The effects of Tax Day. The 10-Year Treasury yield rose to 4.31%, 30-Year Treasury yield to 4.91%.

By Wolf Richter for WOLF STREET.

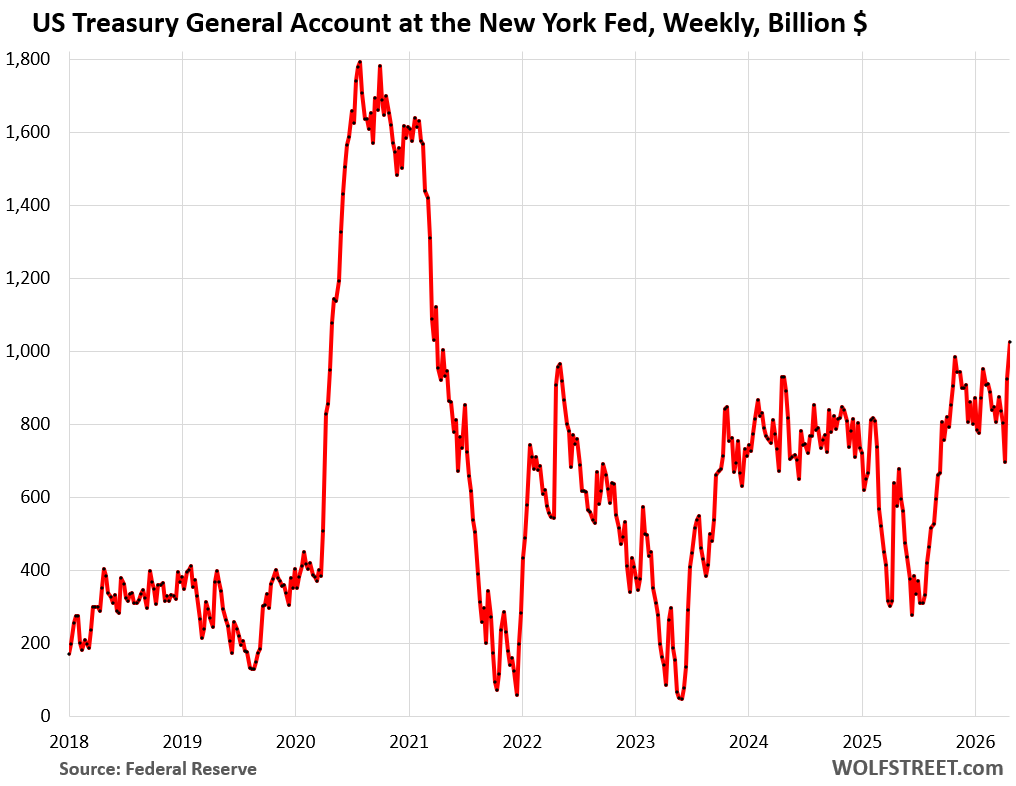

Around Tax Day, large amounts of cash from estimated quarterly taxes, capital gains taxes, and underpaid income taxes from businesses and individuals flow into the government’s coffers, and the balance of the government’s checking account, the Treasury General Account (TGA), has swollen to over $1 trillion, the highest since April 2021.

In response to this seasonal influx of cash, the Treasury Department has trimmed back the issuance of Treasury bills (terms of 4-52 weeks) in recent weeks, including this week. Trimming back the issuance of T-bills has caused the overall debt to dip below $39 trillion again, even though the outstanding balance of Treasury notes (2-10 years) and bonds (20 and 30 years) continued to grow. When this cash influx slows in May, the Treasury Department will increase the issuance of T-bills again.

The Treasury Department has increased the “desired level” of the TGA to $900 billion this spring, from $800 billion a year ago, to comfortably accommodate the huge amounts of cash flowing through that account on a daily basis, including the amounts needed to pay off the maturing debt of over $500 billion a week.

The US government sold $524 billion of Treasury securities this week, in eight auctions. Of these auction sales, $480 billion were Treasury bills, with maturities from 4 weeks to 26 weeks, most or all of them to replace maturing T-bills.

Amid this seasonal influx of cash, the Treasury Department reduced the size of three T-bill auctions (4-week, 6-week, 8-week) this week by a total of $35 billion compared to the same week in March.

| Type | Auction date | Billion $ | High Rate | Investment Rate |

| Bills 4-week | Apr-23 | 81 | 3.60% | 3.66% |

| Bills 6-week | Apr-21 | 75 | 3.61% | 3.68% |

| Bills 8-week | Apr-23 | 76 | 3.61% | 3.68% |

| Bills 13-week | Apr-20 | 95 | 3.61% | 3.69% |

| Bills 17-week | Apr-22 | 70 | 3.61% | 3.70% |

| Bills 26-week | Apr-20 | 83 | 3.59% | 3.71% |

| Bills | 480 |

“High rate” v. “Investment Rate”: The Treasury Department provides two different calculations of the yield at which T-bills were sold at auction.

T-bills are sold at a discount to face value, and at maturity, the holder gets paid face value; the difference is the interest. There are no coupon interest payments, unlike with notes and bonds. The “high rate” reflects the yield of that process.

But the fact that T-bills have no coupon interest payments makes the “high rate” calculation not comparable to Treasury notes and bonds where holders are paid interest every six months. So the Treasury Department also provides a conversion calculation of this discount yield into a yield that is equivalent to the yields of coupon securities, so that these yields can be compared, and it calls this yield the “investment rate.” Both the “high rate” and the “investment rate” are published in the auction results of T-bills.

This investment rate is higher than the “high rate” and matches fairly closely the “constant maturity yield” published for trading in the secondary market around the time of the auction.

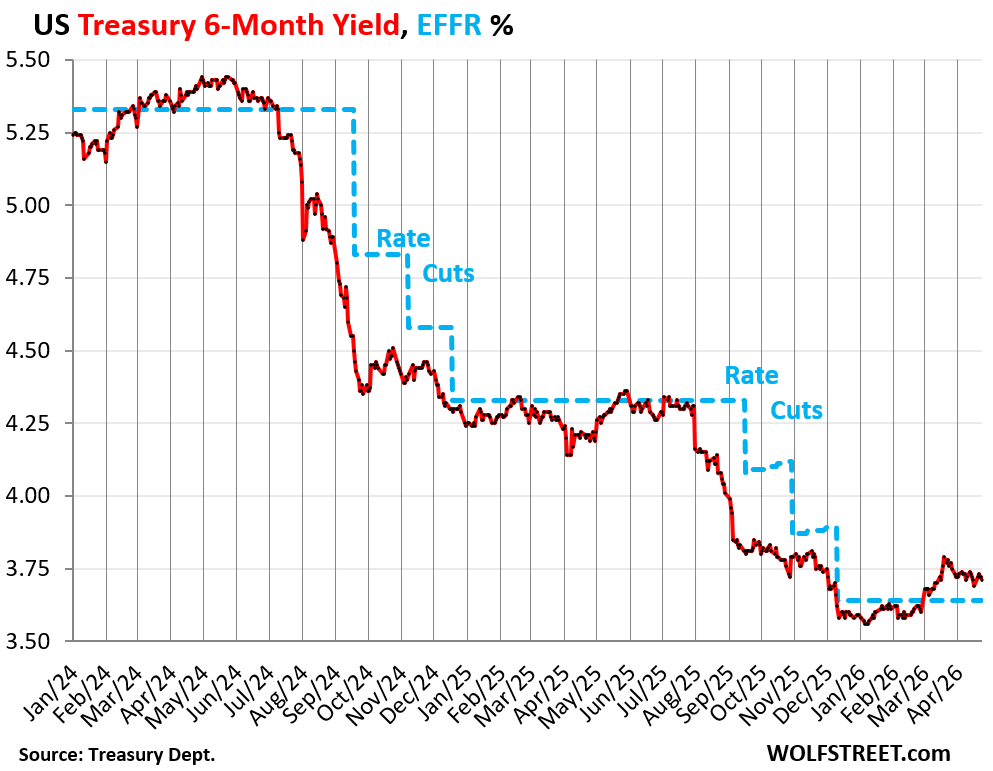

6-month T-bills, for example, sold at a “high yield” of 3.59% on April 20. But when recalculated as a coupon-equivalent “investment rate,” it was 3.71%. The auction took place in the morning of April 20. In the secondary market at the same time, the 6-month constant maturity yield was also around 3.71%.

The 6-month yield, which closed on Friday at 3.71%, is currently above the Effective Federal Funds Rate (EFFR) of 3.64%, which the Fed targets with its policy rates. This shows that the bond market sees no rate cut in the six-month window, but maybe a slight chance of a rate hike.

But inflation rates are on track to surpass T-bill yields, or already surpassed T-bill yields, depending on the inflation measure. But T-bills are bracketed by the Fed’s five policy rates and react to those policy rates and the expected policy rates – they don’t react to inflation fears.

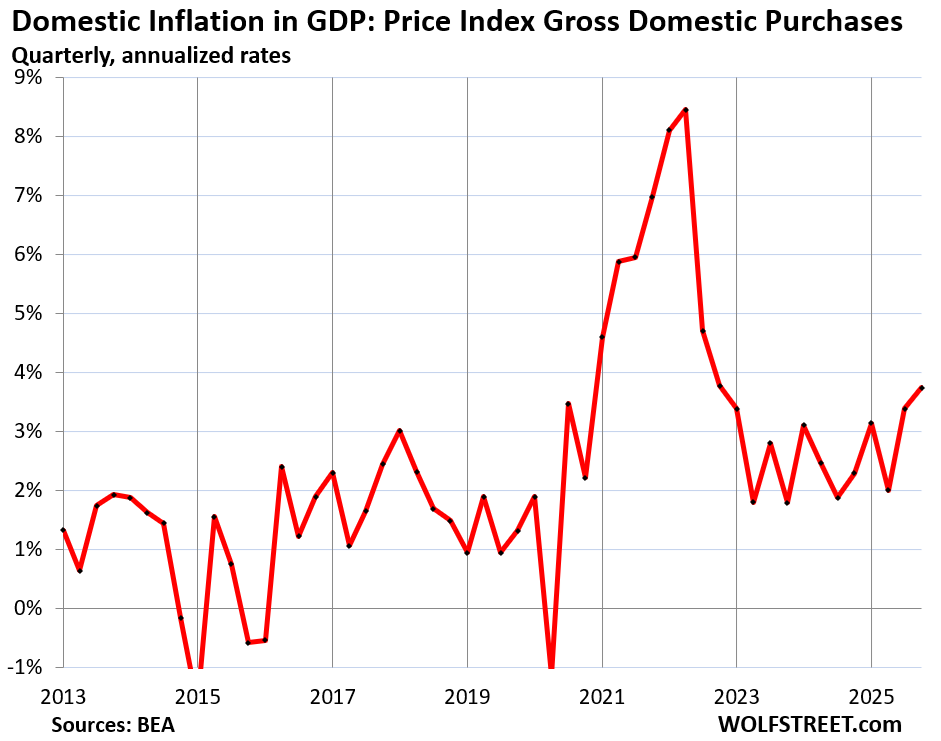

The PCE price index, which the Fed favors for tracking consumer price inflation, has moved close to 3.0% year-over-year through February, not yet including the energy price spike in March.

But the last three month-to-month readings through February were all near or above 4% annualized. The March readings, to be released next week, will spike from there due to the fuel price spike. These readings are already above T-bill yields.

The Price Index for Gross Domestic Purchases, an inflation index for the broad domestic economy that tracks inflation facing consumers, businesses, and governments and reflects inflation in GDP, accelerated to 3.1% year-over-year in Q4, not including the energy price spike in Q1.

But it accelerated in Q4 from Q3 to 3.75% annualized, so already above T-bill yields.

The Q1 measure of this inflation index will be released next week, and it will contain the fuel price spike across the economy in March, which will likely push that inflation rate further above T-bill yields.

The US government also sold $44 billion of Treasury notes and bonds this week, spread over two auctions: 5-Year Treasury Inflation Protected Securities (TIPS) and 20-year Treasury bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| TIPS 5-year | Apr-23 | 29 | *1.37% |

| Bonds 20-year | Apr-22 | 15 | 4.88% |

| Notes & bonds | 44 |

*TIPS yield is paid on top of the inflation protection that TIPS holders receive. This inflation protection is based on CPI and is added to the principal, and so the principal of the TIPS grows over time with CPI. The interest rate (the percentage is fixed for the term of the TIPS) is applied to the entire principal, including the inflation protection. As the principal grows over time with CPI, the interest payments increase, though the interest rate remains fixed.

In a year when CPI averages 5.0%, these 5-year TIPS sold at auction on April 23 with a yield of 1.37% will earn 6.37% combined. The 5.0% of inflation protection will be added to the principal, and the 1.37% interest will be paid on the total of the original principal plus the accumulated inflation protection.

TIPS have nasty tax consequences though: the inflation protection counts as taxable income. Each year, the portion of inflation protection that was added that year will show up on the 1099-INT for that year — so TIPS trigger a tax liability every year on the inflation protection that won’t actually be paid until maturity. Keeping TIPS in a tax-deferred account, such as an IRA, avoids that issue.

Brutal bond math: The $15 billion of 20-year bonds, with a coupon interest of 4.625%, were sold on Wednesday at 96.74 cents on the dollar to get to a yield of 4.88%, which is where the yield in the secondary market was running at the time. On Friday, the 20-year yield in the secondary market also closed at 4.88%.

But there won’t be any 20-year bonds maturing until 2040 because the Treasury Department halted the issuance of 20-year bonds in 1986 and restarted issuance in 2020, and the entire $15 billion of 20-year Treasury bonds sold this week add to the overall debt as no 20-year bonds matured.

This is how the long-term debt grows. 20-year bonds are new, and every single issue adds the entire amount to the long-term debt.

Similarly, with longer-term notes and 30-year bonds when they’re sold at auction: The maturing issues are much smaller than the current auction sales, and the difference adds to the long-term debt. Even if the government doesn’t further increase the size of the note and bond auctions, the outstanding balance of notes and bonds will continue to grow as much bigger new issues replace the maturing issues.

In recent months, for example, 10-year notes were sold in issues of $45-$50 billion at the monthly auctions, replacing maturing notes issued 10 years ago, of $20-$25 billion. So at each 10-year Treasury auction, the outstanding balance of 10-year Treasuries increased by about $20 billion.

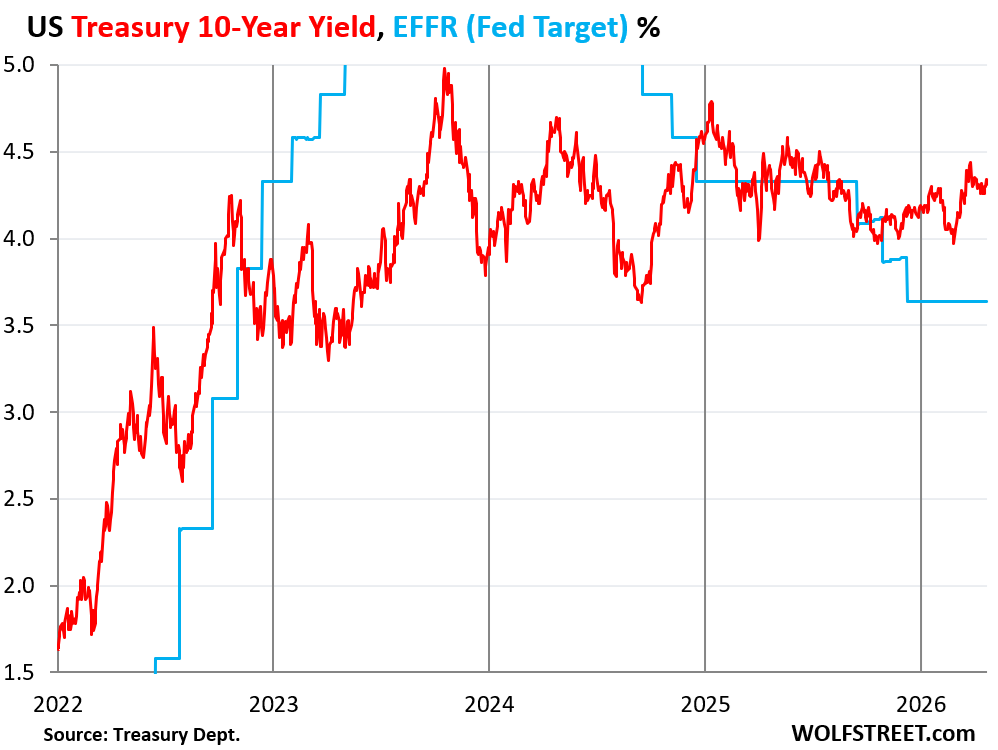

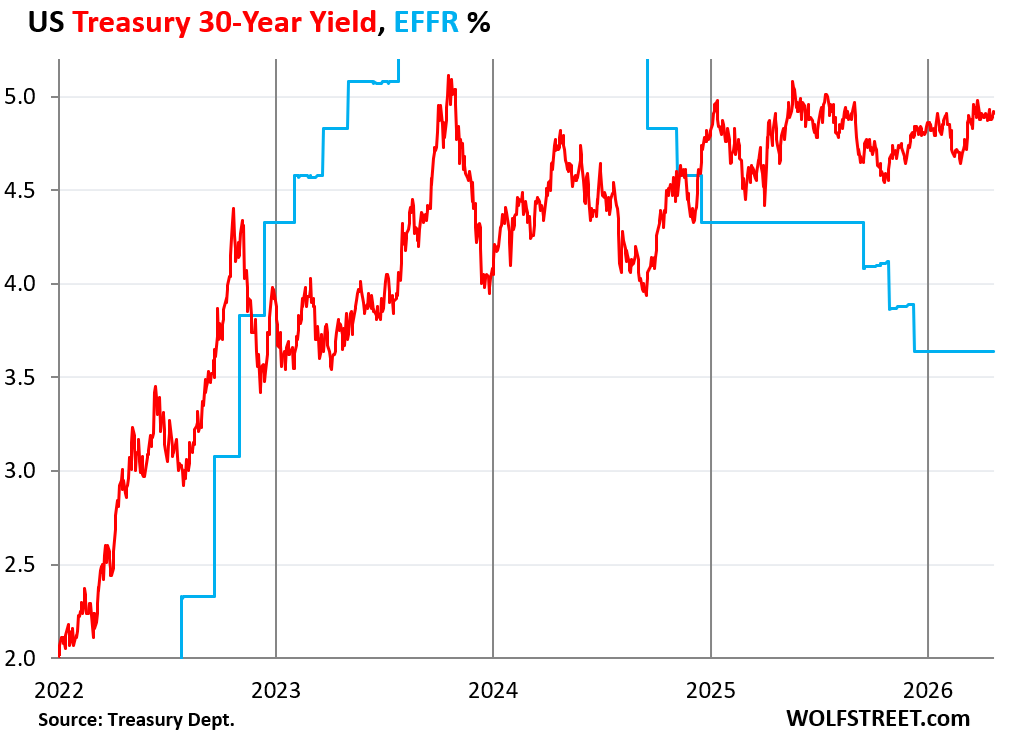

The 10-year Treasury yield rose by 5 basis points during the week to 4.31% on Friday, back to where it had been two weeks ago.

Higher bond yields in the market mean lower bond prices for existing holders, and vice-versa.

That longer end of the bond market doesn’t dance to the drumbeat of the Fed’s policy rates, but to fears and hopes about the future, especially the imagined path of inflation and the expected supply of Treasuries to fund the ballooning deficits that may require higher yields to attract ever more investors.

The 30-year Treasury yield edged up to 4.91% on Friday, up by 3 basis points from a week ago, and up 1 basis point from two weeks ago – so minimally changed over the past two weeks.

It has been hovering near 5% since mid-March. Over the past three years, it exceeded 5% several times briefly.

Obviously, the very long end of the Treasury market completely blew off the Fed’s rate cuts. What we can see is how the end of QE at the beginning of 2022 and the start of QT in the second half of 2022 allowed those long yields to rise:

In case you missed it: The Largest Foreign Holders of US Treasury Securities and the “Basis Trade”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yields still seem low given the current environment. But what do I know!?

Agreed but I think it might be good relative to what might be coming. Unlikely rates will increase and not out of the question short term sees some small cuts over next 18 months.

Why do you think short term rates would see some small cuts? The last six or so times the Fed did that resulted in the market pushing long term rates higher. Each cut, same result. It seems likely we’d be looking at sustained seven-handle mortgage rates going down that path. I sure wouldn’t want to have to answer for causing that, especially if I just started a new job at the Fed.

I wouldn’t bet against 2 25 basis cuts by the end of 2027. Not sure what the Fed will do with more inflation and a softening job market. Wouldn’t bet it happens either but toolbox has few options. The Fed might be okay with lower short term rates even with high inflation. They just won’t issue a lot of long term instruments

The 10-year Treasury was yielding 0.5% right before inflation exploded up to 9%. Yet they tell us the bond market knows what is coming.

No. That was the effect of QE, when the Fed was buying every 10-year in sight. I explained that in the article. That’s what QE does and is supposed to do. And you know that.

Investors who bought those 10-year Treasuries in 2020 at a yield of 0.5% got their faces ripped off when the 10-year yield started rising and the market prices of their bonds began to plunge. Some banks collapsed because they’d done precisely that.

And bonds are supposed to be safe lol

They are safe in terms of credit risk. Bondholders who hold to maturity will not lose a penny. They will get paid face value. But if they want to sell before they mature, they’re subject to market value and market value is subject to yields — these are different risk for people who want to sell early. But the closer a bond gets to maturity, the more the market price approaches face value, and a few months before maturity, market price and face value are nearly the same.

AI will bring tremendous deflation in the 10-30 year window. That’s the counterweight.

Thank you for explaining these auctions in such detail.

“including the amounts needed to pay off the maturing debt of over $500 billion a week”

Insane

The current situation isn’t too far from ZIRP on a real basis.

3.6% interest less 3.6% inflation = 0%

ZIRP (Zero Interest Rate Policy) means policy rates = 0%. So 0% policy rates and 2-9% inflation rates, producing negative real interest rates, including long-term rates. At one point during ZIRP, real mortgage rates over -4%. That’s ZRIP.

Short-term risk-free interest at 3.7%, like today, and inflation at 3.7%, coming, so with real short-term risk-free interest rates at 0%, is not ZIRP.

Interest rates should always and forever be equal to inflation. No “looking through,” and no dual mandates.

Then maybe no one would lend? And there would be no demand for this stuff?

I think maybe he meant at a minimum?

Which interest rates, Mr Data? There are lots of different interest rates. And which inflation gauge? There’s a lot of those too.

If what you’re looking for is the Easy Button to save for the future and match CPI-measured inflation, look up TIPS and I bonds.

FFR, and some yet-to-be-determined measure of inflation that accurately reflects peoples’ actual experience of inflation. OER, for example, ain’t it.

My point is meant to be more broad. The Fed should not be “winging it” on interest rates (again, FFR). What I am saying is that the purchasing power of the dollar should be protected. Or, as Warsh (and others) said, inflation is a choice.

That sounds like something Chat gpt would espouse. No, what the economy needs is high real rates of interest for saver-holders. Then you need to channel the savings through an intermediary which invests in real things. Intermediaries necessarily invest quickly or they lose money. If savings aren’t reintroduced quickly then a dampening impact is generated.

The conventional interest rate model is

Int Rate = Inf + Risk

risk includes the probability that the dividend paying entity goes bankrupt

by that measure I think the 10 year should be over 5 pct.

“risk includes the probability that the dividend paying entity goes bankrupt”

If you really think the US is going to go bankrupt, you’re looking at a fall of the Roman Empire situation. If you really believe that, you should be spending time differently than arguing on the internet about a few bps difference on treasury yields. Relative to every other major country on earth, we have almost no default risk.

LOL! “Slowly at first…”

Yes, America will always be able to print currency to cover it’s bills, hence never go bankrupt, but considering the cohort of people in control and their lack of integrity, I don’t think anyone should be acting like this is a good thing.

I think a better response would simply be; “you really think there has been a free market in America where the bond market is accurately pricing in risk? LMFAO!”

Clearly this person is naive, ignorant, or some combination of both. It’s a club, always has been.

How about this…

When inflation is THIS, Fed Funds are THAT plus X

no subjective “transitory” misjudging. Hard Rail monetary policy.

(Take a 3 month moving average of inflation if you must.)

The government borrows at rates so attractive so as to perpetuate the creation of debt……yet they complain about the debt sevice.

I like it! Although, to best match the average citizen’s experience of inflation, the should look at 5 year inflation. That would prevent the ludicrous hand waving in economics whereby large price jumps (such as post-Covid) can quickly be ignored, since they drop rapidly out of the discussion.

Well since we live in a social democracy, I am able to poke holes in your testimony.

Firstly the obvious discrepency connoted in your phrase ” Hard Rail monetary policy” leaves me baffled about what you are thinking.

The federal government is the only entity in our federalist structure that can create currency. The states have to run a balanced budget.

I think the last thing the Federal Reserve Bank of the United States of America is guilty of is a lack of liquidity in the world economy.

The problem is that no one seems to be paying enough taxes to at least slow the ludicrous increase in national debt to 38 trillion dollars creating IMO evidence of excess.

I was thinking that a Fallini film that I saw in the early 80s and judged as farcical is apropos to the current situation

“The problem is that no one seems to be paying enough taxes to at least slow the ludicrous increase in national debt to 38 trillion..”

really? It’s not a spending issue but a lack of taxation? BTW, its more like $40 Trillion.

“Hard Rail” monetary policy regarding rates would remove the subjectivity of setting rates. 400 PHD’s at the Fed missed the “transitory” inflation that wasnt.

Taylor Rule would be an example of hard rail.

No more “we will rely on the data”.

Then, “we will see through the data when appropriate”.

“BTW, its more like $40 Trillion.”

It’s $38.96 trillion. It came down some, as the article explained painstakingly.

“A billion here, a billion there, and pretty soon you’re talking real money”…. update that to “A Trillion here….”

What would be really interesting is when the rate on the 4-week, 6-week, and 8-week bills starts to rise, which could happen if the Treasury tries to fund too much of the deficit with short-term paper. Doing this cuts the interest the Treasury has to pay, but may overwhelm demand.

Financial Repression: Federal Reserve suppressing interest rates while stoking inflation is the definition of financial repression. There is also a Wikipedia article on it. The whole situation is now clear: generate inflation through low interest rates for the oligarch class to buy up housing, gaslight the proletariat from protesting through “transient” deflection, slow roll inflation fighting to entrench inflation, maintain tax breaks for oligarchs to guarantee their ability to avoid inflation financial loss, and then leave Federal Reserve office maintaining a defense of weaponized incompetence. Definitely the truth of the “time will tell” saying.

Financial repression was when the Fed had interest rates at 0%, with T-bill yields going below 0% periodically, while it was pushing down long-term yields below 1% via huge amounts of QE, while inflation was heading to 9%.

Now short-term rates are 3.7% and the bond market is on its own, taking yields wherever it wants them to be. That’s not financial repression at all.

Sounds like Bernie Sanders Press Secretary

A situation where treasury bills are lower than the rate of inflation represents a stimulative policy stance. That means it stimulates economic growth and inflation. It encourages people to spend or invest because they suffer a real loss by hiding out in treasury bills. This juices economic growth, but eventually all that spending starts to compete with itself, and prices for stuff and labor get bid up.

Interestingly, the Fed’s switch in policy stance from restrictive to stimulative came about not only because of rate cuts, but because of rapidly rising inflation too. Inflation rising above short terms rates itself functions to make policy more stimulative. That’s why if the Fed doesn’t act fast with rate hikes, their control over policy could slip out of their hands.

I don’t see Kevin Warsh and the most dovishly-inclined FOMC in decades getting ahead of the curve any better than they did in 2021.

Americans might respond to inflation being above short term rates by trading their cash for things, but foreigners have the choice to exit the currency. E.g. would you hold a currency if it was steadily losing purchasing power and there were no safe bonds to buy that could change that situation?

“…treasury bills are lower than the rate of inflation represents a stimulative policy stance..”

It seems designed to FORCE a behavior.

Alternatives for your money? Stocks, Real Estate, Gold.

Pumping the first two are politically favorable. The midterms are mighty important to the President.

This is how 20 Cowboys can herd 5000 cattle. When did the Fed become engaged in “forced” behavior? (disguised as promoting a healthy economy and main street) There was a time when interest bearing securities balanced a portfolio. Now its “all in” for Stocks or Gold. Not a good condition, IMO.

It could push one or the other investor to get out of T-bills and into stocks. But someone has to buy those T-bills, and someone has to sell those stocks, so overall the market cannot change, every single T-bill will have a holder, and every share will have a holder, it’s just that holders hand them to each other, so it doesn’t cause market-wide shifts.

But there is an AI mania. While many big stocks are down 50% or more, such as some software stocks, AI mania has driven semiconductor stocks out the wazoo.

A little honesty in reporting. Do you think with the next auction they should advertise “Only suckers invited “? Or do you think they should do the ‘unthinkable’ and jack up interest rates 3-4% from where they are right now?

It’s an auction, the price is the yield, so competitive bidders decide at what yield they want to buy, and they submit their bids, and the high rate is the yield at which all securities can be sold, and everyone then gets the high yield.

With TGA balance so high and Treasury securities supply went down, why FED had to jump in and keep buying 40B Treasury securities every month from Dec 2025. They are doing it in the name of Reserve management. Even if they did, they should stop it much before Tax day. Whom are they helping?

If Banks need money, they can borrow it from Discount Window or SRF.

All Assets are ATH and Powell thinks we have liquidity issues. Same like when entire US Real Estate market was on fire in 2020-2021 and FOMC thought they need to buy MBS and do QE to boost economy.

Powell stood up to Trump, he did 2T QT but that’s too less compared to how much FED printed and long lasting damage they did to USA. We need Regime change in FED. Only time will tell if Warsh will be Trump’s puppet.

But until we have Powell as FED chair, we wont have smaller balance sheet.

It’s NOT $40 billion “every month.” They already slowed it down last week.

It WAS $40 billion a month through mid-April “Tax Day” to get ready for the big liquidity drain around Tax Day, when hundreds of billions of dollars leave the banking system to go to the TGA, which is at the Fed, where this liquidity vanishes. That was in the original announcement of it last year.

So that $40 billion was through Tax Day. They already slowed that down last week, and will slow it down further this week and every week, as re-announced in greater detail in mid-April.

I agree — they obviously didn’t have to do that. They have the SRF that is designed to handle those kinds of seasonal liquidity strains. But Powell is the architect of the “ample reserves regime,” meaning that liquidity should be ample-supply-based not demand-based. And lots of demand at the SRF, as we saw at the end of last year, means to him that reserves are no longer ample, and he didn’t want to shift to a demand-based liquidity system. Powell is out the door next month, by which time those T-bill purchases will already be minimal.

Me thinks many “Old Man Yells At Clouds” in today’s comments section.

Thoughts on what may happen.

While interest rates have been moving toward a normal yield curve and their goal is to get one or maybe two 25 basis points rate cut by year end and then rolling over the ever increasing debt short term. If this does occur then long term rates will definitely go even higher and actually reflect the real rate of inflation.

And yes, Powell turned out to be a real dyed in the wool Keynesian.

While Bernanke, Yellen, and Powell turned up QE and were buying up treasuries from asset holders at a premium and this cash ultimately landing in M2 and then being reinvested in the next bubble so the cycle goes…

I encourage readers to look at the historical evidence of FED failure. Many people have written about this.

Wes, you say “ their” goal is two 25 point rate cuts. FED has no such goals. They have a dual statutory mandate.

IMO, the dual mandate was foolish act by Congress and is impossible.

“Price stability “ is important to a country’s currency or money. If this half of the mandate means price of all assets, then it means no inflation. Not a 2% target rate of inflation.

Interest rates are simply the price of money. The federal government, the Congress, and any entity/institution created by Congress has no business setting the price of money, bananas or beef in a free market and capitalism.

Markets should trade freely, including money market, borrowers, savers and lenders and the resultant trades establish information to glean the price of money…or interest rates.

If you study economics and deferring the consumption of assets today versus saving and allowing others to consume such assets, human nature requires an incentive to save. Thus, real interest rates in a market will seldom be negative.

How are countries institutions (administration , Congress, press, higher education, financial markets) focus on what the FED is doing ( interference ) instead of the underlying illness is dumbfounding ; but more importantly intentional to mislead the sheep.

Price stability measured in value of what the dollar will buy since 1913? Failure. Measured since 1971? Failure. Pick a date? Failure.

Yet we focus on FED? Laughable.

There are solutions! Painful real solutions. But, the current FED with a dual mandate is not a solution, it is big part of the problem.

Will not waste readers time with my prescriptive solutions; just will say that one must understand the “ disease”; the electorate must understand the disease….before one can articulate the cure or remedy….and the remedy will not taste good to the people.

When the FDIC lowered its insurance from unlimited transactions deposit insurance to $250,000, we got lower inflation accompanying the “taper tantrum”. And we got lower unemployment, and higher real rates of interest.

You see, the economists are running the economic engine in reverse

–Danielle Dimartino Booth’s book: “Fed Up”, pg. 218

“Before the financial crisis, accounts were insured up to the first $100,000 by the FDIC. That limit kept enormous sums in the shadow banking system. After the crisis, the FDIC raised the insured account limit to $250,000. But trillions of dollars still sate outside the traditional banking system. The “safe” money had no place to go expect money market mutual funds and government securities, leading to a shortage of T-Bills and a corresponding drop in yield.”

The dual mandate…..

We have been drilled to accept the concept.

But the actual language refers to THREE mandates……and the third is omitted because it has often been ignored. (ZIRP era)

Promote stable prices

Promote Maximum employment

AND the omitted third…..

Promote “Moderate Long Term Interest Rates”.

Moderate defined as neither too high OR TOO LOW. They certainly allowed “too low” when the long rates went (driven) to all time lows, 4000 yr lows.

Legally, the Fed really has only 1 Mandate, and 3 Goals:

“Federal Reserve Act, Section 2A. Monetary policy objectives:

The Board of Governors of the Federal Reserve System and the Federal Open Market Committee

shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production,

so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

(Nothing is omitted, I just split up the sentence to make it clearer.)

The ONE legal “mandate” is the “shall maintain” part: “shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production”.

That one “mandate” is in service to THREE goals: “maximum employment”, “stable prices”, “moderate long term interest rates”.

But those goals are not mandates – there is no “shall” or “must” to them.

Since the Federal Reserve Act was passed, the data clearly show that the “monetary and credit aggregates” have grown Much Faster than the “economy’s potential to increase production”. There is now too much inflation AND too much credit/debt.

For data on “monetary and credit aggregates”, consider FRED data series TOTBKCR “Bank Credit, All Commercial Banks” as well as the national debt/GDP ratio.

Taking the merits of your observation, you should make certain CNBC, Bloomberg and even the Fed should stop mentioning a “dual” mandate.

Report back with how that goes.

The Fed is a Politburo-wannabe. It’s actions are the same as central planners’ actions in any communist regime. The Fed determines short-term rates, not the market, and so tries to influence the economy. It is amusing that so many so-called capitalists support the existence of the Fed.

Ghost of Andrew Mellon, is that you?

Just curious.

Do you think that your articles make a difference in the logarithms for any of the markets.?

Or is it just super small in the big picture of the world wide web??

I suppose it would be nice if the sense you made… would make a difference somewhere.

I’ve never noticed that my articles make even a scintilla of difference in the gigantic Treasury market.

My key Treasury articles, like this one, get between 20,000 and 50,000 reads, which is pretty big for my site. This one is now at 25,000 and still going strong. The last one on April 11 got 47,000 reads. But the Treasury market is gigantic and global, and I’m just a little voice in my little corner here. And I’m not trying to influence the market; I’m trying to explain it.

Like I said….

Just curious if you ever noticed anything.

It probably would be helpful if it did I suppose.

Huck, I hope you mean algorithms, not logarithms. It is unlikely the markets care much about the inverse operation of exponentiation.

The 10-year has been hovering at right around 4.30% enjoying itself for weeks despite higher inflation reports and the known fact that fuel prices will cause it to ride higher. I’m amazed it’s almost pegged; maybe going up or down 2-5 basis points here and there.

It had dropped to 3.97% at the end of February and risen as high as 4.44% at the end of March. Now it’s in the upper portion of that range. That’s a range of nearly 50 basis points, which may be about normal for a three-month period.

So the issue for the next 10 years isn’t inflation “today,” but inflation over the next 10 years. If the market believes inflation will be 2-3% over the next 10 years, a 10-year yield close to 4.5% may be what you can expect. A hawkish Fed can make that happen.

Long tail of internet doomerism making it to the boomers. I bet they don’t realize Alden’s ability to bear a child either.

The yield (interest rate) on 10 year US Treasuries will be likely and very soon be well above 5% and headed much higher.

You would think so, but nothing works as it is supposed to (manipulation).

If one believes long-term rates are being manipulated lower, then it would not make sense to be in that currency. Buy Australian dollars, Swiss francs, Brazilian real, etc.

I don’t think sp.

I have been hearing this for long time, it touched 5% for a moment and then went down.

Do government bond markets matter when all central banks can create as much currency as they want to purchase their respective governments want them to? Bond markets meant something when there was at least a sliver of true price discover and an internationally accepted set of rules. It should be clear to everyone that those days are long gone and the MATH behind a fractional reserve system is what it is.

Nothing matters until it does.

Eventually, investors will lose their appetite for USD’s. But that might be occurring now or it might occur in 10 years.

@wolf “But inflation rates are on track to surpass T-bill yields, or already surpassed T-bill yields. But T-bills are bracketed by the Fed’s five policy………”.

So, lets say inflation goes up to 6% in the next 6 months (just as an example). Are the t bill rates likely to be well under these rates ? If yes, then roughly how much ? Like off by 100bps or more, or maybe like a few 20 – 30 bps.

T-bill rates move with the Fed’s current and expected policy rates within their term window. If the Fed keeps saying that the energy price spike will be short-lived, and it’s not raising rates, then T-bill rates won’t change all that much. If the Fed starts talking about rate hikes, esp if other inflation factors are moving, then T-bill rates will rise to try to stay ahead of those rate hikes.

Federal Reserve officials are expected to leave interest rates unchanged this week at a gathering that’s being overshadowed by the latest twists in a political drama surrounding the leadership handover at the US central bank.