A new role for the SPR. It wasn’t designed for that.

By Wolf Richter for WOLF STREET.

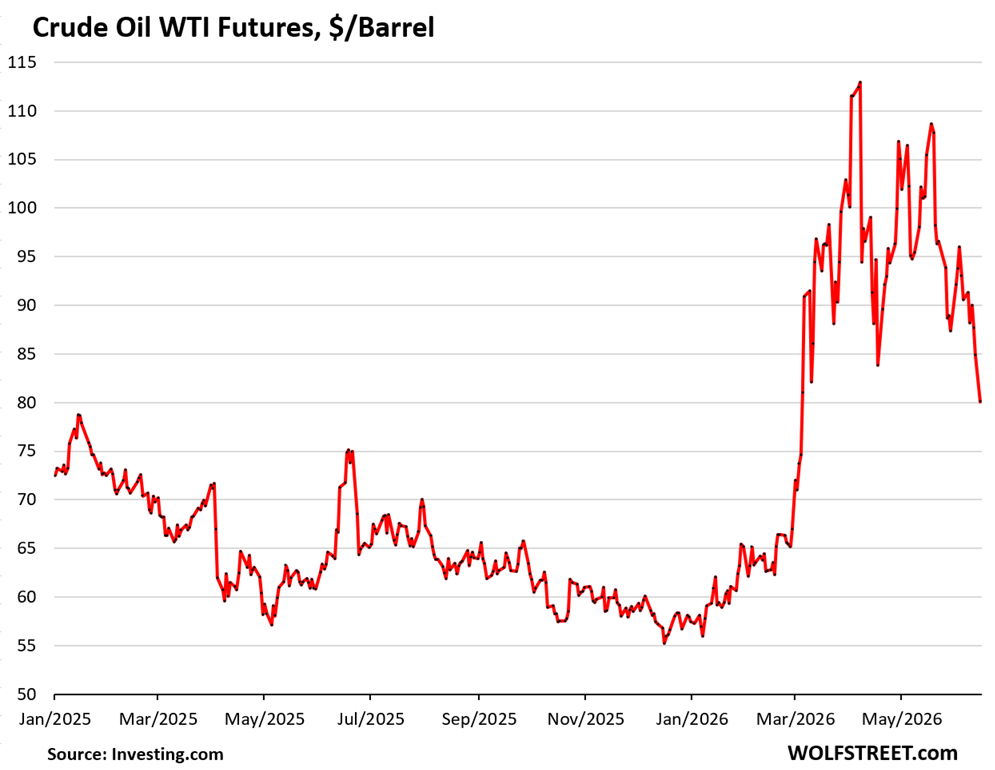

Crude oil prices continued their plunge after a memorandum of understanding was agreed to between the US and Iran over the weekend. Both sides said that the Strait of Hormuz would reopen as soon as the MOU is signed.

Futures for the benchmark grade West Texas Intermedia (WTI) fell by nearly 5% today to about $80 per barrel at the moment, the lowest since March 5, and down by about $35 from the peak during the Iran-war spike on April 6.

Prices between $60 to $80 per barrel are where US frackers can operate profitably without causing further demand destruction that would come on top of the long-running structural demand decline for gasoline in the US.

This structural demand decline for gasoline in the US has been going on for years, as motor vehicles became more efficient, as hybrid power trains and EVs gained market penetration, and as per-capita miles driven has been dropping for over two decades, reducing US gasoline consumption in 2025 to where it had first been in 2003.

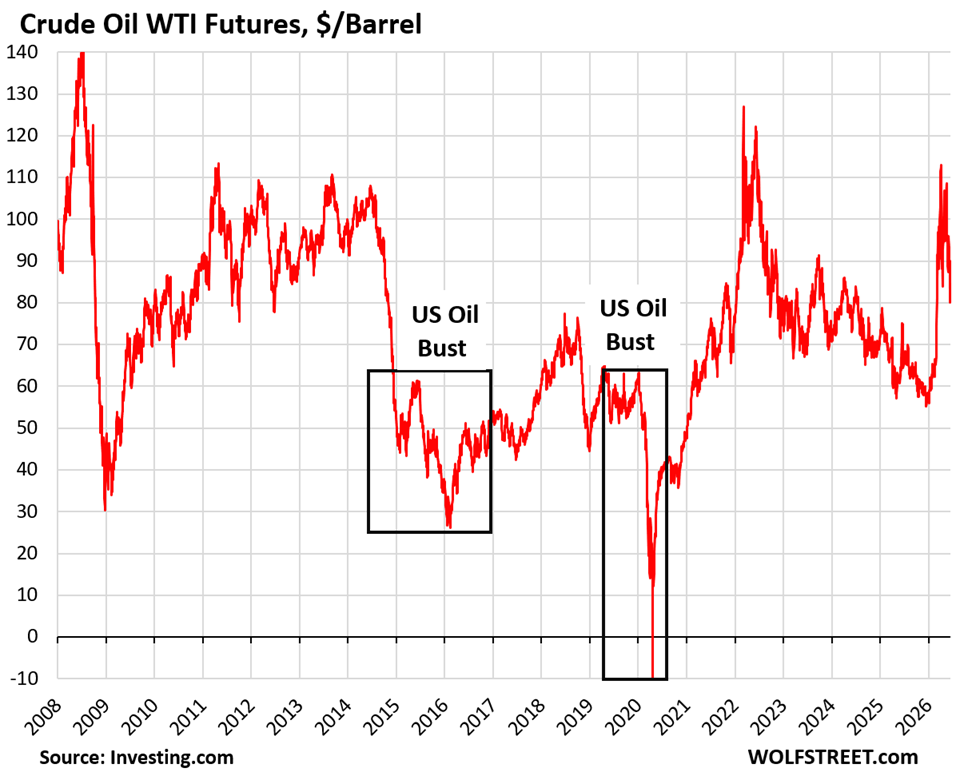

When overproduction and the subsequent oil glut hit US producers and prices plunged, it triggered two oil busts – or maybe two waves of the same oil bust – over the past decade, during which hundreds of frackers filed for bankruptcy.

Despite substantial overall inflation over the past 20 years, the worst crude oil price spike occurred in 2008, when WTI briefly kissed $150. The price spikes in 2022 and this year never reached those levels.

Government uses the SPR as cudgel to beat down Oil-Price Mania.

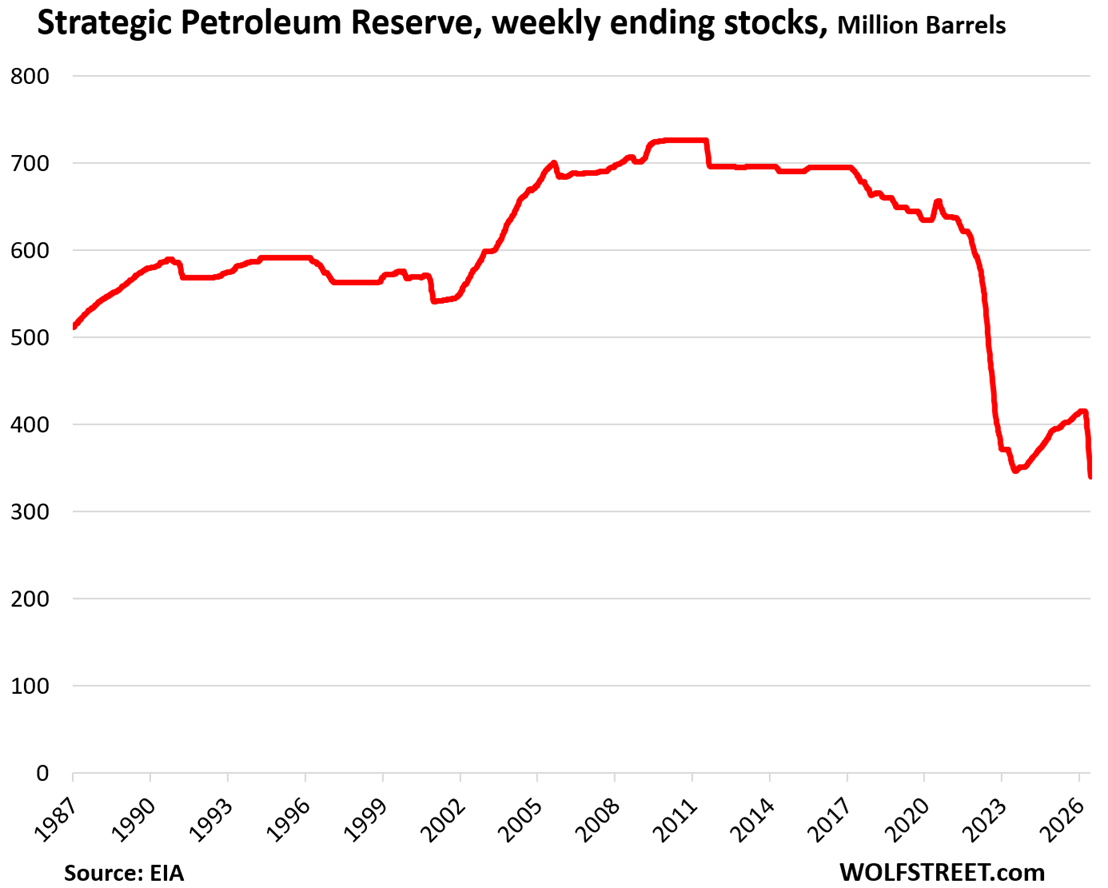

One of the tools that the US government and other major governments around the world, including China, now have to put a lid on price spikes are their Strategic Petroleum Reserves.

The SPR in the US was created in response to two massive oil shocks in the 1970s when the US was dependent on crude oil imports from OPEC. The idea was to give the US some reserves that, in addition to its own production, would prevent the US from running out of oil for a period that would be long enough to line up alternatives.

But about two decades ago, fracking in the US became a major force. Over the years, the US became the largest natural gas producer in the world, the largest crude oil and petroleum products producer in the world, the largest exporter of LNG in the world, a major exporter of crude oil and of value-added petroleum products, including gasoline, diesel, and jet fuel – even refineries in California. It became a net exporter of crude oil and petroleum products, importing crude oil to refine and exporting the value-added product, such as gasoline, diesel, and jet fuel. And over 60% of the crude oil that US refineries do import comes from Canada and Mexico (see charts at the bottom of this article, and analysis and charter here).

This raised the question about 10 years ago what to do with the SPR since it wasn’t needed anymore to avoid shortages. Starting in 2017, under the Trump administration, the US began slowly draining the SPR for that reason. Between 2017 and the end of 2020, the SPR was reduced by 8.2%.

Then came the war in Ukraine when oil prices spiked in the US, as US production was by then connected via massive exports to global markets. And this changed the purpose of the SPR from preventing shortages to beating down speculative manias. The Biden administration dumped large amounts of crude oil on the market to push prices back down. After prices had calmed down, the SPR was being slowly refilled at lower prices than the prices at which the crude oil had been sold during the release. Sell high, buy low.

The Trump administration has been doing the same during the Iran war. The SPR dumped large amounts of crude oil on the market very quickly, putting a lid on the speculative price spike in the US, and pushing prices back down.

The level of SPR level has now dropped by 75 million barrels, to 340 million barrels, as of June 12. More than the entire amount that had been refilled between mid-2023 and early March 2026 has been dumped back on the market in three months.

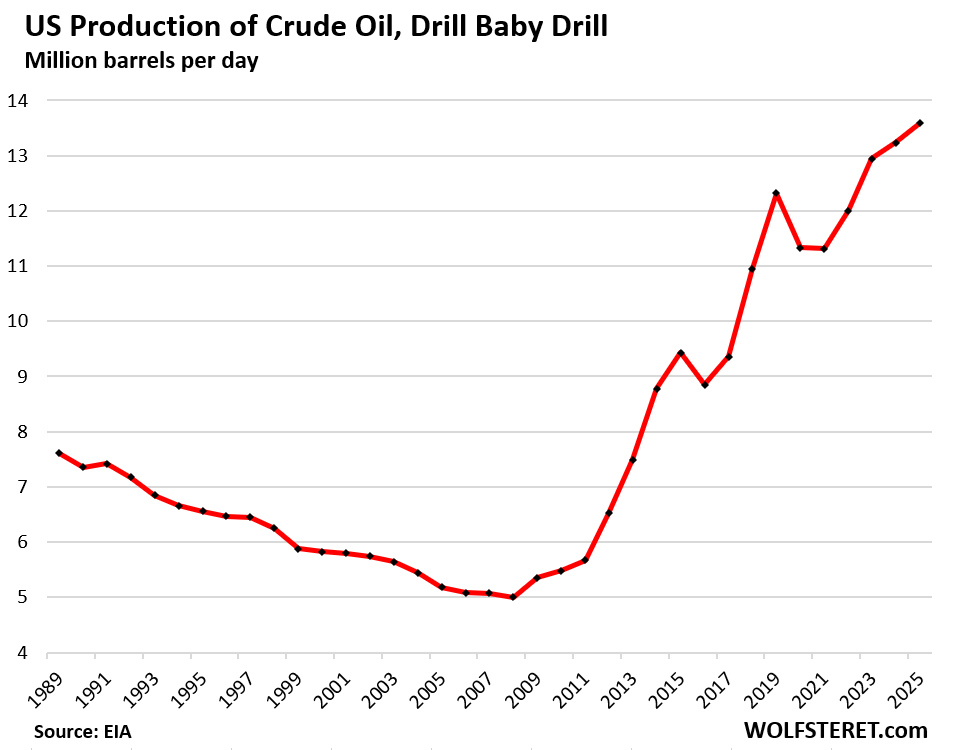

Summary of US production, imports, and exports.

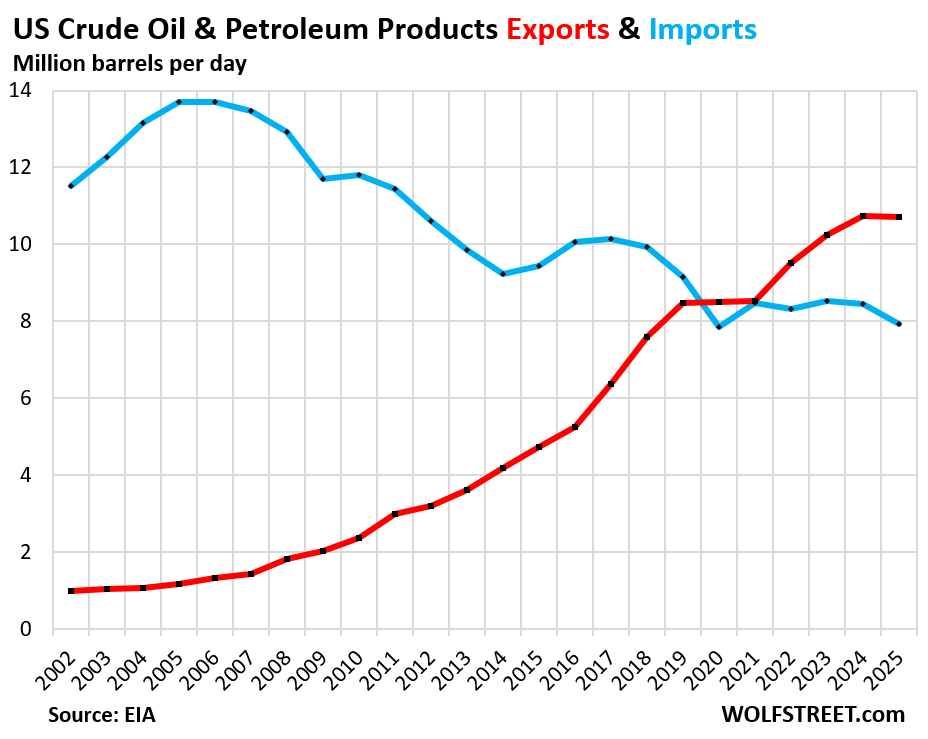

US crude oil production has risen by 172% since 2008, to a record 13.6 million barrels per day (MMb/d) in 2025.

The two kinks in the chart in 2016 and then again in 2020-2021 were the results of the two Oil Busts when overproduction caused the price of US crude oil to collapse. As hundreds of oil-and-gas drillers filed for bankruptcy, production declined, which allowed the price to rise again into a survivable range.

Net exports (exports minus imports) surged in 2025, as exports of crude oil and petroleum products were roughly stable at 10.7 MMb/d and up by 495% from 2008 (red), while imports declined to 7.9 MMb/d, after having peaked at nearly 13.7 MMb/d in 2005 (blue).

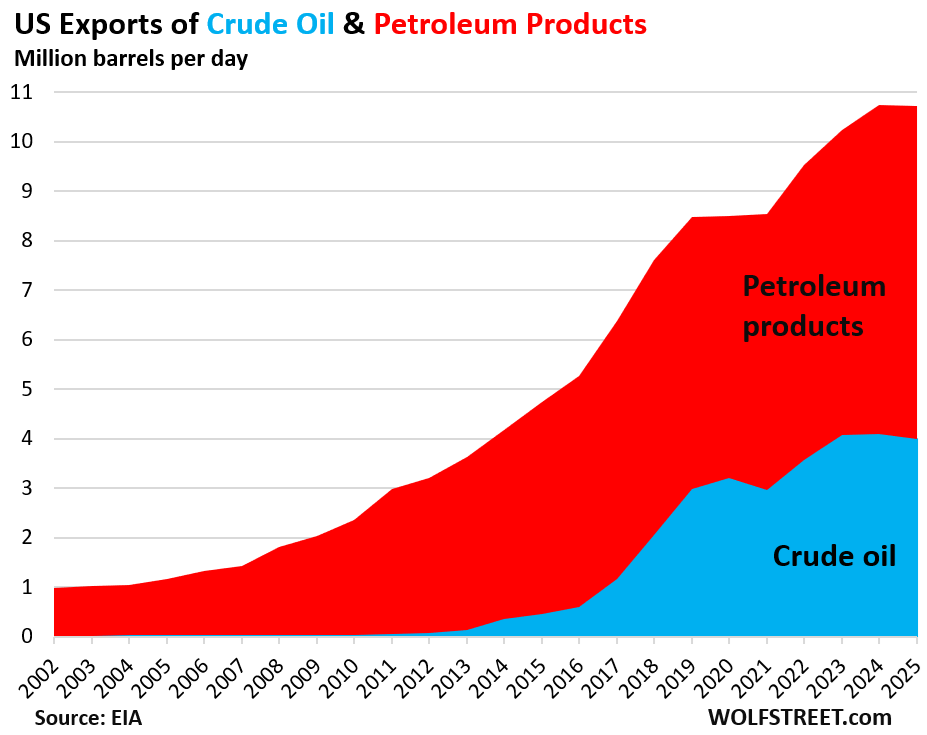

Exports of petroleum products rose to 6.73 MMb/d, accounting for 63% of total exports. Exports of crude oil declined by 2.9% in 2025, to 3.99 MMb/d, accounting for 37% of exports.

Importing crude oil, refining it, and exporting the value-added product is a huge profitable business for refiners in the US.

Even refineries in “oil island” California are doing it. With local demand on a long downward trend, what else should refineries do with their refining capacity? California produces some crude oil. Refineries also buy some from Alaska and foreign countries, and some from US producing regions brought in by oil train. California refineries then export some of the gasoline, distillate, and jet fuel mostly to Latin America. West Coast (PADD 5) refiners exported 0.41 MMb/d to other countries in 2025.

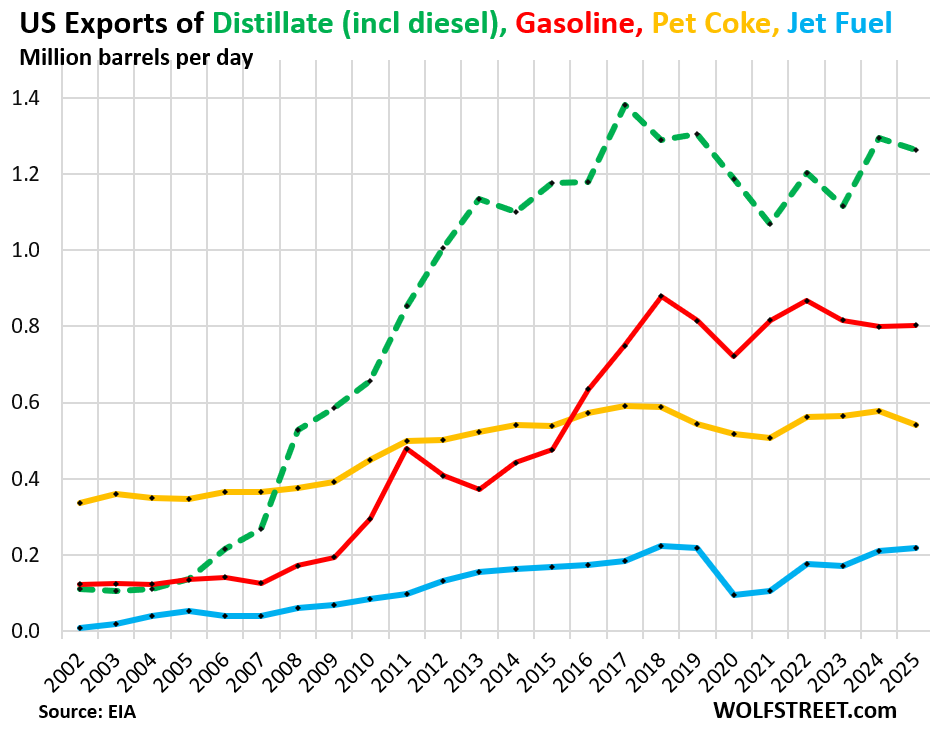

Among the many petroleum products that the US exports are finished petroleum products, the largest categories of which are by export volume:

- Distillate: 1.26 MMb/d

- Gasoline: 0.80 MMb/d

- Petroleum coke: 0.54 MMb/d

- Jet fuel: 0.22 MMb/d

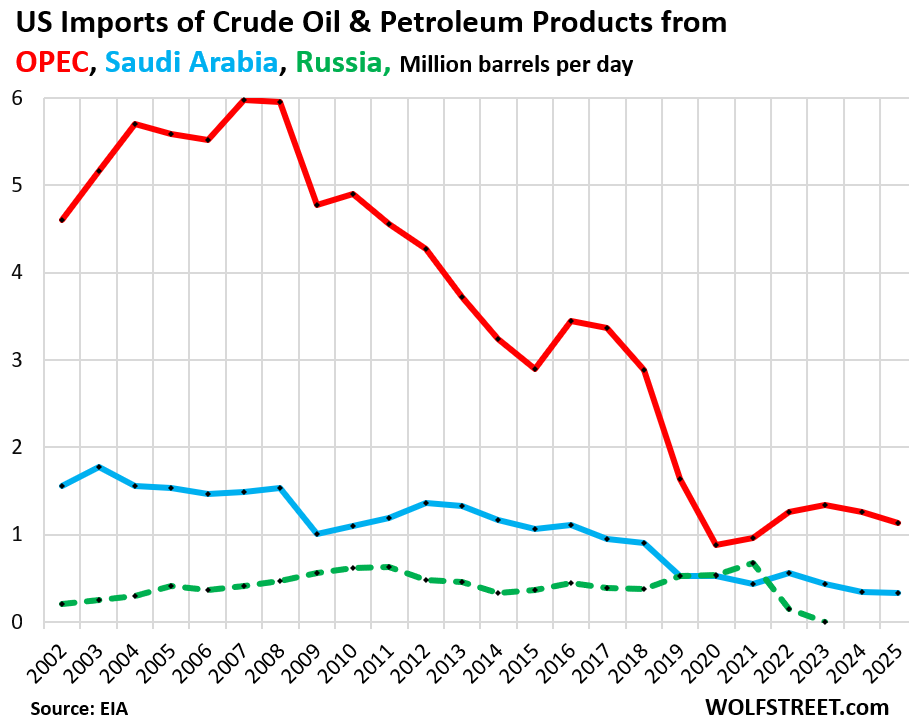

Imports from countries other than Canada and Mexico: Over 60% of the crude oil that the US imported in 2025 came from Canada and Mexico. Refiners purchase crude oil wherever it’s the best deal. Russia, never a large source, fell off the list in 2022. OPEC only provided 14% of US imports. Saudi Arabia is shown separately here, but is also included in OPEC imports.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The definition of success in commotidity intervention has long been defined as making a profit.

An easy profit was available for last few months and a couple of years after Russia’s SMO. Sell the spot, buy forward.

The gap between spot oil and 6 month forward oil has been $50-60 – incredibly easy money if your job is to sit on oil and wait until short term shortages.

Conventionally this is very sound intervention again.

Don’t blame them for the politics

A wolf masterpiece of documenting the facts which often, like now, diverge from the official narrative.

The disconnect is between the futures price for a barrel of oil which has been falling all the while

Trumps War has supposedly cut the supply of crude substantially yet the price is falling. An irrationality that is obviously outside the range of expected responses

We have a “Federal Reserve” to stabilize the cost of money…why not another “Federal Reserve” to stabilize the cost of oil?

Beating down oil and interest rates to hand in hand

imagery and politics

Oh I know this one.. they can’t print oil. Or they would stabilize it to $500 per barrel.

Speaking of prices…..

“Even if you don’t need more stuff, these early Prime Day deals are too good to pass up”

Am I the only one who is bothered by this kind of “thinking”.

Some are of the opinion that the last thing that the Federal Reserve bank thinks about is what is the best policy to ensure a stable economic life for the majority of us every day people.

The American carcase being consumed by the hyena is not a pretty site,

Granted, China cut its oil imports by 40% and there was a massive rationing across gulf-dependent economies, which had an effect on oil prices as well. Plus re-routing, etc.

The physical mechanics of oil reservoirs is that if you drain them past a certain point, you damage their storage capacity and ability to draw down further. There is a limit to how much you can take from the SPR. We’re approaching that point.

You only have to drain them enough to break the speculative mania, and they did that weeks ago.

Arkham…every storage technology has some limitation/associated costs. Can you be more specific on the limitations of underground salt caverns used for the SPR and how those compare to other oil storage technologies?

On to the next crisis! With fervent abandon!

Yee-Hawwww

This one is far from over…:)

This one was over two weeks ago. Manias are like a fever. Once they break, things calm down.

Why are you so certain that the price action is just a speculative mania?

There has been a very real supply disruption that will not be resolved simply by ending the Iran war, bc that doesnt fix the infrastructure or cover the 3 weeks that tankers spend in transit to re-establish a steady supply flow to Asia.

These charts are US specific, but the oil market and prices are global. There is very real demand destruction and shortages in net import countries, so why are high prices in a net export country a sign of price mania rather than a reflection of increasing export demand?

Your export chart also ends before the start of the war in Iran, making it of limited use for the analysis you are doing.

Patrick….what is your breakdown on demand destruction? (vis causes and trends)

Asian energy prices (oil, gas, coal) have been increasing since 2022 – the Ukraine/Russia crisis. A similar situation applies in Europe.

Is the claim you make vis Asian costs uniform across all countries?

That is an odd take. Nothing has changed, the straight is closed and reserves are falling.

Also all recessions have had recoveries along the way before going down further, kind of debunks that idea.

N Caverly

“Also all recessions have had recoveries along the way before going down further, kind of debunks that idea.”

Huh? What does this have to do with a recession?

I have no idea why so many people here are agitating for $150 oil. It’s half that right now. And the US is awash in it.

Well a recession is def apart of the conversation with oil prices, I’d say they’re kind of inversely intertwined in this scenario. If gas were to jump to $150 as people are talking, recession seems unavoidable.

I don’t necessarily want $150 oil, but the idea that everything is hunky dory doesn’t make sense. Its current price is irrelevant, assets are mispriced all the time. Saying the US is awash with oil doesn’t changed anything.

Again the reality is the Straight is currently closed and world reserves(including the US) are falling off quick, seems less than optimal.

N Caverly

WTI is around $76 not $150. I know it hurts, but that’s where it is, and for the reasons I indicated.

Strategic Petroleum RESERVE

Federal RESERVE

both empty? Is this like “deferred asset” classification of paper losses?

Stock Market must go up!!!!!!!!!!!!!

You would think because of the high prices in CA that refiners would want to sell in-state.

Yet if the profit margins are the same as anywhere else in the country then the only logical conclusion is that the difference in high prices stem from Sacramento taxation policies.

That would be a incomplete conclusion. California does obviously have high taxes but it also creates a unique blend and this can be more costly, especially when there are refinery issues. So it is more costly to refine as well.

On a percentage basis, how much do state taxes, CARBOB policy requirements and aging/drawing down refinery capacity impact the cost per gallon in CA on a percentage basis?

Not disputing your factual points. It amounts to “it costs more to produce a gallon of gasoline in CA”.

It also costs more to “sell” a gallon of gas in CA with one of the highest minimum wages “and” the highest costs of running a business and keeping the state happy (it is bad running an apartment I can only imagine how bad it must be running a gas station dealing with even more California government entities.

Well, at least California has the countries best infrastructure:)

Apartment…no argument from me.

Just an aesthetic observation absent factual support: I have lived in CA several times in different decades during my life. Truly, the coastline/N CA number among the most beautiful places I have been privileged to live in.

Visited Monterey last year (drove there from CO)….San Diego a few years ago. Every appearance of infrastructure decay. Conversations with locals – not academic surveys – suggest that generations who have inherited much of the wealth have no clue what they are doing.

I’ll stop here since the subject is too close to home for many.

High prices doesn’t mean high margins. The high prices in California are driven by the cost structure, not demand.

Great summation and informative.

Definitely calming down, Definitely. For now and probably for a while more. However, the supply issues in all sectors will take many months to seek out normal across the world market and who knows if the crack war negotiators can actually bargain anything meaningful and lasting beyond a 1 pager? (sarcasm intended). I think prices will come down more still, steadily down with stability, but there will be future tolls/fees and gamesmanship with 20% of the total supply as the ME adapts to the new reality. This might add a few bucks per bbl, overall.

The multi national oil companies are there for one reason, make profits. They are not our friends. The only thing worse would be Govt in total control of energy as opposed to ‘the market’. How to limit this industry’s political influence is a problem. Their product powers our lives and their influence permeates everything.

I read last week that Feb 28th did more to promote alternative energy than any lobbying could have ever hoped for. Lots of plan B planning going on.

Countries will fill their empty SPRs, before the next event ==> higher oil prices. Hormuz opening can send oil price higher until Q4. Thereafter higher LNG prices during winter 2027.

Yes, this.^

It is going to take weeks to months just to get the oil moving again, and months to years to bring all the lost capacity back online, if ever.

Plus, all those empty strategic reserves will now have to be refilled, and whatever country is desperate enough to pay whatever it takes to fill theirs first, is the country that will be setting the marginal price of oil.

In short, oil will be supply-constrained and oil prices will be high for the foreseeable future, probably forever. Yes, there will be demand destruction, but that sanitized term belies the reality of what’s going on. “Demand destruction” of this magnitude means people starving in the Third World, riots, wars, failed states, and governments collapsing.

The fallout from the idiotic Iran War is just starting.

You act like the Hormuz Crisis is something new that emerged from Epic Fury. Threats to Hormuz have been a deep concern to the oil markets and the US Navy since the Iranian Revolution. As it turns out, the disruption due to Iran’s theats to and attacks on neutral shipping have been far less severe than anyone knowledgeable had any reason to hope. (For illustartion, compare oil prices now to where they were 4 years ago or 18 years ago. Iran’s little “side hustle” was far from the worst oil crisis this decade let alone this century.)

Yea…I tend to discount this sort of predictive hysteria when it does not account for the history of the industry under examination. Market price is the result of multiple factors of which non-stochastic political black swans such as the recent Iranian nuclear intransigence (SoH threats) are only one component.

O&G CAPEX by the majors has been on a long-run decline since at least 2013 – that may change soon in the off-shore sector.

It’s routine to note that refinery capacity growth in the US has been slow. The mismatch in oil types and US refinery input requirements has also been documented.

Production of new bulk transport shipping ship has been in decline for at least a decade mostly tracing to big losses following over-investment/major losses a decade or so ago. New ship building capacity growth has been slow – recall that is one area Trump declared a security interest for the US.

Pozar has written extensively on the predicted impacts of sanctions on shipping routes, shipping capacity mismatches to the rerouting and cost/insurance impacts.

In the bigger picture, how can Iran have such a visceral impact on market prices but no claims about the four year Ukraine/Russia war?

If SPR management is an issue, why no comments on the drawdown (i.e., requirement to refill) used to combat inflating gasoline at the pump prices circa 2020-2024?

There are studies asserting that, in the US, the exploitation of low cost fracking reserves has reached its endpoint – the marginal cost is going up.

It’s a complicated market – and not the ideal free market. There is, obviously, oligopoly powers (capital flows), but if there is any industry has been heavily influenced by political events, policies, anti-free market gov’t intrusions – it is O&G!

Along with all of this have been gov’t policies favoring Climate Change driven national energy policies – EU being the obvious example. Without dipping one’s toes into these ideological waters, one has to concede that these policies have directly influenced O&G markets.

Though a couple comments touched on the FED, I think the best point of the article is government interference on price of oil! Just inappropriate.. Same as government created FED interference with price of money. Also inappropriate. Creating winners and losers. Let the market allocate capital, assets, prices.

“Let the market allocate capital, assets, prices.”

You’re not wrong but it’s also the government doing the bombing. That kinda defeats the point of the “invisible hand.”

Obviously one doesn’t excuse the other, it’s all bad! May we be lucky enough to get an ever slight hedge to further inflation and expansion of the money supply.

The “bombing” is not an O&G driven event – however much cynics think that is the case.

This was a nuclear weapons security issue. One that is not over.

Iran is a bad actor and has been for decades. Been there many times with access to real time information – Iran is a major exporter of global violence. Iranian resources and personnel have directly impacted security globally to include state sponsored terrorism. One can debate the exigencies of the moment, Israeli rhetoric and the morality of war as a solution…but the emerging growth of the Abraham Accords is an indicator that other ME countries are seeing a path forward that contains Iran.

Iran was “weeks away from building nuclear weapons” for many, many decades according to world leaders who had other interests (coincidentally, i am sure) in dropping bombs on Iran.

Strange how, despite the many “soft on Iran” administrations we’ve seen since the 90s, each of which went years at a time without blowing anything up, those scary nuclear weapons never actually appeared.

A cynical person might begin to suspect the “weeks away from nukes” bogeyman was never actually hiding under the bed, despite what our parents claimed.

Whoops…operator error. Apologies WOlf. Please delete my double post.

The problem now of course is the fact that the largest “private” companies are now dependent on government contracts. Also, can we claw back all the bailout cash as well?

Wake the hell up, K-street is the problem, with the financial “services” sector leading the capital mis-allocation and mal-investment.

It’s been this way for 40+ years.

Please, this has been the case for 50+ years. Tell me, how many “private” companies do we have now that are 100% dependent on government contracts or that would have been long dead if it wasn’t for taxpayer-funded bailouts?

Shut down K-street before you do anything else. At the heart of all the problems is the fact that your representation is fully OWNED and they have been rewarding bad behavior for 50+ years. Their response to the great financial fraud should have made that clear to everyone.

The US SPR plunged between 2020 and 2023 to 350 Mb. It bounced back up to a higher low, before dropping to an all time low last week. SPR low reached a climax selling in June. It can stay in a trading range for years. When Iran deal with its 60 days option and 60 days extension expire, with their unrealized promises from both sides, bad things can happen: Bab al Mandab and the Hormuz straits can be closed in unison…

What we are learning now is that Hormuz was never “closed”.

Tanker operators were initially spooked by Iranian threats and attacks but after the initial shock, began to move oil again. The support of the US Navy was a big part of this. But an underappreciated piece of the puzzle was discounting by the gulf exporters. Iraq openly offered a $30+ per barrel discount for tankers willing to load at Basra in May. That’s $60 million in extra profit for a VLCC willing to exit Hormuz without Iranian “permission”. (Other exporters also likely made secret discount deals but this is speculation.)

Money talks!

Man, oil transit has only been a small fraction of what it used to be. And now with the MOU, it is still a fraction.

Trump is lying left and right.

With the risk of an angry Wolf, and deletion of comment, I’m going to post a little history. I’m old enough to remember the oil embargo of 1973. We had threatened to strike over a nickel an hour raise, thankfully we settled without the nickel. That October the company raised our wages by seventy cents an hour. Most thought it was an attempt to break the union. Little did we know the whole story.

On the first chart you can see the actual price of a barrel of oil. Just scroll down to the first chart. Others are inteesting but not to this note.

https://www.macrotrends.net/1369/crude-oil-price-history-chart

Above the question was ask about regulating the price of oil.

Originally there was a type of regulation by western oil companies. I believe it was even allowed/encouraged by our government. You can read a blurb under The Setup: 1970 – 1976. On the next link as you read the history.

https://priceofoil.com/articles/oil-price-history

Oil was the lubracation of the industrial revilution. Without it we would have been lost.

I wonder if the price of oil starts raising again when the intervention stops and hormus opens up. There is still a hughe supply/ demand imbalance.

This is only the story. Everywhere that had gas before the war still has gas. Lol all these people long on oil mad.

Damned good article, thank you.

The Iran war started on Feb 28. CL gap up between Feb 27 and Mar 2. CL breached Apr 17 lo @78.79. It’s in the Mar 10 fractal zone, on the way to the gap. Paper traders, in a wild short covering, can send CL up, before closing the gap.

One of the more interesting things about the past 50 years: The inflation-adjusted price of gasoline in the USA has been basically flat since the 1970s. Mostly between $2 – $4 in 2023 dollars.

The government does a very good job of ensuring stable gasoline prices, despite all the technological and market changes in the oil and gas industry.

Big price increases are political problems from voters. Big price declines are political problems from donors (oil companies and people dependent on the oil industry).

So smoothing out that price is a political priority across party lines.

And now the SPR is another very useful tool in the toolkit to manage gas prices.

Yes, gas is cheap. But if you use a lot of it, and the price goes up, like some businesses, it could hurt.

How’s the Venezuela situation going to play out. Largest reserves in the world and Trump has the cards.

Lemme guess, you’re long on crude. All mad the people paying less for gas.

Who’s “you”?

When replying, please include the screen name of the commenter you’re replying to, unless you can directly nest your reply under that commenter’s comment.

Fed day bs. SPCX mania: gap up today on lower vol. Trade at 213, at

the center of today’s bar.

The Permian has a pipeline bottleneck. The Middle East has a shipping and geopolitical bottleneck. In both places, the challenge is moving the glut to where buyers are.

“Waha has now remained in negative territory since February 4, marking 89 consecutive trading sessions below zero. That extends the gap versus the previous longest negative streak of 27 sessions in 2024.”

You’re spreading falsehoods about oil on my site to pump up the price of oil?

Waha has zero to do with crude oil in the Permian. It’s a regional natural gas pricing benchmark for natural gas produced in the Permian. The pipeline shortages concerns natural gas, not oil. The US has so much natural gas, it doesn’t know what to do with it, and the price remains at collapsed levels. LNG exports are limited by the capacity of the LNG export terminals (new ones coming on line nearly every year).

A price rise is how the market prevents a physical shortage. The SPR serves the same purpose by storing oil in amounts above what is economically efficient in order to shield the government from the economic and political consequences of geopolitical events, thereby reducing pressure to yield to the will of our enemies.

…and the SPR has a value to the US economic to smooth boom bust cycles similar to how the Farm Bill impacts US food and farming.

The buy low sell high was incorrect Wolf you forgot to add the ongoing cost of storage they sold SPR at a loss according the Dr. Anas. As a follower of his on X you and followers may want to understand the “strategic” nature of the SPR historically and it’s current implications. It is no longer as strategic. The oil business is an oligospony and it’s machinations are somewhat outside of all financial experts even the oil related ones. Your general insights are good but if you look at the track records of even the best in the business they fail to predict what is happening now or going to happen. The best insight I can provide the Wolf followers now is that the world is de-stocking hoping for lower prices later this is creating a bidless market in financial and physical. The REAL deal will be Maersk and other shippers going back into the gulf. As per Jeff Currie 60M barrels may be able to leave now but there is is no commitment for ships returning. Saudi/UAE can come online sooner but Qatar/Kuwait/Iraq longer. In terms of understanding SPR I will send you an email link.

Here is a snippet of the summary I will send:

US SPR Releases

1. Test sales

– make sure everything is functional, small amounts, coordinated with some companies

2. Congress Mandates Sales

– mandated sales since 2015 to cover cost of SPR & to renew SPR & supplement budget

– significant sizes (350M barrels in next 7-8 years)

– Biden admin has authority to time that

– still 26MB still needed to be sold (mandated)

3. Exchanges

– other issues

– congress can prevent president

4. Emergency Sales (non minimums from congress)

– major events require massive withdrawls from the SPR

A. Desert Storm 1991,

B. 2005 Hurricane Katrina

C. 2011 Arab Spring

D. Biden Withdrawl (180M largest ever)

The oil market is so complex and incredibly flexible that even the best experts like Jeff Currie might get things wrong. We are now in a massive de-stocking phase where most of the world believes the price will be cheaper later this year so both physical and paper markets are not bid. Massive disconnect. Currie estimates about 60M barrels will flow out shortly but it is all about new tankers going in – seems there is no clear understanding how that will happen. Recovery shall be quick in Saudi/UAE and now Qatar but Iraq/Kuwait not so much. We have erased about 1B barrels of production/inventory thus far. Remarkable how flexible the oil market is. If IRGC or factions decide to interrupt things we are in big trouble.

You’re forgetting about the drillers in the US. They’re unleashing a flood of production because the price is high; and they’re hedging future production at these prices. Fracking can ramp up so fast it makes your head spin. That’s why we’ve had two oil gluts over the past 12 years that caused the price of oil to collapse and sent hundreds of drillers into bankruptcy. Above $60 is the sweet spot for frackers.

FWIW as mentioned:

“The mismatch in oil types and US refinery input requirements has also been documented.”

Swapping oil produced in Mexico with US crude to satisfy the input requirements of US refineries is a bit in the weeds, but none the less a reality.

The US is a HUGE exporter of gasoline, diesel, and jet fuel to Mexico, and imports small amounts of crude oil from Mexico to refine it, and sell the product back, and has a huge trade surplus in petroleum and petroleum products with Mexico. US refineries constantly invest lots of money in new equipment to refine whatever makes them the most profit. I’m really tired have to read over and over again the same BS about US production and refining.

Oil should be so easy. just examine supply and demand. Unfortunately, producers ( private and public and government ) AND big consumers obfuscate SO EFFECTIVELY that even the analysts that bother to physically visit facilities get their forecasts wrong. And I’m not even mentioning the paid and unpaid nerds trying to calculate the ‘floating oil’ (LOL!!!). The airlines completely lost their fear of running out of jet fuel weeks ago so I’m inclined to think we have enough oil……until we don’t and that is the position that we are all in.