Tightening is a slow process, and there is still a flood of excess liquidity chasing after yield.

By Wolf Richter for WOLF STREET.

Financial conditions for junk-rated companies have tightened only a little since the Fed started tightening in early 2022, from the loosey-goosey levels in 2021, and they remain loose by historical standards, though the Fed has jacked up interest rates by five percentage points in order to tighten financial conditions, including for junk rated companies. These junk-rated companies generally don’t have enough cash flow left over, after paying their operating expenses, to cover all their interest payments; in other words, they have to borrow new money to pay interest on existing debts, which puts them into a precarious spot when financial conditions tighten.

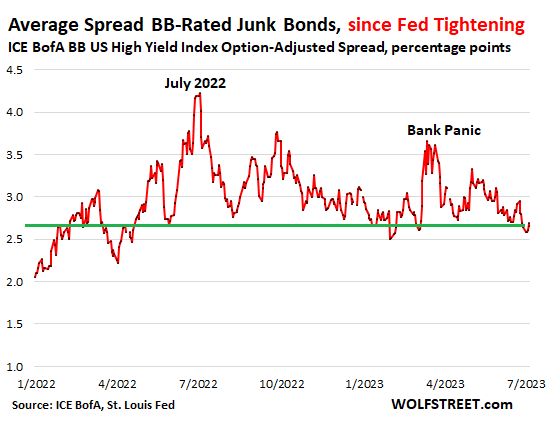

One measure of tightening financial conditions for junk-rated companies is the spread between junk-rated debt and debt that has no credit risk (Treasuries). For example, the average spread of BB-rated bonds, the upper end of junk (my cheat sheet for corporate credit rating scales by ratings agency) was just 2.66 percentage points as of Friday’s close (for an average yield of 7.13%).

That spread of 2.66 percentage points has narrowed from 3.6 percentage points in March during the bank panic, and from 4.1 percentage points in July 2022!

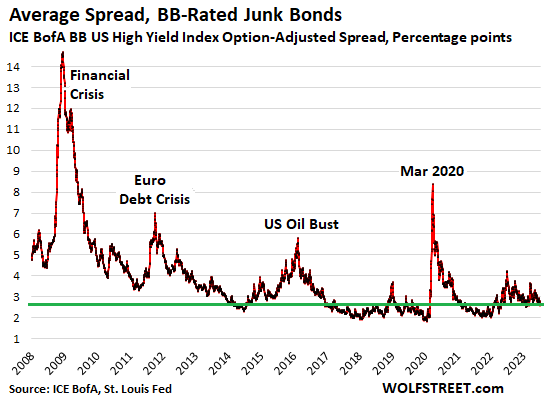

In March 2020, the BB-spread widened to over 8 percentage points. During the Financial Crisis, it widened to over 14 percentage points. So this spread of 2.66 percentage points is still narrow, still speaking of loose financial conditions, with investors still chasing yield and taking on risks with little extra compensation.

Here is the long-term view. This is one of the astounding signs of our times: still too much liquidity chasing yield, taking on big risks for little extra compensation, despite the Fed’s tightening:

Some companies that have long teetered go over the cliff.

Lots of these overindebted junk-rated companies will have to restructure their debts in bankruptcy court at the expense of stockholders, unsecured bondholders, even secured bondholders, and holders of their leveraged loans. That’s part of the cycle, that’s how it’s supposed to work, that’s how the corporate-debt burden on the economy gets relieved.

Investors got paid to take those risks, and they took those risks to make money, and now those risks are coming home to roost.

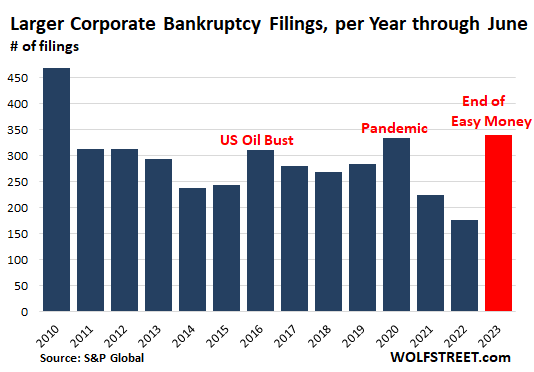

Bankruptcy filings by larger corporations in the first half of this year rose to the highest level since the same period in 2010, when they were coming down from the Financial Crisis.

Another 54 of these companies filed for bankruptcy in June, same as in May, bringing the first-half total to 340, according to S&P Global’s bankruptcy report for companies that are publicly traded whose bankruptcy filings list at least $2 million in assets or liabilities, and for private companies with publicly traded debt (such as bonds) whose bankruptcy filings list at least $10 million in assets or liabilities.

But they’re up by only 20% from the Good Times in 2019 and by only 9% from 2016, when the US Oil Bust sent a bunch of oil & gas companies scrambling for bankruptcy protection, though the Fed has now jacked up interest rates by 5 percentage points.

And in 2021 and 2022, bankruptcy filings had plunged to abnormal lows as the economy was awash in Easy Money trying to find a place to go.

During the pandemic, the Fed bent over backwards to bail out corporate America, including by buying corporate bonds and bond ETFs, including ETFs that focused on junk bonds. And it cut its policy rates to near 0%, and it bought trillions of dollars of Treasury securities and MBS over a few months, flooding the economy with what would ultimately be $4.6 trillion of insta-liquidity that went chasing after everything, and of course, now we have inflation.

So the Fed is now doing the opposite: interest rates are over 5% and QT marches on. And you’d think this rapid tightening – the most rapid in 40 years – would have a more serious impact on financial conditions and on bankruptcy filings.

And it’s sort-of astounding — I mean, nothing astounds us anymore here, but still — that the financial conditions are still so loose, and that corporate bankruptcy filings haven’t shot higher.

Sure, some badly managed banks collapsed, and SVB Holdings is included in this list of bankruptcy filings. Other companies finally filed this year that should have filed long ago but because of easy money were able to drag out the moment.

This included several big retailers – most prominently Bed Bath & Beyond, David’s Bridal, Christmas Tree Shops, and Tuesday Morning – that in 2023 finally joined the slew of big retailers that have filed for bankruptcy since 2017, and most of them were liquidated.

Their enemy wasn’t high interest rates and tightening financial conditions, but a structural change in how Americans shop: ecommerce. This retailer-bankruptcy-and-liquidation dance has been going on for years, and we here have covered it since 2017 under the category of Brick-and-Mortar Meltdown. And it will keep melting down year after year until it’s done, and tightening might only speed up the process.

Bankruptcies occur for a variety of operational and financial reasons, such as years of mismanagement and bad decisions (including over-the-top risk taking and binging on debt); structural changes in the economy, such as the shift to ecommerce; competition; inadequate cost controls; fraud, etc. And tightening is just a wakeup call. It enforces a discipline that ultimately produces better economic outcomes in the future.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The medicine has not reached an effective dose.

What medicine? This patient was on Placebo!

maybe maybe not

1st slowly then quickly

“Inflation” helps the disease!

(….in keeping your metaphor, a way of saying inflation is also bailing out the junk)

Lol, no tightening visible from the long term bond spread.

Also, I hear FHLB is providing liquidity (advances) as well to make up for fed QT.

Your second line — what you “heard” — is ignorant BS designed by morons for morons, and you fell for it with exemplary energy. I don’t know who’s spreading this BS. But it needs to stop.

The FHLBs borrow to lend. They do NOT create money, like the Fed. The FHLB borrowed $1.46 trillion in the bond market, by issuing $515 billion short-term “discount notes” (similar to Treasury bills) and $944 billion in bonds. Then they lent this money in short-term advances to the banks.

FHLBs are part of “wholesale funding” for banks – and always have been.

The flow is:

Bond market => FHLB => banks.

To replace:

Bond market => banks, or depositor => banks

Because the FHLB borrows every dime it lends, it does NOT counteract or “make up for” QT. This meme that FHLB lending makes up for the Fed’s QT is braindead BS designed by morons for morons.

The FHLB can borrow at a lower rate because their securities are “agency” securities, with similar tax advantages as Treasury securities, and then they can lend to banks at a lower rate than some banks can borrow at from other sources, such as from depositors or in the bond market. Banks reduce their cost of funding that way, and make more money. That’s what is going on here.

Banks could still borrow in the market or from depositors, instead of from the FHLB, but they’d have to pay more in interest. It’s padding bank profits by lowering the cost of funding. That’s all this is doing.

BTW, this $1.46 trillion in FHLB debt outstanding (“agency securities”) is not counted as part of the US national debt though the US government is on the hook for it. Same with other “agency securities.”

I’ll be first to admit that Wolf understands FHLB advances better than I do. Whether or not they matter in the big picture, they certainly think they matter. I gathered this information off of their website:

“In the 2008 and 2020 crises, the FHLBanks were lenders of first resort and stepped up to keep liquidity in the market when other funding sources dried up.”

To put things in perspective, FHLB Advances (per FRED) exceeded one trillion dollars (as of Q1, most recent data). This is higher than 2008 and higher than 2020.

Wolf was replying to Leo’s full statement: “Also, I hear FHLB is providing liquidity (advances) as well to make up for fed QT.” Your comment seems focused on FHLBs providing “liquidity.” As a result, you’re missing Wolf’s key point in replying to Leo: “The FHLBs borrow to lend. They do NOT create money, like the Fed.”

When you mention FHLB “Advances” exceeding one trillion dollars, you have to remember the FHLBs borrowed those “advances” and removed them from somewhere else in the financial system. That’s why the FHLBs do not “make up for” the Fed’s QT as Leo asserts. QT destroys money, just as QE creates money. FHLBs can’t do either, they can only transfer existing money from the purchasers of their bonds to the banks that use FHLBs for wholesale funding. In short, FHLBs can’t “make up for QT” because they can’t engage in QE.

At least that’s my understanding of Wolf’s explanation.

Thetenyear,

FHLB is a lender, period. Banks have access to those loans. When those loans are cheaper than deposits for some banks, and cheaper than issuing bonds, or preferred shares, or whatever, banks borrow from the FHLBs, to save money.

That’s how it is.

It’s up to policy makers in Congress to change that.

What is new now is that deposits have gotten expensive for banks… 5.5% for 6-month CDs? That’s a horror for banks. They can borrow for less at the FHLB.

“It’s up to policy makers in Congress to change that.”

Just to add to that: Why does the government have to back lending to banks — with the original intent of making mortgages cheaper? Why does the government have to buy-insure-guarantee three-quarters of all residential mortgages just to make them cheaper? The government is running the residential lending show, and it’s now further diving into broader lending via the expansion of the FHLBs. The government already owns $1.4 trillion in student loans. The government has issued loan guarantees for all kinds of stuff for Corporate America. In my opinion, the government needs to stop its involvement in all of this. It’s up to Congress. But that’s not going to happen.

Well said, and thank you Wolf.

The United States government should not be in the private or commercial banking business.

But don’t banks create money by lending it into existence? And the money is destroyed when it is paid back or defaulted on?

Why the US government is into lending and financial guaranties? Money creation. Money is created as debt and without money creation no monetary inflation and little possibility for the government to run budget deficits.

Hey Wolf,

It might help all of us here to get some more information on the FHLB and its activities. I’ve been looking at their bonds lately, but I’d love to get a more in-depth article from someone who is experienced with them (like you) to give us how they’re actually affecting the overall loan and housing markets.

I watched a good FHLB primer. They were born in about 1934 to try to help individuals get home loans by taking them on as collateral.

Ninety years later their mission has morphed to being a lender to big banks. Spiking FHLB loans mean banking system has stress.

“Spiking FHLB loans mean banking system has stress.”

What it means is that deposits have gotten expensive for banks… 5.5% for 6-month CDs? And then the inconvenience and expense of having to sell those CDs through a broker. They can borrow for less at the FHLB. And so they save money by borrowing from the FHLB.

Remember that banks’ basic business model is to borrow short and lend long. They need to borrow cheaply. But short-rates have gotten expensive. Banks used to borrow from depositors cheaply or for nothing. Now, deposits are fleeing to money market funds or Treasury bills if banks don’t offer higher rates. This comment section is full of these kinds of comments.

But banks cannot offer all their clients 5.5%; way too expensive. They’ll keep the sticky deposits at 0.1%, or 1% or 2%, and to replace the much smaller amounts of fleeing deposits, they raise money in the wholesale market: brokered CDs and FHLBs.

FHLB new bonds are listed at about 6%. With operational costs, etc, I don’t see how banks borrowing from them is cheaper than paying 5.5% on a CD. There is something I am missing?

It sounds like a bank can borrow from at least five sources – depositors, the bond market, other banks, the FHLB, or the Fed.

(I guess Fannie, Freddie, etc. are more for selling off loans/laying off risk rather than borrowing per se…although I can envision possible gray areas).

My guess is that the Fed has to be the lowest cost source of debt…but that it comes with more limitations, strings, and scrutiny. I would hope that the FHLB (with its implicit Gvt backing) would be the next least attractive to banks (but who knows…the FHLB may have been captured by the banking industry and act more like an insiders club than an Agency per se).

I wonder how much cheaper FHLB loans to banks are, compared to Fed loans.

The Fed’s collateral requirements are very tight. Depositors, other banks, and preferred stockholders (bond market) don’t require collateral at all. FHLB’s have much looser collateral requirements than the the Fed (mortgages including CRE, HELOCs, PPP loans, etc.)

I work in the Farm Credit System, we’re GSE wholesale funded. I wonder if people will look to it next as something to howl about if FHLB is suddenly getting so much attention.

The FHLBs were forced to bailout mortgage system during last Fin Crisis when Freddie and Fannie were bust.

I kbow it was a long time ago, but try to keep some historical perspective.

Yeah, just the opposite. The FHLBs are investing in O/N RRPs, draining liquidity.

If the Fed is serious about reigning in inflation it will raise rates. If it wants to forestall another banking crisis it won’t.

If the Fed is serious about reigning in inflation it will simply cease to exist

Sounds like banks simply use the FHLB to increase their profits. Why aren’t their lending rates at the same level or above free market rates so they become a lender when needed rather than when convenient and profitable to borrow from? how are their rates set?

Wolf, this is sort of off topic but maybe not, it being that you monitor how much money is available (e.g. too many spending like drunken sailors or too few) to do this or that in the economy.

We are having MASSIVE flooding in Vermont at present.

https://soberthinking.createaforum.com/gallery/soberthinking/1-110723120455.png

My home is not at risk but the destroyed road and bridge infrastructure and flooded homes damage will undoubtedly amount to many MANY millions of dollars, never mind the downstream negative effects of businesses closed for a few months while repairs are made. I suspect Property Insurance Corporation executives are not having a good day. I know the big Insurance outfits have a fund for these eventualities.

Obviously there will be a sort of boom in money available for those insured. I may be a pessimist, but I do not see how all this insurance money becoming avialble will actually help in the long run, simply because the Insurance corporations will resort to higher premium rates. Since you are an expert in these matters, I would be grateful if you would share your thoughts on the efects of all this insurance money becoming avialable now in Vermont.

The insurance companies will have to sell assets or else borrow against them to get the cash they pay out.

Good article

Oh it’s TERRIBLE to see all those rich people losing money like that! Has the FED not thought about the agony those people are going through…?

You don’t know what pain is until you have to cut your 10 night stay at the Four Seasons Maui down to 7 nights.

Seems like a good time to be short JNK.

Nope, been there done that and covered for a tiny loss. Like watching paint dry. You’re better off going after individual companies that are complete scams, like some of these restaurant chains that are bleeding red ink

Raise taxes. Claw back the free money that has nowhere good to go. Reduce inflation and reduce deficits.

And before the inevitable complaint: no, the idea is not to raise government spending. It’s only to reduce deficits.

Raise taxes? Question is on who? More politically impossible to raise taxes on anyone than ever.

Individual income taxes will go up in 2025 or 2026 when the Trump tax cuts expire.

And of course taxes go up on the working class…

Will also be a huge housing crash.

Not on anyone but on everyone? A cut on all transactions when money is transfered from one bank account to another bank account would be very effective.

Or maybe just have all banks to always round down the last digit and pay the last fraction in tax. 😉 Remember that story?

It’s current government spending that is substantially causing current inflation. Where do you think the demand is coming from? The US economy didn’t shut down during the pandemic (in 2020) and then miraculously come out booming on the other side. Such an inference is absurd.

To reduce inflation and deficits, government spending needs to be cut.

To get rid of this highly concentrated fake “wealth”, need to reverse prior QE and government spending, as that’s where it mostly came from. The US economy is nowhere near actually wealthier as it appears on paper.

To cut inflation government deficits must be cut. Government spending do not cause inflation as long as it is only tax collected that is spent.

Government may continue to spend as long as they tax accordingly. (With the implications that follow.)

what ever the fed reserve does the current federal government under cuts with ma$$ive $pending ! its seems every local-county- state governmental body is still struggling to get all the funds they have received from dc out the door !- cities are still getting “emergency covid funds” ! it will end but I for one have no idea when

It’s obvious and it was one of the routes to initiate massive inflation in addition to the PPP and other money handouts to the already well off.

Good article explaining junk interest spread. I still believe that the money managers are convinced QE is coming back and they just have to wait it out. They will be wrong.

I suspect lots of this crap is hidden away in funds that people own and know nothing about

It’s coming. Jamie Dimon said as much; US banks are going to consolidate and shrink and that means companies as well.

Keep thinking about the threat to the US dollar and you will be on the right side of what happens.

One thing to keep in mind is that your typical “leveraged” (ie, junk) loan has a term of 7 years and roughly the same for junk bonds (which long ago used to be 10 yr maturities…but which have been sliding for a long time…last year’s junk issues’ maturities fell to 5.1 yrs!!!…nobody wants to be owed money when the music stops…)…so it takes a while for “interest rate winters” to kill off junk issuing companies…whose true moment of truth is when they have to try and roll-over their debts’ *principal*.

(Although leveraged/junk bank loans typically have floating rates…which can apply the vise sooner, to a more limited extent).

And…these junk-y companies try to re-fi at lower rates whenever possible…so a whole lotta junk may have been issued in 2021…at 2021 ZIRP rates.

So, it may not be until 2026-2028 (when most/all of ZIRP era junk has to have rolled-over) that the full effect of unZIRP will have been felt.

And I’m sure there are plenty of speculators out there who are sure the Fed will have to pivot long before 2028…

Spot on. Private equity went nuts on low cost debt during the pandemic, and most of it isn’t due until 2025 or later. If rates are still high in 2025 there will be a private equity bloodbath.

Business cycles clean out the bad managers, concentrating first on those who are long on leverage and short on profits. The blood-letting seems nigh…

Though painful for their employees (and creditors), it is the worse for society if these companies are protected through policy/subsidy. But for Fed policy, many would never have materialized.

Wolf, is there any longer-term rule of thumb on BB spread-over-treasuries that you could point to as a “reasonable” target or norm? A post WWII average might be of interest.

This basically shows whatever Powell is doing to tighten financial condition is not enough or working.

And the astounding and infuriating thing is that when you read Fintwit or the front page of any economics website or newspaper you see one prominent pundit after another screeching for Powell to stop or even to start easing.

All these pundits and mainstream media are owned by the wealthy.

Wealthy don’t want the interruption to streaming of cheap money. Hence this clamor for pause or/and easing.

BTW: Powell already paused and I am sure he is waiting for good opportunity to ease and lower rates.

In next few years, I can assure you, the rates would be lower and fed balance sheet would be much higher.

I hope people can see through this and act accordingly.

No doubt he is waiting for a reason to lower rates. Won’t be this year though and not next year either the way things look now.

The bond market is waking up though and is factoring in one or two more 25 point hikes by the Fed this year at this point.

And depending on how stubborn inflation is there might be a need next year for at least another two to four 25 point hikes.

These central bankers are really gunning for a head-chopping. I guess they didn’t learn from the French Revolution.

Huh? Bankruptcies up, but tightening isn’t working?

We are literally in the 1st inning of a 9 inning game. There is going to be plenty of bankruptcies happening in the future.

Economies the size of the U.S. do not turn on a dime. Especially after 30 years of easy money. It is going to take a few years for all of this to work itself out.

Christmas Tree Shops was largely a browsing and impulse buy place, along with some regular staples, like a big step up from Dollar Tree. Used to go to the one around the corner almost weekly for this or that, better prices than online too. Place was always packed, could never get down an aisle and long lines at the reg even a weekday. On weekends, forget finding parking or a cart. Not quite as enjoyable as back when it was a dollhouse inside and out, but it certainly helped stretch the budget during the daycare days.

About a year ago it lost its huge selection (supply chain issues?) and got comically overpriced. All but stopped going, popped in randomly last month and it was deserted at 2pm on a Saturday. Was a bit of a zoo yesterday for only 10% discount on what little was left. It needs to die, but I’ll miss it.

Lili – I miss Minderbinder’s egg arbitrage in Jos. Heller’s ‘Catch-22’…

may we all find a better day.

I am a big believer in looking at 100 year history of valuations. Stock market is still in the 90% plus percentile on many valuation metrics and the junk bond market is priced for close to perfection as well. At some point we will have to swing to the bottom percentiles on a price to sales or market cap to gdp measures.

I think just falling to long term median is about a 60% lower valuation on the SP500 and junk spreads would blow out to double digits. But one day we will challenge the all time valuation lows which is price to sales or market cap to gdp falling 80% or so.

I did that for a long time, too, waiting for the stock market to revert to historical means. I think, though, that e-banking changed the dynamics efficiently that the new average is now higher. There’s simply more money from more people which makes for more demand with the same supply. I wouldn’t say that the current market is fairly valued but I would say that the “historical mean” is going to have changed since investing in the stock market became so easy.

There is truth in what you say, but there is a limit to how much you can grow the multiple on sales. In other words once you have grown the multiple from one to 2.4 you have to keep it there. It was a one time joy ride due to zero rates and zero competition on interest bearing accounts.

With short end rates at 5% plus and rising and interest cost for companies rising I could see mean reversion happening this year. Maybe even an overshoot on the down side if Fed has to go higher to break inflation.

The change is completely psychological and caused by human beings which means it can and will reverse. This is just a long cycle.

The so-called “fundamentals” never bought a single share or other asset and no, it’s not different this time either.

The difference is that the outcome will probably look different on a price chart because of future inflation, so nominal prices may not look like 1720 or the 1930’s.

I don’t think it is only psychological. There are simply more people doing investing which means more money chasing the same supply. That’ll raise the baseline.

There are certainly some major psychological factors related to this that will likely abate some over time but to what degree I don’t think anybody knows.

It would also be revealing to examine the maturing issues for the ICE BofA US High-yield Index used on the chart.

Especially the next 3-4 years, in which I suspect the majority come due.

My old boss once told me good times breed bad businessmen while bad times breed good businessmen.

Seems we might be on the back side of record breaking “good times” at this point. Hope we haven’t completely lost the ability to manage in bad times.

I expect some big luxury designers to go bust by next year. They keep increasing their prices while the quality and design are in decline. Some of it is just pure junk not desirable at any price. Even the perfumes are not great anymore.

Glad to see you posting again Petunia…

Does that in your view refer to Versace, Jimmy Choo and Michael Kors? I’m asking out of curiosity because Capri Holdings Limited (CPRI) which owns these brands seems to be trading at a discount (PE 8 and stock price down 45% over last 5 years) and although it has a lot of debt I don’t see any obvious insolvency issues. I’m curious if that’s who you had in mind. Disclosure: I don’t own any CPRI stock.

Honestly, all the major design houses are overpriced and underwhelming. Why anybody would spend 10K on a Hermes, Chanel, or Dior bag is beyond me, and I am an admitted fashionista. The exclusivity in my opinion is a big fat lie, these bags are everywhere.

These are the kinds of results you get with a fake inflation “fight.”

Don’t show up to a gunfight with just a knife.

I’ve particularly liked this one:

‘I don’t like to engage in a battle of wits with an unarmed opponent.’

or

‘No good deed goes unpunished.’

I think even those can be viewed in context of the federal reserve and the accumulation of so much power by the apex financial institutions that they no longer need to justify their activities to anyone or maintain a consistent enough system that the logic and rules of it can be trusted by the majority of people. Another way of saying it is, there is such an imbalance of power that those with the power don’t need the consent of those they rule over.

That’s what should happen (from a logical and moral standpoint), but will the Fed allow it? QE and inflation are powerful tools to support asset prices, while avoiding excessive push back from the silent majority. The Fed reports to the top 1%.

Meant as a reply to Old School.

What FED intends to do is ample clear by what they have been doing for last 15 years or so.

Now FED has to do the charade of tightening by hiking rates and QT which are not really making any impact. FED can at least say, they are trying but they very well know that what they are doing is not enough.

Don’t believe me, look at the data for last 15 years or so. Home prices going up again, stocks/cryptos all up again.

How can you day it hasn’t made any impact? Inflation has dropped from the high single digits to the mid single digits. Sure, it hasn’t dropped to less than 2%, but I don’t think that is the plan.

Bankruptcies are up, liquidity is slowly draining from the pool. Sure it could go faster and further, but that might have much more adverse consequences.

2% or lower inflation is the plan.

Why? For the simple reason that the entire house of cards is built with the expectation that inflation is between 0% and 2%.

Getting outside that range is bad for the system regardless on which side you get out of it. It is just that it isn’t bad immediately so they can take some time instead of getting Volcker out of retirement

Speaking (loosely) of loosening, house prices are now *up* YoY according to Black Knight.

Only by 0.1%, but up is up–and there were a lot of people here plugging their ears and refusing to hear stories of packed open houses and bidding wars having returned to some metros this year. I guess now you’re going to have to plug your ears and refuse to hear hard data? Sure, this is just Black Knight, but what will you do when Case-Shiller inevitably reports the same? “Prices always go up during spring selling season” only works as a hand-wave for so long.

When Powell promised a “bit of a reset” in housing last year, many of us hoped he was employing his usual understatement and that he really meant a significant reset. As it turns out, on a national level we no longer even have the bit of a reset–just the same batshit prices but at higher rates. And the West coast metros where prices are still down YoY are closing that gap.

And the MBS rolloff continues at its glacial pace, accomplishing close to nothing, with no sign of outright MBS sales any time in the future.

Think of an aircraft carrier turning at sea, it takes a long time but once it begins its hard to stop….They just started turning it…

Case Shiller and the National Association of Realtors DISAGREE with Black Knight:

https://wolfstreet.com/2023/06/22/home-prices-drop-year-over-year-by-most-since-2011-as-investors-pull-back-amid-dismal-sales-and-rising-supply/

NAR: In May, the median home price declined by 4.3% from the peak and by 3.1% year-over-year, and the largest since December 2011 during Housing Bust 1

Pea Sea – The one part of you are not including is that now Treasury is issuing a pile of Treasuries and over time, this will drain excess liquidity. Last time the Fed reduce the balance sheet it only took a while before it hit the stock markets.

Real estate will take 3-5 years to hit bottom. At the end of this cycle, there will be a ton of pain and foreclosures.

Or at least a historically normal foreclosure rate.

I’m wondering if the pandemic has caused a structural shift in how foreclosures will be handled going forward.

I’m guessing there will be heavy pressure on mortgage servicers to offer 12 month forbearance as standard operating procedure.

Whether that’s inhibiting price discovery or good policy will remain to be seen.

Home builders stocks need to roll over before any type of crash will occur. I am amazed at how strong they are. Wall Street looks ahead and right now they do not think builders are not in any danger a slow down in building. During HB1, the home builder stocks rolled over and started to crash in 2006 and lost almost 50% within by of their stock price by 2008 while all the other indices where making ATH. Then median prices of homes rolled over a year later in 2007 and finally the stock market crashed in 2008.

The home builder stocks will roll over, and then you may really see a drop in house prices. I have tried shorting these home builders so I am not a real estate shill. Also it is a hedge against my rental home price appreciation.

What I am seeing in my area is houses in the lower 50%tile are still going up in prices. The 2022 $300k houses are now $330k. Houses in the upper 50%tile are flat or dropping a little. I see houses listed above 1 million have dropped $100k to $200k. If I go look at new home subdivisions. The homes that were priced $550k in 2022 are now priced at $580k. If I look at new home subdivision where homes were 950k in 2022, they are $940k in 2023.

So most people on this blog are probably looking at houses at or below the median and thus most will post comments saying house prices increasing.

That is what I’m seeing in my southwest metro area. Affordability sucks compared to pre-pandemic times, but it’s much better here than lots of other places. There’s a really noticable cutoff right at $400k here. Houses below $400k in my neighborhood list on Thurs/Fri and are reliably pending by Monday. $400k-$450k listings are sluggish, and houses above $450k mostly sit. Buyers still jump fast on anything they see as an opportunity, but there’s a profound change in the mix.

I hightailed it out of the failure pile that is CA and bought a nice pueblo-style 1,600sqft house on a 1/4 acre corner lot in a nice neighborhood with the best schools in town in 2022 for $335k. To my absolute amazement, a similar house across the street on a smaller lot closed last month for $385k. A somewhat fixer-upper on a tiny lot up the street just went pending at $390k after being listed for a weekend.

These are the effects of huge lightning-fast money printing up against cautious and ponderous tightening by the Fed. Higher interest rates are having an effect at the higher end of the market, but plenty of buyers are still desperate to buy something even if it means lowering their standards to pick at whatever scraps fall to the median price or below.

Same batshit over-valuations…but with 33% YTD fewer sales in CA. (Thank you, unZIRP)

Fine so long as for-sale inventory remains at 10 yr lows…and nobody in CA ever dies, changes job locations, or retires ever again…

But as those things actually occur, for sale inventory accumulates, prices fall…and then the (over-leveraged) screaming starts.

(“The house…is calling from inside the house!!).

“I guess now you’re going to have to plug your ears and refuse to hear hard data?”

Except it’s not hard data, it’s seasonally adjusted. Why would you seasonally adjust year over year data? The whole point of the year over year number is to remove variances based on time of year (seasons).

I’m not saying they are wrong, I’m saying it’s not hard data.

Black Knight?

My cousins, barber’s pedicurist’s landscaper says that home prices are up even more.

In northwest Chicago suburb of Palatine it seems from a Zillow search that more than half the homes listed in the 400-600k range are vacant.

Not many moving in that range, though subjectively it feels like many fewer than usual listed.

The action is below 300k

Maybe if someone convinced Powell & Yellen to *** Stop Bailing out Billionaire Uninsured Depositors ***

Then the liquidity might slow or freeze. But the Billionaires are in control of our Plutocracy, the Law is ignored or made up.

“Reaching” for a mere 2.6% in yield over safe Treasuries is the definition of insanity.

I hope a lot of those junk bonds have a little surprise in store for investors in the next 3-5 years. Perhaps getting familiar with the rules of Chapter 11 bankruptcy would be a good start. Hint – if its not secured debt, you could end up with pennies on the dollar, or even nada.

Wolf,

Isn’t the credit default risk on the average junk bond currently running around 1.5% per year?

How does that compare to previous credit spread fluctuations?

Back to normal, from abnormal lows, expected to rise further:

Here is about “leveraged loans,” which are a good indicator. They’re issued by junk-rated companies, but banks sell them (too risky for them), either as loans to be traded, or they’re securitized (CLOs, etc.).

In June, 4 issuers of leveraged loans filed for bankruptcy (they’re included in the 54 bankruptcies above), bringing the default rate to near 3%. Over the past 12 months, $24 billion in defaults, via LCD/Pitchbook.

“After sharp rise, US leveraged loan default rate finally nears historical average,” approaching 3%. “Market pros expect the rate to climb higher still,”: LCD/Pitchbook.

Thanks. It is amazing with the current default rate that credit spreads haven’t opened up.

Are you seeing increased covenants in leveraged loans and/or convertibility features coming in yet? I haven’t found a lot of evidence of this becoming widespread to date.

And I am amazed this hasn’t happened yet.

During the dot com meltdown, it got started mid 2001.

This cycle, the downtrend began November 2021, so I would have expected this showing up in a big way by January of this year, but no dice.

I am really having trouble understanding why the bond market is not whipping out the standard asset backed security agreements by now.

There ***SHOULD*** have been enough defaults by now.

What explains this?

Yes, investors are demanding and getting more investor-friendly terms on junk-rated bonds and loans, including the biggie secured bonds instead of unsecured. Covenant-lite deals are apparently a little harder to get done.

Home prices going back up in May 🤣

Market still frozen, mortgage rates at record highs.

What a mess 🤮

In May, the median home rice fell year-over-year by 3.1% to $396,100, the fourth month in a row of year-over-year declines, and the largest since December 2011 during Housing Bust 1, according to the National Association of Realtors.

https://wolfstreet.com/2023/06/22/home-prices-drop-year-over-year-by-most-since-2011-as-investors-pull-back-amid-dismal-sales-and-rising-supply/

It rose by 50 percent plus in last 3 years

So it is soothing to hear that it fell by 3 percent or so.

:)

Remind me Jon are you in SoCal?

Recall that per Case-Shiller during the last bust, the first year of price declines after the peak was about 4%…..

Patience my friend, let’s reconvene in 2025 and take stock of values and trajectory then.

Yeah — rocketing all the way up to the top of the bottom.

Not record highs. I built my first house, barely qualified for a 30 year mortgage with a 10.5% rate. Somehow survived and moved 3 times since.

Hopefully it’s not the old playbook of load up on debt, take massive dividends and dump on the poor old Stockmarket retailer. You gotta read the fundamentals of the business and see which management has skin in the game

I’m getting close to 5% on my Treasury MM fund. Why would anyone want to venture into the junk bond market and take that risk for a minuscule extra interest rate. Well, some people are stupid but greedy.

Agreed.

A 2-4% annual premium for a junk bond (that will lose 80%+ in a bankruptcy) seems way too thin to me.

If junk companies have a 10% annual chance of bankruptcy (guessing here), then the annual “expected loss” on their bonds is 8%…for which people get 2-4% over zero risk Treasuries.

If the annual chance of a junk bankruptcy is 20%…their expected loss is 16%!!! For which buyers happily accept 4% Treasury base + 3% Junk premia…

Man…that is some thinly sliced baloney.

Clearly they don’t think the risk is 20%. They’re expecting that the government or Fed will bail out either their borrower or them directly. I’m not saying they’re right or wrong, just that that is their thought process.

Don’t worry, everything will be “bailed out” with a super tanker worth of “liquidity,” just watch.

I think you are wrong. Let’s bet.

I think there is a far difference between responsibly gradually deflating a 30 year bubble and panicking and sending super tankers (helicopters not big enough???) of money.

The other day I went out drinking one night after work. I will admit I had more than I was planning to. I went home and went to sleep and set my alarm to get up and go to work knowing I wasn’t going to get enough sleep.

The next day at work sucked. I was hung over and tired. It was a terrible day.

Though according to several posters here, I was dying and probably should have stuck a gun in my mouth.

generative AI talking … crap in crap out

Rate hikes, QT, QE, CPI, Inflation, we all know the stats.

The bottom line is the FED will never allow markets to crash or come down to any return of pre pandemic normal as the COST of ever trying to take care of most people, rejuice the system, etc is just too HUGE to even consider.

Unless the less haves start rioting willy nilly across the land ( if they can leave the comfort of their easy chairs, remote, Netflix, Candy and soda)….

It ain’t going to happen…get used to the new normal and emotionally remove yourself from the game, watch and observe.

I hope everyone here has built up a nice nest egg to survive comfortably.

Enjoy.

This has been my opinion after going over things over the years.

Fed works for the wealthy and won’t allow the asset prices to discover true price.

But at the same time Fed needs to have this charade going on that they care for common joe. It is a tough act.

But with the current rise in asset prices of all kinds and fed now paused it should be clear to everyone that for whom the fed works.

I see inflation going down but it already damaged poor and middle class.

Essentials of life are out of reach for most.

Currency devaluation is the end game which is happening right in front of us for last fe decades.

It’s like a slow boiling frog.

I’m starting to come around to this line of thinking. The problem is that assets are so heavily concentrated among a small group , and since money is fungible, it’s easy to rebalance from stocks into housing, which is why housing is now out of reach for so many. The Fed needs to deflate the asset bubble, and by a large amount.

One place where I don’t agree though is that the pause is the issue. The problem is the gargantuan balance sheet. It should be down to $6 billion by now.

The current balance of the Federal Reserve balance sheet is around $8.3 TRILLION and should be considerably higher in my opinion as it supports a $22+ trillion a year US economy and hundreds of TRILLIONS of dollars in assets.

Don’t worry, the FED balance sheet would be much much higher in next few years.

It’s a matter of time when FED would start buying all sorts of bonds and cut rates.

jon,

You may be bitterly disappointed with your fervent hopes for bond buys, LOL. If the Fed cuts rates from 5.75%, by 2-3 percentage points, over four meetings, any recession will be gone, and it won’t buy bonds. And by that time, inflation will resurge again.

It bought bonds as stimulus when its rates were already at near 0% and it couldn’t cut further because its rates were at its “lower bound.” The Fed doesn’t do negative rates, not even during the big-bad Financial Crisis, and not even during the pandemic, as you can tell, and much less during a run-of-the-mill recession.

It might even continue with QT after it cuts rates – this has been discussed many times and is now on the table as a real possibility. So that would be the opposite of your scenario.

The surplus in the supply of loan funds has kept junk bond rates lower than they otherwise would be. The economy is being run in reverse.

Wolf,

Aye, the current narrow spread for junk reminds of an earlier era. The spread was just 2.68 on Christmas Eve, 1999.

Complacency has consequences…yet the addict never recovers until first hitting rock bottom.

The reverse repo balance at the Fed is $1.8T. It’s not unreasonable to think this balance represents an approximation for the amount of excess stimulus created by the Fed. Think about it, banks would rather park money at the Fed versus loaning it out at higher rates. In other words, the big banks have very little confidence in the economy at the present time. Meanwhile equity investors could care less. Eventually, something has to give.

Cue the Market Rally!

Market knows the fed will bail out no matter what, no place to go but up.

Maybe a lot of it is due to global money being invested in these zombies rather than American money? RE is moved at the margins, is this sort of money as well?

Also, what bank loans money to anyone, even a well connected company, to cover just the interest on loans? That doesn’t make any sense to me at all.

Bed, Bath & Beyond is a prime example for a company that was done and over, but then some “financially connected” financiers bought it Out, piled huge amounts of debt on it, Shot the Share price to the moon (no problem if you know the right people) and made a Killing by looting the corpse right before it finally went down. I think there is also an episode of “The Sopranos” that explains how that works.

My guess is the same people are buying those junk Bonds now.

So, is this what are called vulture capitalists? But who would loan money to them? It makes no sense unless it is just a giant con job.

BB&B was always a poor bet. You could pay $79 for a shower curtain there, then walk a half block in the mall and pay $7.99 for the exact same thing at a different store. Same with many other items. Blanket $250 and $49 at the other store. I went in twice and walked by several times and there were never very many people at all and I only saw one person ever buying anything.