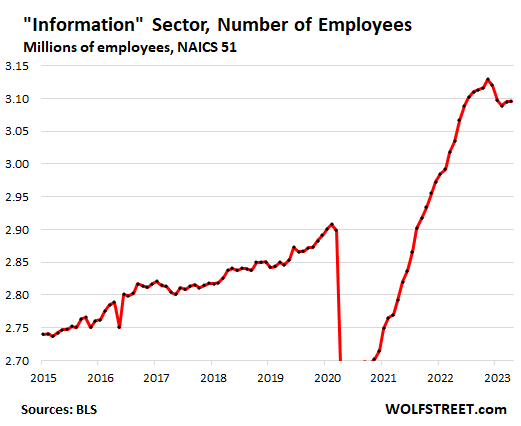

Even employment in Information has been rising for months despite layoff announcements, after a dip last year. Month-to-month wage growth re-accelerated.

By Wolf Richter for WOLF STREET.

We’ve been waiting for the landing now for a year – soft or otherwise. The Fed has jacked up interest rates to over 5%, which a year ago seemed unthinkably high, and everyone has gotten used to it, businesses and consumers. Prices have been rising at a hot pace, though price increases have shifted from gasoline and food and used cars to services, and people and businesses have gotten used to it. Wages have been rising at a similar clip, and everyone has gotten used to that.

Some horribly managed banks collapsed and were dumped into the ditch, and everyone knows there will be a few more banks to get dumped into the ditch, and so what, everyone has gotten used to it. A couple of PE-firm-owned auto dealer-lender chains, specialized in selling overpriced used cars at huge interest rates to subprime customers, collapsed. And there were some fiascos in Commercial Real Estate, and they’ll keep coming.

All the while, employers are hiring, people are working and making more money, and spending it, and the labor market just keeps cruising along at a good altitude. All it has done so far is that it has come down from the stratosphere.

And the soft landing – or any landing – of the labor market that the Fed has been looking for, well, the Fed is just going to have to keep looking for it, because for now the labor market just isn’t landing.

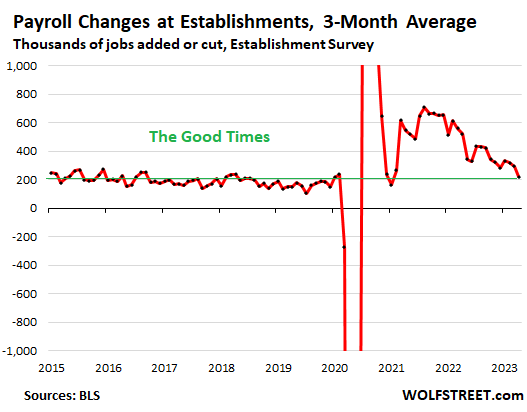

In April, 253,000 jobs were created by employers. There are now a record 155.7 million payroll jobs, based on surveys of establishments by the Bureau of Labor Statistics today. Over the past 3 months on average, 222,000 jobs were created per month. This three-month average, which irons out the month-to-month variability, is at the upper end of the range during the Good Times before the pandemic:

The drop in tech and social media employment is already over. The lay-off announcements we hear are global, and the ones that get into the news are by huge companies, and they’re still hiring, even while they’re laying off people, and the laid off people are quickly hired by other companies.

The Information sector serves as a stand-in for tech and social media companies we hear about. The sector covers only a portion of them; other companies are spread over other sectors. But it gives us an indication.

After a hiring binge through November 2022, the number of employees in Information fell off 1.3% over the next three months through February. But even in this hard-hit sector, employment is resilient and rose again in March and April. Now at 3.1 million, employment is where it had been in June and July last year, and remains below the peak, as companies are rebalancing their work force and wringing out the excesses:

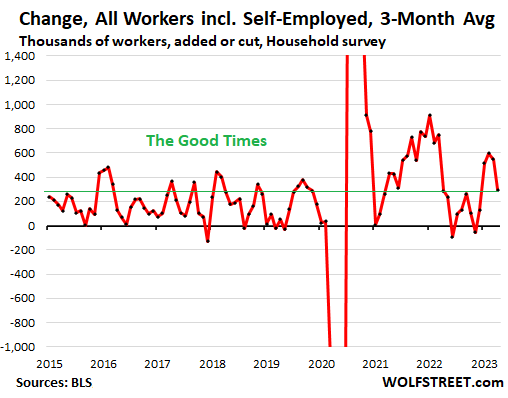

Total jobs, including gig work. In the broader household survey, which includes other types of jobs such as the self-employed and contract work in addition to payroll-type jobs at establishments, showed that 298,000 jobs were created on average over the past three months through April, which is also at the upper end of the range of the good times. This pushed the total of all kinds of jobs to a record 161.0 million.

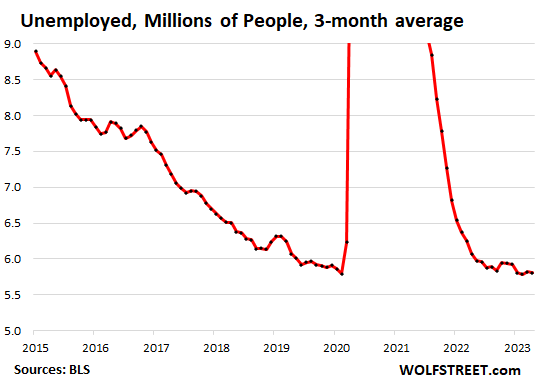

The number of unemployed people who are actively looking for a job dropped in April to 5.66 million, the lowest in 22 years, according to the Household Survey by the BLS.

The three-month average dropped to 5.81 million, in the same low range as in the prior months, and along with February 2020, the lowest in 22 years.

This is still a very tight labor market, and most people who are getting laid off and fired for other reasons or no reasons are quickly finding other jobs.

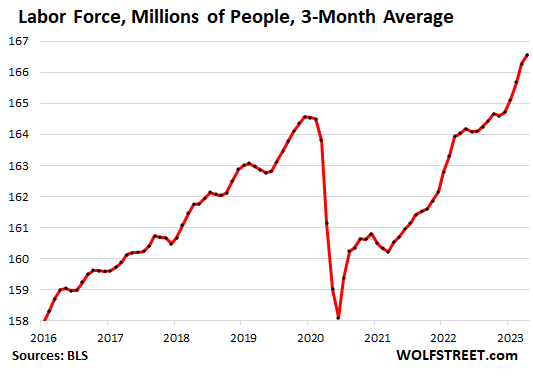

The labor force is growing as the tight labor market and rising wages are pulling people back in. In April, the three-month average rose to a new record of 166.7 million people who are either working or actively looking for work:

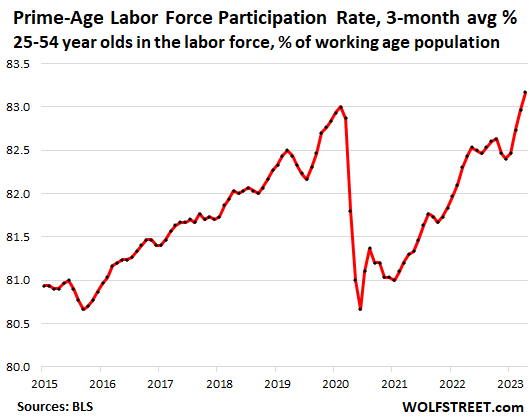

The prime-age labor participation rate – people aged 24 through 54 either working or actively looking for work – rose to 83.3% in April. The three-month average rose to 83.2%.

Both were the highest since before the Financial Crisis. People in their prime working age are now participating in the labor market, working or actively looking for work, at a rate not seen in 15 years.

The prime-age labor participation rate eliminates the complex issue of the so-called “excess” retirements that have rippled through the labor force during the pandemic.

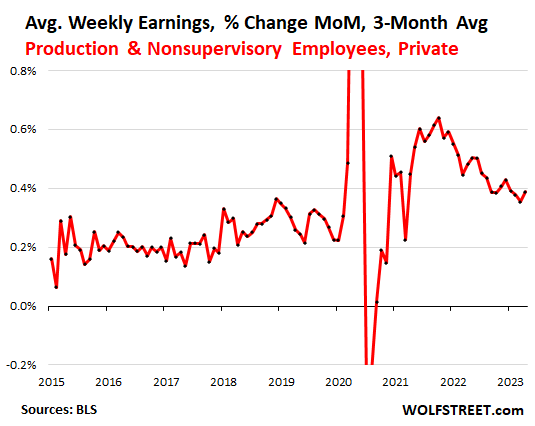

Wage growth cooled off, but looks like it’s ticking up again.

Average hourly earnings of all employees in April rose by a hot 0.5% from March, the highest month-to-month increase since March last year, and much higher than in the prior months. The three-month average rose by 0.34%, up from a growth rate of 0.28% in the prior month.

Average hourly earnings of production and non-supervisory employees rose by 0.4% in April from March. The three-month average also rose by 0.4%, which, annualized, comes in at just under 5%. These are engineers, teachers, bartenders, technicians, drivers, retail workers, wait staff, construction workers, nurses, etc. in non-supervisory roles.

The month-to-month re-acceleration in wage growth might be an early indication that the decline in the growth rate of wages has ended, and that wage growth is stabilizing somewhere near 5% year-over-year, rather than continuing the downward trajectory that started a year ago (when wages grew 7% year-over-year).

Here’s the three-month-moving average of month-to-month wage growth of production and non-supervisory employees:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is what happens when you scale back rate hikes prematurely. The FED should have continued with 75 basis point hikes the entire time. Instead, they chose to entrench inflation even more.

Do check the inflation reading next week! I predict it will change course, and will get revise 0.1% to 0.2% higher after a couple of months :).

Here in Tucson I can tell you so many businesses whether suppliers or restaurants

are short on workers – talking 1/3 tables sit empty

or you get the we’ll get to you in couple weeks maybe

or we don’t have these parts/supplies

and btw price has DOUBLED

I paid day workers $20+ to get enough bodies on project

still ended up on day 3 with 2 – myself and son

Wow, did you guys see the news on RE in the BayArea:

“Bay Area home prices spike 17% as sellers pull back”.

Sales volume is low, sellers are not making an appearance and homes are still selling.

The resilience – considering the uncertainty, sky high prices and high rates – is really astonishing.

Richard,

LOL, BS, propaganda for the ignorant 🤣 That was from February to March, month-to-month median prices get a little jumpy and plungy, don’t they?

Year-over-year -13%

From peak: -20%

Data via the California Real Estate Association, same as your headline month-to-month data.

Would have helped if you had read a little more than the headline… this headline stuff is just hilarious when people stick it in the comments dressed up as some kind of global truth, LOL. You guys crack me up.

Hi Wolf,

Yep, -13% yoy

-20% from peak.

I like so see that. I am in the process of buying and hope for lower prices :). Although, not trying to buy in the Bay Area.

Nonetheless, I couldn’t believe prices in the BayArea went up 17% month over month. That’s a huge freakin jump – again, considering the current environment. That doesn’t sound like the spring selling season is cooling in then bay area – at all.

I am not paid to prop up the market and I don’t benefit from higher prices – at all. It’s me being surprised, almost shocked at such a jump. Completely unexpected.

Don’t get sidetracked by month-to-month changes in median price. If more high-end homes sell than the month before, the median price spikes, not because houses have gotten more expensive, but because the mix of what sold shifted. Median price is heavily skewed by mix. And that happens a lot in the spring.

Agree. What they’re trying to do is look like they’re trying hard, without actually doing it. They would love a few more years of 8% inflation while pretending that they don’t.

They really need to drain the swamp more quickly. QT isn’t working fast enough.

If the Fed were anything other than shysters they wouldn’t have bought MBS.

They had no remit for MBS.

Housing was already absurdly high.

The only reason to buy MBS was to cause inflation.

Therefore the Fed cannot be trusted. Ever.

Totally agree

We all should know fed is a fraud and fed only works for their rich masters .

I respectfully disagree with that Fed scenario and propose a different one.

Hypothetically speaking, the Fed is an apolitical agency that pays no attention to the Presidential election cycle. In reality, they are walking a tight rope between what needs to be accomplished financially and the effect they have on the outcome of the up-coming election. Carter vs Reagan.

They have a late January date with infamy where the credit mess and the temporary suspension of asset prices reverses, nagging inflation that persists at the same rate, the concentration of wealth into a cartel of banks that represent significant domination of publicly traded markets, etc. are politically expedient to deal with.

I agree with their current approach not only from the political sensitivity aspect but also from a logical perspective that the gradual unfolding of a bloom is better than an explosion.

A gradual unfolding is like water torture, getting pin-pricked to death. Better to eradicate the problem swiftly.

It’s the same principle with cancer. You need to cut it out.

Right now, anyone who does not own a home is forced to accept a huge amount of uncertainty. It’s to the point where many of them will never be able to buy a home, or have children, or retire, without taking on unbearable financial risk, which is watching 6-10 years of working income evaporate in the wind.

The Fed made the mistakes that caused this problem the last few years. The Fed needs to quickly reverse the elevated asset prices and inflation before they become entrenched.

The Fed should be aiming to create a quick asset price reduction, to quickly reverse inflation. A period of deflation is in order to reverse the huge inflationary gains of the 2021 to 2023 period. Otherwise, we’ve just witnesses a massive, permanent 20% wealth transfer from lower income classes to wealthy classes. The Fed’s job is not to permanently rearrange wealth based on experiments gone bad, or whims. Major wealth changes should be based on decisions of the people impacted, not some authority from above.

The Fed needs to reduce the darn balance sheet, like yesterday. In particular, the Fed needs to get serious with its MBS reduction.

And those who do own a home are forced to accept a great amount of uncertainty as well. That’s called risk…. you accept it when you buy (or seek to buy) non-liquid assets.

Maybe I’m stupid, but what if the Fed does sell the MBS? I don’t believe that cancels the mortgages….. they’re still in effect at the current interest rates and terms – the Fed would simply take a haircut on the value of the security, and those losses might effect the remittances to the U.S. Treasury, exacerbating the budget deficit. It might also serve to make mortgages more expensive and harder to get…..

So…. how does that improve housing affordability? Enlighten me.

If the Fed sells MBS, long-term interest rate will rise, thereby kicking off a cycle that reduces inflationary investment. Any deflation that occurs would just be a reversal of runaway inflation we’ve experienced the past few years, to get the economy back to a sustainable baseline.

Sure, this would lead to debt write-downs, asset price declines (stocks, LT bonds, and RE, etc.), but it would stop inflation quickly and reduce asset prices to a level that encourages confident investment. Financial stability would be restored; the future would be bright. The generational wealth transfers would correct.

In short, those who benefited through mistakes of the Federal Reserve would transfer some of their wealth to those who actually earned it.

I agree with you 100%, I am in that same boat you speak of.

I am in late 30’s and can’t afford a home, child or a wife.

This is rediculous and the current owners who bought way over price because of FOMO, sorry but that is their stupid fault.

When it came to unleashing qe and rate down they did it in a explosive way which per you is OK.

But for the opposite which is qt and rate hike we need to go at glacial pace whic seems to have meaningful impact 🤔

I really dont think ANY of this is about rates. It is about the fact that the central bankers STILL have trillions on their balance sheets. The rate they are performing QT on a global basis (Fed, ECB, BOJ, others) is pathetically slow, compared with how fast they increased it. Since money is fungible, the actions of the ECB impact the US and Japan, etc.

So why is the pace so slow? Because they simply cannot sell it faster without incurring even more massive losses. The unrealized losses were at one point around a trillion for the Fed. Does the ECB have an even bigger unrealized loss, since they went even lower with negative interest rates? and who knows what the situation is with the BOJ?

Total and complete incompetence. The much smarter way to tighten economic conditions would have been to sell off the balance sheet when interest rates were much lower.

Selling the balance sheet would have a different mechanism for transmission of tightening. It would have popped the bubble on asset valuations, hitting the rich and corporations in the pocketbook, which would have pulled back the hot job market and real estate market.

The unrealized losses should have NEVER reached this level. NEVER.

The path the central bankers chose has propped up bubbles in the short term, but massively increases risk in the long term, as they have a balance sheet that could fall into even greater unrealized losses if interest rates are forced to move higher.

At some point in the next 3 months, I see long term rates exploding higher and that is when things get nasty (real estate, equities, bonds, government budgets), it all gets real ugly.

Perfectly put into a nutshell, I command you Sir!

don’t forget about the sillyness of the banking crisis

someone is spoofing these banks – so they can go short

or ECB can push their problems down road

while FED fusses with US issues

not sure what is taking place here

don’t get caught in crosshairs

Can you explain to me why losses at the FED matter at all? They are not a going concern and print their own currency.

Agree shut will hit the fan soon!

And only another 15% Fed Funds Rate increase is needed ….. to match Volcker’s 20% Fed Funds rate in 1981 ( prime rate was 21.% then also) ……

The Fed chief refuses to even bring up the excessive Federal spending which is now the driving force in this recent inflation. Volcker and Greenspan brought this up repeatedly. They are on record. Powell won’t even suggest that this is having any impact. A reporter asked a direct question and he dodged it. That’s because he’s a political hack of the worst order. He will have to keep raising interest rates as the current rate increases haven’t done squat to dampen inflation. At some point the interest rate increases will lead to a total collapse of the banking system. He needs to do us all a favor and for the sake of the country, hand in his resignation.

Expect more rate hikes and higher inflation!

Meanwhile, what’s with the one month TBills? Yields jumped 1%?

Article coming. It’s wild.

There’s a lot of wild in this market nowadays.

Benw like banks failing and markets going up,absolutely bs. Then they parade tech executives into White House forAI conference,more bs it’s about fedcon . Exit stage right

The 1mo leaped 107 basis points overnight. May the 4th be with you!

The yield curve is as insanely inverted as I’ve ever seen it, and has historically been a very reliable barometer of recessions (hence my username on here).

But don’t just take my word for it, marvel at it yourself:

Another market truism that has been learned and re-learned time and again: “Don’t fight the Fed.”

Wolf, the landing might be cancelled for now, but IMHO we are well on our way to that involuntary landing site.

In the meanwhile, I’ve got a vast majority of my net worth in 3 to 6 month T-bills, re-investing as needed, and enjoying very safe 5%+ returns that aren’t even taxed by the state.

When there’s blood on the street (at the involuntary landing), I’ll redeploy in the market. Until then, 5%+ APY is helping to keep the FOMO in check.

That wasn’t overnight. That happened yesterday after the T-bill auction, but there was some kind of issue (Tradeweb?) that caused the charts not to be updated. The official closing data yesterday by the Treasury Dept. reflected the big jump (to 5.76%), and today, the yield actually FELL to 5.59% at the close today.

I don’t think I’ve ever seen wild stuff like this.

And the yield curve has been inverted since early July. That’s what happens when the Fed pushes up short-term rates and the stupid-ass banks refuse to sell their long-term securities because they believed in the pivot BS, and bought more instead, and so now this is causing those stupid-ass banks to collapse, and now they CANNOT sell their long-term securities because they would lose a ton of money and collapse, and because the banks bought, instead of sold, at the time, and because lots of others bought instead of sold, long-term yields were pushed down. This is what caused the yield curve to invert. It doesn’t predict anything; it’s a reaction to the Fed pushing up the front end, and banks holding down that back end.

Is it called a landing when the plane crashes into the ground at 600 miles an hour?

If the Fed are so keen to remove inflation why:

1. don’t they fully include land prices into inflation stats, instead only incorporating the monthly cost of carry?

2. Why did they buy MBS,with no remit, no expectation upon them to do so?

Question 1 is the answer to question 2. Housing is how they print when they don’t want it to show up.

What’s going on with the High Yield sector? Are the spreads widening?

Not really. Spreads widened a little bit a year ago into June, and then they just wandered up and down a little. CCC spread is now where it had been in June; BB spread is where it had been in May. There is no financial stress in the system. And the Chicago Fed National Financial Conditions Index is still negative and has dropped over the past month.

It’s like everyone has gotten totally used to the higher rates and higher inflation, and is fine with them, and no biggie if a few banks collapse, and so the financial conditions are not tightening.

This inflation fight is far from over. I smell another wave.

Intellectually, it is hard to imagine a completely opposite regime of monetary policy, the “flywheel”, from the dominant QE philosophy to a more sober Keynesian emphasis. The disruption is profound. The chaos is certainly reflected in the series of grotesque economic graphics that your article featured, as well in the functioning, or not, of the public markets. Which includes the largest single market in today’s universe, US Government debt.

In summary, mis-pricing is always suspicious.

I await your wisdom.

When is the next in-person party?

I’m saving this page to come back and comment after this article agrees like milk a few months from now. Lol

Last paragraph of gametv’s comment up thread.

Bond traders are taking advantage of the debt crisis. They know one side is going to blink, most likely Biden. At one month out, the 4 week treasury bill is now dropping in price with people hoping the crisis will get averted, so the yield will crash, pushing the bond price up, making them money.

That’s my guess at least.

That is an interesting take from the casino point of view but hardly representative of the upper median citizen of this country who is unable to participate in any meaningful way. Taking advantage of others misery is not making money in the traditional sense.

There once was a light at the end of the tunnel. Now that light is moving farther away as we approach. I’m not going to make sense of what I just said, only it’s dragging on.

If 4-week yields are up wouldn’t that mean these bills are being sold rather than bought?

Every sale has a buyer.

So soft landing on approach. Please raise your seat tables to the upright position and deposit your trash when the attendant passes by. :)

Nevertheless, remember your seat cushion can be used as a flotation device. In the event you do need to use it, feel free to keep it, compliments of Powell Airways.

nah, not soft landing…I think with numbers like this, we’re headed for first class comfort landing…a landing so smooth, you won’t even noticed the tires hit the tarmac..

Hmm…strange time we live in…just what IF Pow Pow is able to pull it off and tame inflation and keep the economy churning as business as usual…think I seen it all and at this point probably rule that out…

Speaking of soft landings… I remember back in the 90s I was on a 737 from Maui to the Big Island. I thought the landing gear was going to break off!

> first class comfort landing

Watch Canada

When I saw the report, I thought “ohhhh, market is going to hate that, higher for longer ahead.”

Slight miscalculation.

It’s a win-win situation for Wall Street.

1. If rates stay high / go higher, it’s because the economy is strong. Stocks go up.

2. If the economy weakens, the Federal Reserve will lower rates, juicing asset valuations. Stocks go up.

Tis the way it’s been… good news is good news, bad news is good news.

In an asset mania, yes

Well each one of us must examine ourselves whether each transaction that I am considering is programmed by Wall Street AI or by free will.

Perpetual motion zombie dance continues, years and years after I thought it possible.

Estimate how long you think the madness can last and then multiply by 5.

Now I will watch Powell’s “data dependent” reaction next time.

still still still way too much money slashing around out there. It will take rates over inflation to turn this around. And some aggressive QT.

Agree with Longstreet.

Wife and I went to Bay St Louis, MS last night expecting to find a seat overlooking the bay. This is an artsy community usually very slow on a Thursday night.

Parking lots all full so settled for a bar & grill inland.

So much money is loose and sloshing, huge bets are placed on financial assets — stocks AND bonds. You can invest with AND against the fed. Something is out of whack here. You can bet every slot on the roulette wheel and have money left over. Which portends prolonged confusion. Which suggests to me, more aggressive tightening is called for.

Huge bets denotes, win or lose, ones capital is at risk which brings to the forefront the actions of the Federal Reserve Bank of the United States of America in the ongoing resolution of the problem that spawned the QE era. The back story that, since the mark to market requirement was dissolved, flamboyant, leveraged financial entities have defined the past 15 years,

They will fail the common investors and hard working families.

When the dance is over ,lock the windows ,=Russia

Maybe this is what a soft landing looks like in the crazy world we find ourselves in now. After all, I’m pretty sure everything looks dandy from the perspective of the 0.01%.

I’m starting to think so, the planned landing will be so soft that it will take 10yrs to touch down, but more likely we just overshoot all the runways and hit a mountain instead. Though as wolf says over and over, relatively speaking this has been the fastest rate hike cycle in a long time, so for all those who believe the system is dependent on ultra low rates then 5.25 is high for a lot of people.. curious to see what happens over next year or so now.

That’s why folks get rich. Peasants take the first losses. They are at the bottom of the capital structure, and insurance regime.

Peasants often take the first losses because they attempted to live like the rich and went ass-end-over-tea-kettle into debt to do it.

Many average folks get *rich* (as in millionaire next door types) because they have patience. I personally know many. They spent their money on things that generated wealth, not a $70K pickup and a $1,400 phone.

So true ,autos worst investment in history,followed by fraud Enron ,banks ,houses they all crash it’s like a merry go round ,which company falls off first.going to get way worse .USA doesn’t manufacture enough at a reasonable price to compete ,can u spell RESET

Interesting how we first worlders must shave that fraction ever smaller to be sure we’re standing on the right side of the line…

Isn’t being in the top single percenter digits great enough? We’re leading the rat pack and mostly we were born into the lead, that’s kind of like an inheritance! And yet the criminality in our society is amazing, and that’s why we shave the fraction….

The 3 mos average chart that is posted is showing clear deterioration.

Isn’t that the more important chart especially for a coincident/lagging indicator like employment ( especially post COVID) when labor simply couldn’t be found and thus encouraging companies to hang on or hire employees on an even more lagging basis?

What it shows is a RETURN from the Stratosphere to the high cruising altitude of the Good Times.

I think it is too early to tell but certainly the trend line in the “Payroll Changes at Establishments 3-Month Average” is pretty steep going down. As you say we are now back to the “Good Times” level but what makes you so sure it is going to start plateauing at this level as opposed to continuing the downward trend?

I mentioned many times, the average Fed Funds rate over the last 50 years is 4.75%. So it is no surprise to me that employment numbers just cruise along like they are normal (or as Wolf says, good times). The current 5.25% Fed Funds rate will not put a significant damper on employment.

Nor will it do much to reduce inflation, as we have seen. The rate must go much higher and faster, and if Powell really wants to get down to 2%, well, rates probably have to go double digit. It’s been done before, the country survived, actually thrived eventually. We are all still here.

So it has been a tough week for Powell. He must be thinking, what the hell do I have to do to get unemployment up so inflation will go down. I think he may have given up on waiting for the proverbial lags to kick in. He will realize that much higher, much longer is needed. He needs to seriously review what Volcker did.

I will end with the scary part. Raising rates by 50 or 25 basis points every month and half allows the economy to adjust to get back to where it was before rates were raised. So far only a few banks have eaten it and some auto dealers (all run by crooks imho). The poor may be suffering from high prices, but most are on the dole which is COLA. Otherwise it is party time for most workers.

Bullard said in November that a 7% terminal FFR might be necessary. At 5.25%, the FFR is now slightly above ALL ITEMS inflation. Most likely, a 6% FFR would really start to slow the economy. It’s unlikely that the Fed will get to 6% before October of this year. They’re most likely going to pause in June, and it makes sense. Swings in the FFR easily take 18 months to really start having an effect. What’s needed to push the economy further down the recession / slowdown path is a 5-7% selloff in the stock market. A zig zagging higher stock market increases people’s wealth effect, meaning they keep spending money. I agree with Mish & others that the jobs market is continues to look very resilient. Last, I think JPowell is playing the long game for a reason. He really doesn’t want the housing market to tank and with good reason. JPowell knows, for the next 24 months, 6% 30YFRM mortgages aren’t going to tank housing. It’s all about housing. They’re scared to death of what “eventually” will become a wave of foreclosures, if unemployment rises to 5%.

“They’re most likely going to pause in June, and it makes sense. Swings in the FFR easily take 18 months to really start having an effect.”

Bullshit. Your entire post.

I agree with Depth Charge, this is a bullshit post. Powell has strongly intimated that he WANTS to bring housing prices down. The idea that he somehow afraid of doing so is nonsense.

Then why did he buy MBS?

Housing market is not tanking but going down in prices in an orderly fashion

I personally believe this ridiculous asset market needs to come down a lot for the good of common people

We need more hikes and aggressive qt

Lincoln said, “the Lord must have loved the common people because he made so many of them”.

“What’s needed to push the economy further down the recession / slowdown path is a 5-7% selloff in the stock market”

The sentiment that stock market can only go up in a long term is so entrenched now that 5-7% market selloff will hardly leave a dent in it. As other posters pointed out, market is in a mania, and it will take a real shock treatment to break this mania IMHO (similar as it is with the psychiatric patients in a mania).

AK,20-25% will deflate the balloon,but not enough . Everything is overleveraged,except brk

The 2% target is a false goal

What of the previous two years…never happened (14%?)

YOY time frame means little IMO

February and March got revised way down, right?

All revisions are included in this data. What you see is post-revision.

In addition, the three-month moving averages here smoothen out the month-to-month squiggles so you don’t get distracted by statistical noise and can focus on the trends.

Thanks, I was also wondering about the revisions.

Yes, revisions are always and automatically included in everything I do. The employment data, as well as a lot of other data, get revised every month, and the revisions are always automatically included.

Occasionally, I want to show both in the same chart: revised and unrevised, and I will make that clear and color-code it.

Here is one of those rare examples:

https://wolfstreet.com/2023/02/10/cpi-just-got-revised-up-for-october-through-december-revisions-take-a-bite-out-of-disinflation-hoopla/

Also try to find the revisions in this chart. This is the total number of employees, 156 million. The revisions are such a small number compared to the 156 million that they cannot be seen here.

It’s worth knowing that you update the charts to reflect revisions even if they’re not readily visible because of the scale. Thanks again.

So there is little evidence that the BLS is “cooking the books” with the business Birth-Death model? Lately, I also noticed the revisions were downward.

Harry Houndstooth,

January was a HUGE upward revision, much bigger than the downward revisions in Feb and Mar. And back then, the blogosphere got all riled up because it was an upward revisions. Now they get riled up about the downward revisions, LOL. These people people don’t even understand what they’re talking about. They’re just producing clickbait.

I can’t be the only person whose IRA cash account prior to these rate increases was earning a $1 a month and now that cash is paying me over $300 a month. The added income for retirees has to be in the hundreds of millions of dollars.

Good point. Plus add in the SS COLA increase the past 2 years. That has to add up to a lot too?

Ru82 ,it adds up too less money because of under reporting of inflation.THEFT

Sure, you might come out ahead in the short term if your expenses

are low and fixed, but your long term savings are being eroded by inflation. That short term outlook is what is feeding into the inflaion mindset.

Yes Old folks sometimes get sick and sometimes need to buy a new vehicle, Then the Bank of Mum and Pop feels and sees the inflation.

Too bad the cost of everything you buy is up more than 300$ a month

Inflation is theft

and those who promotr any inflation or allow inflation when they are charged with not allowing any inflation (stable priced) are thieves themselves, serving a different master

Doesn’t this indicate that the Fed’s gradual rate hikes really have not had much of an impact on inflation? That inflation is likely to continue on at the present unpleasantly elevated level we now enjoy, far above the supposed Fed target of 2%?

Quite frankly, this market leaves me with a queasy feeling deep in the pit of my stomach. Some economic indicators are screaming recession; others (such as employment) are supporting the return of the “Good Times.” Market is panicked on potential bank runs – then a day latter races skyward on Apple earnings. Half the pundits are proclaiming SPY 4500 by December, and the other half are buying gold, ammo and canned goods. PEs are at nose bleed levels, debt is at $32T and nobody seems to care. Are we going up, down or sideways – my God, for the first time in my life, I have absolutely no clue. Thus, the churning guts…

DDG ,the pros can’t figure out ,what the hell is going on either,but the billionaires club know,and the end game is always to buy assets for Pennie’s on the dollar.JamieDimon is the fox in the henhouse. dANGEROUS

The market is not the same thing as the economy.

I think that feeling is widespread. The Federal Reserve has created a massive amount of macroeconomic uncertainty with its constant interventions, flip-flops, and mixed messaging, and short-term focus, most of which acts to reduce confidence and increase moral hazard, as well as systematic risk.

The Fed is contorting itself trying to reduce inflation while retaining the asset price bubble.

For everybody’s sake, the Fed needs to increase the rate of QT so asset prices come back to Earth.

Not gonna happen. Bears getting rekt, get used to it and move on already!

What is means is higher rates for longer.

It happened before and itd happen again

Just keep your popcorn ready 😉

Looks like you are in the camp that market can only go up

Not sure why it’s confusing. Employment is always high at the beginning of a recession/end of debt cycle. How could it be otherwise?

Ditto. Many of the indicators I follow have us teetering on the edge. We’re very close, but dragging it out.

think of employment as resolving the past: too many businesses created by free printed money and business decimated by Covid deaths and retirements. This past equilibrium will probably resolve itself this year imho. Now think of layoffs, business closures, bank failures, debt ceiling, massive deficit spending, dollar devaluation, biting inflation geopolitical uncertainties, RE and stock bubbles, etc…think of these as resolving the future. Very bleak outlook. So the past will be resolved shortly and the future has already begun, and has a long long LONG way to go(to resolving).

Based on anecdotal evidence, some of the layoffs will be accomplished by *retiring* people. A friend of my daughter’s at GAP just got launched…. after 22 years. He’s over 50 and they, seemingly, cut the high salaried older people. That accomplishes two things: Gets rid of the high salary (duh) and lowers their cost of providing health insurance as it’s cheaper to insure young ‘uns. Might also have an impact on the cost of their 401K corporate contributions as the younger folks often don’t participate and, if they do, their salary is less.

Same thing happening at auto plants and staff. Stellantis is offering buy outs to 3,500 hourly and an unknown number of salaried positions. GM launched contract workers at their “Global Technical Center”. Contract workers don’t often show up in the industry numbers as they technically still have jobs at their agency…. but the agency may not be able to place them. My old alma mater used to crow about how they never had a layoff, but would kick the long term contract workers to the curb without blinking an eye.

I didn’t know that The Gap was still around.

If Stellantis makes a new 95 Intrepid I’d buy it.

How much AAPL do you want to own on the morning China moves on Taiwan?

Fantastic company, but…..

This is why Warren got out of tsm, Taiwan = sacrificial lamb

ONCE INFLATION BECOME (AS POWELL LIKES TO SAY) “ANCHORED” IN SERVICES, IT DOESN’T GO AWAY. IT FEEDS ON ITSELF. THE ONLY WAY TO ROOT IT OUT THAT WE KNOW IS INTEREST RATES HIGHER THAN THE RATE OF INFLATION FOR LONGER AND SIGNIFICANT SHORT TERM ECONOMIC PAIN.

Please locate the CAPS LOCK key on your keyboard and press it exactly once, which then allows you to type in lower-case.

😆😂🤣.. it’s so much better when the site owner intervenes.

People who type in all caps: Your message is hard to read and ignored by more people than if you had just typed normally, it does the opposite of what you intend. To put another way, your message stands out for sure, but only as one to ignore because it’s not coming from a serious person.

Cheers

…maybe Dan just needs a new vision rx?

,may we all find a better day.

Sorry. It was accidental. And then I didn’t feel like retyping it.

I learned to type on an Underwood.

I checked out self storage rates to store some of my business materials. They are up 300% from 10 years ago, Up 25% YoY, and there is a waiting list for units of 10 x 20. Inflation is not going down. Its accelerating. All these Powell interest rate increases haven’t done squat.

SC,

I can explain that one. Everyone who took all their Covid stimmie money and bought jet ski’s, boats, classic cars, guns, and hot air balloons need somewhere to put it. You know, in case there’s another government emergency.

Courtesy of J-Pow and the Fed.

People die, there are whole housefulls of stuff and what do you do with it? A guy a few years ahead of me has well to do parents, one died, one in rest home, and just reams of stuff he can’t dispose of promptly.

phleep wrote: “… there are whole housefulls of stuff and what do you do with it? A guy a few years ahead of me has well to do parents, one died, one in rest home, and just reams of stuff he can’t dispose of….”

I live in a retirement complex. This is a very common situation. The children aren’t getting married & forming new families.

So the demand for gently used stuff is zilch.

We have been watching one new couple move their stuff in, and wondering how they (and all their stuff) will possibly fit in the unit.

Who in the hell got enough stimulus money to buy all this stuff,my son and brother,business owners. Biggest scam in the world

I’ve never understood why so many people spend so much money to store items of such little value.

I have too much stuff in the garage that we only use periodically (e.g. camping stuff, sports equipment, tools, etc.). Every time I think of getting a storage unit and think to myself I would come out ahead just buying it new and selling it when I am done with it then storing it in a locker. Oh well, for now I will deal with the clutter.

How else can we have the auction shows for the foreclosed on storage units?

“I’ve never understood why so many people spend so much money to store items of such little value.” Have you considered this: half of the people are less than average – aka: stupid.

Apple, it’s a psychological problem along a continuum — for some people, the “hoarders” it’s debilitating.

I think George Carlin had a great skit on this particular topic lol.

As an asset holder I’m glad we’re not going to experience the doom and gloom the bears have been waiting for. You’ll just have to accept that the world is thriving and enjoying life while you wait for doomsday with your gold, bullets, and canned food. Enjoy!

It’s different this time?

I learned long ago that, as a day trader or as a predictor of the timing of doom, I know less than nothing.

Yes, just like every time before 😕

Have you ever went without food,not pleasant .

So is there any rational reason for the Fed to pause next month?

There is a twin mandate to control inflation and maintain employment. The second part is under control, so there is no reason to abandon the first…

Inflation is steadily falling yet the economy is robust, so yes there is good reason to pause and let inflation fall while economy adjusts and avoids a recession. It won’t bring stocks or real estate down as anticipated by gears, but it great for the working class.

Firstly, stocks, real estate and other assets are a function of inflation. If houses cost 20x the average income, that’s inflation.

Secondly, even if you exclude assets, inflation is NOT “steadily falling.” Sure, some things are, but then prices skyrocket in other things. Have you been paying any attention at al?

“Inflation is steadily falling”

This statement is technically true but misleading: the rate of price INCREASES has come down a bit, but prices are still increasing.

Its like cruising down a highway and slowing down a little. You still haven’t stopped or gone backwards.

Calculus. 2nd derivative.

Kramartini asked: So is there any rational reason for the Fed to pause next month?

LOL. Yes. Continuing to raise rates will create more insolvent banks. But that might not stop them.

I don’t claim to know what the FED will do next month. But you can toss all that chatter about “mandates” into the trash. It is just word salad to justify their existence.

Nobody wants to work anymore

LOL

From the article above:

“People in their prime working age are now participating in the labor market, working or actively looking for work, at a rate not seen in 15 years.”

Sorry, my sarcasm font didnt load properly.

I sense a Yogi Berra joke in there somewhere. Nobody wants to work — everybody already has a job!

I had never looked at the prime age labor force participation rate, only the overall. Seeing this graph made me curious, and I looked at the prime age population graph. Its almost scary. the number of adults in the US aged 25-54 hasn’t moved meaningfully in almost 25 years. All of the boomers are now out of this cohort, and even with net in migration the US really isn’t growing this segment of the population

I find that interesting too!

It’s pretty much the same or worse for all other developed economies.

Two earner households mean fewer babies. High daycare costs mean fewer babies.

Everyone I know has 0 to 2 kids. Most of those kids are old enough to be in the labor force.

That’s why I read WolfStreet

I don’t know anyone who doesn’t have a job,but I worked 53 years is that enough ,labor

All the data that comes in just makes the complaining by the billionaire ZIRP/QE beneficiaries even more repulsive. Everything is flying high yet they’re squealing like stuck pigs.

They were conjuring up lies of a complete economic collapse to try to force the FED to stop doing even the bare minimum. These filthy, useless eaters need to have their fortunes seized. The future of the young is sitting in their bank accounts, but even that’s not enough for them.

The longer this “no landing” scenario continues on, the worse the outcome for the working class and the poor. Yellow Powell and Co. are financially incentivized to not do their jobs. They face no repercussions. Hell, Bernanke received an award for his assault on the working class. This is a terrible system. I do not believe it can be fixed.

If FED has been really serious, they would have raised rates by 50 bps at least and do QT more aggressively.

With a wet lettuce ditherer Powell it’s impossible even if rightly needed.

Beware a person too anxious to smooth everything.

Say what you will about Powell, he’s orders of magnitude better than Greenspan, Bernanke and Yellen. He cant lay all his cards on the table but he does a pretty job of communicating within the framework he has to abide by.

Greenspan used to mumble and talk in circles like Mayor Daley (both of them).

Yes, interest rate increase won’t matter as much as aggressive QT. Otherwise the stock market meme stock and bitcoin pumping will continue unabated, which is a moral hazard for society and very unproductive way of resource allocation that only benefits the 1% and doesn’t go into actual economy.

I think Powell got dealt a bad hand by current administration delaying his confirmation by six months and by too much fiscal spending. Plus the Fed staff models told him inflation was transitory.

He got a very late start and with the policy lag he might have been 2 years behind on slaying inflation. The pain is going to start kicking in as the world has too much debt to handle 5% increase in rates for very long. Every month is going to have new victims, til its just too many.

Everybody seems to think the Fed’s actions are too meager. I think we can probably agree that the Fed rationalized away the inflation numbers as “temporary” for too long. However, I think the Fed has very good reasons for taking it slow, measured and predictable in its efforts to stem inflation.

The Fed wants to gradually apply the brakes on the economy, not slam on them and have the entire banking and financial system thrust headlong through the windshield. It is incredibly easy to accidentally engineer a slowdown that is much deeper than was intended. They are just trying to slow this thing down without crashing it hard.

Interest rates are still well below the inflation rates if accurately reported. So business just raise their prices to cover their increased financing costs. This will keep on going on and on with no end in sight. Congress can’t even pass a budget and can’t cut spending in any meaningful way.

Not long ago, doctors, lawyers and engineers were respected professions.

Now, its bartenders, waiters and engineers as the disposable hired help.

Just wait for it, AI has white collar jobs firmly in it’s sights. 10 years from now you will be either a lawyer/doctor using AI or unemployed. Tyler Cowen (amoung many others) thinks AI is on the order of society disruption as fire, the printing press, or the wheel.

My daughter left her last career entirely because she saw the writing on the wall. That was 2016. She was tasked to oversee a project that, if one paid attention, was designed to put her entire department out of work.

observation-I have been saying to my wife for some time now that ‘thursday is the new friday around 10 am driving today on a traffic jammed 4 lane highway observed -the office building parking lots almost empty the restaurants and stores parking lots packed – perhaps employers simply need to hire more people due their workforce instead of working from home are in reality playing from home

“We pretend to work and they pretend to pay us.”

WFH. Lower carbon footprint and lower probability of your personal chalk line on the sidewalk in the big cities.

The difference between “high unemployment” such as 2016 to now is about 5%. These entire Federal Reserve discussions are basically involving a slight trend or noise.

Since it looks like we are in 1970s style “stagflation” and Since President Ford’s WIN (Whip Inflation Now) button didn’t work, the unemployment rate is going to have to hit the 10% of Volcker’s time. The psychology in those days, a very very mild version of Weimar Republic, was to buy whatever now, that ended when interest rates gave real returns above inflation; not this slow tortoise crawl toward so sub level of effectively that will fool the public.

Unfortunately, the seventies are well remembered by those who were teens “in the day.”

I was in my mid 20s, with our first baby.

It was an awful time. Both the inflation and the crash that followed. We were very lucky my husband kept his job.

I emigrated from the UK to New Zealand in the early 70s.

There was a nice +92 basis point move in 1 month treasury bills today.

1 month T-bills are getting whiplash.

Wells Fargo Bank cannot even hire tellers. I was in another branch today and there was one teller working the drive in and the inside stations at the same time. One teller told me that they can’t get help. The pay is peanuts, just above minimum that they have “Turn off the lights” on payday. They are pressured to sell products that no one wants to get commissions.

At another branch a homeless squatter occupied the whole sitting room near the inside entrance. They had 3 bank employees tied up trying to figure out how to get the person out of there.

And that’s why Wells Fargo has a net profit of of 25% in Q1.

They can get help, they just don’t want to pay for it.

No doubt they’d like some nice powerless immigrants stuck on closed work visas!

How stupid are they call cops it’s called trespassing

Seems to me 32 trillion dollars is still floating around like ferry dust?

$32T in ferry dust? How much is it per lb.? If so, how much would real fairy dust be? I mean, it is real, isn’t it?

My piano tuner just charged me $350 to tune and “clean” my grand piano. A couple of years ago his charge was $125. Outrageous. But there are so few of them around anymore. A dying trade. So he can charge whatever he wants now.

Get a nice yamaha digital grand piano. Sounds really good, never out of tune. Playing wont feel the same, but you have your choice of about 400 instruments so its pretty fun. And easy to move!

Yes, my spouse did that and never looked back. I am sure there are nice piano tuners out there, but they got harder to find.

So, now, easy to move; and no wreaking of tobacco, needs a bath tuner needs to be located and endured(with apologies to the minority of tuners who are otherwise). Always in tune. Plus the neatest part is the headphones! This means you do not need a ‘piano room’. Like buying several hundred sq ft of floor space. That was something we did not realize would happen.

Tony,

IIRC, that’s a Steinway, no?

Think of travel expense and travel time added to a professional service charge of, say, $150 an hour.

Also, if this person did a good job and put your piano in tip-top condition, and if you average the cost of the service rendered to your investment & piece of art & musical instrument by the years between tune-ups, it might not seem so bad to pay $350.

A week ago, the Minnesota Orchestra had Garrick Ohlsson working over a Steinway for Beethoven’s First Piano Concerto. It sounded pretty damn good!

Prairie Rider—

Correct, Steinway 7 ft grand. Yes, it’s worth the money. My point was regarding the mindset where he can justify almost tripling the rate for his services, and yet, people like me just smile and pay it.

(Once purchased, a quality piano is low-maintenance. It gives unlimited thousands of hours of pleasure, uses no electricity or resources, and can outlast a human. There are still working grand pianos out there from, say, 1896.)

If you have grand piano ,you can afford $350 to clean and tune it or just let it set and look pretty ,.

Tony,

You’re lucky your piano tuner came back.

Mine was named Mr. Opporknockity. And we all know he only tunes once. 🤪

Fed stopped raising rates in July 2006, and unemployment hits its lowest point almost a year later in May 2007 and the recession officially started in Jan 2008.

Other than credit delinquency, unemployment is probably the most lagging indicator, still early days.

I mean it is possible there was just so much money floating around and so much momentum in the economy that the rate hikes and reduction in money supply are just slowing things down from overheated to normal or to ‘still overheated but not as much’, but it is still too early to rule out the alternative scenario which is that we are just in the normal interval between rate hike cycle and recession.

Good point Some Guy

The leading indicator of a recession that works 100% of the time and often years in advance is the expansion itself. You know with 100% certainty that the expansion will be followed by a recession. That’s how it has always played out in human history, by definition. There is an expansion, and after the expansion there is a recession. Always. Now we’re in an expansion, and you know with 100% certainty that the expansion is predicting the arrival of a recession.

The ONLY thing we don’t know is when the recession will arrive. And that’s where unemployment comes in. It tends to nail the beginning of a recession, in part because that’s how the NBER has defined an official recession in the US for decades: a broad-based economic decline that includes a significant decline in the labor market. So you know that for the NBER to call out a recession, you need to have a significant decline in the labor market.

Wolf wrote: ”The ONLY thing we don’t know is when…”’

Unfortunately for folks who might be able and willing to buy ”on the way down, knowing you can hold through the bottom”,,,

there is at least one more little thing we don’t/can’t/wont know in advance:

HOW FAR DOWN???

Wolf read an article on internet about market cycles,that run in 18.6 year cycles with examples ,so 2007 +18.6 2025 also is e nd of business tax cuts expiring . This will get ugly

The cycle started in 2007, yes, but the price bottom was in 2012. So using an 18 year cycle, the bottom should be 2030.

US corporate credit downgrades are increasing, foreshadowing corporate insolvencies and rising unemployment. Unemployment is usually very low in the months preceding a recession.

1. In terms of corporates, credit downgrades are EXPECTED to increase in the future. They’re PREDICTING an increase in default rates in 2024. But none of that actually increased in a significant way.

2. Credit ratings don’t mean anything. SVB collapsed with an investment-grade credit rating.

https://wolfstreet.com/2023/03/11/svb-financial-had-investment-grade-credit-ratings-from-moodys-and-sp-up-to-collapse-then-ratings-got-slashed-in-one-fell-swoop-to-default/

3. CRE is a different ballgame. Retail CRE has been in meltdown mode since 2017 and got whackamolied during the pandemic. Lodging CRE has been hit hard during the pandemic and hasn’t recovered. Now we have office CRE and multifamily CRE getting in line that the trouble counter. These are structural issues that have nothing to do with a recession.

4. There is no financial stress in the markets (St. Louis Fed Financial Stress Index), and financial conditions are still loose and became looser over the past month (Chicago Fed National Financial Conditions Index); high-yield spreads are where they were a year ago; the BB yield is amazingly narrow. Leveraged loan issuance loosened up again, in another sign financial conditions are getting looser.

LOL, whackamolied is a keeper.

The tallest building in Minnesota, 1.4 million square feet of office & retail, and the first big skyscraper in Minneapolis, the IDS Center, is past due on its $154 million mortgage.

Accesso Partners is in negotiations with J P Morgan Chase & Co to negotiate a forbearance agreement. “Florida-based Accesso a decade ago paid $253.5 million to acquire the tower.”

“The overall office market is challenging now for property owners. Remote and hybrid work are pushing vacancy rates up (office space = 19.2% vacant & retail = 38.7% vacant in IDS).”

“It is very hard for offices to get refinanced now. Sometimes the loan just goes to purgatory,” said Manus Clancy, senior managing director with Trepp, a New York-based firm that tracks commercial real estate loan data.

I went to Minneapolis last year. The city has become a dump, and a lot of people now prefer to either work from home or work in the suburbs. I’m not surprised downtown office towers are struggling.

Prairie Rider,

Thanks. Yes, this is playing out everywhere. Landlords know that their towers are worth only a fraction of what they used to be, maybe only land value. And they don’t want to bear all the losses obviously, and so they’re going to shuffle a big portion of the losses to the lenders (such as CMBS holders here).

This mortgage that defaulted has been securitized, and CMBS holders are on the hook. JPM issued the original loan and then securitized it and shuffled it off the investors. The “special servicer” is the entity that collects a fee to represent the CMBS holders.

All major office defaults that I have looked at so far were on mortgages that banks securitized into CMBS and shuffled off to bondholders, and the bond holders are on the book (bond fund holders, et al), and not the banks.

From the yield inversion it seams a serious recession is imminent. Worse then 2008. Once it starts inflation and employment will plummet and the fed will pivot. A Crash landing is coming. You need to pick up speed, in order to crash land.

The expansion is a predictor of a recession. There is ALWAYS a recession after an expansion, by definition. We just don’t know when. You know when the sun rises, a recession is coming; you just don’t know when. You know when a hurricane makes landfall in the US, or when the yield curve inverts or whatever, that a recession is coming. You just don’t know when.

The yield curve has been inverted since July, as a result of the Fed pushing up the front end, and the banks buying long-term securities to push down the long end, and now some of those banks have collapsed for that very reason, LOL

But the labor market will tell you when.

There should be under normal economic policies a responsible recession once maybe twice a decade. Why do we keep analyzing this?

And life is the leading cause of death…

The labor market is saying there will be no recession. I see help wanted signs everywhere. The only unemployed people today around here are people who do not want to work for various reasons. Real Estate is booming back to pre-pandemic levels. Traffic jams are everywhere.

Went to local Home Depot people panhandling,while there’s a huge sign up that says we’re hiring. ,all though I feel sorry for them I only give to the women . While on vacation in Cabo San Lucas was told to only give money to grandmothers, because the parents take money and drink it up ,while grandma feeds the kids.

Until there are more people looking for work than there are jobs – labor will be in short supply. It’s just that simple.

Raising rates to force business to cut back on labor expense works just fine when labor is available. That isn’t the case this time.

I expect inflation to re accelerate once Congress agrees on a new debt deal.

Amazon seems deeply concerned about the tight labor market.

This evening I was told by my DSP that they need to reach an 80% or greater average where at every stop the van must be turned off. My DSP must achieve this by May 19th or they will be made an example of and my DSP and everyone that works there will there will be terminated.

My DSP also handed me a handout regarding delivery feedback.

The first week that you receive any negative feedback, you will receive a written warning.

The second consecutive week that receive any negative feedback, you will lose 1 day of work.

The 3rd consecutive week of receiving any negative feedback, you will lose 2 days of work.

After 4 consecutive weeks of receiving any negative feedback, you will be terminated.

It just keeps getting more and more bizarre at Amazon. The owner of my DSP took a second job as a cop? I am not making this stuff up.

Amazon is known for execution. They don’t play around. It’s always been that way.

The unemployment rate in Utah as reported by the Govt. is suppsidly around 2%?

Amazon’s goal is to have every driver, deliver to around 250 locations a day. So, 250 times a day anyone can provide whatever feedback they want and Amazon accepts their feedback.

Amazon does not operate in a bubble, if the unemployment numbers being reported by the Govt. are accurate, how is this possible? Business execution does not begin to explain what I am reporting.

Execution is turning into desperation as the free money environment that has allowed Amazon to thrive is drying up.

Amazon’s business delivery model has always relied on revenue growth, not profitability as its main driver.

Amazon executive are desperately trying to somehow revive revenue growth and they are willing to throw everyone and everything under the bus in the hope that Wall Street does not turn on them.

The retail sector has been decimated by Amazon and yet there is no real profit to show for their efforts. Delivering junk for free is a terrible business model and is the main reason most retail business never even considered the idea.

Once Amazon is finally forced to included all of actual costs involved in delivering junk for free, that exotic bar of soap that you could have purchased at Bed Bath and Beyond for $3.00 will now cost you $9.00.

My relative who works at Maher Terminals said container traffic from China is drying up. This is the stuff Amazon sells. I see change in the wind for Amazon if this trend continues.

Robert (QSLV)

BLS data is a draft, until the final revision. Reading the back of the book first will not give you the full story.

Anything about the economy — or maybe even mankind — is a draft. There is never a final version. You make do with what you’ve got. If you want a final version, go to the Bible.

Lol

LOL! Maybe the reports should first be labeled ‘draft’, as if they ‘realistically ‘ meant anything.

So let me be a little clearer: YOU are a draft, and every day that draft that is you changes, and you have to make do with all the changes your entire life. Your final version doesn’t exist. YOU change every day, and as YOU change, the economy changes in myriad little ways. People who seek a final version, like I said, need to go to the Bible.

Bible NOT a good example Wolf, as it has been ”revised” many times,,, almost always previously supporting the wishes of those who paid for it to be revised,,,

”The ONLY CONSTANT is Change” eh

OK, then, take it off the list too.

It’s not widely known that the University at Buffalo School of Management has since 2019 produced their monthly Job Quality Index (JQI). One chart uses 30 years of data to show a steady decline of job quality that bears on the interpretation of US private sector job market and wage reports.

Apparently, the wage reports trend upward due to the higher paying, higher quality jobs. But the employment counts are mostly weighted towards the lower paying, lower quality jobs — aka U.S. production and non-supervisory (P&NS).

This seems to jibe with Wolf’s phrasing that “people and businesses have gotten used to it” where the better salaries of quality jobs make it easier to shrug off the effects of inflation. Maybe the general wage inflation helps delude everyone to some extent.

I admit to being astonished that the rapid interest rate rises haven’t precipitated a recession, which I figured was sort of the point of the Fed’s recent behaviour — to disemploy a bunch of people in order to reduce demand.

Maybe I should take seriously Mosler’s assertion that the increase in interest payments represents a massive fiscal stimulus?

It’s not that astonishing when you consider that many businesses have committed credit facilities, many of which are fixed rate. Rate increases don’t affect them until it’s time to refinance their facilities, which, if you’re a zombie company, becomes impossible at these much higher rates. See Bed Bath and Beyond and Party City.

There is always a lag with these.

1) A Jeff Gundlach week. Since Apr 3 SPX is pumping muscles above May 17

2022 hi/lo, above May 12/17 Anti backbone. SPX might rise above Jan 24 2022 low and close > Oct 2020 close, for fun and entertainment.

2) The debt ceiling might rise again with an ultimatum : either cut gov spending and trillions of unfunded obligations, politicians promises, or no more money for u, to the gov.

3) The two sides will stiffen their positions. Since the gov can’t the two branches will separate from each other, blaming each other, until things resolve.

4) Meanwhile the Fed might raid in “other” people bank accounts, your money, without your knowledge and permission, to finance the gov. to save us from default.

How would your #4 play out? Just wondering…

Vacancy is the most dreaded word in real estate. Withdrawals is the

most dreaded word in the banking system.

CA had both. One third of SF commercial RE is vacant. Withdrawals

sent 3 CA banks to the recycle bin.

If politician cont to behave like children, not like adults ==> Prairie Rider and Tony might withdraw their money from their banks and put it elsewhere, perhaps inside their Steinway or speakers…

Speaking of withdrawals, Wells Fargo may not like me anymore after I took $30,000 out last week and left them with one month’s expenses in my checking account. I told them I needed one more month to clear out some electronic transfers after which I will be closing out my account for good. I also told them they can charge me their $25/month fee for not having enough funds to cover the minimum balance requirement. It’s worth $25/moth to get rid of them in an orderly fashion.

Wells Fargo, Citicorp, JPM without a doubt have become giant behemoths that are totally disconnect from the customer base. Customers are nothing by “numbers” in a computer database.

With money market funds and miriad other financial vessels paying 4.5%+, why would you ever keep more than expenses in a checking account?

At roughly $32 trillion of debt and growing excluding unfunded obligations the train crash that is inevitable is moving ever close. The realities of irresponsible fiat currency policies that attempt to mask corruption don’t have many more years to play out. The acceleration of what is BRICS is happening for a reason.

Perhaps the trillions that have been printed is enough to reach escape velocity so there will be no landing. Might crash into the moon though.

Fortune: In fact, according to an analysis conducted by John Burns Research and Consulting, institutional investors—those owning over 1,000 homes—bought 90% fewer homes in January and February than they did in the first two months of 2022.

Low interest rates, easy access to capital, soaring rents, and skyrocketing home values were just too good a deal for Wall Street types like Blackstone and iBuyer players like Opendoor Technologies to pass on. Of course, that’s all over now: Institutional homebuyers are pulling back—fast.

Look no further than Invitation Homes, the largest owner of U.S. single-family rental homes, which recently became a net seller. In the first quarter of 2023, Invitation Homes bought 194 homes while it sold off 297.

That’s a jarring shift. Just a year earlier, in the first quarter of 2022, Invitation Homes—which Blackstone helped to grow before divesting in 2019—bought 822 single-family homes and sold off only 147.

Interesting observations.

Lawrence K. Roos, past President, FRB-STL was cited, in the WSJ’s “Notable and Quotable” column, April 10, 1986, as follows: ”…I do not believe that the control of money growth ever became the primary priority of the Fed. (i.e., under Volcker). I think that there was always and still is a preoccupation with stabilization of interest rates.”

They’re changing the rules mid-game again, fighting against disinflation and deflation:

“As of May 8, homeowners who are straining to pay their Federal Housing Administration (FHA) mortgages have another lifeline: the 40-year mortgage modification. The FHA has instituted a new policy allowing financially strapped borrowers to have the term of their mortgage lengthened to 40 years, thereby reducing the monthly payments. The previous term limit for a loan modification was 30 years (360 months).”

We are in the most overheated economy in history and these filthy scum are already planning bailouts of the debt junkies. The scam is central bankers print massive amounts of money and hand it to the wealthy who in turn lend it out with fraudulent loans to saddle the working class and poor with debts they cannot repay, then use the US taxpayer to backstop these faulty loans so they don’t default and destroy the value of the loan collateral.

What this does is prop up artificial bubble prices to prevent the young from ever achieving home ownership, and guarantee that the rich scum continue to prosper via socialism at the expense of the US taxpayer and society as a whole. It’s time to burn it all down. It’s all corrupt and rigged.

Take a deep breath and calm down.

You’re reading this the wrong way. These are mortgages that are going into default because the borrower cannot make the payments.

They’re NOT new mortgages to purchase a home.

Mortgage modification is a classic method of trying to keep a mortgage out of foreclosure. Lenders want the payments, not the house. Mortgage extensions have been done a gazillion times for decades because lenders do NOT want to end up with the house. But if you have a 30-year limit on a 30-year mortgage, extending the term is kind of hard, unless you go over 30 years. That’s what this is about.

I understand that this is about existing mortgages. But there has always been a solution – FORECLOSURE. Or BANKRUPTCY. You yourself have stated this. Foreclosures are what are needed to help bring prices back down to sane levels. They reward and allow the financially prudent to buy a house and punish the people who were reckless, as it should be.

Paying off a 30 year mortgage is not a pleasant thing, even more so is paying off a 40 year mortgage. This makes the borrower a willing slave for most of his conscious life. I’m sure very few people will pay off a 40 year mortgage for a number of reasons. This is not salvation, but enslavement. One does not know what will happen to him tomorrow, much less in the next 40 years.

As it was said, lenders and banks wants payments, not houses. And for sure not a lot of houses that have to be sold, depreciating the collateral of the other mortgages they get payments for.

Landlord and rental is a different business that lenders do not want to be in.

Why don’t we go with 100 year mortgages like Argentina did? We are copying everything they’ve done. Why not copy this???

Per $100,000 in loan amount at a 6.5% interest rate, the payment drops from 632/month to 585/month. Average loan amount approximately $350,000. Another $165/month to the monthly budget isn’t going to save anyone’s home from foreclosure. Don’t worry DC, you’ll still get your bankruptcy. It’ll just take a little longer.

A minor point from out here in the weeds. I realize “change” is the lighting rod for data that is presented by Gov’t and others. But, in my opinion, I don’t think “change from xxxx ago” should be stated on its own. Rather it should be used as a convenience foot note to the actual presentation of the compared data.

An example might be “Change from last month” when last month’s data had been massively revised up,… or down. Without the data, plus the amount of restatement, the change can be most misleading both positive and negative.

Actual data also provides some perspective on the change. Say something changes by 5 data points. 25 widgets to 30 widgets is a 5 point upward change or 20%. (OMG the sky is falling or, happy days are here again). But a 5 point change from 250 to 255 is only a 2% change. (Meh..)

Just sayin’…

Here is what you asked for. Happy?

Try to find the revisions in this chart. This is the total number of employees, 156 million. The revisions are such a small number compared to the 156 million that they cannot be seen here.

You cannot see anything on this chart in terms of April compared to prior periods, except that employment keeps growing by an undefined amount. Which is why I’m not posting it anymore. Waste of time.

What happened to rovotics and automation. People were supposed to be losing jobs. Here’s one nobody is watching: US Productivity is at -2.70%, compared to 1.60% last quarter and -6.00% last year. This is lower than the long term average of 2.15%: Seems maybe business is not investing in tech?

Productivity is probably dropping because more workers are demanding a better work / life balance.

I have customer and was trying to get a PO processed for some work. The manager, she was out on maternity leave for 4 months and the managers director who could also sign was also out for 3 months on his paternity leave.

So this company had to delay the project for 3 months. Several of the managers reports did not have much to do for 3 months. So basically you ended up with 6 people not doing very much work for 25% of the year.

When my children were born, I took a vacation day on the day of the birth and went back to work. Even if I wanted to take more days off, I only was allowed 2 weeks or 10 days of vacation per year. Now the company I work for gives new college hires 20 days of PTO. It took me 10 years to get to 20 days of PTO. Now they get 20 days and possibly 3 months of PTO. An employee could potentially miss 30% of the work year.

I am not saying this is right or wrong but productivity has to be dropping. Maybe in the future AI bots can do people jobs when they are on PTO.

1) Those who own more than 1,000 rental units during the zero rates

era will pay 6%/9% in the next commercial loans rollover.

2) The expanding rental units might join other commercial RE and become toxic in the next recession.

3) Low unemployment rate don’t protect from recessions. Its a mirage.

4) Are banks assets toxic. Your cash in the bank is a promise to pay u back, an IOU. The Fed IOU your banks cash, your money in the Fed.

5) In Jan 2008 Fed Assets were 900B before rising to 8T.

6) Cash in the banks was a flatbed of about 300B oin real dollars bills, but

since Oct 2008 banks IOU rose to 4.1T in Dec 2021, before tumbling 1T to 3T. After the Fed hikes to 5% its up to 3.3T.

7) Cash assets of commercial banks in the Fed was zero before before

Oct 2008. In 2008 the banks didn’t want to lend to each other. They deposit their money in the Fed. The Fed liked it so much they asked for more. Our gov fell in love with their new power. US gov financed RE, health care… other bs. The Bank’s cash assets in the Fed, your money in the Fed, plunged 1T from 4.1T in Sept 2022 to 3T, but after Fed hikes to attract money it’s up to 3.3T.

8) All commercial banks asset are down 1T from 18.1T in Apr last year to

17.1T. Something is wrong.

Currently, I’m betting long term yields go down because of the economy going down (GDP qtr4 2.6% to qtr1 1.1%). Made some decent money in EDV over the last 3 weeks. Just buying EDV when 30 year yield goes high and selling when it goes low. But this is a current point in time decision. I have no idea how long this will last. A lot of cross currents involved.

1. The Fed’s inflation fighting vs system’s belief in pivot

2. Long term perspective on long term rates

Look at a chart of the 30 year yield going back to the 40s. We see the

yield’s inexorable rise into the early 80s. And the inexorable fall since

then. For me the early 80s was the beginning of the Boomers as an

investment class. Prior to that was a G.I. generation investment class.

Seems like the GI gen needed to be induced to buy bonds. But the

Boomers were all too willing to buy bonds. Which way will the

Millennial generation flip? They are a Hero generation like the GI so

maybe they have to be induced to buy bonds in which case yields go

up. And if they are like the Boomers yields will go down. And by my

calculations the Millennial generation investment class is scheduled to

arrive in the early 2020s.

Oh! But wait! Is it time to be very afraid?

generation flip.

Banks…….How big of a problem ?

Charles Schwab is rumored to be in trouble, yes Schwab is not only a brokerage, but also does banking for its customers.

The landing will come, will not be soft.

A few Too “Big to Fail” banks/brokerages will be saved, others not so lucky.

When ?

Soon ? Next year ? Five years ?

Thought it would have happened already, thus I do NOT know.

Thankfully. Wolf and those who post, help me make better decisions.

In preparation for landing, be certain your seat back is straight up and your seat belt is fastened. Please secure your investment items, stow risks.

Wolf, why have there been so many down revisions of new jobs recently? (Including Feb and March.) Do you think April will ultimately be revised down, too?

There have been HUGE gigantic UP Revisions, including in January.

The revisions are included in this chart of total employment. You can see a few of the up-revisions because they were so big. The down revisions difficult to see because they’re smaller, and they didn’t change the trend, and over-all growth has been rock solid, despite revisions: