It’s ugly, but slightly less ugly.

By Wolf Richter for WOLF STREET.

What portion of tax receipts gets eaten up by interest payments on the monstrous Treasury debt? That’s the question. And we got data on it today for Q4.

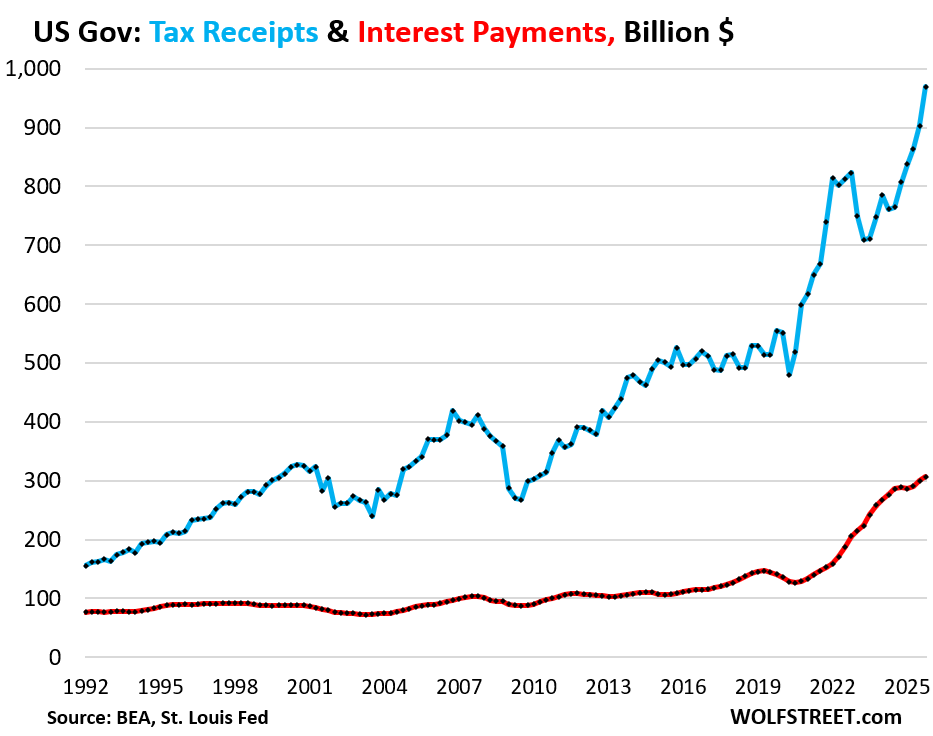

Tax receipts by the federal government jumped by $67 billion (+7.4%) in Q4 from Q3 to a record $902 billion. For the whole year, tax receipts jumped by $456 billion (+14.6%) to $3.57 trillion (blue line in the chart below).

Interest payments by the federal government on its monstrous Treasury debt rose by $7 billion (+2.4%) in Q4 from Q3, to $307 billion (red in the chart below). Interest payments don’t occur in a vacuum, but in the context of funds coming in to pay for them: tax receipts.

This measure of tax receipts, released by the Bureau of Economic Analysis today as part of its revised National Accounts data, tracks the receipts that are available to pay for general budget expenditures, such as interest payments, defense spending, government salaries, etc. Excluded are receipts that are not available to pay for general budget expenditures and are not included in the general budget, primarily Social Security and disability contributions that go into Trust Funds, out of which benefits are paid directly to the beneficiaries, and those payments are also not included in the general budget.

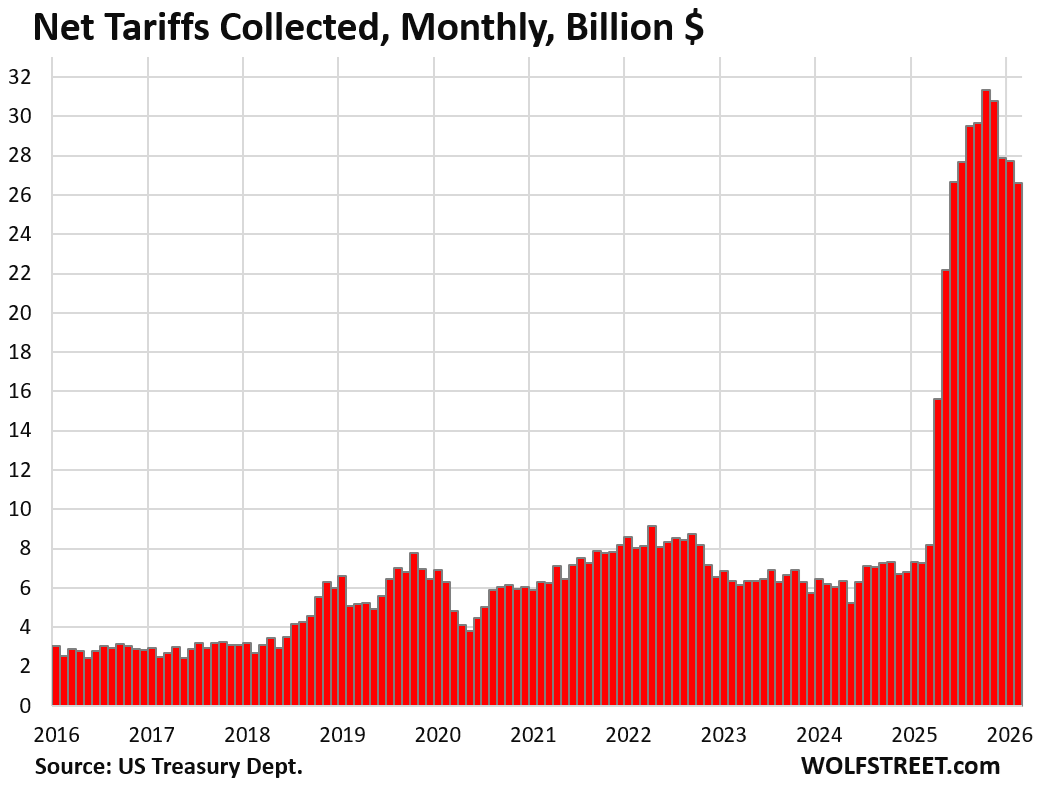

A growing economy generates more taxable income and higher tax receipts – both from corporate and individual taxpayers. Growing asset prices generate capital-gains taxes. But those capital gains tax receipts can drop precipitously when asset prices drop, such as in 2022. In addition, in 2025 there were the revenues from the new tariffs.

Tariffs amounted to $90 billion in Q4. For the past 12 months through February, they amounted to $304 billion, per the most recent Monthly Treasury Statement.

But the Supreme Court struck down part of those new tariffs, and the government will be paying out refunds of some of those tariffs. At the same time, the government already announced replacement tariffs under different laws. So in 2026, net receipts from tariffs, including refunds, will likely be smaller. But that was the situation for Q4.

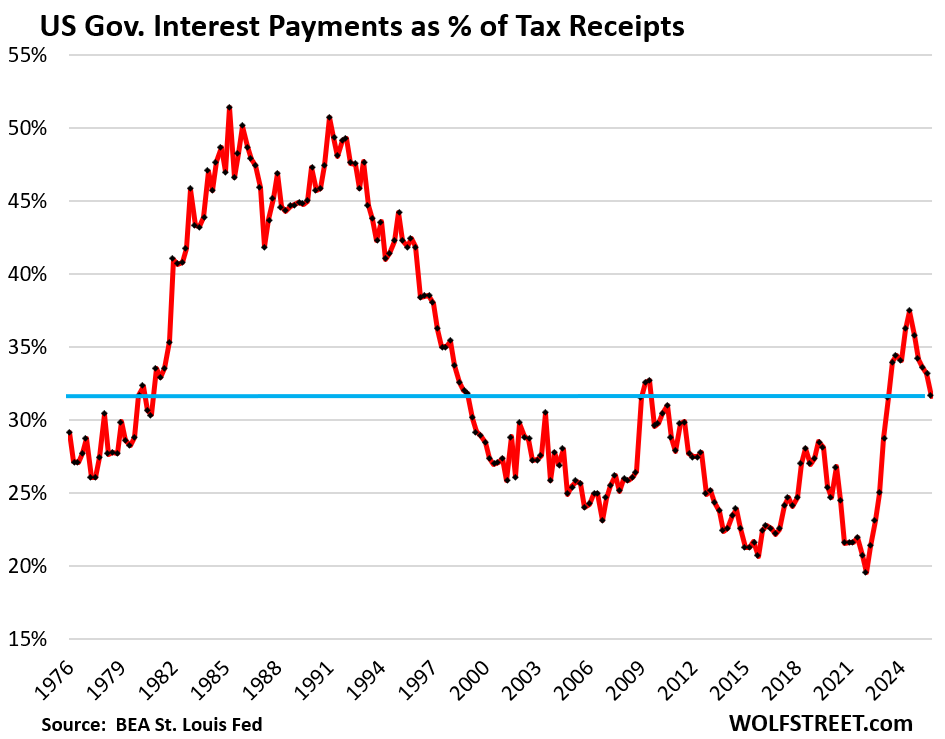

Interest payments as a percent of tax receipts: Interest payments in Q4 ate up 31.6% of the tax receipts available to pay for them.

Ugly, but slightly less ugly than in the prior quarters. The high in Q3 2024, at 37.5%, was the worst ratio since 1996, when the ratio was receding from the crisis times in the 1980s.

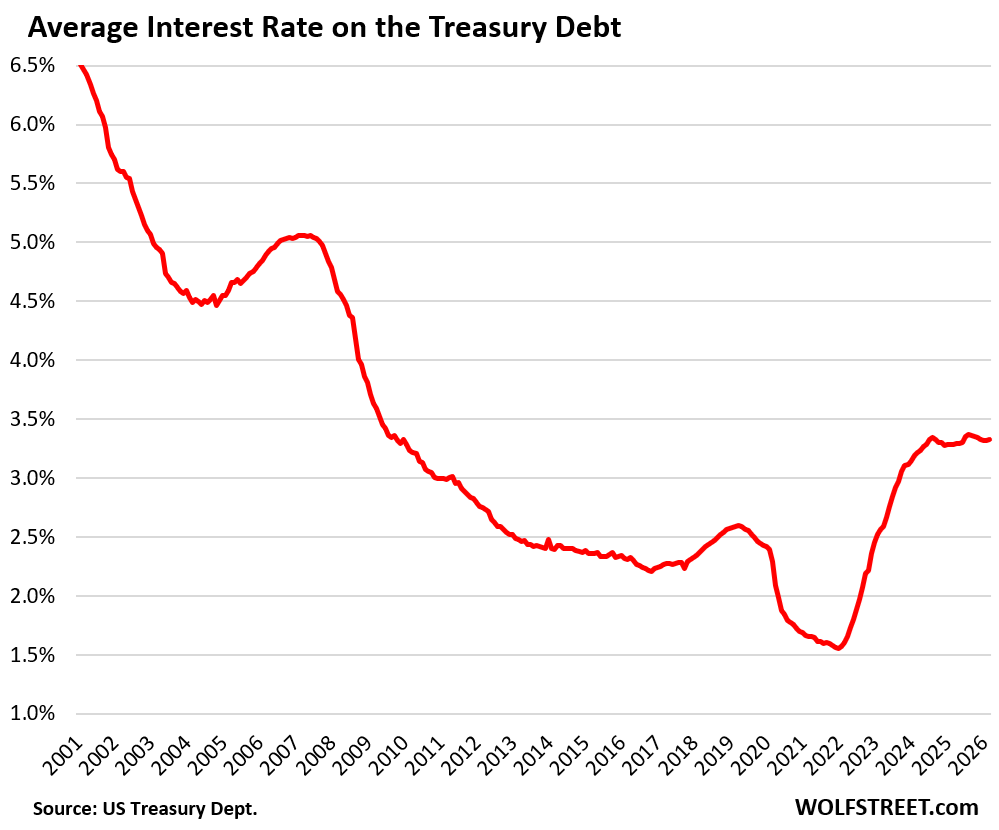

The average interest rate on the Treasury debt was 3.33% in March, according to data from the Treasury Department, having stabilized since Q3 2024 between 3.30% and 3.37%, after more than doubling since the Fed first hiked its policy rates in early 2022:

New interest rates enter the interest expense when old Treasury securities mature and are replaced with new Treasury securities at the new interest rate, and when additional Treasury securities are issued at the new interest rates to fund the deficits.

There are currently $6.8 trillion in Treasury bills outstanding (terms between 1 month and 12 months), and they constantly mature and get refinanced in huge auctions every week, and issuance is also slowly being increased.

As the Fed cut its policy rates, the interest rate that the government paid to sell new T-bills fell from over 5% in mid-2023 to about 3.6% currently, which pushed down on the interest expense.

But when longer-term debt is issued at auction, their interest rates are often higher than the rates of the securities that matured and that they replaced.

Recent 10-year note yields at auction were over double the yield at which the maturing notes had been issued 10 years ago. And the size of the 10-year note auctions has roughly doubled from 10 years ago. So the government paid over double the interest rate on over double the amount, which quadruples the dollar-interest expense on that issue from the issue it replaced.

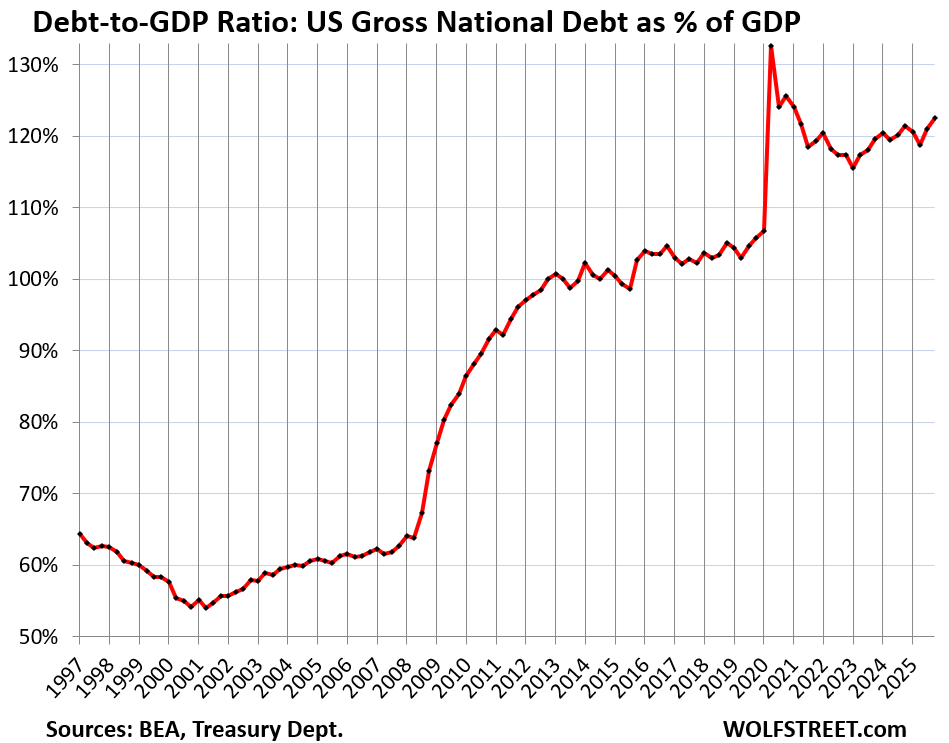

The ugly Debt-to-GDP ratio rose to 122.5% in Q4 and is now back on trend.

The ratio for Q1 and Q2 had dropped because of the effects of the debt ceiling, which prevented the debt from ballooning but drained the government’s checking account. At the beginning of Q3, the debt ceiling was raised, and debt issuance spiked in Q3 and Q4 to refill the government’s checking account.

The pandemic was unique in that GDP collapsed in Q2 2020, while the debt exploded, and the ratio spiked in a breathtaking manner. As GDP bounced off, while the growth of the debt slowed somewhat to still very high growth rates, the ratio backed off through 2022.

But in 2023, it started rising again even as the economy was growing at a rapid rate. The problem has been the $2.2-plus trillion in new debt that was added every year for the past three years by the Drunken Sailors in Washington:

But there won’t be a default on this debt because the US issued this debt in its own currency and can always create more currency to service the debt (the Fed buys some of the debt). So default is not the issue.

The issue is inflation. In an already inflationary environment, creating money to service an out-of-control debt would cause inflation to spiral out of control, crush the economy, and lead to years of wealth destruction and lower standards of living. Everyone knows this – even the people in Washington.

So the go-to hope seems to be to trim the annual deficits a little, including through tariffs, to where economic growth (as per nominal GDP) and modest inflation (3%-5%) outrun the growth of the debt, which would gradually over the years whittle away at the problem and lower the burden of the debt. This scenario assumes that there won’t ever be another recession, good luck with that.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

A very efficient mix of graphs and text, as usual.

Yes! Wolf your communication style is unmatched on the internet. Never change!

So many moving parts, so little discipline.

Wolf, what happens if there’s a recession? It seems like assets can crash like the Dotcom bubble, but then quick intervention restores everything to even a higher baseline. For the Dotcom era and even the Great Recession, asset prices took a while to sort out and then build the momentum from ZIRP / QE. It feels like we are heading towards an economy that can be in recession in definition, but certain assets could be protected regardless.

I mean, is that practically possible? Thoughts?

If there is lots of inflation, there won’t be any intervention. The Fed might let the recession solve the inflation problem on its own.

I believe you have said the quiet part out loud.

Which was exactly the mentality of the 1970s.

People thought: “How can we have stagflation if we are in recession and inflation is plummeting?”

Only when the decade was done did they see the bigger picture which had played out.

Wolf, Chris B., et. al.

There was a time when I was comfortable following all of this but after my stroke, I’m fascinated but confused.

It seems to me the stagflation of the 70s was really a sort of depression in activity because it led to such a massive restructuring of the economy and the loss of millions of jobs.

Perhaps the Fed has this horrible idea as an option but I don’t think the population is in a mood to tolerate anything like that right now.

Wolf, the financial markets collapsed during the Great Depression but the reality was many families did just fine through that time. My great grandparents built a bigger house and hired more help. Please take some pity on those who see depression now- they are among a growing number who are struggling even though the financial markets are thriving. It’s a sort of inverse from my great grandparent’s days.

If the Fed is hoping to follow this narrative, will jobs simply be offshored from China to cheaper countries? This outcome might explain the friction between the Fed and current leadership? I’m afraid we might truly need a massive amount of fairy dust.

Wolf, thank you for your analysis- it’s appreciated.

Has there been any history of the reserve board allowing the nation to enter recession with no action? I can’t think of any. This would be a first. Just interested to know if anyone knows.

Volcker hiked massively into and in the middle of a recession, twice, first in early 1980 and then again in early 1982.

During the recession of 1973-1975, CPI inflation went from 7.4% at the beginning of the recession to 11.8% near the end of the recession. That’s where the term “stagflation” came from: a deep recession and massive accelerating inflation at the same time.

In 1919/1920, the juvenile fed did little to pull us out of the recession following WW1 and Spanish Flu pandemic, but the federal government cut its spending by well over half and approximately a year and a half later the roaring twenties commenced. Basically, the same following WW2 and the 1930’s depression, federal government massively cut spending initiating the strong post war recovery.

Since the private sector funds government, I believe this demonstrates when government becomes an increasingly larger portion of the economy via too much spending, the private sector becomes capital constricted slowing investment in wealth producing ventures. The obvious result is lower tax revenues for government funding and larger debts leading to deficits. It becomes a self-reinforcing downward spiral.

For this reason, I believe congress must cut spending to initiate GDP growth. The fed can assist by refusing to purchase federal debt forcing government to fund through the private sector which will force rates up. More expensive debt service should force congress to cut spending, but there is need to buy votes also.

I want to believe that!

If I could write the perfect fairy tale, it would be something close to your last paragraph.

One might need an unending supply of fairy dust.

High inflation, high interest rates, high nominal growth, negligible real growth. US economy may stay on drugs for the foreseeable future.

I am sure it will make a few more trillionaires. And let the leftover population fend for themselves. For them there will always be squid games, arranged for the Musks and Bezos’s. Where else will the trillions be spent.

I agree

The money tree needs pruning

Time for some tuff luv baby

Wolf, right, Volcker’s “action” was that, the Reserve raised rates. However did any FRB merely let the country enter a recession to kill off inflation? In order words they did not intervene?

Well, the Fed could do a Volcker and hike into a recession rather than do nothing. If you have accelerating hot inflation in a recession, what are you doing to do as a central bank? Make the inflation even worse and destroy the economy?

Better to reign in hell then to serve in heaven

Do you know what made the tax receipts jump so much in Q4?

If Q4 total was 900 Billion

And Q4 Tariffs were 90B, my math says tariffs are only 10%, and I have a fuzzy memory that you cover this percentage before in a previous article.

Is the economy doing so great that tax receipts jumped so much?

But public perception seems to say it’s terrible.

A quagmire!

Tax receipts grew 20% yoy, or by $163 billion, and that doesn’t surprise me, and I don’t think it surprises people who read all my articles here. That’s the result of “letting it run hot.”

It just surprises people who think that everything is constantly collapsing, in a recession, or depression.

Income withholding taxes, estimated quarterly taxes (corporate and individuals), capital gains taxes, tariffs… those are the biggies.

Half of the 20% ($163 billion) yoy growth in tax receipts in Q4 came from the $90 billion in tariffs. Of that $90 billion in tariffs in Q4, $80 billion were new yoy. That $80 billion was just extra. That’s half of the growth in tax receipts. I’ve been talking about the tariffs in numerous articles for a whole year, and how much difference they make. It should surprise no one.

The other half of the 20% growth in tax receipts: Nominal GDP in Q4 was 5.5% higher than a year ago. Quarter to quarter annualized rate of growth of nominal GDP was 4.2% in Q4, 8.3% in Q3, and 6% in Q2. They’re “letting is run hot!”

So, despite the collapse in spending by the federal government due to the lockdown, Q4 had decent economic activity. Q3 nominal growth was hot. So beyond that shutdown issue, there was a lot more strength in the economy. That economic activity generates income taxes. Companies are super-profitable, and that generates taxes. Employment is at record levels, with rising wages, which generates growing income taxes.

There was a HUGE rally in the stock market over the past few years, and that generates enormous amounts of capital gains taxes when investors sell those stocks. Capital gains taxes come and go. After a bad year for stocks, capital gains taxes plunge. You can see that in the chart. They make a huge difference, up and down.

But in 2026, tariffs won’t add to growth in tax receipts anymore. They might slow overall growth of tax receipts.

I’d love to hear your thoughts on the amount of leverage in the financial markets today v historical and how that might impact the markets in a risk off mode.

If inflation persists I as believe it will, the rollover of longer dated treasures as you note will add more pain to the deficit. There could be a colossal unwind of many asset classes as we are in uncharted waters and an unsustainable debt burden that cannot be solved by growth alone. Perhaps IV is way under represented.

The Bond King thinks the real wake up call is around $40T. Right around the corner.

You seem to be saying that tariffs are beneficial to balancing the budget but don’t make clear that 1) tariffs are a tax on consumption, and 2) the way the budget may be balanced is through increased taxes. The latter is correct but it’s it’s now achieved by two dirty tricks – inflation, and claiming exporting countries pay the tariffs. Two dirty tricks that affect the poor more than the rich. Regardless, government spending will keep increasing beyond its income because that’s what we vote for without recognizing that there’s no free lunch.

Your 1 begs qualification.

Tarif is a tax on consumption only so far as it may be passed on to the final consumer. Not every importer, the actual tarif payer, has sufficient pricing power to achieve this. For those, the tarif becomes a tax on corporate profit. This has been demonstrated within these pages by our hosts prior posting of corporate profits over time, as I recall.

Your 2, every tax is someone’s sacred ox. Deciding whose gets gored is politics.

Perhaps we should aggressively breakup monopolies and monopsonies to reduce such pricing power and so protect the poor?

Perhaps we should call money in politics, that sustains the status quo, by it’s proper name, bribery?

Ultimately, we all get what we deserve.

Forgot to add conclusion….

Tariffs are neither intrinsically good or bad. They are just another tool in the box.

It’s the political intent and effect that matters.

The stated goal of onshoring is laudable.

The kak-handed, capricious implementation is not.

Our imported competitors got slapped with some section 232 tariffs to the tune of 10-15%, scheduled to rise to 25% in two years. The market leader raised prices 5% in response, and I assume are still trying to figure out what to do with the rest of the cost pressure without sending customers running for the hills. Still waiting to see how the other importers respond.

We produce 100% domestically and are holding prices flat and actually cutting prices on larger deals. Why? Market share and economies of scale. We’ve been fighting and losing to importers for decades. Now is the time to get aggressive, not complacent.

The tariff response is a lot more nuanced than tariff-haters like to say.

If we’re successful at bringing home some more bacon, it means hiring, overtime opportunity, and a much-needed raise for our American workers.

I 100% agree on enforcing anti-trust laws, but I have zero hope for that happening any time soon.

john overington

“1) tariffs are a tax on consumption,”

BS. they’re tax on corporate profits. Companies are having a very hard time passing income taxes on to their customers. And as a vast body of articles and data published here shows, the passthrough to consumers has been minimal. Most of it is just a corporate income tax. But companies got huge tax cuts in other areas, including new ones for 2025, and they’re not passing on those tax cuts to consumers either 🤣

Let’s hope we don’t get to 5% persistent inflation as that would mean the real value of the dollar would get halved every 15 years.

This would crush anyone receiving a pension without a COLA adjustment, a fixed annuity, or even most 10 and 30 year bond holders since the yields on those have been sub-5% for decades.

I think bond buyers still have their heads buried. The term premium they are accepting the reality in front of them is mind boggling.

I would be interested in Wolf’s and other enlightened folks’ opinions regarding China’s total debt.

I just read this headline:

“China’s government debt has surpassed the European Union’s for the first time, marking a major shift in the global debt landscape”.

Just finished my taxes.

My “total tax” divided by AGI was 3.46%.

It’s never been over 5% for the past ten years. People in more fiscally-responsible countries must be slack-jawed. Maybe I’ll emigrate to your country to avoid the consequences of the US’s coming currency collapse.

If you’re wondering where the ballooning US national debt comes from, it’s because taxes are too damn low on six figure earning millionaires like myself.

5 figure AGI here.

My “total tax” divided by AGI was 7%.

I would think if you and the other millionaire’s. billionaires and trillionaires paid what I did it would help lower….. then again maybe not.

5 figure AGI here also. My total tax divided by AGI was 12.8%. WTF. I also live in FL, so no state income tax. I sincerely don’t understand why there’s such a large spread between us three. No dependents. Filed single.

Gross/Total income will yield correct % rather than AGI as ALL deductions have been subtracted with AGI. I use the standard deduction so don’t have an unlimited supply!

My total tax divided by TAXABLE INCOME was 10.6.

Single retired with SS.

And we wonder why the Federal Debt is $40T?

The government has plenty of tax receipts. If they quit flushing it down the toilet, they would be fine. Income raxes are just one element of tax receipts. The BBB had a huge impact for seniors.

Wolf!!! Looking at tax receipts to interest payments, it looks like we are better off today than in 1990s. Isn’t 1990s supposed to be boom years? Why as the interest payments so high at that time?

The 1990s were the years when the US was finally exiting the crisis of the 1980s.

Chinas debt is owned almost entirely by its own central bank/ regional banks and their localities and citizens. Minuscule amount of foreign held debt.

Not sure how that would effect the world economy

China’s debt ponzi is far bigger than the Fed’s US ponzi.

“ At the end of 2024, the aggregate amount of China’s bond market was RMB 177 trillion, and the aggregate amount of the interbank bond

market was RMB 155.8trillion, accounting for 88% of the aggregate amount of China’s bond market. “

177+155 = 332 trillion RMB @ US$48 trillion

https://www.nafmii.org.cn/englishnew/overseasparticipation/pandabond/resources/202504/P020250423396158840864.pdf