Even during tax refund season! Exactly what Americans need. But it’s not helpful for big fleets, such as Hertz.

By Wolf Richter for WOLF STREET.

Seasonally adjusted, prices of used vehicles that were sold at auctions across the US fell 2.3% in April from March, to $18,151, the lowest since April 2021, and down by $5,423 (-23%) from the peak in January 2022, according to today’s Used Vehicle Value Index by Manheim, the largest auto auction house in the US. The index is adjusted for changes in mix and mileage.

From February 2020 through the crazy peak in January 2022, auction prices had spiked by a mindboggling 64%, or by $9,252. The historic plunge so far has surrendered 59%, or $5,423, of that $9,252 spike (red in the chart below).

Not seasonally adjusted, the index dipped 0.6% in April from March, to $18,834, down by 18% from the peak. The plunge so far has surrendered nearly half of the pandemic spike (blue).

These auctions are where dealers buy to replenish their inventories. Supply to these auctions comes from rental fleets that sell some of the vehicles they pull out of service (usually 2.5-3.5 million vehicles per year), and it comes from finance companies that sell their lease returns and repos, from corporate and government fleets, etc.

Year-over-year, the index fell 14% in April. Prices fell in all major vehicle categories on a year-over-year basis, according to Manheim today:

- Luxury cars: -12.9%

- SUVs & crossovers: -14.6%

- Pickups: -15.2%

- Midsize cars: -16.8%

- EVs: -17.5%

- Compact cars: -17.6%.

Even during tax refund season. The big difference between the seasonally adjusted decline (-2.3%) and the not seasonally adjusted decline (-0.6%) is explained by tax-refund season, which lasts through April, and is usually very strong for used car prices, because tax refunds make great down-payments, and ever since there have been tax refunds, used-vehicle dealers have gotten their slice of the pie.

In the five years before the pandemic, the not-seasonally-adjusted index rose 1.5% on average in April from March, with no month showing a decline. But this year, it continued to drop in April (-0.6%), which caused the seasonally adjusted index to fall by 2.3%.

Despite retail sales that are up year-over-year. These price declines occurred even as retail sales of used vehicles in April were up 9% year-over-year, according to Cox Automotive, which owns Manheim.

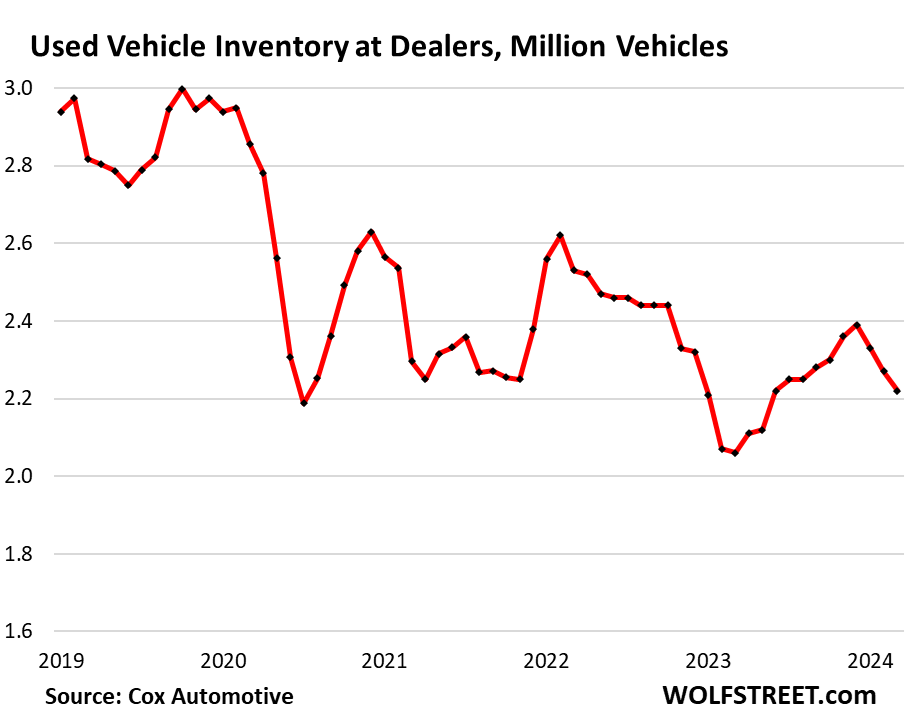

And despite declining inventories. Used retail inventory dipped to 2.22 million vehicles on dealer lots at the beginning of April, according to the latest estimates from Cox Automotive, compared to a range of 2.8-3.0 million in 2019.

This inventory trend – inventories are adequate, but barely, and they’ve declined for months – sheds an interesting light on the historic plunge in prices. It’s not a supply glut that is driving down prices in this historic manner; it’s gravity (the Greek myth of Icarus comes to mind).

These price drops are exactly what Americans need, but… That ridiculous price spike during the pandemic ate a huge hole into household budgets, not only via purchase prices, but also in auto insurance premiums; the CPI for auto insurance has been spiking by 20% year-over-year. And the used vehicle market is now undoing some of the damage, unlike new-vehicle prices, which have gotten stuck at very high levels.

But it’s not so great news for companies that own lots of vehicles. Hertz got crushed by these plunging residual values along with a post-bankruptcy propaganda coup-turned-toxic. And three online used-vehicle dealers, including Vroom in January, are being dismembered in bankruptcy court. It’s not easy for the industry to work through this normalization of the used vehicle market.

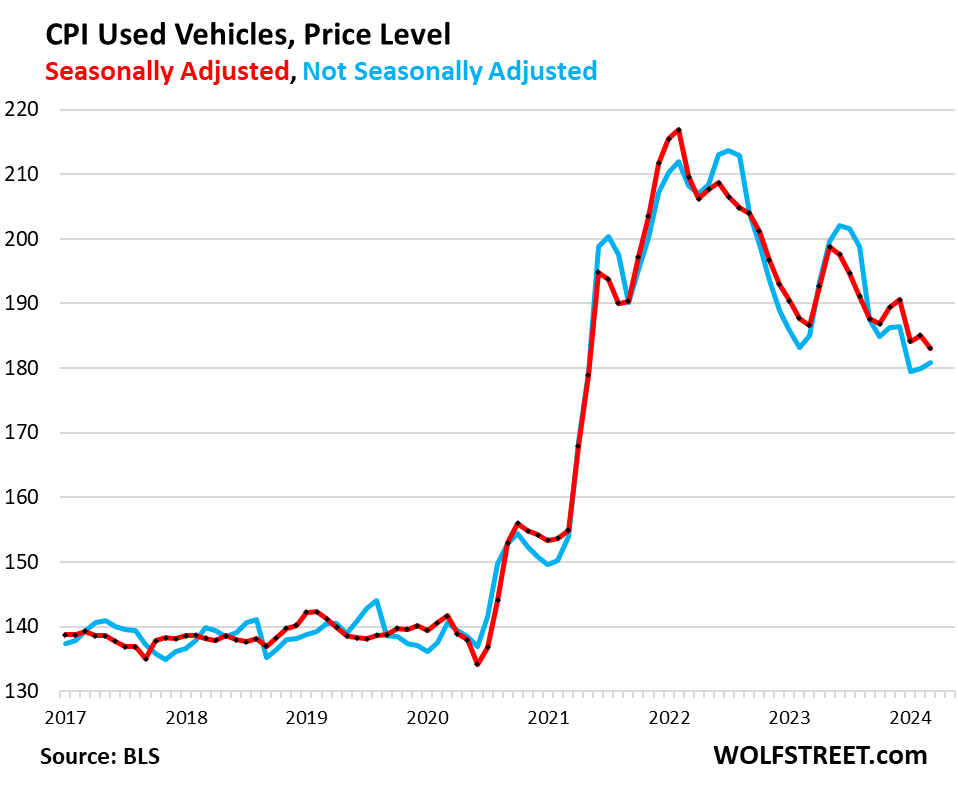

Retail prices, based on the Consumer Price Index fell by 1.4% seasonally adjusted in April from March (red); not seasonally adjusted, it dipped by 0.4% (blue).

From February 2020 through the peak at the end of 2021, it had spiked by 53%. From that peak, it has dropped by 17% (seasonally adjusted), having given up nearly half (48%) of its pandemic spike.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, Do you know why Carvana stock is doing so well?

Carvana did a debt restructuring by implicitly threatening its noteholders with a bankruptcy filing. Prices of those notes collapsed and got bought for cents on the dollar by PE firms and hedge funds, that then agreed to do a debt restructuring that forgave nearly $1 billion in debt, which kept Carvana out of bankruptcy, and the hedge funds made a bundle.

The rest is Carvana hype, same meme crowed as before.

Hi Wolf, just a quick question on this. How did PE make such a bundle? Did they forgive the debt for equity and subsequently made money on the appreciation? Sorry if silly question just curious and I don’t have the details.

If you buy the debt for 15 cents on the dollar, you can forgive 40% of its face value and make a bundle. I think they also got some goodies when the new debt was issued. I don’t remember the details of the deal, that was last summer.

Sounds like an interesting situation/expensive game of chicken.

Unsecured bondholders are a lot more exposed than they frequently think (historic returns to them in bankruptcy might be 25 cents per face value dollar of bonds…in this debt debauched age, it might be 10 cents on the dollar.)

But…the equity holders (usually with insiders holding a huge chunk) get *zero* in bankruptcy. So I wonder how said insiders bluffed the unsecureds regarding a bankruptcy filing.

People buy bonds to get returns – not 50%-80% haircuts/screwings.

So I wonder why the unsecureds weren’t able to more effectively fight back/raise holy hell.

PE always makes money on every deal they do. Someone else gets thrown under the bus and they walk away with a pile of cash. They’re ruthless enough to throw anyone and everyone under the bus for $$$. That’s the game.

PE has thrown every grandma under the bus multiple times between gutting pension plans, blowing up healthcare costs, and printing credit against everything. It’s really quite awful.

Regarding PE firms – how do the higher/normal interest rates affect them?

@CCCB,

PE certainly will sell their grandma for a nickel, but they do occasionally lose vast sums on a bad bet. See Envision and KKR for one example.

Two questions.

1. Is Carvana’s business somehow fundamentally different from the other used car dealers that you’ve covered? I would think the decline in used car prices would compress their margins much like with Hertz.

2. What would need to happen for used car prices to decline back to pre pandemic levels, if at all possible? You’ve mentioned fewer new cars being made means fewer used cars later available. Do you think it will take a return to pre-pandemic levels of supply of new vehicles and/or substantial price cuts or both?

This is not a “normalization” in prices imho but rather an ongoing collapse in peoples pocket books. The demand(need I should say) is there, the money is not. Its a wipe out in inflation and we are starting to see the wipeout spread to other sectors. My car business is stagnant and spotty since January, and this wipeout has barely not even started at the rich…yet. Some nice things which used to get calls like in full size, now get not one(gas related I figure).

Sales are up 9% yoy. Despite the higher interest rates.

“ongoing collapse in peoples pocket books” is the funniest bullshit I’ve read all day.

https://fortune.com/2023/08/16/americans-savings-nearly-depleted-sf-fed-study/

https://www.wsj.com/articles/once-flush-savings-accounts-are-starting-to-run-dry-11675691637

https://www.businessinsider.com/us-households-on-brink-household-savings-dry-up-september-fed-2023-9

these articles have credibility. The Fed lowering and revising lower? Not funny bullshit happening. I know firsthand street level lower and middle classes now hurting Upper class not hurting ..yet.

Steve,

The headlines/articles you linked are stupid clickbait bullshit. They’re talking about the “savings rate” (=income minus spending). That saving rate was huge during the stimulus time, giving rise to this fake theory of “excess savings,” that is somehow supposed to be burned off now. But the savings rate is STILL 3.2% meaning that even now consumers save 3.2% of their income and are still ADDING to their savings. That “excess savings” BS theory has been debunked many times, including here. Only clickbait dumbass articles still try to get some morons to spread these headlines.

Here are the actual savings, in trillion dollars, in money market funds and CDs, by these consumers.. This does not even include the trillions of dollars consumers plowed into T-bills, bonds, and stocks. Consumers are LOADED. All you have to do is RTGDFA:

https://wolfstreet.com/2024/04/27/money-market-funds-t-bills-large-cds-small-cds-americans-learn-to-arbitrage-the-higher-for-longer-interest-rate-environment/

I don’t think “excess savings rate” is all BS. After all, it wasn’t invented by clickbait journalists but SF FED analysts. My interpretation of the idea is that there is some base saving rate that is needed for saving enough money for retirement / sudden health / other expenses. When covid hit, people stopped spending and suddenly saved up huge excesses of money that they don’t really need on top of the base saving rate that already covered their needs. Once the economy reopened, they were happy to splurge and spend that excess (your drunken sailors). However, there is some point after which the excess savings are all spent, and people need to return to keeping up with their pre-covid sensible base saving rate. The SF FED analysis tells us that we arrived at this point, people depleted their excessive savings. Of course they are still saving 3.2% as they responsibly should, but there is no excess money slushing around in the economy driving up the prices crazily. Which is also observed in all the metrics you track (house prices, car prices, etc).

It doesn’t indicate that things will crash, though if businesses expect similar splurge in the future as in the last few years, they might be up for a rude awakening and that could induce a crash. I’d expect them to be smarter, in which case we would only see price stability instead.

“After all, it wasn’t invented by clickbait journalists but SF FED analysts.”

LOL. Not the SF Fed, but a young guy, Hamza Abdelrahman who graduated from college in 2020, came up with this theory while at the SF Fed. And then it was turned in to braindead clickbait headlines by the media because it worked, because people clicked on this stuff and spread it because it fit their narrative (“Americans are tapped out” which is bullshit).

Economists — some fresh out of college, others with PhDs — working at the Fed is a huge Federal Reserve program where all Federal Reserve Banks in the US give university economists a chance to get this stint on their resume, and in return they can never ever criticize the Fed. There has been some good reporting on this issue of how economists in the US get compromised by their stints at the Fed.

Anyway, this chap, three years out of college, came up with this theory, and everyone spread it around because it suited their narrative. It was completely bogus and has been debunked by the facts and by other economists. In this theory, there is an essential confusion about the flow of money (savings rate, what the paper uses, and it continues to be positive) and the stock of money that consumers have (actual savings and investments that continue to rise).

Just look at the actual amounts consumers have in investments and savings. They’re huge, and they’re still going up as consumers are still adding to them every month. I cannot believe people are still clinging to this narrative despite all the facts. In 2030, people will still claim that very soon, next month, consumers will run out of their pandemic excess savings.

Wolf, that’s quite depressing to hear about the made-up research at the fed. Haven’t heard it before but it’s illuminating, I won’t take their word at face value.

Now I understand why you linked some proxy charts for the overall household savings. What it’s still missing is that much of the money that went into MMF and CD is probably coming from selling stocks, so it still doesn’t show an accurate picture of the overall savings. I don’t know how to think about the stock market part, on one hand it has also gained a lot (so one could say that households have even more savings there), on the other hand it is driven by corporate buyback programs and hedge fund speculation which makes it harder (for me) to know whether households have increased or decreased their equity.

Playing the devil’s advocate, looking at the PMSAVE chart (https://fred.stlouisfed.org/series/PMSAVE) we see that households are savings less money – even in nominal value than pre-COVID so some of the “hardship” must be true. Yes, it’s not real hardship as households are still saving money just at a lesser rate than a few years ago. Then, household composition is also changing… do you think it’s fair to say that people are saving at a lesser rate now?

” much of the money that went into MMF and CD is probably coming from selling stocks,”

It came from savings accounts and checking accounts that didn’t pay interest, and people moved it into instruments that did pay interest.

Total deposits in the US are close to $18 trillion, not counting credit unions. Money Market funds are over $6 trillion. T-bills are at nearly $6 trillion and soaring! This is not all household money, of course, this is total, but it gives you a feel of the magnitude of this cash floating around, and big part of it is household money.

Your link to PMSAVE shows the “seasonally adjusted annual rate” (SAAR) of monthly savings. So last entry was for March, it showed $671 billion SAAR. So divide that by 12 to get an approximation of the monthly figure, which would be about $56 billion in added savings in March.

“Savings” here does not mean putting this money in a savings account. It’s just math: disposable income minus personal consumption expenditures. People might use it to buy stocks or make a downpayment on a car or a house.

Seasonally adjusted annual rates were made useless during the stimulus era because each month that stimulus occurred, it was multiplied by about 12 to get to an annual rate as if that stimulus occurred every month for 12 months in a row, which is of course nonsense. I stopped using those charts for that reason. They’re now meaningless when comparing to covid times.

But these charts are meaningful if you compare current time to pre-covid time. And you see that the current $671 billion SAAR is at the low end of the 2013-2019 SAAR of $575-$900 billion. You can also see that it is substantially higher than before the Financial Crisis. The savings rate (PSAVERT) of 3.2% shows the same thing: people are saving just fine, less than they did in 2013-2019, but more than they did before the GFC. They’re saving – that’s the main thing, they’re adding to their wealth, instead of tapping into their wealth.

I sold my car dealer ship 3 months before 9/11 and of all of the decisions I have made in my life, that is the one thing I don’t regret.

And a year before 9/11 we sold our house for double its price and bailed out of Baghdad by the bay and the state with no regrets.

I agree with el lobo that consumers are absolutely drowning in cash and that they spend like drunken sailors while their nest egg continues to grow.

All I have to do is look around me at retail settings &

restaurants and witness an outright gleeful level of conspicuous consumption. Multiply on to that the nonchalant payment of exorbitant rents & prices for home purchases and you have clear evidence of how cash rich consumers are (who needs the SF Fed or brain washed recent economics grads to tell us anything?!).

As for the market for cars, it completely befuddles me.

What befuddles me as well is why all the angst about high interest rates when cash is plentiful and being shloshed around like an over-full beer mug? People are paying $25 for a lousy cheese burger and shelling out half of a million dollars cash to buy a two bedroom bungalow! What’s the big deal about credit costing more than zero percent?

Thanks Wolf, for stirring the pot, as always!

Max – dunno, maybe it’s bigger proportion of the society that got generationally-used to availability of, playing, and occasionally winning, with house (low-interest) money?

may we all find a better day.

Bitcoin has no intrinsic value and still sell 60k a coin. It’s just a game of music chair. There is no need to explain the short term pricing of any assets.

The state of price of bitcoin defines how loose the financial conditions are .. generally speaking .

I don’t know if you are old enough to remember thr hype/market bubble in Beanie Babies. Little stupid plush toys, selling for hundreds and even thousands of dollars.

Of course the bubble burst.

However here we are many years later and there are still Beanie Babies listed on eBay for a few hundred dollars. There is very little volume, but they still sell. It is mostly believers/collectors selling to other believers/collectors.

The point is, many years (or even decades) from now, there will still be a few Bitcoin being traded at otherwise outrageous prices.

It is the volume that matters though. There won’t be shoeshine people suggesting to their clients that they buy.

You might not find value in BTC, but all value is subjective to utility. Does BTC have utility? To me it does. I very much dislike having my wealth in a money system which I find wrong and unjust (USD). This is my personal perspective. I also like having direct control of my wealth – I don’t trust the middlemen (government). BTC is the first and only wide spread digital money-like system which the holder solely controls the transference of value. BTC allows me to control/transport/send any amount of value, held on a secure digital device, on paper or even in my head, all the while immune from confiscation, and reconstitute the value in local currency. All this done with pseudonymity. It’s like gold that can be teleported. For all it’s faults, BTC is a watershed idea/tech – it will be interesting to see how governments and society react.

Just as interesting, imagine a world where anyone anywhere can issue or invest in “shares” on a bitcoin like network. For example, when google/apple threatened to take X on their platforms, Musk threatened to make his own phone. That would take huge amounts of capital – unable to obtain withing within system without “regulatory” approval. Musk, with is personal clout, could issue tokens (shares) in a new venture. Of course, in the current system the government would stop him. Think of all the small scale value creating projects ($10M-10B?) around the world that are not happening for lack of capital access. Crypto may become a free market, elastic money system, as revolutionary to finance/capital as central banking.

“BTC is the first and only wide spread digital money-like system which the holder solely controls the transference of value. ”

There’s literally 10s of thousands of crypto-currencies which all behave essentially the same as bitcoin. Many are “wide spread” by any reasonable metric.

Bitcoin was not the “first”: eCash, E-Gold, hashcash being some examples of decentralized pseudo-anonymous transfer systems.

If you think you “solely” control the transfer of your Bitcoins, then you misunderstand the technology: such transfers require the cooperation of the army of ‘miners’ who ledger the transfers. This is why your transfers take 30 minutes to be confirmed, and why you are paying a fee to have them do the work- the same fee which spiked to ~$200 for a moment last month.

I think you are mistaking the concept of “utility” for the concept of “someone is willing to trade me fiat or goods or services for it”. The former will continue to exist even if the latter ends: gold can improve electronics, art can give joy when viewed, real estate can house people.

But if everyone were to lose interest in buying your bitcoin, what could you possibly use it for?

grant – your two concluding paragraphs have made this a rare day for me in our Age of Mammon. Many thanks!

may we all find a better day.

Grant

Other crypto’s are not wide spread and are not money-like. There exists few coins (understand coin vs token and proof of work vs staking). There is not a single metric by which any other crypto remotely approaches BTC with respect to being wide spread.

Precursors to BTC were all totally centralized, so could be shut down by controlling a single set of servers (they only had one miner). This is why they all failed (govt force).

I need assistance to transact, but only I and I alone can initiate the transaction, thus control it. Anyone can mine and all follow the same rules, so all are incentivized to process all transactions that meet the rules. Even if some did not process a specific transaction, others would, and once processed can’t be reversed. It has never happened that miners not process a transaction over time. The fee is free market priced based on space on the chain, due to the trade off between space and decentralization.

Money is not an end use good, but has the most important utility of any human invention. If everyone looses interest in any money, what good is it? The value humans put on gold is almost all due to its use as money, and this is due to the fact that nothing works as good (divisible, fungible, durable, scarce and verifiable). The exchange rate is just supply and demand and is irrelevant to the utility of money. People will not loose interest in monies that are very good at being money. If humans come up with better money than existing options, crypto, fiat, metal or otherwise, we will use it. Please let me know when you come across it – I’m serious.

Mitchell – I take your point, but it sounds like another case of a tool becoming more important than the mission, and the dead ends that may lead to…best.

may we all find a better day.

I know nothing about the car business. Do higher interest rates affect the supply on the lots? Do dealers try to move cars quicker when the interest cost of having them sit idle on the lot is higher?

Dealers always try to move used vehicles quickly, but now there’s even more urgency because prices are falling faster than normal.

Plus, floorplan interest rates have risen, obviously, and so inventory funding has become more expensive, which is another incentive to manage inventories well.

Higher interest rates have a downward pressure on used vehicle sales and prices, in theory. But only about 37% of used vehicle buyers finance their purchase (Experian data), while 63% pay cash (we’re among the cash payers), which limits the impact of interest rates. So, unit sales are still up 9% year-over-year.

Higher sales and lower inventories would normally translate into upward price pressures. But not this time; gravity is just too strong, it seems. The whole thing is very unusual. By unusual, I mean I have never seen anything like this before in the four decades I’ve been looking at this.

“But only about 37% of used vehicle buyers finance their purchase (Experian data), while 63% pay cash (we’re among the cash payers), which limits the impact of interest rates.”

Interesting, since 85% of *new* car buyers finance.

Sure, used cars are cheaper but I’d guess that half of used sales are only about 50% cheaper – that’s still a hefty chunk of change.

Interesting that 85% will finance a 35k purchase but only 37% will finance a 17k purchase.

Bunch of reasons, in addition to the cost of the vehicle. New vehicle loans and leases are a lot cheaper than used vehicles financing. Lots of new-vehicle loans are subsidized by the captive finance companies (such as Ford Credit). In addition, new vehicle leases can be very attractive for people who’d have the cash to easily pay for it. It’s a super-hassle-free way of driving a vehicle. Dealers push new vehicle financing very hard, it’s big profit center for them.

How is leasing attractive in anyway to wealthier people? That seems like a pretty raw deal financially when you can buy a 100k mile well maintained Honda for 10k and drive it for a decade and still sell it for a few thousand.

I’ve never leased anything but I remember when I learned how it worked I thought it was insane to do.

Trucker –

Wealthier people are likely more often business owners and leases have advantages there.

Wealthy people may also want to use some of their excess money to have a new, under warranty car often with a maintenance plan…and willing to pay some to continue to get that new car feel every 2-3yrs

The wealthy can be smart with their money but they can also have freedoms to make certain money decisions that aren’t always the most frugal.

”when you can buy a 100k mile well maintained Honda for 10k”

Not anymore you can’t, at least not if you want a car that’s less than a decade old.

I think that the experience of used car dealers and their inventory are a great lesson for those who want to see disinflation in the overall economy.

I don’t think they will learn from it rhough.

They should. Experienced dealers will. But the past few years have taught less experienced dealers a bunch of bad tricks. Those who have only been in the industry a few years have seen the value of their inventory rise over time, which destroys the incentive to move things quickly. This is not normal. Used vehicle prices normally drop, plus the carry cost adds up.

More experienced dealers know that you have to move stuff fast. Even if you sell at a loss, cut it, get most of your cash back, and find another deal. Some now are refusing to lower their prices, and others are following the market down without cutting prices fast enough to move inventory.

However, when a bank pulls your flooring line and the rollbacks show up to take your collateral, the game is over.

All I know is that none of this 59% dealer wholesale price decline has shown up meaningfully in the used Ford Ranger market. Somebody up the food chain is pocketing that money. There was a decline in the first couple of months, but I do agree with Wolf’s assessment of spring being high cotton season for car sales due to tax refunds.

Note that there are two measures here: The one you mention is the 59% unwind of the pandemic price spike, not the decline of the total price — meaning that over half of the pandemic price spike has unwound.

Im interested to see if prices go all the way back. If 50% higher is the new normal it’s still damage done.

Weather inflation continues or not, the new overall price level will be higher.

My guess is that it will depend on which segment of the market you are shopping in. The high rates could bring the high end of the market below the pre-2020 trend. Most Americans can’t buy things if the bank won’t loan them the money.

The low end of the market is probably permanently higher. Many people have gotten priced out of the market segment they would have previously shopped in, but they still need to drive something.

I know I could use a new car, but I’ve been sitting on my hands waiting. I ended up paying a few thousand more in federal taxes because I’ve moved a bunch of money into treasuries. No refund this time.

“I ended up paying a few thousand more in federal taxes because I’ve moved a bunch of money into treasuries. No refund this time.”

I owed the FED a pretty good chunk, but I got a refund from the state. One of the reasons I like T-Bills vs CDs.

hold your cash ,when deflation hits move quick . my guess 9 months

Ever since I’ve been an adult, people have threatened with deflation later this year or whatever. In my entire adult life, we only had a handful of quarters of mild overall CPI deflation, always due to a plunge in oil prices. The Core PCE price index (which excludes energy) never went negative YoY. So, by now, I just laugh about these deflation-mongers. They’re a joke.

wouldn’t deflation have occurred at various times throughout the developed world had the governments not tried so hard to stop it from happening?

Deflation is stopped by inflation; exactly what Jerome Powell’s Federal Reserve did the QE (Quantitative Easing) for.

In March-June 2020, the Fed did $3 trillion of QE to absorb the $3 trillion in new debt issued by the government over the same period to pay for the pandemic relief programs amid the expected collapse in tax revenues.

“In my entire adult life, we only had a handful of quarters of mild overall CPI deflation”

True…but it is worth pondering why more than a few industries *are* capable of turning technological advancement into cheaper prices…while some of the biggest fish find it “impossible”.

Isn’t it curious that the large wooden boxes we live in are 10x more expensive following 60 years of technological development – while microchips have become 10,000x more powerful at 10% of the cost.

Cas127,

Yes, it’s curious. Services have driven inflation in the US for many years. Manufactured goods have a tendency to get cheaper (same product over time), or price goes up but the product gets a lot better (cars), or price goes down and product gets a lot better (laptops… I’ve been buying $800-laptops for 20 years, and the one I bought earlier this year is a supercomputer compared to the one I bought in 2002). But houses and real estate are not manufactured goods, and they involve a lot of costly services (architect, general contractor, electrical services, etc.).

“But houses and real estate are not manufactured goods, and they involve a lot of costly services”

That is pretty much the consensus response…but…

1) the line between manufactured product and homebuilding “service” can get pretty blurry. It isn’t like zillions of very advanced “services’ don’t go into microchip production (cutting edge electrical engineering for one) and isn’t like the “big wooden boxes” of SFH don’t actually consist of oodles of mass produced products, stamped out for decades, and decades, and decades (drywall, concrete, dimensional lumber, wire…).

I recognize that a bunch of ZIRP-advantaged guys in work clothes are intimately involved in the SFH process (especially in incremental marginal output, relative to chip production) but still and all the dichotomy of price trends over decades of technological advancement is striking.

2) Historically “finance-able” industries seem particularly subject to this inflationary disease – finance is the fuel without which the price inflation would self-extinguish. So SFH housing relentlessly goes up, college tuition (see student loans) relentlessly goes up, and car prices (perhaps usually less relentlessly) go up.

I am a general contractor so take my input with a grain of salt.

It is indeed a wonder that computers are amenable to automation yet the boxes we call single family homes aren’t. Maybe because computers have national security implications whereas single family homes don’t.

Take homes with perfectly square wall and floor modules as an example. Yeah, they’re damn near perfect (at carpenter resolution) and go up in 2 or 3 days, but the foundation isn’t ever built to that resolution. So you get framers racking the wall modules to get it tight to the sill plate and it twists the walls, and that twist is transferred to the floor module. By the time you reach the second story, you can roll a marble down your supposedly flat and level floor. Carpeted floors are useful for hiding that kind of defect. In case you were wondering why million-dollar homes built in 2023 have cracked drywall in 2024, modular construction is one reason. The older method of stick framing would fix that, but it’s more expensive, more labor intensive, and requires more skill to do well. Same with plaster. The modern version of plaster, as applied to drywall, is called a level 5 finish and is very expensive for the above reasons.

If only someone would build a machine that grades, digs, pours, frames, roofs, installs windows and doors, routes plumbing and electrical and mechanical, hangs drywall and then installs beautiful finishes in colonial or Georgia federal or Victorian or modern or whatever interior style you want. In primitive form, such a machine exists. It’s called a construction crew.

Maybe once our brain trust finishes the AI project, someone can start a space program to unify and automate the trades. Until then you’ll have to hire people to build your home.

I hope you’re on to something, Flea. But where does the 9 months prediction come from? It’s mother’s day today. Could your 9 months be a play on gestation time?

Every time I hear someone say tax refund I correct them and let them know they gave a free interest loan to an uncle, who just paid it back after a year.

You’re not wrong, but you’re not “correcting” anything, because “refund” is already the correct word to use when someone is repaid a sum of money.

Hopefully you’re not ‘one of those customers’ who returns a sweater to Walmart and then tells the clerk “you’re not refuding me, you’re repaying an interest free loan”.

DM: Retail Chain Sam Ash Music Shutting Its Doors Entirely…

Beloved family-run US business to shut down all stores after 100 years of trading

An iconic family-run music business has been forced to shut down all of its stores after 100 years – killed off by online retail.

I thought it a bit weird killed by online retail as folks buying guitars/drums/mics/gear ect. want to check em out/try in person.

I am sure some folks then go online but feel tis a lot more to story then online sales as stated,feel perhaps a lot of folks just can’t afford gear(sad,was in a band meself).

A friend bought many guitars over the years in store,he would bargain for extras but usually walked out with something,was with him when he got his Les Paul custom,beautiful sounding and looking instrument.

Sam Ash (and everyone else) cannot compete with Sweetwater. They have a very flexible return policy and have a huge stock which ships immediately.

Guitar Center recently went bankrupt and restructured, but I think they eventually will vanish too.

Local guitar center was on life support for a long time. No inventory, never anybody in there. They’re kinda coming back around with stock but nobody is ever in there.

Guitar center has an online centric presence know as musiciansfriend.

Trucker – speaking of music retail, I imagine the local Spokane acoustic scene no longer supports small local shops like ‘The Sound Hole’ off of Sprague, where I got a great deal on my cosmetic-second (but musically-first!) Bozeman J45 back in the early ’90’s? Best.

may we all find a better day.

Any beta on Guitar Center?

do not agree killed by online maybe some but mostly lack of of disposable cash for expensive music items. Inflation victims showing up everywhere, and spreading, faster now.

Maybe higher auto insurance costs are adding to purchase hesitation. It’s possible that even well off Baby Boomers are reaching a new inflection point (for many things).

“purchase hesitation?” LOL. Sales are up 9% year-over-year, despite higher interest rates and higher insurance costs. Inventories are down too. But prices were crazy, and they may be in the process of normalizing.

As an auto enthusiast, I follow a lot of the private auction sites like “Bring a Trailer” and “Cars & Bids”. The last 30 days is the first time I’ve seen a number of highly sought after cars go un-sold due to reserve prices not being met, and other highly sought after cars sell for *significantly* less than they would have in the last 6 months.

Case in point 2020 Porsche Taycan GTS. Listed new for $151 (likely sold originally with a significant markup, as well): bid to $64,000 and did not sell.

2016 Porsche Cayman GT4: New for $106,000, bid to $96,000 but reserve not met.

2022 BMW M5 CS: New for $149,000 (and most of these were pre-sold with a $25,000 – $50,000 markup); Sold for $130,500.

In talking with some friends in the enthusiast community, it seems there are a lot of people who are starting to unload cars at prices that would have worked 6 – 8 months ago, and finding no takers.

It would seem that a little bit of normalcy is returning.

now i understand just a market adjustment,not deflation. all in hoe you word if

Deflation is a broad-based decline in prices across the economy.

If gasoline drops in price, it’s not deflation.

Noticed the same thing.

For the last 6+ months they are getting RNM / No Sale on 20-30%

of the auctions. It is not limited to just the high end stuff.

A 1990 BMW 3-Series M3 just went for $200,000 last week and a 1972 BMW 2002 just went yesterday for a record $100,000 on BAT…

1990’ies BMW 3-series M3 are in short supply. And somethin very different from a 2020 something M3.

Around here you see something of the same on farm tractor pricing. The last pre all electonics before about 1990 catch higher prices than later models. Old MF135 or Ford 3000 series prices have esentially stabized. Price depend only on condition, not age.

Week in Review — May 5th, 2024 – Doug Demuro, Cars & Bids

We’ve just wrapped up another great week on Cars & Bids! Notable sales ran the gamut, from some of the best American sports cars of the last few years – including a Cadillac CT5-V Blackwing that brought $109,000, a Camaro ZL1 Coupe that sold for $47,500, and a nice C7 Corvette Grand Sport Convertible with an automatic that brought $59,000, among many others – to Japanese and European icons. At the top of that list is an R34 Skyline GT-R V-Spec in Midnight Purple II that sold for a strong $188,500 after 9 minutes of overtime bidding!

This week is another exciting one on Cars & Bids! We’re starting it off strong with an Ultraviolet 991 911 GT3 RS, truly one of the most thrilling modern sports cars. The excitement doesn’t end there, though, as this week we’re hosting everything from purpose-built race cars – such as a 2,300 pound Radical RXC Spyder that features a 650hp Ecoboost V6 and a sequential transmission – to some of the most desirable new enthusiast cars, including a 6-speed manual Lotus Emira V6 First Edition and a supercharged V8-powered Ford Raptor R. I’m equally excited, though, about some low-mile examples of truly special cars. That includes a 26k mile E46 BMW M3, as well as – perhaps most notably – a 996 911 Turbo Coupe with just 13,500 miles. Happy bidding!

People always going to speculate some cars are getting bid up hoping for the next set of fools.

Only a few rare ones will command more in the future a ton of these will lose value as others did.

See the 80s and 90s, my old wine club friend told me how a few of his buddies sold those lousy Daytona’s for the new diablos….

Not like they needed more $$ but during the good times lots of fools part with their cash

I’m just gonna throw this out there: it appears he’s excited?

maybe “Super” excited . . .

there are also several levels AFTER “normalcy” in the business cycle, this cycle being the biggest bubble in history.

On Facebook Marketplace, during the pandemic era “four-eye” Fox Body Mustangs were listed and selling for $15k-$20k. Lately I’m seeing those same era Mustangs (1983-1986) selling for $8-$12k. They aren’t exotics but an illustration of how things have changed.

Are used cars a candidate for your pantheon of Imploded Stocks?

Maybe I should create a separate side-room for them?

A show room!

How could they be in the pantheon when prices are still up 50% in four years?

We’re just joking. Used vehicles don’t fit into the pantheon anyway because they have value and utility for real people, even if the price is down from the peak (which is a good thing), whereas stocks in our pantheon of Imploded Stocks are just get-rich-quick gambling tokens that crashed.

Like with real estate in most places, still up 50% since pre-pandemic. A 50% rise in homes and cars in 4 years would have been extraordinary by itself. Throw in the even greater increases and subsequent decreases, it just makes it all staggering to witness .

DM: Biggest hospital bankruptcy in decades affects 2.2 million patients across eight states

The largest private hospital chain in the US filed for Chapter 11 bankruptcy on Monday after months of financial instability. In a shock move, it has now put all its hospitals up for sale.

Good catch.

Just think how crappy the hospital business must have been run since,

1) Health care is among the most heavily subsidized industries, and

2) The looming threat of death tends to undercut negotiating power/demand elasticity…

Inflation kills, deep down, inside out and all around.

Tax refund? Never heard of such a thing……

Thinking it was 06 last time I purchased new truck.

Cash buyer for used. I could not find a 2nd work truck

worth prices they were getting.

Now I’m sorting through all of the affordable ones.

I would imagine only thing holding up new work trucks is back log of

fleet purchases by the big contractors.

Backhoe or Mini Excavator, used would have to be in great condition

to be tempted. All the manufactures are offering 0% @ a minimum of 4yrs. Some areas of this economy….not so hot.

250 thousand miles on my SUV is what I plan on driving it till, then buying used again. I wonder if the vehicles 50 yrs ago could take the abuse…..don’t think so.

People holding onto their vehicles longer?

People buying used as opposed to new, might be a reason for fewer cars on the used dealers lots, as well as the stubbornly high prices of new…. And whatever else you said… probably in one of those charts.

Icarus the Greek, buying used wings….high mileage…

In past days I bought up to 10-year-old Cadis (in like-new or near condition) for $5,000, then it became 15-year, and my latest (6 years ago, and still $5,000 before the bubble) was a now 25-year old + like-new Cadi driven by the legendary “little old couple” with 50,000 miles on it, new tires, and had dealership maintenance at all the required intervals.

Never had a problem with any of them, and getting a $70K or 80K car for peanuts because they depreciate horrifically has always been a pleasure.

I’ve put about 5,000 miles on the latest one, again, trouble-free, and may drive this now almost antique for many more years.

By that time I hope that that at the current rate of declining prices the bubble will have fully deflated and prices will be back to my comfort level. As long as the car doesn’t talk to me, doesn’t have touch screen, and doesn’t report everything to command control central it’s a candidate.

On second thought, I may just keep this one forever.

…the failure to perform “maintenance at all the required levels” seems endemic, these days (it’s often neglected upon the cost-discovery of keeping something running reliably long-term, relying on not ‘fixing something that ain’t broke’, until, of course, it is -frequently at a PNR …acknowledging, of course that the contemporary period for ‘longterm’ has increased for many things…).

may we all find a better day.

may we all find a better day.

Maybe I’ll keep her forever,

Here I am at manheims used car lot, looking,

Hoping the used car I’m eyeballing was well maintained and not abused- cared for.

It was owned by a respectable elderly lady is what I was told…

Now that I have her, knowing how to maintain, diagnose, and fix her. Note, She seems a bit unstable at higher speeds.

3 weeks later… All good… I think she likes me.

Hi Wolf, US population is increasing by 2 million a year. Yet new car sales is nit close to 18 million a year that was accomplished in 1983. Why? US population was around 220 million in 1982 and now 340 million. Yet new car sales are lower. Used cars were there in 1982 too. What is your view?

I have discusses this stuff many times in the articles over the years. Not going to repeat it in the comments.

Not Wolf Ram, but here’s my take:

1. As Wolf has commented many times, the durability of vehicles in general, at least until getting to the actual HD pick up trucks, 3/4 ton and above was pretty poor.

2. The pricing was much lower, as in you could buy a new 1/2 truck for a couple thousand in the sixties.

3. In general, the quality was based on extensive ”value engineering” the dodge 360 engine being an example of one released BEFORE the VE had been done and was legendary.

4. IMO, dealers did not have the same profit motive for their service depts. as they do these days, except perhaps the very high end ones, and many folx did their own maintenance, etc.

(Been driving since 1953, but all anecdotal, not statistical as Wolf is.)

The engineering is successful to the point the profit is in conflict with the empathetic imperative that underlies the concept.

The tolerance of the grift that We, the American family, is willing to tolerate is theThe tol exact reason for the invention of the business model

Of my five vehicles, the only one that gives me serious trouble is the newest; a 2002 BMW 525I Touring Wagon. Its computer driven garbage is just that, garbage.

But i like the car overall.

Anyone who buys a car built in the 21st century deserves what he gets.