“If this isn’t the peak, we’re probably close.”

Commercial real estate prices over the past many years have done only two things, in this sequence: boom at a blistering pace to dizzying heights and then crash violently.

The benign description for this elegant and repetitive process: “the end of the credit cycle.” Credit gets just a little tighter and a little more expensive, as investors are once again opening their eyes to risks and want to be compensated for them at least a little bit. Then cap rates can no longer compete with rising corporate bond yields. The lofty lease rates commercial property owners have been charging and that made all this possible smack into ordinary run-of-the-mill economic ills that cause vacancy rates to rise.

This coincides with a construction boom and lots of supply hitting the market for years to come. Suddenly the entire math, dragged out to prove that there is no bubble and that prices are sustainable, collapses. Then these highly leveraged investments crater under their pile of debt and drag down commercial mortgage-backed securities (CMBS) with them.

Been there, done that.

No one knows exactly when commercial real estate turns from blistering boom to bust, but there is no tapering or plateau, nor a period during which prices take a breather, or suffer even “modest declines,” as insiders have recently envisioned. There is only boom or bust. And when the bust comes, it does so suddenly and relentlessly.

But not yet. November was still the boom. And what a party!

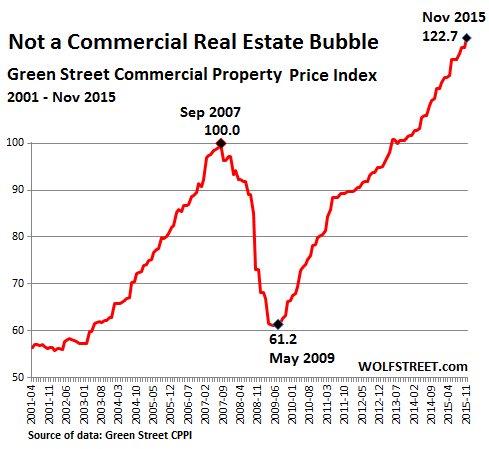

Commercial property prices jumped nearly 2% in November from October, according to the Green Street Commercial Property Price Index (CPPI). Year-to-date, they’re up 10%, after having already jumped 10% in 2014. They’ve more than doubled from their Financial-Crisis low in May 2009 and are now nearly 23% higher than they’d been in September 2007, the peak of the prior totally insane bubble that imploded with stunning financial pyrotechnics:

Even on an inflation-adjusted basis (using average annual CPI), prices now exceed the prior insane bubble peak by 12%.

“Cap rates have been holding firm, and in some instances, even moving lower as investor demand for commercial property remains strong,” the report pointed out. “The question is whether that trend will continue. Cap rates look low when they’re compared to corporate bond yields. Said another way, properties look expensive. If this isn’t the peak, we’re probably close.”

However, peaks are not followed by plateaus, as the chart shows. They’re followed by something entirely different. And Moody’s, which rates the debt and CMBS associated with this boom, is now too getting nervous, after Fitch Ratings had begun fretting in September. Moody’s warned that the leverage in CMBS “as measured by Moody’s loan-to-value (MLTV) ratio already tops pre-crisis peak levels.”

What has been keeping debt-service coverage strong has been the super-low interest rate environment. But the Fed is likely to raise rates this month, and yields of riskier bonds are already rising, with the riskiest end blowing off the top: B rated bonds currently yield over 8%, up from about 5% in mid-2014. And for CCC or below rated bonds, the low end of the junk-bond spectrum, yields have soared to over 16%!

So Moody’s warns that “the expected rise in interest rates in 2016 and beyond will reduce this cushion” of high debt service coverage:

With commercial property prices exceeding pre-crisis peaks on an inflation-adjusted basis and most mortgage debt still sized as a percentage of current market value, we are entering the late stages of the current credit cycle.

When Moody’s says that prices exceed “pre-crisis peaks on an inflation-adjusted basis,” it makes a classic credit ratings agency understatement: as everyone agreed afterwards when the market was crashing in 2008 and 2009, those prices had been truly insane and not sustainable.

And September 2007, too, had been near the end of the credit cycle, and had been the end of the seven-year commercial property cycle, with majestic results.

Rising interest rates and tightening credit – the end of the credit cycle, as Moody’s calls it – will put all kinds of pressures on debt service coverage, on cap rates, mortgages, CMBS, and prices. At the same time, the end of the credit cycle will hit the real economy. And when property prices come down hard, despite all their glorious justifications, the math dissolves into mush, and much of the debt that built the boom loses its foundation.

Investors are already getting bloodied as the Great Credit Bubble implodes viciously at the bottom. Read… “Distress” in US Corporate Debt Spikes to 2009 Level

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Moody’s, now there is someone you should trust…….

Re: collapse of markets. While working for Block Brothers in August 1982, I had my largest sale (list and sell) 200k on land with a 10 % commission.

Next month the market collapsed.

When folks asked me when it collapsed I answer: at 2:23 PM Sept 12

A multi res prop that sold for about 250K in 1982 sold for 75 in 1985.

Location, Nanaimo, BC, Canada

“But the Fed is likely to raise rates this month”.

Every time I read that utterly stupid statement I have to ask myself if the idiots who write it actually even begin to understand what that implies.

Everywhere you look is that ridiculous statement.

Do these people actually understand what it takes to raise rates. Do they think some announcement is made on a megaphone and a button pressed at midday and voila interest rates have miraculously risen 25 bp or whatever.

She might ANNOUNCE a rate rise, but actually accomplishing it is something very very different.

To start with, with the current debt levels and yield curves the amount of liquidity, because the is THE driver of base rate rises will have to be reduced in exactly the same way that liquidity is increased by printing drives rates lower.

Its a difficult calculation to be sure, but it can be done and the current range of the amount of liquidity that would need to be withdrawn from the market is between $350 billion and $800 billion.

And what exactly does anyone think will happen to the economy if the Fed decides to withdraw that amount of liquidity from the market.

Does anyone seriously think that even if the idiots announce a rate rise they will then actually reduce liquidity to that extent.

And what of the last shreds and dregs of credibility of the morons at the Fed, when announcing a rate rise and failing to withdraw liquidity to the extent required then keeps the rate stuck precisely where it is now.

Better watch out for a major false flag event, something really big, before Dec 16 th to enable them to back off and make excuses.

Gil, the current rate environment has CAUSED these problems, and the Fed finally understands that too. That’s why they’re really trying to raise rates. Asset bubbles are a function of low rates, and the Fed knows they have to stop these bubbles from inflating further, or they’ll cause even more damage when they blow up.

Don’t you think that with rates going up soon it will become more expensive for government too service debt and pay interest.

We are in “no mans land” and either way we go consequences are to be paid.

True, that would be an issue if rates went up a lot, for example, with the 1-year yield at 4%. But I don’t see that at the moment. I think they’re trying to nudge them up a little, just enough to let out some of the hot air, but not enough to cause financial tumult. That’s their plan. Reality may differ.

I think you’re right in saying that “we are in ‘no man’s land.”

I can’t predict the future, but I can report that on 2 January 2007, the 1-year yield was 5%.

Gil,

I appreciate your comments and insights. I was not aware myself but it makes intuitive sense.

It also explains why the FED has been dragging their feet to date.

There are empty stores, empty office suites, empty commercial and industrial sites, everywhere. Who in their right mind would invest in this sector? Is it simply a result of cheap financing? Surely, it is not based on future demand?

You make a very valid point.

Recently I started seeing a number of empty stores even in some of the most fashionable Swiss streets. By speaking with locals it appears the dual pincer of high prices being their own cure and declining business (despite the BNS “heroic” efforts the franc has gained a lot on the euro and even on the almighty US dollar) is making itself felt.

This is among the most valuable commercial property in the world, not small stores in a remote backwater. Prices are still insanely high but are bound to come down: the number of Asian customers swarming on the Bahnhoffstrasse in Zurich to buy Swiss watches has dwindled to almost nothing. The change in just two years has been nigh on unbelievable.

But elsewhere things are even worse. In my backwater area commercial property is going through a glut of epic proportions, and it’s about to get a whole lot worse. From my mountainside I can see the new gigantic mall being built by Ikea of Sweden taking shape.

Note this isn’t a new Ikea store: that is staying where it is. This is a mall built by the Swedish giant which will house other shops.

How well things are going can be gauged by the fact they are offering one year of free rent and subsidized utilities for five.

It’s a “war between poors”, as we say around here, with Ikea attempting wooing shops away from the insane numbers of malls that sprouted between 2002 and 2010 down in the plain, most of which have a lot of empty floorspace.

Now. even if there’s an economic upturn those malls won’t fill up, ever.

Take away immigration and population growth is a thing of the past. Wages will remain depressed and debt burdens high.

Worst of all, eBay and Amazon are literally murdering the average mall shop. If things start to look up again, people will buy online, not at the mall: the longest depression in recent memory was a boon for Amazon & co as it taught people the same can be had for less… and with next day delivery!

In the city I’m in (Perth, Oz) a squirrel could get from one end of the business district to the other without touching the ground just by hopping across the “For Lease” signs. It peaked here a bit earlier due to the commodities crump but it’s something everybody will witness all too soon.

hidflect, are prices in Perth coming down from their commodity bubble levels, or have transactions just stopped?

hidflect,

You should tell your non-Oz readers that there is only one problem with your example – we have no squirrels in Oz. Plenty of foxes and millions of feral cats though.

After a check, I found out that some Indian squirrels have escaped from Perth’s zoo. If you see any, you should give a call to 9366 2300

You have to remember that commercial vacancy is all about location and land use. In Los Angeles there shopping malls that are packed to the brim and expanding. Meanwhile other malls just a few miles away are ghost towns, this is based on sustainable user preference just like the pretty girl getting all the attention. Same thing on a larger geography as some cities like Arcadia are booming with Chinese money and this is unsustainable. So aggregated charts like these only tell part of the story.

In my area warehouse space is $150 sf and residential is $300. I think that now or in the future commercial property will be the better investment as those number will begin to meet.

Here in UK the prices of commercial property investments have disconnected from the rental values that the investment is supposed to be buying. Rents are not growing (outside hot spots) yet investors are competing with one another to pay higher and higher prices, which means lower yields. Something’s got to give and it won’t be rents.

Wolf I do not see how assets are any more inflated today than when they were in Setember. That is why it is hard to believe the narative that the FED see’s the bubble and wants to raise rates. Its like one day waking up to the revelation you are an alcoholic.

We made an offer on a house in the last week in San Francisco. We were up against 3 or 4 cash buyers and were the only non-cash buyer and with fairly traditional terms (20% down and 30-year mortgage pre-approved).

While the owner liked our offer and expressed an interest in giving it to us, there was only so far we could go in price and honestly the home was not really worth even what we offered. We were asked to be the backup if the main cash offer fell through. Doing our diligence, it was obvious it needed at least 50 to 100 thousand dollars in basic repairs over the next 0 to 5 years (not remodeling/vanity repairs). It was a relatively small home with a huge amount of deferred maintenance but in a good neighborhood that we very much liked.

Aside from the cash offers (Chinese nationals we believed based on what we saw at multiple viewings), there were a number of contractors who looked at it. The listing agent gave us some future remodeling advice she had gleaned from contractors that she said had passed on the home (our read was that it was too much work for most people and no real guaranteed profit on a flip either). I’m a little relieved we didn’t get it.

Something seems wrong when citizens cannot afford housing at home and the IRS scrutinizes their finances at tax time. Meanwhile they ignore sources of foreign money. Meanwhile foreign nationals dump huge sums of money on vital resources like housing they might not even live in (sometimes without even seeing the house first) and they don’t have to account for a thing.

It’s time for this to change.

Yes. It’s also worth noting that most of this money is taken out of China illegally (there is a limit of $50,000) so by allowing this to go on, we are being complicit in illegal activity. There needs to be a hefty transfer tax on US real estate purchases by non US citizens. I don’t think this would ever happen, because TPTB want to prop up housing prices by any means necessary.

The one thing I really know a lot about is retail shopping. The upscale independent yuppie boutiques are closing even in yuppie neighborhoods in NYC and Philadelphia. When upper middle class women don’t shop it is because they can’t. Not a good sign.

For those of you that are fashion challenged, it was reported in a NY paper, that Patricia Fields, the “Sex in the City” fashion stylist and boutique owner was closing her store after many decades in business. When a business like hers, with a long successful history and upscale brand, has to close and was not purchased by anyone, things are really bad.

I think that all the real estate ghost investing in luxury residential is luring investors into commercial investing. But the customers are not there.

As a commercial real estate broker in the last collapse in CRE. I completely agree with the writer, that commercial real estate crashes are straight down. I sold over $300,000,000 in the two years prior to the collapse in Florida. In late 2007 I had 14 deals under contract (multi-family, retail , and office). 100% of these deals had financing. By the end of January, 2008 ALL my deals fell through, and Commercial lending had ceased completely. The indicators now are actually worse than back then. I am seeing CAP rates of less than 2% now. Their is a lot of “stupid money” out there now as people are just trying to find somewhere to put their cash. I fell this time the crash will be epic in real estate (commercial and residential), Bonds, securities, treasuries, and stocks. I know this time I will not get crushed as I learned my lesson the last time I lost everything. Thank you for making others aware of this.

I don’t think majority of people is aware of this monumental tsunami wave approaching shores . History is always repeating itself.

Last time you got crushed and learned mistake, but millions more are lined up to learn the same lesson in investment over and over again.

Commercial real estate is a tough market. Locations, the economy and trends can fall out of favor faster than their lease runs out. Like borrowing short and lending long, risk runs high.

well, it’s like this: if nobody wants to live or do business there, or wait till someone does, what’s it worth?

owner retiring, liquidation sale, i’m quittin’ the business.

I don’t know whether multifamily is included in the definition of “commercial RE”, but I can remember buying multifamily buildings in downtown Sacramento with cap rates of 11 to 13 in the 1990’s. Now, it seems cap rates are in the 3 to 6 range, and no problem selling. It does make me wonder if a new generation of real estate “investors” have totally ignored the past fluctuations in value. When cap rates are this low, there is really no room to maneuver, and no cushion. Betting on continual rent increases might not be the best tactic in this market. Wake me up in 2020 and I’ll look at the RE market again. Until then, maybe US dollars are the best place to invest.