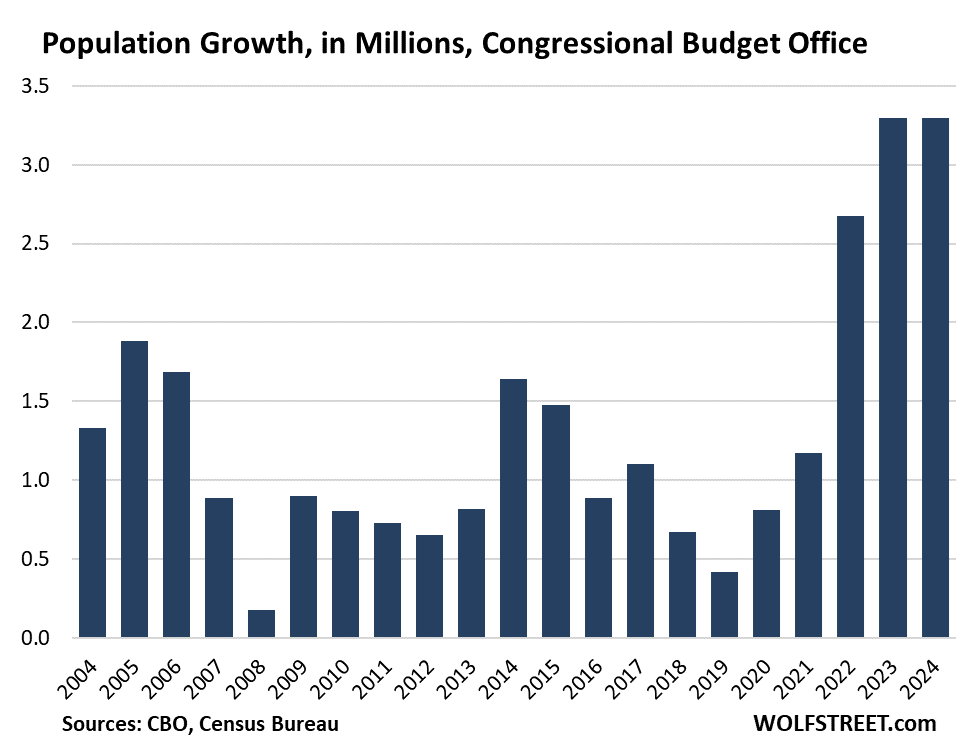

This demand growth is adding to renewed inflation concerns. The huge waves of immigrants in 2022-2024 are part of this demand growth.

By Wolf Richter for WOLF STREET.

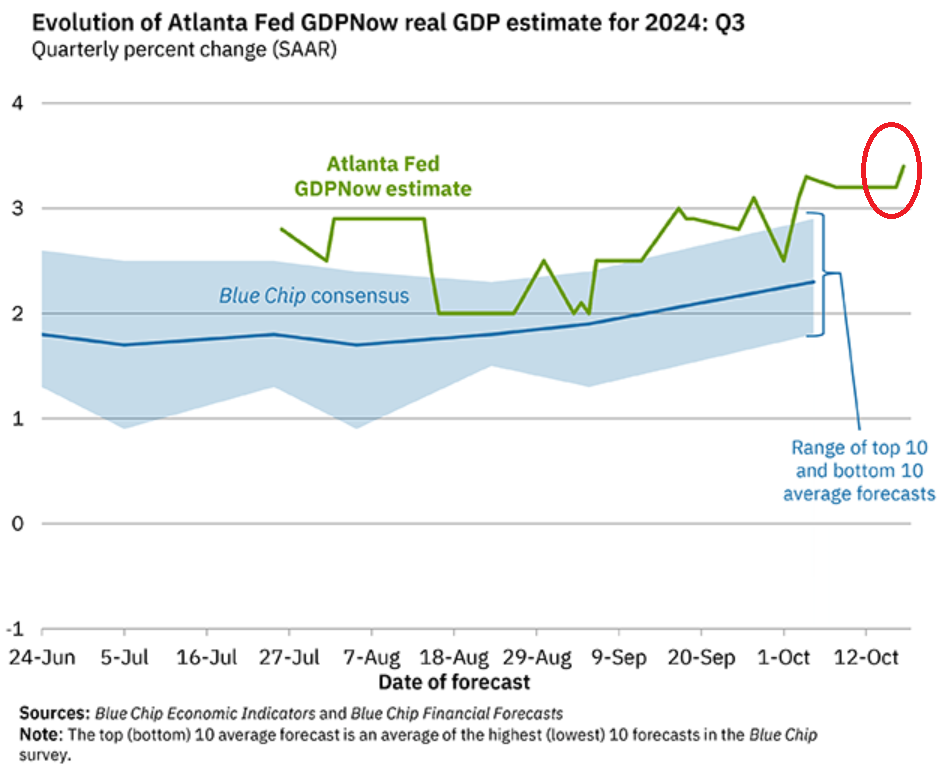

Upon the release of the retail sales data today, the Atlanta Fed’s GDPNow’s estimate for inflation-adjusted GDP growth in Q3 rose to 3.4%, nearly entirely because the inflation-adjusted growth of its consumer spending component got boosted by retail sales today.

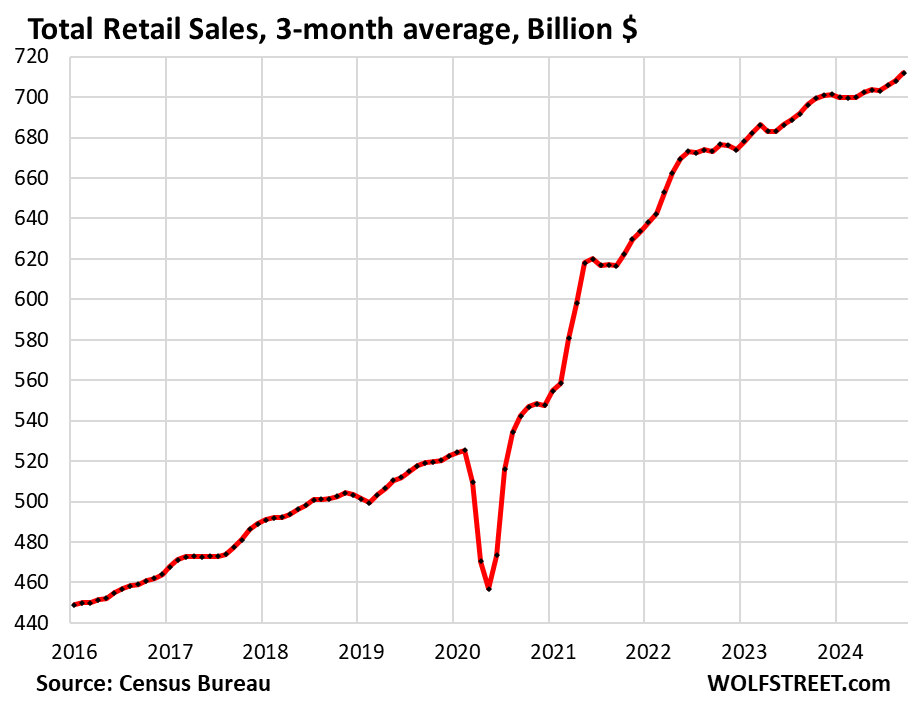

Retail sales jumped by 0.4% in September from August, seasonally adjusted, and August and July retail sales were revised higher.

The three-month average, which includes the revisions and irons out the month-to-month squiggles, jumped by 0.6% — annualized, that’s a growth rate of 7.0%!

Adjusted for inflation, retail sales are even hotter because prices of many goods that retailers sell declined, in particular gasoline and durable goods (motor vehicles, electronics, tools, appliances, furniture, etc.). Food prices are one of the exceptions among goods and have continued to rise.

Consumer spending on goods is adjusted for inflation by the inflation rates of those goods. Since mid-2022, many goods have experienced deflation. We track the CPIs of the big categories of goods here with charts, including the CPIs for used vehicles, new vehicles, food, gasoline, energy, apparel and shoes.

And if adjusted for deflation in those goods, inflation-adjusted spending is even higher, as reflected by today’s rise of the Atlanta Fed’s GDPNow.

The 10-year-average inflation-adjusted annual GDP growth for the US is about 2%. If GDP growth in Q3 comes in anywhere near the Atlanta Fed’s estimate of 3.4%, it would be another quarter of a much higher than normal growth rate.

The past four quarters of real GDP growth were all revised up as consumer income, spending, and the savings rate, were substantially revised up. Three of the four quarters had much higher than normal growth rates:

- Q2 2024: +3.0%

- Q1 2024: +1.6%

- Q4 2023: +3.2%

- Q3 2023: +4.4%

Today’s retail sales data are an additional sign in a trend that led us to muse over the weekend: What If There’s No Landing at all, But Flight at Higher Speed and Altitude than Normal, with Higher and Rising Inflation?

Immigration explains part of it. The US population has surged in 2022 and 2023 by 6 million people due to immigration, and in 2024 has continued to rise, according to the Congressional Budget Office, using ICE and Census data.

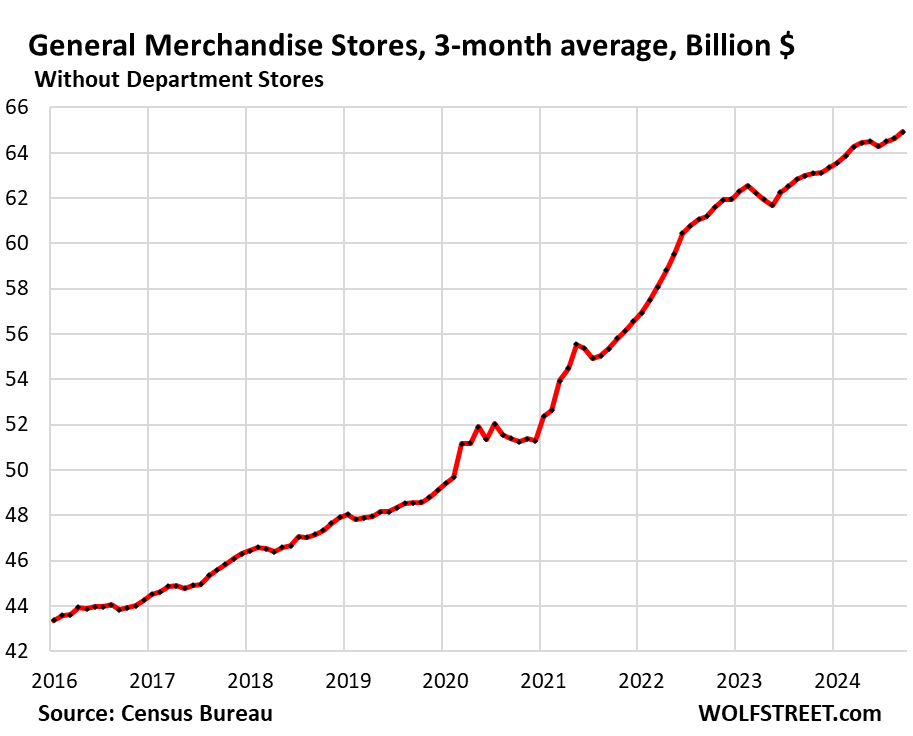

These newly arrived people work, or are looking for work, and they’re buying stuff, though they’re generally not big spenders but rather frugal. But even their frugal spending is pushing up retail sales to some extent, especially in certain categories, such as at food and beverage stores, and at General Merchandise stores, which include Walmart, the largest grocer in the US, which is what we can see here.

Retail sales in total and by category.

To iron out the month-to-month squiggles and revisions, we like to look at the three-month averages, which all charts below show (all seasonally adjusted).

The three-month average of total retail sales rose by 0.6% in September, and by 2.3% year-over-year, despite deflation in many goods that retailers sell.

Note the slowdown in retail sales late last year and early this year. But our Drunken Sailors, as we lovingly and facetiously have been calling them for over a year, are in top form once again, splurging at retailers.

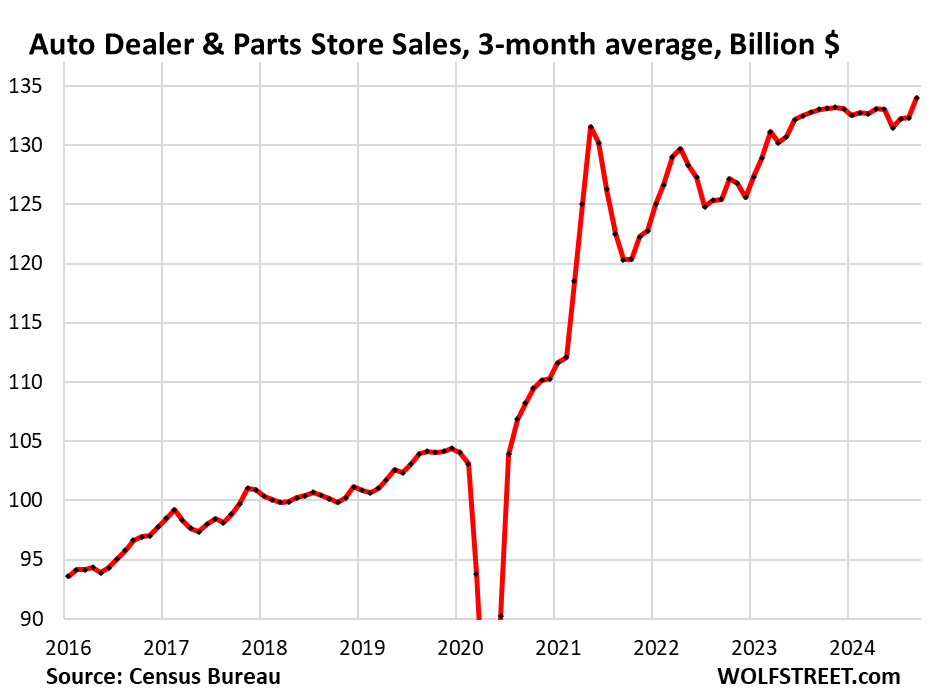

New and used vehicle dealers and parts stores (#1 category, 19% of total retail):

- Sales: $134 billion

- From prior month: +1.3%

- Year-over-year: +0.7%

The spike in dollar-sales in 2021 and 2022 was caused by ridiculous price increases. Starting in mid-2022, prices have dropped, as used vehicles spiraled into a historic plunge. The relatively flat dollar-sales for the past 18 months, despite rising retail unit-sales, are a result of these price drops:

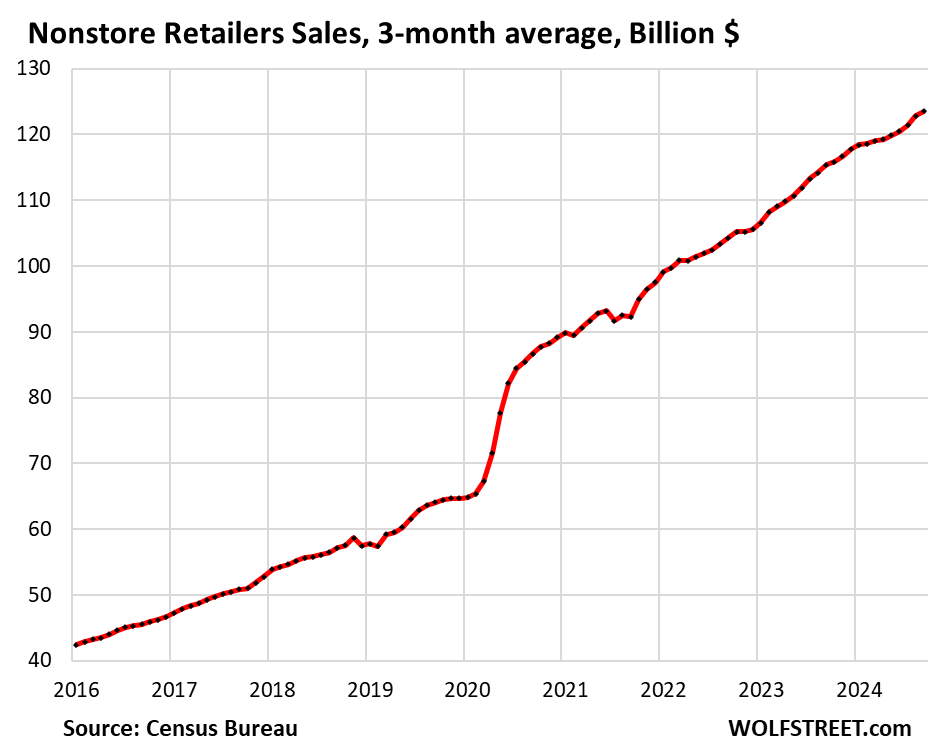

Ecommerce and other “nonstore retailers” (#2 category, 17% of retail), includes ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets:

- Sales: $124 billion

- From prior month: +0.6%

- Year-over-year: +7.0%

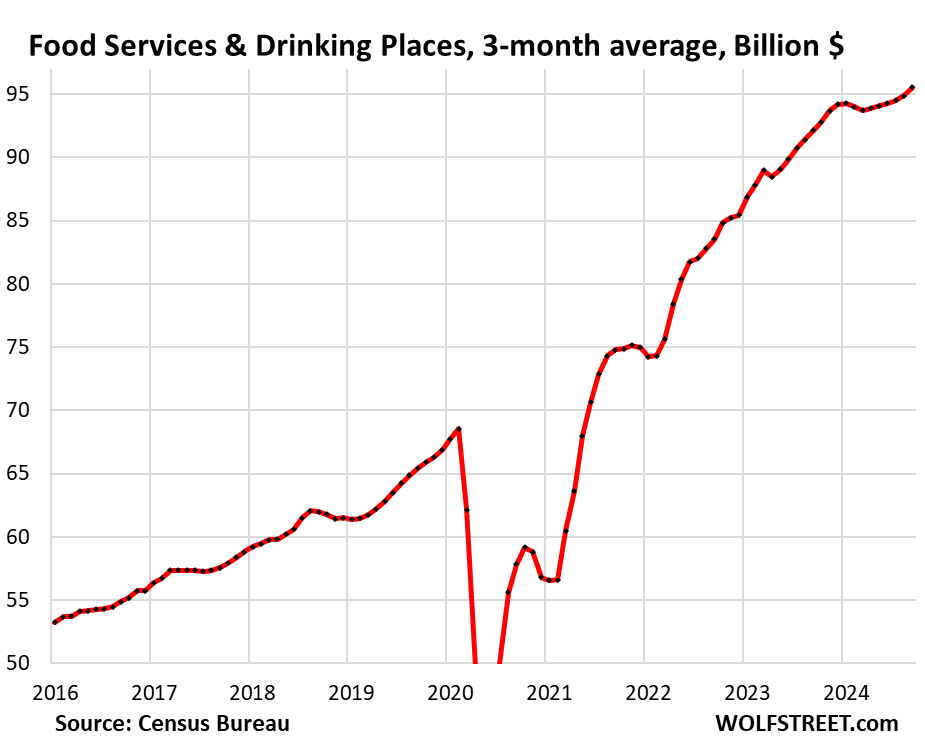

Food services and drinking places (#3 category, 13% of total retail), includes everything from cafeterias to restaurants and bars.

Much of it is very discretionary spending. After a slowdown – an actual decline! – earlier this year, growth resumed over the past five months and has recently picked up momentum:

- Sales: $96 billion

- From prior month: +0.7%

- Year-over-year: +3.7%

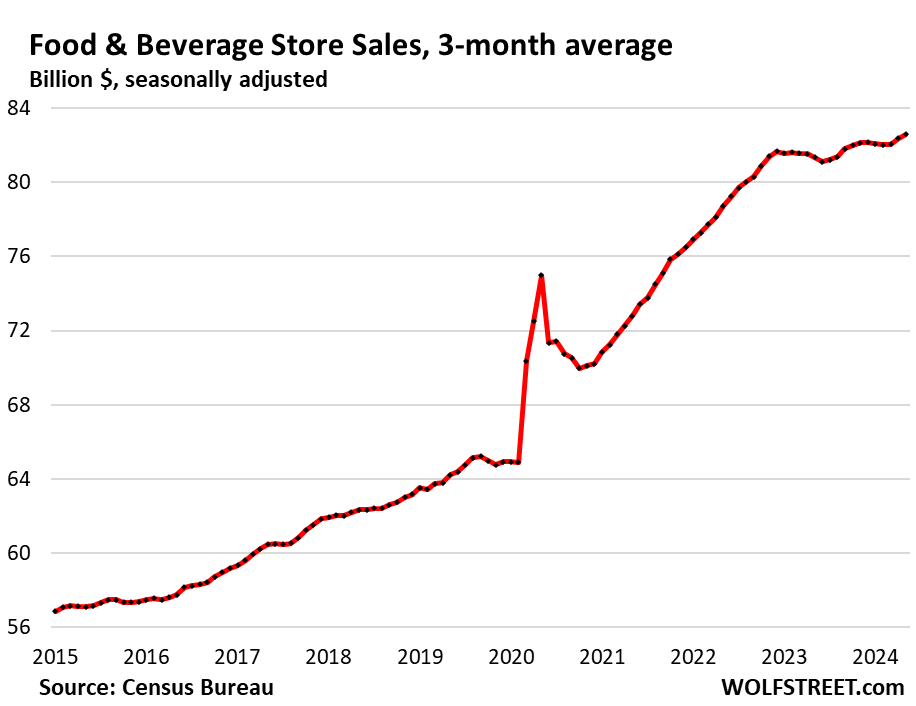

Food and Beverage Stores (12% of total retail). Prices, after exploding from 2020 to early 2023, flattened out at very high levels, and recently have been rising only slowly, according to the CPI for food at home:

- Sales: $84 billion

- From prior month: +0.5%

- Year-over-year: +2.3%

General merchandise stores, without department stores (9% of total retail), including retailers such as Walmart, which is also the largest grocer in the US.

- Sales: $65 billion

- From prior month: +0.4%

- Year-over-year: +3.1%

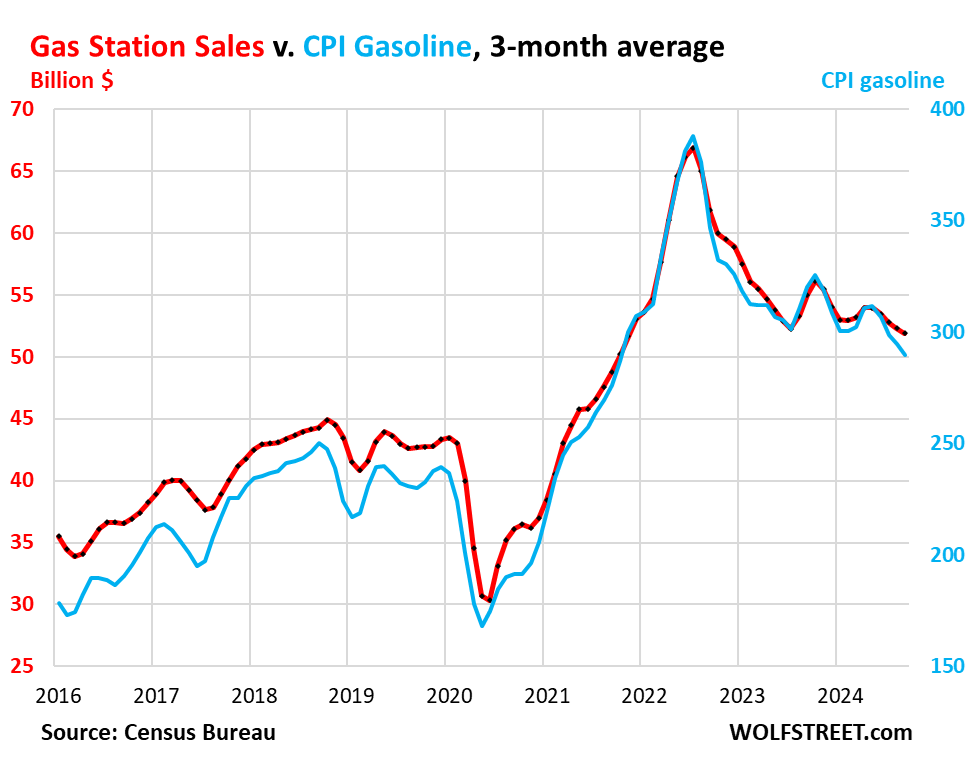

Gas stations (8% of total retail sales). Dollar-sales at gas stations move in near-lockstep with the price of gasoline. The price of gasoline plunged from mid-2022 through mid-2023, and has since then meandered lower, including in September. These price declines push down sales in dollars:

- Sales: $52 billion

- From prior month: -0.8%

- Year-over-year: -5.6%

Sales in billions of dollars at gas stations, including other merchandise that gas stations sell (red, left axis); and the CPI for gasoline (blue, right axis):

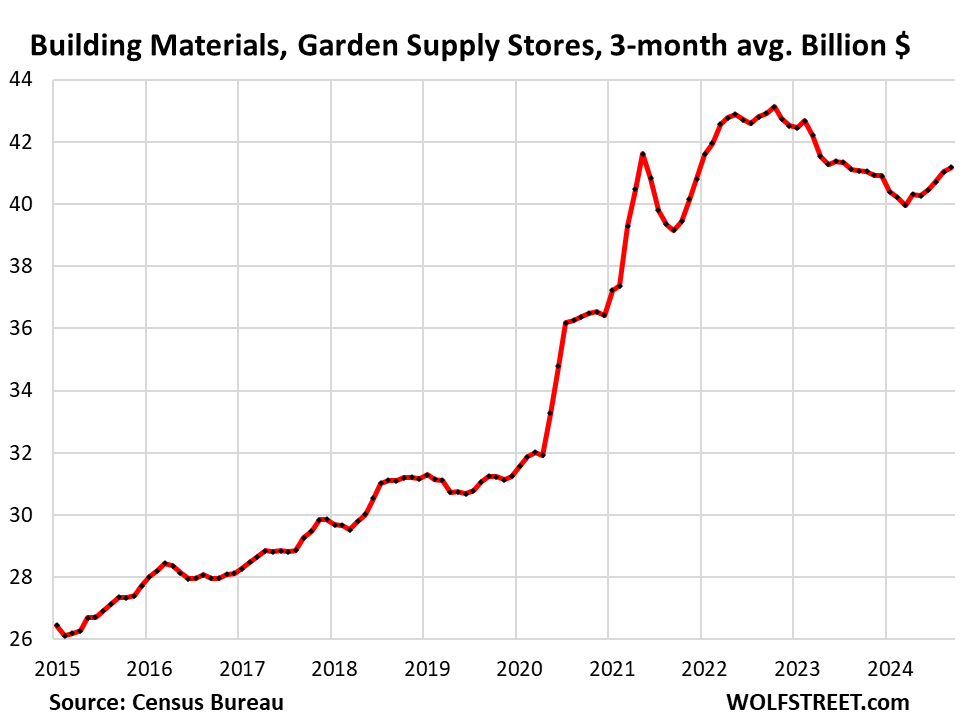

Building materials, garden supply and equipment stores (6% of total retail). The pandemic-era remodeling boom fizzled in late 2022, and expectations were that spending would revert to trend, and that process occurred for a while. But in the spring this year, growth picked up again:

- Sales: $41 billion

- From prior month: +0.4%

- Year-over-year: +0.2%

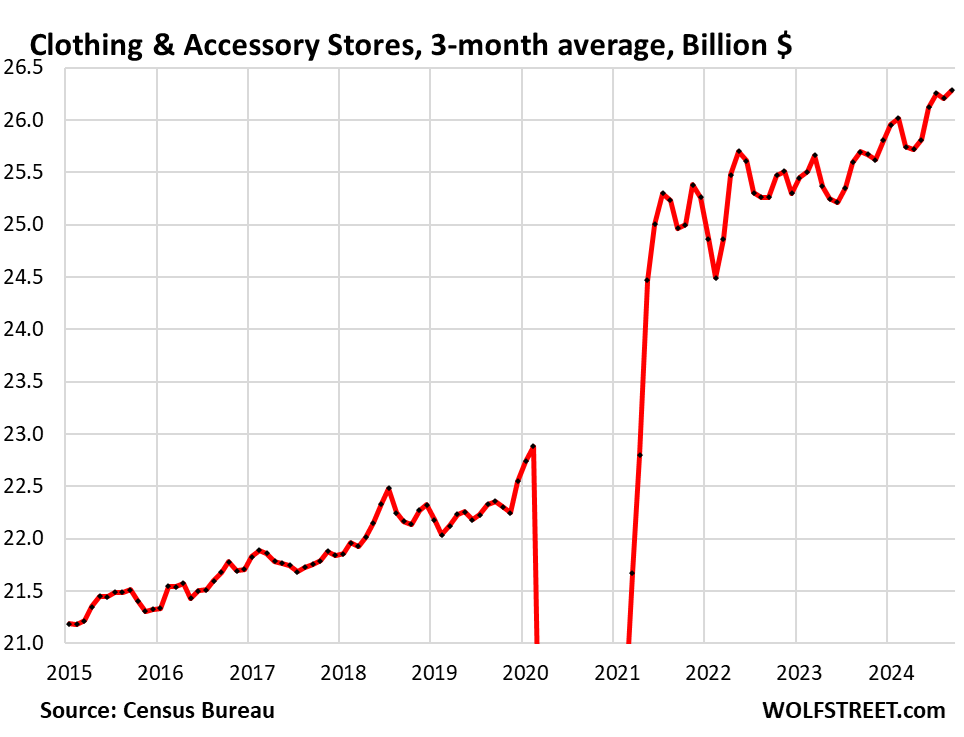

Clothing and accessory stores (3.7% of retail):

- Sales: $26 billion

- From prior month: +0.3%

- Year-over-year: +2.3%

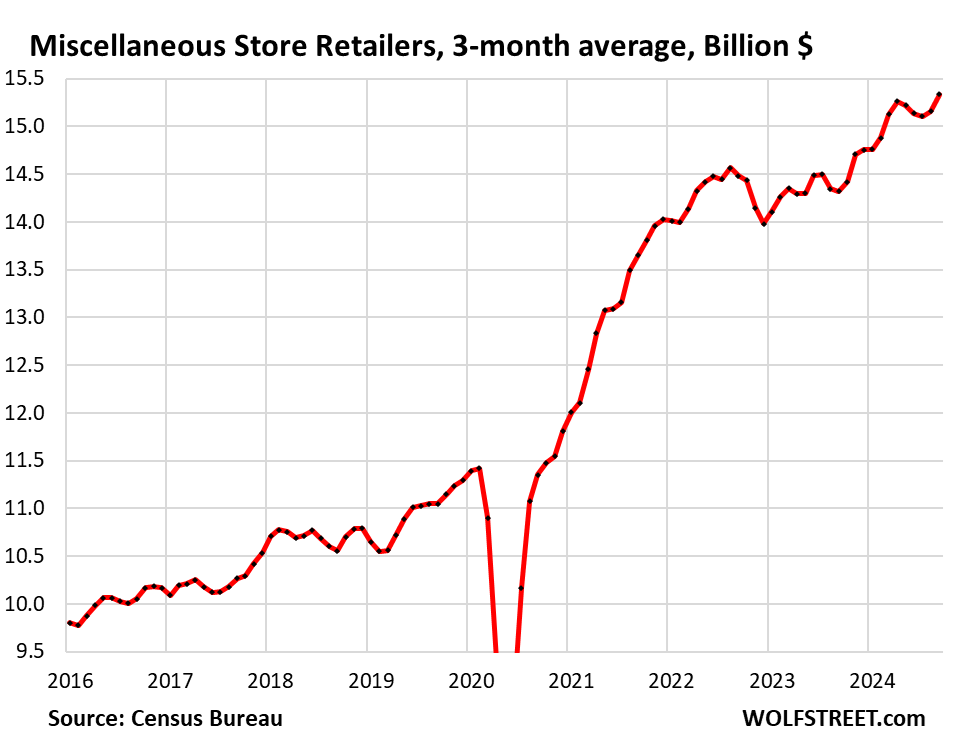

Miscellaneous store retailers (2.2% of total retail): Specialty stores, including cannabis stores. Cannabis had seen large price declines last year and earlier this year. But recently, prices started to rise again, according to the U.S. Cannabis Spot Index (there is no CPI for cannabis yet), and this is likely the reason for the sharp increase in the three-month average:

- Sales: $15 billion

- Month over month: +1.2%

- Year-over-year: +7.1%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good news!

Is the true? While this seems a bit hyperbolic like most Zero Hedge articles which must be taken with a grain of salt (along with all sources including you) but the last year has shown massive adjustment after adjustment of economic data, to the point the US numbers are hardly more believable than China.

—

On an unadjusted basis, Retail sales fell a shocking 7.5% MoM…

Source: Bloomberg

This was the biggest positive September seasonal adjustment in history…

whatever,

you posted ignorant bullshit in bad-faith.

So let me walk you through this.

1. You’re talking about SEASONAL adjustments to retail sales. And they’re always big in September.

2. But this September, seasonal adjustments were bigger because Labor Day for retailers’ reporting fell into AUGUST, DUH. Labor Day weekend is huge for retail. But sales over the Labor Day weekend counted in August. So August was seasonally adjusted DOWN and September was seasonally adjusted up in part to reflect the shift in the holiday. You can see that in the blue line in the chart below.

3. Last year, Labor Day weekend fell into September reporting. So last year September sales were big because they included the Labor Day weekend that this year fell into August.

4. Seasonal adjustments reduce sales on some months and increase sales in others, and the net effect over 12 months = 0.

5. Seasonal adjustments are a percentage of not-seasonally adjusted retail sales.

6. Not seasonally adjusted retail sales this year have been the highest ever, so seasonal adjustments, up and down, have been the highest for every month because they’re a percentage of NSA retail sales, which have been the highest ever. DUH!!!

Why does my site attract ignorant bad-faith bullshit like you just posted? This is exasperating and such a waste of my time.

Love you site Wolf! My second daily read after WSJ.

Don’t waste your valuable time/energy replying to these idiots. Just delete them.

Most of us are quietly and gratefully ready your content 🙌🙏

It wasn’t bad faith at all – I specifically wanted your feedback on the Zero Hedge article (which would have read correctly if I had a full keyboard “Is this true below the dotted line?”). I then *specifically* said it was hyperbolic from Zero Hedge, and put a dashed line referring to the “below”, basically saying “gee Wolf, this is probably BS from ZH, what is your feedback?”

And you confirmed it was BS – providing a counterpoint to The ZH article, which is what I was curious about.

This is bad faith? Or was it that I said I take everyone on the internet including you with a grain of salt?

At any rate lesson learned, I won’t ask you to provide any more counter points from Zero Hedge from a legitimately curious reader since you get nasty about it.

Yes, it is great news to keynesians. Debt out the wazooooo for growth!

[content deleted by Wolf]

I deleted the content because you didn’t read the article and have no idea what is in the article, and so posted dumb questions and BS statements about it that you wouldn’t have posted if you had read the article.

Commenting guideline #1:

https://wolfstreet.com/2022/08/27/updated-guidelines-for-commenting-on-wolf-street/

1. Do not comment on what you imagine the article says based on the headline or the first paragraph. If you haven’t read the entire article, do not comment on the article itself because you don’t know what it says, and your imagination is likely wrong. A comment will either go into the shredder or get slapped with “RTGDFA” if it’s clear to me that a commenter is discussing, or especially arguing with, what they think the article said, when the article didn’t say it.

It’s followed by commenting guideline #2:

2. If you didn’t read the article and want to comment, great, no problem, many commenters do, but make sure it’s not about what you think the article said. Your comment could be an anecdote, experiences, or observations related more or less to the topic, and that’s always welcome.

Trade deficit is a NEGATIVE on GDP. It’s subtracted from GDP. This economy grows DESPITE the trade deficit. If this economy had a balanced trade, growth would be much faster. That’s the tragedy of having offshored production for two decades.

Back in the day when trade was more or less balanced, annual real GDP growth ran between 3% and 6%. With the big trade deficits for the 10 years before covid, annual real GDP ran between 1.5% and 3.0%. That’s what the big trade deficit does. It’s a bad deal except for stocks.

Wolf’s replies to BS are awesome. Thank you Wolf!

Yes, there’s something strangely gratifying when Wolf gets pissed and slams someone. I guess I’m just glad it wasn’t me getting slammed.

How – the power of schadenfreude (…a splendid courtroom soliloquy about the phenomenon by James Spader’s character in the old ‘Boston Legal’ TV series…).

may we all find a better day.

Since the economics world is using an air vehicle analogy: there is a crash, hard/soft landing, and most interesting an uncontrolled “pitch up” (altitude) leading to a stall as vehicle speed kinetic energy is converted to gravitational potential energy with a much greater crash and most likely a “flat spin” all the way down.

Gary-

Might as well go a step further:

In such a “flat spin,” will the Cirrus Airframe Parachute System (CAPS) be deployed once the critical airspeed and altitude parameters are breached and the need for “plunge protection” becomes evident.

Will the CAPS style response (whether monetary, regulatory or fiscal) provide temporary relief, and what will be the fallout of those responses?

Such are (or should be) the questions of managed money. For now, though, the altimeter is un-alarming…

Given upward atmospheric limits to suborbital flight (and the specter of another inflationary burst), I should have said ”the altimeter is relatively un-alarming.”

As expected by most readers of Wolf Street, Powell has egg on his face. He and the rest of the Fed Governors will spin it in multiple ways but the fact remains that the Fed jumped the gun with the 50 basis points cut in September.

These guys should be tarred and feathered due to their bias towards delayed rate hikes and early rate cuts.

May inflation continue to deal them further blows until they come to their senses.

Will this prevent them from cutting in Nov? I have my doubts, time will tell, still almost another month to go. Maybe they will be working OT to spin a narrative to once again cut to pre-emp any down turn coming…

A pause is the right thing to do, since raising is completely out of the question, just do the right thing Pow Pow

If they do a face-saving 25bps cut and then pause for the forseeable future, that wouldn’t be the worst thing in the world imo. Bonds are taking the hint with long yields rising.

If inflation will go up then it would be a bad news. But this is good. 😊

I have a hard time believing anyone at the FED is oblivious to the fact that all this data gets revised giving possibility to inflation and labor metrics reversing course against their decision, yet they went and cut prior to confirmation. I really really REALLY would love to know what they were actually thinking when they took the decision, why did they need to cut first and wait to see. I don’t believe I ever will though, all I got is theories from the social media jungle

Me too.

There’s no egg. They followed the data and made a reasonable decision. It may not have been the _right_ decision in hindsight but they had to make their choice without the benefit of that.

Plus, the cut was a single one, not overly large, and left the current rate still well above the inflation rate.

Remember that an interest rate equal to the inflation rate is considered by many to be “neutral”. Some even advocate tying the two with no slow ramp-up/down.

” They followed the data and made a reasonable decision. It may not have been the _right_ decision in hindsight but they had to make their choice without the benefit of that.”

Or could’ve waited the couple weeks for the revisions? Would the economy disintegrate in 2 weeks without a 50point cut? Don’t get me wrong I believe these are very smart people I just don’t get why they moved early, maybe I’m missing something

Yep. All they had to do was hold off for another meeting, and they would have had a convenient excuse of the election to stay out of politics.

But no, they caved in to the pivot mongers on Wall St. looking to fire up another housing bubble.

I hope they get a double-digit CPI print next year as their reward.

Powell has no egg on his face.

He is not facing any consequences of all thr bad decisions he made in last few years leading to high prices of things and housing .

The egg is on the face of working Joe.

I am lucky I am invested in asset markets but a lot of my friends are not and they are hand to mouth in many ways.

Powell was rich before and richer now along with other Fed members.

Sean, tar-and-feathering is probably a more lenient punishment than being ridden out of town on a rail. In the latter case, you probably end up split in half rather than getting nasty burns and massive humiliation.

You’re a bit off, though, in your sharp criticism. The rate hikes were sudden, consistent and dramatic; this single rate cut was headed for more cuts, and was based on some real employment and inflation information AT THAT TIME.

But, if they cut again, I’d say bring your tar and feathers.

“bias towards .. early rate cuts.”

with the rate, they simply follow the market. EWI likes to write about that.

This fully debunks the claims of “worst” economy ever, in “U.S. history.” lol. Or claims that the economy was so much better under the previous admin. The people spouting this stuff off, and parroting others shouting that b.s., are the same “headline readers” that never look at the data. But it always goes back to “belief” versus “reality” doesn’t it??

I’m not sure how you define “worst” but it’s definitely the most “fucked up” economy that I’ve ever seen.

If there’s a big recession with 10 million people out of a job, some of them for years, and college grads’ careers set back by years, would that be less “fucked up?”

I think I understand what you mean – that there are some “aspects” of this economy that are fucked up, such as the government deficits, the massive liquidity still sloshing through everything, too-high home prices, too much inflation, etc. But overall economic growth has been amazing me for over two years. I expected these much higher interest rates to do some real damage to the economy, jobs, etc. But they didn’t. This is the best economy since the 1990s* (and it had aspects that were fucked up too; I don’t know of a time when the economy didn’t have fucked-up aspects, that’s just what we get).

*not so ironically, we had similar interest rates back then.

I graduated high school in 1979. That was fucked up, but much different. High unemployment. High gas prices. No gas…. The pandemic created opportunities for stimulus or “acts” to be past with enormous amounts of money. Now it seems like everyone is drunk and drinking from a fire hose.

I lived in Brazil and Chile for a while. You have not seen anything yet! We used to spend our paycheck two weeks before we got it, and never saved a dime. Inflation was so bad that the currency devalued by 100 percent in about a year.$100.00 exchanged for Crs. was A foot high stack of 10000 Cr notes! I saved money by buying a car which I sold for twice what I paid for it when I left. You could get twice the bank’s official exchange rate for US dollars anywhere. The military kept order and moved on Favelas , poor city districts, when people were starving and robbing the rich.

The USA needs to straiten-up an fly right before it is to late. Just like a household, you can not borrow money indefinitely to pay household bills you will go broke!

One way this economy is screwed up (PG language) is that there is no safety net for anyone except the absolute poor.

Unlike Europe, where there is more of a support system from the government. In Germany, if you have kids you are legally not supposed to be laid off.

The US is more and more becoming just a brutal rat race, like that Netflix show “3%” where everything is a competition and only a few make it to “O Maralto” (the offshore island paradise.)

IMO it is pointless to participate in a rat race where most of the rats die. That’s what we’re becoming. Gen Z has already figured it out, that’s why you have a generation of men gaming and hanging out in mom and dads basement, rather than climbing the corporate ladder.

Eventually its all going to implode as you cannot beat a dead horse.

” I expected these much higher interest rates to do some real damage to the economy, jobs, etc. But they didn’t.”

Wolf,

Perhaps this is because the “damage” has come in waves instead of all at once?

Trump’s tariffs culled weak companies. Covid culled weak companies. Rising rates culled weak companies. It seems like every year there has been a wave of hard times coming for a very specific industry.

What are we left with, then, if not the strongest, most resilient, and recession-proof private sector in history?

Dan, you’ve got it bass-ackwards. Those tariffs protect weak companies; they do not cull anything that’s wobbling because foreign competition is reduced. How f’in politically naive that one is. But if you’re in a cult, yeah, it’s the worst economy in the history of the country.

Isn’t that a f’in lie?

Yes. It’s a lie.

Just add it to the pile of lies.

“I expected these much higher interest rates to do some real damage to the economy, jobs, etc. But they didn’t.”

I didn’t, and I said so at that time, that the “pause” was premature and a massive mistake, and I also said this rate cut was reckless and stupid. These people clearly know what they’re doing is wrong, but they do it anyway because it massively benefits their personal net worths.

Another way of skinning the economy status would be to compare with what else is out there. Europe: Germany, France not go good. China not good, Japan not good. Where is a good normal economy?

Luxembourg.

Whether people think its good or bad now, the US could get our economy in a lot better shape with just a little self discipline and austerity for a while. Stop deficit spending, pay down debt, keep the mbs draining all the way to zero, campaign finance reform, reinstate Glass Steagall, let the free market determine interest rates. And for the upcoming election, the party most aligned with that is Libertarian.

Nothing will fully debunk. I just saw article titled “Elon Musk believes Warren Buffett is ‘preparing’ for a Kamala Harris presidency, as Buffett sells off stocks and grows his cash pile to $277 billion“. This is just unreal. BS in so many ways.

Poor, kindly ol’ Warren doesn’t have enough lucre, needs MOAR. All of these billionaire pigmen need to be humbled.

It’s one of the worst economies ever for lower wage earners. Massive deficit spending during good economic times resulting in massive inflation. Which is then exacerbated by massive illegal immigration.

Wages have been outpacing inflation…until the full effect of wage suppression by immigrants entering the workforce sets in. The end result will be continued inflation while higher wage earners continue to spend and do well…while lower wage earners fall farther behind.

Well done! Mission accomplished?

As Reagan would say, “Let them eat trickle down.”

Current administration is apparently saying “let them eat inflation”.

The immigrants are why the economy is so good. They are doing all the jobs non-immigrants refuse to do. I’m in a construction related field in Florida, they are making a lot of business owners wealthy and it’s sloshing over to the rest of us. Keep em coming.

Those goings on in construction have been happening since 1985 at least!

Our good buddy Drunkenmiller said yesterday that he thinks the 10 yr rate should be tracking nominal GDP.

From BEA: “Current‑dollar GDP increased 5.6 percent at an annual rate, or $392.6 billion, in the second quarter to a level of $29.02 trillion, a $9.5 billion larger increase than the previous estimate”

From our friends at Bankrate: “Typically, the gap between the 10-year Treasury yield and the 30-year fixed mortgage rate spans 1.5 to 2 percentage points. For much of 2023 and 2024, that margin grew to 3 percentage points, making mortgages more expensive”

This nice, hot retail spending is awkward for the Fed and even adds pressure to equity valuations, especially if the 10 year starts to accelerate to 5%+ — a few analysts are suggesting 6% range.

If we get rate cuts, a whole bunch of stuff is gonna seem really crazier than things are now.

Sadly, I don’t know why there’s a difference between Drucks nominal BEA GDP and GDPNow:

“the Atlanta Fed’s GDPNow’s estimate for inflation-adjusted GDP growth in Q3 rose to 3.4%”

Seems to be the annual rate? Seems like the drunken sailors have done well plundering!

1. Drunkenmiller’s suggestion of the 10-year yield running near nominal GDP growth is a twist of the more common version that the 10-year yield expresses expectations of future inflation rates (but that’s hard to measure). So if today, market participants expect inflation to average 4% over those 10 years, they would price the 10-year yield at 6% today. It might come out to be about similar.

2. the spread . “Bankrate…For much of 2023 and 2024, that margin grew to 3 percentage points, making mortgages more expensive””

That’s BS. The last time it was at 3 percentage points was on November 2, 2023. Then the spread narrowed sharply. All year long, it has been between 2.25 and 2.6 percentage points, except for three days in March when it went as wide as 2.75 percentage points.

In addition, the Fed’s QT of MBS will keep the spread wider than it was during QE — reducing the spread was part of the reason for the Fed’s QE at the time. But those times are gone. The Fed has said many times that it will continue to shed MBS even after QT ends, at which point it will replace them with Treasuries. So the times of the narrow spread during QE are gone:

3. Nominal GDP “Sadly, I don’t know why there’s a difference between Drucks nominal BEA GDP and GDPNow:”

Nominal GDP is NOT, repeat NOT, adjusted for inflation. GDPNow is an estimate of inflation-adjusted, repeat inflation adjusted, GDP.

The BEA produces:

— nominal GDP (“current-dollar” GDP) = not inflation adjusted

— “real GDP” = inflation adjusted.

The Atlanta Fed produces:

— an estimate of the BEA’s “real GDP” ahead of the release.

Damn. You’re good!

Thank you for the expansive clarity I appreciate the insights you have.

As you know, I like to bounce around to look at additional perspectives — which usually end up adding distorted noise.

I like the stars to align, and WolfStreet really has the world’s finest planetarium and telescopes!

Ps: I saw a comment you made in a prior comment: “ This is the best economy since the 1990s*”

What amazes me, is the almost universal rejection of this best economy ever — I detest politics, but it’s baffling as to why so many people are in denial — and are so willing to believe that the country will accelerate into some magically improved status, because of a tax cut that will supercharge the deficit. Baffled doesn’t come close to being the right word!

If a tax cut supercharges growth more than the deficit, the debt to GDP ratio could decrease.

Redundant,

I can’t understand it either. People seem to view the economy through a political lens. Most have no actual grasp on GDP growth, inflation, or unemployment relative to historic norms.

Maybe it helps that I put faith in no politicians?

According to CBO and The Joint Committee on Taxation, tax cuts expand the deficit — imaginary GDP growth will not make the deficit disappear, especially with decreased tax revenue.

The absurdity of that argument relies on magic pixie dust and a strong ingrained sense of denial — and a ridiculous belief that GDP is going to explode like an ai stonk.

I have absolute total faith in stupidity winning this argument.

Redundant,

on this: “… it’s baffling as to why so many people are in denial ….”

I believe there is a vulnerability in humans, a hackable trait: cognition and factual evidence can be over-ridden by a sort of card trick of introducing a catchy, ultra-simple, stimulating narrative. A big part of leadership is explaining/reducing reality to a popular narrative, for the “benefit” of those lazy or deficient in forming their own. Unscrupulous sales types live off this, and sometimes exercise a toxic “leadership.” Capturing attention and being entertaining are the killer app. Just reach a critical mass of the lazy or gullible or otherwise susceptible, and bingo.

We didn’t experience 30% inflation over 3 years in the 90s, that’s the obvious difference.

As usual, you are the clever one.

But I believe you know the answer to your own questions.

Our country is restless, their is no order.

Doesn’t take much for the cattle to stampede under these conditions.

Doesn’t matter if they are fat and watered…I just watched Rawhide, with Rowdy, Gill Favor and Wishbone.

Home Toad, I enjoy your imagery and use of metaphor. The choice of sheep rather than cattle, I think, would be more accurate. Or honey bees. They’d sacrifice themselves to protect the queen. And the queen, being the head of the hive which every underling would give up their lives for, is a supreme example of fascism in its finest form.

Love your analysis. Very thorough and in depth. Shows someone spending some time, brain cells and questions and doubts what Feds, M(W)all Street are trying to sell us. Keep up with the good work. Regretfully only able to read 1 report a day to usual inbox flooding. But keep up with the work !! Thanks JM

Yes, I haven’t found fault with Wolf yet, either. Mind you, I’m not nearly the expert that he is. I would be curious to know where Wolf got his knowledge of finance and the markets from. Is he an autodidact or did he get training?

Of course your “reality” is based on your superstitious belief that GDP actually measures the value of goods and services produced, which is conceptually absurd. GDP measures GDP and a higher number is generally (but not strictly) associated with good things. It is those other good things that matter.

“…that GDP actually measures the value of goods and services produced,”

No no no no. GDP doesn’t measure production. It measures SPENDING and INVESTMENT by the economic players (consumers, businesses, governments).

GDI measures the economy from the other side: it measures Gross Domestic INCOME.

The natural instinct is to find comfort at a big GDP number. IMHO this should not always be the case as government spending forms a large part of the calculation, which to my mind is out of control and is only increasing the debt the interest upon which costs the country as much as the defence budget annually

“as government spending forms a large part of the calculation…”

I hate to disappoint you: Federal government “consumption and investment,” as it’s called for GDP calculations, was $1.49 trillion in Q2, or only 6.4% of total GDP of $23.22 trillion. It contributed only 27 basis points to 3.0% GDP growth. So if federal government consumption and investment had been flat, GDP growth would have been 2.73%, still far above the 10-year average.

You can look all this stuff up if you wish, instead of spreading nonsense.

https://www.bea.gov/sites/default/files/2024-09/gdp2q24-3rd.pdf

Wolf,

“Federal government “consumption and investment,” as it’s called was $1.49 trillion in Q2, or only 6.4% of total GDP of $23.22 trillion.”

Why are you comparing a *quarterly* expenditure number with an *annual* GDP number?

Shouldn’t that expenditure number by roughly *4 times* as high in *annual* percentage terms?

These are all ANNUAL RATES. Everything concerning GDP and its components is expressed in annual rates. That 3.0% GDP growth was an annual rate also. That $23.2 trillion GDP was an annual rate. The $1.49 trillion in federal government consumption and investment was an annual rate. So they can be compared.

Instead of posting ignorant BS here, click on the link I gave you to the BEA’s website. It all came straight from the BEA’s GDP table. Your stuff is so exasperating!

Andre and CAS127 especially, consistently blame the gummint for all things evil.

The late Chas. Munger recommended that investors should “invert, always invert”. If you invert government functions, what are you left with? MadMax libertarianism.

Are these guys on Putin’s payroll? /s

Maybe GDP should really be GDI instead then?

GDI and GDP look at the same economy from two different sides: income vs. consumption and investment of that income. So they should be about the same over the long run, and they are close, but they differ quarter to quarter.

Real GDI v real GDP growth:

Q2 2024: GDI growth = 3.4%, GDP growth = 3.0%

Q1 2024: GDI growth = 3.0%, GDP growth = 1.6%

Q4 2023: GDI growth = 5.1%, GDP growth = 3.2%

Q3 2023: GDI growth = 2.7%, GDP growth = 4.4%

Oops. That was supposed to be a reply to 1stTDinvestor…

If immigration is pushing up the number then would not GDP per capita be a better measure? And trade deficits subtract from GDP but not govt fiscal deficits?

For the overall economy, it doesn’t matter who does the spending. It’s the overall economic growth and job growth that matters.

For social studies or social-justice studies or whatever, per capita GDP might be better. Per capita GDP is not a measure of the economy but a measure of the average individual’s GDP. Per capita GDP grew by 2.5% in Q2.

Taylor Swift is still touring in the U.S., so of course our GDP is growing rapidly. :)

The EU economy is kind of sluggish right now, they need to get Taytay to do a big tour of Europe to get their economy growing.

Chinese is also having economic troubles, but the CCP would rather mass produce copies of Taylor Swift and flood the world market.

Don’t forget all the tech billionaires decided they must have a nuclear plant to go along with the yacht & jet. Sun, wind, & burning barrels for the peasants.

Taylor Swift toured Europe this summer, with many dates across the UK including five concerts at London’s Wembley Stadium.

For these events, the Guardian reports, she was given police protection by the capital’s Special Escort Group, a unit normally reserved for the Royal family and senior politicians.

When challenged, both Prime Minister Starmer and Home Secretary Cooper denied that the free tickets and hospitality which they and their families enjoyed had ANY connection with the policing arrangements..

Swift is the whipping post now. How about the guy who denied losing the election that he lost and, instead, cost the lives of police, destruction in the Capitol, scads of money prosecuting the insurrection, etc., etc.?

Sobering charts which illustrate perfectly why the recent 50 bps rate cut was not only unnecessary, but recklessly stupid, if not criminal.

Otherwise known as business as usual now, sadly.

Could you tell me what you mean by drunken sailors?

I believe he’s referring to us, the American people, because we keep spending money as if we were drunken sailors.

Because sailors aren’t known for making sound financial decisions when imbibed.

“Facetiously” calls them that, due to all the claims they are broke.

I just read that another half a trillion has been added to the deficit in the last few weeks. It will reach $36 trillion soon. How long can this continue? The shocking part is that it’s an election year and neither candidate bothers to discuss this. If inflation picks up again with the significant economic growth we are witnessing, could that cause a mini market crash?

Just wait for the refinancing wall in 2026, 2027 and beyond when trillions must be sucked out of the financial system to accommodate this new debt at higher rates. Late 2025 the market will pay attention to it, if not sooner. We will see about it then which consumers swim naked. All the data on this site is backwards looking, and even if it looks the consumer is better than anytime in the last decade, I doubt it that the FED and the Treasury dept can stop this problem. Their goal was always to suppress long term yields, but let’s see what happens.

“…refinancing wall in 2026, 2027 and beyond when trillions must be sucked out of the financial system to accommodate this new debt at higher rates.”

“must be sucked out” is not how refinancing works. Refinancing means old debt gets paid off at face value, so the borrower has to pay out the cash to lenders, and then lenders reinvest that cash in new debt that the borrower issues. There is no money “sucked out” of anything. Another expression for refinancing is “rolling over debt.” I have T-bills that “roll over” — get refinanced — every few months. It’s really smooth. Debt gets rolled over ALL THE TIME every week, including notes and bonds, no problem.

The problem is NEW issuance, NEW debt that’s in addition to the existing debt. It’s not a problem at the moment either, but some day it might. And this new issuance that adds additional debt will likely keep longer-term interest rates higher.

Lenders aren’t going to be reinvesting that repaid principal, they’re going to be using it to lick the wounds on portfolios corrected by 30 or more % in real estate, and rebalancing their liquidity ratios.

The Fed’s removal of vlaue from the market, however too slowly, has to come from somewhere. Higher treasuries and rates means fewer projects (target investment yields require a risk premium over the 10yr, now. Much harder to hit) and more expensive debt. Multifamily alone has been reset 30% or more, depending on the market, and office and other commercial are even worse.

Too many maturities are going to leave equity wiped, and at least some principal wiped. So there won’t be a dollar for dollar reinvestment into our economy. Not without help, like from TARP or RTC.

The debt wall is certainly going to cause problems. The reversion from the free money/ZIRP era must have consequences.

Many corporate loans are also floating rate, i.e. SOFR+400bps. These rates go up right away rather than when the debt rolls over.

Who knows how much longer. Japan debt to GDP is over 200% so we are probably okay to at least to 200%. Based on charts, it probably will take at least another 20 years before we hit 200% GDP.

But Japan has a declining population so maybe not a good comparison.

All recent data and last 2 months revisions have shown Economy is doing good, Labor Market is good and there are more risks to inflation.

It is very clear FED made a mistake of cutting 50 BP instead of 25BP. Had they done 25BP, they would have option of another 25 BP and pause. Now Pause is going to be difficult to communicate. That too when Powell told about possibility of another two 25BP by Year end.

Fed’s Waller calls for ‘more caution’ on rate cuts and Boastic is open for Pause. But I don’t think there will be Pause in Nov meeting. It is like accepting they made mistake of going 50BP.

Under the influence of Keynesian dogma, academicians have been trying for too long to analyze interest rates in terms of the supply of and demand for money. A “liquidity preference” curve is presumed to exist which represents the supply of money. In this system interest is the cost which must be paid, if lenders are to forgo the advantages of liquidity. All of this has little or nothing to do with the real world, a world in which interest is paid on transaction accounts.

“Had they done 25BP, they would have option of another 25 BP and pause. Now Pause is going to be difficult to communicate. ”

Nah.

Several of the Fed governors, including Bostic and Daly, have come out in recent days and said they’re open to a pause at one of the two meetings this year.

Ooooooohhhhh, how edgy of them…….

Because many commenters are talking about Powell, my two cents is that Powell lost all credibility with the 50 basis point slash, which had nothing to do with his much-touted data dependence and all to do with the election (he wants to keep his job, and Trump has pretty much said he is gone). Senator Warren gave him the ultimatum in a much publicized letter demanding a 75 basis point cut. Powell will go down in history as one of the all-time worst Fed chairman, pretty much in a dead heat with Bernanke. Appropriate for a deadhead.

As for retail being strong, the return to normal interest rates (around 5%) netted me $50,000 extra over the last year, risk-free. I didn’t go out and spend it all, but I spent more than I used to, and continue to do so. I am sure I am not the only person who has experienced this. If there is a sizable chunk of modestly affluent consumers experiencing this, there should be no surprise that the CPI is no longer going down, and in fact is starting to turn up again, and the economy will keep chugging along. The record paper profits made on Wall Street and in housing probably have a similar impact.

We do not see the data the FED has access too. Sometimes perception and future sentiment outlook can drive markets.

Maybe they saw sentiment declining and the 50 bps was what the market needed to feel good about the future. I read a lot of corporations were hesitant on spending capital with the previous high interest rates. Now they may feel more confident.

We will never know if they did not cut rates that the economy could have crashed. What we do know is we now have a no landing.

The Fed saw the spooky labor market data in August that we saw too, and it was spooky, and this is what I said about it then:

https://wolfstreet.com/2024/09/06/the-fed-has-room-to-cut-rates-are-high-relative-to-inflation-and-job-growth-could-use-some-juicing-up-to-maintain-momentum/

But two weeks after the Fed meeting, the spooky data was all revised away. The Fed didn’t have that data at the time of the meeting because that data hadn’t even been collected yet:

https://wolfstreet.com/2024/10/04/ok-forget-it-false-alarm-labor-market-is-fine-bad-stuff-last-month-was-revised-away-wages-jumped-no-more-rate-cuts-needed/

The BS conspiracy theories about the Fed are really getting old. Don’t spread them here.

We all saw the “spooky” data point. But that is just one incident. Only an imbecile would make an important decision based on one data point. Dropping 50 basis points on one piece of data is not “data dependence”, it is data stupidity. If you think Powell is not a jackass, then something else was going on, and my view is he was under a lot of pressure from Democrats. We will never know for sure, of course.

In a so-called free market economy, it is idiotic to have a group of 12 people determine short term interest rates, but that is another topic. It does smack of a centrally planned economy, like the USSR. We all saw what happened to it.

Sorry Wolf. I did not think business and consumer sentiment was BS. I thought the FED may look at those too but maybe not. Anyway….they were not looking good.

CEO Sentiment turned down in August after rising for 18 months.

The Conference Board Measure of CEO Confidence™ in collaboration with The Business Council fell to 52 in Q3 2024, down from 54 in the previous quarter. While this was the lowest reading in 2024, the Measure remained above 50.

CEOs’ assessment of general economic conditions turned negative in Q3:

26% said economic conditions were worse than six months ago, up from 16% in Q2.

Only 20% of CEOs said economic conditions were better, down from 30% last quarter.

CEOs’ assessments of conditions in their own industries also turned negative:

31% said conditions in their own industries were worse than six months ago, up from 26% in Q2.

26% of CEOs said conditions in their industries were better, down from 30%.

Consumer confidence dropped in September to near the bottom of the narrow range that has prevailed over the past two years,” said Dana M. Peterson, Chief Economist at The Conference Board. “September’s decline was the largest since August 2021 and all five components of the Index deteriorated.

ru82

1. “The Conference Board Measure of CEO Confidence™ ”

LOL, this stupid-ass Conference Board with its “Leading Economic Indicator” (LEI) has been saying the US economy will head into a recession “next quarter” since August 2022. And they’re still saying it. I ripped them apart publicly over this 11 months ago. These are just bullshitter organization. READ THIS:

https://wolfstreet.com/2023/11/20/leading-economic-index-predicts-recession-for-early-2024-after-having-predicted-a-recession-for-late-2022-early-2023-mid-2023-late-2023/

2. Consumer confidence has become highly politicized and partisan. Look at the partisan divisions of the University of Michigan Consumer Sentiment Index.

INDEX OF CONSUMER SENTIMENT, October 2024:

Overall: 67.9

Democrats: 91.9

Independents: 62.6

Republicans: 44.5

This means that Biden-haters hate the economy no matter what happens in the economy. These surveys are utterly useless in gauging the economy but are a good indicator of the partisan divisiveness of everything. But it wasn’t always so. This link below gives you the table all the way back to 1980. And you can see how much worse the partisan divisiveness has gotten. Just don’t confuse this with economic information. It’s Republicans expressing their hatred for Biden

https://data.sca.isr.umich.edu/fetchdoc.php?docid=77075

More great work. Thanks. I hope you are not casting pearls to swines, and more personally that I am not one of the wines.

I’m sure that one party would have us believe that with all the Haitian immigrants coming into the country, this retail sales growth is only because Petsmart and Petco are having to replace all the pets that are being eaten.

Sales generally produce profits, which is the PE ratio, which drives stocks higher. But I don’t think I will ask for my investment to “stop winning.”

I can’t wait for the election to be over, so hopefully, we will get fewer stupid comments about this being the “worst economy ever.” and be able to have a reasonable discussion.

This article makes a great case of a roaring economy driven partially by immigrants.

Having read a lot of your articles and tried to pull facts from one and facts from another and wonder how they would work together I have one question about the real estate market. What should the price of real estate be?

Here’s what I know or think I know:

0. I have a million theories, and occasionally one is right

1. Population is up so demand for real estate should be up. But that does not explain the huge bubble.

2. Inflation is up, but again it is only a partial explanation

3. Corporate and overseas investment in real estate has been up

4. The Chinese economy is crashing bigger than they will admit. Particularily in the real estate market. And their structural political problems will prevent them from solving this. They can not solve their problems until they change the relationship between the Party and the economy.

5. Corporate investors have made huge paper profits because of the bubble.

6. All of this growth screams for no interest rate cut from the Fed.

7. What i remember in previous RE bubbles was that our friends in Florida led the way back to reasonable prices. They seem to be doing it again.

8. The demand for housing is different in different areas so we might have too much housing in one area and not enough in some other area.

9. The Chinese are abandoning properties all across Southeast Asia.

10. Significant investments in home remodeling during the COVID years raised the value of homes.

11. Some or all of the above could be wrong but the question remains the same. If the bubble is crashing where will we end up and can we guess how soon?

So, my guess is that corporate buyers will become profit takers. The price of real estate will fall. But what should real estate be worth? Can we take the charts from so many of your columns and add a cone of uncertainty, like the National Hurricane Center, around where we think the prices will end up?

Real estate is only worth what a buyer is willing to pay for it and the seller agrees Otherwise, its “value” is a guess based on historical closed sales prices.

Yes, in a simple sense. I think you need to add the behavioral piece. Price is affected by sentiment, and sentiment is affected by storytelling. If fomo and the herding instinct has the crowd in its teeth, prices will rise. If fear and trembling are gripping the crowd, prices will wither. Bubbles appear in retrospect, after they burst.

I do think that there’s a way to value R.E.: the cost of replacement of the structure, the ratio of income to price, the relative cost of money, and some reasonable measure of land value.

What has happened, though, is that the cost of construction has morphed so much that per/sq/ft of building cost in some areas (metro SoCal, for instance) are 3 times greater than what they are in other metros where house and land prices are simply cheaper. Both land value, in L.A., for example, and construction costs are both stratospheric compared to cities like Richmond, VA. If tickets to see “Hamilton” are $800/ea in Seattle, but $200 in Greenville, SC, the performance is the same. It’s just that ticket sellers can pull it off in WA but not in SC.

Home prices used to be more closely related to income rates. It seems like 75 years ago (before the golden “debt age”) Americans would be able to buy a home for close to a year’s wages.

Over time it crept up, 2X, then 3X-5X of a median salary. Until today it seems that the base is now a strong multiple of a median salary.

Several dynamics are in play: financing (rates and structures), home size (having grown in size regarding sf/person, but now bifurcating), desirability (cities used to host the most desirable jobs, and now they’re remote. People discovered the beautifully less populated areas of our country).

Finally the “bubble fuel” IMO was in part related to the desire to flee urban areas, while “intending to return to the city after normalization.” Then home prices rose and nothing has “normalized.”

Let’s accelerate into the unknown!

Charlie: #9: …concentrating on acquiring Taiwanese and generating South China Sea real estate/sealane suzerainity instead?

may we all find a better day.

Can you please send your email address to the Federal Reserve,they need a dose of reality…

It would be a good idea if members of the Federal Reserve go grocery shopping with their significant others and they can see the real economy in action

There are CEOs that command enough political influence that they can force articles to be read at the FOMC’s meetings. The “big boys” actually control the economy – but aren’t doing a good job of it.

LMAO!

“The “big boys” actually control the economy – but aren’t doing a good job of it.”

You should visit where they live and play and then ask yourself how they can afford it….since they’re doing such a ‘bad’ job. I have met more than a few of these “big boys” and I know a slew of people that work at Kukio, Hualalai, Mauna Kea, et. al. and the story is universally the same. These CEO’s are truly Wolf’s drunken sailors. There is one word you must never speak to one of these neo-feudal Kings of finance: “No” Once spoken, banishment is quick. A more gluttonous, self absorbed group of people you have never met.

Visit Aspen, the Hamptons, etc. It’s the same all over. Regular Joes and Janes make a good living in the trickle down world of these self absorbed clowns, but you must never deny them their pleasure.

WAIONO, yep, pleasure and prestige. If you could sell prestige by the bottle, you’d be the wealthiest person alive. Btw, they don’t give a rat’s a** about the poor.

TrueValue just went bankrupt. Cited slumping sales. Several other well known brands, while they might not be that dire, are saying the same thing. Wal-Mart said something to the effect of the low-end consumer is not doing well. The high-end consumer is doing well.

As I have said before: in whatever city you live in, the top area pricewise has simply pulled away from the other areas to a much larger degree post pandemic. That same effect may have rippled down (or perhaps its bottom up) to consumers. I question the institutions we have know what to do anymore in a number of areas.

Had a hunch so did a quick Google. Private until 2018, then bought by PE firm ACON.

Sales probably affected by online, but more likely it was strip mined and saddled with debt and presto: bankruptcy.

Obviously the model works, they are being bought again and will continue to operate.

ACON. What a great name for a PE investment company.

The buyer, Do It Best. is a member owned Co-op, owned by the individual stores.

I googled around, but was unable to find out if Acon made money here. But perhaps Wolf or another poster here can find that info ?

I don’t believe what you’re describing shows a weakness or social imbalance in regards to sales. Retail sales “jumped”. Simply an evolution from brick and mortar, to e-commerce. It was happening prior to the pandemic, but accelerated as people were almost forced to try it, being locked down. I’m getting old, grouchy, and set in my ways, but I love e-commerce. I would rather argue with myself about a purchase than deal with someone that knows far less about it than I do. The supplier for these retailers are selling their widgets on line thru various outlets like Amazon much cheaper. Even if your not a prime member, most times you can pay the overnight rate and still get it cheaper. Online sales items have complete descriptions, pictures, part numbers, and reviews. Up next Auto Zone and Orielly auto parts.

I recently bought a 5 quart jug of synthetic motor oil and Amazon shipped tham to my front door for LESS than Walmart and TEN DOLLARS less than the local O’Reilly. Once the poor learn that the can buy oil and other auto parts from their phone we will need a lot less auto part stores.

Look up RockAutoDOTcom online. You’ll see prices much lower than Amazon, O-Reilly and WallyWorld.

But does Amazon take back your waste oil?

SomeGuy,

“Wal-Mart said something to the effect of the low-end consumer is not doing well.”

This is a blatant lie. Walmart (learn how to spell it) had a blowout quarter, driven by grocery and ecommerce; as did Amazon. You’re abusing my site to spread bullshit to promote your BS narrative.

In addition to what Pilotdoc, Joebagodonuts, and ApartmentInvestor said:

The dollar stores, which rip poor people off with minuscule quantities in the package, are not doing well. They’re part of the Brick and Mortar Meltdown, as I have been calling it since 2016, where ecommerce kills brick-and-mortar retailers. Low-income people are now making enough money, after big wage increases, to shop at Walmart and get a better deal, LOL, and they’ve figured out how to buy online with their smartphones for less, and get it shipped to the house without having to waste money on too-expensive gasoline.

https://wolfstreet.com/tag/brick-and-mortar-meltdown/

@Wolf to give @SomeGuy a break it has less than ten years since Walmart changed their name getting rid of the dash.

“Walmart changed its legal name from Wal-Mart Stores, Inc. to Walmart Inc. on February 1, 2018”

I already gave him a break on spelling, which is why I put it in parenthesis, to indicate that it’s not important.

All my poor friends know the dollar store is a ripoff. They shop at Goodwill / Savers / thrift stores instead of buying new.

Short – …at least in our area (Sonoma County), item availability/selection/quality (older, non-stylish, contemporarily-functional furniture, as well as castoff flatpack/flimsy items being some exceptions) continues a long-term decline at those venues. (…mebbe an availability/selection improvement coming with recent drunken-sailor spending, but wonder about that supply-stream’s quality component given our contemporary quality/price preferences for so many, now-usually imported, less-durable retail goods …Craigslist a significant player in this phenomenon, as well…).

may we all find a better day.

These data confirm what many have been saying, there is plenty of liquidity in the system.

“Full faith and credit”

Interesting times.

“plenty” is a misnomer, “still way too much” would be more correct, I believe.

Thank you. The economy REMAINS grossly overheated.

Yes, by “plenty” I mean fucking ridiculous…

CONgress needs to balance the damn budget.

This is at the heart of “fucked up” economy that I refered to earlier. To the individuals on here that continually bash the Fed. (You know who you are.😅) The unknown excess liquidity and immigration make their job pretty damn difficult.

USA consumer spending: a graph that keeps going up and to the right

It’s the “prosperity forever” chart!

No, it’s the shop-till-you-drop chart.

With e-commerce, you can shop even after you drop.

Don’t see how one gets “shopping therapy” with e-commerce.

Number of packages delivered still counts as “neighbor points”

, though…..I guess….

I know drugs seen on TV are available for those who purchase 2 of same item and forget it….or just purchase anything and forget….

I’m astonished at how many people here think that cutting 0.5% has much of anything to do with this retail spending data.

Wage growth out pacing inflation. Spending holding up even with rates well above CPI and PCE (which are trending down to very near 2%). Home prices stabilizing. Unemployment sub 5%. What here is not to like? This is how the middle class grows. The longer we can maintain these numbers the better, and if that means a few 0.25-0.50% rate cuts than so be it. Better than having to resort to huge deficit spending packages to bail out billionaires and megacorps.

70-75% of americans are unhappy about the economy. so either things aren’t as rosy as you present, or they’re wrong to be unhappy.

which is it?

They’re wrong to be unhappy. But if you’re in the cult… the worst economy in history is truthy.

lol okay i’ll bow out here. clearly you think there’s no gray area between best economy eva and worst economy in history.

“I’m astonished at how many people here think that cutting 0.5% has much of anything to do with this retail spending data.”

“The longer we can maintain these numbers the better, and if that means a few 0.25-0.50% rate cuts than so be it.”

I’m confused. Your first sentence is pretty clear, but your other sentence implies you believe there *is* a correlation between Fed cuts and consumer spending.

Kind of a short run long run sort of effect. I don’t see a cut in mid september causing big retail spending numbers in september.

Looks like growth and inflation in China and Europe is slowing down what is the difference between them and the U S ? Is it all the government spending here that is driving the economy ?

“Over the past three decades America has left the rest of the rich world in the dust. In 1990 it accounted for about two-fifths of the GDP of the G7. Today it makes up half. Output per person is now about 30% higher than in western Europe and Canada, and 60% higher than in Japan—gaps that have roughly doubled since 1990. Mississippi may be America’s poorest state, but its hard-working residents earn, on average, more than Brits, Canadians or Germans.”

-per The Economist

Might have to do with things like that. The article also mentions our light touch regulations and the fact that we spend during crises. Yes the stimulus after the pandemic fuelled inflation but it also ensured that the U.S. has grown by 10% since 2020. That’s 3 times the pace of the rest of the G7. In contrast to stingier Germany, that has been mired in a recession for 2 years.

how much of that growth results from government deficit spending? even if government doesn’t spend directly, much of the money ends up in the hands of businesses, individuals and others who spend it. it’s the multiplier effect.

it’s all great in the short term, but it assumes there is no limit to what the u.s. can borrow on a federal level at reasonable rates.

Wow, stunning.

With all the bitching and moaning on-line you would think ….

Well the US has a debt per capita of around $105,000. Im not too knowledgeable on how it all works but I feel like that could reduce our living standard at some point.

van – to reposit, living standards already declining, debt-per-capita a leading indicator of the ‘socialize’-half of the ‘socialize all risk/privatize all profit’-capitalism equation…

may we all find a better day.

Yeah. I now just substitute “austerity” for inflation…..and it is trickling right on down the net wealth chain….and accelerating.

Still, we all still enjoy the huge living standard boost from the having most bad-ass military and alliances on the ball.

J. Powell must be losing sleep. GDP growth again accelerating above normal after a short respite in Q1 2024; stocks hitting new highs; gold hitting new highs; bitcoin at multi year highs, all with a FF rate significantly over inflation readings. Excess reserves are still much too high and are “leaking” into the economy causing excessive growth. If he doesn’t take back the .5 % rate decrease at the next meeting double digit inflation is coming.

” …double digit inflation is coming.”

Those of us retirees with a bundle in money market funds can only hope.

Being a saver, I invest in treasuries and a little mm funds but I do not hope inflation spikes again. Inflation is hardest on the poor, who have it hard enough already. I think higher inflation would be a net negative for our country.

RickV. I have 60+ years exposure to gold coins, and I would not put much faith into the current high gold prices.

I recently had a visit with some other “old farts” who lived through and remember the peak 1980 prices for silver and gold. One was a coin dealer with 58 years of experience. We all agree that sentiment (speculation ?) is rampant right now. Our feelings were based on the spread between older but still nice AU-UNC silver & gold coins. The spread is negligible, and a lot of really nice old coins are being bought and sold as bullion. Today, scarcity has little to do with the price for most PM coins (other than a few key rarities). One caveat here, I am an “insider” (or at least I was).

OK. Where am I going with this? (old age sucks). Prices for precious metals peaked January 1980, and anyone who bought into the mania had to wait almost 30 years to break even. On the other hand, this time could be different, and that was what everyone was thinking in 1979. If you really want to destroy a paper fiat currency, start a war.

Regarding Crypto: I have to agree with Wolfie. They are gambling tokens. With one exception: there is a market for old tokens (physical “good for” tokens). With crypto you don’t even have that. I will also stick my neck out here, and say that someday the Dutch Tulip Mania will be compared favorably to Crypto.

I also remember the “Nifty Fifty”.

Old Ghost,

I too have 60+ years exposure to gold (and silver) coins. And yes I have a few silver eagles I paid $45 for in the 80s (the price is offset by pre ’64 silver coins I picked from circulation and put away in the ‘60s with my father), and a few gold coins I bought in the ‘70s. I do think this time is different: the US has confiscated Russia’s Treasury securities scaring the other BRIC nations including China, India and Argentina who no longer trust putting their trade surpluses into the US dollar and US securities. They appear to be moving a significant portion of their surpluses into precious metals (gold has now passed the Euro as the second largest reserve asset by dollar value). How far will it go? Who knows. And I agree old age sucks!

RickV and Old Ghost, it seems you both agree on the realities of old age. But, if I had to choose between the opposing arguments you both present on gold, for that I’d lean toward the Ghost.

Speculation is rampant, not only in PM but in crypto, meme stocks, spacs, nfts, AI stocks, antiques, vintage autos (which, imo, are what SLR cameras are to digital photography), multi-million dollar shacks in primo locations, ocean-front properties, art objects, Bibles with the American Constitution bound inside… You may want to add to the list.

Some things are different this time, but some things aren’t.

Federal Surplus or Deficit [-] as Percent of Gross Domestic Product (FYFSGDA188S)

https://fred.stlouisfed.org/series/FYFSGDA188S

The fiscal largesse is obviously contributing to gDp.

Looking forward from this report, a recent post at kiplingers suggests the Feds future rate cut focus is increasingly screwed up, especially with this retail inflection point:

“Annual inflation numbers for the rest of this year are not likely to drop below the September rate of 2.4%. This is the result of the relatively soft price increases that took place in the fourth quarter of 2023, which will make year-over-year comparisons in the upcoming Consumer Price Index reports seem like little progress is being made on inflation”

Yes, we’ve been saying this for months right here. It’s the fading “base effect.”

It’s transitory.

It’s at times like this you think the FRB are being unaccountably negligent in order to run hot on inflation to melt away those debts.

You can’t question their logic, but the tiniest bit of imagination saw this coming the moment they cut rates.

However, they do what they do… all I need to know is when to BTFD again ;-)

With inflation-adjusted GDP growth trending higher than average, largely driven by strong consumer spending, what do you think are the long-term risks to the economy if this ‘no landing’ scenario persists, especially in terms of income inequality and structural imbalances in consumer behavior?

A generation of higher interest rates.

Poor like you-

Agree with Short TLT above, and add two other likely outcomes:

1. Expect to see a big increase in academic literature “word-count” search for the term “un-anchored inflation expectations.”

2. Whiplash-inducing rate volatility.