Investors lost interest too: Sales to all-cash buyers plunged 24% year-over-year.

By Wolf Richter for WOLF STREET.

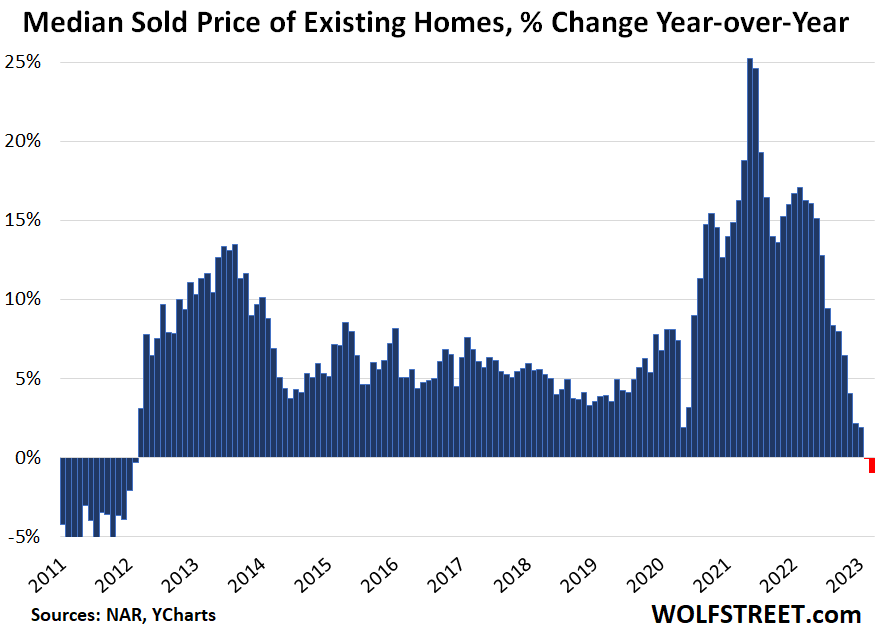

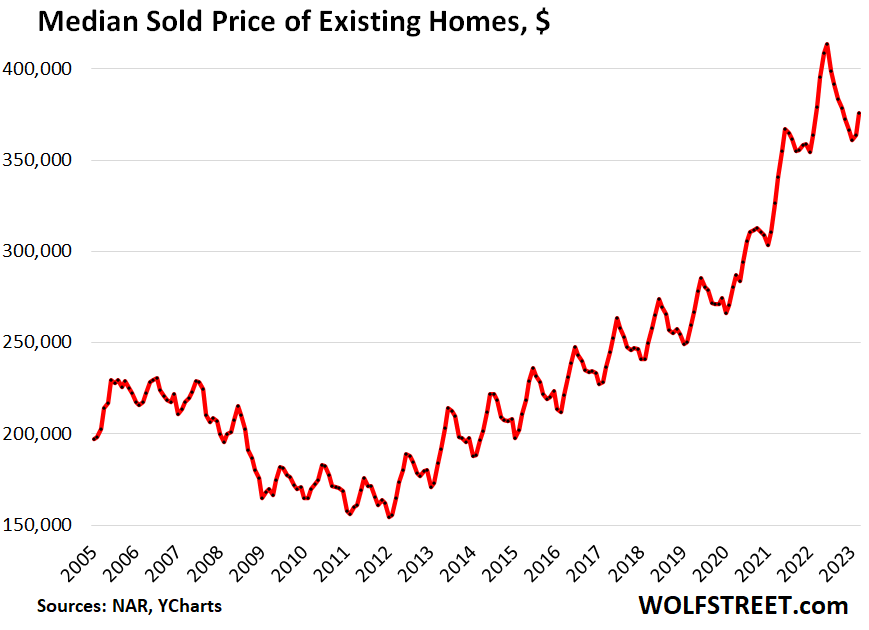

The median price of all types of previously owned homes – houses, condo, co-ops – whose sales closed in March, fell year-over-year by 0.9% to $375,700, according to the National Association of Realtors. This was the second year-over-year decline in a row since February 2012, when the market emerged from Housing Bust 1 (historic data via YCharts):

For single-family houses, the median price fell 1.4% year-over-year, the second year-over-year decline in a row. But for condos, the median price still increased 2.1% year-over-year.

The year-over-year decline of the overall median price came despite the 3.3% month-to-month increase in March from February. But it’s spring selling season when prices typically rise, and that increase was smaller than last year’s February-to-March increase; hence the bigger year-over-year decline.

The median price has fallen by 9.2% from the seasonal peak in June 2022 (historic data via YCharts):

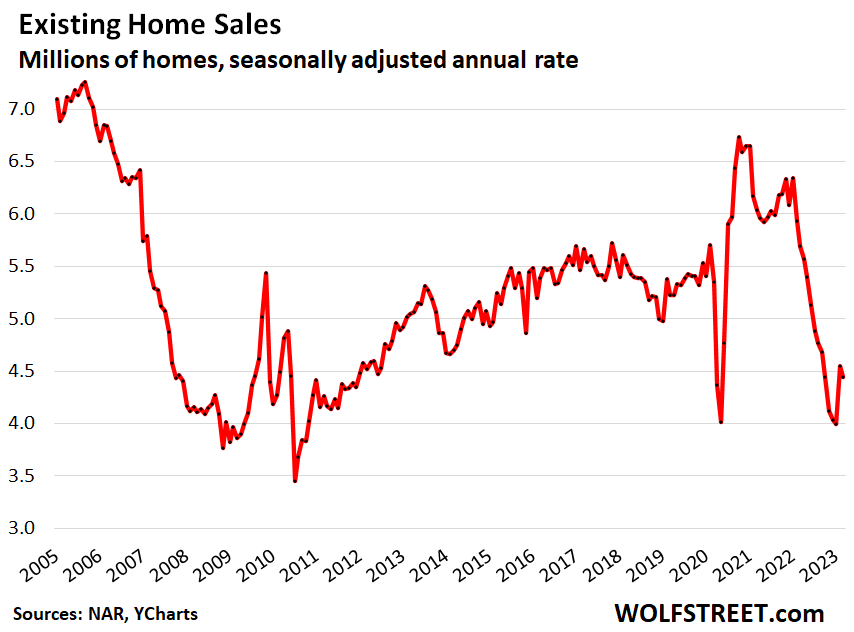

Sales of previously owned homes fell by 2.4% in March from February, to a seasonally adjusted annual rate of sales of a dismal 4.44 million homes, undoing part of the jump in February from deep-dismal January, which had been the worst month since 2010. So there had been 12 months in a row of month-to-month declines through January, an increase in February, and now another decline in March.

Compared to March 2022, sales were down 22%. Compared to March 2021, sales were down 26.5%. Compared to March 2019, sales were down 15%. Compared to March 2018, sales were down 19%.

Priced right, just about any property will sell. And lower prices would bring out the buyers which would help unfreeze the market, given these mortgage rates.

But sellers – including those that bought a home and moved into it but haven’t put the home they moved out of on the market, which was the thing to do to ride up the price spike all the way – well, they’re are still thinking that this too shall pass. “This too” being the 6%-plus mortgage rates, or rather the 4%-plus mortgage rates, which we had exactly a year ago, because that’s when the market started to derail.

Actual sales in March – not seasonally adjusted, not annual rate – fell 21% year-over-year to 360,000 properties. This was up from February, as it is nearly every year due to the seasonality of home sales, but it was up less than in March last year.

Sales of single-family houses, at a seasonally adjusted annual rate of 3.99 million in March, were down 2.7% from February and down 21% from March last year.

Sales of condos and co-ops, at a seasonally adjusted annual rate of 450,000 in March, were flat with February and down 29% year-over-year.

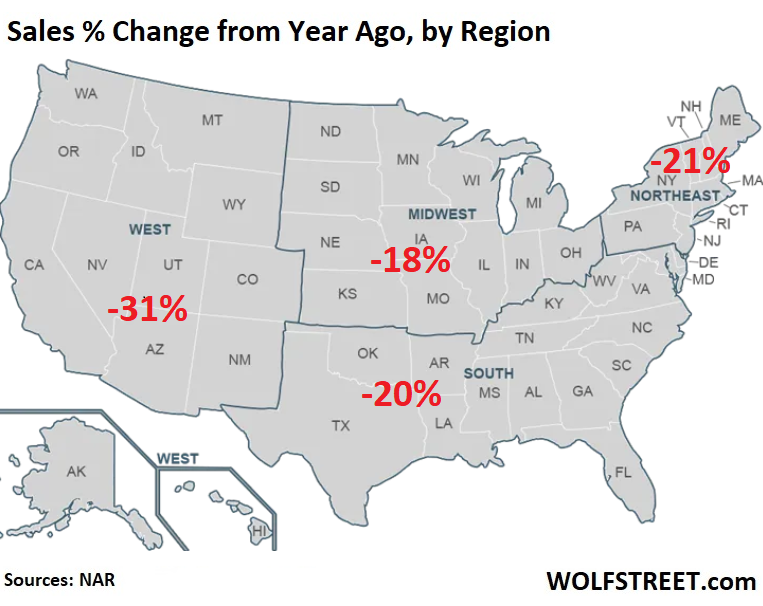

By region, year-over-year sales plunged in all regions (percent change from year ago, map via NAR):

Sales to all-cash buyers – often investors and second home buyers – plunged 24% year-over-year to 96,000 properties in March, from 127,000 properties in March 2022.

Median days on the market lengthened. Homes that actually sold spent 29 days on the market in March, up from 17 days in March last year, according to the National Association of Realtors.

Another measure of median days on the market also lengthened: Homes were either sold or were pulled off the market after 54 days in March, up from 36 days a year ago, according to realtor.com.

Months’ supply, at 2.6 months, was up from 1.9 months a year ago, but remained low by historical standards.

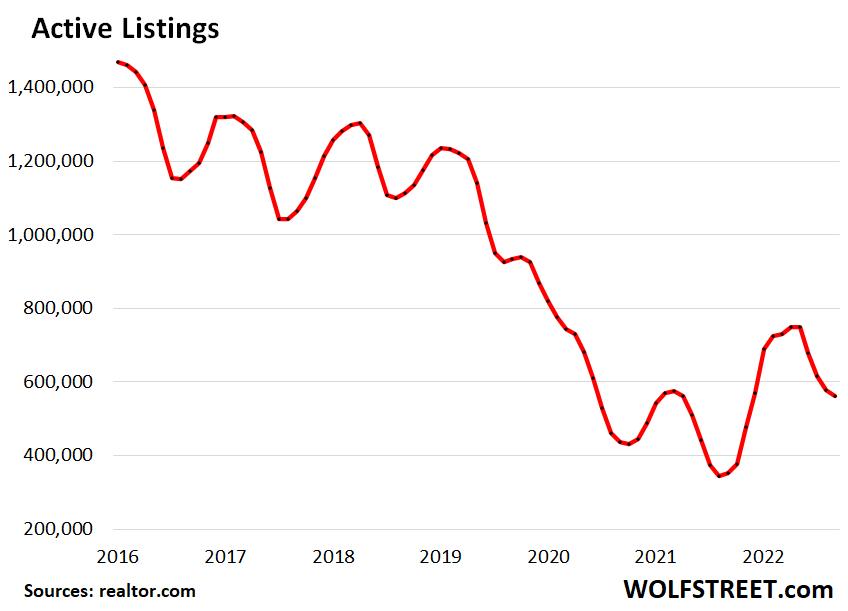

Active listings (= total listed inventory minus properties with pending sales), at 563,000 properties, were up by 60% from a year ago. The first three months of the year are usually the low points for active listings, and if historical patterns play out, they will rise from here.

But active listings remained low by historical standards as potential sellers are still trying to outwait the increase in mortgage rates, and as potential buyers have pulled back, and the market – as depicted by the dismal sales despite lower prices – remains partially frozen (data via realtor.com):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow! Cash buyers are even pulling back.

Cash buyers ain’t stupid. They know that higher mortgage rates mean they should get a better price, cash or not.

Why catch a falling knife?

Everyone is saying 5.25-5.50 terminal Fed rate ……. The flood of money printing to inflate this asset bubble is not gone and will continue to fuel inflation. Big surprise coming to the markets when inflation spikes back up.

Right. Why would cash buyers make a move after prices have been bid up by noncash buyers? You’d be dumb as a doorknob.

Best to wait till there is blood in the streets.

Good. I hope yall flippers sink. You’ve had your day in the sun. Time for homes to become affordable again. Sick and tired of people putting makup on an ex army barracks from world war two and selling it for a half million. Yall need to get your minds right, and the debts under control. Greedy jumped up little $#/>$.

When rates were around 2-3% everyone said buy now because these are historic lows and this will never happen again! And then when they went up to 4% plus, everyone started running around like indignant chickens screaming that rates are so high and have to come back down. Social media and the internet have fried our brains.

Oops, wasn’t meant as a reply!

A “cash buyer” who is an investor can get a 5 year Treasury at 3.5% with zero risk and zero carrying cost. But “cash buyers” are actually for the most part not “cash” they are borrowing without a mortgage and the rate on that money has risen substantially, reducing the ROI on real estate. Rents are beginning to fall as a glut of new rental inventory hits the market and smart investors, those who can borrow most cheaply see this.

A single month vacancy eats 8.25% of your income plus get ready costs of approximately 2 months of income ,16.5% ,and suddenly that investment property is a money pit. A wise man once said “he who panics first, panics best”

This is very accurate.

I was formerly invested in a REIT that was taking my (and all the other investor’s) cash and buying entire neighborhoods of houses for 30% over the already inflated list price. Then they were immediately turning around and taking out variable interest rate loans from a major investment bank and refinancing the property on a loan at 50% LTV.

They had plenty of cash, but I guess that wasn’t enough! They explained that this strategy of refinancing was to “enhance” returns (didn’t mention anything about “enhancing” downside risk of course).

I realized that if the houses in the REIT are simply revalued to *current* market price on paper, I would take a 50% loss. If house market prices go down by 25%, which is still higher than 2020 levels, I would take 100% loss. Pulled most of my money out and very glad I was able to escape before the inevitable redemption gating begins.

I imagine this REIT is not the only fund that has done this, as I would imagine many copy each other’s strategies. But after witnessing this, it would seem that a doomsday is looming on the horizon.

I don’t think they were all cash buyers? It could be bought with “cash” on leverage

That’s a really good point. Likely a lot of “cash” buyers weren’t actually cash buyers.

Plus, a lot of cash was coming from home sales in HCOL areas and stock sales, both of which aren’t too hot right now.

Back ~ 3 years ago when HELOC was ~ 3%, just max out and pull out the equity in the house to be sold before putting it on the market.

REITs often buy with cash using borrowed money.

Then there are people moving from one state to another who sell house to get cash and then buy house with this cash.

I rent a home for sale outside Austin TX which was just listed for sale. I am moving and have witnessed the slowdown. The number of people looking is minuscule yet the realtor / homeowner told me it would be sold overnight. They’ve had 3 viewings. IMO it’s a $375,000 house listed for 468,000. The people looking don’t even check out the yard or upstairs. All the new rentals I’ve looked at have had reduced prices or have been stubbornly sitting for 1-2 months. I’m updated via email on price changes and it’s frequent.

Owners are very delusional as always and will find out the hard way it’s getting harder to find willing and able parties set to overpay in this new housing bubble bust 2.0. Anybody who doubts this is insane. Especially with the new law making mortgage rates higher for those of us with high credit to subsidize those who have bad credit.

Buyers have been over paying in Austin for 20 years now. Why would they stop no?

Because all those cushy tech jobs have disappeared and all those h1bs can’t get another job to stay in their overpriced houses. Tech salaries have also taken a hit in the last few months.

Maybe, but I haven’t noticed it. (Yet.) My outfits still hiring.

Austin has been in a lardy overpriced/over-speculated frenzy since at least 2006; maybe before. You go to dinner or for a pint Ave you are are bound to overhear someone talking about real estate. Too many of the interesting people have been squeezed out by the yuppies & the climbers. It is a shame.

The West shows the largest drop (-31%): this is where the tech boom really mattered. Fear is finally setting in after the latest layoffs with Disney and Meta, and many workers are postponing home purchases due to fear of layoffs. Read Team Blind and LinkedIn stories: hundreds of resumes sent out and no calls or interviews.

The stalemate is incredible though: many homeowners want even more for their homes than during the peak and deny any correction has taken place. The entire stock, Crypto, and housing markets now hang on the belief in the imminent Fed Pivot.

We shall see if Jerome caves in once again. If he does not, kiss housing and asset bubbles goodbye. If he does, kiss the dollar goodbye.

I think the housing data will be uglier once the debt ceiling is raised, and the avalanche of new treasuries flood the market and raise the rates.

Yes. Asking prices remain high even here in flyover land. Some additional price cut activity along the way but overall prices still very inflated and inventory is paltry. The decent properties are still selling quickly – but only because there are so few of them.

I think the resiliency of the job market has caught Powell off guard. So I don’t see a “cave” this year.

Obviously, the Federal Reserve has ZERO INTENTION TO ‘PIVOT’ and will continue to increase the Federal Funds Rate to at least 5.25%.

If Grand Jay stays on course and the Pivot narrative finally suffocates this would absolutely be top10 anime betrayals ever. I’m living outside of the States and even here my head has had been hurting from people believing in eternal inflation and low rates for years now.

Several in my circle are ditching 3% mortgages, and moving up 1.5x from what their current place sells for at 6%+. 2x their monthly payment (at today’s prices) and 3x+ what they’re actually paying from when they bought a few years ago. Asking prices are a bit lower here but houses are still getting 10+ offers.

The psychology of “they could afford that? I wonder what we could afford…” is real and drives people back into the market even if monthly costs are tulipmania. I think it’ll take a lot to break it.

Agreed.

I feel like the only way to break it is to literally break the consumer with job losses…?

You have to give it to these people of holding on to never ending optimism/hopium or whatever you will call it.

The only reason you would do something like that is to basically think rainy days will never come or if it does they will bounce right back up..

Hopium is a helluva drug

How much of it is to appease the wife unit?

I’d say 80%+

The Fed will have to destroy the housing market in order to save it 🤣

Prices in my area, Woodstock GA – 30188, appear to be very resilient. Still waiting for the real crash beyond just transactions. So far, it’s been mostly a nothingburger outside of 8-10 major markets.

Extremely pleased to see 30YFRM moving higher, 6.67% as of today per MND.

According to redfin- 30188 has a 52k population and yet 189 properties active with almost 100 at 90+ days?

Median sale price is down 40k since the top of 2022.

Compare that to my old neck of the woods 80439

Less than 25k population, 90 properties sitting forever and median price topped in 2022 at 1M, and is now down to the mid 800s.

It’s a slow moving train most people won’t see it until it’s too late.

The trains light is on,and the whistle is blowing ..But still many will be run over,at least they can camp below the bridges

Definitely good news and as always contrary to what MSM is trying to still sell the FOMO crowds on…oh the market has turned around because interest rates is starting to dip and we are at a soft landing…blah blah…

In my neck of SoCal, watching the comps there has been a bump up in closed prices this Spring but not so much as to hit the peak Spring ’22 levels. I’m forecasting the price declines will resume in late summer through the end of the year, although it won’t be steep. I don’t think the jury comes in on where the trough ends up anytime soon. Maybe 2026-27ish.

What effect is the fee to be charged to home buyers with credit scores of 680 or higher that goes into effect on May 1 expected to have on sales to buyers with scores above that figure? This fee on top of the higher mortgage interest rates could convince people that this isn’t the time to buy.

Loan-Level Price Adjustment Matrix you can look it up.

If you take the average good creditor at 740 and 400k at 6% and keep to a a 15 – 20% down, around $40 a month more give or take $10 bucks.

The effect will range from very little to nothing.

Read the tables yourself and you’ll wonder why you gave any credence to the alarmist article you read in the New York Post or the Moonie Times.

“Alarmist article”

Its not about the amount, its about the principle: interest rate is the price of risk, and this yet another attempt to manipulate it.

The question I was answering wasn’t about the “principle [sic].” It was about the likely effect on sales. The answer, again, is either zero or close to zero.

In the context, MM used “principle” correctly.

Principal = school administrator

Why are buyers with good credit scores being penalized?

It “levels the playing field” because working hard and paying your bills might allow you to improve your life for you and your family. You should feel bad about doing anything like that. If you don’t feel bad about it, this should correct your selfish thinking.

Its a conspiracy!

Lucca,

They’re not. You fell for Swimmer’s nonsense. Read my explanation below and click on the link and look at the tables.

Swimmer and other here:

Did you people fall for some political hoax? Quit reading the NY Post!!! You’re spreading ridiculous misinformation.

Read the actual source and tables (linked below):

Low credit-score borrowers always had MUCH HIGHER loan-level price adjustments (LLPA) than high credit score borrowers. That continues. The changes only reduce the gap between them.

Example, with the LLPA changes included:

FICO over 780 and LTV of 90%: LLPA = 0.25%

FICO below 639 and LTV over 90%: LLP = 2.625%

After the changes, these low-FICO score borrowers still pay 10 times the rate that high-FICO score borrower pay.

Look at the figgin tables:

https://singlefamily.fanniemae.com/media/9391/display

Wolf, I don’t see how it’s misinformation. Even if the rates are still far apart, it seems to still be true that this administration has chosen to raise fees on folks with higher credit scores specifically to reduce fees on folks with lower credit scores. Some may think this is a fair change. But I don’t think it’s unreasonable for others to say they don’t like the change and think it’s yet more social engineering to benefit the administration’s favored groups.

Loan-level price adjustment (LLPA): Risk-based pricing adjustments that vary based on credit score, loan-to- value ratio, type of product, and various other factors, charged at the time of origination.

What is LLPA on a mortgage loan?

Loan Level Price Adjustments (LLPAs) were introduced by Freddie Mac and Fannie Mae almost 15 years ago. They have been around so long they are de rigueur; all mortgage lenders factor LLPAs into mortgage rates every day. LLPAs are fees charged by lenders to borrowers to compensate for risks associated with the loan.

Loan-level pricing adjustments (LLPA) are not new. They were introduced into conventional mortgage lending in April 2008. The loan-to-value ratio is a measure of risk used by lenders when deciding how large of a loan to approve. For a home mortgage, the maximum loan-to-value ratio is typically 80%.

Yeah, I’d like some clarification too. I looked at Wolf’s link, and it does appear that the riskier buyers pay more, as he indicated.

But, does that mean it’s a hoax that the average loan for the person with good credit will not pay about $40/mo more? Did the Post make that up out of whole cloth?

I have no idea. Just asking.

I may give a random panhandler a dollar a day, but not a government stooge.

I hear Thailand is nice

How are they raising fees on one buyer to fund another? If you put down 25% and have stellar credit, the additional cost is 0.0%. So what if all the higher risk stuff is shifting around? Isn’t that what actuaries are for? To figure out the right risk-to-fee numbers so the US taxpayer doesn’t have to eat it for your recklessness?

Wolf’s counter doesn’t hold to me. He simply says (links) the statement that people with bad credit pay more. That’s here a non-sequitor to the actual issue.

That the low credit will pay more with or without the change is not the debate. The difference is now the good credit will pay more and the bad credit will pay “a little less more.” Yes I’ll give him that.

Still in usual terms the bad credit may not pay that higher rate when it defaults. Thats risk. But that good credit theoretically will reliably pay thier higher rate. So it’s on the face at least a decline in exposure for the financials.

Yet to me the rub is that all this asumes the low credit is even given that chance to pay more and maybe mess up. There are not a lot of buyers able to pay those low credit monthlies.

So from my viewpoint what’s really going on is Fannie is making it so that it gets a more reliable cash flow no matter what happens.

If the bad credit acts badly they at least are now securly getting some extra fees from the good credit. And more likely, under the guise of helping low credit borrowers the bank is just charging more to good credit because it simply can.

Because in reality NOTHING in this says they have to even give out the risky low credit loans.

I mean I don’t think they give out many of those low credit loans. That’s a killer payment for a guy with bad credit from being poor.

All they are saying is IF they ever originated such loans from their great magnaminity to a person who can pay way more than the rest of us… they would charge them a little less now.

So (of course) they now will need to charge the rest of you more to cover that potential outcome.

How many loans are below this threashold versus above it? And what’s the actual cash difference.

1. People with high FICO scores — investors — were big defaulters during the mortgage crisis (they just walked from their multiple investment properties), and insurance rates were woefully off. In other words, high-risk borrowers had subsidized the low-risk borrowers.

2. Your car insurance works the same way. High risk drivers pay more than low risk drivers. And so if the insurance company sees after looking at the accident data that it overcharged the high-risk driver and under-charged the low-risk drivers, it will adjust the rates, and you won’t even notice. All you know is that your rate went up. Until then, the high-risk drivers had subsidized your insurance rate.

The freeze is real. As a credit union mortgage lender, I have not been this slow in a spring market since I got into the business 11 years ago. It’s brutal out there.

Hmmm….do you know of any peers who lived through 2008/2009?

Was gonna say the same thing. 2005 to 2012.

Gabriel I do, I am not saying that the current market is as rough as the post crash meltdown. Just commenting that it is definitely the worst of my 10, almost 11 years in the business. It’s like a neutron bomb went off.

3 of my friends in the mortgage biz. Deader than a doornail. You would never know it watching them still spending money hand over fist. Skiing in Aspen. Family trip to the Big Island. Theatre, concerts, dinners out. It’s amazing to watch.

Falcon I know of plenty like that as well. I can tell you that there a fair amount of us who are also battening down the hatches and preparing for this down period to last for some time. I have cut spending wherever I can and am actually looking at possible avenues out of this business. I know i am not the only one.

That said, no sympathy for my peers who are living large. eventually the piper comes calling.

Youre not alone. As a used truck dealer, I have not seen this dead a spring since I started this business 20 years ago. Worse than last recession already.

There are still pocket of insanity (stupidity?) out there.

My wife and I have been looking for retirement property for 5 years. We finally found a place. It was down 25% from the original listing. We offered 75% in cash. After the haggling, we ended up at 80%.

On the day we made our 80% offer official, the seller got a cash offer for full price. We declined to participate in a bidding war.

Who are these people still offering full price cash? They could have outbid us and saved themselves hundreds of thousands of dollars.

Southern California is one of those pockets of insanity/stupidity. Inventory is so ridiculously low that any halfway-desirable properties still draw FOMO idiots knocking each other over for an opportunity to overpay.

You did the right thing. You’ll eventually find something you like even better, and a nutball won’t swoop in. Patience is golden.

People who are wining today in bidding war would be loser in next year or so. Similarly, people who won bidding war in 2021 and 2022 are losers now.

the agent probably called one of their investor buddies after you made the offer

Maybe an arrogant person worth $50M ?

Over 8% of Americans are millionaires, not sure what percent are over $20M.

Too many as far as I’m concerned but I’m not about to pull a Sanders/Warren and demonize all of them. Yawn.

Hopefully those worth $20M and above did something that benefitted society. I dont have any problem with people being rich unless they got that way w/o doing something(s) useful.

Of course value is somewhat in the eye of the beholder. I value AI researchers, good musicians, good comedians.

Theater, opera and 90% of visual arts not so much (Escher excluded).

I also don’t value countries that allow investors to buy up huge amounts of real estate while rents simultaneously go up quite fast.

Does that mean I believe in government regulation ? Yes if it seems necessary to achieve certain objectives. If those objectives can be met w/o govt. regulation so much the better.

Let’s compare the %age of American citizens who could afford buying a home:

60s/70s approximately 70% of adult citizens could afford homes, largely because most of them held good paying, full time jobs

2021-23: only 48% of adult citizens can afford buying a home. Part-time, low wage jobs with huge costs of auto/home loans; Insurance, Energy, Tech costs; Health Care, Rising Bank rates that all add up to the woes for multiple millions of citizens.

Rubicon

Not sure where you got your stats, but a 22% drop in those who can afford to buy a house vs 60 years ago does not sound that bad, especially when renting has become more preferable in the past 20+ years.

70% to 48%? Mathematically that’s actually closer to a 1/3 drop in the # of people who can afford at these prices. That’s pretty significant.

Most housing related sites i read or listen to (Utubers) spend very very little time discussing apartment related matters.

Thirty five percent rent… did a very brief internet search but was unsuccessful determining how many are apartment vs.

SFH/duplex/townhome rentals.

That said… 35% total and yet discussion of apartment related concerns is almost trivial (< 5%). This is unfortunate.

How To Lie With Statistics, a great book. Easy application here….”Sure, prices are flat vs a year ago, but prices are UP this month. The long awaited bottom in housing is now behind us, and a healthy upward trend can continue.”

Signed, Your Friend,

Lawrence Yun

You gotta give it to Lawrence…if they make a part 2 of that movie Thank you for smoking, they should include him as part of that lobbying squad and propaganists characters.

3 out of 4 houses for sale in my hood are under contract.

Wow, people in your hood are dumping that many homes? Do they know something we don’t?

Why you make fun of people? what he meant was %75 of homes are under contract. Same as my area, north Los Angeles

Now , don’t get me wrong, seasonally, there were condos and houses that was sitting for months during the winter. But now we are approaching the buy and sell season, so a lot of homes are now selling fast and even with 2-4 percent overt asking. Hope its just short term and home will adjust more, since they are still very unaffordable.

Crazy, but about 12 of the 24 home builders that on public stock markets are very close or may be breaking above all time highs this past week .

NVR, DHI, SKY, PHM, TMHC, TPH, UHG, CVCO, GRBK, LEN, IBP. Most of these are up 100% from the lows of last year.

It’s truly insane. In 2008 I started loading up on long-term puts of home builders, which panned out very well. This smells like another opportunity.

Wolf, can you please address the southeast and particularly Atlanta? Prices here are still going up, especially in the affluent northern suburbs. We keep hoping for some relief but none so far. Our prices are still low compared to the west coast or the northeast, but prices for something nice & move-in ready has almost doubled over the past 3 yrs, and now our spring market has very little for sale resulting in high prices for the few available. Our adult daughter is trying to buy and she just keeps watching the prices continue to go up. Wolf, if you can provide any insight on this market, that would be very appreciated.

Old Northeasterners have been moving to the sunshine states for years.

A lot of times they hate it and leaves a couple years later. Sometimes they stay.

With more Boomers retiring, this trend will probably continue.

It’s a bit crap for workers too. Look a Florida. COLA and median wages are low and yet tons of pricey real estate and money from pensions.

Start a gardening company, become an Estate Attorney, Wealth Manager or open a nursing home. Any business that services wealthy old people will prob do well for the next 10 years :P

The numbers are going to remain small for a long time as people who refinanced or bought the previous few years at rock bottom rates can’t or don’t want to move and have a much higher payment. The reason home builders are up is because the market recognizes that existing sales are going to struggle and people will be forced to buy newly built homes. Many of the home builders have maintained prices by providing incentives or buying down the loan rate.

Yeah it’s Principle, Interest, Taxes (PIT). I is deadly and P has to pay for it. T doesn’t matter much except in NJ, IL, CA. We’ll see if P pays the piper but sellers need to wake up, maybe get cut in half I’d reckon. FED to the rescue like the stock market?

Moi ,T always matter ,there progressive and brutal ,

Starting 5/1. People with good credit and 20% down payment will have to pay more to subsidize high risk borrowers? Is this even legal?

LMAO. LLPA payment tables were changed slightly, and the whole internet is losing its composure because of a few overblown articles in tabloid newspapers trying to make political hay from it.

“Experts believe that borrowers with a credit score of about 680 would pay around $40 more per month on a $400,000 mortgage under rules from the Federal Housing Finance Agency that go into effect May 1, costs that will help subsidize people with lower credit ratings also looking for a mortgage, according to a Washington Times report Tuesday. ”

If this is true, that would be an extra $480/year and $14,400 for 30 years that you have to pay. Crazy

cookie,

Did you people fall for some political hoax? Quit reading the NY Post!!! You’re spreading ridiculous misinformation.

Read the actual source and tables (linked below):

Low credit-score borrowers always had MUCH HIGHER loan-level price adjustments (LLPA) than high credit score borrowers. That continues. The changes only reduce the gap between them.

Example, with the LLPA changes included:

FICO over 780 and LTV of 90%: LLPA = 0.25%

FICO below 639 and LTV of 90%: LLP = 2.625%

After the changes, these low-FICO score borrowers still pay 10 times the rate that high-FICO score borrower pay.

Look at the figgin tables:

https://singlefamily.fanniemae.com/media/9391/display

Guilty myself of falling for that. Based on what you posted it looks like a storm in a teacup.

Wolf,

What’s the misinformation?

Read my comment.

It is crazy times (even out here in podunk America…pacific northwest). An undeveloped property near me (remote, no timber, no power and NO WATER RIGHTS) was bought at a tax sale last December by a realtor for $95K and just sold for $175K (on market for 1 week). How does that pencil out with a construction loan, solar power, and required water collection/treatment system installation? And it’s far enough out they would have to work remotely (if not retired). That’s a chunk of cash if it’s just a weekend camp site. Now I’m waiting for my property assessment to get jacked some more (already went up ~20% this year). Still wishfully hoping for a return to sanity.

We need suckers for price discovery. If all sales freeze, there can not be price discovery

People pick them up “for retirement.”

My brother bought one and assures me utilities will be to his lot by the time he retires in 10-15 years.

It’s aspirational buying tbh. Who needs numbers?

A relative inherited a lot in Nevada that his parents never retired too (and still in the middle of nowhere 30 years later)

in markets, volume is always the confirmation of price action.

The real estate market is extremely illiquid sale prices may be moving down, but so is the volume traded.

not until the damage in the commercial real estate sector spills into and tips over the pyramided real estate games in the residential sector will we see true price discovery.

IMO

How does the commercial real estate sector effect the residential sector?

It doesn’t

You sure about that?

The lenders, borrowers, and speculators are all tied together.

In my zip code, median house price is down 37% YOY but prices are down only 5% (if at all). That’s because there’s very few sales except at the low end so median house price change reflects sales mix, not price change.

“very few sale” …

and to my point, low volume tends to lessen the importance of any price point. Volume confirms price action.

Good point.

As home sales fall, it makes it harder to determine price discovery of the true value of a house. Low volume sales can distort the actual value. It may be too high or too low.

The media value of houses in my city are 290k, but the average new listing is 620k. That is because 80% of all new listings are new construction. Out of the 325 homes for sale, 275 are new construction. Normally it would be 25% of all homes new listing sale is new construction.

This is distorting prices IMHO

Very good post.

Distinction between existing home sales (only), new home sales (only), or both should be made more often. Especially whether new construction is being included or not (to your point).

And whether its SFH only or SFH+duplex+townhome.

I thought Wolf (or someone else i read) indicated that Case-Shiller does its best to adjust for housing mix effects. Am I correct on this ?

By the way a Utuber (RJ Talks) stated that Freddie Mac has a home price mechanism that is more up to date than Case-Shiller and whose graph very closely tracks it. He showed a chart in which both CS and Freddie Mac graphs were displayed and the differences seemed quite small. I forget how many years they went back.

Can anyone corroborate the FM should closely approximate CS in general ?

Its Freddie Mac House Price Index (FMHPI).

The Freddie Max Home Price Index has one HUGE issue: it’s based on mortgages. So when the buyer pays cash and doesn’t use a mortgage to buy the home (28%), that home is not included in the index. There is a systematic difference (not random) between buyers who pay cash, and buyers who use a mortgage. So the index is skewed by the absence of cash deals.

Wolf,

Good to know, I suppose that might have been obvious to some others here. Still, its interesting that the graphs seemed to approximate each quite well in his presentation.

Maybe there is more difference than met my eye although the Utuber

(RJ Talks) made a point of their similarity.

Since you say the difference is systematic, if it’s variability is small enough, one clearly could use it as an adjustment to very closely approximate Case-Shiller.

FMHPI + adjustment = Case Shiller

But maybe the variability is more than is desired by the experts… resultant inaccuracy outweighs the benefit of more recent price update (?)

In any case, thank you for the insight.

Everyone agrees Rez real estate is slow moving and localized, and comments reflect pockets of no slow down etc. WOLF’s articles every month or so touch on national trends, which are in fact sloooow moving.

I think we’re not giving the average homebuyer AND seller enough credit. The current stalemate might just neutralize the big “bust” that is manifesting like a pinhole leak (down 1.4% YOY). Even if this pace TRIPLES over the next 3 years, the median is down maybe 12-15% from all time highs ? That’s not even a reversion back to the 2019 trend line.

Buyers and Sellers learned something from the GFC which was housing-based. No harm in treading softly from either side.

Look at the slope of the case shiller plots. Wolf provided them recently. That will tell you what’s going on. The YOY numbers are confusing at best

Low inventory is a good point . The sales percentage down are not a function of price but affordability at current prices and with inventory low those folks with the shadow inventory have not elected to sell . This process clearly takes more than a year when QT started.

BS ini

I agree this will take awhile – but I believe when this all stabilizes (sometime between 2024 and 2027), we will see more of a flat-to-down trend, which started in 2022, and the rise will start again. Compared to 2008-2012, median pricing will look like backing out of your driveway as opposed to riding down the double diamond ski slope. It will frustrate real estate haters and lots of SFH rental investors who were seeking the crash, but overall, prolly a good thing.

The only metric worth a hill o beans is case shiller. The rate of decline is amazing. Forget about the other nonsense from NAR, black knight, etc.

Month over month is the only number to watch from here on out in this housing Correction/ Crash.

I am selling a bridge right now. I know this is a little unusual but it is a really good deal. Is anyone interested in buying it from me? I will give you a good price.

Opendoor just laid off 22% of their workforce which amounted to around 560 employees. The firm ended 2022 with 12 thousand plus homes in its inventory.

AI is very good at overpaying for homes and buying them sight-unseen.

AI hasn’t figured out that it’s hard to sell homes profitably after you overpay for them.

AI = Artificial Idiocy.

Are you sure you don’t mean GI?

AI is very good at making management rich and investors poor. AI has done its job.

The media has started calling lots of software AI. AI has ALWAYS included many areas of advanced software. I already posted about that many months ago.

But AI = Artificial Idiocy ?

Its so smart it has you fooled. The field that is, not necessarily any one piece of software that could be over hyped.

AI research probably encompasses the smartest people on the planet.

Physicists and others can disagree… I’ll stand by my statement w/o any support.

But of course not all AI research, products have been successful.

Its been over 25 years since AI defeated the best chess master, no small feat. It gets played down and some AI researchers would claim its not really AI. Just sophisticated software. Not for me to argue that one. I dont follow its advances but safe to assume its somewhat more advanced than what the average person knows it can do.

Read about Doug Lenat sometime. Interesting AI researcher, been around a long time now.

“Some people get rich studying artificial intelligence. Me, I make money studying natural stupidity.”

– Carl Icahn

Homeowners may be hoping for a return of 2021-22 prices, but builders seem to be more realistic.

I signed a contract on a house in New Braunfels, TX last week. New construction home built to order, but buyer couldn’t close. Builder listed the unit, then lowered the price. When I went to see the property, I was ready to make an offer, but before I could open my mouth, the builder’s agent lowered the price (again) to within $500 of what I was going to offer. Agreed to a price $5,000 below that (about 25% below comparable pre-owned home listings in the area).

There is a lot of land out there and builders can make money at a discount from today’s prices. This is what will break the back of the market.

Probably the best way to go — just bloody build.

The flash flooding and the drought issues always gave me me pause about that area— same with Dripping Springs. Otherwise, I think NB is a pretty damn’d nice spot to land.

You obviously don’t mind 90 degree days… like about 120 of them or even 100 degree days (50,of them). Its all there at accuweather, just choose the month tab and go to 2022 summer months !

Eleven years in Dallas… blood thinned I’m sure… but body/mind never quite could accept so much hot (and humid, spring early summer) weather.

As I’ve mentioned before, I live in a booming rural red area in the South that hasn’t been able to build client-funded custom homes fast enough since 2017. Spec homes are usually 1% of sales but non-existent in 2023. I recently built a home on the lake here and listed my old home a few weeks ago.

My old home was under contract within two hours and closed for cash in two weeks. It would have closed in just over a week, but we had a catamaran trip in the BVI we weren’t giving up. I purchased this home in 2015 and doubled my money. Homes selling in the $700-$950K range appear to be selling for 5-7% off the 2021 peak.

I probably left $20K NET on the table, but I had a local person paying cash that paid for all of his inspections and all the closing costs himself, so I didn’t want to look a gift horse in the mouth in this financial environment. My home was in ready-to-sell condition and needed nothing.

Had this been someone from California or a NY/NJ “halfback,” I would have squeezed it for every nickel.

The joys of inflation. LOL House doubling in price in 8 years.

Meanwhile, they’re probably the same people who were hollering all over about the price of eggs….

Hey, don’t worry about tanking values, or even tanking sales, the Govt has arrived to help!!

“Starting May 1, Americans purchasing a new home or are refinancing their existing mortgages will have to pay higher mortgage rates and monthly fees if they have a higher credit score, The Washington Times reported on April 18.”

Remember the last time the Gov’t stepped in and supported massive numbers of unqualified buyers for mortgages they couldn’t afford to pay? THAT went well didn’t it.

You are probably the fourth person to post this story. While the fees were adjusted, they are only for risky high loan to value borrowers. And the poor credit folks stillo pay 10 times more the the good credit borrowers. Why don’t you stop reading Moony newspapers like the Washington Times? Read Wolf’s prior replies. Garbage in, garbage out.

The right wing messaging machine is strong. Rewording a change in how the loan level price adjustments on mortgages into a punishment for the “good people”. It’s brilliant PR.

Google puts 70 acre campus on hold. This mega project in San Jose was signed in 2021, bad timing, and was estimated to have had 17 billion in economic impact. To get approvals thru the NIMBY guys, G either agreed or was shaken down for all kinds of park land, affordable condos, etc. G has severed ties with the big RE outfit hired to manage all this and gone instead with a cost cutting ‘bean counter’ type. The site is idle.

Just saw this on CNBC. Reminds me a bit of WeWork although of course there is real co here.

The big guys seem to smell the coffee while the little guys are still at the punch bowl.

Read a comment on another website, Google is instituting a lot of cost-cutting internally. I think it’s not doing so well.

What has Google done for the consumer in the past 20 years? Everything has been bought and monetized, crapified, or they throw out eventually.