QE hangover a little less atrocious after years of QT and lower interest rates.

By Wolf Richter for WOLF STREET.

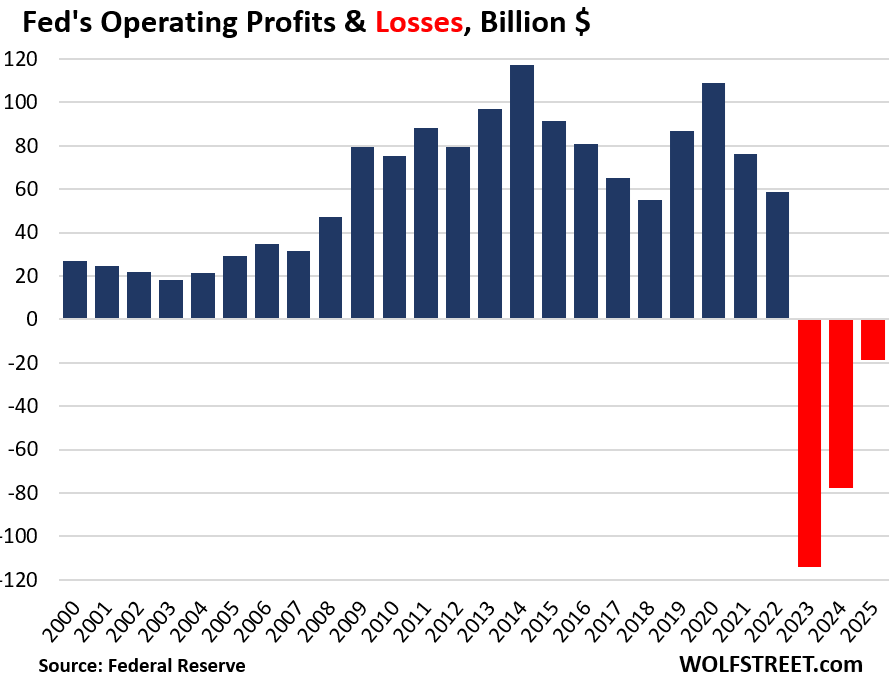

The Fed disclosed in its audited annual financial report today that its results in 2025 were less atrocious than in 2024, which had been less atrocious than peak-atrociousness in 2023 when the hangover from its prior monetary policies of ultra-low interest rates and QE had set in.

This is the consolidated report of the Federal Reserve System consisting of the Federal Reserve Board of Governors – a self-funded federal agency whose governors and chair are nominated by the President and confirmed by the Senate – and the 12 regional Federal Reserve Banks, such as the New York Fed, the San Francisco Fed, the Boston Fed, the Dallas Fed, etc., which are private companies whose shares are held by the largest financial institutions in their districts. The financial report was audited by KPMG.

Today, the Fed disclosed two types of losses:

- An operating loss of $18.7 billion, compared to operating losses of $77.6 billion 2024, and $114 billion in 2023 (red columns in the chart).

- Cumulative “unrealized losses” of $844 billion at the end of 2025, an improvement from the $1.06 trillion at the end of 2024, on its holdings of Treasury securities and MBS.

What happens to the income and losses: The Fed creates its own money and therefore cannot become insolvent. But these losses matter to the Treasury Department – and the taxpayer.

The Fed has to remit nearly all of its operating income to the Treasury Department (similar to a 100% income tax). From 2008 through September 2022, the Fed remitted $1.36 trillion (blue columns in the chart above). At Treasury, these funds became part of the tax receipts. Those remittances stopped with operating losses in September 2022.

The Fed’s income:

- $155.3 billion interest income from its securities portfolio: $106.6 billion from Treasury securities and $48.0 billion from MBS, mostly purchased before 2022. The Fed’s QT reduced its holdings by $2.4 trillion from peak-balance-sheet in mid-2022.

- $3.1 billion in other income, including: $1.6 billion in “foreign currency translation gains”; $0.5 billion from services it provides to banks; and $0.9 billion from “reimbursable services” it provides to government agencies.

The Fed’s interest expenses: $167.4 billion, of which:

- $147.7 billion paid to banks on their Reserve Balances (cash they deposited in their accounts at the Fed, just under $3 trillion at the end of 2025)

- $19.7 billion paid to its counterparties, mostly money market funds, on their overnight reverse repurchase agreements (ON RRP) balances at the Fed, which dwindled to near $0 in 2025.

The interest rate that the Fed pays on reserve balances and the interest rate that the Fed pays ON RRPs are part of the Fed’s five policy rates, respectively 3.65% and 3.50% since the last rate cut in December.

The Fed started hiking its policy rates in March 2022, and on a quarterly basis started booking operating losses in Q4 2022, after years of huge gains. And these rate hikes continued through mid-2023, so its interest expenses ballooned with the rate hikes. In September 2024, the Fed started cutting its interest rates, and its interest expenses began to decline.

At the same time, the Fed began unwinding part of its Treasury and MBS holdings under its QT program. This liquidity drain had the effect of reducing reserve balances and ON RRPs. By the end of 2024, ON RRP balances were near $0, having dropped by over $2 trillion from their peak in 2021. By the end of 2025, reserve balances had fallen just below $3 trillion. And so the dollar amounts the Fed was paying interest on got smaller.

The rate cuts combined with the reduction in ON RRPs and reserve balances reduced the Fed’s interest expense to $167.4 billion in 2025, from the peak of $281 billion in 2023.

The Fed’s operating expenses: $9.8 billion, of which:

- $4.4 billion in salaries at the Federal Reserve Board of Governors and the 12 regional Federal Reserve Banks. By comparison: JP Morgan Chase compensation expenses: $54.5 billion. Truist Financial, a much smaller regional bank: $2.2 billion.

- $2.7 billion in operating expenses of the Federal Reserve Board of Governors including printing and managing the Federal Reserve Notes (the paper dollars)

- Smaller expense items include: $577 million for pension service costs; $352 million for occupancy; $286 million for equipment; $245 million for the Consumer Financial Protection Bureau, which is funded by the Fed.

The “unrealized losses”: $844 billion.

The Fed’s cumulative “unrealized losses” on its holdings of Treasury securities and MBS declined to $844 billion at the end of 2025, from $1.06 trillion at the end of 2024, and from $948 billion at the end of 2023.

Unrealized losses represent the theoretical losses the Fed would have incurred if it had sold all its $6.47 trillion in securities at market prices on December 31, 2025.

These cumulative unrealized losses are the difference between the securities’ amortized cost (which will be equal to face value by the time the security matures) and their market value at the end of the year:

- Securities at amortized cost: $6.47 trillion ($4.39 trillion of Treasuries, $2.08 trillion of MBS)

- Market value at year-end: $5.63 trillion

- Cumulative unrealized loss: $844 billion.

The Fed bought most of these securities years ago when yields were far lower, and therefore market prices a lot higher, than at year-end 2025. As yields on Treasury securities and MBS soared from very low levels starting in late 2020, their market values declined.

For example, at the low point in August 2020, the 10-year Treasury yield had dropped to a silly low of 0.5%, when the hype in the markets was that it would soon turn negative. In October 2023, the 10-year yield briefly kissed 5.0%. That was fun.

The Fed’s unrealized losses declined in 2025 largely because longer-term yields declined modestly between the end of 2024 and the end of 2025, which means that prices of those securities rose. For example, the 10-year Treasury yield declined to 4.18% at the end of 2025, from 4.55% at the end of 2024.

The Fed’s unrealized losses also declined because securities holders get paid face value when the securities mature, and as they get closer to their maturity date, their market value approaches face value, and the unrealized losses diminish and eventually vanish.

MBS are paid back mostly via passthrough principal payments at face value as the underlying mortgages are paid off when the home is sold or refinanced, and as regular mortgage principal payments are made. Even though QT stopped in November 2025, the Fed continues to shed its MBS at the pace of those passthrough principal payments and replaces them with Treasury bills.

Dividend paid: $1.69 billion, up from $1.62 billion in the prior year. Despite the losses, the Fed paid the statutory dividend, as required by the Federal Reserve Act (FRA), to the shareholders of the 12 Federal Reserve Banks, namely the largest financial institutions in their districts.

The largest shareholders got paid a rate equal to the 10-year Treasury yield at the auction just before the dividend payment was made, on the amount of their paid-in capital. Smaller shareholders got paid 6% on their paid-in capital. The dividend rate is capped at 6% for all shareholders, which kicks in when the 10-year Treasury yield rises above 6%, which used to be normal, but hasn’t happened in decades.

The annual report describes the formula laid out in the FRA for how the dividends are calculated.

“The FRA requires each Reserve Bank to pay each member bank an annual dividend based on the amount of the member bank’s paid-in capital stock and a rate determined by the member bank’s total consolidated assets. Member banks with total consolidated assets in excess of a threshold established in the FRA receive a dividend equal to the smaller of 6 percent or the rate equal to the high yield of the 10-year Treasury note auctioned at the last auction held prior to the payment of the dividend. Member banks with total consolidated assets equal to or less than the threshold receive a dividend of 6 percent. The threshold for total consolidated assets was $12.8 billion and $12.5 billion for the years ended December 31, 2025 and 2024, respectively.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Auction today of the five year treasury was almost 4%!

“ $577 million for pension service costs” – so Janet Yellens retirement? Does George Akerloff really need such a cushy home? lol just kidding around.

It’s neat how open all this info is, in light of well uhhh some people not being open about things as a strategy.

I can’t help being frustrated and sick to my stomach as a small business owner also with rental property and the government forced me to utilize and extend all my credit lines to survive while also telling my renters they didn’t have to pay rent. And these jackholes write their own rules and print their own money. The deck is stacked

There is nothing immoral in this:

“The Fed creates its own money and therefore cannot become insolvent. But these losses matter to the Treasury Department – and the taxpayer.”

One of the key points in the Communist Manifesto is the call for the centralization of credit in the hands of the state, which includes the establishment of a national bank with state capital and an exclusive monopoly.