Foreign demand for the ballooning US Treasury debt is an increasingly important issue. But how much of that demand is actually “foreign?”

By Wolf Richter for WOLF STREET.

The US government’s $39 trillion in debt is held by all kinds of investors, including foreign investors. When investors lose their appetite for this debt, yields would rise until they’re high enough to attract new investors. Higher yields mean higher borrowing costs and even bigger deficits for the US government. All eyes have been on foreign investors to see if they start losing their appetite. And some have – especially China and Hong Kong – but others have piled into it.

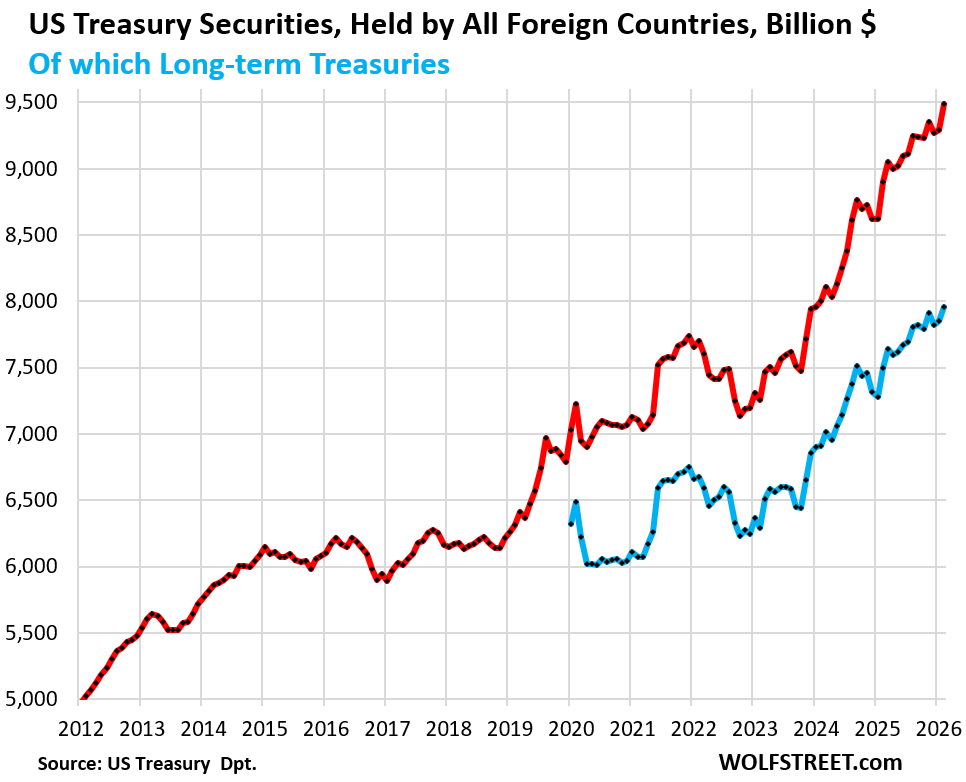

All foreign investors combined piled on another $198 billion of Treasury securities in February, and $587 billion over the past 12 months, bringing their total holdings to a record $9.49 trillion, according to Treasury Department data today (red line in the chart below).

Of that $9.49 trillion, $7.76 trillion (84%) were long-term Treasury securities (blue), and the rest were short-term Treasury bills.

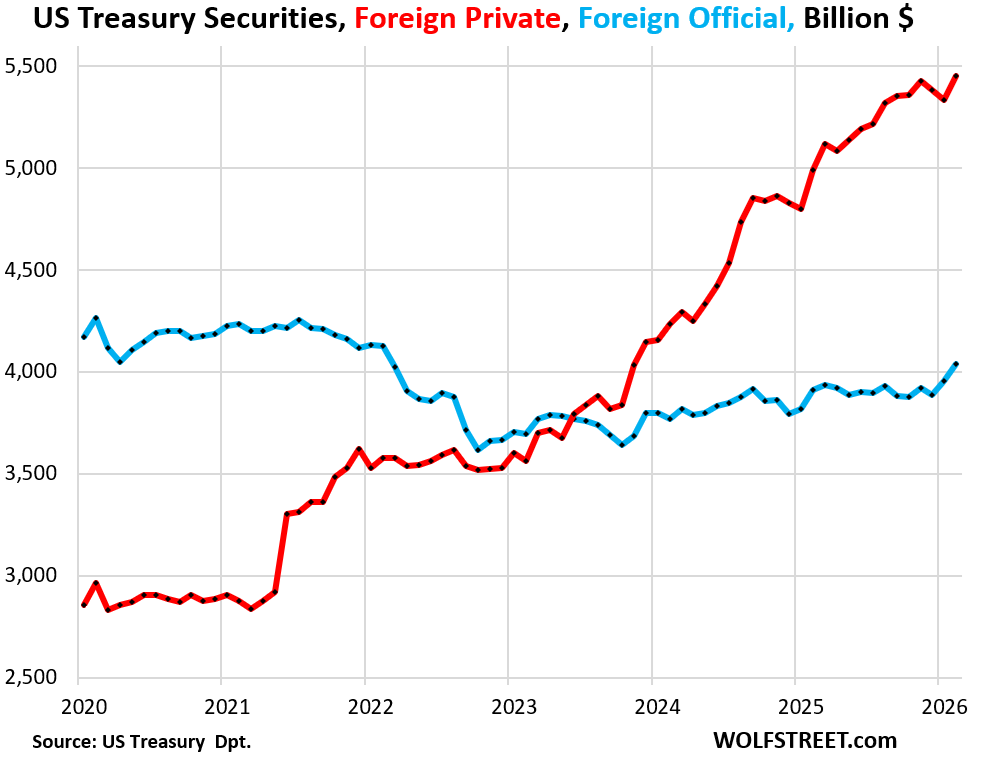

The driver behind the multi-year increase were “private foreign” holders: they increased their Treasury holdings by $117 billion in February, and by $461 billion over the 12-month period, to a record $5.45 trillion (red in the chart below).

These private foreign investors include financial firms in other countries, foreign bond funds, foreign companies, individuals in foreign countries, but also US hedge funds domiciled in the Cayman Islands, such as those engaged in the “Basis Trade,” and Corporate America with financial entities in Ireland, such as to legally dodge US taxes.

“Foreign official” holders, such as central banks and government entities increased their holdings by $81 billion in February and by $126 billion in the 12-month period, to $4.04 trillion – well below their holdings a few years ago (blue line).

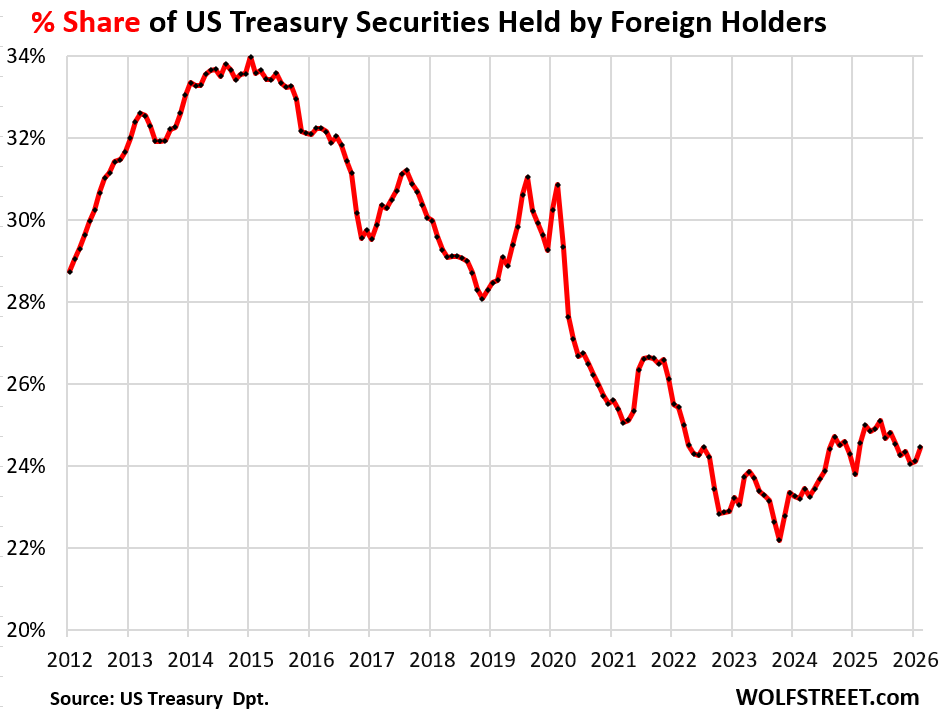

The share of total Treasury securities held by foreign entities had peaked at 34% in 2015, then fell to a low of 22% in October 2023, and has been marching higher since then.

However, during the Debt Ceiling period in January through June 2025, the US Treasury debt did not increase, while foreign holdings continued to rise along trend, and so their share rose. Starting in July 2025, the US issued large amounts of debt to refill its drained checking account, in addition to funding the ongoing deficits, while foreign holdings continued to increase along trend, and their share then eased.

In February, their share rose to 24.5%, the highest since September, after already increasing in January.

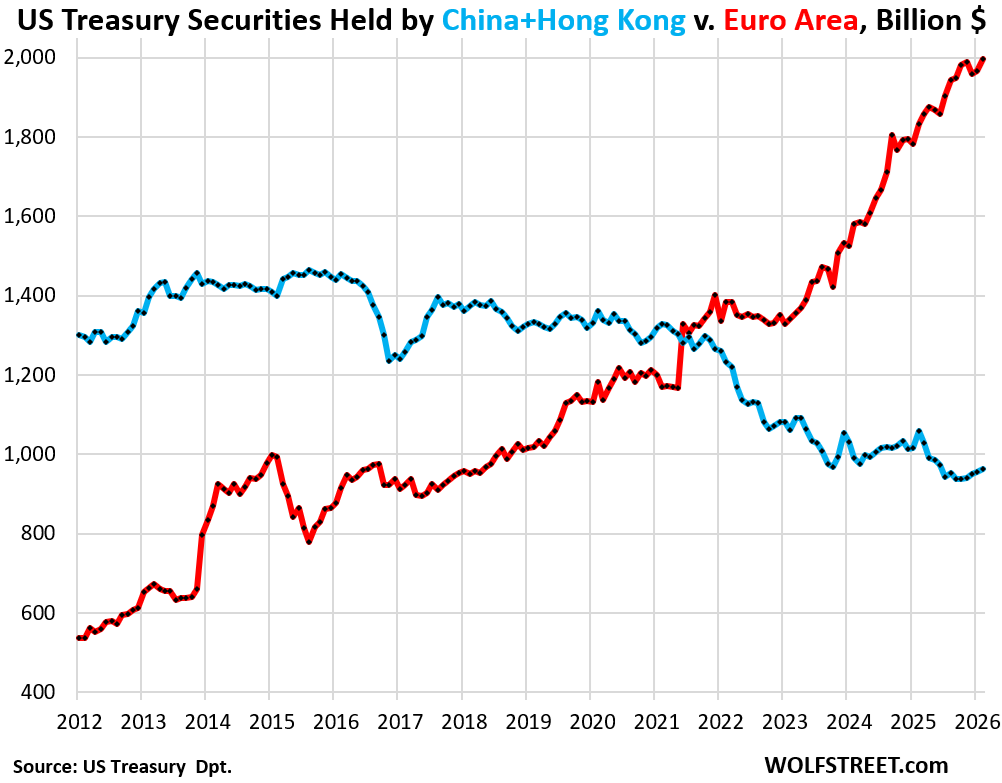

Big Shift: China & Hong Kong versus Euro Area.

China and Hong Kong combined added $8 billion in February, but over the 12-month period shed $96 billion, bringing their holdings to $962 billion. They have cut their holdings by more than one-third over the past 10 years (blue in the chart below).

The Euro Area has been loading up on Treasury securities hand over fist and in February added another $32 billion, to a record $2.0 trillion. Over the 12-month period, the Euro Area added $164 billion (red).

The biggest holders in the Euro Area are the financial centers (Luxembourg, Ireland, Belgium) and France, whose banking system also has functionalities of a global financial center. Their combined holdings accounted for 82% of the Euro Area’s total holdings. More in a moment. But Germany, a big exporter to the US and the largest economy in the Euro Area, only held $109 billion and doesn’t even make it to the Treasury Department’s list of top 20 “Major Holders.”

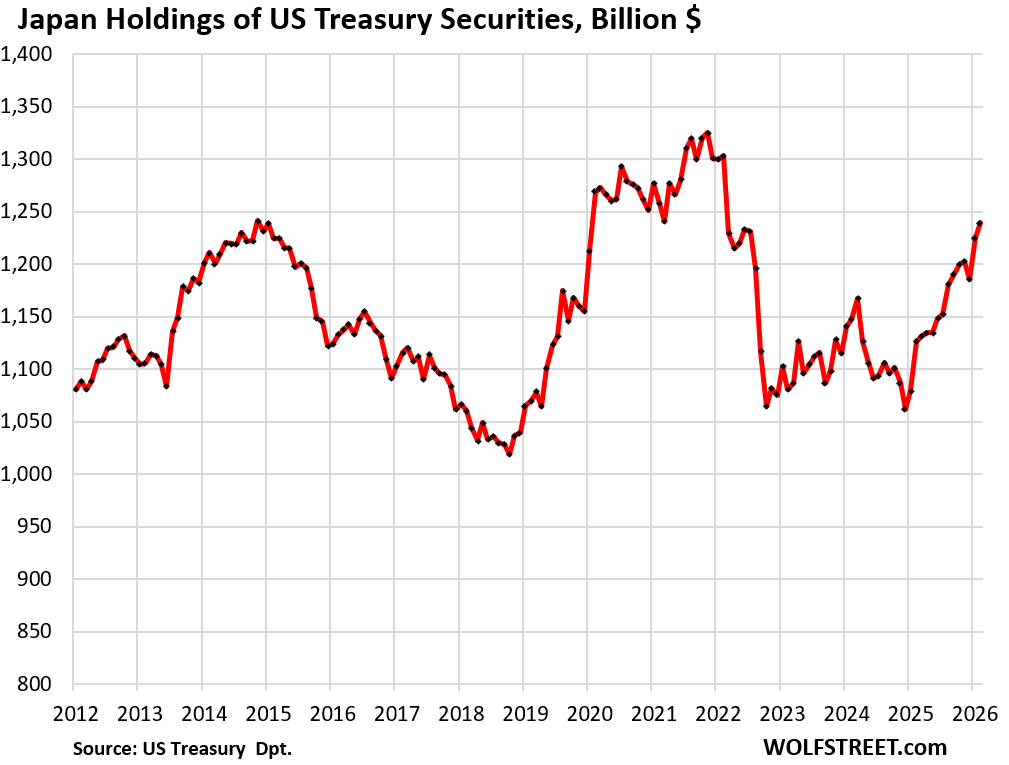

Japan’s holdings of Treasury securities rose by $14 billion in February, and by $113 billion over the 12-month period, to $1.24 trillion.

Japan’s holdings have remained in the range between $1.0 trillion 1.3 trillion for many years, despite the large fluctuations in between. Japan periodically sold large amounts of its USD holdings and purchased yen with the proceeds to the support the plunging yen.

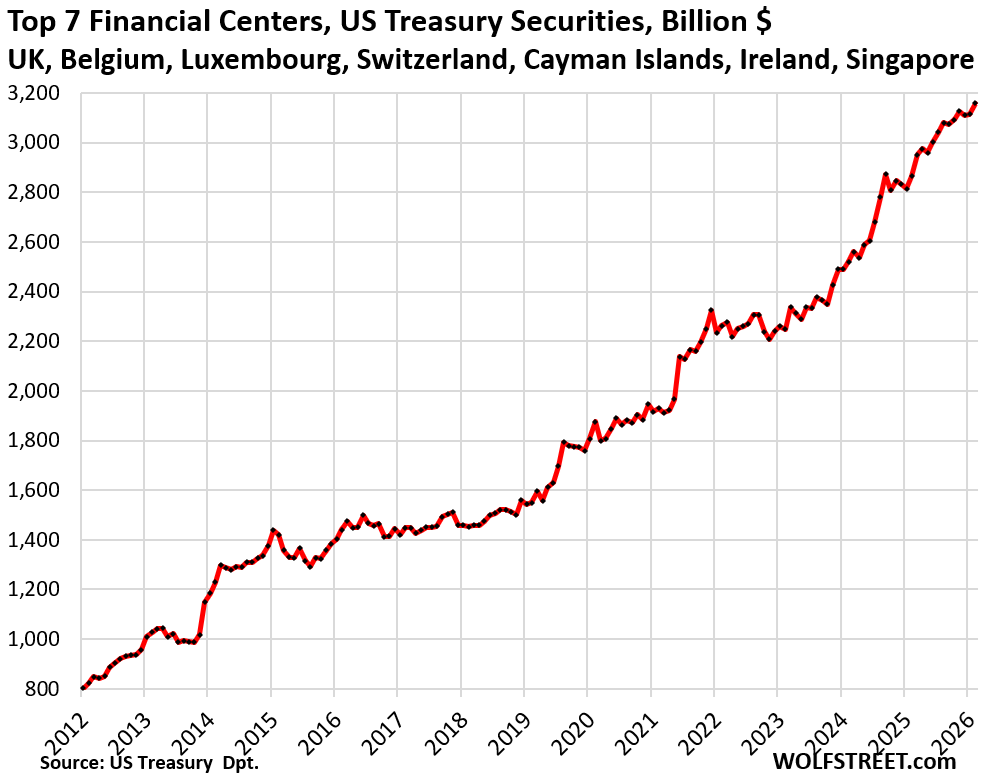

The seven largest financial centers piled on another $44 billion in February and $295 billion over the 12-month period, bringing their total holdings to a record $3.16 trillion. They more than doubled their Treasury holdings over the past 10 years.

Changes in February, and total Treasury holdings:

- United Kingdom: +$18 billion, to $897 billion

- Cayman Islands: +$10 billion to $443 billion (or closer to $2 trillion, according to the Federal Reserve’s analysis of the basis trade, see below)

- Belgium: $4 billion to $455 billion

- Luxembourg: -$0.3 billion, to $446 billion

- Ireland: +$9 billion to $351 billion

- Switzerland: -$2 billion to $287 billion

- Singapore: +$7 billion to $280 billion.

A big portion of Treasuries at these financial centers are held by US entities. These countries specialize in handling the financial holdings of global companies, hedge funds, individuals, and governments.

For example, Ireland is a favorite for US Big Pharma and Big Tech to store their profits. Belgium is home to Euroclear, which has $40 trillion in assets under custody for companies, governments, and wealthy individuals around the world.

And the Cayman Islands are where US hedge funds are domiciled, including those that are engaged in the huge “basis trade.” More on that situation in a moment

The “basis trade” and the Cayman Islands.

Many big US hedge funds are domiciled there, and their Treasury holdings would normally count as holdings in the Cayman Islands.

But the $443 billion in Treasury holdings currently attributed to the Cayman Islands massively undercounts the actual Treasury holdings by US hedge funds that are domiciled there.

The Federal Reserve Bord of Governors, in a report last October, showed that Treasury holdings by Cayman-domiciled US hedge funds were undercounted by $1.4 trillion at the end of 2024.

The report found that the Treasury International Capital (TIC) data, which these numbers here are based on, fails to capture a big part of the Cayman-domiciled US hedge funds’ Treasury positions and instead accounts for them as US domestic holdings. Other government data has a better handle on the Cayman-held Treasuries, according to the report.

These Cayman-domiciled US hedge funds engage in the basis trade. They’re highly leveraged in these positions. They’re long (they buy) Treasury securities and are short (they sell) Treasury cash-futures. It’s a massive business. In normal times, it provides liquidity to the Treasury market. During times of turmoil, such as in March 2020, those trades cause the Treasury market to seize – and the Fed ended up stepping into it to get it going again.

So the actual Treasury holdings in the Cayman Islands would be close to $2 trillion, not $443 billion – more than any other country.

And total “foreign” holdings would then be close to $11 trillion, not $9.49 trillion.

But these holdings by Cayman-domiciled US hedge funds are foreign holdings in name only. That’s the same issue with the other financial centers that hold Treasuries of US entities. That’s not really “foreign” demand for US Treasury securities.

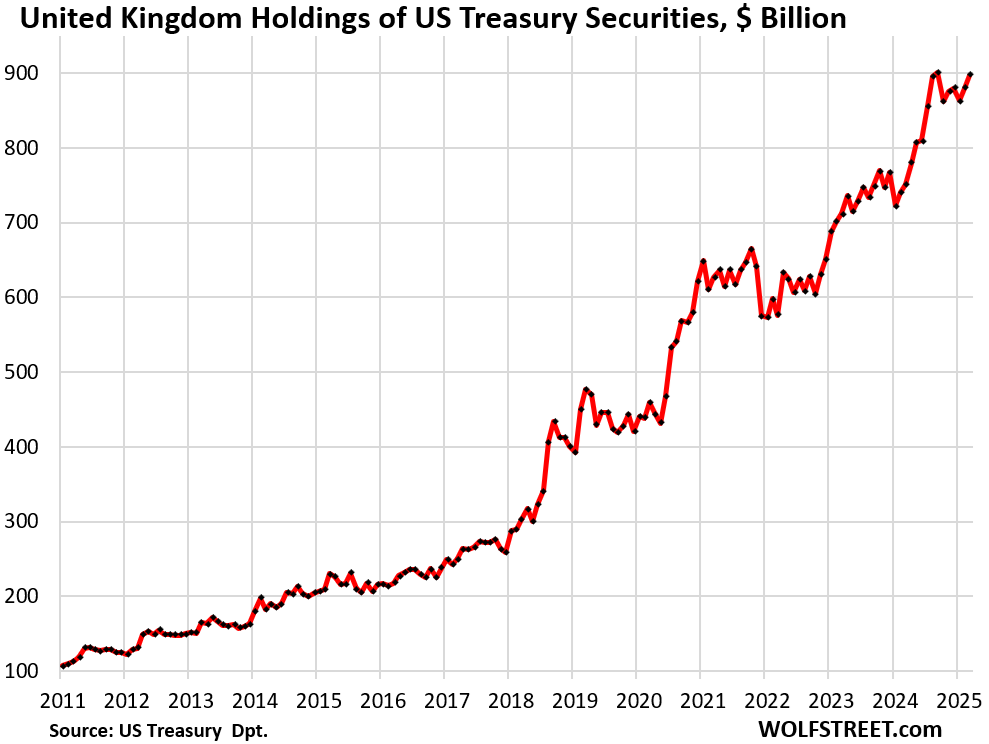

The United Kingdom is the “City of London” financial center. Its Treasury holdings rose by $18 billion in February and by $147 billion in the 12-month period, to $897 billion. The record was in August 2025 at $901 billion.

Canada’s holdings have been gyrating up and down in massive spikes and plunges in all of 2025, and that continued into 2026. In February, they jumped by $50 billion, after the plunge in the prior month, to $446 billion.

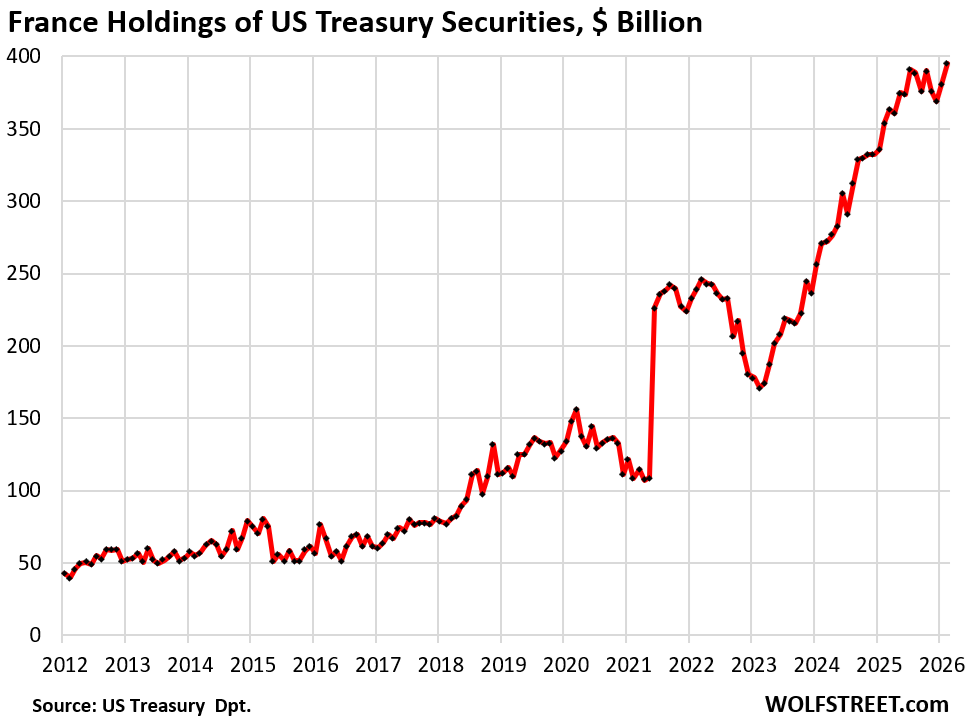

France’s holdings rose by $15 billion in February, and by $41 billion in the 12-month period, to a record $395 billion.

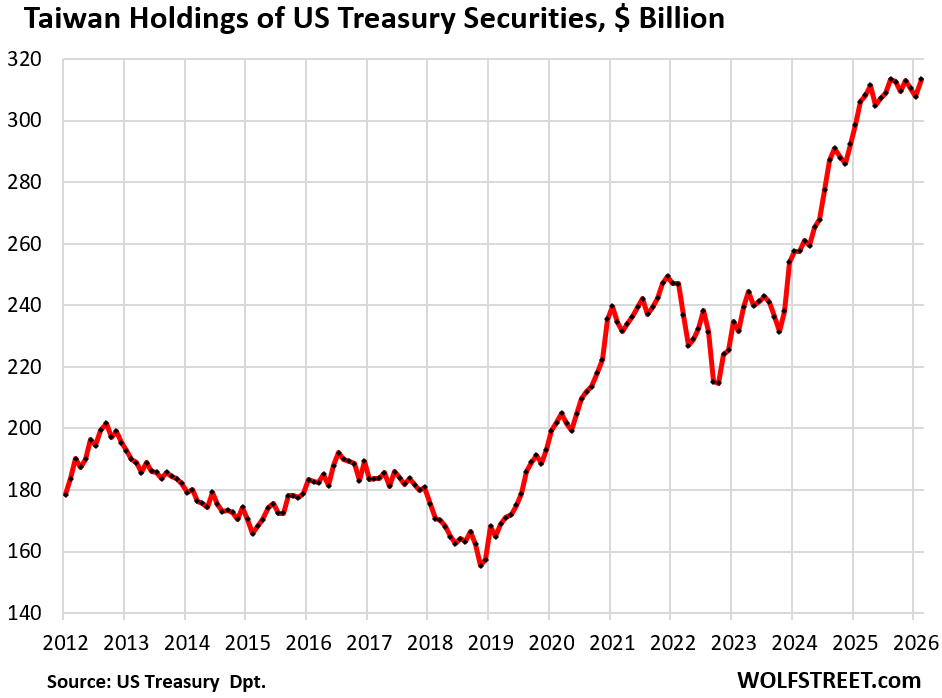

Taiwan’s holdings rose by $6 billion in February to $314 billion, and were up by $7 billion over the 12-month period:

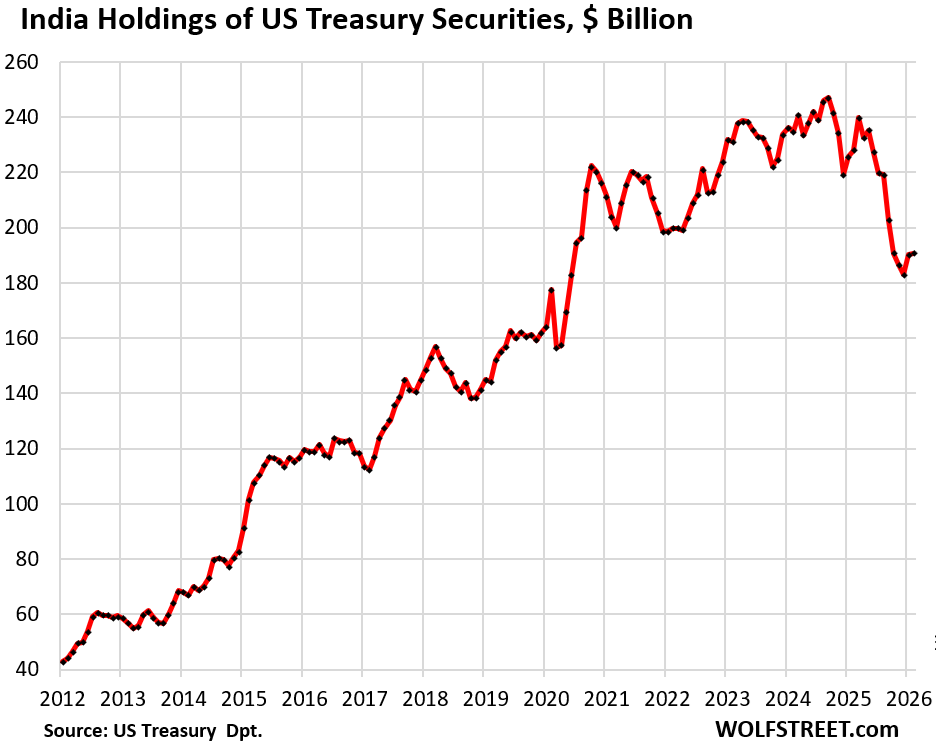

India’s holdings have risen over the past two months, to $191 billion, after dropping sharply from the peak in 2024 ($247 billion).

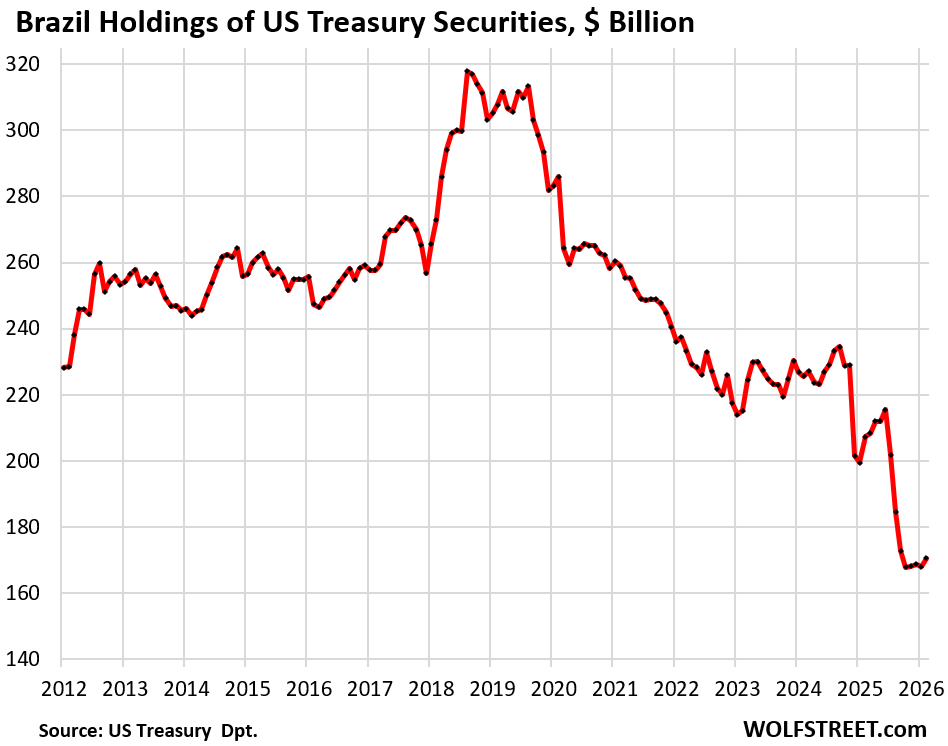

Brazil’s holdings have edged up over the past five months to $171 billion, after a 46% decline from the peak in 2018 ($318 billion).

In case you missed it: US Government Interest Payments, Tax Receipts, Average Interest Rate on the Debt, and Debt-to-GDP Ratio in Q4 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

These debt numbers are incomprehensible

We’re adding to it by around $2 Trillion a year

It’s unsustainable

If owners start to dump T’s the bond market could crater. The resulting high interest rates would kill the stock market as well.

We’d be saying the same thing even when the debt is 100 trillion dollars

Ample demand for us debts at current rates and economy and markets are doing awesome

Markets maybe. Economy, no, IMO

I’d love to agree with you but if you look at any metrics about economy, there are no signs that economy is doing bad.

@Jon

Inflation is quite high.

Is that an economic problem?

Why can’t it continue like Japan? Don’t quote me, ballpark figure 250 of GDP would be around 70 trillion? In US debt.

I know if government buys its own debt it is inflationary.

Could the DOW go to 100,000? Why not. The stock markets are fundamentally changed in the last 20 to 30 years. It’s untethered from the economy and measures of worth. News driven. Good news is good. Bad news is good.

It cannot continue in Japan either — and it didn’t because the yen collapsed. The BOJ has been doing QT for almost two years to fight inflation and the collapse of the yen. And Japan’s Debt-to-GDP ratio has come down quite a bit, from 258% at the peak in 2020 to 232% now, same as in 2016.

Plus Japan doesn’t have a huge trade deficit that needs to be funded – unlike the US. The US has less leeway.

Interest payments taking up an ever larger portion of tax receipts would crush the dollar and with it the purchasing power of Americans who depend on imported goods.

The question I have is:

Am I reading this correctly that the country only means that the broker of record holding the bonds is in that country, but we have no idea who actually owns the bonds?

While it is an interestimg trend to observe the trends, does this really give us insight into the motivation and “leverage” of these countries?

Chinese holding dropping is likely illustrative, as I would guess the ultimate owners are mostly Chinese, but all these financial center numbers appear mostly meaningless to me. What am I missing?

“What am I missing?”

everything except your own narrative.

Amazing to think how despite such large numbers, the Euro Zone is just one year’s worth of deficit, China 6 months, UK 5 months, India 1.5 months, etc.

“Foreign demand for the ballooning US Treasury debt is an increasingly important issue.”

If I were to write it, I would be tempted to say

“No one wants to touch that ***t with a 10 foot pole!”

“At those low yields.” It ALWAYS comes down to yields. If they’re high enough, there’s demand.

It’s all voodoo economics! We all appreciate the scam and criminal enterprise and the terrible injury inflicted on the poor and middle class.

As long as the predatorclass prospers! This is the underlying physics and mechanics of the system.

The predatorclass prospers! Fuck every thing and every one not predatorclass!

Demand for high yields is voodoo economics? I think that’s just economics…

This standard Bernie Sanders line that most of Americans is poor is getting old. You may be poor. Not most of the people are poor

Some day well come to find out that these Cayman hedge funds are actually government programs run by the 3 letter agencies. What else could it be at this point?

Not to worry… tether, usdc and trumps stablecoin empire will suck up all excess bond issuance.

We are all saved by crypto!

I believe that there is more than a grain of truth in what you said.

“What else could it be at this point?”

THE BASIS TRADE.

RTGDFA instead of fabricating homemade conspiracy theories for the entertainment of bored people.

Wolf- The flaw in the data is that The tick report shows The MARKET value of the holdings in US DOLLARS. So it ignores the currency effect.

For example as of February 28th, the US dollar had declined by 12.7% against the Euro to year. Measured in Euros, European investors did not increase their holdings. The entire gain in US dollar value of their holdings was entirely due to the surge of the Euro against the dollar. The amount of treasuries that they hold denominated in their home currency actually fell. They were net redeemers or sellers.

Yes, TIC data shows market value. So changes in yields affect market value, and those effects are visible in TIC data.

No, exchange rates have nothing to do with this data on Treasury securities because TIC tracks Treasuries in USD and reports them in USD. There is no currency conversion involved.

Interesting, so by measuring in strictly USD it measures using absolute values.

Like my own Treasury portfolio. It’s measured in USD, because Treasuries are denominated in USD, and exchange rates have nothing to do with them, and the portfolio at my broker only fluctuates with market prices, not exchange rates. But my portfolio at TreasuryDirect doesn’t fluctuate with market prices because it’s listed at face value (what the government actually owes at maturity). It does not make one iota of difference what the euro is doing.

Like an S&P 500 ETF in a brokerage account, such as SPY, it contains US stocks denominated in USD, and it represents their value in USD, and it is traded in USD. It does not make one iota of difference what the euro is doing.

There is no complexity here. And there is nothing “interesting” about this. It’s just how all USD-denominated in-the-US-issued securities are valued in the US.

You’re right. I have a logical flaw here.

The TIC levels are reported at MTM, not face.

Europeans exchange euros to dollars to buy the paper. A year ago their Treasury paper holdings were worth 100. Today it’s worth 86. The TIC is showing that their holdings rose to 110. Would imply that they bought heavily, averaging down in euros. I got lost in the weeds with the house analogy. My property is worth more in USD because I paid for it in euros.

The Treasury purchases are the opposite. My bad. It’s embarrassing to make an error like that. I pulled my post.

The irony is that I kept questioning the AI about my logic because I felt that it was wrong, but couldn’t work out the string. The AI repeatedly went through the logic and assured me that it was correct.

AI sucks, supporting the point of my AI series debunking it.

Hi Lee! Been a while!

Useful information Wolf. Looks like Brazil is also moving away from western debt and economically still has good growth potential.

This is funny. Brazil’s holdings are tiny compared to the total. They barely made the cutoff. they don’t really matter to anyone except BRICS worshippers.

That is funny. Lots of good things happening in Brazil in the biotech space, but hey, to each their own. It’s a global market and always will be.

but why?

does Europe NEED the revenue from the Yields?

and they obviously can’t WAIT until yield go higher?

and if the cay man eye lands lads are money huge money off T futures, they probably don’t give a shit about yields?

Ireland’s holdings is not just tech and pharma profits. The country has become the main domicile for European ETF’s and that is a main driver of holdings increases. Most of this increase has been since 2000.

These are USD holdings of Treasury securities. Are Treasury security ETFs such a big thing in Europe? Even in the US, the largest Treasury ETF (SGOV) holds only $85 billion.

This reports seems to reflect geopolitics.

The steep declines of holding by China and by Chinese controlled Hong Kong reflect strategy to promote the yuan and to reduce exposure to US after US pushback on China. It is likely that this trend will continue

Similarly, the declines holding from Brazil reflect strategy of socialist government after US pushback on President Lula da Silva’s election & policies. This trend might change if socialists lose the next presidential election.

It will be interesting to see trend of India’s holding over the next few months.

Look forward to more Wolf’s articles

Brazil’s decline started in 2018. Lula had nothing to do with that until 2023, because he wasn’t in office at the time. He was in office from 2003-2011 and again since 2023.

During most of that decline, Bolsonaro was president (1 January 2019 – 1 January 2023).

As a brazilian, let me assure you this has nothing about geopolitics As Wolf already pointed below, Brazil’s president between 2019 and 2022 was Bolsonaro.

The decline in Treasury holdings happens because of selling done by Brazil’s Central Bank in moments of steeper decline of the currency or because of financial outflows. Brazil’s real has fallen sharply against the dollar between mid-2017 and 2020, then recovered a little and fallen again in 2024. And in 2025 UD$ 33B left the country, even with brazilian Real rising.

Question below:

I wanted to know more specifically why so many US hedge funds and endowment/pension organisations are located in Cayman.

The blurb said this:

No Entity-Level Tax: The Cayman Islands imposes no taxes on profits, dividends, or capital gains for funds, which prevents an extra layer of taxation from reducing investor returns.

Avoiding Double Taxation: By using offshore vehicles, foreign investors and U.S. tax-exempt investors (like university endowments or pension funds) can avoid U.S. taxes on certain types of income (specifically “unrelated business taxable income” or UBTI) that they would otherwise owe if they invested in a domestic U.S. fund.

Legal Deferral: Cayman tax laws allow U.S. fund managers to legally defer taxes on their personal performance fees (carried interest) through offshore

My question is why is this allowed to continue? If a production/manufacturing company chooses to make US bound products in overseas facilities to boost profits they are ‘encouraged’ to repatriate production back to US through tariffs, media attacks etc etc. So why are US financial entities allowed to make untaxed/reduced taxed profits wheeling and dealing on ‘the people’s debt’, thus adding to the total debt and actually debasing the currency through inflation?

It seems like there are different rules and standards for different power groups. The financial manipulation groups add nothing valuable to society other than allowing a ‘skim’ to attach to the currency and the current necessary debt used to fund operations and programs. Yet, there is so much propaganda or negative coverage about companies avoiding taxes and their fair share of obligations, example Apple. Seems to me such buyers of Govt debt are no more than clever parasites.

I thought the reply would be that if these people actually had to pay taxes on their earnings, they would require a higher return to even bother financing Govt debt. But then that is the same excuse used for higher priced manufacturing…..producers would have to be paid more for their product by the customer to make it worthwhile to build any product onshore.

A manager hired to build widgets at home pays taxes on income, but a Cayman money manager doesn’t? A manufacturing company pays taxes on profits after deductions but money trading businesses don’t? Sounds criminal to me.

What’s next, financing Govt debt with crypto on the dark web and let taxpayers foot that bill too? Seems like the next logical step for insiders.

The Cayman-domiciled hedge funds don’t invest in Treasury securities to earn a yield. They buy Treasuries to back Treasury cash-futures that they create and sell, arbitraging the price difference in the market between Treasuries (what they buy) and Treasury cash-futures (what they sell), and they multiply the arbitrage gains through leverage.

“These Cayman-domiciled US hedge funds engage in the basis trade. They’re highly leveraged in these positions. They’re long (they buy) Treasury securities and are short (they sell) Treasury cash-futures. It’s a massive business..”

And is it the case they’ve made productive value for us all? A good days work in that some where?

As opposed to, I don’t know, say, a 2nd grade teacher who can’t make ends meet anymore and is exiting that “business”.

Most of that type of trading is automated. They offer a product for which there is demand: treasury cash-futures that investors want or need, such as to hedge something, and they’re willing to pay for this product. That’s a business model.

The problem is that it is highly leveraged and huge and can causse, and did already cause, huge problem when things go awry.

MW: Former Treasury Secretary Henry Paulson warns U.S. needs an emergency ‘break-the-glass’ plan if Treasury demand collapses

Higher yields! That would work. They’re too low now. Inflation is in the process of rising above Treasury yields.

Inflation-adjusted T-Bond yields have been hilariously low for years.

The MSM and the Financial Press are clueless on this issue.

Countries maintain a soft peg of their currencies to the US dollar by buying US assets. Maintaining that soft peg keeps their currency perpetually cheaper than the US dollar, making their exports more attractive and therefore locking in their position in the global supply chain.

“legally dodge US taxes”

No wonder regular people get upset about their taxes, no irish malt or dutch sandwich for them.

need to make a correction.. for

themus.A basis trade is an arbitrage strategy used by investors, particularly hedge funds, to profit from the price difference (the “basis”) between a cash asset and its corresponding futures contract. It involves buying the cheaper asset and selling the more expensive one, aiming to profit when the prices converge at expiration.

The most common form is the Treasury cash-futures basis trade, where investors buy US Treasury securities and sell Treasury futures.

So if Japan’s 250% debt-to-gdp ratio is too high and caused severe problems despite positive trade deficit and largely local ownership, what number for US will be deemed too high?

By some estimates, debt-to-GDP ratio may hit 175% in next 30 years. That clearly is possible if annual deficits stay at 6%. Say nominal growth is 5% and so GDP goes to 130T in 30 years. Annual deficit = 2-8T and so we add on say 5T on an average = 150T of additional debt, resulting in ~200T in total. That is not too far from the 175% estimate in 2056. Clearly a good thing for the SPX, not so much for inflation.

Does this kind of extrapolation break down somewhere in the middle ? Do we expect common sense to return and voters to show some judgment? Or do we expect everyone to be happy with their equity portfolio’s 10X returns, ignoring that inflation went up by 10X as well ?

I saw that the tariff refund portal will be active soon with an estimated 166 billion to be refunded. How will these refunds be paid for by the government? Will new debt have to be issued to cover this?

The US government has $971 billion in its checking account as of Thursday evening. So that will provide the immediate cash.

But yes, long term, the refunds will increase the debt.