Sales drop further, new listings & inventory rise. Prices: Toronto -16% from peak. Vancouver flat for 9 months, -2.5% from peak. Calgary & Quebec hit new highs. Edmonton condos back to Dec 2006!

By Wolf Richter for WOLF STREET.

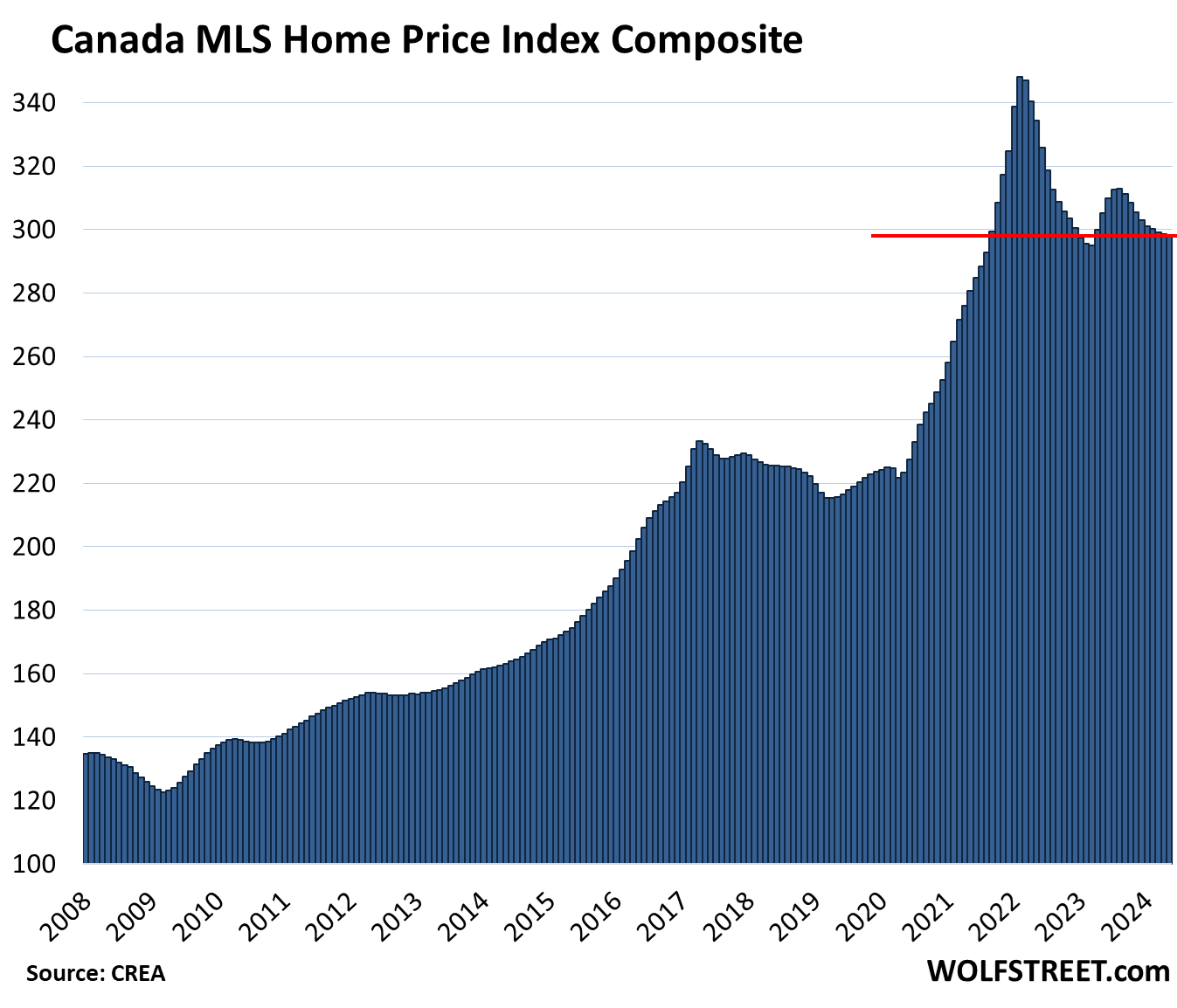

Home prices in Canada edged down 0.2% in May from April, the ninth month in a row of declines, seasonally adjusted, according to the Composite MLS Home Price Index from the Canadian Real Estate Association (CREA) today. Condo prices fell faster than single-family prices.

From the peak in February 2022, the index is now down 14.4%, and is back where it had first been in September 2021.

Year-over-year, the index fell 2.4%, the second year-over-year decline in a row (-0.9% in April). But there were big differences, with Calgary and Quebec City rising to new all-time highs, while prices in other metros fell further, such as Greater Toronto where condo prices continue to carve out multi-year lows.

Spring selling season is a dud.

Home sales edged down by 0.6% in May from April, the fourth month in a row of declines. Year-over-year, home sales fell by 5.9%.

New listings rose by 0.5% in May from April, the fourth month of increases over the past five months.

Slower sales and rising listings drove up inventory and supply. Overall inventory listed for sale jumped by 28.4% year-over-year, to the highest level since before the pandemic, and the second biggest jump on record, according to CREA. Supply rose to 4.4 months (up from 4.2 months in April, up from 3.9 months in March), back to prepandemic levels.

The Bank of Canada cut its policy rates by 25 basis points earlier in June, to 4.75% for its target of the overnight rate, after keeping them for 11 months at 5.0%. But it said QT will continue. The BOC has already shed 64% of the securities it had added during the pandemic. This tightening has thrown some cold water on the silly exuberance in the housing market through early 2022, fueled by the BOC’s free-money policies.

Home Prices in the most splendid Housing-Bubble Markets.

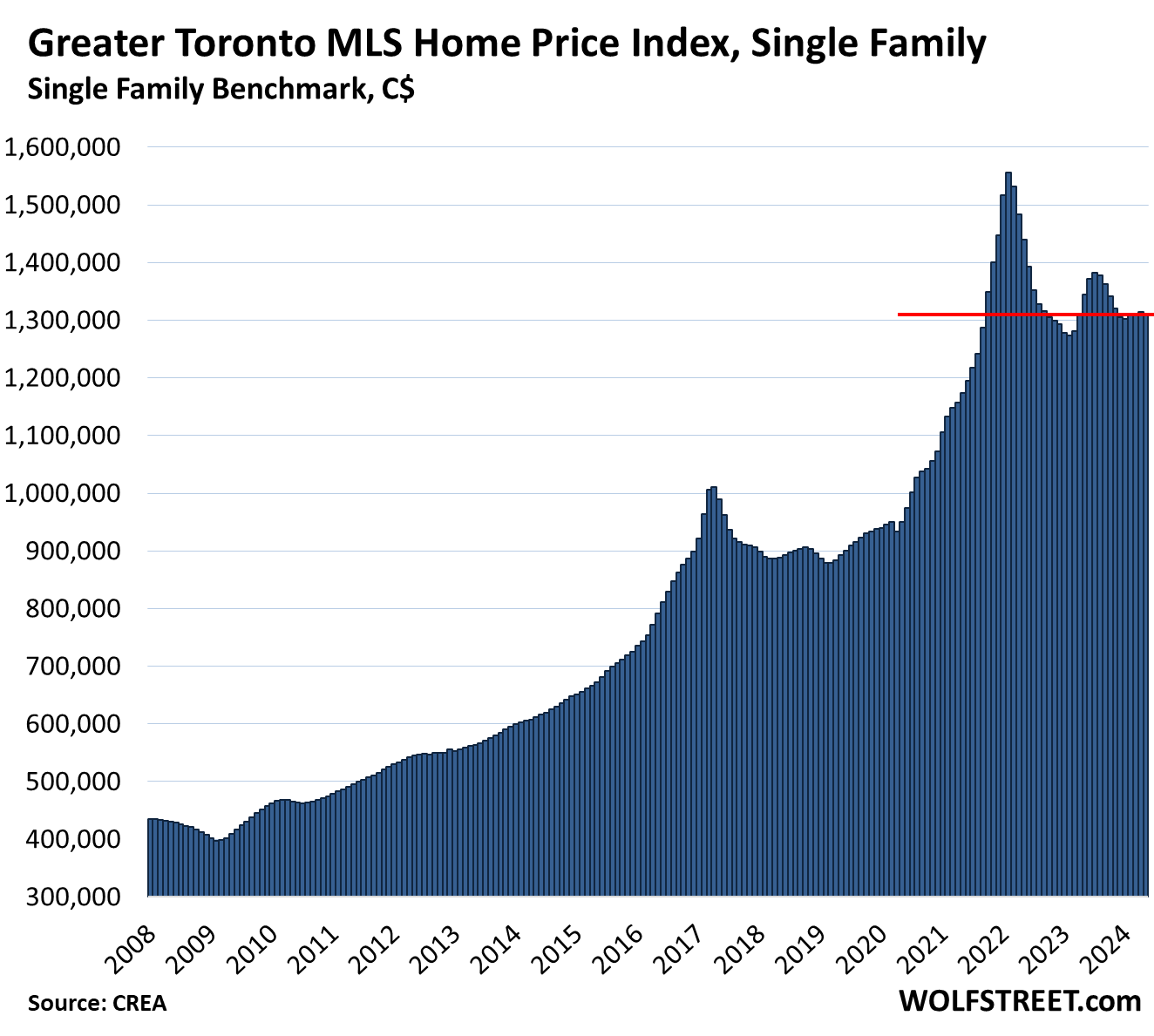

Greater Toronto Area, single-family MLS Home Price Benchmark Index (all prices in Canadian dollars):

- Month-to-month: -0.3% to $1,309,700; below October 2021, and roughly flat for six months.

- From peak in February 2022: -15.8%, or -$246,000

- Year-over-year: -2.6%.

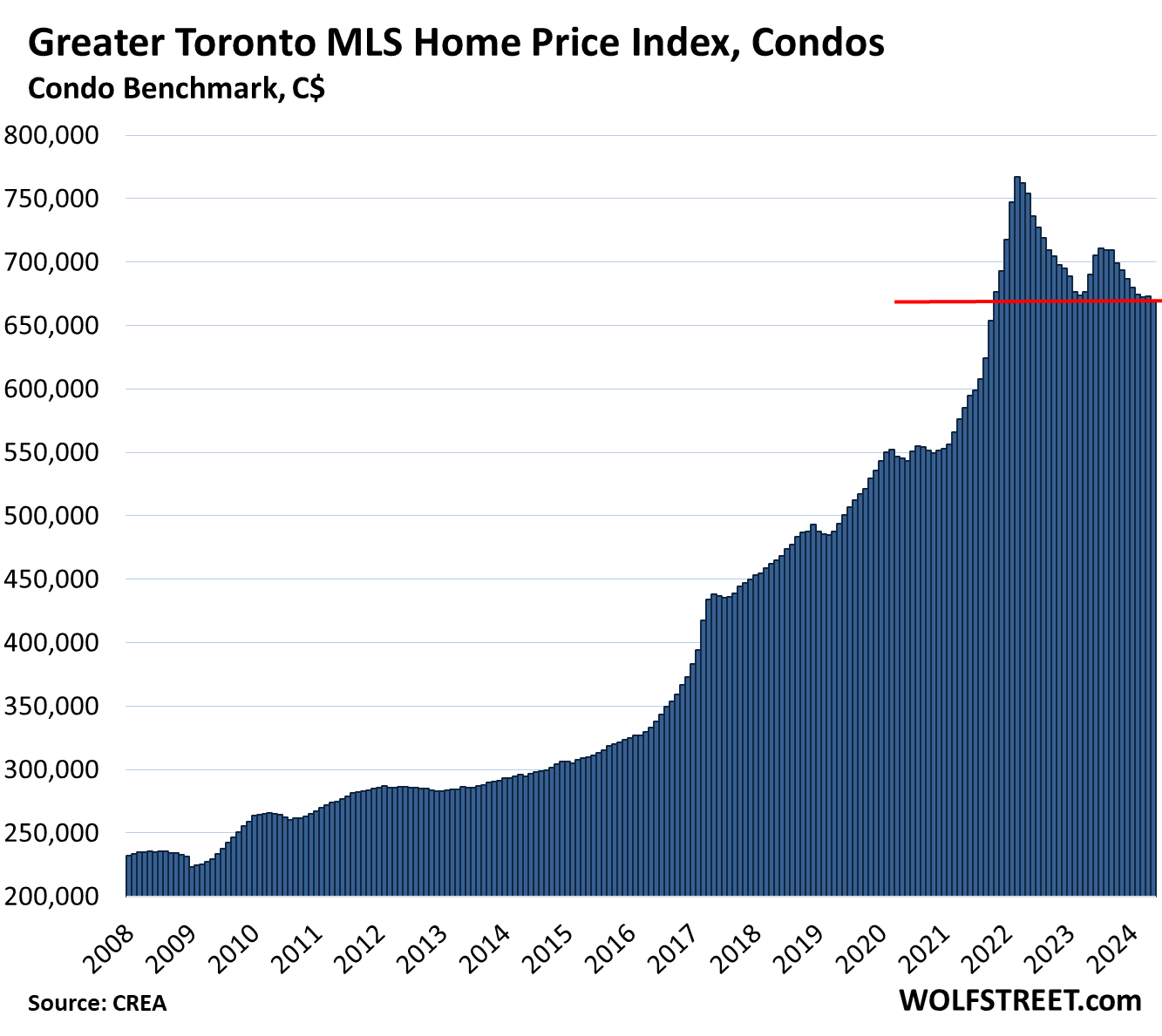

Greater Toronto Area, condo benchmark price:

- Month-to-month: -0.6% to $669,100, the lowest since November 2021

- From peak in February 2022: -12.8%

- Year-over-year: -3.0%

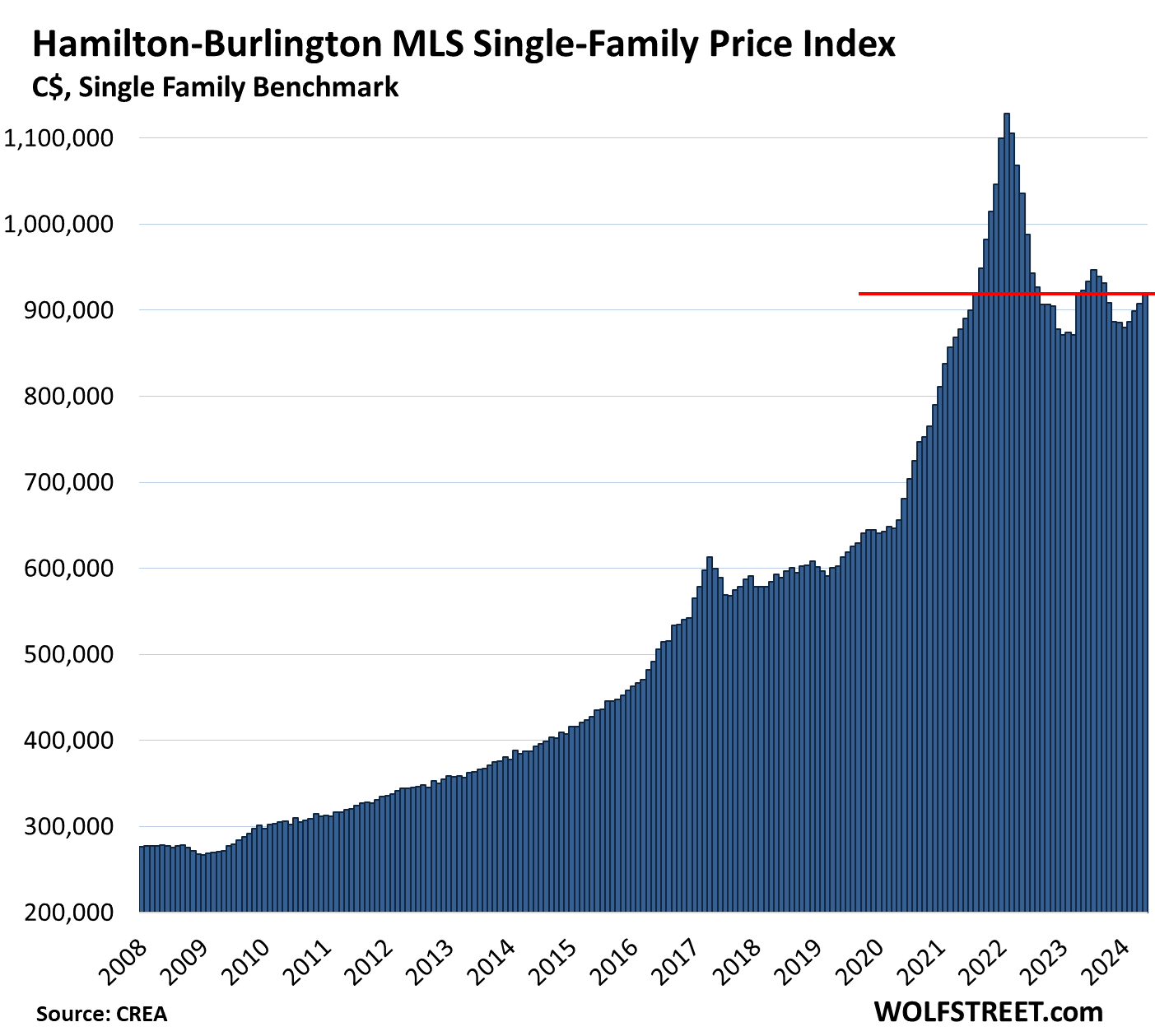

Hamilton-Burlington metro single family benchmark price (in the “Greater Toronto and Hamilton Area”):

- Month-to-month: +1.2% to $918,100, first seen in August 2021

- From peak in February 2022: -18.7% or -$210,800

- Year-over-year: -0.5%

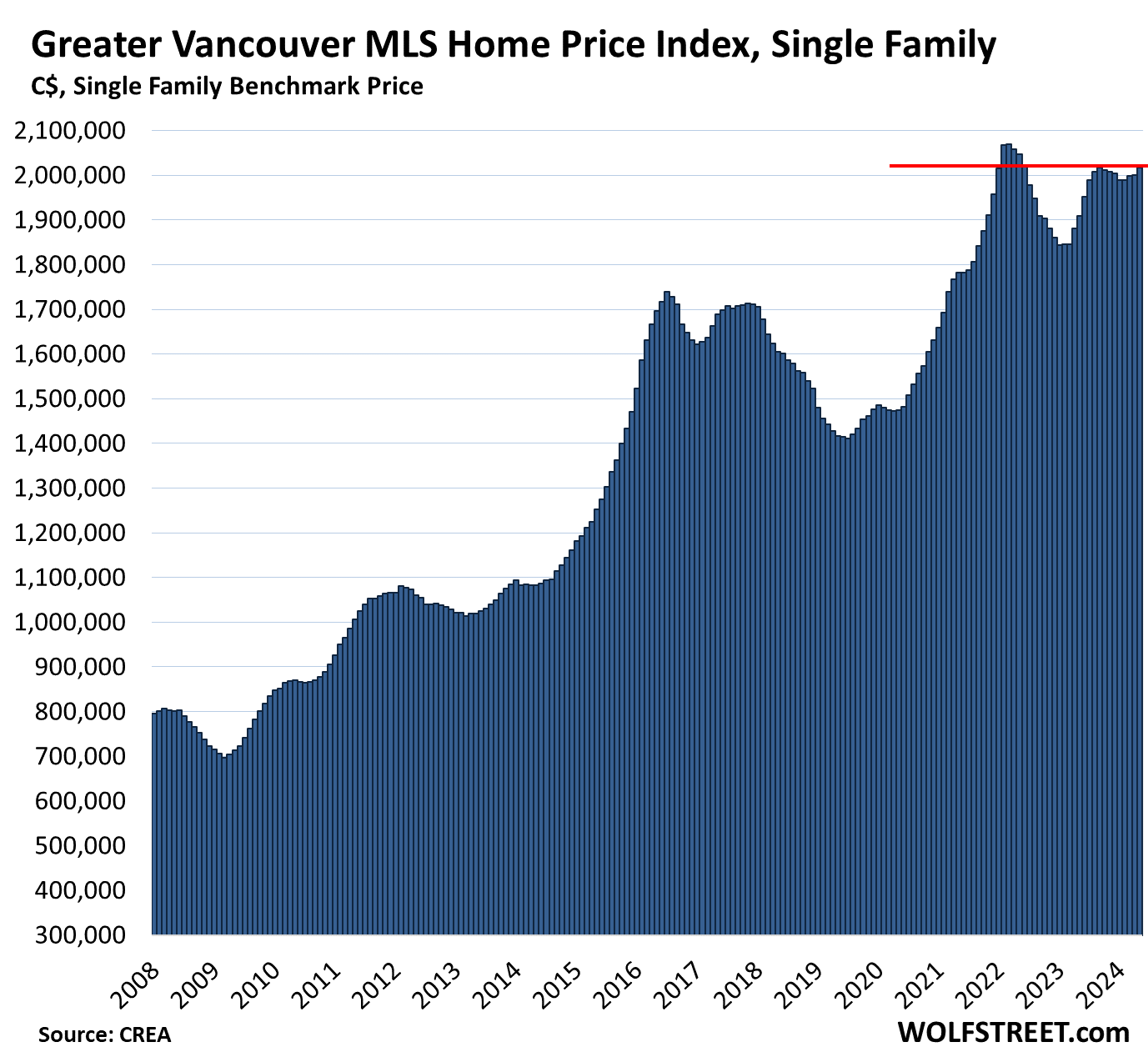

Greater Vancouver single-family benchmark price:

- Month-to-month: +0.8% to $2,016,200, first seen in January 2022, roughly flat for nine months.

- From peak in April 2022: -2.5% or -$42,200

- Year-over-year: +5.6%, the smallest gain since July 2023.

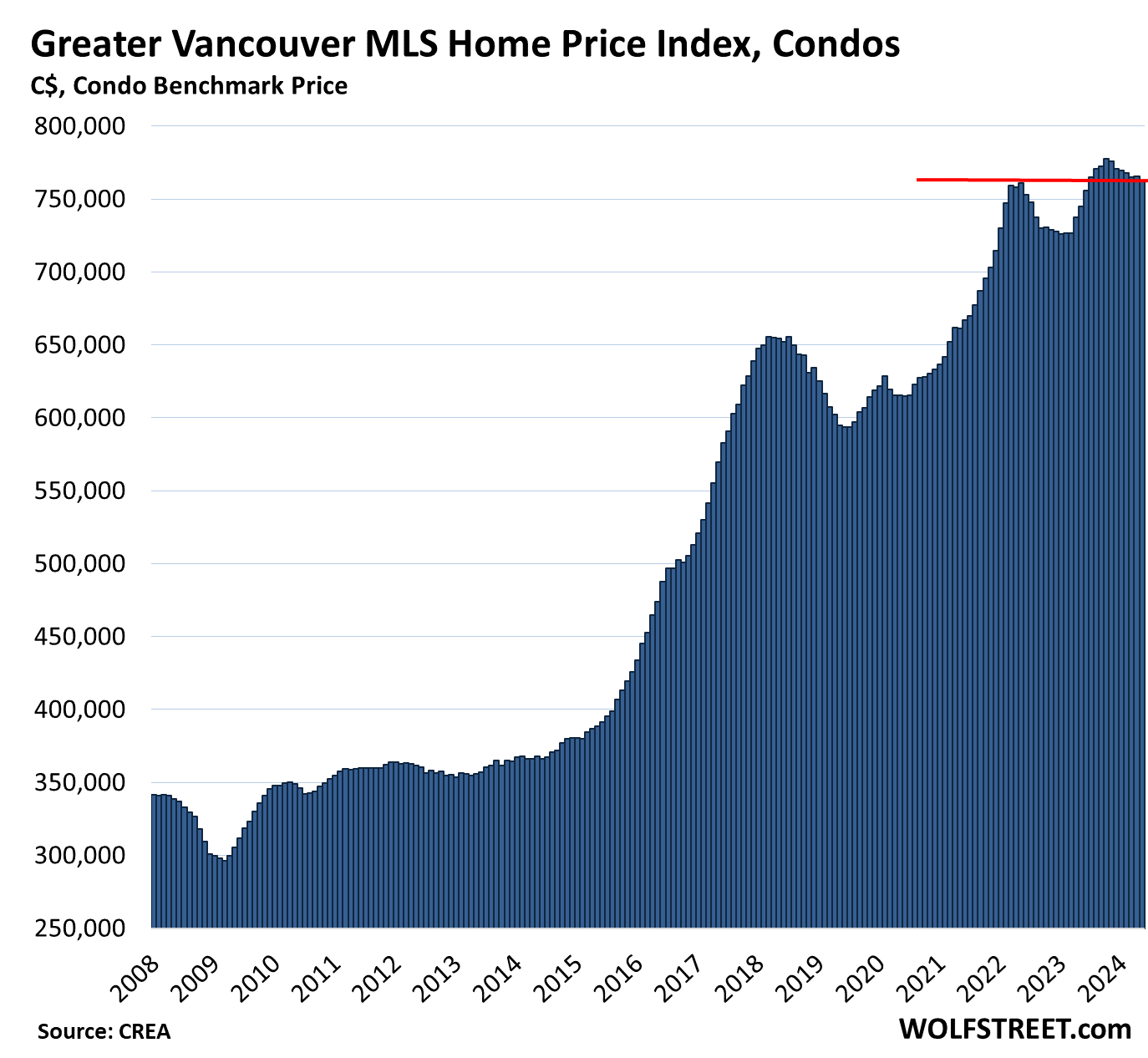

Greater Vancouver condo benchmark price:

- Month-to-month: -0.4% to $762,200, about the same as in May 2022.

- Year-over-year: +2.3%, the smallest gain since June 2023.

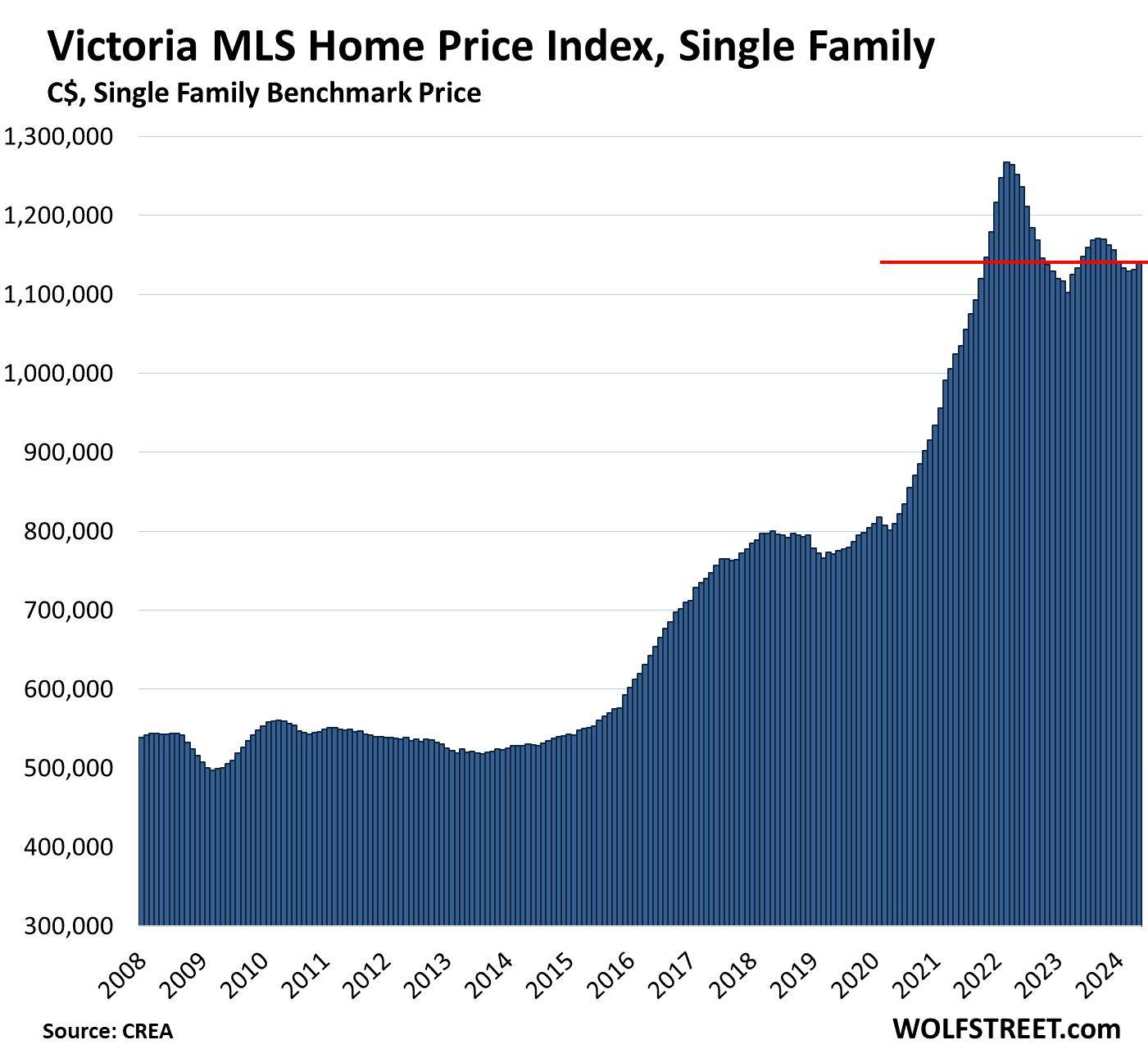

Victoria, single-family benchmark price:

- Month-to-month: +0.7%, to $1,139,400, first seen in November 2021

- From peak in April 2022: -10.1% or -$128,000

- Year-over-year: +0.5%.

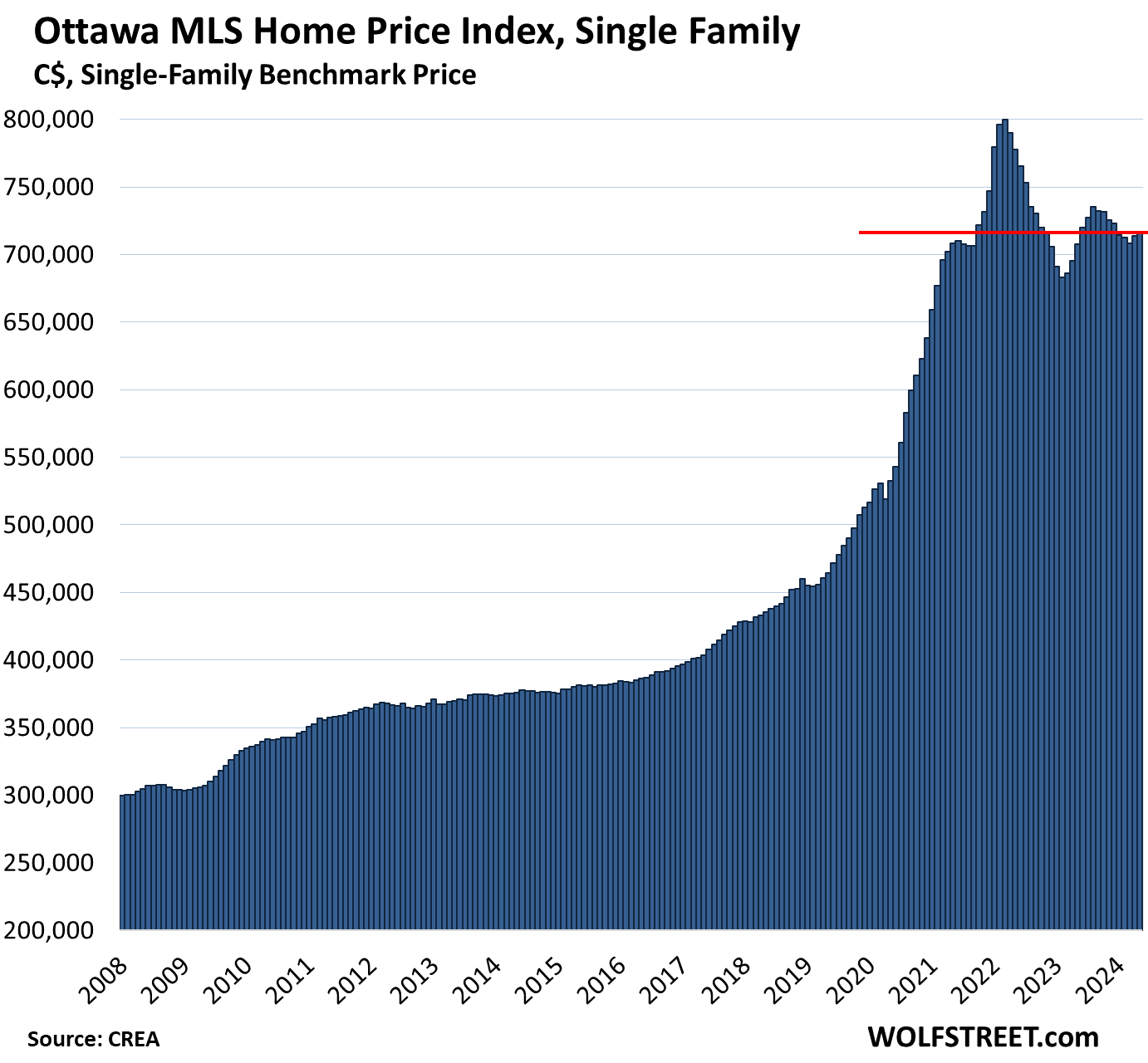

Ottawa, single family benchmark price:

- Month-to-month: +0.8% to $716,600, first seen in October 2021

- From peak in March 2022: -10.4% or -$83,000

- Year-over-year: +2.7%.

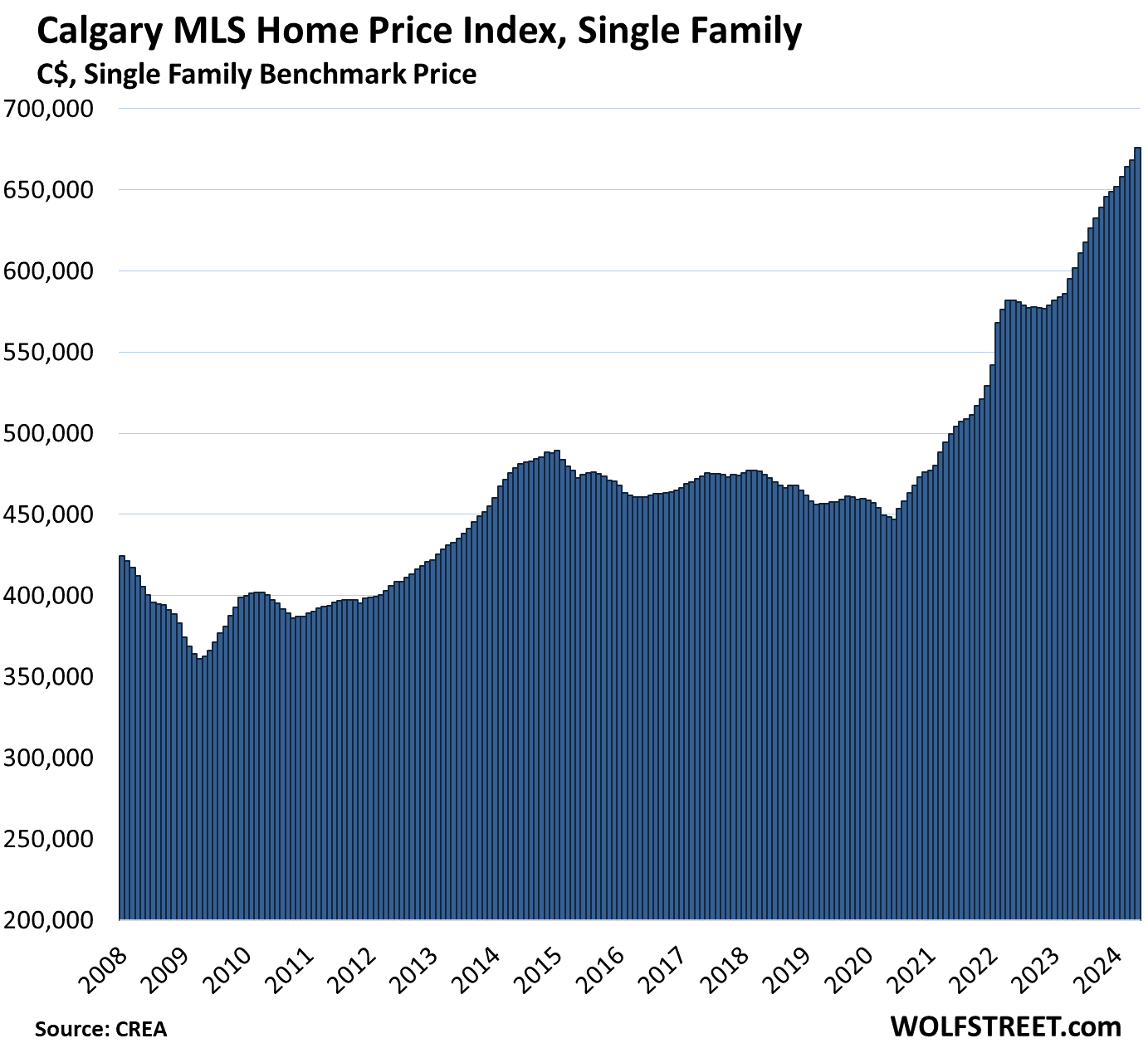

Calgary, single family benchmark price:

- Month-to-month: +1.2% to new high of $675,800

- Year-over-year: +12.3%.

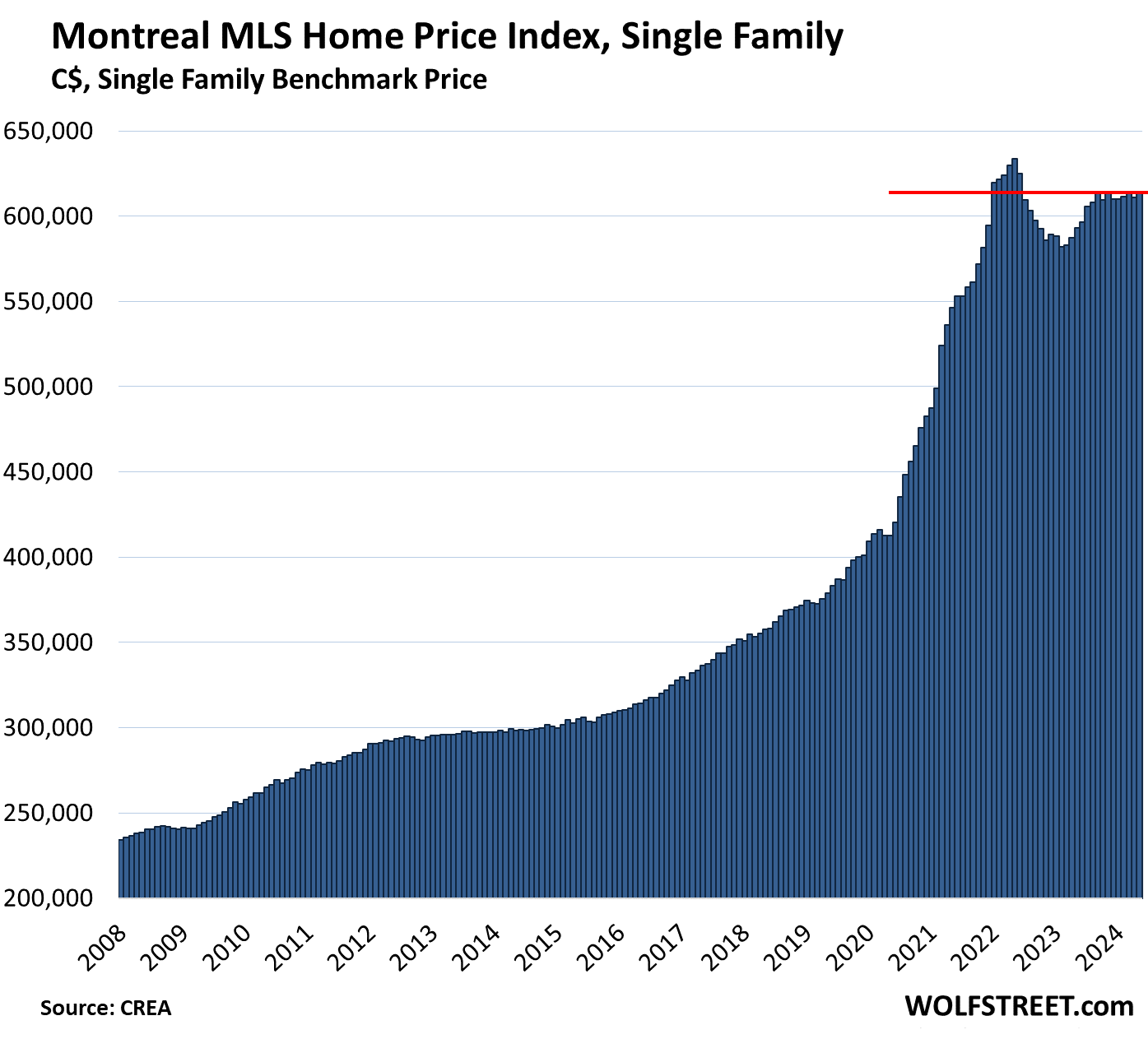

Montreal, single family benchmark price:

- Month-to-month: -0.4%, to $613,000, first seen in February 2022, and essentially unchanged since September 2023.

- From peak in May 2022: -3.2%

- Year-over-year: +3.4%.

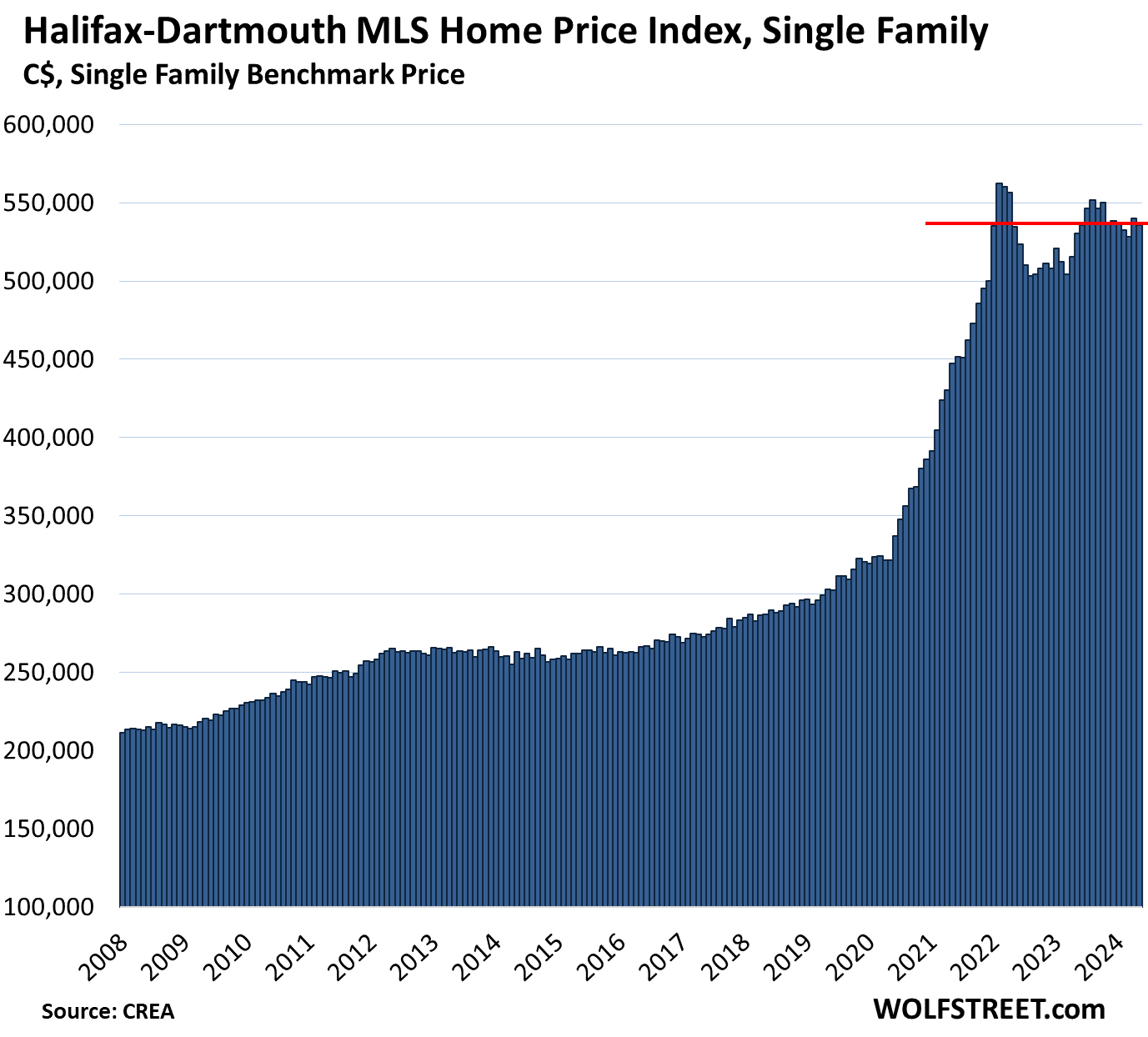

Halifax-Dartmouth, single family benchmark price:

- Month-to-month: -0.8% to $536,000

- From peak in February 2022: -4.7%

- Year-over-year: +1.1%, the smallest year-over-year gain since the year-over-year drop in May 2023.

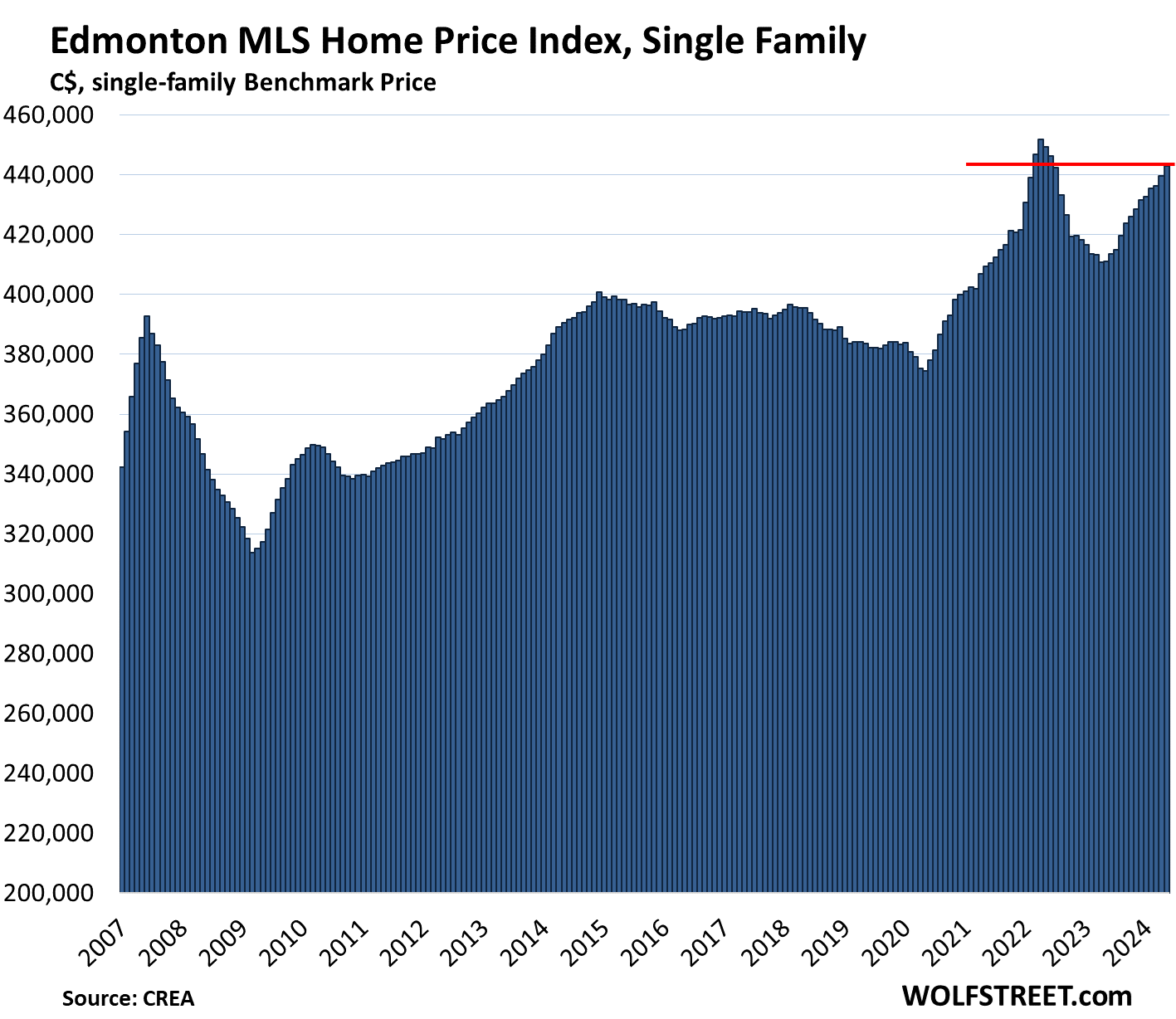

Edmonton, single-family benchmark price:

- Month-to-month: +0.7% to $442,800

- From peak in April 2022: -2.2%

- Year-over-year: +7.7%

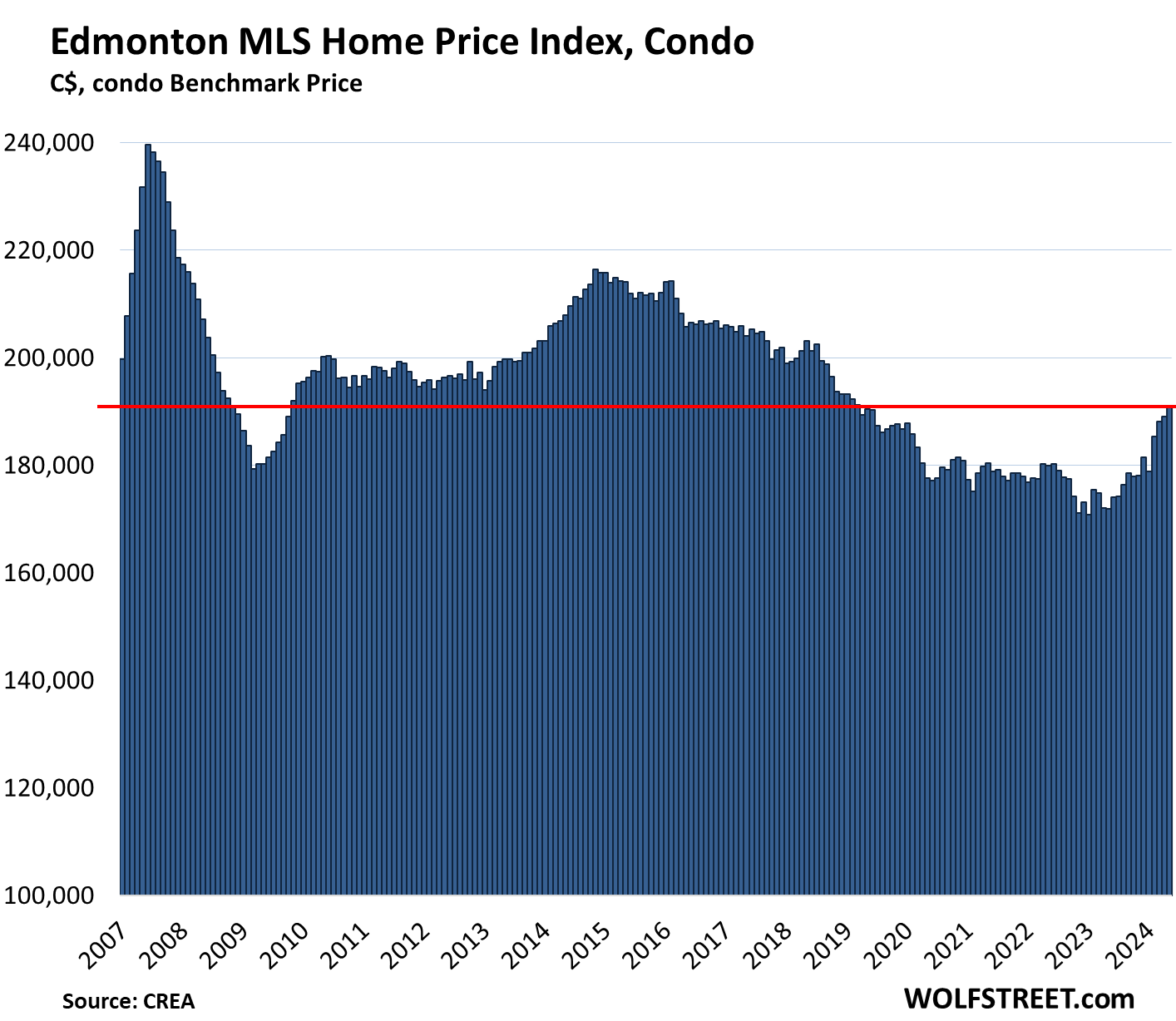

Edmonton, condo benchmark price: What an epic bubble looks like afterwards. Roughly unchanged since December 2006 and down 20.4% from peak in June 2007.

- Month-to-month: +1.0% to $190,900

- From peak in June 2007: -20.4%

- Year-over-year: +11.1%

- First seen in December 2006.

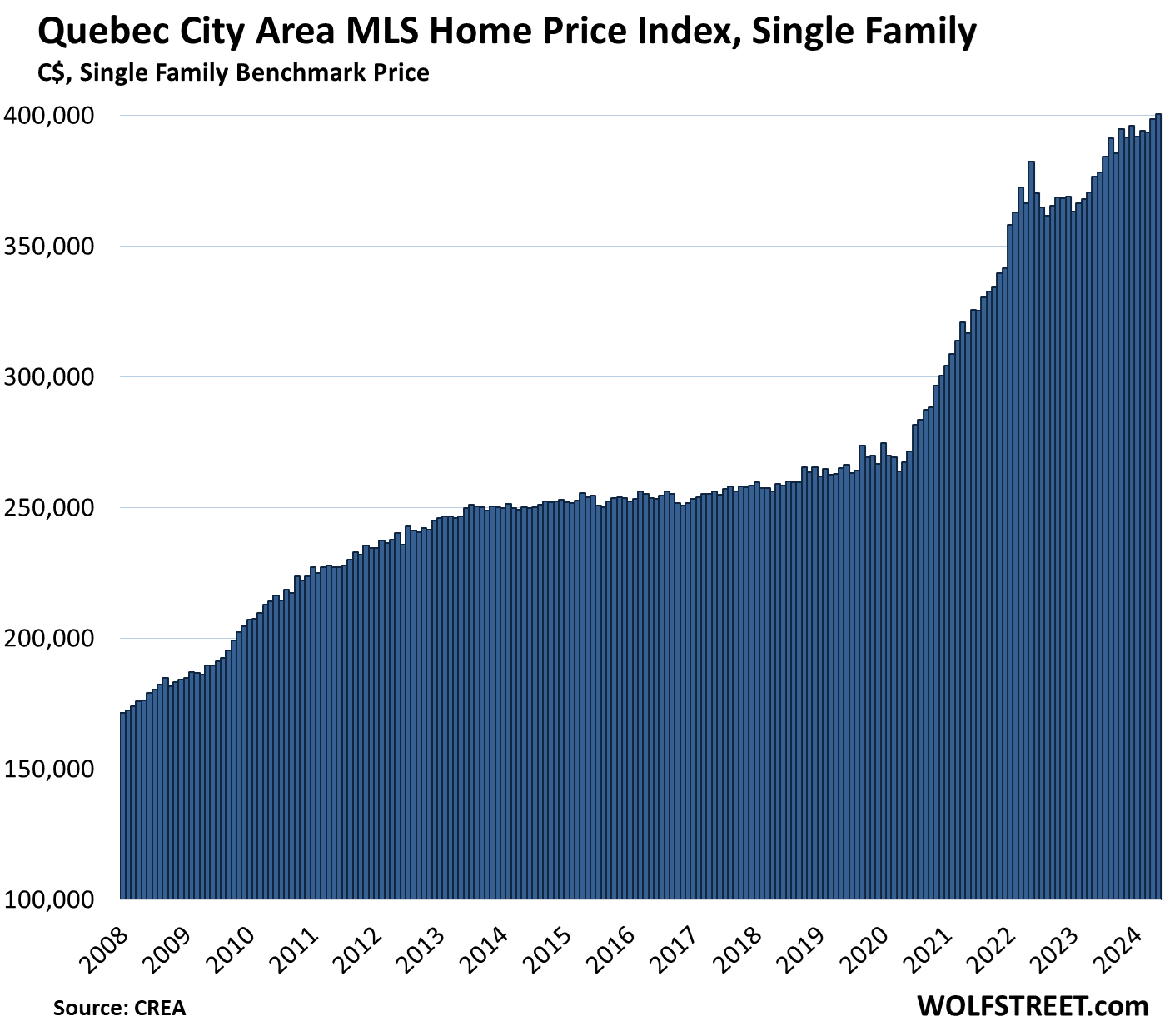

Quebec City Area, single-family benchmark price:

- Month-to-month: +0.4% to $400,400

- Year-over-year: +6.3%

- Eked out new high.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

MW: Treasury yields rise by most in over a week on brighter U.S. economic prospects…

lunch break read. :-) Good stats and data as always.

What we are seeing on the west coast is a stagnated market, but price drops still remaining sticky. Changes to Federal capital gains tax for secondary properties in the next 2 weeks has pushed closing dates forward and put some real concern out there. Changes in ourprovincial short term rental policy has also prompted a lot of selling/listings in vacation destinations like Kelowna and Victoria, but also killed off that buyers niche as intended. Still, the prices remain too high for new buyers to buy those disliked B&B listings. Folks are in a wait and see mode. In my remote area there are 14 current listings, some are way overpriced and are even the butt of jokes, but they always stay at the same price. One has been listed for two years.

Another issue is that it is now against the law for an agent to represent both seller and buyer…a historic middleman role meant to bring both sides together. That has been the tradition for decades. But due to corruption, mostly in the overheated Vancouver and Victoria markets, that was removed some years ago in the hope to foster more competition with defined agent roles. Instead, there are under-the-table wink wink nods between the listing and purchaser agents, (often in the same company or agent consortium) without much actually changing. Plus, a listing agent these days often names a high price beyond any possible chance to actually sell the property….. just to get the listing. The hope is to wait out the lull and just get something/anything out of it. What that means is instead of the usual 1-2 specialist agents for remote waterfront or vacation properties, we now have new agents that no one has even heard of with their names on signs on overpriced property. They have simply told the sellers what they want to hear instead of what is possible.

I have family who recently accepted an offer subject to selling the buyer’s Kelowna condo. It probably won’t finalise in this market. A few years ago we were asked by a family friend to list a place with their son who was a new agent in an entirely different city. Why would we do that, he didn’t know the market at all, but he would still get the listing commission. Crazy.

I’m wondering if Paul has noticed that the homes that are selling are extra nice? It seems to me that in CA a higher percentage of homes that are “move in ready (often will ALL new carpet and paint) are the ones selling. I just heard that a guy I know sold his home on the SF Peninsula and after looking at the photos on Zillow I’m guessing that they spent at least $100K to paint the place stage it and and upgrade the landscaping. I was not aware that it is now “against the law” for an agent to represent both seller and buyer in Canada. I’ll be interested to see if we have more or less agents representing “both” the buyer and seller in the US after the new rules related to the NAR settlement earlier this year that will require more disclosure of fees to buyers kicks in two months from now.

Wow, those are ridiculous “markets”, especially Quebec. Having spent a lot of time there in my youth, I can tell you that those larger homes become a significant heating liability in the winter, perhaps global warming will change that.

The Feds were promoting heat pumps a while back, especially in the East. What they didn’t promote was that in under 35F degree temps you need dual-heat installation costing 10s of thousands of dollars. And in a lot of the East coast they don’t even have NG; it’s oil or propane.

My air source heat pump does the bulk of the heating down to nearly 0F now. 2021 install. Impressive technology. I live in Minnesota, 0 is a normal temperature in winter.

“… does the bulk of the heating …”

Yes. Typically electric baseboard or dual furnace is recommended.

Alternatively, the geothermal option for cold climates, but capital cost can be prohibitive for many, and HP equipment life is shorter.

I lived just North of you and am not a fan of baseboard heating. One winter cost me $400 a month (at 10c/KW hr) for an 800 sq ft house. But a lot of houses have NG furnace, can be combined, so cost is much less.

Cannot rule out another leg down as long interest rates stay relatviely stable

I wonder if buyers are increasingly unable to qualify for a mortgage? That would suppress demand.

How many pending…end up back on the market, is something to include.

First time home buyers might be shocked at the shack they can’t qualify for.

You have the right idea

Same here, sticky prices. New build is not an alternative, either, as construction cost are steep and up over prior years.

For affordability, price is one aspect. Interest rates another, ( from zirp to jacking rates; and short terms in cdn). Cummulative inflation another. Tax increases another. All combined, a massive financial savergy by cdn govt and central banks.

Daydreaming that one day Wolf will publish something like just like this headline below…a man can dream…

“The Most Splendid Housing Bubbles in “Southern California”, May 2099: Prices Drop Further, -14.4% from Feb 2022 Peak, -2.4% YoY, back to Sep 2021. Spring Rally Dud

If people are finally being confronted with the reality that their investment in a house is not going to appreciate by huge percentages every year there is hope that the mania and crazy speculation and FOMO will diminish. It was a guaranteed return of massive gains and now it is not. I don’t think average people pay attention to economic news. They saw other people making hundreds of thousands and they wanted to jump on the bandwagon. Now it looks like a gamble.

Exactly this; you might as well be a preacher standing outside the casino entry, shouting about temperance…nobody’s listening

Hold on, Let’s Look at the Other Side of the Canadian Housing Market

The recent headlines might paint a picture of a bursting Canadian housing bubble, but let’s dig a bit deeper. Here’s another perspective:

Cooling Market, Not Crash: Yes, prices are down from their February 2022 peak, but they’re still comparable to September 2021. This suggests a correction, not a dramatic collapse.

Regional Variations: The story isn’t uniform. Calgary and Quebec City are hitting record highs, indicating strong local markets. While Toronto and Vancouver might be experiencing a cool-down, it doesn’t represent the entire country.

Inventory Rise: Increased listings are a positive sign. It suggests a return to a more balanced market where buyers have more options and sellers might need to be more competitive.

Spring Dud? Maybe Not: Spring sales might not have been record-breaking, but a slight decline after a period of exuberance is natural.

Interest Rate Impact: The Bank of Canada’s recent rate cut could signal a shift that could eventually stabilize the market.

I never thought that. LOL

I live in the Midwest and the price of houses have barely kept up with inflation.

As a matter of fact, up until covid, the house I had lived in for 18 years had required just as much maintenance work that was equal to the price appreciation of about $120k.

2 new roofs (one was covered by hail insurance), new HVAC, replacing carpet every 5 to 8 years. refinishing the hardwood every 5 years. Replanting or reseeding grass. Fixing water leaks. Replacing 14 windows. Refinishing the kitchen cabinets. Replacing the garage door. 2 water heaters replacements. Soft water machine yearly maintenance. Painting the outside of the house and many other miscellaneous items.

I bought the house when it was 5 years old. A lot of expensive stuff needs to be replaced starting when a house reaches the 12 to 15 year mark.

Change the 2nd home sales from Capital gains to ordinary income and the Treasury could reap a windfall. That kind of thinking worked great in California when the government increased the percentage on the upper tax brackets; nobody noticed it and the deficit went away. Seriously, is some Airbnb or whatever 2nd property owner even going to dare to speak up or be heard if they do. Don’t feed that tired old BS of the Realtors that rental or whatever housing will disappear, somebody will be living in it.

By definition capital gain is not income, and 2nd home capital investment is typically made with after-tax funds. Especially onerous is capital gain on cottage property, which is often passed down to the next generation with no funds changing hands but which attracts capital gains.

We have been seriously brainwashed even considering capital gains as a legitimate revenue source for the government. Ironically, it’s not a huge source of tax revenue, but is purely punitive for the individual.

What makes it “illegitimate”? the fact that it’s the law legitimizes it.

Are we supposed to cry for children of affluent parents being taxed when they get a windfall vacation property inheritance?? There’s always a few choices to handle it:

1. Pay from savings and/or rest of inheritance

2. Get a mortgage

3. Sell the property

If this is “not a big source of tax revenue” then it should be trivial for heirs to handle the cost.

All markets, including RE have multiple macro/micro inputs that influence buying or selling. We’ve experienced similar things here in Germany/Europe since the GFC of 2008/9 when zirp interested rates

(ie unlimited money printing) by EU CB’s) to avoid a deflationary depression. Our interest rates in the EU are still far lower than the

US/Canadian market. My question would be has the prices of

tangible assets gone up, or had the values of the currencies go

down due to money printing? It seems rather obvious that INFLATION

is a tax caused by too much money (debt/printing) in circulation causes

price inflation, ie rising prices. My second question is give the global

debt, as well as the US borrowing another USD 1,000,000,000,000 Trillion

every 100 days DOES THIS WHOLE thing end up in a 1929 debt default, or DEPRESSION, or does it go the way of 1923 Weimar hyper-inflation (the

currency (which is not money, it’s debt) becomes worthless and results

in an economic collapse? Any of your thought would be helpful. It would appear a nice ending is not in the cards???

logic would assume it ends in one of the two which both equal in a collapse. My guess is the Fed/Washington just changes the game… money is simply allotted and people are for all intents and purposes slaves as freedom as we’ve known it will be a thing of the past. This in fact is already happening through inflation which is nothing more than wealth transfer, making your productivity worth-less. Debt is slavery. You will work very hard and be compensated for only what they deem appropriate, fluctuating on a daily basis for the common good. Digitized transactions in a communistic format under their total control.

Summer will be another leg down in all Canadian RE markets. Multi family will be punished the most as rates make them impossible to pencil. The great reckoning is now upon us.

It’s a bit ironic reading all the housing bubble headlines when you live in the hottest real estate market in the country (Nashua-Manchester did it again in April). Admittedly the Canadian market at large fundamentally is much more bubbalicious despite some regional markets remaining afloat.

Have to wonder if foreign investors have bailed out of the Canadian market and have shifted their focus to the US where home prices have been more resilient. I do suspect some of the spring strength in prices we’ve seen domestically will fizzle through summer. Even in the greater Boston area, it seems demand is quickly softening. Higher for longer rates wants to deflate…

The Chinese only buy where prices are highest and taxes especially property taxes are lowest.

While there is certainly a possibility of housing declines in the USA and Canada that would be noticable (across the board), it is unlikely the declines will be too significant. The amount of cash pumped into the market over the early 2020’s means roughly 160% of the M1 cash in 2019 existed in 2022. A $300,000 house in 2019 should have been $480,000 by 2022. Add in the other QE like government debt growth, creating more cash and cash-equivalents to circulate and you went from (US) $22.7T in 2019 to $33.2T in 2023. Based upon all that federal easing, a house which was $300,000 in 2019 should be $618,766.52 at the end of 2023. Anything less than that, and real GDP shrunk (which it did).

Thanks Wolf. FYI anyone interested in Toronto GTA specifically Rob pushed his weekly Monday updated on X (link below). FWIW I live in west GTA. In my immediate neighborhood I have definitely seen an increase in listings. Seems the small/mid-sized renovated or not renovated houses have been selling. Larger ones 3k+ sq ft sitting longer. This could end up being like the 90’s for us where prices were flat for a decade *shrug*

Rob’s data GTA…

https://x.com/rob_siglio/status/1802715374611202421

Hamilton/Burlington way down; a lot of those buyers were Toronto buyers willing to commute to ‘save’ money by buying in outlying communities and not just H&B. But H&B are a nightmare commute from Toronto, even more so lately, as if it could get worse. Add in gas prices and you lose.

In neighborhoods in Toronto there are anomalous results; a lot of houses are still going hundreds of thousands over list (and not low-ball lists).

Condos not a good market except one I watch down by the beach in our neighborhood; 1200 – 1500 ft have had sales lately going 300K+ over, which hadn’t usually happened – they were already fairly pricey. Foreign buyers? Condos that size at that price would look like gifts to them. Also, for decades, one or two kid ‘students’ could always be found living in fairly luxurious properties. A recent example was a student in a luxury apartment with a Rolls Royce, a Bentley, and a Ferrari in the basement.

It’s also interesting how the TO market has changed over time – when I was in the biz for a while all the listings used to show whether a house was all-brick construction. All non-brick, even brick-front houses were rather harshly called ‘junk’ properties and it was even difficult and pricier to finance them. For years the construction designation hasn’t appeared and the junk properties after being tarted up start at over a million.

My Mom lives in Ennisclare (condo complex on Lake Ontario) in Bronte. It’s basically God’s Waiting Room and there’s a steady turnover as the elderly move themselves in after selling their single family homes and are moved out (one way or another) — hence constant work for renovation crews. It’s in fairly high demand due to the rapidly aging demographics.

Bigger picture the structural headwinds against residential real estate are high — prices were already much in need of adjustment and we’re only partway through approximately a 5 year process of renewals which are going to be painful. Either these are going to result in selling pressure or demand destruction in the rest of the economy as mortgage holders are forced to spend an increasing percentage of their income on mortgage payments.