Preconstruction condo flippers left twisting in the wind.

The lure: Buy a preconstruction condo from a developer in the early stages of development. The initial deposit is small, and in a booming market, the payoff big. Additional payments need to be made as the building progresses, but lenders are eager to lend as condo prices soar. Everyone is in nirvana. This bet has been hot in the condo construction boom around the country. But in Miami, the bet is now collapsing. And preconstruction condo flippers, the lucky ones that could sell their units at all, are bathing in a sea of red ink.

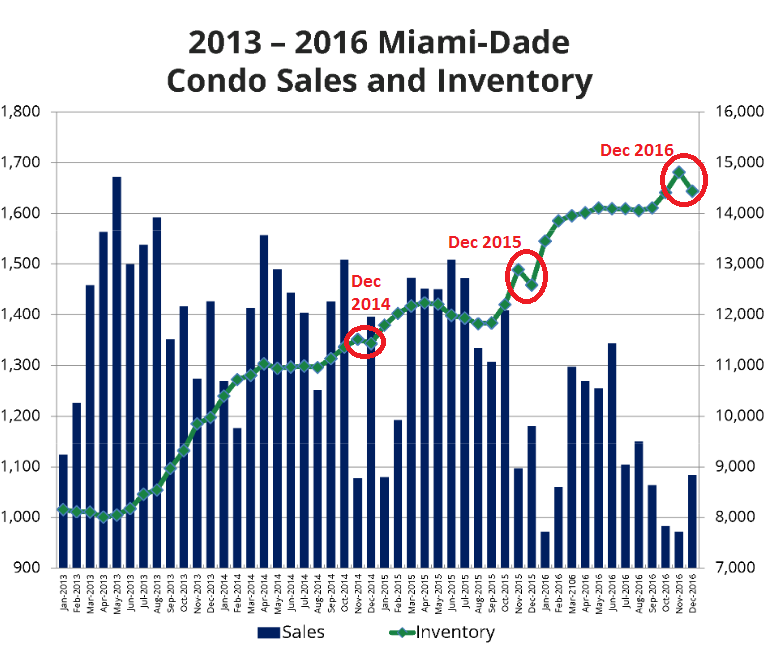

First things first: The overall condo market in Miami-Dade has gotten tough, with the inventory of condos for sale ballooning and with sales plunging.

In December, 1,084 condos and townhouses were sold, down 7% from December 2015, down 22% from December 2014, and down 24% from December 2013, according to the Miami Association of Realtors. While the median sales price still edged up 1.3%, the average sale price dropped 12.6%, and the dollar volume of those sales plunged 19.4%

Inventory of condos listed for sale on the Multiple Listing Service (MLS) jumped 16% from December a year ago, to 14,436. At the current sales rate, 12.7 months’ supply. But as we’ll see in a moment, developers don’t list all their unsold units on the MLS in order to avoid the appearance of a condo glut, and these inventory numbers are understated.

This chart by StatFunding shows the decline in sales and the surge in condos listed for sale. Note the seasonal drop in inventories from November to December. I added the red marks to show just how much the inventory glut has ballooned over the past two years:

This is not a great market for preconstruction condo flippers and for developers that have recently completed or are now completing condo towers that began sprouting like mushrooms a few years ago.

Andrew Stearns, CEO of StatFunding, tracks the Miami-Dade market for preconstruction condos along with the money that is being made, or lost, in those transactions; and he tracks the condo units that developers have been unable to sell. He notes in his January report:

From 2012 to mid-2015, Miami developers sold all units in each project within months of completion of the project. The inflection points of previous condo cycles have been marked by developers getting stuck with unsold developer units.

And that’s now happening.

Of nine large projects completed since late 2015, ranging from 90 to 390 units per project, with a total of 2,080 units, developers are still sitting on 400 unsold units, or 19% of the total. Of them, 327 are listed for sale on the MLS.

The newest addition, the CityCentre Rise, was completed in September 2016. Its 390 units should have sold during the development process, but didn’t. Now the developer is sitting on 217 unsold units, or 56% of the total. And only 20 of those units are listed for sale on the MLS.

This shows how the MLS inventory-for-sale numbers understate the total count by understating the new units that are completed and that developers are sitting on but are not listing on the MLS. Developers don’t want to pull the covers off the enormous condo glut.

This condo glut is starting to leave skid marks.

The developer of the 190-unit EchoAventure, completed in August 2015, has taken out a bridge loan secured by the 15 unsold units, a sign that even the developer is not expecting to sell them anytime soon, after having failed to sell them over the past year-and-a-half. According to the report, other developers haven’t repaid their construction loans.

But it’s costly to carry unsold units as the developer has to pay taxes, maintenance fees, and insurance.

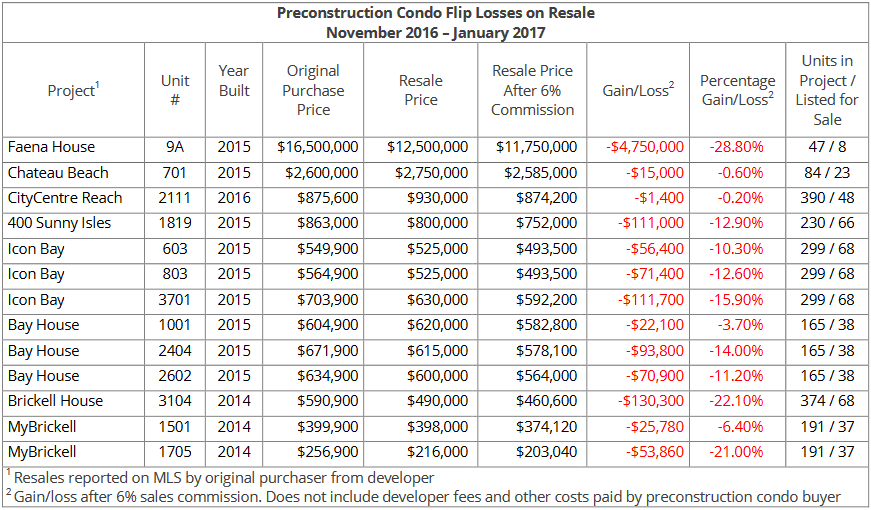

In this environment, condo flippers – in direct competition with developers – are taking some heavy losses, the lucky ones that could sell their units at all. Here are some of the units they were able to unload from November 2016 through January 2017, with losses indicated after 6% sales commissions. The most expensive condo in the batch generated a loss of 28% (click to enlarge):

Condo flippers are increasingly willing to take a loss to unload the unit. So the number of preconstruction condos listed for sale at a loss continues to climb. And “because there are so many listings-for-losses in the market,” according to Stearns, “comparable sales prices are trending down….”

The pain is likely to get worse. In addition to the units that developers are sitting on, and those that preconstruction flippers have bought and are trying to unload, there are more than 10,000 additional condos that will be completed in 2017 and 2018!

“Unless something extremely positive and unexpected occurs which completely changes market conditions,”Stearns writes, “Miami condo flippers should expect losses on resale to continue.”

And this is how a condo construction boom turns into a condo glut that unravels the overall condo market – unless of course said miracle happens, and it would have to happen by about right now.

There has been a generational shift in the US housing market after the Financial Crisis. It has turned Wall Street into the largest landlord. And Wall Street gets its way, as the government buckles and guarantees buy-to-rent Mortgage-Backed Securities for the first time ever. Read… Financialization of Rents Gets Taxpayer Guarantees

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf when will you ever learn to put a positive spin on the negatives? If MSM was reporting the same stats, then you’d get something like:

“Sales are down due to supply shortage. Prices are soaring, but cooling down which should provide a good opportunity for the first time buyers.”

Who needs reality when we all can be happy in la la land?

oh man, Cyrus- that is SO funny and too TRUE!

Thanks kitten. I know; all real estate video clips from MSM, or real estate agents and companies, whether it is American, Canadian, or Australian use these 2 phrases “lower sales due to supply constraint”, and “Opportunity for first time home buyers.”

It’s as if there are a few at the top of the ponzi scheme, and they come up with terms and phrases, and the brainless peons in MSM, and the sharks in real estate are told to use the same terms to find new victims to keep the ponzi going.

Looks like Ms Yellen needs to fire up the inkjet again

How will that affect demand?

It will get inflation roaring and get people to buy real estate as a hedge

Music to my ears. Here in SF Bay area, developers have been on an apt/condo building binge for over a year now and show no signs of abating. This is going to make the 80’s housing glut look like a practice run.

From time to time I go thru a $1M+ open house and the realtor usually asks why we’re not ready to buy right away and I say, “Nah I’ll give it a couple years when prices are 40% off.” They always act a bit indignant and push the, housing prices will always go up, spiel. And I comment on fact that their number of days on the market keeps creeping up and I see more reduced price signs appearing every day. That usually shuts them up.

I do the same thing Patrick It’s so much fun to annoy brokers isn’t it?

Oh come on, an earthquake will create a housing shortage for sure. And 40% off is probably still overpriced.

Earthquake ?

In Florida ? Not too very too likely. At least not anytime soon.

Florida is 100 feet ( mean ) above sea level, and much of the coast is barely above sea level.

http://thetruthwins.com/archives/what-would-happen-if-a-giant-tsunami-hit-florida

QUOTE FROM ABOVE LINK : “Most people don’t realize this, but almost the entire bottom half of Florida is just barely above sea level. If a giant tsunami did hit Florida, there would be nothing to stop it from sweeping across the entire state…”

Condo glut will be ameliorated by a YYYuuuugggee undersea earthquake just west of Spain and Portugal.

SnowieGeorgie

Snowie Georgie, no– when Not So Sure said to wait til “an earthquake,” he’s not speaking on florida— it’s what all San Franciscans who’re left holding on in this toilet bowl always say to feel better / like things will return to normal once there’s a big quake and all the carpet bagging riff raff are shaken til scared off.

but i’m also… NOT SO SURE anymore. (of anything at all.)

Yeah, I stayed focused on FL condos when the focus had shifted over to S.F.

Thanks for the clarification.

So a tsunami is a possibility in the great NorthWest ( WA , down to OR, a bit ) and all of Florida as well.

I wonder how SanFrancisco will do in the next earthquake ?

It could be much bigger than the last few century’s experience suggests.

I feel relatively safe from earthquakes and tsunamis here in the northeast .

https://en.wikipedia.org/wiki/1755_Cape_Ann_earthquake

But, we are overdue for one as we get close to 300 years since the last one. Much of Boston is like the filled areas of S.F, and will liquefy if a good sized earthquake hits the area.

SnowieGeorgie

We’re not waiting for the big wave here. We’re waiting for the first bank to refuse to issue a 30 year mortgage in Florida due to sea level rise forecasts. Expect all real estate to be down 60% within a year after that. If 2017 warming is similar to 2016 even without El Nino and a lender gets skittish it could be as soon as 2018. Of course A mortgage crisis that dwarfs 2008, but with no recovery….

I’ve been doing the same here in Portland, although, admittedly, I’ve been doing it for a few years, so a 40% drop would get the prices right back to where they were 3 years ago when I started. Argh!

I’m looking for early 1970’s prices, but cash-only (or gold) in pdx.

The huge amount of pre-construction flipping looks similar to what was going on at the Spanish Costa before 2008. Buyers from countries like UK, Netherlands and Germany purchased condo’s without even visiting the area and often resold them at a profit before construction was finished; the gains were usually reinvested in the Spanish RE market for additional or bigger properties. Easy money until the game of musical chairs suddenly stopped.

Still, I haven’t seen many stories about EU flippers losing everything due to the Spanish RE bust, maybe because prices there are still strongly elevated (like 40-50% down from the top, but for many earlier buyers without a doubt still several 100% up …). I do remember reading that many properties were kept off the market by the banks for a long time. And many flippers were probably saved because their native homes – that were often used as collateral for the loan – in most cases kept appreciating, except for a small dip after 2008 (and even if not, they could take out an additional loan on their first property for almost zero cost thanks to the ECB). In some cases they probably used black money to buy the Spanish properties and now prefer to keep silent, just in case ;-)

AFAIK, this kind of pre-construction flipping is almost non-existent in Netherlands. Maybe because supply is always below demand here, or because developers normally only start building when at least 80% or so of a new development has been sold on paper?

I also wonder with so much flipping activity, how sure can we be of data like original purchase prices? There are so many opportunities for crooked developers to use kickbacks and artificially inflated sales prices, maybe it works a bit like the art market nowadays where the dealers use all kind of tricks to push prices up and buyers are happy accomplices??

To me, this is how a financialized economy distorts markets, and makes suckers out of people who want to do old-fashioned business. Builders who thought that pre-construction sales meant a good demand for condos are getting shafted. What there is is a big demand to finance condos. The buyer/flippers are looking a short-term deal, much like a loan, with the wrinkles that the gain will be taken as capital gain rather than interest income, and the party who pays off the “loan” will be different from the “borrower”. Like the long-term bond market, maybe?

On completion, the biulders then find that the finished units they still own have to compete for market share with the units that they “sold” before, in a market where nobody really has that much money for condos.

Maybe waiting for 80% pre-sold would get you a few real buyers in the crowd, but I wonder how you could be sure, when the existence of the finance business has loused up the market signals this badly.

it’s definitely about speculation (short term) and not investment; you can’t expect much yield from properties that are empty most of the year and a dime a dozen …

in Netherlands we don’t have any tax on RE gains so it really is easy money; and for properties in Netherlands the mortgage is tax-deductible as well (of course, many people financed foreign properties by taking out a bigger mortgage on their Dutch home: heavily subsidized low, and zero tax on any gains ; easy money …).

Indeed I’m not sure those 80% pre-construction buyers in Netherlands are all going to live there instead of just trying to flip it in 1-2 years. I’m not hearing the frenzied flipping stories I heard 10-15 year ago, but maybe people are just keeping a bit more silent because of all the shady deals going on behind the scenes. e.g. the loan on the property is no longer income tax-deductible here if it is a second home or if you rent out the property. But the tax office doesn’t want to know if you are cheating, so as long as you keep silent you can pocket tax-free rent, huge tax subsidies and tax-free capital gains on several properties …

There were so any UK buyers ripped off in Spanish developments it was taken up at the highest levels of government- at the PM level.

An entire city council in Spain was arrested for allowing a huge unauthorized condo development on park land. Over a thousand units were looking at demolition, even though many had been pre-sold.

As to what recourse those folks have- who knows.

A close friend of ours recently sold his town house in Spain- an interesting property alright about a hundred years old, and although he didn’t lose his shirt and lived there quite a while. he found out some things about the Spanish real estate ‘industry’

There are no particular requirements to be a realtor, and no such thing as a listing, so he would see his unit advertised by people he’d never met. The photo would have the house number blurred out so no one could contact him directly.

There is also no law against a ‘net listing’, an agreement where the agent keeps whatever he can get over the ‘net’ to the owner. So he would see his unit advertised at different prices.

One kind of quaint thing- about a week before the closing. This is big expensive deal in Spain and in many countries, which have secure property rights once you have them, but they do not have a truly modern system of Indefeasible Title or Torrens system.

The title must be investigated by your notary to be sure it’s valid.

This is similar to the old Doctrine of Notice in the English- speaking world a century or more ago, wherein the buyer had to take notice of unregistered claims.

Anyway just when he thought this month- long process was over- his guy phones and says I’ve just found a condition on the title: a certain lady has the right to stay overnight for a day or two when she’s passing through.

This was an old entry, no one knew if she was alive or what. She never turned up, but our friend had to accept this to go ahead.

Caveat emptor and then some.

I know about the illegal construction and demolition (Almeria IIRC) although that demolition was mostly to make an example (also for developers), and not a significant percentage of the illegally build properties. It’s really sad and should be a warning about Spanish RE (and Spanish law in general) indeed.

I don’t think the Spanish realtors are much different form the Dutch ones. Anybody can be a realtor here too, although they tried to control things a bit for years through mandatory (very expensive) realtor club membership in order to use the main (monopolistic) RE website. There are some more rules for negotiations with potential buyers compared to Spain, but that’s about it – and realtors are always very clever in finding loopholes around the regulations.

My brother lives in Spain, even ten years after buying he still doesn’t know exactly where all the land is that belong to the property. It’s not worth much, but the whole registry can be very shady. And he also has to deal with idiotic regulations like giving people access right through the property to a well that no longer exists etc. …

We have something a bit similar in Netherlands with ‘recht van overpad’ (right of passing through?) which applies to many gardens and small alleys in inner cities. Even if you own it, sometimes a dozen other people have the right to use the garden or alley for access to their own home or garden, even if they have other means of access. It’s a royal PITA, I will do everything I can to avoid such clauses if I ever buy a home again.

Here’s a comment from a Scandinavian I saved from those days:

“The banks are on the verge of bankruptcy. They don’t have any money left. They have tens of thousands of flats and construction projects estimated at fantasy amounts on their balance sheets.

A lot of these objects are impossible to sell and have a negative value since demolition is the only option. The rest may have a maximum market value of 20% of the book value.

The banks cannot sell since this would force them to lower their prices and the whole house of cards comes tumbling down.

I have a flat on the Costa del Sol, in a complex where the banks own roughly 80%. Those who bought their flats desperately want to sell, since the whole area is decaying. The banks do not pay the maintenance fees, and have not done so since 2008, in the hope of shifting these accumulated costs onto future buyers. Private buyers who once paid cash and are trying sell have lowered their prices to EUR 30-50,000, but nothing much is happening. The banks have their flats for sale for the same price as in 2007, app. EUR 200,000, otherwise their balance sheets will crash. Those who bought with mortgages have long since stopped paying the banks and have abandoned their flats. Many of those who have left did not even empty their pantries and fridges, so the places are full of vermin and cockroaches.

During the golden years a lot of people from South America came to Spain, got jobs, bought houses and flats with mortgages of 110%, no problem. They were the first to abandon their houses and flats and left Spain. Subsequently many other foreigners and Spaniards have abandoned their overleveraged houses and properties.

Up until 2007, thousands of very poor quality houses and flats were built along the coasts. The aim was to build as much as possible in as short a time as possible, sell fast and make a pile of cash. Now, after a couple of years, it turns out that some of these buildings were constructed on foundations that shift and/or move, so the houses are falling apart all on their own. I have seen examples of people who have paid their life savings for their dream house and after a couple of years they are banned by the authorities from going anywhere near them. It is too dangerous since they have ten-inch cracks and are falling apart.

The banks have also lent money to thousands of houses that were constructed without building permits, where local authorities demand demolition. These negative value properties also have fantasy valuations in the banks’ books.

The banks have lent money to practically anything, with incompetent bank employees granting loans of 150% of a fictitious, out-of-proportion value (since all prices would continue to rise in all eternity and the envelope with the 5% kickback does wonders). Building permits and things like that could just be ignored. Faked building permits could always be bought from local civil servants, if necessary.

The Spanish real estate market is an utter morass, a complete disaster that few people realise the full scope of. Reality is scary, with banks and a building trade that have acted in hair-raising ways. The real deficits in the banks are gigantic, of Biblical proportions!

And the banks have desperately hoped that the market would turn around and a miracle would happen. But miracles don’t happen often and now reality has caught up.

So the Spanish state, which is bankrupt, is going to refinance a bankrupt banking system with money from northern Europe’s tax payers via the ECB?

Somebody has to put a stop to this!”

In Spain appraisers are employed by the banks

It’s the same in Australia too. Wonder if that could be part of te problem

in Netherlands most appraisers are not employed by the banks, but the same problem exist. They know they have to hit a certain target, otherwise they will soon not get any new business.

Some (many?) appraisers simply ask what the target value of the mortgage is and then appraise the property for almost exactly that price; and of course most prospective buyers think this is great.

The bad construction is indeed an additional time bomb both for the banks, current owners and prospective buyers.

In Netherlands loans of 120% were completely normal 10-15 years ago, and I have even heard about 200% loans and all kinds of strange piggy-back mortgages … But at least the properties themselves have usually good construction compared to Spain and probably many other recent EU properties. During the boom years many properties were delivered to the buyers with dozens of shortcomings / flaws, but most of that was of a cosmetic nature and relatively easy to correct.

Looking at ‘foreign home buying’ TV shows where people (often from UK) are looking to buy on the Spanish Costa, it often strikes me that the properties shown are still hugely expensive, more like small 200-300K euro flats than the 30-50K properties mentioned above. Maybe those TV shows are financed by the banks as well ;-(

In the interior of the country it is now easy to find attractive properties for low prices (like 3-10x cheaper than similar property in Netherlands), but that has probably always been the case.

“So the Spanish state, which is bankrupt, is going to refinance a bankrupt banking system with money from northern Europe’s tax payers via the ECB?”

Let’s hope for the Spanish state that those northern EU speculators still have some money left to pay taxes, after the losses on their Spanish and native properties are booked ;-)

biblical, exactly right.

42% of rentals in Manhattan are offering incentives of 1 to 3 months free rent. Something is changing on the demand side.

Correct people are moving to sane places like the Carolinas and Texas

Do not worry, I am sure the cracks are not structural :)

A whole lot of “stupid” is being fixed in Vancouver right now, as detached house sales are down and have been so by around 75% for 6 months running.

Speculators have ditched plans to build on the empty lots they paid 1.5-2 million for and have ads up that say stuff like:

“Prime building lot with final approval, ready to be picked up.”

I’ve seen new houses up for sale in neighborhoods where a developer is trying to sell his empty lot for about the same price.

You know there’s blood flowing when that’s going on.

When I looked at Vancouver rental market on Craigslist, I couldn’t believe how cheap rental is in comparison to hot spots in US; even Toronto is not much better. Australia doesn’t seem to be any better rental wise.

Price of a house, and how much you can rent are always related; otherwise, what is the use of purchasing more than one house? So, if you consider how much income you can generated from houses in Vancouver, Toronto, or hot stpots in Australia, the average prices should be around $300K at best.

A$300,000 for an average price of a house in an Australian ‘hot spot’?

For my suburb in the Melbourne area you would have to go back to 2005 to get a median price under A$300,000. And my little part of Oz isn’t even considered anything like a ‘hot spot’. Too far out from the CBD.

But stats lie………….

Because of the large size of the suburb, the huge growth in population and number of new houses being built has kept the median price low.

Too many cheap quality houses being built on stinky little lots the further you go from the train station in the past few years. Those houses and new developments didn’t exist in 2005.

If you were to take the same sample of housing that existed in 2005 and look at the median price now for that sample my SWAG would be around the A$800,000 area or higher.

Many ‘hot spots’ are in or near the Melbourne CBD and have distorted the numbers for housing prices in Victoria.

For example, way back in 2005 you could get a house in Brighton for a median of A$1.1 million. Today that median is A$2.2 million. From 2013 the median price in Brighton has moved up by more than average price of a house in Australia. ( I wonder when the median price was A$300,000 in Brighton – 1970 ????)

Now look at a couple of areas that have been impacted by Chinese buying. In 2005 the median in Box Hill was A$487,000. Today it is A$1.4 million.

Mount Waverley was A$425,000; Now it is A$1.05 million. Glen Waverley was A$419,000 and now it is $1.18 million.

Many areas in Victoria have seen an annual rate of appreciation over the past ten years of less than 2%.

Even suburbs next to each other have seen huge differences in price changes.

So next time you see the ‘doom and gloom’ articles about how Australia is going to crash just remember: the facts in real life are quite different than presented.

(About time for one of those ‘doom and gloom’ articles, isn’t it???)

Lee, you don’t seem to comprehend much. If you have an extra house, what do you want to do with it? Bring your grandma to live in it? You want to rent to generate income.

Now, you want to rent out a $1.5 mil house to get a $1200 month in Australia? It would take you exactly 104 years to get your investment back, assuming you have paid it in cash. If you have mortgage, then it would take you probably 250 years to get your investment. It’s all about investment; something you don’t seem to know anything about.

‘Price of a house, and how much you can rent are always related; otherwise, what is the use of purchasing more than one house?’

Specifically- not.

The price should be related, but in an overheated market this quickly fades, and in a bubble market becomes insignificant. In this environment, the buyer is NOT seeking the use of the property or its rent. He is seeking the profit from the flip. I’ve been a realtor in a market where houses were being ‘double deeded’ i.e, flipped again before the first deal closes, so the lawyer has to deed it twice at the closing, once to the first buyer, next to the second buyer. In this environment no one wanted a renter, especially if the house was new.

In this phase the RE market is not much different from the market in art, or tulip bulbs, neither of which generate rent. And of course hot stocks like social media are priced far beyond their ‘rent’ or dividend.

However when the bubble bursts, RE regresses to the rent it can generate. A sign of a truly busted market is a street full of For Rent signs.

Needless to say, the crash after the early 80’s ‘double deeding’ phase was epic. One condo project site that sold for about 250 in 1982 sold for about 75 in 1985

Cyrus,

Well you must be one of those know nothing fake posters or in other words a rude little pr*ck.

Thanks for denigrating me and I’ll return the favour.

Your post shows you are s Sargent Schultz, “I know nothing” about the Australian market.

First of all, try renting a “A$1.5 million dollar house” for A$1200 a month. Good luck you doofus.

Second, you don’t know anything about negative gearing which changes the returns one can make on the house.

Third, there are things called capital gains which have eclipsed the returns from any rent.

Educate yourself and then try and put up a post with some facts in it.

Don’t worry MIAMI the Russians are coming. They will save the condo deflation scenario. NYet ! Hold onto your assets .

http://www.cnbc.com/2017/01/30/russian-buyers-suddenly-warm-to-miami-real-estate-in-a-big-way.html

That’s what people are saying here in Turkey too jb

The Russians are already in south Florida. There are towns and condo buildings full of them.

Take a look at the number of postings on Craigslist for SF Bay area offering “1 Month Free” : http://sfbay.craigslist.org/search/apa?query=%221+month+free%22&availabilityMode=0

Seems as if they are getting desperate :).

One month free? That’s nothing when I see one year free it may mean something Maybe but it could be a trend change

The condo craziness in south Florida has been spreading northward into Ft. Lauderdale and West Palm Beach for the last couple of years. The West Palm Beach push is more recent with the new president being a constant figure in the area. People there knew he would win because the rest of south Florida is considered unattractive due to uncontrolled immigration.

Miami’s problem with demand is mostly that it is no longer considered a cool place. The increased immigration from unfashionable places has dampened the appeal of the place considerably. In the last few years I lived in Florida, we went out of our way to avoid it. Ft. Lauderdale has been attracting the cool people for the last couple of years because it is more affordable and less well known by immigrants.

So the condo craze continues:

http://www.sun-sentinel.com/local/broward/fort-lauderdale/fl-fort-lauderdale-lucky-landowners-selling-high-20170128-story.html

“Miami’s problem with demand is mostly that it is no longer considered a cool place. The increased immigration from unfashionable places has dampened the appeal of the place considerably.”

Is this true? I mean beyond your personal anecdote, nothing I could find really supported this. Wealthy Latin American immigrants (and nonimmigrant investors) have contributed a significant amount to the demand in Miami.

From virtually everything I’ve read on the topic, it’s a supply issue that is collapsing the market… has nothing to do with how ‘cool’ the area is because of immigrants (and I will not accept, based on your posts, that you keep your finger on the pulse of what is ‘cool,’ no offense).

The wealthy are never the cool people, they follow the cool people. Miami is over. You don’t have to trust me on that, you can go there and see for yourself.

To be honest I NEVER liked Miami or Florida in general Too many transplanted NYers and the tropical weather with the bugs and other poisonous critters galore Not my cup o tea

I lived in Florida many years now Im out west in Cali and notice that theirs a ton more bugs out in Florida than west. Mosquitoes everywhere in Florida but their nowhere to be found out west. Also a lot of nyers indeed flock to Florida.

the boom is over. something about momentum, i think.