But they’re earning more than they’re spending, and despite spending like drunken sailors, they’re saving a lot.

By Wolf Richter for WOLF STREET.

Income fuels spending. So here we go: The income from all sources that consumers earned, but without transfer payments from the government (Social Security benefits, unemployment insurance, VA benefits, etc.), has been outrunning inflation since July 2022 – and did so again in July 2023.

So “real” income (income adjusted for inflation) from wages and salaries, interest, dividends, rental property, and personal business, but without transfer payments, rose by 0.2% in July from June and by 1.4% year-over-year, according to the Bureau of Economic Analysis today. Meaning, consumers out-earned inflation by a significant margin.

The three-month moving average rose by 0.2% for the month and by 1.8% year-over-year. This income growth is a function of the rising number of people who are working and earning money, plus rising wages and salaries, rising interest incomes, rising rental incomes, etc.

![]()

Drinking directly from the punch bowl…

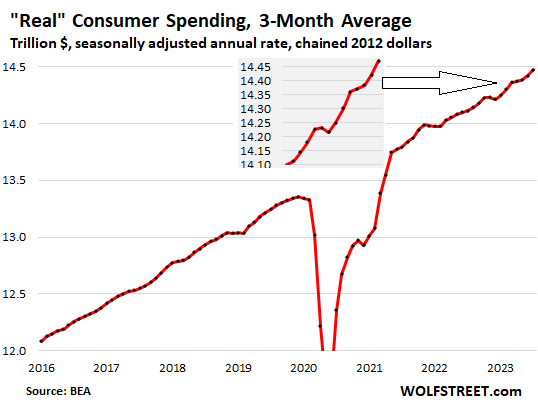

“Real” consumer spending (adjusted for inflation and for seasonal factors) jumped by 0.6% in July from June, which was a heroic feat.

The three-month-moving average, which irons out the month-to-month variation, jumped by 0.4% for the month, and 2.5% year-over-year.

The “real” spending growth of 2.5% year-over-year matched the average growth of the good years before the pandemic, but back then, interest rates were a lot lower. For example, interest rates on new vehicle loans have nearly doubled since then, as the Fed is desperately trying to take away the punch bowl to slow down this party, but consumers will have none of it. They’re still spending like drunken sailors.

In the insert, you can see the decline late last year. But everything accelerated this year:

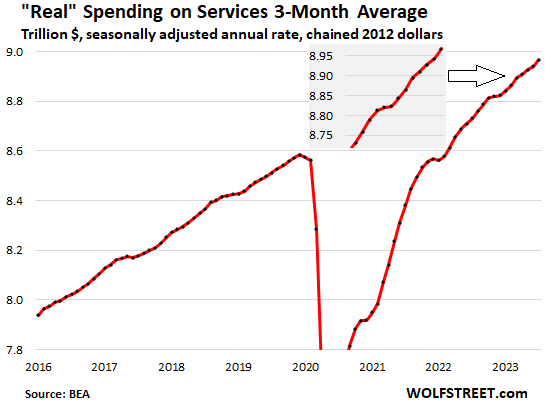

“Real” spending on services jumped by 0.4% in July from June. The three-month moving average rose by 0.3%. Year-over-year, real spending on services jumped by 2.7%.

This means they’re doing a lot of spending on services because inflation is raging in core services at the second-worst rate since 1985, and they’re outspending this raging inflation with ease.

Services, which accounted for 62% of total consumer spending in July, include housing, utilities, insurance – talking about price spikes! – healthcare, travel bookings, concert tickets, streaming, subscriptions, repairs, cleaning services, haircuts, etc.

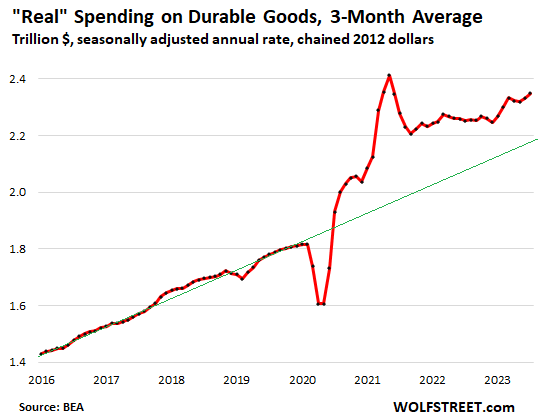

“Real” spending on durable goods spiked by 1.4% in July from June. The three-month moving average jumped by 0.7% for the month. Year-over-year, the three-month average jumped by 4.3%.

This growth was helped by the unwinding of inflation in durable goods – the PCE price index for durable goods has turned negative – and the consumer dollar goes further than it did in prior months and a year ago when it comes to buying motor vehicles, appliances, furniture, electronics, tools, etc.

The pandemic-era spike of spending is far from being unwound, and instead consumers are spending in parallel the pre-pandemic trendline, but at a much higher rate. This is just astonishing:

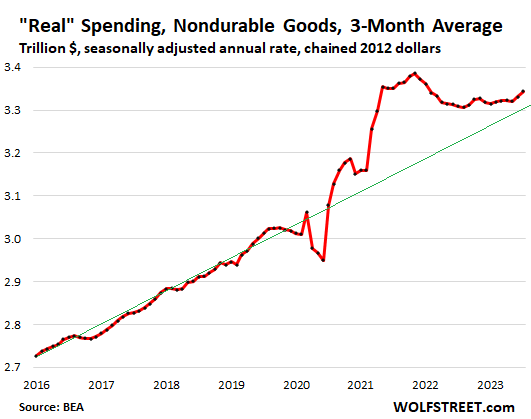

“Real” spending on nondurable goods jumped by 0.7% for the month. The three-month average rose by 0.4%. Year-over-year, it rose 1.1%. Nondurable goods include food, fuel, clothes, shoes, and supplies.

Consumers saved $706 billion in July seasonally adjusted annual rate.

In terms of dollars and saving money, and in terms of Americans being so tapped out and poor that they have to borrow from their credit cards to pay for beer, well, LOL. All figures seasonally adjusted annual rates for July:

- Total income from all sources, including transfer payments: $22.87 trillion

- Disposable income (total income minus taxes and contributions to social insurance): $19.97 trillion

- Spending on goods and services: $19.26 trillion.

- Consumers saved (didn’t spend): $706 billion

This savings of $706 billion represents amounts that consumers earned but didn’t spend. That doesn’t mean it went into a savings account. It might have been used for buying stocks or paying down debts.

As a reminder, all these dollars are seasonally adjusted annual rates, meaning if everything continues at this pace for 12 months, the total savings would be $706 billion.

And these savings will add to the huge wealth that consumers have already piled up in their stock and bond portfolios, 401k’s, bank savings products, money market funds, Treasury securities, home equity, etc.

In other words, consumers are spending like drunken sailors, but they’re earning more than they’re spending, and despite spending like drunken sailors, they’re saving lots of money.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I wonder how much of this is happening in the top 5-10% crowd. How’s Joe Sixpak and Larry Lunchbox doing? I suspect that breaking it down into different income strata, a different story appears. Just my suspicion. Yes, the article is about the economy as a whole. It is not a social studies class. However, we know where the phrase “let them eat cake” led to.

That infamous phrase was never uttered by Ms. Antoinette.

I think it was bacon-wrapped brioche if you translate it directly.

Whatever she uttered, it did not work out well for her.

Yes, it resulted in a new meaning for a “severe haircut.”

It may have been Louis XV or his mistress, Madame de Pompadour. Or it may well have been Marie Antoinette. When I did a Google search on the famous sentence, one article attributed it to the Queen of France shortly before she was beheaded.

The top 50% of households are loaded with wealth. Even the next 20% are doing pretty good. It’s the bottom 30% that is always squeezed.

65% of households are homeowners, which tells you something, given how home prices have shot up.

So….

Which group does the fed want to cut spending in aggregate?

What does the fed want to see in future income growth trend?

How does any of the above 2 directly affect inflation?

Lowering demand makes it harder for companies to raise prices. If their sales are dropping, they’re more likely to price aggressively to keep their sales up. If a landlord raises rents when there is less demand, he might lose tenants, and then he cannot fill his units at the rents he wants, and he has to cut the asking rents… that’s how rent inflation slows.

I have to add one more comment here, because the language bothers me. This idea of ‘homeowner’. Is this someone who owns outright? Or someone who just borrowed their ass off? That doesn’t tell me anything about the real economic boots on the ground situation. Plenty of folks borrow their butt off to get into a house. How much equity do they have? That’s the real story. So homeowner Shmo-homeowner. Like you said, a lot of these young folks have been buying this property. Ok fine. Sure young lad/lass your payment is affordable… at 3%. But your price was 500k. *You* have to pay that off… Or find another sucker to sell to. I guarantee that persons life is going to change in five years. Oh and that 500k. Well… it’s also called an amortization schedule… and that total cost… well.. yeah. You ain’t selling to me. I can’t afford it. My point is ‘homeowners’ really is a loaded word that doesn’t tell you shit. Sure… they legally own the property but it doesn’t tell you dick about how much equity they have, which is the real story.

Dick,

Borrowing (debt) is a form of capital to be deployed. The two forms of funding are debt capital and equity capital. Get used to it. That you don’t own something because it was funded with debt capital is just plain idiotic BS.

I’m getting really exasperated with this BS.

Dick,

Equity doesn’t mean squat either. Equity today doesn’t mean equity tomorrow. My 40% equity in my home in 2008 disappeared in about 2 months.

@Petunia – I’ll bet that was a good two months though. The people now buying RE at today’s prices may experience a similar period of positive investment perception. What a truly fine investment I made. I believe I’ll pat myself on the back for the third time today.

Possibly followed by a not-so-positive period that may include an underwater status on their mortgage loan. That scenario is certainly still possible. Wolf has pointed out repeatedly that the RE market has a slow reaction to economic trends. In the words of Jackson Browne, “don’t think it won’t happen just because it hasn’t happened yet.”

Hope you didn’t go underwater in the 2008 brouhaha. I rented throughout that whole mess and managed to avoid it.

Somebody with $500K debt has to pay the bank $X every month in interst for that privilege.

Somebody with $500K equity is NOT earning $X every month in interest for that privilege (because the money is tied up in the house instead of invested).

Either way, they’re short $X every month because they have a house. The actual number of X will vary, of course, but the principal idea remains.

Dick, your argument breaks down on a few levels.

1) About a third of homeowners own their homes outright. It has been that way since WWII. Curiously it is the people at both the top and the bottom of the economic food chain who are in this situation. The rich man can afford to pay cash for his mansion the same way that the poor man can afford to pay cash for his shack… and bankers aren’t really interested in financing either of them. So the REAL story is NOT about “how much equity they have.”

2) “Shelter” is a fundamental building block of humanity… right there with food and clothing. Go ask Dr. Maslow… these are basic problems that have to be solved before you can work on higher level problems/aspirations. So the question isn’t how much are new “homeowners” paying for their mortgage (or how much “equity” do they have in their home) but rather what is the Delta between what they are paying for their mortgage and what they would be paying in rent. Whether that Delta is positive or negative depends on location… in plenty of communities it is “cheaper to buy than rent.”

3) Most People understand their own financial situation better than you ever will. Along with that, Most People make good financial decisions most of the time. Going from renting to buying a home isn’t a decision that Most People take lightly. So your playing head games with young people by criticizing their buying a home isn’t likely to work. Instead of getting them to think of themselves as being idiots for buying a home… you are instead convincing them that you are an idiot for offering an opinion about their OWN financial situation and decisions.

SpencerG

I think the idiotic thing here is to buy at these prices and interest rates.

Something has to give before a purchase is made.

JuliaB… haven’t you been paying attention to Wolf’s articles? Not many people are buying at these prices and interest rates…

https://wolfstreet.com/2023/08/22/home-sales-plunge-further-as-demand-vanished-at-these-prices-even-cash-buyers-pull-back-supply-keeps-rising/

Most are HOMEOWERS and not homeowners as only about 1/3 of people who titularly ‘own’ houses they live in do so with any mortgages. Most are merely HOMEOWERS for many times more than their houses are fundamentally worth. This is a huge issue in our economy where people ‘think’ their houses are ‘wealth’ when in fact they are huge liabilities.

As bad as the situation looks in the US, pity the recent homebuyer in Canada, where mortgage interest rates are typically reset in 5 years or less. 30 year fixed rate mortgages disappeared in the early 1980’s when interest rates went sky high.

You say you own your house outright, as in no more mortgage payments, or you bought with cash. Try not paying your property taxes and see who owns your house. You are always renting, to the bank for a while if you take out a loan, and always to the county or state.

If one’s IQ is larger than their shoe size, any homeowner would include their property taxes in their rent equivalent. My taxes on this barn are about $240 a month. My “lost opportunity” at the current 5% return, based on what cash I laid down, is $1,854/mo. All in is about $2,100/mo. Add in insurance, it’s about $2,200. We have a voluntary “sinking fund” of $500 a month for repairs/maintenance. We have yet to use $6K per year on repairs as we figured out how to insure major repairs (and, no, it’s not a home warranty).

Current “value” is subjective but it should sell for about $260K more than I paid for it at the low end. If it falls 50%, I’m close to a break even. What I didn’t pay in “rent” will cover the delta.

You can’t rent this house for $2,200 a month. It’s more like $3,600. If one were to do seasonal, it would be $6,000 per month for 6-7 months. (I don’t consider the sinking fund in the rent equivalent because it’s not a fixed expense – and we still have most of it earning 5%)

So, simple math… my rent is -$1,400 a month less than it would be, plus I have a potential for a $200K+ appreciation (which you can’t get from rent receipts), my “lost opportunity” is factored in.

Don’t pay your rent vs taxes? You’re out in the street as well. Stupid argument.

We did the same for our daughter years ago during the last meltdown. Helped her get into a house in 2010… she carried it. Her cost to own was $1,400 a month vs. her smaller nearby apartment that was $2,300 a month. Her costs didn’t move much over the 6 years thanks to Prop 13. She sold it for a $260K profit net 6 years later (and not at the peak).

Amortization schedule? Hahahaha! Shows how financially naive you are. Do you know how to impact an amortization schedule? Make one extra payment per year against principal and cut your term and interest paid. Get a big bonus? Forego the bass boat and pay down your principal. Can’t do that with rent.

Worried about your life changing? You have an asset to sell. If you life changes in a rental there may be notice requirements in your lease and they’ll eat your damage deposit and last month’s rent plus other potential penalties. A loss is a loss, no matter how you sugar coat it.

In a sane world one buys a house to live in. Not study Zillow or Redfin daily to watch the house lottery winnings (or losses).

Lastly… over the past several decades (and likely centuries) common people amassed wealth through property ownership. Yes, some lost their undies by being stupid, but the same stupid can be found among those who bought Louis Vuitton handbags, $100K pick-em-ups, or an RV. My grandparents left their house to their kids…. they split up the proceeds. Paid for my university degrees. My Mom lived off her sale-of-home proceeds in her last years. Both were owned outright (of course sans tax liability – duh). You’ll never own your apartment and your AMC meme stock might be worth bupkus.

When money/credit can be conjured/counterfeited at will, then all asset prices are illusory.

The carrot in front of this mule is withering and rotting. Somewhere, somehow, someone is going to have to feed and water the Old Girl.

I think we will know the answer long before $40 Trillion and 10% interest costs.

FWIW, Covid “Savings/Assets” on the left hand side of the National Balance Sheet conveniently ignored the Liability/Debt on the right hand side.

Katz, you never own your house or your barn, even if you say you “own it outright”. You always pay property taxes, although a lot less than a rent equivalent, but with a big upfront cost to get that lower monthly payment. If you get lucky, your home might appreciate, if you bought at the “wrong” time, you could be underwater. Buying a house is a lot trickier than most people think. Basically I agree with all your points.

I agree with your insight into homeownership, Dick. In rural Northern California where I live people are struggling to make ends meet, whether rent payments or home payments. The second especially when the cost of fire insurance can hit $8K/year. To me, Wolf occupies a rarified world of big data that belies, as in damn lies, the living experience in the rural community I call home.

I’m from Europe and I’m flabbergasted by the way everything is borrowed (at least it seems that way) in the US.

A mortgage for a house I can understand…but paying $1000/month on a car, I just can’t even fathom. Maybe it’s because I was raised differently with ‘if you want something, save up for it’. Kind of the opposite of instant gratification.

This era of central banker fraud has now put everything in hyperdrive, it seems. From my outsider perspective, it seems that money has become the single greatest contributer to inequality. All these bubbles, these manias, the societal breakdowns…these are symptoms of a sick society.

But, things aren’t great in Europe either.

Because this system is so broken, so hopelessly corrupt, even after 15 years of saving, I can’t even come close to affording a home in my area. Prices have increased by 75% in just 4 years.

Or should I say, the currency has devalued by 75%?

And my savings are yielding between 0,01% and if I take a 12 month CD, 0,70% after taxes. I have no desire to risk what little I have on the stockmarket and I have no access to government bonds. It wouldn’t make much sense either, since the commissions through brokers are too damn high anyway. The whole thing is ridiculous.

Meanwhile the banks charges 22% on creditcards, 11,5% on personal loans and close to 5,5% for mortgages. Obviously the ECB isn’t even close to being done, so these mortgagerates will move higher still.

Despite being in recession, prices aren’t dropping one bit.

I’m in Ireland and there’s a shortage of 150.000 to 200.000 houses easily. And keep in mind, the population is at 5 million. That’s a staggering number.

I was wondering if you had thoughts on this, Wolf?

Thank you.

Harry,

Thank you for your comment. I think we all need a reminder that things aren’t hunky-dory everywhere ELSE.

As to paying $1000 a month for a car… it really isn’t the financing that is the problem. Like any asset, as long as a car will last ten years there is not much of a problem financing it for ten years… and in America new cars tend to last twelve years while the financing of a new vehicle is usually for six years or less.

The REAL problem is that we Americans overpay for cars. We don’t view them as simple transportation tools. Instead, we spend so much time in them that we want them to have every amenity imaginable. It is not enough that they have an AM/FM radio… they have to have a combination Satellite Radio/Bluetooth Dock… with Bose-quality speakers no less. And that is just the “sound system”… it is not uncommon for them to now have heated seats with inflatable Lumbar support backrests. Separate video systems for every seat except the driver’s seat.

I am not making any of that up… rather mediocre American cars today have more and pricier amenities available than you could have gotten in anything but a Rolls Royce twenty-five years ago.

My observations jive with your numbers. I’m 65 and grew up in a factory town. Today’s world is very different than when I was young. Many more restaurants, casinos, overpriced cars, over 2000 sq ft homes, etc. All the way down to pure bred dogs and body art. You need a broadly significantly wealthy populace to support all that.

If all they build are 2000 to 4000 ft² homes thats what gets bought.

Condos, townhomes exist.

But can’t buy a 1000 ft² home unless its pretty old… likely 60 years or older.

Even in the 80s it was hard to find a new home 1100 ft. At least in cities around Dallas where I then lived.

I wish you could see all the neighborhoods in my (quite wealthy overall) city, that has multigenerational OWNED homes, many including aunts, uncles and cousins. Mobile homes parked in back, no cars in garage…PEOPLE live there. All contribute what they can, from granny’s SSC to several Jack in the Box workers, uber drivers, back yard mechanics, etc, etc. Hell, in those areas we even have bicycling street vendors plus trucks.

This has happened before……the Gilded Age, the roaring 20’s….quite a few drunken sailors then, too.

“65% of households are homeowners, which tells you something, given how home prices have shot up”

In other words, all is fantastic? 50% are “loaded” with wealth?

Let the stock market experience a 2008 style crash and let home prices collapse and lets see who is “loaded” with wealth

Not to mention prices on everything are going through the roof on everything.

Not everyone lives in San Francisco, New York etc.

I live in the Bay Area and am well into the bottom 50%, perhaps even Wolf’s notion of the bottom 30%. While I agree with everything you said, PLEASE do not HELP the Plutocrats create a totally divided country and simply take over, and then run their puppet government as they see fit. There is still some small chance of making democracy work….VERY SMALL…..but don’t HELP them hate other citizens simply because of where they LIVE.

They need a “common enemy” to pull this off, as has been known by all of those who want to be at the very top since civilization began. And 51% common enemies is enough under this noble democratic effort of ours.

DON’T let ABE LINCOLN or my dead friends down any further….PLEASE!!!!

Wolf, like you said a long time ago, you wanted a site that collected SMART people. You have DONE it, regulars and readers.

Please listen to them (yes, as always I know this is YOUR site 100%) You can’t keep it to only MBA Econ talk…..not in these troubled times.

I may be up past mid nite reading these comments, it’s that informative…and….yep, it IS Sociology.

Also – Fidelity has said they have a record number of 410k millionaires. They also said that average 401k account was putting away over 7.5% of their paychecks into their 401k retirement and even increased their 40k1 savings rate during the 2022 stock market downturn. The downturn did not phase them.

1) By “wealth” do you mean the value of residential real estate? Because what we should have learned from the last time people were this “wealthy”, was that it ended ugly, and rather precipitously.

2) “The top 10% owns most of the financial assets while the bottom 90% has more of their net worth tied up in real estate.”

3) “The top 10% holds 70% of the net worth in this country while the bottom 90% accounts for 75% of the debt.”…. In other words, the bottom 90% are relatively leveraged because their debt levels are 2.5 times their net worth levels. Whereas the top 10% debt levels are less than 1 times their net worth.

4) Here is some perspective about the current situation:

The last business cycle time period when the savings rate was this low corresponded with the peak of residential real estate values in 2005/2006… prices then started to roll over, and delinquencies were already soaring in late 2007, many months before the GFC event in Sept of 2008.

======================

Conclusions:

1) “When people are leveraged, “wealth” can disappear very rapidly.

2) When the savings rate is this low, what typically happens next is a rapid rise in the savings rate.

Bottom line:

Focusing on what happened last month or this month does not help one to understand what will happen next.

Wolf, I’m confused. This article seems to contradict what I’ve been reading and hearing elsewhere.

From this article from the SF Fed: Aggregate savings peaked at $2.1 trillion in August 2021. As of June, the San Francisco Fed estimated that aggregate savings had dropped to $190 billion.

https://www.frbsf.org/our-district/about/sf-fed-blog/excess-no-more-dwindling-pandemic-savings/

I can’t figure this economy out. Every bit of macro news I see is horrible with the exceptions of NVDA (which I’m convinced is a fraud) and ANF. Yet, the shopping centers and restaurants are still packed. I go to Home Depot, it’s completely packed but they are issuing bad guidance. Nothing makes sense to me…

This is the biggest braindead bullshit ever. Everyone knows this. Only pure morons don’t, including those that spread it. Consumers have something like tens of trillions in financial assets, including $10 trillion in bank savings and $5 trillion in money market funds that are liquid. And they continue to SAVE, even in July, to add on top of their pile of assets. Running out of savings? My ass.

You fell for some moronic BS produced some moronic academics that put in their one-year stint at the SF Fed to write papers and stuff their resumes.

Top 50 percent of USA are loaded in wealth? I guess I’m blind because our monetary policies may have had sense but in the last 30 years with the last decade being extremely irresponsible and it’s the majority that pay who least deserve it. They should gamble on their own dime

Oh oh, I know this one. Joe Sixpack is standing in line for Tesla Cybertruck.

Wrong, we went for a Nissan.

I got a Toyota

Yes, most of the savings accrue to the top. Same as it’s ever been for the most part.

cb:

Nonsense. The “top” isn’t even included here because they make most or all of their income from capital gains, and capital gains are not included here.

The 1% make nearly all of their income from capital gains! Musk’s and Buffett’s income and wealth is entirely from capital gains. So their income isn’t included here.

The income data here doesn’t include capital gains (from stocks, home sales, etc.), and doesn’t include the income from stock-based compensation plans, such as stock options, that are widely available to tens of millions of employees. This is how wealthy people – yes, millennials, LOL – make a big part of their money, and it’s not included in income here. So the income figures here understate the actual income. These people can save the stock-based income and spend all their wages, and still increase their wealth in leaps and bounds, and that’s fairly common.

The fact that capital gains and stock based compensation are not included in this income data, leans to making my assertion even truer.

Of how much use is income data without the consideration of capital gains and stock based compensation? Capital gains are income.

The fact that the 1% makes most of their income from capital gains just points to widens the wealth gap.

Nobody argues about the wealth gap. What’s import to understand is that a huge number of Americans have lots of wealth and money, even if their net worth of $700k or whatever is minuscule compared to the 1%. And the income of the top, as I pointed out, is not included here. This is the income of people who work for a living and make money off rentals, farms, small businesses, interest income, dividends, etc.

@ Wolf –

Don’t the 1% make a tremendous amount of money off of interest and dividends? Is that included in your income numbers?

Sure they make some, but that’s not how they got their wealth!! Buffett and Musk didn’t get their wealth from interest and dividends.

Also, if the income is to a corporate entity, it’s counted as corporate income and is not included here. I don’t think Buffett has a lot of personal cash in T-bills, it’s through his holding company.

If they earn personal interest income and dividends, it’s included here.

@ Wolf –

Thanks. Clarifying.

Wolf said: “Also, if the income is to a corporate entity, it’s counted as corporate income and is not included here.”

————————————-

There are a great number of small businessmen operating under an LLC in this country. Think small contractors, for one. They do a ton of spending under their LLCs which I suspect are largely personal spending, such as $100,000 pick-up trucks, entertainment, sponsoring local activities ‘for advertising’, etc.

Are these this LLC expenditures called out as part of consumer spending?

Is LLC income treated as personal income?

I’m a mental health therapist and the fear of a climate catastrophe coupled with coming out of covid lockdowns has ppl living as if it’s their last day. Then add Americans difficulty with managing finances . I see this with many of my clients. I’ve never seen it so bad. Ppl feel as if they have a limited future and we’re at the point of no return. Why not spend? is the thinking process.

Very insightful. I see a lot fatalism in my travels, too. And…they’re not wrong to feel that way.

So what do you tell those clients that feel hopeless?

Personally, I’d tell them to turn off the teevee, put down the smart phone, stop following “influencers” that make them feel inferior, possibly look at what they do have and the opportunities that avail them, and how to capitalize on that, rather than falling down a rat hole.

My daughter has a male friend that had marginal parents (they never grew up) and never taught him life skills. Interviewing, how to save and invest, why you buy quality that lasts a lifetime rather than junk that you replace every year. The poor guy had the most ill fitting clothing and, despite his experience in bio-tech, skill sets, education, etc., was never considered for advancement.

I bought him a proper suit, had a few shirts custom tailored for him (he’s a large man, not fat… just large… hand like hams), showed him how to tie a silk necktie appropriately scaled to his chest, select proper dress socks and shoes, so he didn’t look like he just fell off a pumpkin truck. Daughter helped him reconstruct his resume and then found a consultant who worked with him on further tuning the resume and interviewing skills. It appears he just landed a job in LA at LA pay.

These folks need to establish goals and find a mentor to guide them…. Deciding that life is all about YOLO in their 30’s might yield a bad outcome when they hit 50’s and beyond as it’s unlikely that the world is going to end.

Katz — The bootstrap pep talk jazz only has so much traction — until it doesn’t. The traumas and turmoils which converge upon the human psyche are not as prosaic a matter as you suggest, and everyone copes with their trek through the shitheap in their own way. I’m glad your coin landed on the side it did. Don’t believe for a second you’re not lucky.

By the way — the fact is, you really do only live once. So what’re you saving it for? Go tour a convalescent home or an ICU…it’s a compelling ass’d argument to dip your bread in that gravy while it’s still hot.

ElK/bul/VT – consideration of the long, subliminal tail of existential fear baked into the ‘duck and cover’ (and that threat still extant along with more recent ones) generation may be worthy of inclusion in the YOLO discussion. As does what makes one wander into forms of apparent catatonia over agency…

may we all find a better day.

Bulfish, obviously, you’re saving for your kids and grandkids. Who else would you be saving for?

To hire El Katz as a Success Consultant for all of them? Guy that damned good isn’t cheap, ya know? Silk ties are hard to tie…hell he can probably tie Macaroni!

Total first impression ace!

Another thing to consider is with less younger couples having children, how you think about money, who you spend it on (yourself), and retirement all changes when you plan to not have a child. It’s not the blueprint laid out in the generations before.

91B20 1stCav (AUS) — perfectly put.

Anyone living with paralyzing fear of a “climate catastrophe” is in need of a little education about what climate change actually entails, the human race is about 1,000 times as likely to destroy itself with war than for a 1 or 2 degree change in temperature over 50 years to have any meaningful impact on a person’s life.

Very good Dr Happy1. What right wing think tank do you work in? Oh, and your data please, I’m sure it’s no trouble for you…… inquiring minds want to know.

One of the most interesting things I’ve seen is the staggering amount of recent fiction being produced around the theme of “the world is ending”.

The Witcher and Ragnarok on Netflix are great examples of this.

I don’t think it’s a coincidence, but rather good artists are picking up on the zeitgeist. There’s definitely something ominous in the air and people are absolutely living as if it’s the end times.

“and people are absolutely living as if it’s the end times.”

No they’re not. They’re still saving money. They’re making a lot, and they’re spending a lot, and they’re stills saving some portion of their income to build wealth for the future they believe in. Read the article.

And that doesn’t even include capital gains, such as stock-based compensation, and capital gains in brokerage accounts, 401ks, etc.

Hopefully you’re doing your job of helping them out of that fatalistic, dysfunctional mindset and restoring them to be mentally healthy and productive people.

“Consumers” lumped into one giant homogenous pot. If the bottom 50% owns so little compared to the rest, does it mean the numbers are skewed heavily toward the top?

The top 50% of households are loaded with wealth. Even the next 20% are doing pretty good. It’s the bottom 30% that is always squeezed.

65% of households are homeowners, which tells you something, given how home prices have shot up.

Do the stats even exist breaking it down by bracket? Is it in the raw data?

Wealth (assets minus debts) per household:

In bold is the top 50% of US households:

“Top “0.1%”: $133.8 million

“Remaining 1%”: $19.8 million

The 2% to 10%: $4.4 million

“Next 40%”: $768,000

Even the “Bottom 50%”: $69,100

https://wolfstreet.com/2022/09/26/my-wealth-disparity-monitor-september-update-qt-rate-hikes-dropping-stocks-bonds-reduce-outrageous-us-wealth-disparity/

People need to quit posting this BS about Americans being poor, and that only the 1% have money. It’s just braindead BS. I’m sick of it. People who believe this BS will NEVER understand the US economy and will come up with BS conspiracy theories when consumer spending is strong.

The wealth disparity is huge, and that’s a problem, but there are still lots of people who are very well off, including lots of people who read this site.

According to a recent US Census Bureau’s household wealth report published in June 2023,

Percentile 2021 dollars

10th . . . . . . . . . . . . . $0

25th . . . . . . . . . . . . . $16,560

50th . . . . . . . . . . . . . $166,900

75th . . . . . . . . . . . . . $604,900

90th . . . . . . . . . . . . . $1,623,000

https://www.census.gov/content/dam/Census/library/publications/2023/demo/p70br-183.pdf

Wolf,

768k for 50 to 90%.

Most of these folks own a home.

If someone has 10% equity on a 500k home does their assets include 50k or 500k ? Obviously it should be 50k but just wondering if that is indeed the

case ?

Where is this spelled out ?

Federal Reserve data, which I covered here:

https://wolfstreet.com/2022/12/21/fed-tightening-reduces-horrendous-wealth-disparity-that-qe-and-interest-rate-repression-have-wrought-fed-data/

“768k for 50 to 90%.”

I cited “wealth” = net worth = assets minus liabilities.

$50k in home equity (10% of $500K) adds $50k to wealth.

…for ‘Murica, perhaps a reprise of the late film director Mike Todd’s observation on personal worldview:

“…I’ve been broke plenty of times, but I’ve never been poor…”.

may we all find a better day.

“which is an indictment of the wealth distribution in America”

I agree, “indictment”, as in requiring legal action right now.

Add climate change and it becomes 50 years ago….

…..but it ain’t over til it’s completely ignored by all.

I hear you, Wolf. I employ about 300 “Joe Sixpacks”, and the construction site lots today are full of high-end HD trucks hitched to boats, UTVs, etc. all ready to head their northwoods cabins for a long holiday weekend. I’d also bet the only item of debt is the vacation home, not the toys. My motorcycle dealership is also one of the largest UTV dealers in the state, and he told me the number of people NOT financing is killing him, as financing is a major source of revenue for him. I’m sure this varies regionally, but our neck of the woods is doing just fine.

Joe six pack has joined the sailors in the good times. We should print another 10 trillion and hand it out then we can all be even better off.

Don’t toss me into the pool but I think we as a country owe 33 trillion dollars, or is this nothing to worry about, just some silly numbers.

DD,

And that is one TOTAL success “story” out of what town? Powerful Union!!!!….or are you just extra generous and losing some family dynasty money?

Why do we always bother discussing “wealth” or net worth relative to spending? They just aren’t one-in-the-same. So 65% (ish) are homeowners, and 61% (again, ish) of Americans own stocks. The problem is that nearly 90% of stocks are held by the top 10%, and their wealth tied up in real estate is less than 20% through the top 10%. 10-50%ers, that jumps to 35% or so, bottom 50%ers it’s at least half of their wealth. The majority don’t have liquid assets. We can argue on net worth, but the bottom line is if that segment doesn’t keep up wage-wise, they’re screwed. On top of which, where do we think the majority of non-favorable debt lands? Guessing not with the top 10%. It’s the haves and have nots, the top will consistently spend like drunken sailors, while the rest spend just to try to live.

People need to quit confusing “wealth inequality” (which is huge in the US) with “Most Americans are poor and tapped out” which is bullshit.

The 50% to 90% of Americans have from large to huge amounts of money. See my numbers in bold above.

Even the upper portion of the bottom 50% have quite a bit.

I’m so sick of this constant Americans-are-poor bullshit. It belies the US economy. I’m going to mass-delete this BS. I’m tired of people abusing my website to spread this BS.

@ Wolf,

“I’m so sick of this constant Americans-are-poor bullshit. It belies the US economy. I’m going to mass-delete this BS. I’m tired of people abusing my website to spread this BS.”

There are many on this site, from regulars to drive-by trolls, who make a lot of unfounded and unsubstantiated assumptions about everyone else’s finances. They should take that “Americans are all broke” crap to Z*r**h*dge, where the US consumer has been 30 days from mass bankruptcy for a rolling…3000 days.

Amoung other careers, I used to “sell” reverse mortgages. Talking with old (I mean OLD) folks, many were literally eating cat food, although they had houses mortgage free. Showing them how they could enjoy a better life and not make payments (A)until the house was sold, or (B) until they passed away, almost all said they wanted to leave something for the kids.

Wolf ,

You are sounding like a cheerleader to me.

American homeownership rate has been between 61 and 69 percent for a very long time.

With home prices going up up and away you’d think it might have reached 75% by now … humans tend to be momentum driven.

Its not even 70%.

But about 50 other countries have over 65%

homeownership rates. Wikipedia has a list.

You’ll find the US in the middle to the bottom.

There are lots of “renters of choice,” people with plenty of money who don’t want the hassles of homeownership and who want or need the flexibility of renting. Those monthly rents are fairly high. Everything that has been getting built over the past decade has been higher-end, marketed to renters of choice. Some of these apartments are $20k a month in Manhattan. $6k a month rents a nice 2-BR in San Francisco. SFH too. If you want something really fancy, you go higher. People who rent these have plenty of money, and it’s a huge market, and it has attracted a huge amount of investment. Americans are very mobile, we move all the time. There is nothing wrong with renting.

BTW, Germany has a much smaller homeownership rate than the US. It’s not good or bad. People need to get off this BS.

Yeah, Wolf is sounding like a total cheerleader lately with this everybody is rich with money coming out of their ears, spending like drunken sailors thing.

I’m not buying it. If it were true, then that would mean the FED and .gov actually found the magic money tree and can just print prosperity. Doesn’t add up.

Just as Wolf is sick of the”everybody’s poor” thing, I am nauseated with the “everybody is rich” thing.

“the “everybody is rich” thing.”

Nobody here said that, other than you.

A lot of this “wealth” is unrealized based on inflated valuations in real estate or equities. When a normalization event occurs much of this “wealth” may suddenly evaporate. I think this is the issue causing confusion regarding the wealth gap.

All the incessant chatter on CNBC et al about Federal Reserve pivoting & imminent rate cuts etc is just insane at this stage.

There’s been a lot of progress made in lowering inflation. Skipping rate increases at upcoming meetings so long as inflation doesn’t reaccelerate? Sure. But cutting rates in this economy?

Every time data comes in hot, the markets simply price out rate cuts by another month, then continue rallying. They don’t care anymore.

America is a different world than Canada.

In Canada, TikTok is promoting “Canada job fair long lines” in Toronto, Brampton, KW, etc.

Canadian bank stonks are holding at least 40% of mortgages with over 30 year amortizations.

Canada is considering a student visa cap, because Canadians are complaining that their teen can’t get hired anymore to work summers at fast food joints.

Recently, I’ve discovered that the job agencies want to pay minimum wage C$15.50 for a Bachelor’s Degree holder who is fluent in Python and financial analyst software. Meanwhile in Seattle, a similar job goes for US$150,000 a year with Amazon or Microsoft.

The average bachelor’s degree holder who can code in Python isn’t getting a $150k/yr offer from Amazon & MS. Those are for top tier candidates.

I guess “top tier” may mean different things, but “levels dot fyi” website suggests that Amazon L4 software engineer gets ~$170k total comp, and L4 seems to be the lowest tier that website is tracking.

“L4 is a software engineer in the greater market, someone who usually has between __one to three years of industry experience__. In this level you will be responsible for some component work, you may improve features in tools & are responsible for solving problems across products.”

1-3 years is basically a fresh grad.

I guess I should apply to Amazon then…

that website looks like bs to me. been in the industry decades.

@Dick Levels FYI is the premier site for salary tracking. It’s self-reported, so it does tend to skew high, but it’s definitely in the ballpark. If you’ve been “in the industry for decades” and you’re just learning about Levels FYI, then I’m not surprised that you feel underpaid, because you’re definitely not using the tools available to negotiate your comp upwards.

American companies are offering internships & jobs to Canadian comp. sci and data analyst grads. I’ve gotten the website from a friend. Data Analyst jobs with a knowledge of programming and financial software pay a premium in Amazon.

Meanwhile, Toronto employers want to pay third world sweatshop pennies while demanding Manhattan elite lawyer rents.

At a job interview, the interviewer who couldn’t really speak English properly asked me if I knew how to conduct automation and advanced programming in various software, including Excel. I said yes, but that requires a higher salary than C$14.25 at the time (minimum wage).

When the interview was over, the company immediately rejected me. Toronto wants wage serfs.

So I gather that you have a CS degree from University of Toronto with experience, but can only find a $10.49 USD sweat shop job hacking out code, still get rejected, still unemployed, while blaming illegal student immigrants who can’t speak English properly taking your job.

But the fools at the FAANG/MAMAA and fintech would hire you if you were a US citizen for your

Gen Z skillz for at least $150K.

As a manager in big tech – I can confirm that levels fyi is very accurate. There is a giant gap in pay between the Faang companies and all others. For example – my brother has an identical role to mine in a lower tier old school software company. I literally make 5x what he does

Jason, this is most likely correct.

My previous job in a non-IT company in an IT role in a “bad” region only brought me ~60k salary. I know first hand that folks with “decades of experience” there were making 90-100k tops.

Moving to a “good” region (similar COL, but abuntant jobs) bumped me to ~120k almost overnight. My friend in one of FAANG companies is making at least twice than that, so I can totally believe that the gap “FAANG vs IT jobs in “bad” regions” may easily be 4-5x.

We have UPS drivers making $170K in salary + benefits. And they don’t even speak Python.

I keep reading stories about pythons in Florida. Is Florida Man making $170K now?

Florida Man has moved into selling homeowner’s insurance policies since speaking Python requires more than 12 words. A lot more money in insurance in Florida.

As someone who spent 15y doing interviews for Google and those high-paying jobs you descibe, “a Bachelor’s Degree holder who is fluent in Python” means next to nothing. In all honesty, it’ll probably be a weak candidate.

Doesn’t mean that someone who took on student loan debt to study STEM and data analysis should be paid Canadian minimum wage.

Might it be a supply and demand issue? Maybe there’s too many graduates for the market to absorb, so they feel they can pay peanuts.

“Should”???

People get paid, generally, the market value of what they contribute. A degree may make you able to contribute more by making you more caoable but having a degree in itself isn’t worth anything directly to an employer.

And suggesting that someone should be paid more because the have more debt? Sounds like, “To each according to their need.”

ElK/Brian – good responses to whiffs of inherent entitlement, class-ism and disrespect for certain types of actual labor performed by ones fellows…(one result of the conversion of institutes of higher learning from places of learning and improving the individual’s ability to think, to one of too-often selling an illusion of getting your ‘success’ ticket punched in exchange for ever-heftier fees…).

may we all find a better day.

may we all find a better day.

The average American consumer is pretty much illiterate on the economy. Something like 60%+ thinks we’re currently in a recession, which is far from the truth. Then they tell pollsters they’re getting squeezed by inflation (which may be true) & are cutting back on spending as a result, then go and spend like drunken sailors regardless.

Just look at the holidays. Last year (2022) had 8% inflation, and many poll respondents said they would spend less on holiday shopping vs. the previous year. Instead, Black Friday had lines around the block (tend to be lower income shoppers.) There were lines around the block for the new iPhone (higher income.) The National Retail Federation said both nominal & inflation-adjusted holiday spending jumped to a record high.

“Something like 60%+ thinks we’re currently in a recession,”

Most people cannot even define a recession.

Oh, oh, I can define a recession! It’s two consecutive quarters….never mind. ;-)

The US has used the SAME definition of a recession for longer than I have been alive, and you’re engaging in ignorant-BS-mongering.

The NBER, which calls out recessions, has defined a recession as a broad-based decline of the economy, including the labor market. It doesn’t even have to be 2 quarters. The last one was shorter. That has been the same for many decades. If you look at past recessions, everyone had a decline in the labor market, sharply higher unemployment rates, and sharply higher unemployment insurance claims. You cannot have a recession with a booming labor market. And people have been spreading ignorant BS about this.

Even if we have a recession, they usually only last 2 or 3 quarters on average. Once we are in an official recession the FED freaks out and becomes very accommodative. From what I can tell over my investing history, the moment you hear the words ” we are in a recession from the FED” …..buy stocks because they are about to juice the economy. LOL

…I recall an older saying: “…a recession’s when your neighbor’s out of work. A depression is when YOU’RE out of work…”.

may we all find a better day.

Jackson,

I’m one of those that complains about the cost of living and then goes out and spends like a drunken sailor. This is why, my tv broke, my washer broke, and the car needed expensive repairs. So now I have a new tv, new washer/dryer set, and a new car. The appliances are paid for and the new car has 25% equity because we got a good deal on the trade in. You can guess where all our extra money will go from now on.

LOL… I feel your pain. I have a 21 year old dishwasher that needs the spring in the door replaced. Probably a $80 fix for a service guy and a $15 fix if I do it myself. Still, last week I caught myself looking at the prices of NEW dishwashers.

Ha! Trouble is that our 21 y/o DW could be repaired for $400, no guarantee that something else wouldn’t go south. New ones are built for the landfill economy. Very cheap crap designed to fail in 5 years. No spare parts will be made. Part of re-shoring and retooling the economy needs to be a return to quality manufacturing. Our fridge is GE again a replacement of a 19 yo model. made in KY, but obviously not solid as the old one. I guess I’m a codger, talking about the good ‘ol days. Not MAGA, but manufacturing of durable goods has cheapened to the last widget by the bean counters.

SG, et alia on here:

THE reason to buy a new generation DW is NOT the cost of repair, it’s the cost of the clear energy excess between the old and the new.

We are continuing to examine closely the cost differential between even 8 y.o. appliances, including AC ( a biggie$$$), as well as others such as DW, dryer, etc…

Savings of energy alone, without regard for delta for repairs,,, for the updated frequently pay off within 2,,, repeat TWO years.

Folks on here IMO are not only sufficient in math, but can ””’probably”” figure this out for ”their” selves AND their family, though many family in my experience ”don’t want to be bothered” with net savings, sometimes even in spite of limited income…

Thanks again WR for the clear and clearly updated information.

VintageVNvet…

It is almost pathetic listening to you criticize other people’s math skills. NO… the payback period for a new dishwasher isn’t “TWO YEARS.” According the Department of Energy when they instituted the new dishwasher standards in 2012… “estimates a median payback period of 11.8 years for a new dishwasher.”

“Median”… THAT assumes you fit their prototypical American family of 4 to 5 people in a household running the dishwasher on a nearly daily basis… a description that I would wager most of Wolf’s reader’s households do not fit. I only run mine twice a week or so.

A dishwasher is not like an air conditioner where new chemicals and technologies means that there is a quick payback for investing in a newer model. At the end of the day a dishwasher is like a hot water heater… you add water and heat (and in the case of the dishwasher you spin the water around). There are not a lot of ways to massively increase the efficiency of that process.

There are bigger fish to fry with energy conservation in U.S. homes than with a dishwasher that runs occasionally and is not a big power draw. The biggies, for starters, are adding insulation and tightening up the air losses in a home. Once that’s done, look at A/C and refrigeration efficiencies.

SpencerG,

I don’t think VVNvet’s comment criticizes the math skills of people on this site. I think you misread it. His comment also discussed energy savings from newer appliances generally, and though he mentions dishwashers, it is not clear the 2-year payback period he mentions applies specifically to that appliance. I’m not sure to what degree he is correct about the 2-year period generally, but it may apply to me since electricity is expensive in CA. I will probably take his advice to do the math for myself.

Sealing up an older home and adding insulation without evaluating the entire structure is a recipe for disaster. Trapped moisture, inadequate ventilation, lack of air exchange, improper venting, can lead to a lot more expense and heartache than the $50 a month you’ll save on climate control.

Houses are systems…. and everything needs to be reviewed – even the simple things (Like where does your over the range vent get it’s make up air? Your fireplace flue or your gas furnace/hot water heater flue? ) need to be considered.

Replacing the door spring on a dishwasher is child’s play. It’s usually the “string” that controls the counterbalance spring that snaps. Kitchenaid’s are notorious for that (Kenmore Elite, higher end Whirlpools are all the same machine with different stickers).

RojoGrande…

I suspect you are right… I am being too harsh on him. I think he copied and pasted something in there so it was hard to see where his own thoughts started and ended.

But I do get annoyed with people assuming they know more about a situation than the person who is actually living with it. It is one thing to offer a different perspective (“have you considered what the payback period will be for the new one… newer appliances are more energy efficient than older ones”)…

but to just arbitrarily say “THE reason to buy a new generation DW is NOT the cost of repair, it’s the cost of the clear energy excess between the old and the new. … those are words not likely to be deemed helpful by most competent adults.

In my case the concern isn’t electricity costs or payback periods but rather how much longer I can expect the plastic drum inside the dishwasher to last… plastic gets brittle with age. I have already replaced the lower dishrack due to rust.

The simple truth is that I actually LIKE this dishwasher. It is quiet but not too quiet (I can hear when the cycle ends). It is pretty fast compared to modern dishwashers (the new government standards make the new ones take longer to wash the dishes). Clearly it is well made if it has lasted this long. Etc.

AND YET… I caught myself looking at new ones last week… “just becuz…”

LOL…

In Canada at least in Nova Scotia Heat pumps are really popular. We have had one for 10 years and they save a bunch of money. My seasonal neighbor from the states says ” the people in my area dont have heat pumps ” then he goes on to tell me that his electric bill is 400 a month without burning wood and the window air conditioner is too heavy to install. the guy is a millionaire. jeez . The two great inventions that will save Americans money but few will even consider them are heat pumps and Bidets. Cut your heat bill and drastically reduce the amount of toilet paper you have to buy. No thanks that would be un American.

Weed and hookers?

Re “Something like 60%+ thinks we’re currently in a recession, which is far from the truth.”

The classic line: “It’s a recession when your friend loses their job. It’s a depression when you lose your own job.”

Updated for Stagflation: “It’s a recession when your friend can’t pay their inflating bills. It’s a depression when you can’t pay yours.”

Methinks that a lot of Wolf’s “Drunken Sailors” are actually having such “personal recessions”, being forced to spend more and more to get less and less, and resent inflation that the believe benefits others at their expense.

“being forced to spend more and more to get less and less,”

The income and spending figures in the article — and in all the charts — are adjusted for inflation. Consumers are outspending inflation by a good margin, and they’re still saving money.

Then that means the FED should do more QE, and the government should keep spending and handing out free money and all that. I mean, look how great it turned out, with everybody all rich and saving more than they’re spending with all this inflation and stuff.

BTW, if things are so rosy, why is there even any talk or worry of inflation? I mean, everybody is just outearning and outspending it.

Powell should definitely pause at this point. Or better yet, cut. If he cuts rates and restarts QE, people will have even more money. And he should definitely start buying even more MBS, because all of those cashed up homeowners you speak of will have even more dough.

Inflation is tax on everyone, including asset holders, high-income people, and low-income people, and everyone in between. A small tax can be digested. If that tax gets big, it’s very disruptive to the economy.

Lower-income people have a huge problem when big inflation hits the basics (housing, food, gasoline, etc.), where prices can spike, esp fuel, and far outrun even strong income gains. That’s a specific issue that Powell keeps pointing out as well.

You’re twisting things around.

Wolf-

“ Consumers are outspending inflation by a good margin, and they’re still saving money. “

If consumers are spending and saving more, would it be correct to assume that employers are paying more?

If yes, what is the impact on corporate earnings? Does a continuation in that respect lead to an “earnings recession” at some point?

And if that’s true (asking, not saying it is…), does an “earnings recession” lead eventually to the uncomfortable season of job losses?

Yes, wage pressures on corporate earnings are a thing. Wall Street analysts have already been talking about it. The union deals are pretty clear, and the companies are named. It’s harder to see with other companies where wage increases happen on the quiet.

The FED destroyed pricing. They printed too much and overheated the economy, blowing bubbles in everything – The Everything Bubble – and they don’t want to pop it. So, it’s just raging away, doing incredible structural damage everywhere.

“Everywhere” including the rest of the Planet where economies are falling down Like dominos because they are basically giving away their stuff for free if they trade in Dollars (which most of them still do). Even Saudi-Arabia is in recession now, believe it or Not.

DC-

More like a stampede than a bubble, I think.

The central planners are unhappy with the direction and want to head off the cattle, but they will be equally unhappy if they merely change the direction of the raging pack.

That’s the never-ending loop when central banks are charged with controlling the direction of the economy.

Last point, letting market sort out it’s own direction without central bank intervention (as it did in 1921) also involves stampeding cattle, but they calm down much faster.

P.S. – If interested in learning about the impossible cross-purposes of the Fed, spend a hour digesting this excellent 1979 summary by Arthur Burns: The Anguish of Central Banking

https://fraser.stlouisfed.org/files/docs/publications/FRB/pages/1985-1989/32252_1985-1989.pdf

nice analogies jh::: please continue.

Within the WOLF’s guidelines for HIS site,,, far damn shore,,,???

(((Q marks because IMHO we need a ”definitions and acronyms page on WS)))

thank you

Thank you VVNvet-

And a sincere thank you to you and your buddies for your service to our country.

John H. – I take the kind intent of ‘your buddies’, but would much prefer ‘our fellow citizens’ (…and thank YOU for any efforts you have doubtless made-not necessarily military-in aiding our common weal…).

may we all find a better day.

It all comes down to, inflate or die!

Consumers spent 97% of what they earned.

$706 billion in “savings” is just 3.1% out of the $22.87 trillion they earned: 0.706/22.87.

This is less than the 3.5% personal savings rate reported from the July data.

This represents the philosophy best embodied in Isaiah’s words: “Let us eat and drink, for tomorrow we die.”

What’s your problem??? The BS statement circulating is that these tapped-out consumers have to borrow to spend. I shot that BS down by telling you that the savings rate shows that they don’t borrow to spend. They earn more than they spend. And they save. Is that so hard to grasp?

Wolf—No offense intended. I’m not saying these consumers are borrowing. I’m saying they are spending almost every dollar they have instead of saving.

Three percent savings rate is abysmal. It means they are barely saving anything at all. It’s a habit of present orientation, not future orientation.

If they were saving 10 or 15 or 20 percent, prices would decline. And so would interest rates.

It’s not abysmal. The income data here doesn’t include capital gains (from stocks, home sales, etc.), and doesn’t include the income from stock-based compensation plans, such as stock options, that are widely available to tens of millions of employees. This is how wealthy people – yes, millennials, LOL – make a big part of their money, and it’s not included in income here. So the income figures here understate the actual income. These people can save the stock-based income and spend all their wages, and still increase their wealth in leaps and bounds, and that’s fairly common. You need to get realistic about the wealth in US economy.

It’s simple. Americans love to piss and moan about everything. After shopping, bitching is the No. 1 American pastime, lol!

“let them eat cake”

cb – …and have it, too…

may we all have a better day.

Humans, in general, love to piss and moan. Read Gilgamesh (2nd millennium BC), or the Chinese Book of Songs (11th-7th century BC). Different times, same complaints.

Dissatisfaction and envy are the principal drivers of human innovation. Happy, well adjusted people don’t make history, and they’re terrible consumers.

And the Fed may still raise the FFR 1 or 2 more times and then have to contend with higher for longer. So, the top 50% with money in the bank or markets get even richer, pushing the recession out even further.

I just can’t wait to see what the annualized total interest expense is for Q3 & eventually Q4. Q2 at $970B is block buster. Love it!

It all makes you scratch your head trying to figure out what’s going to cause the “eventual” downturn in the labor market? And predicting its is just utterly futile.

Cheers!

This is quite a different take on the 3.5% personal savings rate.

$700 billion of savings sounds like a large number, but just a few months ago, savings rate was approaching 5% while incomes were increasing. The percentage is dropping rapidly, as intended by the Fed. It is staggering the amounts of money consumers are spending.

For reference, pre-COVID the personal savings rate was almost triple at 9%.

What this tells me is that people are getting raises (or higher dividends), and they are now in the process of blowing almost all of it.

There have been many examples of madcap spending just before a fall, a good example being the Roaring Twenties.

On top of that, of course, the USA is prone to disasters, mainly due to its size. Anything could pop along, be it another 1907 earthquake taking out all the tech companies or maybe the USA could eventually get as warm as the 1930s and millions flee to a cold, wet place called California. Somebody could then, write an award winning novel or two, about those times.

What’s your problem??? The BS statement circulating is that these tapped-out consumers have to borrow to spend. I shot that BS down by telling you that the savings rate shows that they don’t borrow to spend. They earn more than they spend. And they save. Is that so hard to grasp?

This is an odd response, as I didn’t say anything about debt. As you suggested in your article, debt is irrelevant because part of this “excess savings” might be used to pay down debt.

The point was that consumers are spending more of their money now as a percentage of earnings than even just a few months ago, and especially before COVID, when they were saving significantly more on a percentage basis.

Anecdotally, I’ve seen a lot of people that better fit what Wolf has been saying here. They have a low savings rate because they choose too, but it is still net positive usually. During covid it was like they were forced to not blow all their money because of the lockdowns and lower social pressure to spend amd brag. They are all working class too and making under $70k total. It’s tight but it has always been tight in the working and poor classes, the numbers are just higher due to inflation. I think the social unhappiness I’m seeing around me is from the fact that a lot of people are starting to realize how big the wealth gap is and that ~60 to 80% of the country isn’t in the middle class like they all wanted to think they were. Middle class always needed to be defined as the 33% in the middle of income or wealth distributions or by the older meaning of the middle of the social heirarchy (those not part of the ruling class but also not part of the masses such as high earning prestigious professionals, managers, successful small buisness owners, etc)

“I think the social unhappiness I’m seeing around me is from the fact that a lot of people are starting to realize how big the wealth gap is and that ~60 to 80% of the country isn’t in the middle class like they all wanted to think they were.”

Quite possible the various forms of social media and streaming TV, etc,. have glorified wealth and raised awareness to the disparity in wealth/incomes that have always existed. But FYI, the middle class is same size as it always has been…

Carlos,

I took SS early because I needed the money. Look at my previous posts to see where it is going. I see working people, my age, tapping into retirement incomes more and more. Several people we know have taken a pension or SS and continue to work full or part time. This is how their incomes are growing, nobody is getting a raise.

This piece provides an interesting counterpoint to the more dour analysis over at Mish Talk.

Mish is a perma bear whose claim to fame for the last decade was that he was reporting a high likelihood of deflation (over inflation). We all know how that worked out.

On top of that when I used to follow him, I found that his returns as an advisor lagged S&P performance consistently as he promoted crackpot theories and generally crackpot investments like precious metals.

I stopped reading his blog a couple of years ago because it was feeling like a similar Chicken Little website. I don’t miss his nonsense at all.

According to Mish, consumers have been imploding for 10 years?

I’m brand new to his stuff. Don’t know anything about his history or the overall timbre of his outlook. His post on this particular subject was simply interesting for contrast. I’m not on anyone’s amen corner — just groping in the fog like the next slob when it comes to reconciling this bizarre economic landscape. The reality, though, is that everyone’s lens is biased and has more than a few hairs trapped in it. Thats part of what makes sentience valuable to me — the artifacts.

Michael Shedlock (Mish) used to post on Silicon Investor in the late 90s and early 2000s. He was the “Max Pain” guy–his schtick was identifying the spot at which most options would expire worthless under the theory that market makers would try to manipulate prices to that point, thus creating maximum pain for all option buyers.

In the late 2000s, as I remember, he started up his own website and began commenting on the economy. He was a professional photographer who taught himself some economics. He got some attention and began interviewing bearish pundits like Mark Faber. He was always a bit of a perma-bear back when I used to read his stuff, but I lost interest years ago. I hope he’s doing well.

Thanks for the analysis, I have been wondering about this tapped out talk for a long time.

I wonder how it looks like if we compare revenue to core inflation? It might give an idea of the long term trend, I suppose.

Punchbowl? CNBC now handicapping a pause in September at 89%.

Would these stats look as good if the federal government were running say a 2-4% deficit:GDP instead of something around 6-8%?

Has the US govt ever run this large a deficit in a year(s) where growth is decent and unemployment virtually nonexistent?

What do they do if (when) unemployment turns up to 4-5%, run a 15% deficit?

That enlightening analysis validates Atlanta GDPnow’s numbers.

That GDPNow is scary-crazy high. I assume it will come down as the quarter progresses, but Q3 GDP growth, from the initial data we have, could still end up being very high.

Based on this and rising government interest payments, any sane society would increase taxes to strike a better balance. ‘course, I have complete faith that the US govt. won’t consider that for one second.

While raising taxes is one solution… the government just not spending as much as it does is another. EITHER/BOTH would take cash out of the economy… and NEITHER is likely to happen.

Sadly (for all of the abuse they take), the Federal Reserve has been the only competent adult in Washington for the last decade or so.

HA HA HA ………………

How can 20% inflation in three years be considered competent, when the target is 2%? The Fed is responsible for inflation.

How can the highest wealth concentration in centuries be considered competent? It’s a direct result of the Fed’s misguided policy to create a wealth effect.

You set a low bar for competence.

The Fed is NOT the only entity that is responsible for inflation.

When the elected government is voting (in a single year) to spend an additional three TRILLION dollars MORE than it was expected to take in over the next few years… and calling it the “Inflation Reduction Act” no less… you get inflationary pressure that is hard for a Central Bank to stop.

Once the pandemic ended, so should the federal “emergency” spending. That is the basic thrust of Keynesian economic theory. That it did NOT means the Federal Reserve is now pushing a string with interest rates rather than pulling a rope with all of the tools at its disposal. As much as people want to put this inflationary period on the Fed due to their delayed response… the real blame belongs to the elected branches of government who were perfectly willing to run up the federal debt with wild abandon.

I have a theory about how the “tapped out” narrative came to be. It’s based on my recollection that it appeared around the time after the GFC. For a time after that, let’s say from 2008 until 2013, people were relatively poor because of all that had happened, so they lost their houses or their houses were worth less , jobs were hard to come by , and the jobs situation was slow to rebound from the crisis. But now after a decade of Federal Reserve and deficit spending driven wealth effect asset bubble and an improved job market, it really does seem kind of silly to keep claiming American consumers are tapped out. What surprises me is the resilience of the narrative — apparently Americans feel poor even though in the aggregate they really aren’t.

I think you are onto something. The FEELINGS of the American public about their financial situation often is a LAGGING indicator of where they actually are. The one exception seems to be Inflation… when gas and groceries go up the consumer is VERY up-to-speed on the situation.

That, AND the theory-pushers think the theory will help speed up the Fed pivot. You know how a lot of people think if they keep saying something, it will magically be true…

These are truly the best of times. I was born in 1962 and haven’t seen an economy as good as this in my lifetime since I was a little kid. I grew up in Titusville, Florida, next to Kennedy Space Center. Our neighbors were all engineers and technicians from around the country. Everybody made decent money, spent it, and seemed generally optimistic about life and the country. This is the first time I’m feeling that same vibe from the folks around me.

It’s difficult for me to understand the cause of this explosion of activity. Pent-up demand after COVID? Trump and Biden’s stimmy payments? Optimism from wage growth? Government spending? All of the above? Whatever it is, keep it up!

Kent-

Good post. Your description of the early 1960’s reminded me of a period 10 years ago when I was fascinated by the Andex (formerly Ibbotson) charts that mapped out the annual market performance of the major asset classes, including major news events.

Here are some interesting takeaways:

1950’s decade-

S&P total return: 19%

Long-term Govt Bonds: -0.1%

Inflation: 2.2%

1960’s decade-

S&P total return: 7.8%

Long-term Govt Bond: 1.4%

Inflation: 2.5%

1970’s decade-

S&P total return: 5.9%

Long-term Govt Bond: 5.5%

Inflation: 7.4%

Your reference to the 60’s made me think of the fact that the 50’s and early 60’s included a cantering inflation, which by the end of the decade had begun to gallop.

In addition (or maybe as a result), from the stock market peak in 1968 investments went through a very rough patch, as you can see by the 1970’s numbers above. Imagine 12 years of negative real returns for stocks AND bonds…

I know we are not IN the 1970’s now. Many of today’s circumstances are worse by magnitudes (systemic debt to GDP and equity valuations near the top of the list),

Maybe this is the “best of times” and worst of times (apologies to Dickens), though far be it from me to try to time the top.

John H. – …remember the bills, human and fiscal, for a long and protracted Cold War conducted worldwide over that time period…

may we all find a better day.

91B20-

I hear you. Hope we aren’t headed that way, but it feels like we may be.

The Andex chart I referenced above bullet points these geopolitical events:

1950 – Korean War

1956 – Suez Canal crisis

1957 – Sputnik

1960 – Berlin Wall Built

1961 – Bay of Pigs

1962 – Cuban Missile crisis

1967 – Six Day War

1964 – Vietnam War

1968 – Tet Offensive

1973 – Arab oil embargo

This observation from Will Durant (c.1980) is interesting:

“In the last 3,421 years of recorded history only 268 have seen no war.” The Lessons of History, Will and Ariel Durant

John H. – and those were just some of them. (Have always felt our recent adventures in the Middle East were, in part, a replacement for previous-and-steady post-WWII MIC economic drivers that greatly shrank in the wake of the Soviets’ bad manners in walking away (for awhile, anyway) from the game…). Best.

may we all find a better day.

It’s all who you’re spending time with. I rode the coattails of rich people through 15 years of QE (which I always knew was bad for the country and dollar long-term) and I gained wealth – and my ideal home – in the process. I’m young and I feel like I’m made. All my rich neighbors are beefing up their houses with hundreds of thousands of dollar additions.

Go into work, everyone is bitching about the cost of gas (although to be fair, they’re still adding to their sneaker collections and buying other worthless garbage). Others my age and younger who did not or could not get assets in time to have them “quantitatively eased” feel like they just got knocked down a peg. I don’t feel bad for the ones who just wasted their money all these years, but I do feel bad for the (responsible) ones that were just too young. They may really have a more uphill battle than they previously did.

Old guys who missed out and/or don’t have a house are all bitter, like Dick.

It’s an interesting response. I kind of like it.

But I’m not sure the old guys are bitter about it like you say.

Not sure how old you are, but have you ever been on the TGV?

If you haven’t you should try it sometime, if you catch my drift.

I haven’t ridden one for a while now, but every day I feel like I’m still on the TGV.

But I’m not bitter at all for riding this train.

At peace perhaps, but not bitter.

Looking forward to my next TGV ride:)

$706 billion divided by 134 million—the number of US “consumer units” in 2021 according to BLS—is around $5200 per household per year. The federal poverty level for an *individual* in 2023 is $14580. So much saving!

Exactly. Not only that, how many have to put some money into 401K and retirement account — which can’t be touch for another 20-30 years.

0.7T is only 3.5% of the net income. Most people would have to contribute more than that to get a decent retirement. Average salary of 70K/yr and a 3.5% contribution doesn’t mean much for our “average American”.

If you go and plot “this extra-saved money”/GDP over time, I wonder where are we at in the whole scheme of things.

BS. Both comments.

1. You’re confusing “savings” (= adding $5,200 to your wealth) with “income” (money that gets spent or saved).

2. If you can save $5,200 a year that’s pretty good. In a household of two earners, that’s over $10k a year in added wealth.

3. The income data here doesn’t include capital gains (from stocks, home sales, etc.), and doesn’t include the income from stock-based compensation plans, such as stock options, that are widely available to tens of millions of employees. This is how wealthy people – yes, millennials, LOL – make a big part of their money, and it’s not included in income here. So the income figures here understate the actual income. These people can save the stock-based income and spend all their wages, and still increase their wealth in leaps and bounds, and that’s fairly common. You need to get realistic about the wealth in US economy.