that they’re approaching that ample level, they said.

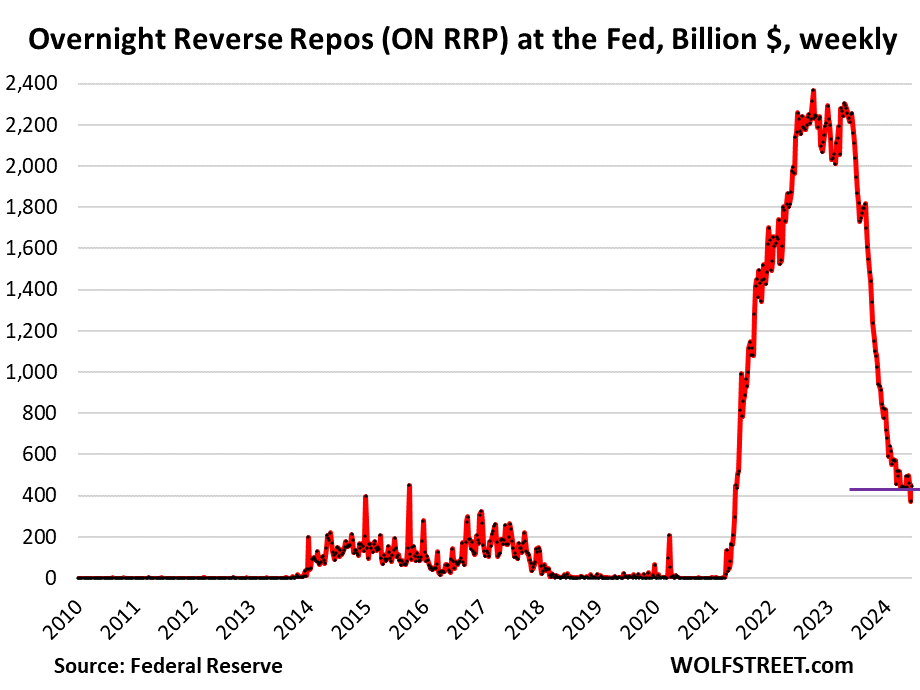

ON RRPs: -$1.92 trillion from peak, to $448 billion. This is where the $1.71 trillion in QT has come out of. And the remainder ($0.2 trillion) has shifted from ON RRPs to reserves.

The Fed offers ON RRPs to domestic counterparties and currently pays 5.3% interest on them. They have been used mostly by money market funds. Other approved counterparties are banks, government-sponsored enterprises (Fannie Mae, Freddie Mac, etc.), the Federal Home Loan Banks, etc.

ON RRPs represent excess cash that money markets don’t know what else to do with. ON RRPs have existed for decades, but in normal times, they’re zero or near zero. And now they’re going back toward their normal level:

The three liabilities not affected by QE/QT:

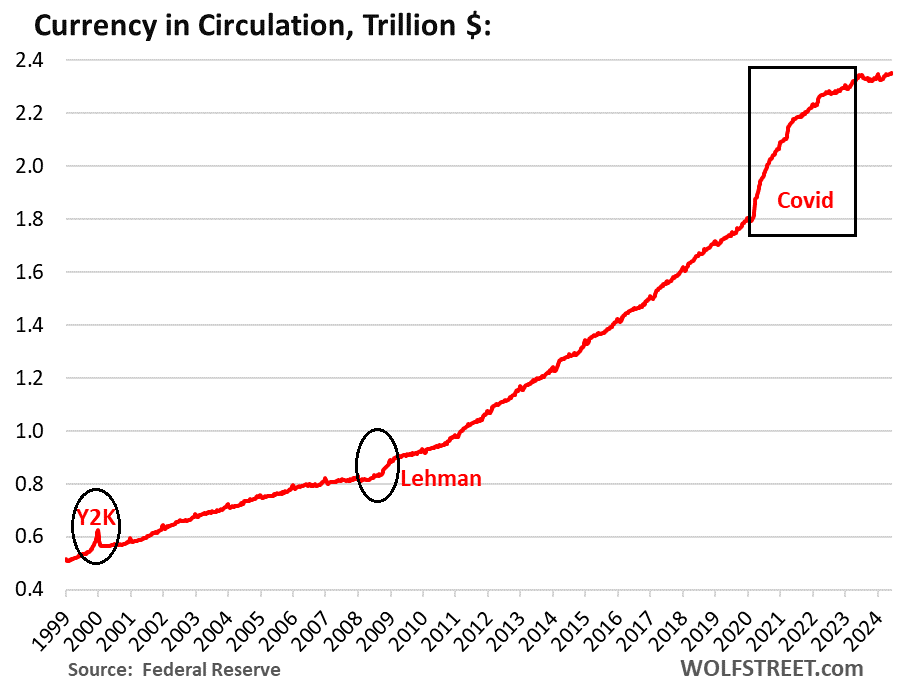

Currency in circulation: $2.35 trillion. These “Federal Reserve Notes,” as it says on each of the bills, are in wallets and under mattresses in the US and globally. It’s entirely demand-based: When customers demand currency, the banking system must have enough on hand. Foreign banks have relationships with US banks to get US currency for their customers.

Banks get the currency from the Fed in exchange for collateral, such as Treasury securities, with the effect that the Fed’s interest-earning assets increase with currency in circulation dollar for dollar.

In other words, when you withdraw $100 cash from an ATM, the Fed gets your $100 in exchange for some pieces of paper that pay no interest, and it invests your $100 and earns interest on it. This interest income from seigniorage used to be the way with which the Fed (and other central banks) financed their own operations and then remitted the remaining profits to the government.

Demand for currency soars during uncertain times, such as Y2K, the months after the Lehman bankruptcy, and Covid. From February 2020 through June 2023, currency in circulation had surged by 30%.

But for the past 12 months, currency in circulation has been little changed: $2.352 trillion on the Fed’s balance sheet today, versus $2.346 trillion at the end of June 2023.

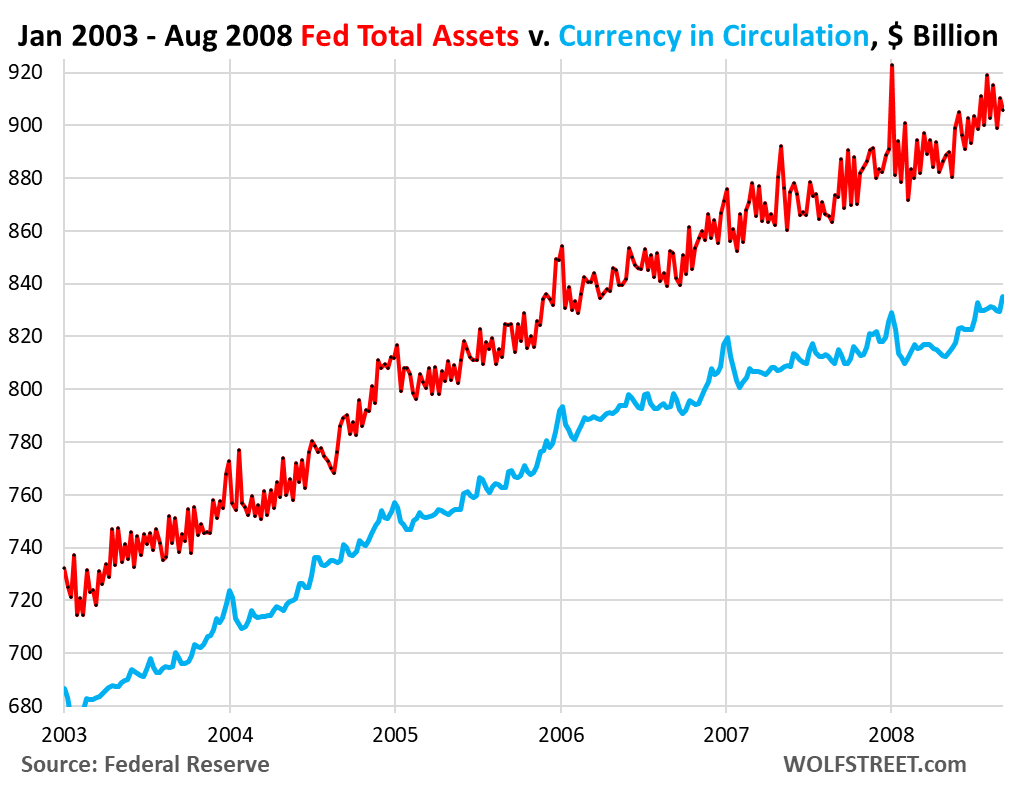

Before 2008: Currency used to be the main factor in increasing the size of the Fed’s balance sheet until 2008, when QE and the addition of the TGA ballooned the Fed’s balance sheet beyond recognition.

Between 2003 and August 2008, just before QE started, the Fed’s total assets rose by 26%, or by $190 billion, from $720 billion at the beginning of 2003, to $910 billion in August 2008. Over the same period, currency rose by 23%, or by $155 billion.

Total assets (red) are so jagged because the Fed used overnight repos to provide liquidity to, or drain liquidity from the banking system via its SRF. But the vast majority of the Fed’s total assets were Treasury securities that grew steadily as a result of growing currency in circulation (blue).

Treasury General Account (TGA): $650 billion. The Treasury Department’s checking account at the New York Fed has massive daily inflows from its Treasury auctions, tax collections, tariffs, fees, etc., and massive daily outflows to pay for what the government spends.

During periods when debt sales are limited by a debt-ceiling fight in Congress, the TGA gets drawn down to scary low levels, at which point the debt ceiling fight is resolved, and the government issues a lot of T-bills to bring the TGA back up to operational levels.

The TGA is not influenced by QT or QE, but by the Treasury Department’s management of the government’s finances (cumulative inflows minus outflows).

The government’s checking accounts used to be with regular banks, primarily JP Morgan, but during the Financial Crisis, the government moved it from the banks to the New York Fed, so if these banks collapsed, it wouldn’t take down the government’s ability to pay its bills.

RRPs with foreign official counterparties: $385 billion. The Fed offers reverse repurchase agreements to “foreign official” accounts, where other central banks can park their dollar cash. The account balances are determined by decisions of foreign central banks and are not a result of QE or QT.

The chart shows both, ON RRPs with domestic counterparties (red) and RRPs with foreign official accounts (blue). ON RRPs will go to zero or near zero as QT progresses; while foreign official RRPs will keep doing their thing.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

I’m almost done doubling the price of everything.

The grocery store begs to differ.

Great article that adheres to the precept that binds us all together.

Some would suggest that it is only the current brand of horseshit that the rubes might be willing to get behind. Willingly paying for it the whole time.

Real tour de force on the “official” big money pipelines. Grasp bits and pieces, but didn’t come away with “the big picture”…AT ALL….tried…… Thanks for laying it all out, though, I stopped at minor headache.

THIS, however will stick in my head and maybe be mulled over….never knew about it…it seems pretty damned important, especially in the before and after sense…..maybe even all the way back to 1913.

The government’s checking accounts used to be with regular banks, primarily JP Morgan, but during the Financial Crisis, the government moved it from the banks to the New York Fed, so if these banks collapsed, it wouldn’t take down the government’s ability to pay its bills.

Always best to control money pipeline(s)/storage tank(s) or have tap(s) into any given system, rather than just have some money going thru them all…even a LOT of money……THAT, I am becoming MORE sure of.

Still not as secure as some control over important legal or military pipelines.

Probably evident I am somewhat confused…..or senile?

Neither has my local property tax assessor or homeowner’s insurance company. These people are trying to squeeze blood from a turnip.

J-Pow is the man. Crazy how the FED tuned the dials to the exact settings to engineer a no landing. Housing prices flattened out. Stock Market has kept going up. Unemployment stayed low. Oil prices did not spike. Energy prices are still low because of tons of new green energy projects.

In the meantime, the FED also reduced their holdings.

They increased rates just enough to slow down inflation but not to slow down corporate borrowing and expansion.

Honestly, they have done a much better job than I ever imagined. I thought the sudden rise in during in 2023 would certainly have already caused a recession.

Hats off.

Inflation has slowed down seems to be constant. Even it if is a little high, constant inflation is better than rising inflation of deflation.

Are you serious? Inflation “a little high”? It’s 3%+, and much higher in services, that’s way above their bogus 2% target and assures the continued decimation of middle class purchasing power.

And no one can say anything about any Fed policy until QE is wound down to where it was in 2007, whatever that new level is per the Fed’s need to balance obligations, 4 Trillion or whatever it is. Celebrating before that is basically “mission accomplished” horse crap.

Yes he is serious. It is so simple that it should be easy to understand. 3% really is only a little high compared to target. It was 9%+ before.

3%< 9%.

So while it is higher than target, it is only a little high.

Also calling the 2% target "bogus" reveals more about you than anything. It reveals your ideology and inability.

Good luck. Past experice (TMF) shows you really need it.

“They increased rates just enough to slow down inflation but not to slow down corporate borrowing and expansion.”

The Fed has crushed the commercial real estate sector.

$29,000,000,000,000: A Detailed

Look at the Fed’s Bailout of the

Financial System

Perhaps you can make sense of this study from Levy Economics Institute. It’s above my pay grade but the numbers don’t seem to jive with what the Fed is stating for liabilities. Outstanding loans that will never be repaid are not a liability?

Waiono,

People came up with this $29,000,000,000,000 BS years ago, but it has been debunked. What these idiots did was add up all the loans that matured and were renewed. If on Monday, I lend you $100 for a week, and the next Monday when the loan is due, we renew it for another week, and then a week later for another week, and we do these rollovers of the same loan for 10 weeks in a row, I still lent you only $100, but renewed the loan for 10 weeks. And so some braindead idiots added up all these rollovers of the same loan and said that I lent you $1,100 ($100 original loan plus 10x $100 in rollovers), when in fact, I lent you $100 and renewed the loan for 10 weeks. That’s what happened with the Fed’s bailout numbers. The debunk – what I just told you – was widely published, but no one read it because that $29 trillion or whatever fantasy is just a lot more titillating. And that braindead garbage still gets dragged around the internet, even today, LOL.

Wouldn’t work-from-home (offices) and online shopping (stores) be a far bigger contributor to CRE problems?

The mall CRE sector has been crushed since 2017 — see our Brick and Mortar Meltdown series. Office got crushed by a dual force, the structural problem and interest rates (see our CRE series). Multifamily and the others are now getting crushed by interest rates, though structurally, they have reasonably sound demand. Multifamily is the largest CRE sector out there.

Totally Wolf! They care so much about price stability that only 58% of the homes for sale in Bend, OR cost over $700K. Totally reasonable. Keep shining them on Wolfie. MBS’s, ETF’s – everything is on the menu next downturn.

The Commercial Real Estate sector crushed the CRE (with the help of the pandemic and tech advances that have rendered offices and brick and mortar retail redundant).

;)

Multifamily housing corrections are 30%+. I know you likely.includee that in your thiught, but I think that fact, during a massive hosing supply shortage, is often lost

One heck of a tax on an asset class that needs relief from government, not further burden.

Yeah it’s all perfect, smooth sailing from here on out. All risk has been removed from the system, you can pretty much guarantee yourself that asset prices will never substantially drop again. Everything has reached a permanently high plateau…thanks to the Fed.

What color is the sky in your world? You are for sure not living in this reality when you say the FED won’t let asset prices drop.

Ask office CRE owners about asset prices never being allowed to fall.

RU82

Totally agree here. Considering the enormous problems the Fed had to deal with and with no help from congress or the previous and current administrations, the Fed did/is doing a heck of a job.

You misunderstand. The true job was to throw the economy into recession, not kick the can down the road for future generations to deal with.

You think locking renters out of the housing market was a good idea? How about record wealth concentration? Would you like another 22% inflationary step up over the next four years?

There are millions of non-asset holders, mid-wage earners, and fixed income dependees who disagree with you.

you beat me to the game by 13 minutes but i hadn’t refreshed.

let’s also clarify that it’s not just non-asset holders, but non-significant asset holders.

a lot of people claim that 55% of americans or whatever own stock through their 401ks. the purpose of this misleading number is to make the average american think that a bubble stock market, and government measures taken to protect it, are good for the country as a whole. if it’s good for the country as a whole, why not support it?

the problem is that the benefits of the stock market are very concentrated. anyone whose 401k went from $20,000 to $30,000 over the past couple of years is much worse off, as the cost of living has skyrocketed way beyond that.

only the top couple of percent make out well.

Excellent points, Bobber. The govt’s economic policies have fueled the growth of inequality. Inflation takes a terrible toll on the lower and middle class. The rich don’t care. All of their assets keep pace with inflation, and their basic needs require only a small percentage of their income. In addition, all of this massive government borrowing is lining the pockets of the rich who are collecting 5%+ interest on their money market funds and T-bills.

One unmentioned item in this excellent article is the Fed’s income statement. The Fed lost $114.3 billion in 2023. If you ask the “experts”, they will tell you this is just a “bookkeeping entry” because the Fed can’t really lose money. Uh huh. And why, pray tell, is the Fed losing money? For the same reason that is squeezing regional banks. They are stuck with Treasury debt that they bought during their massive QE spree. That debt is paying low interest, while the Fed is paying the money parked in RRPs at over 5%. In essence, the Fed is essentially bankrupt, but nobody cares.

Meanwhile, a recession (if it comes) will have the potential to sink tax receipts if the market tanks. Our economy is incredibly financialized. A huge chunk of tax receipts come from the wealthy’s gains in the stock market and in interest income. If those tax receipts tank, the federal govt is SCREWED. The deficit will blow out even bigger.

In my opinion, there is simply no way out of this mess. It is very, very bad. And those who keep denying how bad it is will not be well-positioned to gain from the carnage that is going to ensue. Go watch some YouTube interviews with Lyn Alden. She tells it straight. You have been warned. Ah, my public service announcement for the day! :-)

“One unmentioned item in this excellent article is the Fed’s income statement. The Fed lost $114.3 billion in 2023.”

I discussed this on January 12 when the Fed released its preliminary financial statement:

https://wolfstreet.com/2024/01/12/fed-reports-operating-loss-of-114-billion-for-2023-as-interest-expense-blows-out/

Read that article. It would help you get a better handle on some these issues. This is from that article:

The Fed is required to remit all its leftover income – after paying its expenses and statutory dividends – to the US Treasury Department, a form of a 100% income tax bracket.

Since 2001, the Fed has remitted $1.36 trillion to the US Treasury. Even over the first eight months in 2022, the Fed still remitted $76 billion to the US Treasury. The remittances stopped in September when it started to lose money.

Over the last months in 2022, the Fed booked $16.6 billion in losses against future remittances (red for 2022 in the chart below); and in the year 2023, it booked $116.4 billion in losses against future remittances.

No. You misunderstand. You need to educate yourself.

The FED has very little to do with the concentration of wealth in the U.S.. The laws in the country have far more to do with it.

Do you want to lower the concentration of wealth in the country? The lowest hanging fruit to doing so would be to increase access to basic healthcare for everyone. The ACA is one of the few things that slowed the increases in the concentration of wealth in this country of the past few decades.

I bet your sources of information don’t tell you this. I bet they rely on your ignorance to tell you that healthcare would be better if it was more market based.

People who say that don’t understand healthcare and they don’t understand markets (despite pretending it is their religion).

It is the laws in their country that determine the distribution of wealth in this country. Unfortunately the wealthy have invested a lot of money getting the ignorant in this country to vote against their best interests.

Blame it on the immigrants.

It should also be noted that much of the recent inflation has been concentrated in services. This means workers. Worker wages have been the biggest driver of inflation.

This is great foe thr working class. It is terrible for the retired on a fixed income.

i actually think the fed has done a decent job starting in the summer of 2022, but i don’t think for a second it makes up for the awful job they did for the 13 years before that.

however, i wanted to point out two things. the general fear of deflation should not and cannot apply to assets, like housing and stocks. housing prices have flattened out, thus far, at a rate unaffordable to most people. that’s in large part why sales volume has collapsed.

secondly, a manic stock market that just goes up and up without regard to fundamentals is bad. first, it worsens wealth inequality, which is already at a breaking point. two, it contributes to goods and services inflation, and possibly indirectly, housing inflation. three, it means that ordinary people must use their 401ks to buy in at nosebleed valuations, and hope that they stay high. four, the higher it goes without regard to fundamentals, the worse the collateral damage when it ultimately pops. when, not if.

stocks going up when it’s based on actual productivity increases is good. stocks going up based on multiple expansion is not. that’s just the sign of a bubble.

The Shiller PE has been trending higher since the early- to mid-1980s, peaking with the Y2K mania (roughly 44x) and now approaching the recent high of about 38x. The long-term mean is 17.13x. I’ve pondered this phenomenon for some time now, and I’ve concluded this is an artifact of several factors.

1) There are approximately half as many publicly traded companies today as there were in the mid-1990s;

2) the general public is sold on dollar-cost-averaging and have their 401-k’s on autopilot;

3) stock buybacks have consistently reduced the actual shares outstanding.

So there you have it, simple supply and demand. Lots more dollars chasing far fewer companies and shares. So is it a bubble? I thought so for quite a long time, but where else are people going to put their long-term investment money and still have liquidity? Even the COVID panic only brought the multiple down to about 27x. The 2008-09 disaster took the multiple to about 14x, which is just past the long-term mean. Another place people are investing their savings is real estate, another “bubble” as it were. Of course, cash is always an option (money markets), but even with today’s rates, 5% doesn’t look too attractive.

So there is the conundrum. Is it a bubble, or is it simply the least-bad option? Personally, I’m uncomfortable with a 35x multiple ore anything near that level, but I don’t think most people thing of it that way or, at most, even think about it at all.

Unless you own assets, the Fed has

given you a lower standard of living.

If you own assets, you have done well

for now.

And if you were saving to buy a house, the Fed has given you a *much* lower standard of living. And they’ve failed to make anything more than a microscopic dent in that massive problem they caused.

Auto workers, UPS workers, many airline workers, semiconductor workers, all have a higher standard of living than they did a few years ago regardless of their ownership of assets.

Several concepts that should be passed onto the young people of our society.

Do not trust the Fed to save your money unless your already rich.

The elephant in the room is the corruption that grants our trusted servants a closed, criminogenic environment. Which they apparently are for public sale.

Within the first quarter of 2024 blue-chip firms have borrowed a staggering $529.5 billion – a substantial jump from the previous borrowing high of 2020, at $479 billion in Q1. January and February alone set records for borrowing.

——–

Blue Corporations either think current interest rates are not restrictive. They are on pace for a record year of borrowing

Corporate expansion is due primarily to high inflation giving 99% of the companies license to raise prices, sometimes to gouging levels. CEOs love inflation, because it justifies price hikes, whether they’re needed or not.

Next, the Fed created the entire housing mess by cutting rates to near ZIRP and keeping them ultra low for two years. As soon as the economy started to expand after having contracted for only 6-8 weeks, the Fed should have started to slowly raise rates.

And then we got their MASSIVE expansion of its balance sheet. The ONLY reason why things haven’t fallen apart is due to the significant increase in the money supply. And now, they’re slowing the pace of QT.

My property taxes have gone up 33% in the last three years, My homeowner’s insurance has gone up 20%. Both of these are directly due to the Fed’s completely unwarranted $2.7T in MBS purchases since 2008.

So, I guess my point is that it’s all fake. The Fed has printed trillions of dollars in liquidity that has fueled the rise in national debt. This excess liquidity is used to purchase treasuries during the good times, so the Fed doesn’t have to purchase treasuries directly.

Prices of most goods are falling due to lower demand which has nothing to do with the Federal Reserve.

So we’re talking “durable goods,” not all goods. And with durable goods, the tsunami of supply is very helpful.

The Federal Reserve is now nearly completely irrelevant and controls so little money in the US economy that it can be entirely ignored.

🤣❤️👍

Wolf: Please explain with statistics, not emojis. Does the FED control so little money that it is irrelevant?

I was rolling on the floor laughing so hard I was speechless.

SoCalBeachDude has a very strong humorous streak.

Hold on there, small pack animal, a donkey which Quick Draw relied upon for intelligence about the proper response during a chaotic episode of human trauma.

The Fed is hardly toothless but rather the opposite that Fed is the muscular bully of the world’s reserve currency. No one else has been willing to assume the burden of being the reserve currency which is available in sufficient quantity to suspend a number of asset price bubbles through inflation

Maybe QT will become restrictive eventually. Too date the only squeeze on economic activity has been, as usual, on the working guy. With no apparent squeeze on the speculative which continues to defy credulity with their claim that AI is not a mentally challenged entity without the capacity to evaluate the morality of it’s programmed propensity for violence.

dang – …’Babalouie’… , as I vaguely recall. (…and Quick-Draw’s timeless, fancy pistol-handling: ‘…Bang!, (raises pistol to blow smoke from muzzle)-Bang!,blow-Bang!,blow, blow,Bang!…).

may we all find a better day.

I remember during the market crashes of 2008 and 2020 the financial media droned on about a “liquidity crunch.” I remember specifically in 2020 how the treasury market suddenly evaporated, also referred to a liquidity crunch.

Only now do I really understand what that means. It means investors want to cash out their securities, but there’s no cash or cash-like assets available. So, prices plunge until someone with cash is willing to buy. Hence why money printing is called “plunge protection.”

$3T extra liquidity since 2020, and it doesn’t even make a dent in covering the $18T+ stock market run up since 2019. Profit taking from 2019 by itself would trigger an asset meltdown like the world has never seen.

Something is propping this all up. Maybe it’s a side effect of the massive issuance of government or corporate debt. Maybe it’s some new form of money printing we’re not collectively aware of. Perhaps it’s just delusion, faith, and momentum from a manic market.

I’m sure whoever is pulling the levers is doing everything they can to keep it propped up, but if that ever slips, things are gonna get very nasty.

It’s 4 Trillion of QE since 2020 and massive Federal deficit spending. Not rocket science.

Do the math (and be honest with yourself), look at the fundamentals of housing, stocks, cryptocurrency; then compare the differentials between those fundamentals and the price runups; then subtract the expansion of government debt and money printing.

Inflation and government spending simply cannot fully explain what basic arithmetic reveals as the greatest asset bubble in history, somewhere in the $40 – $60 Trillion range.

I just call it the $50 Trillion asset bubble, because $50 Trillion sounds so unimaginably and hilariously clownish, it’s hard to believe that it’s real.

I don’t know the size of the asset bubble, but I think we will have a pretty clear picture when QE is fully unwound and when (or if) Federal deficit spending is forced to unwind by bond buyers.

I think you are missing the multiplier effect on government deficit spending. It’s way more inflationary than reserves parked at the fed or on its balance sheet. As for asset prices, they are at the margin, so none of it needs to be backed with actual money. The stock market, housing etc is all priced based on what the current fraction being traded is at. So again doesn’t need actual dollars to back it up.

I’ve always been a little bemused by the fact that the cumulative value of an entire market is set in people’s minds and on paper balance sheets by the last miniscule sale, which is how you get a $50T bubble out of oh lets say $5T in sales or whatever.

That’s also why the constant propaganda of those who own 80% of the assets is so important, so they can milk their living expenses off of it and make their deals back n forth. Can’t have panics upsetting that apple cart when everybody tries to unload at once.

Value is what you get, price is what you pay. Utility is the basis of value so that’s what I aim for.

@Happy1,

The dreaded bond vigilantes have already shown up, which is why interest on bonds are so high. The catastrophic crash in bond values already happened. It smooth sailing from here.

It’s nice out, think I’ll go out and have a picnic, some potato salad.

Being in the eye of the hurricane is cool, the birds are singing, sky is clear…look, the sun is shining.

Good times for our economy until it gets torn to pieces and scattered to the wind.

kent, the 10 year is at 4.2%. no one would buy at that rate unless they were confident qe would return. the bond vigilantes are not back. not by a long shot.

carlos, i agree with you. the fed balance sheet is near where it was at the end of 2020, as wolf richter wrote in this article. at the end of 2020, the s&p was around 3,700. right now it’s more than 50% higher.

the fed printing does not explain all of the rise. a lot of it is pure bubble mania.

Hi Carlos: I agree with your point about the massive asset bubble, but the math is not as simple as looking at federal deficits and money supply expansion, although they are certainly part of the reason. You have to also take into account the ludicrous amount of leverage in the system, not to mention the plethora of derivatives. This madness was definitely caused by govt policy of zero interest rates. If you can borrow for virtually no cost, they why not load up on debt and speculate? When I buy a stock, I take the money out of my bank account. I don’t borrow it on margin, or take out a home equity loan, or buy derivatives like call options. But I am a foolish outlier who shuns debt. I won’t engage in this madness. I bought gold in 2019 at $1300 and my “wealth adviser” told me I was nuts. Uh huh. Oh, and I am NOT a gold bug. I will sell my gold when the doodoo hits the fan and snap up some great equity bargains during the ensuing panic. Good things come to those who wait. I am blessed that I have had a long, happy career that fortunately left me comfortable in my old age. But I have made FAR more money managing my own portfolio and relying on the foolishness of politicians, policy “experts”, and speculators. So, at this point, I will sit out this party and wait for the hangover after.

Carlos,

the prices are set at the margin. If I pay $1 extra for 1 share of Nvidia the “value” goes up $25,000,000,000. Now imagine what extra $3T in liquidity can do. The tide lifts all boats. Well, all mega-yachts anyway.

Yes, that’s exactly how a bubble works.

If you could create $20T in wealth by printing $1T, why not keep doing it forever?

The only contradiction with my version of reality is what you said. I don’t agree even if you have convinced yourself that you are able to influence the millions of generations too come.

Well it’s hard to itemize each thing that I read that suggested that you are apparently disraught about things over which you have no control.

I challenge you to compare the insanity of love as a suspect not a villian.

I stand by my original call. If the Fed can get the balance sheet below 7 trillion, I will be surprised. The Fed has enabled bad behavior and broken their charter. The Fed never should have been allowed to purchase MBS. But I digress, international trade and trade settlement is all that matters. Fiscal responsibility is on CONgress, and it’s up to them to do the right thing. If they don’t, then our international trade partners will force the issue. Full FAITH and credit as it were.

Hedge accordingly.

Hi WB: You are very wise indeed. Agreed on all points. Excellent observations. Look out below, because this is going to have a VERY bad ending.

You forgot too brag about what your original call was, exactly because that claim being shown to be false can paint a BS artist as an impostor.

Had I bought microsoft at 25 cents then I would be one of the rich without wealth, twisting our humble history into a gaudy performance of it’s only make believe

What the heck are you even trying to say? If “ifs” and “buts” were candy and nuts, we would all have a merry X-mas? Unhappy? Make different choices.

Interesting that RRPs haven’t gone to zero yet. Seems like there’s still plenty of liquidity availability lend to the repo market. GCF rate is 5.39% as of this a.m. – less than 10bps higher than the (risk-free) RRP rate.

Very very informative article/explanation and comments.

Are these decision makers part of some kind of conspiracy, or just hanging on by juggling decision balls and hoping for the best? “Let’s do this and see what happens”.

Besides the anger inducing prices at the store, inflation hides so much. Things like: What is a livable wage? Fair returns for landlords and investors. Affordable housing. Retirement plans. Then there is the scapegoating, and questions, fair questions about policy. Example, is forgiving student loans necessary, or is it just another subsidy for post secondary institutions and releases them from real accountability….market accountability. Why are countries so rich in resources, food production, and energy unable to ensure a small room for sleeping and cooking for the vulnerable? Then Elon gets his 44 B payday. This morning.

Anyway, working from home Wolf nails it day in and day out. Hopefully this complicated complicated system holds together. I’m just not sure who it serves?

Excellent points, Paul. Again Wolf Richter illuminates the dark shadows and helps educate us to the facts. I especially like your astute observation about how govt policy “experts” are following the PhD strategy of “Let’s do this and see what happens.” A casual look at the Fed’s track record of predicting the future path of anything shows how truly clueless they are. And they are not alone. We all need more humility and less smug certainty. My investing motto is “Embrace Your Ignorance”. Oh, and “Buy Low, Sell High”.

With due respect, the PhD strategy is the best example of pampered children insuring their status.

That is your problem. You think the FED is predicting the future.

The FED reacts to current data. It doesn’t anticipate or predict. That is why the dot plot is so silly. It is asking a bunch of people who are trained to react to current data to predict the future.

Monetary policy is very risky these days. When the Fed started QE, I don’t think they envisioned the extra liquidity being such a hot potato that drives up asset prices. They went down that road because they thought it was a good way to keep the financial plumbing clear, so that markets wouldn’t lock up. Bernanke’s wealth effect was a harmful side effect that he rationalized to himself a benefit.

QE with a $1T balance sheet in a low price environment is a lot different than QE with a $7T balance sheet and sky-high asset price multiples. The 10-year Shiller p/e for the S&P500 is near record levels. Housing market to income ratio is also near an all-time high.

Even if they did another large QE from here, I don’t think it would make much difference. P/E’s can’t expand without increased earnings. QE provides the cash to buy things, but it won’t provide the earnings.

I think we are at a tipping point where asset prices are so high, the Fed’s tools don’t matter much. The timing of the crash will depend on how quickly the Fed reduces interest rates, as that can stimulate earnings and delay things.

Any decline in fiscal spending could trigger an asset price correction as well.

It’s take a while longer, but I think we are finally near the point where asset prices must correct because they can’t go higher. For renters who want to buy, savers, and mid-wage earners, it’s the light at the end of the tunnel.

After 15 years of being whipped by the Fed, these folks are noticing the Fed’s arm is getting tired.

Yes indeed. Caught between a rock and a hard place. There is no way out of this mess. Years of zero interest rates, QE, and huge fiscal and trade deficits are coming home to roost. Policies have consequences. We have gone from valuing the U.S. dollar by the gold standard, to valuing it by the “PhD standard”. We should change our currency from “In God We Trust” to “In PhDs We Trust”. As for me? I don’t trust them.

One of the biggest laughs Wolf inserted into this article is that anyone anywhere *ever* thought JP Morgan would “collapse.”

The FED exists to ensure that will never happen.

The government moved its TGA for other reasons.

I wonder if you realize that during the 2007-2008 crisis, there were a couple of major banks that failed.

JP Morgan is one of the best run banks so it didn’t. If it was poorly run than maybe it might have. What if it was run like WAMU?

The government doesn’t want to rely on being able to determine well run banks to determine where to keep the TGA. Hence they moved it to the FED.

What a great, informative article !!!

I read some of the comments here about what a great job the FED is doing.

Who can tell what happens 12 months from now. If things blow up 12 months from now, is the FED doing a bad job then or is it a consequence of a bad job now.

When you fly an airplane, one of the most critical ideas is hat the pilot keep ahead of the airplane. As soon as you start reacting you are playing with disaster.

The FED can do nothing about geo-political risks. Another branch of our so-called government is nominally responsible for that and seems intent on creating conflict around the world.

The Bank of the US is making stealing deposits from customers it doesnt like, the new normal. Many customers see this and it makes them anxious to find another bank. The US attitude is “so what”. Any banker that is so arrogant that she does not fear a run on the bank is dangerous.

From my perspective as a small-scale landlord in the Midwest, I’ve noticed that while asset values have been on the rise, rent prices haven’t kept pace. This has led me, along with several other landlords, some much larger than myself, to sell off our properties. The resulting decrease in supply, particularly in single-family homes, has significantly pushed up asset prices. Each month, we’re seeing new highs in sales prices, accompanied by higher rents due to the shrinking availability of rental properties.

There is still more value to find in the Midwest. Bring your sale proceeds and/or remote jobs and enjoy early summer bugs and don’t forget “Winter is coming!”.

I see the same thing. I am seeing a slight increase in inventory but relative to the rest of the U.S., prices are cheap. What is interesting is that over the past month i am again getting bombarded by call, text and letters to buy my rental homes. It had slowed down last year but this bombardment is on par with 2021-2022.

What is odd is 70% of the callers have pretty thick asian or indian accents. This was not the case in previous years. I used to just hang up on them but now i am curious were they are located. I now ask them were they are located and they will say they are local. But it is clear that many of these calls are from call centers.

Wolf,

Another great clear and understandable post! Thanks so much for explaining what’s going on to this “

“seasoned citizen”.

And commenters … thank you guys too. It doesn’t matter whether or not I agree with what you suggest.

Hearing … well READING … other people’s opinions is a great way to learn.

Hi Anon: I fully agree. Not only is Wolf a genius, but there are many educated, articulate readers who leave really good comments that we all benefit from!

S&P500 is up 14% YTD.

Russell 1000 up nearly that.

Russell 2000 is now down YTD.

The bottom 1000 stocks in the R2K are in crisis. Main Street is in trouble and no one is talking about it.

Thanks Wolf for another great article. We all benefit from your excellent analyses!

Wolf, what happens when reverse repo hits zero? It is pretty clear that banks are not ready to buy more Treasury debt at current rates and Treasury will keep printing more debt every month. Is this the reason why Jamie Dimon claimed few months ago that he could imagine much higher rates?

ON RRPs hitting zero is the normal condition. Nothing happens. Part of that excess liquidity has been mopped up.

Money market funds are huge investors in repos, commercial paper, bank CDs (not the stuff you buy as retail investor), T-bills, demand notes, and other short-term instruments, plus ON RRPs. Right now, the cash coming out of ON RRPs is going into these instruments because they pay more than ON RRPs.

Look up the portfolio holdings of a big money market fund, for example, Schwab’s SWVXX. You’ll see.

https://hosted.rightprospectus.com/SF/MMD/Fund.aspx?cu=808515605

There are $6 trillion in money market funds, and only about $400 billion in ON RRPs. So keep that in mind.

Short-term yields are bracketed by the Fed’s policy rates and expectations of its near-future policy rates. Right now, everything is still stuck at 5.5% for six months. So the Treasury market is not really betting on a rate cut this year.

But longer-term yields are very low, and they have fallen amid huge demand in recent days. They should come up. And I expect them to.

In a scenario where rates drop substantially or whatever amount to compel people to pull money from MMFs, where would it go? Deposited with banks? Curious as to your thoughts on this, Wolf.

It might just roughly stay where it is, if rates drop to the 3-4% range.

Thank you, Wolf, interesting. What struck me was that this Schwab fund doesn’t own any T-Bills directly. Do you have an idea why?

Schwab (like all others) has a separatee group of Treasury money market funds that hold T-bills and ON RRPs only. But it pays less interest.

Money market funds are huge investors in repos, commercial paper, bank CDs (not the stuff you buy as retail investor), T-bills, demand notes, and other short-term instruments, plus ON RRPs. Right now, the cash coming out of ON RRPs is going into these instruments because they pay more than ON RRPs. – Wolf

So why should we assume that the reduction of ON RRPs represent an actual decrease in “liquidity” versus a transfer of “liquidity” to other instruments that pay better as you stated?

We are about to pre Boss Fight levels.

🤭

It’s going to be interesting to see how quickly the TGA falls in the 2nd half of the year as we move towards the debt limit restart on 1/2/2025. In addition, how quickly will the RRPs balance move towards zero over the same period? And what happens when liquidity starts to dry up somewhat early next year, if the economy is still treading water and doesn’t give the Fed reasons to spin up QE.

Hi Wolf,

A small typo: ‘ bleu ‘

Best wishes from a persistently cool and wet England!

That’s my French soul talking.

Wolf,

My understanding is that both repos and reserves allow banks to park excess liquidity elsewhere and earn interest. If this is the case, why do repos exist at all? Why don’t banks park all their excess liquidity at the Fed and earn 5.4%? Or are there different counterparties, rates, etc.?

Not sure if I am missing something critical here.

Banks lend to the repo market when repo rates are higher than interest on reserves. That’s not always the case, and then they don’t lend to the repo market.

I understand that on any balance sheet assets = liabilities + capital. However since the Fed is an unusual institution (i.e. can’t go bankrupt, print its own currency, etc) why could it not also make up its own balance sheet accounting equation, declare that its asset + its tiny fixed capital will be allowed to go lower than its liabilities hence increasing the possible amount of QT.