Wall Street hocus-pocus has done an awesome job.

The Dow-20,000 hats have come out of the drawer after an agonizingly long wait that had commenced in early December with the Dow Jones Industrial Average tantalizingly close to the sacred number before the selling started all over again.

What a ride it has been. From the beginning of 2011 through January 27, 2017, so a little more than six years, the DJIA has soared 73%, from 11,577 to 20,094. Glorious!!

But when it comes to revenues of the 30 Dow component companies – a reality that is harder to doctor than ex-bad-items adjusted earnings-per-share hyped by Wall Street – the picture turns morose.

The 30 Dow component companies represent the leaders of their industries. They’re among the largest, most valuable, most iconic American companies. And they’re periodically booted out to accommodate a changed world. For example, in March 2015, AT&T was booted out of the Dow, and Apple was inducted into it, as its ubiquitous iPhone had become the modern face of telecommunications. New blood with booming revenues replaces the stodgy old companies. In aggregate, revenues should therefore rise, right?

And there has been a huge binge of acquisitions, from mega-deals such as Verizon’s $130-billion acquisition of Vodafone in 2013, to the many dozens of smaller companies that Apple, Cisco, IBM, and others have bought. These mergers bring the revenues of the acquired companies into the revenues of the Dow components. And in aggregate, revenues of the Dow companies would therefore soar, right?

But the other day, I was asked about the revenues of all Dow components, after having lambasted the revenue debacles of two, IBM [Big Shrink to “Hire” 25,000 in the US, as Layoffs Pile Up] and Cisco [Cisco Buys 45th Company in 5 Years, Revenues Still Stagnate].

So here we go. Fasten your seatbelt.

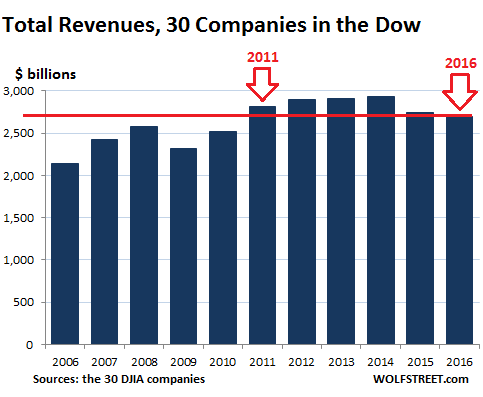

The chart below shows total aggregate revenues as reported under GAAP by the 30 companies that are today in the DJIA. This includes Apple, for example, though it only joined in 2015; and it no longer includes AT&T. For 2016, these 30 companies reported aggregate revenues of $2.69 trillion. That’s down 4.4% from 2011 and the worst year since 2010:

OK, you say, it’s the oil bust’s fault. The energy companies did it. Sure enough, there are two huge energy companies in the Dow, Exxon Mobil and Chevron. Alas, their revenues started dropping long before the oil bust occurred. Revenues peaked in 2011 for both of them, at a combined $740 billion. By the end of 2014, before the oil bust hit in earnest, revenues had already dropped 16% to $624 billion. And by 2016, they were down to $351 billion, having plunged 53%.

Of the Dow components, four, including Exxon Mobil, have not yet reported their earnings for fiscal Q4 2016. To approximate revenues for the fourth quarter, I took the year-over-year growth rate of the first nine months and applied it to the revenues as reported in Q4 2015. It’s not perfect, but it’s close. And given the vast aggregate numbers – trillions – any divergence for that quarter gets lost in the rounding error.

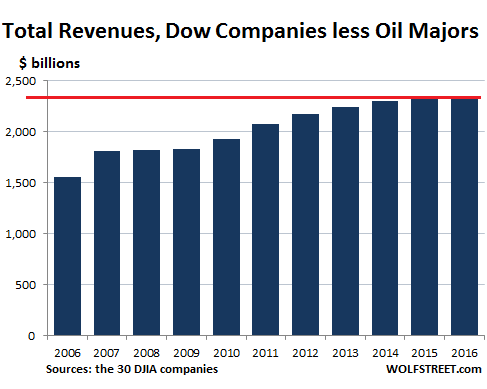

So here are the revenues of the Dow components without Exxon Mobil and Chevron:

Ah-ha, you say. It’s all the oil bust’s fault. Without the oil companies that have been ravaged by the oil bust, revenues are fine. OK, maybe not fine. Revenues without the oil bust companies are up 13% since 2011. That’s an average annual growth rate of 2.5%, barely above the rate of inflation!

But the DJIA hit 20,000 with the oil majors in the average. So in looking at the relationship between aggregate revenues and stock price movements, we need to leave them in the mix.

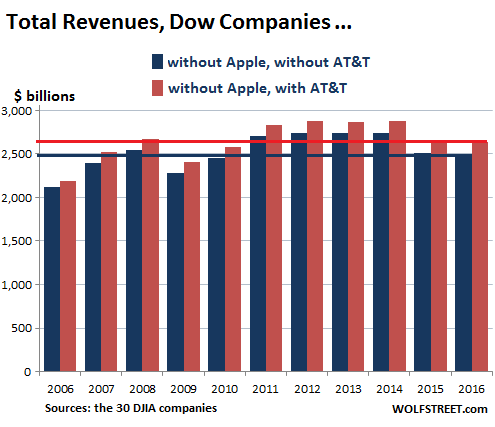

And reality looks even worse. Apple, whose revenues have skyrocketed by over 1,000% since 2006, from $19.3 billion to $216 billion, became a Dow component in 2015, replacing AT&T. And its revenues weren’t part of the 30 Dow components until 2015. So here’s what the aggregate revenues of the Dow components look like without Apple (blue columns) and without Apple but with AT&T (brown columns). A pure stagnation fest:

In both scenarios, revenues in 2016 were lower than they had been in 2008. Only 2009 and 2010 were lower. So in terms of revenues, 2016 was for the Dow components ex-Apple the worst year since 2010! And this despite the five-year binge in acquisitions!

So how have the last two years been? Don’t even ask.

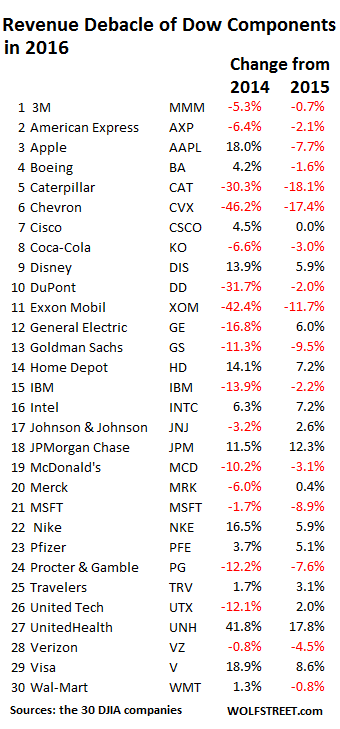

Of the 30 companies in the Dow, 16 sported declining revenues in 2016. And 17 sported declining revenues over the two-year span since 2014! Only two of them are oil companies! This table shows that inglorious list in all its beauty:

But the stock market is full of hocus-pocus, and actual revenues, as reported under GAAP, over time, are obscured the best way possible, just as magicians obscure their sleight of hand by distracting their audience with some flashy moves. So when I bring up “revenues,” everyone says, “Who cares about revenues?”

OK, I get it. It’s all about the adjusted ex-bad-items earnings-per-share – the Great American fiction – along with “leveraged share buybacks” funded with borrowed money, other forms of adroit financial engineering, and crowd-pleasing new metrics.

This relentless and eager focus on Wall Street hocus-pocus explains in part why the DJIA has soared 73% over the five years to 20,000 even as aggregate revenues, despite the delirious acquisition binge, have been mired down in a sea of stagnation.

The US economy hasn’t escaped the consequences of this corporate revenue stagnation, as hopes for a strong finish were gutted. Read… Back Below “Stall Speed”: 2016 Economy Matches Worst Year since Great Recession

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So the Dow is rigged; along with Gold and Silver Markets and Stock Prices all over. Just how many Trillions does the US Government owe the Federal Reserve?

4.4 trillion!

You could buy it back and collapse or you can pay interest on the amount for say a billion years?

Would you like to see the repayment schedule?

I don’t think that is correct. The 4.4T in reserves on the Fed balance sheet is not just public debt. It is also mortgage-backed securities, private debts. And some gold.

The Federal Reserve only owns about $2.5 trillion in US Treasuries and they are essentially interest free to the US government as the Federal reserve annually rebates more than 94% of its profits to the US Treasury as it always has done which last year amounted to about $92 billion. The Federal Reserve only owns less than 14% of outstanding US Treasuries and the other 86% are owned by other parties with the largest owner being the US government itself through its various agencies with the largest holder (owner) being the Social Security and Medicare Trust Funds with more than $5.5 trillion of US Treasuries. The $1.9 trillion balance of the Federal Reserve balance sheet is mostly held in MBS instruments for a total balance sheet of $4.4 trillion.

Saved me the job.

This site run’s on Facts, not the fed owes 24 trillion garbage.

Its the main thing that makes it viable.

In 2014, global equity markets consisted of $63.5T in securities…while global bonds were $81.5T (SIFMA 2015 Fact Book). Per the BIS statistics for 2Q16, global bonds have had risen to $92.7T.

Ask yourself…now that the 30+ year interest rate cycle has turned (per the U.S. Fed raising rates in Dec with expectation of additional increases in 2017)….WHAT ARE SMART BOND INVESTORS GOING TO DO?

Debt…unlike equity….HAS TO BE PAID OFF OR ROLLED FWD. The INABILITY to do so…because cash flows no longer support rolling it forward at higher interest rates…results in increasing defaults…which accelerates the rate at which interest rates rise. This is entirely predictable….so the smartest bond investors are going to shift their money elsewhere…but WHERE?

The only market that can absorb even a fraction of the shift will be the global equity markets….with the markets having the most stable or appreciating currency being the largest recipient. Currently this is the U.S…..so even though our equity multiples are historically high…they WILL go higher. (Think back to the Roaring 20’s)

Since the collapse of Bretton Woods….the trend in global capital has been liberalization…..increasing freedom for capital to move wherever it desired….until RECENTLY. Increasing domestic financial problems (rising need for higher taxes now that the FINANCIALIZATION-created growth bubble has stopped…and in threat of reversing) is forcing politicians to introduce increasing barriers to the free flow of capital (see China….rising nationalistic trade policies in the U.S. and Europe). Some countries will begin to be frozen out of the bond market….whether due to a commodity price collapse as occurred in Latin America in 1928…or realization that teetering-on-the-edge-of-collapse EU-issued bonds HAVE NO market other than the equally-teetering-on-the-edge-of-collapse ECB (as the last and only buyer).

Take your pick….either Greece or Italy ALONE is enough to push the ECB over the edge into cascading collapse….and BOTH are collapsing before our eyes.

Take your pick….either Greece or Italy ALONE is enough to push the ECB over the edge into cascading collapse….and BOTH are collapsing before our eyes.

As in 1928 and 08 the US event was made global by a trigger in Europe.

1929 was the collapse of an Austrian bank, 08 was driven global and huge by greece.

Today everybody is pointing the finger at china the potential Europe (Clubmed) to cause globalisation of an issue again is HUGE.

I don’t think China and Japan are being singled out. The problem with both is that their systems are more opaque to Western financiers and wedded by the hip to their respective governmental systems….so both will be supported until their gov’ts collapse under popular revolt.

Europe is the most likely folcrum for where the crisis comes from just because the support for the banks there is the ECB and EU….not the national gov’ts directly. As Italy and Greece show….the NATIONAL gov’t is somewhat powerless to prevent the collapse of their banks…as there is no national currencies to fall back on to devalue the liabilities. The problem there is that with members talking about leaving the EU (Britain, Greece, some Eastern Europe areas)…the confidence of the markets in the EU as a continuing entity is massively reduced…..and without that confidence…the EU currency (needed to bail out of the Greek, Italian, Spanish, French, German, etc. banks) evaporates like a fart in the wind.

“he confidence of the markets in the EU as a continuing entity is massively reduced…..and without that confidence…the EU currency (needed to bail out of the Greek, Italian, Spanish, French, German, etc. banks) evaporates like a fart in the wind.:”

This is the inherent principle flaw, in any fiat currency, with no tangible asset base..

This is why P45 is so globally dangerous, as he has the ability to undermine that confidence in the $ US>

chinese financial system is deliberately opaque so you can not see what the State is really doing, paying its bills by physically printing TON’S of CNY.

The amount of physical cash in circulation in china, is deliberately undeclared.

This is before you look at the amount the State has digitally created with no counter double entry (Digital printing), to pay its accounts.

At least in the US and Europe you know how much they have created, in what manner.

Japan is not Opaque it simply make’s you wait for the annual statements.

( Why should we release this information to pesky foreign journalist, who simply want to pick holes in it, and project negativity about us constantly? They can wait for the annual reports to be translated) being the attitude in Tokyo.

$4 trillion

– In spite of the DOW rising above 20,000 some other indicators didn’t confirm that move. E.g both the yield curve and the DOW Theory “diverged” from the DOW since say early december of 2016.

– The DOW is getting “high” on a substance (I hope it’s legal)

– Some other folks have branded it the “Donald Trump Kool Aid”.

Why the legal stuff is the worst stuff

Sounds more like Double Bubble gambling to me. Remember the old Far Side cartoon where one of the cows says “Wait a minute. This is grass! We’ve been eating grass!” https://www.pinterest.com/pin/493566440396361251/

When that happens, everyone will run for the exits.

All that foreign cash pouring into the US (Mostly CNY) has to go somewhere property is looking tricky, so markets look better.

Various financial pundits, talk of the great ball of chinese money that bounces from bubble to bubble in china

There is another great ball of chinese money bouncing around the globe what happens to America (Dow Etc) when that ball bounces to another place??

Nah–it’s 25+ trillion of central bank (printed) money in financial assets

Absolutely false, Mickey. The Federal Reserve has not “printed” $25 trillion of financial assets at all, and has only increased the monetary based by $3.6 trillion as a result of its 3 QE programs with 100% of those funds always remaining inside the primary and excess reserves accounts of its member banks inside the Federal Reserve. The Federal Reserve only purchased EXISTING SECURITIES consisting of MBS instruments and US Treasuries from US member banks with those member banks having NO NET GAIN WHATSOEVER and with the cash proceeds being deposited into their reserves accounts inside the Federal Reserve which is precisely where that $3.6 trillion has always remained.

As to financial assets, the markets have bid them up to absurd, preposterous, and stratospheric levels based on gambling, stupidity, false perceptions, and hopium and those assets will be coming crashing down in stocks as they are not supportable based on the fundamentals and there is NO CASH AVAILABLE TO CASHIER THOSE STOCKS OUT at anywhere near current price levels.

Total stocks in the US are now market valued at more than $27 trillion and bonds are valued at more than $47 trillion and yet the total M2 money stock is only $13.276 trillion which includes all cash, checking accounts, and savings accounts in the US as of 01/16/2017.

“Markets can remain irrational for longer than you can remain solvent” keeps playing in my ears.

Wolf, the statistic I would be interested, having worked in pension accounting is, what would earnings be if the internal rate of return of their pensions were adjusted to 3.75%, which is Ray Dalio’s estimate of total returns for the next ten years.

When I look at UPS, 7.75% ROR extimate and $9 billion in pension liabilities, I’m thinking bankruptcy, not peak earnings.

Non-Gaap accounting means never having to say you’re sorry for revenue declines. Read the book, “Where Are the Customer’s Yachts” for advice on what’s next.

Visa integrated european operations to pump up sales. I coincidently went thru this exercise thursday.

Here is another issue. In the stock market you pay up for growth. Where is the growth with gaap pe somewhere around 25. What about PEG ratios.

Bloomberg reported this week that central banks own 25 trillion of traded stocks and bonds. Thats about 15% of whats out there.

Daily FOREX looks to be 4 trillion. Shed trading for real trade and other transactions and we have 3trillion of lets call it speculative trading by thise with deep pocket where nobody says anything about churning that trade.what does that mean, could it be by gosh, manipulative.

by the way, forget CAT and IBM and WMT et al for a moment.

SBUX and COST, two really well run newer companies: SBUX used to see growth in the upper teens %, and with new stores of perhaps 3-4%, it is not seeing 7% growth.

Costco pretty much the same, used to be in the teens and now 3% although gas sales have had some effect.

Our population here in US used to be around 2% or more and now its .7% (that we know of) and the average is increasing (think our ponzi Soc Sec and Medicare and Prescription Drugs) and now think about the kids deferring families which also defers housing and cars and mini vans and diapers and rapidly changing clothes sizes.

I think we are in a qualgmire for many reasons but in the end rather difficult to fix and cannot be turned on a dime.

When you look at population topping and decline, think about the velocity of money. Both topped in the 1995-7 time frame. What a coincidence!

Wolf–your data matches fairly well with mine which I used the IBD marketsmith charts –about 2/3 of the Dow stocks have reported covering the 4th calendar qtr 2016 as several have Jan or Feb qtr ends.

I am wondering to what extent the revenue numbers took a hit on account of the strong dollar. Was it in any way significant ? Anyone want to chime in ?

do no tknow but when dollar is weak and sales improve nobody complains about that.

All true- but to have these lousy flat lines just after the largest shot of financial adrenalin in history- that is ominous.

The parallel I think of is going to a doctor and having your blood pressure checked. If it reads a bit low, he thinks no big deal. Then you tell him you’re taking massive doses of a blood pressure booster.

What does he do? He phones for an ambulance.

“All true- but to have these lousy flat lines just after the largest shot of financial adrenalin in history- that is ominous.”

Policy has had exactly the intended effect: to restore and enhance the financial markets without restoring the real economy, thereby enriching the wealthy at the expense of the subject population.

The hyperrich will quite naturally complain, not because they are not getting richer, because they are, but because they do not yet have everything. Which brings you to the next phase, which is to put Social Security into the stock markets, discontinue all other social programs, and remove any remaining taxes on the wealthy. This is expected to put the DJIA well over 30,000, again while revenues are in decline, further enriching the wealthy while reducing the 99% to destitution when the markets go bust.

This in turn will result in more rounds of bailouts for the rich while the subject population again gets nothing. History repeats itself, sometimes rather loudly.

The U.S. national debt can be expected to at least double, which will be just fine with the hyperrich because they won’t be liable for any of it.

Felix_47:

‘“Markets can remain irrational for longer than you can remain solvent” keeps playing in my ears.’

Karma can stay unbalanced longer than you can stay serene.

FYI, Orwell’s “1984” is #1 on Amazon’s bestseller list, while “It Can’t Happen Here…” by Sinclair Lewis is at #4.

https://www.amazon.com/best-sellers-books-Amazon/zgbs/books

I meant to say population groth is decreasing and SBUX sales growth is NOW 7%.

Wife is all over me to get out of house now!

SBUX growth is 7%, my cup of coffee at SBUX just went up 20-25%. There is now growth……

I now brew at home, only a matter of time before everyone else does too, except the debt addicts (watch how many people pay with something other than cash).

$2.45 for a cup of coffee, seriously,

dow 20,000 WHO CARES! ?

I added the closing prices from Dec-20-2016 and got 2,903.35

If you multiply that total by 6.8798 you get 19,974.62 Divisor is .1453519

On Oct-12-2016 the ‘dow’ closed at 18,176.32

The 30 DJI stocks totaled 2,652.87

A factor of 6.85157 would have shown the ‘correct’ total, 40 trading days earlier. Divisor .1495952

The usefulness of non-Gaap reporting is far greater than the nonsense that this “important” index is based on.

Those that focus on the SP500 are getting a better view of the market. At least it’s focused on Market-Cap which means the ‘adjustments’ are done daily by the market and not some scrivener.

My favorite is EBITDA. And add lotsa Goodwill to the balance sheet.

We’ve been living in a matrix of ambiguity and obfuscation for quite some time when it comes to the world of finance (what matters to most people). In this age of algorithmic programmed-trade executions, we the the boorish proletariat can only go along for the ride.

The financial markets are on the amphetamine of free money from the government. The S&P 500 chart is nearly straight up. This will not end well.

You won’t find those revenue drops discussed in the general media. This means all earnings gains over the past many years are from unsustainable sources.

Let’s add up the plays that have been employed for many years to temporarily inflate the profits:

-Cost-cutting (layoffs)

– Stock buybacks

– Issuance of debt at suppressed interest rates

– Cash acquisitions, which allow companies to increase earnings without increasing the shares outstanding and without need to amortize the purchase price (the goodwill).

-Lax pension funding rules (allowing companies to use a 7-8% assumed rate, as noted by another poster), which drastically understates true pension cost

-Aggressive tax planning and lax tax enforcement, allowing companies to report huge profits in zero-tax jurisdictions.

-Reported revenue “growth” includes a 2% inflation subsidy the Fed adds to their top lines every year.

-Outsourcing of labor to jurisdictions with low wages and few worker protections.

-Reporting profits on a non-GAAP basis (cherry-picking)

-Reporting sales growth on a constant currency basis as the USD rises (a recent change in approach)

You have to wonder if this can go on much longer, given the illusions have been in place for several years now. The public can’t pinpoint the causes, but they sense corporations are screwing them. The pension holders, in particular, will likely revolt when it becomes clear their pensions have been intentionally underfunded to pad profits of the 1%.

I do see some of this ending now. Trump is hammering the outsourcing play. Foreign countries are vigorously attacking the aggressive tax planning, as part of a coordinated effort. Stock buybacks lose their power as stock prices rise and companies can buy fewer and fewer shares with their fixed cash flow.

I think the stock market collapse could happen any moment now as a result of this.

Tina and the magic stock repurchases?

Making it look like growth by reducing the capital account?

Shareowners being taken to the cleaners by their boards?

It is hard to imagine Stock Market exuberance will continue much longer after Week 1 of this new Presidency. We are on the edge, as far as I’m concerned.

Stability is good. Predictability produces confidence, or at least allows sober investment considerations. If this upheavel continues much longer people will rush for the exits to lock in. After that, the stampede begins. It could happen anytime. People will have to find buyers, fast…and we all know there is only one way to do it; drop the asking price.

I know people who have already started to hunker down, both mentally and financially.

Revenue does not matter. The march is on to a monopoly in every sector. The trust busters have been paid to stand by and watch. The profits are going to be astronomic.

sell what to buy what?

Potash ( potassium fertilizer) to feed humanity.

Land for the same reasons.

Seed companies

Lithium ( meaning, in all cases, producers and the actual commodity itself, using an ETF )

Gold, Silver and P.G.M. ( again the metal, and also the mines )

Uranium for power ( metal and porducers, both )

Agricultural land bears repeating

Personal firearms manufacturers

Bullets too

Copper, steel, moly, aluminum and mang, now plentiful, might become good to own, again, soon.

Tungsten is ALWAYS good.

OIL ? Who knows ?

Water and pipe and water-pumping companies.

–

Once you see beyond our current so-called “deflationary” malaise, lie that it is, the future is crystal clear.

–

Start with Lithium, Gold and Silver. OK ?

SnowieGeorgie

In my last comment ( my reply to you ) I forgot to add a hundred or so BFs ( Ben Franklins ) safely and securely stored. In a waterproof container.

YOU NEVER KNOW WHAT’S COMING NEXT. A poster a few weeks ago said my penchant for BFs is wrong — and AJs ( Andrew Jacksons ) are better.

I am sure he is right, but I am stuck in a BF groove.

All of the things I mentioned are just several of the planks in a quite secure platform.

SnowieGeorgie

OK — one final point which should have been my FIRST POINT :

TO DO WELL — buy low and sell high.

Americans, in general, tend to do the opposite. They chase high fliers that are rising.

TO BUY LOW, buy things when they are out of favor, even despised .

http://energyandgold.com/2016/04/22/nobody-knows-anything-investing-common-sense-from-bob-moriarty/

Is that stocks, now ? NO. Is that real estate now ? I think not. Bonds are a bit more complicated. Bonds are going DOWN, because interest rates are RISING.

THAT IS A TRUISM, my friend. Do you think that interest rates have completed this cycle of rising ? I guarantee that interest rates have a long way to go before they are done rising, Are normalized. ( There will be hiccups along the way to be sure.)

What IS OUT OF FAVOR now ? What is, in many ways, DESPISED ? What has been down for several years ?

COMMODITIES !

Buy low sell high NECESSARILY MEANS THIS :

(1) Buy what is OUT OF FAVOR

and

(2) Sell what is ADORED.

Buy low sell high is contrarian. Be a contrarian and make money, or follow the crowd, and watch out below.

CONTRARIAN IS A DIFFICULT ROAD TO FOLLOW.

SnowieGeorgie

“THAT IS A TRUISM, my friend. Do you think that interest rates have completed this cycle of rising ? I guarantee that interest rates have a long way to go before they are done rising, Are normalized. ( There will be hiccups along the way to be sure.)”

The economy is pushing on a string. Growth is tepid at best. Deflation or disinflation are still the #1 threat to the global economy.

The 10-year will hit 1.5 before it hits 3.

I kind of agree the 10 year goes down next–but then its a gonner as everybody realizes we are a credit risk.

companies borrow for 2 reasons-to fund growth or to fund losses. Countries too.

Could you imagine if Wolf did a chart that was adjusted for inflation?

look at the companies that really indicate true growth like CAT ‘s. United Health Care’s revenues

are up due to OBAMA care (fiscal stimulus) . JP morgan ‘s revenue is up from fixed income trading/revenues ? and probably triageing cheap

fed money . why Goldman Sachs and JP Morgan are in the sacred DOW should tell you a lot. NET NET -Dow represents multinational companies . this revenue stagnation is global

There are really only four broad options for most investors- stock and bonds and real estate and commodities.

Real estate is not liquid so that caters to a particular submarket of the investment community. We’ll ignore it.

Which means that if bonds are tanking in a deflationary environment that mocks commodities why wouldn’t stocks rise?

You can juggle figures until you’re blue in the face, rant about reality all you want but money must go SOMEWHERE to earn a return.

The best least bad place right now is stock.

Revenue stream limited?

Corporations can go to zero-based budgeting and cut costs.

Here’s an article about that: Note that job cuts are not mentioned anywhere! People are not worth mention to corporatocracy accountants:

http://www.reuters.com/article/us-usa-companies-budget-idUSKBN15E0CF