“It seems unlikely that yields are going to go back to being as low as they were before the pandemic”: Yellen.

By Wolf Richter for WOLF STREET.

By now everyone sort of knows that inflation has been re-heating in a very disconcerting way for months, and that the inflation saga is far from over. There are all kinds of discussions about the future of inflation in the US, and it seems there is a rough common denominator forming: The future of inflation in the US is more inflation – more than there was before the pandemic, when the “core PCE price index,” the Fed’s favored measure, rarely went above the 2% line, and then only briefly and by a hair.

But not a whole lot more inflation, just some more. The thinking is that fiscal priorities are fueling inflation, that the monstrously ballooned and still ballooning debt since the beginning of the pandemic needs to be dealt with through inflation, and that the time has come when the price of free money becomes known.

And this higher inflation means that interest rates will be higher – not only “higher for longer,” but higher without going back down to where they’d been in the years before the pandemic, so higher forever?

The White House released its budget proposal on Monday. It was larded with higher interest rates as far as the eye could see. And today, Secretary of the Treasury Janet Yellen was asked about that.

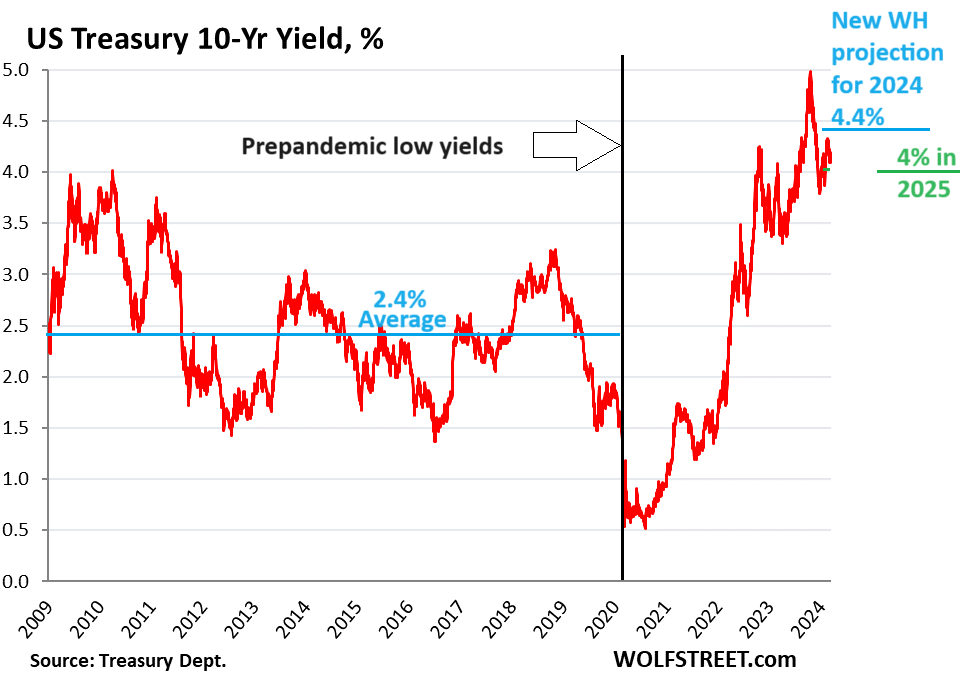

In the years from 2009 to the beginning of the pandemic, the 10-year Treasury yield averaged about 2.4%, according to Bloomberg.

The White House budget proposal projected that the 10-year yield would average 4.4% in 2024, up from its year-ago projection for 2024 of 3.6%, and up from the average in the decade before the pandemic of 2.4%.

And it projected the 10-year yield to average 4% in 2025 and to 3.7% in 2029!

The budget proposal also projects that the 3-month yield will average 5.1% in 2024 (it’s at 5.48% today). A year ago, the White House projected that it would average 3.8% in 2024.

And that 5.1% projection might have come out even higher if Lael Brainard, director of the National Economic Council, hadn’t intervened, according to Bloomberg’s sources.

In other words, given the new reality of inflation, both short and long-term yield projections got ratcheted upward substantially over the past year.

“I think it reflects current market realities and the forecasts that we’re seeing in the private sector, that it seems unlikely that yields are going to go back to being as low as they were before the pandemic,” Yellen told reporters, according to Bloomberg.

“It’s important that the assumptions that we built into the budget are reasonable and consistent with thinking of the broad range of forecasters,” she said.

In January, she’d already hinted that yields might not go back down to prepandemic levels. “There are people who feel quite strongly that nothing fundamentally has changed, and [yields] will eventually settle back,” Yellen said, according to Bloomberg at the time. “But the strength of the economy also suggests that perhaps productivity growth and potential output growth have increased and the level [of yields] would be higher.” And so “the jury’s still out” on how far yields could still drop, she’d said in January.

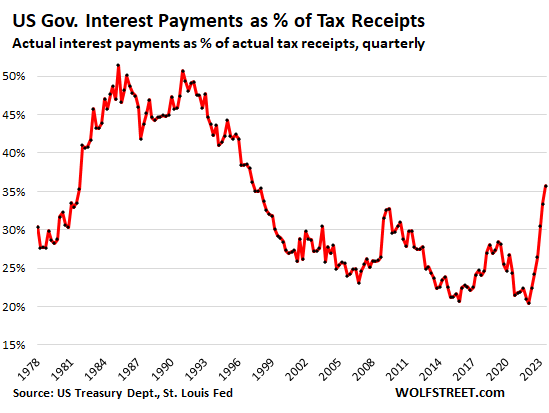

Higher interest rates in combination with the ballooning debt cause interest payments to soar. But inflation inflates tax receipts, and economic growth also boosts tax receipts. So the number to watch is interest payments as a percent of tax receipts, and it’s ugly, but not as ugly yet as it was in the 1980s:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In before the first “the fed will cut by May!” comment……

I say June and 50bps and none other until after the election.

Told you so………

Late to the party dude, this has been obvious for months. They’re stuck. They have high short rates to suck up the excess cash, while long rates are near the ‘new normal’. Result is inversion perversion.

When they cut 3 mo and 6 mo, cash becomes loose and spikes prices. When they raise 3 mo and 6 mo they cut purchase of 1 year and longer. Why do I want a 10 year bond when my money market pays better.

They are saying this now because they are worried that inflation is heating up again in election year.

Didn’t you hear from the horse’s mouth : “The landing is and will be soft.”

In other words there is going to be no landing, the 1% will be bailed out and tou will be made poor with high inflation.

God bless America

Inflation eats the purchasing power of all assets equally. A mono-billionaire doesn’t necessarily “feel” inflation because, like, who cares if grocery prices jump, but they’re still losing purchasing power on their assets. If inflation is 10% over a two-year period, the mono-billionaire’s assets lose $200 million in purchasing power.

So what is going up in price, besides groceries? Or is just the dollar losing value? In which case it’s pretty much everything.

Lots of stuff actually DROPPED in price for the past couple of years or so, including used vehicles, consumer electronics, energy, etc. But other prices rose, auto insurance and some other services spiked, rents continue to grow at a red-hot pace. Read all about it here:

https://wolfstreet.com/2024/03/12/beneath-the-skin-of-cpi-inflation-february-inflation-saga-far-from-over-core-cpi-core-services-cpi-in-ominous-6-month-trend/

Unless of course, their assets increase by way more than inflation due to a mania because “there’s no better place to be than in U.S. tech stonks.”

But there is also the risk that, in addition to losing in purchasing power of their assets, their asset prices actually plunge. It goes both ways.

Wolf, respectfully, your first sentence does not make sense. Inflation devalues fiat currency (i.e. money), but it does not necessarily cause a devaluation of other asset classes, particularly real estate. Indeed, inflation makes the value of many assets classes go up, otherwise the devaluation of fiat currency would have no effect.

Von Meren,

It does not make sense to you because you don’t want it to make sense to you.

So let me help you. If you have a property worth $1 million and 10% inflation, then the purchasing power of the property dropped by 10%. Maybe the price of the property also drops, say 70% as in an office building, and then your total loss — loss of purchasing power plus loss of market price — is even bigger than 70%.

If your property price rises 10% to $1.1 million, and there is 10% inflation over the same period, the purchasing power of your property drops to $990K ($1.1 million minus 10% inflation).

Anything that is denominated in dollars loses purchasing power when the dollar loses purchasing power. Your hope is that market price increases will be higher than the loss of purchasing power, and sometimes it is, and sometimes it isn’t, sometimes market prices plunge even as there is inflation, see commercial real estate. Stocks can do that too just fine.

In my opinion only pure, simple cash would have that amount of loss. Other classes of assets may remain unchanged or even increase. It depends.

Long duration bonds can easily lose more than cash. Even if you hold them to maturity, you may be stuck on a lower nominal yield than you can earn on cash.

P.S. On reflection, I guess you meant cash under the mattress or in a non-interest-paying current account. That would be worse than bonds–apart from European or Japanese negative-yielding bonds!

Pure wisdom dispensed daily. You can miss your morning coffee or your vitamins, but you do not want to miss these articles.

Eloquent, timely, and focused creations that make humorous the idea of replacing Wolf Richter with Chat GPT or any Artificial Intelligence in our lifetimes.

PPI smoking hot this morning.

Higher for longer.

Wolf, yes, but people believe, based on the last 15 years, that the Fed will protect stocks and thus that they’re a good inflation hedge.

Enough people believe that, and it becomes true.

Inflation eats the purchasing power of dollars. Inflation has been evidenced through the irrational increase in the valuations of assets. The billionaire class has benefited so hard throughout the inflationary period. Even though things cost them more too, their gains are that much more outsized. The public loses again.

As a retiree living off my savings, the 10 fold raise I got this year on interest will far exceed many years of inflation.

When purchasing power of fiat currency drops, money flee to assets. In general, the increase in assets value more than compensate for drop in currency purchasing power.

“but they’re still losing purchasing power on their assets”

Right…and needs to be kept in mind every time somebody says,

1) “Well, rising interest rates may have slammed the market prices of those ZIRP-era Treasuries hugely held by banks but,

2) “So long as the banks hold those mark-to-market-impaired Treasuries to maturity…the banks aren’t out anything…”

Yeah, well, really, not so much.

Because while the banks won’t have to take a hit due to declines in the market prices of their ZIRP era Treasuries…the repayment of principal the banks get at maturity *has already been* damaged by inflation (which is exactly why the Treasury *market prices* fall…to offset that inflation-induced fall in principal repayment value).

So, banks don’t really come out of inflationary-eras unscathed, even if they hold their assets (35%+ being in G-issued securities) to maturity.

The only winner from inflation is the fiat-printing Government…which conjures buying power from unbacked thin air (actually, stealth confiscation of private wealth).

Which, from the G’s perspective “is a good thing” since the G is an enormous debtor, with no realistic alternative method of debt repayment (taxes? The G gave up being constrained by tax revenue 25-50 years ago).

Wolf,

If the fed, in their discussions, decides to weight the various metrics such that mortgages/rent inflation is seen as the largest problem, could they say “well, increasing rates is actually causing inflation, so lowering rates will lower inflation”?

Since it would be a political win, a win with the public, a win with wallstreet, and since they can make a case for it by stressing the impact of mortgage/rent inflation on the whole, what do you think the chances are they’ll do it?

Since 2020, many said shut-downs+printing=inflation. But they were ignored for political reasons until inflation was a monster.

All the assets that the rich buy can decline concurrently as the result of a popping asset bubble: real estate, stocks, bonds and collectibles.

Leo,

I’m with you. With that level of debt, the CRE time bomb and banks’ unrealized losses, it’s a no-brainer — they will lower rates. The hell with inflation. They’d rather have the little guys will suffer but that’s nothing new.

Econ 101: the marginal value of the dollar to the billionaire is less than it is for the hundrednaire. The billionaire already has all the *rap he/she wants be it mansions, food or feel-good EVs – plus they can afford full time drivers, pilots, etc!

Or regression to the mean?

Well, I thought the article was quite good, presenting the facts, as currently understood to be facts given the proviso that the final values, after review by competent academics, will be recorded as the official record of what happened. Therefore, of significant financial interest about an extremely important slide rule about the likely economic future of America.

The best case prediction of the long term interest rate structure, revises it’s estimates of future inflation greater than the generous 2% target.

Yellen, although a poster child of what’s wrong with the philosophy of the Federal Reserve, is a pretty good analyst with the power too impose her vision of the required economy of the United States and, in many ways, influence the world economy.

Right up to the moment the immiserated middle class natives pick up their pitchforks and begin searching for the culprits/instigators. They will be joined by taxpayers of many stripes.

It’s all about the exploding debt. Every unit of purchasing power the government spends comes from somewhere. If it’s not collected in direct taxes, it’s collected in inflation. Or purchasing power is eaten up by higher interest rates. The only alternative is the government repays its debt…

The government repays its debt? This isn’t The Onion. That was a good one.

Which leaves … direct taxes and inflation. And you can be sure most of it’s not going to be taxes either. The gap is too big.

The inflationary conclusion follows as night follows day…

But the internet makes it much, much, much harder for the G to effectively lie to the public about the primary source of inflation.

It ain’t 1994, 1984, or 1974…and tens of millions are already educated enough (and/or easily educated enough) to tell Biden exactly where to shove his Snickers.

The Fed will erode the debt with steady 3% inflation.

This only works if the government is spending less than it’s bringing in. Otherwise it still has to borrow and, because of inflation, it’s now borrowing at higher rates, so the debt continues to grow.

But inflation erodes the purchasing power of that debt, and inflation inflates tax receipts and nominal economic growth, and therefore inflation reduces the burden of the debt. Inflation is the classic solution for a country to deal with its debts.

“Inflation is the classic solution for a country to deal with its debts.”

And so you agree with me that it’s intentional.

Clearly, the Fed’s 5.5% rates (highest in decades) and QT (biggest ever) are “intentional.” There is nothing accidental about them.

Except government spending always increases faster than inflation. It would still have to hold spending where it is, which it has never done.

Not sure,they will erase the old debt, but create so much new debt that you won’t see any difference.

As long as the deficits keep growing,you can expect inflation.

The day they cut the deficits to zéro,you’re back in a normal economy.

And a normal society.

Gerard-

“The day they cut the deficits to zéro,you’re back in a normal economy….”

… and a make-up depression (make up for 20 years of over stimulating by monetary and fiscal technocrats).

Not trying to disagree with your assessment, but a zero deficit means confiscatory taxation or severe austerity or both, either or both of which will crush the “animal spirit” out of both producers and consumers proportionally — for a while.

That’s the price society will pay for “managed money” and a controlled economy, financed by debt and enabled by central banking.

The debt does not erode away. There is no such place called away. Like all debts, it must be paid…or expunged in other atypical ways.

Inflation makes past debt cost somewhat less in current dollars…but it is still there, choking out future meaningful investments.

That is only true if the increase in income is less then the cost of the loan. If done correctly (and that is something of a specialized field of study) any loan results in a breakeven or increase in government revenue compared to the loan.

The problem in the USA is that the loans are/have become a structural necessity instead of being budgetted for repayment after having been used to bring future revenue forward.

Depends upon the real rate of interest. Financing nearly 40 percent of WWII’s deficit through the creation of new money laid the basis for the chronic inflation this country has experienced since 1945. Interest rates, especially long-term, would have average much higher had investors foreseen this inflation.

I can still remember the first time a coke machine wanted more than one coin. A quarter wouldn’t do it. Before that, there had been almost no change in the price of a coke or much else. That was in 74. After the Arab/ Israeli war the Arabian countries had broken the grip of the Seven Sisters, the giant oil cos, and the price of oil began its rise from a few dollars a barrel. Oil is a input to everything. This more than any factor began post- WWII inflation. Then politics took over.

When Reagan took office the accumulated DEBT, not the annual deficit, was one trillion dollars. This includes the WWII debt. Four years later it was two trillion. This began the political reality for both parties of ‘deficits don’t matter’.

Now the US adds a trillion to the debt every 100 days.

Don’t blame this predicament on WWII spending.

Yes, there is no wiggle room with a mortgage loan, which IMO is important to pay for as long as possible.

The current period can hardly be compared to the post WW2 economy. Frankly, the WW2 veteran entered a manufacturing economy on the rise rather than the decline in good paying jobs with family level benefits that faces the current returning veteran.

And cuts spending on wars which are no direct threat to the safety of the country.

We have harmless countries to the North and South and lots of fish on the other sides. We don’t need to be involved in wars although we have only not been in war for 17 years of our history. A good chunk of our debt was not only unnecessary wars but by international standards illegal. Our spending is more than the next 10 highest countries combined. That said, the next cold war is here so let the spending begin!

It is increasingly exhausting hearing my fellow Americans pretend they have no enemies and no risks if they abandon the rest of the world. This isn’t little house on the prairie. We depend on global resources amd industries in allied countries to run our economy. And you can’t move a mine back to the US. Even if we pretend we are an island nation, the British figured out the way to play that game hundreds of years ago, which is to ensure no one power dominates all the lands on the much bigger Eurasian/African continents. If we want to make sure global wealth and resources are available to the US without paying crushing tribute to China/India/Russia/whoever then we have to be actively involved globally through alliance networks. We and our allies are the only ones who want to play the free trade game. All the other major powers don’t let that nonsense go on in their controlled lands.

GrumpyVet,

The global resources are available to Europe and the US as a result of military might and not respecting other cultures. China, Russia and India were not even industrialized countries at the time Europe split up Africa via the Berlin conference. It appears you favor that the biggest bully in the room can simply take what they want or overthrow any government elected by the people to advance America’s economic interests. There will for the foreseeable future to have a military but not for purely imperialistic means. Despite your characterization of Russia, India and China they do participate in the market economy as clearly seen via trade. I suppose I could be exhausted by those that believe in American Exceptionalism which of course has very different meanings internally versus externally. Our military and policies has also radicalized much of the World against us so it should be no surprise when that blows back.

Good points.

We stayed out of WW1 and WW2 as long as we could. Most of the expenses and damage to economies were to those involved in the war at the beginning.

I am not sure if anything good economically came out of the the wars we spearheaded like the Vietnam war or the Gulf Wars except lots of debt, loss of life, and PTSD.

What value was achieved. What value will be achieved in the Ukraine conflict if Ukraine wins. What value is lost in the the US economy if Russia wins?

Fish on both sides? That’s the reason the UK slept in the 30’s, when the bomber was being developed. ‘We have the navy, we’re safe’. Fast forward: The ICBM doesn’t worry about water.

There is one thing historians mostly agree on: WWII could easily have been avoided if if if aggression had been met head on, instead of letting it slide. Japan began its conquests a decade before Pearl. Closer to home, Italy invaded Ethiopia years before Germany was in a position to do anything. But H noticed and what a gambler he was.

Sure, it’s Britain and France that share most of the blame at this stage. We know that from the captured documents that when Germany re-occupied the Rhineland their troops had orders to pull back if France moved. But the UK, France’s ally dithered. So Germany got away with it. Then came Czech, and they got away with that. Big bonus: the excellent Czech Skoda munitions industry came with the deal. plus of course Czech gold.

It should get these isolationists attention that Sweden, neutral for over 200 years, smells the coffee.

Well, that’s not likely too happen which brings us back to the start where as I was arrested for protesting against the destruction of Iraq,

I asked myself similar questions.

They don’t seem to be concerned by the exploding debt as you do. The loss of your purchasing power seems to be last thing on their mind.

They seem to be making a mistake in policy that has anchored inflation at twice the published goal.

Their greatest armor at this point seems to be nonchalance, pretending it is no big deal.

Happy1…make that 3.5-4% inflation.

Looks like the new “neutral rate” is 3.5 to even 4%. Ouch, but the Fed is not acknowledging this YET!

Totally agree. The government understates actual inflation by at least this amount.

For those of you who were not around in the 1980’s, home mortgages peaked around 1985 at about 17% and banks were paying about 17% on certificates of deposit and trying to make loans at about 20%. Savers loved the rates and borrowers hated them. In the last 5-6 years borrowers loved the rates and the savers detested the non existent rates. There needs to be

balance between the two groups and to do away with the modern market interest rate theory. It seems to me that rates are about normalized now whereby each side is not feasting at the expense of the other side.

I’d LOVE to get 17% on a CD.

In a low inflation environment, such high rates sound wonderful, but what if 15% inflation is required to get us there?

Many of us think asset inflation counts as inflation, in which case we’ve had more than 15% per year for the past 4 years.

Yes, and enjoying those 17% on a CD with 15% inflation ongoing will kill your wealth really quickly when paying a good chunk out of those 17% in income taxes.

Sure but what is giving you a better yield in an environment with 15% inflation?

At that point, simply losing less money than everyone else puts you ahead.

I lived through the Eighties, 17% was rough. Everything purchased reflected that 17% number and prior years inflation hurt the dollars purchasing power. It’s alright today, just buy assets that appreciate more than inflation. Real Estate in certain markets is strong if one is buying from a cash position.

The high interest paid on CDs back in ’82-3 were the result of fear – fear that inflation was still climbing and that 17% on a CD is a sucker’s bet. Everyone didn’t say, “Wow, 17% CDs! Gotta get some.”

Taking things out of context – Monday-morning quarterbacking – distorts history.

You can still ladder your maturities – nothing about 17% rates means you have to lock in duration.

“It’s alright today, just buy assets that appreciate more than inflation. ”

You make that sound a lot easier than it is – and ironically I wouldn’t put RE in that category unless you’re getting income from it.

Exactly. Higher for much, much longer. The alternative is much worse. The sun will rise and life will go on. Suck it up buttercup!

Try 1982, when even a small saver could get 16.55% on a 30 month insured CD at their local savings and loan.

Small for the size of the purchase or small for the number of folks who could afford to purchase a CD.

No one on this blog ever talks about un-employment. FYI, The Midwest was hit the hardest in 1982 with un-employment rates approaching 30 %. Rockford IL. had the highest in the nation with 30 % un-employment. AND, employment is one of only two mandates the FED has. The other mandate is stable prices and frankly, on the whole prices are relatively stable. Yes, housing is not but housing is not the mandate.

I was thinking small for the size of the purchase. One of my older relatives told me years later that she had been buying 30 year zero coupon bonds at that time. Not bad for someone who had no business degree or had even been to a 4-year college.

The cause-and-effect relationship between “interest rates” and “inflation” is not so well established that one can say with certainty “rate cuts reignited inflation” in the 1970s, nor that “rate hikes will tame inflation” today. Falling rates certainly didn’t reignite inflation from 1982-2019, just asset-price bubbles!

Just because “everyone believes it” doesn’t make it true – especially in economics. And just because something “worked” in the 1970s doesn’t mean it will work today; the system is organized differently now. Changing rates back then came with different side-effects than it does today.

In the 1970s economy, driven mainly by manufacturing, credit availability was tightly linked to rates, in a way that is no longer true in todays service-based economy with “ample reserves”.

Also, the Federal Reserve managed differently in the 1970s; the Federal Funds Rate was not set the same way it is now, nor linked to other rates. In 1974 the 3-month T-Bill maxed out around 9% (nowhere near the 13% blip in Fed Funds). Today the T-Bill rate hugs Fed Funds because of Interest on Reserves and other arrangements that didn’t exist in the 1970s.

Finally, in the 1970s, oil-supply and labor politics came in waves, and those episodes drove inflation too.

I think we’re about to rediscover how little we really know about the causes of inflation. This won’t stop economists from claiming omniscience about it all, and selling us on persuasive policy platitudes with zero accountability for success or failure…

“Falling rates certainly didn’t reignite inflation from 1982-2019, just asset-price bubbles!”

We also had two major deflationary trends during this era of falling rates:

-Cheap goods imported from China

-Cheap energy from the shale revolution

We still have the latter, but the former, not so much in the increasingly-fragmented world.

Great observations Wisdom Seeker. A little more in the 1970s here just to bring everyone up to date. 1.The oil embargo was somewhat like the recent pandemic; coming out of nowhere quickly and causing great consternation among regulators and politicians 2. The U.S. went off the gold standard, 3. Wage and Price controls were initiated causing tremendous dislocations. Oh, and that pesky war thingy as well. Oh, and one more thing, a president was forced to resign. As Rosanna Dana used to say, “it’s always somethin'”

The only time the US gov’t interest payments to tax receipts that even comes close to going vertical like the very end of that last chart is when interest rates were about 3 times what they are now. So even if interest rates half over the next couple years the spending burst by the US gov’t is huge and would still be on a stiff upward trajectory if gov’t spending isn’t trimmed back. It is hard to see spending trimmed that steeply in the near future.

Im confused. Can’t we in the usa go full on japan model and simply print away until we have a 3 times debt to gdp and growing while keeping the tiniest of interest rates that are way under 1% just like japan does without a care in the world? Free as a jaybird chirping la la la la la, rite past the graveyard?

And if not, how come?

Who picks who gets a interest rate hall pass?

Oh and heres a monkey in the wrench…. Brainards ppt is a group that reports to the president, so it’s political.

No wonder so many top congressional leaders are dropping like flies into retirement lately.

Me thinks they have seen the light.

And it ain’t pretty.

A lot of reasons why we couldn’t “do like Japan” in the United States that my econ prof pointed out. For one, Japan has the advantage of a massive trade surplus (at least until recently, and still fairly balanced), the US has the world’s biggest trade deficit, by a big margin. That tightly limits the potential for the US to try something like that. And, nature of the debt is very different, Japan’s national debt was heavily internalized and its own equivalent of T-bills issued with some differences to ours. We’d take a much bigger hit going down that route.

And, Japan also had very low inflation during this period. For the US, just trying to “print things away” would lead to massive inflation and hyperinflation when we’re already struggling with such pressures. It wouldn’t be Japan for the USA, more like Argentina or Zimbabwe for us. Still other issues added on, for ex. Japan being much more homogeneous and high trust as society has a way of making it easier to put up policies to cushion effects of high debt either way.

And there’s also the types of debt. It’s easy to forget, but a big part of the US debt crisis is from those tremendous costs from the wars in the Middle East from 9/11, not only Iraq and Afghanistan but that mess in Syria too where we were trying to get rid of Assad for.. something. Maybe $7 to 8 trillion down the drain to get defeated in wars that weren’t in the US interest. (By comparison support for Ukraine is a bargain, and we’re just getting rid of old weapons anyway to stop a breakdown in international conventions that would cost us a lot more without giving help) Japan doesn’t have this kind of burden.

Great article. 2nd paragraph delt should be dealt.

There is an absolutely massive speculative melt-up going on in all of the asset bubbles.

Yes, assets are priced as though ZIRP is just around the corner.

Do the big boys know something we don’t?

People think the fed is going to cut. That’s it.

FOMO is a great motivator especially if you missed out on the last run up.

Right, but cutting isn’t enough. Rates have to return to 0 for today’s valuations to be reasonable.

It’s going to keep going up as long as society remains as unequal as it is — a lot of the money injected into the economy via the income interest channel goes to the wealthy, who in turn spend it on asset purchases.

And higher interest rates on a large (and increasingly large with record “peacetime” deficits) outstanding Federal debt means more money injected into the economy via the interest income channel than ever before.

I think higher is forever now, given the debt and spending levels. The supply side is not fully healed and may never be due to the conflicts we currently have. We have enjoyed ZIRP for what a decade or more? Now we cannot adjust fast enough to maintain our lives in this environment and perhaps never will. What we have now is a tail of two economy’s. More social programs will be employed to help but only make matters worse. The FED has to crash the economy in order to save it. None of this soft landing will occur,it’s impossible IMO

It is politically untenable. It will only be addressed if the pain people continue to feel from inflation starts to exceed the pleasure they feel from government deficit spending.

A tail of two economies is right. I see endless articles expressing the confusion the elite have as to why “inflation isn’t all that bad so why are the middle class upset?”

Money printing caused asset prices to go up as much as the increase in m2, but it will have caused as much inflation by the time its done. The asset prices help the top 10% enormously, but only make it that much harder for a middle class person to buy a house, for example. Meanwhile the top 10 percenters portion of monthly income that goes to food or to fill up their tank is negligible, but for a middle class person that’s probably 60% of their take home paycheck.

But unfortunately, they voted for this, and likely will again.

Thanks Wolf. Seems to me Yellen keeps insinuating yields dropping and is avoiding “yields rising.” They are still jawboning their book. What a year this will be! Looking forward to it. Many thanks to you Wolf.

Looking forward to it? It’s disgusting. I can hardly follow it anymore this country disgusts me so much.

Same. I no longer stand for the anthem and I fly an upside down flag in front of my house.

Ein

So you hate the country because you find it hard to make money ?

Because making money is the ONLY reason for the existence of the USA ?

Got it!

To OutsideTheBox,

Despite the blessings to many inside the USA with money, it is one of the worst places in the world to be poor.

The USA government does not take care of its people. They use the rhetoric and prospect of lifting up different minorities as a cudgel to hurt the majority, and then ignore the minority they promised to help.

The USA isn’t a nation of people or a true country, it is an economic zone. The elites running the USA want and act as if every worker bee is a fungible unit, completely replaceable and wholly unremarkable.

As the currency winds down and the military complex of the whore of Babylon is defeated you too will have to face this truth.

No. I hate what the country has become because it’s now run and controlled by spoiled children with a myopic attitude. A country where people vote themselves free money to go shopping with (stimulus bills) is not a country I’m proud of. Nor is a country that doesn’t control its border and then has the courts and media stop any attempt to do so.

Ein

So you admit you are being ruled by paternalism, paranoia and xenophobia ?

Got it !

I rotate flags. One of my favorites is Angola, although China is flying currently. I hate the policies of this country and its history of imperialism and worldwide genocide, along with the political system. I truly hope at some point people wake up and people organize as I would love to see change that benefits Americans collectively as a whole as most would love change to buy where to start? For now we are stuck with creating enemies and arguing who can use what bathroom so not quite there yet! I will pop a cork when the hegemony of the US military and economic system is balanced. Doubt I will see that but it will undoubtedly show up within this century. Many Americans are fiercely loyal to a system they hate and of course much of that is whitewashed history and propaganda. Society is continual evolution and this is certainly not the end state.

The Indians and buffalo who roamed this country a few years back would wonder about your statement.

Do you mean the Indians we killed and took their lands back then? The buffalo? Well, the Indians were killing them too!

Anthony A,

Revisionist and reductionist is always fun. Besides the genocide of 15 million native Americans many of the buffalo were wiped out. The native Americans hunted them sustainably for food, those committing genocide killed them mostly to starve the native Americans and for other reasons.

Anthony A

I doubt anyone here has killed Indians or buffalo.

My comment was directed at desert rats statement that this country disgusts him.

Sure the Treasury and White House are trying to jawbone yields down; what do you expect, that they jawbone up the yields, LOL? But they admitted here that it cannot really work over the longer period. All they can accomplish is avoiding a sudden upward explosion of yields, which could be a problem.

Nobody can jawbone yields anywhere. The market determines yields and the fed follows the market. Obviously debt markets think 4% money is cheap and are buying it up hand over fist. The stock market apparently agrees.

Both parties of our government do, however, think they can eliminate the bottom half of the economic cycle. This serves both parties’ reelection agendas.

They’ve done the equivalent of eliminating winter because voters hate the cold and created a massive water shortage afterwards because there was no snow melt to refill the reservoirs.

Sentiment is a factor in markets, and rhetoric affects sentiment. Which is why they use it as much as they can.

A lot of the higher weight gold bars are running out of stock at my preferred dealer. Something on the horizon.

A big crash in the price of gold?

The same observation in my small, but affluent neighborhood. My local dealer has a buyers’ waiting list for bullion.

All while there is a news blackout of gold surpassing ATH.

All while there is a news blackout of gold surpassing ATH.”

LOL. Conspiracy bullshit. Google the phrase: gold all-time high

It’s all over the place: CNBC, Bloomberg, MarketWatch, WSJ, JP Morgan Insights, Forbes, Barron’s…

So is gold an attractive investment now, Wolf?

I think the answer is “yes.”

I won’t keep you guessing….

In a fractional reserve system debt is “money”. I know Wolf thinks debt can be “inflated away”, but the fact is debt has grown exponentially for 50+ years. This is true globally as well. Expending the monetary base is fine IF production is expanding and trade is increasing etc.

To quote Von Mises – “There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

You’re referring to numerical values. But the purchasing power of those numerical values is what matters, and the interest payments as a percent of tax receipts is what matters.

People who are praying for this debt collapse don’t understand the nature of inflation.

BTW, your quote talks about a “collapse of a boom” (bubble), not collapse of the debt, or the economy, and sure, bubbles collapse, such as the CRE bubble and we’ll get more of that in other areas, and sure investors will take it on the chin. That’s normal. But it has nothing to do with government debt. That’s an entirely different animal.

“But the purchasing power of those numerical values is what matters,”

YES, so much so that eventually the producers demand something else for payment.

Nah, looking back at history, you know they’ll take dollars. Dollars are just a payment instrument. They’re not a religion.

Looking back at history, everything you are saying about the dollar was said about about the pound sterling. Dollar usage in global trade settlements is decreasing. This is a fact. Not the end of the world, but the average Joe and Jane will see significant decreases in the quality of life. The message is, don’t be average, it’s a competitive global market…

Same as it ever was.

So which currency is better? The euro? the yen? the toilet paper called ruble? The RMB? take your pick.

There have always been competitors to the dollar at all levels, in recent years, the euro, yen, and for some trades the RMB. The dollar has never had a monopoly. Who are the idiots that think that the dollar ever had a monopoly?

Businesses in neighboring countries have always settled trades in their own currencies – that’s just common. They might price a product in dollars, but settle the deal in pesos or RMB or whatever. In terms of trading currency, the euro has been roughly on par with the US for years. Crude oil might be priced in dollars and get paid in euros, no problem. Been that way for a long time, and before then they settled the invoice in Deutsche marks. This stuff is routinely negotiated up front as part of the deal. That’s not bad for the dollar, it’s just how it is.

The entire Austrian School was based on nothing more than thought experiments… zero empirical research, but the past 30 or so, post-Reagan years provide plenty of data. Cutting taxes results in a pool of wealth, which does not go anywhere, the very definition of “pooling.” So we now have a concentration of wealth amongst a handful of new robber barons and a hollowed-out middle class. I’m not sure when folks are going to realize this fairytale is nothing more than that, but Von Mises, Hyek and the rest of those hacks have been proven empirically wrong.

Tom V.-

Two questions:

1. How long can debt growth exceed GDP growth?

2. What happens when fiscal deficit as a percent of GDP reverts to mean? (And how does the monetary authority react to THAT crisis…)

I found Adam Fergussens When Money Dies (or better yet Constantino Bresciani-Turroni, The Economics of Inflation – A Study of Currency Depreciation In Weimar Germany (1937) fascinating and instructive.

Argentina and Japan are interesting real-life ongoing experiments.

Disparage and disregard at your own risk…

Respectfully

Austrian school has been proven dead right as it relates to hard money. Gold was 35$ an ounce in 1970 and is 2,000$+ now. The economics of lower taxes you are describing are also dubious, no one actually paid those higher rates pre 1980 because the tax code was riddled with loopholes. And remember JFK also cut taxes massively in the early 60s, so we have had more than just the recent past for empirical evidence, and the 60s were a boom decade. There has been a massive expansion of the upper middle class since the 80s mostly because the value of mathematical abilities in finance and computing has increased 100 fold, there is vast upper middle income wealth now compared with 1980. There has been a broad decline in the middle class because the value of manufacturing labor and run of the mill basic white collar office work has declined as cheap overseas labor decimated manufacturing and computing replaced the need for broad layers of office based white collar jobs.

The middle class rose early 1930s to late 1970s. Greenspan and heirs decimated the middle class. The collapse of Wall Street will help Main Street, in my view.

“Higher Forever? Higher Inflation & Higher Yields Are Here to Stay”

Do you think this is valid for Europe too?

I sometimes wonder if the two or three years for expansion of credit to seep into prices is correct, and that actually what we see now is inflation coming from the last two decades. We are in an era that previous assumptions don’t hold true. In 1951 men had life expectancy only up to 66 and women to 77. This has gone up by a decade.

But even this is talking on repeat, the currency has been debased too quickly and its clear and obvious to everybody. There are also many pension funds/investment funds that state they are fully funded with IOUs only. Not tangible assets. There will be a point that creditors will simply not roll over the debt. Italy for the EU. I think the UK will have our nose rubbed in borrowing costs so we will be forced to behave, currently over 5% of GDP goes on debt servicing. The US sadly is bankrupt including even internal pension schemes. But it all staggers on. Its incredible to see.

Yellen is worse than Powell. Everything she says is old news. She is without a doubt the most boring speaker ever to hit the lecture circuit. I hit the mute button every time she opens her mouth. The elephant in the room is the 1 trillion federal budget deficit every 100 days. Until that is brought down, nothing these people say or do will have any impact in the near or long term. A train wreck is in the works. Just noticed crude just went over $80/barrel. I’d like to see it go to $100 or higher. That may help get some of the cars off the road and releive some of the traffic jams that have become the norm here since the end of the pandemic.

Kakistocracy via those that think they are the clerisy.

Ein

They say…..It takes one to know one.

Whoa, you got me!

Sahm is solid.

Did she apply and was she turned down for Yellen’s position ?

At $100 WTI, you will see an even bigger boom in the US oil patch. The US is the largest crude oil producer in the world. So higher oil prices are good for part of the US economy. And consumers can handle $100 WTI. It was over $100 for a few years through mid-2014… and that was almost 10 years ago. It’s more problematic for consumers these days when it goes over $150 or $200, but US production would ramp up so quickly at those prices, it would make your nose bleed, and overproduction will push the price back down, which we have watched over and over again.

Oil won’t go that high as long as there’s a natty gas glut. The latter is priced like $10/bbl oil which puts a ceiling on Brent/WTI prices.

Higher gas prices also won’t affect EV owners.

The WH predicted that, on average, the 10-year yield would be 70bps /higher/ than the 3-month yield for this year.

Fascinating.

Right. Just the same I’ll take the opposite side of that trade and predict that the yield curve will become even more inverted.

In other words, WH predictions are worth their weight in raw untreated sewage.

White House economic predictions are biased political statements. The little people will pay the price.

I need to finish my coffee before commenting on WS… that should have said 70bps lower not higher.

The WH predicts the yield curve will, on average, be inverted throughout the year. That’s the fascinating part.

We need that J-Powell prank account to tell us that all is well, rates are going back to 0, inflation was slayed, and the Fed will soon be backstopping bitcoin and run-down trap houses in SW Atlanta.

Where are you, Jay?

Hiding in Argentina.

Makes you feel like an american billionaire, right, lol.

One argentine peso = 0.0012 USD. You’re now a 0.1 percenter!!!

I think you ask the right question Wolf. My answer is that we will run the economy hotter now. Safely hotter with a 70% services economy, services being highly recession resistant, and QT, QE, and the interest rates for great control.

I expect a tech boom that dwarfs the internet boom with; AI, Quantum, Space, Gene Therapies, Self Driving Cars, Humanoid Robots and who knows what else. The markets will generally rise and rise with only occasional corrections and few or no bear markets.

With 3-4% inflation and few or no serious recessions it will be a heck of a ride. I hope we can remember the human and life side of the equation but I am skeptical.

Thomas, you forgot the sarc

What’s a sarc?

Minutes thinks your comment is sarcasm…. usually indicated by /s (at the end, I believe)

CCCB,

I don’t waste time on sarcasm. If Minutes actually thinks that I would guess he is not very good at the market. What the economy and markets are going to do is obvious.

Everyone is going to access the internet on Cisco hardware…

Inflation is the fairest tax you can have. The grocery shopper pays theirs when they check out and the billionaire pays theirs when they buy a Lamborghini. The genie is out of the bottle. The federal government has realized they don’t need to raise taxes anymore just print all they need and blame others for the inflation. Income taxes and inflation is the true way to assess what you are paying to fund the Federal Government.

Totally disagree. Inflation punishes those at the lower end of the income brackets much worse.

It only punishes those who spend and borrow more than they make, or than they should be spending or borrowing, or than they can afford to spend or borrow.

The poor spend a higher percentage of their income just

to live. The rich don’t have to buy a Lamborghini but the poor

have to buy the basics just to

stay on the wheel.

So, you’re advocating for pissing off six out of 10 people on a rolling basis?

I agree. The point is that a fully loaded truck purchased thru an LLC and used as a write off avoids income tax, self employment tax, and add to that the registration/insurance all deductible. The regular joe has to pay in taxed dollars thus giving the rich a lavish truck to drive the family around on vacation as a ” company vehicle” I am sure I am missing some factors but the point is the rich have so may ways to skip out on taxes and the one tax they can’t avoid is Inflation.

I have also heard inflation described as the cruelest tax because it destroys the value of people’s savings.

With CDs and some savings accounts paying 4-5% some of that is recouped.

Now, yes. But what about from 2020-2022 when rates are 0, but inflation was a total of 20% during that time?

Dead wrong. It punishes retirees and the poor. Wealthy people spend a tiny fraction of their wealth on cost of living. Inflation is the most unfair tax. That’s why people are so angry about the economy at the moment.

The world has become addicted to low interest rates and “free money”.

Starts at the government level with the Fed and ends when borrowers are getting free money.

Ultimately, society pays the price with inflation and serious distortions throughout the economy.

Addicts must hit bottom before they can recover.

We can hope for some kind of a soft landing.

Cheers,

B

Users and addicts both stop when they encounter enough PAIN.

no….not at all… the pain is not experienced and thats the whole point …..You will see ACCIDENT /DAMAGE/UNINTENDED CONSEQUENCE / etc….something not exactly known .[predictable? maybe ] ….wear

seat belt.

Japan gave big (by their standards) this week.

Big pay raises

Powell should be fired. PPI up 6%

Contrary to the FED’s technical staff, retail MMMFs are nonbanks. Purchases and sales between the Reserve banks and non-bank investors directly affect both bank reserves (outside money) and the money stock (inside money).

I was thinking locked in a concentration camp and forced to stamp license plates. But being fired would be a good concessionary prize.

One thing that has been known for a long time, since the 1800’s for sure, is that there SHOULD be a “cost” to money …

“It is a fact of experience that when the interest of money is 2% (or less),

capital habitually emigrates and is wasted on foolish speculations, which never

yield any adequate return. If the old, tried, and safe investments no longer yield

their accustomed returns, we must take what they do yield, or try what is untried.

We must either be poorer or less safe; less opulent or less secure.”

– Walter Bagehot

– mid-19th Century British journalist and businessman

That has been know for thousands of years since Biblical times.

Anon,

Euclid: Things which are equal to the same thing are also equal to one another.

So your house is equal to so many dollars, or bonds, or diamonds and they are equal to each other.

So houses yield rent and bonds interest.

The biggest cause of our inflation is the increase in the money supply over the last 1-1/2 decades. People spend more when they have more ‘bills’ in their pocket. They are not cognizant enough of the ‘bills’ shrinking value.

‘Inflation is always and everywhere a monetary phenomena’. — mostly…

Howdy Prisoners. Finally two Lone Wolf articles in a row I completely understand. Usually his articles and numbers are way beyond my pay grade. Hopefully millions of others knew that since 2008, we have been going the wrong way. AGAIN. Good Luck Youngins

“It’s important that the assumptions that we built into the budget are reasonable”. A truly profound and profane gaslighting statement.

Wolf,

What are the odds of an inflationary recession?

My guess is that since no one has seen one (in the US) since the 1970s, all the economists would be in denial.

If I had to bet, I would say 90% an inflationary recession hits within 1 year.

What do you think?

I just don’t see a recession. It’s very hard to get a recession with government deficit spending like this, and employment as strong as it is, and with wage increases to support consumer spending. That may change some day, but today, that’s what it is.

Oil and some commodities have broken out upside……everybody on this site knows what that means……no need to elaborate. The game they played emptying the oil reserve is over. Just give it a couple months for the effects to translate.

Can’t waif for the next fed governor to hold a presser and announce that we need to be patient.

The kicker is that it looks obvious now that Russia has the west beat in Ukraine……meaning that all the goodies from that area will be sanctioned away from the west permanently.

Yup…….just you wait……we’ve done our job. Depends on what you see as your job…..transferring all the wealth to your good buddies…..yup.

“The game they played emptying the oil reserve is over. Just give it a couple months for the effects to translate.”

I’m not so sure – oil has been elevated by geopolitical risks (Red Sea etc.), yet domestic natty gas prices are extremely low. There’s only so much oil can rise when other hydrocarbons are magnitudes of order cheaper.

Be thankful we don’t have Germany’s energy policy…

One ridiculous Fred chart I enjoy, is looking at spread between 10 year real treasury and 90 day a2/p2 paper.

I guess that just helps me ponder extreme conditions. I’d post a link, but it’s illegal. In a way that may abstractly imply why rates will remain higher for longer.

The O/N RRP rate puts a floor under short term rates – same rationale applies to the 13-week bill. After all, the Fed is the most secure counterparty.

The 3 month/10 year spread just tells us that bond traders are (still) expecting rate cuts and capital gains on gov’t debt.

I don’t disagree, but the current floor policy, is plumbing architecture id an upgrade on prior plumbing that didn’t work.

It’s still worth watching stressed out collateral that’s connected to highly over leveraged bets.

Old FYI from info highway, assessing GFC stress:

“Other categories (A2/P2 non-financial, AA asset-backed, and AA financial) experience increased yields and/or term spreads for at least some time during the crisis, consistent with credit risk concerns. While term spreads may be indicative of liquidity issues, the fact that term spreads

increase more for categories with higher perceived credit risk indicates that the crisis in the money markets is related more to increases in perceived counterparty (credit) risk, with liquidity concerns being a secondary factor.”

My wife is Vietnamese and has lived through a lot of serious inflation in her life. Her simple description of inflation is that prices are not going up, money is losing value.

Sounds a lot like Ben Bernanke economics which seemed to make most of the population quite a lot poorer.

Not long ago, one could buy pretty much any good or service from the world wide lowest price bidder. This helped keep inflation in check.

Now we have tariffs, sanctions, wars (physical and cultural) crimping the supply chain. I predict little change in inflation without a societal one.

US tariffs were much higher from the 1930’s to the early 1960’s. Read up on the Smoot-Hawley tariff bill of 1930.

Not talking about the 30s-60s, when there were periods of inflation and wars.

I was pointing out the deflationary pressure of a worldwide bidding war for just about any good or service. Something that technologically could not have happened in 1930. These technological pricing gains have been wiped out for political causes. Not saying rightly or wrongly, it just is.

Tariffs are good as the world economy flourished under tariffs until someone got the bright idea about world trade which put everyone into eternal poverty.

I don’t think the Fed is going to cut at all this year. Inflation is going to sit around 3.5% and they’ll have to keep delaying. And the market will keep anticipating and praying.

The ten year might creep up to near 5% again as it very briefly was last fall.

Totally agree. Services inflation is rampant. Until people are losing their jobs, it will not be cooling.

Artificial intelligence (AI) will drive US *deflation* for the next 10-20 years. Doing (way) more with less. We are in a new paradigm. I just wrote a 1000-word report for work, in 30mins, using an AI engine. Normally, it would take 1 day… US inflation is not going to be a problem in the future.

We are all hoping you are correct. ……but sometimes unforeseen issues with technology arise that delay immediate universal implementation. Let’s hope not.

R2D2,

“We are in a new paradigm. I just wrote a 1000-word report for work, in 30mins, using an AI engine.”

Then why do you still even have a job, if AI can do your job? You’re contradicting yourself.

But then, the lousy report with fake data that AI generated for you might CAUSE you to lose your job for having trusted AI, LOL.

Very obviously not. AI is just utter BS nonsense.

Because boys are going to magically manage all processes without prompts, oversight, compliance, security…

This is more of the same “paperless office” hype.

AI will lead to dislocation but in the next several years at the very least, likely more inflationary.

Massive increases in computing will drive huge demand growth for circuitry, which will require a massive increase in energy. And all of these inflationary forces are just at the hardware level

“This is more of the same “paperless office” hype.”

Time to update your impressions. The paperless office became reality a long time ago.

My office has been paperless for at least 15 years. If I do get a piece of paper that is important, it gets scanned and then shredded. I don’t even have a filing cabinet. All data is backed up and stored off site, so if the house burns down, I still have the data, LOL. Works great, saves huge amounts of time.

Most big-company offices are largely or totally paperless for the same reasons.

Sure, there are some quaint exceptions, like the small company my wife works for, which still uses SOME paper; they export US meat to Asia, and their Asian counterparts are still using faxes and they FedEx each other shipping documents, etc. But most of their other documents are electronic.

@R2D2 you’re probably redundant if your report audience can query the chatbot themself.

We are already flooded with noise, making this noise generation easier does not help productivity, as the bottleneck moved to a short attention span.

Vadim, if generating the report were just a matter of querying the bot and blindly accepting its output, it would have taken 30 seconds, not 30 minutes.

Biblical prophesy states the opposite will happen with. A quoted line from the Book of Revelation “not even gold will save you” is an ominous warning for future inflation. The timeline is only defined as the end times somewhere in the future.

People are wringing their hands over nothing. The average Fed Funds rate over the last 50 years has been in the 5% range. All we’re doing is returning to normal. It only seems abnormal because we got used to the extremely low rates since the 2008 cash. It is not good for the economy to live on “speed” for too long. Thankfully this is now ending so our economy can return to normal.

MW: Corporate defaults are happening at fastest pace since financial crisis, according to S&P

MW: ‘Perpetually optimistic’ investors worry Fed won’t cut rates three times this year…

2-3 months ago, they KNEW the Fed would cut 7 times this year 🤣

It’s entertaining and enlightening to take a look at what happened to the 10 year real Treasury rate through the trump term.

Obviously the pandemic didn’t help…

However, as rates seem to be interacting with inflation dynamics and staying higher for longer, I wonder how rates will eventually react to instability if the election is chaotic. It just seems we’re already in a state of chaos, but what’s a rug pull look like?

FYI:

On July 27, 2018, he told Fox News’s Sean Hannity, “We have $21 trillion in debt. When [the 2017 tax cut] really kicks in, we’ll start paying off that debt like it’s water.”

Nine days later, he tweeted, “Because of Tariffs we will be able to start paying down large amounts of the $21 trillion in debt that has been accumulated, much by the Obama Administration.”

In fact, the Treasury make a massive miscalculation about their debt servicing costs, and now they are stuck in a situation where most of the taxpayer money burned for interest payments. The only solutions are a (massive) higer inflation, permanent rising debt levels or higher taxes.

Unlikely that the treasury will make an arithmetic mistake that might coincide with your absurd assertion that they made a mistake which is ridiculous you should be ashamed for being so wrong about that which is right in front of you,

Just read an interesting Wells Fargo article where they make their Fed QT prediction.

They think Fed will reduce caps to $30B treasury and $20B MBS starting on 7/1/24 and expect the balance sheet to grow in 2025 due to organic growth in liabilities, not QE.

I’d bet on Wolf Street preduction over theirs, I’m really surprised they think the Fed would reduce the MBS cap.

“They think Fed will reduce caps to $30B treasury and $20B MBS starting on 7/1/24 …”

I would quibble with the date, I think it will come later.

But that type of slowdown might be close to target. Here’s what WF is saying:

1. no slowdown in the MBS runoff – the MBS run off has been well below $20 billion every month anyway, so they would just keep running off at the current pace.

2. Treasury run-off gets cut in half. I have suggested that also, but it would come later, I said.

In addition, I said that they may play with T-bills, replacing notes and bonds with T-bills. Waller put that on the table.

If the Fed is going to limit QT to runoff (and not sell securities), why is there a separate cap for MBS instead of just one cap for overall runoff?

How would too much mortgage prepayment plausibly lead to market turmoil ?

Parallel question:

How /could/ too much mortgage prepayment happen in a tightening environment with QT & rate hikes?

Because most mortgages are at much lower rates than current rates, anyone with extra cash can earn a smiliar or better yield stuffing it into MMFs/CDs/etc than paying down extra principal. So fewer pass-thru pricipal payments to the MBS.

Refis have crashed and the housing mkt has slowed way down – ergo the rate of mortgaes being paid off has also tanked. In this context, what could even cause MBS runoff to run above the cap?

All of these decisions were a compromise by the members of the FOMC, Powell had explained some time ago.

During QT-1, they also had separate caps for Treasuries and MBS.

I think the idea is to keep this predictable. But MBS runoffs are unpredictable because they come off as a result of passthrough principal payments, so the Fed is separating them from the Treasury run-offs which are predictable like a clock because all maturity dates are known to the day. If there were only one cap for both combined, then in a month when few MBS run off because of low passthrough principal payments, which would not be known beforehand, then the Treasury run-off would be bigger than expected.

I don’t think it’s necessary to separate them, but they fear that QT could produce chaos, as withdrawing liquidity suddenly and by surprise can get very rough. They want it to be smooth and calm running in the background, and slowly enough so that markets can easily move the liquidity around to where it’s needed.

When something is too good to be true it never lasts. Meaning the bottom will fall out of interest rates to fleece all the retirees and savers of any real return on their money. That must be just right around the corner because since 1990 its always been the same thing.

In the US at least, in the 1990s, the 3-month T-bill yield was always HIGHER than CPI inflation. For much of the time, it was 1-2 percentage points higher than CPI inflation. It fluctuated with inflation but was always higher. It’s only since interest rate repression started that the T-bill yields were below the rate of CPI inflation. So the current scenario of T-bill yields above CPI inflation is the old normal.

Don’t worry RT, there is currently, no bottom on interest rates necessary. The current problem seems to be the potential for a blow out on the upside of interest rates.

All of those victims you identified holding a 30 year bond at 2 %, lost 40 + pct of the value when the 30 year bond went from 2 to 4.3 pct. They are likely to lose even more if they hold on to the bonds expecting the interest rates to fall, which is unlikley.

The long term interest rate structure is significantly under-priced, if one were to believe that Biden is more likely too re-implement a progressive tax system that would reinvigorate America or that Trump won’t do exactly what he did before, bust the budget with give aways to the rich.

At this time in the history of the world is a laughably short term history of the United States the vice presidency may be called upon to replace the old guy that expired of natural causes, 1 std deviation longer than the expected life expectancy of a decade less.

In the mean while, we are likely on auto pilot, with the political appointees running the agencies in charge.

Of course the normal distribution is predicated on the variance, minimizing the sum of the squared error between the prediction and the measured.

Mathematically, to me, my 20 year old model was what the infantile models inviting the disadvantaged person to divulge information that is really none of there business.

That being said, I think that inflated asset prices are the first wave that causes general inflation in the human population. Caused by an expansion of the Fed balance sheet all the while the Fed refused to recognize the asset price inflation as the precursor of the current consumer inflation.

One should never view the shenanigans as the truth.

Which brings up St. Patrick’s Day as a quasi holiday celebrating humanity, as Patric was known for.

And a pretty good reason to spread one’s blarney among the community.