If residential mortgages get messy, banks are largely off the hook this time.

By Wolf Richter for WOLF STREET.

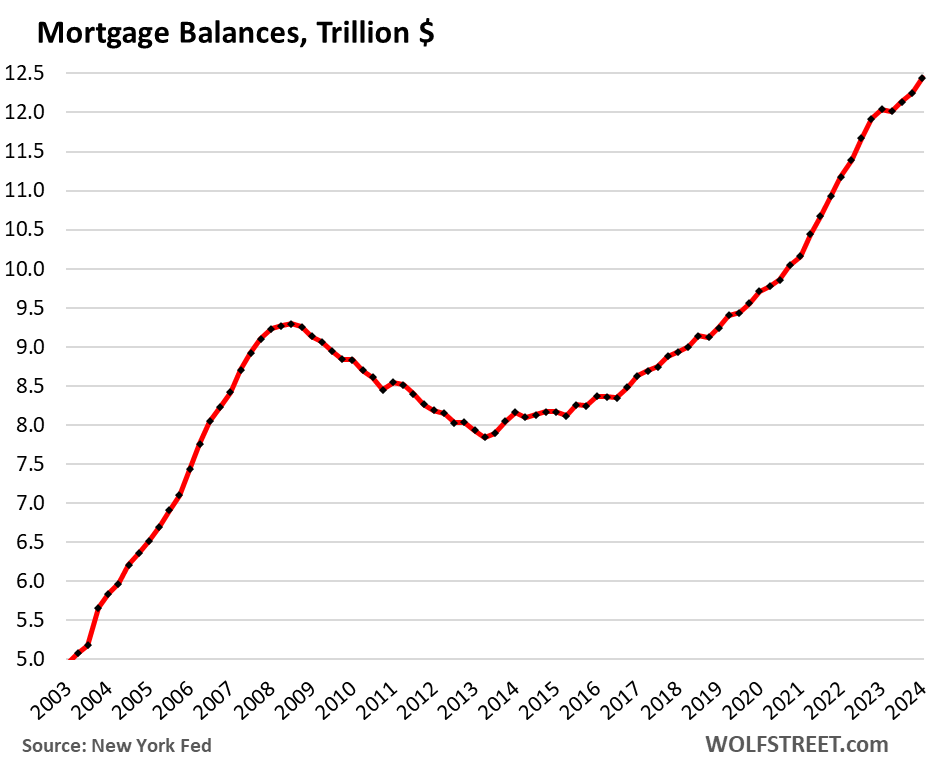

Mortgage balances rose by $190 billion, or by 1.6% in Q1 from Q4, and by 3.3% year-over-year, to a record of $12.4 trillion, according to the Household Debt and Credit Report from the New York Fed. Mortgages account for 80% of total household debt.

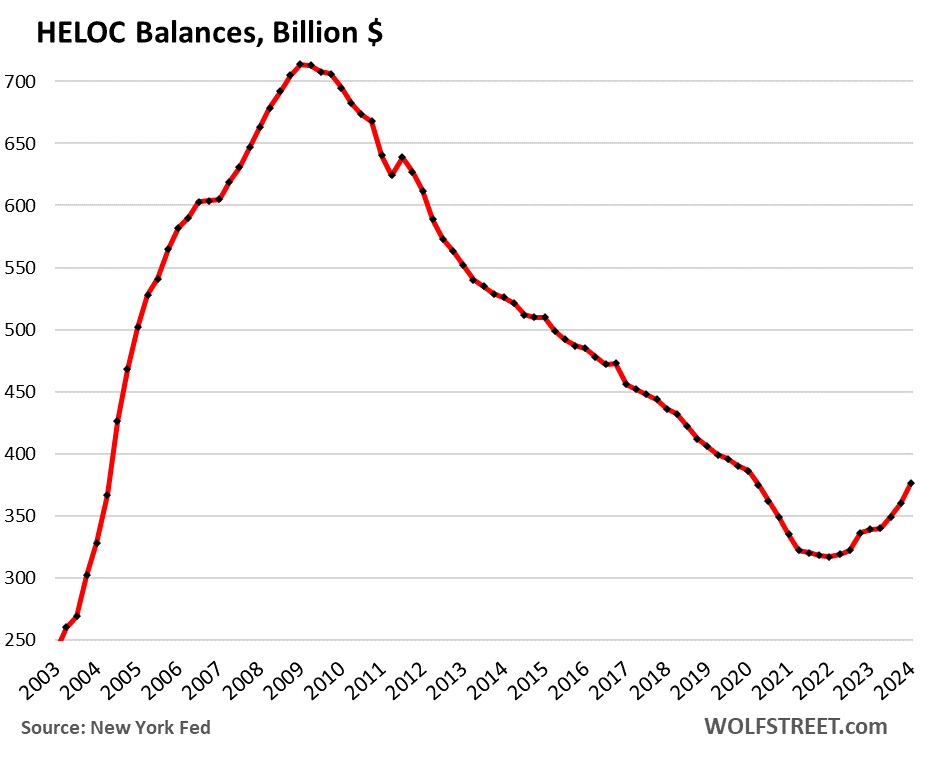

But HELOCs (home equity lines of credit) are rising from the ashes. Balances jumped by 4.4% for the quarter, and by 10.9% year-over-year – more in a moment.

In terms of mortgage balances, the relatively small 3.3% year-over-year increase is the result of several factors that pull in different directions: Still sky-high home prices that require larger mortgages; purchases of existing homes that have plunged; mortgage origination volume that has plunged; while purchases of new houses have held up, as prices have dropped 18%, and buyers are financing less expensive new houses. And a big part of homeowners with 3% mortgages are not selling, and they’re not buying either, and so they’re not paying off their 3% mortgages, and they’re not getting bigger new mortgages to buy more expensive homes:

But HELOC balances are rising from the ashes.

HELOC balances jumped by $16 billion, or by 4.4% in Q1 from Q4, and by 10.9% year-over-year, to $376 billion. Despite the recent surge, HELOC balances remain historically low after 13 years of incessant declines.

HELOCs are a way for homeowners to turn their own money buried in their home into useable cash. But to get to their own money, they have to pay Wall Street fees and interest on it.

The 7% mortgage rates have made cash-out refis – which refinances the mortgage plus the cash-out at this high rate – too expensive, and refi volume has collapsed. A HELOC may come with interest rates of 9%, or whatever, but it applies only to the amount drawn on the line of credit, and not the mortgage which continues at 3%.

Second-lien mortgages accomplish the same as a HELOC, but have fixed payments over a fixed term. They too are an expensive way for homeowners to turn their own money buried in their home into useable cash as Wall Street will exact its pound of flesh.

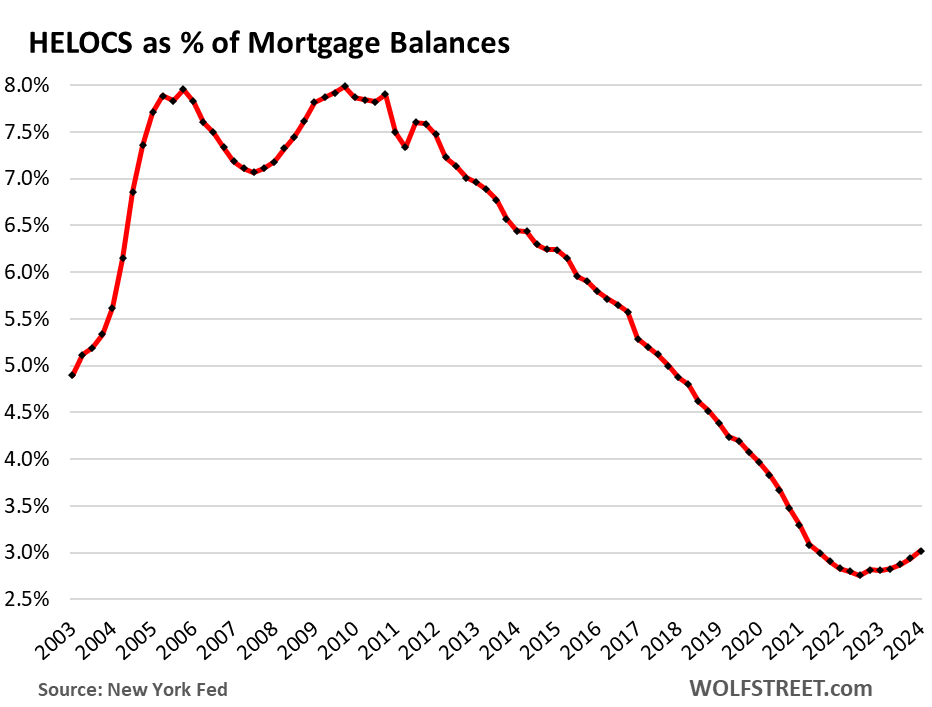

HELOCs are still a tiny portion of the housing debt, accounting for just 3.0% of total mortgage balances in Q1, having barely moved up from the historic low of 2.8% in Q3 2022. Once upon a time in 2005 through 2012, HELOCs amounted to 7-8% of mortgage balances:

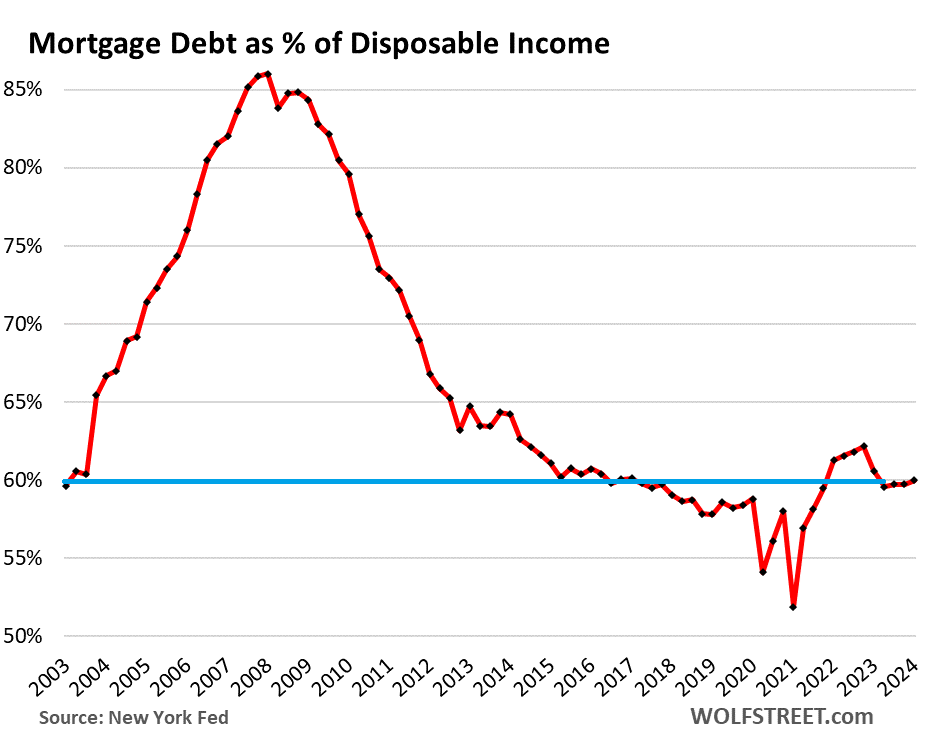

The burden of mortgage debt.

To measure the burden of mortgage debt on households, we can compare mortgage balances to disposable income, which is what households have left over from their total income, after payroll taxes and social insurance payments, to deal with their costs of living and service their debts.

Disposable income is income from all sources but not capital gains (wages, interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.), minus taxes and social insurance payments. And disposable income has surged (data from the Bureau of Economic Analysis):

- Quarter over quarter: +1.1%

- Year-over-year: +4.3%

- Since 2019: +26.7%.

The ratio of mortgage balances to disposable income has been roughly flat for the past four quarters at around 60%. Note how the ratio dropped in 2022 and Q1 2023, as wages surged. Recently, wage growth has slowed, and the ratio has stabilized near historically low levels:

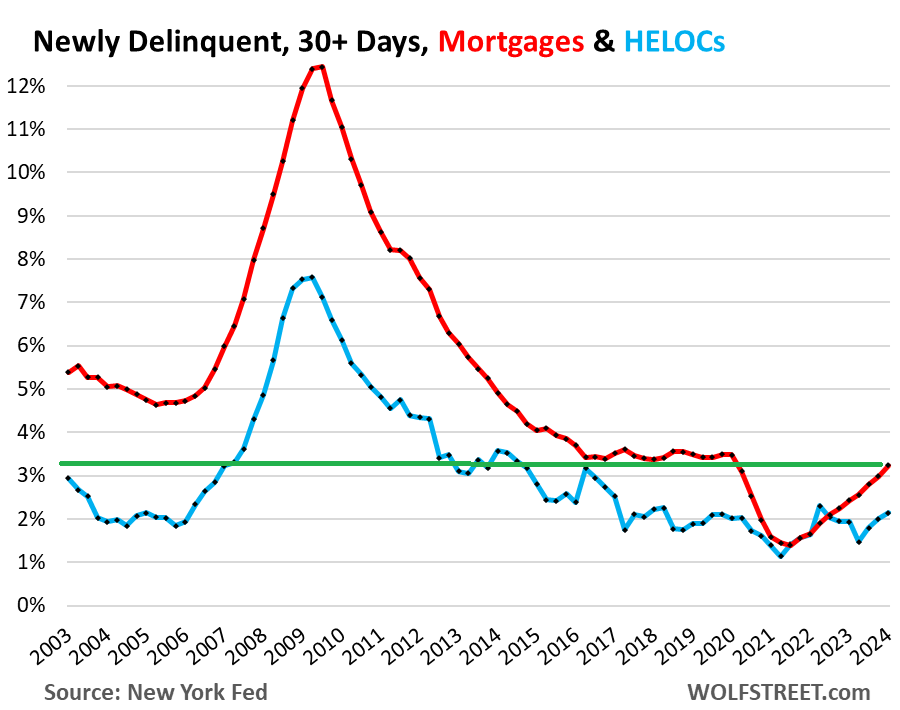

Delinquencies haven’t normalized yet.

Transitioning into delinquency: Mortgage balances that were delinquent by 30 days or more ticked up to 3.2% of total balances — still lower than any time before the pandemic (red line in the chart below).

HELOC balances that were delinquent by 30 days or more ticked up to 2.1% (blue line).

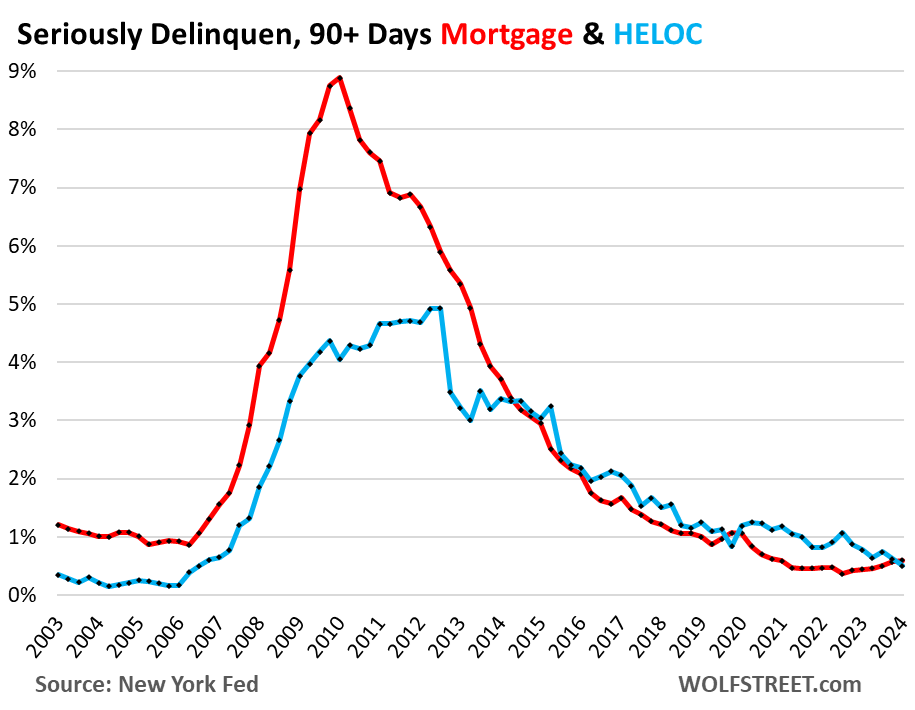

Serious delinquency: Mortgage balances that were 90 days or more delinquent edged up to 0.6%, compared to 1.0% and higher before the pandemic (red line in the chart below).

HELOC balances that were 90 days or more delinquent dipped to 0.5%, the lowest since 2006 (blue line).

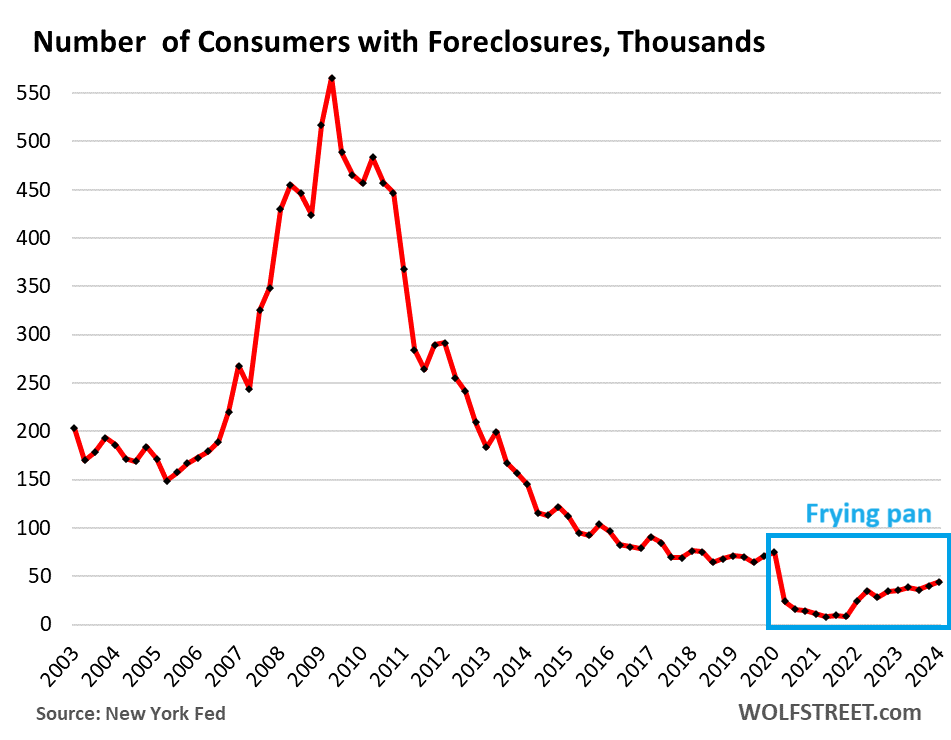

Foreclosures in a post-pandemic frying-pan pattern.

During the pandemic, with mortgage forbearance and foreclosure bans in effect, the number of consumers with foreclosures plunged to near zero. They have risen since then but remain far below the Good Times lows before the pandemic.

In Q1, there were 44,200 consumers with foreclosures, compared to 65,000 to 90,000 in the years 2017 through 2019. In other words, they’re not even normalizing yet. The post-pandemic frying-pan pattern has cropped up in a number of other data as well:

Foreclosures won’t be a problem until…

…home prices sag and people lose their jobs. That’s the short version.

Homeowners who purchased their homes more than two years ago and didn’t cash-out-refi have lots of equity in their homes as home prices have surged in the years through mid-2022. And that’s the vast majority of homeowners. But more recent homebuyers can get into serious trouble fairly quickly.

If a homeowner with a lot of equity cannot make the mortgage payments because they lost their job or had a medical emergency, they can sell the home, pay off the mortgage with the proceeds, and have some cash left.

If unemployment surges and over a year’s time a million homeowners cannot make their payment anymore, they can sell their home, pay off their mortgage, and go on.

The problem arises when home prices plunge to multi-year lows, and suddenly a larger portion of homeowners are underwater. Being underwater for a homeowner is no biggie as long as they don’t have to sell. They just hang tight, quit looking at Zillow every day, and life goes on.

But if they have to sell, it gets complicated. If lots of people lose their jobs and can no longer make the mortgage payments, and have to sell, then it gets a little messy because it drives down prices even further. The result will be that homes will become more plentiful on the market, and more affordable to buy, which would be welcome by lots of people and would solve a crisis.

Banks are largely off the hook this time.

The mess would mostly hit taxpayers, who now are on the hook for a large majority of the mortgages – not banks. The exception are HELOCs; the government has not yet taken them under its wings. But HELOC balances are still small.

Banks have relatively few mortgages on their books; they sell most of them off to government entities which turn them into government-backed MBS and sell them to investors. Banks not being on the hook for the biggest part of the mortgages is one of the fundamental changes since the mortgage crisis. So this time, the Fed can let the housing market do its thing without having to worry about the financial system collapsing under the weight of imploding mortgages. The financial system might get tripped up by other problems, but not residential mortgages.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“But more recent homebuyers can get into serious trouble fairly quickly.

If a homeowner with a lot of equity cannot make the mortgage payments because they lost their job or had a medical emergency, they can sell the home, pay off the mortgage with the proceeds, and have some cash left.”

I think the consequences of this issue are hugely ignored by the market. A fire sale by “recent homebuyers ” can bring down the comparables in entire neighborhoods and cause a cascading effect.

Those who took out HELOCs won’t feel so rich anymore as their home prices come down too but they have to service the debts.

P.S. Many of these recent buyers have also bought vacation rentals.

Yes, the vacation rentals coming back on the market for sale is something to watch for as the revenge travel boom cools a little.

In terms of the recent purchasers: most homeowners don’t HAVE to sell, even those when one of the two bread-earners loses their job for a while. Most people can tough something like that out for a few months. Even during the horrible mortgage crisis, only something like 11% of the borrowers defaulted on their mortgages, and that was at a time when prices had plunged variously by up to 50%.

I took quick peek at vacay prices

obscene comes to mind

$230,000 for single wide mobile

it’ll reset in time

Amen. Ive seen a few in a small town in my state NC. I was shocked 😲.

“only something like 11% of the borrowers defaulted on their mortgages, ”

Do you have a source on this Wolf?

My recollection was that there were about 8 million defaults out of about 50 million homes with mortgages (another 25 million SFH were mortgage free) yielding a 16% default rate.

8 million defaults out of *75* million SFH (including *all* SFH then, both those with mortgages and mortgage-free) would be in the ball park of the 11% number.

But I’m not sure it is kosher to use *all* SFH as the denominator, since 25 million mortgage free homes *could not have defaulted*.

Working off memory.

There are a bunch of numbers, and I’m sure which I cited. You cited total defaults of all mortgages during those five years. I might have remembered the maximum “default rates” from that time, which measures defaults at a point in time, say monthly or quarterly. We normally cite default rates that way, as at that point in time. Loans come out of the default basket when they transition to the next step, such as a foreclosure sale.

“In terms of the recent purchasers: most homeowners don’t HAVE to sell, even those when one of the two bread-earners loses their job for a while. Most people can tough something like that out for a few months.”

Good points Wolf, and I would like to add that those “few months” have already started ticking for many high flying tech workers in the Bay Area who were laid off since last year. Know of several who were let go from Google, Meta, and others (in some cases couples who were making 600k+ combined and both got laid off). They have not found jobs since last year or have taken jobs at substantially lower pay, sweating bullets over the high cost of their mortgages and other expenses.

I don’t believe this at all. Big Tech is hiring like crazy amid raging A.I. mania. Just look at levels.fyi; there are numerous $500K+/year new offers being handed out like candy every day. The industry’s most recent recession was 2000-01.

Sign up for TeamBlind and go to the layoffs section, apparently you don’t really know what is going on.

Wow. That seems like a lot. Neurosurgeons must be feeling a little tetchy, looking around wondering why in hell they went to all that trouble when they could’ve just moved to Silicon Valley, rolled up their sleeve and plunged a fist into all that candy going around.

Thankfully, one senses that the nerd wave is cresting and a refusenick backlash looms; a kind of zeitgeist shift akin to punk v disco. Hopefully this will lead to a pullback in Americans spending their hard-earned devalued dollars on the latest whiz-bang grabassery which helps subsidize a few bizarrely wealthy and totally narcissistic Randian maniacs.

500k being handed out like candy? Tell that to my BIL, a silicon valley guy for 30 years who has been struggling to get a new job since being laid off last year.

Sactown,

“…for 30 years…” That may be problem right there. Don’t take it personally. It’s not you. It’s called age discrimination. You may be at the beginning of feeling it. It’s an uphill battle. I keep my fingers crossed.

These HELOCs need to be made more attractive by the banks. Perhaps using some of that excess equity to “buy down” the interest rate for the borrower, but a big enough chunk of equity to help make the banks stronger; i.e., more profitable. A further benefit of “buy downs” is that they increase desire for the financial product.

Don’t worry, peoples wants will make the HELOCs attractive.

According to the National Association of Realtors, all cash buyers went from 10% of buyers in 2003 to 32% of all buyers in Jan 2024. Tha’s yet another reason for the relatively small 3.3% nominal increase in mortgage balances.

Your statement, along with a previous comment about Bay Area layoffs and housing, reinforces something I’ve been noticing in my Sunbelt city neighborhood for the last 24-30 months. Every single house that comes up for sale is purchased with a few weeks and it’s always a Washington or California license plate in the driveway a month later. This neighborhood used to be a “move up aspirational” jump for locals that had good jobs and wanted to settle in. Now it’s all west-coasters cashing out there and paying cash for houses they consider cheap. But they are paying four to five times what I paid 20+ years ago.

I think the west coast is being populated by Asian cash buyer immigrants who buy out laid off Google employees or Seattle retirees, and then they take that cash pile into the central states and increase prices – by 50% in the last four years. I guess you could say the trade deficit with China over the last thirty years is being somewhat recycled back into increased housing values and equity in Nashville or Dallas or Phoenix.

Interesting point. Could you expand/elaborate how the trade deficit has recycled and therefore caused this?

“HELOC balances that were 90 days or more delinquent dipped to 0.5%, the lowest since 2006 (blue line).”

2006 is an ominous comparison point! But I guess in 2006, anyone who wanted to cash out refi could do so and HELOCS were not in favor.

I just saw a quote by Elon musk, who I rarely agree with. He said that the original sin in the 2007 crisis was both lenders and borrowers believing that real estate prices could never go down. I think we know better now, at least I hope so.

We do not know better this time around, I think.

It wasn’t so much that they thought prices would never go down, it was that they thought rates would never go up. (Sound familiar??) At the height of the bubble in 06 something like half of all loans were adjustable-rate

Excessive debt is the downfall of corporations, governments and individuals.

The key word is “excessive”. If lenders AND borrowers stay within debt limits they can reasonably service, there should be no problem. Properly used, HELOCS and second mortgages can be very useful financial tools.

“Excessive” rises and falls with the prevailing socioeconomic outlook.

And thus follows the greed and fear wave.

The only way to avoid this trap is to limit things based on static metrics.

But then you see politicians and business whinge that ‘growth is being held back’ by ‘over restrictive regulations’… forgetting that these restrictions would also stop the troughs in economic output.

And politicians and greed always win… until they don’t.

The numbers say that the trend is downward, but it’s rolling down a very gentle slope right now.

As time rolls on people have to sell homes for one reason or another and this pricing sets the market rate. There’s just not enough people buying at current pricing to move the needle quickly.

Deficit spending seems to be the overriding factor in keeping inflation afloat, working against the Fed, with the Fed of course working against its prior self. Messy times.

“He said that the original sin in the 2007 crisis was both lenders and borrowers believing that real estate prices could never go down.”

Nothing has changed

Today, the majority of buyers are speculators, as was the case in 2007.

They still believe that prices will rise forever.

Gravity causes something thrown into the sky to fall back to earth.

The higher it is thrown, the greater the damage on contact with the ground

This was my comment to the comment of

Kevin L

“Today, the majority of buyers are speculators, as was the case in 2007.”

Source?

The source is the real estate market in Bulgaria, Eastern Europe.

I follow announcements every day to convince myself and I am convinced that what I am saying is true.

Properties bought months ago are being sold again but at a price increased from 20 to 60 percent.

I also follow the Montreal market, same thing.

See also prices in Vancouver in Realtor.

You can see what were the prices for these properties purchased over the years. Sort of like Case Schiller in the US.

There are many properties purchased before one or two years that come at a 30 to 50 percent more expensive.

“Nothing has changed. Today, the majority of buyers are speculators, as was the case in 2007.”

It’s arguably worse now. The value of houses as a “number always go up” speculative investment play far exceeds houses’ utility as shelter. Houses are essentially “HoomCoin” at this point.

This is why we can have empty houses along with a large homeless population, $150,000 mobile homes brokered by hedge funds, and competition from big money speculators for every single house that hits the market.

If number *didn’t* go up anymore, but went down like it did in 2008-2013, this would not only all come to an end, but it would snowball downward like it did in 1990 Japan.

agree with you.

But like I said, sooner or later gravity will do its job.

In Bulgaria, 40 percent of the properties are empty, and in the capital Sofia, the empty properties are 35 percent.

At some point, even just 5 percent of them coming on the market for sale will trigger an avalanche of falling prices.

Compared to having an AirBnB above me, an empty condo sounds like paradise.

“Despite the recent surge, HELOC balances remain historically low after 13 years of incessant declines.”

With apologies for repeatedly dwelling on more distant past, how can we expect U.S. household debt/GDP to have risen from 25% in early 1950’s, to 44% by 1970’s, to 72% in 2000’s, to recent levels around 100% for past 20 years, and expect anything other than severe volatility in asset prices, purchasing power and interest rates (stats from McKinsey Global Institute “Debt and Deleveraging,” 1/2010)?

Three of the four debt components in McKinsey’s study increased by over 200% between 1952 and 2009. Government debt did not increase as much, but only because of normalization off of the WWII debt spike.

Increased debt levels aid volatility and thwart sustainability.

My question: What has allowed the relentless growth in debt usage? Fingers point to central banking, fiat currency, government interventionism (banking, housing, farming, education, etc.) and policy goals the emphasize economic growth over currency sustainability…IMHO. Would be interested in other opinions.

John H., I think that “currency sustainability” is a factor in the Fed’s decisions that commenters here do not consider. The U S dollar is still strong relative to other currencies and that’s a major headwind to exporting and a boon for imports from overseas. The Fed seems eager to lower rates for this reason, and, of course, for stimulating one of the most important economic engines in our economy: housing. Those two reasons, and others, seem to me to explain why the Fed leans toward lowering rates.

Wolf’s article is showing us that, in spite of debt run-up, debt seems to be better managed today than in the past 20 or so years.

The COVID stimulus and the financial collapse completely freaked-out the leadership and are the catalysts for the high inflation rate that is still haunting us. But that’s been tamped down fairly effectively although we still don’t have clear sailing. With back-to-back economic crises, the Fed has done a yeoman’s job of keeping the system from buckling. Fed-haters here need sedatives.

Yeoman’s job?

We have egregious levels of inflation, debt and wealth concentration. A large segment has been locked out of home ownership because home affordability is at all-time lows. A larger number of people have been locked out of investment markets, which are priced so high, Hussman publishes strong data indicating the stock market return over the next 15 years will be negative.

If that’s what is required to keep the system from buckling, a large portion of society would rather see it buckle.

Even if you spend all your time looking at aggregate statistics, you have to realize the situation is unsustainable. How long can we keep raising the debt-to-GDP ratio and liquidity-to-GDP ratio? These are temporary drivers of artificial growth.

The paper games that have been played in the monetary system have been largely facilitated by the military industrial complex and the underlying petrodollar system. See “Confessions of an Economic Hitman” for a full historical perspective. Winning/losing world wars has consequences. Unfortunately, maintaining military might (basically being a global bully) to keep the global population trading in your fiat script has huge energy and resource inputs. While the dollar isn’t going anywhere anytime soon, the world has had enough of America’s bullying and with China’s rising (another gift from Nixon) the availability and cost of resources and energy is causing problems. Debt is essentially created from nothing these days, so it really has no value/meaning anymore. Play stupid paper games, win stupid prizes. At the end of the day demographics matter, and empire come and go. Regardless, with the vast majority of earth’s population happy to trade outside of the dollar system now, things will get interesting. Do you have a tradable skill or own/control/manage productive capital? You better. “Traditional” economic principles are coming back, you better understand what counterparty risk and money-good collateral are. Just my two cents.

Interesting times.

Under any objective analysis, the welfare state is responsible for the Federal deficit. Social spending accounts for half of Federal spending. It will not end well.

In the US, social spending (mostly Social Security and Medicare) has its own revenue source, and is thereby self-funded. Social Security alone accumulated a surplus of 2.7 trillion over the past three decades.

The manipulative agenda-driven stuff about “social spending” never ends. Same BS my entire life. The dad of my high-school sweetheart talked about it the same way to me back then.

@Wolf,

With due respect for your excellent blog and analysis, Social Security spending exceeds payroll tax income, Medicare spending and Medicaid spending also exceed payroll tax income, and the other health care and welfare spending has no dedicated source of funding. Social Security, Medicare, and Medicaid is half of the Federal budget. Welfare programs are another 18%. Defense is 13% and interest is 11% (and rising very rapidly).

Everything else the Federal government does is just 18% of the budget, roads, national parks and forests, regulatory agencies, etc.

Unless deficit spending is controlled, there will be no budget for anything but entitlements. The fastest growing elements of Federal spending are entitlements and interest. This can’t be fixed if 68% of the budget is off limits (entitlements) and it’s really 79% if you include interest, which you have to.

The idea that our spending problem can be fixed without cutting entitlements is a fallacy.

Happy1,

You’re abusing my site to spread manipulative agenda-driven BS about Social Security. READ THIS:

https://wolfstreet.com/2023/10/23/social-security-update-trust-fund-income-outgo-and-deficit-in-fiscal-2023/

Total income from all sources: +$111 billion from the prior year, or +10.7%, to a record $1.15 trillion in the fiscal year ended September 30 (green line in the chart below). By category of income:

Total outgo +$129 billion, or +12.0%, to a record $1.20 trillion (red line), on the 8.7% Cost of Living Adjustment, the biggest since 1981, and more people at retirement age and drawing Social Security benefits. Benefits paid accounted for 99.2% of the outgo; the remaining 0.8% were made up of transfers to Railroad Retirement programs ($5.6 billion) and administrative costs ($4.3 billion).

The Social Security Trust Fund: -$50 billion, or -1.8%, during the fiscal year, to $2.67 trillion.

The Trust Fund invests the $2.67 trillion in interest-bearing Treasury securities and short-term cash management securities. These securities are not traded in the secondary market, similar to the popular I-bonds that many people are holding at TreasuryDirect.

It’s a good thing that the securities in the Trust Fund are not subject to the whims and occasional chaos of the secondary market: The value of these holdings – similar to the value of our accounts at TreasuryDirect – doesn’t fluctuate with the prices in the secondary market. The Trust Fund holds Treasury securities until they mature and then gets paid face value for them. Day-to-day price fluctuations are irrelevant for the Trust Fund.

The Fed’s interest rate repression created the deficit.

The Trust Fund earned $63 billion in interest on its Treasury holdings in the fiscal year, down by 42% from the peak in 2010, the year of peak interest, though the Trust Fund balance was smaller in 2010 than today.

As a result of the Fed’s interest rate repression starting in 2007, the interest rate that the Trust Fund earned was cut by more than half.

Today’s interest rates would eliminate the deficit.

If the Trust Fund had earned an average 5% on its balance of $2.67 trillion this year, it would have earned $133 billion in interest income, instead of $63 billion, and the Fund would have had a surplus of $20 billion!

If longer-term Treasury yields normalize in the 4% to 8% range, as was the case between 1990 and 2007 (they were even higher in the prior 20 years), the Fund’s income and outgo would be back in balance. But it would take a few years before the low-yielding securities would be replaced by higher yielding securities.

@Happy1,

If the employee contribution to payroll taxes were increased by just one third of one percent, then Social Security would be collecting more than it is currently spending. To put that in context, someone making $40000/yr would have to spend an extra $133 *annually*, aka just $2.56/week to “shore up” Social Security. My point is that people keep pretending Social Security is a catastrophe, when in fact it can be fixed for less than the cost of just one cup of coffee *per week*. It is nowhere near “hopelessly spiraling into doom” as people keep insisting.

No Happy……the endless USA war machine caused the deficit.

See Afganistan…. 20 years of military spending.

It makes Happy 1 happy to punch down now and then…..wonder what specific targets he has in his mind?

Not too hard to guess……

I remember exactly where I worked when I first heard people talking about how they had made so much money that they didn’t have to pay into Social Security anymore….sounded stupid then and still does.

The demographic issue seems to be moving to the front burner. Two years ago it was obscure articles about how Japan is getting old. Now I read a few articles a day about birthrates in the US.

This country does have one ace up it’s sleeve that will really change things though – people want to live here. I think the US population is going to crest 400 million by 2100, even as the global population is lower than the 8 billion of today. Maybe a lot lower but I won’t be here to see it.

All we have to do is invite the smartest 10 million Chinese and smartest 10 million Indians and so on from the rest of the world and our cities stay full. Native populations might cash out and move inland but our national numbers will keep increasing. That’s why real estate over time is kind of a sure thing. Thirty years from now does anyone believe any house in the United States is going to be worth less than 3-5x todays “price” in FRNs? They might be worth less in gold but that’s also true from 2004 to today. In 2054 a lot more people will be using US dollars (FRNs) to pay rent and mortgages and they’ll tell stories about how their grandpa bought a house for under a million back in ’24.

Ol’ B-

“In 2054 a lot more people will be using US dollars (FRNs) to pay rent and mortgages and they’ll tell stories about how their grandpa bought a house for under a million back in ’24.”

That’s an excellent conjecture, and well-phrased, too.

Good likelihood of being correct, unless:

A. Gresham’s law is correct

and

B. One of our rivals in the global “hamper” of countries comes up with a currency system that is slightly less soiled than our own “dirty shirt.”

Perhaps a resource-rich and reinvigorated Argentina??

I’ll take wisdom and character over intelligence any day of the week. “Intelligence” is what has driven the dystopian financialization of everything.

John H

How about unrelenting advertising, social media influences, and a large bunch of people who feel they are entitled to buy stuff they cannot afford?

A chosen people making bad choices.

Paul S-

Good points.

Besides the media pressures you describe, the “chosen people” are also following their leaders (governments, and many academics):

Regarding governmental influence:

“There is a natural tendency in men to follow the example of the Government under which they live. The Government is the largest, most important, and most conspicuous entity with which the mass of any people are acquainted; its range of knowledge must always be infinitely greater than the average of their knowledge, and therefore, unless there is a conspicuous warning to the contrary, most men are inclined to think their Government right, and, when they can, to do what it does.”

— Walter Bagehot, Lombard Street

The most interesting part of the article……

“Banks are largely off the hook this time.”

A game changer for sure.

Very interesting to consider the implications of this and what the next down cycle will look like.

Here’s a very recent article from Lev Menard and Morgan Ricks (Vanderbilt U) on the case for banking to become a public utility as the early banking laws intended them to be: https://cdn.vanderbilt.edu/vu-URL/wp-content/uploads/sites/412/2023/09/13223316/Banking-Brief-Graphic-PDF.pdf

Maybe Wolf will post this.

1) Most mortgages are between 3% and 4.5%, the lowest in 80 years. At this ideal condition mortgage debt as % of disposable income is still 60%. At 7% mortgage this ratio will rise along with the cost of : maintenance, taxes and insurance.

2) The Rent inflation is fake : OER northeast, OER midwest, OER south and OER west. The rent component in the CPI is the highest ==> the CPI is fake.

3) [1M] SPX : If June close < Feb close, or if July close < Mar close bad things

might happen !

So good to see you commenting again!

My daughter had to drop the rent 10% in order to get new tenants for the house she rents out in Austin. And she was lucky!

So silly. Just paint the kitchen gray and put a Willie Nelson pillow on the couch. She’ll be able to charge treble the year prior.

Do you live there? Rents are crashing along with prices. In fact there is a population exodus going on in Austin now.

US gov debt is $34T. What’s the Real debt ?

Howdy Folks. Thank goodness the Govern ment is on the hook this time and not the banks. Govern ment knows what it is doing and will make sure nothing bad happens. OK 3 % ers, since you imprisoned yourself, why not HELOC your way to Freedom? Takes guts but you can do it…….

A HELOC to start a business is an extremely risky and stupid idea.

Howdy Outside TB. Wrong again. A Entrepreneur will use all means necessary to grow wealth.

LOL….use credit cards instead?

Howdy ru82. I am 66 and had to put other expenses on credit cards a few times to make a payroll. Or when a deadbeat did not pay on time. Always pay credit cards off within each month.

Howdy and sorry if this violates posting rules. Discover would issue a card with a year end cash back that totaled the yearly cash back. I would put thousands of dollars on credit cards like this and at the end of the year get double cash back. Then cancel the card and renew. Every year was double cash back. Made some money off the credit cards while using their money. Had as many credit cards needed to pay expenses during the month and keep my cash in the bank. Just one way to use credit cards by Entrepreneurs.

Anyone who constantly refers to homeowners with a 3% mortgage as ‘prisoners’ and recommends HELOCs to finance your latest whimsical business idea, all the while calling himself ‘debt-free’ sounds…loopy.

Howdy Julie. You are not a Entrepreneur I take it. At least learn from the Lone Wolf. He showed you how most 2nd homes are owned by Ma and Pa and not Blackrock. If a prisoner opens its eyes and leans and works hard and has some guts, they could easily own a 2nd home like Ma and Pa did. I have too Youngins myself doing exactly what I have been typing about.

HELOCs are now competing against credit cards. The rates are better.

Maybe consumers have figured that out. It’s better to pay ~10% on their consumer debts than 21%.

And given the equity many homeowners have, they might have a higher effective credit limit than what their credit cards offer them.

The rates on HELOCs have always been a LOT better than on credit cards, and they have always competed with them. But most people don’t use their credit cards to borrow; they use them as payment device and pay them off every month and never pay interest. Close to $6 trillion were run through credit cards in 2023, and nearly all of it got paid off.

@ Wolf –

Wolf said: “HELOCs are a way for homeowners to turn their own money buried in their home into useable cash. But to get to their own money, they have to pay Wall Street fees and interest on it.”

————————————————

Wolf, would it not be more correct to say that HELOCs are a way to turn equity buried in their home into usable cash?

…… and at the same time, potentially expand the money supply. ??

Delete or adjust this comment as you will, but I would appreciate your point of view on this.

Also, is it Wall Street that gets fees and interst from HELOCs, or the banks?

If you have “a lot of money,” it includes the equity you have in your home as well as the equity you have in your other assets, plus whatever else you have. “Money” means a lot of things.

In my Random House Webster’s Unabridged digital dictionary, “money” has 20 definitions, things like: #7 “capital to be borrowed, loaned, or invested: mortgage money”; and #9 “wealth considered in terms of money: She was brought up with money”; and #11 “property considered with reference to its pecuniary value.”

Wolf-

Isn’t the process of converting longer term assets into spendable “money” (the money creation process) at the root of the inflation problem?

It’s what the Fed does when it monetizes federal debt by buying US Treasury securities. It’s what banks do when they lend on collateral to businesses. It’s what individuals do when they borrow against their home or future income.

Probably showing my ignorance, but seems to me HELOCs are a tool for homeowners to increase their present living standard, but the trade-off is that they are one more brick in the inflationary wall, adding NEW buying power — and more systemic risk — to an already fragile and emergency-prone financial landscape.

In other words, do money creating contracts between commercial lenders and household borrowers hinder the central bank’s progress toward a 2% inflation rate?

Most bankers are like generals……they always know how to fight the last war well…….and lose the next one. Strategic economic thinking is not their strength. Relationship building is what they do best.

Wolf you seem to have an axe to grind over the helocs. You have some bad experience with them? I think characterization of the banks as BOE (Banks of Evil) as shown in Despicable Me is a bit unfair. They don’t go door to door forcing people to get a heloc.

Wolf doesn’t have a problem with Helocs, I know because I was trashing them recently and he objected, rightly pointing out that they have their place in some situations.

SomethingStinks,

No axe to grind. As I pointed out in this article, HELOCs are becoming more popular again but levels overall remain low, and consumers are in good shape. That’s the main point about HELOCs in this article. I don’t think I made another point.

I don’t even think I mentioned “banks” and HELOCs in the same breath in this article. The discussion about banks was about how they rolled off their mortgages to the GSEs, and how a mortgage crisis won’t hit them as hard as last time (= “off the hook.”)

“… characterization of the banks as BOE (Banks of Evil) as shown in Despicable Me is a bit unfair.”

I have no idea where you found this, not here.

“HELOCs are a way for homeowners to turn their own money buried in their home into useable cash. But to get to their own money, they have to pay Wall Street fees and interest on it.”

Again, this is a weird take. Do you expect people to receive collateral-backed loans of cash at interest rates of 0%?

Reality is not a take.

Wolf has mentioned that assets fall under the classical definition of money – though I agree it still “feels” off to use it this way.

When I look at my house, I don’t see money. I see a roof, frame, walls, etc. I exchanged my dollars for the house because I value it more than the dollars.

No, I expect people to understand that they’re borrowing their own money and paying interest on it. They could sell the house and use the cash. What this drives home is the fact that equity in a home is very expensive to actually use.

Decades ago, there was a different name for cash cow housing…it was “money pit”. I’ve read just about all books by James Grant, and subscribe to his newsletter. From the late 1800’s until 1953, housing was dead money, money pit, and nobody ever considered being a home owner as a wealth accumulation vehicle. I have a book, called “How to invest in Stocks”, dated …1953. The opening paragraphs state that investing in R/E is akin to throwing away money…. LOL.

Wolf said: “Homeowners who purchased their homes more than two years ago and didn’t cash-out-refi have lots of equity in their homes as home prices have surged in the years through mid-2022.”

——————————-

I don’t think is true in your home town, San Francisco.

Well, probably. But June 2022 was the peak in SF too. And it was a huge spike. Prices are down from that spike. But if they bought in 2021, they’re probably close to OK-ish.

But we’re talking about a national mortgage problems, like last time, not local mortgage problems.

9% on only the outstanding HELOC balance. Pay off high CC debt at a 9% rate could be an open door. But would need to control their future spending, a truly scarce discipline from what I can tell.

I’ve forgotten, if a HELOC goes into default, but the first mortgage is paid on time, does the HELOC lender have ability to foreclose on the secured property? Do first mortgage lender’s terms have a say in whether a second mortgage can be attached to their collateral (home)?

Seems like it could get messy if HELOCs take off again. Yes? No?

Howdy Imposter. HELOCs can build wealth if you know what you are doing and can add and subtract like a squirrel.

If your returns/earnings are above the 9% you are paying on the HELOC, sure, but given the percentage of new businesses that fail within the first two years, taking out a HELOC to start a business is not, in my opinion, a wise choice. If you have an existing business and a steady income stream, sure, but….

Howdy Zaridin. You have to understand Entrepreneurs. We are not all the same but driven by?????? I can t explain why I became one at age 19 but did become one. For me, it was the only way to live…….

Yes. No. Yes

Make sure you apply and get the HELOC now and before one loses their job. Even if you do not plan to use it.

I just read a story of a lady who lost her job and now is struggling to pay some bills. But she has over $200k in Home Equity. She wants to tap into this equity to ty her over until her next job. The kicker is the bank will not let her take out a HELOC since she is unemployed. Ouch.

Wolf… just for posterity… I believe in the statement below you meant ‘green line’ and not ‘red’.

Transitioning into delinquency: — still lower than any time before the pandemic (red line in the chart below).

I think that’s pointing out the fact that mortgages are the red line and HELOCs are the blue line in that chart.

I was referring to the mortgage delinquency rates, which are captured by the red line.

“The exception are HELOCs; the government has not yet taken them under its wings.”

——————————

I read somewhere, may have been Wolf Street, that moves are underway to get Freddie Mac to start dealing in 2nd trust deeds.

2nd mortgages are not HELOCs. 2nd mortgages are discussed separately in this article. So read on.

Howdy 3 % ers. Did you know? DBA or LLC, HELOC, 2nd House, Schedule C. Lots of legal ways to prosper and uncuff yourself.

You’re really pushing this narrative. Are you selling HELOCs, perchance?

Howdy Zaridin.. I am retired and RVing around the country and own no RE. I just love learning about the FED here and found the Youngins thinking interesting. Just an old fool with an internet connection and a lot of time on my hands…… Till I drive to the next beautiful landscape without people.

Just visited San Fran Mr Lone Wolf. I did just imagine seeing the Lone Wolfs Lair from the Golden Gate Bridge. A Bucket list now checked marked………..

I like my 3% prison. I’m having a brand new tankless water heater installed right now.

Wolf, data/chart request for you: I’m curious about the mortgage debt burden based on household wealth.

I don’t know if you’ve investigated, but I’m curious if you are interested or could compile the charts. I spent some time trying to piece it together by combining 1) the mortgage balance data by wealth distribution from the FRED with 2) disposable personal income distribution data (“distribution of personal income”) from the BEA.

If it’s valid, it takes a little work, but it could prove insightful. The way I went about it is by combining BEA Table 2.1 with Table 2.10 to estimate DPI by band, matched them up with the FRED data (WFRBLB50102, WFRBLN40075, etc.), and then converted the FRED data to annual values to match up with the BEA data.

My quick analysis shows an inflection point between 2020-2021 (obviously). By the end of 2022, mortgage balances for the:

Bottom 50th increased from 72% to 91% of DPI

50th to 90th increased from 89% to 106% of DPI

Top 10 percent increased from 69% to 73% of DPI

You understand the data better and whether categories are being mixed and other pitfalls. You’re in a much better position given your knowledge and experience to evaluate its usefulness (and correctness).

Wondering if you think there’s any mileage in this approach.

Given that NOT making crucial repairs on a home could lead to serious structural issues and loss in value in one’s primary investment, HELOCs, even with fees and 9% interest, are a sound financial choice WHEN used to maintain housing. I imagine they are going to be quite useful to the Florida condo owners who have been suddenly hit with six-figure HOA assessments to handle deferred maintenance.

Almost like owning a condo is a liability.

Excellent post Wolf!

I find it very helpful when you define certain financial terms. Like disposable income as you did in this article.

And it’s quite rewarding to read all the comments too!

It’s fun to read how others think about things. I already know what I think. DUH!

So reading other people’s various takes on things is a good way to keep sharp.

+1

Question about mortgage balances vs disposable income chart. Is that the actual mortgage balance or the monthly payment vs disposable income? The percentage looks kinda low to me. Thanks!

Mortgages are actual balance in $ trillions. Deposable income = seasonally adjusted annual rate, meaning what it would be for the whole year if the current pace continues. So it’s annual income to total mortgage balances.

Howdy Lone Wolf. How long will we have to wait for the CPI? HEE HEE

MW: Stock Market Today – Dow rises more than 280 points, S&P 500 on pace for record high after April CPI reading sparks relief rally…

I would suggest that people in the US focus on getting their mortgages paid off completely as opposed to borrowing any more money all.

Why pay off a 2.7% mortgage when T-bills yield double that?

You haven’t priced in the risk of foreclosure.

HELOC’s typically come with introductory “teaser” rates of less than 5% for the first six months of the initial draw, which would look quite attractive to homeowners desperate for access to reasonably-priced credit.

The rate will then reset to Prime+ anywhere from 2% to 5% after the introductory period. That is when the problems begin.

Mortgage debt as a percentage of disposable income is 60%, but there’s going to be a lot of data disparity at the individual household level. For example, home prices in many coastal areas are 6-8 x median income, and some households are putting only 3.5% down on a mortgage. The mortgage debt-to-income ratio for these home buyers would be more like 600%, not 60%.

On the other side of it, there are lots of people with huge incomes and zero mortgage debt. These people are pushing the ratio down.

Great point, Bobber-

While examining the big picture is essential to understanding the current situation, DIS-aggregating the “averages” is also essential to understanding fully what’s happening (or what is likely to happen) at the margins where prices are determined.

Useful insights are gleaned from examining the margins, as MBranfors does below…

Wolf, I’m a 32 yr Veteran of Finance. I live in one of the nicest communities in the state of Washington. Gig Harbor has an average home price of 800k. The average income is 80k, above the State average of 70k.

That means the average resident could not afford to buy the home they live in. Furthermore, it means they WOULD NOT QUALIFY to refi their current mortgage….

Too low for too long eventually created a problem, and now these higher rates and make believe (which you have chronicled extensively) are coming to roost…eventually. These housing prices, like office buildings, are grossly overstated as illustrated by lack of income….

An hour after reading your article, in my email in box comes an ad from “Bankrate” for guess what…..HELOC!

They must be listening! :-))

Mortgage balances with a historical look-back to 1949:

https://fred.stlouisfed.org/series/MDOAH

As one can see, the Fed governors stopped publishing this data in 2019/Q3, but since the data go back to 1949, I think this data is a good addition to the chart that Wolf posted in the article.

1. Your link is total mortgage balances, including commercial mortgages. So it’s about $5 trillion higher than household mortgage balances.

2. The Fed did not discontinue this series. The “St. Louis Fed” (privately held bank) discontinued collecting it from the Federal Reserve Board of Governors (government agency), whose data this is as part of its Z-1 financial accounts series.

3. The Z-1 data is still published by the Federal Reserve Board of Governors, including a metric for total mortgage balances, including CRE mortgages that you linked, and a narrower metric of mortgages on 1-4 unit properties owed by households and nonprofits. So that’s not the correct data either.

4. I gave you the correct data, mortgages owed by households only. That is data from Experian, released by the New York Fed.

5. Any 85-year data series that is not adjusted for inflation is going to look like your chart, including GDP. Here is GDP (not adjusted for inflation) going back to 1949: It went from $280 billion to $28 TRILLION.

https://fred.stlouisfed.org/series/GDP

I’m not complaining about your data, Wolf, not at all. I just thought it would be interesting to find something that went further back in time.

I wonder why FRED stops collecting data from time-series that are still available. Seems shady, like they want to hide something from the public. This happens with alarming frequency: I look for something on Fred, and by golly, they have discontinued publishing it.

“I wonder why FRED stops collecting data from time-series that are still available. Seems shady, like they want to hide something from the public.”

The St. Louis Fed, which put together the charting services called FRED, is NOT “The Fed.” It is one of the 12 regional Federal Reserve Banks (private companies held by the largest financial institutions in their districts). FRED collects data from a million sources, including private sector, the OECD, the Bank of Japan, etc. The data in this instance come from the Federal Reserve Board of Governors, which is a government agency and has its own easy to use data and charting service. That data set may still be on FRED but in a new format, and they discontinued the old one — which they do a lot. Or it may not be.

It’s not a useful data set at any rate, because it’s THE WRONG DATA for housing because it includes $5 trillion in CRE mortgages.