Price cuts and mortgage-rate buydowns pull sales from previously owned homes.

By Wolf Richter for WOLF STREET.

Homebuilders have cut prices, they’ve built at lower price points, they’ve offered mortgage-rate buydowns and incentives, encouraged to do so last year by plunging sales, a huge wave of cancellations, and an inventory pileup. Dropping input costs and unsnarling supply chains have kept their margins halfway intact. And buyers have come – shifting from buying previously owned homes, where sales have plunged by 20% year-over-year, to buying new homes.

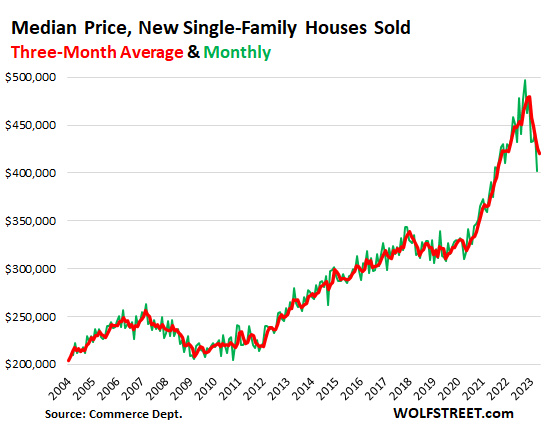

The median price of new single-family houses sold in May fell by 7.6% from a year ago, and by 16% from the peak in October, to $416,300, back where it had been in September 2021, according to data from the Census Bureau today. But these prices do not include the mortgage-rate buydowns and other incentives.

Median-price data jumps up and down a lot (green line). The three-month average (red line), which reduces some of the noise to show the trends, fell 6.3% from a year ago, and by 12% from the peak, to $420,200, the lowest since November 2021:

The average price of new single-family houses dropped by 6.6% year-over-year to $487,300, down 14% from the peak last July.

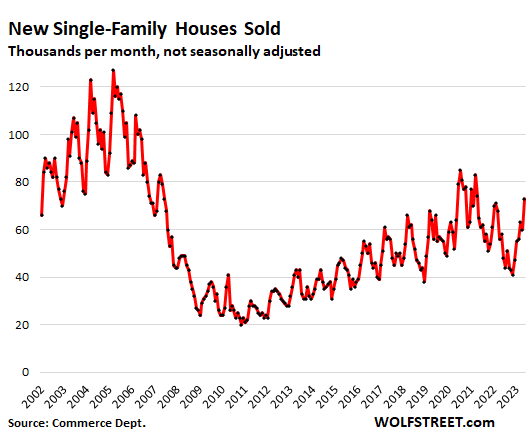

The seasonally adjusted annual rate of sales of new houses jumped 20% year-over year to 763,000 houses, and was up 23% from 2019.

Actual sales – not seasonally adjusted, and not annual rate of sales – jumped by 25.9% year-over-year to 73,000 houses in May, the highest since the pandemic bubble in the spring of 2021. Compared to May 2019, sales were up 30%.

These “sales” are sales orders, not closed sales. Cancellations are not subtracted. Many of the sales orders in late 2021 and early 2022, which show up in this chart, were then cancelled in late 2022, amid a huge wave of cancellations as surging mortgage rates made buyers unwilling or unable to stick to those deals at those prices.

Since then, lower prices and mortgage-rate buydowns have stimulated sales, but sales remain well below the booms during the pandemic and during Housing Bubble 1 from 2001 through 2006. So this isn’t exactly something to write home about, but they have come up a lot from the lows late last year and are above the sales levels in the years just before the pandemic:

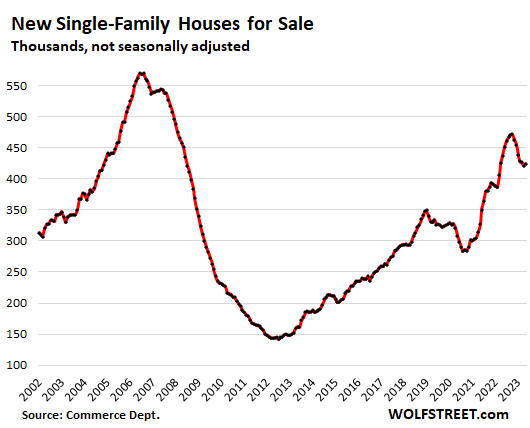

Inventory for sale in all stages of construction rose to 424,000 houses in May from April, the first month-to-month increase, after six months of declines, since the inventory pileup late last year. Compared to May 2022, inventory for sale was down 3%, as the lower prices and mortgage-rate buydowns have been successful in working down part of the inventory pileup, but the current surge in housing starts is adding more inventory. And that’s a good thing:

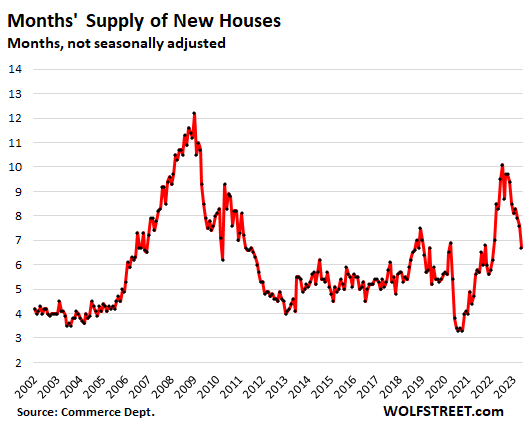

Supply has fallen from an astronomical 10-month supply last July, to 6.7 months in May.

Elbowing in on sales of previously owned homes. Homebuilders are the pros. They’re going to have to build and sell houses no matter what the market is. And they responded to the market and offered deals – while homeowners are sitting on their hands, trying to outwait this market. And benefitting from this disconnect, homebuilders have pulled in buyers that would have otherwise bought a previously owned home.

And so it makes sense that construction starts of single-family houses jumped in May for the fourth month in a row, after a big drop in the second half last year as unsold inventory was piling up. While still below the peaks during the pandemic bubble, starts of single-family houses in May were 18% higher than in May 2019.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My neighbor got transferred and so has to sell the new ( when purchased) house he has been in for only a year and a half. First weekend ( open house) it was crickets. Before second weekend of open houses he cut the price by $40,000 and the crowds came swarming in. If he sells for that new price he will be able to cover selling costs and get his down payment back plus a bit of change left over. But most homeowners are not as rational as this guy and tend to ride the market down cutting prices tool slow and staying behind the curve the whole way down.

It’s always best to be the first one to cut prices on the block.

Better to be on the train than under it.

“Supply has fallen from an astronomical 10-month supply last July, to 6.7 months in May.”

And the Realtors keep saying that there is no supply!

10 months isn’t astronomical. 6 months is normal.

What weve been seeing over the past 2 years of under six months is normally unheard of except in extremeely hot markets.

Hopefully his employer will pay for his moving costs.

Employers and recruiters are low-balling candidates as there are too many laid off folks searching. Bad time to switch.

Transfers usually come with moving costs and realtor fees paid

Where are you getting that info from?

So the days of your company buying your house when they transfer you are gone?

Back in 2009, a 30 person department where I worked were told that if they wanted to keep their jobs, they had to be in the new office 1500 miles away within 3 months. No moving or house selling financial help. They were offered a small severance in a terrible job market if they decided not to move. I have not heard cases like that yet. Most companies are just trying to get people back into any office.

In auto racing, the first guy to lose is still on the podium. Your neighbor sounds wise in that he did not will to be the last to lose.

Wolf – I still feel this is astonishing given 7% 30 year fixed. I get the rate buy-downs, etc., but even with that new home sales are surging even higher? Where is this supposed recession? LOL. Commercial real estate crash incoming!…nope not really. I continue to say what I see in my market and it is depressing and shocking as a buyer on the sidelines. In my market: home prices for existing homes very sticky high and more than a “seasonal” uptick, inventory at record lows, buyers are a plenty and ready to pounce quickly, new home builders building like crazy and selling with buy-downs “free” upgrades, etc., Teslas everywhere, bars & restaurants are absolutely packed, layoffs?…not here. The coming recession is cancelled. Mr. Bluffer Jay Powell has refused to truly bring house prices down meaningfully as he promised he would (shocker) “bring into balance” LOL. MBS sales – where are you? Real rates are arguably still negative/flat/stimulative, and not restrictive as they are at or below CPI and real life inflation, and the QT is anemic. So sad. Am I wrong? I know many feel and see what I reported here.

LOWER PRICES are the cure for slow demand. If the price is low enough, you can sell anything. They sold empty old office towers in San Francisco for 70% off the 2019 price levels. They sold empty office towers in Houston at an 80% loss to the CMBS holders. Existing home sales are way down because prices haven’t fallen enough — though they have fallen in most places.

The recession that has been ballyhooed for over a year, well, I’m still waiting for it and looking for it. Inflation will be higher for longer, and rates will be higher for longer. And residential real estate is a lot slower moving than CRE. But homebuilders have gotten the message.

Wolf, I did a deep dive into historical data on investment real estate cap rates in Toronto. I found that since the 1980s cap rates and the prime rate have been closely related. In 2006 I bought a small apartment building that was returning 6% net, prime rate at the time was about 6%. In 2018 when the prime rate was about 3% I sold the property at asking price which was priced at a 3% cap. I was lucky. If cap rates where to be close to the prime rate today prices need to fall by more than 50%. A friend said I’m oversimplifying. Maybe I am. But maybe we will return to the norm. I’m waiting patiently. Sellers are waiting for interest rates to drop, buyers are waiting for prices to drop. The result is a market with little activity. Everyone is waiting.

Everything new sells the day the sales office opens in Markham, Canada. Richmond Hill is the same.

If you had to venture a guess, Wolf, how much longer are we going to be waiting for it. Looking to be a first time home buyer, but don’t want to be left holding the bag. How much of a “buydown” would be acceptable to mitigate the risk of impending losses down the road?

JR,

If you have the urge to buy a home, and if that is what makes you happy, buy a home. And if the market tanks on you, don’t worry about it, make your payments, and quit looking at Zillow every day to find out how much money you lost. Live there for 30 years and pay off your mortgage and you will be fine. Just don’t expect to be making $500k in profit on a $20k down-payment over the next five years.

What wolf said. But if you are really into the numbers there are mortgage calculators online that have fields and sliders to show how much your “points” can impact your monthly payment. Basically pay few thousand now for a lower interest rate now, pay a hundred or few hundred a month less, and you will recuperate the cost in 3 or 5 or 7 years. Similar to how you do hybrid car vs non hybrid car calculation. How and why the home builders are doing this is also based on careful calculation. If they pay your points for Z, and can sell the home for higher price Y, and help you save interest over 30 years X, and X>Y>Z, then why not? It’s a win win for both of you since the bank makes too much money anyway.

Final note: the above is fine tuning of cost and life planning. Nothing can prevent an “Impending losses” if or when it happens. Keep monthly payments manageable and with a fixed rate. Good luck!

Thanks, Wolf. I don’t mind waiting another 6 months or more. Will I be better off waiting for higher interest rates, hoping they will drop prices substantially to lower overall financing cost? Or is it looking more like a 2- year game to buy at the “bottom?”

How do you think the bailouts are going to impact single family housing prices and rates?

With increasing inflation rates, it’s difficult to track “price drops” and actual home value. Are your case-shiller charts the go to for this?

When does spring selling season typically end?

My town is the same way. Same overpriced, never updated 50+ year old homes on the market for 2020 prices. The price existing homes are listed at hasn’t dropped, but rates have gone up, so now you’re paying even more for the same less as 3 years ago.

All of the new construction is still unbuilt and sitting at $800k+ asking because builders got the land basically for free 3 years ago.

Until there is some real pressure on homeowners to sell homes, there will be a relative dearth of homes for sale and homebuilders will do well.

What we really need is to reverse decades of poor policy on housing.

1. Cut the mortgage interest deduction (there is no reason to subsidize home ownership, it merely increases prices)

2. Dramatically cut the red tape and costs of regulations for building new homes. The cost of regulations on new homes is up to 25% of the total price.

3. Privatize the whole mortgage market, so there is no longer a subsidy from the government. This would help to reinforce market pricing of risk.

4. Force originators of mortgages to keep their mortgages. The current method of having originators package them into MBS causes problems with risk management that will keep cropping up until originators actually have to bear the risk of default.

To go even further:

5. Cut the maximum length of a mortgage to 15 years. This would allow people to pay off their mortgages, reduce interest costs and help to fund retirement savings (because a major expense is paid for).

6. Restrict large financial institutions from owning homes for rental.

7. Increase taxes on land ownership – provide less financial incentive for hoarding of vacant land, which will increase home-building and suppress scarcity.

Along with the trend toward remote work, we can ease the scarcity premiums on land and provide better, cheaper housing for millions of people.

Overall, we want policies that incentivize new home building (which creates jobs and allows us to upgrade the housing stock over time) and we want to disincentivize the financialization of the housing sector (land hoarding, rental ownership, interest payments to banks).

Howdy, As a newbe here and dont take this the wrong way, but NO thanks.

Also, tax short-term rental properties as commercial, as it’s being used for a commercial purpose. This is easy to enforce in places that have gone to registering short-term rentals. Want to convert to a long-term rental or live in it? Fine, you give up the short-term rental permit.

Sounds like a nifty way for politicians to give tax abatements to those hedgefunds buying up houses.

If they rent them out long-term, they’d pay the same amount in property tax they do now, or perhaps less since commercial tax receipts would be higher. And it would incentivize them to rent long-term instead of short-term, driving down rents. So I’m not sure what you mean, or how renters would be hurt.

Commercial developments in my neck of the woods often receive tax abatements.

For example, Tesla’s facility outside of Austin will save over $50.4 million over 15 years in school taxes thanks to generosity of parents whose children attend school at Del Valle ISD.

Tesla just purchased 6,000 acres outside of Austin to build their very own town. I wonder if it will be taxed?

I’ve worked with pretty large hedge fund managers (and tangentially dealt with PE firms) and this doesn’t happen. It would be horrible optics for politicians to go along with it in the same way they do for big businesses looking to build factories or new headquarters (doesn’t provide jobs or cache).

There have been a few instances where HFs have cut deals with other countries, usually in the Third World.

Many areas already tax short term rentals same as the hotel business

I mean property tax (which the property owner pays) rather than sales tax (which the renter pays)

1. “Cut the mortgage interest deduction (there is no reason to subsidize home ownership, it merely increases prices)”

Oh! You mean just like Student loans (no reason to subsidize someone’s college education) where the cost of easy money drives up the price of education at institutions of higher learning?

Yes JimBob, exactly like that. College costs have averaged +5% inflation since 2000. The lack of bankrupcy protection for lendees is also a mistake.

“you took out a loan, now pay it back”

“you gave a 18 year old a 200 thousand dollar loan for a basket-weaving degree, now write it off”

These statements are not mutually exclusive.

The theory behind “investing” in a degree is for the student (borrower) to improve their earning capacity by pursuing a degree that will provide income to repay the loan and provide prosperity in their future.

The loan amount should be commensurate with the degree being sought. A degree in underwater basket weaving has a market value of near zero, so such a degree should be self funded if that’s the area that you wish to study.

Student loans should be like betting on a horse race. Highest potential should get the biggest purse.

Oh. And you can thank the high earners (i.e., doctors) for defaulting on their student loans, taking the 7 year bankruptcy hickey, having someone else eat the 100’s of thousands of dollars, and then they emerge later on with both the income and the write off.

That is a short story of how student loans became no longer eligible for discharge in bankruptcy. It’s the result of human behavior…. just like most sh*tty rules.

Good luck re-engineering the entire housing and mortgage industries. None of those are going to happen. We’re all entitled to visualize our utopian world though.

Mine has no income taxes and free top quality medical care.

Sadly, tend to agree – if DC has been engaged in stupid, counter-productive, corrupt policies for decades…there is less than zero reason to believe they will ever stop…until *their* welfare is threatened…then hysterical blame shifting and panicked policy shifts…far too late.

DC as currently structured has proven itself incapable of reform for 50+ *years*…it has witnessed increasing ruin and…incentivized more ruin.

As for #2, please provide some sort of justification for this crazy high %. As for everything else, no thanks!

There’s absolutely NO housing shortage in the sense that there are not enough homes being built. That’s patently false.

There is, however, a massive affordable home crises. And, you’ve got a ton of homeowners now that can’t sell their homes due to their extremely low mortgage rate and, or the fact that they did a 90% cash out refi.

In both cases, everyone had better get used to this situation. It’s not changing anytime soon. The only way it changes meaningfully is for a moderate to severe recession to hit. And for the millionth time, Congress isn’t going to let GR2.0 happen again. The GR & pandemic have enshrined three massive market engineering responses:

Rent relief

Mortgage forbearance

QE on the part of the Fed to soften the blow economic downturns.

“1. Cut the mortgage interest deduction (there is no reason to subsidize home ownership, it merely increases prices)”

This was originally intended to support the nuclear family by making housing more affordable for single income families, with a stay at home mom and a couple of rug rats. Such a quaint notion, no? It also added to the stability of cities by making home ownership attractive. So… your “solution” is to declare further war on the middle class, correct? Do you honestly think that once a person has lower cost of housing, they’ll save for retirement? Or would they buy a new iPhone and an “Emotional Support Truck” to tow their bass boat? Not saving for retirement is, again, not anyone’s problem but the person who refuses to do so. It requires management. Managing money is work. Much easier to make excuses for not doing so. (We started saving for retirement when I was 23 and my wife 22. Neither one of us made much, but we managed. My friends had Porsche’s and Corvettes. I had a Beetle.)

“2. Dramatically cut the red tape and costs of regulations for building new homes. The cost of regulations on new homes is up to 25% of the total price.”

You do realize that much of the land in areas such as Seattle is unavailable for multi-family housing, don’t you? As are other areas like Mini-noplace. It’s caused by zoning. Removing zoning constructs creates a situation where you’ll have more wildcat development that exceeds the area’s ability to support the population (hospitals, schools, police, roads, sewer, water filtration, parks, to name a few) creating an instant ghetto. Interesting perspective from a poster who wants to get rid of regulations but then recommends new regulations. Maybe you need to take a ride through Kentucky to see what lax regulations buys you (try a tour around Rough River State Park) or non-touristy Florida.

“3. Privatize the whole mortgage market, so there is no longer a subsidy from the government. This would help to reinforce market pricing of risk.”

You must be young. Us folks who lived in an era of privatized mortgages have seen that movie before. Loans are then only given to people who have excellent credit and rates are adjusted accordingly if you don’t. Subprime? Fuggedaboutit. It also leads to redlining. Certain ethnicities need not apply. If you’re overextended due to student debt? Too bad so sad. You’re a poor credit risk. See “Community Reinvestment Act”.

“4. Force originators of mortgages to keep their mortgages. The current method of having originators package them into MBS causes problems with risk management that will keep cropping up until originators actually have to bear the risk of default.” See above. Plus: Down payments would return to the 20% plus range. No more zero down / 5% down. How many people does that cut out? Sure, prices may fall, but they still wouldn’t qualify.

“5. Cut the maximum length of a mortgage to 15 years. This would allow people to pay off their mortgages, reduce interest costs and help to fund retirement savings (because a major expense is paid for).”

Anyone with an IQ larger than their shoe size knows how to cut a mortgage term simply by adjusting their payment behavior. In our case, we made additional principal payments (easy to set up with the lender) early in the loan. However, if we hit a rough patch, we could go back to the amortized payment without penalty. I don’t care if people get 50-year mortgages. It’s none of my business. Shouldn’t be yours either. It’s up to them to manage their finances. If they can’t, then they pay the “stupid tax” and be forced to eat their own cooking.

“6. Restrict large financial institutions from owning homes for rental.”

Somewhat agree…. but I’d term it corporations not “financial institutions” as financial institutions usually end up owning homes when the loan defaults and they do their best to dump them and mitigate carrying costs. However, that won’t necessarily drive prices down for the retail buyer as banks would prefer to do business with corporations that aren’t flaky, are totally unemotional, and can buy blocks of homes rather than one-at-a-time with individual purchasers who will pick them apart. Much of what corporations/investors buy is bundled junk. Some is high grade, but others need significant repairs/renovation. The average schmuck, who can barely afford to purchase it, can rarely afford to fix it – and it might not appraise. Few people could really handle a *fixer* in the truest sense of the word.

“7. Increase taxes on land ownership – provide less financial incentive for hoarding of vacant land, which will increase home-building and suppress scarcity.” So… you want to kill the small farmer, correct? What one does with their land is their business. The reason taxes are lower on vacant land is that vacant land uses near-zero municipal services. It doesn’t call the cops, doesn’t call the fire department, doesn’t send a corn stalk to school, doesn’t need roads, streets, snow removal, water treatment, sewage treatment….. Once developed into housing, the taxes skyrocket – as they should.

The issue isn’t necessarily “more homes”, it’s affordability (one doesn’t run hand in hand with the other). People want to live in a Malibu mansion on a barista’s income, but that ain’t happening. What has to happen is their expectations need to meet reality.

El Katz,

Well stated, point by point.

At the end of your “1, I could hear Janis Joplin singing to me,

“Oh Lord, won’t you buy me a Mercedes Benz?

My friends all drive Porsches, I must make amends”

And to your last point. A nice little crib just went for sale on the St. Paul side of the Mississippi @ 404 Mississippi River Blvd S; asking price of $2.75 Million. Nah, just a bit out of my league. C’est la vie.

404 Mississippi River Blvd south

Isn’t that Lucas Davenports house?

Note: Janet had a Porsche. A 356 convertible.

KGC,

You mean Janis Joplin?

She had a 1964 that she bought in 1968, two years before she died of a heroin overdose. A poster of her hung above my bed.

Re Point 1. All interest was deductible when the IRC was enacted in 1913. At the time this made sense for two reasons: 1. the income tax applied to very few households and the consumer lending industry was almost nonexistent, so personal interest expenses weren’t really a consideration by Congress at the time, and 2. interest paid by one person is income to someone else so it can be taxed to that person. As the consumer economy developed in subsequent decades, Congress started to disallow the deduction of interest expenses related to personal expenses such as credit cards, auto loans, personal loans, etc. Eventually, probably due in large part to the influence of the real estate industry, the mortgage interest expense deduction was all that remained. Keeping it probably had something to do with supporting families, or at least that’s how it’s defended now, but it was backed into by Congress which never had the political will to take it away.

Fully disagree with your responses to 1,3,4,5. The chips should fall as they do. All of the “solutions” have made the problem 100 times worse.

If banks don’t want to lend their own money to people, that’s not the government’s business.

When banks can’t/won’t lend we have these periods called depressions. Most people tend to think that’s a government problem to resolve.

@El Katz please write more comments. This post is beautiful.

Getting rid of central bank prior QE for MBS would be the first thing to do.

Much of the income supporting home prices comes from government deficit spending. No, the economy isn’t actually booming. It’s a combination of loose financial conditions and loose fiscal policy.

The Fed (Bernanke) delved into the MBS market breaking a tradition of the Fed staying out of MBSs and the long end.

He wins the Nobel as we now deal with the ramifications.

The Feds massive unrealized losses in their MBS portfolio is a gift to all who locked in foced all time lows.

Congress is too scared of homeowners to repeal the mortgage-interest and property-tax deductions. However, if they were smart, they could increase the standard deduction to the point that most homeowners will better off claiming the standard deduction than itemizing. That also would make the tax system more fair for renters.

Isn’t this already happening? Trump’s tax law raised the standard deduction to $26K for a married couple. $26K in mortgage interest at 3-4% interest rates is a multi-million dollar house. Most don’t need to itemize anymore.

Yes, exactly it was a step in the right direction. Corrupt housing subsidies are inflationary.

Renters don’t vote.

Americans don’t vote. Voter turnout, especially in state and local elections, is minuscule. Only 69% of voting-age citizens are even registered to vote, and only a portion of them votes. In the 2022 Congressional elections:

“Among the citizen voting-age population, homeowners had higher voter turnout than renters, with 58.1% of eligible homeowners and 36.5% of renters voting.” (Census)

This is symptomatic of the sense of disenfranchisement Americans feel when it comes to casting a vote for this that or the other egomaniac vying for high-office. Trying to parse which evil of the lessers will do the least harm every few seasons is a quiet form of torture.

You vote with your wallet.

Wolf,

You are so right that many citizens in the USA do not vote. My state of Minnesota is a bit of an outlier as we always have a good voter turn out.

bulfinch,

You are also right in your comment. Sad, but true.

From Baltasar Gracián, four centuries ago: “Never open your door to a lesser evil, for other and greater ones invariably slink in after it.”

If voting mattered, they wouldn’t let you do it.

George Carlin (IIRC)

This already happened for 2018.

Apparently there’s noo shortage of folks who want to bleed homeonwers dry… because paying $6500/yr in property taxes on a <1000sqft ranch isn't enough.

Come awn down to Texas…everything’s bigger

You’re living years behind the rest of us, do you think every homeowner is itemizing their return and claiming mortgage interest after tax reform? IRS stats for FY 2019, straight from the source: 87.3% of returns claimed standard deduction.

Well you do need to overcome the standard deduction which I think is $12,500 for a single person and $25,000 for married filing jointly.

So that is $12,500 in all interest paid toward your mortgage. Or $25,000 all interest paid.

I mean that’s some rarified air to be hitting the ceiling of a mortgage that meets the $750,000 mark and most of it be interest.

And with doing the calculations it just helps you out some. Not much, but some. As in maybe you get a tax return at the end of the year for an extra 10-12k.

In Omaha my s-I-l friend listed small ranch no updates in years for 215,000$ sold for 260.000$ in a week = NUTS . It will probably be a jingle keys in a few years . Unless inflation makes payment free

This is meaningless because you don’t indicate what a house like that sold for a year ago. But Omaha is one of the places where prices have continued to rise. By national levels, they’re still very low, with a median price of $277K (per Zillow).

Move to Omaha for cheap housing? I’ve always touted Tulsa for cheap housing. It’s an even better deal.

Tulsa is another city where prices have continued to rise, thanks to my ongoing recommendations for people to move there (I lived there for a long time, went to HS there, got a graduate degree there, worked there, and know whereof I speak, LOL). The median price per Zillow has now finally edged over $200k, up from $122K before the pandemic.

K thanks wolf

So no unemployment and no recession this year. Higher for longer till something breaks!!!

I still get the feeling, that there is a big swan of different colours somewhere.

Sometime in the next 5 years we all better be prepared for a rogue AI scenario. The most likely target is the electrical grid.

And it speaks Chinese

The biggest thing that the Fed is in charge of has already broken into a million pieces: price stability. Now they’re trying to fix it.

I think the fear of a recession must be subsiding. Most people do not want to buy a house with a recession looming on the horizon and thinking the price of their home will drop.

What has changed over the past 8 months. The stock market is up this year, the FED has paused and indicated maybe one or two more small hikes. That is big difference than last fall when people were probably thinking the FED may raise rates to 7% or higher and almost all economist were saying a recession was a sure thing in 2023.

Instead we have inflation dropping, interest rates close to an end, and the stock market rising. 6% mortgage rates is still a decent deal .

Demographics have increasingly outstripped new home starts since 1959.

I don’t know if things have been going pear-shaped that long…but (ironically) tax reform in 1986 definitely put a hit on SFH/multifamily construction and the 2009-2013 implosion hangover definitely gutted new HH construction (which was very slow to crawl out of that impact crater).

Hopefully the new apartment construction numbers bear fruit (go to actual completion…not a certainty the last few years apparently). “Under construction” is very high…but for some reason “completions” are lagging/vanishing over the last few years – sorta odd with record high rent increases.

Of the apartment complexes I’ve seen under construction locally, not one doesn’t have “luxury” in their description. I don’t think that improves affordability in any way, shape or form.

If the rents don’t keep pace with the cost of maintaining the facilities, amenities, carrying costs, taxes, etc., then the property will fall into decline, vacancies soar, and the developer/owner defaults.

High rents also controls the occupants. Having lived in Chicago during the housing projects debacle, I saw first hand what kind of element those apartments attract and the effect it has on the occupants. They turn into the same environment as a prison, without the guards, as they were “no-go” zones for the police. Google “Cabrini-Green”.

There’s no free lunches folks.

Luxury just means granite counters and plastic floors. The fit and finish and craftsmanship is atrocious on these complexes. I’ve got some great stories of what it’s like to live in a brand new “luxury” apartment.

“Come rent at our brand new basic, rudimentary and primeval new apartments!”

Not true.

US Population didn’t increase a lot in last 1 decade or so in comparison of new homes being built.

It is a propaganda by the media saying that there are not enough homes.

The issue is: Over financialization of real estate by yield seeker. To solve this, we need more rate hikes and more QT.

> Over financialization

yes, what increased was the supply of fiat money due to low rates.

now rates are higher there *will* be less fiat money.

prices *will* fall (further).

people who don’t understand this but who bought property because it always goes up will see it going down and demand from this vector will reduce.

Well you see, ummm. Most people have 2 children. And so those children have 2 children as well. And then we have oh 4 people. Then those 4 have 2. Then you are are at 8 children and so on and so forth thru time.

So yeah. It’s not the media lying, which yeah I mean is fun to say day in and day out. Rail against those pesky journalists fist to the sky! Weeeeeeee

Anyhow

This will affect the supposed monetary value of my home, but

A) I’m not selling anytime soon

and

B) if the price of a home doesn’t come down, how the heck are the next generations supposed to afford one?

I don’t want to live in a nation of renters. Because my prosperity CANNOT come at the expense of others. That’s just not sustainable.

You’re one in million, literally. The overwhelming attitude in this country is “to heck with you, I got mine”

He doesn’t even need to be altruistic.

If you own a single home, high house prices are bad for you.

Higher property taxes to live in the exact same house.

Higher transaction costs when you want to move to a similar house.

Higher maintenance costs as all the property speculation bids up contractor wages.

“Downsizing” isn’t happening en masse so that can be disregarded.

From 1980 to 2022 renters have gone from 65.5% to 66%. I wouldn’t worry about it too much.

The “next generation” can afford a home. No, it’s not backing to a golf course, doesn’t have 4 bedrooms, 4 baths and a pool. It’s in a lunch bucket neighborhood, possibly with yard cars.

From my point of view, children of boomers and their grandchildren feel entitled to live the life that their old geezer relatives have now… the “life they grew accustomed to”. Anything less is a step down and unacceptable.

It’s great to have dreams and ambition… but it’s unrealistic for most to expect that as their first house when starting out.

I don’t watch what my house is worth. I don’t really care. A house, to me, has always been nothing more than a place for me to keep my family and my stuff. I never took a HELOC, a cash out re-fi, or anything of the sort. Anyone who does has a spending problem that can’t be helped and the inability to process the fact that they are putting their housing security on the line for trinkets.

If one were to do an honest assessment of another’s consumer behavior, they can tell what’s important to them. If they own the latest iPhone, a Louis Vuitton handbag, a BMW, several gaming consoles, and rent a $3,500 / mo apartment? It’s fairly obvious that they’re not serious about owning a home.

As I’ve said on several occasions, looking back at my salary when I bought my first home vs. today’s cost of the same house, using input from the inflation calculator, the price to income ratio is nearly the same. The housing $ are larger, but so are salaries. And, yes, that neighborhood had yard cars.

Do we really need this dumbass argument on every housing market article? I feel like I’ve read this template a thousand times including the standard “latest iphone” section.

You devalue the currency and pay them more of it. Been working like that for 50+ years in USA.

By the way, that also makes you poorer.

Prosperity ALWAYS comes at the expense of others.

Mr Wolf Sir, building at lower price points seems pretty important to me. People should consider starter type homes that fit their need at that time.

Unless there is widespread rezoning of land to higher density, “starter homes” will be a thing of the past in major urban areas. Lot prices are too high to build starter homes on, unless you way out into the exburbs.

RV’s and manufactured homes (trailers) are the new starter homes in Texas. In Florida, RV and trailer parks are bought up by investors for cash flow or being demolished to build expensive homes and condos.

The only thing that’s going to bring down home prices is a big recession that increases inventory substantially. Otherwise, unless fed funds hit 7% and mortgages are in the double digits, it won’t happen. Yes, low inventory matters.

In Florida, many new neighborhoods ARE starter homes. 3/2, 1,800 Sq ft with a lot barely big enough to walk sideways between the houses isn’t exactly a home to aspire too. Most of these neighborhoods have 5 cars in every home, cars crammed everywhere in the treet, driveway, blocking sidewalk. Nightmare. But still “from the low $400s”

1800 sq ft is not a starter home ,try 1000 sq ft raised 2 kids in it nicely

Yes. The problem today is that people think a starter home is a 1,800 SF, 3BR, with 2 beautiful baths, plus granite counter tops, decent appliances, and a two-car garage in a nice neighborhood. That used to be the aspirational home that people dreamed about when they bought their 1,000 SF, 1BR, 1 bath, no-garage home in a so-so neighborhood. The three of us siblings shared a small bedroom. Worked OK.

>>widespread rezoning of land to higher density

Here in Raleigh NC area most new SFH builds are put on 0.14ac – 0.2ac lots with the former apparently being the smallest one local municipalities would approve. I am sure if builders were able to put houses on even _smaller_ lots, they surely would. And yes, same as crazytown mentioned about FL, these houses sell for $400k and more.

That said, I am not sure how else to rezone it without accidentally slipping into townhome / MFH territory – what is here already is pretty questionable even from the safety standpoint – there was a house fire in our development recently and I’d say it was a pure miracle (and a very quick response from local FD!) that neighboring houses were not damaged.

I see the beginnings of a repeat of a 2005/2006 style home lending fiasco. We appraised a home for $310K is a crime infested neighborhood that needed at least $250K worth of repairs. The land value was about $200K. What lender would be so stupid to put a loan on a piece of crap like this. USAA sent us out to do this for a taxpayer guaranteed loan. The best thing to do with this home is demolition. Most of the lenders we deal with now are so desperate to make loans that they will do anything to make a deal. They could care less if the loan defaults as by the time this happens they have sold the loan to someone else.

You might be right. I just read that two of the largest mortgage originators are now offering 99% LTV loans…only 1% down and credit scores as low as 620 will be approved. Reminds me of the no-doc Ninja loan days.

Good thing I come here the headline else where:

“Home prices increase again in April, signaling a recovery”

At this point does reality even matter?

That’s a different section of the housing market, previously owned homes; and I’ll start working on that as soon as I’m done working through the comments here.

That was a month-to-month figure. Prices fell by the most since 2012 on a year-over-year basis.

This will force home sellers to lower their price(s) aas well. Pass me the popcorn ………………….

In Canada 1/3 of people think that having a floating rate mortgage is the way to go. Was only 19% of people with floating rate pre-Covid. Maybe there’s some lingering brain fog to explain this when there was lots of chances to lock in under 2%.

Guess the “gut wrenching decision” you were talking about with buying high rate long bonds will also apply to people tired of suffering increasing monthly costs and locking in high mortgage rates.

People went onto variable rate because home prices in Canada became so detached from wages that taking variable to eek out a 0.2% saving became necessary to make the payments.

Lots of people here paying a lot of money for not much house.

Based on the May money #s, there will be no recession this year.

— Michel de Nostredame

The most interesting number would be the size of the “buydowns” offered by the builders as a measure for their desperation and a hint how fast they will go the way of the Dodo bird.

@Franz Agreed! That would be interesting data.

I am thinking the pandemic craziness is going to be difficult to unwind. That, zirp and air bnb might end up being one of the biggest bubbles. Saw some data on how incredible the growth has been in air bnbs. Got to think many of those properties are going to get dumped.

Some properties then will return to LT rental markets hopefully.

I’ve used Airbnb on occasion and I’m not impressed by it. The larger places that fit 10 or more folks together in prime locations have some attractiveness to me for get togethers, but the rents they charge for those places take all the value out of it. When on my own with immediate family, it’s much better to hotel it.

I have to assume many others feel the same way. I see more downside than upside with the Airbnb game at these stratospheric levels

I looked at a place to stay for a few days, the rent was comparable to a hotel. And then the $150 cleaning fee drove me away.

It’s your property, you clean it.

I don’t stay in AbNB unless I am with a large group.

AirBnb takes advantage of this. When you are with a large group, they know you will agree to spend more. Nobody wants to be seen as the tight wad that spoils the occasion.

It would be decent deal if they didn’t add all the fees, which doubles the price of everything.

Bobber, a slight offtopic, but I recently discovered that if you log into airbnb using a Canadian VPN, it will show total price with all fees and taxes included – making a site much easier to use.

For us, Americans, there is a separate option to “show total price”, yet (surprise!) it still does not include tax. Probably most Americans just don’t care about taxes, fees and other add-ons, and people from other countries do… /s

Their prices used to be competitive with or better than hotels only a few years ago. But that’s not the case anymore. To make matters worse, oftentimes there are obnoxious, onerous requirements besides, like “wash all dishes, take all trash, strip sheets and put in washing machine, and check out by 10 AM.”. I wish I had just made that up, but I stayed at a place with those requirements.

According to msm news articles, here is one article headline: “Home prices rose for third straight month in April, S&P Case-Shiller index says”.

Honestly, after increasing prices in last 3 years by 50 plus percent, a small drop in price is just a noise.

I absolutely don’t see any slow down in housing in my area. Housing is becoming hot again like stock market.

I know WR quotes price from peak of last year but I see big picture spanning few last years and housing along with stock market is still on fire.

Absolutely no respite to common joe when it comes to housing.

Things won’t change, unless FED starts selling MBS outright but they won’t do it for reasons we all know well.

Housing is so called hot in my area too. It may feel hot but then again this is on low inventory and low sales. Sure the few houses for sale may go quickly and have a lot of people looking but this is still not the same kind of hot when you have normal inventory and sale volume.

IMHO. Numbers are skewed by these low sales volume in my opinion.

If all of a sudden, two times the number of homes were added to the for sale inventory, I am guessing things would be different.

Thus, low inventory and low sales volume is keeping a floor under housing. Maybe the builders can keep up the current pace for a couple of years then we will see the true home market value as more homes are added to the inventory. But until inventory catches up, things will be hot.

jon,

1. Case-Shiller tracks prices of existing houses, not new houses, different data.

2. in the Case-Shiller that you cited: Year-over-year, prices fell for the second month in a row and by the most since 2012:

https://wolfstreet.com/2023/06/27/the-most-splendid-housing-bubbles-in-america-june-update-second-year-over-year-price-drop-since-2012-biggest-drops-in-seattle-san-francisco-las-vegas-phoenix-san-diego-portland-denver-dallas/

And since you’re in San Diego, year-over-year:

This will force home sellers to lower their price(s) aas well. Pass me the popcorn ………

One thing I’ve noticed with the new home sales (teardowns) around here is that there seems to always be a lot of construction vehicles surrounding the home after the sale and after the people move in. This goes on and on sometimes 2 years after the sale of the property. What this tells me is that builders are cutting corners, using substandard building materials and essentially building crap. A million dollar plus home should not need all these repairs The new homeowners have to fix all the problems created by unethical builders and fraudulent home inspectors. You don’t see this problem with existing home sales where the homes are over 70 years old.

Yep. Most flippers will cut corners. You can count on that .

A remodeler will have to get the home owner to sign off before they get the final payment. So remodeled homes are typically the better deal.

70 year old homes are built with redwood, doug fir, or old growth pine – not this fast growth junk available today. Dig around in your garage and find a 2×4 that’s several years old and then compare it to that in your local lumberyard. Look at the growth rings. Softwood is weak. Plus termites love it. Most were sheathed with wide boards or CDX.

Now? OSB sheathing. Particle board cabinets. Plastic supply lines. New, untested materials (remember the Dryvit debacle?). Cheap lav valves. 5-year life span appliances. CPVC supply lines.

I watch people in my community tear out quality materials in their quest to make their house HGTV-worthy. Then I watch the junk they’re getting installed and I have to scratch my head. Who would choose to replace solid wood trim with cardboard (aka MDF)? Ever see an MDF face frame that could hold a screw? Me neither.

There’s some dicey doings in old houses, too — asbestos tile (which is, admittedly, gorgeous stuff — like flecked Irish tweed for the floor), Kimsul (crepe impregnated with asphalt) and lead paint (alas, also beautiful); but otherwise, I agree — the old stuff was miles better, both structurally and aesthetically. Even barracks were built better than what’s tagged as “luxury” today. Nobody knew they had it so good.

There are VAST differences between locations with regards to older and newer construction qualities EK.

All the houses on our (3 nominal blocks) block in the saintly part of the TPA bay area were built in 1950 with exactly the same floor plan – though some had the plans upside down, so mirror images. They are basic CBS with plaster directly on block inside and out…

None were built with any ”fill cells”, ( that is cells in the block filled with rebar and mortar to make a solid connection between foundation and roof.)

Nor did any of the high rent area houses I worked on in the early 1960s in Naples, FL have any connectors for uplift resistance as are required these days.

That is just one of the differences, and there are many others mandated by modern building codes that enabled new houses built to 1994 codes to lose just a few shingles while the old ones next door were flattened in a hurricane (Charley??) in 2004 in the Punta Gorda area when I went to estimate rehab work.

I also did tons of repairs years ago to old houses in the SF bay area that had very deficient roof framing and sheathing, albeit of ”old growth” doug fir that was full nominal size ( not planered )… etc.

This is a situation that must be evaluated on a case by case basis, and by qualified personnel BEFORE the forensic engineers and expensive repairs become required.

Codes have changed… granted. Soft stories in earthquake country need proper reinforcement and some of the old homes aren’t bolted to the foundations. Heck… some are even built on sleepers on the ground (lookin’ at ya Texas).

Lots of variables…. but I’d still rather have the right old home and update it than buy a cardboard house that outgasses lord knows what from the glues, foams, and untested material used to assemble it.

Good thing about buying new construction in FL is it keeps the property insurance more manageable as they have to be up to code. I’d take a newly built house over an older one any day.

I agree on lumber and MDF, but GRK screws and PEX are improvements, not sure who bothers with CPVC anymore… though at least the old galvanized was hot dip instead of electroplated like now. I will also argue for PVC flooring- waterproof, consistant, no swelling from humidity, does not dessicate, bugs can’t eat it. Point being there is a lot of shady junk now, but some improvements available as well. Problem being that shady junk is standard equipment.

UBS cutting half of Credit Suisse staff and about 35,000 or 30% of combined staff after merger: Bloomberg

There is no end of markup in housing. Sure some cities are landlocked or small very desirable areas again based on Geography. However, most places have no end of land around them. Plenty of water as 10% of the usage goes to cities; other uses such as well water to grow alfalfa in the Arizona desert for export to Saudi Arabia need the rest. The cost of basic building materials are relatively cheap.

The so called housing market dovetails into the housing industry through the planned or exploitation of zoning, unique local building codes mainly to prevent modular construction, and superficial environmental issues such as San Bernadino California endangered kangaroo rats, etc (which might become more bountiful with outdoor pet food and water).

An example of artificial squeezing of housing is the manufactured home (the familiar single, double wide etc components). These have their own construction standards derived from the 1970s improvement of the mobile wheeled home. No problem for people to live safely in them in rural areas, but modular construction, that switch for whatever needs to be at all different places to meet the unique experiences found all over this great land (landlords) from sea to shining sea, and even in the purple mountains majesty to which we all sing.

Simple. We’re at 5.25% right now and the only thing feeling any pain is the commercial real estate market.

Housing – no. Car prices – no. Wages – no. Insurance – no. Medical – no. Other services – no

Quite the contrary. Give us a reason why rates shouldnt go substantially higher if the intent is to slow price increases that are a runaway train after a decade of many trillions of dollars of deficit spending.

If if prices of all things stay where it is now, it means inflation has gone to zero.

It also means that working class has lost this battle to own life essentials which I think they already are.

If Powell was serious, he’d have hiked instead of Pause in June.

If it (powell) hiked in June it would have had pressure to stop there. I didn’t buy the ‘Hawkish Pause’ at first, but now I do. Not sticking up for powell, although he is a great actor, like Reagan- not good movies, but pretended to be pro American in office pretty well.

The commercial RE market leads the residential RE market. If the CRE market crashes there will be no income base to maintain the high housing prices. They will go down in concert.

Swamp Creature: Or will companies get cheaper rent and keep higher margins because of it? They could hire more/ pay more with the savings on rent. Cities will lose out on CRE taxes, but may be good for businesses?

Americans have made lower price points illegal through the building code:

Tiny Homes – Illegal

Residential Fire Sprinkler – Stupid waste of money (there are stats that show only a WORKING smoke detector is needed)

Prohibitive setbacks

Excessive school fees to build

Etc.

Bonus: Outlaw lawns. If Americans quit wasting away water on grass and tropical plants in the desert it would prob help. Also wastes gas on mowers, fertilizer, etc.

The UK suspended repossessions – beat that!

The govt also tried to tell banks to raise savings rates today.

The UK has fully given up on “the process” as far as the free market goes.

Watch for more developments…

I should also add that Canada has effectively neutered repossessions too.

Customers who can’t pay the higher rates have their amortization increased.

Price discovery is banned. Where you saving responsibly? Sorry, the market is only allowed to go up. Up 25% is completely fine. Down 10%? Ah, not so much.

Sprinklers are very cheap to install in new buildings. They’re only expensive to retrofit.

Sprinklers almost always put the fire out way before it spreads. I don’t know how you can say a smoke detector is all you need.

Einhal.

You’re misinformed. This is why we ALL piss money away to save a very small amount of people

Cheap? Thousands for no reason?

6000 people die in US to fires, but all they need is a working smoke detector.

Wolf cited 763,000 new homes per year. If they sprinklers are costing $3,000 per home…

$2,289,000,000 per year in installed sprinklers. + Maintenance costs on all existing systems.

With a working 2 type smoke alarm you have about a 1% chance of death in the event of a fire.

Sooo .118% chance of fire. If there IS a fire you have a 1% chance of death.

Your odds of a fire death are approaching 0%. That same money could be spent on higher probability death events… or saved.

If you’re still scared, add a working fire extinguisher in the kitchen.

You should probably be more scared of junk food and beer (cancer, obesity, heart disease) or your car!

P.S. – Multifamily is a different story. This is for SFH.

Swamp Creature: Or will companies get cheaper rent and keep higher margins because of it? They could hire more/ pay more with the savings on rent. Cities will lose out on CRE taxes, but may be good for businesses?

The stickiness of used home prices is because, as Wolf says, “homeowners are sitting on their hands, trying to outwait this market.” Some just can’t believe that their homes are declining in value. Right now they are hoping against hope that the declines they see will reverse. Reality will eventually smack the homeowners in the face, and they will capitulate, or just give up thinking about selling. Greed has consequences.

Read the discussion above by Wolf and me about percent change, and note the difference between percent increase and percent decrease in dollar terms. Somehow I think this might be affecting homeowner psychology, but this is just a guess.

Another problem brought to us by ZIRP is that some homeowners are sitting on 3% mortgage rates. They might really want to move, but realize they would be paying more than twice the monthly mortgage for the same priced house they are living in. I hope they like where they live, because they are sort of imprisoned by their historically (hysterically) low mortgage rates.

I would rather buy a new house than a used house. At least on a new house I get a warranty and hopefully I can find an honest inspector to find the shoddy construction. Used houses have a host of problems that a lot of inspectors will not find or will overlook (you basically buy all the previous owner’s problems).