Just a slower-growth muddle-through economy that adjusts to higher rates and sticky inflation.

By Wolf Richter for WOLF STREET.

It makes sense to see a recession later this year. The Fed has hiked interest rates with the top of its policy rates now at 5.0%. Businesses and consumers haven’t had to deal with these kinds of short-term interest rates in 15 years. Three banks have blown up because long-term rates have risen sharply, and they got caught not preparing for it, and depositors then pulled the rug out from under them. Economists are widely predicting a recession later this year. Even the Federal Reserve’s staff projections, prepared for the March meeting and mentioned in the minutes, included the possibility of “a mild recession starting later this year.”

So the recession scenario later this year is getting baked in. Wall Street’s megaphones, assorted hedge fund gurus, and the occasional bond kings are all on board: We’re going to get a recession, and the Fed is going to be forced to cut rates this year to deal with it.

Rate cuts is what all these people want, because they hope that it would put an end to this horrible misery where the money isn’t free, and they’re counting on it and they’re betting on it.

But before the cuts, there will be one more hike, they figure. The likelihood of a 25-basis point rate hike on May 3 has risen to 87% today, according to the Investing.com Fed Rate Hike Monitor, which is based on CME Fed Fund futures. So that is now kind of a done deal, as far as markets are concerned.

If the Fed hikes its policy rates by 25 basis points, to a range of 5.0% to 5.25%., markets then expect rate cuts by year end.

The likelihood of one or more rate cuts by December is 87%, according to the Rate Hike Monitor. Specifically:

- One cut: 30%;

- Two cuts: 35%;

- Three cuts: 18%;

- Four cuts: 4%.

Some things in the economy have started to wobble. Three mid-sized banks collapsed in March – two crypto-eager banks, Silvergate Bank and Signature Bank; and the startup-centered bank, Silicon Valley Bank. They all were concentrated on a peculiar bunch of depositors with lots of uninsured deposits: crypto companies and massively funded startup companies. Then there was some contagion, and other banks got hit by runs and were teetering for a few days.

But the Fed’s liquidity programs largely ended the deposit flight, banks have been paying back those loans, and now all eyes are back on bank earnings – and so far for Q1, bank earnings have been pretty good.

Earnings at the largest banks benefited from the spread between what they’re paying on deposits and what they’re charging on their loans, and revenues at the four mega-banks all jumped. They all increased their loan loss provisions, but the banks generated so much in profits that it barely made a dent. JPMorgan’s CEO Jamie Dimon is still seeing “the storm clouds” on the horizon that he saw a year ago, but they’re still on the horizon. He said that the US would eventually have a recession, and everyone can agree with that because eventually, there’s always a recession.

But what if there’s no recession this year?

Consumers slowed their spending late last year. But this year, they got used to all the stuff going on around them, and they picked up their spending.

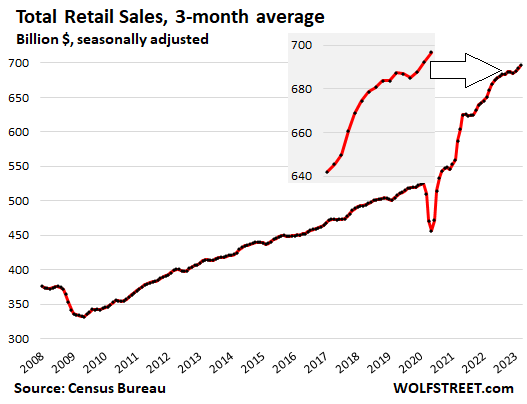

We saw that in retail sales for the first three months: Q1 was up by 1.7% from Q4 and by 5.4% from the same period a year ago, despite plunging prices of gasoline and dropping prices of many goods that retailers sell:

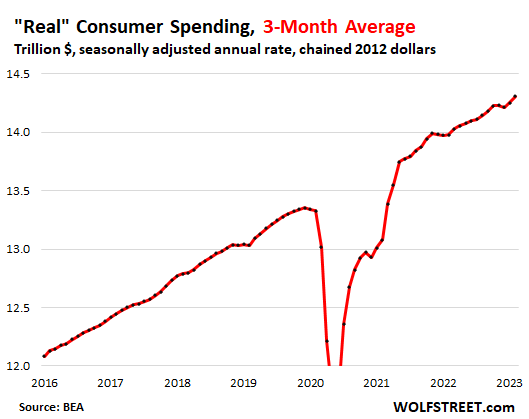

And we saw it in overall consumer spending, which includes services, and all of it adjusted for inflation, through February. The three-month moving average of “real” consumer spending, adjusted for inflation, was up 2.4% year-over-year. Better than just muddling through, but a notch below the 2.9% “real” consumer spending growth on average in 2015 through 2019, when interest rates were a lot lower. You can see the slowdown late last year and the pickup this year:

St. Louis Federal Reserve President James Bullard told Reuters in an interview that “Wall Street is very engaged in the idea there’s going to be a recession in six months or something, but that isn’t really the way you would read an expansion like this.”

They may see rate cuts in the near future, part of a recession-breeds-accommodation view of the world, he told Reuters, but “the labor market just seems very, very strong. And the conventional wisdom is that if you have a strong labor market that feeds into strong consumption … and that’s a big chunk of the economy.”

“It doesn’t seem like the moment to be predicting that you have a recession in the second half of 2023,” he said. These recession forecasts “are coming from models that put too much weight on the idea that interest rates went up quickly,” he said.

And “what about the pandemic money still to be spent off, both at the state and local level and at the individual household level?”

The trillions of dollars that the government handed out directly to consumers, businesses, and state and local governments are still sloshing through the system. States like California are racking up big deficits on an accounting basis, but they’re still sitting on piles of cash from the pandemic, and they are spending it.

Consumers are awash in cash. You can see that in the deposits at banks which hit $18 trillion by the end of 2021 and have now dipped to $17.4 trillion, which is still huge. You can see it in the different measures of money market funds that have all shot up. Consumers have also parked a lot of cash in Treasury bills. Many of these instruments are paying from 4% to 5% in interest.

That’s a lot of additional cash-flow that consumers are now getting. On, say, $10 trillion of all these instruments combined, an average 3.5% interest rate would generate $350 billion a year in cash flow that consumers didn’t get 15 months ago during the near-0% era, and that they now get to spend. And many, especially retirees, are spending every dime of that cash flow.

I’ve been saying for a while that this is a weird economy. It has refused to go into a recession despite the higher rates, and despite some wobbles in some areas. Instead, it’s adjusting to the 5% rates and to higher inflation. Everyone is getting used to it.

“Inflation is coming down, but not as fast as Wall Street expects,” Bullard said. To get a handle on inflation, Bullard feels that the Fed should hike further after the May meeting to push its policy rate into the mid-5% range.

“You want to be responsive to incoming data through the summer into the fall,” he said. “You wouldn’t want to be caught giving forward guidance that said we’re definitely not doing anything and then have inflation coming in too hot or too sticky.”

Once interest rates are considered “sufficiently restrictive” to slow inflation, Bullard felt “the bias would be higher for longer” to make sure inflation is fully under control.

And so the economy muddles through with muted growth, relatively high inflation, and 5%-plus short-term interest rates, and it’s adjusting to it, and consumers and businesses are getting used to it, and they’re sustaining this inflation by getting used to it, and so there’s no recession that would cause the Fed to loosen monetary policies, and after 14 years of free money, we’d be in a new era where money isn’t free anymore, and that would be a bummer for Wall Street.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

An alternative way for the Fed is to let the inflation rise, do no more QT or QE, and let the system finds its new equilibrium. In this scheme, the 50T borrowed by the US Govt by end of 2024 will not be a big number, the stock market does not drop, and everything works out in a few years. Comments?

Change the word ” works ” to blows. out in a few years.

Lol wallstreet was so happy to see bank runs that stock markets jumped 10% in the process. What’s bad for economy is now good for markets! This is because wallstreet expects that What’s bad for economy will cause fed to Pivot and give free money to wallstreet’s casino.

I say that wallstreet needs to be taught a lesson by 99% who are impacted by real economy. It’s simple: Move your money to 3 month TBills to earn 5% through treasurydirect.gov and dump all your stocks for 1 year.

AGREE… SO much!!!

Thank you for expressing clearly what I have been only thinking for many many moons…

Stocks initially sold off hard (S&P 500 to 3800s) during the bank panic. What caused the current rally was the Federal Reserve Put.

By invoking a “systemic risk exception” (where there was no systemic risk) and bailing out the wealthy & politically-connected clients of the failed banks, Wall Street received confirmation the Federal Reserve Put was still in play.

To Wall Street, it’s irrelevant that shareholders weren’t bailed out. In 2008, AIG’s shareholders took a 99% loss – it’s AIG’s clients/counterparties (Goldman et al) that were made whole. SVB was not a mom & pop bank. Too Big to Fail is still in play and that’s all Wall St needed to know.

I’m for it. Wallstreet can pound sand.

That certainly is an “alternative way” for the Fed, in the same sense in which ramping up the drinking is an “alternative way” to deal with the problem of alcoholism.

2 years back Pakistan was running inflation rate of 10% as its central bank boasted of very tight interest rate of 7%.

Now Pakistan’s central bank runs a very “tight” monetary rate of 21%, but the official inflation has jumped to 35%.

Worse is that Pakistanis are standing in miles long queues at food district centre’s for 10Kg bag of floor that often results in death from stampede triggered by desperation.

So I asked “J Pow” about this and here is how it went.

Leo – Can this high inflation happen in America in 2 years?

J Pow – Our monetary conditions are very “tight” and we plan to tighten them further. But between you and me, they are designed to keep real rates negative, just like what pakistan central bank did, so that inflation can keep going higher as we print more money. So don’t expect different results.

Leo: But US has so much farm land. We can never be short on food.

J Pow: Pakistan also has so much fertile farm land, still they are now hungry. Never doubt the capability of central bankers like me to EFF things up!

Leo: But US is a nuclear power.

J Pow: So is Pakistan, even as it goes bankrupt.

Leo: But US is a capitalist country where free markets encourage productivity.

J Pow: Pakistan is also a capitalist country. Central banks distorted free markets in Pakistan hurting productivity just like here. See our trade deficits are already like Pakistan.

Leo: But we have so many rich billionaires that can open businesses to prevent poverty.

J Pow: There is no shortage of rich Elites in Pakistan. Even today they import many luxury cars, when thier central bank is out of dollars. The rich will be made richer at expense of 99%.

Leo: US is a constitutional democracy that should result in good governments.

J Pow: LOL, did you miss how we now arrest former leaders. That sh!t was literally learned from Pakistan.

Leo: I don’t want Americans to die in stampede in food queues.

J Pow: Leo, you are so misinformed. Americans will not die in stampede. We have too many guns. People will just shoot each other to shorten queue!

I love it, so great and the fact you hit it on the head. The rich find ways to F the rest of us.

Guido’s idea:

*If you just stay drunk, no hangover!*

Very American.

Same as, “Just keep borrowing until you die and you never have to pay!”

Disagree. The fed balance sheet over 8 trillion is monstrous and outrageous. It is a symbol of wanton money printing, destructive inequality and what has gone wrong with our society. Of course Wall Street loves it. It is for the justice of humanity that they have to keep doing QT and keep shredding the balance sheet.

If the Fed has the resolve to keep rates above inflation long enough, history says inflation should continue down even with a stronger than usual labor market, right? I feel like in the same way that inflation expectations can fuel inflation, recession expectations can fuel deflation. Maybe a sluggish economy for years could be that soft landing unicorn? Would that be preferable to a (shorter) recession that we bounce back from quicker and stronger?

New Wallstreet Mantra: Bad earnings increase the probability of a recession and hence Fed will Pivot soon. So markets must rally on bad earnings!

There’s little evidence that consumers are changing their behavior. Wall Street & financial media started crying about a recession in late 2021, when the Federal Reserve first began signaling a pivot to tighter policy. 1.5 years later, the recession has not happened. The broken clock has been wrong too many times for the fearmongering to have any impact.

Personal savings rates (FRED: PSAVERT) are near an all-time low. This is not how consumers typically behave when there’s an impending recession. Instead, they sharply increase their savings.

Or maybe the belief is if there’s a recession, Congress will hand out free helicopter money again, so there’s no need to save.

Savings are for losers ,last fifteen years . I’m one of them

Pity the ethnically diverse, US multi billionaires that invested their money in China primarily, so their CCP co-owned, quasi-slave employing subsidiary or their family trust owned company sells the CCP companies’ products at inflated prices to their US company (so the US company pays little or no US taxes). Now, the CCP is refusing to let them take their money out.

The CCP’s Chinese government-as-a-criminal-gang may not have enough US dollars given its enormous needs and ginormous liabilities!! LOL No way their fake GDP and other misrepresentations will dig them out of their hole. That CCP government’s oncoming economic collapse may, very possibility trigger a major, world-wide recession

Curve will eventually re-vert, sooner than later, and ish hits the fan.

“do no more QT or QE”

That’s what they are doing already. Asset holdings are rolling off naturally, not being sold

QT = shrinking assets. No sale required. Roll-off due to maturing securities is QT just fine.

Great analysis, thanks. I’m not sure that the regular people will feel the weight of a recession as much as the wealthy will. Which of course the conundrum.

The regular people have been in a recession for at least several decades.

IMO, it is the result of the gov’s misguided policies as prescribed by Princeton and Harvard and their kin. Which reminds me to recommend an old album

The James Gang Rides Again

Even the data support the obvious conclusion that, rather than being a cost push inflation, a philosophy that was sold on the basis of the union COLA clauses, which as it turns out, was never the cause. How could it be when the adjustment metric was at best political.

not the inflation that we have now which is almost exactly the inflation we had in the 70’s’

What I meant to say was that the COLA clauses only were activated by the measurement of inflation. They were no more a cause than Wednesday of next week.

Every business person awakes with the intention to increase profit by squeezing the louts for a nickle and eventually realize the golden solution, increasing the price of their moribund products.

Eventually, the sales from that strategy decline, in a manner that convinces the monopolist of the wisdom of Macroeconomics 101, the structure of markets and the likely outcome.

“Comments?”

Dumb. Very dumb.

Yes, there will likely be civil unrest and war(s), judging by history.

If we need an axample of how “unrest’ is done, just look at the persevereance of the French.

You would never know it is going on if you only watched the MSM.

“Unrest” is fairly routine in France. It’s part of how their politics and democracy work. “Descendre dans la rue” (hard to translate, meaning going down from our apartments into the street to gang up and cause trouble) is the expression they use, as a threat of sorts. If you, M. Président de la République, don’t do this, we’re going to descendre dans la rue! They do this to win or protect political concessions, government handouts, subsidies, etc.

I lived in Paris for a while over two decades ago. Even then, periodically, this kind of stuff was how their democracy was done. You learn to navigate around it. You kind of get used to it. There’s always something.

Déscendre dans la rue = Take to the Streets!

Very French and usually effective. Not working so well this time, but it has in the past.

France has far fewer natural disasters than America so overall we are far less disturbed in our lives than, say, a NYC resident in the winter or a Texas resident during hurricane season. Or anyone living in Tornado Alley.

So basically adding a zero to all bank notes but we don’t use words like “stealing”?

No one of any significance would be harmed by this.

Let them eat cake!!!

1) The 14 amendment : debt incurred to suppress resurrection will be

paid. In the next 2Y US gov debt might rise to $35T.

2) The gov will do what it takes not to avoid default, pay SS, defense, pump the regional banks and reparation…

3) Recession : forget about it.

4) A poison pill for future republican administration, if it ever come.

I guess the no landing or soft landing scenario is looking more and more like the new reality..

Guess time to throw in my towel and hoping the housing market will correct anytime to “normal” level in SoCal..perhaps this is the new normal and perhaps this time is different…disappointing to say the least..

Wait a minute… this article is talking about spending (such as consumer spending), inflation, and higher interest rates. It’s not about housing. Housing won’t fare well with higher interest rates. But house prices are not part of how we measure GDP. House prices can decline in a growing economy just fine. Higher mortgage rates will do it. And higher mortgage rates are a function of higher inflation, which is a function of many things, including a reasonably strong economy.

I know I know Wolf, just doing my old man rant :) and since housing is my #1 focus that’s why I threw it in my earlier comment. The whole notion of consumers getting used to higher prices, I think there’s some of that going on with the housing market, at least on the surface it looks that way in SoCal for now…

Trust me, I know you’re right and I am on that same camp, it’s the patience part I need work on…

I’ve felt very strongly.about this for at least the last 6 months.

The Fed has made.a.serious mistake doing 1/4 point increases, not wanting to piss off Wall St. and crash the market to reality. Sorry S&P at 3640 isnt reality.

Doing the 1/4 point rate hikes allowed the markets to absorb the ‘shock and awe’ and here we stand wondering why it’s so resilient.

The Fed should’ve been doing at least, and should be doing in May, a 1/2 rate hike.

There IS a point where the Fed hits a ceiling in hikes, due to debt payments, we all know that,

What happens when the Fed hits the ceiling and cant raise further, say 5 1/2 or 6% Not a chance in hell the Fed can raise higher.

PS, I dont forsee a housing crash either. Prices soften from absurdity, YES, but not crash. I hear this year after, year, after year, heres the reality

There’s a housing shortage,

Covid created demand, WFH

Higher rates = No sellers

Builders have been managing their supply very tight, maximizing profits

The only blimp I see on the radar that could possibly stir this sh1t stew up enough to cause ripples is the CRE market.

We’re starting to see defaults, there’s $1.25 TRILLION needing to refinance in the next couple years, and they’re running a 18% vacancy rate in many markets.

Could that eggon the coveted ‘recession’ once and for all?

Nothing else is working…..

Radar is not needed to see a blimp. Hopefully it is not the Hindenburg.

If the things you say are true then why has the CS index had such a steep decline in so many markets?

Jim,

When 10% of housing is vacant 2nd, 3rd, 4th or 5th homes…

Tiny homes are illegal (zoning and have to build on wheelbase).

Maybe there are other problems?

If they started zoning and building 3 BR 900 sqft houses it would help a lot (like in the 1950’s)

Also, unemployment will spur people to sell their *extra* houses. The so called “AirBnBust” could help as well.

Wolf

New construction spending is not part of the GDP calculation? If I recall correctly, only pre-existing homes are not.

Read again what I said:

“But house prices are not part of how we measure GDP.”

There is nothing about construction spending in my entire comment. Nor about home sales. But “house PRICES.”

Even if there is a recession, it will hardly be deep and long-lasting. This would cause, if at all, a WEAK rate cut. We are no longer talking about zero interest rates here, and we are not talking about QE at all. However, if the recession is deep and pervasive, then we may already see low interest rates. I guess that’s what Wall Street is expecting and hoping for.

But with 5% inflation, rents will be going up 5%, and housing supplies still low and building is not going to match demand. So with those factors how can housing prices drop?

I’m eyeball deep in student loans with more piling on (a healthcare degree, not a degree in Fine Arts or Philosophy major. But big ups to NYS for practically holding a gun to nurses’ heads to take out another $20k+ in loans for a BSN lest be unemployable. I hate this state so much) and I’m sitting back waiting for the distraction circus to end in Washington and student loan payments to kick back in.

Thanks to inflation, the loan payments are still gonna sting me and I have a solid grasp on my budget, can’t imagine rents and house prices continuing to stay sky high when us educated but broke lot have to toss an extra $500+ at our loans again.

Or I’m just looking for a silver lining that isn’t there and that’s fine too. Its all going to hell in a hand basket anyway.

Wolf,

re “this article is talking about spending (such as consumer spending), inflation, and higher interest rates. It’s not about housing. ”

I think prolonged ‘stagflation’ the conclusion that your article is supporting b/c high interest rates will kill growth in housing transactions, which consumer spending on is a huge pillar of GDP growth, and likewise will kill new auto sales which consumer spending is also a huge pillar of GDP growth (jobs & supply chains), and high interest rates combined with lower consumer demand/sentiment (and the anti-wealth effect of a flat/down stock market) will kill new inventories building by companies, with is a huge part of GDP. So, companies (like I’m doing) will make up for lower volumes with higher prices and cutting quality, and people having the Fed stimulus $ will continue to pay it.

All that will also constrain new credit formation, even if banks are not afraid of a financial system event.

Those are all the pillars of GDP growth pushed downward by high interest rates; hence, prolonged ‘stagflation’ the conclusion, not recession, right?

Don’t give up Phoenix. The housing market will correct. It will just take some time. Be patient.

Be patient. It will take a while for more debt to roll over and bankruptcies to begin in earnest. On existing debt, real interest rates aren’t even positive yet. People hoping for a pivot will just have to keep waiting, the fireworks haven’t even begun.

When there are fewer short squuezes left to be had by the updated algorithms with there new AI enhancements, the market will fall more easily.

Until all the shorts and longs have given up, there “seen” stops will be captured and squeezed, causing the market to zig zag all over the place in the direction that causes the most pain.

Eighty percent of the market is traded by programmed machines.

I came here to mirror this sentiment. I’ve about given up on the American dream. I wonder if we’re alone? What’s the point if we can’t own homes. No home, no retirement.

“The American Dream? You need to be asleep to believe it.” George Carlin

Haha, now that is funny!

Gotta wait for all the desperate dans who blink first to finish taking their respective plunges…once you’ve run low on greater fools, then you’ll see some cooling off.

Millions of boomers will expire. Meanwhile they will be selling housing to downsize and pay for life. I would ask how old you are. I didn’t start buying a townhouse until I was 37. It took that long to pay off student loans and save up the down payment.

What are student loans,hahaha

We were 24 when we bought our first house. Married 7 months. It was a crapshack, but it was our crapshack. No granite. No hardwood floors. No dishwasher. No central A/C. One bathroom. One car garage. Lunch-bucket neighborhood. Had a patio door that opened to dirt. Nicotine so thick on the windows that we needed a razor blade to wash them the very first time. Had to prime the walls with shellac based primer to get rid of the stench. Used appliances – $50 refrigerator that took a day to clean.

You’d be hard pressed to find someone who would be willing to undertake such a project in today’s market, especially in the condition that we bought it.

But home ownership was the most important thing to us… and we sacrificed the fancy cars, trendy clothes, and Club Med vacations that our friends enjoyed. They thought we were stupid for buying a house that young (or getting married at that age).

Wife unit also had student loans when we got married. Somehow we muddled through.

When I was 24, my rent on a dark basement studio apartment was $1300/month while I worked two jobs and still had to take out student loans for college which was a ‘cheap’ $200-300/credit (paying over $500/credit now 17 years later).

You’d be hard pressed to find a Boomer who wouldn’t still call me lazy for not working ten jobs and buying a house for the price of a pair of flip flops and a strawberry like they did in ’76.

100% agree. I have a great job. Make good enough money. Doesn’t seem to matter. And no, I’m not going to go ghetto or live own some loser utopia where you walk, bike or whatever with your neighbors that all sing together on their way to work at the WeWork Office. Just wanted a normalish home in a decent neighborhood where you don’t get accidentally shot opening the wrong mailbox or driving up the wrong freaking driveway.

Nah. I got three boys 12 and under. Think I would tell them military service for this country where a freaking house is out of reach? (BTW, our military is great.). Oh but we’ll send money to another country for their war, make sure a dude can dress like a chick, make banks for billionaires whole… but for the me’s out there- you get zip. Nada. Not even a level playing field.

Sorry for the Depth Charge level rant (as he is the master) but I have learned a lot from this site and from all the comments. Sadly, the thing I have learned the most is that for the average dude that saved up some (no, not millions) has no debt whatsoever, can hold his own in frugality with anyone here… your out.

Done. Thanks for showing up.

Buy some land and build a house.

Thumbs up 👍👍for that rant, mate!

I live in Phoenix and can completely agree with EVERYTHING you just said. I grew up in the ghetto and no way am I paying 400k for a whole in the wall house surrounded by drug addicts (ex addict myself) and wanna be gangsters who will shoot you if you look in their general direction.

I’ve come a long way in life from who I once was and now have a decent job that would be considered good pay 3 years ago but because of this printing mania from the gov ment it’s reduced my spending power to minimum wage levels 3 years ago.

I continue to follow and read Wolfs articles looking for a glimmer of hope and reading all your guys comments to hopefully one day be able to buy a home for my wife and kids that I won’t have to spend more then half my check on each month.

The way this country is ran and the wicked, greedy, selfish, power hungry, etc, etc, etc individuals who live off the backs of us hard working peons and living off the backs of my kids and grand kids future need to be brought out back and shown some love (wink wink).

Maybe one day I will be blessed by God to obtain that home for my family, but until then I’ll continue to read Wolfs articles, learn and grow in knowledge of the financial things going on around me and occasionally get that laugh I need from all you comics in the comment section lol.

There’s my little rant. Thanks again guys. Until next time, God Speed.

Considering the lag effects of tightening and the fact that many 100% accurate recession indicators are sending warnings,. I wouldn’t bet my livelihood on the no recession chant. Things turn quickly as the rate hikes take effect.

Ya, our heloc just went to 8.25. thankfully the balance is zero.

Exactly. It is lack of patience.

We are headed for recession. Fed will cut rates.

Truth,

I didn’t go to med school.

I’m not a doctor.

I have no patience!

Soon retirees will outnumber workers. Retirees have gotten wealthy the past year all thanks to higher interest rates. Such was not the case in the 1970’s and early 1980’s where retirees were only a small percentage unlike today. This is the case for no recession as retirees are spending a lot more money due to the wealth effect from higher interest rates.

Just leave that hell hole already Phoenix. I recently did, and it was an excellent move. In a much less crowded and much less expensive southwestern state, my new job pays about what I made in CA. The difference is that I can now raise a kid and keep the wife perfectly comfortable on one income as a homeowner in a nice part of town with much better schools than my son would have gone to in SoCal.

I happily high-tailed it out of that literal garbage fire of a state and readily contributed to this undead economy with a big smile on my face. My landlord gladly jacked the rent to $3k/mo for whatever sad sucker replaced us as tenants. I dumped money on uhaul, airfare, a home purchase, new furniture and lots of other stuff. My wife and I were right in line with Wolf’s graphs, and I couldn’t be happier with our decision.

Face it… We’re in an economy akin to a supercharged version of the 70’s. We’ll be in an inflationary malaise that is nominally good but horribly anemic and damaging for the middle class in real terms for a while (I mean actual real terms, not tarted-up government numbers). And don’t expect to ever see pre-pandemic house prices again. The pimply-faced teenagers at Del Taco are making $15/hr+ in SoCal these days… The value of the dollar has made a major shift and it will keep shifting until all those new trillions are fully digested by the economy. And when the economy eventually gets sick and pukes from its over-eating (which could still be years away), we’ll print some more!

I feel your angst while waiting for the “crashes” we all hope will come. The time to throw in the towel is understood. generally, too mean that all hope, the only thing that most of us ever had, is gone.

I don’t believe that. Like all of us, sometimes the situation seems bleak than suddenly, if we haven’t lavished in our own misery to the extent that we are unable to respond to an opportunity. Even then. One window is always open.

The economy is a giant SuperTanker loaded with cash and spending power.

I think Wolf’s “what if?” question may produce a surprising answer.

We remain in a negative real interest rate world.

B

LOL, Wall st corps and banks looking for a recession soon to end this 5% misery. No one is qualified or knows how to make a profit in this high-percentage environment. Stock buy-back is not on the table so what to do?

Go small business, people are ready for quality goods and services.

It’s really pathetic. How many of these companies have been around longer than 15 years and suddenly can’t live without free money. I mean, I get it. Free money is a hell of a drug for the bottomless pit of greed that is corporate America. Guess it’s time to get back to earning a profit by providing valuable goods and services instead of VC or Government Welfare

I can’t believe how anchored in unreality this economy became. That is, until I look at how long and largely the free money regime was done. And now the unreality seems hard to shake for so many. I can’t believe the pivoting implied in prices.

I agree with some of the sentiments you expressed but not the philosophy that somehow found a way yo blame the homeless for the American dysfunction. Let me suggest an alternative proposition. It is welfare for the wealthy that far exceeds the helping hand expenditures that we extend to our most defenseless citizens.

If we don’t get a 5% per year recession for the next twenty years, we might as well just QE ’til we drop. Mother Nature says so. Of course, I understand that doesn’t compute for most people and is wildly off topic, but big picture and all that.

Yatzzee! Not off topic, its a bullseye!!!

Now that we established we can’t mess with Mother Nature, and we already know people are creatures of habit, next question….. what economic law would apply?

Is there a long term all time chart for an applicable market? Perhaps one with a impeccable macro hit rate?

Unfortunately you’re right dude. Some will get it most will just do what the meme and the Twitter tells em, which would be called what? How would that apply to markets?

I hope this may help someone.

Great article on behaviors!

P.S.

Remember we are all responsible for our own financial decisions. There is a winner and a loser in every trade. If we make the wrong read, listen to the wrong people, or talking points and end up on the wrong side…. it’s nobody’s fault but our own.

We all can chose to go long or short.

No blaming politicians, the fed, China, or anyone else for our bad call or timing.

Biden, Powell, or the CCP didn’t put a gun to anyone’s head and force them into the wrong play. No sour grapes.

@John,

Govt or the Fed doesn’t need to put a gun to the head if it can easily get away with borrowing from future and with devaluing your labor.

Dollars that you have represent your hard work that went in to earn them. Your labor provides value to those dollars.

When the Fed prints dollars out of thin air, where do those dollars get their value from?

By stealing the value from everyone else’s dollars.

disagree.

The Fed decided to pump money into the system. We were told QE to be temporary in 2009. There were those who knew it would not be temporary.

The Fed pounded long rates to FORCE investors to take more risk or get slaughtered by inflation.

Manipulation by fiat

“We can all chose to go long or short.

No blaming politicians, the fed, China, or anyone else for our bad call or timing.”

That sounds great in theory, but it’s complete BS in practice. If the Fed and politicians set the rules and let people play the game accordingly, it might make some sense. However, it ignores how the world actually works. The problem is the rules change in the middle of the game. Whether it’s banning short selling during the GFC, bailing out selective groups and industries (AIG, to save its counterparts, GM bondholders, etc.), or even the uninsured depositors at SVB, those are decisions politicians and the Fed make that pick winners and losers.

There are many other examples of politicians and the Fed picking winners and losers. There’s no way to know in advance who the favored parties will be, except they’re usually politically connected. I think personal responsibility is important, but the way in which our system only applies it selectively is why so many people correctly view it as corrupt and rigged.

Of course the system is corrupt and rigged. What are you, personally, capable of doing about it? Probably nothing.

What you have to learn is how to prosper despite their machinations. The keys to that haven’t changed much over the decades I’ve been alive. Listen to their words, but watch the actions. Stay the f@*# out of debt. Financing a burger at 25% APR is stupid – but that’s what you do when you buy said burger and let your balance revolve. Be your own bank. If you own your house outright, pay yourself *rent*. Make *payments* to yourself on the car you bought for cash. That serves multiple purposes: Among them, replaces the money you spent, keeps your funds out of the hands of the banksters, and expands your funds so you can buy the next car/couch/house or whatever.

Learned this from relatives who survived the Great Depression. It’s served us well.

You don’t have to live like a pauper to do so… because eventually you have the where-with-all to do whatever you want along with the flexibility to adjust for the ups and downs without inflicting damage to your quality of life.

El Katz,

I was pointing out the idealized world John L describes doesn’t exist in practice. That’s why, as you say, “listen to their words, but watch the actions.”

Of course I can’t do anything about the system, except take advantage of it as the rules allow. Fortunately, that’s something I’m particularly well placed to do. I agree with and have put into practice much of what you say about how to live one’s life.

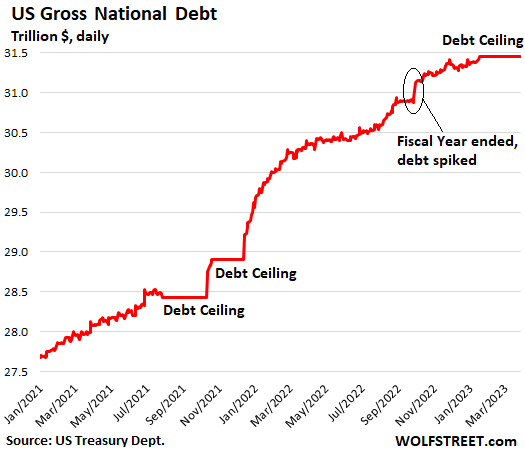

It will be interesting to see your May Fed balance sheet installment quantifying QT Wolf. I wonder if the Feds March liquidity programs that vaulted the balance total higher have been repaid. My bet is a hard NO.

We’re $1.1T in the red 1/2 though FY 2023, so $2T seems extremely likely. That’s a lot of inflationary monies being spent by Uncle Sam, including what will be at least $800B in interest expense going into a lot of rich people’s pockets.

I’ve been saying since last fall that a 2023 recession is unlikely. 2024 is a safer bet. And I agree with Bullard. The labor is way too robust for a recession this year.

And as always, Wolf, makes some very good points about the macro situation surrounding this very unusual economy indeed. Last December, Bullard said 7% might be needed. Sounds like he’s pulled back from that a bit, but 6% is really starting to look not only possible but likely.

Myself (and I think most financial pundits) are shocked higher rates haven’t crashed the economy yet. If you told me back in say Feb 2022 how high rates would be for much of 2022 and now 2023 I would have said the global economy could never handle it.

Rates are not high. They are more negative now than last year. It doesn’t matter what you put your money into it is losing value, so best to just spend it now. Also, while asset values are under pressure, the capital value of debt is being wiped out at a phenomenal rate. If people can hold on to the bucking bronco of nominal interest payments, in a few more years their debts will be miniscule.

It’s a wild ride right now, but things are still very much in favour of debtors. If fed really wants to slow the economy it needs to push real rates positive or much closer to that point. Then people with the huge debts will really feel what pain is. I doubt they will do this, so I’m spending before the fed incinerates my savings.

What are you in such a hurry to spend on?

Case of Stag, full tank of high-test, Flamin’ Hot Funyuns & a Juggs subscription renewal.

“best to just spend it now”

I see this mentality a lot in my social circle (millenials) – the value of saving for the future is completely absent.

I see a lot of $$ being spent by folks who don’t even have $1000 in emergency funds. I guess I can’t really blame them, 15 years of savers getting screwed have fundamentally altered how money is perceived & valued. And now we’ve added significant inflation into the mix.

Not saving, building some reserves, as a cornerstone of one’s financial life, has been foolish every minute of that time.

$1000 emergency funds, unless you are referring to physical cash stashed in your home, I don’t see the point. Most people have credit card with credit line and cash advance much higher than $1000 for emergencies.

That is still a gamble. Saw a lot of credit cards dramatically cut their limit or completely close people out in 2009.

15 years of savers being screwed?

Can’t a saver put savings into the S&P500? I’m an idiot and I figured that out. What is the return over the last 15 years? Not too bad I would guess.

If you put money in the bank the last 15 years you screwed yourself.

A big difference now though is that most millennials are paying into a workplace pensions scheme (certainly the case in most of Europe and Australasia). So they’re not actually being that dumb – they’ve got money going in that will supposedly pay for their basics in retirement, and the rest is about choosing whether they want to spend their fun money now or hope that it is still worth something in 20-30 years time when they (potentially) retire.

Faced with that choice, can you blame them for concluding that perhaps it’s better to get that whole trip to Japan this year, rather than half a trip to Japan in 20 years time (if even that?).

Additionally, most millennials I know don’t expect to really retire. They want to keep doing stuff as long as they can, because they generally enjoy their jobs. With the rise of remote and flexible working many see a future where they just keep trucking along in some form or other until they’re in the old people home. Consider the massive sacrifices it takes to get an extra $10k of annuity by the time you’re 65, vs how few hours (maybe 10 a week) it would take to get that same income if you can keep working in some capacity.

Nissanfan,

Not every sudden expense can be paid with credit. When I totalled my car in 2018, I bought one from a family member and paid 10K in cash. The same car purchased (financed) thru a dealer would have been 15K – and I didn’t want to finance & pay interest since I had that cash for exactly that reason.

What if I need a new roof tomorrow and the contractor only takes check etc.

grimp,

Sure they can – that’s where my money was for the last decade.

But now its in CDs and Tbills. My ladder’s average yield to maturity is 4.9%. I don’t think we’ll see the sams returns in the stock market that 15 years of artificially low interest rates have delivered us.

Jon W,

I am a millennial & feel exactly this way re retirement:

Covid lockdowns taught me that I need something to do to stay sane. Despte being paid to sit at home by my fulltime job, I signed up for Doordash and did deliveries for a couple hours a week – BOTH for the cash & a reason to get out of the house.

here we go again with the ‘poor me’ ‘life is sooo’ hard’ comments. people with first world problems getting all of their financial planning advice from like minded bloggers. never any personal accountability to learn, grow, adapt to the realities of an always fluid, ever changing world. we’ll ok … this is a great breeding ground for lot’s more sheep in a land of wolves.

1982 or 1990 its been at least the past 33 years that savers have been fleeced.

“Rates are not high. They are more negative now than last year.”

Untrue. Per the rate on iBonds, inflation over the last 6 months x 2 = about 3.8%. Overnight rates are 5%. That’s positive. Is there any measure of inflation that is currently running materially >5%?

Core PCE YOY March 2023 was 4.6%. Based on my recent personal experience my guess is that inflation is actually running about 8% annually. Core PCE is a statistical construct designed to understate real world price inflation.

“designed to understate real world price inflation.”

No, core PCE is designed to remove the highly volatile commodities-based food and energy components to get a feel for underlying inflation.

For example, gasoline prices have plunged. So has inflation plunged? No. Core PCE removes gasoline so that you can see what’s going on with the underlying inflation, such as in services.

I report services PCE separately so you can see the inflation in services, and not to understate inflation.

READ THIS:

https://wolfstreet.com/2023/03/31/services-inflation-rages-at-worst-rate-since-1984-keeps-core-pce-feds-yardstick-in-same-high-range-energy-goods-cool/

Jon w

Djon Y

This strategy is apologetically stupid

If someone has 100k, he has that much. Yes, with inflation, the purchasing power falls, but if a person decides to buy something, he has this money as a basis. He who spent them has nothing. And there will be nothing because that’s how he lives. And mass wages won’t outpace inflation forever, because then we’ll go into a spiral. Assets will not grow forever because there simply isn’t such a market. At some point the coin will turn and you will need money which you will have to take on credit but credit makes you a slave for years to come and keeps you in the dark due to the many circumstances that may befall you. Cash gives you freedom.

You can quit the job you don’t like, you can go on a trip, you can pay for your children’s education, or buy a house if you have enough money or move to another city or country.. And all this without worrying about how you return the money

Years ago in my country it was shameful for a person to say that he had credit or a loan because that said that person had no money and that is why he resorted to credit. People worked and saved, and if they had to take out a loan, they took out minimal amounts, which they used the already saved money to buy a property, for nothing else.

“Spend it now”.

Stupidest. Advice. Ever.

Whatever you buy will likely be worth less 15 seconds after you take possession of it than if you simply kept the cash and absorbed your “loss” to inflation.

Buy a car? 20% as you drive over the curb. Couch? -75% the minute they drop it on your floor. Dinner out? -100%. TV? Near -100%. Latest iGadget? -90% shortly thereafter.

The financial naivete of people never ceases to amaze me. You’re not enduring 10% inflation per year. Not even close. If you didn’t buy a car, your loss to “inflation” on vehicles was zero – but if you drive a new one over the curb, you lost 20%+++ (an possibly 100% of the sales taxes if it’s not a net-of-trade taxing state) plus future depreciation. Own your own house? Housing inflation near zero as your *rent* is fixed (not considering taxes and insurance). Clothing? Buy better quality, more durable, and classic styles and you can look stylish for near zero, but for that which wears out eventually. Food? Move from prepared food to stuff you cook yourself. There’s no way a package of cheezy poofs is worth $6 – you can buy organic popcorn for a buck a pound in bulk and pop it yourself for the price of a $10 silicone popper (no oil or butter required) and the juice it takes to power the microwave for 2.5 minutes – and the silicone popper lasts for years. Plus you’ll be healthier. Services? Eat at home. Add a week between haircuts. Clean your own house. Pick your own weeds. Paint your own bathroom. Wash your own car. Skip the fake nails. Dump unused/infrequently used subscription services. Prescriptions? Shop online. One drug that I am prescribed cost $90 per month with insurance. Found it from an online U.S. based pharmacy (both generic) for $11 plus $5 shipping. $16 for 90 days (plus the $5 shipping) vs $270 with “insurance”. Bundle together three prescriptions? The shipping is still $5 for the lot.

All this arm waving is hysterical. Use your head for something other than a hat rack.

Well said!

I always priced anything I wanted to buy ,in how many hours of work/price of item . Made decisions easier

“Rates are not high.”

Quite right. I’m old enough to remember the 1970s here in the UK, where inflation went over 20% for two years. I got used to think in real (inflation adjusted) terms. But much of the financial media hasn’t got the message yet, and still thinks in nominal terms. Interest on savings accounts here is currently -7% real. As a hedge against inflation, I recently invested in a UK residential REIT that has 50% LTV and the majority of its debt fixed for 20 years at 3.5% nominal.

The real economy can handle these rates. At least one-third of inflation is profits. If rates at 6-7% kill off the predatory parts of real estate, banking and finance, so much the better. Of course, since America has a limited real economy, I can see how this makes wealthy people with stock portfolios nervous.

It’s simple…… they were slow to raise and haven’t raised enough. Muddling around 4.5% isn’t “high” at all. Talk to me when the rates become what they should have been in late 2022….. 7-8%. That would have done the trick without question.

Economists have successfully predicted 8 of the last 3 recessions.

In this case, the collapse of the everything bubble has been 6 weeks away, for the last 6 months.

They printed over $10 TRILLION. It’s got legs. The people screaming “RECESSION!” were trying to scare the FED into a pivot.

Powell derides monetarism and believes that the quantity of money doesn’t affect inflation. He was caught wrong footed when inflation proved non-transitory due to trillions of dollars of helicopter money that he helped drop on the U.S. economy. Powell is not only wrong, he’s stubborn. It’s a dangerous combination.

From my limited perspective, I too don’t see a recession coming soon. All these hopeful projections and large scale reporting are difficult to reconcile with my daily personal observations. My family and I call it the congestion report. When times are good the roadways are full, when times are bad the roads are open and traffic is light.

I too live in the Bay area and work a regular in the office job, Monday -Friday, but enjoy going skiing in the Lake Tahoe area on the weekends. The traffic is bumper to bumper, constant the entire 3-4 hours, even with gas being $5.00 + per gallon here locally and $6.50 per gallon in Tahoe. The ski resorts are packed, lift lines are long, the parking lot is full before the resorts open for the day, lift tickets are $250 per day. People line up to buy $20 hamburgers and $12 beers all day.

Local restaurants are completely booked every evening. Local shops are now requiring you make an appointment to be able to get a sales person to sell you products, which now cost 25% more then a year or two ago.

People are demanding higher salaries, and being paid more. Companies are charging more for all services, and getting it with waiting list of customer demand. Consumers are willingly paying more for the things they want. Continued inflation and tight labor markets going forward seem much more likely then a recession and wishful thinking for a return to extremely low cost money.

The number of full time residents in Tahoe jumped 10x over the last 2 years. All those folks you mentioned are now considered locals.

They are not considered locals yet. The locals hate them with a passion.

…an ever-present aspect of emigration, immigration, and human nature…

(…a mild comment illustrating this was the British one about the U.S. military presence in the U.K. in WWII: “…the Americans are overpaid, oversexed, and over here!…).

may we all find a better day.

No recession coming in the Denver area either. Heavy traffic, and if you can even get service, you will pay for it, but first you have to wait for it.

Cement trucks rolling out at 3:00 am, and staying out all day. Trucking in general, is still doing fine.

The only negative I see personally is that the starter homes are pretty much done for now.

Still a lot of work on new, big industrial warehouses. New sites being developed.

From my perspective, we have more rate increases coming.

I’m in Denver too, and concur. If you look at the State Demographer’s numbers you’ll see close to a million new residents expected in the next 10 years. Yes. A million. Not a typo. This in a state that currently has a pop. of about 5.9 million.

Wow, those demographers have some sweet crystal balls!

That’s a little over a 1.5% population increase per year. That’s pretty consistent with Colorado’s growth rates from 2006 to 2019, so the demographers must be anticipating a return to that trend.

I fear there’s not enough water to handle that many newcomers.

I agree. In the Bay Area, it feels to me like the dams burst around Jan 1st. People haven’t been doing what they wanted to do for 2-3 years and now they all want to do it, and will pay any price. Like One Thousand Dollars a seat to see Kenny Loggins at Mountain Winery.

As for Tahoe, combine the dam burst with the first good snowpack in six years, and yeah, everybody wants to go. First time the resorts haven’t closed on Feb 1st.

At work I hear “that person has left the company” at least once a week, both internal and from customers. Any not from any layoff.

One more rate hike is not going to contain this flood.

“People haven’t been doing what they wanted to do for 2-3 years and now they all want to do it….”

I’m so sick of hearing that (no offense). People began doing whatever they wanted in 2021. And had all that year. And then all of 2022. We’re 2.5 years past legit lockdowns. Travel has been unhindered pretty much the entire time. Something else is at play here.

“Something else is at play here.”

It’s called $10 TRILLION in printed money. It didn’t just disappear. They never did the math, they just dropped a liquidity bomb.

Sounds like the period of euphoria that comes before a crash.

My son in law ,and daughter both work for a national trucking company in Omaha . Freight is way down first sign of trouble.PREPARE

Goods!! Trucks move goods, not services. Demand has moved from goods to services, inflation has moved from goods to services. This has been a HUGE theme here for at least a year. I’ve been belaboring this ad nauseam from all kinds of angles. Services is nearly two-thirds of consumer spending. That’s where it’s at now.

But ain’t moving goods a Service?

Not for consumer spending, unless you the consumer pays for it directly. If a retailer gets a truckload of lamps, and is invoiced for the cost of the merchandise plus freight, it’s NOT consumer spending. Eventually, all this will end up in the retail price of the lamps that consumers buy at the retailer, and that price will be for goods (the lamps).

If the consumer buys a plane ticket, that’s services, and those are up 30%. The price of the ticket (a service) includes everything that goes into providing the service, such as jet fuel, staff salaries, bags of mini-pretzels, sodas, leasing costs of the aircraft, etc., some of which are goods. But the ticket that the consumer buys and pays for is a service.

Sounds like the end of every bubble.

Why would anyone still go there? Rhetorical. No answer necessary.

Lift tickets might be $250 per day, but a season pass with Epic or Ikon is something like $900 per year.

Supply chain disruptions are now a feature of the economy, not a glitch. Consumers adjust. More people are working under the table, making alternate living arrangements. It really is a recession economy.

We’ll have to see unemployment actually get above normal levels first, no? I get that a recession is supposed to raise unemployment and reduce inflation, but what if it doesn’t? As you said, it’s a weird economy, and labor force.

Imagine 10% of working-age adults vanish: GDP gets crushed, but as a layman I couldn’t confidently say what happens to unemployment and inflation.

Yeah, that’s another thing banks and corporations are doing: laying off as much as possible to help make things LOOK worse. They get big airtime and CEOs sobbing. They might get a little bump in their stock price. But the 5% Fed ain’t budging.

Maybe the economy will fall from the TOP down if it’s going to. Maybe workers are finding new means of a living away from these monopolizing giants.

I have always felt that a fair return on savings is an economic engine, feeding consumption. When rates are suppressed artificially, it is the government that benefits and increases their spending due to the cheap borrowing costs. But when rates are fair and near or over the inflation rate savers will turn into consumers and the benefit shifts from the government spending to the saver/consumer spending.

The great differential here is the consumers spending their interest earnings do so in a more efficient way than the government spending funds raised from floating, low interest debt

That was always my thinking as well; when you’re permanently hedging against future uncertainty, (and no future is anything but uncertain, but I digress), you don’t exactly possess the cavalier mindset for frittering your earnings on discretionary purchases. I realize it’s salad days of late for the American shopper, but I suspect it’s largely fueled by windfalls/affluenza and ignited by a mixture of fatalism & YOLO.

I don’t think this lasts.

Question:

How much (%) of bank earnings is from Fed payments on excess reserves? A source for bank earnings new since 2009

Whether banks park their cash at the Fed as reserves or in Treasury bills, the income is roughly the same. If the Fed paid 0% on reserves, the bank would switch their cash to Treasury bills and make roughly the same.

However, reserves are instantly liquid and don’t require a sale, unlike Treasury bills which have to sold to get liquidity.

There are also regulatory differences between the two.

Let me add to the confusion. I am in Sao Paulo, Brazil this week. The currency value is about the same as 18 months ago, but grocery and clothing prices (domestic goods for Brazil) are broadly up 25-40 percent. The wealthy areas are busy and free spending.

Good thing you’re not in Buenos Aires. Inflation is currently over 100%.

BA such a nice place but the everyday middle class in Argentina do struggle daily because of inflation . My heart and prayers are with them.

A mild recession would be the best case scenario. If we don’t get a recession we continue with stagflation which is a worse outcome.

“Instead, it’s adjusting to the 5% rates and to higher inflation. Everyone is getting used to it.”-wolf

The average federal funds rate 1971 to 2022 was 4.6%. There is nothing strange about today’s 5%. What was strange was adjusting to over a decade of free money. I guess young people thought it was the new norm and would last forever. Now there are complaints about mortgage rates at 6.4%. The average fixed rate on a 30 year mortgage 1971 to 2022 was 7.6% or so. My point is none of the current numbers are unusual, in fact, they are just about average. There is no reason to think they in themselves will cause a recession.

Having said that, there are some very extreme bubbles now that are in fact not normal. These are, say over the last ten years, single family home price increase, and stock market price increase. These suggest a kind of mass insanity.

Correct.

Gaslighting by the Fed and Wall St.

The mantra that Fed Funds belong under inflation and that 5% is high.

This is historically rediculous.

I have trouble understanding those that assert that Real estate is over priced. I basically recall over the past 50 years or so that it has always seemed overpriced.

It is basically symbiotic with the money supply. So, RE is basically flat.

It’s not that real estate is over priced but that wages have not yet fully reached this new level. RE will wait till wages catch up.

Jeesh. RE isn’t close to flat. It’s a roller coaster except for some interior markets. Just look at the CS plots. Normalize w.r.t. inflation if you wish. Any way you slice it, it ain’t flat.

This is an incredibly innumerate comment.

> Wages catch up

This began in 1997.

You could argue RE is flat if you only look at list prices and only at the non-bubbly markets.

I track the St Petersburg, FL market closely. In 2019 you could’ve gotten a large, beautiful home on the water, in a golf community, with a pool and a boat dock for a monthly payment of $4000. In 2023 that same $4000 payment will get you a decent SFH in the middle of middle-class suburbs on a busy street two blocks from the mall. Meanwhile the large home on the water will now fetch a monthly payment of $13,000.

It convinces me that no one is buying anything with 20% down right now. Middle class families can’t afford a $4000 payment, and I conclude that they must be carrying proceeds from the inflated sale price of their prior home. People buying with 20% or less are shut out. They can’t afford the payments for homes that match their acceptable lifestyle, and they don’t want to buy a crappy condo in a crappy neighborhood just to say they own something.

“they don’t want to buy a crappy condo in a crappy neighborhood just to say they own something.”

That’s how the real estate game used to be played. It was called “climbing the property ladder”. Now everyone wants to start near the top… something along the lines of the commercials that tout “get what you deserve”.

Sadly, sometimes what one deserves is to get it up the chute.

LMAO

We are getting excess spending because GenZ and millennials have given up on the ‘american dream’. They know they cannot afford to buy a house, or start a family. They know there’s going to be no retirement for them, and probably no jobs either (AI?). They are living in their parents’ basement and buying trucks, crypto, or traveling. These are secular shifts in behavioral patterns. Beware of the tectonic movements just beneath the surface.

Sad but true

Again with the doomsaying about Millennials and Gen Z? A lot of them are filthy rich! Name one Millennial who is living in his or her parents basement. This doomsaying is complete nonsense. Who do you think is doing all the wild spending out there? I’ll give you a hint – it’s not Baby Boomers like me. I buy nothing! I own everything I need and really only buy food and the occasional tank of gas.

You got that right. Millennials are primarily the ones who went and bid up housing prices to ridiculous heights.

Escierto we must be riding in the same boat

Anecdotally I have a lot in my age group who fit this description – milennials who still live at home and don’t have much in the way of savings due to their spending habits.

This shows how much easier school was back in the day.

You can’t use anecdotes to support a position.

Data show more millennials are living at home.

“We are getting excess spending because GenZ and millennials have given up on the ‘american dream’.”

Maybe many of them don’t like the ‘American dream’ (nuclear gender-defined and structured family models, two weeks off per year, boring suburban neighborhoods, etc.)

In modern times, change is so fast that people who are two generations apart in age, have, in general, significantly different brain structures and psychological realities.

Yeah, some are struggling in terms of assets, like my niece who is developing her own indigenous plants landscaping business, and works on other related side jobs. She does no fit the spender stereotype because she has nearly zero discretionary money to spend. And if she did, she would not be flinging the money to the winds. The “American dream” for her is currently checking out a tiny house as starter. I’m trying to whet her and her sister’s appetite for saving by giving them I-bond gifts every Christmas.

I’ve been thinking about this but I think you have it backwards:

ZIRP and the credit bubble have *enabled* people to stay single / live alone longer, where before they could not afford to do so. Living alone is a LOT more expensive than shacking up.

Very true. We always planned on having a paid off home before retirement and it didn’t turn out that way, due to the GFC. Instead we have no home and no chance of having any paid off housing in retirement. Therefore, we don’t plan on spending much time in America when we do have to retire. We will become nomads where ever we can live comfortably on our retirement income. It’s not what we originally planned but it is what’s on the table now.

All those landlords, car manufactures, and retailers are in for a rude awakening when the transients transit out of this economy.

I think for the geography, Mexico would be my favorite and most convenient location to go. And the Food! But too bad the corruption and crime, literally, heads roll there. Otherwise, Mexico (likewise on south) would be a world destination and a booming economy.

I lived in Mexico for seven years. Violent crime is primarily confined to the criminal class. The drug dealers like to shoot each other, but if you’re not involved in drugs commerce or organized crime you’re unlikely to be a victim. Corruption exists but it is a non-issue in daily life.

A friend of mine plans to retire with his wife to Panama in June. They’ve checked out many of the alternatives and decided that’s best place for them. They don’t want to retire here in the SF Bay Area.

Something to consider.

Great plan until they bankrupt SS. Then you’re in a foreign country with no income. Always have a plan B,C good luck

Most millenials I know are doing great, financially-much better than this Gen X saver who paid off their student loans and keeps getting screwed. I’m just going to spend all the money I saved and wait for a handout. I’ll buy a house I can’t afford and stop paying the mortgage. The government will bail me out.

The assumption that a recession will be anti-inflationary is behind the market melt up.

A raise, pause, raise again Fed will invite a 70s redux.

Who at the Fed decides how much of a rate hike or cut there will be? Is this something they vote on?

No one knows his name, but it’s Depth Charge’s drinking buddy. They usually get pretty sh*t faced and break some sh*t.

Ha, ha! I figured Depth Charge was behind it in some way.

I await his comments on Wolf’s article.

I heard that early in his term, FDR would be in bed and just pull an exchange rate of gold to dollars out of his head. He laughed about it, I think with his neighbor, Henry Morgenthau, who became his Treasury secretary.

Bloomberg,diamond, and fink

The FOMC (Federal Open Market Committee) which is comprised of 12 people made up of the 7 members of the Federal Reserve Board of Governors plus 5 Federal Reserve Presidents of the from the 12 regional Federal Reserve Banks and all policy decisions are made by consensus of that 12 member FOMC.

Don’t be naive,there puppets ,told what to do

QUestion: Could “stagflation” be a cunning tool to end runaway “unsustainable” growth. There are “limits to growth” in our world.

(The latter quotes were the name of a seminal study printed in the mid 1970s by Randers and Behrens, {avail on youtube} about how we couldn’t just keep juicing up capitalism any further without reaping a REAL crash driven by finite planetary resources, so i’m using the word “growth” in that sense). Certainly “the elite planners” have raised the fire alarm on “sustainability”.

First and foremost, the Fed wanted this inflation, contrary to what they’ve said or what pundits think. It is the only way out of a terrible debt situation across the economy. It is also very painful and will continue in fits and starts for some time. The initial inflationary impulse started things moving. Alot of people buy the “story” that this was due to COVID free money combined with supply chain shortages. That is only partially true (and the free money was planned). In reality, many businesses raised prices simulataneously to increase their profit margins. Various and sundry “stories” ensued like the big egg inflation and of course, Putin’s Ukraine inflation.

All this said, the Fed is now in the business of “managing” the inflation train. Not letting it go too fast but they have no interest in shutting it down quickly. Thus the interest rates we see.

The Fed knows there will be collateral damage even at these modest interest rate increases, but there will also be positive impacts like interest income that hasn’t existed for some time. They plan to manage through the unexpected hiccups.

Will we see recession; most likely. Will the Fed knee jerk down if that occurs? Most likely not much. They are in the game now of keeping “it” between the ditches, as it were. Inflation will continue (wage increases) but slow down. Some parts of the economy will do fine; others not so good. Everything is a trade-off.

One final note, the Fed will NOT be doing QE or ZIRP anytime soon. The rest of the world is fed up with our easy money and is moving away from the dollar. These are very dangerous times for the US dollar and anything less than strength won’t be allowed.

The inflation measuring month over month and one year over the next is a mask for what really happened.

The metric should be over 2 or 3 years…..the “spikes” in inflation must not just be forgotten but included in the “damage report”.

The fact the Fed only talks about lesser increases to be stacked upon the spikes is a tell. Never a word about rolling prices back.

Three years at 2% (without compounding) is 6%. We’ve got something in the neighborhood of 20% over 3 years. To point to month over month increments dismisses this damage.

This is why government employees in Canada are currently striking and asking for a 24% wage increase over the next 3 years. And that is reasonable.

I agree somewhat, but, all debt is increasing imo exponentially. So fast that even inflation cannot keep up. At some point we just cannot borrow anymore.

The global economy is more reliant on US Dollars than ever and nearly 88% of all global transactions are done in US Dollars.

I have a question on what is going to happen to the bond market when the debt ceiling is raised and the Treasury goes on a bond selling spree to refill the TGA? It’s months away yet I hear little about the ramifications. I understand it will suck liquidity out of the system and may be a headwind for equities but am not sure about what happen to prices/yields in the bond market. Do they have to auction bonds with higher rates to generate enough demand? What effect will it have on the prices/yields for currently issued bonds?

WFH,

Great questions. Here are a couple of basic dynamics.

The Treasury Dept. has to fund the deficit operations by:

— collecting taxes

— drawing down the TGA (Treasury General Account, the government’s checking account at the New York Fed). BTW, the balance jumped today by a whole bunch because tax payments, including estimated taxes, started coming in, including mine, LOL

— issuing new bonds. Bond issuance has been close to normal, but not quite enough

— using the so called “extraordinary measures.”

These “extraordinary measures” are key. It means that the Treasury essentially doesn’t issue its special nonmarketable securities to the government pension funds; it just collects the contributions, and they flow into the general budget and get spent. Normally, it issues nonmarketable securities for these amounts, but during the debt ceiling fight, it doesn’t. Those special nonmarketable securities are part of the debt, and part of the debt ceiling.

So when you look at the total gross national debt you see the flat spots of the debt ceiling fights. And you see the spike the day after the debt ceiling was lifted. Those spikes were the nonmarketable securities that the Treasury issued essentially with the click of a mouse:

But when you look at marketable securities and nonmarketable securities separately, you can see that marketable securities continued to rise, and nonmarketable securities have been declining.

I explained all this here, with charts for both of these categories:

https://wolfstreet.com/2023/04/03/the-extraordinary-measures-the-government-uses-in-the-debt-ceiling-farce-to-delay-a-default/

So now, in terms of your questions:

The nonmarketable securities do not impact the market or liquidity. They’re between the government and the government pension funds. So the Treasury department will issue a huge amount of them on the day the debt ceiling is lifted to make up for all the nonmarketable securities it didn’t issue. And I will write my customary post-debt-ceiling article with a headline, like: “Gross National Debt Spikes by $500 Billion in One Day.” But they don’t impact markets or liquidity.

Then, to replenish the cash in its TGA, the Treasury will also gradually increase its issuance of securities. So maybe it wants to lift the TGA by $200 billion, so it will increase issuance of marketable securities by $200 billion in addition to the normal issuance, over a two-month period, for example. So this is where investors will be asked to come up with $200 billion or whatever in a relatively short amount of time. And to accomplish this, it might entail higher yields and lower bond prices. So there is this impact on the market. But it’s not huge.

I couldn’t find the breakdown or total amount of non-marketable securities bought by government agencies, which seems like a crutch that helps maintain liquidity in the system. But did find related information about the Social Security system, which relies on two legally separate trust funds: the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund. At the end of 2022, OASI asset reserves were $2.7 trillion.” It would be interesting to know which other government agencies own the unmarketable securities, and how much.

“The interest rate on new [non-marketable] securities acquired by the two Social Security trust funds is the average of market yields for traded [marketable] U.S. government debt with terms of more than four years. For example, in 2021, the two trust funds’ average of the 12 monthly rates for the non-marketable debt they purchased was 1.4 percent.”

This seems related to complaints I have read over the years about the pool of taxpayer paycheck contributions to Social Security being typically held hostage to lower interest rates of (average of >4 year term Treasury securities) as well as being whittled away by dollar devaluation / inflation.

In November 2022, the interest rate for new special issue debt bought by the Social Security trust funds was 4.25 percent, up from 1.625 percent in January. Sounds better, but still net negative yield for the Social Security fund due to inflation.

It seems that this government debt inspired bloodsucking of governmental agency funds (by issuing low interest non-marketable securities) is a significant reason why “Social Security costs exceeded total income including interest for the first time” in 2021.

The TSP (Federal Thrift Savings Plan) owns $294 billion of the nonmarketable securities.

drifterprof,

“I couldn’t find the breakdown or total amount of non-marketable securities …”

And then your whole discussion on Social Security, LOL

You crack me up. Why didn’t you just click on the link to my article that I gave you above. And that article has a link to my discussion about the Social Security Trust Fund, including the interest rates, and all.

So you could have saved yourself a lot of trouble with just two little clicks, and would have had some real answers instead of the Googled stuff.

I did click on the link and read it for the second time. But I did not find any specific breakdown of the full set of nonmarketable securities and how much is allocated to the various government agencies.

I remember reading your excellent article about the Social Security Trust Fund, and checking back, it refers to “special issue Treasury securities.” So I assume that is another way to describe “non-marketable” Treasury securities.

I still would like to find a breakdown of the total non-marketable Treasury securities bought by all government agencies. Sure, it’s great for taxpayers to have no-risk securities to have their money in no-risk securities. But why would the government have to sell its own low yield no-risk securities to it’s own pool of taxpayer funds? That seems like a rip-off.

Is this suggesting that there might not be a proper “recession” in the real economy, but that might not stop the collapse in asset prices?

Could that happen?

Happened in 1987.

Denial of reality is a BEAUTIFUL thing! There are so many possible Black Swan events hovering (Geo-political), not to mention the increasing prevalence of violence (mainly in big cities) and increasing intolerance of different views (both sides).

64% of people are living paycheck to paycheck (per CNBC 1/31/23). It just seems to me that people (in general) are whistling past the graveyard while they just choose to keep on spending more and more to get less and less. But… YOLO, right? I might just be a doomsayer, but at least I can SEE the real possibilities of big problems ahead and plan for lean times while hoping it doesn’t play out that way. But, HEY.. that’s just me..

“What’s normal anyways?”

-Forrest

Rosarito Dave,

“64% of people are living paycheck to paycheck (per CNBC 1/31/23).”

That is BS. The NY Fed does a similar type of survey, and the headlines cited in the media are always the same braindead BS that people just keep spreading around without ever reading the actual articles.

In the NY Fed survey, the question is: “How would Americans cover a $400 expense?” (essentially the same as paycheck to paycheck). And the headlines about it are always shocking, but bullshit.

This is what the New York Fed said:

88% can pay for it just fine. Only 12% wouldn’t be able to pay for it right now.

They split up this way::

78% wouldn’t even have to borrow at all to pay for it. Of them:

45%: with checking or savings account