All that makes sense, but why are there still any cash-out refis when people could take cash out via HELOCs, without losing a 3% mortgage?

By Wolf Richter for WOLF STREET.

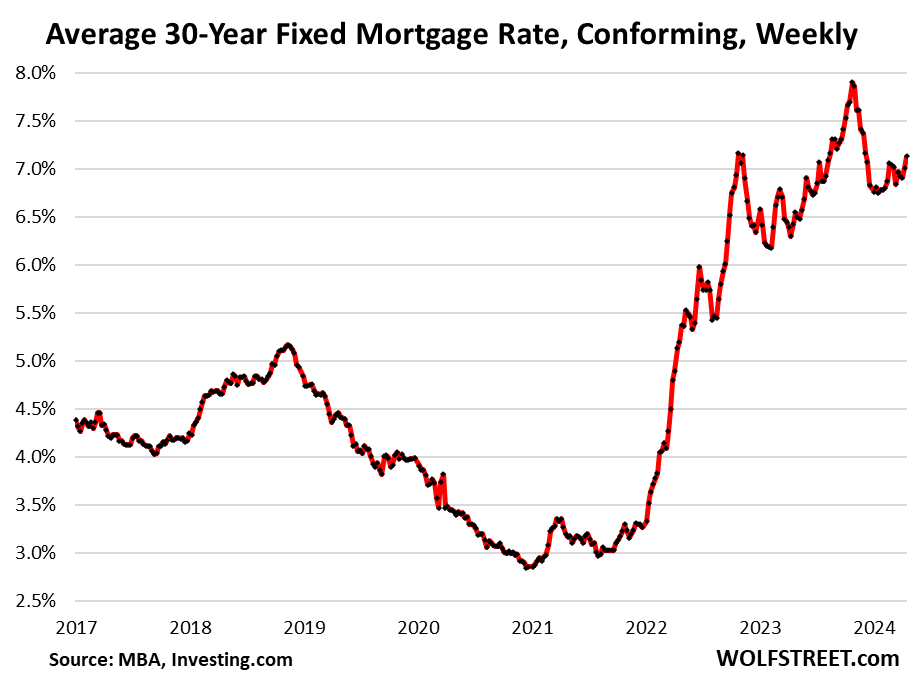

Mortgage rates continue to trudge higher from the abandoned Rate-Cut-Mania low. The average conforming 30-year fixed mortgage rate rose to 7.13% in the latest week, the highest since early December, according to the Mortgage Bankers Association today, as the 10-year Treasury yield has re-surged amid the Fed’s vigorous backpedaling on its December rate-cut visions after the presumed-vanquished inflation raised its ugly head again.

The MBA’s measure of the average 30-year fixed mortgage rate has risen 37 basis points from the Rate-Cut-Mania low of 6.76% in early January:

Still going higher. A daily measure, produced by Mortgage News Daily, which leads the fray by a few days, surpassed 7.13% a week ago and hit 7.50% yesterday, the highest rates since mid-November when Rate-Cut Mania was two weeks old. Today it’s at 7.43%. At the end of October, this measure kissed 8% for a day.

Housing market still frozen because prices are still too high.

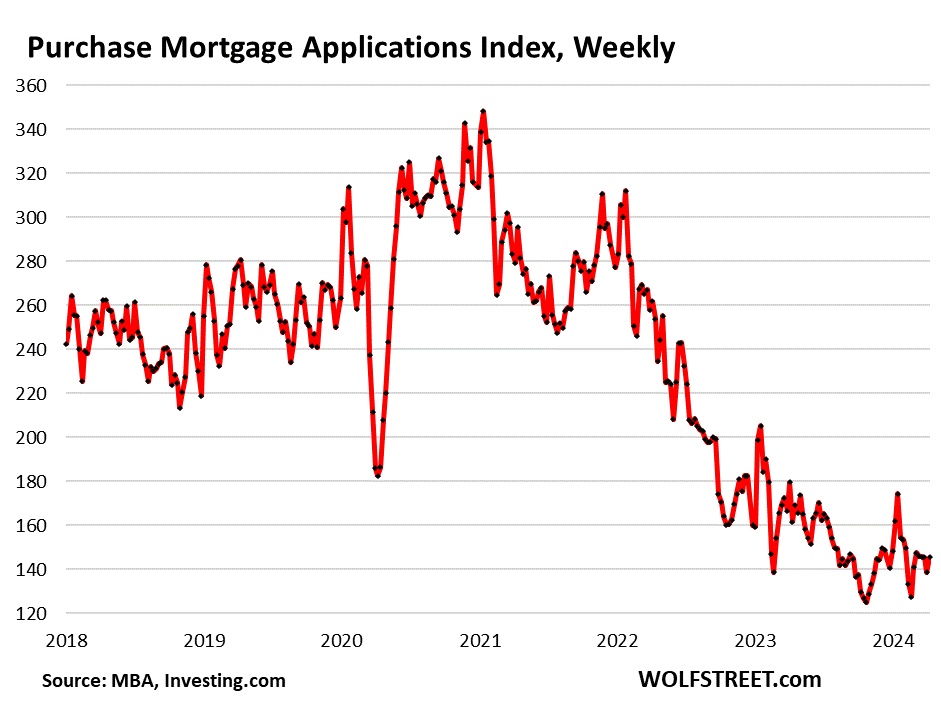

Mortgage applications to purchase a home have been wobbling near the record lows set in November and then again in February in the data going back to 1995. The cute mini-spike after the holidays during the waning days of Rate-Cut Mania only lasted a couple of weeks, though it created all kinds of hoopla, and didn’t really budge much from the record lows.

This is how far mortgage applications to purchase a home have plunged from the same week in the prior years – a sign that the housing market remains frozen because prices are still too high. While many potential sellers are still thinking that this too shall pass, many potential buyers have gone on strike:

- From 2023: -10%

- From 2022: -43%

- From 2021: -51%

- From 2019: -48%

The low level of mortgage applications to purchase a home tells us that sales of existing homes will continue to drag along the low levels that have been in effect for over a year:

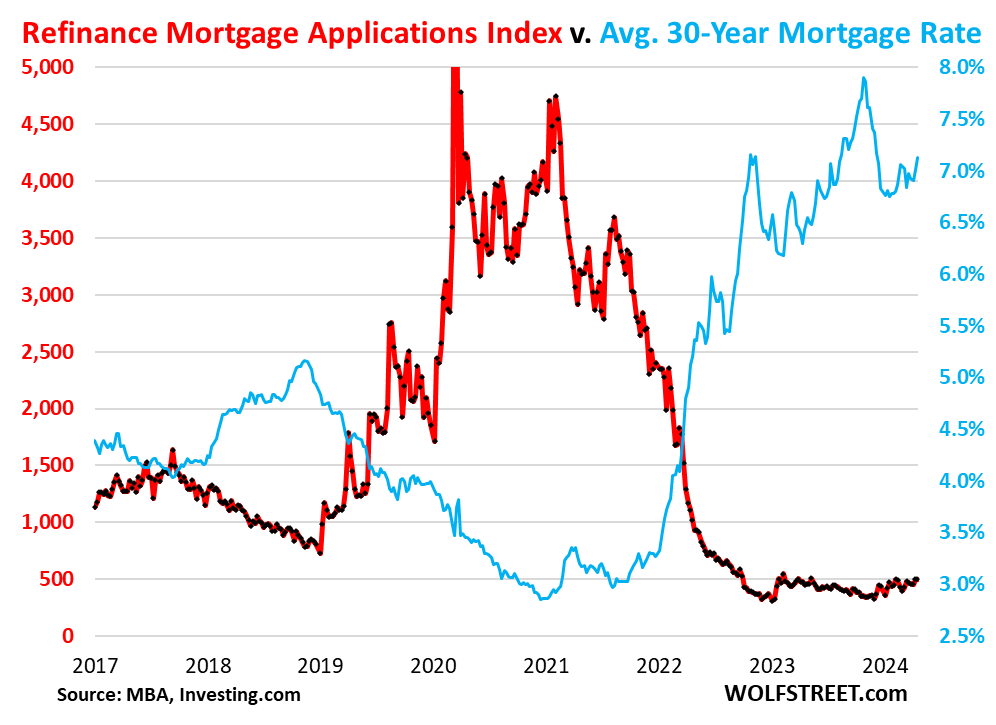

Mortgage applications to refinance a home have been wobbling along historic lows for 18 months. They had seen a huge boom during the 2.5%-3.0% mortgage-rate era, and as mortgage rates began to rise in the fall of 2021, when the Fed began to pivot from raging inflation being just a “transitory” nothingburger to the fastest rate hikes in decades and the biggest QT ever. The mortgage market saw this coming and rates shot higher from these record low levels, and refis began to plunge.

In the latest reporting week, refis were down by 66% from the same week in 2019, and by 84% from the same week in 2021.

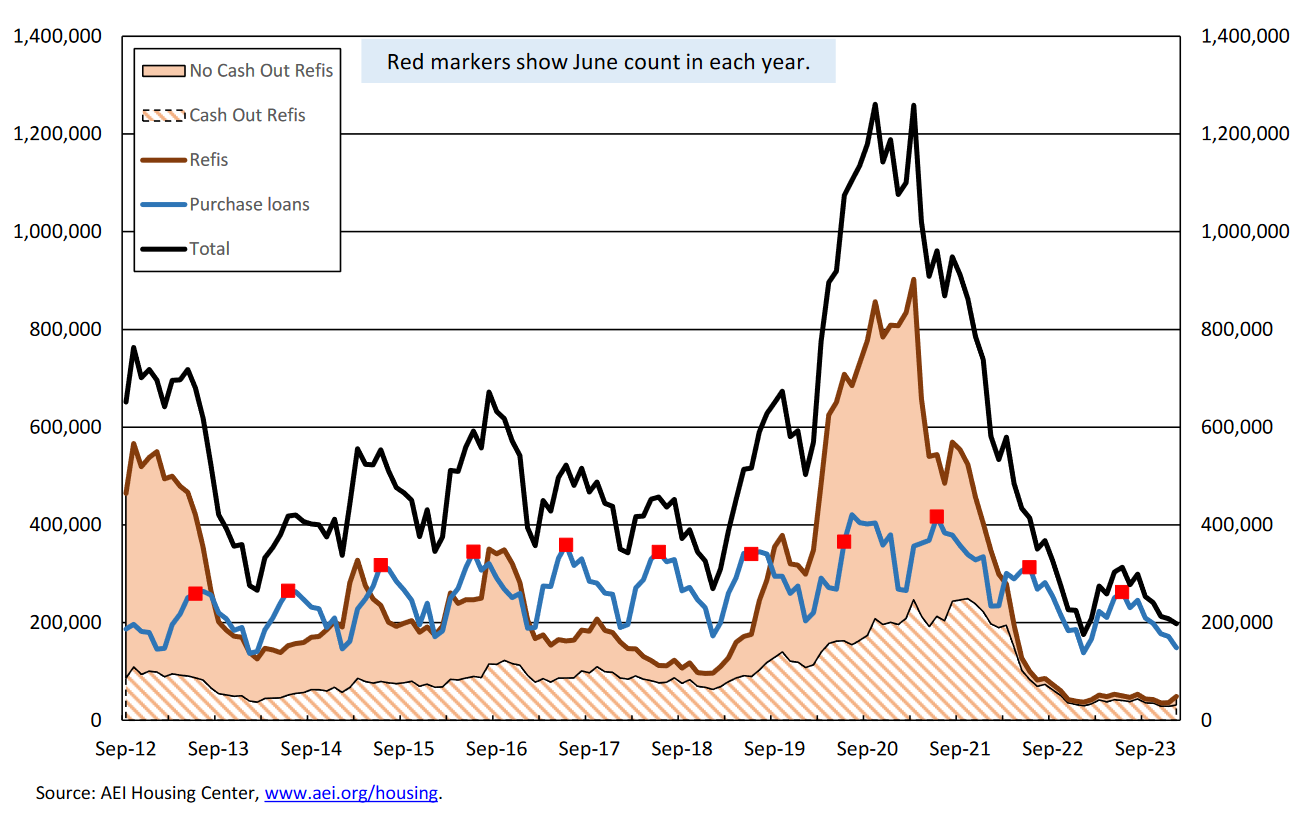

Why are there still any cash-out refis? Because people don’t know about HELOCs?

No-cash-out refis vanished almost entirely as mortgage rates have surged, as you’d expect.

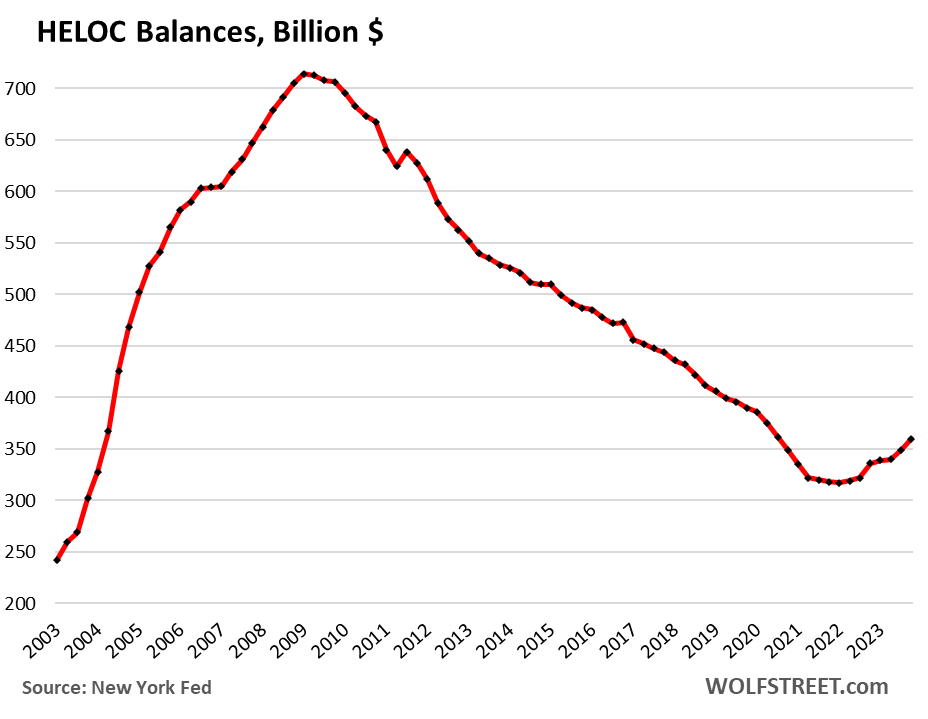

But as you’d not expect, there are still cash-out-refis, though volume has plunged. This according to data from the AEI Housing Center.

Cash-out refis (brown stripes) have accounted for nearly all refis for over a year. Non-cash-out refis, in solid brown, have essentially ended (chart and data via AEI’s Housing Center):

Which is puzzling. It just doesn’t make sense. If people have enough equity in their home to get a cash-out refi, they could instead get a HELOC for the cash-out amount. If they need $100,000 to fund a big emergency, or want $100,000 to fund a bet-the-farm startup or a crypto Hail-Mary gamble, why not get a HELOC for $100,000 at 7% and keep the old 3% $500,000 mortgage? Would save a lot of money over getting a 7% $600,000 new mortgage.

HELOC balances have been rising, so some people are following this strategy. But why were there still any cash-out refis at all? They should be down to near zero, logically speaking, with HELOCs taking their place. Perhaps because people don’t know about HELOCs? Or because people can’t do math?

HELOC balances remain low, but after declining for 13 years from the peak in 2009, they turned around in 2022 when mortgage rates began to surge and as refis began to plunge. Since that low in Q1 2022, through Q4 2023, outstanding HELOC balances increased by $43 billion, according to New York Fed data.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I made the “mistake” of paying down my principal and paid off my house. Wish I could have seen the future as now I could be making several percent staying in my loan. That said, really nice to have the house paid off. Only hassle now is tracking all my property tax and other related expenses since no escrow account.

“…tracking all my property tax and other related expenses…”

Yeah… has to be real tough keeping track of two six month real estate tax payments and one yearly insurance payment

Well put, Top-Gun.

problem is high cost of insurance and property taxes

have 1 more to pay – avg increase 38%

next year expect more

Some states collect property taxes quarterly.

And they never said it was “real tough” just that it was their only hassle. And it can be a hassle to remember.

You having a rough day?

and in some areas it can be once a year or monthly. Whatever it is though check with your county to see if there are any special deductions for elderly, disabled, low-income, vet etc. I will be taking in my rebate request any week (or month) now.

It actually can be a real PITA. I had my first house paid off at some point, and when I started paying those two bills, I had to go find my decades-old checkbook. My wife paid all the other stuff, so I hadn’t worried about ash&trash bills for years.

This house, I paid off a lot of my mortgage balance with the purposeful plan of keeping some leverage in stocks. Never occurred to me we’d get away from ZIRP, as that has been around all my adult life. It was a calculated move, but I really wish I had kept the balance as large as possible, obviously.

You can’t get every decision completely perfect. Just get them mostly right and try not to think about too many what-ifs.

Anyone who thinks the profit from selling a house will get them anywhere are in for a rude awakening.

Property is a bad investment unless you are an immigrant willing to do the tedious perfedity that is required.

A rude awakening is what profit seeking house seller deserves, a few hundred grand in profit will certainly traumatize the bank account.

But…. wang….dang, now where will we go?

Song….me and you and a dog named boo.

Profit? “Buyers’ strike” = unrecognized FMV decline. Wonder how lenders/hedge fund investors will bear the ultimate losses.

Let’s say I bought a house for 100k in 1950 and say I sell it today for 500k. Did I really make any profit? Perhaps I just kept up with the inflation caused by excessive government spending. An ice cream cone cost 5 cents in 1950, I saw one for around 3 dollars the other day.

In short, there is no real profit in selling you large home today. Seniors do not move unless they have to move.

And a down sized home costs as much as the big one you have after fees, state and federal gains taxed and moving expenses on the old home sale.

So if you want more big homes for sale, Mr state and US government official, reduce my gain taxes and sales fees.

But I do not think this is ever going to happen, and I do think inflation is going to get much worse.

Wolf’s article, subtly suggested that when he said

” They should be down to near zero, logically speaking, with HELOCs taking their place. Perhaps because people don’t know about HELOCs? Or because people can ”

The mortgage market has no option other than be ruthless.\

“near zero” but not, which implies there are some really unscrupulous RE people.

OMG, don’t tell me that might be true!!! /s

Thanks for this comment thread that’s on topic. I’m also left wondering and looking for a reason as well. As both of you point out (and Im not quoting direct )

1. Perhaps the mortgage industry steer customers away from HELOC to make bigger commissions or eventually take the house.

2. Perhaps there really is no limit to st????ty.

Could we dig deeper in case the above two generalizations don’t fit?

With the so called tight lending standards, either move would call for the application to on good financial grounds right?

Or perhaps, there are still quite some 1995 loan that can be cash out refinanced but missed the boat?

I’m an evil mortgage broker. Thanks for the label, Obama. I personally caused the housing crisis and values to zoom during the decade of Zirp. I’m sorry and you’re welcome. I’ve brokered two cash-out refinances this year. When rates were low, God-fearing bankers and benevolent credit union employees saved homeowners from satan-worshipping commission-hungry mortgage brokers and promoted “first position” HELOCs. Dubious idea at best, disastrous as rates soared. A client recently refinanced his 9.0% variable rate first-position HELOC with a $400k balance to a 30-year fixed rate mortgage at 5.75% with a $400k balance. He owns a calculator. Fannie and Freddie report this as a cash-out refinance because loan proceeds paid off his HELOC balance. The other scenario reported as a cash-out refinance is when a buyer pays cash for a home and immediately refinances 80% of the purchase price. This “delayed financing” is reported as a cash-out refinance, even though it’s the final step of a purchase transaction. Back to my lair.

I also paid my house in Southern California and am mortgage free.

I am losing money on rate arbitration but sound sleep I get at night because of absolutely no debt is precious .

I don’t regret.

Similarly here in the ”saintly” part of the TPA bay Jon.

Almost certainly losing $$ on some metrics, but also certainly doing well with no mortgage.

IMHO, and in spite of the propaganda otherwise,,, THE best thing is to get to the point of NO mortgage or rent.

One of the, perhaps ONLY recommendations after many decades of analysis of ”future trends” of costs for SO many items, from ”site and civil” to ”red metal” structural steel,, to final finishes.

It’s great to not owe money on your house. We paid off our first house in 10 years. We paid off our next house in 5 years. I’ve convinced about 6 of my co-workers to pay of their mortgages over the years and they have all been glad they did.

Even though there are all sorts of financial gymnastics you can do when you have a mortgage, you never know what might happen and having a paid off house really takes the pressure off.

Maybe it’s like in Canada. People are maxed out on their HELOCs already (pre-pandemic buyers) OR don’t have sufficient equity to draw on (pandemic buyers)?

If they bought in 2022-2023 then almost certainly there’s little equity to pull from unless they put a good chunk down.

If they have enough equity to do a cash-out refi, they have enough equity to do a HELOC.

If they’re maxed out on their HELOCs, than cannot do a cash-out refi either because the refi will have to be large enough to pay off the mortgage plus the HELOC. And then there’s no cash left to out.

Your confusion on why cash outs instead of helocs is even more pronounced when you consider the closing costs on a 1st mortgage are MUCH higher than doing a heloc.

Doesn’t California (huge share of mkt) have different foreclosure rules for different forms of home lending?

Not sure how it might work in this case, but if it is harder/impossible to foreclose certain kinds of refinancings, the banks not make them available in CA.

cas127,

This is the furthest thing from legal advice ever. I think you’re talking about California’s non-recourse mortgages. Purchase mortgages are non-recourse (the mortgage that you bought the home with). Refi mortgages are now also non-recourse, EXCEPT cash-out refi mortgages. With a cash-out refi, only the amount that refinanced the existing mortgage is non-recourse. The cash-taken-out is full recourse, and they can go after your assets to collect it. HELOCs can be recourse and can be non-recourse. So in terms of the cash-out part, it makes no difference whether refi or HELOC.

Could it be that the banks won’t give out HELOCS because they want the higher margin products to stem their losses

Paul,

1. Did you see the huge profits of banks? No “losses to stem”

2. I’ve seen ads for HELOCs, so someone is eager to write HELOCs, LOL.

3. HELOC balances are up, as you can see in the last chart.

4. But that’s a false choice. Because Lender A has your mortgage and Lender B offers you a HELOC, and Lender B makes money off the HELOC. But if you refi with Lender A, instead of getting a HELOC from lender B, then Lender B makes no money at all.

These have to be 5 or 7 year ARMs that are coming due.

Thank you. At least that could *potentially* make sense. Like Wolf, I was also puzzled about the cash out refis.

What’s the difference between a HELOC and a second trust? Aren’t they essentially the same thing?

HELOCs are revolving lines of credit, so they can be drawn up and paid down over some period of time. A 2nd mortgage is typically all funded at closing, then amortizes over a defined period of time.

In a default situation is one type any better than the other?

For the lender, the refinance is better because the loan is in the first position. HELOCs are considered second mortgages.

Yes. But for the borrower, they’re the same, both are secured by the property. So a default on either one could lead to a foreclosure and the loss of the house.

There are generally two reasons a cash out refi would win out over a HELOC.

1. In Texas, where I originate, you can only have a single equity loan tied to a property. Many people have previously refinanced with cash out and are left with a refinance as their only option to draw cash. This is based on state law and less likely to be the primary as Texas is the only state I know of that requires this.

2. The second and most likely is debt to income ratio. Most HELOC’s are treated as a 1.5% payment on the outstanding balance. An actual mortgage would be a cheaper payment for the same amount borrowed in most cases making it easier to qualify.

I just closed a loan Monday where the client was declined for a HELOC but a cash out refi worked when everything was wrapped into it. It will change the individuals life since most of what we paid off were 20+% rates.

isn’t it easier to qualify for a cash-out refi then a Heloc? Because the bank stays as 1st lien holder, assuring the asset.

elbowwilham,

Why would you get the HELOC from the same lender as the original mortgage? Nothing to do with it. You shop around for the best HELOC rates and terms. And that’s where you go. Your mortgage holder continues to have the 1st lien.

But you gotta do the MATH, borrowing $100,000 at 8% and $500K at 3% is a HECK OF A LOT CHEAPER than borrowing the entire $600K at 7%. And you can pay the 8% HELOC off after your project is finished, and it’s back to only the 3% mortgage.

Maybe in some states the first mortgage would get a non-recourse or at least some kind of beneficial treatment, whereas HELOC would not?

Alternatively, people might be doing the full refi rather than the HELOC b/c they plan to repay very soon and want to minimize # of liens for other purposes? (e.g. borrowing against Home A in order to make down payment for New Home B, before selling Home A).

Another difference between a HELOC and 2nd Trust is the former has to be put back into the home as a home improvement to get a tax deduction. The latter does not.

Doesn’t a second trust require an appraisal? And a closing. Where as a HELOC doesn’t? If so, that’s another difference.

I’ve heard of divorce decrees “splitting” the home equity by doing something like a cash out refinance to take someone’s name off a mortgage. Then again people might just not be able to do math.

I know of two cases for my in-laws where this was done due a D.

This actually makes a lot of sense. Given the relatively low volume we’re talking about, divorce (and similar situations that require dividing proceeds while changing who is on the first mortgage) seems the most plausible explanation.

ShangtrOn-

This talk of divorce has got me thinking of tom jones,”what’s new pussycat” singer.

With all those women and underwear lying around he married only once at the age of 16.

So…. over 10% of home mortgages in US are over 6%. Many of these people could have gotten a lower rate if they knew or cared.

Many have mucho dinero in bank drawing zilch interest… don’t care.

Guess if its not broke why fix it thinking.

In addition to the Divorce situation, there could be death-of-owner scenarios where the inheritors of the property want to access the equity and stretch out the payments as long as possible (minimize repayments) prior to selling the house.

A third variant would be Struggling Grandmas, who have high equity levels, wanting access to the cash before selling en route to retirement homes.

In situations like that, the HELOC math might be a negligible difference but the HELOC adds needless complexity & hassle?

Finally, utterly dumb question but if someone owns a house outright (no mortgage), then takes out a mortgage on the property, is that considered a cash-out refi? (It’s definitely not a purchase mortgage, right… I’m wondering if the statistical aggregators have enough bins to accurately capture all the situations. Sort of like the Federal Reserves concept of “household” wealth vs. institutional, where the “household” category includes all kinds of other situations but they only have a handful of bins so it all gets stuck there…

@Wisdom Seeker 2.0 asks:

“if someone owns a house outright (no mortgage), then takes out a mortgage on the property, is that considered a cash-out refi?”

As a former commercial lender I can tell you that we never called any loan that did not “refinance” (aka payoff) a current loan a “refi” but I did a few of them (all after a conservative no-debt parent died and one kid that wanted to keep the property needed cash to buy out his siblings. This was rare in my 40 years in real estate since the children of most real estate multi-millionaires are slackers that sell as soon as they can and spend like “drunken sailors” (I hope to avoid this with my kids, but as they get older I can tell that there is not way to teach my kids the lessons I learned growing up poor and working six-often seven days a week pretty much every week from 14 to 44 (when I finally got married and promised my wife I would take most weekends off)…

Wisdom Seeker 2.0,

As a current mortgage lender, the answer is yes, that is considered a cash out refinance.

I’m a traditionalist conservative, but even I think you’re trolling.

What the hell? I’m a woman who has generated plenty of wealth. But whatever. You proved that you’re not living a full life. Sucks to be you.

X

Spoken like a bitterly divorced man.

Welcome to Japan. Absolutely is nothing shared between spouses, can’t even open a joint bank account. And technically, you cannot even give money to your spouse without incurring a gift tax if you go over a certain (low) yearly amount.

Interest rates are generally lower on cash-out refinance than a HELOC, so maybe some crafty mortgage salesmen convince them it’s better?

which earns the salesman a higher commission maybe?

Likely yes, since the amount financed by the loan factors into how much a loan originator is paid.

Forgot to mention that the term for a refi is longer. So the mortgage salesman can make the monthly payment sound more appealing when spreading it out over 30 years.

That is exactly what I concluded too. People are not good at math and they only think about the monthly payments not the long term interest charges. So spreading the refinance over 30 years versus higher monthly payments for 5 year HELOC repayment suits their here and now cash flow.

You say this as if you expect them to be able to afford whatever payment is thrown at them.

A higher payment for a shorter period of time will save them on interest, sure, but allowing them to have a payment they cannot afford is just silly.

There are regulations on how much payment can be allowed based on the income earned and documented. I have had plenty of clients who wanted a 15 year but could only afford a 30.

Wolf,

Do you think that realtors who function as buyer’s agents will need to figure out how to offer mortgage brokerage services as an add-on in order to survive?

It would seem that there would be zero appetite to pay the average buy side broker’s commission in this market unless there was a value added service included.

I have heard that some brokers are offering mortgage brokerage services as an add on (maybe because otherwise they will be out of business).

Do you have any thoughts on this?

I know a Realtor who’s trying to change her career. It’s pretty bad out there. But mortgage brokers are also trying to change their career. It’s pretty bad out there for them too.

It seems unless you have one agent that both represents the buyer AND lines up the financing, there will be both (i) concerns about the buyer’s ability to close, and (ii) lack of perceived value by buyers at paying the agent fee.

This would likely cause a shift in how real estate sales are done, and reduce the profitability of bank real estate lending operations.

If it goes this direction, every buyer’s agent would end up working directly with a mortgage broker and splitting commissions, and most of the companies issuing the paper would probably not be regular banks (at least in the higher priced, nonconforming limits markets).

Have you asked your Realtor friend what she thinks?

I think this will turn into a “do tons of training and additional work to keep your current job” without a raise or promotion scenario.

Dual agency where the Realtor (this is the trademark name/title for NAR members) or real estate agent or real estate broker

can represent both the buyer and seller. There could be conflict of interests and some states do not allow this.

In the MLS databases, you can not put in buyer’s commission in the fields. You need to call the broker and see if the seller will pay a commission. You need to talk with your buyers etc. This is like the perfect storm of frozen market, election year, anti-trust actions, etc. This will kill the weak and the strong will survive. The established, full time brokers are eating all the food in their sphere. New folks have absolutely no chance to survive, unless they are under someone’s wings. There is going to be a lot of consolidation or if not, just death.

They are calling RELO or something like that Real Estate, Loan Officer. You can have both and are similar structure where you have to part of a real estate brokerage or loan brokerage, until you can roll your own in a 3 years or so.

What I see now is do what you need to do to survive. These part-timers soccer moms are toast.

Now, this is just for residential real estate. The attorneys are smelling blood in the commercial real estate waters. Different markets because the idea is protecting poor grandma from these greedy bad people from taking money from her and her home. Commercial folks are just sharks eating other sharks.

But, same freaking real estate license. Those commissions are built in, but….this is could all change.

I think if you are starting out, you need to be a full-time RE and loan officer make it in the future. Good luck.

Howdy BVW. Most Unrepresented Buyers are going to lose thousands of dollars during the inspection period of used homes.

I have always had a gut feeling that in a real estate transaction the general perception is that the seller agent provides the most value and the buyer agent the least. Looking back I could have bought my house directly from the seller agent without any issues, but since my buyer agent was “free” I went ahead and worked with one. Oher than providing some hand-holding and showing us some properties, the buyer agent put at most 8 hours of work in to earn the commission. To be fair, I’m sure a lot of buyer agents put in a lot of hours on buyers that never buy a home, but I remember feeling that it was unfair for the seller to pay my buyer agent commission when a responsible teenager working a summer job could show us properties rather than a 2.5% commission realtor. I believe that buyer agents and potentially seller agents as well will at some point be replaced by a company providing these services with salaried employees for either a fixed cost or lower commissions.

beatleme: When I bought my house, I found the one I wanted on my own using Zillow. My agent helped negotiate an offer below list price, recommended a good home inspector, and handled the paperwork. That’s definitely worth something, but I think fixed fee would be more appropriate than 3% commission for an “easy” transaction.

Anecdotal but relevant: here in southwest Florida, you can’t swing a cat without hitting a few realtors…and I’m seeing a *lot* of postings on LinkedIn for former realtors looking for new opportunities.

Howdy Lone Wolf. YEP, created Real Estate Bubbles do exactly that.

You’ll see Realtors and mortgage brokers working at car washes in the very near future. Interest rates on mortgages are going up to 8% or higher by the end of the summer. The housing market will be frozen for the next year until we have a major recession which will bring down housing prices along with interest rates.

The money for buyer’s agents will be in getting lower prices. Think about this deal:

I tell my agent: I’ll split the savings with you 50/50 for every percent you knock off the top of the price. You reduce it by $20,000, I’ll give you $10k.

How is that working?

My loan officer (not broker) is also my realtor. It’s really convenient and he’s a lot more flexible with his commissions because he’s getting them in multiple ways.

He just sold my house for 2% commission to an unrepresented buyer. We agreed to 4% in the case of a represented buyer (1%/3% split) or 2% in the case of a unrepresented buyer (2%/0% split).

Dan,

Can you find out if this is becoming more prevalent?

Also, what geographic market are you in?

I think that hybrid mortgage/real estate brokers will be the future. And a lot of realtors will simply not be able to compete, and be forced to drop out.

Perhaps they are worried about interest rates continuing to climb. Cash-out refi is a fixed rate, HELOCs are normally floating.

Price does matter when rates are high. I purchased a house in 1985 when an FHA loan was at 11%. But that was o.k. because the house was only $45,000 and that made the mortgage payment $475. Unlike now, most of use who bought houses then did non-cashout refi’s as interest rates declined over the next 30 years.

Howdy Folks. HELOCs are great. Some Small Business owners used them for decades. You can build wealth using them. Since millions of Prisoners are locked into their existing homes for decades, unlock the cuffs and take a chance. Takes guts and a lot of hard and scary work. Opps, just answered the Lone Wolfs question. Why there aren t many HELOC customers………

I used a heloc 20 years ago in the last boom to buy some property and relocate, then sold the house in town and immediately paid off the heloc and put the remainder made on the sale in long term investments. A heloc is still just debt to me and I hated it, but it is still a good way to relocate or downsize without doing a few extra moves and/or renting. It will save you money, for sure.

If you eschew debt the current situation is only interesting and offers savers a break for a change. Many folks who loaded up on debt in the days of free money are learning a very hard lesson. Nothing is free and there is always reckoning. Always.

DFB,

I understand where you are coming from, but advocating for folks to use HELOCs to start businesses should be stressed to use with extreme caution. Perhaps, you are a business person, but almost all people are not and honestly, should use caution before destroying their last line of defense.

I consider the home to be the last line of defense when everything goes wrong, the castle. Attacking is great, but it is defense that saves you when you mess up. I sense you are retired, bored, and without a care. I am an active investor and business person with businesses with payroll. I am still in the fight. I welcome your insights and experiences, but I have to draw a hard line when you are advocating HELOCs for businesses.

hmmm..it’s safe to say with all that’s going on in the last 4 years in the housing market, nothing make sense is the norm, this is just par for course.

Market is still frozen, sadly price is still frozen too definitely in SoCal. Been hearing from friends tons of people are showing up at open house as well in South OC. Don’t know how true and it’s not like the houses listed are bargain priced hence why people are showing up, unless you count a 1200ft house in Mission Viejo for $950k a bargain…

“Which is puzzling. It just doesn’t make sense. If people have enough equity in their home to get a cash-out refi, they could instead get a HELOC for the cash-out amount. If they need $100,000 to fund a big emergency, or want $100,000 to fund a bet-the-farm startup or a crypto Hail-Mary gamble, why not get a HELOC for $100,000 at 7% and keep the old 3% $500,000 mortgage? Would save a lot of money over getting a 7% $600,000 new mortgage.”

Some are variable rates, maybe rate cut mania convinced some peeps and they could finance a car or pay down credit card debt. Just guessing here, you would know better than me Wolf.

IMO both types of loans mean you’re struggling financially. Frankly, I think it’s a difference without much of a distinction.

No, but your brain seems to have fallen off a cliff (the all-Americans-are-struggling cliff).

Taking equity out of the home can mean:

— You have better things to do with $100,000 than tie it up in a house. Maybe you want to start a company, or do massive speculative bet on cryptos or whatever. See article. A lot of entrepreneurs self-finance their new company by leveraging their home. That’s a classic method. We’ve read lots of stories about people leveraging up their home to make investments than they expect to return 100% to 1,000% in fairly short time periods.

— you want to remodel you home in a big way, which would also ad value to the home, so you’re putting the money you draw out of the home back into the home. That’s also a classic reason for a cash-out refi or HELOC

In Canada it is/was HELOCs to:

A) buy pre-construction to then assignment sell

B) buy STRs

C) give kiddos a down payment.

Essentially we spent our credit bubble inflating RE with questionable lending practices.

I hope the US chooses a different path.

Most business ventures fail, especially those financed by home loans.

Why remodel a home now, when it’s value is about to crater.

The time to take equity out was when rates were in the 3% range (all that did are “WINNERS”).

Now… only dummies do it.

Yeah I’m struggling to see how doing a HELOC to start a business is prudent investing.

Anything that claims to return 100% must be extremely risky… what if your investment gets wiped out?

Not sure what current HELOC/ReFi rates are… but I guess it could make sense to HELOC at say 8%, and then put it all into mutual funds yielding 12%. You could use part of the distribution to pay the monthly payment and reinvest the rest back into the fund, so part of it compounds. In theory, your investment balance would grow faster than the rate that the HELOC accrues interest.

Of course, this might not really be an arbitrage when taxes are factored in.

I didn’t say all Americans are struggling so stop with the personal insults. I don’t believe that, I read your articles. I am happy to be corrected, not mocked and belittled.

Wish I had worded it differently to avoid your wrath. I was just surprised that Helocs were being recommended and discussed here with such casual advocacy, that’s all.

If you’re using your house as collateral for a loan it’s a hella risky thing to do, and btw most Americans aren’t entrepreneurs, is that an acceptable generalization for you? And some Americans are not financially disciplined and get into trouble using their house this way.

I wonder if anyone is even paying the full 7% mtg rates? 1/3rd of all home purchases are all cash. Probably much of the rest are new built home sales where the builder likely buy the rate down to 5%-ish.

Existing home sales will stay low until rates fall. Someone buying an existing home with a minimal down payment has to take the full force of those high rates. No way they can afford this.

“new built home sales”

I’m not so sure… in my area new builds aren’t really a thing.

Volume has crashed, but there are definitely still some very smart people taking out 7.x% mortgages to buy existing homes.

BackRoad notes that 1/3 of all home purchases are all cash.

I’m an older, retired guy.

ALL of my acquaintances that have moved (most to be closer to their grandchildren …

some to downsize or for better weather) have done the all cash thing.

I think he has … um … nailed it.

New home sales are still only about 18% of existing home sales (but that’s up from 10%).

The proportion of cash deals increased only some; paying cash when mortgage rates are 7% is pretty attractive if you have the cash.

Its interesting – Rocket is one of the largest originators and our current servicer. It does not currently offer HELOCs. And if memory serves it hasn’t for some time (X years). Wonder why.

Even in a hostage situation I wouldn’t Refi my first (at 3.75). Sorry honey ….

There are plenty of banks that offer HELOCs, including Citi. You might have to go to a bank. I don’t think Rocket ever offered HELOCs, would be interesting to confirm. Rocket is not a bank, and it cannot fund loans and carry loans on the balance sheet like banks fund and carry loans. It has to sell its mortgages, and they usually go to the GSEs (Fannie Mae, etc.) and government agencies. And they don’t take HELOCs for securitization (though there’s some discussion about that now).

Some people have adjustable rate mortgages. So, the refi rate is probably about the same as their existing rate, once they hit the adjustment date. They having nothing to lose getting a cash out refi. They have probably built up a lot of equity and really want to get their hands on some of that cash. Yes, a HELOC would do the same thing but it would be floating rate, probably tied to the Prime rate. A fixed rate refi gives them protection against further increases in interest rates. Admittedly, that was a contrarian line of thinking over the last 12 months. But they know the pain of a 200+ basis point increase in rates. My adjustment date is next summer.

The Plunge Protection Team was busy buying the long end of the yield curve. “Stellar 20Y”.

L😆L

TLT should be $85.

If you’re short TLT you have to have a longer term outlook. Last bond bear market took >20 years for rates to peak.

“Perhaps because people don’t know about HELOCs? Or because people can’t do math?”

Hmm…math is hard…just like so many still think 20% drop from the top and then if it recover by 20% they are at a wash..yup math is real hard…

Or how many can simply do a excel spreadsheet and compare cost to rent vs cost to buy and see a giant difference in expensive market…once again math is hard…

Howdy Phoenix If a person has credit card debt, a HELOC is a better way to go. Of course, if they have credit card debt, a HELOC would probably cause them to lose their home too.

I remember seeing real estate agents and loan people posting on social media to “marry the house; date the rate!” back in late 2022-2023 when mortgage rates went up. Also people doing creative 2-1 or 3-1 buy downs to get into a house maybe they couldn’t afford. It would seem there are many house poor people who bought from 2022 on.

I’m curious what % of mortgages are adjustable rate or had initial interest rate buy downs by the seller or lender? From what I remember 3-2-1 buy downs were being pushed in 2022 and a lot of sellers buying down interest rates in 2023. Everyone expecting to refi before their rates went up significantly…. I wonder how those people are doing now? Even with a cut or two my guess is their best case is 6.5%.

House prices need to fall 75% in the most bubbly areas to return to historic affordability levels. That’s how bad the math is.

75% is pretty steep, maybe in some areas it’s accurate.

But since a 75% drop in housing would be a replay of the near system-ender of 2008, instead maybe houses will stay flat for a while while inflation is 5-8% a year.

A house that sold for $500k in 2021 and rented for $2500 then might sell for $520k in 2030 but rent for $4500.

In any case, I think that by 2035 due to budget deficits and money printing housing will be UP at least 50% from today. Gas will be $9 a gallon but real estate will keep climbing.

Rent is pretty much flat and vacancy rates are starting to trend up in a lot of areas. Also there was no housing shortage in 2019… the housing ‘shortage’ is a lot of residential being turned into Airbnb, people opting for more space, i.e. people who’d normally have two roommates each wanting their own place because wfh and COVID, as well as other demographic shifts. A small recession would normalize these things.

This is my thinking too. Housing on average bounces around within a range, while wages & rents “catch up” in price over the next decade via inflation.

Rents won’t rise while vacancy rates are rising. Rents were able to skyrocket solely because of super low vacancy rates. Which made people want to build and everyone want to become a landlord. Thus increasing supply. They may slowly catch up but it will be very slowly minus unforeseen events (like massive immigration, another pandemic, etc)

Secondly, inflation via wages causes inflation in everything…. that is bad. Really bad.

Lastly, a mild recession fixes all of this if our politicians would just let it happen (but that doesn’t get people reelected). Recession means decrease in travel, which means a lot of Airbnbs end up on the market increasing housing supply. People choose to have roommates or live with their parents. People become more cautious with their spending. Inflation goes away, we maybe get a 10-15% drop in housing prices which is fine because most people who bought 2020 or earlier have 40%+ equity in their houses – so it’s not 2008. It just means instead of making 40% when they sell maybe they make 20%. Housing prices normalize somewhere in the middle between the peak and 2019 prices, and interest rates come down to a new normal with a fed funds rate in the mid 3%’s and combined with some small salary increases housing is affordable again. But for this to happen the politicians actually need to let the economy slow down.

I wrote a paper in one of my accounting theory classes in 2006 that predicted 2008. My professor called it alarmist and gave me a C. Lol. Similar to back then, the current bubble follows new accounting pronouncements, this time around revenue recognition that allow a lot more subjectivity around how revenue is recognized on multi year contracts, have a high degree of estimation, and imo pull a lot of not actually guaranteed revenue forward. The numbers aren’t real anymore and audits don’t really do anything, it’s not a problem until it’s a problem which is generally when a recession hits and everything starts to deflate.

Will this happen hard to say. Fed seems to be heavily influenced by wall street and politics. They waited wayyyyy too long to raise rates trying to give ample warning to wall street it was coming. Now they desperately want a chance to cut. Per every economics and monetary policy theory class I took, they should let the mild recession happen. It’s a normal part of the business cycle that removes excessive speculation and bubbles before they get too big. Delaying it or trying to avoid it forever tends to create larger bubbles and promote excessive risk taking and adds to the risk of a bigger recession like 2008.

MB is right. Wage inflation is the inflation that they fear most. When did they finally raise rates? When wage inflation started to take off. The younger generation isn’t affording houses at these prices, so its wage inflation or house prices drop.

Let’s say I bought a house for 100k in 1950 and say I sell it today for 500k. Did I really make any profit? Perhaps I just kept up with the inflation caused by excessive government spending. An ice cream cone cost 5 cents in 1950, I saw one for around 3 dollars the other day.

In short, there is no real profit in selling you large home today. Seniors do not move unless they have to move.

And a down sized home costs as much as the big one you have after fees, state and federal gains taxed and moving expenses on the old home sale.

So if you want more big homes for sale, Mr state and US government official, reduce my gain taxes and sales fees.

But I do not think this is ever going to happen, and I do think inflation is going to get much worse.

If you exceed the itemized deduction amount for Federal taxes, you can deduct ALL of the cash-out refi interest paid no matter what you used the cash for . For HELOC’s, the cash out must be used to improve the home in order to be deductible. Proof is required.

If I needed cash to achieve my extravagant lifestyle (ie I needed a piggy bank), I’d cash-out refi if my loan balance was small and I had high equity in the house. I’d max out the refi and refi again if rates fell, or, if rates rise, I’d put the extra cash in a more liquid higher earning CD. If I was a gambler, I’d take all I could out at 7% and wait for Treasuries/CDs to reach 8+%.

Also, believe it or not, some homeowners completely missed the 3% refi boat. Their current interest rate could be 5%,6%, or higher. One of my relatives was that way. They were comfortable with their 5=6% mortgage payments and didn’t bother to refi. Too much work, too little time was their puzzling excuse.

Even I was at 4.8% in 2019 because I didn’t refi until the rates dropped 1-2%. The costs to refi didn’t make sense otherwise and there was a remote possibility rates would fall even further.

Consider: if you have a 30-yr. mortgage that’s amortizing, and you live in the house for more than, say, 10 years, you will have a sizeable amount of money (dead money) from the principle payments you’ve been making each month that become larger and larger portions of your monthly pymt. Aside from the appreciation of the house over time (if it does…), you will have sunk money into that asset that will earn nothing for however long you hold the property. And if you’re happy as a clam, making the final payment on the house, the 360th one, add up the total expense of all interest paid and the opportunity cost of 30 yrs. of earning nothing on the principle, and then look in the mirror.

It may be worth selling every 4 – 5 years, hopefully getting a tax free capital gain on any property appreciation, and move on down the line.

Howdy HowNow. Quite please dont tell them. Thats exactly what some folks do. Imagine no mortgage and just HELOCs. Selling and repurchasing again and again. A starter home that turns into a mansion with out a mortgage???? NO Way….. HEE HEE

The down-side is that you become nomadic, wandering from property to property…

Downside????? HEE HEE. Never saw it that way. Movin on up is fun……Selling the final building and owning NO Real Estate is wonderful for some………

You miss the point, HowNow. Your example is wrong because it excludes the biggest fact of our modern economy: inflation.

The house is not the asset. It’s the declining principle balance you owe that is eroded by the depreciating dollar.

You pay back the principal with dollars worth less and less.

If you sell and reset every so often, you lose out on the primary hedge fund Americans have against the declining dollar.

It’s the one bet you can count on: short the dollar.

P

Correct !

Plus these two NEVER price in the risk associated with HELLOCs or the expense/aggravation of moving every few years.

Howdy Folks. Some people love to work their way for a living and don t play at the Casinos . Its AOK. to be different and do things your own way. Its what entrepreneurs do. Now if all those 3% prisoners started a small business ? Its what older folks did back in the day.

“sunk money into that asset that will earn nothing”

Its earned me the ability to not pay increasing amounts of rent to keep a roof over my head.

Your analysis would be correct if the alternative involved living rent-free somehow, i.e. moving back in with parents. But paying rent is also “sunk money” just like the interest expense (and prop taxes etc.)

I agree. It is less stress trying to time the market and failing ( or succeeding) sometime.

I know a few who claimed they sold at the peak in 2006 (or foreclosed) and bought back in in 2012/2013 at the bottom. Rents weren’t going up so were able to save/make money while renting.

Maybe that’s the game. Are refi’s or HELOC’s no-recourse? ie Ride the price up, take as much money out that the banks will allow and walk away if house prices plummet?

From a few I know who tried, timing was critical. Some sold in 2005 and then bought again in 2015. They paid more for the same house in 2015 but with the latest bubble, they have made so much money.

If you have a job and family, that turns into a vagabond life.

My crystal ball fell off a shelf and broke in the 1994 Northridge quake. I miss it.

I meant:

It is less stress than trying to time the market and failing ( or succeeding) sometime.

“But why were there still any cash-out refis at all?”

“I can calculate the motions of heavenly bodies, but not the madness of people.”

— Issac Newton, 1721 (shortly after having lost huge amounts of money in the South Sea Bubble craze)

From Jason Zweig’s commentary in Graham’s “The intelligent investor”:

In the spring of 1720, Newton felt that the South Sea Company’s share price had gone mad and sold for a gain of 100%. “But just months later, swept up in the wild enthusiasm of the market, Newton jumped back in at a much higher price and lost L20,000 (approx. 3x more). For the rest of his life, he forbade anyone to speak the words ‘South Sea’ in his presence.”

I know the pain when an individual, like myself, lost the money in a similar manner as Newton, betting against the tolerance of one’s fellow human beings to resist the urge to double down.

DC, I get it. But know that when the stock market collapsed in ’29, the economic leaders felt that a “cleansing” was needed, that the excesses could somehow be washed out.

Here are a few “facts” re: that “cleansing” from Chat GPT: from ’29 – ’33, approx. 1/3 of all farms were lost by owners, and in ’33, 45% faced foreclosure. Home construction dropped by 95%. By ’33, 10 million Americans lost their homes.

Maybe you’d like a reconstitution of the Spanish Inquisition. Try calling John Cleese.

Today’s Fed doesn’t want another cleansing if it means tanking the economy to restore an earlier status quo.

The 750 Square foot Boston north shore condo above mine just sold after being on the market for less than a month. It would have sold sooner but the first offer apparently fell through. The owner did nothing to it and pocketed 90K for simply sitting on it for about 5 years.

With a zero down 7.5% 30 year mortgage the payment would be about 2K, plus another 650 HOA fees. Add in taxes and insurance, and we’re well north of 3K a month. I am renting my unit for $2150 and I thought that was crazy. I suspect even with the big mortgage interest tax deductions, the new owner is going to quickly regret that decision.

Sold for 45K in 1993

Sold for 150K in 2002

Sold for 151K in 2007

Sold for 155K in 2012

Sold for 190K in 2019

Sold for 280K in 2024

@makruger it is hard to get a $0 down loan so odds are the buyer put something down and has a payment not a lot higher than your rent in the same building after taxes.

P.S. Looking at your sales history numbers I was thinking it looked like San Francisco Peninsula home price numbers – with one less zero…

I just looked at the home I bought (in Burlingame) for $460K in 1994 and sold for $1.2mm in 2005 the current Zestimate was exactly $2.8mm….

Boston prices went nowhere between the dotcom crash and hb1 but took off like a rocket after 2012.

I wonder what percentage of home buyers are now first time homeowners. That percentage has to be going up because sellers don’t want to sell. I know for me the only people that seem to be selling are dead people.

“I see dead people! Selling their houses, that is.”

“Zombie” real estate, where every new customer is treated to a free dinner.

Their are probably many dead people who still own houses.

Have to be advantages of not reporting them as dead.

Nobody knows he’s dead or cares.

Grandpa still sitting in that chair, hasn’t moved in 10 years.

Maybe the cash out refi = one payment that is the same or less per month because a less than 30 year loan is turn into a 30 year loan. A HELOC means two payments, right?

IMO most people look at monthly payments, not what something costs. And yes, people suck at math.

Too me , the stock market is a suckers bet. The representative from my brokerage called me, out of the blue, pitching a dog. Haven’t heard from them for nearly a year.

Dang- the only reason your broker would call you is that, to you point, you have a track record of being a sucker…

When my company moved me here 25 years ago they bought the mortgage rate down to 7 pct from the market rate of 9 pct/

I recently did a cash-out refi after rates had shot up a bit when we were thinking we would rent out our previous home rather than sell it. Why did I do that rather than take a out a HELOC? Because the house was fully paid off, making the HELOC unnecessary. We were not giving up any low rate loans.

Is this situation rare? Of course. But it is not zero.

If I understood correctly what you said:

1. What is a cash-out refi in terms of the data tracking? Definition from the Mortgage Bankers Association about its refi data: “A cash-out refinance is defined as a refinance mortgage that resulted in a loan amount 5 percent or greater than the previous loan amount.”

2. So this would not a “refi” in the data since there was no payoff of a previous mortgage. You just mortgaged a home that you owned free and clear. You didn’t “refinance” anything. So it wouldn’t show up in the MBA’s data as a “refi.”

You understand correctly. I figured it would be included, since the lender did refer to it as a cash-out refinance during the process (refinance as opposed to purchase).

In any case, if the remaining balance on the old loan was very small but not zero, then it would show up in the data, and the previous rate doesn’t matter much.

There may well be a difference in the way people refer to something, and in how the data is actually tracked (automatically).

“why are there still any cash-out refis when people could take cash out via HELOCs, without losing a 3% mortgage?”

Maybe people believe that mortgage rates will go down and they will refinance at lower rates while real estate prices will go up forever to the moon and back!

They don’t qualify for a portfolio product like a heloc and need more cash to qualify with paid down debts along with a full 30 year amort instead of 10 or 20. All the r/t are divorces that aren’t paying off debts.

Refis should be read as last resort options to selling unless converting old FHA in the last 3-5 years to conforming to drop mi.

It’s a spicy world of denial rates in refis 😊

“…why are there still any cash-out refis when people could take cash out via HELOCs, without losing a 3% mortgage?”

For many, it is about monthly payment. With a refi, the loan can be re-amortized over 30 years and the monthly payment is lower than keeping the mortgage and adding a HELOC.

Consider:

Mortgage: $300k @3% monthly payment: $1,265

Loan was paid for years now the balance is $150k

Person wants $50k cash out.

=========================

Option 1: Refi

Refi $200k @7% monthly payment: $1,331

=========================

Option 2: HELOC

$50k HELOC at 8% 20yr- monthly payment is $418

Total house payment: $1,265 + $418 = $1,683

=========================

The cash out refi has a lower monthly payment.

Anecdotal observations: I don’t know if this means anything at all.

We moved from a high priced suburban area to rural area in early 2021. Sold the old place in a weekend. While looking for new houses, we lost on several bids made over the asking prices almost no price reductions back then.

Now out of curiosity, I look at the on line offerings for both my rural location and my former suburban location.

I see more rural offerings now have a significant number of “price reductions” in the 10 to 15 percent range whilst the suburban (much higher priced) offerings do not seem to have many price reductions at all. Totally unscientific but something I’ve notice this year so far.

Its like a broken record. Every time Wolf puts out a new batch of statistics that home prices are going down, and sales are at a standstill a predictable cast of characters come out of the woodwork proclaiming that is true everywhere but their neighborhood. And of course the “bad” houses are declining in sales price but the “good” houses like theirs are not.

Sometimes its Boston, or San Diego, or Long Island or some other magical place that is immune to the laws of supply and demand. Perhaps this could be believed when it was only houses in the ” beach communities” of So Cal. But it seems to be spreading to almost anywhere a commenter in denial might be living. Soon it will be the suburbs of New Jersey, or Detroit or Witchita.

People don’t want to admit they might lose money if the feds keep rates high.

I live in San Diego. Houses haven’t made it past their spring 2022 peak. I also know a number of people buying in San Diego because according to them homes values are going to boom again as soon as the feds cut rates so they need to get in now. It’s delusional thinking but FOMO is a hell of a drug.

You can rent a home for 30-40% of what the mortgage would be so I choose to rent and wait this mess out.

A story…

2 years ago my brother bought a house in Utah for 700k. I, being very wise told him before he bought to reconsider, rent, wait. Now his house is worth more and he is happy.

But what is a wise man…but a fool.

Sure.

But if you bought in May 2022 in San Diego then you would still have no equity…

Well, since you mention it I took a look for the first time in a few weeks. Manchester NH Zillow Home Price Index up 10% year over year- first time in double digits I believe. I’ve seen no cool down in the buying frenzy in that market. Can’t speak to other markets.

You’re comparing a point in time to a point in time. The lows and peaks were not year over year comparative because highs and lows were based on interest rates, not seasonality like normal. I’d look at prices compared to the 2022 peak and see where you’re at. That’s probably the only valid comparison at this point with interest rates being between 6.25 and 8 in the last 12 months.

Also overall though I wouldn’t be surprised to see housing prices up in some areas as long as the stock market is up. FOMO is a real phenomenon if you read any books about market psychology. Anecdotal but the number of people who have told me they’re buying another house because real estate only goes up and will always return 20% yoy is shocking (none of these people have a financial background for the record). That’s impossible because 1) at a certain point very few people would be able to be approved for a mortgage. Thus supply would increase over demand 2) for the few who could afford it, it would be a terrible investment because they wouldn’t rent for a reasonable return on the investment. There’s a ceiling at some point…

Another reason people keep buying, lenders desperate to stay in business are doing anything they can to make a loan. I got pre-approved recently for $150k more at 6.25% than I did at 3.125%. In both cases it was the same lender, my credit score was identical (800+), and I had 20% down. My salary only increased $12k during that time period. The first case was reasonable based on my income. The second case came out to a mortgage payment that was $1500 less than my monthly take home pay which isn’t a lot to live off of. Yes I could decrease my 401k contribution to 0% to make that loan feasible, but even doing that it still doesn’t leave a ton of extra money. My point with this is we haven’t hit that ceiling where you run out of buyers yet, because lenders are upping the amounts they’ll lend just to stay in business and non financially educated people will buy whatever they’re pre-approved for.

🤣 You just made his point. A town somewhere with a population of 115,000 — make sure you draw conclusions from this town to the US overall, LOL.

I live in a 1 million + metro and am surrounded by upper middle class (albeit non financial industry) professionals. And all I hear from anyone I talk to is they need to buy another property before it doubles again. Anecdotal yes, but from what I have gathered the general population is not super financially literate. They saw their friend or their parent or their coworker get rich, they better buy more soon too before it goes even higher is the general attitude for the last 2 yrs.

Also my main point was FOMO can prop up a market for a long time. As was seen with most historic bubbles.

I guess you’re making this in reference to my comment (which I guess is removed because I can’t find it)

Can I post links to certain websites or addresses to prove it certainly is happening in my backyard?

I will say that homes in Florida in my dad’s neighborhood are going up forsale but they are sitting and getting offers under asking, but either the seller is going ‘no lowballs I know what I got’ or their agent is telling them to remain steadfast and eventually someone will come along…so they have been sitting for longer than the average

Yes, I was responding to your comment. It really is depending on where you live. I’ve posted that (so far) Boston metro which includes Manchester/Nashua hasn’t seen any slowdown and instead prices keep going up. 2-family properties that may gross total $3200 in rent selling for $480k. The math doesn’t work- but FOMO is real for sure. It’s feeling a bit like 2005/2006 in this area right now.

Should add- many of these buyers are first time homebuyers who want to house hack for a year, then rent it out and buy something else. That’s why I say, math doesn’t work unless rents go up big time.

Big assumption that people posting this type of comment /want/ to see prices remain high.

On the contrary @MM. I want them to drop into the gutter because I’m sick of seeing it. Market here needs a reality check. I really don’t want to pick up and leave, all my family (well 98% of it) lives here and my career pays well.

But I guess people on here think I’m fibbing. I really wish I was.

I do understand frustration at RE thumpers being delusional about the coming asset price corrections that higher rates *will inevitably* cause.

But

Not everyone that posts about stubborn prices in their reigional market is that.

Wolf reminds us that housing corrections are slow moving, and it took 5 years for HB1 to correct. Maybe I’m just being impatient, but similar to what Rick expressed, I continue to be surprised at how stubbornly high prices remain in the MA/NH Boston commuter corridor.

Why cash out refinances over HELOCS?

1. Cashout Refi rate is as low as 5.875% while HELOCs are typically over 10%-11% right now. The salesman will show the blended rate and then bring up that HELOCs are floating rates and could get higher. Customer goes for the fixed lower rate

2. Divorces are typically a forced cashout refinance

3. Mortgage salesman have higher commissions on Cashout Refis over HELOCS. (50%-100% higher commissions typically)

4. (Not a reason for C/O>HELOC) but it should be noted there’s a big push in the industry to get all that delinquent credit card balances into a fixed cashout. It’s a desperate push to get things going with such low volume right now

Cheers! Hope that helps

Perhaps because people don’t know about HELOCs? Or because people can’t do math?

Likely some hard sales jobs being done by some rather unsavory lenders. There will always be a few consumers out there who truly can’t do math, and can be talked into anything. If they cross paths with the wrong loans salesman…

There is really no reason to avoid a mortgage while higher rates are translating into lower prices, which isn’t really the case. There will be time to lock in lower rates. A couple years ago my broker was offering PLOCs at a special rate of 2%. Now they’re 9%.

I get a little irritated with this “sky is falling” sort of dogma. When I purchased my first house, 35 years ago, I had a 30 year mortgage at 10.5%. Seven years later I sold the house and moved to Florida where I bought a house with a 15 year mortgage at 7.5%. My current, 5th house, was financed at 3.99% for 15 years some 7 years ago. I paid it off last year. My point is that interest rates go up and they come down. People who want a house and have the means to buy a house should just pull the trigger. A house is a home, a domicile and not just an investment. When interest rates come down, refinance the loan. Don’t wait on the sidelines and wait for the rates to come down to 3%, which may not ever happen again and if rates do come down, then you’ll be back in bidding wars over a house that’ll get priced way out of your comfort zone. Listen to your inner Kai and make the choice that is best for you. Cheers.

The affordability problem is not 7% mortgages. The problem is 40% price appreciation in a short time plus 7% mortgages. 7% mortgages at 2019 prices would be totally fine. They irresponsibly created a bubble. Encouraging people to buy things keeps the bubble inflated. People sitting on the sidelines let’s the bubble deflate. We probably won’t go back to 2019 prices but there should be some normalization as return to office, pandemic travel and fomo die down probably ending with prices in the middle of 2019 and 2022 pricing. So no the sky is not falling but normalization is needed. Or a better way of putting it, do you know a bubble that hasn’t eventually popped?

IMO that’s potentially disastrous advice, based entirely on hindsight, at a time when Long term trends seem to be reversing. In slow rising RE markets, buying might work out. On the coasts where prices have risen 100% in 5 or 10 years, it’s very risky to buy. If you want a secure financial future, you have to consider downside risk, rent v buy math, and opportunity costs.

I agree people need to live their life, but that shouldn’t mean having everything you want right now. Some patience and financial discipline can help people avoid major financial pitfalls.

Those who got caught up in the 2008 crisis wish they thought a bit more about downside risk. Those fancy houses, boats, SUVs created more stress than enjoyment.

Your last few sentences were my idealogy when COVID was in full swing. I was giddy that there was gonna be a recession and housing prices were coming down when the rates would go up. Instead they plateaued or started increasing, as the general consensus was ‘crap that housing price drop isn’t happening, better get a home before it’s unaffordable’ and people FOMO’d housing to oblivion. RE agents certainly assisted in feeding that frenzy.

My foreman told me ‘it ain’t gonna happen like you think it is, if I were you I’d buy now, deal with the pain of the mortgage for a year or two’ until my title kicks in and I get higher pay. I didn’t listen and we’re paying the price now.

As the saying goes, the best time to buy was 10 years ago, the second best time is now. At my age I’m committed to getting a home and that’s going to be my place for the foreseeable future or until conditions get so dire here we’re forced to leave.

Your foreman was only “right” because the Fed continued to print money for years after it shouldn’t have and kept rates at 0 for too long.

Absent that, you would have been right.

Aptly said.. the affordability problem is not high rates but high high prices.

I got lucky and sold my properties at peak in coastal CA.

These prices at these rates are really absurd.

Some thing has to give in .. not sure what..

Rates are going up and up.

“As the saying goes, the best time to buy was 10 years ago, the second best time is now.”

You will be writhing in pain from the financial beating you will be taking as you lie awake, restless, in your pressboard box prison while watching neighboring properties selling for 40 cents on the dollar. Even Jerome Powell told the young people to wait to buy a house. He knows what’s coming. Alas, enjoy your FOMO!

@DC, Powell has been on the blunt end of criticism here for the lousy job he has done, yet I should listen to him about when the best time to buy is? What makes him qualified to speak gospel on that matter when everyone on here more or less agrees his job handling the inflation should have him tried and hung?

Bobber,

The Fed’s true purpose is to defend the Treasury market and the dollar more generally.

As long as there is demand for USTs, the Fed can and will let unemployment run above target – in the same way they’re now letting inflation run above target.

They will also throw the stock market under the bus and let asset prices crash if doing so becomes necessary to protect credit markets.

You are a good example of how people suffered because of feds policies.

I honestly think this is the worst time to buy but boy I have been so wrong…

Thanks

2 things here.

When it comes to HELOC vs cash out refi, how much is left on the mortgage? If it’s a small amount (I haven’t done the math to figure out how small) it may actually be cheaper given the interest rates on a HELOC are 7.5 to 10.3% in my area, while a mortgage can be had for 6.5% still.

Also, this right here is the tale of 2 economies. The ones who bought their homes at 3 to 4 percent interest vs 7 to 8, or not at all. If you’re at 3 to 4, you have cash to spend. 7 to 8 or renting, you most likely don’t have much if any cash to spend. This is going to take years to correct.

I wonder what the actual need for housing is ? Does the country have enough housing stock or are there more bodies who would like housing if it was affordable, but go without ?

Has there been under or over investment in housing ? If sales are down, wont that mean a decline in investment in housing ? If there is actual demand for housing that cannot be met due to unreasonable price which inturn causes underinvestment in housing, then how will that impact the future.

Does turning housing in to a speculative asset mess up the whole ability of the market to regulate supply/demand ? That is spur new production or liquidation ?

There are a lot of market forces beyond supply and demand that are keeping home prices up. From venture capitalists, to banks that don’t want another 2008 repeat, etc. This is why I get frustrated by people that tell me capitalism should be 100% free market without regulation. It’s supposed to be about supply and demand and it is so far from that anymore.

That makes sense.

I dont support Capitalism. I do support free enterprise.

The end point of the financial/corporate/government/capitalism we have tends to be the end of free enterprise

While, over here in Chicago’s north shore, the market has never been hotter and the prices have never been higher. I’ve been outbid on 3 properties since the start of the year. Wish I would have bought in 22 or 23 A line of people waiting to get in an open house last weekend. I saw a couple writing an offer on the hood of a car.

YOU are the problem. YOU are still bidding. YOU’re driving prices higher. You cannot complain about prices being too high while you drive them even higher.

Why do YOU complain when others do the same and bid against you???? You’re NOT entitled to a no-bid home purchase at the price you want.

Either buy and overpay, or stop bidding. But as long as you bid, you have no right to complain about high prices, because YOU are driving them higher. Multiply yourself by 10,000, and you see the impact.

There is plenty of supply. Sales are below where they were, prices in Chicago seem to have maxed out last year… but they’re way too high. You people need to stop bidding, and prices will come down.

YOU bidders did this:

People complain about the problem but never realize that they are part of the problem.

FOMO is a powerful emotion making people blind and illogical.

Additional comment. This seems like stagflation. Lower number of sales with rising prices. I don’t think that is the same as a buyers strike.

Across the country, prices peaked in June 2022, and are lower now, and the March increase, which is normally huge, was puny. Inventory up, supply up, price cuts highest since 2017, sales in the dumpster:

https://wolfstreet.com/2024/04/18/home-sales-clobbered-by-mortgage-rates-most-price-reductions-for-any-march-in-years-new-listings-active-listings-surge/

Wolf,

Do you think this will result in consolidation of lending/realtor activities at some point?

It seems like technology would support that now.

To me, this feels like the shift from the old days in plumbing– certain plumbers would only do drain lines, others only water lines, yet others only gas lines.

Now all plumbers do each. Why? The technology is simpler and one person can be trained to do each one. Market dynamics force each plumber, to be economically viable, to be skilled in all three.

Do you feel that is an apt analogy– namely that the technology will enable real estate sales and real estate financing to finally merge?

Wolf, something that I’ve been curious about, who has taken the biggest hit on the cheap mortgages that were issued in 2021-2022?

I understand that most banks package/sell mortgages as MBS shortly after they lend the money to borrowers. So presumably it is the buyers of those MBSs that have seen a tremendous loss in value in their MBSs… Is that right? Or have they been passed around so much that the losses are spread throughout the MBS system?

We are talking about astronomical sums if you consider just how many people in the U.S. refinanced and got those cheap 3% mortgages… Homeowners have made out like bandits, but either the original lenders or whoever bought those MBSs have taken a huge hit.

Nah.

1. As long as homeowners make payments, there is no “hit” to these mortgages. They’re fine.

2. If a homeowner pays off the mortgage (sale or refi), there is no “hit” either, because the remaining principal balance gets paid off.

3. MBS (bonds backed by pools of mortgages) trade in the market, and rising interest rates causes bond prices to fall, universally. So holders of MBS will see the market value decline or rise in the opposite direction of market yields. So MBS holders take a hit if they sell the MBS now, instead of holding them until they’re gone (see #4).

4. MBS holders get the passthrough principal payments from the underlying mortgages (from payoffs and from monthly payments), so they’re getting paid every month some principal at face value, and so their exposure to the old MBS shrinks each month without a loss. And after some years, the MBS get called at the remaining face value, and the holder is out of them at zero loss.

5. MBS only get in serious trouble when there is a tsunami of mortgage defaults coupled with a plunge in resale values of the homes. This is what happened during the mortgage crisis. But now, the government guarantees most residential MBS, so the taxpayer takes the credit losses, not banks or investors.

“MBS holders take a hit if they sell the MBS now”

Sure but what about the opportunity cost? That capital could have been earning 5.3% in risk-free treasuries, but instead its earning ~200bps less in yield, in an asset with slightly more credit & much more duration risk.

MBS investors aren’t realizing a loss, but they’re underperforming the risk-free rate of return.

That’s not the trade. Just a very simplified example with some stylized numbers. As MBS are impossible for me to calculate due to their unpredictable passthrough principal payments, I will ignore the issue of the principal payments. But it’s the same fundamental math:

If you have a $1,000 MBS that you bought when issued with a yield of 3.5%. And now the yield for this type of MBS yield is 7%, you might be able to sell it for $750 now so that the buyer can earn 7% yield.

So you book an immediate capital loss of $250.

And then you can invest that $750 in 5.5% T-bills or whatever. But you don’t get to re-invest the $1,000 face value because that’s not the cash you have. You have $750.

And when you invest the $750 in an instrument with a similar risk profile as your old MBS, you’re going to get roughly the same dollars (dollar interest income and dollar capital gains/losses) to maturity as you would if you had kept your $1,000 MBS. That’s how yield works. You cannot get around yield.

That’s why, after interest rates rise, you have no incentive to dump the old bond and buy an equivalent new bond. You’ll just be out the fees of the transaction, and the income (interest plus capital gains and losses) will be the same.

People complain about the problem but never realize that they are part of the problem.

FOMO is a powerful emotion making people blind and illogical.

Reading all this is quite confusing. Here is my situation today,

Got a 25 K HELOC back in Feb this year to help defray costs associated with selling our current home of over 25 years. Did a cash out refi several years ago with a 3% 30yr fixed rate. Retired drawing SSI and wife unemployed.

Bought the home for 110K in 2000 now valued at $390K and we owe 125K

Selling for 1M next month due to location next to large commercial development project that will incorporate our property.

Not sure on how much we will pay in cap gains as state says they are tied to our tax rate, which is ZERO.

We want to buy a bigger home. Was looking back in 2018 at 6K sq ft custom homes that averaged 550-800K at that time. Easily obtainable with 1M at that time as a cash buyer.

Now those same custom homes are starting at 1.2 and up to 2M so we are now looking in the 3500-4000sq ft range. Prices are around 650-900K

Our net on sale of our home is approx 780K

As I said we are mid 60’s so not a ton of time left. We have a son that’s 100% disabled that needs to live with us hence another reason for a much larger home. Ours is 1400 sq ft now.

Right now we plan on putting down all but 125K which we will finance. The payment is the same as our current house payment.

It’s possible depending on the home we buy to put anywhere from 70K up to 200K in the bank.

We have spend our savings on helping our sons pay their bills since 2010 so our bank account is very low. That’s why we took out a small HELOC to get us through the sale of our home etc etc etc.

We also are under contract to sell another piece of property to a developer for 2.3M that’s in its 12 month of DD. Close is scheduled for May 2025 with a 2 month extension if needed but they have to pay us 25K if they exercise this extension.

Question, should we continue this course, or should we pay off the asking price of our larger home if less than 780K and live on what’s in the bank plus my SSI until hopefully our other property sells next May?

Our monthly income is only $1500 per month. In NC my real estate taxes on primary residence are 50% since I’m over 65. We never pay the bank escrow for taxes and insurance. Why let them make more money!

We aren’t broke but putting all our money in the new house would make it harder to live a more leisurely life.

Comments?