Even in Miami and Tampa, prices down for 5th month in a row.

By Wolf Richter for WOLF STREET.

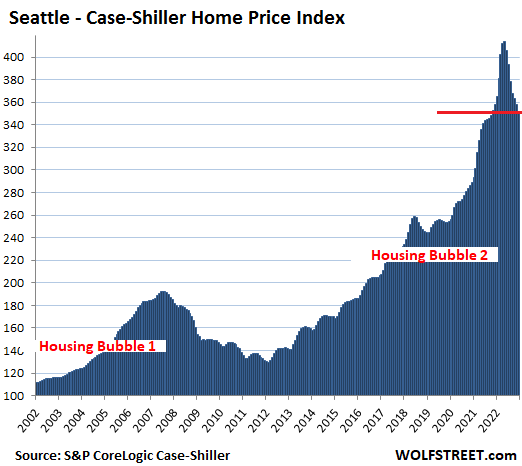

Just for a foretaste, Housing Bubble 2 in Seattle:

Housing Bubble 2 is deflating relentlessly, not under the pressure of an unemployment crisis – far from it: the labor market is still historically tight with the highest pay increases in four decades, and an increase in unemployment would be the next shoe to drop on the housing market – but because mortgage rates have reverted to the normal levels of 6% to 7% that existed before the money-printing era started in 2008. And home prices that exploded over the past few years, fueled by mortgage rates of 3% and lower, don’t make sense anymore – and never made sense to begin with.

Today we got the S&P CoreLogic Case-Shiller Home Price Index for “December.” The time span here: a three-month moving average of home sales that were entered into public records in October, November, and December, reflecting deals made largely in September through November.

On a month-to-month basis, today’s Case-Shiller Index for single-family house prices dropped in all 20 metros that it covers. The biggest month-to-month drops, those dropping at least 1.0%, occurred in:

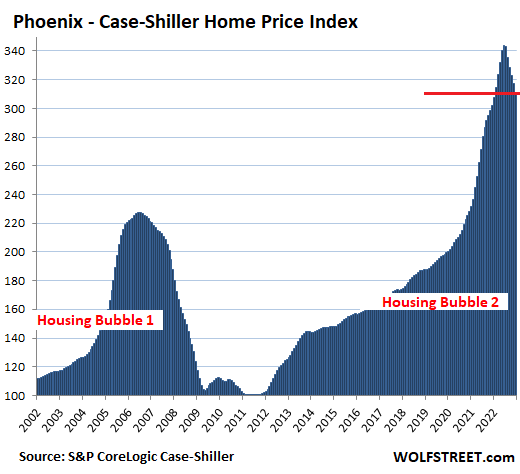

- Phoenix: -1.9% (second month in a row! The babe is moving fast)

- Portland: -1.9%

- Las Vegas: -1.8%

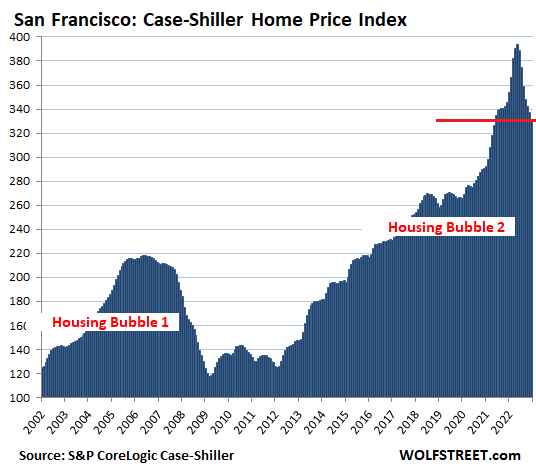

- San Francisco Bay Area: -1.8%

- Seattle: -1.8%

- Denver: -1.3%

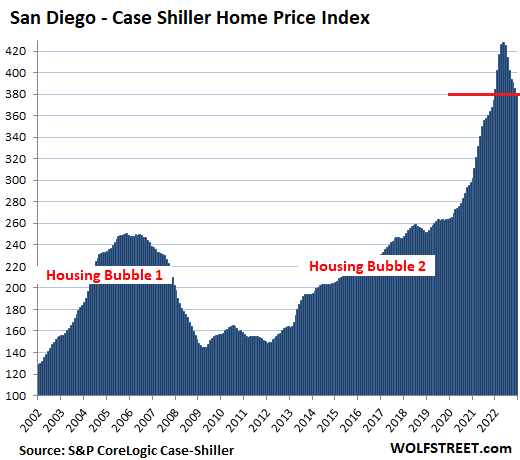

- San Diego: -1.3%

- Chicago: -1.2%

- Minneapolis: -1.2%

- Dallas: -1.1%

- Detroit: -1.1%

- Charlotte: -1.0%

From their respective peaks, which ranged from May to July 2022, house prices dropped the most in these metros:

- San Francisco Bay Area: -16.0%

- Seattle: -15.1%

- San Diego: -11.1%

- Phoenix: -9.4%

- Denver: -7.5%

- Las Vegas: -8.8%

- Los Angeles: -8.1%

- Portland: -7.9%

- Dallas: -7.6%

The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors (methodology). This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices, but it lags months behind.

Median-price indices reflect the price in the middle of all homes that sold that month, and can therefore be skewed by a change in the mix of homes that are sold, which can be an issue when a market undergoes sudden and dramatic changes, such as in 2022. But median price indices are lot more current.

The San Francisco Bay Area is the leader here. The Case-Shiller index for single-family houses has now dropped 16.0% from the peak in May. On a year-over-year basis, the index is down 4.2%.

By comparison, the median price index by the California Association of Realtors for the San Francisco Bay Area – median prices being a lot more current but less reliable – plunged 35% in January from the crazy peak in April.

The Case-Shiller index for the San Francisco Bay Area plunged faster in the seven months since the peak in May (-63 points) than it had spiked in the seven months up through May (+53 points).

The index for “San Francisco” covers five counties of the nine-county San Francisco Bay Area: San Francisco, part of Silicon Valley, part of the East Bay, and part of the North Bay.

- Month over month: -1.8%.

- From the peak in May: -16.0%.

- Year over year: -4.2%.

- Lowest since May 2021.

In the Seattle metro. The chart shown at the intro as foretaste:

- Month over month: -1.8%.

- From the peak in May: -15.1%.

- Year over year: -1.8%.

- Lowest since October 2021.

San Diego metro:

- Month over month: -1.3%.

- From the peak in May: -11.1%.

- Year over year: +1.6%.

- Lowest since December 2021.

Phoenix metro:

- Month over month: -1.9%.

- From the peak in June: -9.4%.

- Year over year: +2.9%

- Lowest since January 2022.

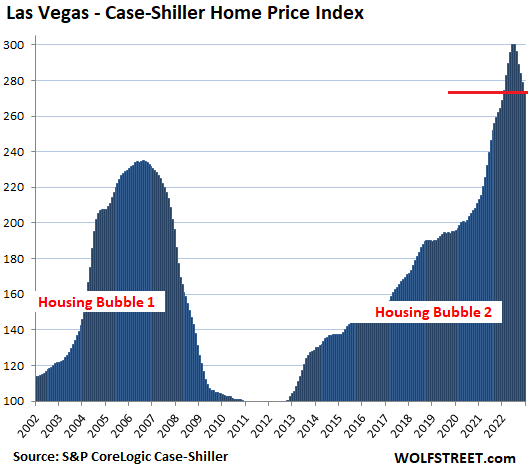

Las Vegas metro:

- Month over month: -1.8%.

- From the peak in July: -8.8%.

- Year over year: +3.6%

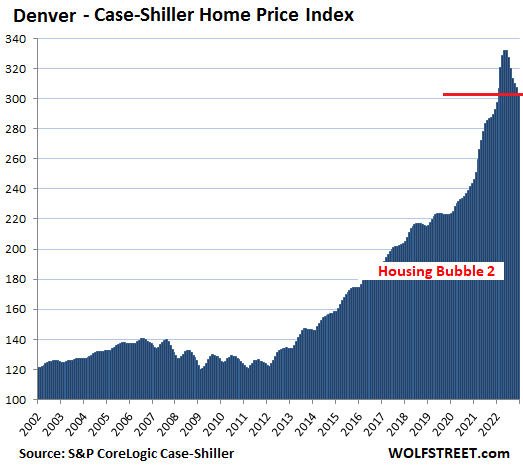

Denver metro:

- Month over month: -1.3%.

- From the peak in May: -8.7%.

- Year over year: +3.5%.

- Lowest since January 2022.

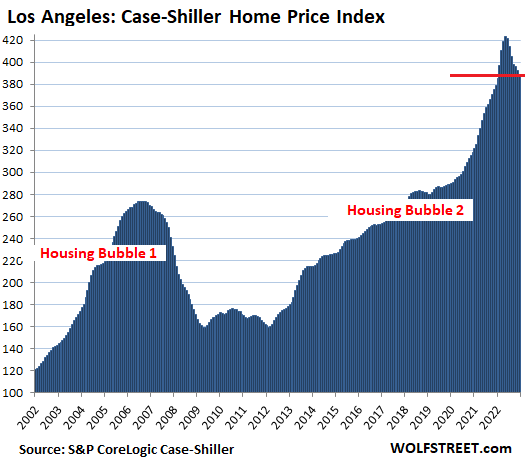

Los Angeles metro:

- Month over month: -0.8%.

- From the peak in May: -8.1%.

- Year over year: +2.7%.

- Lowest since January 2022.

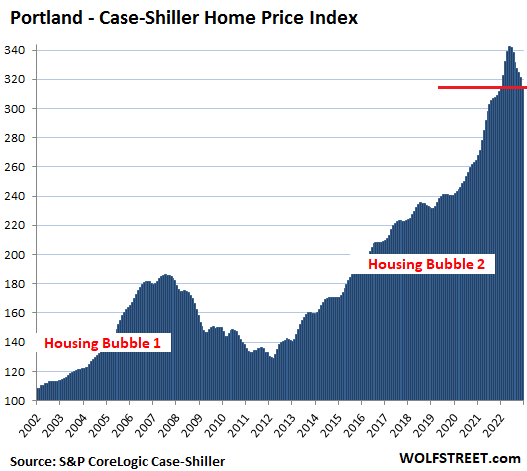

Portland metro:

- Month over month: -1.9%.

- From the peak in May: -7.9%.

- Year over year: +1.1%.

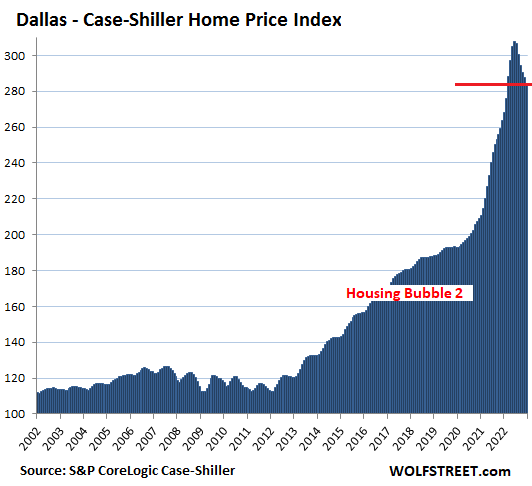

Dallas metro:

- Month over month: -1.1%.

- From the peak in June: -7.6%.

- Year over year: +7.9%

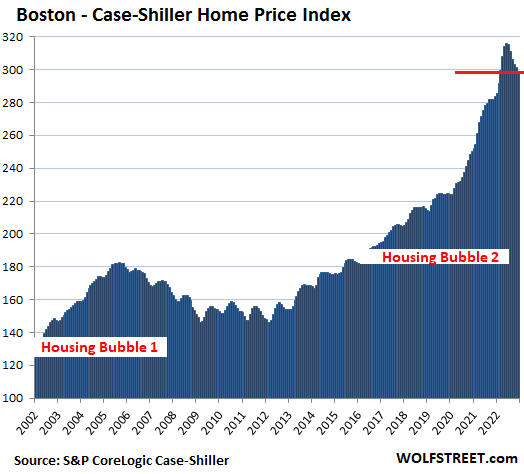

Boston metro:

- Month over month: -0.9%.

- From the peak in June: -5.5%.

- Year over year: +5.2%

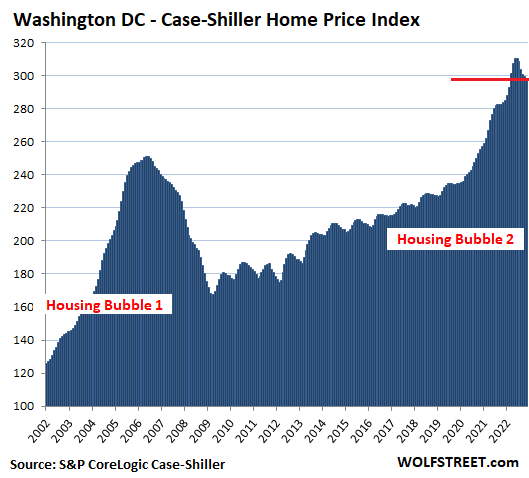

Washington D.C. metro:

- Month over month: -0.4%.

- From the peak in June: -4.3%.

- Year over year: +4.3%

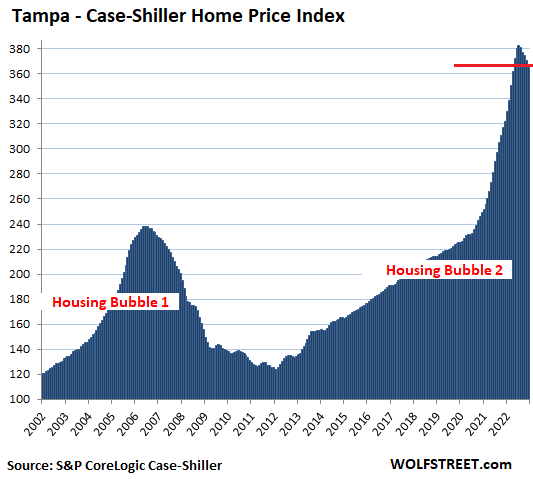

Tampa metro:

- Month over month: -0.9%.

- From peak in July: -4.0%

- Year over year: +13.9%

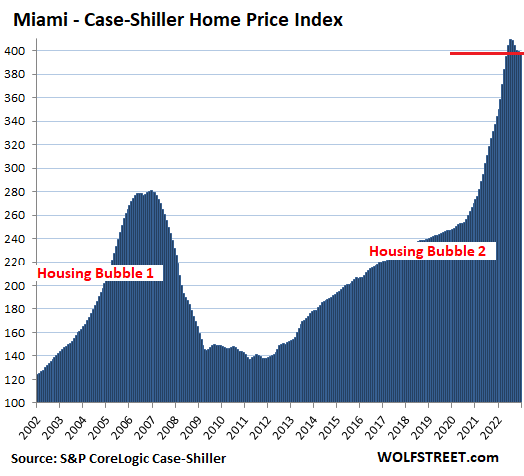

Miami metro:

- Month over month: -0.3%.

- From peak in July: -2.6%

- Year over year: +15.9%

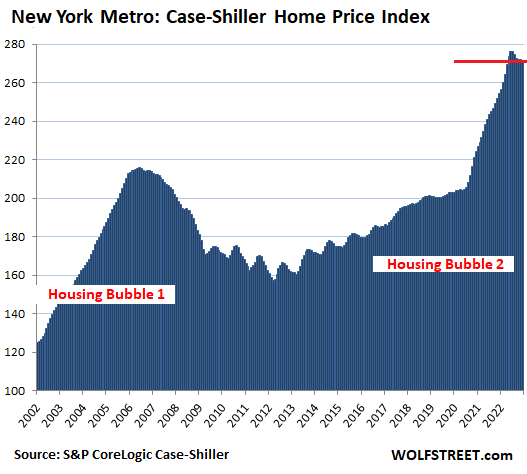

In the New York metro:

- Month over month: -0.2%.

- From peak in July: -1.8%

- Year over year: +6.6%

For the Miami metro in December, the Case-Shiller Index had a value of 399 points. All Case-Shiller indices were set at 100 for the year 2000. This means that Miami house prices are still up 299% since 2000, despite the recent dip. This makes Miami the #1 most Splendid Housing Bubble in terms of price increases since 2000 in the Case-Shiller Index, having surpassed the prior #1s, at different times, Los Angeles and San Diego, in 2022 because their prices dropped faster than prices in Miami.

The New York metro, with an index value of 271 – house price inflation since 2000 of 172% – forms the taillight of this list of the Most Splendid Housing Bubbles.

The remaining six housing markets in the Case Shiller index haven’t risen nearly as much and don’t qualify for this list. All of them have been seeing prices declines over the past few months. In “December” month-to-month: Chicago (-1.2%), Charlotte (-1.0%), Minneapolis (-1.2%), Atlanta (-0.7), Detroit (-1.1%), and Cleveland (-0.8%).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Bot sure if valuation comments are allowed here, but one useful metric to look at these bubbles is house price to rent ratio

I know the Fed uses that and it seems obvious there is serious economic stress occurring.

Hillbilly rocket science indicates housing and rent need to be entirely reset ASAP.

These latest little haircut trims are on the extreme side of being minimal, but, it’ll take several years to return to pricing ranges related to income levels.

It probably makes sense to see three years ahead with about a 30% + drop.

This is a standard feature in my CPI articles:

Per your chart, all they needed to do was stay the heck out of the housing market for good. Things were healing in 2012. Instead, look what QE and government backed mortgages did.

Given that this *century* has seen nothing but home price madness, the greatest service the peanut gallery here could do would be to offer up brief ideas for financial structures (new mortgage forms), that might stop this society destroying roller coaster.

Government, bankers, and home builders won’t do it, they are the authors of the present ruin.

Basically, a mortgage structure is needed that could somehow lend at a *long-term* average of rates – not coke-and-poppers ZIRP, nor gotta-strangle-our-inflation-baby 20%…

It will take a better brain than mine to work out the details, but I think it can be done.

The housing cost insanity has to stop. This roller coaster will ruin the country.

All that’s needed are interest rates above CPI, 20% down, and no government guarantee on mortgages – you know, the way things were before they repealed Glass-Steagall.

cas127 – I have a very simple idea that will stop nearly all housing bubbles in their tracks. Pass a law that the longest term of mortgage possible is 15 years with a minimum 15% or 20% down payment.

The benefit of this law would be that people could pay off their homes and then save for retirement, or people who get a late start on buying a home could still pay off their home in a reasonable time period.

Of course, home prices would adjust downward. And there would be ALOT less interest paid to the lenders over the duration of the home loan.

Another idea is to allow people to put money aside tax-free each year to save for their home down payment. Why? Because with the larger downpayment of 15%-20% it will take them longer to save up a down payment, so the extra tax break would help people to get into a home at a younger age, but since their down payment is larger, they have more real skin in the game on the home. This would cut down on the default rate.

And of course, the other idea is simply to force all mortgage loan originators to keep a financial stake in the mortgages, rather than bundling them and selling them off or passing them off to Fannie/Freddie. That would cut down on the incentives to just put everyone into the maximum loan possible and loan quality would be important for originators.

Per Wolf’s chart, it’s stunning how OER undervalues homes. But, anyone with 1/2 a brain already knows this.

You got this backwards. OER represents RENTS. It doesn’t “undervalue” homes with regards to the CS line. It shows how ridiculously OVERVALUED homes (CS line) have become.

Surely this is about more than your average middle class homeowner. We’re talking about some of the most expensive homes in America skyrocketing in price due to action from the Fed. Now who does that really benefit? I’d imagine some investment firms in tax friendly countries are pretty huge players (and big winners) in this ludacris housing market.

The test will be how quickly and how dramatically the Fed reacts when something blows up. The fact remains that we are in the 3rd housing bubble over the time period of a 30 yr mortgage and it’s turned middle class home ownership into an overpriced carnival game.

Waiting for depression when my grandma got 80 acre farm for 800$ savings account that couldn’t be repaid ,money for land swap,was told good luck .Owned till she passed God bless her best influence in my life

Its pretty clear that the powers that be took centrally planned house prices from being mainly a function of income to a function of interest rates. Once you do that you can not go back to prices based on income without burning things down.

My guess is housing will join the list of things like education and healthcare that starts to get opaque financing and credits. Upper middle class will pay the freight is my guess.

The problem is property taxes they are equal to interest and principle, take the taxes out it’s criminal.

DEPTCH CHARGE: Here here. The only thing worse than letting capitalists bleed us dry is government “assistance”.

CAS127: I think your brain will do just fine. You seem to be a thinking person, and anyway, your brain can’t be any worse than those at the controls.

GAMETV: My eye started twitching at “pass a law”.

The mirror to that chart is the Schiller home index divided by income per capita.

It’s challenging to quantify the economic impact from pandemic and compare this bubble to the GFC, but there has to be a fairly serious drop in current markets, to bring about some normalization or equilibrium.

As you’ve said recently, there’s always willing buyers near fair prices, but at some point, there’s going to be cascading falling knives.

@ CAS 127 –

Get all the government/taxpayer subsidies and the FED/Banker debt slave schemes out of the picture and prices would drop like a rock.

No VA, FHA, Freddie Mac, Fannie Mae, FED buying mortgage backed securities, etc.

Totally with you cb, except for the VA part:

Any and every person willing and able to put their life on the line to protect USA SHOULD be rewarded with ”home ownership” IF ”they” want it. Etc.

Never used mine,,, though have thought from time to time I should have done so, now many many decades ago…

( Always qualified and did either ”private money” or ”other” lower rates . )

BTW, still have , somewhere, the original hard copy VA ”authorization” letter and brochure, God Bless the VA…

Was that a Cal-Vet loan you had papers for? (Had to enter military in CA). I had lots of friends who had them and they were a super good deal. Very low interest, but somehow adjustable, because I remember a lot of bitching (in garage beer drinking sessions when I rented a room from a Vet buddy) when they went from around 4% to 6% in the early 80s. IIRC.

I’m waiting for the Home Price Index line to intersect with the CPI line again just like it did in 2012. This means housing tracks inflation again and speculation is removed.

The House Price index line still has to fall or the CPI inflation line has to rise.

This is the most awesome chart ever.

The lines on this chart are totally arbitrary because setting the index of June 2000=100 is totally arbitrary. If the chart had started in 2004 the line would go well below rents, for instance. There’s nothing magical about where and when the lines intersect here.

BOTH indices are set at Jan 2000 = 100 so they have the same starting point and to make it possible to compare them.

Homes may be going down but my 500 sq ft over 62 (mostly, some 55 in bad shape or made it into less obvious disability) hotel style low income zero frills rent just went up 10%. We are run by FPI, some big PE outfit that owns lots of stuff all over….DEFINITELY not what I was expecting from home price drops and reading articles like this. I also notice a few more cars and much nicer than when I moved late 2010….and some working folks, I think.

This town has lots of big money retired and rich Docs caring for them, but still a lot of poor and homeless.

Even got a Big SUV from Texas, so it’s not all one-way.

Anyone that put 3% down in 2012 and sold in 2022 got a heck of return on that 3%. Probably in the 100% per year range. not bad if tax payer was going to pick up the losses if it didn’t work out. Probably a little different buying in 2023.

Pre-pandemic the last time mortgage rates were 7% like today was late 2001. At that time the median national house price was about 150K which is about 250K in 2023 dollars. But the current median home price is about 360K. So houses seem to be overvalued by around 45% compared to 2001 – since mortgage payments normally increase in line with rents and rents increase in line with general inflation.

Assuming inflation averages 5% over the next 3-4 years, then house prices would need to drop about 5% a year to return to 2021 pricing. When the Fed talks about a reset and correction being needed for the housing market following the pandemic bubble, this might be what they have in mind. Gentle deflation over a 3-4 year period with small nominal price drops each year and letting inflation do the rest of the work.

Correction:

then house prices would need to drop about 5% a year to return to 2021 pricing

should read:

then house prices would need to drop about 5% a year to return to 2001 valuations

This is impossible. TV told me real estate can never go down. My real estate agent said the same.

Tell them same RE agent to conduct a simple experiment, have him throw a baseball straight up in the air, stand at the same spot and look straight up. Have he/she tell you if that baseball just end up staying flat in the air, apply that final test result to the housing market…rinse and repeat if needed.

Get ready for the gov’t interventions that attempt to keep the party going. We saw this in 2001 and 2008. Bank bailouts, suspension of mark to market accounting, short selling bans, foreclosure bans, mortgage relief/refis, and anything else they can imagine.

If you get into trouble, don’t mail in your keys. Just stop making payments and live in your house for free. If they change the rules again you’ll be able to stay there for years before they can actually evict you.

If you’re hoping to snag a cheap house, you have to get very lucky. Only junk in need of major repairs will hit the open market. Banks will hold onto their inventory so prices don’t get slammed down. They’ll package all their foreclosures and sell them off market to large corporations. This is history, not a prediction.

Good luck out there.

Yet even with all of those government countermeasures, in HB1, housing prices still absolutely collapsed. It was not difficult to “snag a cheap house”. Just required patience.

We snagged a “jewel box” in the East Bay in 2010 out of foreclosure. Sold by the bank. One day showing with best and final. The only reason we won (offered full price) was that ours was an all cash offer with a 15 day close. The dufus’s that were competing with her on the day of the showing were blabbing about their strategy. She took notes and remained stone quiet. It also helped that she looked like she was about 17 at that time and no one took her seriously.

The bank countered with a $5K bump – which we agreed to because the house was about a 95%-er in terms of condition.

Daughter unit looked for a place to own for two years. We spent $100K more than her original budget, but that’s sometimes how it goes. I couldn’t have bought a dump and improved it to that level for anywhere near what we paid. Thank the lord for god-awful decorating.

Just yesterday I learned of a new scheme: “Home equity IPO.” Apparently this is exactly what it sounds like… people sell “shares” of equity in their home to “investors” to take cash out.

I also learned recently that the average homebuyer age is 53 yrs old, highest ever. As well as that 51% of age 35-45 buyers and 79% of age 25-34 buyers receive financial help to buy from their parents, also highest ever.

So my conclusion is now more than ever, equity from other (inflated) assets is being used to buy (inflated) homes. The problem, as a millennial totally ready to buy a home, is there’s no way to know when this will crash down, or whether the govt will allow it to at all. IMO the govt is complicit in blowing the bubble. And it’s clear that politicians on both sides would be happy to blow it bigger if it gets them more votes.

Not to mention certain “envelopes”, or “insider tips” slid their way…

good one H, exactly the situation when WE, in this case the family WE, had to relocate back to the saintly part of the TPA bay area to care for very elderly parents.

In Spite of our CASH, banks holding foreclosed RE would NOT deal with us because of their choice to aggregate for their PE and hedgie friends, no doubt bribing the banksters at that time or knowing they could go to work for said hedgies and PEs,,,

Time and enough to completely crash the ”HOME” market so that anyone and everyone who can and will take care of their home will be able to buy at somewhere close to the 2.5 home cost to income as was the case before all this very ridiculous

exxXagerat TONS occurred to help only those who DO NO WORK,,, but just prey on those who do.

NOT just in USA these days, but all over the world from what I read on Wolf’s WONDER and many other sources around the world….

I guess you need to ask their timeframe. LOL

From Wolf’s chart, it looks like if you bought in 2003 and missed selling at the peak in 2007, you were back in the money by 2013. Looks like about 10 years. Same with buying at the peak in 2006.

Thus housing may be at 2021 levels in 2031? Mabye 2024 to 2025 will be a good time to buy.

BTW…. These housing charts look like an increasing exponential curve. But then again, so does the government debt.

What is up with rent equivalent. It needs to get with the party.

/sarc

Harrold,

I today’s Fed economy, housing prices never have to go down.

Heck, the Fed didn’t even lower rates to negative values in 2020 like some predicted. (Personally, I would have refi’d at a negative rate mortgage. I might also have purchased a fleet of houses at some inflated value hoping to refi at an even more negative rate).

Negative values go on to infinity.

Let the good times roll! :-)

My requirement in 2020 was a negative 100% mortgage. It never happened.

The Fed manipulation of rates in 2020 is just mind-boggling. It didn’t even have to go negative to cause tremendous damage to the housing market and cause massive inflation.

The lack of speed that they reacted to the massive housing bubble blow-up suggests they don’t have state-of-the-art supercomputers working on this.

Wonder what those folks who bought last spring are thinking right about now? A falling knife has no handle, Godspeed to anyone whos signed in the last 12mo.

I am also wondering how the “bIdDiNG wARs iN mY NEigHbOrHoOd aRe sTiLl HapPenInG” squad can keep lying through their teeth.

Most will be in denial and just think we’re in a silly little gully. Pow will pivot in no time and to the moon we go again…or millennial, Gen Z or Gen Alpha will save the day.

SCOTUS is about to pick their pocket for a cool 20k. Doubt they are in the forgiving mood. In fact, note to self: add the anti fire wax coating to the car.

The 10K to 20K payments is not where most the cost, or in my mind, moral hazard comes from it is the pegged maximum payment (I think 5% of discretionary income) that is the poison pill.

Personal experience from my explorations in Southern California is that there are still bidding wars for the “cheap” homes of around $1m or so, plus some crazy overbids by people who seem to be unaware the market is turning.

I looked at three houses last month. One house was listed at $1.05m, and had 18 offers, selling for $1.15. One house was listed at $1.3m and one at $1.4m. Both of those went $100k over asking to the only bidder.

I predict all of three of these new homeowners will regret their purchases soon.

The issue is that there is very low supply of homes and a few dumb buyers are keeping the market afloat.

No bailouts for stupid and greedy people is my only motto.

I’ll offer up a few regular thoughts:

“Why won’t this avocado tree I planted grow?”

“That one neighbor is really weird”

“Whoa… mortgage rates are high now.”

“People really should slow down on our street”

“Livin’ here is pretty sweet compared to that shitty house we were renting”

“House prices are down, that sucks”

On the last point, it’s a bit like thinking of my 401k and getting pissed off when the market goes down.

Sure, things could go terribly wrong and we’d have to sell and lose our shirts. However, we were in a good financial position and went in pretty clear eyed that our house’s price would go down, and that it could take a while to recover (maybe never?).

With the time horizons at play, it becomes tricky to account for and rationalize the full range of possibilities (ie cancer).

The most typical thought is “hey… not too bad”

Thanks WR!

I am waiting for people to come here and say that they are re-seeing bidding war and how many home sin their area has sold above asking price.

And most of them will be telling the truth. The world is never as simple as you want it to be, and nothing goes to heck in a straight line.

Bidding wars and over-asking closes HAVE come back to some areas during the last two months as rates dipped and conditions visibly eased, aided by the pivot narrative. I’m seeing them myself. I don’t expect them to last much longer, now that rates are on the way back up and the pivot narrative is losing its grip on people, but it’s silly and pointless to pretend they aren’t happening now.

They aren’t happening now.

Believe what you want to believe.

These RE articles are like the EV ones, you mention this stuff and the shills crawl out of the woodwork. No, bidding wars are not happening anymore outside of very select markets. I do not think these commenters are telling the truth. The reality is that houses go on the market and sit sometimes for months. And I’m not in a low rent area. Actually the trend as of very recently is that there is very little on the market at all. But going back to last year the trend was a lot of stuff on the market and very little of it sold, and much of it was pulled off the market without selling.

Can confirm from Phoenix, bidding wars and multiple offers are still happening in areas people want to live.

Higher crime areas west of the 17 freeway is where you can get a better deal, but…people don’t want to live there.

No, I’m not a realtor.

People want so badly to believe that the market is in free fall. Especially on these comments. But it just ain’t so yet.

“The only reason sales are happening is because some dumb people don’t know the market is turning.”

Well, if enough dummies agree that the market isn’t turning….then the market isn’t turning.

Not saying I’m bullish on housing, but the market is not as ice cold as some folks wish it to be.

When the price of a house gets very high, how do the criminals live in those areas?

It’s very strange. What do people think wishful thinking will accomplish? Housing prices are bound to fall because they’re unsustainable. so why bother pretending that they’re required to fall in a straight uninterrupted line, or to pretend that rallies don’t occur during downturns? It’s puzzling. And people get so emotional about it, too.

Amazing how people are so sure what’s going to happen. At least they pretend to. We had heard about bubble 2 pipping for how many years now? Covid, forbearance tsunami and now interest rates. And of course there is always the upcoming recession and mass layoffs. Meanwhile, this is happening: “Jobless claims fall again and stay below 200,000 for seventh week in a row”.

The City of Phoenix itself is a monumentally mismanaged s*** hole…. Hobo’s and drug addicts everywhere the houses are under 500k and the city will never do anything about it. …….The suburbs are MUCH better, and the property values in Mesa Scottsdale Glendale Gilbert etc are not falling nearly as fast… I just advertised one of my rentals in North Glendale for apx $700/month more than my previous tenants and got 50+ solid applicants on the first weekend …..VC cash buyers are grinding a little harder on price from what I hear , but they are still advertising like crazy on TV and buying everything that makes sense.

Agreed. No need to assume every poster is lying. While the data doesn’t lie, it only gives averages and there probably are houses that still go over asking with multiple bids.

I wonder though: could these be because smart owners, or smart RE agents advising them, are telling them to price lower than a few months ago to sell rather than sit in this market?

IOW, it doesn’t really matter whether there were multiple bids over asking. What matters is what the final price was and whether that’s higher or lower than what it would have gone for last summer.

Even in the depths of housing bust 1, plenty of houses on auction by banks had multiple bidders over the minimum reserve price. But the final price was much less than what the house would have gone for a year earlier

I think the issue is using the real but rare biding wars on desirable (read: appropriately priced) properties to continue the delusion that housing in general is not going down (it is).

Most sellers still seem to have their heads in the clouds and need to come back down to earth.

How many of these multiple offers over asking are fabrications? Shill bids designed to stoke an auction style competition…is there actual any transparency to buyers? Is there a log or a chain proving such wars aren’t pure BS?

…perhaps the old journalistic verity coming to mind: “…if it bleeds, it lede’s…”.

may we all find a better day.

To be fair, you need knifecatchers. That’s what transpired in January/early February. Prices are set by people buying all the way down.

True.

I know several people who call themselves real estate investors not buying at these prices. But they are itching to get back into the game. They could be potential knife catchers.

But in my area, there are no more fixer uppers on the market. LOL All the low end existing homes that hit the MLS have already been remodeled.

We may not see fixer uppers until we start seeing foreclosures?

True, as if you currently have zero volume (i.e. no sales) then you can’t compare prices now to the past month, and 12 months ago.

So if the last price was recorded in March 2023 and there are no sales for the next 9 months, then the December 2023 price level is set to the latest sales price which was in March 2023.

Hence, the change in sales price for December 2022 to December 2023 is based on March 2023 data.

“ I am waiting for people to come here and say that they are re-seeing bidding war ”

Happened just recently in January. Interest rates went down briefly. It’s all a function of supply and demand. We have historic low inventory (below 1M of active listings) and a strong job market. Plus inflation is high>higher wages.

Housing services is about 18% of core PCE which is what the Fed watches closely. And this meltdown is just beginning. By the time it hits bottom, inflation won’t be an issue. The Fed needs to be patient. It would help if Republicans stopped giving the rich tax breaks and tax evading loopholes. That crew is the one that fuels asset inflation and the ‘boom and bust’ financial cycle that bedevils our economy. Some effing common sense out of Congress would be nice.

Note the chart I just posed in the comments above, Case Shiller v. CPI rent. CPI tracks rents, not home prices, and rents are not correlated with home prices. Home prices plunged in 2007-2012, and rents continued to rise until the two lines met in the chart. And then, QE kicked off the next housing boom, the lines separated again. And now they’re on track to converge again somewhere years from now.

Two opposite scenarios – one a financial-induced bust that resulted in defaults, lowered home values, and then a *lowering* of interest rates that made it easier for people to buy vs. rent. Rents should then lower, and indeed they at least flattened for a period.

Now we have a general inflation, 6% nominal wage growth, and a raising of interest rates. Much less affordable to buy now even as people have more nominal dollars, and so one would expect an acceleration of rent growth that keeps pace with inflation and the unaffordability of buying (indeed thats what it looks like in the data).

So a convergence, potentially, but driven more by rent increases and at a much different rent to value point than previous.

How did you choose June 2000 to start your index? You’d have very different conclusions if you had arbitrarily started in a different year. If you had started the chart in 2006 you’d say housing was an amazing bargain after 2008 and played catch-up for years…

BOTH indices are set at Jan 2000 = 100 so they have the same starting point and to make it possible to compare them.

The Case-Shiller index has been set to Jan 2000 = 100 by Case-Shiller for many many years.

I set the OEOR index to Jan 2000 = 100 to give both the same starting point and allow for comparisons on the same scale.

The largest loophole of all that gives most of its benefit to the 1% is the SALT deduction, and the party you named limited it, and their opponents want to reinstate it. Besides, tax policy has very very little to do with this home price inflation, which is as almost all inflation is, a monetary phenomenon. This is the doing of the crazy Fed.

Midwest and North Carolina flat…

C’mon Raleigh you so and so… I need a pool, a floatie raft and one of those fruity drinks with the colorful umbrella to have the perfect amount of relaxation. Needed to balance the heck all these crooked lines are going in. :)

“Prices will just slide sideways” “Inventory is still low” “The fed will pivot soon” “the market just bottomed”

Its going to get harder and harder to cheerlead this thing, especially as the rest of these markets reach YOY negatives. Stay watching how they twist the narrative

Lawrence Yun, as always, will be the head cheerleader.

Yeah, that chump forecasts 1.6% price declines over 2023. LOL. Already there and playing with house money…

Lawrence should write a book like David Lereah (Chief economist for the NAR) did in 2005.

“Are You Missing the Real Estate Boom?: The Boom Will Not Bust and Why Property Values Will Continue to Climb Through the End of the Decade – And How to Profit From Them”

There are still a few copies left on Amazon. Look it up.

Haha, I just saw an article titled “Real Estate Bottomed in January”

More articles are turning Bearish finally though.

What was it, 4 or 6 months ago that most analysts were saying like 12% gains in ’23

Yep, the trolls roll out the mindless tropes but never back them with statistics. Fine by me, theyre obviously in over their head and will suffer mightily in the coming years.

Oh no, SD? Say it ain’t so….what happened to everyone’s favorite SoCal paradise. It can only flatline right? Good to see either way

On the hand, come one LA and OC, don’t let your little brother to the south outdo you on decline like this, come back with a vengeance , go big with 30-40% plus please

“On the hand, come one LA and OC, don’t let your little brother to the south outdo you on decline like this, come back with a vengeance , go big with 30-40% plus please”

L.A.’s eviction moratorium doesn’t end till March 31st, but something tells me there’s gonna be some of that ‘pent-up demand’ we always hear about… to the downside.

Rob,

Is that when they start the process?

Eviction takes 90 days. I’ve heard evicting families with kids can take significantly longer.

That means March 31 is actually July. Then you have to remodel, because your angry tenant you evicted trashed the place. So now you’re talking September.

Home owners go broke and it becomes Blackrocks problem at a discount price.

With nothing to support this intuitive grasp of how these housing bubbles propagate they seem to start at the major wealth centers (San Francisco) and like ripples in a lake spread across the country in waves.

Unwinding them does not begin at the farthest region of the kingdom but instead starts from the epicenter where they began.

In this sense we’re seeing the same pattern as the previous bust. The wealth centers leading the way before making their way to rural land values.

“Unwinding them does not begin at the farthest region of the kingdom but instead starts from the epicenter where they began.”

This was not the case last bust. It was like a flood, where the last to rise was the first to recede. I expect much similar results this time around.

Nope, youre wrong. San Diego was the first major city to experience 20% annual appreciation after the fed cut rates to 0 after 9/11. You can verify by looking at copies of Forbes, Fortune and Money magazines in that time frame, since they all did articles on the phenomenon since that kind of appreciation had never been seen at that scale. The high end areas (mainly Rancho Santa Fe) in SD topped in late 2003. The ghetto areas of SD were still being bought and flipped into mid 2005.

I agree with Depth Charge. Seattle real estate bubbled on in 2006-2008, then weakened in last half of 2009, only to drop seriously in 2010-2011. Real estate agents claimed Seattle was different all along, but prices of condos dropped more than 50% eventually.

Back then you had very weak owner profiles. NINJA loans and arm loans. Everyone who could fog a mirror would get a loan. Owners today have a strong balance sheet with good credit, high equity and low locked in rates. If the employment market turns, house owners have options: rent out the house at a profit, get roommates or simply get a lower paid job and still be able to keep the house. Which industry sector is seeing an over investment today? In other words, which sector is going to get hit hard? And what about the rest of the market? Maybe some lose their job and have to sell while others do well and buy the houses at a discount? It’s never that simple that Joe Schmoe somehow just benefits and can finally buy a great house at 50% off.

That’s how I remember ’08 too. At that time I was in Toronto, further out in Windsor properties lost near 50% but in TO we had years of stagnation. I wasn’t watching charts back then just listings for lower end condos so averages and medians might have been different at various ranges, for me at my range nothing changed at the time. This time around it seems TO is getting hit, but the most drastic drop in the greater TO area seems to be Hamilton, it’s not a pretty town that had no business seeing price spikes to begin with but too many younger professionals got priced out of GTA proper and went there because at least it has GO Train which connects to downtown TO, along came the speculators/investors ofcourse. Now Hamilton is unwinding the quickest it seems.

I know most people here are American, but that’s exactly what has happened where I live (Sweden). In the posh Stockholm suburb of Lidingö, prices are down 28% from the top in March 2022, the national record … so far … this time.

An idiot former colleague of mine bought a house there in April 2022 for SEK 15 million, so he’s now down a cool SEK 4 million or so (app. $400,000). In one year!

Anything can be a bubble. They are hard to spot when it’s part of your book. Moreso, I suppose, when you are leveraged.

Fundamentals are why I think this ride ends in tears. Price to income sucks, wage inflation cannot make up the difference, there is no housing shortage as rents are stabilizing, and inflation takes away another debt gorging party.

Absent government intervention bringing back liar loans or dumping massive additional stimulus, housing looks terrible as a long term investment.

Sorry, sfr looks like a terrible investment. Maybe mfds still ok, I dunno.

The government cannot change the outcome longer term. That’s a myth.

It’s going to take a while, but the end of the bond cycle in 2020 is going to impose real austerity on both the government and country years (not decades) from now. Other key is the DXY.

For the record, as a Realtor, I’m receiving emails offering NoDoc asset backed loans up to $3 Million. 1-8 units fix and flip.

:-O

I’ll take $3 mil. Just wire it to me.

NATE

“…..Absent government intervention bringing back liar loans or dumping massive additional stimulus, housing looks terrible as a long term investment….”

Don’t forget moratoriums / forbearance / Jingle mail squatters. I stated it before – the hey days of SFR rentals are in the past. Multi-fam low ROI will be all that’s left for residential RE investors. Bonds will do better.

“ government intervention bringing back liar loans or dumping massive additional stimulus, housing looks terrible as a long term investment.”

What? We won’t see liar loans in our lifetime again. At least not in the US. Have you tried to buy a house lately? Boy do they dissect you. It’s the exact opposite of a liar loan.

The homeowner in the US is in the best shape ever. Low locked in rates, high equity and high inflation. Wages are going up. Plus inventory is extremely low. Sometimes it feels as if people don’t want to see reality so they just make up their own.

And yet home builder Toll Brothers stock is up after beating expectations. I thought the builder stocks would turn.

Their sales orders collapsed by 51% yoy = future revenues. They’re living off their backlog. The hype-and-hoopla show has totally brushed aside the issue of the collapsing sales orders. The sales orders of all homebuilders have collapsed by 40-60% yoy.

Toll brothers just pulled out of purchasing a property I own in Seattle after investing nearly 500k into the project. Their plan was to build 20 townhomes in a rapidly growing area near a new light rail station. They would rather take that hit than lose even more down the road. Pencils down in developer land.

Troll Brothers announced plans for a subdivision adjacent to our community last December. A development of 489 acres….. north and east of Snotsdale, AZ. Applying for rezoning. Figure it will take 3 years before they can build. (There’s no infrastructure to support it as ours is too small and outdated).

“They paved paradise and put up a parking lot”.

Jesse – you still want to sell?

I think the optimism is goes beyond that. Bloomberg had an article about this, sort of, how new construction will be the only real source of supply for awhile, for all the reasons we’ve been hearing about legacy owners not selling. So demand will be high.

FTR, I’m not buying it, and am considering a short of the top 5 names. I hate being net short like that, so an still looking for a semi-decent hedge for a long/short.

And buyer cancellations for the bid production builders were up in the 60-70 percent range as well, compared to 15 percent or so the previous year’s Q4. So new orders are in half (will get worse) and previous orders canceled at that magnitude. Their buydowns and other incentives will carry them only so far so slow the sinking ship…

Bernanke is responsible for the housing shortage. He bankrupt half the home builders. Then Powell suppressed interest rates to historically low levels stoking housing prices (reweighting risk assets).

It’s Gresham’s law: “a statement of the least cost “principle of substitution” as applied to money: that a commodity (or service) will be devoted to those uses which are the most profitable.

As an owner and RE investor I have an interest in short supply and elevated prices. It keeps people from moving to CA. It’s already too crowded. People like me always vote against new construction in our “backyard” >nimby. It’s not fair but it benefits us: high inflation > my wages and rents and asset values go up while my debt is low and locked in at low rates. It’s a dream honestly. Things can stay that way if I can have it my way. Sucks for renters. I’ve been there and luckily I got myself into my first house and started buying rentals.

Greedy People like you are the problem. I hope you loose everything.

I call that capitalism. Greed is part of the game. I don’t run a charity. Very hard to lose everything. The only way that could happen is if I sell all my assets and gamble the money away in Vegas. But I won’t sell RE and will hold on to the locked in low rate for the entire duration of the loan(s). Thank you FED.

He bankrupt the small mom and pop builders. I knew of a few.

The big builders were bailed out by their congress friends who received a lot of lobbying money. Congress got the IRS to write some new rules that kept the big builders from going bankrupt.

Congress rewrites the rules. The IRS simply follows the rules they are given.

Here are some Redfin median price charts for some large Seattle suburbs, for viewer amazement/amusement:

https://www.redfin.com/city/20001/WA/Woodinville/housing-market

https://www.redfin.com/city/14913/WA/Redmond/housing-market

https://www.redfin.com/city/9148/WA/Kirkland/housing-market

All I can do is shake my head.

Based on the CPI graph (same as corelogic) we have 1/3 down to go before the market is healthy again. In the meantime it’s obviously better to rent.

Many people leveraged people will lose it all. Just like last time. It will be denial at first then doubt then realization then panic then despair…then up.

I’ll buy when desperation is palpable. Or when banks no longer lend. As usual.

Just got the “Rent Now, Buy Later” email from Realtor.com

Attention Portsmouth, NH

Rent to own is pretty treacherous for the seller and provides some interesting leverage for a buyer/renter. Almost two different contracts – long term lease tied to a purchase. Dicey. Depending on the terms, of course.

You should jump on it. There was a guy on here saying ” buy now or be priced out forever”.

Should be interesting to see how much heat the Fed and Powell can take.

A real estate bust would bring out the whiners running to our gummint bureaucrats, lobbyists and congress for help as they have for several decades.

Time will tell.

A housing bust would bring out whiners for sure. . .but it would also make a lot of normal working class people wake up from the struggle fog of current inflation life, and go:

“Wait, this was a just a bubble, AGAIN!?! How many times are we going to let these fools at the Eccles building fail at their jobs?”

“Wait, this was a just a bubble, AGAIN!?! How many times are we going to let these fools at the Eccles building fail at their jobs?”

uhhh you do realize its all the same people at the top of every industry, government agency and so forth. You’ve been letting them fail since at least the late 90’s and nobody seems to notice……. whats on TV tonight?

I can see that it’s a bubble, and that the Fed is a disaster with it’s policies.

It’s the average American that doesn’t even know what “Federal Reserve Note” actually means, that I worry about. Like pigs to a slaughter. . .

Also, what can one guy in California do vs the unelected Fed governors board? I’m just a little fish(in a big pond), so stop it with the “you’ve let them do this” nonsense. I was just out of high school when the last housing bubble popped. Now I’m just another 30-something that’s looking at astronomical asset prices and wondering how my future is gonna play out.

I am in a very tough spot. My wife and I are ready and eager to start a family and settle into a forever-home. Despite living in one of the above-mentioned very HCOL markets, we are very fortunate and can afford to buy a house. HOWEVER, I read this blog (and comments) religiously and know that it makes zero economic sense to buy a house right now.

Pretty much a head vs heart situation.

Sellers are in a more difficult position. They want you to buy their biggest asset at top dollar to lock recent gains and fund their retirement, but you are waffling.

Each week that goes by, they lose home equity, while you accrue 5% on your savings.

Patience is the trump card in this situation, and you are holding it.

Well said – good advice

Correct Bobber. Also, this situation is compounded for the sellers who have few or no investment assets outside of their home equity.

The smart ones in that group have already sold. The remaining sellers are in a tight corner.

I’ll add, the homeowners in my neighborhood of $1.5-$2.5M homes have been losing $10k to $15k of market value per month, for the last 8 months or more.

So yes, it pays to wait for a trend reversal. The downward trend is clearly in place now. Only 2nd or 3rd inning. Things may be looking good for buyers around Spring of 2024. So sign that year lease, crack a beer, and enjoy watching your interest earnings rise and home prices fall.

Don’t even think about thinking about buying until the Fed actually begins an interest rate reduction cycle. That’s when you consider buying, with an eye towards a refinancing later.

You still might not catch the bottom, but at least your losses will be manageable and reversible over time. Right now, long-term financial damage is meeting up with eager buyers.

Now that I think more on it, the market value losses in my neighborhood have been in the range of $40k to $60k per month the last 8 months.

That’s the equivalent of a 20% total loss so far, which matches the lagged Case-Shiller indicator. If market losses are more in line with the updated median price statistics, the loss would be double (i.e, loss of $80k to $120k per month).

And losses so far only wipe out the 2021 gains. There’s a lot more pain to come.

Only a fool would jump into that meat grinder at this time.

Terrence

If you haven’t bought until now, it makes full sense to wait several more years.

The tide has turned. But this process is slow. You are excellently positioned. You have money and can pounce any time.

What do you have to lose? Couple years’ rent and possible price reversal – the latter you can monitor and act.

But consider this: if you pull the trigger now, you might miss once in a lifetime historical opportunity if the markets really crash hard as many predict. May not happen, of course, but the “this time is different” BS is much less convincing to me.

I feel you. We’re in a similar position. After starting a family recently, we needed to upsize so we sold my LA bachelor pad last summer and moved into a cozy rental while we looked for a bigger family friendly house (and hoped to watch prices fall while we collected 3%-5% on our next down payment). That was going on a year ago and now my wife and I are both working full time at home and our kid just turned two and is running amok. That cozy rental now feels way too small and the little man needs a yard to run around in for everyone’s sanity. Patience is great and all but by the end of this year I imagine we’ll break and just pull the trigger on whatever the best deal is at the time in the housing market – probably this coming fall. At some point it becomes about what will make your family the happiest. I really hope this downward trend in prices continues through the spring and summer selling season, however I won’t be surprised if denial runs strong and they take a quick beat this spring before resuming their path downward. We’d really appreciate another 8% haircut by the end of the year. Another 20-30% decline is probably what’s needed but 2025 feels like a lifetime away.

Terrence, just look at Wolf’s charts. It’s not as though housing prices are anchored in concrete – they fluctuate dramatically. And, imo, they are at completely unsustainable levels. These home prices are completely dependent on 3.5+% interest rates.

Just wait… recessions are inevitable and when they bring substantial unemployment, prices drop. Maybe not across the board, but for people who have to sell…

This may not be do-able, but one strategy is to buy and occupy a unit in a duplex, triplex or quad. Eventually you might buy a sfr and then rent out what you’ve occupied. May even teach other family members frugality and delayed gratification.

Besides reading the sky-is-falling news I’d also look at just data driven reports without the FUD. If you buy a home for your family you really don’t care that much if prices go up or down. As long as you can comfortably afford the house and don’t over stretch you are fine over the long run. The idea that you can time the market and somehow buy a dream home at 50% discount is just that: a dream. The reality is nobody can time the market. Buying a house for your family is about stability and creating memories. I was in your spot and when I bought 90% of people told me: you lose your equity, you bought the peak. Many years later I find myself not regretting that decision once. If you can afford a home in a good location, by all means, go and be a homeowner. Down the road you will face many opportunities to purchase a rental investment or buying opportunities in stocks and even crypto. Buying a home for my family has changed our life’s for the better. I hated renting and the uncertainty of ever increasing rents. My interest rate when I bought was crappy but the beauty of being a homeowner is you can take advantage of lower rates down the line. Your financial situation only improves as an owner (locked in debt and increasing wages over time). Inflation is your friend over time if you own assets. Right now I wouldn’t rush into buying but look at houses that you like and even make a low offer to see if the seller would go for it. People are scared right now and the FUD is all over this market. The problem with betting on lower prices is: we haven’t seen an increase in inventory and as soon as rates go lower buyer demand picks up (just saw that in January). People who tell you during a recession prices go down don’t know that lower rates translate into higher affordability and ultimately higher demand. They pretend everyone loses their jobs, nobody buys and prices crash by 50%. Okay, if you believe that, don’t buy. But if you believe that recessions hurt certain people while others thrive than that’s in line with history.

Your view has a desperate “all-or-nothing” tinge to it, kind of like the FOMO thinking.

What’s wrong with waiting a year to buy? You act as though a decision to rent for a year or two will permanently disrupt a family. You are missing the big picture.

If the goal is to protect your family, the best thing you can do right now is avoid catastrophic losses and wait it out. Memories of losing $100k or more in a matter of months, along with relate stresses, aren’t the memories you want to make.

“ Memories of losing $100k or more in a matter of months,”

So, if you are so good at timing the market, did you buy at the beginning of 2020 right when Covid happened? You must have purchased houses left and right because somehow you knew the market will skyrocket. And now you must be selling because you know the severe drop is coming within in months. When I read comments like this I smile because it reminds me of when a ton of people told me how the market will crash and how my equity will go down the drain. That was right when Covid hit. And in 2018 as well. Lol. Now I sit very pretty with low locked in rates and lots of equity across the RE portfolio. Meanwhile inflation did it things and renters paid down principal.

This – you gonna lose 100k right after you buy. How often I heard that in the last ten years. I do the opposite of what people advise and keep buying rentals as soon as I can comfortably afford it. I use comments like yours for entertainment. In a few month when the market has just gone sideways you will tell me the same exact thing. I bet you have for a while and will continue to do so. Typical market timer. You just move the goal post.

Nothing wrong with raising kids in a rental. I was raised in a rental until 12. We had our first kid in ‘09, the same year I turned my house over to the bank. Raised 2 boys in a rental until we bought again in ‘14. My boys didn’t care if the house was rented or mortgaged.

Agree. I don’t know why families should risk a huge financial loss in order to play with the kids in the yard, as opposed to a nearby park. The reasons people cite for “needing” a house reflect a lot of tunnel vision. These are times when lack of common sense and clear thinking can cost people a lot of money.

What is he risking?! He said he can afford to buy. One of my good renters is moving out – sadly. He is buying a house. He’s been good to me and I won’t penalize him for breaking the lease agreement. Good for him though. Avoid the FUD and buy when you can afford it. This market timing BS never works out. I have seen it for the last ten years now. I bought a rental in the past and the market went down slightly then kept trending higher. Once you have a fixed debt burden you care very less about the house value

Fluctuation. Over time housing goes up. Inflation becomes your friend. And you stop worrying about should you buy or not and you stop worrying about increasing rents and other BS that comes with renting. Having renters is fantastic, being a renter for a decade or longer sucks! But to each their own. I can only share my personal experience. I am not a realtor or RE cheerleader. Owning RE just has been very good for me and I love that we have 30y fixed mortgages in the US. That’s not common across the globe. I never regretted once that I bought any of these houses. As long as you buy in a good location and do your due diligence you will be just fine. And if housing goes down, so what. You have a house! I know soo many people in my circle of friends and family who would love to be able to afford a house. If you can comfortably afford it now it’s a no brainer to buy in my opinion. Our lives changed so much for the better when we bought our first home. Too much to write here.

I had friends in your position in March 2007. They were about to get married and wanted to buy a place. Time of life is a big factor. Though I rarely give direct financial advice, I said not to do it because the market was clearly coming down. I was very familiar with our market because my wife and I had thought about moving up in Fall 2006. My friend said the home they wanted had already dropped their list price from 725k to 675k. They bought it for 655k.

Fast forward to February 2015 and they have two kids and want to move closer to family in Kansas. They sell the place for 562k, so the total loss after commissions was around 130k. These things can play out over long periods. They’re probably like you in that they could afford taking the hit and bought a place for just under a million in a KC suburb in 2015. Still, it’s not pleasant absorbing the loss.

If it’s your forever home, you’ll probably be fine. Life happens though. Just realize if this bust continues your home’s market value may be under the purchase price for a long time.

Wolf. How does it feel to live on Ground Zero?

I have been warning fellow real-estate professionals that the cheerleaders could no longer hang their hat on the Year Over Year (YOY) numbers being positive. YOY has just turned negative in most hot spots and for the next 3 months the YOY will expolde to the negative twice as fast as the current MOM number. From here the two numbers move in opposite directions untill around May-June 2023. At that point the year old number will crest and then start to move down when the crash all started a year ago.

They just need a new narrative to spin.

“The sharp decline in year-over-year real estate prices, combined with rising mortgage rates and difficult employment outlook creates a unique investment vortex for home buyers wishing to position themselves for long-term real estate gains.”

How does that sound?

Yes. Home buyers will likely be looking at opportunity. It may happen faster than in 2008 as the public will throw in the towel sooner. The ethical issue that kept people in their mortgages is not going to deter short sellers this time.

“How does it feel to live on Ground Zero?”

TBH, it was insane exuberance and bubble mentality here. It was crazy, all around, real estate being the smaller element. The biggies in that insane exuberance were cryptos, startups, and stocks. Some of that bubble insanity has now leached out (still plenty left), and the whole place calmed down a little. It feels a little more sane, actually. Bubble mentality is not a good thing. And I’m glad it popped.

Seattle was bad too. People paying 1.6 million for old 70s houses, etc. Tripping over each other to overbid on shacks with no inspection. Developer ever tore down a really nice house to build a new home on the lot. It is now sitting there month after month with all the lights on at night so homeless people don’t sleep in it. My bad for all of this, y’all.

Wolf – auto-c hard at work in destroying nuance in the ‘Murican tongue, no doubt, but it would be splendid if leeches could be employed in removing insanity…

may we all find a better day.

It’s interesting how home prices can jump by 20% for many years straight, then decline just as fast. If the Federal Reserve had any sense, they would have gotten a little unnerved by that movement. After all, they unabashedly assumed responsibility for managing the economy. Doesn’t that require some thoughtfulness and respect for consequences?

Anyone notice the stormfront hasn’t passed the Mississippi yet?

Troubling

I have. It sucks.

Thanks wolf and I see the need to put in dreamy highs but all these markets seem to be up y/y. Guess that just underlines how far they have to go down before sellers expectations get reset and sales volume normalizes, it is a long way off.

Also, the notions that price discovery happens at margins, I can’t assail that idea although those w 3-4% 30 yr loans will take alot for them to sell. You have speculators who will sell, the 3 D’s , those downsizing with alot of equity all to sell before those in lifestyle stasis w 3% mortgages will want to buy at 5%. Unless there a recession and widespread default, can’t see the fed allowing that to happen though.

Guess it’s all speculate on factors and wait and see.

“I can’t assail that idea although those w 3-4% 30 yr loans will take alot for them to sell.”

Not really. Many will just walk away. It doesn’t matter what the rate is when the house is only worth 50% of the mortgage amount. People don’t like paying for any asset that has halved its value. The largest number of defaults last time were prime loans, and the main reason being negative equity.

Correct those folks outsmarted their lender with strategic default.

Exactly, they saw their neighbors defaulting without consequence thanks to bail outs and said “why should I continue to pay my upside down mortgage”

That only works if the mortgage you try to walk away from is new purchase money. Refi’s aren’t eligible for jingle-mail without recourse.

Ooops.

A meaningful portion of the price spikes during ‘housing bubble number 2’ appear to have occurred during the 2020 – 2022 time period.

This seems very odd because that time period was heavily impacted by the COVID pandemic. In New York COVID vaccines were first released for healthcare workers in December 2020, and it took many more months before it was widely released first for seniors only, and then for different age groups. NYC schools stayed online throughout the pandemic and didn’t reopen until September 2021.

I would imagine that the logistics of meeting with real estate brokers, viewing a house, and then arranging for closing and moving would be very difficult during this challenging period. Especially in the largest cities of the Case Shiller Index. With those kinds of obstacles, why would prices surge so far away from their historic norms?

Is it possible that many of this time periods purchases were made by businesses or investors, and not by individuals who need a house where they can reside?

Videos, drone footage of the house, inspections waved, appraisals waved or reduced to drive-by appraisals, documents exchanged and signed via Docusign, houses bought before the buyer ever set foot into it. The industry modernized in a hurry.

I was house-hunting in the Bay Area during that period. Instead of going to open houses, you’d have to sign up for a time slot, so you wouldn’t be in there with other people. Also you’d have to sign a COVID liability waiver every time. That was the only real difference.

I was hoping that increasing acceptance of WFH would lead to migration out of the area, such that housing prices might stabilize and I might have a snowball’s chance of buying. Unfortunately, what happened instead was that a bunch of overpaid nerds (myself included) spent all day every day inside apartments that were really too small to make that enjoyable, and also we had nothing else to spend money on, so that down payment just kind of materialized in our bank accounts. Hey, let’s buy a house!

post after good post by Wolf, one thing that often comes through is a strong sense of schadenfreude by his readers, and a general bitterness and negativity. human nature I guess.

Posts like yours accusing people of “bitterness and negativity” are generally from individuals who are getting their asses kicked financially, as their houses plummet in value.

you are off 180 degrees, and that’s the truth. ponder that.

I think what you term “bitterness and negativity” is simply an outgrowth of frustration with a grossly distorted system. A system that has long rewarded leverage and speculation, and trashed savings and prudence.

And old age…

HowNow,

Yes, I forgot to add: GET OFF OF MY LAWN!

There’s a counterpoint to schadenfreude and it’s when anyone apportions it to someone(s) in order to seem above such vulgarities. Kinda like how people who say no-ones better than anyone else feel better for having said it.

What I see is a lot of exasperation with the hyper-credulous house worshippers who helped distort the market by feverishly buying at the top of the market rather than assessing past as prologue & voting with their wallets. I can’t tell you the number of times I was told in the past 18 months here in Austin—“yeah, but it’s not a bubble.”

Amen, I can agree to what you’re saying

And with people buying crypto on the expectation that it’ll be a world-recognized currency after the civil war, or SPAC investors who trust the PE fund that’s floated it with the name “Nano-genetic-bioparticle”, or NFT museum administrators, or meme investors, or beany babies… Why are people puzzled that housing prices have gone haywire?

“They don’t ring a bell at the top.”

I saw a flip in Austin (we’re foolishly looking there) that dropped from over $1M to @ $600K. Still, no takers. Freeway noise is never a “feature”…. it’s always a “bug”.

Wow. Foolish is right — but by all means, if you need a nice hole to chuck your money in, party on. The last vestiges of what made Austin Austin left the building over 10 years ago. Enjoy the hype.

If it’s 600 now, that means it was probably 375 in 2013. Non-disclosure state means it’s hard to track histories.

Bul – recalling again H.S.Thompson’s timeless dictum: “…when the going gets weird, he weird turn pro…”.

may we all find a better day.

15 years of savers being punished with 0% interest rates is worthy of bitterness imo.

+1000 MM,,,

though WE, in this case the small family WE only started recently after selling the farm to take care of very elderly parents.

For damn shore hurting those LEAST able, eh!

+1M

so if your business model as a get rich quick like me ‘influencer’ has been promoting building short term rental empires … now what do you do?

A. don’t change anything … keep the hype flowing with pictures of yourself at the beach

B. tell your sheeple that they will get fleeced and lose their money, so wait for a better day

C. start looking for a real job cause nobody reads or watches your stuff anymore and your STR units don’t cover your carry costs

Lawrence Yun and SoCalJim think that now is a good time to buy :) Heck, everyday is a good day to buy RE.

Don’t know about SoCalJim but Lawrence Yun probably has the easiest job in the world, say the same thing since before 08 and pretend he is an objective economist rather than a balant RE paid shill. I would love to one documented case of him actually warning people not to buy based on unbiased data, if someone can find that, I’ll send you a $20 gift card..

Just a simple search on google though “Did Lawrence Yun ever warn people not buy real estate?” yield results like this going back to 2008…lol

Dec 28, 2007 — Yun forecasts essentially flat prices in 2008. Yet, he also believes there’s at least a one in four chance that prices will fall more than they did this year

May 13, 2008 — One could reasonably argue that Yun is committing consumer fraud by trying to entice people to buy into a market that is poised to fall further.

Feb 1, 2013 — Lawrence Yun said, “AAR’s weather may be cold, but its housing market is on fire.” Now, … While real estate licensees will inevitably become more.

Nov 11, 2022 — NAR’s Lawrence Yun Predicts US Home Prices Won’t Experience Major Decline, Could Possibly Rise Slightly in 2023 if Mortgage Rates Remain at 7%.

Feb 21, 2022 — “If people are waiting for a price to decline, well, it’s not going to happen,” Yun continued, predicting healthy price gains in 2022

Some of the rose-tinted goggle wearers on here are not much better, with their fanciful tales of all cash buyers, bidding wars, and houses going for above asking. All of that is stuff that I haven’t seen since late 2021. If I didn’t know better I would say that there is a coordinated effort by real estate shills to spread disinfo across every major econ blog, because these guys are sure everywhere.

Well, to them I say, as a famous troll on Zerohedge used to say:

“There you go again, taking falling housing prices personally.”

BFB wasn’t a troll!!!!

That was very definitely still happening in 2022. I know because we participated in some. Thankfully without success although it didn’t feel like good news at the time! And it definitely continued into at least the third quarter (I think there was enough pent up demand to sustain it early in the interest rate rises)

I think it’s all changed now, but we’re out of the market now. And of course, the agents are still telling us how this market is special and won’t get hurt that much.

Just do the opposite of whatever Lawrence Yun predicts or advises and you’ll do fine.

It’s not just Yun. There’s a whole ecosystem of influencers, reality shows, real estate journalists, financial journalists, PR and lobbyists, government entities, etc. that echo each other … but hey … if people have no critical thinking skills and buy into the hype then it’s on them … not Yun.

Here is one thing most in real estate do not know that will protect many who own homes. California passed a huge increase in how much equity a person can protect by homestead.

If you homestead BEFORE any creditors come after you they cannot force you to sell your house with the major homestead filing that can act as an effective deterrent to some one wanting to force payment based on your home equity. No wait, that also just changed now the homestead does not have to be filed prior to any judgment filed.

No way will those who think real estate is great way to make money once they face those savvy enough to used homestead AND bankruptcy to fight back. And they will which will be pure hell for real estate investors.

Why is Fed dragging their feet in cutting Balance Sheet? That’s where majority of the ILLS come from — Persistent High Inflation, Negative Real Yield, High Employment, LOW 10-Year Yield and hence Low Mortgage Rate.

Yes, if Balance Sheet shed $1.2 trillion proportionally by now just like how Bank Canada trim their holdings, 10Y yield should be 5% and Mortgage Rate should be 8% .

Interest Rate still way below Inflation, and Fed and praising minions pretend they never understand why UnEmployment is stubbornly low, Inflation is stubbornly High, Economy and Spending are stubbornly Strong, etc.

Hypocrites.

I’ve been using Zillow (and other places) to help my kids look for a house in my area. I’ve been setting the max price to $350K (which I consider very high for our area) and recently the number of listings went from about a dozen down to one. I increased the max price to $500K and it only added two or three more. I get the feeling that people have just decided to sit tight rather than take a hit on the price, but that’s just a feeling. I have no real idea if that’s the case.

Just an anecdotal point, but it points to something happening, but I’m not sure what.

I’ve been noticing the same.

People can’t sell because they can not afford to buy again. Now it’s default time who runs out of liquidity first. Everybody is in wait mode to see whose dominoes will fall first.

You are right in what you say unless people move elsewhere.

I am headed to to the South as it still has places not out of hand like in the Blue coastal states.

Have lived in SoCal for 68 years and you cannot even get to the beaches to surf let alone for a family outing.

Even if the market dumps further I will be able to do well by relocating and many in my million dollar home neighborhood are getting ready to escape like myself.

What a shame for Californians tool lose the beautiful state to socialist rising and capitalist outrage as useless as a watchdog without teeth and a weak whimpering protest.

Adam Smith,

We’re counting on you to leave. Don’t disappoint us. It’s way too crowded here, and home prices are way too high, and it needs to get less crowded and prices need to come down, and we’re counting on you to help us get this accomplished. Thank you for your service.

Back in 1988 I visited a friend in Los Angeles and I was dismayed at the quality of life. We wanted to go camping but she said you would have had to have made a reservation months earlier. In Texas, life was good and the complete opposite of California. Now, Texas has the exact same problems. Even down to having to reserve a camping spot months in advance. In 30 years this place has been completely trashed.

Is that just a hint of exasperation in your voice, Wolf?

You did introduce the idea of a “return to normal” in your lead-up, and in fact, this would be welcome for Californians, perhaps more than those in most other locations. I’m among the optimists who believe that we’re headed for better times for working people (the middle class), though I don’t expect to get there in a straight line (Wall Street has to fail or become irrelevant first, which I do anticipate).

NB: I’m a California taxpayer, albeit fractional, and I’ll be back at “home” in North San Diego County in mid-March (and San Francisco for a few days in April).

These losers sound like all those NYrs who moved to Florida decades ago to get away from all the problems they created, and are now creating the same or worse problems in their new location. Overcrowding, overspending, high taxes, traffic jams, inflation in the cost of living, environmental destruction and pollution, high insurance costs, urban heat island climate change.

Yeah because these idiots think by Spring they’ll be rescue by selling season miracle and Pow Pow will tick his little tail between his legs and pivot hard and demand will rush back in… if that doesn’t work, put the house for rent at some ridiculous asking rate hoping some other sucker will pay your mortgage..

Like Wolf said, those who panic first panic best.. the rest, good luck with that knife catching endeavor.. rude awakening soon enough.

Same. With same parameters too.

My house at the low end is at 700K (Zillow), on Realtor.com it is at 860K at the high end of three metrics, on Realtytrac.com which shows data element analysis to say the house is potentially at 900K.

I have a 3.25% 360K mortgage at 2K a month with insurance, property tax and mortgage with say 300K equity.

Even if my excellent retirement income goes down like it has requiring me to make 15K more a year to maintain status quo I have lots of room to trim do what is needed to survive. I see at least 1/3rd have other family moved in or moving in in the last two years.

I would argue that inflation has done one good thing is keeping a real estate bloodbath from destroying thousands of lives….

In this vein I would say to those in real estate that your strategy be damned…..

Is it too early to infer that this might be the early stages of a trend “away from the west.” And does “less west” count (Texas; North & South Dakota)? I searched Google, and you only get longer-term trends, like “since 2010” if you don’t narrow your search terms pretty tightly.

I’m interested more in “since 2020,” which is hard to find even if that’s what you ask Google. I note that Florida, Georgia, the Carolinas and Tennessee (!) are pumping pretty good growth numbers in the east. Evil old Washington, DC continues to suck in the lemmings, as well.

I finally found a US Census link which shows growth just for 2022. Your call on posting the link, Wolf….

https://worldpopulationreview.com/state-rankings/fastest-growing-states

I will predict that what we are seeing is the collapse of the last real estate bubble of the American Empire. We had 40 years of declining interest rates which was the major driver of real estate prices, and now that has turned. We are probably in for 40 years of an increasing cost of money no matter what the fed wants. By the time that is over our countries ability to create credit will be long over and we will be back to a time when those desiring a home will have to save up their turnips and chickens to trade to a local housewright in exchange for a simple dwelling.

This country, or rather it’s fiat currency, has run its course. WW2 gave us a lot of financial prowess. But the central banks have used up the currency’s legitimation by their greedy debt expansion agenda with so many willing takers. The great fall was getting off the gold standard. Without another currency, winning a world war, or something unusually dramatic I say our country defaults unwillingly and or hyperinflation sets in. Every great empire in history gets replaced at some point. When I look around, I see only ‘passed the point of no return’. We do not have a moral population who could weather a depression amicably, so I see no viable solution that is doable.

Allot of truth. Can’t disagree. We’ve been on a 50-60 year debt super cycle. Where we end up nobody knows, but I’d guess in a much lower standard of living to put it mildly.

Heff

But it seems like this time, the bad debt is held by the Fed. All those MBSs absorbed by the Fed at sharply lower interest levels.

This wasnt the case in past debt “super” cycles.

Nonsense. Bad debt is NOT held by the Fed. All the MBS that the Fed holds are guaranteed by the US government. The government and therefore taxpayers are on the hook for the bad debt, and there will not be any credit losses for the Fed.

And if it the Fed continues to let the MBS roll off its balance sheet via pass-through principal payments, as it has been doing since June, without selling them outright, there will not be any kind of loss for the Fed on the MBS.

If it sells some of the MBS, it might lose some money, but not because of “bad debt” but because yields have surged, same with all bonds.

READ THIS: