While pundits looked with their magnifying glasses for tariffs in consumer goods prices, it was in services, which are not tariffed, where inflation took off again. Shocker? No

By Wolf Richter for WOLF STREET.

The shocker was the re-acceleration of inflation in services. Services are not tariffed. They include housing costs, medical care, health insurance, auto insurance, subscriptions; telephone, internet, and wireless services; lodging, rental cars, education, movies, concerts, sports events, club memberships, public transportation, water, sewer, trash collection, motor vehicle maintenance and repair, etc. And that’s where inflation re-accelerated.

While the pundits out there were busy searching with their magnifying glasses for signs that tariffs are getting pushed into consumer goods prices, it was in services – especially non-housing core services – where inflation took off again.

Inflation in durable goods (including new vehicles), apparel, and footwear, which catch a substantial part of the tariffs, barely budged, with new vehicle prices dropping, as automakers ate all of the tariffs because they could not pass them on because demand in June was already weak, and what was needed was incentives that translate into price cuts – and we already knew that from their earnings warnings.

But the re-acceleration of inflation in services, especially non-housing services, was just one more nasty surprise that inflation tends to dish up.

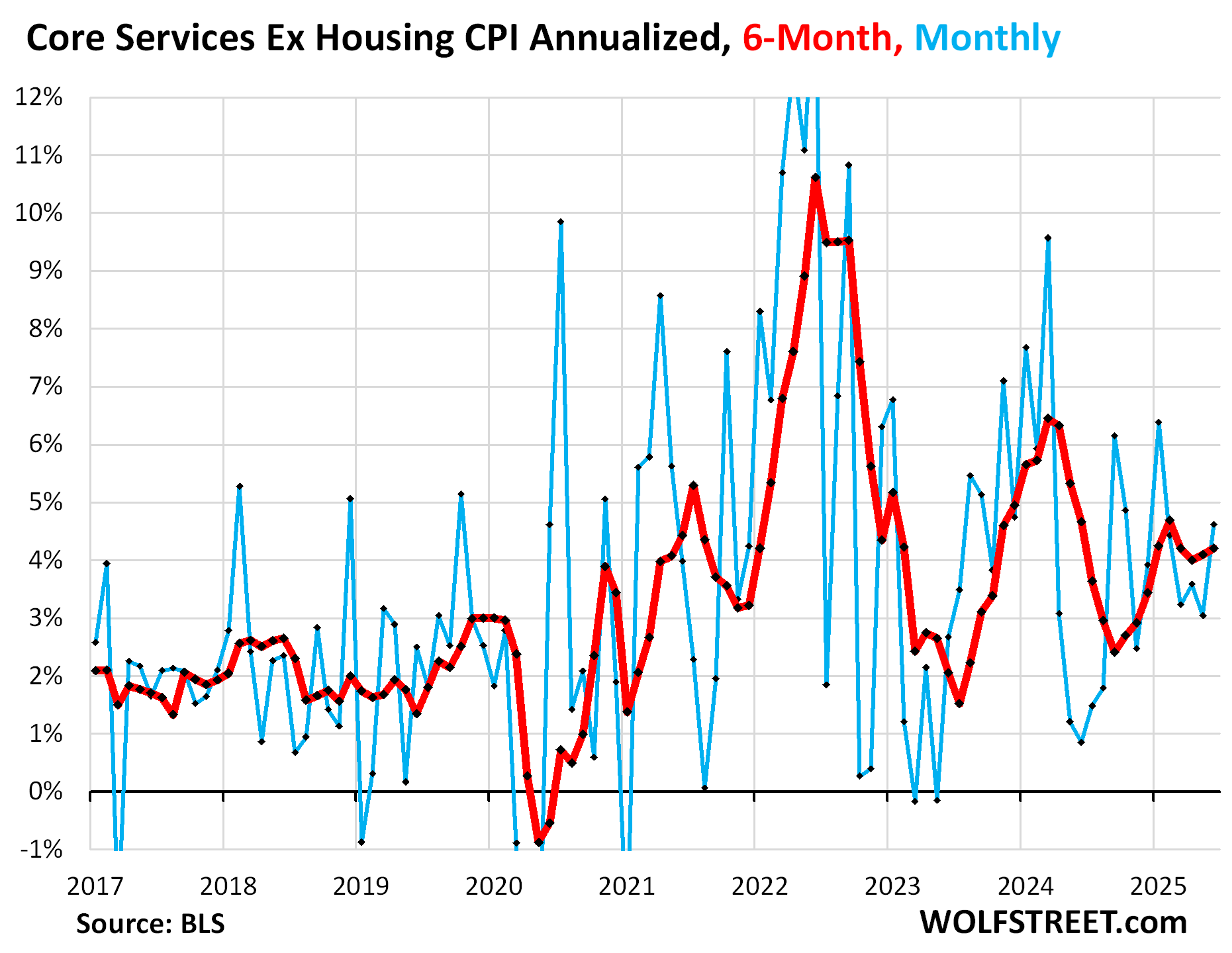

Core services without housing jumped by 0.38% in June from May (+4.6% annualized), the worst increase since January. None of these services are tariffed.

The six-month average accelerated to 4.2% (red in the chart). So that’s a worrisome development.

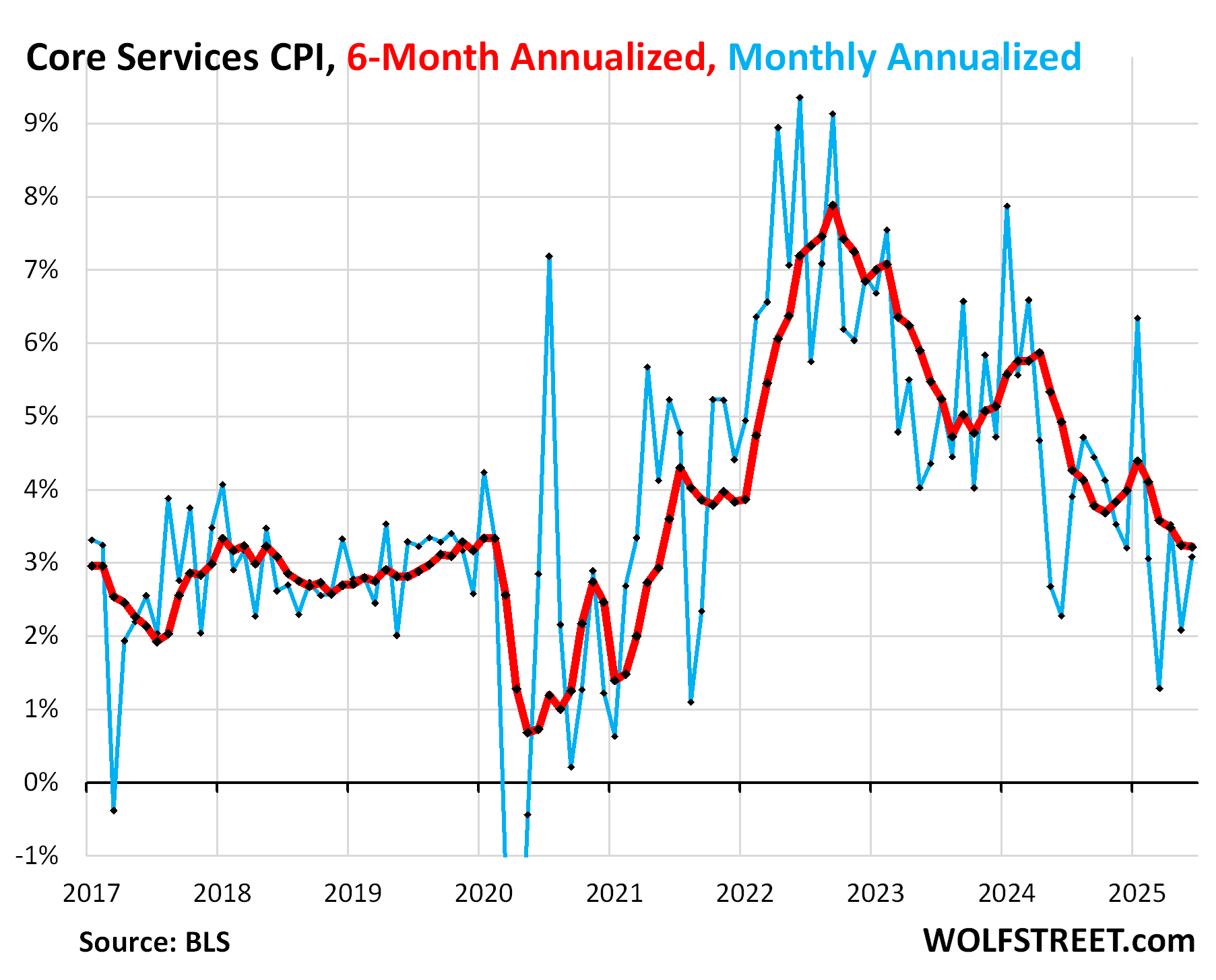

Core services with housing also accelerated. They’re the biggest component of CPI, accounting for nearly two-thirds of overall CPI. They rose by 0.25% in June from May (+3.1% annualized). Housing costs also accelerated in June from May; more in a moment.

The six-month core services CPI rose by 3.2%, same as in May.

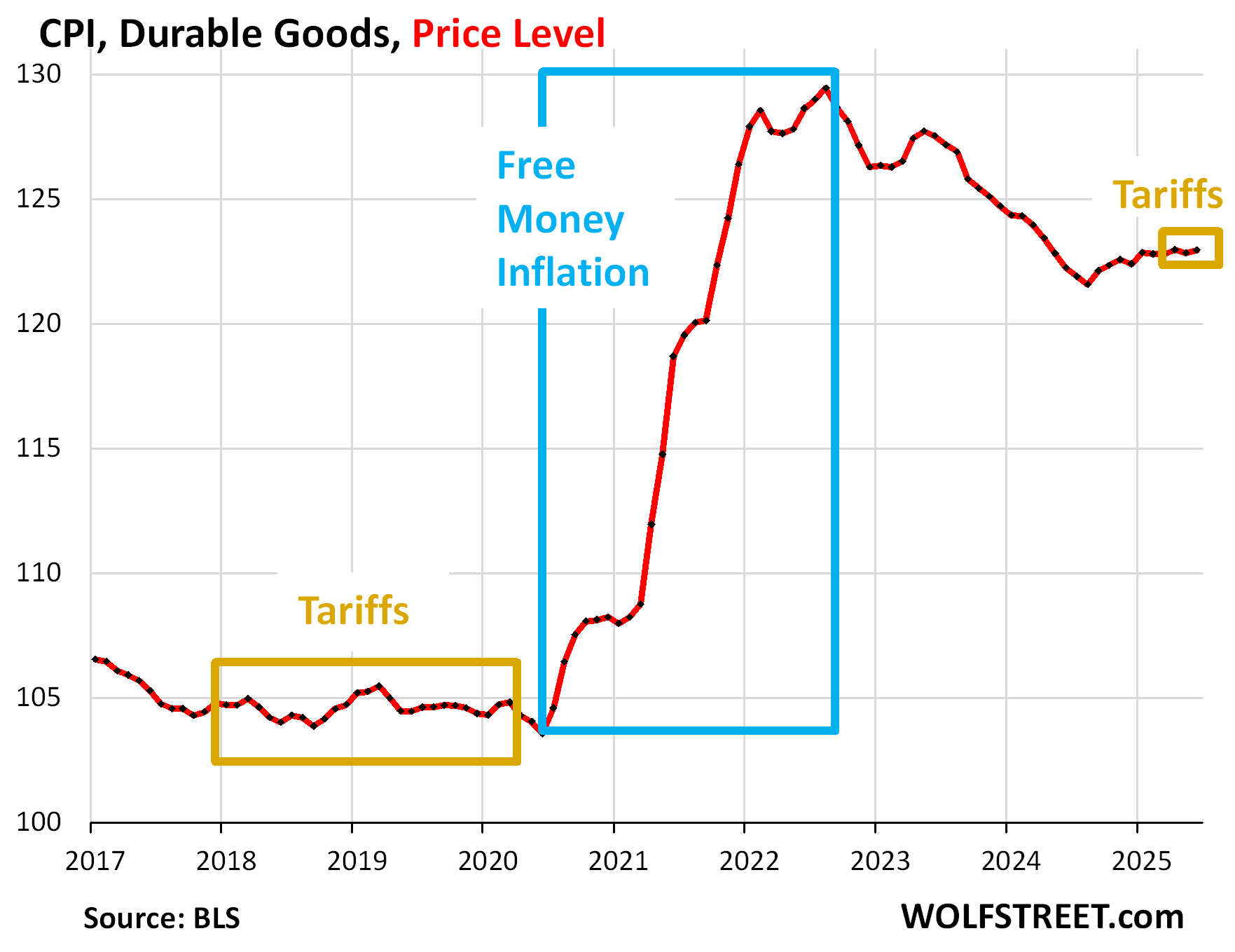

Durable goods prices barely budged, inching up 0.09% (+1.1% annualized) in June from May, and year-over-year were up just 0.6%.

The durable goods CPI had spiked by 25% during the free-money era. Then in mid-2022, prices declined for two years (negative CPI), but from September 2024, prices inched up again through January, and since then have been roughly flat.

This chart shows the price index, not the percentage change. It clarifies just how violently prices spiked during the free-money era, how they declined for two years, and how they’ve inched higher from the low point last fall.

Apparel and footwear are also tariffed if imported, and much of it is imported. The CPI for apparel and footwear rose by 0.4% month-to-month, undoing the equal drop in May, with no price change over the two-month period.

Year-over-year, the CPI for apparel and footwear declined by 0.5% (deflation).

The chart shows the price level (not the percentage change). So prices remain below where they’d been for the last nine months in 2024.

So far, companies have eaten the tariffs because prices are already high from the 2020-2022 burst of inflation, when consumers were willing to pay whatever, and companies made record huge profits; for now, consumers are not willing to pay whatever again. Raise prices and they will not come.

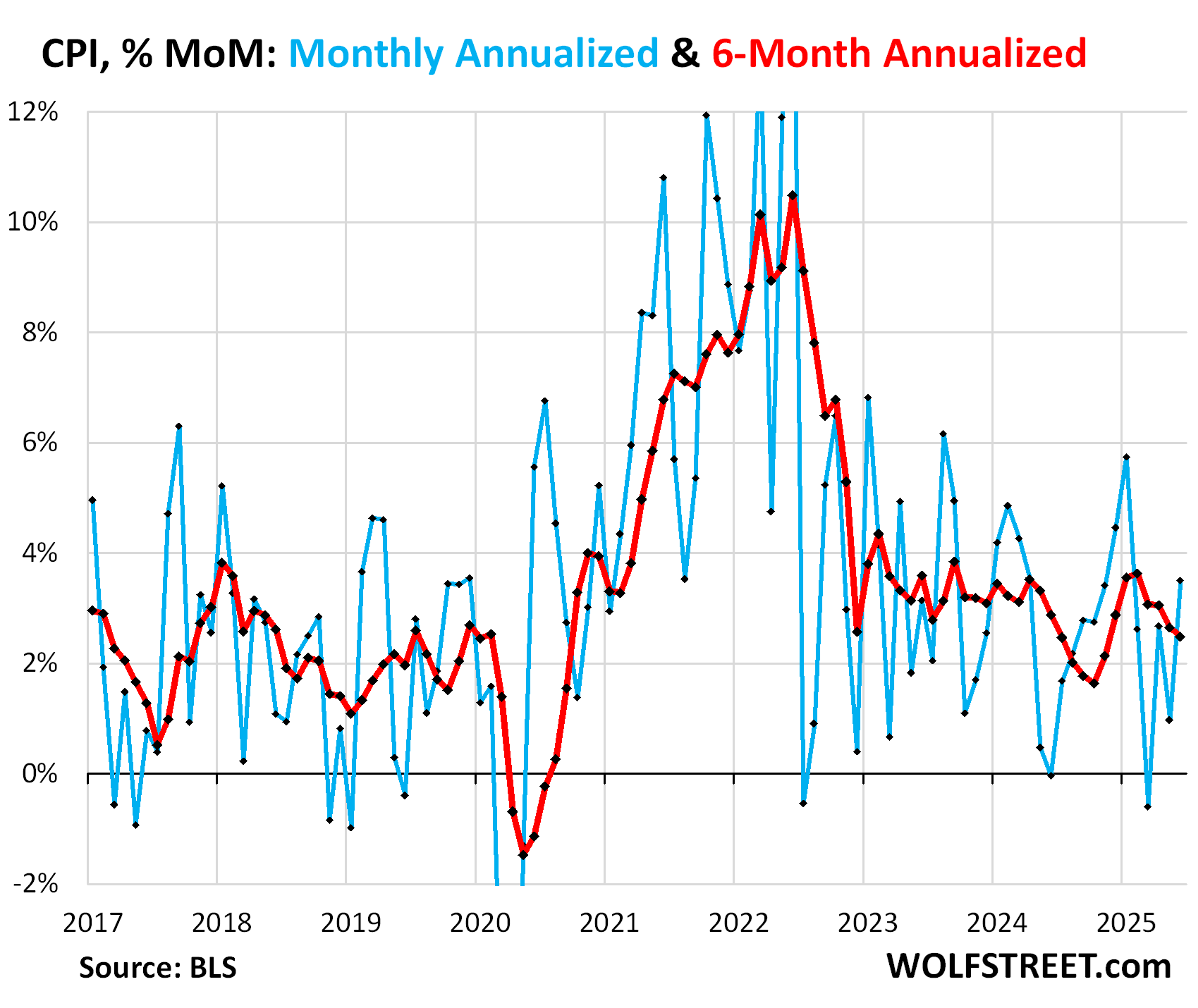

The overall CPI rose by 0.29% (+3.5% annualized) in June from May, a sharp acceleration, and the biggest month-to-month increase since January (blue in the chart), driven by services and energy (natural gas, electricity, and gasoline).

The 3-month CPI jumped by 2.4% annualized, the highest since March.

The 6-month CPI rose by 2.5% annualized, a deceleration of the prior months (red in the chart).

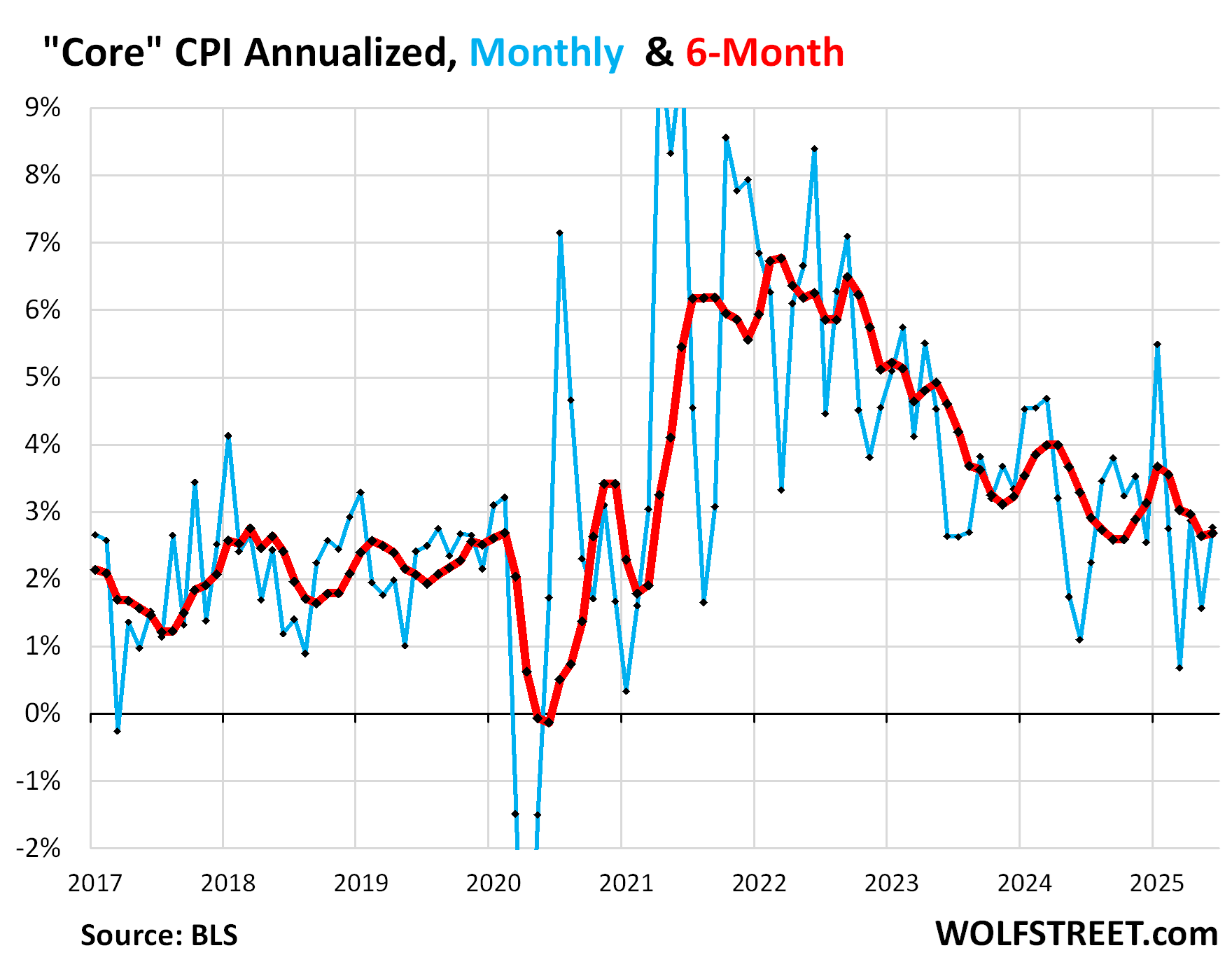

“Core” CPI, which excludes food and energy components to track underlying inflation, accelerated to +0.23% in June from May (+2.8% annualized).

The 6-month “core” CPI rose by 2.7% annualized, a slight acceleration from May (red).

Major components of CPI, year-over-year price changes:

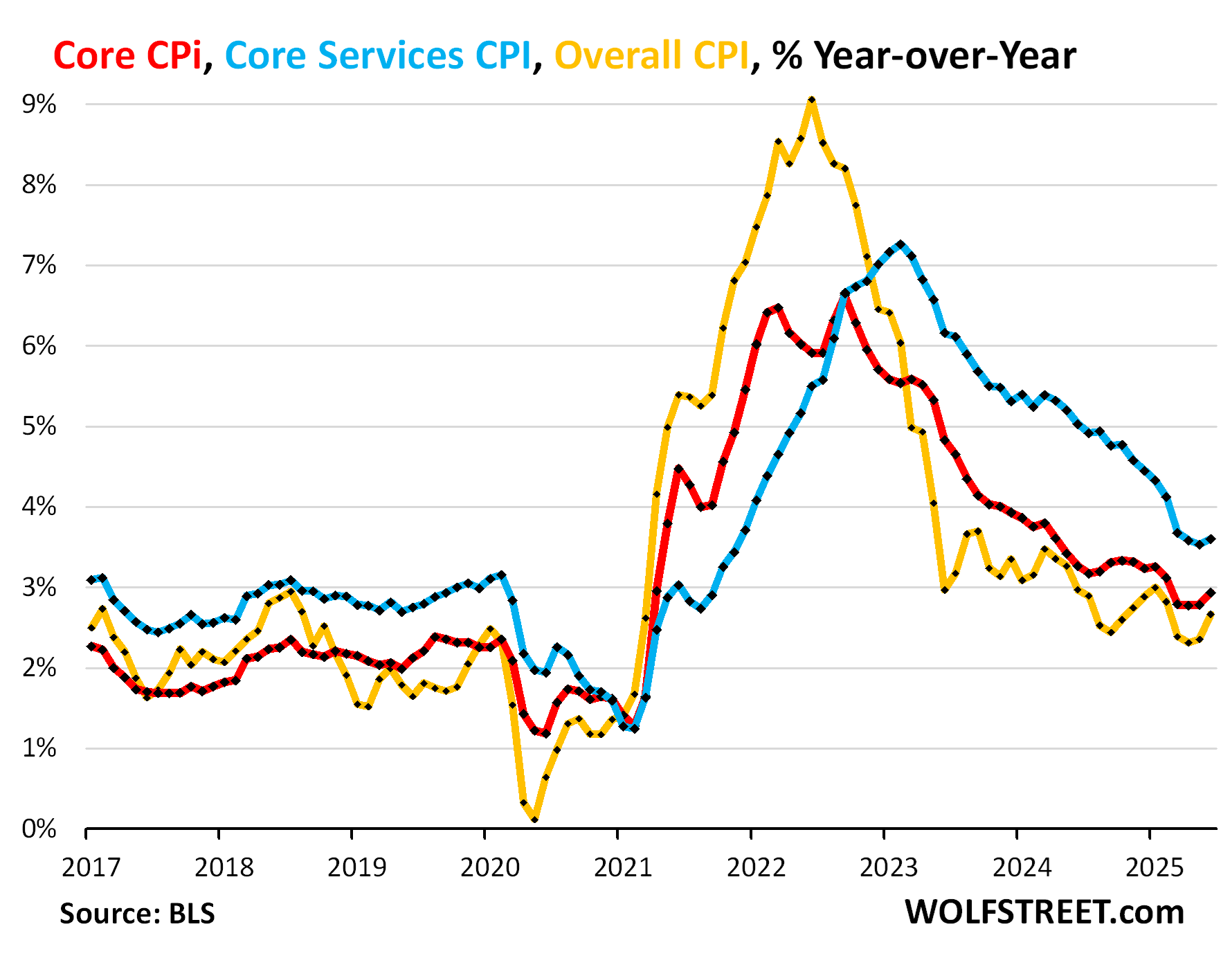

- Overall CPI: +2.7% (yellow), a sharp acceleration from May, the second acceleration in a row, and the biggest increase since February, despite a year-over-year drop in energy prices.

- Core CPI +2.9% (red), an acceleration from May.

- Core Services CPI: +3.6% (blue), an acceleration from May.

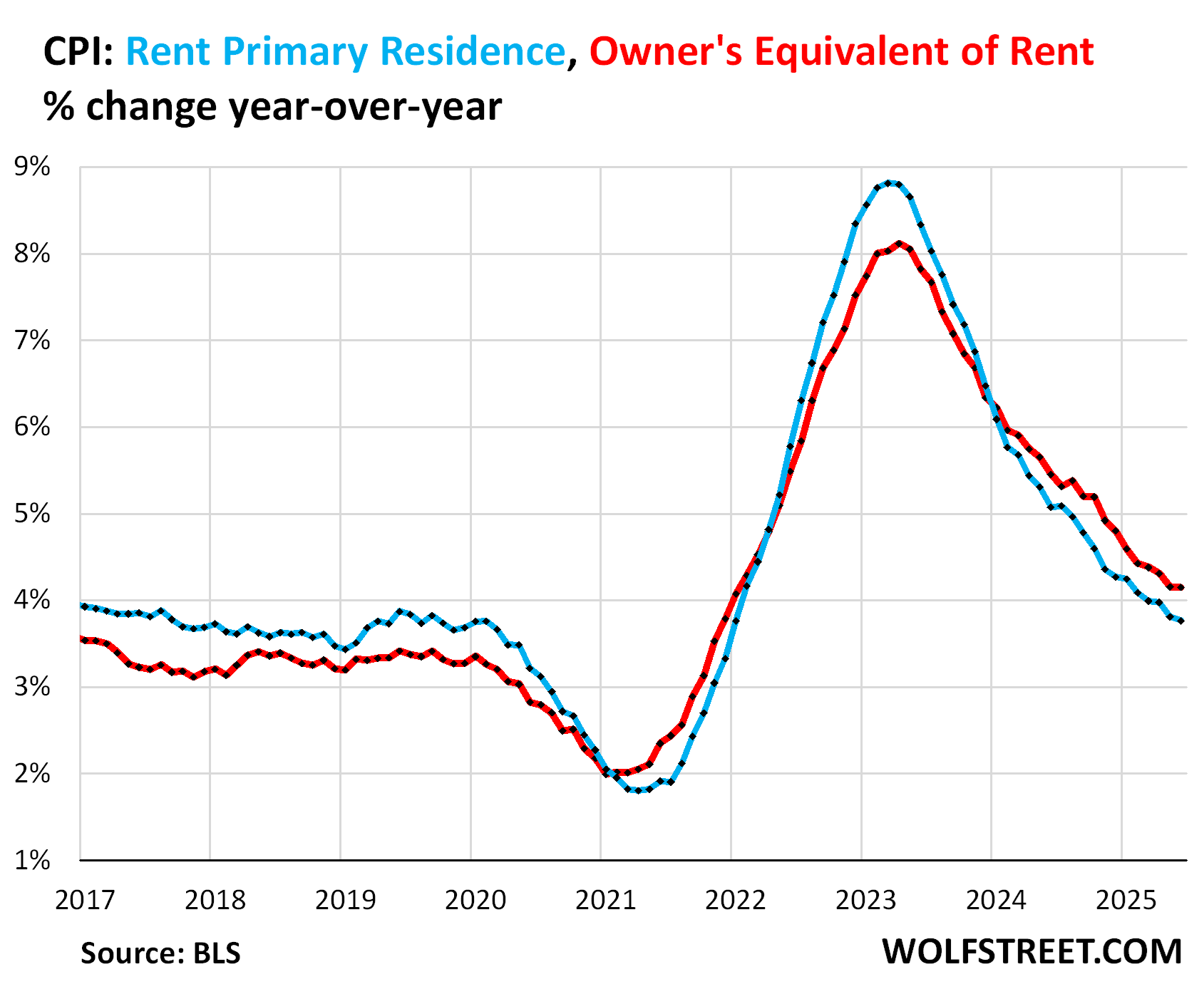

Housing components of core services.

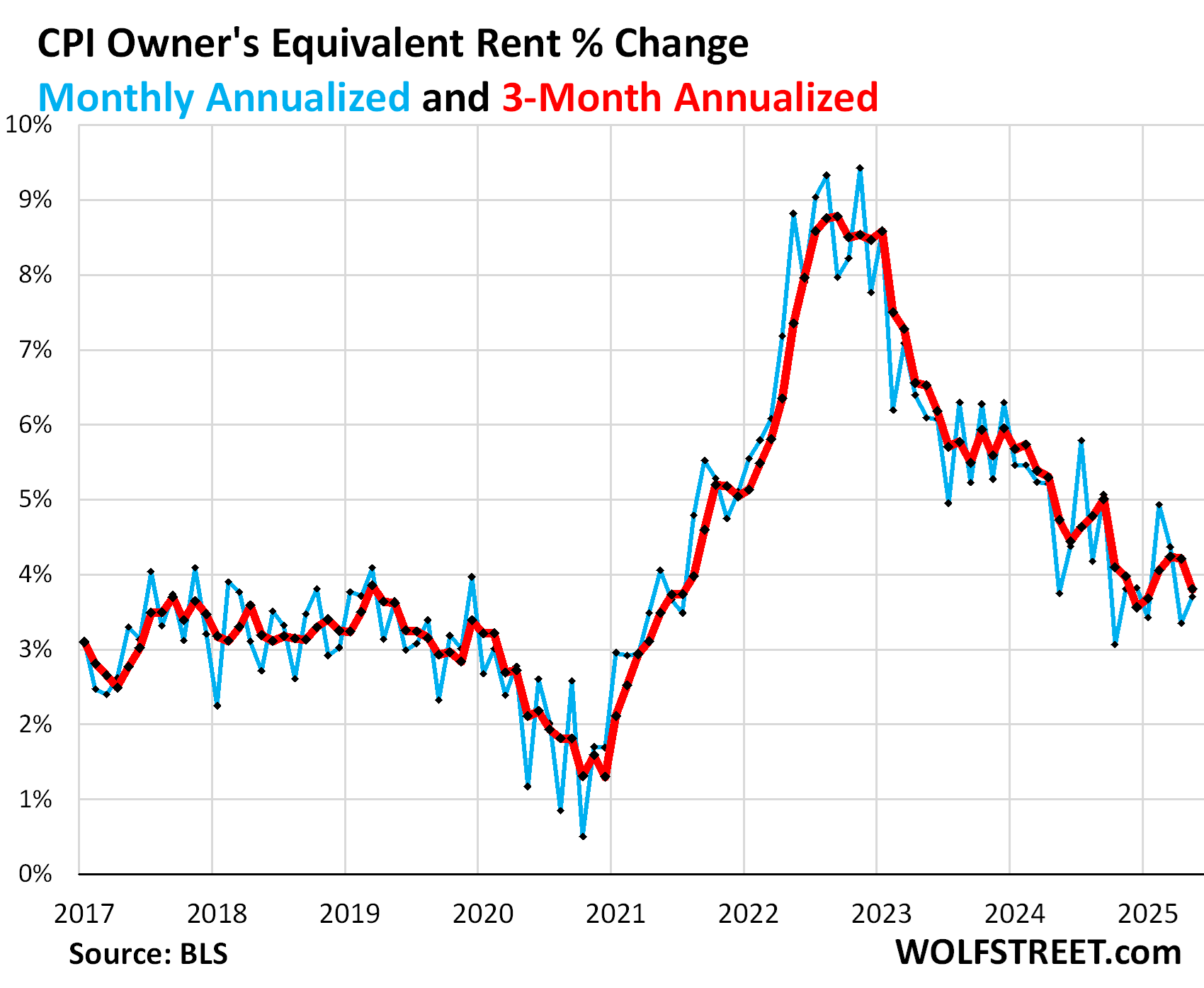

Owners’ Equivalent of Rent CPI accelerated to +0.30% (+3.7% annualized) in June from May.

The three-month average decelerated to +3.8% annualized, still a faster pace than late last year.

OER indirectly reflects the expenses of homeownership: homeowners’ insurance, HOA fees, property taxes, and maintenance. It’s the only measure for those expenses in the CPI. It is based on what a large group of homeowners estimates their home would rent for, with the assumption that a homeowner would want to recoup their cost increases by raising the rent.

As a stand-in for homeowners’ expenses, OER accounts for 26.2% of overall CPI and estimates inflation of shelter as a service for homeowners.

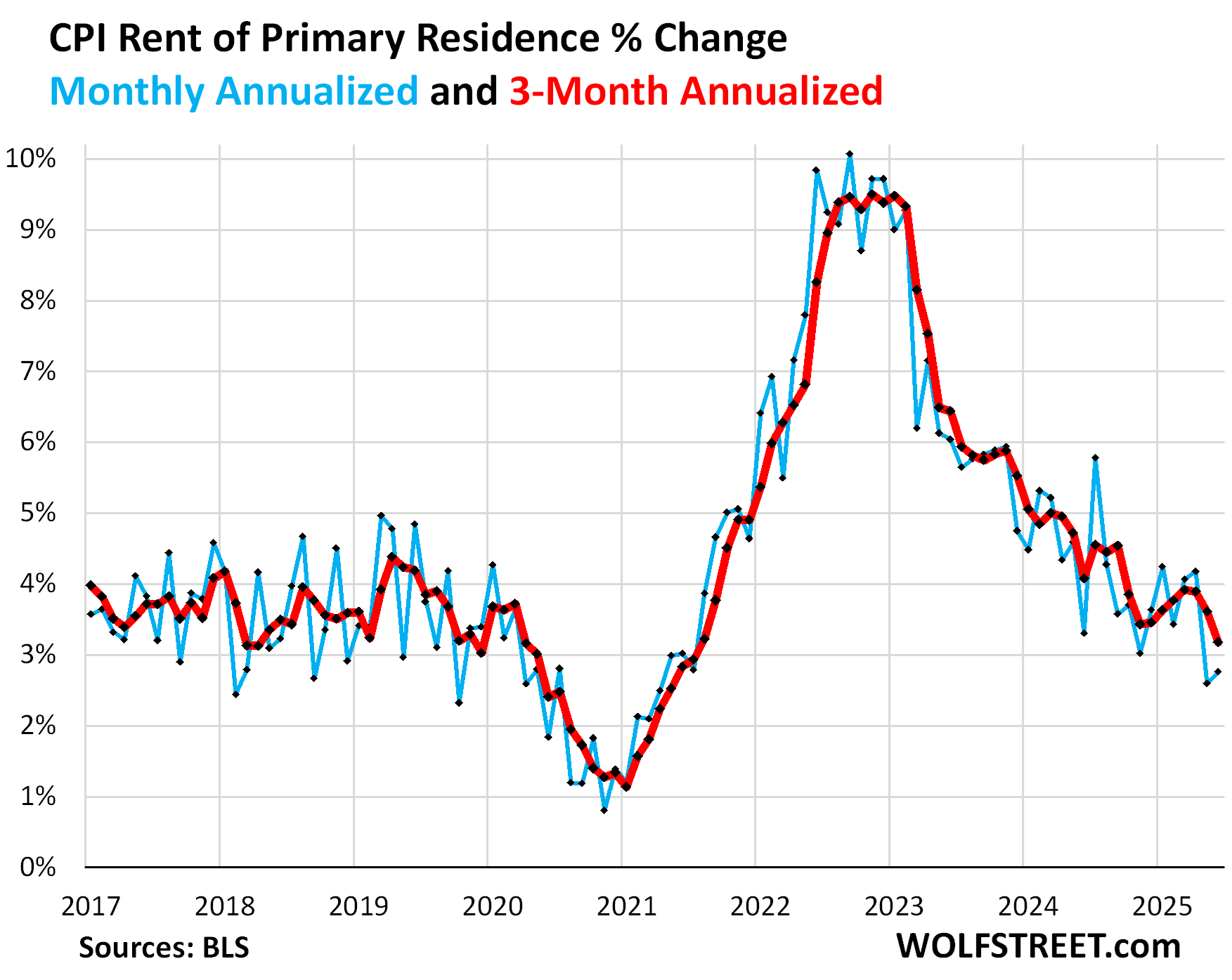

Rent of Primary Residence CPI accelerated a hair to +0.23% (+2.75% annualized) in June from May, after the sharp deceleration in May.

The 3-month rate decelerated to +3.2% annualized, the lowest since August 2021.

Rents are no longer the driver of services inflation – the drivers are now in other services summarized by the “core services CPI without housing” in the first chart above.

Rent CPI accounts for 7.5% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised vacant units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants, who come and go, pay in rent for these units.

Year-over-year, OER rose by 4.2%, same increase as in May, and still substantially higher than before the pandemic (red in the chart below).

Rent CPI (blue in the chart below) rose by 3.8%. It is now back in the same range as before the pandemic.

The historically unusual situation of the OER running hotter than rent CPI may be due to the surging costs of homeowner’s insurance, which homeowners may be taking into consideration when estimating how much their home would rent for.

The table below shows the major categories of “core services.” Combined, they accounted for 64% of total CPI:

| Major Services ex. Energy Services | Weight in CPI | MoM | YoY |

| Core Services | 64% | 0.3% | 3.6% |

| Owner’s equivalent of rent | 26.2% | 0.3% | 4.2% |

| Rent of primary residence | 7.5% | 0.2% | 3.8% |

| Medical care services & insurance | 6.7% | 0.6% | 3.4% |

| Food services (food away from home) | 5.6% | 0.4% | 3.8% |

| Motor vehicle insurance | 2.8% | 0.1% | 6.1% |

| Education (tuition, childcare, school fees) | 2.5% | 0.2% | 3.4% |

| Admission, movies, concerts, sports events, club memberships | 2.0% | 0.2% | 4.0% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.6% | 0.6% | 4.3% |

| Public transportation (airline fares, etc.) | 1.5% | -1.8% | -5.6% |

| Telephone & wireless services | 1.5% | -0.3% | -0.5% |

| Lodging away from home, incl Hotels, motels | 1.3% | -2.9% | -2.5% |

| Water, sewer, trash collection services | 1.1% | 0.4% | 5.4% |

| Motor vehicle maintenance & repair | 1.0% | 0.2% | 5.2% |

| Internet services | 0.9% | 0.5% | -2.3% |

| Video and audio services, cable, streaming | 0.8% | 0.2% | 3.0% |

| Pet services, including veterinary | 0.5% | 0.7% | 5.6% |

| Tenants’ & Household insurance | 0.4% | 1.1% | 4.8% |

| Car and truck rental | 0.1% | 3.2% | 3.8% |

| Postage & delivery services | 0.1% | 0.4% | 3.1% |

Details on durable goods prices.

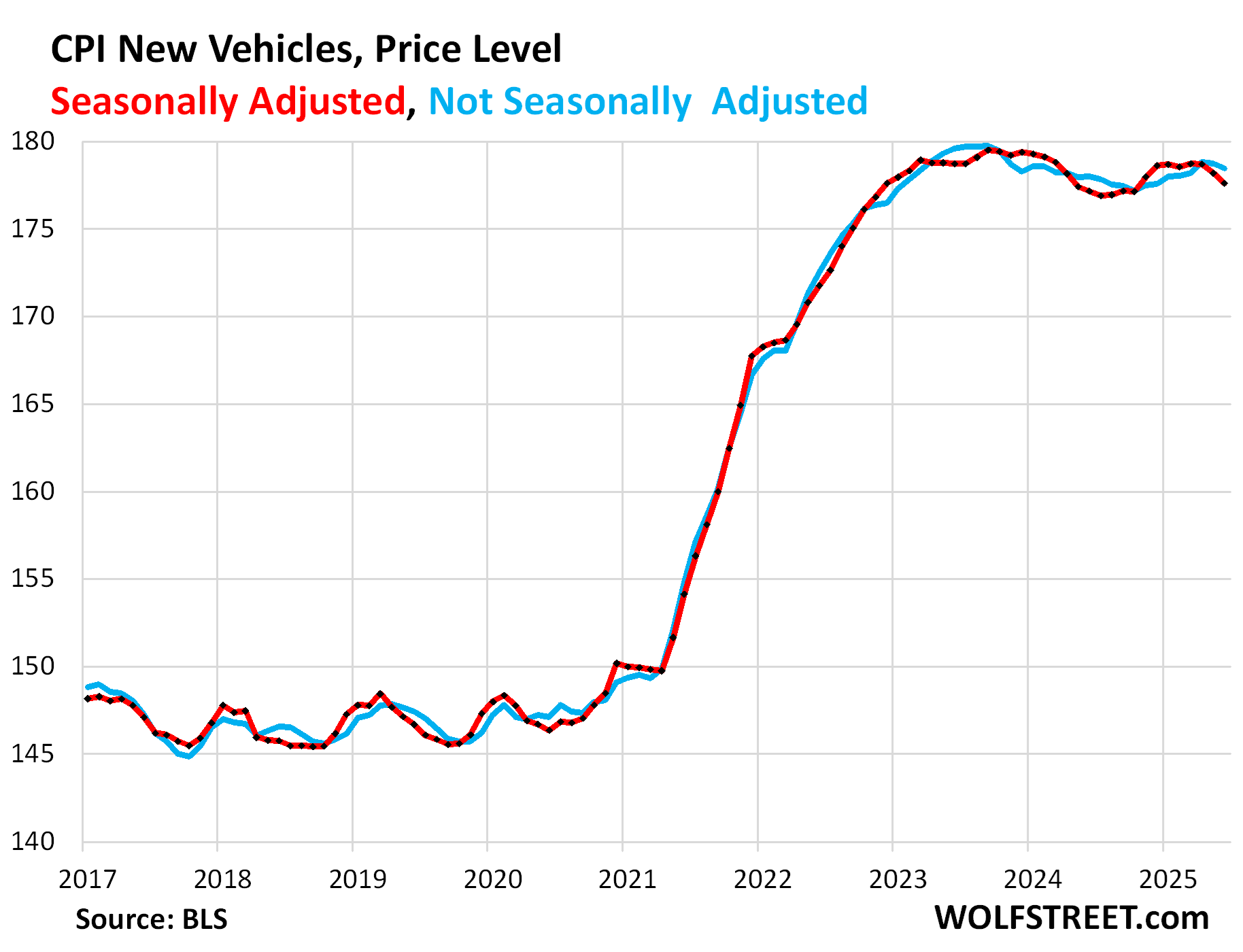

New vehicles CPI declined by 0.34% (-4.0% annualized) in June from May, the third month in a row of declines, seasonally adjusted.

Year-over-year, the index edged up by 0.2%. The price level remains below where it had been in all of 2023 and in the first part of 2024.

The spike during the free-money era, which resulted in massive historic profits for automakers and dealers, drove prices to the economic limit beyond which higher prices kill demand, and prices cannot be raised, and tariffs cannot be passed on to consumers without crushing sales, and automakers know it, and disclosed in their earnings warnings that they’re eating the tariffs, and that they’re trying to dodge them by shifting more production to the US.

GM, which makes a large portion of its US vehicles in Mexico, China, South Korea, and Canada, and moved much of its supply chains overseas, is among the hardest-hit. Tesla and Honda, whose vehicles are among those with the most US content, are among the least hit.

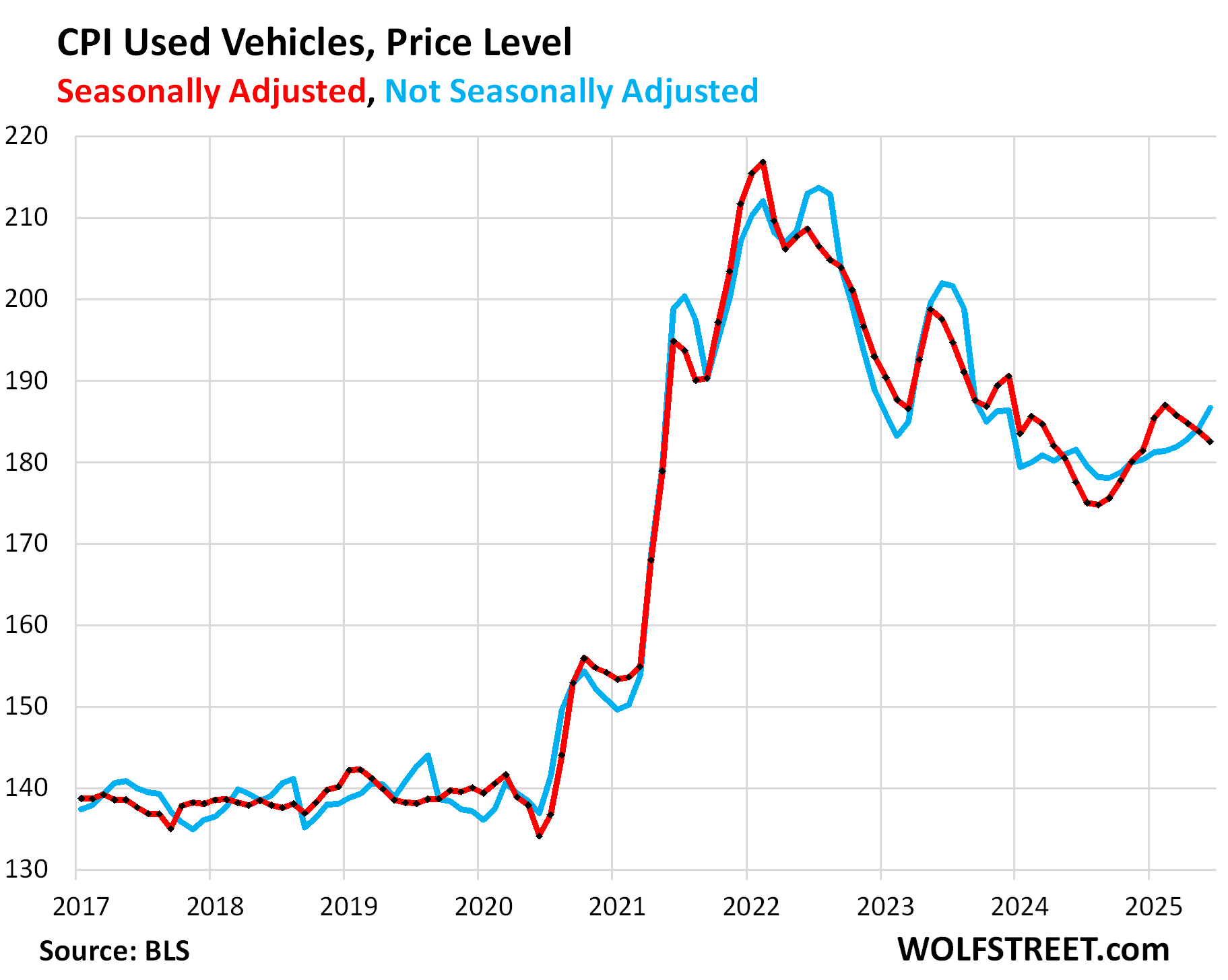

Used vehicle CPI fell by 0.7% in June from May (-7.8% annualized), seasonally adjusted.

Year-over-year, used vehicle prices rose by 2.8%, the sixth month in a row of year-over-year increases, and the biggest one yet. But the year-over-year comparisons are hitting the low point of the price plunge.

| Major durable goods categories | MoM | YoY |

| Durable goods overall | 0.1% | 0.6% |

| New vehicles | -0.3% | 0.2% |

| Used vehicles | -0.7% | 2.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 1.0% | 1.7% |

| Sporting goods (bicycles, equipment, etc.) | 1.4% | -2.5% |

| Information technology (computers, smartphones, etc.) | 0.0% | -4.7% |

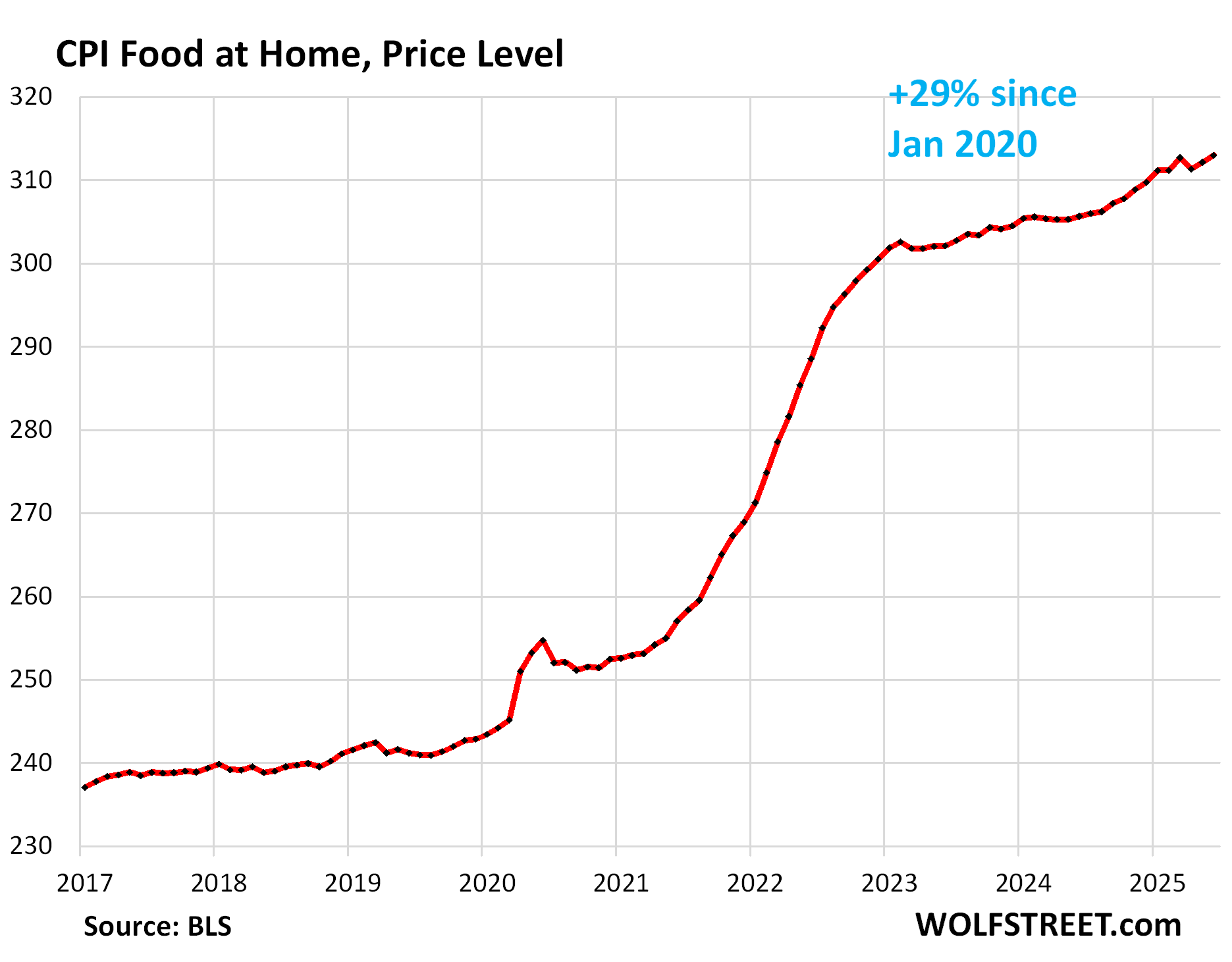

Food Inflation. The CPI for “Food at home” rose by 0.28% in June from May (+3.4% annualized). Beef has been the culprit for a long time and has become extremely expensive. But egg prices continued to plunge, as they unwind their avian-flu-driven price spike.

Year-over-year, the index rose by 2.4%. Since January 2020, food prices have surged by 29%.

| MoM | YoY | |

| Food at home | 0.3% | 2.4% |

| Cereals, breads, bakery products | -0.2% | 1.1% |

| Beef and veal | 2.0% | 10.6% |

| Pork | -0.3% | 0.5% |

| Poultry | 0.6% | 3.4% |

| Fish and seafood | 0.1% | 0.9% |

| Eggs | -7.4% | 27.3% |

| Dairy and related products | -0.3% | 0.9% |

| Fresh fruits | 1.3% | 3.4% |

| Fresh vegetables | 0.6% | -1.3% |

| Juices and nonalcoholic drinks | 1.7% | 3.0% |

| Coffee, tea, etc. | 0.7% | 7.8% |

| Fats and oils | 0.4% | -1.4% |

| Baby food & formula | 0.9% | 1.8% |

| Alcoholic beverages at home | -0.2% | -0.1% |

Energy.

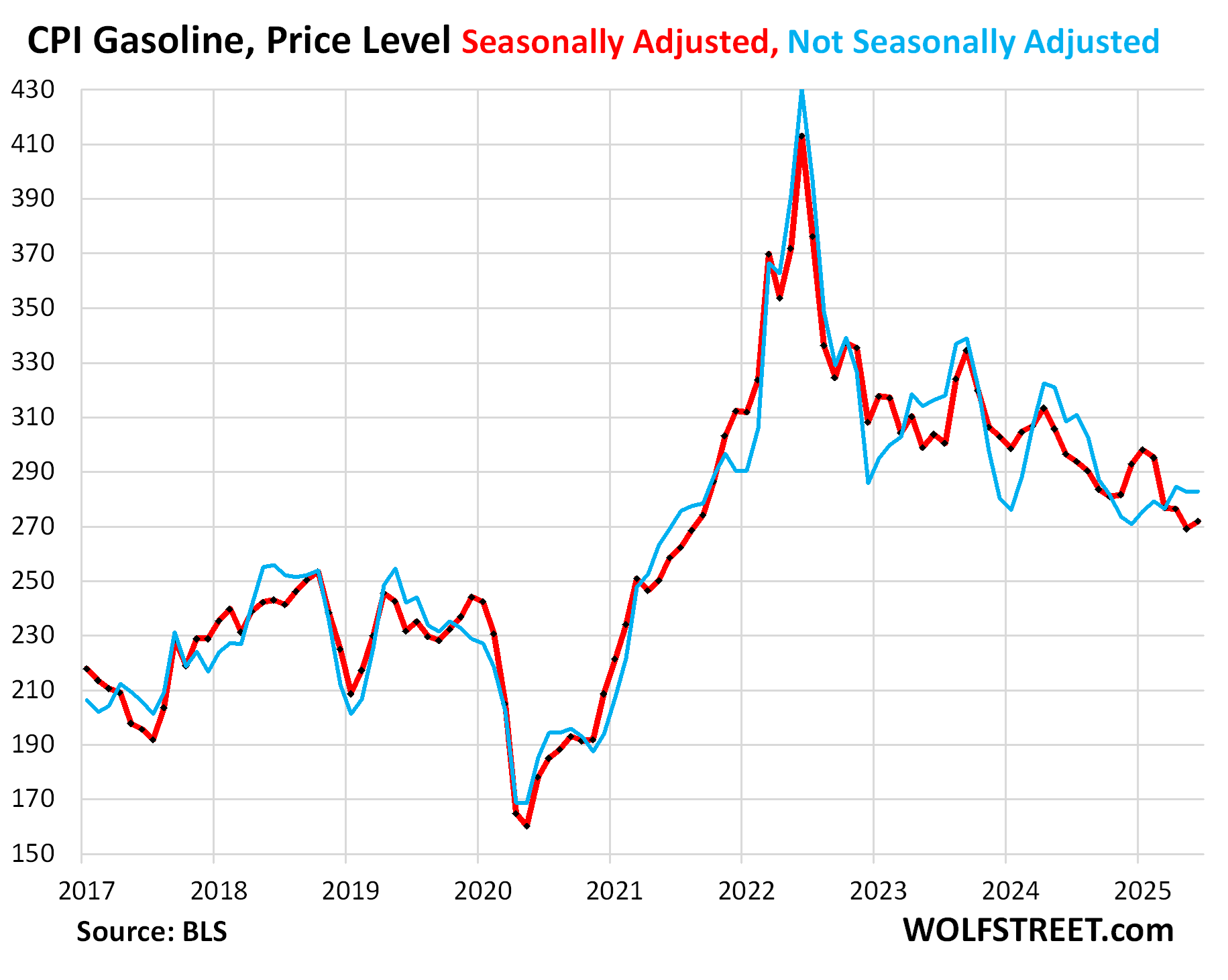

The CPI for gasoline rose 1.01% in June from May, seasonally adjusted. In May, prices had dropped to the lowest level since September 2021.

Year-over-year, the gasoline index fell by 8.3%, on lower oil prices. Gasoline makes up about half of the overall energy CPI.

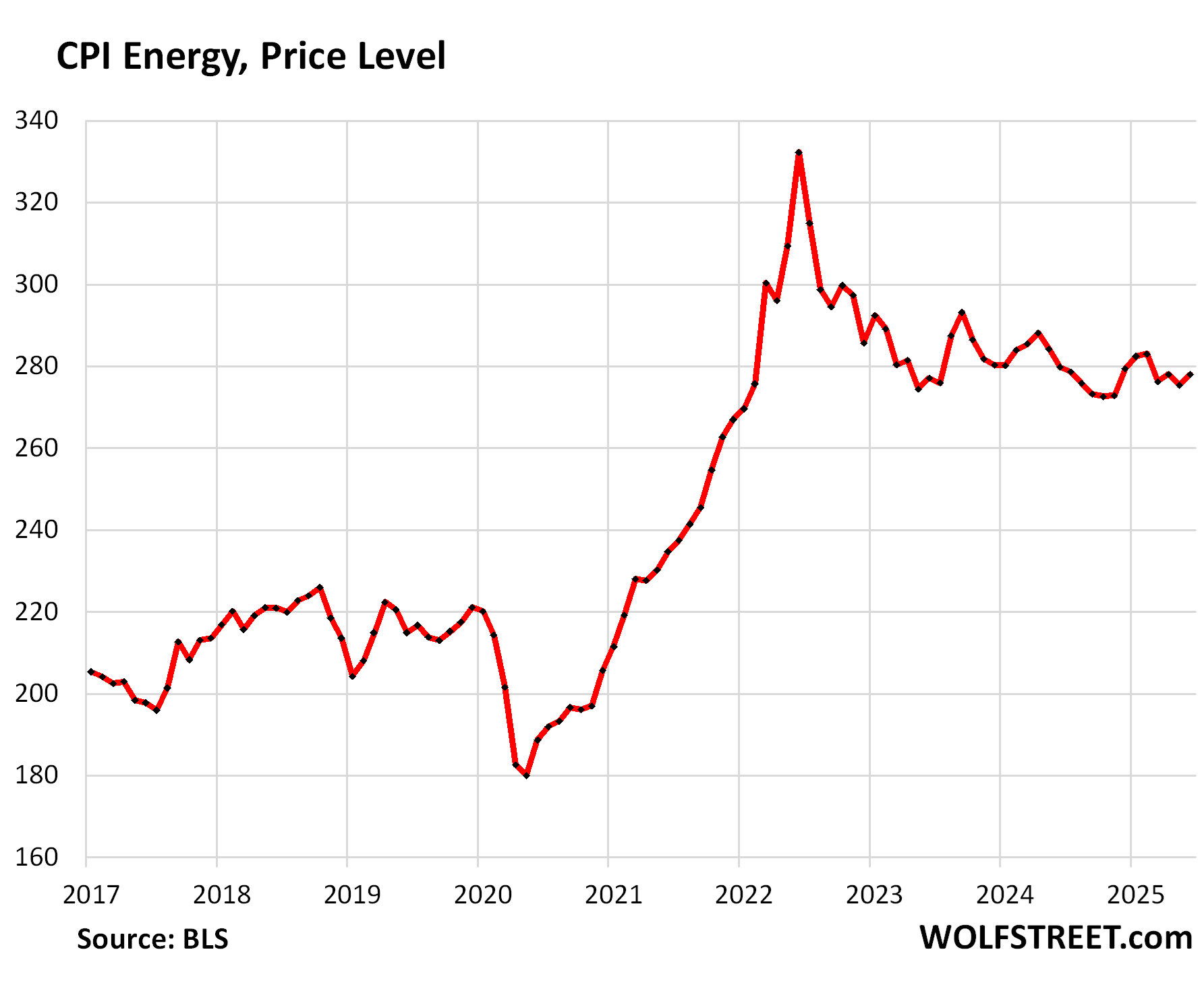

The CPI for energy overall jumped by 0.95% month-to-month. On a year-over-year basis, the index still dipped by 0.8%. Despite the ups and downs, the index has essentially been flat for two years, but at much higher levels than before the pandemic.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 0.9% | -0.8% |

| Gasoline | 1.0% | -8.3% |

| Electricity service | 0.9% | 7.5% |

| Utility natural gas to home | 0.5% | 14.2% |

| Heating oil, propane, kerosene, firewood | 1.0% | -2.0% |

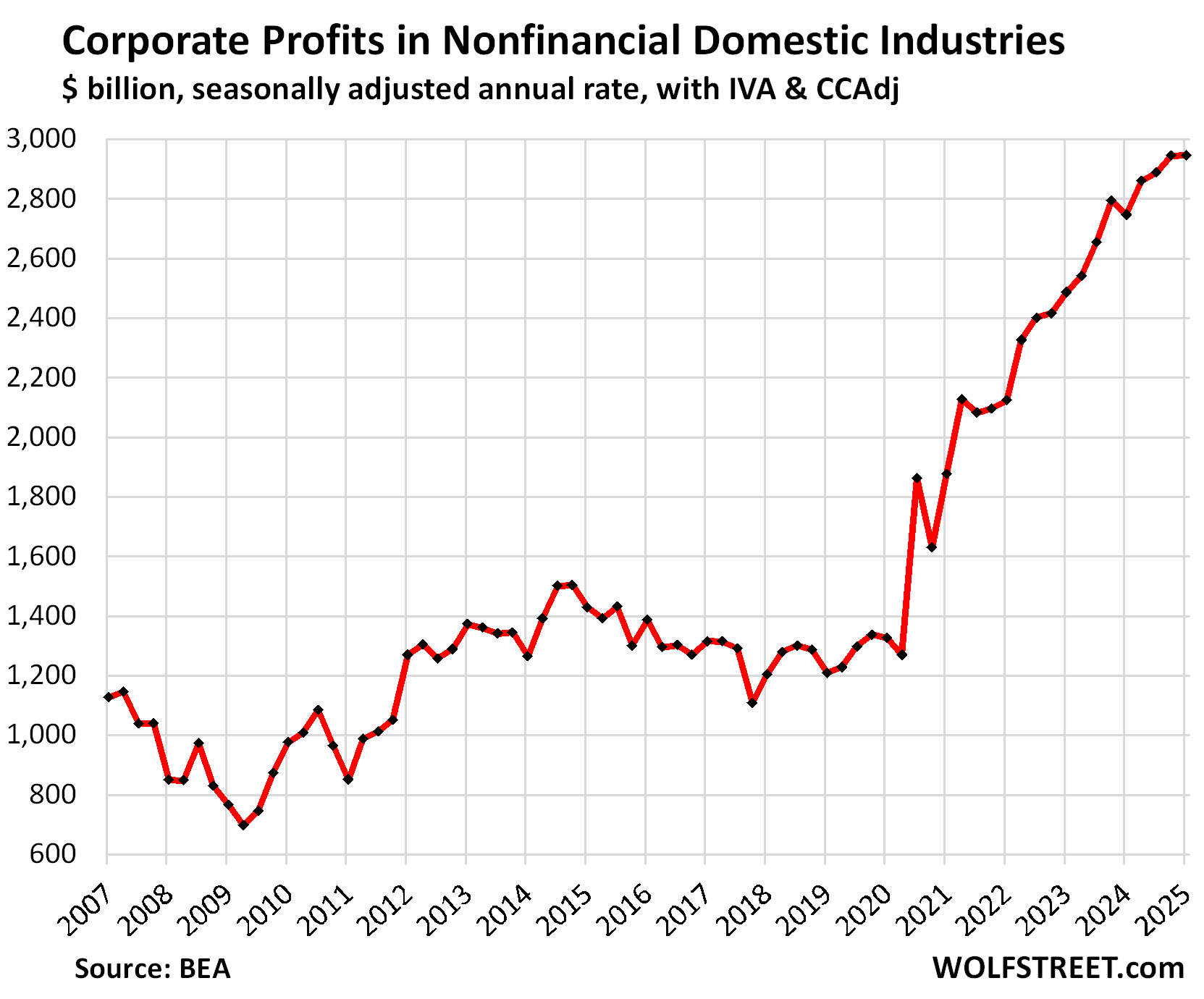

Companies have lots of room to eat the tariffs, after making gigantic profits as they jacked up consumer prices in 2020-2024 to very high levels. Now they’re finding out that consumers have had it, that they’re no longer willing to pay whatever, that price increases are a demand killer, and that tariffs are now hard to pass on because consumers reduce their purchases of those products in response.

Since Q1 2020, pretax profits of incorporated businesses of all sizes in nonfinancial industries had spiked by 122% to an annual rate of nearly $3 trillion, while Tariffs are currently collected at a rate of about $300 billion a year, which would roll back only a small portion of this huge spike in profits gained during the inflation era:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good, if Pow Pow is still around in Sept, he better not cut any of the short term rates. 4.2-4.3% return on Tbill is still good enough, not looking forward to TINA environment again

The insurances are killing me personally: home; auto and health. Premiums seemingly know no bounds. Even shopping around and bundling can’t find relief. Aside from those expenses we can control ourselves and costs. Resturants, clothing, vacations…we can decide what we choose to moderate. Residential maintenace for small items are doable and for the handy andy type are fine, however major maintence (reroof) can be a killer.

I just got my annual homeowner’s policy bill last week. It’s up 34% from last year. This is getting sickening…..auto insurance cost was just as bad last go around.

My broadband went up 60%. I could switch, but that would be even more expensive.

Unpossible. Why I was informed by this very commentariat that my massive increase in California home insurance was unpossible.

The real problem is that the FED has completely broken the economy. It doesn’t matter what CPI is when you have these massive spikes and blowouts in needs areas like insurance, food, etc.

This is why they were grotesquely premature to pause and cut – they didn’t snuff inflation out and have instead left it festering, while badly hurting people financially in the process. The entire system is deformed, with prices distorted and asset bubbles raging.

As Wolf has pointed out many times, interest rates are still well above inflation and thus “restrictive”.

The plan by the Fed isn’t 2% ASAP but 2% as soon as practical without risking something breaking. That seems to be working.

I just got my homeowner’s insurance bill as well. I suppose I should count myself fortunate that mine only went up 25.2% from last year. Ugh!

Insurance companies are sending drones to examine your roof. They are requiring a home inspection to renew your policy. Then they send some junkyard dog contractor to your house to do the inspection and to find reasons to up your insurance rate, or require a roof replacement that is not necessary.

I just got a letter from my insurance company, demanding all the above.

Yields are meant to be linear. Why should short term roi be higher than the 2 year? That’s what is broken here. Servicing debt short term isn’t a long term option and 5 billion a month at 4.5% is a joke. No one should take the FED seriously at these rates, given their current plan.

Food inflation, specifically beef, is at the lowest stocked herds since the 50s.

Services inflation again propping up the CPI. Energy up due to political constraints (cost of regulation and taxation for ya).

Apparel prices static. Good that we decided to close loopholes on shipments less than 800 bucks (no import tariffs) making business competitive once again.

In short, Powell is a disaster. We will see how many other fed members are in dissent when he holds rates.

As much as I express utter contempt for Pow Pow, with this admin, I am really afraid who they will have in mind as the replacement. Gotta remember any resemblance of conventional wisdom, norm or decorum is definitely not applicable in current time. The next FED chairman will likely be extension of someone’s will regardless of how much destruction it will unleash.

The Federal Reserve Chairman is just one of twelve voices on the FOMC (Federal Open Market Committee) which sets policy interest rates and that is one of the least important of many things that the Federal Reserve does.

What fed chair is a good one to you? Because I can’t think of any

Can you point to a time where conventional wisdom not and decorum produced good things for us?

Conventional wisdom and norms got us QE and zirp, like 4 housing bubbles, a hollowed out middle class from globalization… Etc

Judy Shelton would be a great replacement

‘Good that we decided to close loopholes on shipments less than 800 bucks (no import tariffs) making business competitive once again.’

That would be a micro business to deal in less than $ 800 shipments.

Maybe Walmart can break up their apparel orders into many 799 $ units.

Nick Kelly,

It was the huge Chinese retailers Temu and Shein, along with many smaller ones, and the B2B platform Alibaba, that abused the loophole to ship directly from China to US consumers. They didn’t pay the tariffs while Walmart paid the tariffs.

As wolf mentioned, it crippled the Chinese manufacturing. Temu shirts for 3 bucks and they were avoiding import tariffs. Then China attempted to import goods to Mexico to build and stamp their label. That’s why Mexico has tariffs imposed on them as well. Look at their trade deficit to China and try explaining why it nearly doubled in 5-7 years. That was huge. This is a game of chess not checkers.

I’d say interest rates are about where they should be except perhaps a bit higher.

The feds GOAL is 2% inflation. Thus 4% interest is only 2% real return.

It’s the previous 2 decades that have been the destructive aberation.

Powell may be holding rates because “the data” or because of TDS, but holding or increasing rates is the correct policy. What people don’t like is that it will take a decade of this rate regime to make a real difference in restructuring the economy back to a production mentality from a financial rents mentality

I think we all believe inflation will soar…

the weak dollar is a big part of it…

and if prices are still rising with oil in the mid 60s barrel….

WHAT IF?

Copper, Mexican tomatoes, beef, …….the list is endless. Where will price declines appear?

Copper is tariffs but the tomatoes are because Mexico violated an agreement and beef is because of that worm

I’ll preface this by saying I don’t believe tariffs will significantly impact inflation, but I had two 250′ rolls of 12/2 Romex in my Home Depot cart last friday at $123.00 per roll. I finalized the size of the subpanel and rest of the job on Saturday with my electrician, added everything, and when I checked out Monday, the price of the romex was $146.00 per roll. That’s 19%. I bought the last two Walmart had on Monday online for $135.00 per roll. Look today. $145.00 or more from every online retailer I recognize. I only see Ali express selling it for $122.00 right now, but I won’t buy there. I understand copper wire gets offset by clothes prices or vehicle prices coming down, but if everyone is raising the price at the same time on something like this, then I don’t see how that couldn’t count as tariff inflation.

Slickfish:

Here is a copper chart. Click on the “10Y” at the bottom of the chart to see the 10-year chart. Copper started surging in March 2020 through March 2022, then dropped and gave up part of the gains, and then, in mid-2022 started surging again.

There was a huge s pike in March 2024, and then it dropped off again. Copper is a very volatile commodity, lots of ups and downs.

Since March 2020, copper is up 161%.

Only the last 16% was the jump from the tariff announcement (click on the 1M for a one-month chart).

No one blamed the tariffs for the 100% plus surge in copper prices from March 2020 to January 2025, including the spike 14 months ago. But with the last jump suddenly people get all tangled up in their own underwear about the tariffs the tariffs.

https://tradingeconomics.com/commodity/copper

Wolf – Thanks for an incredibly insightful analysis, one that cuts through all the nonsense that I have read so far today in news outlets that I read regularly. I am bewildered by the inability (or unwillingness) of even the news outlets that I trust to grasp what is really going on with inflation. Again, thank you.

Yep, Wolf is my crystal ball…he has been spot on with his analysis.

Agree.

Also share common cause with Ryan. My insurance rates, specifically auto, have escalated by large percentages. Too many folks living in hurricane prone locations (or recurring fire zones) has to be one causal agent for this – their burden is shared by everyone (at least in the state I live in).

My Florida home (Miami Beach) insurance has not budged this past year. My California (Bay Area, admittedly near potential fire zones) premiums have doubled.

Clap for the Wolfman!

Howdy Folks. Same old same old every where else. ” CPI inflation came in lower than expected”. Party on . Knew I would find the truth here.

Thanks Lone Wolf

Inflation will come under control once we have 350-500 bn annual tarrif revenue reducing deficits, and we get rid of department of education 300bn USD budget (at least reduce by 100 bn

USD)

Inflation will escalate dramatically in the coming months as tariffs are factored into the prices of good sold combine with ever increasing services inflation. The Federal government will continue to endlessly run deficits of more than $1.7 trillion adding to nearly $40 trillion federal debt.

I wish there was an easy way to make a bet with you. I would put a lot of money into that bet. Tariffs are never going to be enough to reduce the debt. Never.

Naive.

Totally agree. And it’s time for SCOTUS to return tariff making to Congress, where it Constitutionally belongs.

What you are witnessing is the effects of each individual member of a congressional party give their power willingly over to one leader. None of them have individual power now. They are all collectively weak. So are the voters. All the power has been handed over. So things that used to be delegated by congress no longer are.

You all laugh but be careful…orange julius will stamp his feet twice as hard at pow pow and maybe call him a double dog bad work then you’ll all see.

Yep!

I’d say there was a bit of goods inflation underneath the surface in June. Honestly hope it is just seasonal noise.

Seasonally adjusted in June;

Appliances: +1.9%

Sporting goods: +1.4%

Footwear: +0.7%

Motor vehicle parts: +0.6%

I can show you lots of goods prices that dropped. That always happens. Month to month in different line items, some rise, same fall, and the next month they reverse. If you only pick the ones that rose in June from May, and ignore the one that fell from in June from May, or ignore that the price increase in June only undid the price decline in May… then you’re peaching a lie.

I gave you a chart of your item #3: footwear, so my chart was apparel and footwear, RTGDFA, it rose 0.4% in June after falling 0.4% in May and has gone nowhere and is below where it was a year ago. These fluctuations are normal.

Here is the chart again (4th chart from the top) of your #3 that you refused to look at above… show me the tariffs in your #3 item:

The reports are all very hokey and designed to confuse. I do not buy a major appliance every month, but I pay for food, insurance, and utilities every month.

Tariffs will show up, they just needs a few more months to figure how to pass it along.

You can depend on american business to be only about margin. Nothing has changed.

consumers are now allergic to price increases when they buy goods. They buy online, and there is unlimited competition and instant price comparison. They shop around. They don’t buy. They’ve had it with getting screwed by corporate price hikes. Jacking up prices without losing sales is not easy anymore. It was easy in 2020-2022.

What is showing up now is inflation in SERVICES, that’s the biggie, that’s 65% of what consumers spend their money on. It’s very difficult to comparison-shop healthcare services, insurance, housing costs, broadband providers (how many compete for your business?), etc. Consumers are sitting ducks for price increases in services. That’s what drives inflation.

I wasn’t really preaching anything, I looked for some goods that I figure come from China, and they’ve gone up in price in June.

I agree, if you sit around waiting for CPI to go up because of tariffs, when CPI is 65% services, and not all good are tariffed, you might wait a long time.

first headline I saw this morning on yahoo started “Tariffs final show up in June inflation….”

no shame

Thanks. That was comprehensive. The trend is your friend, We will see what happens tomorrow and the data drops ahead.

Good job, Wolf!

And they want the rates lowered? Housing may do a u-turn here, when inflation makes cash worth less monthly.

I dont think so.

The problem with housing is.. high prices along with 7 percent rates leading to extreme unaffordibility.

If inflation remains high it means rates are not coming down it mean more un affordibility.

Only the President and other real estate agents want rates lowered. Conservative savers want them raised.

Exactly. If rates go up, I can finally earn a decent return on my savings account. In a few years, I might even have the capital to start a business. Without higher rates, I’m stuck.

Make sure you earn at least 4% on your savings account now. If not, you’re getting ripped off. Check your last statement. Look around for higher-paying CDs, or you might want to look at a brokerage account where you can buy money-market funds (earning around 4.1% – 4.3% now), higher-paying CDs, or T-bills (about 4.3% now, and you can set them up on auto-rollover). An account at TreasuryDirect.gov also works for T-bills.

If you get 2% or 3% on your savings account, yank your money out and put it somewhere else.

Inflation is making housing more expensive – because your cost of ownership includes those insurance increases and property tax increases. Devaluation of the $ has no impact to workers who are paid in the $. Monthly housing costs compared to monthly salaries are unaffordable – prices going up makes them even less affordable which means even less buyers

The 20 and 30 year bond yields are now past 5%, as I mentioned they would be a few days ago. Watch long term bond yields and read Wolf’s stuff, if you want to see reliable reflections about inflation. Ignore all the main stream media.

TLT down to $85 @ close today.

I would not short the TLT, you have to pay the dividend. Since it began trading in 2007, it has never closed below $80. If it stays in a trading range for another ten years–which is possible–you would lose 45% in dividends by staying short. If it happens to go up for any reason, you would get hammered. Much better shorts out there. Good luck.

I am correcting myself, The TLT began trading in 2002, not 2007.

The lowest close was in May of 2004, it closed at $80.65.

It’s been a great trade for me so far. Puts liquidated with 50-100% gain and none have expired worthless so far.

The dividend on TLT is also nothing to write home about. I’m aiming for about 10% annual return with my fixed income holdings.

@ShortTLT,

If you are earning 10% yield on your fixed income investments in this market, you are investing in the junkiest of junk bonds. Good luck with that…

TBF is the inverse TLT and you don’t pay for it. At least directly out of pocket.

Be careful of the time decay on TBF. It’s not meant to track a longer-term trend of higher rates (and lower TLT price).

Now, we see that inflation mostly comes from service industry. If there is a recession coming, the demand for various services will decrease (e.g. People cut their gym membership, Netflix subscriptions etc). However, we are far from a recession

Are there other ways to lower the inflation in service sector?

Use less services. Lower demand should lead eventually to lower prices, but it may take a while. Do people right now really need a gym membership and Netflix? Buy some weights and a bench. If you have to watch tv, try tubi or pluto (they are free).

Some of the more costly services with questionable value:

Low deductible insurance

Private schools

Cosmetic medical care

Kids travel sports

Investment advisors

Trendy restaurants

High end travel vacations

Storage services

Lending services

Just watch TV at the gym. 2 dolls this Christmas not 12.

Try eating the dogs! Shop smart avoid Walmart.

Whoops that’s an extra 73 mile return drive.

Change your own oil and cut your own hair (or have a friend do it).

mow lawn, try to fix appliances before replacement, minor car repairs (changed battery on Ford Escape, have to remove either airbox OR both wipers and two big plastic skirts with clips), eat out 1x per month usually Taco or Chic Filet, shop Food lion using online and paper coupons, cut own hair, wife dyes own hair, shop at Sierra for discounted shoes/shirts, take 1 vacation every 3 years, grow own weed, buy cider/beer in 1/2 barrel keg and use CO2 & kegerator ($1/ 12oz for English Strongbow Dry cider), ferment small batch cider in Fall, walk own dog, clean own house, run 2.4M retirement portfolio myself, use Amazon pharmacy for 96% off generic cialis, buy refurb old version cell phone and keep using years after cracked screen, cancel Spotify and get out old CDs, one or zero video streaming services per month. did I forget anything?

You still paying for pedicures?

Bond market sends troubling signal on inflation that should concern investors

They read my inflation article LOL

But why is bond market so worried if expense pruning (education dept) and tariff will rake in 4-5tn over 10 years?

It won’t. Deficits are on track to exceed $2 trillion a year ahead.

Because the bond market isn’t stupid

Because they use better sources of information than you do.

The Education Department is a rounding error in the Federal budget. Entitlements, the military, and interest are what matter.

Also, tariffs are not going to solve the budget crisis. Thinking $4-$5 trillion over 10 years matter means you’re either bad at basic math or you do not understand the budget.

JimL,

Tariffs are estimated to bring in an additional $300 billion in their first full year, and June ran at that pace, so if that stays flat over a 10-year span, that’s $3 trillion. If that increases with economic activity and inflation, then it would run higher. Obviously, all 10-year budget forecasts are going to be wrong. But current estimates point that way.

@Wolf, assuming Tariffs work, wouldn’t their income decrease over time as manufacturing gets reshored and the trade deficits decrease? Unless more changes are made, we would end up with the same problem that caused all this in the first place: loopholes and low taxes on corporate profits.

“…wouldn’t their income decrease over time as manufacturing gets reshored and the trade deficits decrease?”

Yes, that’s the purpose. Tariff revenues would be replaced by the vastly larger revenues collected by federal, state, and local governments from manufacturing in the US, from the well-paid direct employment it creates, the direct income it creates — all taxed — and from the secondary and tertiary effects that manufacturing in the US entails… this starts with planning, constructing, and equipping the facilities and infrastructure and continues with running the actual plant, its suppliers, including local suppliers, including for the people who work there…. which is why manufacturing in the US so important. The effects of manufacturing are huge and widespread. But imports just syphon out the money.

Crypto bills fail in Congress…

and yet barely made a tiny ding in price, still at $117k….no stopping this rocket back to the moon and straight to Pluto..

Strange time we live in when Saynor and Cathie Woodshed is looking more like the oracle than the oracle himself

Trump browbeat the holdouts the crypto bills will pass

A nice book end is reading more about this in his Durable Goods posts or even his “Inflation & Devaluation” compendium.

Wolf,

Nvidia added $2 Trillion in market cap in under 3 months. Has to be a world record.

Nvidia and Broadcom are now 10% of S&P 500.

Their combined annual revenue is about 1.3% of S&P 500.

Considering that S&P 500 itself is not cheap, and comparing values and revenues of hi-fliers like Nvidia, Microsoft, and Broadcom to revenues and market caps of such markets as Japan or China, we can conclude that in apples to apples comparison 1 American tech apple is worth 30-40 Asian apples.

Just back of a napkin analysis. Probably nothing.

P.S. – if I include after-hours quote (so far), it looks S&P 500 (SPY) did outside revesal today. Again probably nothing.

You want to see some insanity, forget Nvidia, at least they are actually bringing in money. Check out Newegg stock and the return on the past 3 months…looks like tech enthusiasm hype is still around.

Stop complaining, some of us are patiently waiting for this bubble to burst to multiply our wealth like the big fish always do. Signs signs everywhere signs 🛑!

Broadcom is not in the top ten weightings, Nvidia and Microsoft are 13.5% of the S&P. The combined valuation of just those two stocks is now $8 Trillion. The analysts and TV commentators are ignoring valuations for now. At some point, the music has to stop.

Do microsoft and apple have a monopoly (duopoly/biopoly) in personal computing?

Two choices, essentially.

Are there other examples in which the consumer only has two choices?

J J Pettigrew

Broadband to the house? I now have 3 if you include wireless, but it’s not the same as cable or fiber. Until three years ago, I had two if you include wireless, and one if you don’t.

gas & electricity: 1 choice, take it or leave it. And big rate increases every year.

In many rural areas, including smaller towns, there is only one health insurer, and only one hospital, if they’re lucky and the hospital hasn’t shut down yet.

Oligopoly means several: there are only four automakers that make full-size ICE pickup trucks, and they have for 2 decades exhibited oligopolistic pricing behavior, which is why pickup trucks, which used to be cheaper than mid-size cars (think F-150 v. Camry), are now a lot more expensive, and automakers make HUGE profit margins on their full-size trucks, and have slim margins on their cars. I have long complained about this oligopolistic pricing behavior in full-size trucks.

There are many examples like that.

If you’re dealing with internet advertising, you will see that Google has essentially a monopoly on the backbone of internet advertising that you cannot get around anymore, and it has a monopoly on other aspects of it. The FTC has won two lawsuits against Google on this for now, and there’s more going on.

Between Google and Meta, there is very little room left for others, and they’ve driven publishers out of business because they suck up most of the funds that advertisers spend, and there’s almost nothing left for publishers that publish the ads. I’m right in the middle of this, and I see it every day. These are criminal enterprises, and they need to be cut into little pieces, like they did Standard Oil back in the day.

There are lots of examples like this.

It makes perfect sense: I recently switched to NVDA powered SmarTP: twice the flush and half the wipe! /s

I see people defending this mania, observing how EVERYTHING must simply be powered and enhanced by AI.

It’s kinda handy, but it’s not solving anything; rather it’s handy for fakes and knockoffs, turning a generations mind to mush (I am appalled at how many people can’t recognize AI work).

CPI is trending slightly up, which suggests rates are where they need to be or possibly too low.

Today’s tariffs are certainly not deflationary.

The final paragraph in this article is really something to be appreciated.

Regards,

Shocka

Shocka Locka

In the penultimate paragraph you read, “Companies have lots of room to eat the tariffs“.

I read, “Shareholders have lots of room to eat the tariffs”.

If they are not inflationary, bonds don’t have to create any room to eat the tariffs.

Anecdotal but after a very tame increase 6 months ago, my latest auto insurance renewal quote is up almost 20% and frustratingly, is still the best price I’ve found so far.

I’d be curious to see graphs of motor vehicle CPI (from the durable goods category), overlayed with motor vehicle repair and insurance CPI components from the services category.

If vehicles themselves are coming down in price after the initial spike, so too should insurance and repair costs… at least in theory.

In theory, we are a free market based economy there should be real competition in the insurance industry. However, as the insurance companies operate under oligopoly practices, competition remains a mere theory, not practice.

Free markets always lead to monopoly due to a lack of regulation. You are looking for something called “competitive capitalism”. You can find that far more in may sectors in China, which is why prices are so low there.

Oligopoly? You should look at how many market participants are in the insurance industry across commercial and personal (aside from CA where too much regulations discouraged more market participants). Please compare that to tech / agriculture etc. The industry’s premium margins aren’t fat (esp compared to most industries) if you look at their numbers. The main issue with casualty insurance prices is nuclear verdicts / PE backed litigation outfits professionalizing the space. The main issue with property insurance is weather- related claims are worsening (more events and more exposure in critically exposed areas). All in all, the insurance companies including investment income running at 6-12% ROE doesn’t speak to a greedy industry practice.

I can see the wide grin running across your face as you’re writing the word “shocker” as you’ve been warning about services since the Fed started thinking about lowering rates. Wolf for Fed chair!

Very stimulating, as usual!

After reading your blog post, looked at a random chart somewhere that shows:

Percentage point contribution to month-over-month core PCE inflation

That looked like supercore PCE is really jumping and so, had to go to FRBSF to look at another cool similar chart:

Figure 4: Contributions to 12-month “supercore” services PCE inflation

FRBSF, has beautiful chart for just PCE, which shows a nice evolution of how goods and service inflation dynamics were tightly connected, rising like twins after pandemic in around 2021 — but then, goods inflation exploded (defying transitory miscall).

I think, that’s a huge factor to be looking at again today, especially with tariff uncertainty, which is not baked-in yet.

Back to Supercore chart — the “other services” components (which you indicate are now up 4.3%) — were the rocket fuel for persistent inflation (after the transitory rethink).

As I relive that period, I was always curious about the Baumol Effect:

“ To remain competitive for workers, services must raise wages, which then translates into higher prices, even without significant productivity improvements”

A classic example is a barber, raising prices, but not being more productive.

It just seems, that as service inflation bubbles higher a bit, tariff inflation is still percolating below the surface, kinda like Deepwater Horizon ….

That said, the thing that kills service inflation is a recession — absent that, we see higher inflation.

What you call “super core” is my first chart: core services without housing.

These clowns paused too soon, then actually cut rates which was impossibly reckless and a dereliction of their duties. The stated “2% inflation target” should be illegal. Stable prices and a 0% inflation rate should be the mandate to which they are held. Look at how they have massacred the working class and the poor.

2% is planned destruction of the currency.

How this is allowed is the real scandal.

Have any Congressmen recused themselves from voting on the Crypto legislation? Didnt think so.

Here Here. If Congress won’t demand this, it is time to end the Fed.

The POTUS said yesterday that the FED should cut rates to below 1%. That is beyond reckless, it’s diabolical.

Can I do a double dog dare him to find someone to carry it out? If that means it will rock the long bond market to 6% and maybe close to 10%, then by all means do it. I can then lock my money in there and not ever having to worry about TINA again…assuming there’s still value left in the dollar down the road..

Maybe best way to fight this is to let him F around and find out or TACO bell his way out it.

The thing is, artificially loose monetary policy has historically driven asset price inflation instead of CPI (see 2008-2020), and Trump knows that & is betting it’ll be the case.

If the Fed cut to 1%, long bond yields would rise to 7 or 8 percent, which would destroy the stock market. Why deal with stocks which supposedly average 8% return over time (a number I question) with risk, when you could get 7 or 8% in Treasuries guaranteed with no risk? Trump should shut up about Treasury interest rates. I am generally good with the other stuff he does, but Bessent or somebody really needs to clue him in on how interest rates work.

Bessent is Trump’s lap poodle and will continue to perform inane little tricks to entertain him. He appears to be neither an original nor independent thinker. His concept of leadership is not doing what the country needs based on facts, data, but what Trump spews out based on emotions and disjointed political economic ideology.

It would be glorious for anyone with reserves waiting to be deployed, like my wife and I. Hell, I’d be selling off all my extraneous stuff, including my RV, just to throw as much cash as possible at an 8% Treasury.

Renting right now, as it’s cheaper than buying, but if I still had my former home, I’d be selling that sucker too to dump the proceeds into an 8% note.

May even kick in a kidney or lung to get quick cash. Probably wouldn’t need them long anyway, because mortgage rates would be 12%, homes would be back at 2012 valuations, the stock market would be down at least 70%, and blood would (probably) literally be flowing in the streets.

I mean, it’d be fantastic for my family, right up until the roving hunger gangs got us.

Thanks Wolf.

Inflation in Services is deep problem and wont be going away anytime soon. Wages have gone up, Rents have gone up so Service Providers are going to pass the cost to Consumers.

Hopefully, Trump Puppets Bowman and Wallers see this report and have some conscious. Both were very hawkish last year and now want FED to see through those inflation numbers and cut as early as July. Shame on them.

Hope majority on FOMC will see this report as it is and dont cut anytime soon until they put inflation genie back into bottle.

Durables percent change from June 2024 by Census region:

Midwest: 2.2%

South: 0.5%

West: 0.7%

Northeast: 0.4%

Services percent change from June 2024 by Census region:

Midwest: 4.2%

South: 3.5%

West: 3.4%

Northeast: 4.4%

You have to admit that some services are affected by tariff. For example homeowners and auto insurance. A lot of house construction material and car parts have been tariffed which would raise insurance companies cost which is being passed on.

Like tariffs increase raw material prices and component prices that go into airplanes, and then the airlines have to pay more for their airplanes, and then when they finally take delivery of the planes, years after ordering them, they pass on the higher costs of these planes to the fliers that buy tickets to fly on them? I may well have passed on before these tariffs hit airfares, it would take that long if ever….

Meanwhile, airline fares actually declined month-over-month and yea-over-year.

In terms of your scenario — tariffs increasing construction costs and thereby driving up homeowner’s insurance for existing homes that were built 30 years ago and of new homes that haven’t even been built yet – well, you’re gonna be in the same boat as me waiting for tariffs to hit airfares.

There are a lot of other factors that will hit homeowners’ insurance, and they’re real and have been happening for years, such as as hurricanes and wildfires, and of course, oligopolistic or even monopolistic pricing practices, those are big culprits here.

Few words which characterize most accurately, most vividly the present state of the US economy:

oligopolistic or even monopolistic pricing practices

I think you demonstrated his point without realizing it.

Tariffs won’t show up in durable goods for a while since there are long term contracts involved and other factors as well. Any short term effect of tariffs on durable goods should be to reduce demand (which is precisely what is happening). The effects will more quickly show up in services which have a goods component related to them (like car repair and therefore insurance or home repair and therefore home insurance).

For a while the increase in car repairs was labor related. Absolutely no doubt. However I am fairly sure the recent (last two months) the increase in car repair is more parts related. The price of car parts has soared.

Don’t get me wrong, there are other factors dominating inflation in both home and car insurance (climate related disasters), but they are only masking the effects of price increases in car parts and home building materials.

It is unbelievable that the current administration has only been in office for 6 months (it feels like years if not decades) and so ridiculous tariffs have been around for even less time, but so far we have mostly only seen the short term benefits of tariffs. The longer term effects are still to come (although it should be noted that even in the short term, the effects if tariffs have made Americans poorer as reflected in the buying power of the dollar). The longer term effects are just starting to show up in terms of car parts and building materials.

I say this as someone who thinks there is some value in selectively and we’ll thought tariffs.

I haven’t noticed any significant increase in car parts prices in the last 2-3 months, even those made overseas.

The issue I have is the quality of many parts is junk. I’d rather pay more for something known to be better quality: there’s a time cost for redoing a job due to a prematurely-failed part.

Car parts have not materially risen based on my itemized parts lists. However, my dealership’s hourly went from $145 to $195 from 2022-present. $50/hr more in three years. Labor shortage combined with general inflation. Not sure if the owner has had to eat any margins or not. Probably not because the demand is there.

Independents lagged a little, but around my neck of the woods, and unless you’re going to the shade tree, they’re running $175. Cars are getting too advanced for most independents to keep up well, along with finding good help. After experiencing too many callbacks at independents recently (or just shoddy work), and with only a small overhead for the dealer, I’m 100% back to the dealership service bay for the time being.

It’s all labor costs (and margin protection).

JimL,

“However I am fairly sure the recent (last two months) the increase in car repair is more parts related. The price of car parts has soared.”

Month to month price change:

May: -0.14%

June: +0.23%

Combined two months: +0.10%; annualized = 0.60% = almost NO INFLATION.

Here is the chart for auto repair costs, price index. SHOW me the tariffs!!!

SMS – many “shadetree” mechanics are dealership techs with a side hustle. You’re getting the same labor, but with their own tools and jack stands rather than a lift bay. Less overhead = lower hourly rate.

I do oil changes for friends in my driveway for anywhere from $50-$60 depending on what their cars need. No need to pay $120 at a dealership.

Should have never lowered rates last year. 2% is a pipe dream.

There was zero reason to drop 100 points but Powell was trying to make Biden look good – didn’t work out

Absolutely, StPeteDave. Powell’s cuts during election season 2024 were clearly politically motivated. I don’t believe that I’ve heard a valid counter argument.

–Geezer

The FOMC which is the 12 member committee at the Federal Reserve who makes all policy interest rate decisions is completely apolitical and does not make any decisions out of so-called ‘political motivation’ but around well-agreed data points.

“I don’t believe that I’ve heard a valid counter argument.”

That’s because you refuse to hear any valid counter argument because you made up your mind because you only allow yourself to hear BS that fits your narrative.

At the time of the FOMC meeting, the labor market data was weak and heading for bad, and inflation had cooled a lot. That’s the info the Fed had for their mid-September decision. Then – in the weeks and months after the decision was made — all the data was revised up substantially: labor market OK, inflation re-accelerating.

I wrote several articles about this in detail at the time. And for you people to come along and spread this BS is just goofball material. Read my old articles from that time!!!

Start here, labor market data weak and going for bad just before the September FOMC meeting with this chart, from September 6:

https://wolfstreet.com/2024/09/06/the-fed-has-room-to-cut-rates-are-high-relative-to-inflation-and-job-growth-could-use-some-juicing-up-to-maintain-momentum/

Then two weeks after the September FOMC meeting, the upward revisions started. It started on October 4:

https://wolfstreet.com/2024/10/04/ok-forget-it-false-alarm-labor-market-is-fine-bad-stuff-last-month-was-revised-away-wages-jumped-no-more-rate-cuts-needed/

And then this from October 13:

https://wolfstreet.com/2024/10/13/what-if-theres-no-landing-at-all-but-flight-at-higher-speed-and-altitude-than-normal-with-higher-and-rising-inflation/

Then this from October 17:

https://wolfstreet.com/2024/10/17/landing-cancelled-retail-sales-jump-prior-months-revised-up-boost-atlanta-fed-gdpnow-to-3-4-inflation-adjusted-gdp-growth/

And keep going… There are lots of articles about the up-revisions and the data mess that the Fed was facing.

Wolf, then why didn’t they just wait?

Rates were nearly double the rate of inflation at the time. That was a big thing, pretty restrictive. They’d been at 5.33% for over year, inflation coming down, labor market suddenly going to hell… wait for what?

They cut by only 100 basis points from 5.33% to 4.33%. They didn’t cut to 0%. Rates are still above the rate of inflation.

I know that there are some people here that want the Fed to blow up the economy, but that’s not the Fed’s job.

I guess you could call this a counter argument-

Powell also raised rates thru the roof during the Biden administration, started QT, etc. Not exactly screaming political motivation to help Biden’s party.

Nope.

And it was a jumbo rate cut. Jerome Powell and Co. should be tarred and feathered for the damage they have caused.

I’d bring the tar but it is too expensive due to tariffs 😉

Powell is worse than Bernanke, and worse than Miller the former fed chief who’s only executive experience was running a golf cart company. Powell’s new Fed building renovation is 200% over budget and doesn’t even have a cafeteria.

Remember when we were told inflation was transitory? Good times

Has anybody asked Weimar Boy why it’s still transitory-ing?

The U S Constitution is clear

CONGRESS controls the “Minting” (creation of money)

How did the Fed abscond that power? Crisis after crisis….and created by whom, exactly?

The Federal Reserve Act of 1913. Go read it.

Do you wish to point to the section dealing with the Fed creating money and managing the money supply?

” Federal Reserve notes, to be issued at the discretion

of the Board of Governors of the Federal Reserve System for the

purpose of making advances to Federal Reserve banks through the Federal reserve agents as hereinafter set forth and for no other purpose, are hereby authorized.”

for the purpose of making advances

I don’t like Powell, I think he’s a vacillating weaselly scumbag, but compared with Trump, he’s the adult in the room on this matter, and that should scare people.

Trump wants to re-inflate the asset bubbles when we didn’t even deflate the last one…

Well to give Pow Pow some credit, the man never defined the timeframe on this transitory definition. Stretch out the lens of time, everything is transitory. He didn’t come out and say inflation is transitory for 6 months to a year and that gave him a way out and we’re still this transitory journey.

As with everything, it’s all about context. One of the most notorious regime in modern history was in power for 12 years, can be consider transitory, heck even modern homo sapien only been around for 300k years and likely would not be around 300k to a million year from now, in the grand scheme of the earth history, we are also very transitory.

Lol well I suppose you are right in that sense. In a million years we are set

So far it’s been 4 years of 3%+ inflation

Hopefully this is just a blip and the trend starts going down again. It did this in 2023 and 2024 as well. Unfortunately short of a massive recession prices won’t drop quickly

Where is the 2% trajectory line on the CPI chart from 2021?

Well below where we are now.

And ask, why is YOY the metric? How about a 4 year window?

This is why the bulk of services inflation is in services with housing as Wolf explained. You have to have a running furnace/AC, if you have a mortgage, you have to have insurance. We had to replace the furnace in November, the AC in May and eat an insurance increase as well as property tax increase. Midwest- Ohio and I’m a property and casualty agent so even with my discounts the increase hit us too. You can increase your deductible up to your risk threshold, pay in full and cross your fingers – only relief available.

Man refrigerant, r22, is like 40-50% higher than 3 years ago. I had to get my AC recharged.

Couple that with minimum wage increases and local utilities raising rates by 4-6% it isn’t surprising to me that stuff is going up

Eric86, I had to recharge my car AC and had never done it. So I called the local car repair shop and they wanted $150 just to check out my AC system, before doing a recharge. I went to Autozone, bought a recharge kit for $50, read the instructions, and did it myself (it was not difficult, just a little weird). My contribution to Whip Inflation Now.

Oh I was speaking of home a/c. Like 400 per pound. R22 is being phased out so it is super expensive and the new refrigerant doesn’t work on older systems.

I often wonder what effect things like that have on CPI.

TTM Core PCE has been stuck around the 2.7% level since May 2024. How much longer will it take for them to publicly admit that (a) current rates aren’t restrictive enough or (b) they’ve unofficially given up on the 2% target. It’s not really a credible target if they’re allowed to overshoot it for 4.5 years straight…?

(There is tremendous pressure from Wall St & DC to lower rates to juice markets, not out of economic necessity. But the FOMC’s current views regarding sub-3% neutral rates etc. started from before the election.)

Tariffs aren’t a major driver of inflation. For all the chaotic back & forth policy coming from this administration, the current economy is largely the same as it was last autumn: ~4.1% unemployment, ~2.7% core PCE.

Consumers & businesses have gotten accustomed to 4.5 years of elevated inflation. The fastest way to get rid of it is with a recession that lowers demand.

These analyses and great, thank you. I think it would be great if you could also include the values/graphs for other inflation metrics like median CPI, Cleveland fed trimmed mean CPI or Dallas fed trimmed mean PCE (when available), as these graphs clearly show that median inflation rates are still well above target (and for some haven’t moved much at all in the last two years). Or have a separate post or discussion about them. In any event, thanks again.

BLS quality adjustment index

I would love for someone to build a BLS quality adjustment index so we can all see how much our standard of living goes up each year.

We know goods CPI was running -2% before COVID. So how much was the adjustment.

I have to go with Core Services as the better measure even with all its issues.

Dang dirty 30 pushed through 5 today. That services number can be fixed, but good by real estate going through the disaster.

Meanwhile, we just wait for more of the above. It’s going to be long and hard until this mess is done.

The crisis of 2036 will now be from now until it’s all solved and stable, or blows out and we get a new new deal.

Fun and games.

I wonder if insurance is going to be what blows up housing based on stupid valuations plus legitimate risks like floods, fires, Cthulu, whatever. There is so much money floating around that I think a lot of small time speculators are paying property taxes and trying to ride out the downturn. If insurance drives folks to sell at lower prices it will eventually drop insurance rates along with valuations.

Where I live (Wake County NC) a SAS algorithm essentially sets assessed values, and the algorithm has a vivid imagination. The current valuations are based on the massively inflated values of fall 2023.

Abolish property taxes and just have a sales tax for local jurisdictions. There is zero reason why we should be taxed on unrealized gains aka increases in property value.

Errr because they take up more land and therefore on average use more services? Because it incentivizes people to downsize rather than always chasing higher asset values? Because it’s less regressive to the non and small property owners? Because excessive sales taxes hurt businesses and damage local economies? There are plenty of reasons.

Also try funding a state like Illinois or New York with just sales taxes, it’s not going to happen. Higher income taxes would be the only other option.

The services that use more land would be water, sewer, etc and those are usually non-advalorem taxes or paid for by impact fees.

Higher income would be fine. There is no reason why my taxel bill should go up just because of a hot real estate market. I get no benefit from my house doubling in value. I can’t sell it. All I get is higher taxes and higher insurance.

They should at least freeze the value you pay for it.

The wealthy have an obligation. Property taxes in NC fund education for everyone. Each property requires services such as fire police etc. Sales tax are regressive. Property taxes make sense to me. One can challenge one’s evaluation..

Income taxes are much more equitable. Retirees in high cost areas bear a disproportionate burden with property taxes. Ideally there would be no property taxes IMO

It is the fact that property taxes are taxing and unrealized gains. If they want to keep values flat at your purchase price then fine but stop with the raising of values.

I too live in Wake County, NC. Property valuations went through the roof for the latest 4 year true-up tax evaluation. The region isn’t correcting much yet, but there is suddenly a LOT more inventory on the market than when we moved here in 2022, which then continued through most of 2024.

A lot of houses around here sold for $700,000+ in the last five years, when the previous owner paid $300-$400k. Tax values don’t uncap immediately in NC until the new evaluations. It’s conceivable that anyone who was already on the margin for their mortgage can’t eat the extra $100-$300/mo just in tax payments, especially if they have student debt that’s now getting called on. Insurance has gone up a ton as well. Between the two, it’s conceivable that most people are paying substantially more per month. Not to mention any maintenance costs, which are through the roof and are likely getting deferred/kicked down the road.

The home I’m renting now would cost me a minimum of $1,000 extra per month to buy, before any repairs/maintenance. Add in those anticipated outlays, and I’m easily $1,500-$2,000/mo ahead right now. That’s money that I can spend, invest, save.

If I invest the equivalent of a $140,000, 20% down payment on a $700k home, put in just an extra $1,000 per month, and earn even 5% interest, things are looking pretty good vs. owning a home after 30 years; plus, I’m not locked down with an illiquid asset and can move whenever, as-needed.

The math doesn’t make any sense to buy a home right now unless you just HAVE to have your own place and can’t get over the narrative of “you’re just throwing away money on rent.”

Just a little perspective here:

Cumulative CPI increase (2009-2025): The Consumer Price Index has seen a cumulative price increase of approximately 49.84% since 2009.

Interpretation: This means that what cost $1 in 2009 would cost roughly $1.50 in 2025, according to the Bureau of Labor Statistics consumer price index.

The cumulative impacts of deficits are destroying the future