What the Fed wanted to accomplish. But the bond market hasn’t been playing along and “is too complacent” about the coming onslaught.

By Wolf Richter for WOLF STREET.

Long-term Treasury yields have been far lower than short-term Treasury yields for a year, as the Fed pushed up its short-term policy rates, but the Treasury market has refused to play along, and long-term Treasury yields have been slow in following. But this phenomenon is now facing massive headwinds.

Markets are going to have to absorb a flood of Treasury bills (Treasury securities with maturities of one year or less) in the coming months, estimated at something close to $1 trillion, as the Treasury is trying to refill its depleted checking account, the Treasury General Account, while also covering higher outflows and lower tax receipts (we discussed this most recently here). This has been teased in a series of Treasury department announcements that keep getting worse.

The net new issuance will pull liquidity out of other markets and put upward pressure on short-term Treasury yields and on other interest rates, including for CDs, as more and more buyers need to be found to buy these bills, and higher yields will do that.

We knew that. And it’s happening. Investors in bills and CDs are finally getting some yield, after 15 years of getting screwed.

For example, today, the Treasury sold $162 billion in securities, of which $120 billion were Treasury bills with juicy yields:

- $58 billion in six-month bills at an investment yield of 5.45%

- $62 billion in three-month bills at an investment yield of 5.34%.

- $42 billion in two-year notes at a high yield of 4.67%, amid very strong demand. Longer-term yields are still far below short-term yields.

The Treasury department wants to refill the TGA account to where it reaches $600 billion by the end of September. Borrowing to refill it will have to cover a lot of spending, lower tax receipts, plus the extra portion needed to increase the cash balance.

By the end of May, before the flood of new issuance started, there were $4.0 trillion in Treasury bills outstanding, about 16.4% of total marketable Treasury securities ($24.3 trillion at the time).

With the flood of Treasury bills now being issued, their share will soon hit 20%, which is seen by the Treasury Borrowing Advisory Committee as the upper limit for the US to fund deficits at the least possible cost to taxpayers, according to JPMorgan Chase, cited by Bloomberg.

The Treasury will soon have to issue more longer-term debt (notes and bonds) by increasing the auction sizes, to keep the proportion of Treasury bills in its pile of total marketable securities from ballooning out of whack.

Sales of Treasury notes (2-10 years) and Treasury bonds (20 and 30 years) are expected to rise, starting in August, according to the head of US Rates Research at Barclays Capital, Anshul Pradhan, cited by Bloomberg. He predicts that the net rise in notes and bonds from August to year-end will be nearly $600 billion, and ramp up further in 2024, when about $1.7 trillion in notes and bonds would be added, nearly double this year’s expected additions.

To find buyers for this added debt, yields would have to rise. He added, “We believe the rates market is too complacent.”

At the same time, some big buyers are unloading:

- Foreign buyers shed $140 billion in holdings in April compared to a year earlier, according to the Treasury Department’s TIC data.

- US banks shed $210 billion in Treasury securities and $332 billion in government-backed MBS in May compared to a year ago, according to Federal Reserve data. They’re struggling with unrealized losses from holdings that they’d bought when yields were ultra-low.

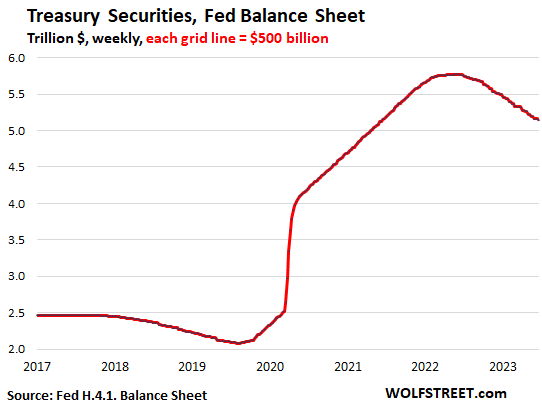

- The Fed has been unloading Treasury securities at a rate of $60 billion a month, month after month, as planned (its holdings of MBS are rolling off at a much slower pace):

It could result in a “demand vacuum” that would be resolved by higher yields for longer maturity securities, according to Bank of America, cited by Bloomberg. Yield solves all demand problems, and long-term yields have been much lower than shorter-term yields, with the 10-year Treasury currently at 3.71%

The higher long-term yields needed to attract enough buyers to sell the onslaught of notes and bonds would steepen the yield curve and push other long-term rates higher, such as mortgage rates and the rates companies would have to pay to sell new bonds.

This is of course precisely what the Fed wants to accomplish by hiking short-term policy rates and engaging in QT in order to throttle inflation back down. These policy measures have to translate into financial conditions – financial conditions need to tighten in order to get the magic done – but they remain amazingly loose. The markets refusal to play along so far has made the Fed’s job a lot more difficult. But as long-term yields rise to deal with the flood of issuance of notes and bonds begins later this year, the Fed might finally get some help from the bond market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Indeed, and the 2/10 year inversion on yields has never been higher than it has become now which is very recessionary for the days ahead.

They’ve promised us a recession for over a year, and we’re still waiting for it, LOL.

The yield curve is a RESULT of two factors: the Fed pushing up the short end at the fastest rate in 40 years, and the bond market being slow in following with long-term yields. That’s all. No magic to it. Now we’ll get the bond market playing catch-up.

As always, the long end of the bond market is dumber than a doornail. In August 2020, the bond market pushed down the 10-year yield to 0.5%, talking about how the 10-year yield would go negative, which has now wiped out four banks and put a bunch of other banks on the brink because they believed in this nonsense, and as huge participants in the bond market, loaded up on bonds at the time.

is this why Jerry said there would be at least 2 more rate hikes

I always thought he was looking thru rear view mirror

By God, I think he’s got it ! Great article and comment.

In the sense that I have felt for a long time that the long interest rate is an unstable disequilibrium. An artifact of the gilded age of QE, where the focus has been enticed to the excitement forgetting the most likely outcome in the decades ahead.

The long term interest rate is as far below equilibrium as the S&P index is above equilibrium. My opinion. Probably wrong in so many ways. One can only hope, that generally, the main point is at least accepted as a plausible scenario.

We shall see

As an aside, I have no delusion that the 20 year dividend will reach 6+% where it would be logical to at least hope the long rate reflects the inflation risk, which currently is raging at 2.5 X the target of 2%’, by the short term filling of the Treasury feed bag.

The Financial ballast provided by the Fed’s engorged balance sheet girth of 9 trillion or so I think will absorb the event like a …..

I’m sorry sir. You’re trying to play by the old rules. We’ve updated our rules to 2.0. And no, you cannot withdraw your ante. Please try again.

The long bond just does not believe Jerry.

Can you blame them after watching the Fed response to SVB et al?

March/23 = Apr/2007? Hope not.

Selling $120 billion in Treasuries that you need to revolve in 3 to 6 months, means you have extreme confidence in your confidence game.

What happens to this thesis if the Fed has to cut (short term) rates b/c the economy deteriorates? The exact opposite of the author’s thesis. The long term rates at 3.81 on the 20 year then becomes attractive. Not so fast.

Would you have interest in a spreadsheet that simply analyzes and makes calculations off of public FDIC data that calculates every banks true fmv capital? It is ugly out there.

An inverted yield curve does not cause or even predict a future recession. It is the market’s prediction of a future recession, but no guarantee of it and definitely not a cause.

I think the inversion is more of a supply-demand issue caused by Fed policy.

If the Fed is indeed forced to issue more long term bonds after they reach a cap on short term issuance, that might be the time long term rates really take off.

I agree with you in the gilded era of QE where the interest rate gas been driven to zero by the issuance of currency. The yield curve is an artifact, a residual. Still controlled by the opus of QE promise of a soft landing.

The classical interpretation of the yield curve inversion, developed over the coarse of human existence, no matter how sketchy, skewed towards hope, it may be, but it does not apply in the age of QE.

Inverted yield curve stresses many financial institution models, from banks (visibly) to some shadow bank models (less visibly), thus constraining credit, and becoming not just an indicator of economic slowdown but a cause.

gametv…

If the Fed is indeed forced to issue more long term bonds after they reach a cap on short term issuance…

The Fed doesn’t issue bonds… long-term or sort-term. The Treasury Department does. Other than that I agree wholeheartedly with your comment. I have always thought that the “inverted yield curve = upcoming recession” is more myth than reality.

Wrong. An inverted curve causes recession because banks can no longer make a profit by borrowing short and lending long. Thus they cut back loans, the lifeblood of the economy, and down we go.

Nah. Banks still make money on the spread — in fact they make more money on the spread — because:

1. they lend out at much higher rates, and

2. their average cost of funds is a lot lower than the marginal top interest rate they pay on CDs because a lot of their deposits are near-0% demand deposits (checking accounts, payroll accounts, all kinds of business accounts, etc.). And also because deposits are sticky, and customers are slow in yanking their money out when they get lower rates than elsewhere.

For example, Wells Fargo in Q1:

Interest expense shoot up by $5 billion year-over-year, from $1 billion in Q1 2022 to $6 billion in Q1 2023.

But its interest income shot up by $9 billion, from $10 billion in Q1 2022 to $19 billion in Q1 2023.

And “net interest income” (interest income minus interest expense) shot up from $9.2 billion in Q1 2022 to $13.4 billion in Q1 2023.

In other words, it made $4.2 billion more on the spread in Q1 2023 than in Q1 2022.

You can get all this in its latest 10-Q filing with the SEC for Q1 2023:

https://www.sec.gov/Archives/edgar/data/72971/000007297123000102/wfc-20230331.htm#i2cecc0ea62d2467a8733a3ebb7a15871_235

I’ve been rolling over my CDs over the last 14 months, most memorably last year dumping a lousy 0.5% CD I bought right before Covid and got a whole 2.5%. Last week I rolled that into a 5.5% 6 month T-Bill.

I kept my fixed rate portfolio at or under 18 months as I expected rates to keep going up (plus that was where the yield was). Once mid-term rates poke over 5% I will start lengthening duration, and if the very long part of the curve gets over 5.5% I might lock up for longer.

My older I-bonds are yielding “only” about 3.5% now, so maybe if the long bonds get way up I may roll those over since those are my “file and forget” bonds.

Interesting

“With the flood of Treasury bills now being issued, their share will soon hit 20%, which is seen by the Treasury Borrowing Advisory Committee as the upper limit for the US.”

This seems like an assumption. In a world where central banks are buying bonds, mbs, bank deposits of SVB etc, raising the 20% limit is like taking candy from baby.

Relying on short-term debt can be very problematic. Bills serve their purpose. But 20% is high.

Also, that: “In a world where central banks are buying bonds, mbs, bank deposits of SVB etc…” has ended. This is the new world of QT. Get used to it.

Japan is the only remaining QE outlier, and they will end it too.

Yeah, that is definitely an assumption. In fact the Treasury Department has posted on its website an analysis from late 2022 that concludes with “The model continues to favor more belly, Bill, TIPS, and FRN issuance, while decreasing issuance in the longer end”

Currently the range that TBAC wants for short-term securities is 15 to 20%… but the fact that they are publishing studies like this means that range is not written in stone.

https://home.treasury.gov/system/files/221/TBACCharge1Q32022.pdf

LOL. That’s what you get for just reading the summary at the beginning of the linked study, and not reading the entire study, and not even looking at the pictures, and not even looking at the dates of the data.

The time-frame that the study looked at ended in Q1 2022. So that was just at the beginning the rate hikes, and before this surge in issuance, and before the surge in short-term yields, before the 5.3% T-bill yields. Back then, the three-month yield was 0.45%, and the 10-year yield was 1.7%.

In Q1 2022, per this study you cited, bills amounted to just under 10% of the total. So back then, the study said that it would “favor more belly, Bill, TIPS, and FRN issuance.” Which is what massively happened already.

Now bills are already at 16% at the beginning of the massive issuance, and heading over 20% shortly, and TBAC said 20% is a threshold. READ THE STUFF YOU LINK BEFORE LINKING IT.

I did READ it… ALL OF IT! I just took a different angle on it than you did.

I didn’t take an “angle.” I looked at the charts in your cited documents, which said where the T-bill portion was at that time (less than 10%), and I compared it to where they’re now (over 16%). They said back then, bills are going to be a bigger portion, and during the following year, they became a much bigger portion, and NOW the TBAC says 20% is the limit, which is double the portion cited in the document, but not much higher than the current portion. Do you see?

The Fed isn’t going to buy treasuries anytime soon. They’re rolling them off their balance sheet. So, all of this excess treasury purchases are going to fall squarely into on investors & banks. I agree with Wolf’s point that fewer treasuries are going to be bought by foreign banks. It’s all part of the de-dollarization.

This is another great article, Wolf!

I am following the same investing philosophy as whatever above.

Stay invested in short term Tbills and CDs paying 5+% for now.

The 6 month and 1 year rates have popped up during the last month flattening the yield curve in the middle. Will that continue to roll up to the 10 year and 30 year bonds? I think Wolf is correct and we will see that in August.

If 10-30 year bonds reach 5-6%, I will start investing in the long term and live off the interest in retirement. My downfall would be if inflation ramps higher (>6%) and long term bond rates go even higher. The upside would be if inflation trends down below 4% and the Fed stops raising rates and lowers them. I could hold the bonds at the high rate at that point or sell them at a profit and go into equities which should go higher barring a major recession. It is a plan with some peril. This worked for my parents in the early 80’s when they purchased some 30 years treasuries at 10,12, and 14%. Timing was everything.

It worked for your parents because the nation could afford the interest on the national debt. Today, TTM interest is just under $600B and that number is climbing rapidly. I get the feeling this is the first step into a never ending debt spiral.

Have you considered what happens if Peter Schiff is right? If inflation doesn’t go away your purchasing power will get killed in long bonds.

The entirety of your investment thesis rides on the bottomless appetite of the US Treasury market to continue until you pass on.

I’m in the same boat… what to do? I’m betting on gold myself.

Then as yields rise, the Treasury may crowd out other bond issuers. The other ones can no longer afford the interest rate. Investors may also shun other bonds then the Treasuries if there is a rising rate defaults on other bonds.

If so, we head for interesting times.

From TFA:

>The net new issuance will pull liquidity out of other markets

It’s like wolf doesn’t think that this would increase long tail down side credit risks for those actors in those “other markets”, eventually forcing central banks to revert to long term trends throughout the history of central banking of effective debasement.

Other markets = stock market? Been saying that.

But borrowing WILL get more expensive for companies too. That’s the idea. Been saying that, LOL, including this weekend, literally,

Other markets: stocks, corp bonds, non-us gov bonds, fx (and futs, options, swaps across all of em).

Do you seriously think that most corps in the world now can sustainably borrow dollars at higher rates over the next 30 years, without another frbny kicking the can operation? lol

Lots of junk zombies are going to finally kick the bucket and restructure their debt in bankruptcy court. That’s how it’s supposed to work. It frees the economy from debt at investor expense, and it frees the economy from dysfunctional companies, and that’s a good thing, and growth returns at investor expense. That’s the classic business cycle. Healthy companies will do just fine, and they won’t have to mess with the zombies all over the place.

And yet all of that was true before the most recent additions this year to frbny programs handing a _temporary_ gift horse to unsecured bank depositors (who are also those “investors” you speak of)… lol

And ppl wonder why the long dated market is trading like it is…

” Then as yields rise, the Treasury may crowd out other bond issuers.”

Well put in explaining what should happen during a category 8 financial transformation from a crackpot economic doctrine too the underlying doctrine that explains what we have done wrong as well as what we need to do.

In my mind, Keynesian macroeconomics is likely, the latter.

Out of naive left field. Investor looks at Corp bonds vs Corp stocks. Hopefully looks at pe, other relevant data. Struggling a bit to get my point across. Why would any investor proffer money for either. I know TINA. Govt or private? Fiat or gold? Simply is there a way out of the trillions of debt pulled forward by fut uristic consumption through increased GDP?7

I sincerely hope you’re right, Wolf. I look forward to yields on notes & bonds rising in the coming months. Mortgage rates need to say as high as possible for as long as possible. Housing is entirely out of whack and needs at last another 25% to the downside which will take time, possibly 2-3 more years at least. And, it’s about time us conservative investors to make good money at low risk.

Don’t worry. Fed funds and mortgage rates are headed higher… a lot higher.

What it will do to home prices remains to be seen. So far, the old playbook isn’t working because things always change just enough that the old fixes no longer function.

One thing is for sure. 7% fed funds (And I believe we’ll see that number by the end of 2024) will kick off one hell of a recession.

Because so many foreigners hold so many dollars ,they’re just repatriated back into America through real estate . Chinese buying up assets,before we revalue dollar to ruble

LOL. The ruble has already been devalued to toilet paper. It now takes 85 RUB to buy 1 USD. In 2013, about 30 RUB bought 1 USD. In 2008, about 23 RUB bought 1 USD.

The USD is still one of the cleanest dirty shirts in the hamper.

“I sincerely hope you’re right, Wolf. I look forward to yields on notes & bonds rising in the coming months.”

Me too. I’m going all in at 11 pct.

In the meanwhile, I’m making bank short term and spending the proceeds in long neglected expenditures.

What Wolf has predicted continues to occur.

Keep up the good work

Just curious,

What does he predict?

I mean he shows us data and explains current moves.

My opinion is that he does not make many projections. He calls people different names and says they are “drinking the Kool aid” so to speak.

He’s pretty tight with his cards about future moves to take.

So when you say “he continues to be right”… well his explanations of the recent past are vivid and educational.

The entire point of his piece is a prediction: long term rates will rise.

Yes, this article is very much predictive, but alot of his past articles have been more focused on the here and now. But he has been saying the markets dont understand that rates need to remain higher for longer for quite a long time.

Honestly, since wolf quoted someone I would see it more as reporting than predicting.

But he did clarify he does agree with him in the comments.

So ok. Slightly predictive.

@sufferinsucatash,

When the FED first started with the interest rate increases last year, EVERYBODY was saying the FED would pivot. Wolf said the FED was serious. Wolf said the FED would not pivot. So here we are, a year and a few months later and the FED has not pivoted.

Nor will they this year at all.

And we’ve only seen the 2nd, 3rd and 4th largest bank failures in US history so far…. everything’s fine…

I mean but he doesn’t say “This is going to happen”

It’s more like “well my opinion on the matter is xyz, these Bozos over here are morons… etc etc. end of article.”

It’s not like “go buy bonds because these guys are all wrong and I’m 100% certain!”

More like a quiet laugh and some hints toward what might play out but not too much of opinion to be pinned down as wrong later…

I’m just saying I don’t see many predictions like a weatherman would, here. Which is cool.

Obviously, you are not a fan of Wolf.

Me neither. Because the idea of being a fan connotes a familial connection that doesn’t exist.

However, I suggest that your pleading for someone to explain the obvious to you. Says so much more about you.

Prediction is a fools errand for a journalist. It immediately turns them into an opinionist.

Wolf is great. And he teaches a lot.

I actually am a fan. But also I am afflicted with one of those annoying strong opinions on matters and so I can’t shut up long. Haha

His prediction is to take Central Banks at their word, which is a pretty ballsy prediction.

sufferinsucatash-

In response to your request for “future moves to take”, without absorbing and analyzing the plethora of truth and wisdom on this website,

I would like to announce my new Investment Advisement entity, Harry Houndstooth, D.I.

Harry Houndstooth, D. I. investment advise will be only be available on Wolfstreet.com.

Our current recommendation is SQQQ.

In recognition of our Grand Opening,

“Harry Houndstooth, D.I. would to like to pay for and send an authentic ” Nothing GOES to HECK in a strAight Line ” mug to the first entity that correctly posts the book and page number that explains what the “D. I.” stands for.

Timing is everything.

I’m thinking that there are so many forecasts for Recession that the “pros” are using the old playbook to buy bonds in anticipation of Fed cutting rates policy in response.

Not many of these “pros “ were around when Inflation was high like now.

Guessing a long bonds bet will prove to be a bad play for these folks ( that command an enormous amount of money)

I think that also, that buying the long bond at this juncture will prove to be a bad bet for mom and pop who buy to hold.

The machine that makes it all go round, I suspect will harvest the rest of the wealth they haven’t already garnered in the crooked game that the US has become.

Wolf, thank you for answering something I’ve wondered for a long time – if there was a limit on how many bills could be issued compared to notes and bonds. I think short term rates are at a good spot, we were at 0% for so long that getting 5% on cash now is amazing, but I’d love to see long term rates push up significantly.

I think 5.5% on the 10-year is a real possibility. The labor market refuses to cool. Car market hot, housing warm, zombies walking in broad daylight, rate hike pause, QT still in early stages, etc.

Long-term inflation going back to sub 2% is the current prediction by many analysts.

Morningstar has it at 1.8% for 2024-2025!!!

(Why We Expect Inflation to Fall in 2023, Morningstar, 5/26/2023)

Insanity. No wonder 10 year is so low currently.

Waiting for reality to hit the 10 year…

They are only saying that to carry water for the giant corporations, who will use that as an excuse not to raise pay in the coming employee review cycles.

Car market is crashing.

LOL, no, where do you get this garbage? The new vehicle market is recovering from the plunge during the pandemic when the market ran out of cars due to the chip shortages. Now inventory of new vehicles is growing again, finally, though still below “healthy” levels, and sales of new vehicles have come up a lot from the lows during the shortages. We’re finally seeing deals and incentives again, the way it’s supposed to be. Used vehicle supply is still constrained by two years of new-vehicle production shortfalls (future used vehicles). Update for Q2 coming in early July.

To Wolf my neighbor owns a used cat lot

Even funnier. You take the fate of a small used-car lot as an indication of the market? If you want to use one company to get a feel for the used-vehicle market in the US, choose the biggest national dealer, CarMax. And that’s just the used vehicle market, not the new vehicle market. And as I said, they’re griping about inventory shortages and cost pressures (high wholesale prices). Their net profit dipped by 9% year-over-year to $228 million, and their sales fell back to normal-ish levels as they’re coming off the huge price-gouge boom during the pandemic that I have covered here endlessly. There is nothing “crashing” here, LOL. But there is some normalizing going on.

I am beginning to think that fiscal spending is going to make this thing very ugly. Government keeps spending,creating more inflation and making Fed keep raising rates causing more transfer payments to deal with higher prices.

T-bills normally pay just over inflation, so you could say they are fairly priced. Don’t think you can say the same thing about the 10 year treasury or stocks with high PEs when inflation is 4 – 5%.

The answer to speed of inflation may be linket to what degree government deficit do create money. If the government debt actually create money that is, the government debt create monetary inflation, inflation measured by CPI will eventually follow.

The trade deficit is the flip side to this. The Weimar republic tried to pay of foreign debt by debasing their currency, that do not work. Th US tries to buy foreign goods and commodities by debasing their currency, that may work for a little longer.

Govt just announced $42B internet initiatives. Basically, 42B more money in the economy.

Fed needs to hie more and do more QT to counteract Govt deficit spending.

I was thinking same thing when I read that headline!

What are you talking about ?

Reviewing the Keynsian postulation of the macroeconomic equation that

GDP = C + G + E + I , whereby E is exports and I is imports, an additive quantity that results in a negative seven percent. Mathematically, for GDP to remain positive, then either C, consumption expenditures or G, government expenditures have to increase by 7%, the current trade deficit.

Whoops. The equation should have been

GDP = C + G + E – I , the additive quantity of Exports minus Imports which the measurement of the trade deficit is a negative 7 pct.

Which means that the American government has to run a deficit of at least 7 pct to maintain a positive growth in GDP unless personal consumption expenditures suddenly increases at an unlikely rate that would counteract the effect of their jobs being performed by foreign labor.

Maybe we could use two quarters of negative GDP about now. How much GDP would get wiped out if we finally kill the zombie corporations?

Brits doing a 12 month foreclosure moratorium.

“Mortgage 12-month grace period: what’s in it for you?” Guardian, 6/23/2023.

They can also:

“Customers can switch to an interest-only deal for six months; or extend their mortgage term and revert back within six months if they want. Neither option requires an affordability check or will affect their credit score.”

Fighting reality of high interest rates???

This stuff is very inflationary by giving homeowners extra cash to spend, subverting the rate hikes. The rate hikes were supposed to curtail spending and thereby reduce consumer price inflation. This is a government fighting for political survival, and their tool is to throw fuel on the inflation fire. That’s one of the reasons why this inflation will be stubbornly high for a long time; there is just no political will to crack down on it (same as in the US and elsewhere).

Howdy, and about time for folks to start earning a little interest. Some folks will never trust the stock market is the long and short of it. Wondered for 15 years when the FED would get its head out of the sand. Inflation is a good thing I guess. Nice article, tells the story true…..THANKS

Doesn’t sound good for stocks?

Good! Something needs to bring the casino down.

I couldn’t agree more. I was a CFO in the late 70s and early 80s. We havn’t seen nothing yet. Debt issued is out of control and normal buyers are backing off.

I don’t see longer term bonds going up in yield.

If it goes up, then mortgage rates would also go up it means prices down for housing which is badly needed.

We need 40% or more correction in housing,

My hood saw 50% or more home price inflation in last 3 years or so.

My goodness, where do you live?

San Diego

Eh, I’m in Florida and a lot of people buying up expensive real estate are foreigners from South America. I’m starting to think we really screwed ourselves running massive trade deficits being a reserve currency. We import goods and give foreigners our dollars and those dollars have to go somewhere. US bonds…sure. But then US equities. US real estate (residential and commercial) and even US farmland. Slowly giving away our local assets as trade deficit dollars return back home. Hope I’m wrong, but having lived in AZ around foreign (Saudi) owned farms and now FL around lots of secondary South American owned homes…not good…

People complained in the 80’s about the Japanese buying up properties. The peak was when Mitsubishi purchased Manhattan’s Rockefeller Center. A few years later they failed to make their mortgage payment.

Ehh. Florida real estate is headed underwater, figuratively and literally.

Yeah 50% is standard.

But remember inflation is silently and invisibly lifting up where the bottom of real estate will fall.

Perhaps this is why the fed is so slow to increase the pain. Once they do and our home values fall, they can interject “oh yeah well your home value fell 25%, but the people on the sidelines who waited lost way more cash to inflation”

Rather than the other scenario, in June of 2022 the fed raises the rates to 10% overnight and every bit of equity you had is gone.

Housing crash is desperately needed. Its eating people alive.

Mortgage rates are directly keyed off the yield on 10-year US Treasuries plus about 3% and that has always been the case.

The spread between the 10-year yield and the 30-year mortgage rate changes quite a bit. By historical standards, it’s very wide now at 3 percentage points. It shows that the mortgage market is ahead of the Treasury market, and sees higher rates for longer. It could very well be that the 10-year yield rises to 5.5% and mortgage rates stay near 7% or go over it a little, and with the spread narrowing to 1.5 or 2.0 percentage points, which would put it back into the normal range.

hard to believe the Fed has injected a few trillion into the mortgage market.

if we had a truly privatized mortgage market, what would the interest rates be? 12% or more? the risk premium might be off the charts with housing prices so high. or maybe there would be no financing available.

The spread between MBS yield and 10 year Treasury is really more an implied measure and forecast of interest rate volatility than the direction of yields.

That’s because the amount of options embedded in standard 30 year mortgages is enormous.

Thus the value of those “options” ( prepayment options

to the homeowner) drives the price of MBS and therefore yield of MBS, therein drives the spread of MBS and treasuries.

Peter,

You’re talking about a different spread.

The spread chart I posted is NOT a spread between MBS yield and 10-year yield, but between the average weekly 30-year fixed mortgage rates as per Freddie Mac data, and the 10-year yield.

“Thus the value of those “options” ( prepayment options

to the homeowner) drives the price of MBS and therefore yield of MBS, therein drives the spread of MBS and treasuries.”

I think that is a good point. If I had a choice in the future of buying a 10 year Treasury yielding 6% or an MBS yielding 7%, I would pick the Treasury.

If mortgage rates peak and then the Fed lowers rates, the MBS will likely be “Called” earlier as mortgage holders refi to lower rates. Worst case could also result from foreclosures or homeowners doing so well that they pay off their mortgage. The 10 year Treasury will continue to pay the 6% for 10 years. If I understand MBS’s correctly, the rate and duration may be variable.

The possibility of an actual market based yield curve? Will we find out what real treasury market based rates are?

Wolf said:

“Sales of Treasury notes (2-10 years) and Treasury bonds (20 and 30 years) are expected to rise, starting in August, according to the head of US Rates Research at Barclays Capital, Anshul Pradhan, cited by Bloomberg.”

—————————————

I’ve not noticed you referencing a 3rd party on such matters before. Usually you are straight at the source.

Anshul Pradhan and I are on the same wavelength on this issue. So it’s not just me thinking that. That was the point.

This asshole may be right or wrong. At the end of the day, only reality rules. Obviously he hasn’t been right yet.

End of inverted yield curve!!! What a wonderful event that would be !!

An inverted yield curve always un-inverts sooner or later.

The inverted yield curve will only re-invert if we enter a recession. That’s the time to buy 30 year Treasuries. You can’t get hurt.

As someone who invests in 30 year treasuries, time to get out? Would be sad, I made some good profits on it in last 6 months or so.

I heard that Michael (Big Short) Burry is buying 30 year Treasuries at 10 to 1 leverage. When the economy collapses later this year he expects pretty large capitol gains and a handsome interest rate coupon to boot.

In order to realize the capital gains, Burry will need to sell the bonds and their interest coupon. I guess he’ll at least collect the interest coupon if the collapse he predicts fails to happen and he doesn’t get those capital gains.

Yeah that is the argument I am hearing from many folks. But plenty of things need to happen for that to materialize. There needs to be a substantial crash or slowdown, fed needs to cut back to 0 and also start buying bonds. I just don’t see that happening. But if it does happen, the upside on the 30 year treasury is just mind blowing. So far I have been trading it more like a stock. Buy low sell High repeat.

The US economy is in a state of significant disequilibrium. We have a strongly inverted yield curve; big fiscal deficits; big trade deficits; a major inflation trend; embedded duration risk in the world economy that is unprecedented; and a smoldering ground war in Central Europe. It’s a recipe for big time volatility and a crash, but timing is everything. If you’re too early or too late, you’re wrong.

Burry got lucky once.

Has any of his other predictions panned out in the past 12 years?

I guess I’m not following. If he’s predicting a collapse, why is he leveraged long?

In the context of rising rates, I’m not investing in any duration that I’m uncomfortable with holding till maturity.

Me too. I’m maybe a little too far out on some CDs at 5 years. I’m a little uncomfortable with my bond ladder for bonds/CDs from 2-5 years. Maybe I moved to longer durations too soon. Yield have been going down, and I didn’t want to miss peak yields.

That is an absurd claim for a fool that invests in 30 year treasuries and claims they made money off the decline in value of the 30 year which is under pressure because it is overvalued.

If you are referring to me, I started investing in them like 8 months ago. During October I grabbed some 30 year bonds down more than 50 percent from their peak in early 2021. Soon I got one big 12 percent profit. Since then I have been buying and selling them with like 2 or 3 percent profit every time. And with this bonds I don’t mind putting in substantial amount of money so even 2 or 3 percent profit is enough to pay my bills for 2 months excluding housing.

You can refer to TLT as proxy for these type of bonds to get an idea of what I am talking about.

There are plenty of folks down 30 percent or more on these bonds if they bought it in 2021.

Hope that helps.

Need some advice from the smart, Wolfstreet readers….should I go for a 52 week or 26 week T-Bill? I have 200K to invest…. Thanks

Howdy , Try Treasury Direct? Has been great for me…..The 3 month T Bill is where its at for me……..

Thanks, D-F -B……I will be moving the $$$ in August….Setting up my Treasury Direct account soon! My CD pays .03 as I write….lol! Frickin Banksters

You can buy and sell T-bills with Schwab, Vanguard, and probably Fidelity for zero commission. Treasury Direct only allows you to buy. If you want to sell before maturity, you have to transfer it to a broker. I only use Treasury Direct for I-bonds (no other choice). They do have an amusing website, right out of 1980.

Anyway, I buy at auction, usually hold to maturity. I buy 4 and 6 month T-bills, laddered in a sort of anarchic way. I have been doing this for over a year and a half and it is working well. After next month, all my T-bills will be earning well over 5%. As for Fed funds rate: higher, longer (as Deadhead Powell has probably said many times).

Schwab has brokered CD paying over 5% out to 2 years.

Treasury Direct has such a clunky website. Their poor customer support also scares me for large sums of money. I much prefer Fidelity. However, Treasury Direct does function.

They finally got rid of their onscreen keyboard for password entry. I just saw that. Great move!

Treasury Direct used to send a card like a credit card with a secret code on it. Their on-screen keyboard for inputting a password was also kind of fun. Like being in a Get Smart episode with Don Adams .

Howdy Mike, try out this website depositaccounts . com. Maneuver through it and find lots of good information.

Mike,

This is not advice because you have to do what is right for *you* with your wealth at your age and your responsibilities. But I will tell you what I’m doing as a newly retired person. For about a year now I have been buying Treasury bills with short durations… 4-week, 8-week and 13-week. When they mature, I reinvest the funds back into new Treasury bills. The interest rates I have earned have climbed steadily, making me a happy man who is now receiving over 5% return, risk free, with no state income tax to pay.

Meanwhile, the S&P 500 gyrates up and down and sideways and now seems more than a bit expensive to me at a Price/Earnings ratio of around 19x. My detailed spreadsheet discounted cash flow analysis tells me that the S&P 500 is overvalued at it’s current level of 4300 and, at best, is just going to gyrate up and down for years, and at worst, is subject to a painful correction at any time. I am happy to sit on the sidelines with a risk-free return of over 5% and watch as the interest rates on the longer Treasury (and corporate, and muni) bonds rise… and the price of assets (stocks, bonds, real estate, etc.) decline. Then I will move my cash out of Treasuries and buy assets again. We’ll see what happens. I may be right, I may be wrong. But my frugality allows me to sleep well at night no matter what. Good luck to you!

A detail: I use both Treasury Direct and Vanguard (brokered) to buy Treasury bills. If you aren’t worried about liquidity, Treasury Direct is fine. I you are worried about liquidity, Vanguard and the like are better because, as William says, you can sell before maturity.

One other note regarding Treasury Direct vs. Vanguard brokered: If you want to pin point your duration and timing, Treasury Direct is the way to go. You can pick from among five or six issue dates for most Treasury bill durations (4-week, 8-week, 13-week, and so on). In my experience the Vanguard brokered platform has offered far fewer options to get the duration I want on the issue date that I want it. That’s why I generally use Treasury Direct even though Vanguard brokered would allow me to sell the bill before maturity without hassle if I needed the cash. Plus, a minor point, but worth mentioning in theory: Being absolutely 100% “risk free” means I need to be dealing directly with the Treasury, not with a middle man. Hope that helps.

Doubting Thomas,

Get out of my head! Eerily similar to my approach. Currently roughly 85% Tbills, 15% equities which have been doing nicely overall taking advantage of crazy volatility with some shortish term trades. Been doing the Tbills a year myself, and a year and a half for my mom. Double the treasury website fun!

For short term I just buy VMFXX. Currently yield is around 5%

Pretty sure you are going to have to pay state taxes on VMFXX interest. The amount varies from state to state. It’s complicated. Check out Bogleheads.org for details. I live in California, so I prefer to buy Treasuries, which interest is completely state tax free.

I will be buying 6 month bills for the next few months. It lets me push taxes into the next year while positioning me to have cash to invest if the bottom falls out. I think the market pain will hit sometime between October and April. That is when student loans restart payments, higher property tax payments, and higher home payments will all kick in, in addition to April tax payments. Some real estate investors could potentially be hurting big time from that combination of factors, possibly enough to initiate a stampede of selling across multiple markets. This is not investment advice because it has a low probability, but *if* it happens, I personally will be in the catbird seat.

Meant “higher home insurance payments”.

PS This all only works because I *believe* (far from knowing) that the markets are currently in a state of unstable equilibrium, all things considered. A great state of things when you can find it. Wish me luck.

Well, i’m a Wolfstreet reader, hopefully that’s good enough for you! =] If you currently believe, like many of us here, that the fed will increase by .25 twice more this year, and perhaps even more in 2024, that can help shape your strategy. As wolf mentions the markets are pricing in fewer rate increases. As the fed increases, so will Tbill returns. Thus, you’d buy shorter 8 or 13 weeks (rather than the 26 or 52) to re-invest at higher rates. You can enjoy earning those increasing rates while analyzing economic data/listening to the fed/reading Wolf, and once you believe the fed will stop raising or will start lowering, switch to 52 week bills or longer options.

Couple Questions:

1. Are references in article to ”end of year” etc., referring to fiscal year or calendar year?

2. Would current low yield bond holders be inclined to discount them sufficiently to make them more attractive to buyers??

3. Anyone care to guesstimate when and at what at what rate the notes and bonds will top out this time???

4. Based on its history to date, does anyone think the FRB can keep from manipulating the treasury yields in the face of political pressures????

Thanks in advance!

Very, very upsetting that the yield curve inversion could become reduced or eliminated. Perhaps there would be some hope if no one bought the long duration treasury bills; Janet Yellen cannot have a deficiency so perhaps the Treasury would change the mix to short term that people are buying at the higher yield than the long term bills and sort of kick the can down the road. Cannot even understand who would buy a long term Treasury bill when the Federal Reserve’s FOMC only plans and makes policy a mere 6 weeks at a time; anything, many times over could happen in those long terms.

For the average citizen, an extremely high yield curve puts a lot of pressure on inflation spending. Under Volcker the yield curve inversion was twice what it is today and that worked wonders.

People will trample all over each other to buy 10-year notes if the yield is high enough, and inflation looks contained. There will be people right here, dropping everything and stopping in mid-comment, to load up on 10-year notes if the yield is high enough, and if inflation looks contained. Yield solves all demand problems.

The problem is — and the problem was last time — that if IF, IF, the 10-year yield reaches 7%, the inflation scenario will be so scary and out of whack (8% core CPI?) that it will take a lot of cojones to commit funds for 10 years at 7%. And then people don’t do it because they fear that inflation will be 10% for years to come. That’s the problem when you get to that point. It has to be a gut-wrenching decision.

Been there, I was one of the 50-60 tramplers in the lobby of an S&L in the glorious spring of 1980. I dumped a 6 mo CD at 18.55% and rolled into a 5 yr at 16.5% and got a $300 bonus for opening a new account. No toasters for me.

Speaking of cojones, does the Fed have big enough ones to let the market determine interest rates float to positive real rates?

Time will tell. But my guess is that they can’t stand the heat.

B

I bought long term corporate bonds as far out as the year 2076 last week.

I have a couple 10-year CDs in my 401(k). Both have a ~5% coupon.

All of my treasury paper is <1 year tho (except my I-bonds).

The government’s deficits must be cut. Otherwise, term premiums are going to go up. Both higher interest rates & higher taxes erode the tax base increasing the volume of future deficits.

Here are my thoughts as points:

1. Govt won’t reduce spending.

2. They may try to lessen deficit spending with more taxes in the coming time. I see this coming.

3.Or FED would cut rates and start at some point QE. They would rely on manipulated inflation metric or just change their inflation goal post.

Higher taxes create fiscal space for the government to invest into. The best thing would be to raise the taxes on the super rich high enough so they can’t bribe politicians. That would stop inflation in its tracks. But that’s a fiscal tool only Congress possesses, and they are already bribed. AWOL.

Wolf: So foreigners are unloading, albeight slowly, their treasury holdings (official papers). I understand that a good percentage of our currency also disappers from our shores (as soon as they are printed) for use by foreigners (distrust of their own currency, to fund their trips abroad when it is difficult to get dollar from offcicial channels and or illegal activties) and sits there unoffcially. I wonder what kind of effect that would have if the reverse process takes place? Folks making vists here more and spend away, buy properties and so on only to add to our inflation?

If the many trillions of offshore dollars ever decide to come back to the US and bid on US real assets, persistent double digit inflation and political instability would be inevitable. It’s one way the country can functionally go broke even though it still produces a lot of “money”.

It’s already happening in South Dakota chinese bought 300.000 acres around a military base already ,bought packing houses,there will never be a war ,they will control the money .

What are they going to do with this land? Steal it and secretly move it to China?

Beyond that there are concerns about Chinese spying operations in the US, hence the concern about Chinese ownership of facilities near US military installations.

The O/N RRP facility volumes have now decreased by $441b, from $2,375b on 3/31/23 to $1961b on 6/26/23.

Contrary to the FED’s GAAP accounting, this increases the supply of loan-funds necessary to cover the FED’s issuance.

This is scary, because it shows deficits do matter.

And what of the Feds portfolio and unrealized losses? They can hide it and ride it out but what of the unhedged banks?

We are headed for a nationalized banking system and digital currency….all driven by terrible bureaucratic decision making.

There will be high demand for the front end at 5.5%. There will be low demand for bonds and notes under 4%. The long duration will have to rise.

The US and others have been covering the shortfall between revenue and expenditure by borrowing. If it’s too expensive to borrow short, they could borrow long. But if both approach the rate of inflation, the jig is up.

Everyone laughs, in hindsight, at those stupid banks, SV etc., who loaded up on bonds paying 1.5 %, and then took a huge loss when they had to unload them. Could a mirror image, the reverse, trap the Fed? What if it issues a lot of long debt at 5 or more % , and then the recession does arrive, driving market rates back down?

The Fed doesn’t issue bonds… the Treasury Department does.

OK: ‘trap the govt.’

Fundamental question is whether the US gov can afford much higher long term rates, or will it finally have to dramatically raise revenue thru taxes and also cut spending.

BTW: this ‘which agency of govt’ shell game has been called out in the UK, with the opposition asking why the BoE, supposedly independent, always issues just as much debt as the government requires to fund itself.

Who owns most US Treasury bonds?

The Federal Government Has Borrowed Trillions, But Who Owns …

The Federal Reserve, which purchases and sells Treasury securities as a means to influence federal interest rates and the nation’s money supply, is the largest holder of such debt.May 11, 2023

So, the long bond market sees recession as more likely than most of the market?

Don’t worry about the decade ahead or even the 10 year rate, have a longer term horizon!!! Billionaire Ron Baron is calling for Dow 900K, yes sir that’s not a typo!! Everyone short will be crushed to bits. Heck, at that valuation, Bitcoin will probably be at a trillion a coin.

Seriously there are some nutty people out there.

I thought the U.S. stock market today was already the most overvalued ever on record more overvalued than 1929 or 1873. If its true I wonder if the rest of the world will rig their stock markets so they go up when they should go down? So far it really hasn’t materialized yet except in Japan.

Another financial data driven masterpiece delivered by Wolf. If, maybe, probably, I think, show the best of the free market, everyone gets their opinion heard. The Hunt for Price Stability will be long and slow grind, Wall Street still thinks they control the water faucet, Fed continues tightening the main valve ever so slowly, their is a bend don’t break protocol.

I agree rates will blowout eventually but bonds may have one more rally in them before they crash.

Could be from money coming out of stocks or recession fears or could be just markets being markets but that’d be my guess.

Personally rooting for recession we really need one IMO. Also rooting for a few that doesn’t bail out the country this time with lowering rates. Slow growth for an extended amount of time would do wonders for this entitled society…. Nobody is innocent in this so don’t blame the youth either. Boomers are likely the most entitled age group at this point

Learn alot from the articles and comments. How crazy or naive is it to think that Normalization of monetary policy, and cremating the ZIRP/QE academic experiment just might happen.

If we hadn’t had the COVID pandemic it would already have happened by now. The Fed hasn’t been shy about saying it wants to return to “normal” over the past decade. They ended the QE program in 2014, announced their QT plans way back in 2016, and stuck with those plans until 2019 when things got gummed up. Unfortunately they had tried to combine QT with rate increases in a slow-growth economy and spooked the markets… BADLY. They should have done one and then the other.

Then again, it is not like they are getting any help from the political side of Washington. Be it multi-trillion dollar debt bills or threats to not raise the Debt Limit… the politicians have done plenty to gum up the works for the Fed. The Fed now seems to be doing the right thing… ignoring the politicians and doing what they know to be necessary. If the politicians want to damage the economy then the Fed isn’t going to bail THEM out any longer.

“58 billion in six-month bills at an investment yield of 5.45%

$62 billion in three-month bills at an investment yield of 5.34%.”

Which, if my math skills are not completely off, implies that said “Treasury” will have ti raise these 120 billion + interest in 3 and 6 months again which will amount to ….. 123 billion.

The next round – assuming rates will Not come down any time soon will be ….. 125 billion.

I wonder when “Investors” lending Money to the gubment realize they are – absent a “greater fool” – paying themselves.

Exponential growth gets you in the end.

This is a good deal for investors. It’s not a good deal for taxpayers. You need to distinguish those two.

1) The banks dumped 210B treasuries and 332B MBS to cut their losses, paying 4%/6% dividends.

2) In the next 15/18 months investors Might pour in $4T to US gov. If

investors refuse to buy long duration, unless the 10Y double to 7%/8%, the Fed Might raid in “other” people bank accounts and CDs to suppress bonds, notes and mortgages rates, to reduce the toxic debt payments burden.

3) The yield curve might stay inverted for 3 more years.

4) In Jan 2025 the next gov might run out of cash.

5) US economy might sizzle due to the raids.

Interest Rate suppressing raids that are actually MOAR QE?? Man you sure can think outside the box.

Yes I think this debt ceiling raise through 2024 means the next administration goes broke on Inauguration Day.

I would not listen to Bloomberg and go directly to the source. As per Yellen’s statement, TGA refill will take place in June, July and September, and they will most likely skip August.

I assume, Yellen will try to pull out the sleeping reverse repos into Treasuries. So, the refill will have as little impact on financial markets as possible. Expect not much volatility or stock market diving down or much rise in long term treasuries.

On the other note, it’s nearly impossible to predict what will happen later this year, even central bankers are clueless and go from meeting to meeting.

Once long term yields will rise, as Wolf mentioned, it’s good news for treasuries and fixed income investors, but bad news for FED, inflation will enter into vicious cycle and will start spiking higher. This is why FED is frustrated with sticky inflation. They sure know, that window for soft landing is closing fast.

Those who are ONLY rolling the short treasuries feel like geniuses right now, but will pay price (loose they profits) later on. Let them learn by experience.

Wolf great article again!

We knew that. And it’s happening. Investors in bills and CDs are finally getting some yield, after 15 years of getting screwed.

Screwed since 1990 or 1981 take your pick. For 33 or 42 years savers and retirees have gotten the short end of the stick.

We will soon see if supply and demand has gone out of style, I suspect not. The other thing, way back in the 1980s when bond traders were fighting the Fed, they were labeled Bond Vigilantes and pilloried in the press. So why isn’t the corporate press all over bond buyers who are fighting the Fed this time around?

Perhaps because its sovereign bank buying that supports dollar hegemony.

Every one tries to dominate with their currency. But few succeed.

This big deal BRICS thing is so funny. The only one not a basket case is China and even the yuan is dubious, as the largest asset in the world, Chinese RE approaches collapse.

Re: India: Vietnam, pop 200 million has as much value manufactured exports as India.

South Africa? Don’t go there. Except to say: every business needs standby generator.

At some point wallflowers dance: ‘ll take yuan if you’ll take rubles..’ The latter having fallen as usual in the last 2 weeks.

Note latest: Hong Kong may be unable to hold US$ peg, its traditional benchmark. The CCP is closing in on the prerequisite for real markets: freedom. The CCP has arrested short sellers or even market commenters for ‘disturbing social order’

The US $ is still the cleanest shirt. The ruble is a rag. If you want to wipe the smile off a Russian exporter, ask if you can pay in rubles.

Saw the following newsbyte June 18th(Unusual Whales). Wasn’t sure what Dalio meant then or after reading the article(which, granted, I didn’t entirely understand).

“Billionaire investor Ray Dalio has said that U.S. government bonds are becoming risky as the country falls deeper into its debt crisis.”

I’m willing to take those risks if I get paid enough to take those risks — in other words, if the yields are high enough. That’s how the bond market works.

You can sell the worst junk-rated corporate bonds with a big risk of default, but the yield might have to be 20% to attract buyers.

Seems like a good bet.

Thanks for the response.

Price decreases as supply increases.

– “Coming Onslaught” ??? Not before the yield curve is no longer inverted anymore. And even then I expect rates (both long term & short term) to go lower. Only after that I expect long/longer term rates to explode higher. But we’ll have to wait & see what the future brings.

– “Complacency” ??? Absolutely !!!!

– The notion that the FED can control interest rates is absurd. E.g. I blame the war in the ukraine much much more for rising interest rates than the FED. Complicated story but it has to do with deteriorating Balances of Trade worldwide.

Lower rates will not be happening anytime soon. You can take it to the bank. Inflation has barely budged from the largest hikes in a long time. It’s not over, and I’d be willing to bet they will have to go higher than they currently think before they finally bring inflation to heel. Out of control government spending is largely offsetting what they are doing right now, so “higher for longer” it will be.

Don’t you think that Treasury and Fed are in a box. In issuing short term treasuries they are trying to draw money from reverse reposes which will not draw liquidity from the system. The downside is higher interest rates. Moving to long duration treasuries will draw liquidity from the system and, as you point out, require higher interest rates. All of this is occurring as the interest expense approaches a trillion dollars a year.

Don’t you think that there may come a point where the interest rate necessary to attract buyers is high enough that the Fed says enough and switches to QE from QT?

The reverse repos (RRPs) at the Fed are a result of Treasury money market funds drawing a huge amount of cash from investors, and they’re buying Treasuries with part of it and they’re keeping part of it liquid via reverse repos at the Fed. And they have also cut their funds on deposit at the banks because now they keep most of their cash via RRPs at the Fed. So these RRPs are an outgrowth of investors storming into Treasury money market funds and of banks not paying enough interest.

“… that the Fed says enough and switches to QE from QT?”

The Fed isn’t going to switch to QE (unless the world collapses). You need to get that out of your mind.

Dishonesty rules!

I am in short term treasuries because my mattress is not safe from fire but am very concerned.

The debt gets bigger and bigger.

The rulers are richer and richer.

There will be plenty of demand for notes, bills, and bonds regardless of the foreign buyers. Pension funds need them to create their annuity streams, companies want them to park their excess cash, and millions of seniors, with cash still in the bank, are going to come into the this market as their home town bank continues to low ball deposits.

Things have a way of going differently than logic expects. With the high mortgage rates, who thought homebuilders would be booming thanks to all the trapped existing homeowners who can’t/ don’t want to sell and move because they’d have to refinance at 6 or 7 vs their current 3% rate?

The Consensus outlook in October 2018 when 10Y UST was 3.0%: 3.5% or even 4.0% in 2019! Then !WTF! down it went until August 2019 when it arrived at 1.5%. When everyone thinks something is going to happen, prepare for the opposite.

The consensus outlook is for rate cuts and lower yields.

“The consensus outlook is for rate cuts and lower yields.”

Maybe the media consensus. But not the real consensus.

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Yes. And in terms of the short-term Treasury market, they’re already pricing further rate hikes, and no cuts this year and not even through mid-2024.