The low point was in September. The Fed faces a scenario of re-accelerating inflation amid a retightening labor market.

By Wolf Richter for WOLF STREET.

The Fed has cited the underlying dynamics of the labor market that were deteriorating through September as one of the reasons for its rate cuts. But since September, these dynamics of the labor market, and other metrics of the labor market, have U-Turned, with the labor market solid and tightening just a tad, while inflation has been re-accelerating since July. And these underlying dynamics are further backing the Fed’s pivot to wait-and-see:

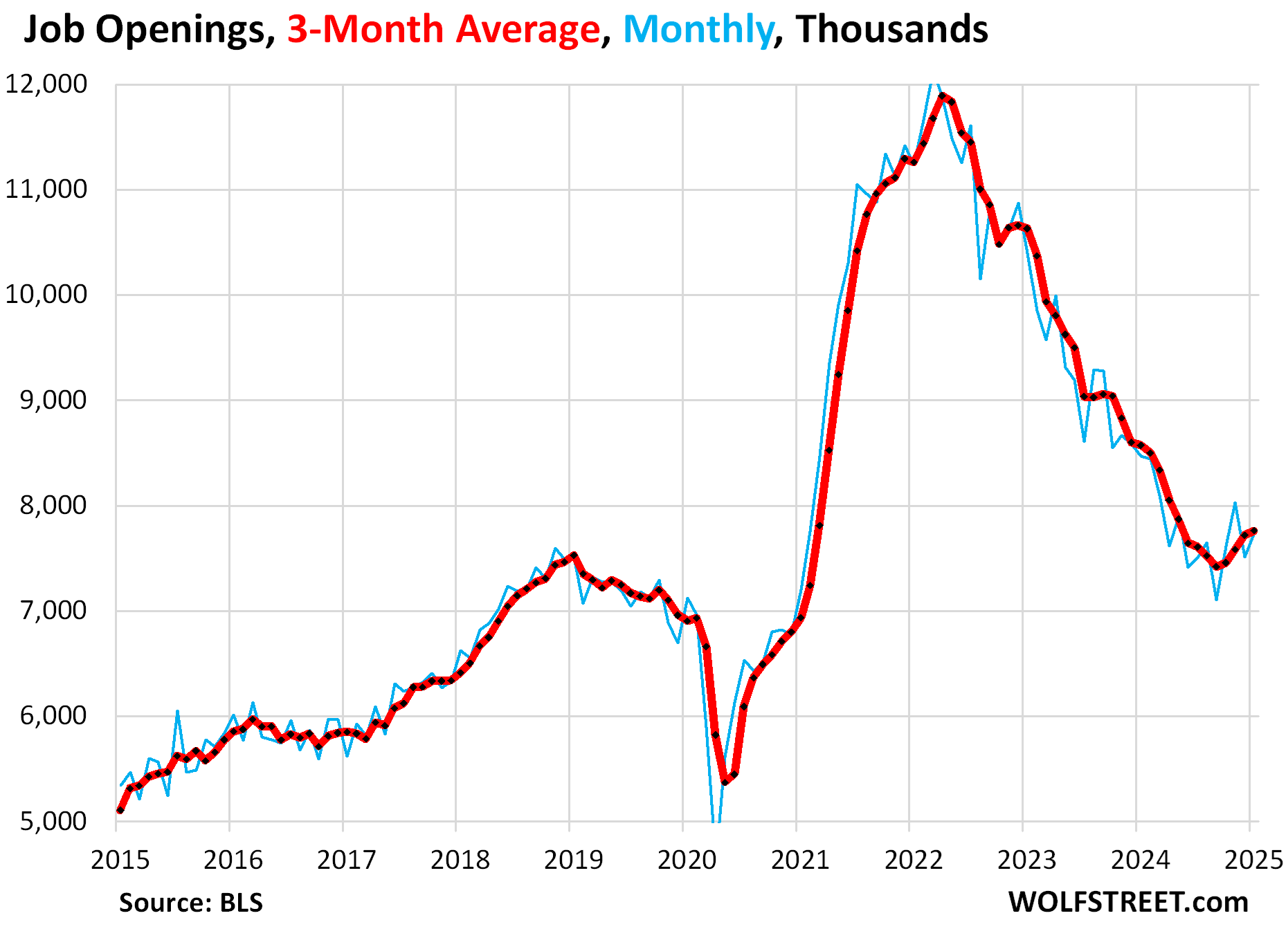

On a month-to-month and on a three-month average basis, all metrics today tightened up further: Job openings rose, with the three-month average reaching the highest level since May. Quits jumped. Hires rose to the most since July. And layoffs and discharges dropped sharply from already relatively low levels.

The triangular relationship in job openings, quits, and hires shows the churn in the labor market. This churn went haywire during the pandemic, as workers quit in huge numbers to get a better job somewhere else, even jumping to other industries. These quits left gigantic numbers of job openings behind, creating gigantic numbers of hires to fill those openings. The entire labor market got reshuffled and many people ended up with better jobs, better working conditions, higher pay, often in other industries.

Then came the corporate crackdown on the churn with announcements of massive layoff in their global workforce starting in 2022 to scare the bejesus out of workers. Only a portion of these announcements actually happened in the US, while these companies were still hiring at the same time. For companies, the pandemic churn had been costly, in terms of lost productivity and higher wages and all the expenses and inefficiencies associated with onboarding lots of workers. And they put a stop to it by scaring people into not quitting – and also by paying them more and trying to hang on to them in other ways.

Workers settled in and stopped quitting. Quits plunged to very low levels, leaving companies with far fewer job openings to fill, and far fewer hires to fill those job openings. So job openings and hires followed quits down. This is the triangular relationship between quits, job openings, and hires that describes churn in the labor market.

Job openings rose by 232,000 – nearly all in the private sector, with federal, state, and local governments combined just adding 3,000 openings – to 7.74 million in January, seasonally adjusted. The low point was in September with 7.10 million openings (blue in the chart below).

This data from the Job Openings and Labor Turnover Survey (JOLTS) by the Bureau of Labor Statistics today is based on surveys of about 21,000 work locations, and not on online job postings.

The three-month average job openings rose for the fourth month in a row from the low point in September. But even the September low point was still above the prior historic high point in late 2018 (red).

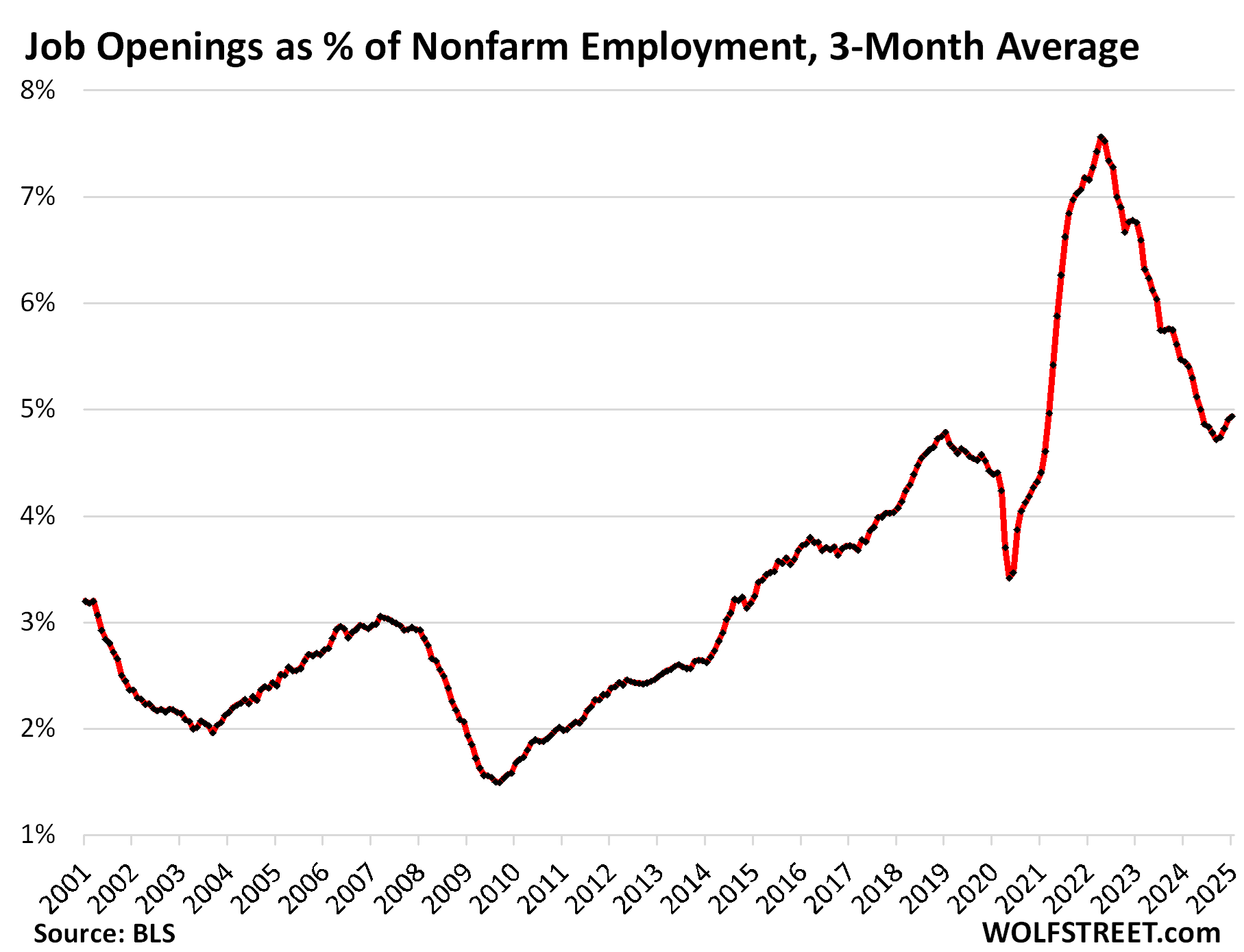

Job openings as percent of nonfarm payrolls ticked up for the fourth month in a row, to 4.93% of nonfarm payrolls, on a three-month average basis. This shows that the labor market is still historically tight, though not nearly as tight as it had been during the period of labor shortages and maximum churn of the pandemic.

During the employment crisis of the Great Recession, that ratio plunged to 1.5%:

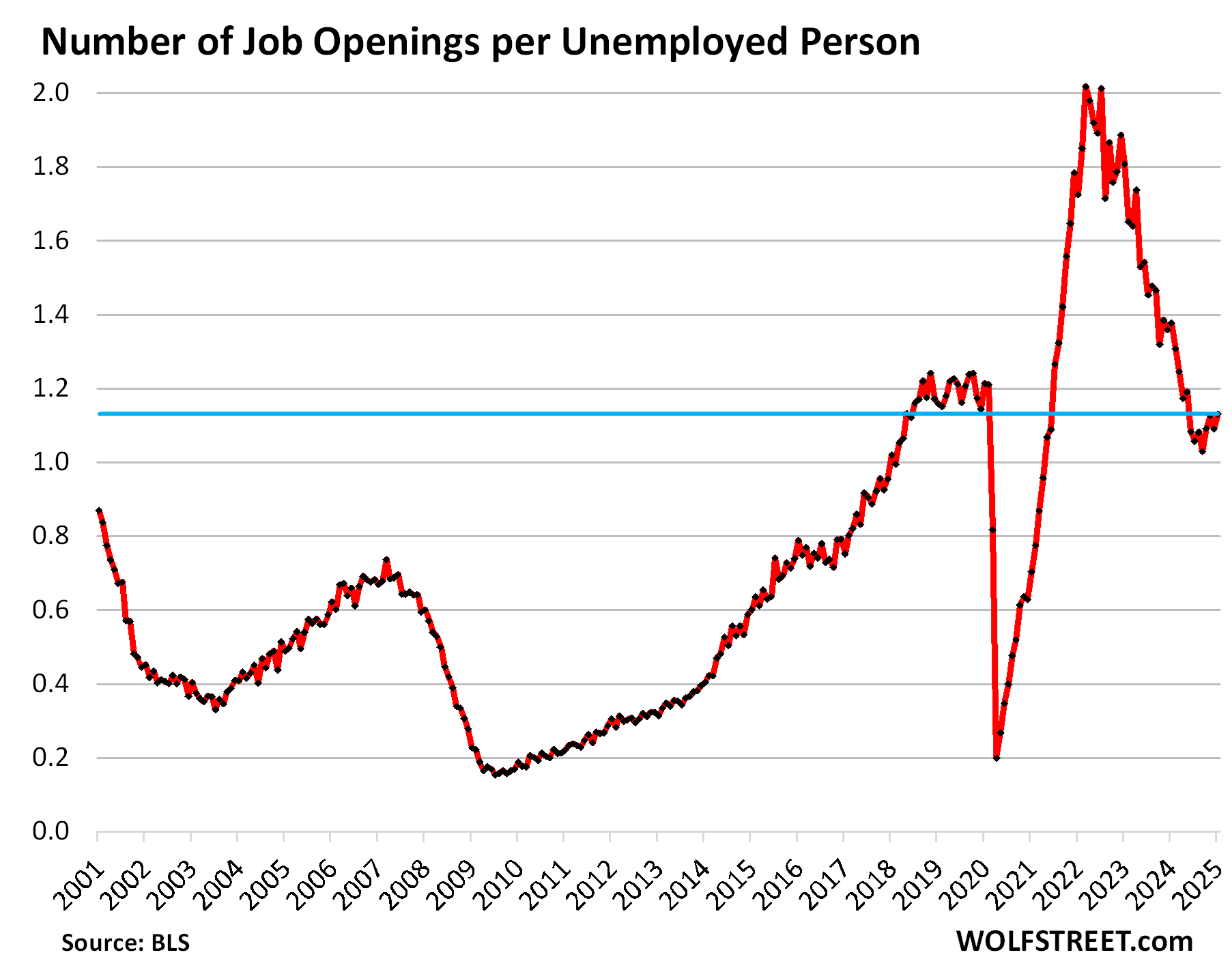

The figure Powell cites a lot: The number of job openings per unemployed person ticked up to 1.13 job openings for each person who was unemployed and looking for a job during the reference period (7.74 million openings for 6.85 million unemployed).

The ratio is the highest since May. The low point had been in September, when the Fed got spooked. It shows a relatively tight labor market compared.

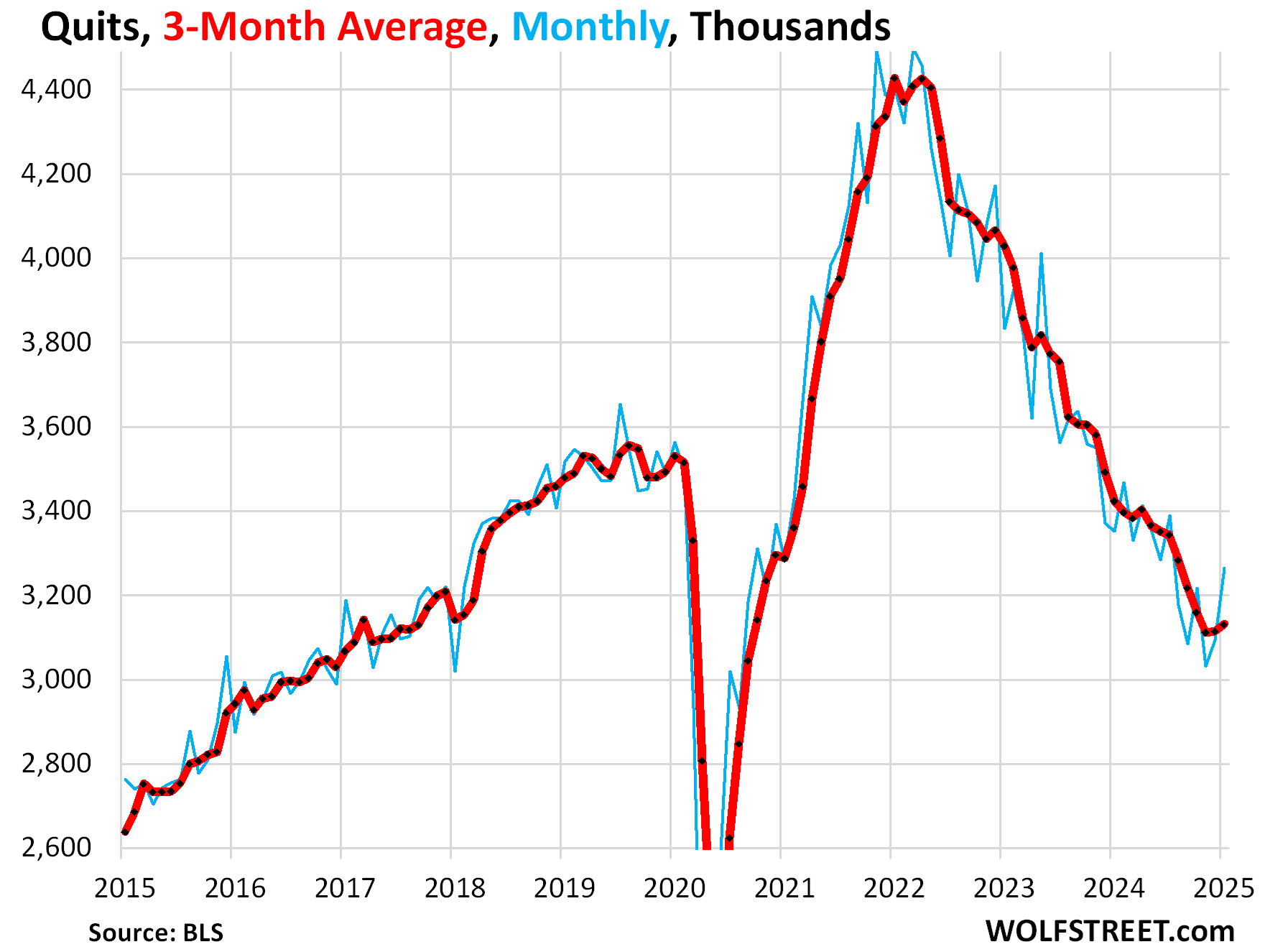

Quits jumped by 171,000 to 3.27 million, the highest since July.

The three-month average rose to 3.13 million, the highest since October, and the second month in a row of increases.

Quits are an indication of how emboldened employees feel to quit a job and go for a better job. Retirements, deaths, etc. are not included in “quits” but in “other separations.”

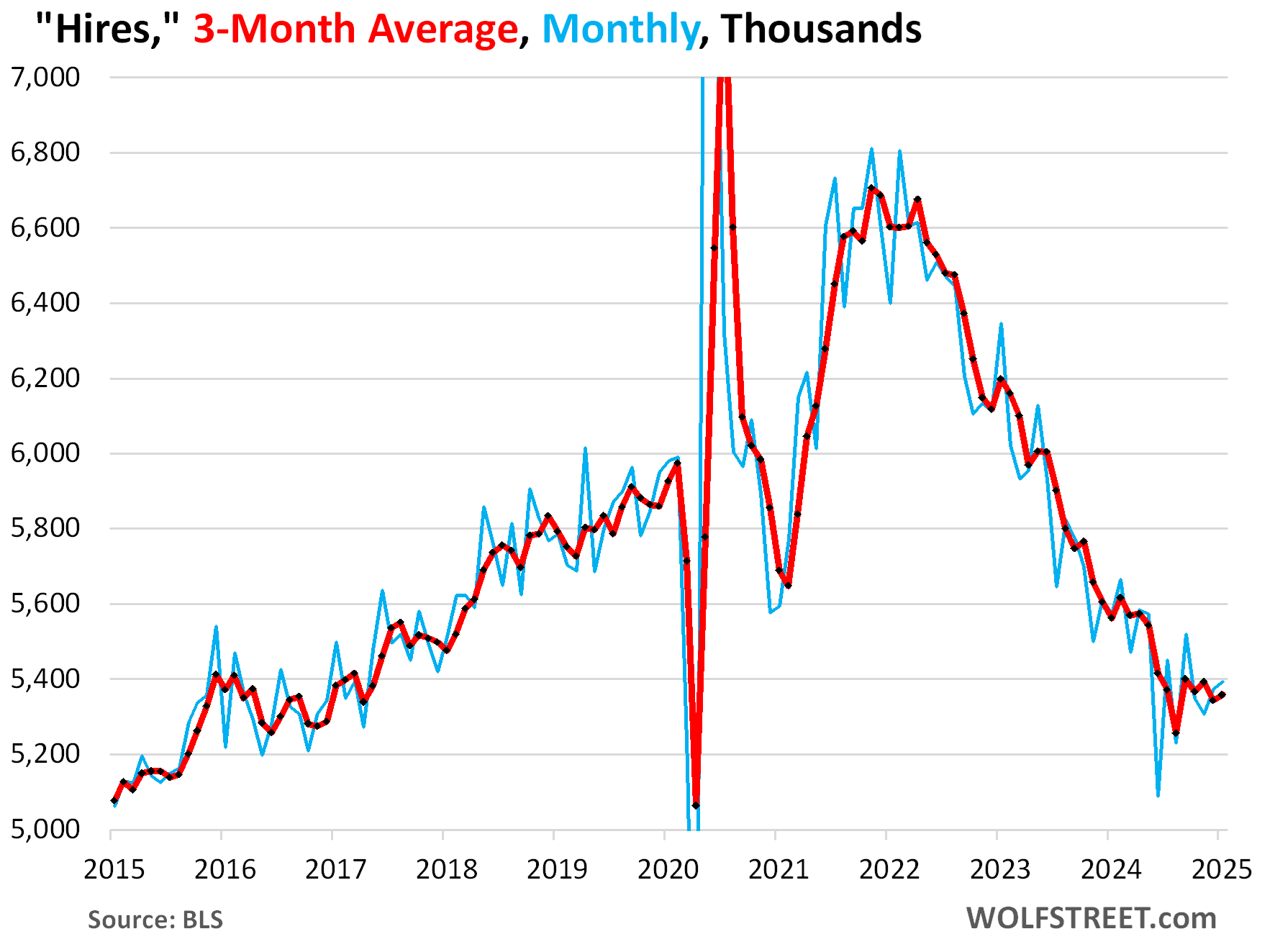

Hires rose by 19,000 to 5.39 million in January, seasonally adjusted. The low point was in June (5.09 million hires). The three-month average ticked up to 5.36 million.

Hiring is very seasonal. Not seasonally adjusted, hires spiked by 1.32 million to 5.26 million.

When the churn began to cool in the second half of 2022, fewer workers quit, so fewer jobs were left behind, and job openings plunged, and fewer people needed to be hired to fill those left-behind openings, and so hires plunged along with it.

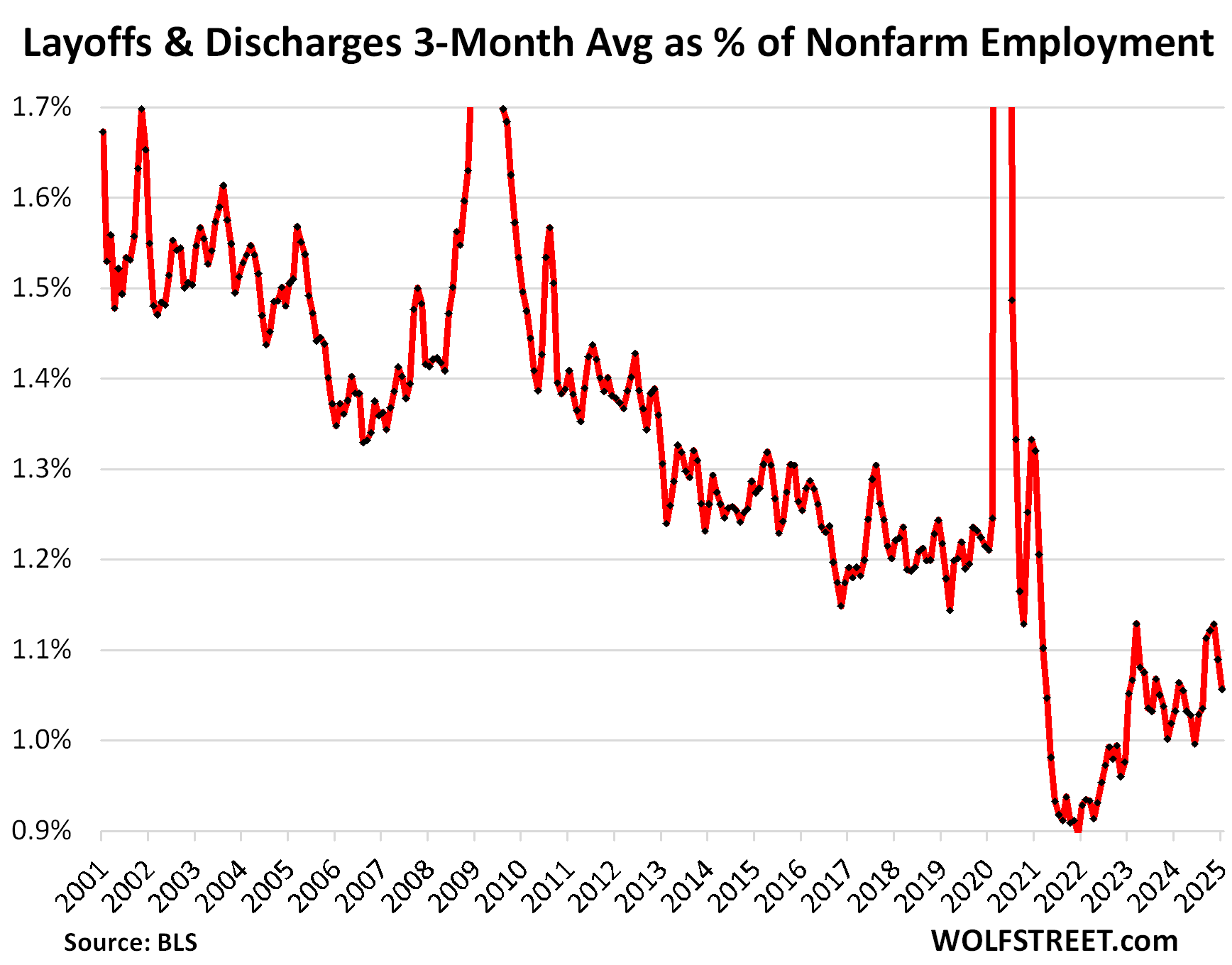

Layoffs and discharges dropped to 1.63 million in January, the lowest since June.

The three-month average dropped for the second month in a row, to 1.68 million, the lowest since August.

They have “normalized” to the low end of the range during the Good Times before the pandemic. Getting fired is a standard feature in the American workplace even during the best times.

Layoffs and involuntary discharges include people getting fired with or without cause. It does not include retirements, deaths, etc., which are in the category of “other separations.”

Layoffs and discharges as percent of nonfarm payrolls fell to 1.06%, the lowest since August, well below any time during the pre-pandemic years in the JOLTS data going back to 2001.

This ratio accounts for growing employment over the years and is the better metric to look at for a long-term view.

It shows that, compared to the size of nonfarm employment, layoffs and discharges are historically low, as employers are hanging on to their workers.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

MW: Dow sheds nearly 480 points as U.S. stocks book more losses on tariff uncertainty

DJIA -1.14% SPX -0.76% COMP -0.18%

“Job openings rose by 232,000 – nearly all in the private sector, with federal, state, and local governments combined just adding 3,000 openings….”

Very nice.

“The Fed faces a scenario of re-accelerating inflation amid a retightening labor market.”

Inflation must be re-accelerating again. Food prices are out of sight. Just bought a 1.52 OZ tube of Wasabi at my local Giant grocery store. Price $3.29. Provides 7 servings of 1 tsp. What a deal.

What we need now is more tariffs, more taxes, and tighter money.

Terrific irony! 🤣 Metaphor? Metaview?

Labor theory is either inscrutable or I dunno. That chart begs a Marxist reading. Are people working hard to obsolesce labor? I just subscribed and got a mug. First time commenter too. I believe people have quit for reasons that don’t appear in the article. Seems like an existential thing. Does pandemic mean ” existential thing”?

R&T: Ford Recalls Wide Swath of Its Lineup to Fix Incorrect Repairs for Prior Recalls. Vehicles impacted include the Mach-E, Escape, Maverick, F-150, Super Duty, Expedition, Corsair, and Navigator.

Something seems to be awry inside Ford Motor Company’s recall and service departments. The brand has issued six recall notices spread across several of its popular product lines over the past two weeks — all to fix issues that were addressed incorrectly in response to previous recall notices with the National Highway Traffic Safety Administration. Here’s what we know about the situation so far.

Just last week, Road & Track shared news of a double recall for the Ford Maverick covering the 2022 and 2023 model years, which impacted hybrid and non-hybrid variants. While those recalls impacted 933 and 141 trucks, respectively, Ford is now requesting a much larger number of its machines return to the dealer. More specifically, the automaker has extended recalls for the 2021-2022 F-150, 2022 Expedition, 2022 Escape, 2022 F-250/F-350/F-450/F-550 Super Dutys, 2021-2022 Mustang Mach-E, 2022 Escape, 2021-2022 Lincoln Corsair, and 2022 Lincoln Navigator.

All of the impacted vehicles were previously repaired by Ford for previous recalls, but the automaker states the repairs were incorrect on each filing. The largest of the recalls impacts the trucks and full-size SUVs, owing to a software issue preventing proper trailer braking. Some 10,627 units are caught up in that recall alone. Others are much smaller, including a whopping two-unit recall for the Maverick due to some module faults.

Still waiting for the punch line…

All the big banks are writing about a coming Trumpcession due to tariffs and cutting down the federal workforce.

I know you have written that the layoffs in the federal government are small potatoes, but I haven’t seen you really write anything on the current news involving tariffs.

Would be interested to read your thoughts.

You missed them, it seems. Here are all my articles going back years on tariffs:

https://wolfstreet.com/tag/tariffs/

Here are the recent articles on tariffs and why they’re needed:

https://wolfstreet.com/2025/03/06/explosion-of-imports-causes-trade-deficit-to-spike-by-96-in-january-yoy-on-tariff-front-running/

https://wolfstreet.com/2025/02/05/trade-deficit-in-goods-worsens-to-all-time-worst-in-2024-small-surplus-in-services-improves-overall-trade-deficit-worsens-by-17/

https://wolfstreet.com/2025/02/03/what-trumps-tariffs-did-last-time-2018-2019-had-no-impact-on-inflation-doubled-receipts-from-customs-duties-and-hit-stocks/

https://wolfstreet.com/2025/01/13/some-basics-about-u-s-tariffs-and-what-trumps-new-economic-team-said-about-tariffs/

The federal government IS the main employer here in the Swamp. These layoffs ARE a big deal here. The fallout is just being felt. Everyone knows someone who has lost their job. It hasn’t affected property values yet.

It was a transitory spooked.

So, Donnie ‘buys’ a new Tesla, and E-Long verbalizes his pipe dream of doubling Tesla production in the next two years. Wishful thinking, E-Long. The dynamic duo. Note -Donnie doesn’t know how to drive – especially a Tesla.

I don’t think Trump even has a driver’s license. He never needed one. Why would he bother?

These 2 knuckleheads. One is the richest man in the world who would still be worth 200 billion if Tesla went to zero. Trump, just one a historic victory to become the President for the 2nd time despite being a convicted felon. I’ll bet every time he gets in that motorcade or steps into a luxury plane or helicopter he wishes he would have learned how to drive. As for E Long , it’s definitely, wishful thinking for a guy who is catching rockets ,putting a chip in someone’s brain that allows them to move things and a host of other over the top accomplishments. What a dreamer

More recalls for the Maverick? My 2022 Hybrid Maverick has been in the dealer twice already for recalls. Good thing it gets fantastic milage to offset the hassle.

It might be interesting to put together a single combined chart of the three – hires, quits, openings, each having a color line or bars…

Fascinating data points that look positive for a soft landing. What a confusing time. Some data points look like we are headed for a recession, others look bullish.

I still think we see a deflationary recession in housing, stocks, and crypto.

Thanks for the data points and your commentary, Wolf!