After ON RRPs go to zero, reserves will decline, further reducing the Fed’s interest expenses and losses. But it’s not straightforward.

By Wolf Richter for WOLF STREET.

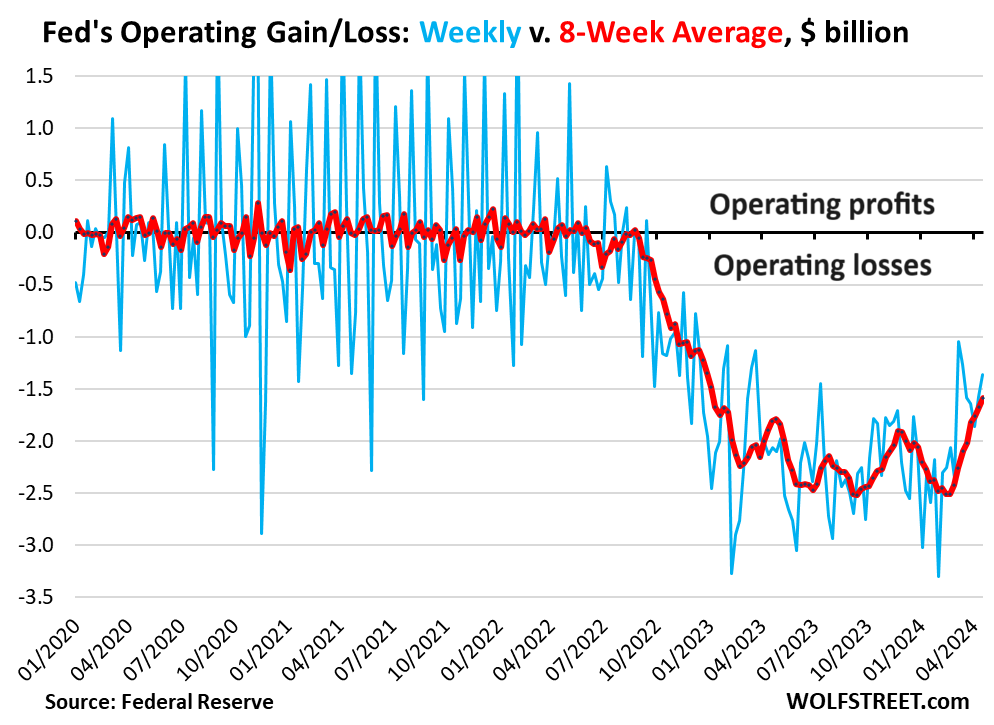

By September 2022, the Fed started losing money, lots of money, as the spread turned negative between the low-yielding securities it was earning interest on, and the much higher rates it was paying on reserve balances and ON RRPs.

Reserves are cash that the banks deposit at the Fed. ON RRPs (overnight reverse repurchase agreements) are cash that mostly money market funds deposit at the Fed. With its last rate hike in July 2023, the Fed raised the interest it pays on reserves to 5.4% and the interest it pays on ON RRPs to 5.35%, and losses ballooned. For the year 2023, the Fed lost $114 billion.

But the operating losses, reported on the Fed’s weekly balance sheet, stabilized in mid-2023 and began to diminish in 2024. The weekly losses in March and April have been the smallest in a year. And the 8-week moving average (red line) improved to $1.59 billion, the smallest loss since January 2023.

The dynamics of the Fed’s losses.

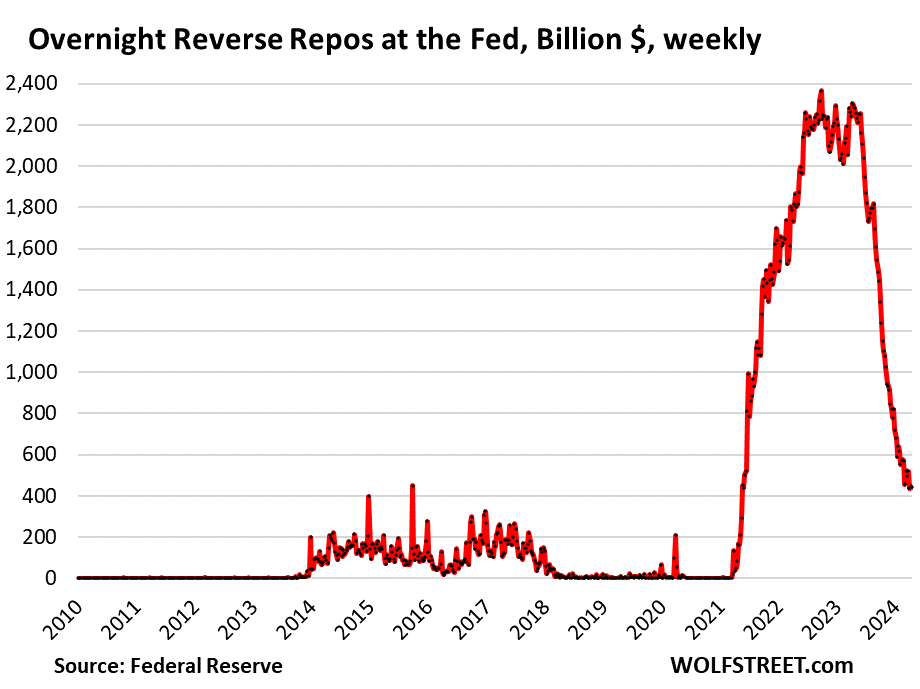

ON RRP balances have plunged by $1.9 trillion from the peak, to $441 billion, as of the Fed’s balance sheet yesterday, which reflects balances on Wednesday. Turns out, the QT liquidity drain is draining ON RRPs first, and reserves second.

ON RRPs will go to zero or near zero, which is their normal status. They signify “excess liquidity that financial market participants do not want,” Fed governor Waller explained in his speech when he laid out some basic principles of QT going forward.

The Fed pays counterparties 5.35% on ON RRPs. But money market funds can earn a higher yield by buying short-term Treasury securities that yield nearly 5.5% in the 1-3-month range, and by lending to the repo market, especially with term-repos (longer than overnight). And money market funds have been shifting cash out of ON RRPs and into these higher-yielding instruments.

In addition, some of the ON RRP balances have shifted via money market funds back into the banking system and therefore into reserves, as we’ll see in a moment

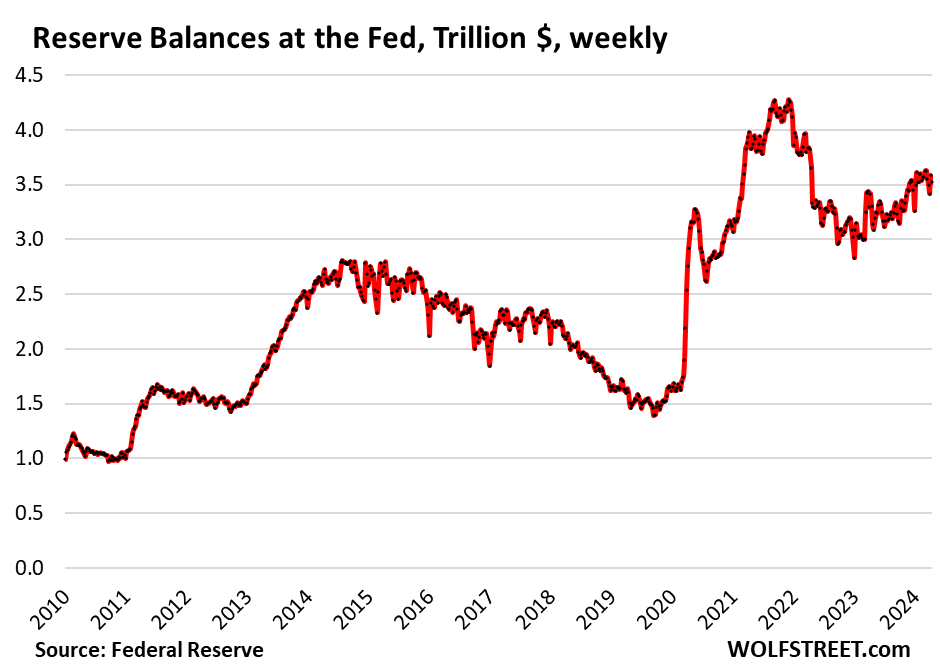

Reserve balances should start dropping again after ON RRPs go to near zero, and as QT continues to drain liquidity from the financial system.

Some of the cash that shifted out of ON RRPs has shifted into reserves in 2023, and reserve balance actually rose, even as ON RRPs plunged. On the current balance sheet, reserve balances fell to $3.52 trillion.

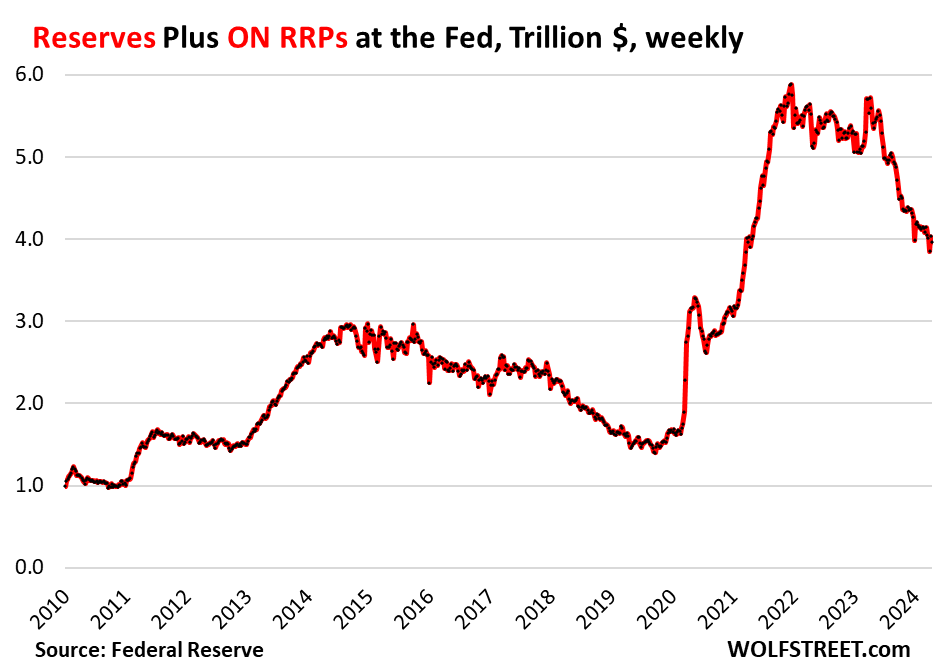

ON RRPs and Reserves combined – that’s what the Fed pays interest on – have plunged by $1.9 trillion from the peak in December 2021, and by $1.4 trillion since QT began in June 2022, to $3.96 trillion, the lowest since March 2021.

When will the Fed break even? Not for a while.

As QT continues, the combined balance of reserves and ON RRPs will continue to fall, which will lower the interest the Fed pays to banks and money market funds.

And if the Fed ever cuts its policy rates (which include the interest on reserves and ON RRPs), the interest the Fed pays to banks and money market funds will decline more quickly.

At the same time, the Fed’s interest income will also decline further as QT works down the pile of low-yielding assets that the Fed earns interest on. So this slows the path to breakeven.

But after QT ends, the Fed would replace the old low-yielding securities as they mature with higher-yielding new securities, and its interest income would begin to rise. And maybe at some point, the Fed’s interest income will once again pay for its operating expenses, and it can break even, but that’s not going to happen for a while.

Losses don’t matter to the Fed. They matter to the US Treasury.

The Fed creates its own money and cannot become insolvent and it cannot become illiquid. Its capital, which is capped by Congress, is not impacted by the losses because the Fed carries the losses as a “deferred asset” in a liability account on its balance sheet, rather than taking the losses against capital.

But the Fed’s losses do matter to the US Treasury Department. The Fed has to remit nearly 100% of its profits to the US Treasury (a 100% tax bracket, so to speak). Since 2001, the Fed has remitted $1.36 trillion in profits to the US Treasury. The gravy train stopped in September 2022 when the Fed started to lose money. And so the Fed’s losses – the absence of the remittances – have swelled the deficits and the debt, and will continue for years to come.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“But after QT ends, the Fed would replace the old […] securities as they mature with […] new securities”

I’m kind of ignorant on Fed-related matters, but shouldn’t we expect QT to end only when the Fed owns very little to no securities?

@%#^&*+*&%$#@

READ THIS (and I mean it):

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

the absence of the remittances – have swelled the deficits and the debt, and will continue for years to come.

nothing NEW here

just more FUNNY MONEY making fiat $dollar more and more WORTH LESS each day

only cost $1,000 per month more for avg family since 2020

consider another $1,000 per month more in 2026 from 2024

see costs of insurance, property taxes, maintenance and fuel and vehicles

Isn’t it important to also consider the income side of the average family when discussing increasing expenses? How far is the family falling behind in real terms?

Even if some may keep up thru wage increases, what about people on fixed income? They’re #ucked. The fed needs to be completely exterminated.

SocalJohn,

Joe said average family. If you change the facts, of course you can change the outcome. Did you read the comment I was replying to, or did you just want to express that viewpoint regardless of its relevance?

Send me all your worthless fiat dollars. I will dispose of them property for you.

joedidee, it may surprise you to learn that none of your concerns are material to either the Fed or the Treasury. Their operations are not conducted for your personal circumstances or convenience. They are responsible for one of the most powerful instruments of national sovereignty. See Alexander Hamilton for details.

eg,

What makes you think the issues that joedidee refers to (exporting inflation to the citizenry in order to perpetually finance the Treasury’s perpetual deficits) isn’t a major issue for tens of millions beyond joedidee as an individual?

Who exactly is “one of the most powerful instruments of national sovereignty” (cue up the Leni Riefenstahl flag waving) supposed to serve?

The interests of the general public (earnings on savings/low inflation) or the very, very frequently failed agendas of DC (see 50 years of deficits driven by reckless spending, ZIRP, and predictably, inflation).

Wolf, I have to admit, it took me a second attempt to gather enough courage to send my initial comment. Your articles on this site are only half of what is interesting here; the other half lies in your replies…

Well, I read the article you linked, thanks for your reply. Yes, I had already read here in this site that the *balance sheet* couldn’t go to 0 due to its several liabilities. However, I hadn’t paid much attention to the “balance” part, which says that assets = liabilities + capital (as I mentioned before, finance isn’t my forte). So, if the Fed’s capital remains relatively stable and liabilities can’t hit zero, then assets also are not zero. Fair enough.

What is not clear to me is *why* the Fed has to have securities as its assets. I suppose if the dollar were backed by gold, gold would likely make most of its assets. But in the case of a fiat currency, why can’t the assets simply be a numerical representation of cash on the balance sheet? Why must it be in the form of securities? Why are securities *actually* chosen?

Anyway, I’m trying to educate myself on this topic by reading some relevant material. I already read that securities were used as a tool to adjust the Federal Fund Rate. It seems it is no longer used for such, but perhaps it is used for other purposes. Perhaps therein lies the answer to my question.

Lastly, I’d like to say that I appreciate MM’s response, though it did fly over my head due to my limitations. However, my deepest gratitude goes to SoCalBeachDude for his/her exceptionally illuminating reply. It was only after reading his explanation that everything became as clear as crystal. Thank you immensely. Keep up the good work commenting here…

HC-

“I’m trying to educate myself on this topic by reading some relevant material.”

Some suggested (and often overlooked or marginalized) reading material to consider:

– Friedman and Schwartz – Monetary History of the United States

– Phillips, McManus and Nelson – Banking and the Business Cycle

– Tilden, Freeman – A World In Debt

– Homer and Sylla- History of Interest Rates

– Grosclose, Elgin – America’s Great Money Machine

– Rothbard, Murray – A History of Money and Banking in the United States

– Palyi, Malchior – The Twilight of Gold

– Steil, Benn- The Battle of Bretton Woods

– Hazlitt, Henry – Economics In One Lesson

– Hulsman, Guido – The Ethics of Money Production

Only a start, of course. Some are Fed-skeptic oriented, some are more historical, and some deal with the inflationary effects of CB policy.

Cheers

PS – It’ll be interesting to see if this lists draws comments from less skeptical commenters…

….also, several of the above books are available to view on Mises Institute website.

“What is not clear to me is *why* the Fed has to have securities as its assets. I suppose if the dollar were backed by gold, gold would likely make most of its assets.”

This goldbug BS needs to stop. Those comments belong on a goldbug site, not here.

The Fed needs securities on its bal sheet in order to fulfil its role as borrower of last resort. Specifically, it needs to have collateral with which to borrow against because repos are secured funding.

Being a borrower is how the Fed sets its domestic interest rate floor. Because the Fed is the safest dollar counterparty, everyone else has to offer higher rates in order to borrow.

No. Obviously not.

Wolf, The loses of the Fed are indeed losses to the Treasury, as you say, and therefore losses to the taxpayers. The Fed is spending taxpayer money without Congressional approval on losing risk positions. It looks to me like now losing “only” $1.5 billion a WEEK may reflect the Treasury’s non-interest bearing deposits in the “Treasury General Account,” which subsidize the Fed’s results but cause a cost to the taxpayer again. Have you looked at that? As of April 17, the Treasury was providing $930 billion in free funding to the Fed. Purposely helping the Fed look less bad? All the best, Alex

Alex,

You’re being silly.

1. The TGA is like a checking account. And big corporate checking accounts pay 0% in interest. That’s how it works. You’re lucky if you don’t get fee’d to death by the bank.

2. You contradict yourself. Since the Fed remits any profits to the government, if it paid the government interest on the TGA, it would reduce its profits by that amount to be remitted to the government, and the results would be obviously the same. It would be a wash.

TGA IS a 0% checking acct, as you say, and such accounts are very profitable to any bank, including the Fed, when it can invest the funds at 5 1/2%. The Fed’s own losses are smaller when the TGA is bigger. Of course, you are right that on the consolidated books of the govt (Fed plus Treasury), it’s all the same either way, whether the Fed pays interest on the TGA or not. But the Fed’s own book loss looks different. In the current case, smaller.

Agree? Best, A

“TGA IS a 0% checking acct, as you say, and such accounts are very profitable to any bank, including the Fed, when it can invest the funds at 5 1/2%.”

Huh? Where would the Fed “invest” the funds at 5 1/2%? I don’t believe central banks function like a commercial banks in this regard.

The first thing you have to wrap you brains around is that the Fed REMITS ALL its profits to the government. After “taxes,” the Fed has zero profit. The government gets it all. It’s not a bookkeeping thing, it’s a cashflow thing.

I have covered the remittances by the Fed to the Treasury every year in January, when the Fed publishes the tally.

So if the Fed pays the government interest on the checking account balance, it reduces the profit of the Fed, and thereby in equal amount the remittances by the Fed to the government. Nothing changes. Whatever profit the Fed makes goes to the government.

The Federal Reserve’s loses cannot be a wash if it the Treasury has no former Federal Reserve “profits” money to take back from. Yes the Federal Reserve has an IOU account at the Treasury, but there is no one but taxpayers or money printing (QE – quantitative easing), and other “twists”/”windows” generating inflation techniques (inflation = the most fundamental regressive taxation). If there is some Federal Reserve profits in a distant era then the time of that era’s arrival plus the number of years in that distant future may have a breakeven, but for now it’s inflation with those interest payments the Federal Reserve is paying to the banks.

This inflation concept is being made overly complex. If you don’t have money and you print some up to hand someone leaving behind an “IOU,” that is inflation; not noticeable at first as it is like pollution slowly dumped into a prestine body of water; or in the dollar’s case not yet totally polluted.

Agree w you G, except for the ”not totally polluted” part:

As one who remembers well when I sold newspapers of FIVE CENTS, and got to keep 2, compared to the DOLLAR and much more these days, that seems sufficiently polluted to be called totally.

Similar total degradation of dollar is even evident in ”official” BLS inflation calculator on web now, and it is very evident to me their numbers are significantly below reality for ”some reasons.”

The sooner ON RRP goes to zero, it is better for all players. The money parked in RRP has no place to go. If it is 0.05%, it will still be there, but this is creating havoc in the markets because this is the money that has no real use in the real economy and such an excess liquid is leading to crazy speculation in all kinds of markets. Most of it was created on a net basis, by the flood of money during the past few years. Even with QT, ON RRP are not going to disappear any time soon because of the short-term interest rates are such a bonanza for older people like me, who for the past many years was getting about 10grand a year in interest, received 250K in interest in t-bills last year! I have no use for this and after I just paid my taxes, the rest sits in tbills or indirectly in ONRRR. If this once poor, but well-educated Indian is enjoying such an experience in retirement, I am sure there are thousands of natural born Americans who are in my boat too! (No pun intended! and I know I landed in JFK!)). Barring an external shock, this economy is not slowing down rest of this year with all the stimulus in the pipeline and there will not be any interest rate cut this year and I will continue to add my tiny shares to ON RRP!

General Account balance has shot up this week, bringing down Reserves and ON RRP for obvious reasons. This will reverse soon as treasury starts bringing down its account balance. QT has been slow thanks to Wall Street threats, and this will delay the disappearance of ON RRR.

5 mil in money market!! good for you! What %age are you in domestic stocks?

With the ON RRP paying nearly the same as T-bills I really don’t see the ON RRP balances as “excess” – they are basically synthetic T-bills. To the holders of funds in money markets they mostly don’t care whether the interest comes from balances in the ON RRP or treasury bills or other short-term holdings directly (might be some nuance in T-bills being state tax exempt).

The Fed is not legally allowed to pay interest to money market funds directly, so the ON RRP is just a loop hole that is selling treasuries to participating institutions (money market funds, mainly) overnight and buying them back the next morning for slightly more money (accrued interest).

I’m thinking after QT is over the fed will buy higher yielding treasuries for the TGA account. So this is a wash and not considered debt as if I bought the treasuries?

The TGA has nothing to do with that. The TGA is the government’s checking account at the Federal Reserve Bank of New York.

Thank you Wolf, for your patient interaction with us.

The wisdom you’ve accumulated through your consistent focus on these subjects (and your ability to articulate it so clearly) supercharges our learning process.

“Since 2001, the Fed has remitted $1.36 trillion in profits to the US Treasury.”

Where does the money come from in reality? Fed is not a business. It doesn’t create value and yet it made so much money.

It’s the interest on Treasuries (and MBS). So when the Fed monetizes the federal deficit, they take a little cut for “operating expenses” and give the rest back to the Treasury.

So in reality the Treasury is NOT paying anything close to 2 or 4 or 5.5% on bonds held by the Fed.

The Fed is not part of the government. They are a private bank chartered by Congress and “owned” by their member banks. The whole thing is very well hidden from most people.

We fold our Federal Reserve Notes and think we are handling US Treasury dollars, the money “coined” as outlined in the Constitution.

Interest income.

Lender of last resort is one of the things a central bank is supposed to be.

Fed doesn’t have money per se. It can make up money from thin air and lend it to the banks, which in turn pay the interest. So what do we call the interest paid on made-up money? It is essentially part of the inflation-tax Fed has imposed on every greenback holders domestic and foreign.

“Creator of last resort” is the more accurate moniker. And it doesn’t even have to be last resort.

It is a special interest organization with the power to pick winners and losers, and it does so at will.

The Federal Reserve is a huge business – a central bank – which earns most its income from the securities it owns.

Being the lender of last resort is adding value to the economy.

The banks would have a much tougher time if they needed to figure out what to do with excess liquidity (or worse, be lacking liquidity).

That is a real value to the economy, banks, and banking customers.

It adds value to some and extracts value from others. They assist in theft for their beneiciaries, and the lesser class pays the price.

Or until QT is over will the rates rise?

Wolf,

Do you think the recent jump in long duration yields is (mostly) due to QT and ON RRPs?

Or do you think that money that would have flowed into treasury bonds is instead moving to Gold, commodities, Bitcoin, etc.?

No.

If RRPs added $1.9T to the banking system from its peak, and QT removed $1.53T from the banking system from its peak, then you could argue that money is being added faster than it is being removed… but RRPs will eventually reach their normal level of zero; only then will the banking system supply of money seriously decrease.

That’s not how it works. There are other liabilities that I don’t discuss in this article that are very important. But I discuss them here:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

Are you suggesting the $1.9T of RRPs that came off the balance sheet is staying in the Treasury General Account? It seems to me that the Treasury exchanged Tbills for that money (1.9 T) and then spent it rather quickly.

I note that the big “other liabilities” you refer to are:

Reserves (cash that banks deposit at the Fed);

Currency in circulation; Treasury General Account; and Reverse repurchase agreements with foreign official counterparties.

Read the article I linked so I don’t have to repeat the article here. You cannot understand this from reading the comments, you gotta read the articles, for crying out loud.

Not the whole $1.9 trillion, about $1.5 trillion was QT. In terms of the remainder: you can see during tax time (four times a year for quarterly estimated taxes, and biggest in April), taxpayers pulled money out of their cash accounts to pay taxes, and that money left money market funds and went to banks and then to reserves and from there to the TGA. Over the past four weeks, we’ve seen this flow in the Fed balance sheet data.

This April has been a huge month so far for tax receipts as capital gains taxes and taxes on interest earned arrived (people, including us, underpaid estimated taxes on interest earned and capital gains during the year). This April is going to be a record month for tax receipts, and they flow from bank accounts and money market funds to the TGA. Even if you sell stocks to get the cash to pay taxes, the sales proceeds flow to your bank account (deposit), to reserves, and from there to the TGA.

But QT and the RRP drawdown are two separate things. The RRP are reserves (liability) on the bal sht and QT removes bonds (asset for the Fed, liability for the USG).

I don’t see how they’re additive like you’re describing.

Meant as a reply to Ev Last

It’s not correct anyway. You need to start reading the articles. QT removes assets and liabilities in the same amounts — so that the balance sheet remains balanced, LOL. That’s why reserves and RRPs are both signs of liquidity, and combined, they go down with QT and also with the movements of currency in circulation and the TGA.

“The RRP are reserves”: that’s BS. Reserves are bank cash, ON RRPs are money market cash.

” (liability)” Yes, RRPS, reserves, TGA, and currency in circulation are liabilities.

“QT removes assets and liabilities in the same amounts — so that the balance sheet remains balances, LOL.”

Ahh yeah I misunderstood Ev Last’s comment.

“Reserves are bank cash, ON RRPs are money market cash.”

Right but major commercial banks have access to the RRP via the BNYM’s triparty repo platform – as do primary dealers and GSEs.

How do you distinguish between the two? Seems like the only difference is where the cash is parked at any given moment.

MM,

We know from the detailed data from the government’s Office of Financial Research, which releases RRP balances by MMF provider on a monthly basis, that banks and the other counterparties, such as the GSEs, participate in ON RRPs only on a minuscule basis.

March 31 was Sunday of the Easter weekend, and bond markets were closed on Friday. April 1 was Monday. So there is a timing difference between the last day of March for ON RRPs (Thursday, March 28) and March 31 for MM Funds. In addition, quarter end always includes some big window-dressing. So we can’t match up the numbers.

But end of February was close, though they still don’t totally match due to timing and reporting differences, but like I said, close:

• Total ON RRPs: Feb 29 = $502 billion; March 1 = $441 billion

• MMF’s use of ON RRPs: $465 billion, which is somewhere in between

Below are the largest MMF counterparties of ON RRPs, at the end of every month. The bank names are the money market funds provided by that bank.

Wolf-

“For the first 95 years of its existence, the Federal Reserve (Fed) did not pay any interest on money that commercial banks deposited at the Fed. These deposits at the Fed, which are considered bank reserves, were treated no differently from reserves held as vault cash, which also earned no interest. Then, on October 8, 2008, the Fed suddenly began paying interest on reserves (IOR) deposited at the Fed.”

— Scott Sumner, Should the Fed Pay Interest on Bank Reserves?, 9/12/19

Aren’t IOR paid to banks, and interest paid to money market mutual fund participants in the ON RRP program, subsidies granted to the financial services industry (as Sumner suggests further down in the article)?

And aren’t there major hazards associated with such a huge subsidy program?

Or am I hopelessly confused…?

They are not subsidies. That is a consequence of Fed raising its short-term rates to control inflation. Fed conceptually cannot say that they are increasing the federal fund rate to 5% and keep IOR and RRP rate below that and that will lead all the money moving to Federal Funds or tbills. Those rates will plunge, and fed will lose control. All this is happening because of the zero-rate policy with QE for so long.

If I understood the system, the whole ON RRP became necessary because FED WANTED TO AVOID NEGATIVE tbill rates in the USA. Couple of years ago, the banks did not want to take big deposits and money markets had to find some safe place to park about 500 billion dollars. Fed offered 0.05% as RRPs. Quickly it ballooned to more than 2 trillion dollars without REDUCING bank reserves.

If Fed had not started RRP, t bills would have gone to negative rates as there was no other safe place to park this super excess liquidity!

Bala-

If the Fed “cannot say that they are increasing the federal fund rate to 5% and keep IOR and RRP rate below that and that will lead all the money moving to Federal Funds or tbills,“ as you state, haven’t they already LOST control?

And if “the whole ON RRP became necessary because FED WANTED TO AVOID NEGATIVE tbill rates in the USA,” as you say, haven’t they already LOST control?

To me, the language of “helicopter money” and “do whatever it takes” and the euphemisms of QE and QT are exhibits A and B at the trial of our managed-economy experiment…

Respectfully

re: “Haven’t they already LOST control”

Absolutely, the money stock can never be properly managed by any attempt to control the cost of credit.

They have lost control of course! Not realizing how much super excess liquidity is in the system, they thought they could control everything by raising rates 3 or 4 percent. With the massive excess liquidity and the current generation of money managers who have not seen 7 or 8% bond rate in their career have been rushing to buy bonds at 4.5% (FOMO.) So, the long-term rates did not raise to the level where it could slow the real economy. With full employment, strange dynamics in housing market, and massive actual fiscal stimulus this election year, I don’t know why the Street Economists were calling for 3 cuts or four cuts this year.

To further clarify, FED used to have required reserve ratio. They suspended that as COVID set in. Fed has flexibility over rates on REQUIRED reserve. When there is no required reserve, in a simplified model, the whole thing is EXCESS reserve and banks will try to make whatever they can.

Bala-

Why did the Fed suspend the required reserve ratio as Covid set in?

(…and what technocratic actions or rule changes will become necessary when the next crisis occurs?)

The “required reserves” ratio of 10% meant that banks had to keep 10% of their deposits in their reserve accounts at the Fed, to have instant liquidity if customers want their money back. But after massive QE, the banks were super-flush with cash, and the average bank had something like 25% of their deposits at the Fed.

Even now, after $1.5 trillion in QT, commercial banks STILL have $17.6 trillion in deposits, and they keep $3.5 trillion at the Fed, so that’s a ratio of about 20%, so that is still double a 10% reserve requirement.

That’s why it was lifted: it wasn’t needed. The reserve requirement is an old measure that predates QE. But when QE came along, bank deposits swelled up and reserves swelled up (even when the Fed was only paying 0.2% on reserves).

The Fed could change strategy and draw down liquidity in the banking system so far that it will have to lift the reserve requirement to 10% to force banks to keep some backup liquidity around. That might mean $3 trillion in additional QT or something like that. I don’t see that happening, but that would put the Fed’s system back to pre-2008 footing.

That’s why is was lifted: it wasn’t need. The reserve requirement is an old measure that predates QE. But when QE came along, bank deposits swelled up and reserves swelled up (even when the Fed was only paying 0.2% on reserves).

Wolf has answered the question. If Fed wants to reduce the interest they pay on reserves, they can restart required reserves on which they are not obligated to pay any interest or can even pay much reduced interest rate and banks will have to keep that reserve with them. Fed will be paying close to 275 billion dollars in interest on reserves this year. In 2020 and 2012, they paid 0.05% on those reserves and all the banks kept the reserves. Even if they work out a ratio by which just a trillion becomes required reserve, they can save 50 billion in interest. Take for example, Jamie (Jamie Morgan Chase) always keeps about 500 billion with Fed as reserves. in 2020 and 2021 he got 0.05% on this. Today, he gets 25 billion a year in interest without lifting a finger. So, Jamie and his very powerful and extremely smart brethren will never allow Fed to even think about required reserve ratio, no matter how small that number is. I agree with you that Fed totally mismanaged the QE, which fundamentally brings in lot of moral hazards. It was sheer malpractice to continue with QE in the beginning months of 2022.

Correction: In my earlier response, the Fed will be paying close to 200 billion on reserves this year and NOT 275. I might have subconsciously included the interest on ON RRPs!

Thanks for the explanations, Wolf and Bala.

My concerns are the gradual expansion of the Fed’s remit, it’s absolute size (balance sheet), and progressive size of its emergency responses.

Also (in the parlance of James Grant): the Fed has an awkward and repetitive habit of stepping on rakes. It seems to solve less mischief than it creates. Bigger is not better, when it come to central banking.

Last but not least, interest rate management over the last decade has enabled government borrowing and deficit spending.

Cheers.

Just because it’s fun!—

“From the perspective of monetary policy, ….1993 seems like a world away. Back then, the Fed’s balance sheet totaled about $400 billion. Now? It’s $8 trillion. So many things we take for granted weren’t even a “thing” back then. There were no FOMC statements…no press conferences…no dot plots…no long-run forecasts in the SEP [Summary Economic Projections]…no policy rule, optimal control or flexible inflation targeting. In fact, there was no inflation target at all! There was no QE or QT, no LSAP [Large Scale Asset Purchases]…no ZLB [Zero Lower Bound], ELB [Effective Lower Bound] or shadow rates… no ample or abundant reserves… no IORB [Interest on Reserve Balances], ON RRP [Overnight Reverse Repurchase Agreement Facility] or SOFR [Secured Overnight Funding Rate]…no DSGE [Dynamic Stochastic General Equilibrium], EDO [Estimated Dynamic Optimization] or SIGMA” [a “new open economy model for policy annalysis]…no FRB/US model… and most shocking of all, no r-star.”

— John Williams, New York Fed President, as related in Grant’s Interest Rate Observer. November 24, 2023, quoting his speech at the 2023 centenary event for the Division of Research and Statistics of the Federal Reserve Board in Washington, D.C.

It is a huge subsidy program — paying interest on bank reserves that Fed had created out of thin air and lent to the banks, which put right back to the Fed as reserve. Confused yet? I am too.

The money were made up in the first place. Yet, Fed pays interests on the made up money that the bank never had. We are living in a fantasy land.

Just to qualify how desperately confused I am. I have studied economics as a PhD student for years until I gave up and went for a PhD in computer science instead. My former classmate works for federal reserve.

Wise choice to ditch econ. Econ should join alchemy in the graveyard of failed disciplines.

Econ is a priesthood of squabbling sects.

“Or am I hopelessly confused…?”

Yes.

Sumner: “This was a sort of implicit tax on bank reserves, ”

Both Sumner and Friedman are wrong about the IOR. Neither excess nor required reserves were a tax. Without the remuneration of IBDDs, excess reserves were “Manna from Heaven”, indeed showered on the system and costless to the system.

The payment of interest induced nonbank disintermediation up until 2011. The IOR rate was greater than money market funds 2 years out. The artificial suppression of rates caused investors to recalibrate. It took demand off the market and stoked asset prices.

Wolf,

Thanks for the update on ON RRP.

Can you explain how the money from ON RPP will go into Reserves?

If those funds had access to Reserves in first place, why would take 0.1% cut and put in ON RRP?

In terms of QT, I understand FED will slow down QT in order to reduce the balance sheet without blowing up.

We still have 450B in ON RRP and around 3.2-3.33T in Reserves. Powell, Waller, Logan all are saying Fairly soon QT reduction. Also based on last Meeting Minutes consensus seems to be 30B cap for Treasury securities.

Fairly soon is now very subjective interpretation. It could be Jun 2024 too.

My point: I feel little early to talk about slowdown in QT. Can sure go with same QT pace for 4-6 months. At least wait till ON RRP to become 100B or less. We still have record level reserves 3.3T and they have brought back SRF.

“Can you explain how the money from ON RPP will go into Reserves?”

Lots of ways.

If I take my cash out of a money market fund and put it into a CD (bank deposit) that is how ON RRPs shift to reserves.

If a money market fund buys the $1,000 T-bill I want to sell, the money market fund might take the $1,000 out of ON RRPs and give it to me, meaning transfer it to my brokerage account, where it’s swept into a bank account, and the bank puts it on deposit at the Fed and it becomes reserves.

Anytime anyone sells a money market mutual fund, the cash proceeds reenter the banking system, become deposits, and may end up at the Fed as reserves.

Savings flowing through the nonbanks never leaves the payments’ system.

Wolf. You being a snarky and annoyed moderator loses its appeal when that’s your reply to nearly every single response you make. You should probably try to throw a few kudos in from time to time. Just saying.

Here’s a kudos to wolf, thanks for your vision, I make good plans with good info.

C

Awwwwwwwwwwww….Look at you wanting a trophy !

Chris,

Awesome advice. Kudos for being so smart that you even know how to use the commenting box. You most definitely get a first prize for participation. You thoroughly thought out and executed your comment, well done. Now start your own website and get drunk on your own advice.

This wins the internet the weekend.

chris, think of him as a snarky grampa with interesting insights.. i’ve friends with less time for bs than him. idk.. he doesnt seem to wear people off. they still comment.

i’d not mind if he has a hall-of-fame of blocked comments. i’m more curious about the stuff he blocks.

Wolf is a great resource for people who just want to learn and correct information and do not care about about being coddled. If you are looking to be coddled, buy a puppy. You won’t learn much about Central banks, but you will be happy.

Great rundown on the whole scheme. I did follow your link and found it informative. I’m going to read it a couple more times once my headache clears up.

The quicker the system breaks the better. Not because it wont be unpleasant but because the longer it goes on the more damage occurs and the more difficult recovery will be.

For Russia is took 10 years and only killed 8 million people or so.

Sure enjoy it while it lasts and if it lasts until I’m dead, then that is effectively forever.

Huh? Did we read the same article?

Wolf is not advocating for the system to break. The opposite actually.

Comparing Central banking to Russia is absolutely silly. It is like comparing apples to moon rockets.

For sure and which Russia 1980s? 1990s?1910s? 2020s? Or pre 1900s? I love the Russian people.

Hey Wolf

If you ever get tired of answering comments and are looking for something else to do, I’d love to see the same data as this article but for the BoJ.

Not aproving my comment doesn´t change anything: QE will start when RRP is at zero, because nobody in the Fed and the Wall Street understand the mechanism.

People have been saying the same BS when ON RRPs were dropping toward $800 billion: When ON RRPs hit $700 billion, the Fed will restart QE, people said. In fact, people have been saying since QT started in mid-2022 that the Fed would be forced to restart QE over the next few months because of yada-yada-yada. Just manipulative or ignorant bullshit and lies.

And no, you do not get to abuse my site to spread manipulative or ignorant BS. Print up this rule and stick it to your fridge as a daily reminder.

Moment, the difference is, i understand the RRP mechanism. I repeat only that, what many so called analysts tell the business world since weeks: If the RRP is empty, the Fed will halt QT and go back to QE, because the banking system will run out of liquidity.

And my link to the New York Fed report “Open Markt Transactions 2023 was not spam. Take a look on page 40, chart 28! These SOMA projections are from the Fed himself, and no BS.

The numbers will just prove your “analysts” wrong. I’m tired of wasting my time on their BS. The Fed has confirmed many times that ON RRPs will go to zero, and then reserves will drop a bunch as QT continues. ON RRPs should go to zero in the second half. So we don’t have to wait that long.

Wolf said: “Its capital, which is capped by Congress,”

————————————

How is this done?

Isn’t the FED’s capital a function of contributions from members plus retained earnings?

It’s “statutory capital,” and the cap is decided by legislation. The Fed remits ALL ITS PROFITS and any “excess capital” to the US Treasury, and so there is no capital accumulation or retained earnings.

As I said in the last paragraph:

“But the Fed’s losses do matter to the US Treasury Department. The Fed has to remit nearly 100% of its profits to the US Treasury (a 100% tax bracket, so to speak). Since 2001, the Fed has remitted $1.36 trillion in profits to the US Treasury. T”

I cover this every year in January when the Fed releases its preliminary financial statement:

https://wolfstreet.com/2024/01/12/fed-reports-operating-loss-of-114-billion-for-2023-as-interest-expense-blows-out/

https://wolfstreet.com/2023/01/13/despite-losses-since-september-the-fed-still-made-a-profit-for-the-whole-year-2022-remitted-76-billion-to-us-treasury-dept/

https://wolfstreet.com/2022/01/15/the-fed-released-its-preliminary-financial-statement-for-2021/

The last chart either outlines how inept the Fed truly was at forecasting the level of QE needed coming out of the Vid experience, or that something else was in play in global financial markets, i/e the reverse repo blowouts in late 2019. So much liquidity was printed that they were able to outright remove the 10% reserve requirement because there’s so much excess. The freight train is off the tracks…how long can the excess absorb $183,000,000,000 in Treasury issuance in a WEEK?

Yield solves all demand problems. The issue will be whether or not CONgress goes full retard and FAILS to balance the budget through some combination of higher taxes (guaranteed) and reduced spending…

If not, then it will be hyperinflation. It’s not personal, it’s just MATH.