But the Bay Area cannot keep up with the spectacular collapse of prices during Housing Bust 1. That had been a doozie.

By Wolf Richter for WOLF STREET.

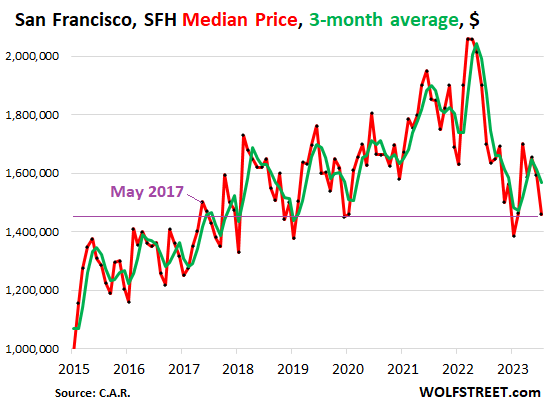

In San Francisco, the median price of single-family houses dropped by 8.5% in July from June, and by 14.1% from a year ago, to $1,460,000 million, according to the California Association of Realtors today.

In the 16 months since the peak in March 2022, the median price has plunged by 29%, or by $600,000 (red line).

The three-month moving average (3mma), which irons out some of the monthly ups-and-downs of median prices, fell by 2.6% in July from June and was down by 23.1%, or by $474,500, from its peak in May 2022 (green line).

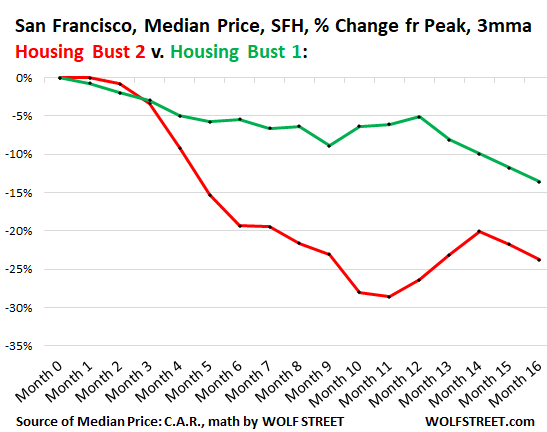

Housing market downturns are slow-moving. Prices don’t plunge overnight, as you’ve come to expect from cryptos. Housing market downturns take years to play out. Housing Bust 1 started in different markets at different times. In San Francisco, the median price peaked in May 2007. Nearly five years later, in February 2012, it bottomed out, having dropped 31% from the peak.

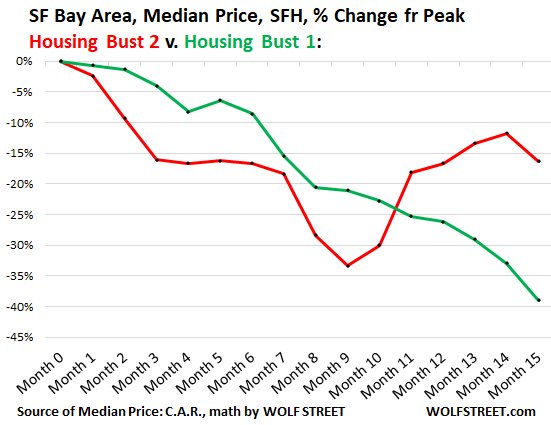

Housing Bust 2 started after the peak in May 2022. May was month zero, and we’re now in month 16 of this downturn.

So we started comparing the Housing Bust 2 in San Francisco against Housing Bust 1, in terms of the percentage drop from the peak.

In 2007, the median price peaked in May; in 2022, it peaked in March. So we’re off by two months, which adds some seasonality to the mix. But we’re using the 3mma for both periods, which irons out some of the seasonality.

So we find:

- HB 2: In month 16, the median price 3mma was down 23.8% from peak

- HB 1: In month 16, the median price 3mma was down 13.6% from peak.

- Both experienced a sucker rally of three months that started in month 10 for HB 1 and in month 12 for HB 2, providing lots of false hopes.

- The rally was steeper in HB 2, after prices had dropped a lot faster.

- After three months, both rallies died and prices headed south, extinguishing the false hopes.

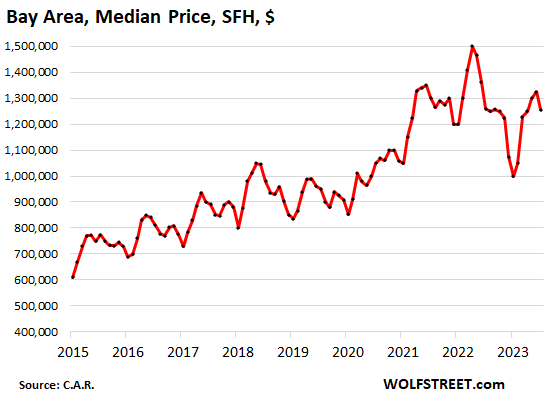

In the San Francisco Bay Area, the median price of single-family houses dropped by 5.2% in July from June, by 0.8% from a year ago, to $1,255,000, as the different counties moved to different drummers.

In the 15 months since the peak in April 2022, the median price has plunged by 16.3%, or by $245,000.

Given the large size of the nine-county Bay Area, with a population of around 7.6 million people and about ten times as many transactions as in San Francisco alone, the median price is less volatile. So the 3mma was not needed, and all comparisons here are between the unsmoothed original median prices.

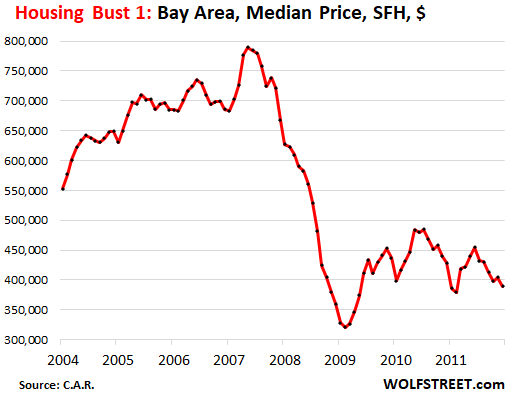

The Bay Area’s Housing Bust 1 was atypical in how fast it moved. April 2007 was the peak. By February 2009, in less than two years, it had plunged by 59%. It then rose and re-dropped a few times, and by January 2012, it was still down by 54% from May 2007. Then it took off again.

In the Bay Area’s Housing Bust 1, the median price plunged over the first 15 months by 40%. Prices just kept plunging without any kind of rally. That was very fast for housing downturns.

Housing Bust 2 started out plunging even faster, but then had this magnificent rally, perhaps driven by the magnificent Nasdaq rally, that has now also ended, and prices turned south again:

Look, the Bay Area, and particularly the most expensive counties, are a part of the US where “Housing Crisis” means homes are too expensive, even starter shacks are too expensive, for people to be able to afford to live here.

So there is constant political juggling over creating taxpayer-subsidized “affordable housing” and other subsidies. The problem simply is that homes are too expensive, and creating subsidies – whether subsidized housing or down-payment assistance, or whatever – isn’t going to help, and may make the pricing situation worse.

What is needed is for the market to sort out this “Housing Crisis.” The market needs to be allowed and encouraged to sort it out. That’s really the only way to solve the Housing Crisis.

The Fed’s interest rate repression and QE, which drove up all asset prices, did an amazing job in the SF Bay Area to create this Housing Crisis. Higher interest rates (we just discussed them, good lordy) and QT (the Fed has shed $759 billion in securities) should be allowed to undo that damage, with the market letting home prices find their balance to where people don’t have to leave – and they did leave in large numbers! – in order to dodge the ridiculous housing costs. The local economy would function a lot better if home prices are allowed to find an economically sustainable level.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, back to my post from the other day about how eye opening the 5.8% Fed GDP Now estimate is. I stated that being halfway through the quarter is an important indicator of where the final estimate might be. Your reply was something about the July data just now starting to trickle. Maybe we’re looking at two different sets of data on the Fed GDP Now website, but it clearly states that the latest estimate is based on 12 data points thus far this quarter. I’d hardly call 12 data points as just starting to trickle in. Again, we all know it’s going to move around quite a bit, uncluding to the downside, but it’s still pretty exciting that it’s shooting up so fast.

More inflation means more rate hikes for longer! Now, if we can just get our real estate sector to move in the same direction as China’s, then we get to see if E Warren trots out rent & mortgage relief. That’s the million, oops trillion, dollar question.

Cheers!

12 out of how many?

There have been NO data releases on “consumer spending” — that’s 64% of the US economy. The July data comes out on Aug 31. That’s the biggie. There are lots of others that are crucial.

Lots of the other important releases for July aren’t out yet either.

So far, Q3 looks strong based on the small amounts of data. But the GDPNow is really just a weathervane this early on. It’ll go all over the place.

Investors own about one in four houses ( google it if doubting ).

With that demand already gone, and investors possibly bailing as prices continue down …

The trend before 2023 looks like “buy the dip” in practice (bull trap?).

The housing market topped in Canada around early 2022, but the Canadian politicians are trying very hard to prevent a real estate price decline.

And our FED isn’t? They successfully isolated the most vulnerable group of people from buying/selling, while forcing a small group of buyers to overstretch their budgets due to low amount of listings. So if something was to break, only that small group will be affected, making their job easier.

The Federal Reserve isn’t in charge of housing policy, housing supply or immigration policy.

Well FED affected it with low interest rates and now with rising rates.

Did you miss Powell saying “The housing market needs to get back into a balance between supply and demand”?

Bingo. Until appropriate (tax) policy changes are made, don’t expect home affordability or inflation to get better. Housing costs and wages are the ringleaders now, in an inflationary doom loop that can’t be fixed without either tax policy changes or massive unemployment.

JeffD, the other solution is new construction. Its a supply and demand problem in many places. San Francisco is seeing a large exodus due to WFH, which is allowing their to be a negative pressure to lower prices finally. Other places are seeing upward motion, or at least lateral motion with higher rates (real price upward), due to this migration. Eventually if therese more houses to be sold than buyers prices will fall, but even though theres a smaller pool of buyers in this market, theres an equally smaller pool of sellers. Average days on market is trending up, a good sign, but still historically low. Wolf’s previous article showed a national 1.5% decrease June22 to June23. I suspect we will see a greater drop by June24 as many of the new starts finish up and pull from the backlog of potential buyers. And of course as prices drop the number of potential buyers will slowly increase again. Theres an equilibrium somewhere, but not here. As rent inflation rages people will still long to escape 7% yearly housing increases by buying *something*, anything.

they did buy 2.5 trillion of MBS, which impacts the housing market.

Central bankers can give their opinions, but they have no authority to give housing permits, open land for construction, maintain the borders, etc.

Just like Tiff Macklem at the Bank of Canada whose opinion was that the Canadian govt’s immigration policy is leading to higher demand and inflation. It’s just an opinion.

Central banks are only legislated to control the money supply and interest rates. Whether retail investors deconstruct every opinion as investment advice is up to them. This is why mutual funds and financial advisors are regulated.

Great- the Fed should immediately unload all the $4 Trillion MBS on the open market and let banks buy and sell that toxic crap from each other. If they can’t handle it, the banks should go under. Instant housing and banking fix, instead of the slow death march of this abusive and obtuse financial system.

Yes they are, trying very hard to prevent a Canadian crash in the overpriced Canadian housing market. They being the fools that created the mess in the first place who now prefer to refer to the cluster explosion that may occur in the form of a 50 pct decline in the selling price of a Canadian home.

High rents and low wages with no benefits.

The Toronto Transit Commission was on the news the other day because temporary workers were complaining about working conditions. The TTC was considered a company where if you got a job, even to tie up the garbage bags, you were set for life with a good union wage, retirement benefits and even RRSP matching (every dollar you invest is matched by the employer).

But my realtor said Real Estate never goes down!!!

I think maybe it’s time for Realtors be held to a higher standard.

Who wants to live in San Francisco??

So many people that it pushed the median price of a house to $2 million? And 2-BR rents to $4,000 a month?

BTW, as this appears to be on your mind, LOL, I now track crime in San Francisco on a special page, with charts of each category of crime going back to 2009, an eye-opener for all those folks who think that “crime in San Francisco is going through the roof,” or whatever.

https://wolfstreet.com/san-francisco-homicides-rapes-robberies-aggravated-assaults-burglaries-larceny-thefts-auto-thefts-and-arson/

The fact that you feel like you have to have a .45 nearby while eating lunch because you fear you might have to shoot your way out of trouble is precisely why I don’t want to be anywhere near wherever that is. I enjoy being in a place where I can eat lunch without fear, thank you.

Can’t be right. 0-hedge says so!

Why don’t you just sell that “bit of everything” Rube Goldberg AV8R POS and go skydive. Learn to be a real BODY pilot. We had a Brit come over in 74-5 for a couple months and he was dumping at 800-1000 ft (not always….though) We all went screaming to the manifest and Albert just said, “That’s what they do over there”. Ground rush city! Plus your groupies on ground can see your smiling face and hear what you say!

Dirty Harry did, although with a grimace. He liked the ladies and blowing away bad guys.

Median prices often tell a misleading story – because they don’t comprehend mix

The market price of the median Bay Area house didn’t fall 59% in bust 1

Why not use case-schiller data ?

Median price works fine if you include a chart, so you can see. Sure, mix impacts median price. But over the longer term is washes out.

I use the Case Shiller ALL THE TIME, on the day it comes out, but it didn’t come out today, and it lags four months behind the median price data, and it doesn’t cover the city of San Francisco, but a 5-county portion of the San Francisco Bay Area, and those problems are big issues, you goofball.

The CS of the 5-country Bay Area plunged 46% during HB1. But that’s not the 9-county area — it excludes, among others, San Jose and the majority of Silicon Valley, where price plunged.

Just because you don’t read my Case Shiller articles, doesn’t mean they’re not there. The most recent one:

https://wolfstreet.com/2023/07/25/the-most-splendid-housing-bubbles-in-america-july-update-3rd-year-over-year-price-drop-in-a-row-monthly-increases-are-just-seasonal-robert-shiller/

I’m just here to see Wolf “initiate” the uninformed new-to-the-site smarties. Lol

Wolf

i just had an epiphany today after paying $80 for a bed in a 16 bed dorm at a hostel in Denver, that these empty commercial towers are eventually going to be converted to apartment / residential towers.

it’s just a matter of their prices getting low enough for the developers to make a decent / obscene profit after incurring the conversion costs.

Thoughts? Have you already assessed this prospect? Thanks

Yes, there have been lots of discussions here over the past year about the issues related to residential conversions of office towers. Not many office towers are suitable for that, and it will be cheaper to tear them down and start over. Some office towers can be converted and are being converted.

“The local economy would function a lot better if home prices are allowed to find an economically sustainable level.”

Agree with this common sense.

However, try telling that to a realtor.

I suggest that the powers that be believe that the current level of housing prices is sustainable and bullish.

The last thing these dip shits are going to do is crash the real estate market if they can help it.

You will probably expire before your wish of an economically stable level, comes to pass.

Waiting for this movie to play all around USA as all of USA was impacted by cheap money.

I am sure people would come out with vested interest saying:

Real Estate is Local.

Not in my neighborhood.

Not enough inventory.

Everyone wants to live here.

etc etc

but bottom line is: its a game of monthly payment and something has to give in.

the market needs distress to truly reset. during housing collapse 1, we had subprime mortgages pulling prices down. unfortunately the government stepped in with low interest rate policies and that put a net under it and then they kept interest rates low.

we need government to step aside completely and allow the markets to work themselves out. it will lead to a healthier economy.

a house is NOT a productive asset and people should be taught that putting all your money in a home is not a good investment/retirement strategy

Mid year they forecasted we will have 4M home sales this year. It looks like that was way off and we will have 5M home sales in the US in 2023. Housing has stabilized at a high plateau. If rates are in the 6% range next year I think the frenzy might start again?

Kind of like Wile E. Coyote running off a cliff and continuing running in midair…until he looks down…

Richard,

Stabilized at very low sales you mean?

Mid 2021 through mid 2023 looks an awful lot like 2006 to 2009. We seem to be bouncing along near the bottom of these 18 or so years of sales levels.

Curious, do seasonal adjustments include adjustments for increases in the population eligible to purchase housing? Or is that not a meaningful factor.

what i have learned from stock charts is that humans create patterns in data that may or may not have meaning. sure, we have bounced off a low and then headed back down to that level, but there is no guarantee that it will not drop even further.

Where is your data from? Existing home sales for July haven’t been released by the NAR, which is the first month after the middle of the year. Maybe your data is from another source.

It leads me to ask: when was the “mid year” forecast made, who made it, and what data shows a surge in sales since that forecast?

Links are always deleted here and references to other sites as well.

Just google

Number of existing homes sold in the United States from 2005 to 2023

When homes sales were discussed here mid year I was laughed at because I said we will have over 4M homes sales this year which I said in context to dispute the “there is no demand” argument. Now it looks like we will have 5M home sales this year.

I googled it and the first two results, Statista and Trading Economics, with results through May and June, respectively, don’t support the conclusion sales will be closer to 5 million. Statista put the annual pace of sales for 2023 at 4.3 million. Trading Economics had annualized monthly data and it ranged from a high of 4.55M in February to a low of 4.16M in June.

Sales in the second half of the year will need to average about 5.7M annualized each month to get to 5 million sales for the year. We’ll see the July numbers in a week or so. However, the Trading Economics forecast for July is only 4.1M annualized. I’m still not sure where you’re getting data suggesting 5M home sales in the US in 2023.

It does seem odd if you were laughed at mid year for saying “we will have over 4M homes sales this year.” Even in the depths of the first housing bust sales always exceeded 4M. They’ve also exceeded 4M annualized every month this year so suggesting mid year they’ll exceed 4M is certainly a reasonable prognostication.

And I am not sure why that seems odd to you. You can experience the same reaction. Just try this: When someone tells you there is no demand for houses and people can’t afford to buy homes at current prices/rates tell that person we will have north of 4M home sales for the year.

Richard,

It’s odd because the people you say were laughing at you must be ignorant of the data. First, you could have simply pointed out that during the depths of the first housing bust, house sales never fell below 4M. Second, the annualized rate of sales has been above 4M every month in 2023. Saying sales will exceed 4M is not a stretch even in the worst markets. Four million is a very, very low level of sales, but I get the sense you think it’s a lot.

You must be joking. Of course people are ignorant of the data. 90% of people who talk about this upcoming RE crash have no idea that we only have 1M active listings and that 2.5M is the historical trend and that we have 4M active listings in 2007/2008. I said it again, next time someone tells you there is no demand and nobody can afford these housing prices tell that person we have 4M home sales annually despite sky high prices and sky high rates.

“we have 4M home sales annually despite sky high prices and sky high rates.”

Sky high??? At only 7%? You must be young and adapted to the last 15 years of interest rate repression by the Fed. Current rates are very normal, and definitely NOT sky high. GMAFB.

ROFL! Bawahahahah you make me laugh. Thank you!

Rates haven’t been this high in many years. They doubled over the past years. On a million dollar home that’s a huge increase on the monthly PITI. Sure, old boomers brag that they experienced 14% rates but they don’t mention that houses only cost 50k not 1M. I am happy with my 3% 30y fixed rate. But for buyers, rates and prices are sky high. I can do the math for you to show you how much that changed for a 1M home (3% to 7% rate increase)? And of course I am young….proud millennial :)

My mortgage was 8% on a 15-year and I got a deal from a collapsing bank that owned the place that I bought!!! Grow up, dude.

Richard,

I wasn’t joking, I was trying to be nice. Speaking of ignorant of the data, you still haven’t said where your 5M figure comes from? It certainly wasn’t in the google search you suggested.

Wonder if the whole supply is low and will be low forever will age as well as inflation is transitory…

It goes hand in hand with the “rich foreign investor” narrative, and “Zoning issues”, and “NIMBYism”, and “not enough housing starts”, durring the boom as to why the kids can’t afford housing without an inheritance or a job at Facebook.. or Meta or whatever. Somehow ultra low interest, “cheap money” was never to blame. Now the same kind of ideas are employed to explain why those same houses “can’t lose value” all the while central banks tighten conditions.

We’ll see what happens but I know here in Canada there’s already people who can’t keep up with their mortgages because they had variable rates or they needed to refinance their fixed rate mortgages. We don’t have those fancy 30yr fixed rates so the pressure from higher interest is applied quicker. I do not for one second believe that our “high immigration rate” (my new favourite scapegoat) is going to save everyone’s 800k 1bed Toronto investment condo. People can keep pretending like monetary policy doesn’t matter, but I don’t buy it, I think we are going for a ride and it’s not on a rocketship, I think it’s a toboggan.

However, if SoCal RE does go south and there’s still work in my industry stateside I’d consider it, absolutely gorgeous down there 😉

30 years fixed rate especially at 3% or Prop 13 in California that benefit people that bought long time ago before the price went nuts are definitely enablers to the extra sense of entitlement most homeowners have in California.

Also give a lot of people the sense of look at how smart I am in getting in the market at the right time and I can’t never lose…

Talk about talking BS..

My realtor friend in socal is saying that this is the best time to buy home because rates are very high so buyers are limited.

Buy now ans refi when rates go lower .

When rates go lower you’d have more buyers vying.

😀😀😀

listening to a realtor for financial advice is dangerous. they have a vested interest in propping up the market.

as interest rates drop there will also be alot more supply of homes for sale because people will feel they can swap out interest rates.

the real issue at play is at what point government is forced to stop propping up the economy. the rate of increase in the debt is unsustainable. the date at which social security must be cut to 70% draws nearer every year (and projections of the date keep getting moved forward). medicare also gets less financially viable every year. sure, we can raise taxes immensely, but that would also kill the markets due to less spending.

it is living on borrowed time and the only question is when the music ends.

Lolol. Creative bunch, realtors are. Corrupt may be a more appropriate word.

Attention monitor:

‘what’s wrong with importing illetrate, godless, scumbag 3rd world crap?’

You will know HB2 is over when a bus driver in San Francisco can save for 3 years and buy a modest house within a 30 minute commute of his job.

Name some instances in human history when and where a low skilled worker/laborer could buy their own house with only 3 year’s worth of savings. For many millennia, renting and serfdom has been the absolute norm. After WWII, the U.S. was uniquely positioned to have a comfortable working middle class because the rest of the developed world’s infrastructure was blown to bits and we controlled the world’s primary currency. That’s not the case anymore, and our grip on world power is not getting any stronger. What makes you think a bus driver in San Francisco should be able to afford a house paid off with a meager 3 year’s of savings? Has that ever been possible?

The average American’s economic power relative to the rest of the world has been fading for decades and it will probably keep fading in the long run. Money printing and accounting tricks don’t work forever.

Can’t wait to see all the not in my area comments (and look there’s still bidding war blah blah)

My guess is there will be plenty still saying the same thing about their LA/OC/SD markets, let it rip, it’s always entertaining

Don’t see bidding wars in my neighborhood. Some houses sit for a loooooong time. Sellers are not willing to reduce their prices and often take the house off the market and re-list many month later. One house that they were trying to sell for over a year now finally went pending. Curious to follow at what price it actually sells. Some houses sold much quicker. No bidding wars. And a lot of people that keep saying prices + these high rates is just insanity.

It’s really hilarious when sellers take their overpriced house off the market, wait 6 months, then re-list it with a $20K higher asking price.

I’ll bite. Somehow my family member’s dumpster fire of a house sold for $40k over asking, and truly the asking price was already ridiculous (no listing/withdrawing/relisting shananigans). Took them over 4 months to close (buyer has conventional mortgage) something about major issues with the foundation, septic, well, plumbing… house is The Money Pit but I wish them all the best with it, certainly nothing a bulldozer couldn’t fix. The appraiser must have been on some good drugs.

But, hyper local. Generally I’m seeing prices drop $15-20k+ in the area. Still pretty stupid prices, at least I wouldn’t/couldn’t pay them.

Thanks Wolf for a data driven and as always informative article. In addition to letting prices to drop to make our lovely region more affordable, there have some real legislative changes these past few years to make it easier to build across California. The ‘granny flat’ has had a small impact, now builder’s remedies are happening up and down California. Rich communities are gnashing their teeth and angry that more housing is going to be built near them.

These changes will also do a lot to restore normalcy by increasing the supply into the market – but that does take time.

There is also a downside to building more. It’s already very crowded here. I don’t like the traffic. If you ask me, I rather have less houses and less people. The more people I know the more I like my dog.

Cmon, Richard — they’re alright. Think about all the goodies previous generations of people left you so you didn’t have to do all the heavy lifting once you arrived on planet Earth: language, mathematics,

onomatopoeia, chronology, electricity, architecture, motorized conveyance, sailing, penicillin, fabric milling, corrective lenses, cinema, the fermentation process, cooking, transglobal communication, the periodic table, the pentatonic scale…a tiny tiny fraction of all the great things left here for you to unpack and begin to enjoy life with a quantum head-start.

Not the worst jerks, people.

That is the most convincing pro-human argument that I have ever encountered. Well done.

I am Not against humans, I just prefer my dog more. He’s not talking back and is always very happy to see me/spend time with me. he only gets upset when I give him a bath or run out of his favorite treat.

I do appreciate that we live in a time during crypto. Bitcoin has been good to me (bought below 4K). Shout out to natoshi nakamoto! Being a millennial I am unfortunately too young to experience space travel though. The other things “given to me” are not helping me with the feeling of getting annoyed at traffic and people. That’s why I mostly work from home :)

Bul – has always fascinated me that so many ‘Muricans oft-seem to prefer the more easily-digested/promoted ‘rugged individual’ narrative over the tougher chew of ‘the power of general cooperation’ (a major driver of the wheel of history/rise-fall of nations)…

may we all find a better day.

Very Well said Bul-, as usual.

But with one BIG caveat from Bertolt Brecht. Guess which short science quote I refer to? (My revenge for making me look up that “O” word, a concept I was already well aware of.

I spend my time unwinding a lot of your “quantum head-start”, mostly all stuff since the Neolithic Revolution brought about the start of “Civilization”…..including the quantum bs. Evolution of alphabet was pretty good, though…..at least I am unable to see fault in it.

Just because we have learned to “use” electricity by “trial and error”, doesn’t mean we have any good idea in hell about what electricity really IS…..can’t see things in that small world, ya know? Same goes for the real BIG and real LONG time scales…..physically unable to grasp or manipulate them.

But yeah, we have done pretty good for being just “doped water”

..And it was all done by “sharing things”……..a “rugged individual” seems to have his main use in KILLING, which St Augustine said that God said is OK..(contrary to the Law of Moses)..if God agrees it is necessary killing.

Has anyone heard of a recalculation of a house’s square footage?

I follow a few homes near me and one home increased by 200 Sq. feet between sales.

They did zero improvements.

Someone was saying on another forum that Fannie Mae or mac changed their calculations.

Seems unfair because this home made an extra $40,000 on this recalculation alone.

In the San Fran area you could add $100,000 easily with these changes. Really helps the seller offload that house with little out of pocket except to the buyer. And their costs are being rolled into a complicated mortgage, so do they notice?

Check to see if that extra 200 sq ft comes from a little sleight of hand trick known as a “finished basement.”

Slap up some drywall over the concrete, install a drop-in ceiling, and roll out a shag rug – and voila, you can add $40K+ to your list price.

Double benefit is that it hides water leaks in the foundation and damage to the upstairs floorboards from that one time the toilet exploded!

Carlos were you featured on HGTV’s house flippers? Ha

Unless these people finished their crawlspace out with some crown moulding… pretty sure it’s just a new formula for calcs. But hey, Airbnb that crawlspace. “Cozy surroundings”. ;)

I would keep all of that on the down-low if in the jurisdiction of Crook County Illinois.

I’ve seen this in house hunting. Requested the building permit and inspections. That ended that deal.

My favorite hide attempt was the suspiciously extra thick insulation on the basement ceiling hiding fully notched joists from a bad bathroom remodel job and an old furnace venting system. Certainly explained why it was The House That Jack Built, bonus was the weight of the first floor sitting on the poop pipe.

200 square feet is about the size of a converted one-car garage.

If I see the word “unfair” one more time, I’m going to puke. The only thing “fair” in life usually has a ferris wheel on the premises.

How much for a tulip?

Oh, ok.

You’re crossing posts with that burn. I appreciate the effort. Ha

That’s crazy that prices have dropped that much in the Bay area. I’m down the coast, just south of San Luis Obispo and our prices are down some from the very peak but not that much. I live in a pretty desirable area and I get calls from realtors asking if I want to sell, that they have buyers who will pay full price, cash.

I figure prices will stay high in most areas until interest rates drop. Then prices will fall as there will be a pent up demand to sell by people who are now trapped due to their current low mortgage “preventing” them from selling.

I also get unsolicited calls from investors some as far away as Florida and New York. Almost anything under 300k in California sells very quick. It doesn’t matter how undesirable the location is. I think Prop 13 is the main reason. And the very generous benefits this state hands out to just about anyone who wants them. Move to another state and you’ll lose all those freebies

Very generous benefits?? What benefits would these be? Aside from Prop 13 which really only benefits those who bought years ago. I’ve lived in California for over 20 years and the only “benefit” I’ve received was being able to take a few extra weeks of maternity leave. In reality we pay higher taxes and more for energy and gas than other states.

Wondering about your opinion regarding if/how China’s Evergrande finally deciding to seek Chapter 15 bankruptcy protection (in NYC) will have any effect on property values in areas like SF?

Just a hunch that any Chinese entities investing/finding financing in property/resources outside of China would probably be involved in property deals/financing inside China as well, so might that hurt in terms of funding for future foreign-sourced property purchases…plus the fact that Chapter 15 typically deals with “cross-border” insolvency cases? Many Chinese offshore bonds now trade at low double- or even single-digit cents on the dollar, and their share values have shrunk 90%, for example.

Will such sector uncertainty lead to a further squeeze on the number of foreign “bottomless cash bidders” who’ve historically helped push up local property prices in certain favored foreign regions, or no? Thanks.

The facts speak for themselves. It is humanity that is tasked with interpreting them.

I’m just not motivated to but a house in San Fran Cisco for 1.4 million rather than 1.5 million before. The San Fran is in a league all it’s own.

Not representative of the average, nor the mean. It is what it is.

A community of snobs, yearning for creative friends. Not the kind of neighborhood I prefer.

Either San Francisco is not a fit for you, OR you are not a fit for San Francisco. It is what it is, like you say. But which is it?

The working class grandeur that made San Francisco what it was has been bought and sold to the point that it is the antithesis of what made it famous in the first place.

Last chance dreamers as opposed to the current trust funders that own the real estate.

Wolf,

Why do you think the local economy would function A LOT better “if home prices were allowed to find an economically sustainable level” in the Bay Area? We can certainly debate how efficiently the Bay Area economy is functioning, but let’s also keep in mind that the Bay Area is extremely small – population wise – relative to the rest of the country yet has so much economic impact on the world. And let’s remember that some of the worlds best economies come with some of the highest real estate prices – just think Switzerland – of similar size to Bay Area in population – where mortgages are taken out over 50-100 years and one can keep 65% of the debt on their property forever.

For a measure of comprehensive narrative, have your readers check out areas an hour away from the Bay Area where home prices are similar to much of the rest of the country – think Stockton or Manteca and their surroundings. They should know that you can live an hour plus away from one of the worlds greatest areas and the Pacific Ocean for the same price as folks pay to live say in Ohio. It’s just not that bad, dude.

Again, I am not against debating high home prices and efficient economies but I worry how your readers interpret such commentary. Like that socal beach guy and the phoenix dude, who are rooting for housing to crash for crashing sake, without considering that other folks choose to make it work paying premium prices to live in premium places AND that some of those very folks from that very economy in the Bay created technologies that enable them to read your posts and share their comments, however constructive and well intentioned they may not be.

Not a native Washingtonian but I’ll take western Washington state especially north of Seattle over the Bay Area. Interesting Washingtonians don’t toot there own horn too much on the web. A little but nothing like other parts of the country.

The whole West faces climate change effects.

Droughts and wildfires can not be ignored.

Second EXTREMELY hot summer in a row in Texas. Weeks and weeks go by eith high temperatures of 102 to 107. Low temps 76 to 82.

Wildfires burning Canada at a record pace.

I’m not 100% sure there’s CC as I don’t read about it extensively. But I’ve lived in WA state for 27 years and the summers are surely hotter the last 10 years. I do keep some records on how many days we have 90 plus temperature days per month. Its not unusual July and August to average 5 degrees above average (last 10 years) and yet they never average below the long term average temperature (I’m talking daily high temperatures).

Droughts a concern big time Utah, Nevada, Arizona, etc. Two summers ago in eastern Washington we were in the severest possible drought catagory. Seem to be headed back that way again this summer.

It could be here in WA state they are much smarter about how to deal with wildfires than 10 years ago…practice makes perfect, well it doesn’t hurt. Me being an optimistic. Walden WA burned two years ago… 30 miles south of here… all homes lost. Floods and wildfires a Huge deal in the US… and drought.

But ahhhh California. Not too many wildfires this year. But heres the thing right…

kids love growing up with snow ! You don’t have to be Scandinavian, Swiss or Austrian.

Older folks… 70 and above… not necessarily, I’ll grant you that. But as long as you can make ends meet financially and are not too elderly… lots of folks prefer 4 seasons.

Malden, not Walden WA.

Alternator-

I’m not trying to speak for Wolf, but as a reader and commenter.

I’m not in the camp that pines for a collapse in asset values. What I yearn for is a market free of government intervention, wherever that leads price-wise.

Concerning intervention into real estate prices, some primary government policy includes:

– Interest rate manipulation (FFR and Fed portfolio)

– Mortgage price supports (acquisition of MBS)

– Mortgage subsidization (FHA, VA programs, etc.)

– Mortgage interest deduction (IRS)

These policy tools are used, ostensibly, to stabilize the economy. The RESULT is that bubbles develop, and exist now, that are both “unsustainable” and “unfair.”

Sustainability of current prices is not possible forever, as it requires an ever increasing policy support. Cut back on the policy support, and crisis ensues. The desire for economic stability (i.e. stamping out downturns by increasing supports) leads eventually to the weimar experience, dire and old fashioned as that may sound. Irving Fischer’s comment about “permanently high plateau” comes to mind.

By “unfair” I mean that the government picks winners (e.g. banks, who are allowed to keep large profits when times are good, but are bailed out with taxpayer dollars when periodic and inevitable financial crisis occurs), and creates losers (e.g. young family formers ravaged by general inflation and high prices for starter homes).

I believe that this “unfairness” is a big part what you hear from commenters who look forward to a bursting of the real estate bubble or for a steep decline in the stock or bond markets.

Respectfully submitted.

John H,

Your post is super well thought out – no counter arguments from me on your reasoning other than it perhaps gives too much credit to some who repeatedly pine for a collapse in asset values on this site without giving ANY reason.

My comment was more challenging the notion that the Bay Area economy could function a lot better with lower housing prices. But if the argument is that it could function a lot better without government intervention (which is just one reason for high housing prices throughout history) then no argument from me.

I feel like you are using a shotgun where a rifle would be more appropriate. Many of your targets are legitimate, but you took out some innocent bystanders as well.

1. The government, per the Constitution, creates money and regulates its value. This is often done poorly, but is not primarily a tool for manipulating real estate prices.

2. VA loans are part of a benefit package for those serving the military. Whether this is a good idea or bad idea, the goal is to compensate military personnel, not manipulate the real estate market.

3. The mortgage interest deduction merely puts owner-occupiers and investors on the same level, rather than giving investors an advantage.

Point 3 doesn’t fly in my book. Investors get an interest expense deduction because they receive income from the home. When people buy homes to live in, they don’t receive income from the home. Why should live-ins receive an interest deduction when receive no taxable from the home? It’s a clear subsidy that is counter-productive at today’s home price levels.

Point 1 doesn’t get off the ground either. The Fed sets the interest rate, which is a key determinant of home affordability and home prices.

Point 3…. I don’t give a rat’s patoot about “investors”. The home mortgage deduction was born when there was such a quaint concept as the nuclear family. It was intended to subsidize families with children (and a stay at home mom) and promote home ownership, which results in stable communities and benefits society as a whole. It’s the “investors” that should be denied the deduction, not the families.

Interest rates only set prices in a clown world. Low interest rates have no effect on how much anything is worth until stupid people, with a limited understanding of personal finance, get involved. I find it absurd that someone will bid a house (or car or ear of corn) up into the stratosphere because their “monthlies” are “affordable”. That’s just simply stupid behavior and they deserve whatever financial whoopin’ they get.

This can work two ways. A country like Switzerland can have high real estate prices because it is desirable. But a country can also be subject to the whims of a poor government which can debase its money, offshore its industry and ruin it geopolitical standing in the world.Eventually that country can become an inflation-racked banana republic with poor economic prospects, no friends around the world and no law and order. Then the value of its real estate can drop very low.

They aren’t making any more Manteca!

So it’s wonderful for prices to go to the sky, but a big problem if they come back down?

TT – how do we often see someone’s internal adding machine (…sorry, giving my age away, again, meant ‘calculator’) stuck on ‘+’ or ‘-‘ ?

may we all find a better day.

As life progresses, the new becomes the normal and the past becomes more distant, in normal discourse.

All the while, the past is the principal measuring stick of the present.

Hey Wolf, any plans on an article about the slowing Chinese economy and it’s possible repercussions? While I feel that there is certainly risk of financial contagion, I also understand that one of the side effects of the pandemic era was the mass exodus of manufacturing to countries like Vietnam, India, Mexico etc.

Californians.

Texans.

New Yawkers.

Floridians.

Bozemans.

Everybody wants to live here. Get a grip.

Keep kidding yourselves boys and girls.

Population declines through much of CA tell a different story.

JD, how big are those declines?

Hopefully China’s current economic issues and youth unemployment will result in Chinese currency controls to prevent money from reaching US real estate; certainly the Chinese consulate in San Francisco should have taken notice. Time for them to book profits and sell.

They’ve already been doing capital controls there, it’s a big reason that the Vancouver real estate market (still an outrageous bubble) hasn’t been propped as much as before, both countries (or at least Vancouver’s government) hate the use of unoccupied real estate as a sink for extra funds. And the youth unemployment rate is a non-factor, that’s just a data quirk from a different way of calculating youth unemployment–they’ve used the old Spain and Italian method of counting up even university-attending students as unemployed, since historically not as many Chinese students attended college, though that’s changed recently. This obviously inflates youth unemployment numbers compared to the US and other countries–imagine if the US unemployment stats counted every college student as unemployed. So they’ve scrapped that method and are adjusting based on those graduated and actual seeking employment, and the numbers are closer to the averages for developed countries.

Free money turned brains to mush, possibly even in S.F.

Are these real dollars? HB1 didn’t have inflation like today…

This website has lead me to believe that the 30-year fixed subsidized mortgage is a bad idea. When the Fed recklessly holds rates down too low for too long everyone should have to pay the piper when they go back to normal levels. Instead there is a whole lot of homeowners that get to take advantage of these low rates for many many years are not allowed to feel the effects of the collective decisions that they participated in (pushing prices up beyond the reach of many). 5 yr ARMs would change a lot of people’s tunes.

Good comment.

I wonder if that isn’t a large part of Canada’s apparent success at minimizing banking crises over the decades?

Canada has gone through some whopper residential price swings, but at least the decision-maker (home buyer) seems to retain most of the risk fallout.

The key word is “subsidized”. There is nothing wrong with borrowers taking advantage of foolish lenders, so long as the taxpayer is not ultimately on the hook…

Except most residential mortgages get swooped up by FNMA and other associated government sponsored programs. Take away that backstopping and it would be very unlikely that 30-yr fixed rate loans would hang around.

“Unfair” ? Isn’t that the definition of a Market. Millions make individual decisions to transact. Each side believes they are doing the right (advantageous) thing. Sometimes they are right, sometimes they are wrong. Thats how adaptation works. We only see what the “wise” choice was in hindsight.

Any banker who kept 3% 30 year fixed Mrtgs on their balance sheet made a very bad choice. Most of those Mrtgs were sold off to someone elses balance sheet and the banks just kept the origination fees and fees they collect for servicing.

In 2012, the Big Mac index had 15 countries around the world which were considered overvalued, in terms to their relationship with US Dollar at the time.

Today, as of august 3rd, there are about 6 countries around the globe with currencies that are considered overvalued, relative to the Greenback.

Somehow, this might relate to insane house prices in the San Francisco region, et al

For some reason maybe that can be correlated to Treasury yields, mortgages or whatever else is under the sun.

When did it become “unfair” to benefit by prudent borrowing at low rates for a long term? Some bureau committee inside HHS? Sounds more like punishing the responsible for the folly of the irresponsible.

I wonder where mortgage rates would trend in a world of mostly ARMs?

Down? Ha!, thats a good one.

It’s not unfair – it’s bad for the economy. We’re seeing why right now. In a world where the Fed doesn’t repress rates, push gobs of money into the economy, and dream up new programs to alleviate risk for lenders, then it works just fine. But with all this nonsense going on, I’m more for passing on risk back to consumers. Enough with the government skewing both ends of the transactions.

This is the issue. Short sighted Fed policy with ZIRP and especially unnecessary QE distorted the market and sent asset prices way beyond incomes across US markets and led to major inflation. Even in Boise Idaho. That’s the definition of failed policy, only recently being corrected when the Fed took inflation seriously. Should have happened far earlier and still needs to be more aggressive, esp on the QT side. Another case where Volcker is worth a read.

It looks like one should sell their home now before it gets worse in San Fran as the drop does not look to be over. If looking to buy, wait a few years.

Houses are TO LIVE IN and not to speculate with.

Nope. It’s both if you have the $. Take a look at Don Nelson, previously of NBA. He has 7 homes on Maui and normally uses them as STRs but now is housing folks displaced by the fire. Isn’t that wonderful.

You can’t do that if you only have one house you live in.

Totally agree with this. If this mind-set caught on more widely we could have avoided a lot of the bubbles strangling the actual productive parts of the US economy. Japan adopted a practice after their own real estate crash in the 1980’s that homes are for shelter, not speculation. And even with their other issues it’s done them a lot of good.

For your calendar:

Powell Speech, Jackson Hole, Fri Aug 25, 10:05 Eastern Time

I have no idea what he will say.

Whatever he will say, the hype mongers on Wall Street and in the social media — and some of the widely expected comments here — will twist it into “dovish.” We know that already.

CNN: Why stock investors are suddenly so scared

Many ‘investors’ are running a sizable profit this year – the S&P 500 is about 14% higher in 2023. But market losses have been piling up over the past month, particularly on growing fears of contagion from an economic slowdown in China. Inflation, Russia’s war in Ukraine and weakness in America’s banks also have Wall Street spooked.

The Nasdaq has dropped by 7.7% in August and the S&P 500 is down nearly 5% this month. On Thursday, the Dow closed lower than its 50-day moving average, a key threshold that investors often interpret as a bearish signal. The index is down 3% this month.

The CNN Business Fear & Greed Index, which looks at seven indicators of market sentiment, is showing signs of fear on Friday for the first time since March. That’s a big change from just one month ago, when the index was in “extreme greed” territory.

Canada RE news today:

Home prices posted the second-highest increase ever recorded in a single month after the one observed in July 2006, according to the latest Teranet-National Bank composite index.

That was just before the real estate markets crashed globally.

LOL. That was from the Teranet Index, which lags 3 months behind due to the sales-pairs methodology. I used to use the data but gave up because the huge lag that produces exactly these kinds of idiocies.

The Case-Shiller has the same problem in the US.

We’re in the era of Fed made boom/bust business cycles for decades now. But going farther back, every greed/mania has ended in a bust/panic. What we witnessed this time was unprecedented unhinged greed without restraint from too much cheap money. Its worth revisiting – look at the charts and see the mountainous upside trough to peak on the booms of the last 2 decades. Then look at the equal downside slopes that followed. That is a complete boom bust Fed cycle that literally erases all/most gains. Lets just look at housing bust 1. Pretty equal boom to bust though different regions fared differently. Now look at the upside trough to peak of housing bust 2. Imagine now its equal downside. Every single person, analyst, commentator, Fed speaker and politician is going to say this and that and have all these theories why this will do that and predict the future yada yada yada this time is different etc…but I say history, math and equilibrium has its own plan. We will get to par one way or another, white swan or black swan, war, climate disaster, financial crisis or unknown new path but it simply happens. Its the boom bust cycle The triggers can be considered irrelevant imho because they are often disguised so no one can plan for them. But the math is there and history shows a lot. This time is different? Only in that equilibrium might surprise on its path. I go with math and history. Look at the upside trough to peak of housing bust 2. Unimaginably unprecedentedly massive. Now imagine its downside to equilibrium. This is what I call reality. Drunken sailors give great and many fun excuses why this or that will or will not happen. Equilibrium chuckles. There is nothing that can stop it, only delay it. How much longer the delay? I just looked at the stock market. Did you? But hey in so many years we recover. Maybe..in so, so, so many years. But maybe not too. Great MMA fight this weekend. Lets get ready to rumble!

Hi Steve,

Not disagreeing with you, but you like so many prognosticators lack specifics.

What will home prices be a year, 3 years from now ? Inventory ? Where will rates be ?

Revision to the mean ? Even if nothing changed, which mean ?

But things do change.

Federer probably averaged winning 1 pr 2 majors a year for quite a while. No more.

Long term means are always changing, perhaps even in nature even if those changes can be miniscule ( I’m not a scientist).

If we go back 120 years for our average, perhaps the average size of a newly constructed home is 1300 ft². If we only go back 20 years it probably us more like 2300 ft². What are the parameters of our analysis. What factors do we include, leave out ? As such, what assumptions are we explicitly or implicitly making ?

I’m not pro RE, I rent, but much what I read either pro growth (or just stable) or pro correction/crash is a lot of speculation.

There are say 10 to 20 factors influencing residential RE prices. Commentatirs focus on two to four of those typically.

And even IF they took all 10 to 20 factors into account… how much weight do you afford to each of them ? How these factors are weighted can of course make all the difference in the world as to conclusions reached.

That said…

There may be some people who know what residential RE is very likely to do the next 3 years and even comment on it.

I have no way of recognizing these people…if they exist at all…from all the other chatter and speculation.

Most people (RE commentators) don’t know much about basic statistics. Don’t know what a chi squared or beta distribution is. Some might not even know what a distribution or random variable is !

They may not have heard of or understand statistical significance, Bayes theorem (not necessarily that relevant here) or Simpsons paradox (definitely can be relevant).

Heck most financial writers are oblivious to the importance of standard deviation (variance) as regards statistical inferences !

We live in a multivariate universe. I chuckle when I see “experts” talk about predictions based on one or two variables, or just look at lines and add more lines. Even apparently useful multivariate models may have missing variables, which, if known, could skew the results.

…and we all know what ‘assume’ does…

may we all find a better day.

DM: Bitcoin bloodbath as price plunges to two-month low amid $1 billion crypto sell-off – after Elon Musk’s SpaceX sells of $373 MILLION in digital currency holdings

The world’s most popular cryptocurrency fell below $25,500 on Thursday night, according to data from digital currencies specialist CoinDesk – the lowest it has been since mid-June.

From Chairman J. Powell, esq, last year at J. Hole:

“Former Chairman Alan Greenspan put it this way: “For all practical purposes, price stability means that expected changes in the average price level are small enough and gradual enough that they do not materially enter business and household financial decisions.”4

Here’s what the old duffer said in May 2023:

“Price stability is the responsibility of the Federal Reserve. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all.”

Some garbled crap from Fed minutes a few days ago:

“Those risks included an abrupt turn in supply chain improvements and “favorable commodity price trends,” alongside the possibility that economic demand might not slow “by an amount sufficient to restore price stability over time.”

The fate of San Francisco rests on price stability…

Freakin realtors…went to an open house in the neighborhood and had to see it myself. Seller just bought a year ago and is now TRYING to sell for over 100k more. I asked the agent and he said the typical realtor BS: a house is worth what someone is willing to pay for it. I said but what changed in one year other than higher rates? He said, he is confident there will be multiple offers. Okay then, good luck.

The dimwit is not the realtor. It’s the person who buys the home under the influence of FOMO.

I don’t know why millennials are so eager to fund early Boomer retirements. The sale of Boomer houses with $1M gains is icing on the cake.

Last I checked you can’t take your house and wealth with you to the afterlife. Aren’t boomers handing down their wealth to their offspring?

Some say, a million dollar home will be considered cheap in 20 years from now. Inflation?

Richard,

Boomers are between 57 and 77 now. The life expectancy of a dude who is 77 today is another 9.3 years. A dude who is 57 today has got another 22.7 years. For dudettes, it’s more (Social Security actuarial table). Many of us won’t be ready to check out for a while. You gotta be patient.

Nah, many will hand it to the nursing home. Last I checked anyway.

three things are certain in life. Death, taxes and RE prices that go up over the LONGTERM. Boomers like everybody else die at some point and the wealth gets transferred.

Wolf mentioned 20y. Can’t even imagine how much our house will increase in price in the next 20y. Easily 2x. Let inflation and time do the heavy lifting for you!

Richard,

“Can’t even imagine how much our house will increase in price in the next 20y”

Look at house prices in Japan, they had their bubble, and then good lesson, helps you imagine what can happen. Look at house prices in Tulsa, they had their bubble, and then from 1980 through 2015, 35 years of more of less downhill, despite inflation. There are lots of markets like that around the US. And you think your market is immune because it’s San Diego? LOL

Inflation means higher interest rates, which means lower asset prices until prices are in balance, and they’re not in balance. We know that because sales collapsed, even in San Diego.

It’s pretty rare to see such enormous declines. What’s even more painful is that for the vast majority of owners it’s a fully leveraged decline. A complete wipeout of their equity in a heartbeat. And likely many upside down. Stuck. For a long time. Good rates or not.

People who bought a few years ago are still OK. It’s a relatively small number of people that bought in 2020-2022.